Pakistan Afghanistan - iuj.ac.jp · Pakistan Afghanistan ... Pakistan rupee real exchange rates ......

39

COUNTRY REPORT 1st quarter 2000 The Economist Intelligence Unit 15 Regent St, London SW1Y 4LR United Kingdom Pakistan Afghanistan The full publishing schedule for Country Reports is now available on our website at http://www.eiu.com/schedule

-

Upload

truongquynh -

Category

Documents

-

view

224 -

download

0

Transcript of Pakistan Afghanistan - iuj.ac.jp · Pakistan Afghanistan ... Pakistan rupee real exchange rates ......

COUNTRY REPORT

1st quarter 2000

The Economist Intelligence Unit15 Regent St, London SW1Y 4LRUnited Kingdom

Pakistan

AfghanistanThe full publishing schedule for Country Reports is nowavailable on our website at http://www.eiu.com/schedule

The Economist Intelligence UnitThe Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newsletters toannual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

LondonThe Economist Intelligence Unit15 Regent StLondonSW1Y 4LRUnited KingdomTel: (44.20) 7830 1000Fax: (44.20) 7499 9767E-mail: [email protected]

New YorkThe Economist Intelligence UnitThe Economist Building111 West 57th StreetNew YorkNY 10019, USTel: (1.212) 554 0600Fax: (1.212) 586 1181/2E-mail: [email protected]

Hong KongThe Economist Intelligence Unit25/F, Dah Sing Financial Centre108 Gloucester RoadWanchaiHong KongTel: (852) 2802 7288Fax: (852) 2802 7638E-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Alexander Bateman Tel: (1.212) 554 0600 Fax: (1.212) 586 1181London: Jan Frost Tel: (44.20) 7830 1183 Fax: (44.20) 7830 1023

This publication is available on the following electronic and other media:

Online databases

FT Profile (UK)Tel: (44.20) 7825 8000

DIALOG (US)Tel: (1.415) 254 7000

LEXIS-NEXIS (US)Tel: (1.800) 227 4908

M.A.I.D/Profound (UK)Tel: (44.20) 7930 6900

NewsEdge Corporation (US)Tel: (1.718) 229 3000

CD-ROM

The Dialog Corporation (US)SilverPlatter (US)

Microfilm

World Microfilms Publications(UK)Tel: (44.20) 7266 2202

Copyright© 2000 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication norany part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permissionof The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

