Overweight (no change) Upside potential intact for our top ... · Technology│Singapore│Tech...

52

Technology│Singapore│July 4, 2017 Sector Note │ Alpha series IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH. Powered by the EFA Platform Tech Manufacturing Services Upside potential intact for our top picks ■ Industry forecasters Gartner and SEMI believe the semiconductor equipment upcycle will last until 2018F, with automotive and Internet of Things (IoT) as long-term themes. ■ We believe further re-rating for tech manufacturing services stocks would have to come from positive earnings surprises, M&As or special dividends. ■ We opine that an M&A between Memtech and Sunningdale would have merits. ■ Our top picks are AEM, Jadason, Memtech and Sunningdale. Where are we in the cycle? Of the eight tech manufacturing services stocks that we currently cover, three can be classified as electronic manufacturing services providers, two as suppliers for companies in the semiconductor industry, two are in the plastic injection moulding business and one in the printed circuit board (PCB) drilling space. As these eight companies serve a diverse industry, we think a better way to assess if their share prices would re-rate is to look at the companies individually, rather than at the overall industry. Potential re-rating catalyst 1 - earnings For the tech manufacturing services stocks under our coverage, we opine that further re- rating could come from earnings outperformance, as well as better-than-expected long- term prospects. We note that Memtech, Valuetronics and Venture have room to surprise investors with possible new order wins or more orders from existing customers. AEM could also deliver positive earnings surprises as operating efficiencies improve and production shifts to lower-cost Penang in 2H17F. Potential re-rating catalyst 2 - earnings-accretive M&As The second potential re-rating catalyst is earnings-accretive M&As. We note that companies such as Venture and Valuetronics were in net cash position at end-1Q17 and are likely to be interested in decent-sized companies with technological capability. In the plastic injection moulding space, we believe there could be synergies arising from Sunningdale acquiring Memtech. As for AEM, given its strong test handler capability, the acquisition of a small tester maker could help it develop new revenue streams. Potential re-rating catalyst 3 - special dividends Looking at FY17F dividend coverage based on our free cash flow estimates (see Figure 15), we opine that Sunningdale has room to beat our DPS assumption for FY17F. We also note that UMS has a track record of paying large special dividends when it reports strong earnings. Given that we are forecasting record-high FY17F net profit of S$40.2m for UMS, we believe the company may pay a high special DPS for FY17F. Memtech could also pay special DPS in FY17F, backed by US$5.7m proceeds from sale of assets. Our top picks Our current small-cap tech manufacturing services picks with more than 20% upside to our target prices are: 1) AEM, 2) Jadason, 3) Sunningdale, and 4) Memtech. Of these four stocks, we believe Memtech and Sunningdale offer some margin of safety as both stocks are currently trading below their book values. Key risk to the sector is order pullback by customers. Figure 1: CIMB Singapore tech manufacturing services coverage SOURCES: CIMB, COMPANY REPORTS Singapore Overweight (no change) Highlighted companies AEM Holdings Ltd ADD, TP S$3.39, S$2.20 close AEM is a leading semiconductor test handler supplier to a major North American semiconductor company. Its test handler products are patented, setting back would-be competitors by 2-3 years. Jadason Enterprises Limited ADD, TP S$0.17, S$0.10 close Jadason is a leading PCB driller based mainly in Dongguan, China. The company also has a plant in Suzhou. Its main business is the drilling of PCBs, as well as the distribution of PCB drilling machines. Memtech International ADD, TP S$1.09, S$0.91 close Memtech is a precision engineering company that has successfully transformed from a keypad components manufacturer into an established supplier to both the automotive and consumer electronics industries. Summary valuation metrics Analyst(s) William TNG, CFA T (65) 6210 8676 E [email protected] NGOH Yi Sin T (65) 6210 8604 E [email protected] P/E (x) Dec-17F Dec-18F Dec-19F AEM Holdings Ltd 7.70 6.49 5.83 Jadason Enterprises Limited 10.98 7.42 7.10 Memtech International 10.20 8.31 6.81 P/BV (x) Dec-17F Dec-18F Dec-19F AEM Holdings Ltd 3.26 2.37 1.81 Jadason Enterprises Limited 1.33 1.22 1.13 Memtech International 0.80 0.75 0.71 Dividend Yield Dec-17F Dec-18F Dec-19F AEM Holdings Ltd 3.25% 3.85% 4.29% Jadason Enterprises Limited 4.55% 6.74% 7.05% Memtech International 3.87% 4.76% 5.82% Bloomberg Price Target Price Market Cap Core P/E (x) 3-year EPS P/BV (x) Recurring ROE (%) Dividend Yield (%) Company Ticker Recom. (lcl curr) (lcl curr) (US$ m) CY17F CY18F CAGR (%) CY17F CY17F CY17F AEM Holdings Ltd AEM SP ADD 2.20 3.39 103.6 7.7 6.5 75.5% 3.26 48.8% 3.2% CEI Limited CEI SP ADD 1.06 1.11 66.5 9.5 8.8 8.3% 2.18 22.9% 8.4% Jadason Enterprises Limited JAD SP ADD 0.10 0.17 52.5 11.0 7.4 68.6% 1.33 12.2% 4.6% Memtech International MTEC SP ADD 0.91 1.09 92.3 10.2 8.3 32.8% 0.80 8.0% 3.9% Sunningdale Tech Ltd SUNN SP ADD 1.77 2.19 240.2 8.8 7.9 3.4% 0.89 10.2% 4.6% UMS Holdings Ltd UMSH SP ADD 1.00 1.15 309.0 10.6 9.7 19.6% 2.09 20.0% 6.0% Valuetronics Holdings Ltd VALUE SP ADD 0.79 0.89 238.9 11.0 9.7 13.5% 1.85 17.6% 4.5% Venture Corporation VMS SP HOLD 11.89 12.01 2,426.0 15.9 14.3 13.2% 1.63 10.3% 4.2% Weighted average 13.3 11.8 15.2% 1.57 11.9% 4.5%

Transcript of Overweight (no change) Upside potential intact for our top ... · Technology│Singapore│Tech...

Technology│Singapore│July 4, 2017

Sector Note │ Alpha series

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Tech Manufacturing Services Upside potential intact for our top picks ■ Industry forecasters Gartner and SEMI believe the semiconductor equipment upcycle

will last until 2018F, with automotive and Internet of Things (IoT) as long-term themes. ■ We believe further re-rating for tech manufacturing services stocks would have to

come from positive earnings surprises, M&As or special dividends. ■ We opine that an M&A between Memtech and Sunningdale would have merits. ■ Our top picks are AEM, Jadason, Memtech and Sunningdale.

Where are we in the cycle? Of the eight tech manufacturing services stocks that we currently cover, three can be classified as electronic manufacturing services providers, two as suppliers for companies in the semiconductor industry, two are in the plastic injection moulding business and one in the printed circuit board (PCB) drilling space. As these eight companies serve a diverse industry, we think a better way to assess if their share prices would re-rate is to look at the companies individually, rather than at the overall industry.

Potential re-rating catalyst 1 - earnings For the tech manufacturing services stocks under our coverage, we opine that further re-rating could come from earnings outperformance, as well as better-than-expected long-term prospects. We note that Memtech, Valuetronics and Venture have room to surprise investors with possible new order wins or more orders from existing customers. AEM could also deliver positive earnings surprises as operating efficiencies improve and production shifts to lower-cost Penang in 2H17F.

Potential re-rating catalyst 2 - earnings-accretive M&As The second potential re-rating catalyst is earnings-accretive M&As. We note that companies such as Venture and Valuetronics were in net cash position at end-1Q17 and are likely to be interested in decent-sized companies with technological capability. In the plastic injection moulding space, we believe there could be synergies arising from Sunningdale acquiring Memtech. As for AEM, given its strong test handler capability, the acquisition of a small tester maker could help it develop new revenue streams.

Potential re-rating catalyst 3 - special dividends Looking at FY17F dividend coverage based on our free cash flow estimates (see Figure 15), we opine that Sunningdale has room to beat our DPS assumption for FY17F. We also note that UMS has a track record of paying large special dividends when it reports strong earnings. Given that we are forecasting record-high FY17F net profit of S$40.2m for UMS, we believe the company may pay a high special DPS for FY17F. Memtech could also pay special DPS in FY17F, backed by US$5.7m proceeds from sale of assets.

Our top picks Our current small-cap tech manufacturing services picks with more than 20% upside to our target prices are: 1) AEM, 2) Jadason, 3) Sunningdale, and 4) Memtech. Of these four stocks, we believe Memtech and Sunningdale offer some margin of safety as both stocks are currently trading below their book values. Key risk to the sector is order pullback by customers.

Figure 1: CIMB Singapore tech manufacturing services coverage

SOURCES: CIMB, COMPANY REPORTS

Singapore

Overweight (no change)

Highlighted companies AEM Holdings Ltd ADD, TP S$3.39, S$2.20 close AEM is a leading semiconductor test handler supplier to a major North American semiconductor company. Its test handler products are patented, setting back would-be competitors by 2-3 years. Jadason Enterprises Limited ADD, TP S$0.17, S$0.10 close Jadason is a leading PCB driller based mainly in Dongguan, China. The company also has a plant in Suzhou. Its main business is the drilling of PCBs, as well as the distribution of PCB drilling machines. Memtech International ADD, TP S$1.09, S$0.91 close Memtech is a precision engineering company that has successfully transformed from a keypad components manufacturer into an established supplier to both the automotive and consumer electronics industries. Summary valuation metrics

Analyst(s)

William TNG, CFA T (65) 6210 8676 E [email protected] NGOH Yi Sin T (65) 6210 8604 E [email protected]

P/E (x) Dec-17F Dec-18F Dec-19FAEM Holdings Ltd 7.70 6.49 5.83 Jadason Enterprises Limited 10.98 7.42 7.10 Memtech International 10.20 8.31 6.81

P/BV (x) Dec-17F Dec-18F Dec-19FAEM Holdings Ltd 3.26 2.37 1.81 Jadason Enterprises Limited 1.33 1.22 1.13 Memtech International 0.80 0.75 0.71

Dividend Yield Dec-17F Dec-18F Dec-19FAEM Holdings Ltd 3.25% 3.85% 4.29%Jadason Enterprises Limited 4.55% 6.74% 7.05%Memtech International 3.87% 4.76% 5.82%

Bloomberg PriceTarget

PriceMarket

Cap Core P/E (x) 3-year EPS P/BV (x)Recurring

ROE (%)Dividend Yield (%)

Company Ticker Recom. (lcl curr) (lcl curr) (US$ m) CY17F CY18F CAGR (%) CY17F CY17F CY17F

AEM Holdings Ltd AEM SP ADD 2.20 3.39 103.6 7.7 6.5 75.5% 3.26 48.8% 3.2%CEI Limited CEI SP ADD 1.06 1.11 66.5 9.5 8.8 8.3% 2.18 22.9% 8.4%Jadason Enterprises Limited JAD SP ADD 0.10 0.17 52.5 11.0 7.4 68.6% 1.33 12.2% 4.6%Memtech International MTEC SP ADD 0.91 1.09 92.3 10.2 8.3 32.8% 0.80 8.0% 3.9%Sunningdale Tech Ltd SUNN SP ADD 1.77 2.19 240.2 8.8 7.9 3.4% 0.89 10.2% 4.6%UMS Holdings Ltd UMSH SP ADD 1.00 1.15 309.0 10.6 9.7 19.6% 2.09 20.0% 6.0%Valuetronics Holdings Ltd VALUE SP ADD 0.79 0.89 238.9 11.0 9.7 13.5% 1.85 17.6% 4.5%Venture Corporation VMS SP HOLD 11.89 12.01 2,426.0 15.9 14.3 13.2% 1.63 10.3% 4.2%Weighted average 13.3 11.8 15.2% 1.57 11.9% 4.5%

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

2

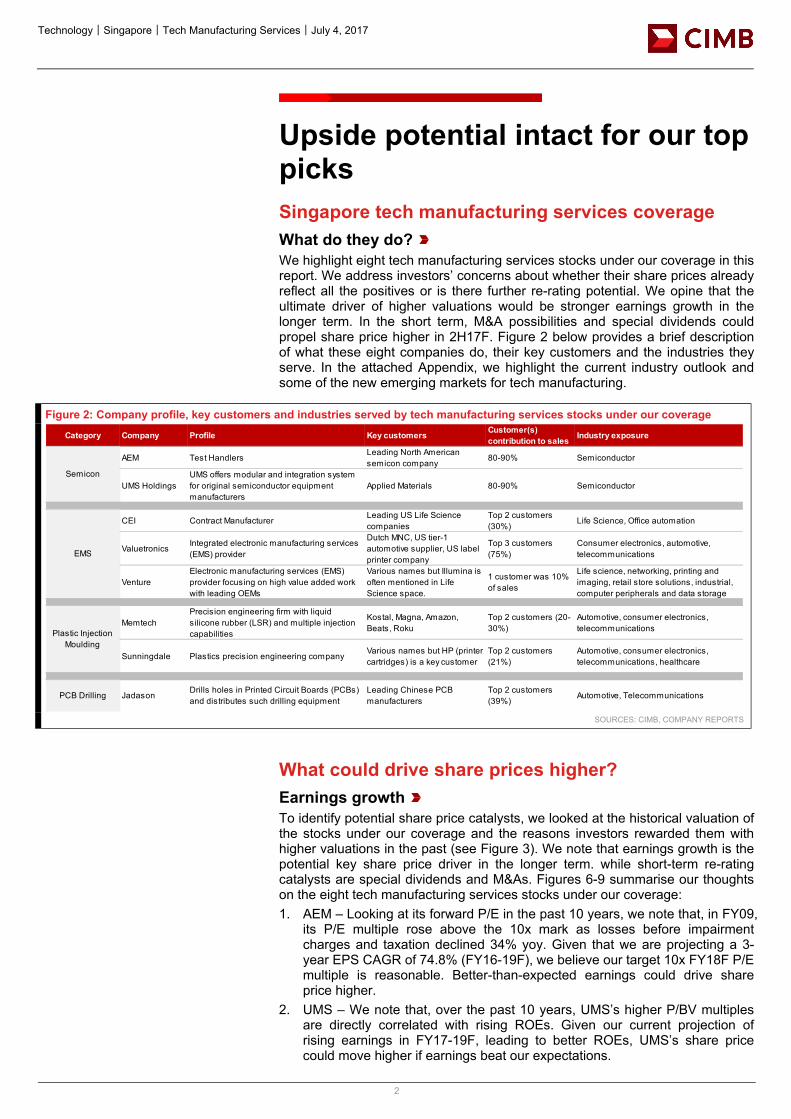

Upside potential intact for our top picks Singapore tech manufacturing services coverage What do they do? We highlight eight tech manufacturing services stocks under our coverage in this report. We address investors’ concerns about whether their share prices already reflect all the positives or is there further re-rating potential. We opine that the ultimate driver of higher valuations would be stronger earnings growth in the longer term. In the short term, M&A possibilities and special dividends could propel share price higher in 2H17F. Figure 2 below provides a brief description of what these eight companies do, their key customers and the industries they serve. In the attached Appendix, we highlight the current industry outlook and some of the new emerging markets for tech manufacturing.

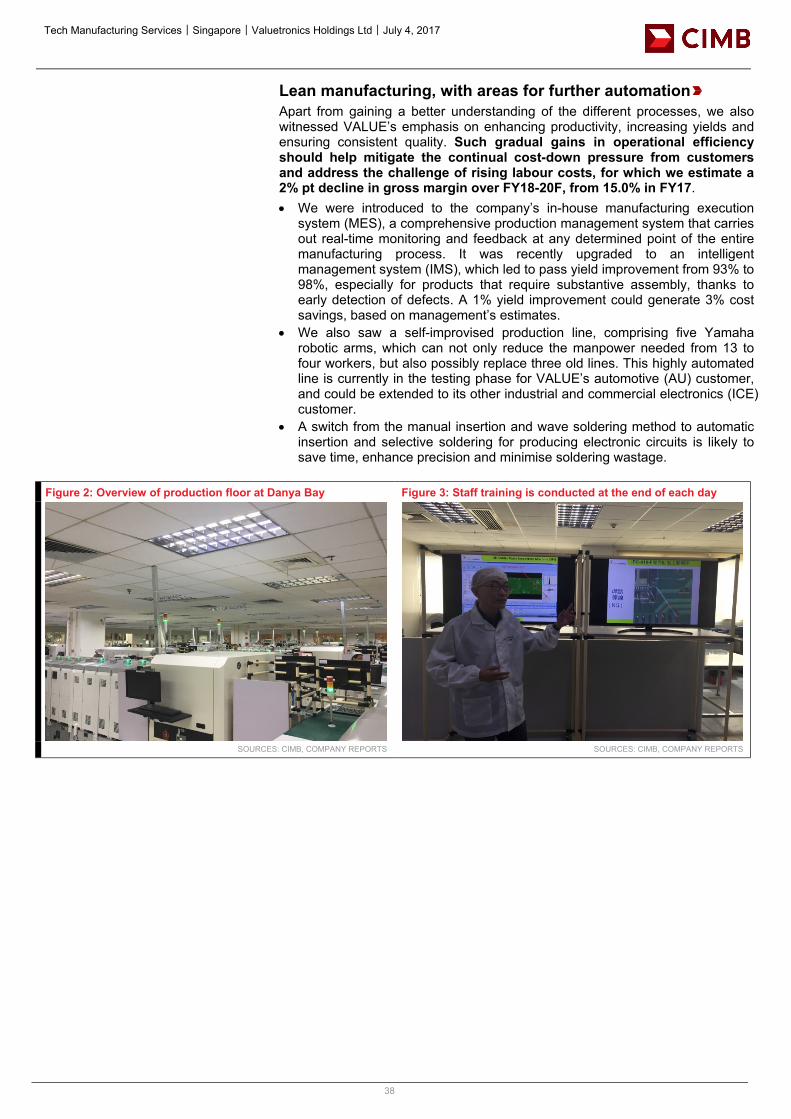

Figure 2: Company profile, key customers and industries served by tech manufacturing services stocks under our coverage

SOURCES: CIMB, COMPANY REPORTS

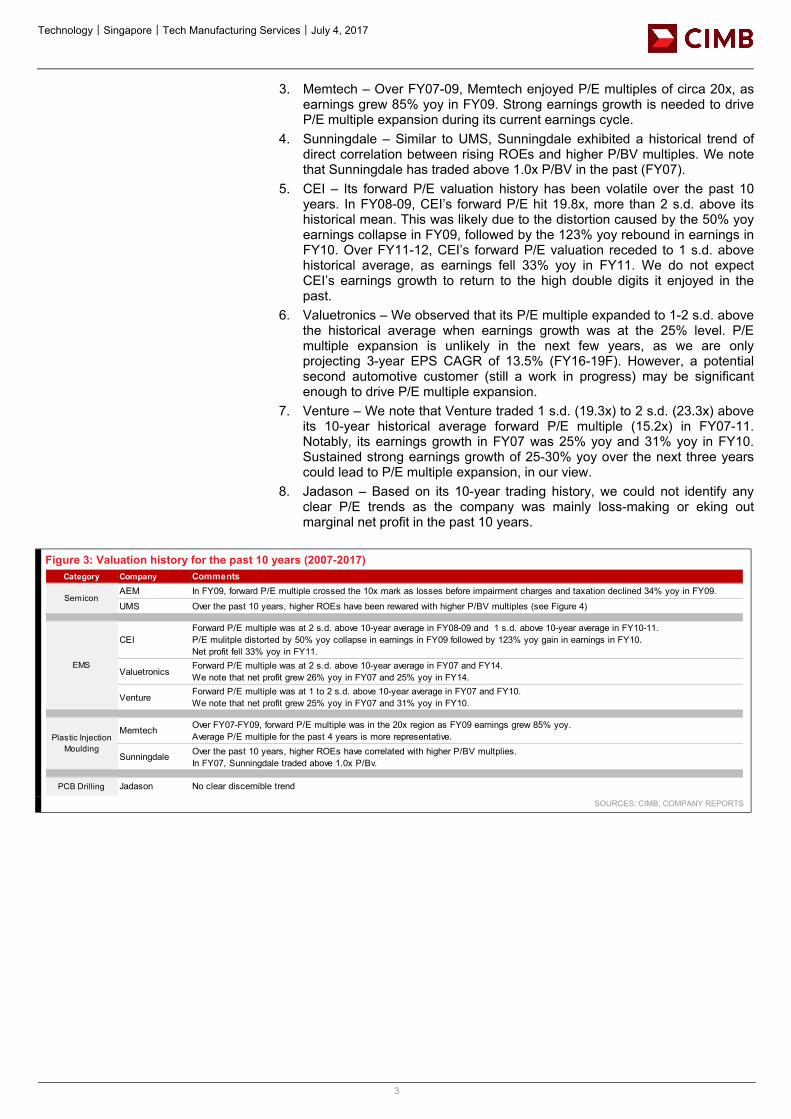

What could drive share prices higher? Earnings growth To identify potential share price catalysts, we looked at the historical valuation of the stocks under our coverage and the reasons investors rewarded them with higher valuations in the past (see Figure 3). We note that earnings growth is the potential key share price driver in the longer term. while short-term re-rating catalysts are special dividends and M&As. Figures 6-9 summarise our thoughts on the eight tech manufacturing services stocks under our coverage: 1. AEM – Looking at its forward P/E in the past 10 years, we note that, in FY09,

its P/E multiple rose above the 10x mark as losses before impairment charges and taxation declined 34% yoy. Given that we are projecting a 3-year EPS CAGR of 74.8% (FY16-19F), we believe our target 10x FY18F P/E multiple is reasonable. Better-than-expected earnings could drive share price higher.

