Capabilities Overview Presentation Overview Presentation. About Baxter

OVERVIEW

PROPOSED INCORPORATION

OF SUNRISE MANOR TOWN

APRIL 3, 2018

Presented by:

Jeffrey Share, Clark County Budget Director

Today’s Presentation

The purpose of today’s presentation is:

To present an overview and answer questions

regarding current revenues/costs and current

levels of services provided by Clark County

within the boundaries of the Town of Sunrise

Manor.

2

Today’s Presentation

Points of clarification:

The Clark County staff is neither “for” nor

“against” the incorporation of Sunrise Manor

Town.

The County’s involvement is solely to provide

interested parties with revenue/expenditure

information and to provide a description of our

current levels of services.

The County considered the current Sunrise Manor

Town boundaries for the proposed City.

3

Overview of

Clark County

Clark County Overview

Population: 2,205,207 – July 1, 2016 (Source: State of NV Demographer / Clark County Department of Comprehensive Planning)

Las Vegas: 29.03%

North Las Vegas: 11.10%

Henderson: 13.57%

Mesquite: 0.92%

Boulder City 0.75%

Unincorporated Clark County

inside Las Vegas Valley: 44.32%

outside Las Vegas Valley: 0.31%

NOTE: Sunrise Manor Town is 9.68% of the total Countywide population at 213,444 persons

5

Clark County Overview

• Clark County is the largest and most complex

governmental agency in the State.

• Clark County provides both regional and town

services.

• Regional services are provided to all residents within Clark County, including those who live within the cities of Boulder, Henderson, Las Vegas, Mesquite and NLV.

• Town (Municipal) services are ONLY provided to residents who live in unincorporated Clark County. These services are similar to those provided by the cities of Boulder, Henderson, LV, Mesquite and NLV.

6

Clark County Overview

Air Quality Mgt

Assessor

Aviation

Clerk

Coroner

Detention*

District Attorney

District Court

Elections

Family Services

Juvenile Justice

Public Admin

Public Guardian

Public Defender

Recorder

Social Service

UMC*

Countywide Services

Admin Svcs / HR

Information Tech

Finance

Real Property Mgt

Treasurer

Support Services

Development Svcs

Business License

Comprehensive Planning

Constable

Fire

Justice Court

Parks & Recreation

Police (LVMPD)*

Public Works

Water Reclamation

Town Services

County Manager

Commissioners

NOTE: Blue text denotes department is a

General Fund department.

* Indicates % of funding provided by General

Fund

7

Current Boundary

of Sunrise Manor

8

Incorporation Background

How to Incorporate?

9

Incorporation Background

Incorporation of an area is governed under Nevada

Revised Statute 266.

The initiation to incorporate may begin through:

a Legislative act

a petition filed by a committee of five qualified electors

(registered voters) submits the proposal to the County

Either option requires a financial feasibility study

from both the County and the State Department of

Taxation (through the Committee on Local

Government Finance).

10

Incorporation Background

If either body finds that incorporation is fiscally

feasible, an election on the question of incorporation

must be held to allow the residents of the Town to

decide whether or not to incorporate.

The election simultaneously offers the opportunity to

select the offices of Mayor and City Council.

11

Sunrise Manor Town Revenues

There are four sources of revenue within the

(current) Town of Sunrise Manor:

Major revenue sources

Property Taxes

Consolidated Taxes (primarily sales tax)

Other revenue sources

Licenses & Permits

Charges for Services

12

OVERVIEW OF

CURRENT AND ANTICIPATED

REVENUES & EXPENDITURES

Property Taxes

Property Taxes- Each governmental entity that has taxing

authority over a particular parcel may levy a rate that, in

total, cannot exceed Nevada’s constitutionally-set limits. The

voters may also impose a levy upon themselves.

Property taxes are based upon a percentage of assessed

valuation of all residential and commercial parcels. The

assessed valuation is used by the County Treasurer to calculate

a tax amount.

Fiscal Year 2018 budgeted real and personal property tax

collections within the (current) Town of Sunrise Manor is

expected to be $4.36 Million.