ISSN 0269-7173

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Contents

3 Summary

Pakistan

5 Political structure

6 Economic structure

6 Annual indicators

7 Quarterly indicators

8 Outlook for 2000-01

13 The political scene

18 Economic policy

22 The domestic economy

22 Economic trends

24 Agriculture

25 Energy

26 Foreign trade and payments

Afghanistan

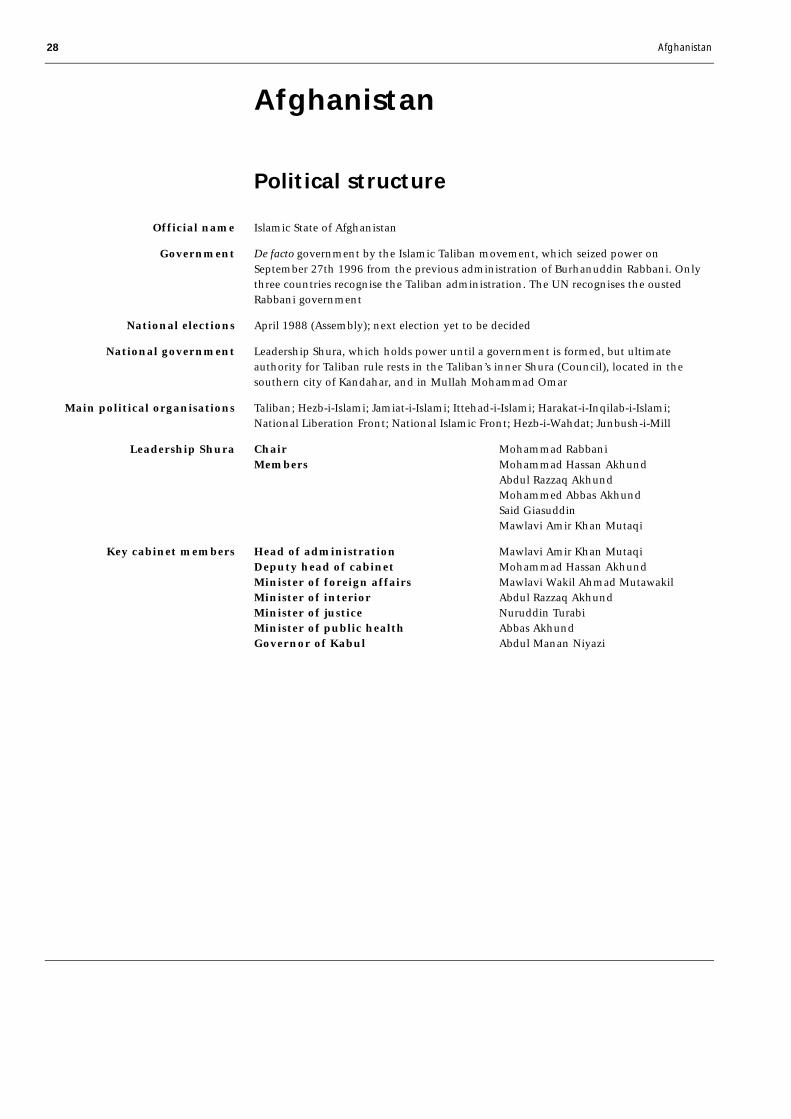

28 Political structure

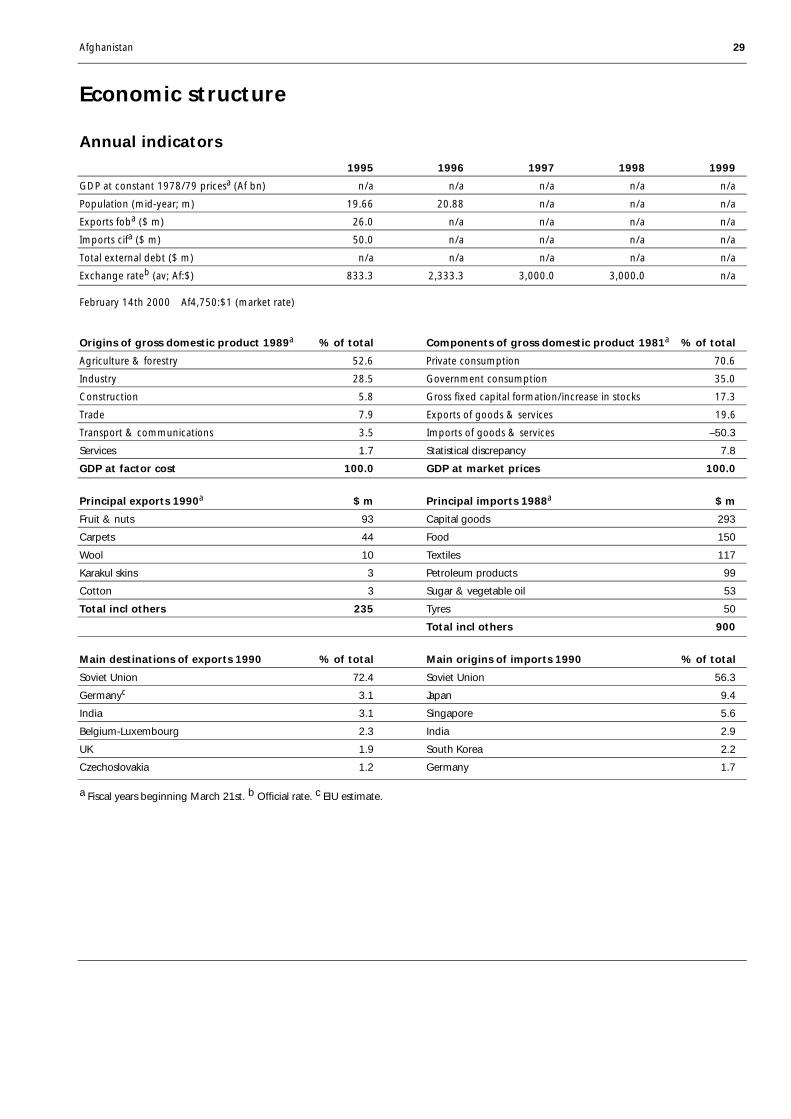

29 Economic structure

29 Annual indicators

30 Outlook for 2000-01

30 The political scene

34 Economic policy and the domestic economy

35 Trade data

List of tables

8 Forecast summary

25 Pakistan: wheat imports

27 Pakistan: merchandise trade

27 Pakistan: international reserves

35 Pakistan: foreign trade

36 Pakistan: structure of trade

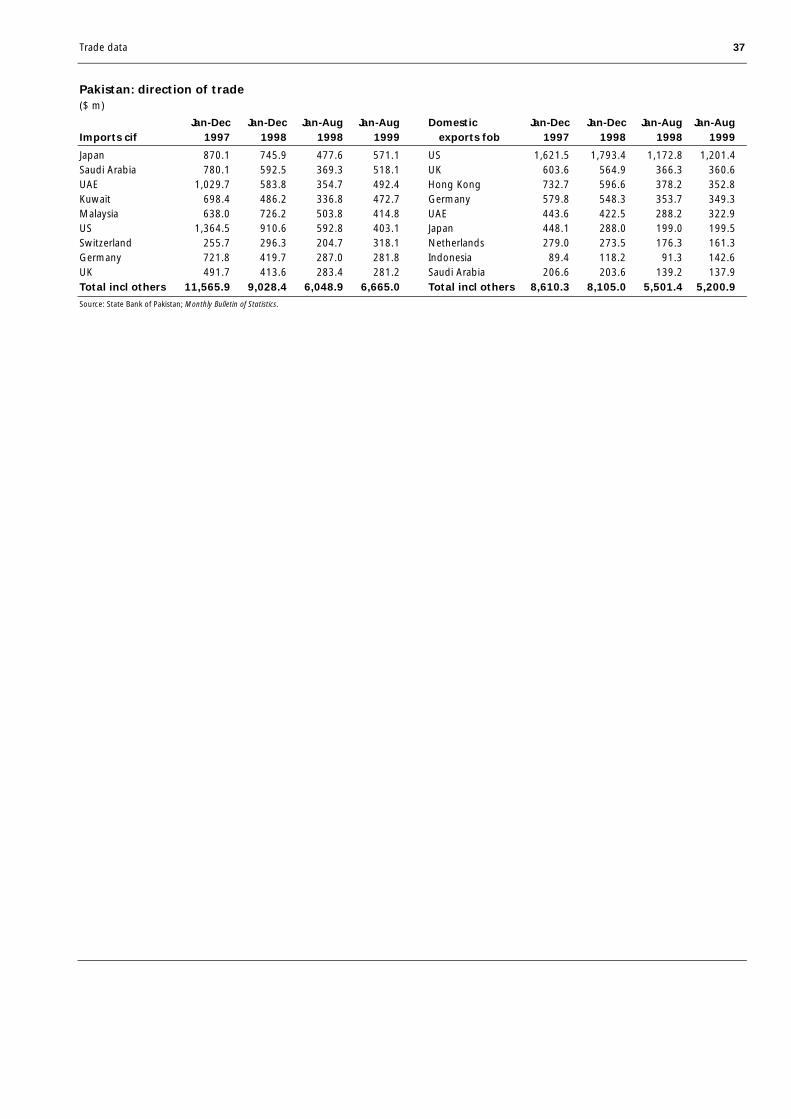

37 Pakistan: direction of trade

List of figures

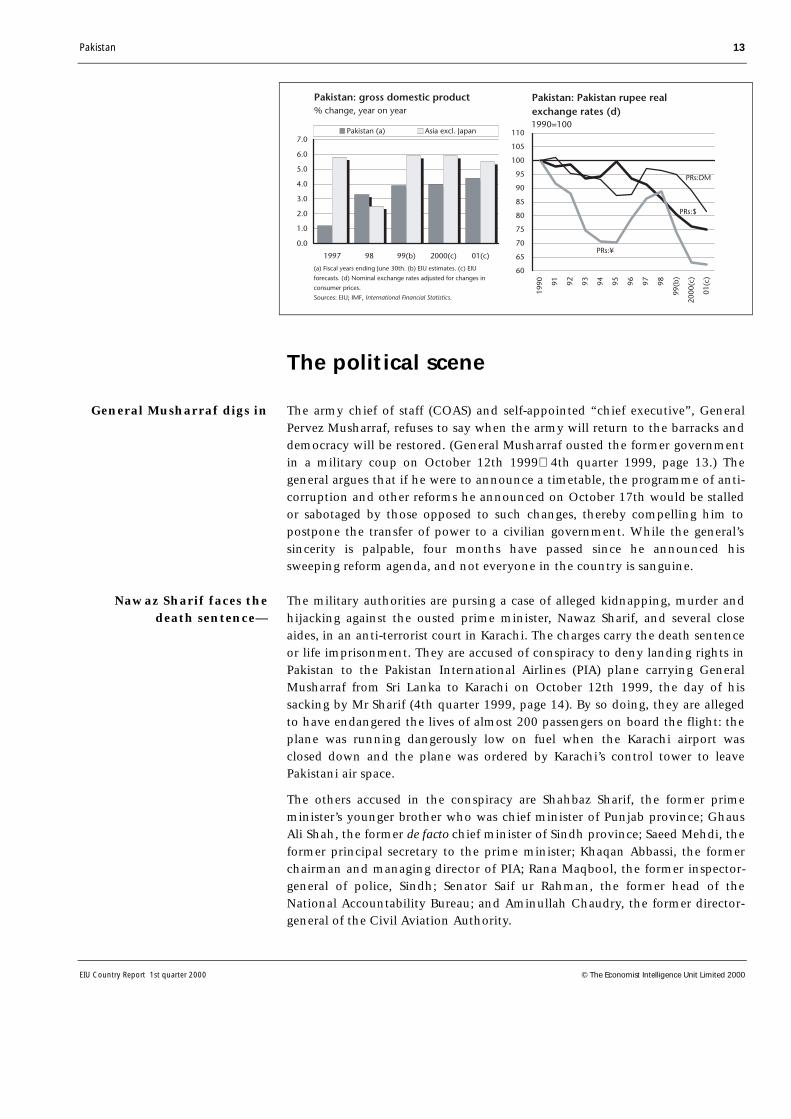

13 Pakistan: gross domestic product

13 Pakistan: Pakistan rupee real exchange rates

22 Pakistan: gross domestic product

24 Pakistan: inflation

26 Pakistan: current account

3

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Summary

1st quarter 2000

Pakistan

The military regime of General Perez Musharraf seems intent on remaining inoffice while it carries out its programme of political and economic reform. Nofull return to democracy during 2000-01 is thus likely. A good agriculturalperformance will boost economic growth this year and next, while lower realinterest rates and improved foreign and domestic investor confidence will resultin stronger industrial growth. Inflation will begin to rise. Heavy debt-servicepayments and the widening trade deficit will keep pressure on reserves.

General Musharraf has continued to avoid giving a timetable for a return todemocracy. Key former politicians face corruption and other charges; the trialof the former prime minister, Nawaz Sharif, is coming to its conclusion. Hisparty has splintered, with one faction seeking a deal with the military. Mr Sharifhas challenged the military’s actions in the courts, but most senior judges havesworn an oath of allegiance promising not to challenge the new regime. Thedrive to clean up politics and the bureaucracy has continued. Another formerprime minister, Benazir Bhutto, has called for the return of democracy.Kashmiri militants have hijacked an Indian plane, and tensions betweenPakistan and India have escalated. The US has called for a return to democracy.

Key economic posts have been appointed. The new finance minister haspromised rapid progress on several policy changes long called for by the IMF. Araft of new policy measures has been announced, including tax reforms to beintroduced at the next budget. Work has continued on a privatisation plan.Some megaprojects have been left in the lurch. Bilateral debt reschedulingagreements have been signed. The stockmarket has surged, but a move towardsshariah law would upset investors.

• The new government has set a target for real GDP growth of 4% in thecurrent fiscal year 1999/2000.

• Inflation has eased, but rising world oil prices may bring further powerprice hikes, reversing this trend.

• There has been a good cotton harvest, and domestic prices have remaineddepressed. This has benefited textile exporters, but not farmers.

• The settlement of power tariff disagreements with the last of 12independent power producers has been agreed. This will boost foreign investorconfidence.

The merchandise trade deficit widened in the first seven months of 1999/2000.Reserves have stabilised, but remain very lowmaybe too low to meet newdebt repayment terms that come into force later this year.

February 21st 2000

Outlook for 2000-01

The political scene

Economic policy

The domestic economy

Foreign trade andpayments

4

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Afghanistan

Fighting between the Taliban and the Northern Alliance is likely to drag onthroughout the forecast period. However, the UN may intensify efforts torestart a peace process, while the Taliban’s position may be weakened by thefreezing of its international assets. The Taliban will remain under internationalpressure, and may face growing challenges from vested interests in areas underits control.

The fighting has continued through the winter, although there has been littlechange in positions on the ground. One Northern Alliance group has called forintra-Afghan talks, but this call is unlikely to be heeded. There are rumoursthat tribal elders have threatened an anti-Taliban uprising. A new UN envoyhas been appointed. Afghanistan has been involved in two internationalhijackings. The Taliban may crack down on terrorist training camps, but hasremained reluctant to hand over the suspected terrorist, Osama Bin Laden. TheTaliban has recognised Chechnya. Afghan exiles, including the king, have metin Italy.

UN sanctions have been enforced, and the Taliban’s foreign funds have beenfrozen. Infrastructure remain in tatters, although a new deal means thatinternational telephone calls can now reach the country.

Editor: Kilbinder DosanjhAll queries: Tel: (44.20) 7830 1007 Fax: (44.20) 7830 1023

Next report: Our next Country Report will be published in June

Outlook for 2000-01

The political scene

Economic policy and thedomestic economy

Pakistan 5

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Pakistan

Political structure

Islamic Republic of Pakistan

Federated parliamentary system suspended by military coup on October 12th 1999

As a result of the October 12th coup, the chief of army staff and chairman of the jointchiefs of staff committee, General Pervez Musharraf, is now designated the chiefexecutive of Pakistan. The prime minister, who held supreme executive authority as aresult of constitutional changes in 1997, has been dismissed. The president remains inplace as head of state. The president is elected by an electoral college, consisting of bothhouses of the federal parliament as well as members of all four provincial legislatures

Bicameral legislature: lower house, the National Assembly, was suspended on October 12th.It has 217 directly elected members who serve for five years, of whom ten representminorities; the life of the suspended National Assembly will last until February 2002unless it is abrogated earlier by the military authorities. The upper house, the Senate, has87 members elected for six years with one-third retiring every two years. (The nextSenate election is due by March 2000 but the Senate will have to be restored by themilitary government.) Each of the four provinces elects 19 senators; the remaining 11are elected from the Federal Capital Territory and the federally administered tribal areas

Pakistan has four provinces, which enjoy considerable autonomy. Each province has agovernor and a council of ministers headed by a chief minister, who is elected by aprovincial assembly. All provincial governments stand dismissed and all assembliessuspended. Each province now has a governor appointed by the military

Originally scheduled for December 2002 (presidential) and February 2002 (NationalAssembly), the next round of elections has been postponed indefinitely. The military-ledgovernment authorities have given no timetable for the next elections

The PML(N) government of the prime minister, Nawaz Sharif, formed in February 1997,was ousted in a military coup on October 12th 1999

Pakistan Muslim League (Nawaz) (PML(N)); Pakistan People’s Party (PPP); Jamaat-i-Islami(JI); Muttahida Qaumi Movement (MQM); Awami National Party (ANP); Jamiat-i-Ulema-i-Pakistan (JUI); Tehrik-i-Insaf (TI); Millat Party

President Rafiq TararChief executive General Pervez Musharraf

Chief of air staff Marshal Pervaiz Mehdi QureshiChief of navy staff Admiral Abdul Aziz MirzaFinance Mohammad YaqubForeign affairs Attiya InayatullahLaw Sharifuddin PirzadaNational affairs Imtiaz Shahibzada

Commerce Razaq DaudFinance Shaukat AzizForeign affairs Adbus SattarInterior Lieutenant-General (retired) Moinuddin Haider

Ishrat Hussain

Official name

Form of state

The executive

National legislature

Provincial government

National elections

National government

Main political organisations

National Security Council

Key cabinet ministers

Central Bank governor

6 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Economic structure

Annual indicators

1995 1996 1997 1998 1999a

GDP at market pricesb (PRs bn) 1,882.1 2,165.6 2,414.6 2,759.5 3,029.5

GDPb ($ bn) 61.0 64.5 61.9 63.9 66.2

Real GDP growth at factor costb (%) 5.2 6.8 1.9 4.3 3.1

Consumer price inflation (av; %) 12.3 10.4 11.4 6.2 4.5

Population (mid-year; m) 130.3 134.2 138.2 141.9 145.6

Exports fob ($ bn) 8.3 8.5 8.3 8.6 8.4

Imports fob ($ bn) 11.2 12.1 10.7 9.2 9.8

Current-account balance ($ bn) –3.34 –4.42 –1.76 –2.03 –2.9

Reserves excl gold ($ m) 1,733 548 1,195 1,028 1,500

Total external debt ($ bn) 30.2 29.8 29.7 31.4b 34.5

Debt-service ratio, paid (%) 26.5 27.1 35.2 27.0b 16.3

Exchange rate (av; PRs:$) 30.93 35.27 40.12 44.55 49.22

February 18th 2000 PRs51.89:$1

% of % ofOrigins of gross domestic product 1998/99b total Components of gross domestic product 1998/99b total

Agriculture 25.4 Private consumption 72.5

Manufacturing 17.1 Government consumption 11.4

Electricity, gas & water supply 3.8 Fixed investment 13.6

Construction 3.4 Change in stocks 2.4

Mining 0.5 Exports of goods & services 15.2

Services 49.7 Imports of goods & services –15.3

GDP at factor cost 100.0 GDP at market prices 100.0

Principal exports 1998c $ m Principal imports 1998c $ m

Cotton fabrics 1,142 Machinery 2,043

Cotton yarn 984 Petroleum & products 1,310

Knitwear 731 Palm oil 627

Ready-made garments 690 Wheat 356

Rice 556 Plastics 305

Total incl others 8,105 Total incl others 9,028

Main destination of exports 1997/98b % of total Main origins of imports 1997/98b % of total

US 20.5 US 11.2

Hong Kong 7.1 Japan 7.8

UK 6.9 Malaysia 7.1

Germany 6.3 Saudi Arabia 6.7

UAE 5.1 UAE 6.6

a EIU estimates. b Fiscal years ending June 30th. c Customs basis.