2. UMS – We note that, over the past 10 years, UMS’s higher P/BV multiples are directly correlated with rising ROEs. Given our current projection of rising earnings in FY17-19F, leading to better ROEs, UMS’s share price could move higher if earnings beat our expectations.

Category Company Profile Key customers Customer(s) contribution to sales Industry exposure

AEM Test HandlersLeading North American semicon company

80-90% Semiconductor

UMS HoldingsUMS offers modular and integration system for original semiconductor equipment manufacturers

Applied Materials 80-90% Semiconductor

CEI Contract ManufacturerLeading US Life Science companies

Top 2 customers (30%)

Life Science, Office automation

ValuetronicsIntegrated electronic manufacturing services (EMS) provider

Dutch MNC, US tier-1 automotive supplier, US label printer company

Top 3 customers (75%)

Consumer electronics, automotive, telecommunications

VentureElectronic manufacturing services (EMS) provider focusing on high value added work with leading OEMs

Various names but Illumina is often mentioned in Life Science space.

1 customer was 10% of sales

Life science, networking, printing and imaging, retail store solutions, industrial, computer peripherals and data storage

MemtechPrecision engineering firm with liquid silicone rubber (LSR) and multiple injection capabilities

Kostal, Magna, Amazon, Beats, Roku

Top 2 customers (20-30%)

Automotive, consumer electronics, telecommunications

Sunningdale Plastics precision engineering companyVarious names but HP (printer cartridges) is a key customer

Top 2 customers (21%)

Automotive, consumer electronics, telecommunications, healthcare

PCB Drilling Jadason Drills holes in Printed Circuit Boards (PCBs) and distributes such drilling equipment

Leading Chinese PCB manufacturers

Top 2 customers (39%)

Automotive, Telecommunications

Semicon

EMS

Plastic Injection Moulding

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

3

3. Memtech – Over FY07-09, Memtech enjoyed P/E multiples of circa 20x, as earnings grew 85% yoy in FY09. Strong earnings growth is needed to drive P/E multiple expansion during its current earnings cycle.

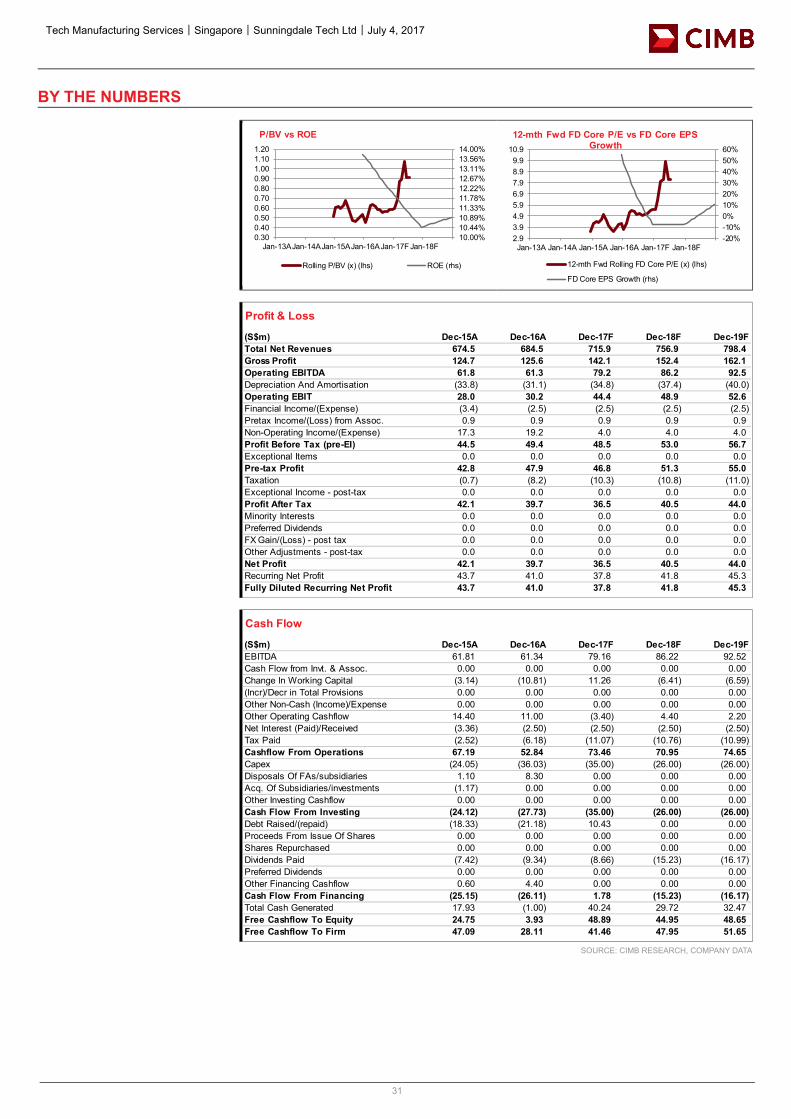

4. Sunningdale – Similar to UMS, Sunningdale exhibited a historical trend of direct correlation between rising ROEs and higher P/BV multiples. We note that Sunningdale has traded above 1.0x P/BV in the past (FY07).

5. CEI – Its forward P/E valuation history has been volatile over the past 10 years. In FY08-09, CEI’s forward P/E hit 19.8x, more than 2 s.d. above its historical mean. This was likely due to the distortion caused by the 50% yoy earnings collapse in FY09, followed by the 123% yoy rebound in earnings in FY10. Over FY11-12, CEI’s forward P/E valuation receded to 1 s.d. above historical average, as earnings fell 33% yoy in FY11. We do not expect CEI’s earnings growth to return to the high double digits it enjoyed in the past.

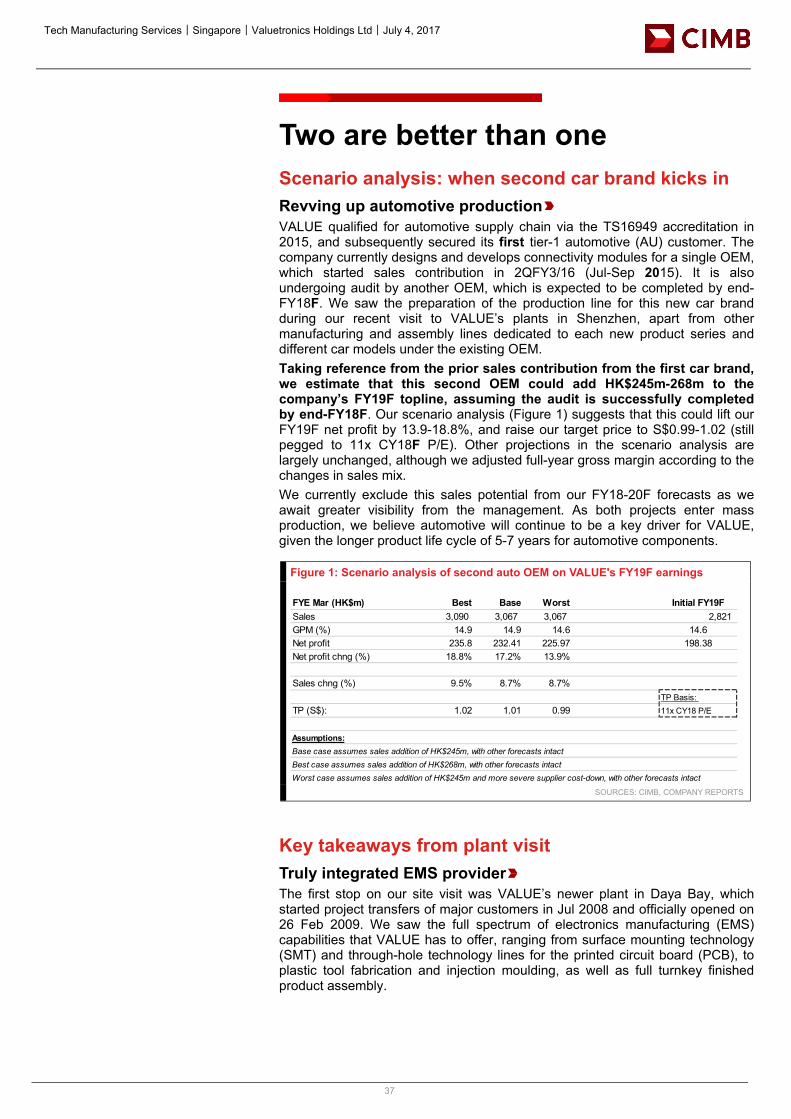

6. Valuetronics – We observed that its P/E multiple expanded to 1-2 s.d. above the historical average when earnings growth was at the 25% level. P/E multiple expansion is unlikely in the next few years, as we are only projecting 3-year EPS CAGR of 13.5% (FY16-19F). However, a potential second automotive customer (still a work in progress) may be significant enough to drive P/E multiple expansion.

7. Venture – We note that Venture traded 1 s.d. (19.3x) to 2 s.d. (23.3x) above its 10-year historical average forward P/E multiple (15.2x) in FY07-11. Notably, its earnings growth in FY07 was 25% yoy and 31% yoy in FY10. Sustained strong earnings growth of 25-30% yoy over the next three years could lead to P/E multiple expansion, in our view.

8. Jadason – Based on its 10-year trading history, we could not identify any clear P/E trends as the company was mainly loss-making or eking out marginal net profit in the past 10 years.

Figure 3: Valuation history for the past 10 years (2007-2017)

SOURCES: CIMB, COMPANY REPORTS

Category Company CommentsAEM In FY09, forward P/E multiple crossed the 10x mark as losses before impairment charges and taxation declined 34% yoy in FY09.

UMS Over the past 10 years, higher ROEs have been rewared with higher P/BV multiples (see Figure 4)

CEIForward P/E multiple was at 2 s.d. above 10-year average in FY08-09 and 1 s.d. above 10-year average in FY10-11.P/E mulitple distorted by 50% yoy collapse in earnings in FY09 followed by 123% yoy gain in earnings in FY10.Net profit fell 33% yoy in FY11.

ValuetronicsForward P/E multiple was at 2 s.d. above 10-year average in FY07 and FY14. We note that net profit grew 26% yoy in FY07 and 25% yoy in FY14.

VentureForward P/E multiple was at 1 to 2 s.d. above 10-year average in FY07 and FY10.We note that net profit grew 25% yoy in FY07 and 31% yoy in FY10.

Memtech Over FY07-FY09, forward P/E multiple was in the 20x region as FY09 earnings grew 85% yoy. Average P/E multiple for the past 4 years is more representative.

Sunningdale Over the past 10 years, higher ROEs have correlated with higher P/BV multplies. In FY07, Sunningdale traded above 1.0x P/Bv.

PCB Drilling Jadason No clear discernible trend

Semicon

Plastic Injection Moulding

EMS

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

4

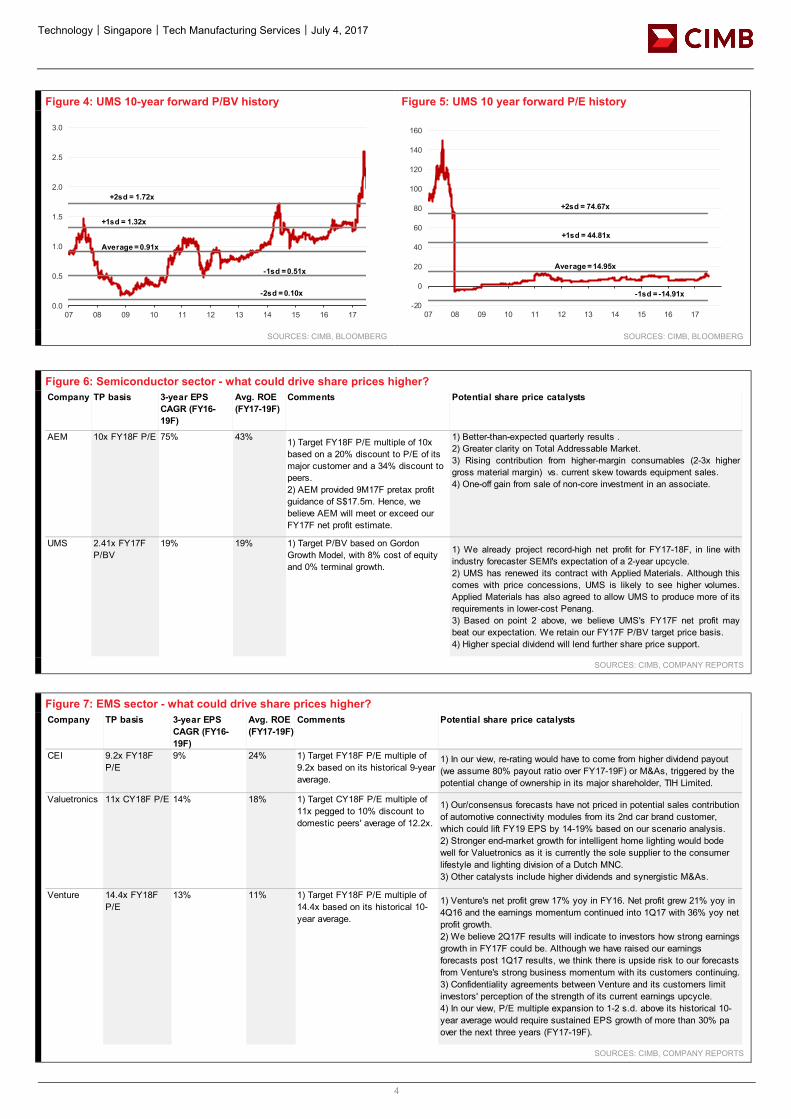

Figure 4: UMS 10-year forward P/BV history Figure 5: UMS 10 year forward P/E history

SOURCES: CIMB, BLOOMBERG SOURCES: CIMB, BLOOMBERG

Figure 6: Semiconductor sector - what could drive share prices higher?

SOURCES: CIMB, COMPANY REPORTS

Figure 7: EMS sector - what could drive share prices higher?

SOURCES: CIMB, COMPANY REPORTS

0.0

0.5

1.0

1.5

2.0

2.5

3.0

07 08 09 10 11 12 13 14 15 16 17

Average = 0.91x

+1sd = 1.32x

-1sd = 0.51x

+2sd = 1.72x

-2sd = 0.10x

-20

0

20

40

60

80

100

120

140

160

07 08 09 10 11 12 13 14 15 16 17

Average = 14.95x

+1sd = 44.81x

-1sd = -14.91x

+2sd = 74.67x

Company TP basis 3-year EPS CAGR (FY16-19F)

Avg. ROE (FY17-19F)

Comments Potential share price catalysts

AEM 10x FY18F P/E 75% 43% 1) Target FY18F P/E multiple of 10x based on a 20% discount to P/E of its major customer and a 34% discount to peers.2) AEM provided 9M17F pretax profit guidance of S$17.5m. Hence, we believe AEM will meet or exceed our FY17F net profit estimate.

1) Better-than-expected quarterly results .2) Greater clarity on Total Addressable Market.3) Rising contribution from higher-margin consumables (2-3x highergross material margin) vs. current skew towards equipment sales.4) One-off gain from sale of non-core investment in an associate.

UMS 2.41x FY17F P/BV

19% 19% 1) Target P/BV based on Gordon Growth Model, with 8% cost of equity and 0% terminal growth.

1) We already project record-high net profit for FY17-18F, in line withindustry forecaster SEMI's expectation of a 2-year upcycle.2) UMS has renewed its contract with Applied Materials. Although thiscomes with price concessions, UMS is likely to see higher volumes.Applied Materials has also agreed to allow UMS to produce more of itsrequirements in lower-cost Penang.3) Based on point 2 above, we believe UMS's FY17F net profit maybeat our expectation. We retain our FY17F P/BV target price basis.4) Higher special dividend will lend further share price support.

Company TP basis 3-year EPS CAGR (FY16-19F)

Avg. ROE (FY17-19F)

Comments Potential share price catalysts

CEI 9.2x FY18F P/E

9% 24% 1) Target FY18F P/E multiple of 9.2x based on its historical 9-year average.

1) In our view, re-rating would have to come from higher dividend payout (we assume 80% payout ratio over FY17-19F) or M&As, triggered by the potential change of ownership in its major shareholder, TIH Limited.

Valuetronics 11x CY18F P/E 14% 18% 1) Target CY18F P/E multiple of 11x pegged to 10% discount to domestic peers' average of 12.2x.

1) Our/consensus forecasts have not priced in potential sales contribution of automotive connectivity modules from its 2nd car brand customer, which could lift FY19 EPS by 14-19% based on our scenario analysis.2) Stronger end-market growth for intelligent home lighting would bode well for Valuetronics as it is currently the sole supplier to the consumer lifestyle and lighting division of a Dutch MNC. 3) Other catalysts include higher dividends and synergistic M&As.

Venture 14.4x FY18F P/E

13% 11% 1) Target FY18F P/E multiple of 14.4x based on its historical 10-year average.

1) Venture's net profit grew 17% yoy in FY16. Net profit grew 21% yoy in 4Q16 and the earnings momentum continued into 1Q17 with 36% yoy net profit growth.2) We believe 2Q17F results will indicate to investors how strong earnings growth in FY17F could be. Although we have raised our earnings forecasts post 1Q17 results, we think there is upside risk to our forecasts from Venture's strong business momentum with its customers continuing.3) Confidentiality agreements between Venture and its customers limit investors' perception of the strength of its current earnings upcycle.4) In our view, P/E multiple expansion to 1-2 s.d. above its historical 10-year average would require sustained EPS growth of more than 30% pa over the next three years (FY17-19F).

