Overview of Nelion Partners Ltd

27

Unlocking superior returns via a diversified African Investment Platform May 2015 Investment Presentation Strictly Confidential

-

Upload

samy-ghannam -

Category

Economy & Finance

-

view

32 -

download

0

Transcript of Overview of Nelion Partners Ltd

Unlocking superior returns via a diversified African Investment Platform

May 2015

Investment Presentation Strictly Confidential

Disclaimer

This Investment Presentation (“IP”) constitutes a ‘Private Offer’ as defined by Regulation 21 of the Capital Markets (Securities) (Public Offers, Listing and Disclosures) Regulations, 2002 under the Capital Market Act, and should not therefore be deemed to be an offer to the public. This IP is for private and confidential use by the recipient, its employees and advisers, and may not be reproduced, referred to or provided to other parties in whole or in part. The recipient of this IP, by accepting delivery thereof, agrees to return it and related documents to the Company if the recipient elects not to invest. This IP is only meant for the person to whom it has been addressed and is strictly not for the use or consideration of any other person. It is illegal to copy, reproduce or distribute this Information Memorandum to any person including the media houses (who are not to publish any contents herein whatsoever).

2

1. Executive Summary

Founded in March 2015, Nelion Partners Limited (or “Nelion Partners” or “Nelion”) is a Seychelles incorporated investment holding company, dedicated to provide its investors with a diversified exposure towards the fast growing African economic landscape. Nelion’s investment strategy is the address attractive opportunities in the following asset classes: • Listed Equities with a focus on the Energy, Banking, Insurance and Retail mid-Cap opportunities,

unlocking value out of mid-term holding positions based on strong fundamentals • Money Market placements taking advantage of attractive market conditions and LCY prevailing rates • Real Estate residential assets with mid-term holding strategies for undeveloped serviced plots in fast

growing middle income areas • Private Equity investments via Seed and Venture capital initiatives, leveraging the founding partners’

network Nelion completed a first capital raising initiative in May 2015, with the subscription of 46 individual investors (besides the 4 founding Partners) for a total consideration of USD 400k (underpinning a 35% oversubscription). Proceeds from the first capital call are channeled into Kenyan and Nigerian listed Equities as well as pre-IPO Private Equity opportunities. Nelion is currently considering the issue of additional shares in order to support the geographic expansion of the portfolio, the formalization of the Investment Management framework and the diversification into alternative Asset classes (Venture Capital & Real Estate).

3

2. Macroeconomic Overview

4

Africa’s Growth Story in 6 Drivers: Macro & Political Stability: Political and economic risk rating of African countries are comparable to the BRIC countries, while Governments reduced inflation from 23% (1995-2005) to 8% (2005-2013), debt from 105% to 52% and currency volatility from 29% to 12%. On-going Economic Reforms: Widespread business-friendly reforms and cross border trade agreements are making it easier to do business in many African countries, Access to International Capital: Capital inflows of USD 84 billion p.a. with the highest return on FDI (9%+) across all emerging markets Seismic Demographic Shift: World’s largest working age population by 2035 of 1.1bn Enhanced Complexity of Economic Pillars: Africa represents a large and growing opportunity in critical industries: fast-moving consumer goods, Financial Services, Real Estate, Information & Technology, Healthcare, Education as well as infrastructure, etc. Commodity Boom: Africa is resource rich and cost competitive to source many minerals / commodities

2.1 Africa: the last Frontier

Africa is home to six of the ten fastest-growing economies in the world. The Gross Domestic Product (GDP) per household in Africa has more than doubled in the last 15 years with around 85 million households currently earning at least $5,000 a year. Rapid growth in population and urbanization has continued to lead consumers within the African continent to purchase more goods and services, in a development that has made it easier for companies to reach consumers with products, services, and communications. Africa’s overall economy should advance in 2015, expanding by 4.5%, showing resilience despite weak commodity prices, terrorism threat and the now curbed Ebola West African epidemic.