Pakistan 7

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Quarterly indicators

1997 1998 1999 4 Qtr 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr

OutputManufacturing index (1995=100) 107.6 134.9 96.2 88.7 109.5 139.8 101.1 n/a

PricesConsumer prices: (1995=100) 125.7 127.1 129.6 132.0 133.7 134.3 135.0 136.4 % change, year on year 8.8 6.1 5.8 6.7 6.4 5.7 4.2 3.3Wholesale general (1995=100) 125 127 130 133 134 136 136 136

Financial indicatorsExchange rate PRs:$ (av) 42.54 43.06 43.14 46.00 46.00 46.00 46.00 n/a PRs:$ (end-period) 43.94 43.94 45.89 45.89 45.89 46.00 51.39 51.61Interest rates Discount (end-period) 18.00 18.00 18.00 16.50 16.50 15.50 13.00 13.00 Money market (av; %) 10.10 14.12 15.10 5.42 8.41 9.37 8.37 8.46 Treasury bill (av; %) 13.52 15.10 15.98 14.74 n/a 12.37 n/a n/aM1 (end-period; PRs bn) 699.8 645.2 653.5 667.2 732.3 715.8 726.8 719.7 % change, year on year 32.5 13.8 12.2 17.7 4.6 10.9 11.2 7.9M2 (end-period; PRs bn) 1,170.5 1,200.3 1,202.3 1,208.4 1,262.5 1,248.4 1,282.0 1,273.0 % change, year on year 19.9 18.3 14.2 13.8 7.9 4.0 6.6 5.3Stockmarket KSE 100 index (end- period; Nov 1st 1991=1,000) 1,746 1,533 880 1,112 945 1,057 1,055 1,199 % change in $ value, year on year –13.2 –12.2 –45.1 26.4 –15.0 11.5 –10.7 13.2

Sectoral trendsCotton (av; production) Yarn (‘000 tonnes) 130.4 125.7 125.7 125.2 128.8 126.3 128.8 n/a Fabrics (m sq metres) 29.9 27.9 27.0 30.2 33.3 29.5 33.7 n/a

Foreign trade (PRs bn)Exports fob 102.67 93.25 97.65 91.62 99.96 94.64 107.60 100.83Imports cif 123.43 102.48 103.18 100.85 112.80 110.71 141.60 125.41Trade balance –20.76 –9.23 –5.53 –9.23 –12.84 –16.07 –34.00 –24.58

Foreign reservesReserves excl gold (end-period; $ m) 1,195 1,271 844 676 1,028 1,650 1,678 1,494

Sources: Federal Bureau of Statistics, Monthly Statistical Bulletin; IMF, International Financial Statistics; IFC, Emerging Stock Market Review.

8 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Outlook for 2000-01

Forecast summary

1998a 1999b 2000c 2001c

Real GDP at factor costd (% change) 4.3 3.1a 4.5 5.0 Agriculture 3.8 0.4 4.5 3.5 Industry 6.8 3.8 5.0 5.7 Services 3.2 4.1 4.2 5.4

Real GDP at market pricesd (% change) 3.3 3.9 4.0 4.4 of which: private consumption –0.3 5.1 6.0 5.0 public consumption 6.8 3.9 2.0 2.5 gross fixed investment –5.4 –2.3 3.0 6.0 exports of goods & services 3.7 –1.2 0.0 3.6 imports of goods & services –11.3 –8.2 7.0 6.5

Consumer price inflation (av; %) 6.2 4.5 7.0 8.5

Merchandise exports fob ($ m) 8,642 8,422 8,876 9,584

Merchandise imports fob ($ m) 9,241 9,761 11,007 11,972

Current-account balance ($ m) –2,031 –2,860 –3,446 –3,630

Exchange rate (year-end; PRs) 45.90 52.56 55.91 60.76

a Actual. b EIU estimates. c EIU forecasts. d Fiscal years ending June 30th.

The army chief, General Pervez Musharraf, installed himself as the new “chiefexecutive” of Pakistan in a coup in October 1999. A central policy of the newmilitary regime is a clean-up of Pakistan’s corrupt political system. About twodozen top politicians, bureaucrats and businessmen have already been chargedwith corruption or defaulting on bank loans. A new law governing “account-ability” has been amended several times, and the National AccountabilityBureau (NAB) can now detain anyone for 90 days without court permission;this 90-day period can be extended almost indefinitely. A conviction under theaccountability law automatically means disqualification from holding publicoffice or becoming or remaining a member of any provincial or nationalparliament. The NAB’s prospective hit list may therefore be expected to includemany former top politicians, including a large number of former and currentmembers of the provincial and national parliaments. The bureaucracy is in fora tough time as well. All those civil servants, high or low, who were rumouredto have done the previous prime ministers’ bidding without regard to rules andregulations or those who are known to “live beyond their means” may expectto be investigated.

General Musharraf has categorically ruled out any political comeback for theformer prime ministers, Benazir Bhutto and Nawaz Sharif. Ms Bhutto wasconvicted of corruption in 1998 during the Sharif regime; she has challengedthe verdict in the supreme court, but the judiciary will be under pressure fromthe military to let the verdict stand. The new regime is also expected to launcha number of fresh cases of corruption and misrule against Ms Bhutto in thenewly established accountability courts. Before the end of 2000 Ms Bhutto’sappeals are likely to have been heard and rejected by the supreme court, and

The military will continueits crackdown

on corruption—

—seemingly secure for nowas political heavyweights

are sidelined—

Pakistan 9

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

she will thus be disqualified as a member of parliament for a period of time.She is also likely to be convicted on several other counts of corruption.

In the circumstances, there is no likelihood that Ms Bhutto, who is in self-imposed exile in London, will return to Pakistan in a hurry and resume theleadership of the Pakistan People’s Party (PPP). Rather, she may be expected tolobby Western governments into pressurising the junta to give a timetable forthe restoration of an electoral democracy, one in which she can still hope toplay a part. However, support for Ms Bhutto within the PPP may waver inher absence.

The former prime minister, Nawaz Sharif, is also facing political oblivion.Along with his younger brother, Shahbaz Sharif, and six others, he has beenhauled up before a special anti-terrorist court and charged with attemptedhijacking, kidnapping and murder, which carry the death sentence. The paceof the trial has quickened in recent weeks. Under pressure from the military,Mr Sharif is likely to be convicted within the next few months. Mr Sharif andthe others will naturally lodge appeals and it is possible that the high court orsupreme court may commute the expected death sentences to lifeimprisonment. With its leader detained, Mr Sharif’s partythe PakistanMuslim League (Nawaz), the PML(N)has split into at least two factions. One,under the leadership of a former federal minister, Raja Zafarul Haq, hasremained loyal to Mr Sharif, and will push for a legal challenge to the militaryregime. The second main faction, led by Ejaz ul Haq, the son of the formermilitary dictator Zia ul Haq, is also pushing for parliament to be restored, but isseeking to curry favour with the military by offering to abandon Mr Sharif infavour of a new prime minister to be appointed by the military.

Following the military takeover on October 12th 1999, several writs werelodged in the high courts and supreme court challenging the legitimacy of themilitary government. When the courts accepted the petitions for hearinginstead of rejecting them out of hand, the generals were alarmed. They had notimposed martial law, rather allowing the courts to function freely in theexpectation that the judges would toe the line. But when rumours began to becirculated that Mr Sharif had bribed certain judges to rule against the newregime, creating a constitutional crisis, the military moved swiftly, forcing allhigh court judges to take a fresh oath of office on January 25th, swearingloyalty to the October 12th Provisional Constitutional Order of GeneralMusharraf (in which he dismissed the Sharif regime, suspended parliament andproclaimed himself as the chief executive of Pakistan) and agreeing to upholdand indemnify every law, ordinance or executive order of the militarygovernment. All but 13 of the 102 judges took the new oath. Hence an uneasybalance has been reached, in which the judiciary will be allowed to functionrelatively freely, but only as long as it rejects any legal challenge to the regime.Furthermore, if any serious legal challenge does materialise, the generals can beexpected to impose fully fledged martial law. Thus the military regime seems tohave cleared the way to remain in office for much of the forecast period.

—and the courts arereined in—

10 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

General Musharraf has not bowed to international pressure to give a timetablefor the restoration of democracy. He and his supporters within the armedforces seem committed to his seven-point agenda, which includes the anti-corruption campaign as well as the revival of the economy. Progress on thesefronts is unlikely to be rapid. With the judiciary cowed and the main politicalleaders of the PPP and PML(N) likely to be in jail or in exile for some time tocome, the EIU expects the current political regime to last at least until 2001. InFebruary officials hinted that a plan for institutional and democratic reformwould be revealed “by the end of next year”, suggesting that the military mayremain in office throughout the forecast period.

However, public goodwill towards the generals has already begun to evaporatebecause the military government is perceived to be short of vision and long onrhetoric. The “accountability” drive has been painfully slow to take off, andhard economic decisions have been postponed. Any serious economic difficul-tiesfor example, the suspension of international aid, precipitating a full eco-nomic crisiscould result in unrest. So far, the government has not touchedthe press or most fundamental rights. But if it faces a real challenge, chancesare that it will crack down harshly, further alienating international opinion.

The forces of radical political Islam will become stronger under the military re-gime. The main reason for this is the military’s overt support for Islamic separa-tists in Indian-held Kashmir. The Islamists see this as a great opportunity toseize the initiative in Kashmir and have launched suicide raids on Indiansecurity forces in the besieged valley. These are taking a heavy toll on theIndian army. The military regime has also whipped up anti-India feelings inthe country, thereby emboldening radical Islamic forces to spill over into thestreets and openly espouse war with India in order to “liberate” Kashmir.