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

5

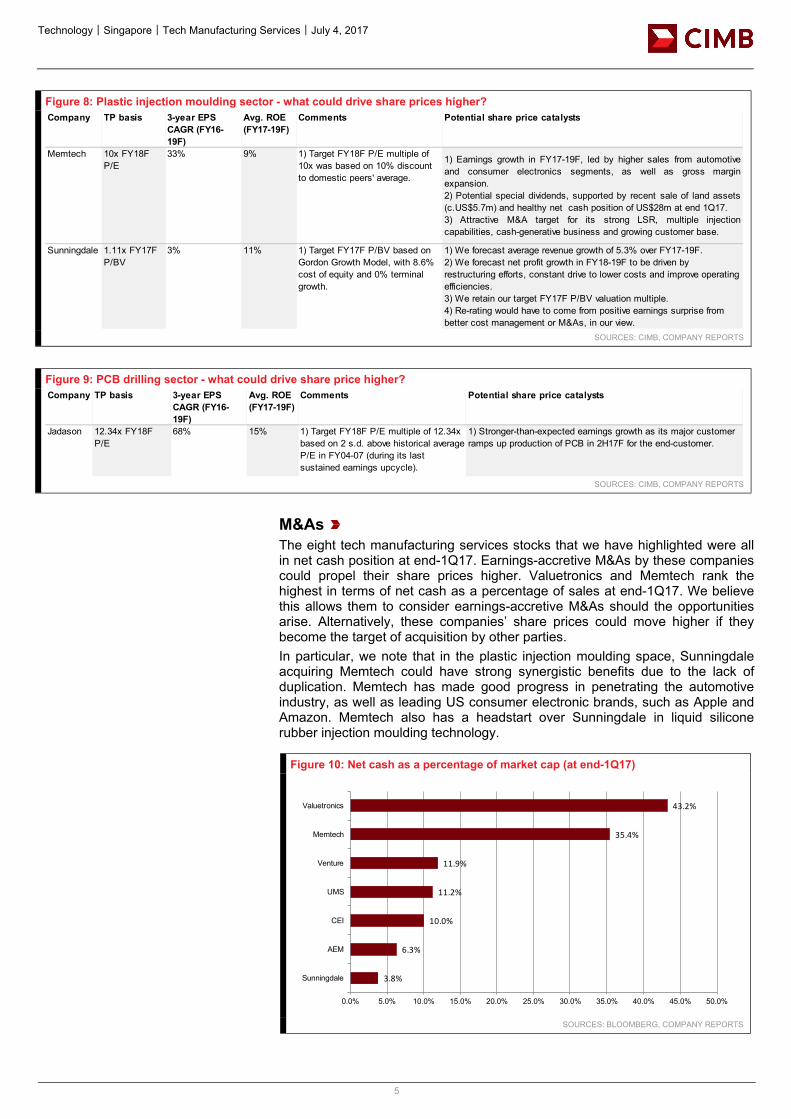

Figure 8: Plastic injection moulding sector - what could drive share prices higher?

SOURCES: CIMB, COMPANY REPORTS

Figure 9: PCB drilling sector - what could drive share price higher?

SOURCES: CIMB, COMPANY REPORTS

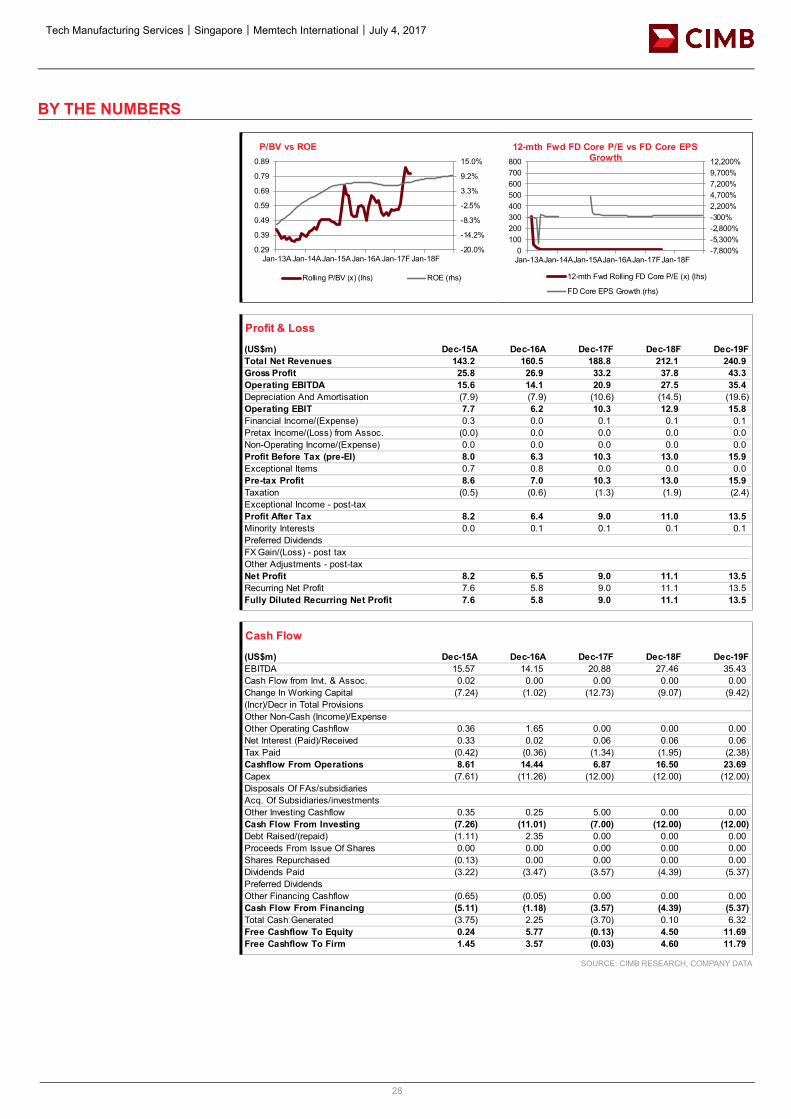

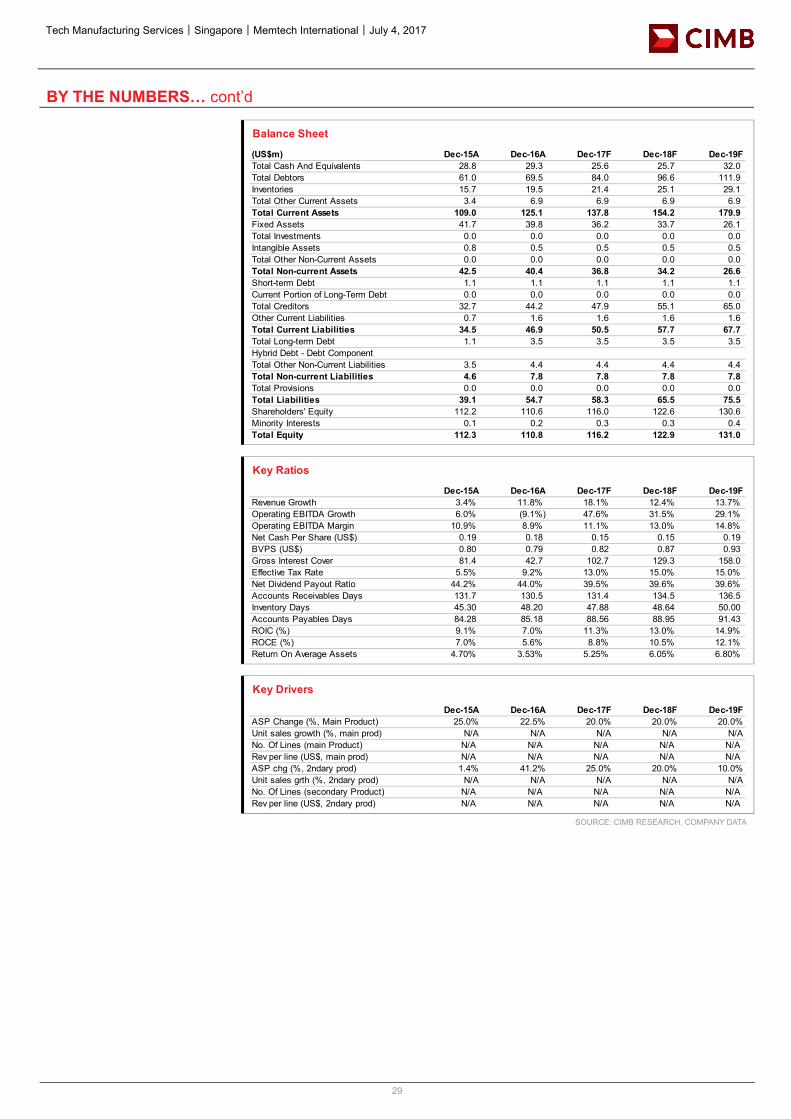

M&As The eight tech manufacturing services stocks that we have highlighted were all in net cash position at end-1Q17. Earnings-accretive M&As by these companies could propel their share prices higher. Valuetronics and Memtech rank the highest in terms of net cash as a percentage of sales at end-1Q17. We believe this allows them to consider earnings-accretive M&As should the opportunities arise. Alternatively, these companies’ share prices could move higher if they become the target of acquisition by other parties. In particular, we note that in the plastic injection moulding space, Sunningdale acquiring Memtech could have strong synergistic benefits due to the lack of duplication. Memtech has made good progress in penetrating the automotive industry, as well as leading US consumer electronic brands, such as Apple and Amazon. Memtech also has a headstart over Sunningdale in liquid silicone rubber injection moulding technology.

Figure 10: Net cash as a percentage of market cap (at end-1Q17)

SOURCES: BLOOMBERG, COMPANY REPORTS

Company TP basis 3-year EPS CAGR (FY16-19F)

Avg. ROE (FY17-19F)

Comments Potential share price catalysts

Memtech 10x FY18F P/E

33% 9% 1) Target FY18F P/E multiple of 10x was based on 10% discount to domestic peers' average.

1) Earnings growth in FY17-19F, led by higher sales from automotiveand consumer electronics segments, as well as gross marginexpansion.2) Potential special dividends, supported by recent sale of land assets(c.US$5.7m) and healthy net cash position of US$28m at end 1Q17. 3) Attractive M&A target for its strong LSR, multiple injectioncapabilities, cash-generative business and growing customer base.

Sunningdale 1.11x FY17F P/BV

3% 11% 1) Target FY17F P/BV based on Gordon Growth Model, with 8.6% cost of equity and 0% terminal growth.

1) We forecast average revenue growth of 5.3% over FY17-19F.2) We forecast net profit growth in FY18-19F to be driven by restructuring efforts, constant drive to lower costs and improve operating efficiencies.3) We retain our target FY17F P/BV valuation multiple.4) Re-rating would have to come from positive earnings surprise from better cost management or M&As, in our view.

Company TP basis 3-year EPS CAGR (FY16-19F)

Avg. ROE (FY17-19F)

Comments Potential share price catalysts

Jadason 12.34x FY18F P/E

68% 15% 1) Target FY18F P/E multiple of 12.34x based on 2 s.d. above historical average P/E in FY04-07 (during its last sustained earnings upcycle).

1) Stronger-than-expected earnings growth as its major customer ramps up production of PCB in 2H17F for the end-customer.

3.8%

6.3%

10.0%

11.2%

11.9%

35.4%

43.2%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0% 50.0%

Sunningdale

AEM

CEI

UMS

Venture

Memtech

Valuetronics

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

6

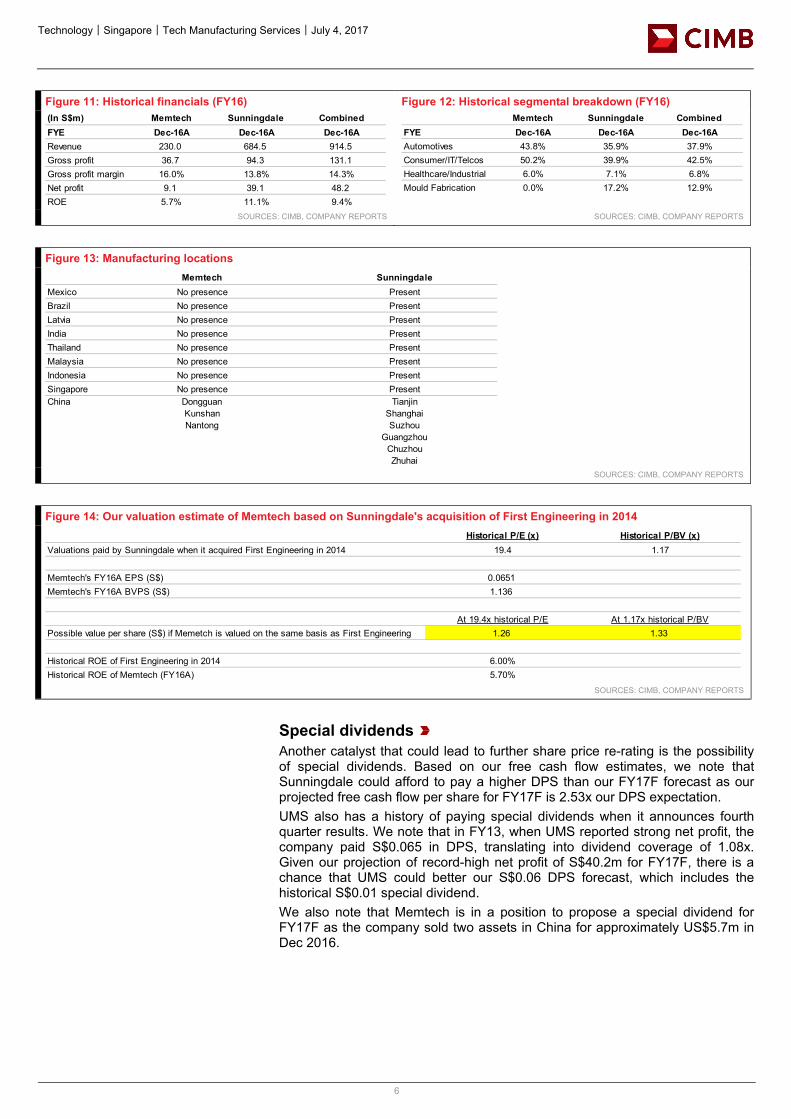

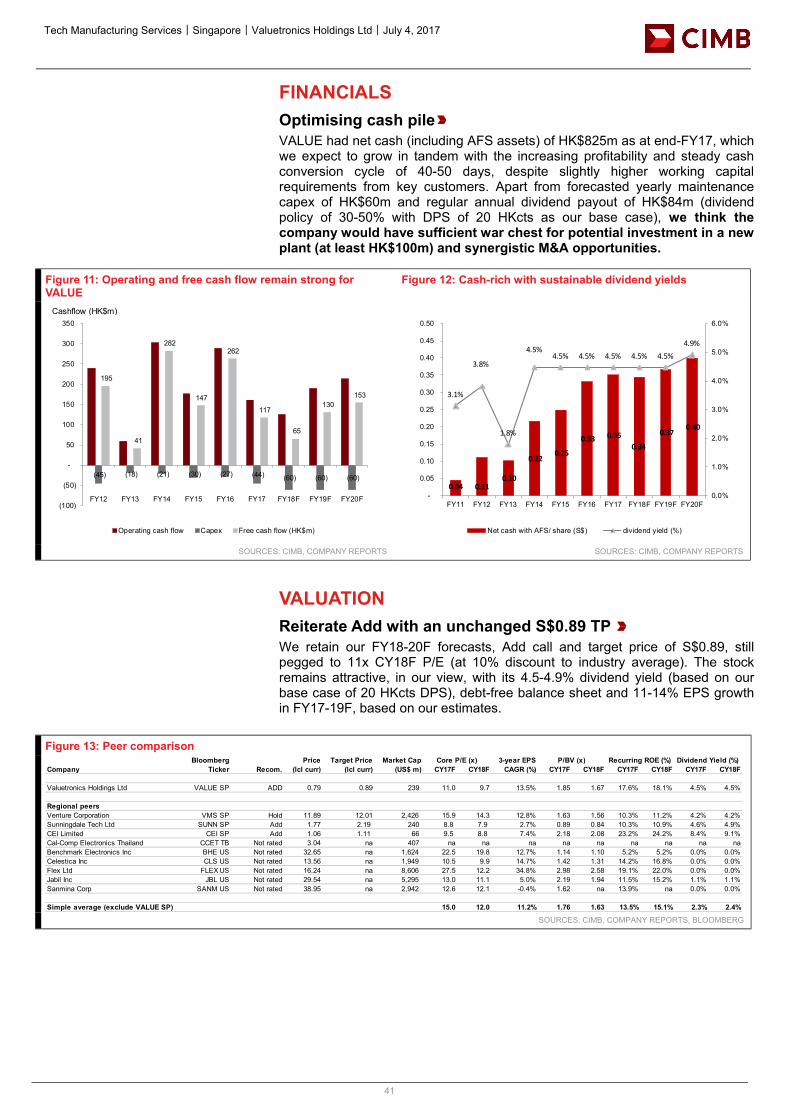

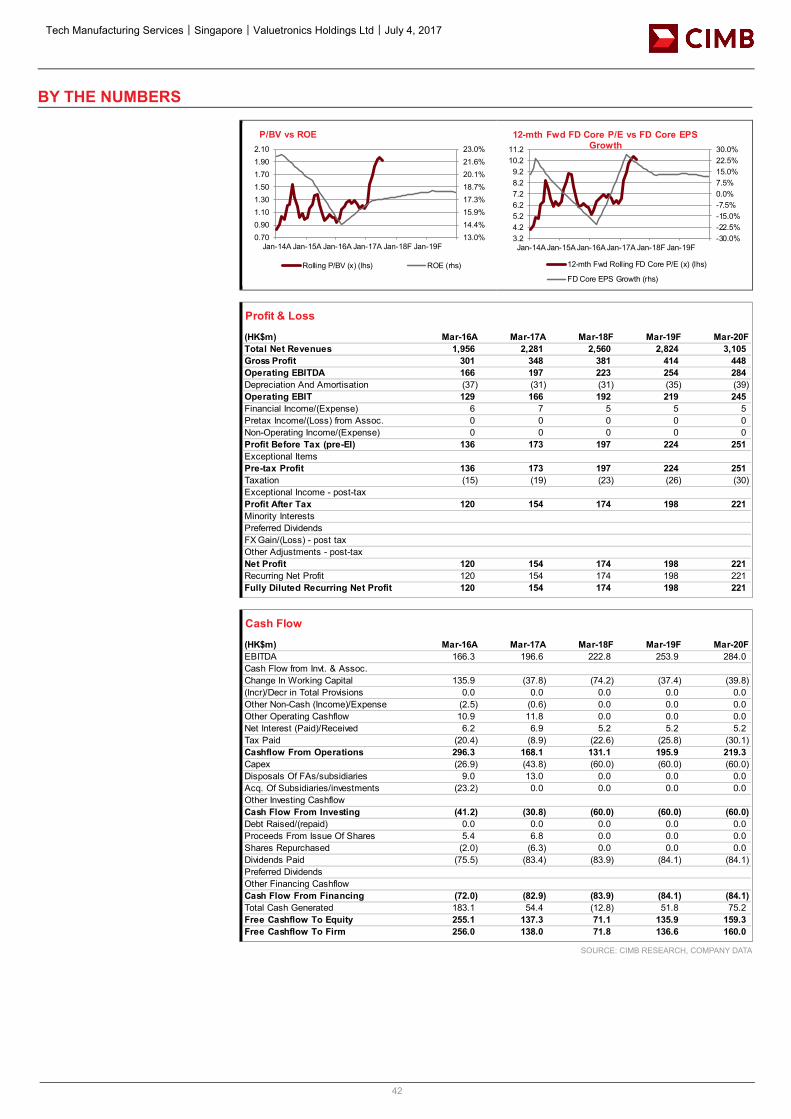

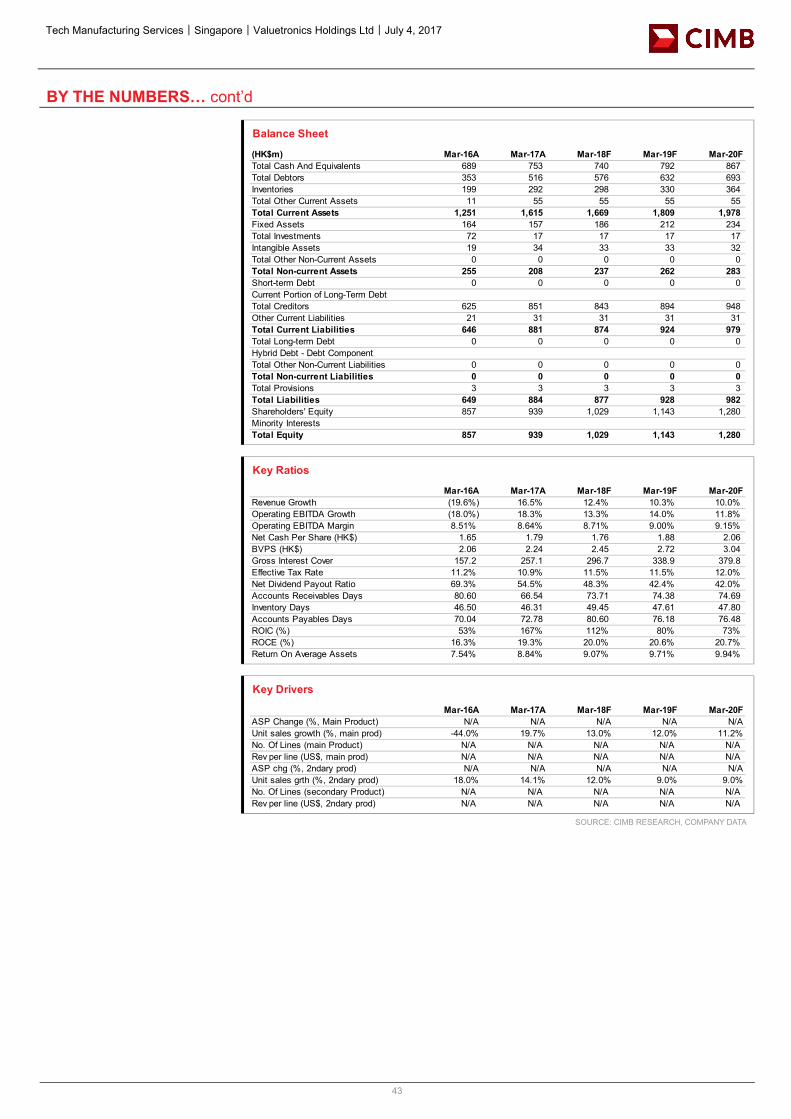

Figure 11: Historical financials (FY16) Figure 12: Historical segmental breakdown (FY16)