5

1

2

3

4

5

6

2.2 Kenyan Macroeconomic Outlook

Kenyan Real GDP growth is estimated at 4.9% and 5.7% in 2013 and 2014 respectively. Besides the recorded performance, Kenya has been classified as a middle-income country after a statistical reassessment of its economy increased the size by 25.3% in September 2014. The East African nation effectively becomes Africa’s ninth largest economy, surpassing Ghana, Tunisia and Ethiopia GDP performance in 2014 was largely led by expansion in manufacturing, construction, trade and financial services sectors with a slowdown felt in both Tourism and Agriculture sectors. Global market prices for key export commodities, Tea and Coffee, remained depressed resulting in the lower agriculture performance while negative travel advisories by some key tourist source countries, due to insecurity concerns, occasioned the reduced tourist arrivals Advancement in manufacturing and construction is expected to carry on through 2015, supported by the higher expenditure allocation by the Government, to Infrastructure and Energy projects (22.6% of Budget) as Kenya progresses towards becoming a regional trade and energy transit hub. Overall, the continued stability of macro factors and high business confidence shall weigh in positively on Kenya’s GDP performance in the year while continued slackening in tourism and Agriculture export earnings will likely dampen growth outlook in 2015. IMF projections estimate Real GDP growth to reach 6.2% in 2015 against Kenya Government treasury estimate of 6.9% The Kenyan economy’s short to medium-term forecast is for sustained and rising growth based on

ü Increased investor and business confidence in the wake of peaceful March 2013 elections; ü A stable macroeconomic environment; ü Lower international oil prices; ü Long-Term Stability of the Kenya shilling, despite the recent volatility; and ü Ongoing reforms affecting security, governance and justice.

1

2

3

4

6

2.2 Kenyan Macroeconomic Outlook (cont’d)

Kenyan GDP Growth

5.8%

4.4% 4.6% 4.7%

5.5%5.9%

5.1%

4.2%3.8% 3.8%

4.8%

5.7%

5.8%

5.8%5.3% 5.4%

6.3%6.8%

3%

4%

5%

6%

7%

8%

2010 2011 2012 2013 2014 2015 F

Kenya SSA EAC

GDP Contribution per sector

Highlight of major Growth Drivers • The Lamu Port Southern Sudan-Ethiopia Transport (LAPSSET) Corridor is the upcoming second largest

Kenyan transport corridor, unlocking enormous regional trade potential towards the Northern land locked countries (Ethiopia, South Sudan).

• Growth in Foreign Direct Investments is fuelled by natural resources, current infrastructure development

and a market leadership role in the Greater East African region.

• Oil and Gas resources: Despite the current global uncertainties, Kenyan oil reserves are currently estimated at around 1 Billion barrels. Alongside the sizeable natural gas discoveries in North Eastern province, the country is embarking on a major infrastructure-development plan. 7

2.2 Kenyan Macroeconomic Outlook (cont’d)

Highlights of the Performance of the Nairobi Securities Exchange

In 2014, Nairobi All Share Index posted a +19.2% return in 2014 making that a three year Bull Sequence, recording an overall return of close to 120% since January 2012.

Over the past 5 years, the Nairobi Securities Exchange has also outperformed its regional and global peers, including main sub-Saharan African, European and US indexes.

8

0

50

100

150

200

250

Feb-‐10 May-‐10 Aug-‐10 Nov-‐10 Feb-‐11 May-‐11 Aug-‐11 Nov-‐11 Feb-‐12 May-‐12 Aug-‐12 Nov-‐12 Feb-‐13 May-‐13 Aug-‐13 Nov-‐13 Feb-‐14 May-‐14 Aug-‐14 Nov-‐14

Chart Title

NSE… S&P 500 CAC 40 LSE FTSE 100 Index MSCI Frontier Index MSCI Emerg Index JALSH Nigeria All Share DJ IndustrialNSE All Share