The high point of Indo-Pakistan détente came during the Lahore summit inFebruary 1999 between the then prime minister of Pakistan, Nawaz Sharif, andthe Indian prime minister, Atal Bihari Vajpayee. Since the military takeover inPakistan, tensions between the two nations have intensified. India holdsGeneral Musharraf directly responsible for triggering the conflict in Kargil lastJune, accusing Pakistan of fomenting crossborder terrorism in Kashmir, and hasrefused to talk with an “illegitimate” military regime. In turn, GeneralMusharraf has said that Pakistan will not talk to India unless it agrees toaddress the “core” issue of Kashmir. Relations between the two countries plum-meted in late December following the hijacking of an Indian Airlines plane byfive Kashmiri militants. Since then, the armies of the two countries haveshelled each other’s positions across the Kashmir border almost continuouslyand a series of bomb explosions have rocked different cities of Pakistan. Indiahas now upped the stakes by calling upon the US to declare Pakistan a“terrorist state” and has pushed for the US president, Bill Clinton, to leavePakistan off the itinerary of his forthcoming trip to South Asia. The war ofwords has intensified, and in early February Mr Vajpayee threatened to seizePakistan-held Azad Kashmir by force. Against this backdrop, unless PresidentClinton, due to visit India in March, is able to act as mediator and talks are

the military may find ittough to fulfil

expectations

but with democracyunlikely to be

restored soon

Islamic extremism will risein Pakistan

resulting in very tenserelations with India

Pakistan 11

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

resumed on both sides, the possibility of another Pakistan-India militaryconflict cannot be ruled out.

Islamabad has been flooded by high-ranking US officials anxious to communi-cate Western concerns to General Musharraf. All have urged the new govern-ment to give a timetable for the restoration of democracy, to take steps to curbIslamic terrorist groups, and to sign the Comprehensive Test Ban Treaty(CTBT). But as tensions with India run high, Pakistan is in no hurry to sign theCTBT. Nor, in the absence of any concrete evidence of anti-US terrorism, is acrackdown on Islamic militant groups based in Pakistan likely. GeneralMusharraf, however, may decide to visit Kabul in an effort to persuade theTaliban regime to rein in the terrorist Osama Bin Laden, a move long sought bythe US. However, the key US demanda definite timetable for a return to de-mocracywill remain illusive. Equally, if President Clinton leaves Pakistan offthe agenda during his forthcoming visit to South Asia, Pakistan would considerthat as a betrayal of a long-standing friendship. In this event, a wave of anti-Americanism could sweep the country, strengthening the hand of anti-USIslamic forces.

The latest $280m instalment of a $1.6bn, three-year IMF structural adjustmentprogramme was held back following the military coup in October. With theagreement of the US administration in November, the IMF began a fresh roundof negotiations with the new government. In a key policy statement inDecember, the government made clear that many of the IMF’s conditionsincluding new taxes aimed at improving the budgetary positionwould bemet, but not until the June 2000 budget. In the meantime, an IMF reviewmission could return to Pakistan in March. It may well discuss drawing up apoverty alleviation programme with less stringent conditions on economicreform. However, if the IMF does not resume credit, Pakistan will facedifficulties meeting new debt-service requirements once the recently agreedmoratorium on payments ends in late 2000.

The finance minister, Shaukat Aziz, expects real GDP growth (output basis) inthe current fiscal year 1999/2000 (July-June) to reach around 4%, up from3.1% in 1998/99. We expect a slightly higher real GDP growth rate of 4.5%.Growth will be lifted by a good agricultural performance—the late 1999 cottoncrop was 10.7m bales. The support price of wheat was raised at the start of thesowing season in November, thereby giving an incentive to farmers to increasethe acreage under wheat this year. Rice production has hit a record 4.9mtonnes. After this strong performance, growth in agricultural output will easeback to 3.5% in 2000/01.

Industrial output will also pick up in 1999/2000, rising by 5%, up from anestimated 3.8% in 1998/99. Growth will be led by the manufacturing sector,which is expected to grow by about 6%. Investment is likely to have collapsedduring the political uncertainty surrounding the military takeover, butconfidence is improving, and stronger investment will help to lift industrialoutput during the remainder of the fiscal year. The government plans tounveil an ambitious privatisation programme during the next nine months,

and more tricky relationswith the US

IMF support remains inthe balance

but a good cotton cropwill lift GDP growth

12 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

which should further stimulate investment and improve efficiency in theindustrial sector. Consequently, we expect industrial growth to pick up to 5.7%in 2000/01. Services will also pick up during the forecast period.

These expectations could be derailed if tensions with India escalate into openhostilities, or if relations with the US are broken off, leading to a US veto ofinternational financial assistance. Either event would result in a much bleakereconomic outlook than the one discussed above.

We expect inflation to pick up in calendar 2000, to an annual average of 7%.The support price of wheat has been raised, while petroleum prices were raisedby 10% in December. Both increases will feed through into higher prices in thecoming months. From mid-year, the imposition of a goods and services tax(GST) will boost retail prices, and we expect international commodity prices topick up in 2000, boosting import price pressures. There could be further energyprice hikes ahead; if Pakistan’s major gas supplying company, PakistanPetroleum, is privatised as planned in the next six months, subsidised gasmight be a thing of the past and gas prices could rise by as much as 50% forcertain consumers. The same would be true of utility companies such asPakistan Telecommunications when they are privatised. In addition, weforecast a further rise in world commodity prices in 2001, when inflation willpick up to an annual average of 8.5%. This forecast is based on the assumptionthat a sharp devaluation of the rupee is avoided.

Merchandise exports will pick up steadily throughout the forecast period, risingby 5.4% in 2000 and by 8% in 2001, in dollar terms. Exports will benefit fromstronger world commodity prices, boosting rice exports, as well as more robusttextile exports. However, imports will rise by 12.8% year on year in 2000 indollar terms, boosted by stronger domestic demand and a hike in world oilprices, and imports will continue to outpace exports in 2001. As a result, themerchandise trade deficit will widen, while the services and incomes deficitwill also pick up. Although workers’ remittances will also rise, this will not beenough to prevent the current-account deficit widening to $3.4bn in 2000, and$3.6bn in 2001.

Pakistan’s debt repayment problems will be exacerbated from 2001, when debtsrescheduled by the Paris and London Clubs in 1999 will become due forpayment. Continued debt payments, combined with the rising current-accountdeficit, and limited investment inflows, will keep up the pressure on Pakistan’sreserves. Nevertheless, reserves will pick up to around $2.8bn in 2000-01,boosted by renewed assistance from the IMF in some form.

Despite the expected rise in reserves, the rupee will continue to depreciateduring the forecast period, falling to Rs60.1:$1 by end-2001. An escalation intensions with India, or the withdrawal of IMF support, would result in sharpoutflows of capital and a much steeper drop in the rupee.

while reserves willremain weak and the rupee

will fall further

Inflation will pick up

The current-account deficitwill rise

Pakistan 13

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

The political scene

The army chief of staff (COAS) and self-appointed “chief executive”, GeneralPervez Musharraf, refuses to say when the army will return to the barracks anddemocracy will be restored. (General Musharraf ousted the former governmentin a military coup on October 12th 19994th quarter 1999, page 13.) Thegeneral argues that if he were to announce a timetable, the programme of anti-corruption and other reforms he announced on October 17th would be stalledor sabotaged by those opposed to such changes, thereby compelling him topostpone the transfer of power to a civilian government. While the general’ssincerity is palpable, four months have passed since he announced hissweeping reform agenda, and not everyone in the country is sanguine.

The military authorities are pursing a case of alleged kidnapping, murder andhijacking against the ousted prime minister, Nawaz Sharif, and several closeaides, in an anti-terrorist court in Karachi. The charges carry the death sentenceor life imprisonment. They are accused of conspiracy to deny landing rights inPakistan to the Pakistan International Airlines (PIA) plane carrying GeneralMusharraf from Sri Lanka to Karachi on October 12th 1999, the day of hissacking by Mr Sharif (4th quarter 1999, page 14). By so doing, they are allegedto have endangered the lives of almost 200 passengers on board the flight: theplane was running dangerously low on fuel when the Karachi airport wasclosed down and the plane was ordered by Karachi’s control tower to leavePakistani air space.

The others accused in the conspiracy are Shahbaz Sharif, the former primeminister’s younger brother who was chief minister of Punjab province; GhausAli Shah, the former de facto chief minister of Sindh province; Saeed Mehdi, theformer principal secretary to the prime minister; Khaqan Abbassi, the formerchairman and managing director of PIA; Rana Maqbool, the former inspector-general of police, Sindh; Senator Saif ur Rahman, the former head of theNational Accountability Bureau; and Aminullah Chaudry, the former director-general of the Civil Aviation Authority.

General Musharraf digs in

Nawaz Sharif faces thedeath sentence—

14 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Mr Sharif and the others were indicted in late December 1999. The case isbeing conducted according to the law governing anti-terrorist courts—which,ironically, were set up by Mr Sharif when he was prime minister, amid muchcriticism by human rights groups (3rd quarter 1997, page 10). A decision isexpected in March or April at the latest, but an appeal is then likely (underamended anti-terrorist court rules, an appeal can be made in the high courtand then the supreme court).

Mr Sharif denies the charges and says he cannot expect justice from what heterms a “kangaroo court”. However, so far the trial seems to have beenconducted in a fairly transparent manner and the court has gone out of its wayto accommodate the objections and points of view of the defence council.Also, there is very little sympathy for Mr Sharif in the country, so hisstatements and complaints are not front-page news in the local press.

Mr Sharif’s troubles are not confined to the trial. His party, the Pakistan MuslimLeague (Nawaz), or PML(N), has split into at least two factions. Some partystalwarts are standing by Mr Sharif in the hope that he may one day stage acomeback. Others, however, are desperately trying to cosy up to the militarygovernment, promising to abandon Mr Sharif provided that General Musharrafrestores parliament and nominates one among them to preside over the transi-tion to democracy as prime minister. The latter, rebel group comprises theformer interior minister, Chaudry Shujaat, and the former population minister,Abida Hussain, as well as two party vice-presidents, Khurshid Kasuri and Ejaz ulHaq (the son of a former military dictator, Zia ul Haq). Implementation of theirplan would imply the indefinite jailing (or worse) of Mr Sharif as well as theprovision of post facto legitimacy to the military takeover. So far, however,General Musharraf has kept them all at a tantalising distance from the army’sgeneral headquarters in Rawalpindi.