SOURCES: CIMB, COMPANY REPORTS SOURCES: CIMB, COMPANY REPORTS

Figure 13: Manufacturing locations

SOURCES: CIMB, COMPANY REPORTS

Figure 14: Our valuation estimate of Memtech based on Sunningdale's acquisition of First Engineering in 2014

SOURCES: CIMB, COMPANY REPORTS

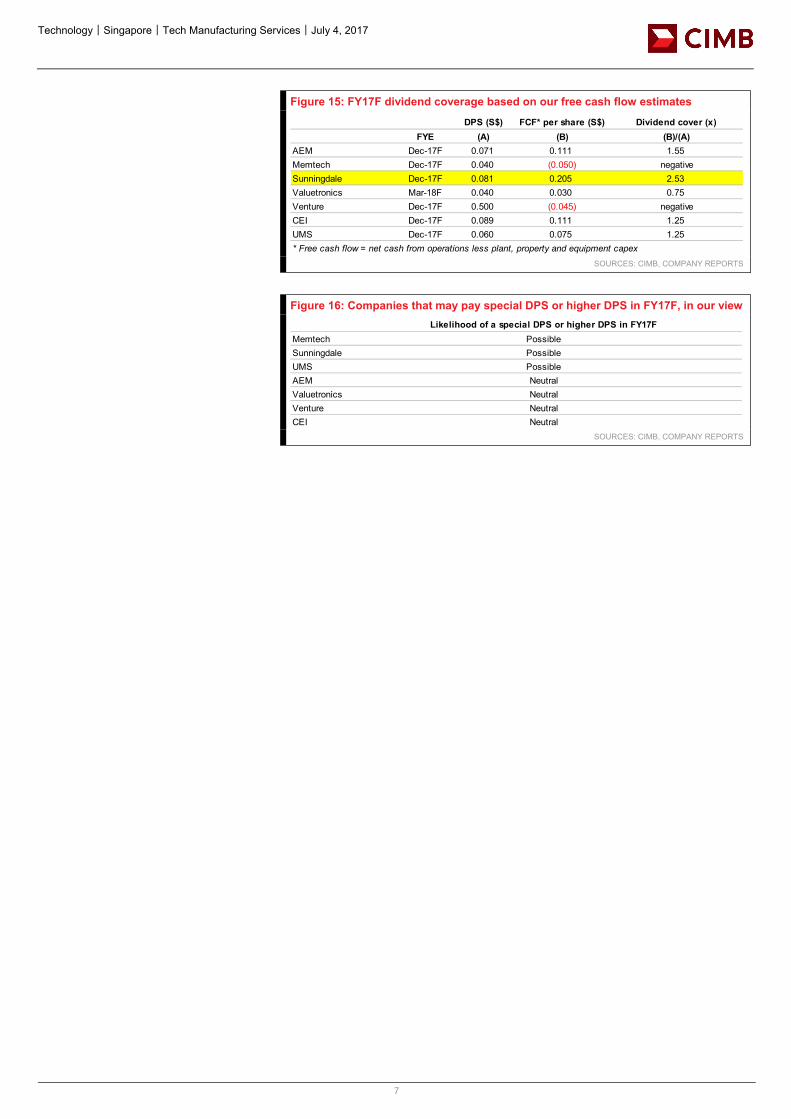

Special dividends Another catalyst that could lead to further share price re-rating is the possibility of special dividends. Based on our free cash flow estimates, we note that Sunningdale could afford to pay a higher DPS than our FY17F forecast as our projected free cash flow per share for FY17F is 2.53x our DPS expectation. UMS also has a history of paying special dividends when it announces fourth quarter results. We note that in FY13, when UMS reported strong net profit, the company paid S$0.065 in DPS, translating into dividend coverage of 1.08x. Given our projection of record-high net profit of S$40.2m for FY17F, there is a chance that UMS could better our S$0.06 DPS forecast, which includes the historical S$0.01 special dividend. We also note that Memtech is in a position to propose a special dividend for FY17F as the company sold two assets in China for approximately US$5.7m in Dec 2016.

(In S$m) Memtech Sunningdale CombinedFYE Dec-16A Dec-16A Dec-16ARevenue 230.0 684.5 914.5Gross profit 36.7 94.3 131.1Gross profit margin 16.0% 13.8% 14.3%Net profit 9.1 39.1 48.2ROE 5.7% 11.1% 9.4%

Memtech Sunningdale CombinedFYE Dec-16A Dec-16A Dec-16AAutomotives 43.8% 35.9% 37.9%Consumer/IT/Telcos 50.2% 39.9% 42.5%Healthcare/Industrial 6.0% 7.1% 6.8%Mould Fabrication 0.0% 17.2% 12.9%

Memtech SunningdaleMexico No presence PresentBrazil No presence PresentLatvia No presence PresentIndia No presence PresentThailand No presence PresentMalaysia No presence PresentIndonesia No presence PresentSingapore No presence PresentChina Dongguan

KunshanNantong

TianjinShanghaiSuzhou

GuangzhouChuzhouZhuhai

Historical P/E (x) Historical P/BV (x)Valuations paid by Sunningdale when it acquired First Engineering in 2014 19.4 1.17

Memtech's FY16A EPS (S$) 0.0651Memtech's FY16A BVPS (S$) 1.136

At 19.4x historical P/E At 1.17x historical P/BVPossible value per share (S$) if Memetch is valued on the same basis as First Engineering 1.26 1.33

Historical ROE of First Engineering in 2014 6.00%Historical ROE of Memtech (FY16A) 5.70%

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

7

Figure 15: FY17F dividend coverage based on our free cash flow estimates

SOURCES: CIMB, COMPANY REPORTS

Figure 16: Companies that may pay special DPS or higher DPS in FY17F, in our view

SOURCES: CIMB, COMPANY REPORTS

DPS (S$) FCF* per share (S$) Dividend cover (x)FYE (A) (B) (B)/(A)

AEM Dec-17F 0.071 0.111 1.55Memtech Dec-17F 0.040 (0.050) negativeSunningdale Dec-17F 0.081 0.205 2.53Valuetronics Mar-18F 0.040 0.030 0.75Venture Dec-17F 0.500 (0.045) negativeCEI Dec-17F 0.089 0.111 1.25UMS Dec-17F 0.060 0.075 1.25* Free cash flow = net cash from operations less plant, property and equipment capex

Likelihood of a special DPS or higher DPS in FY17FMemtech PossibleSunningdale PossibleUMS PossibleAEM NeutralValuetronics NeutralVenture NeutralCEI Neutral

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

8

Risks The key risks for the tech manufacturing services stocks under our coverage are pullbacks or delays in customers’ orders due to changes in global economic conditions. The US$ weakening against other currencies is also a risk to the earnings of these companies.

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

9

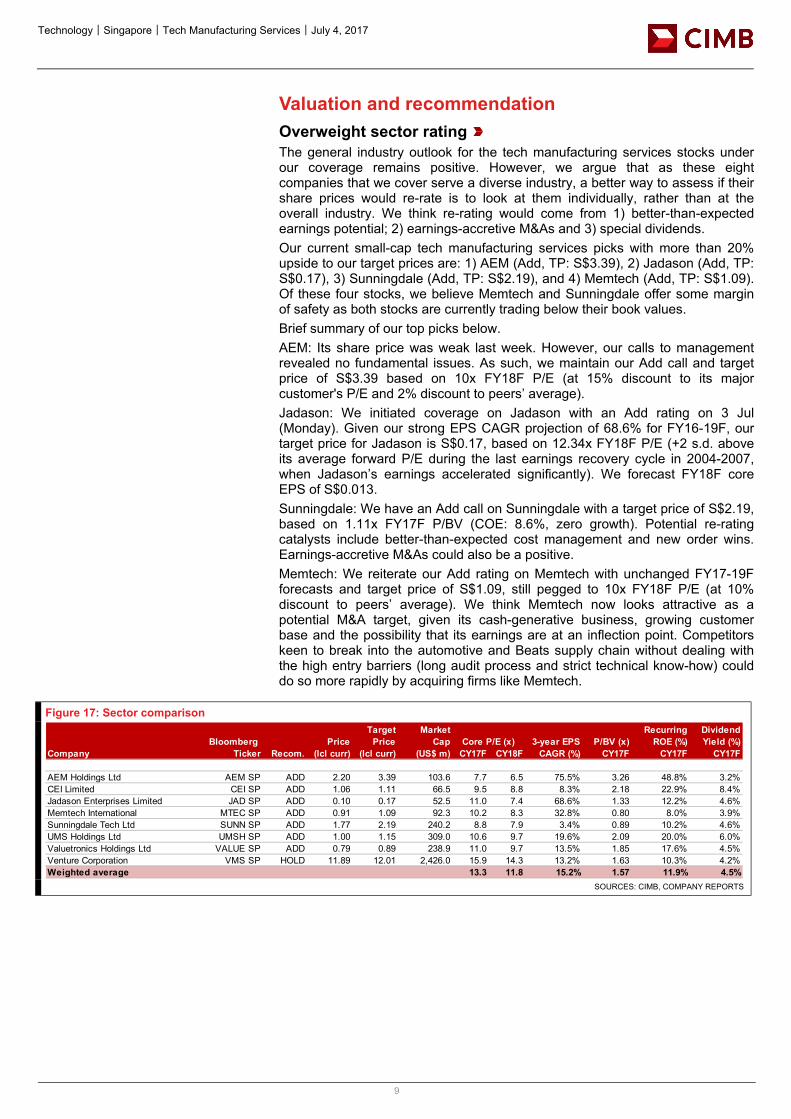

Valuation and recommendation Overweight sector rating The general industry outlook for the tech manufacturing services stocks under our coverage remains positive. However, we argue that as these eight companies that we cover serve a diverse industry, a better way to assess if their share prices would re-rate is to look at them individually, rather than at the overall industry. We think re-rating would come from 1) better-than-expected earnings potential; 2) earnings-accretive M&As and 3) special dividends. Our current small-cap tech manufacturing services picks with more than 20% upside to our target prices are: 1) AEM (Add, TP: S$3.39), 2) Jadason (Add, TP: S$0.17), 3) Sunningdale (Add, TP: S$2.19), and 4) Memtech (Add, TP: S$1.09). Of these four stocks, we believe Memtech and Sunningdale offer some margin of safety as both stocks are currently trading below their book values. Brief summary of our top picks below. AEM: Its share price was weak last week. However, our calls to management revealed no fundamental issues. As such, we maintain our Add call and target price of S$3.39 based on 10x FY18F P/E (at 15% discount to its major customer's P/E and 2% discount to peers’ average). Jadason: We initiated coverage on Jadason with an Add rating on 3 Jul (Monday). Given our strong EPS CAGR projection of 68.6% for FY16-19F, our target price for Jadason is S$0.17, based on 12.34x FY18F P/E (+2 s.d. above its average forward P/E during the last earnings recovery cycle in 2004-2007, when Jadason’s earnings accelerated significantly). We forecast FY18F core EPS of S$0.013. Sunningdale: We have an Add call on Sunningdale with a target price of S$2.19, based on 1.11x FY17F P/BV (COE: 8.6%, zero growth). Potential re-rating catalysts include better-than-expected cost management and new order wins. Earnings-accretive M&As could also be a positive. Memtech: We reiterate our Add rating on Memtech with unchanged FY17-19F forecasts and target price of S$1.09, still pegged to 10x FY18F P/E (at 10% discount to peers’ average). We think Memtech now looks attractive as a potential M&A target, given its cash-generative business, growing customer base and the possibility that its earnings are at an inflection point. Competitors keen to break into the automotive and Beats supply chain without dealing with the high entry barriers (long audit process and strict technical know-how) could do so more rapidly by acquiring firms like Memtech.

Figure 17: Sector comparison

SOURCES: CIMB, COMPANY REPORTS

Bloomberg PriceTarget

PriceMarket

Cap Core P/E (x) 3-year EPS P/BV (x)Recurring

ROE (%)Dividend Yield (%)

Company Ticker Recom. (lcl curr) (lcl curr) (US$ m) CY17F CY18F CAGR (%) CY17F CY17F CY17F

AEM Holdings Ltd AEM SP ADD 2.20 3.39 103.6 7.7 6.5 75.5% 3.26 48.8% 3.2%CEI Limited CEI SP ADD 1.06 1.11 66.5 9.5 8.8 8.3% 2.18 22.9% 8.4%Jadason Enterprises Limited JAD SP ADD 0.10 0.17 52.5 11.0 7.4 68.6% 1.33 12.2% 4.6%Memtech International MTEC SP ADD 0.91 1.09 92.3 10.2 8.3 32.8% 0.80 8.0% 3.9%Sunningdale Tech Ltd SUNN SP ADD 1.77 2.19 240.2 8.8 7.9 3.4% 0.89 10.2% 4.6%UMS Holdings Ltd UMSH SP ADD 1.00 1.15 309.0 10.6 9.7 19.6% 2.09 20.0% 6.0%Valuetronics Holdings Ltd VALUE SP ADD 0.79 0.89 238.9 11.0 9.7 13.5% 1.85 17.6% 4.5%Venture Corporation VMS SP HOLD 11.89 12.01 2,426.0 15.9 14.3 13.2% 1.63 10.3% 4.2%Weighted average 13.3 11.8 15.2% 1.57 11.9% 4.5%

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

10

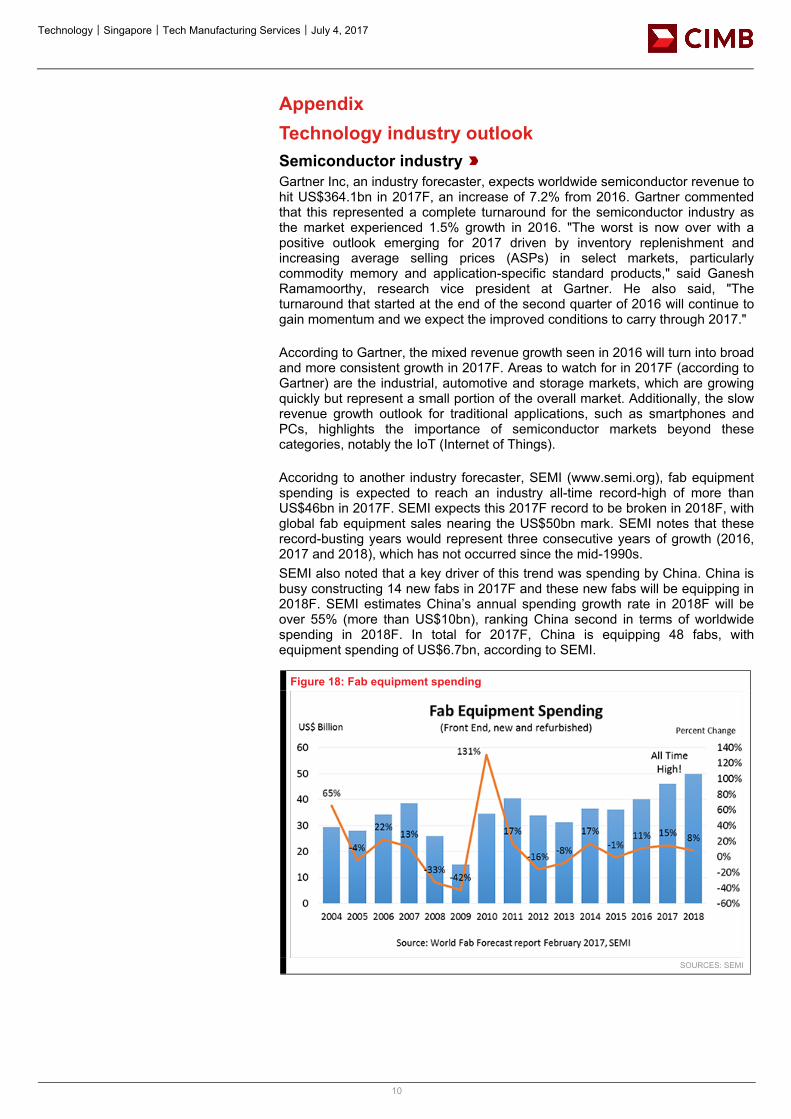

Appendix Technology industry outlook Semiconductor industry Gartner Inc, an industry forecaster, expects worldwide semiconductor revenue to hit US$364.1bn in 2017F, an increase of 7.2% from 2016. Gartner commented that this represented a complete turnaround for the semiconductor industry as the market experienced 1.5% growth in 2016. "The worst is now over with a positive outlook emerging for 2017 driven by inventory replenishment and increasing average selling prices (ASPs) in select markets, particularly commodity memory and application-specific standard products," said Ganesh Ramamoorthy, research vice president at Gartner. He also said, "The turnaround that started at the end of the second quarter of 2016 will continue to gain momentum and we expect the improved conditions to carry through 2017." According to Gartner, the mixed revenue growth seen in 2016 will turn into broad and more consistent growth in 2017F. Areas to watch for in 2017F (according to Gartner) are the industrial, automotive and storage markets, which are growing quickly but represent a small portion of the overall market. Additionally, the slow revenue growth outlook for traditional applications, such as smartphones and PCs, highlights the importance of semiconductor markets beyond these categories, notably the IoT (Internet of Things). Accoridng to another industry forecaster, SEMI (www.semi.org), fab equipment spending is expected to reach an industry all-time record-high of more than US$46bn in 2017F. SEMI expects this 2017F record to be broken in 2018F, with global fab equipment sales nearing the US$50bn mark. SEMI notes that these record-busting years would represent three consecutive years of growth (2016, 2017 and 2018), which has not occurred since the mid-1990s. SEMI also noted that a key driver of this trend was spending by China. China is busy constructing 14 new fabs in 2017F and these new fabs will be equipping in 2018F. SEMI estimates China’s annual spending growth rate in 2018F will be over 55% (more than US$10bn), ranking China second in terms of worldwide spending in 2018F. In total for 2017F, China is equipping 48 fabs, with equipment spending of US$6.7bn, according to SEMI.