14

Comparison of City/Town Tax Rates

Boulder

City

Mesquite Henderson Uninc. Clark Las Vegas North Las

Vegas

State, County &

School

$2.1275 $2.1275 $2.1275 $2.1275 $2.1275 2.1275

Library

Operations &

Debt

0.2239 0.0942 0.0604 0.0942 0.0942 0.0632

City / Towns

(all inclusive)

0.2600 0.5520 0.7108 0.7061 1.0515 1.1587

Emergency

Police 911

0.0000 0.0000 0.0000 0.0050 0.0050 0.0050

Total- Per $100

of assessed

value

$2.6114 $2.7737 $2.8987 $2.9328 $3.2782 $3.3544

15

Example of a current Sunrise Manor Town

Property Tax Bill

Taxing EntityCurrent

Tax Rate

Town of Sunrise (Operating) $0.2064

LV Metro Police Manpower Supplement (expires in 2028) $0.2000

LV Metro Police Manpower Supplement (in perpetuity) $0.0800

Clark County Fire Service District $0.2197

Las Vegas Metro 911 $0.0050

State of Nevada $0.1700

Clark County (Regional Services) $0.6541

Clark County School Dist. (Operations & Maintenance) $1.3034

Las Vegas – Clark County Library District $0.0942

TOTAL $2.9328

16

$4.73

$3.48

$2.36$2.23

$1.99 $2.05

$2.40

$2.75$2.93

$3.16

$0.0

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

$4.0

$4.5

$5.0

FY

2009

FY

2010

FY

2011

FY

2012

FY

2013

FY

2015

FY

2014

FY

2017

(In Billions)

Sunrise Manor Town Assessed Valuation

FY2009 - FY2018

FY

2016

FY

2018

17

$7.08

$6.64

$4.47

$4.02 $3.97$4.08

$4.18 $4.24$4.36

$4.73

$3.0

$3.5

$4.0

$4.5

$5.0

$5.5

$6.0

$6.5

$7.0

$7.5

FY

2009

FY

2010

FY

2011

FY

2012

FY

2013

FY

2015

FY

2014

FY

2018 (

es

t.)

(In Millions)

Sunrise Manor Property Tax Collections

FY2009 - FY2018

FY

2016

FY

2017

18

Sunrise Manor Town

LVMPD Property Tax Rate

Using the Sunrise Manor Town rate, it is expected the

$0.2800 tax rate would generate approximately

$5.92 million.

The County spends approximately $21.8 million on

police services within the Northeast Area Command –

the primary coverage area within Sunrise Manor.

The County subsidizes the cost of police service within

Northeast Command through other Town revenues by

$15.9 million.

19

Northeast Area Command

20

Sunrise Manor Town

Fire Service Property Tax Rate

Using the Sunrise Manor Town rate, it is expected the

$0.2197 tax rate would generate approximately

$4.64 million on the current $0.2197 fire tax rate.

The current annual operating expense per station is

approximately $4.38 million using current County

staffing levels at the SIX stations within the current

boundaries of Sunrise Town.

The County subsidizes the (operational) cost of fire

service within the current Town boundaries by

approximately $21.6 million.

21

Property Tax

Fire Rate

The County’s six existing fire stations within the

current Town boundaries:

Station 16 – 6131 E. Washington Ave, 89110

Station 20 – 5865 Judson Ave, 89156

Station 23 – 4250 E. Alexander Rd., 89115

Station 27 – 4695 Vegas Valley Dr., 89121

Station 31 – 2190 S. Hollywood Blvd., 89156

Station 61 – 150 N. Nellis Blvd., 89110

22

Sunrise Manor Town

Consolidated Tax Revenues

Consolidated Tax – consists of a mixture of tax revenues

from a State consolidated fund consisting of revenues

generated by sales taxes, cigarette taxes, liquor taxes,

real property transfer taxes and government services

(motor vehicle) taxes. The State Department of Taxation

allocates revenue based upon a Statewide distribution

formula. Approximately 85% of consolidated revenue is

sales tax.