Mr Sharif has challenged his detention and that of his family members beforethe high court of Lahore. He has also challenged the military takeover and hisouster from power before the supreme court in Islamabad, arguing that it isunconstitutional and illegal. This has put the judiciary in a quandary. Thecourts are reluctant to appear as handmaidens of the military. But if they wereto hold that the military intervention is illegal, General Musharraf would haveno choice but to formally impose martial law and abrogate all power to him-self. He has not done that so far, and most fundamental constitutional rightsremain alive.

Until the end of January, the courts had been largely free to conduct theirbusiness. However, when rumours gained credence that some supreme courtjudges might have been bribed by Mr Sharif’s supporters, General Musharrafdecided to eliminate the risk that the courts might rule against the legitimacyof his military regime. Hence in late January he ordered the judges of the fourhigh courts and the supreme court to take a fresh oath of office under theProvisional Constitutional Order (PCO) of October 12th according legitimacyto the “constitutional deviation” that occurred when he dismissed the civilian

—and a faction of his partyplans for a future

without him

The military government’slegitimacy is challenged—

—forcing it to put pressureon the judiciary—

—but his counter-chargesreceive little sympathy—

Pakistan 15

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

government, suspended national and provincial parliaments and was ap-pointed as chief executive of Pakistan.

Taking a fresh oath implies that the courts cannot rule on the legitimacy of themilitary government, the chief executive or any person acting on his authority.Fundamental constitutional rights will thus remain in force only to the extentthat they do not come into conflict with the provisional constitution and anyorders made under it since October 12th, placing the judges in a legalstraightjacket.

Only 13 out of 102 senior judges in the country refused to take the new oath.Among them was the chief justice of the supreme court, SaeeduzzamanSiddiqui, and five other supreme court judges; the rest sat on the high courts ofPunjab, Sindh and North-West Frontier provinces. According to Mr Siddiqui,when the military took over, he was assured by General Musharraf that itwould not be necessary to take a fresh oath of office. But the attorney-generaland minister of law, Aziz Munshi, has said that the only other option availableto the military in the circumstances was to impose martial law, which themilitary government does not want to do.

This is not a novel development. When General Zia ul Haq overthrew thecivilian government of Zulfikar Ali Bhutto in July 1977, a similarly wordedPCO was promulgated in due course and all senior judges (save two) quietly fellin line and took the new oath, including Mr Siddiqui who was then among themost junior judges of the Sindh high court.

Lawyers in Pakistan are divided over the new oath. Those who support thePML(N) have denounced the move, saying it is unconstitutional. But manylawyers who are allied to the Pakistan People’s Party (PPP), the party of theformer prime minister, Benazir Bhutto, are more sympathetic. Meanwhile, theUS has weighed in with a strong statement decrying the move as an attempt to“circumscribe the independence of the judiciary”.

Meanwhile, popular demand for a crackdown on corrupt politicians and bureau-crats has buoyed the military government’s so-called accountability campaign. ANational Accountability Bureau (NAB) has been set up under the direction ofLieutenant-General Syed Mohammad Amjad, who has a reputation for probity.General Amjad empowered himself via a rather draconian accountabilityordinance (first promulgated in November, amended several times since then)and arrested over 100 people. Former politicians and senior bureaucrats close tothe Sharif and Bhutto regimes numbered among the many who were arrested.He has already forced the “crooks”, as he is wont to call them, to repay aboutRs10bn ($192.7m) in defaulted loans or misappropriated public funds.

General Amjad says that investigations are in progress against another 100 orso suspects, who will be arrested soon. NAB’s modus operandi is to detain sus-pects for up to 90 days or more (allowed by the ordinance), deny them bail, in-vestigate wrong-doing on their part and then present them before specialaccountability courts for trial. Under the NAB ordinance, those who are foundguilty of corruption or misuse of power can be sentenced to 14 years in prison,a large fine and disqualified from holding public office or contesting elections.

—with mixed reactions

The noose of“accountability” is

tightened

16 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Since its introduction, the NAB ordinance has been repeatedly amended to giveit tougher powers. Another new amendment now in the offing would shift theburden of proof to the defendant. The court would not have to prove guilt; in-stead the defendant must prove his innocence. For example, if a defendantcannot prove that his given sources of income and wealth can sustain his life-style, he could be charged under the ordinance. The ordinance has been chal-lenged in the courts for violating fundamental rights. However, as the courtjudges have recently sworn a new oath to uphold the new order, this challengeis unlikely to amount to much.

Meanwhile, the defunct political parties and the members of the suspendedparliament have come together to demand an early restoration of civilian rule.In fact, the parties of Mr Sharif and Ms Bhutto, who are bitter political foes,have opened a secret dialogue to discuss ways to restore democracyand howto end the anti-corruption drive that is netting so many political leaders. Ironi-cally, Ms Bhutto was convicted for corruption by the Sharif regime (her appealis pending in the supreme court). Her husband, Asif Zardari, has been in prisonsince her government was ousted in November 1996, facing murder and drugtrafficking charges. Shortly before Ms Bhutto and Mr Zardari were convicted ofcorruption, she left the country and has remained abroad ever since. Initiallyshe welcomed the ouster of the Sharif regime by the army in the hope that themilitary would be soft on his opponents. But more recently she has been pub-licly rebuffed by the junta, forcing a change of tack. She now argues for theearly restoration of democracy and has offered to mend relations withMr Sharif, in an effort to put pressure on the military government.

Ms Bhutto has voiced strong opposition to the application of the death penaltyto Mr Sharif, should he be found guilty. Equally surprising, given the long-standing animosity between Ms Bhutto and Mr Sharif, she has warned theauthorities not to victimise the Sharif family and has called upon foreign gov-ernments to pressure the new regime for a timetable for the restoration ofdemocracy. In turn, Mr Sharif’s wife and daughter condemned the killing ofMs Bhutto’s father, Zulfikar Ali Bhutto, in 1979 at the hands of the militarygovernment of General Zia ul Haq. In the circumstances, Mr Sharif is trying tohold onto whatever support is available to him, even if it should come from abitter political foe.

An Indian Airlines plane en route from Kathmandu to New Delhi was hijackedon December 24th 1999 by five armed men claiming to be Kashmiri Muslimsfighting against Indian rule. The plane sought to land in Lahore, Pakistan. Butwhen permission to do so was denied by the Pakistani authorities the planewas diverted to Amritsar, India, where it landed. However, the Indianauthorities allowed the plane to take off again without refuelling. When thepilot radioed Lahore airport for help, warning that the plane was desperatelyshort of fuel and would crash, he was allowed to land in Lahore. The Pakistaniauthorities refuelled the plane and allowed it to take off again. It then landedin Dubai, freed 25 passengers, refuelled, and flew to Kandahar, Afghanistan.The plane stayed in Kandahar until December 31st. While the Indiangovernment managed to reduce the number of demands made by the

The hijack of an IndianAirlines plane has ended—

Ostracised, Ms Bhutto andMr Sharif find new

common ground

Pakistan 17

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

hijackers, it still faced criticism for releasing three jailed Islamic militants inexchange for the release of the passengers. Indian officials maintain thatPakistan orchestrated the hijacking, a view reinforced by the belief that thehijackers subsequently escaped to Pakistan.

Since the episode, Indian and Pakistani forces have traded fierce artillery firealong the line of control (LOC), which divides Pakistan- and Indian-administered Kashmir. Both sides have suffered many casualties. Each accusesthe other of sending troops across the de facto border to attack the other’spositions. There are reports that the campaign by militants against Indianauthorities in Indian-administered Kashmir has intensified. Militants have over-run police and special forces barracks, a trend that is likely to continue,particularly as General Musharraf has recently voiced his overt support for theMuslim insurgents in Kashmir. The Indians have also been accused of shellingseveral Pakistani border towns, and civilian casualties have mountedin Pakistan.

The rhetoric on both sides has become more shrill. General Musharraf has saidthat his government was not averse to using nuclear weapons if the security ofhis country was threatened; he has also deflected questions as to whetherPakistan would pledge to a “no first use” of nuclear weapons, a policy whichIndia has pledged to follow. Meanwhile, the Indian army chief, P Malik, andprime minister, Atal Behari Vajpayee, have both publicly talked of a war withPakistan while the chief minister of Indian-held Kashmir, Farooq Abdullah,continues to ask the Indian government to send troops into Pakistani territoryin pursuit of militants who he says are waging a war against his governmentfrom across the LOC. Matters were not helped in late February when Indiaexpelled several Pakistani diplomats, apparently for spying, followed by a tit-for-tat expulsion of Indian officials by Pakistan.

The web of relations between India, Pakistan and the US is changing. USrelations with India have warmed over the years, and the two countries havenow agreed to set up a joint committee to combat terrorism. MeanwhilePakistan, the historical cold war ally of the US, is falling out of favour. The UShas brought considerable pressure to bear on Pakistan to help extradite fromAfghanistan Osama Bin Laden, the Saudi accused by the US of mastermindingthe bombing of two US embassies in Africa. The US has also called on Pakistanto ban the militant Islamic jihadi organisation, Harkat ul Mujahideen, which isbased in Pakistan. Washington has already declared the organisation a terroristoutfit, alleging that it was behind the kidnapping and murder of five Westerntourists, including two US citizens, in Kashmir in 1995.

The visits of several US senators to Pakistan in January were followed byanother high-ranking US delegation, led by the assistant secretary of state forSouth Asia, Karl Inderfurth, and including the top US official charged withcombating terrorism, Michael Sheehan. The purpose of these visits was toimpress upon the Pakistani authorities that their refusal to act against Islamicjihadi organisations was hurting the credibility of the new military govern-ment. However, while General Musharraf condemned all forms of terrorism, he

Pakistan feels the pressurefrom the US—

—but Pakistan-Indiatensions have risen sharply

18 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

urged the world to focus on the root cause of conflict in the region—Kashmir—by urging India to negotiate a peaceful resolution of the problem. The recentUS delegation also sought a timetable for the restoration of civilian rule—although General Musharraf once again declined.

A decision to leave Pakistan off the itinerary of the South Asia trip planned forthe US president, Bill Clinton, could be taken as another sign of the US’sshifting foreign policy stance. Mr Clinton plans to visit India and Bangladeshin March, but so far has announced no plan to include Pakistan. Mr Clintonappears eager to secure the beginnings of a peace initiative in South Asia beforehe retires this year. (Previous plans to visit South Asia were postponed afterIndia, followed by Pakistan, tested nuclear devices in 1998.) He is also keenthat both countries should support his nuclear-non-proliferation efforts, mostnotably by signing the Comprehensive Test Ban Treaty (CTBT).

However, as discussed above, the US has been unable to secure assurances fromthe new Pakistani government that it is ready to act against terrorist groups, orto give a timetable for restoring democracy. Mr Clinton may choose not to visitPakistan unless the Musharraf regime responds to at least some of the terms ofMr Clinton’s foreign policy agenda. However, the alternative—coming to Indiaand not to Pakistan—would play directly into the hands of the Islamicextremist forces in Pakistan and the hawks in India. Both camps want the USto sever ties with Pakistan: for the hawks in India, the isolation of Pakistanwould be a diplomatic victory. In Pakistan and Afghanistan, the forces ofIslamic extremism would be able to exploit the economic meltdown thatwould inevitably follow a real breakdown in ties (resulting in the USimposition of a veto on multilateral financial support). (Mindful of this, therehave been hints that Mr Clinton may include Pakistan on his tour, but only ina personal capacity, ensuring that the US is not seen as supporting the coup,while also maintaining a dialogue with the military regime.)