Figure 18: Fab equipment spending

SOURCES: SEMI

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

11

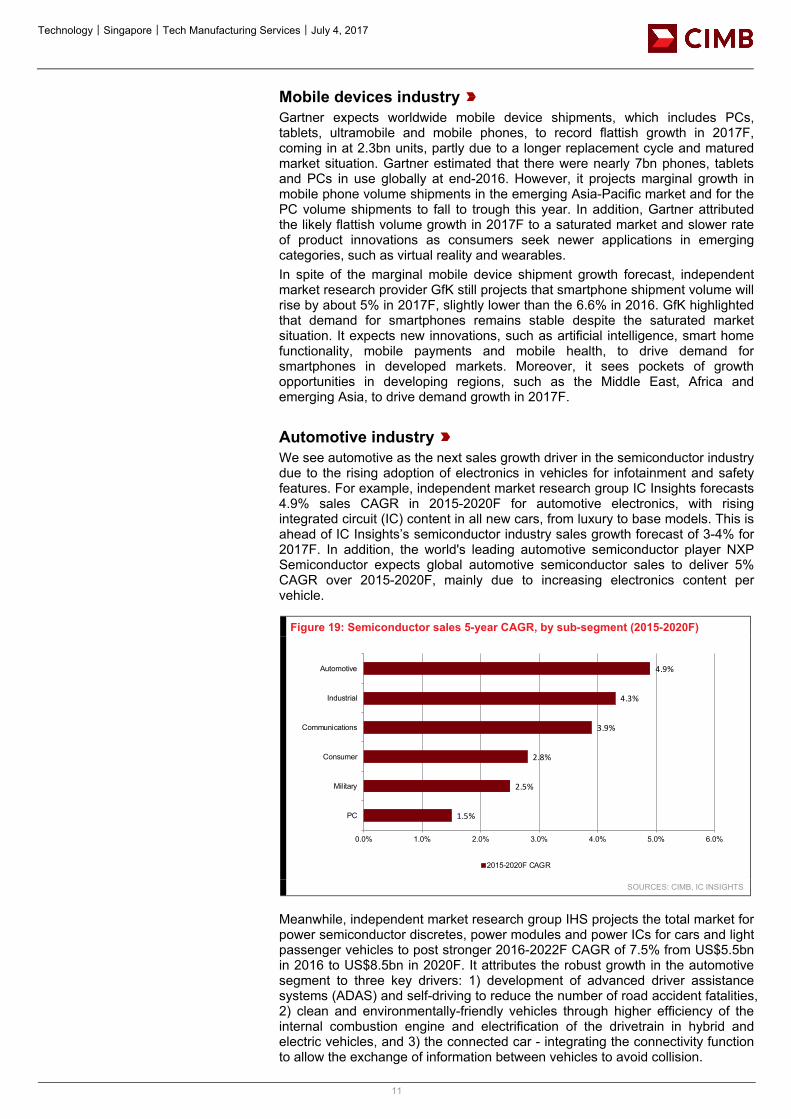

Mobile devices industry Gartner expects worldwide mobile device shipments, which includes PCs, tablets, ultramobile and mobile phones, to record flattish growth in 2017F, coming in at 2.3bn units, partly due to a longer replacement cycle and matured market situation. Gartner estimated that there were nearly 7bn phones, tablets and PCs in use globally at end-2016. However, it projects marginal growth in mobile phone volume shipments in the emerging Asia-Pacific market and for the PC volume shipments to fall to trough this year. In addition, Gartner attributed the likely flattish volume growth in 2017F to a saturated market and slower rate of product innovations as consumers seek newer applications in emerging categories, such as virtual reality and wearables. In spite of the marginal mobile device shipment growth forecast, independent market research provider GfK still projects that smartphone shipment volume will rise by about 5% in 2017F, slightly lower than the 6.6% in 2016. GfK highlighted that demand for smartphones remains stable despite the saturated market situation. It expects new innovations, such as artificial intelligence, smart home functionality, mobile payments and mobile health, to drive demand for smartphones in developed markets. Moreover, it sees pockets of growth opportunities in developing regions, such as the Middle East, Africa and emerging Asia, to drive demand growth in 2017F. Automotive industry We see automotive as the next sales growth driver in the semiconductor industry due to the rising adoption of electronics in vehicles for infotainment and safety features. For example, independent market research group IC Insights forecasts 4.9% sales CAGR in 2015-2020F for automotive electronics, with rising integrated circuit (IC) content in all new cars, from luxury to base models. This is ahead of IC Insights’s semiconductor industry sales growth forecast of 3-4% for 2017F. In addition, the world's leading automotive semiconductor player NXP Semiconductor expects global automotive semiconductor sales to deliver 5% CAGR over 2015-2020F, mainly due to increasing electronics content per vehicle.

Figure 19: Semiconductor sales 5-year CAGR, by sub-segment (2015-2020F)

SOURCES: CIMB, IC INSIGHTS

Meanwhile, independent market research group IHS projects the total market for power semiconductor discretes, power modules and power ICs for cars and light passenger vehicles to post stronger 2016-2022F CAGR of 7.5% from US$5.5bn in 2016 to US$8.5bn in 2020F. It attributes the robust growth in the automotive segment to three key drivers: 1) development of advanced driver assistance systems (ADAS) and self-driving to reduce the number of road accident fatalities, 2) clean and environmentally-friendly vehicles through higher efficiency of the internal combustion engine and electrification of the drivetrain in hybrid and electric vehicles, and 3) the connected car - integrating the connectivity function to allow the exchange of information between vehicles to avoid collision.

1.5%

2.5%

2.8%

3.9%

4.3%

4.9%

0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0%

PC

Military

Consumer

Communications

Industrial

Automotive

2015-2020F CAGR

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

12

Another leading automotive semiconductor player, Infineon, expects the average semiconductor content in vehicles to increase from US$100 in 2016 to US$400 in 2025F due to rising demand for additional camera modules, radar modules, light detection and ranging (lidar) modules, sensors and actuators to accommodate the self-driving vehicles ecosystem.

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

13

New industry drivers - technology is becoming ubiquituous Other than the traditional fields of PCs, mobile devices and the much-talked-about automotive industry, we note that semiconductors/electronics usage is also rising in non-traditional areas. Below, we highlight three examples. Lighting Philips has introduced a lighting system known as Philips Hue. This is a personal wireless lighting system for homes that provides endless possibilities for users to get creative with light and to personalise it to suit their lifestyles. Philips Hue comes with preset light recipes to help users relax, read, concentrate or energise with the optimum tone of white light. Or, for extra ambience, users can use the Philips Hue’s colour picker to create scenes with up to 16m different colours. Users can now control their home lighting systems wirelessly via their mobile devices. All these are made possible with the proliferation of semiconductors in lighting systems.

Figure 20: Philips Hue LED bulbs Figure 21: Philips Hue light strips Figure 22: Philips Hue control systems

SOURCES: PHILIPS SOURCES: PHILIPS SOURCES: PHILIPS

Electronic cigarettes In Nov 2014, Philips Morris International (PMI) officially launched iQOS, the first of its heat-not-burn Reduced-Risk Products (RRPs), together with Marlboro HeatSticks in regular and menthol variants in the pilot markets of Nagoya, Japan, and Milan, Italy. iQOS features an electronic holder that heats tobacco rather than burning it. The iQOS looks like a mobile device and appears to be a Silicon Valley solution to e-cigarettes.

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

14

Figure 23: PMI iQOS

SOURCES: PMI

Life sciences According to a 2016 Deloitte study, most life science companies are entering the second half of this decade with a cautiously optimistic view. In the pharmaceutical segment, Deloitte forecasts that global pharmaceutical sales will reach US$1.4tr by 2019F.

Figure 24: Global pharmaceutical sales

SOURCES: DELOITTE

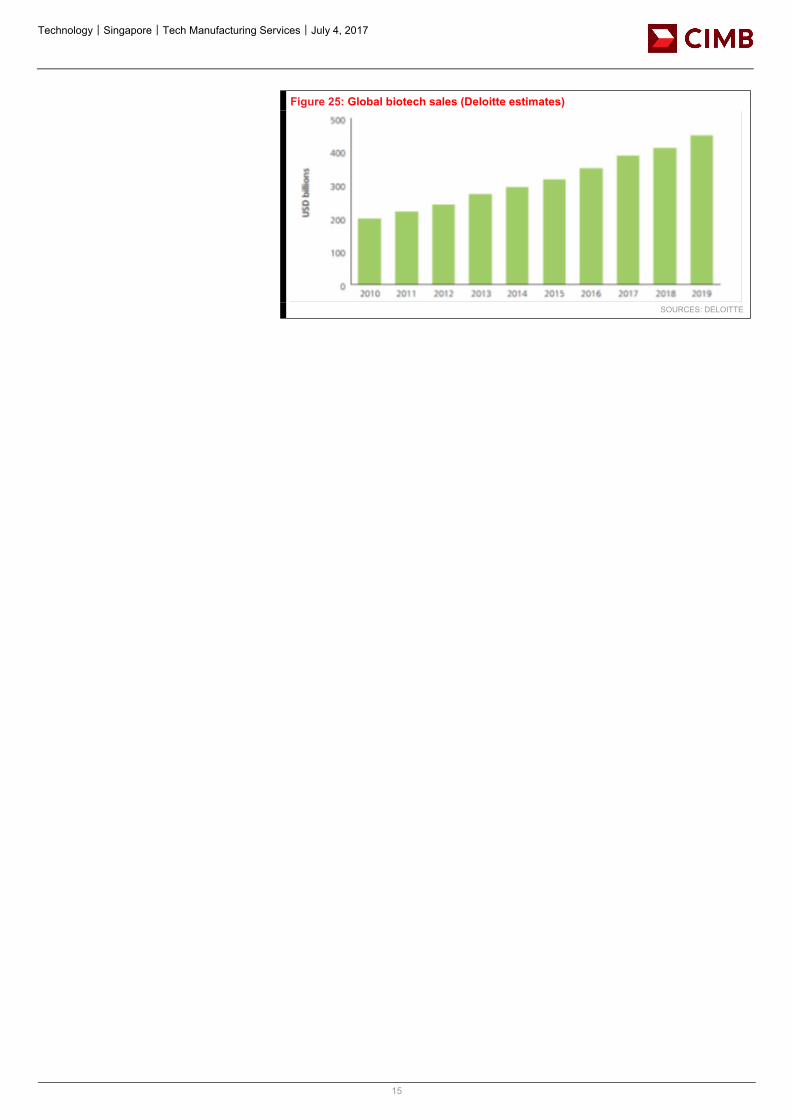

Deloitte also highlighted that biotech drugs (vaccines, biologics) continue to gain traction in the life sciences sector. Most of the top 10 pharmaceutical products (by sales) in 2014 were biotech drugs, including monoclonal antibodies and recombinant products. Deloitte estimated that biotech drug sales amounted to US$289bn in 2014 and it projected that this would increase to US$445bn by 2019F.

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

15

Figure 25: Global biotech sales (Deloitte estimates)

SOURCES: DELOITTE

Technology│Singapore│Tech Manufacturing Services│July 4, 2017

16

Company Briefs…

Technology - Others│Singapore│July 4, 2017

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

AEM Holdings Ltd Visible growth ahead ■ AEM is a leading semiconductor test handler supplier and the sole source for a major

semiconductor company. ■ We project that AEM is on track to 311% yoy core EPS growth in FY17F, backed by

3.3% dividend yield and a net cash balance sheet. ■ AEM is a possible M&A target, in our view. ■ Room for margin improvement as production shifts to lower-cost Penang. ■ Trading at undemanding 6.4x FY18F P/E and 5.8x FY19F P/E despite projected core

FY18/19F EPS growth of 19%/11%.

Leading test handler supplier AEM Holdings Ltd (AEM) is a leading semiconductor test handler supplier to a major North American semiconductor company. Its test handler products are patented, setting back would-be competitors by 2-3 years. With the experience gained in supplying this major customer, AEM is well-equipped to provide automation tools for other manufacturing companies. The company also believes that it is on track for multi-year growth with this customer.

Has the share price peaked? YTD, AEM’s share price has gained 278%, reaching a high of S$2.77 on 5 Jun 2017. The share price corrected to a low of S$2.07 on 28 June, mirroring the tech stock sell-off on the NASDAQ. We believe its share price has yet to peak as: a) AEM is trading at 6.4x/5.8x FY18F/19F P/E versus 19%/11% core EPS growth, and b) AEM is on track to deliver 311% core EPS growth in FY17F, based on our estimates.

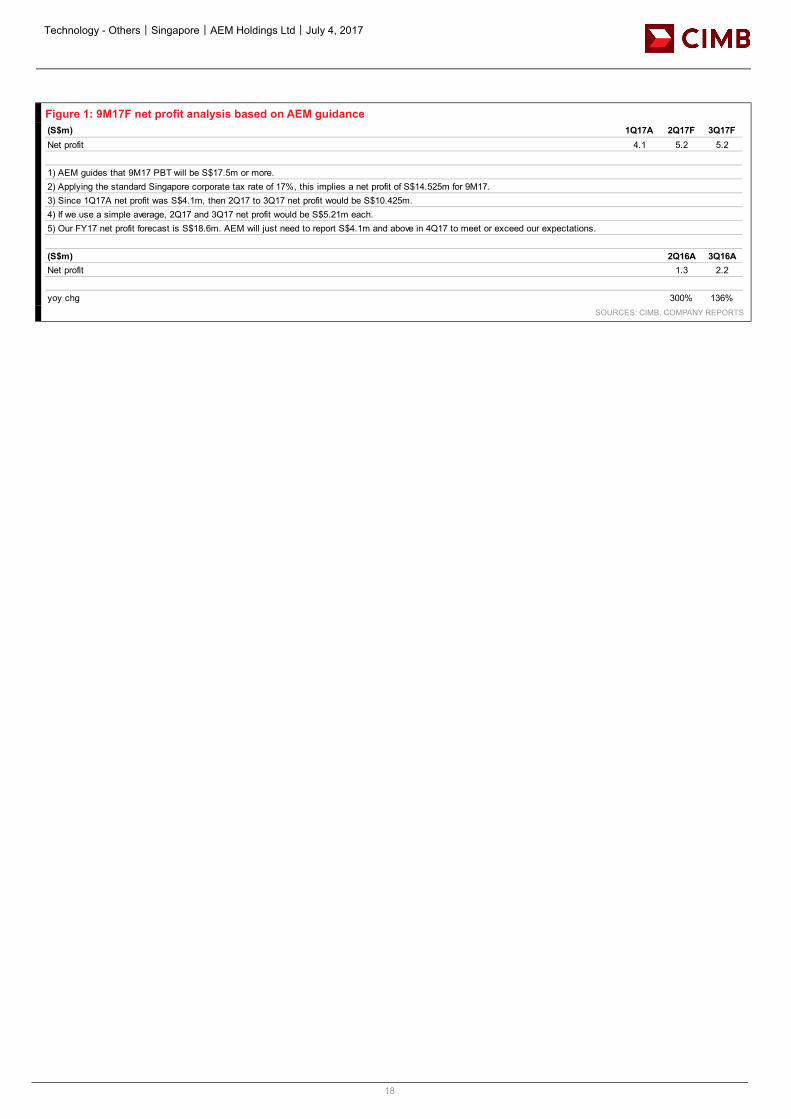

Share price driver #1: Potential FY17 earnings surprise In its 1Q17 results announcement, AEM guided for 9M17F revenue of S$142m and pretax profit of S$17.5m. Based on our analysis of its profit guidance (see Figure 1), AEM is on track to deliver 300%/136% yoy growth in net profit for 2Q17F/3Q17F. We note that sales orders received that can be recognised as revenue in FY17F have risen from S$130m (3 Mar 2017) to S$152m (18 Apr 2017) and subsequently, to S$182m in a 5 Jun 2017 announcement.

Share price driver #2: Potential M&As AEM already has an established management in place and its business with its key customer has taken off firmly. On 5 Jun 2017, major shareholder Orion Phoenix placed out 2.7m shares at S$2.70 to various long-only institutional funds, reducing its stake to 23.96%. Orion Phoenix will need to exit its investment in AEM within the next five years as the fund goes end-of-life. These factors make it conducive for any potential M&A talks with interested third parties.

Share price driver #3: Dividends In its 2016 annual report, AEM Chairman wrote that “with clear visibility of growth into the next few years, we intend to adopt a dividend policy to pay annual dividends, including interim dividends, of not less than 25% of profit after tax excluding non-recurring, one-off and exceptional items". AEM has also indicated its confidence in its current business with the major customer with a 1-for-2 bonus issue (completed). Based on the 25% payout guidance, we estimate decent dividend yields of 3.3-4.4% over FY17-19F.

No fundamental reason for sell-down; Maintain Add Our calls to management revealed no fundamental issues. As such, we maintain our Add call and target price of S$3.39 based on 10x FY18F P/E (at 15% discount to its major customer's P/E and 2% discount to peer average P/E). Order pushback by its key customer is a downside risk to our call.

SOURCE: COMPANY DATA, CIMB FORECASTS

Singapore

ADD (no change) Consensus ratings*: Buy 1 Hold 0 Sell 0

Current price: S$2.20 Target price: S$3.39 Previous target: S$3.39 Up/downside: 54.0% CIMB / Consensus: 0.6%

Reuters: AEM.SI Bloomberg: AEM SP Market cap: US$103.6m S$143.2m Average daily turnover: US$0.99m S$1.38m Current shares o/s: 42.80m Free float: 73.7% *Source: Bloomberg Key changes in this note

No change

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -19.4 57.1 547.1 Relative (%) -18.5 56.1 535.2

Major shareholders % held Orion Phoenix 24.0

Analyst(s)

William TNG, CFA T (65) 6210 8676 E [email protected]

Financial Summary Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FRevenue (S$m) 51.5 70.4 188.0 223.6 237.8Net Profit (S$m) 6.52 4.42 18.44 22.03 24.53Core EPS (S$) 0.10 0.07 0.29 0.34 0.38Core EPS Growth (32%) 311% 19% 11%FD Core P/E (x) 21.59 31.69 7.70 6.49 5.83Price To Sales (x) 2.84 2.04 0.76 0.64 0.60DPS (S$) 0.007 0.012 0.071 0.085 0.094Dividend Yield 0.30% 0.55% 3.25% 3.85% 4.29%EV/EBITDA (x) 25.39 18.07 5.36 4.16 3.20P/FCFE (x) NA NA 13.88 8.51 6.25Net Gearing (52.0%) (20.8%) (28.6%) (40.7%) (53.2%)P/BV (x) 5.97 4.71 3.26 2.37 1.81ROE 32.0% 16.7% 50.0% 42.3% 35.2%% Change In Core EPS Estimates 0% 0% 0%CIMB/consensus EPS (x) 0.98 1.00 0.99

22

322

622

922

0.07

1.07

2.07

3.07Price Close Relative to FSSTI (RHS)

2

4

6

Jul-16 Oct-16 Jan-17 Apr-17

Vol m

Technology - Others│Singapore│AEM Holdings Ltd│July 4, 2017

18

Figure 1: 9M17F net profit analysis based on AEM guidance

SOURCES: CIMB, COMPANY REPORTS

(S$m) 1Q17A 2Q17F 3Q17FNet profit 4.1 5.2 5.2

1) AEM guides that 9M17 PBT will be S$17.5m or more.2) Applying the standard Singapore corporate tax rate of 17%, this implies a net profit of S$14.525m for 9M17.3) Since 1Q17A net profit was S$4.1m, then 2Q17 to 3Q17 net profit would be S$10.425m. 4) If we use a simple average, 2Q17 and 3Q17 net profit would be S$5.21m each.5) Our FY17 net profit forecast is S$18.6m. AEM will just need to report S$4.1m and above in 4Q17 to meet or exceed our expectations.