Fiscal Year 2018 budgeted consolidated tax collections

allocated to the (current) Town of Sunrise Manor is

approximately $11.2 million.

23

Sunrise Manor Consolidated Tax Revenues

(FY2009 - FY2018) (in millions)

$7.83 $7.29 $7.48

$7.99 $8.41

$9.18

$10.06 $10.57

$11.26 $11.21

$0.0

$2.0

$4.0

$6.0

$8.0

$10.0

$12.0FY

20

09

FY 2

01

0

FY 2

01

1

FY 2

01

2

FY 2

01

3

FY 2

01

4

FY 2

01

5

FY 2

01

6

FY 2

01

7

FY 2

01

8(b

ud

get)

24

Consolidated Tax Revenues

Pursuant to NRS 360.740, the proposed City would

be entitled to apply to the Department of Taxation

for an allocation from the Consolidated Tax

distribution account IF:

The new city provides police protection, and

At least two of the following services:

Fire protection;

Construction, maintenance and repair of roads; or

Parks and recreation.

25

Consolidated Tax Revenues

A request must be made by majority vote of the city

council; and

The request must be sent to the Nevada Tax

Commission who directs the Executive Director of the

Department of Taxation to allocate money from the

Consolidated Tax account. It may not continue to

be the current allocated amount.

26

License & Permit Revenues

Licenses & Permits – this revenue source is primarily

comprised of various business license fees, building

permits fees and gaming fees.

The budgeted Fiscal Year 2018 collections for the various fixed

rate business licenses within the (current) Town of Sunrise Manor is

projected at $429,000 (excluding fees based upon gross

revenues such as liquor & gaming, room taxes, etc.).

The budgeted Fiscal Year 2018 collections for gaming device

fees within the Town of Sunrise Manor is projected at $974,000.

Franchise fees are indeterminable as they are based

upon revenues derived from customers within the

specific jurisdiction.

Gaming license fees are County revenues.

27

Charges for Services Revenues

Charges for services – this revenue source is primarily

comprised of various park & recreation fees related

to programming and pool admissions and would be

allocated to the proposed City.

Actual Fiscal Year 2017 revenue collections within the

various Sunrise Manor Town park facilities was

$888,161.

Operational expenditures totaled $3,258,493

(excluding utilities, insurance, building/park/pool

maintenance, etc.).

28

Charges for Services Revenues

Charges for services (continued):

Included within the current boundaries, the

Town/proposed City includes the Club at Sunrise

(formerly the Desert Rose Golf Course).

In Fiscal Year 2017, the Club generated

$870,867 in revenues.

Operational expenses and flood channel-related

maintenance in Fiscal Year 2017 totaled

$2,961,399.

29

Revenues Generated within the (current) boundaries

of Sunrise Manor Town

Consolidated Tax

38.3%

Property Tax

50.9%

Licenses & Permits

4.8%

Charges for Services

6.0%

Based upon recalculated Town revenues of $29,296,277

30

Sunrise Manor Revenues

Revenue Source Projections

Property Tax (includes Real & Personal

Property, Metro and Fire rate)*$ 14,922,236

Intergovernmental Revenues / C – Tax** 11,212,013

Licenses & Permits 1,403,000

Charges for Services 1,759,028

TOTAL $ 29,296,277

• Based upon the Fiscal Year 2018 Sunrise Manor Town Budget, but adjusted to attempt to calculate within the

Town boundaries.

• ** To be determined by Department of Taxation. The current Fiscal Year 2018 allocation is included above.