Economic policy

Before being summoned by the military government to turn around thePakistan economy, the finance minister, Shaukat Aziz, was formerly head ofprivate banking for Citibank in New York. Mr Aziz was given a free hand tonominate the new governor of the central bank (Ishrat Hussain, a senior WorldBank official on loan to Pakistan), the commerce minister (Razaq Daud, amember of one of the top business families of the country), and the chairmanof the Privatisation Commission (Altaf Saleem, who hails from the CrescentGroup, which is ranked among the top five industrial and finance houses inPakistan). Mr Aziz has also chosen the new heads of the Investment Board ofPakistan, Export Promotion Bureau, the Securities and Exchange Commission,the Central Board of Revenue, all the public sector banks and other significanteconomy-related institutions.

Even before being sworn in, Mr Aziz announced his intention to move swiftlyon several fronts. He pledged to settle within weeks the bitter dispute over

—which may dropPakistan from the

president’s itinerary

The new economic czar—

—has promised to taketough policy decisions—

Pakistan 19

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

power rates that had been raging for nearly three years between the Water andPower Development Authority (WAPDA) and the UK-based Hub PowerCompany (Hubco). He also promised to bring in a sweeping goods and servicestax (GST) on retail trade and an income tax on agricultural incomes—measureslong demanded by the IMF, but postponed time and again by governmentsunder pressure from the aggressive traders’ and landlords’ lobbies, respectively.Finally, Mr Aziz has said he fully supports General Musharraf’s October 28thdeadline for the repayment of all defaulted loans.

However, despite the tough talk, Mr Aziz now says that the GST and tax on ag-ricultural income will not be levied until the next budget, due to be an-nounced in June. No explanations for this delay have been offered but hintshave been dropped that he wants to thoroughly revamp the corrupt andinefficient tax collecting administration before asking it to collect the newtaxes. But critics have also claimed that he has been scared by the traders’lobby, which has threatened to shut down shops indefinitely if the GST isimposed, and that he may not want to erode business confidence further byordering the National Accountability Bureau (NAB) to pursue bank loandefaulters, many of whom are among the top businessmen of the country.Also, four months down the line, Mr Aziz’s efforts to negotiate a settlementbetween WAPDA and Hubco have not borne fruit—although talks may beinching towards a solution (see Energy).

On December 15th Mr Aziz announced a series of specific initiatives to stream-line the economy and restore business confidence. Most of the measures havebeen seen before in the economic revival plans of previous governments. How-ever, there were some new measures as well. Among the salient features are:

• all existing tax exemptions will be withdrawn in the June 2000 budget;

• the tax structure will be simplified in the June budget by stressingtransparent and voluntary self-assessment schemes;

• a retail GST and agricultural income tax will be imposed in the Junebudget;

• foreign-exchange remittances of profit, dividends and royalties will onceagain be allowed without prior permission of the State Bank of Pakistan (SBP,the central bank); when the US imposed sanctions following Pakistan’s nucleartest in May 1998, the SBP required all banks to obtain permission beforemaking any remittances, in order to conserve scarce foreign exchange;

• central excise duty has been withdrawn on credit cards and other banktransactions;

• only foreigners will henceforth be allowed to open foreign-exchangedeposit accounts in local banks, in an effort to arrest the “dollarisation” of theeconomy;

• foreign-exchange bearer certificates have been discontinued and incometax immunities available to government bondholders have been withdrawn inorder to stop money laundering and dollarisation of the economy;

—but progress is notyet apparent—

—although a neweconomic policy has

been announced—

20 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

• interest rates on government bonds and securities have been cut;

• Pakistan’s Eurobonds were successfully rescheduled;

• the government’s support price of wheat has been raised to encouragehigher wheat output and reduce dependence on wheat imports (seeAgriculture); and

• a Rs20bn ($385m) poverty alleviation programme has been set up.

No significant privatisation has taken place in the last two years, despitepromises to the contrary by the last government. One reason was the foot-dragging over restructuring the public sector banks, earmarked as first to go onthe block. The second was a lack of foreign investor confidence, owing partlyto the government’s ongoing dispute over tariffs with the independent powerproducers (IPPs; see Energy). However, all three public sector banksUnitedBank Ltd (UBL), Habib Bank Ltd (HBL) and National Bank of Pakistanhavebeen put on a stronger footing, boosted by the loan default paybacks beingenforced by the NAB. Hence the privatisation of HBL and UBL should beginwithin a couple of months. The government will offload 5-10% of their shareson the local stock exchanges, following which the management of the bankswill be offered to strategic investors later in the year. The government has alsosettled terms with 11 out of the 12 IPPs (see Energy). With the final dispute(with Hub Power Co) expected to be settled soon, the privatisation programmeshould soon start to show some progress.

The oil and gas sector will be among the first sectors to be sold off, with thegovernment’s minority interests in nine oil and gas fields up for grabs. Inaddition, the shares of the Oil and Gas Development Corporation, PakistanPetroleum Ltd, Pakistan State Oil Ltd and gas distribution companies SuiSouthern and Sui Northern will be offered to the public. The government’sminority shares in the nine oil and gas fields will be sold, together with thenon-core assets of the two gas distribution companies such as meter readingand liquefied petroleum gas (LPG). The companies will be sold under the aegisof a newly established Natural Gas Regulatory authority. Pak-Saudi FertiliserLtd, PTCL, Karachi Electric Supply Corporation and Faisalabad Electric SupplyCorporation will all be sold thereafter. A new privatisation law will bepromulgated soon. It will ensure that the proceeds of privatisationwhich thegovernment hopes will exceed $3bnwill be reserved exclusively for debtretirement.

The fate of a few expensive megaprojects launched by the Sharif regime re-mains unclear. Under the former prime minister’s ambitious Housing Scheme,around 500,000 new apartments were to be built for low-income groups at anestimated cost of Rs500bn ($9.6bn). However, despite General Musharraf’s an-nouncement on November 26th that the housing projects would not beshelved, all construction activity related to the projects has ground to a halt,despite the fact that the previous government had issued “letters of accep-tance” to 42 building contractors, directing them to start preliminary surveyand levelling work. According to some estimates, over Rs1bn has already beenspent. Over 70% of the total cost of the scheme was to be funded through

Some megaprojects are leftin the lurch

and work is continuingon a privatisation plan

Pakistan 21

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

credits advanced by the public-sector banks under pressure from the formerprime minister. The World Bank, the SBP and other financial institutions arenot supportive of the housing scheme. But a great deal of time, effort andmoney has already been spent on the project, and pressure from the private-sector contractors to continue with the project is also great.

Prior to his ouster, Mr Sharif had also sanctioned Rs5bn for the IslamabadExpressway, Rs25bn for the Islamabad-Peshawar Motorway and Rs15bn forKarachi-Hyderabad Motorway, all of which are likely to be put on hold now.The same fate awaits the Lahore Ring road project, another favourite of theLahore-based former prime minister.

In January 1999 Pakistan signed an IMF-sponsored agreement with the ParisClub of international creditor countries to reschedule $3.3bn in short- andmedium-term debt. The agreement covers the period July 1998 to December2000 (including arrears). Another such agreement to reschedule $877m in debtwith the London Club of financial institutions was also signed at the sametime. By the end of January, Pakistan had translated these into accords withindividual Paris Club members totalling $1.93bn, while all London Clubdonors had settled terms for $877m. As of late January, the 13 Paris Clubcountries which have agreed to roll over their debt were: US ($926m),Germany ($255m), Russia ($40m), Norway ($11.63m), Sweden ($81m), Austria($22m), Spain ($23m), Netherlands ($30m), Canada ($42m), South Korea($35m), France ($398.6m), Denmark ($4m) and Belgium ($66m). Agreementswith the remaining few Paris Club countries must be reached by February 29th,a revised deadline. Negotiations with a few non-Paris Club countries (such asSaudi Arabia and the United Arab Emirates) are also continuing. Finally, in aseparate agreement, China has agreed to reschedule $250m in long-term debt.

Since May 1999 the IMF has held back the third tranche (worth $280m) of the$1.6bn extended structural adjustment facility (ESAF), signed with Pakistan in1998. The early delays were on account of considerable foot-dragging by theprevious government on fulfilling IMF conditions, such as the imposition ofthe GST, the introduction of an agricultural income tax and an increase inpetroleum and gas prices. Following the military coup in October, the IMFpulled back and awaited the green light from the US to continue talks with thenew administration. When that was forthcoming in November, it dispatched ateam to discuss conditions with the new economic team headed by the financeminister, Mr Aziz.

There are also indications that Mr Aziz is considering abandoning the $1.6bnESAF programme with the IMF, of which nearly $1.1bn remains to bedisbursed. Reasons cited for this are inability to meet the fiscal deficit target(3.3% of GDP for fiscal year 1999/2000, July-June) and the government’sdecision to postpone the application of GST and agricultural income tax to thenext budget. Instead, Mr Aziz may show some interest in negotiating IMF andWorld Bank assistance in funding its poverty alleviation programme. An IMFmission was expected in Islamabad in January but the trip has been postponedpending a review of the economic performance statistics of the last six months.

Debt rescheduling ison course—

—and a new deal with theIMF may be on the cards

22 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

By February 22nd the Karachi Stock Exchange (KSE) index had reached 2,004,an increase of 37.5% since the start of the year. Among the factors responsiblefor a revival of business confidence may be counted the appointment ofMr Aziz as finance minister, his statement that the dispute with Hubco wouldbe settled swiftly and his promise to impose GST and agricultural income taxquickly so that critical IMF conditions would finally be fulfilled and the thirdIMF tranche of $280m would be forthcoming. Sentiment has not beendampened by the delay in either the resolution of the Hubco dispute or theapplication of the new taxes. The continuing rally is backed by high liquidity,following a 2 percentage point cut in interest rates in January.

On December 23rd the supreme court of Pakistan decreed that the applicationof interest was “un-Islamic” and therefore unconstitutional. It ordered the gov-ernment to bring all its financial laws into conformity with Islamic provisionswithin the next six months and warned that foreign loans and investmentbased on Western concepts of interests would not be allowed. This was fol-lowed by an announcement that the SBP had set up an 11-member commis-sion to “carry out, control and supervise the process of transformation of theexisting financial system to one conforming to Islamic shariah”. If the decisionwere to be implemented fully, widespread economic disruption would follow.Foreign entities would be deterred (if not prevented) from investing in Pakistanor extending interest-bearing loans to the government. However, the newpolicy may not be fully implemented. There is no precedent as other countrieswith a Muslim majority population, Muslim theocracies and monarchies allowso-called Muslim financing instruments and banking to co-exist with moreconventional systems which are based around the charging of interest.