(S$m) 2Q16A 3Q16ANet profit 1.3 2.2

yoy chg 300% 136%

Technology - Others│Singapore│AEM Holdings Ltd│July 4, 2017

19

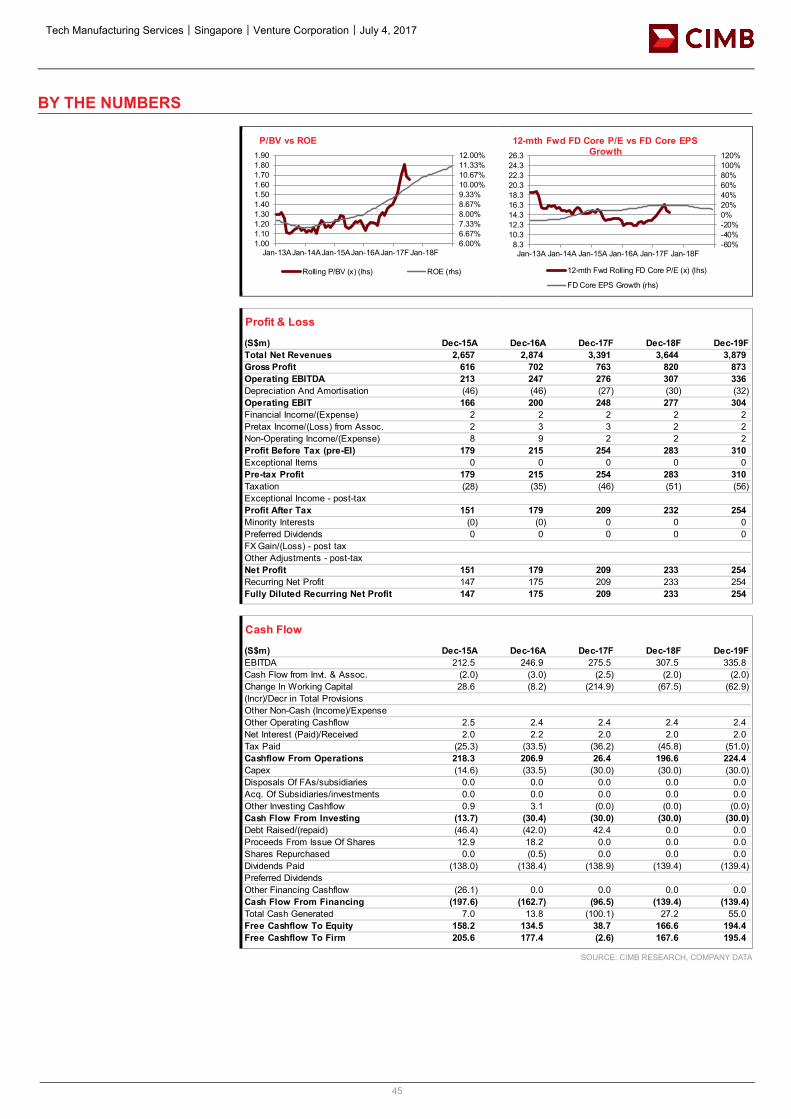

BY THE NUMBERS

SOURCE: CIMB RESEARCH, COMPANY DATA

13.0%

19.7%

26.3%

33.0%

39.7%

46.3%

53.0%

0.03

1.03

2.03

3.03

4.03

5.03

6.03

Jan-13A Jan-14A Jan-15A Jan-16A Jan-17F Jan-18F

P/BV vs ROE

Rolling P/BV (x) (lhs) ROE (rhs)

-70%-20%30%80%130%180%230%280%330%380%

0.61.62.63.64.65.66.67.68.69.6

Jan-13A Jan-14A Jan-15A Jan-16A Jan-17F Jan-18F

12-mth Fwd FD Core P/E vs FD Core EPS Growth

12-mth Fwd Rolling FD Core P/E (x) (lhs)

FD Core EPS Growth (rhs)

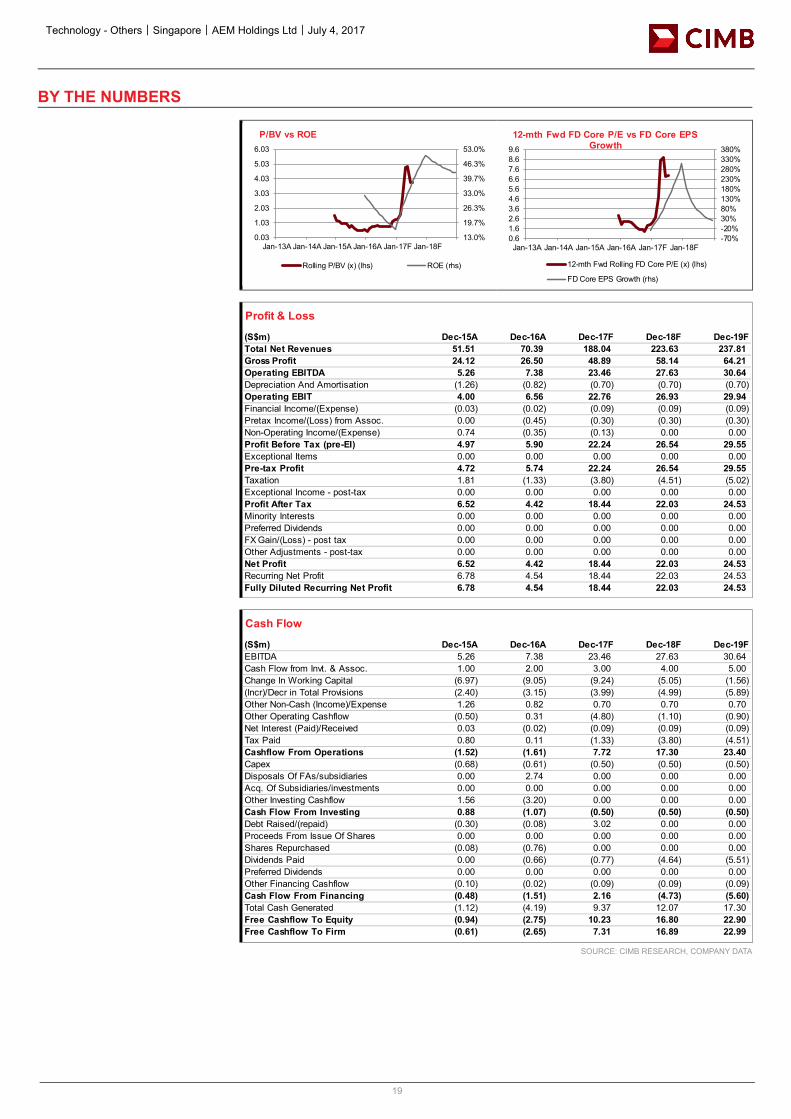

Profit & Loss

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FTotal Net Revenues 51.51 70.39 188.04 223.63 237.81Gross Profit 24.12 26.50 48.89 58.14 64.21Operating EBITDA 5.26 7.38 23.46 27.63 30.64Depreciation And Amortisation (1.26) (0.82) (0.70) (0.70) (0.70)Operating EBIT 4.00 6.56 22.76 26.93 29.94Financial Income/(Expense) (0.03) (0.02) (0.09) (0.09) (0.09)Pretax Income/(Loss) from Assoc. 0.00 (0.45) (0.30) (0.30) (0.30)Non-Operating Income/(Expense) 0.74 (0.35) (0.13) 0.00 0.00Profit Before Tax (pre-EI) 4.97 5.90 22.24 26.54 29.55Exceptional Items 0.00 0.00 0.00 0.00 0.00Pre-tax Profit 4.72 5.74 22.24 26.54 29.55Taxation 1.81 (1.33) (3.80) (4.51) (5.02)Exceptional Income - post-tax 0.00 0.00 0.00 0.00 0.00Profit After Tax 6.52 4.42 18.44 22.03 24.53Minority Interests 0.00 0.00 0.00 0.00 0.00Preferred Dividends 0.00 0.00 0.00 0.00 0.00FX Gain/(Loss) - post tax 0.00 0.00 0.00 0.00 0.00Other Adjustments - post-tax 0.00 0.00 0.00 0.00 0.00Net Profit 6.52 4.42 18.44 22.03 24.53Recurring Net Profit 6.78 4.54 18.44 22.03 24.53Fully Diluted Recurring Net Profit 6.78 4.54 18.44 22.03 24.53

Cash Flow

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FEBITDA 5.26 7.38 23.46 27.63 30.64Cash Flow from Invt. & Assoc. 1.00 2.00 3.00 4.00 5.00Change In Working Capital (6.97) (9.05) (9.24) (5.05) (1.56)(Incr)/Decr in Total Provisions (2.40) (3.15) (3.99) (4.99) (5.89)Other Non-Cash (Income)/Expense 1.26 0.82 0.70 0.70 0.70Other Operating Cashflow (0.50) 0.31 (4.80) (1.10) (0.90)Net Interest (Paid)/Received 0.03 (0.02) (0.09) (0.09) (0.09)Tax Paid 0.80 0.11 (1.33) (3.80) (4.51)Cashflow From Operations (1.52) (1.61) 7.72 17.30 23.40Capex (0.68) (0.61) (0.50) (0.50) (0.50)Disposals Of FAs/subsidiaries 0.00 2.74 0.00 0.00 0.00Acq. Of Subsidiaries/investments 0.00 0.00 0.00 0.00 0.00Other Investing Cashflow 1.56 (3.20) 0.00 0.00 0.00Cash Flow From Investing 0.88 (1.07) (0.50) (0.50) (0.50)Debt Raised/(repaid) (0.30) (0.08) 3.02 0.00 0.00Proceeds From Issue Of Shares 0.00 0.00 0.00 0.00 0.00Shares Repurchased (0.08) (0.76) 0.00 0.00 0.00Dividends Paid 0.00 (0.66) (0.77) (4.64) (5.51)Preferred Dividends 0.00 0.00 0.00 0.00 0.00Other Financing Cashflow (0.10) (0.02) (0.09) (0.09) (0.09)Cash Flow From Financing (0.48) (1.51) 2.16 (4.73) (5.60)Total Cash Generated (1.12) (4.19) 9.37 12.07 17.30Free Cashflow To Equity (0.94) (2.75) 10.23 16.80 22.90Free Cashflow To Firm (0.61) (2.65) 7.31 16.89 22.99

Technology - Others│Singapore│AEM Holdings Ltd│July 4, 2017

20

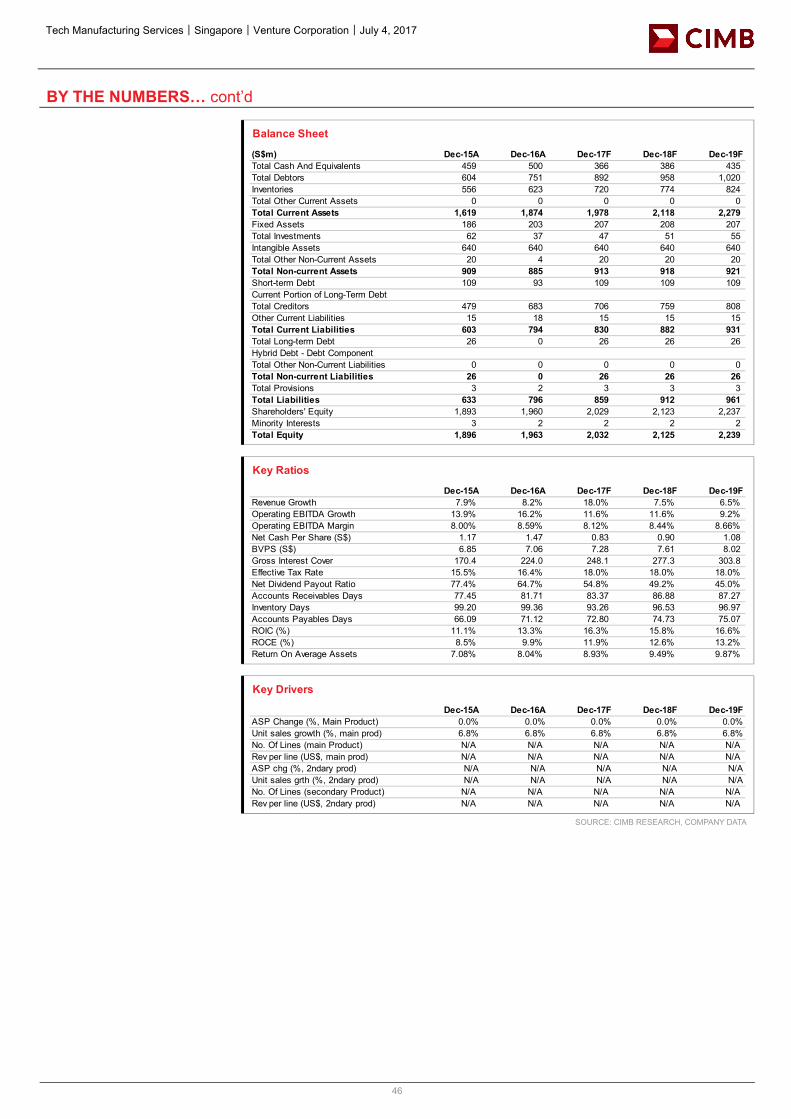

BY THE NUMBERS… cont’d

SOURCE: CIMB RESEARCH, COMPANY DATA

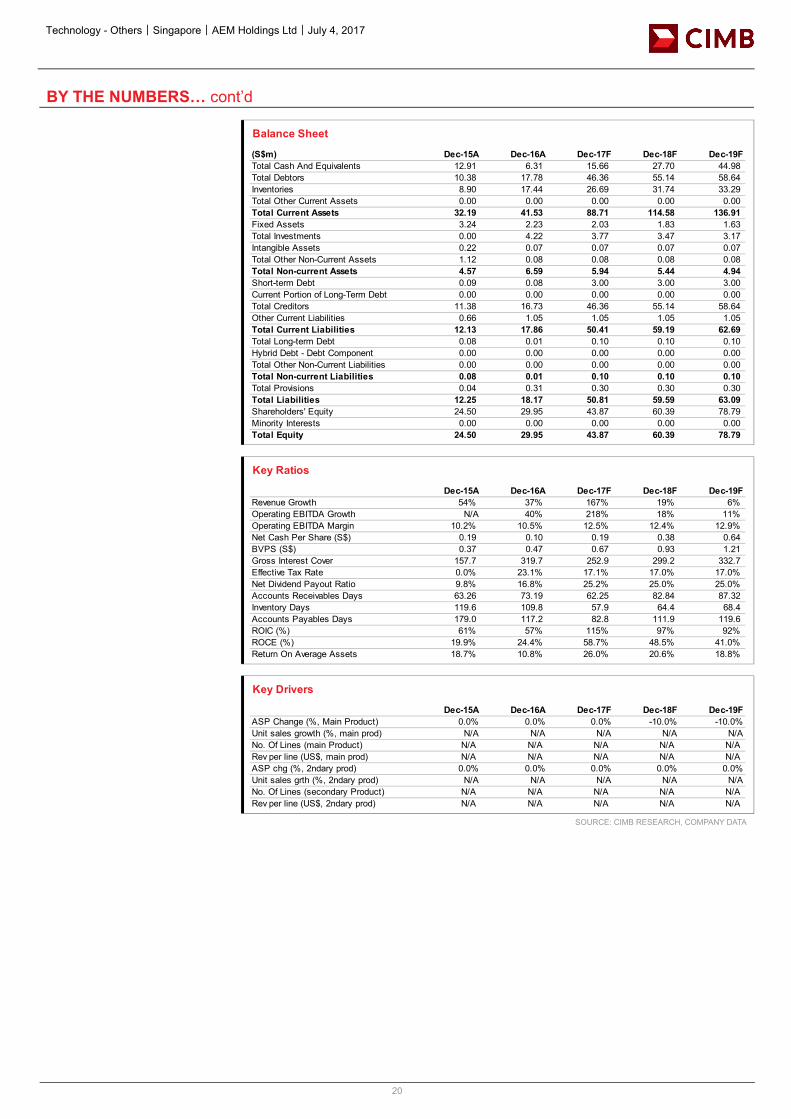

Balance Sheet

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FTotal Cash And Equivalents 12.91 6.31 15.66 27.70 44.98Total Debtors 10.38 17.78 46.36 55.14 58.64Inventories 8.90 17.44 26.69 31.74 33.29Total Other Current Assets 0.00 0.00 0.00 0.00 0.00Total Current Assets 32.19 41.53 88.71 114.58 136.91Fixed Assets 3.24 2.23 2.03 1.83 1.63Total Investments 0.00 4.22 3.77 3.47 3.17Intangible Assets 0.22 0.07 0.07 0.07 0.07Total Other Non-Current Assets 1.12 0.08 0.08 0.08 0.08Total Non-current Assets 4.57 6.59 5.94 5.44 4.94Short-term Debt 0.09 0.08 3.00 3.00 3.00Current Portion of Long-Term Debt 0.00 0.00 0.00 0.00 0.00Total Creditors 11.38 16.73 46.36 55.14 58.64Other Current Liabilities 0.66 1.05 1.05 1.05 1.05Total Current Liabilities 12.13 17.86 50.41 59.19 62.69Total Long-term Debt 0.08 0.01 0.10 0.10 0.10Hybrid Debt - Debt Component 0.00 0.00 0.00 0.00 0.00Total Other Non-Current Liabilities 0.00 0.00 0.00 0.00 0.00Total Non-current Liabilities 0.08 0.01 0.10 0.10 0.10Total Provisions 0.04 0.31 0.30 0.30 0.30Total Liabilities 12.25 18.17 50.81 59.59 63.09Shareholders' Equity 24.50 29.95 43.87 60.39 78.79Minority Interests 0.00 0.00 0.00 0.00 0.00Total Equity 24.50 29.95 43.87 60.39 78.79

Key Ratios

Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FRevenue Growth 54% 37% 167% 19% 6%Operating EBITDA Growth N/A 40% 218% 18% 11%Operating EBITDA Margin 10.2% 10.5% 12.5% 12.4% 12.9%Net Cash Per Share (S$) 0.19 0.10 0.19 0.38 0.64BVPS (S$) 0.37 0.47 0.67 0.93 1.21Gross Interest Cover 157.7 319.7 252.9 299.2 332.7Effective Tax Rate 0.0% 23.1% 17.1% 17.0% 17.0%Net Dividend Payout Ratio 9.8% 16.8% 25.2% 25.0% 25.0%Accounts Receivables Days 63.26 73.19 62.25 82.84 87.32Inventory Days 119.6 109.8 57.9 64.4 68.4Accounts Payables Days 179.0 117.2 82.8 111.9 119.6ROIC (%) 61% 57% 115% 97% 92%ROCE (%) 19.9% 24.4% 58.7% 48.5% 41.0%Return On Average Assets 18.7% 10.8% 26.0% 20.6% 18.8%

Key Drivers

Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FASP Change (%, Main Product) 0.0% 0.0% 0.0% -10.0% -10.0%Unit sales growth (%, main prod) N/A N/A N/A N/A N/ANo. Of Lines (main Product) N/A N/A N/A N/A N/ARev per line (US$, main prod) N/A N/A N/A N/A N/AASP chg (%, 2ndary prod) 0.0% 0.0% 0.0% 0.0% 0.0%Unit sales grth (%, 2ndary prod) N/A N/A N/A N/A N/ANo. Of Lines (secondary Product) N/A N/A N/A N/A N/ARev per line (US$, 2ndary prod) N/A N/A N/A N/A N/A

Tech Manufacturing Services│Singapore│July 4, 2017

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

CEI Limited Tech dividend aristocrat ■ Although the share price has gained 34% YTD and 38% since our initiation in Sep

2016, we think CEI remains attractive as a dividend and potential M&A play. Add. ■ We think a higher dividend payout than our FY17-19F forecast of 80% is possible,

given its minimal capex needs and strong cash generation. ■ Healthy fundamentals, fragmented shareholdings and low valuations make CEI an

attractive M&A target, in our view. ■ We project resilient earnings, with 7.4% 3-year EPS CAGR (FY16-19F). ■ Our FY17-19F forecasts and target price of S$1.11 (9.2x FY18F P/E) are unchanged.

Proxy for medtech and life science An established contract manufacturer with track record of more than 26 years and 70 customers, CEI has c.50% sales exposure to the medtech/life science sector. This has contributed to its steady sales growth over many years. Its topline crossed the S$100m mark in FY11, and has consistently stayed above this level since then. New customer/order wins, coupled with sales recovery from its major oil & gas customer, could nudge its topline towards S$150m before FY19F, in our view.