31

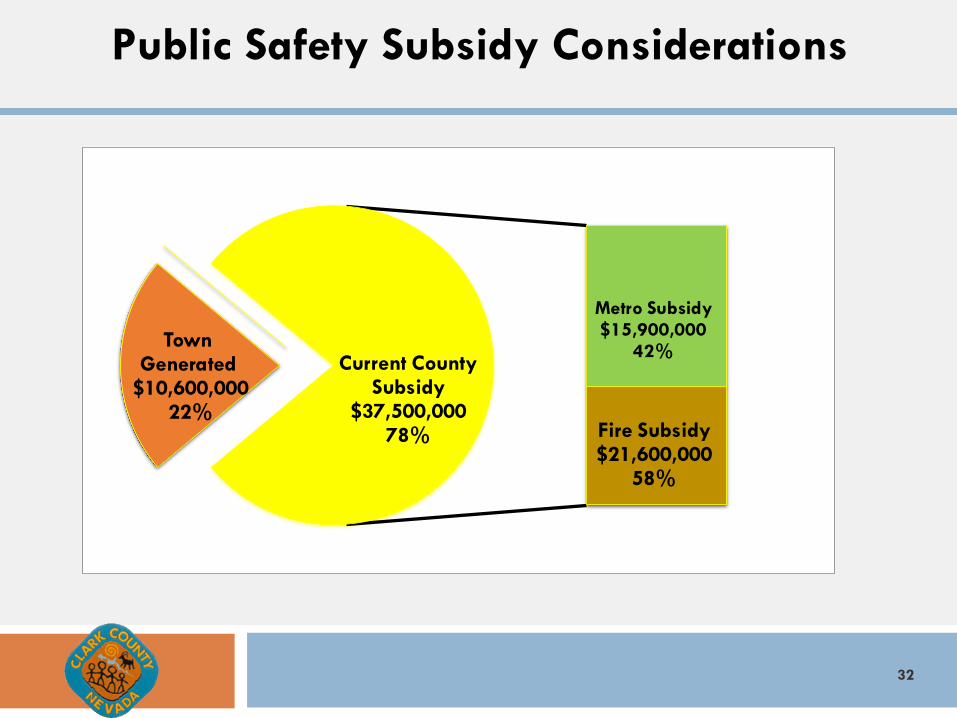

Public Safety Subsidy Considerations

Town Generated

$10,600,00022%

Metro Subsidy $15,900,000

42%

Fire Subsidy $21,600,000

58%

Current County Subsidy

$37,500,00078%

32

Expenditure

Considerations

Expenditure Considerations

Police & Detention

The proposed City will be responsible for paying for

its own police support. The LV Metropolitan Police will

no longer provide this service if the Town incorporates.

The LV Metropolitan Police does not contract out its

services to other entities.

The proposed City would need to either build its own

jail/detention facility or negotiate with another local

entity to house its inmates. The County’s two detention

facilities are both at maximum capacity, and will be

unable to take in another jurisdiction’s inmates.

34

Expenditure Considerations

Public Works and Parks & Recreation

The proposed City will be responsible to maintain its

own public works infrastructure including road

maintenance, traffic operations, signs, streetlights,

traffic signals, pavement markings, etc.

The proposed City will be responsible for the current

County park & recreation facilities within its

boundaries. Existing properties include 225

developed acres with five community centers, thirteen

various-sized parks, Horseman’s Park, Dog Fancier’s

Park, and the Club at Sunrise.

35

Expenditure Considerations

Fire & Emergency Medical Services

If the proposed City does not create its own fire

department, it would need to pursue an arrangement

with a fire department other than the Clark County

Fire Department for fire support.

The County does not provide mutual aid to another

entity unless the expected services provided and/or

call volume are equal to the service levels received by

the County.

36

Expenditure Considerations

Fire & Emergency Medical Services

If the proposed City proposes to perform its own EMS

transport, it will need to establish a program to

comply with local, State and Federal guidelines and

requirements.

In addition to the direct costs of staffing and supplies

at fire stations, there are indirect costs relating to

providing its EMS quality assurance, emergency

preparedness, infection control, logistics, warehousing,

training, mechanics, fire prevention and fire

investigation.

37

Various other issues/concerns to consider

Transfer of Assets

Wastewater treatment

Building & Safety Department

Administrative staffing functions such as Finance,

Accounting, Human Resources, Information

Technology infrastructure, Comprehensive

Planning, Animal Control, Public Response, etc.

Administrative offices for the City

Courthouse, judge and court staff for the City

38

Questions?