The domestic economy

Economic trends

According to the latest report of the State Bank of Pakistan (SBP, the centralbank), during July to December (the first six months of fiscal year 1999/2000),the economy showed “mixed trends”. The good news is that economic re-covery should pick up in the second half of the fiscal year, boosted bystructural reforms and a more stable political environment. Foreign direct in-vestment may pick up once agreements on tariffs have been reached with theindependent power producers (see Energy). Lower real interest rates willstimulate investment. In addition, the government has swapped three ofPakistan’s Eurobonds, together worth $608m, with 90% of the bond holdersaccepting an offer to exchange the three bonds for a 10% six-year bond. Thisshould help towards an upward revision of Pakistan’s credit rating by the majorrating agencies, improving investor confidence. The new government has alsoannounced a package of economic measures including an increase in wheatprices (see Agriculture).

The stockmarket is givena boost—

—but Islamisation rulingsmar investor confidence

Growth is set to pick up

Pakistan 23

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

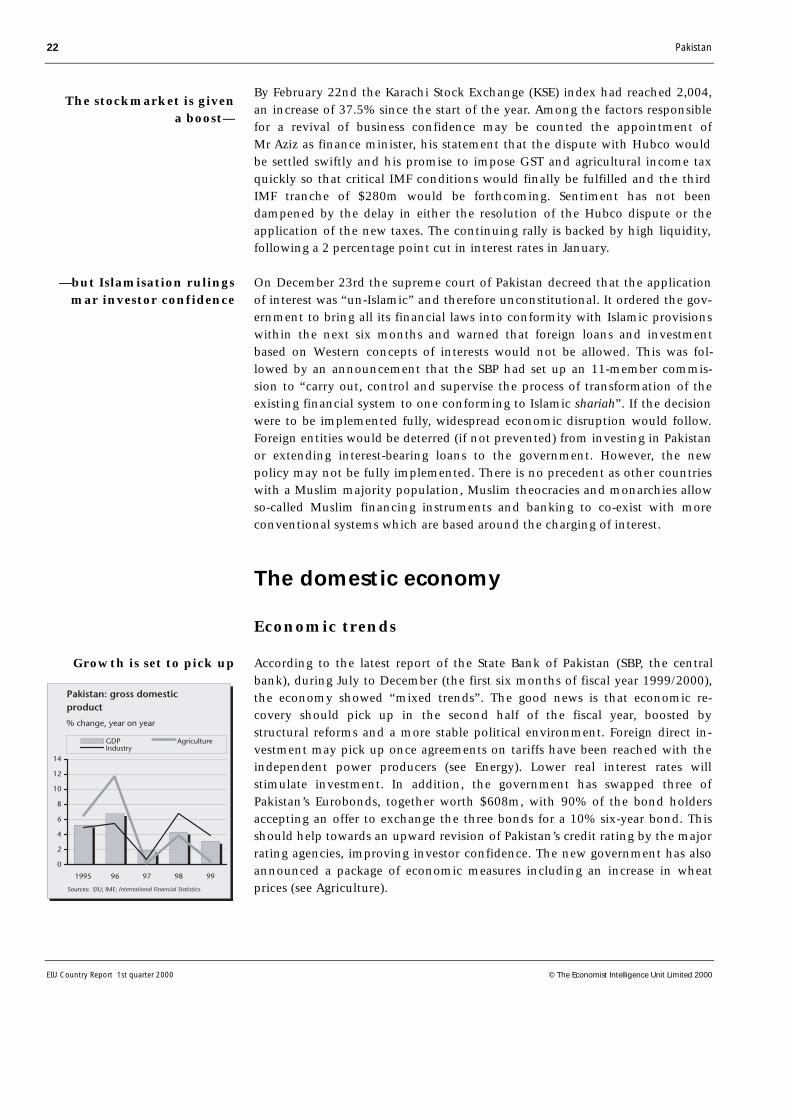

Against this backdrop, GDP is now targeted to grow by at least 4% in the fiscalyear ending June 2000, below the original 5% target set in June 1999 by thethen government, but above the 3.1% growth rate achieved last year(according to the latest revised figures). Following the recent good cottonharvest, the EIU expects slightly higher GDP growth in 1999/2000, of 4.5%.

Buoyed by a crackdown on corruption and tax avoidance, the government hasraised its tax revenue target midway through the 1999/2000 fiscal year fromRs356bn to Rs380bn ($6.9bn to $7.3bn). Total tax collection in the sevenmonth period, July 1999-January 2000, was Rs186bn. Since revenue collectionin the second half of the fiscal year has historically been much higher than thefirst half, the revised target seems realistic. Corporate profits are rising, espe-cially in the resurgent textile sector, while there have been improvements inprocedures for collecting sales tax from the manufacturing sector and whole-sale trade. Revenues have also been boosted by the imposition of a 15% goodsand services tax (GST) on electricity consumption on January 8th, and a toughdrive to identify tax defaulters, by putting them into prison and keeping themthere until they clear their dues. Indeed, if the government had gone aheadand brought in GST on retail trade and imposed an agricultural income tax asoriginally planned, tax revenues for the full fiscal year could have swelledto Rs400bn.

General Musharraf has warned that tax avoidance, whether by traders or agri-culturists, will not be tolerated and army personnel will assist the CentralBoard of Revenue (CBR) in improving tax compliance. The government hasalso given tax evaders until March 31st to “whiten” their undeclared incomes/wealth by voluntarily paying a penalty of 10% of the value of such incomes/wealth so as to avoid possible punitive action. Stringent action to curbsmuggling, which accounts for a loss of at least Rs100bn in taxes, is also beingcontemplated. All in all, the boost to revenue from these varied measures willkeep the budget deficit for 1999/2000 at around 4-5% of GDP.

The bad news is that further tax reform has been postponed until the June2000 budget, while monetary expansion and credit to the private sector haveslowed down, and no privatisation has yet taken place. Further, the tradedeficit has widened sharply, and there has been a net outflow of private capitaltransfers (see Foreign trade and payments).

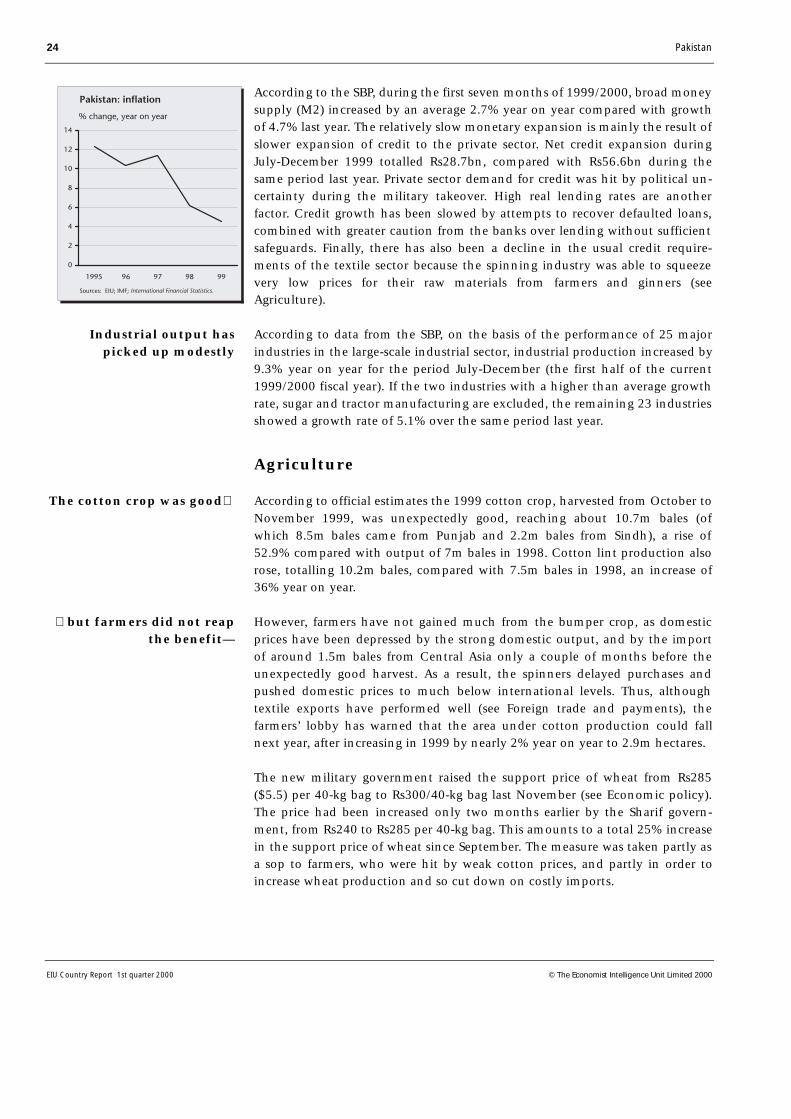

According to data from the SBP, consumer price inflation eased during July-December (the first six months of the current 1999/2000 fiscal year), averagingan annual 3.4%. This was a slowdown compared with the annual 6.5% raterecorded over the same period last year. The slowdown was mainly the result ofslower monetary expansion, and a stable exchange rate. The decline in theprices of a variety of imports (except petroleum), combined with falling tariffs,also helped to reduce import price pressures. Inflation stood at 3.4% year onyear in January. However, world oil prices are now increasing, and domesticenergy price hikes will soon start to feed through into further increases ininflation.

Inflation has eased

Tax revenue is finallyimproving

amid a clampdown ontax avoidance—

but structuralproblems remain

24 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

According to the SBP, during the first seven months of 1999/2000, broad moneysupply (M2) increased by an average 2.7% year on year compared with growthof 4.7% last year. The relatively slow monetary expansion is mainly the result ofslower expansion of credit to the private sector. Net credit expansion duringJuly-December 1999 totalled Rs28.7bn, compared with Rs56.6bn during thesame period last year. Private sector demand for credit was hit by political un-certainty during the military takeover. High real lending rates are anotherfactor. Credit growth has been slowed by attempts to recover defaulted loans,combined with greater caution from the banks over lending without sufficientsafeguards. Finally, there has also been a decline in the usual credit require-ments of the textile sector because the spinning industry was able to squeezevery low prices for their raw materials from farmers and ginners (seeAgriculture).

According to data from the SBP, on the basis of the performance of 25 majorindustries in the large-scale industrial sector, industrial production increased by9.3% year on year for the period July-December (the first half of the current1999/2000 fiscal year). If the two industries with a higher than average growthrate, sugar and tractor manufacturing are excluded, the remaining 23 industriesshowed a growth rate of 5.1% over the same period last year.