Share price driver #1: Highest dividend yield among tech stocks CEI paid 10 Scts DPS in FY16, almost 100% of its net profit, translating into 9.3% dividend yield, the highest among Singapore-listed tech stocks. Based on an 80% payout ratio, we forecast dividend yields of 8.4-9.8% for FY17-19F. Given its cash-generative business, limited capex needs and S$9.2m net cash at end-2016, we do not rule out higher dividend payout ratio in FY17F, which would support its near-term share price.

Share price driver #2: Potential M&A We think CEI could be an attractive M&A target, given its diverse customer base, robust cash-generation capability and fragmented shareholding structure; especially for PE firms and peers looking to expand their geographical footprints. Its valuation also looks attractive as the stock currently trades at 8.8x FY18F P/E, in line with its 10-year historical average, but at a 30% discount to the global industry average of 12.6x.

No exceptional growth but resilient earnings We expect CEI to record a high-single-digit EPS growth yoy in FY17-19F, underpinned by slight sales growth and margin improvements. While such earnings prospects are unexciting vs. its peers, its profitability record has shown resilience since FY04. The company had an order book of S$46.8m as at end-Dec 2016 (vs S$49.0m at end-Dec 2015), which we expect to be fulfilled in FY17F.

Maintain Add We retain our FY17-19F forecasts, Add call and target price of S$1.11, pegged to 9.2x FY18F P/E (historical 10-year average P/E). Downside risks to our Add rating are unexpected order pushback and unfavourable forex movements of regional currencies against the US$.

SOURCE: COMPANY DATA, CIMB FORECASTS

Singapore

ADD (no change) Consensus ratings*: Buy 1 Hold 0 Sell 0

Current price: S$1.06 Target price: S$1.11 Previous target: S$1.11 Up/downside: 4.8% CIMB / Consensus: na

Reuters: CEII.SI Bloomberg: CEI SP Market cap: US$66.50m S$91.90m Average daily turnover: US$0.06m S$0.08m Current shares o/s: 86.70m Free float: 56.7% *Source: Bloomberg Key changes in this note

No change.

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) -8.2 0 43.2 Relative (%) -7.3 -1 31.3

Major shareholders % held Tien Sing Cheong 10.0 Republic Technologies Pte. Ltd. 9.0 TIHT Investment Holdings Pte. Ltd. 9.0

Analyst(s)

William TNG, CFA T (65) 6210 8676 E [email protected]

Financial Summary Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FRevenue (S$m) 132.3 130.3 136.8 143.6 150.8Net Profit (S$m) 10.81 8.81 9.63 10.47 11.24Core EPS (S$) 0.12 0.10 0.11 0.12 0.13Core EPS Growth 62.8% (18.5%) 9.4% 8.6% 7.3%FD Core P/E (x) 8.50 10.44 9.54 8.78 8.18Price To Sales (x) 0.69 0.71 0.67 0.64 0.61DPS (S$) 0.10 0.10 0.09 0.10 0.10Dividend Yield 9.43% 9.43% 8.39% 9.11% 9.78%EV/EBITDA (x) 5.45 7.16 5.39 4.75 4.21P/FCFE (x) 8.33 12.67 6.91 14.45 10.05Net Gearing (13.7%) (22.9%) (27.3%) (25.1%) (25.5%)P/BV (x) 2.29 2.29 2.18 2.08 1.98ROE 28.7% 21.9% 23.4% 24.2% 24.8%% Change In Core EPS Estimates 0% 0% 0%CIMB/consensus EPS (x) 1.01 1.01 1.00

90.0

110.0

130.0

150.0

0.600

0.800

1.000

1.200

Price Close Relative to FSSTI (RHS)

200400600800

Jul-16 Oct-16 Jan-17 Apr-17

Vol t

h

Tech Manufacturing Services│Singapore│CEI Limited│July 4, 2017

22

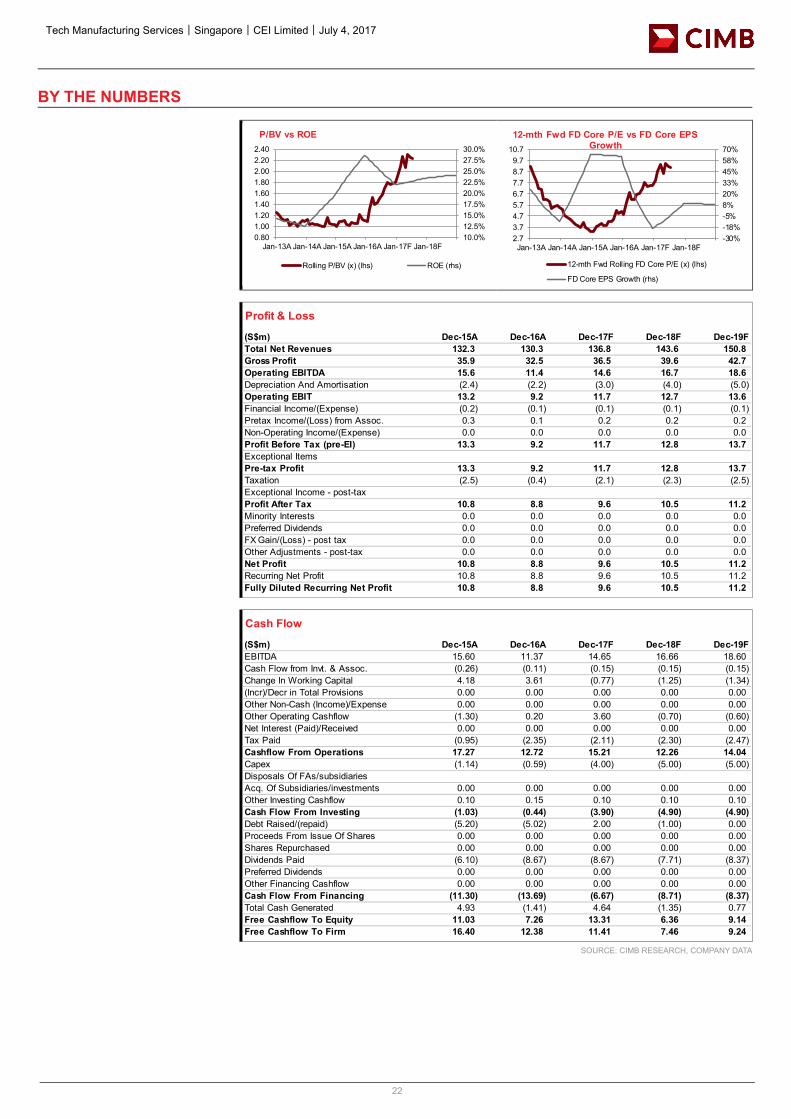

BY THE NUMBERS

SOURCE: CIMB RESEARCH, COMPANY DATA

10.0%12.5%15.0%17.5%20.0%22.5%25.0%27.5%30.0%

0.801.001.201.401.601.802.002.202.40

Jan-13A Jan-14A Jan-15A Jan-16A Jan-17F Jan-18F

P/BV vs ROE

Rolling P/BV (x) (lhs) ROE (rhs)

-30%-18%-5%8%20%33%45%58%70%

2.73.74.75.76.77.78.79.7

10.7

Jan-13A Jan-14A Jan-15A Jan-16A Jan-17F Jan-18F

12-mth Fwd FD Core P/E vs FD Core EPS Growth

12-mth Fwd Rolling FD Core P/E (x) (lhs)

FD Core EPS Growth (rhs)

Profit & Loss

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FTotal Net Revenues 132.3 130.3 136.8 143.6 150.8Gross Profit 35.9 32.5 36.5 39.6 42.7Operating EBITDA 15.6 11.4 14.6 16.7 18.6Depreciation And Amortisation (2.4) (2.2) (3.0) (4.0) (5.0)Operating EBIT 13.2 9.2 11.7 12.7 13.6Financial Income/(Expense) (0.2) (0.1) (0.1) (0.1) (0.1)Pretax Income/(Loss) from Assoc. 0.3 0.1 0.2 0.2 0.2Non-Operating Income/(Expense) 0.0 0.0 0.0 0.0 0.0Profit Before Tax (pre-EI) 13.3 9.2 11.7 12.8 13.7Exceptional ItemsPre-tax Profit 13.3 9.2 11.7 12.8 13.7Taxation (2.5) (0.4) (2.1) (2.3) (2.5)Exceptional Income - post-taxProfit After Tax 10.8 8.8 9.6 10.5 11.2Minority Interests 0.0 0.0 0.0 0.0 0.0Preferred Dividends 0.0 0.0 0.0 0.0 0.0FX Gain/(Loss) - post tax 0.0 0.0 0.0 0.0 0.0Other Adjustments - post-tax 0.0 0.0 0.0 0.0 0.0Net Profit 10.8 8.8 9.6 10.5 11.2Recurring Net Profit 10.8 8.8 9.6 10.5 11.2Fully Diluted Recurring Net Profit 10.8 8.8 9.6 10.5 11.2

Cash Flow

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FEBITDA 15.60 11.37 14.65 16.66 18.60Cash Flow from Invt. & Assoc. (0.26) (0.11) (0.15) (0.15) (0.15)Change In Working Capital 4.18 3.61 (0.77) (1.25) (1.34)(Incr)/Decr in Total Provisions 0.00 0.00 0.00 0.00 0.00Other Non-Cash (Income)/Expense 0.00 0.00 0.00 0.00 0.00Other Operating Cashflow (1.30) 0.20 3.60 (0.70) (0.60)Net Interest (Paid)/Received 0.00 0.00 0.00 0.00 0.00Tax Paid (0.95) (2.35) (2.11) (2.30) (2.47)Cashflow From Operations 17.27 12.72 15.21 12.26 14.04Capex (1.14) (0.59) (4.00) (5.00) (5.00)Disposals Of FAs/subsidiariesAcq. Of Subsidiaries/investments 0.00 0.00 0.00 0.00 0.00Other Investing Cashflow 0.10 0.15 0.10 0.10 0.10Cash Flow From Investing (1.03) (0.44) (3.90) (4.90) (4.90)Debt Raised/(repaid) (5.20) (5.02) 2.00 (1.00) 0.00Proceeds From Issue Of Shares 0.00 0.00 0.00 0.00 0.00Shares Repurchased 0.00 0.00 0.00 0.00 0.00Dividends Paid (6.10) (8.67) (8.67) (7.71) (8.37)Preferred Dividends 0.00 0.00 0.00 0.00 0.00Other Financing Cashflow 0.00 0.00 0.00 0.00 0.00Cash Flow From Financing (11.30) (13.69) (6.67) (8.71) (8.37)Total Cash Generated 4.93 (1.41) 4.64 (1.35) 0.77Free Cashflow To Equity 11.03 7.26 13.31 6.36 9.14Free Cashflow To Firm 16.40 12.38 11.41 7.46 9.24

Tech Manufacturing Services│Singapore│CEI Limited│July 4, 2017

23

BY THE NUMBERS… cont’d

SOURCE: CIMB RESEARCH, COMPANY DATA

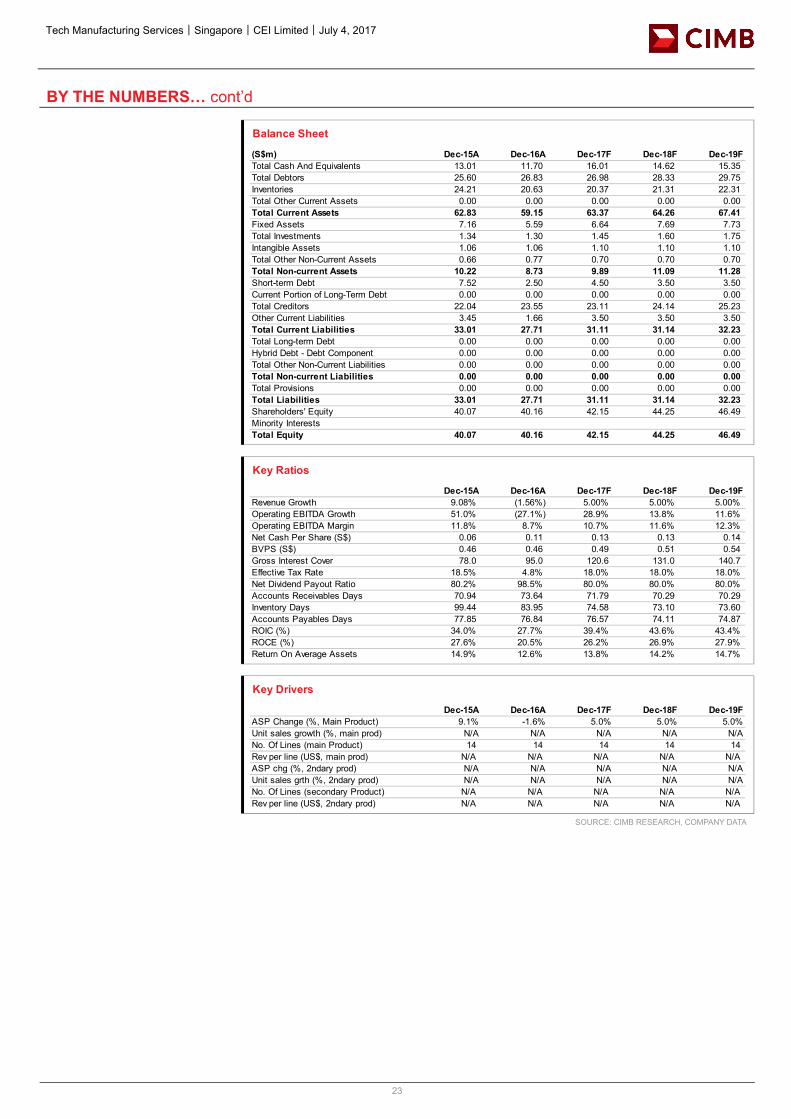

Balance Sheet

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FTotal Cash And Equivalents 13.01 11.70 16.01 14.62 15.35Total Debtors 25.60 26.83 26.98 28.33 29.75Inventories 24.21 20.63 20.37 21.31 22.31Total Other Current Assets 0.00 0.00 0.00 0.00 0.00Total Current Assets 62.83 59.15 63.37 64.26 67.41Fixed Assets 7.16 5.59 6.64 7.69 7.73Total Investments 1.34 1.30 1.45 1.60 1.75Intangible Assets 1.06 1.06 1.10 1.10 1.10Total Other Non-Current Assets 0.66 0.77 0.70 0.70 0.70Total Non-current Assets 10.22 8.73 9.89 11.09 11.28Short-term Debt 7.52 2.50 4.50 3.50 3.50Current Portion of Long-Term Debt 0.00 0.00 0.00 0.00 0.00Total Creditors 22.04 23.55 23.11 24.14 25.23Other Current Liabilities 3.45 1.66 3.50 3.50 3.50Total Current Liabilities 33.01 27.71 31.11 31.14 32.23Total Long-term Debt 0.00 0.00 0.00 0.00 0.00Hybrid Debt - Debt Component 0.00 0.00 0.00 0.00 0.00Total Other Non-Current Liabilities 0.00 0.00 0.00 0.00 0.00Total Non-current Liabilities 0.00 0.00 0.00 0.00 0.00Total Provisions 0.00 0.00 0.00 0.00 0.00Total Liabilities 33.01 27.71 31.11 31.14 32.23Shareholders' Equity 40.07 40.16 42.15 44.25 46.49Minority InterestsTotal Equity 40.07 40.16 42.15 44.25 46.49

Key Ratios

Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FRevenue Growth 9.08% (1.56%) 5.00% 5.00% 5.00%Operating EBITDA Growth 51.0% (27.1%) 28.9% 13.8% 11.6%Operating EBITDA Margin 11.8% 8.7% 10.7% 11.6% 12.3%Net Cash Per Share (S$) 0.06 0.11 0.13 0.13 0.14BVPS (S$) 0.46 0.46 0.49 0.51 0.54Gross Interest Cover 78.0 95.0 120.6 131.0 140.7Effective Tax Rate 18.5% 4.8% 18.0% 18.0% 18.0%Net Dividend Payout Ratio 80.2% 98.5% 80.0% 80.0% 80.0%Accounts Receivables Days 70.94 73.64 71.79 70.29 70.29Inventory Days 99.44 83.95 74.58 73.10 73.60Accounts Payables Days 77.85 76.84 76.57 74.11 74.87ROIC (%) 34.0% 27.7% 39.4% 43.6% 43.4%ROCE (%) 27.6% 20.5% 26.2% 26.9% 27.9%Return On Average Assets 14.9% 12.6% 13.8% 14.2% 14.7%

Key Drivers

Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FASP Change (%, Main Product) 9.1% -1.6% 5.0% 5.0% 5.0%Unit sales growth (%, main prod) N/A N/A N/A N/A N/ANo. Of Lines (main Product) 14 14 14 14 14 Rev per line (US$, main prod) N/A N/A N/A N/A N/AASP chg (%, 2ndary prod) N/A N/A N/A N/A N/AUnit sales grth (%, 2ndary prod) N/A N/A N/A N/A N/ANo. Of Lines (secondary Product) N/A N/A N/A N/A N/ARev per line (US$, 2ndary prod) N/A N/A N/A N/A N/A

Tech Manufacturing Services│Singapore│July 4, 2017 Shariah Compliant

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Jadason Enterprises Limited Drilling its way back to profitability ■ Leading PCB driller in China. ■ Earnings turnaround in FY17F and growth in FY18-19F driven by an existing

customer that won a 3-year supply contract from a leading mobile device brand. ■ Room for gross margin surprise given the significant operating leverage in this

business. ■ Trading at 6.7x FY18F versus 48% earnings growth in FY18F. We project strong

210% yoy growth in net profit for FY17F. ■ Recently initiated with an Add and target price of S$0.17.

Largest and most price-competitive PCB driller in Dongguan Jadason is a leading PCB driller based mainly in Dongguan, China. The company also has a plant in Suzhou. Its main business is the drilling of PCBs as well as the distribution of PCB manufacturing equipment and PCB drilling machines. Its role as a PCB equipment distributor allows Jadason access to the pulse of the industry and the ability to be cost-effective via repurchasing customers’ secondhand PCB drilling machines for refurbishment and addition to its own drilling capacity.

Has the share price peaked? Year-to-date (YTD), Jadason’s share price has gained 375%, reaching a YTD high of S$0.089 on 11 May 17. The share price was largely unaffected by the recent tech stock sell-off on NASDAQ. We believe that the share price has yet to peak as a) Jadason is trading at 9.9x/6.7x FY17/18F versus 210%/48% core EPS growth, and b) dividend payment is likely to resume in FY17F as the company has staged a significant earnings recovery

Share price driver #1: Could FY17 earnings surprise? Earnings surprise could come from 2 sources: a) stronger-than-forecast orders from a major customer, and b) major gross margin expansion as Jadason’s production equipment was significantly impaired in FY15, leading to lower depreciation charges. At the same time, there is considerable operating leverage in this business. Based on our channel checks, drilling for this major customer already started in the first week of July.

Share price driver #2: M&As Jadason has a strong net cash balance sheet. We understand that management is keen to pare down its bank borrowings further and raise its net cash balance. Other than the resumption of dividends in FY17F, it could also use its cash balance for M&As to diversify the business.

Share price driver #3: Dividends Although Jadason does not offer any formal dividend guidance, we noted that, in the past, the company paid 0.50 Scts DPS when operations were profitable. We believe dividend payments will resume in FY17F given our expectations of a return in profitability. We believe Jadason will temper dividend payments given the need to grow another revenue stream to diversify its business.

Recently initiated with an Add We recently initiated coverage on Jadason. Given our strong EPS CAGR projection of 68.6% for FY16-19F, we value Jadason at S$0.17. This is based on 12.34x P/E (+2 s.d. from average forward P/E during the last earnings recovery cycle in 2004-2007, when Jadason’s earnings accelerated significantly) applied to our FY18F core EPS estimate of S$0.013. The key risks are order pullback or delays by customers.