Agriculture

According to official estimates the 1999 cotton crop, harvested from October toNovember 1999, was unexpectedly good, reaching about 10.7m bales (ofwhich 8.5m bales came from Punjab and 2.2m bales from Sindh), a rise of52.9% compared with output of 7m bales in 1998. Cotton lint production alsorose, totalling 10.2m bales, compared with 7.5m bales in 1998, an increase of36% year on year.

However, farmers have not gained much from the bumper crop, as domesticprices have been depressed by the strong domestic output, and by the importof around 1.5m bales from Central Asia only a couple of months before theunexpectedly good harvest. As a result, the spinners delayed purchases andpushed domestic prices to much below international levels. Thus, althoughtextile exports have performed well (see Foreign trade and payments), thefarmers’ lobby has warned that the area under cotton production could fallnext year, after increasing in 1999 by nearly 2% year on year to 2.9m hectares.

The new military government raised the support price of wheat from Rs285($5.5) per 40-kg bag to Rs300/40-kg bag last November (see Economic policy).The price had been increased only two months earlier by the Sharif govern-ment, from Rs240 to Rs285 per 40-kg bag. This amounts to a total 25% increasein the support price of wheat since September. The measure was taken partly asa sop to farmers, who were hit by weak cotton prices, and partly in order toincrease wheat production and so cut down on costly imports.

The cotton crop was good

but farmers did not reapthe benefit—

Industrial output haspicked up modestly

Pakistan 25

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

The target for wheat imports for 1999/2000 is 1.6m tonnes, down from 2mtonnes in 1998/99. Pakistan requires about 19m tonnes of wheat a year fordomestic consumption while around 2m tonnes a year are sold to Afghanistan(in addition, large quantities of wheat are smuggled into Afghanistan eachyear). Domestic production is targeted at 20m tonnes this year. Hence importsof only around 1m are needed; the additional 600,000 tonnes are intended torestore buffer stocks that have been depleted in recent months, as foreignexchange shortages have curtailed wheat imports. It is understood that the USDepartment of Agriculture will provide $125m in credits to fund wheatimports in the current year.

Pakistan: wheat imports(fiscal years, Jul-Jun)

1999/1995/96 1996/97 1997/98 1998/99 2000a

Wheat imports (m tonnes) 1.9 2.4 4.1 2.0 1.6

$ value 439 451 712 254 n/a

a Plan target.

Source: Ministry of Agriculture.

According to data from the Ministry of Agriculture, sugarcane production wasestimated at 43.18m tonnes in 1999, a drop of 21.8% compared with 55.19mtonnes in 1998. The area under sugarcane cultivation dropped by 9%, from1.115m ha to 1.015m ha. The main reasons cited for the fall in sugar output are:

• difficulties faced by the sugar industry in exporting surplus production lastyear which led to delayed payments to farmers by sugar manufacturers;

• higher electricity charges for farmers; and

• low rainfall in sugarcane-growing areas at sowing time combined withheavy rainfall and storms while the crop was still standing.

Exports will be hit by lower output and by the cut in subsidies (last year, exportsubsidies to a select group of sugar manufacturers dominated by the formerprime minister’s family became a scandal, with the result that this year thegovernment has announced that it will not subsidise sugar exports).

Rice exports reached 471,991 tonnes, worth $164.3m, during July-November1999, an increase of 11.7% on the year-earlier period in dollar terms. The ricecrop has also touched a record figure of 4.9m tonnes, leaving about 2m tonnesavailable for export.

Energy

The government’s dispute with the Hub Power Company (Hubco) seems to beinching towards a resolution. The supreme court of Pakistan has begun regularhearings of the petition by the Water and Power Development Authority(WAPDA) precluding Hubco from taking the dispute to an international court

Sugar is not so sweet

The dispute with Hubcomay be finally resolved

in the hope of boostingproduction andcutting imports

Rice exports are up

26 Pakistan

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

for arbitration. It is also understood that the finance minister, Shaukat Aziz, isvery keen on a speedy settlement so that the route for restoration of IMF andWorld Bank assistance to Pakistan is clear. The last stumbling block remains thechairman of WAPDA, General Zulfikar Ali, who has alleged that Hubco, incahoots with the Bhutto government, renegotiated unacceptably high powerrates in 1994 and has since overcharged the government of Pakistan. However,on February 12th WAPDA finally offered to pay 5.4 cents per unit power buy-back to Hubco in the final round of a series of negotiations to find a mutuallyacceptable rate. Hubco had suggested a rate of 6.1 cents on December 7th.

WAPDA authorities claim that the organisation has finally come out of its four-year financial crisis and posted a provisional profit of Rs12.4bn in the July-December 1999 period. This is largely because the government has agreed toconvert a liability of Rs36.4bn against WAPDA into equity, raising total govern-ment equity in the corporation to Rs47bn. Out of Rs62bn in outstandingliabilities, Rs49bn is due from the federal and provincial governments whilethe rest is from the private sector. In turn, WAPDA’s payables amount toRs41.8bn. The improvement in WAPDA’s finances may prove shortlived, how-ever, once the disagreement with Hubco is settled. WAPDA has earmarkedRs11.8bn as a contingency liability fund to pay Hubco in the event of a settle-ment on WAPDA’s terms. Once this is paid out, its profit will becomenegligible. But if WAPDA is obliged to pay more to Hubco, it will go into thered again.

Foreign trade and payments

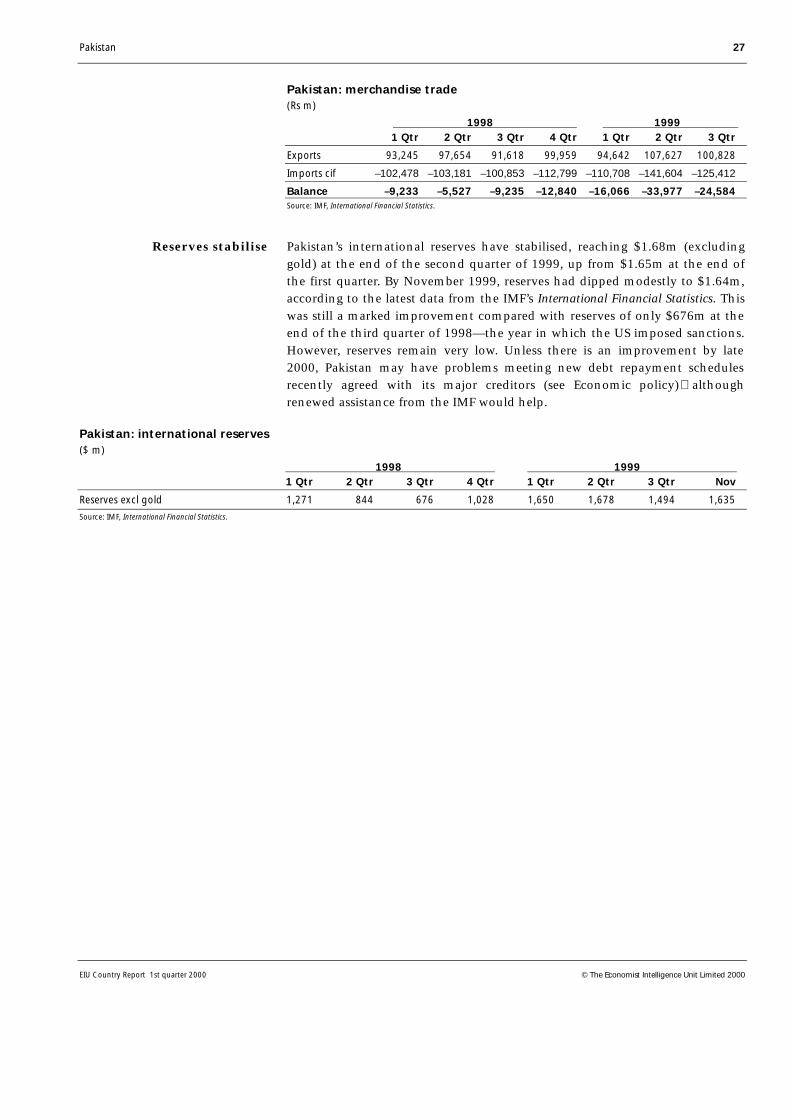

According to data from the IMF’s International Financial Statistics, during theperiod July-September (the first quarter of the current fiscal year), merchandiseexports reached Rs100.8bn ($1.9bn), an increase of 10.1% year on yearcompared with the same period of 1998/99. However, imports (customs basis,cif), jumped by a huge 66.2% year on year in July-September compared withthe year-earlier period, to Rs125.4bn. As a result, the merchandise trade deficitwidened to Rs24.6bn, compared with only Rs9.2bn in July-September 1998.

According to press reports covering more recent data, imports in the seven-month period from July 1999 to January 2000 totalled $5.75bn while exportswere $4.74bn, leaving a merchandise trade deficit of $1.01bn. Merchandiseexports have risen consistently in recent months, picking up by 5.3 % inSeptember, 6.3% in October, 14.1% in November and 8.12% in December 1999over the same months in the preceding year. This export growth has largelybeen on the back of the textiles industry which has been spurred both by agood cotton crop and low prices of lint at home as well as an upturn in worldtrade. Textiles exports totalled $3.1bn in July 1999-January 2000, up by 10.5%compared with the same period of 1998, according to press reports. Riceexports have also picked up (see Agriculture).

WAPDA may be out ofthe red

The merchandise tradedeficit widens

Pakistan 27

EIU Country Report 1st quarter 2000 © The Economist Intelligence Unit Limited 2000

Pakistan: merchandise trade(Rs m)

1998 1999 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr

Exports 93,245 97,654 91,618 99,959 94,642 107,627 100,828

Imports cif –102,478 –103,181 –100,853 –112,799 –110,708 –141,604 –125,412

Balance –9,233 –5,527 –9,235 –12,840 –16,066 –33,977 –24,584Source: IMF, International Financial Statistics.

Pakistan’s international reserves have stabilised, reaching $1.68m (excludinggold) at the end of the second quarter of 1999, up from $1.65m at the end ofthe first quarter. By November 1999, reserves had dipped modestly to $1.64m,according to the latest data from the IMF’s International Financial Statistics. Thiswas still a marked improvement compared with reserves of only $676m at theend of the third quarter of 1998—the year in which the US imposed sanctions.However, reserves remain very low. Unless there is an improvement by late2000, Pakistan may have problems meeting new debt repayment schedulesrecently agreed with its major creditors (see Economic policy)althoughrenewed assistance from the IMF would help.

Pakistan: international reserves($ m)

1998 1999 1 Qtr 2 Qtr 3 Qtr 4 Qtr 1 Qtr 2 Qtr 3 Qtr Nov

Reserves excl gold 1,271 844 676 1,028 1,650 1,678 1,494 1,635

Source: IMF, International Financial Statistics.

Reserves stabilise

28 Afghanistan

Afghanistan

Political structure