SOURCE: COMPANY DATA, CIMB FORECASTS

Singapore

ADD (no change) Consensus ratings*: Buy 2 Hold 0 Sell 0

Current price: S$0.100 Target price: S$0.17 Previous target: S$0.17 Up/downside: 66.4% CIMB / Consensus: 4.0%

Reuters: JADA.SI Bloomberg: JAD SP Market cap: US$52.46m S$72.50m Average daily turnover: US$1.13m S$1.69m Current shares o/s: 722.4m Free float: 55.9% *Source: Bloomberg Key changes in this note

N/A

Source: Bloomberg

Price performance 1M 3M 12M Absolute (%) 19 49.3 426.3 Relative (%) 19.9 48.3 414.4

Major shareholders % held Queeny Ho 32.6 Liaw Hin Hao 4.7 Fung Chi Wai 4.5

Analyst(s)

William TNG, CFA T (65) 6210 8676 E [email protected]

Financial Summary Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FRevenue (S$m) 63.10 57.15 75.10 89.61 97.24Net Profit (S$m) (32.10) 1.83 6.58 9.74 10.18Core EPS (S$) (0.024) 0.003 0.009 0.013 0.014Core EPS Growth 210% 48% 5%FD Core P/E (x) NA 34.05 10.98 7.42 7.10Price To Sales (x) 1.14 1.26 0.96 0.81 0.74DPS (S$) - - 0.005 0.007 0.007Dividend Yield 0.00% 0.00% 4.55% 6.74% 7.05%EV/EBITDA (x) NA 14.73 8.39 5.77 4.54P/FCFE (x) NA NA NA 45.30 11.10Net Gearing (27.3%) (21.7%) (10.5%) (6.8%) (8.8%)P/BV (x) 1.41 1.42 1.33 1.22 1.13ROE 4.1% 12.5% 17.2% 16.5%% Change In Core EPS Estimates 0% 0% 0%CIMB/consensus EPS (x) 0.91 1.12 1.17

52152252352452552

0.0090.0290.0490.0690.0890.109

Price Close Relative to FSSTI (RHS)

50

100

150

Jul-16 Oct-16 Jan-17 Apr-17

Vol m

Tech Manufacturing Services│Singapore│Jadason Enterprises Limited│July 4, 2017

25

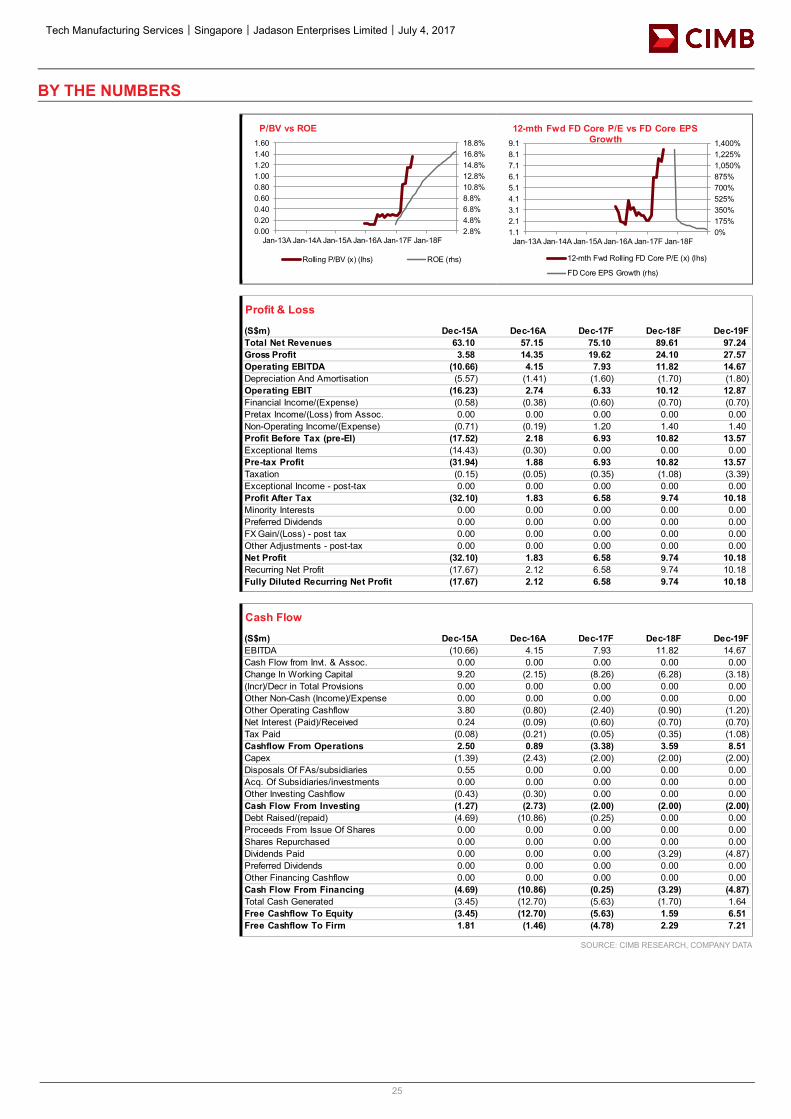

BY THE NUMBERS

SOURCE: CIMB RESEARCH, COMPANY DATA

2.8%4.8%6.8%8.8%10.8%12.8%14.8%16.8%18.8%

0.000.200.400.600.801.001.201.401.60

Jan-13A Jan-14A Jan-15A Jan-16A Jan-17F Jan-18F

P/BV vs ROE

Rolling P/BV (x) (lhs) ROE (rhs)

0%175%350%525%700%875%1,050%1,225%1,400%

1.12.13.14.15.16.17.18.19.1

Jan-13A Jan-14A Jan-15A Jan-16A Jan-17F Jan-18F

12-mth Fwd FD Core P/E vs FD Core EPS Growth

12-mth Fwd Rolling FD Core P/E (x) (lhs)

FD Core EPS Growth (rhs)

Profit & Loss

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FTotal Net Revenues 63.10 57.15 75.10 89.61 97.24Gross Profit 3.58 14.35 19.62 24.10 27.57Operating EBITDA (10.66) 4.15 7.93 11.82 14.67Depreciation And Amortisation (5.57) (1.41) (1.60) (1.70) (1.80)Operating EBIT (16.23) 2.74 6.33 10.12 12.87Financial Income/(Expense) (0.58) (0.38) (0.60) (0.70) (0.70)Pretax Income/(Loss) from Assoc. 0.00 0.00 0.00 0.00 0.00Non-Operating Income/(Expense) (0.71) (0.19) 1.20 1.40 1.40Profit Before Tax (pre-EI) (17.52) 2.18 6.93 10.82 13.57Exceptional Items (14.43) (0.30) 0.00 0.00 0.00Pre-tax Profit (31.94) 1.88 6.93 10.82 13.57Taxation (0.15) (0.05) (0.35) (1.08) (3.39)Exceptional Income - post-tax 0.00 0.00 0.00 0.00 0.00Profit After Tax (32.10) 1.83 6.58 9.74 10.18Minority Interests 0.00 0.00 0.00 0.00 0.00Preferred Dividends 0.00 0.00 0.00 0.00 0.00FX Gain/(Loss) - post tax 0.00 0.00 0.00 0.00 0.00Other Adjustments - post-tax 0.00 0.00 0.00 0.00 0.00Net Profit (32.10) 1.83 6.58 9.74 10.18Recurring Net Profit (17.67) 2.12 6.58 9.74 10.18Fully Diluted Recurring Net Profit (17.67) 2.12 6.58 9.74 10.18

Cash Flow

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FEBITDA (10.66) 4.15 7.93 11.82 14.67Cash Flow from Invt. & Assoc. 0.00 0.00 0.00 0.00 0.00Change In Working Capital 9.20 (2.15) (8.26) (6.28) (3.18)(Incr)/Decr in Total Provisions 0.00 0.00 0.00 0.00 0.00Other Non-Cash (Income)/Expense 0.00 0.00 0.00 0.00 0.00Other Operating Cashflow 3.80 (0.80) (2.40) (0.90) (1.20)Net Interest (Paid)/Received 0.24 (0.09) (0.60) (0.70) (0.70)Tax Paid (0.08) (0.21) (0.05) (0.35) (1.08)Cashflow From Operations 2.50 0.89 (3.38) 3.59 8.51Capex (1.39) (2.43) (2.00) (2.00) (2.00)Disposals Of FAs/subsidiaries 0.55 0.00 0.00 0.00 0.00Acq. Of Subsidiaries/investments 0.00 0.00 0.00 0.00 0.00Other Investing Cashflow (0.43) (0.30) 0.00 0.00 0.00Cash Flow From Investing (1.27) (2.73) (2.00) (2.00) (2.00)Debt Raised/(repaid) (4.69) (10.86) (0.25) 0.00 0.00Proceeds From Issue Of Shares 0.00 0.00 0.00 0.00 0.00Shares Repurchased 0.00 0.00 0.00 0.00 0.00Dividends Paid 0.00 0.00 0.00 (3.29) (4.87)Preferred Dividends 0.00 0.00 0.00 0.00 0.00Other Financing Cashflow 0.00 0.00 0.00 0.00 0.00Cash Flow From Financing (4.69) (10.86) (0.25) (3.29) (4.87)Total Cash Generated (3.45) (12.70) (5.63) (1.70) 1.64Free Cashflow To Equity (3.45) (12.70) (5.63) 1.59 6.51Free Cashflow To Firm 1.81 (1.46) (4.78) 2.29 7.21

Tech Manufacturing Services│Singapore│Jadason Enterprises Limited│July 4, 2017

26

BY THE NUMBERS… cont’d

SOURCE: CIMB RESEARCH, COMPANY DATA

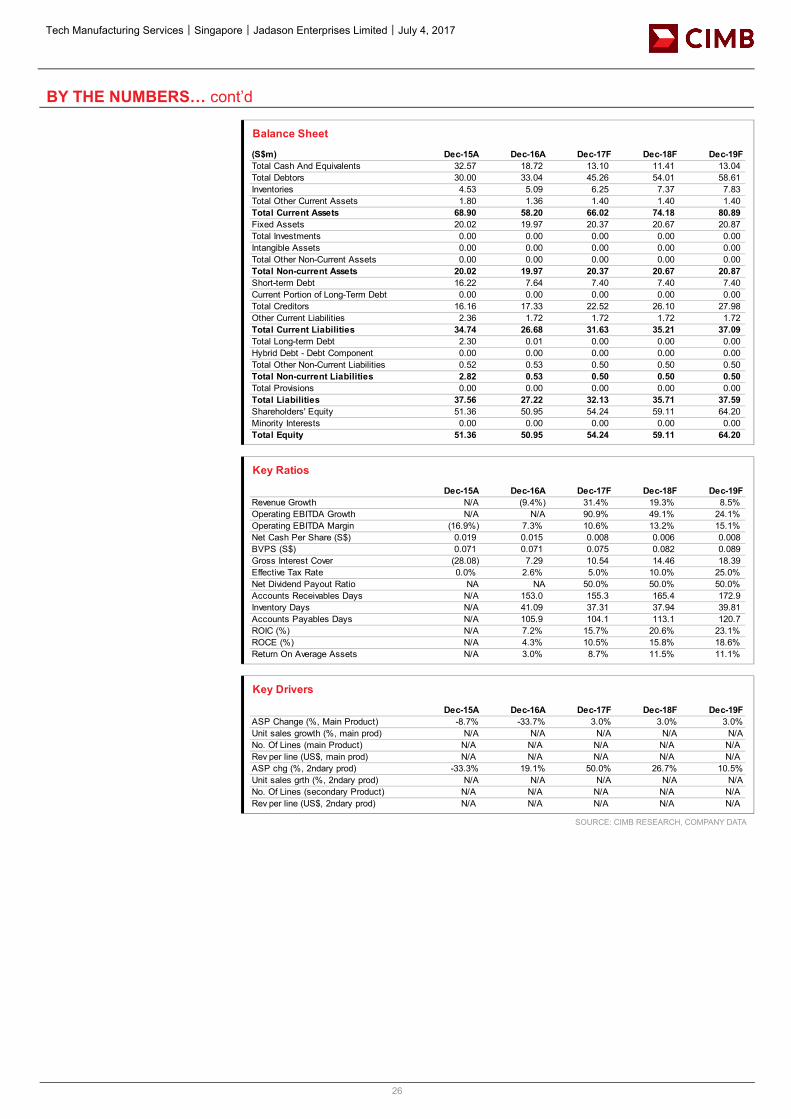

Balance Sheet

(S$m) Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FTotal Cash And Equivalents 32.57 18.72 13.10 11.41 13.04Total Debtors 30.00 33.04 45.26 54.01 58.61Inventories 4.53 5.09 6.25 7.37 7.83Total Other Current Assets 1.80 1.36 1.40 1.40 1.40Total Current Assets 68.90 58.20 66.02 74.18 80.89Fixed Assets 20.02 19.97 20.37 20.67 20.87Total Investments 0.00 0.00 0.00 0.00 0.00Intangible Assets 0.00 0.00 0.00 0.00 0.00Total Other Non-Current Assets 0.00 0.00 0.00 0.00 0.00Total Non-current Assets 20.02 19.97 20.37 20.67 20.87Short-term Debt 16.22 7.64 7.40 7.40 7.40Current Portion of Long-Term Debt 0.00 0.00 0.00 0.00 0.00Total Creditors 16.16 17.33 22.52 26.10 27.98Other Current Liabilities 2.36 1.72 1.72 1.72 1.72Total Current Liabilities 34.74 26.68 31.63 35.21 37.09Total Long-term Debt 2.30 0.01 0.00 0.00 0.00Hybrid Debt - Debt Component 0.00 0.00 0.00 0.00 0.00Total Other Non-Current Liabilities 0.52 0.53 0.50 0.50 0.50Total Non-current Liabilities 2.82 0.53 0.50 0.50 0.50Total Provisions 0.00 0.00 0.00 0.00 0.00Total Liabilities 37.56 27.22 32.13 35.71 37.59Shareholders' Equity 51.36 50.95 54.24 59.11 64.20Minority Interests 0.00 0.00 0.00 0.00 0.00Total Equity 51.36 50.95 54.24 59.11 64.20

Key Ratios

Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FRevenue Growth N/A (9.4%) 31.4% 19.3% 8.5%Operating EBITDA Growth N/A N/A 90.9% 49.1% 24.1%Operating EBITDA Margin (16.9%) 7.3% 10.6% 13.2% 15.1%Net Cash Per Share (S$) 0.019 0.015 0.008 0.006 0.008BVPS (S$) 0.071 0.071 0.075 0.082 0.089Gross Interest Cover (28.08) 7.29 10.54 14.46 18.39Effective Tax Rate 0.0% 2.6% 5.0% 10.0% 25.0%Net Dividend Payout Ratio NA NA 50.0% 50.0% 50.0%Accounts Receivables Days N/A 153.0 155.3 165.4 172.9Inventory Days N/A 41.09 37.31 37.94 39.81Accounts Payables Days N/A 105.9 104.1 113.1 120.7ROIC (%) N/A 7.2% 15.7% 20.6% 23.1%ROCE (%) N/A 4.3% 10.5% 15.8% 18.6%Return On Average Assets N/A 3.0% 8.7% 11.5% 11.1%

Key Drivers

Dec-15A Dec-16A Dec-17F Dec-18F Dec-19FASP Change (%, Main Product) -8.7% -33.7% 3.0% 3.0% 3.0%Unit sales growth (%, main prod) N/A N/A N/A N/A N/ANo. Of Lines (main Product) N/A N/A N/A N/A N/ARev per line (US$, main prod) N/A N/A N/A N/A N/AASP chg (%, 2ndary prod) -33.3% 19.1% 50.0% 26.7% 10.5%Unit sales grth (%, 2ndary prod) N/A N/A N/A N/A N/ANo. Of Lines (secondary Product) N/A N/A N/A N/A N/ARev per line (US$, 2ndary prod) N/A N/A N/A N/A N/A

Tech Manufacturing Services│Singapore│July 4, 2017

Company Note

IMPORTANT DISCLOSURES, INCLUDING ANY REQUIRED RESEARCH CERTIFICATIONS, ARE PROVIDED AT THE END OF THIS REPORT. IF THIS REPORT IS DISTRIBUTED IN THE UNITED STATES IT IS DISTRIBUTED BY CIMB SECURITIES (USA), INC. AND IS CONSIDERED THIRD-PARTY AFFILIATED RESEARCH.

Powered by the EFA Platform

Memtech International All stars aligned ■ Memtech is a precision engineering firm known for its liquid silicone rubber (LSR) and

multiple injection capabilities. ■ We believe its earnings trajectory in FY17-19F will be driven by higher AU and CE

sales orders and better margins. ■ MTEC could be an attractive M&A target, with its strong balance sheet, earnings

profile and established customer base, in our view. ■ Other potential catalysts include new customer wins and special dividends. ■ At 8.2x FY18F P/E and 0.74x P/BV, MTEC remains one of the cheaper tech plays in

Singapore, with 32.8% 3-year EPS CAGR and 4-6% dividend yields in FY17-19F.

Laggard tech manufacturing play As a precision engineering company, MTEC prides itself on its core competencies in LSR and multiple injection technology, which have successfully led its transformation from a pure keypad components manufacturer into an established supplier for both the automotive (AU) and consumer electronics (CE) industries today. It counts many tier-1 AU companies (such as Kostal, Magna and Faurecia) as well as leading CE brands (Beats, Amazon) as its major customers.

+45% ytd, but ripe for valuation re-rating MTEC has historically traded at a steep discount to its peers’ average as a result of its smaller market cap, trading illiquidity and patchy earnings record. We think the stock deserves a re-rating due to: a) its robust earnings growth, and b) net cash/share of 24.6 Scts at end-1Q17 (representing c.27% of market cap) that may be better utilised for higher dividends or synergistic M&A opportunities.

Still an Add rating We reiterate Add on MTEC with unchanged FY17-19F forecasts and target price of S$1.09, still pegged to 10x FY18F P/E (at 10% discount to peer average). Downside risks to our Add call include unexpected project delays or cancellation.

Share price driver #1: Earnings growth accelerating MTEC’s 1Q17 core net profit of US$1.7m was an improvement over the US$0.4m in 1Q16, driven by double-digit sales growth in both AU and CE segments. 1Q17 gross margin of 18.1% benefited from greater volume and economies of scale, up from 1Q16’s 15.9%. We project earnings growth of 22-56% p.a. over FY17-19F, underpinned by increasing orders from existing customers and margin expansion. We note that 2H is seasonally stronger and our forecasts have yet to factor in potential new customer wins.

Share price driver #2: Potential special dividends We forecast FY17-19F dividend yields of 4-6% for MTEC, based on its dividend policy of not less than 30% of net profit. The company has consistently paid dividends, even during its loss-making years of FY12-13. Backed by recent net proceeds of c.US$5.7m from the sale of two land assets in China and a healthy net cash position of US$28m as at end-1Q17 to meet its annual estimated capex requirement of US$10m-12m, we believe a special dividend could be on the cards for FY17F to reward shareholders.

Share price driver #3: M&As? We think MTEC now looks attractive as an M&A target given its cash-generative business, growing customer base and the fact that earnings are possibly at an inflection point. Competitors keen to break into the automotive and Beats supply chain but deterred by the high entry barriers (long audit process and strict technical know-how) could instead seek a faster way by acquiring firms like MTEC.

SOURCE: COMPANY DATA, CIMB FORECASTS

Singapore

ADD (no change) Consensus ratings*: Buy 2 Hold 1 Sell 0

Current price: S$0.91 Target price: S$1.09 Previous target: S$1.09 Up/downside: 20.6% CIMB / Consensus: 12.5%

Reuters: MEMT.SI Bloomberg: MTEC SP Market cap: US$92.26m S$127.5m Average daily turnover: US$0.47m S$0.65m Current shares o/s: 140.9m Free float: 50.0% *Source: Bloomberg Key changes in this note

Not applicable.

Source: Bloomberg