3. Overview of Nelion Partners

9

3.1 Nelion Partners: The Concept

Nelion Partners has been created by a group of business executives sharing a long-term attachment to the African economic landscape and the entrepreneurial vision of structuring a scalable investment holding platform. Nelion Partners is structured as an avenue for the founders to provide a compelling proposition to their network of family and friends without direct exposure to the investable landscape in one of the fastest growing economies in the world. 2014 was an exciting year for investors and investment bankers alike in East Africa. Largely supported by Kenyan transactions, 145 corporate deals were announced in the region (up 49% from the 97 deals announced in 2013), and the Equity markets across East Africa rose by an average of 27%. There are no signs that the on-going momentum will head towards adverse performance over the short to mid term outlook. Nelion Partners will initially channel its capital into Kenyan and Nigerian liquid Equity and Debt instruments, in order to generate a marketable return and track record for future investors. Within the first 12 months, the founders also intend to scale up the Nelion platform via the diversification into alternative asset classes, primarily Real Estate and Private Equity. These initiatives will be funded by follow-on cash calls and debt leverage initiatives.

1

2

3

4

5

10

3.2 Nelion Partners: Business Model

1. Relationship & Trust

2. Strong Deal Sourcing

Capabilities

3. Enhanced Monitoring

Nelion Partners is leveraging the founders day-to-day business involvement in the local Investment and Commercial Banking scene in order to provide robust deal sourcing & research access capabilities. Besides, the initial management team (the “founding Partners”) offers a diversified range of skills and track record covering the key target industries and assets classes (Listed Equities, Private Equity, Real Estate, Fixed Income), hence providing a balanced portfolio. Furthermore, the on-the-ground presence of the founding Partners will support the portfolio management initiatives, with the ability to timeously exploit opportunities.

11

4. Scalable platform

5. Blended Portfolio

6. Diversity of skills

3.3 The Founding Partners

Samy Ghannam – Chairman & Partner Mr. Ghannam is the Corporate Finance Associate Director at Genghis Capital where he heads the Equity and Debt Capital Market advisory activities. He is also the Chief Executive Officer (CEO) at Rinascimento Global Limited, an Investment Holding Company with a diversified portfolio in the Kenyan banking and Real Estate sector. He has been involved in the East African Investment Banking industry since 2009, when he joined the Proparco Regional Office in Nairobi, in charge of sourcing and structuring Private Equity and Debt investments across various industries. Mr. Ghannam holds a Master in Science of Management from EM Lyon, a leading European Business School. Clement Martineau – Vice Chairman & Partner Mr. Martineau is the General Manager of Lighthouse Property Company, a diversified Real Estate Development and Management firm, associated to the Chase Bank (Kenya) Group of companies. He ensures the day to day operations, develops opportunities and then leads and supervise all the projects from residential to commercial. Prior to joining Lighthouse Property, Clement Martineau was managing the Real Estate portfolio (300+ properties across the country) of Orange Kenya, the third largest Telecom operator in Kenya. Mr. Martineau holds an engineering degree in Building Economics from Paris St Lambert, a reputable French building school.

1

2

12

3.3 The Founding Partners (cont’d)

Guy Brennan – Partner Mr. Brennan is a founding partner of Ascent Capital, an East Africa focused Private Equity fund manager with close to USD 80m under management. Prior to joining Ascent, he worked in Investment Banking in Europe before moving to Africa in 2006, joining FINCA, one of the world’s largest micro-finance organizations. He spent the last 9 years living in Kenya, Ethiopia and Uganda. He brings on board tremendous Private Equity experience and extensive regional knowledge. He holds a Bachelor of Commerce degree from the University of Sydney and an MBA from INSEAD. Stanley Gabriel – Partner Mr. Gabriel is the Head of Strategy at Old Mutual in West Africa where he is positioned to grow the relatively new business in the largest economy in Africa and expand further into the region. Previously, he has worked in South Africa as the right-hand man of the CEO of Old Mutual Emerging Markets with a footprint in 17 countries. Stanley lived and worked in Kenya for 3 years where he led projects in distribution expansion and then co-owned a wine and logistics business in East Africa. He will provide a wealth of experience having worked in three of the most strategic economies in formulating and executing mid-long term strategies. He holds a B.Sc (Maths, Statistics and Actuarial Science) from the University of Cape Town and a Diploma in Actuarial Techniques from the Institute of Actuaries (UK).

3

4

13

3.4 Nelion Partners : The Operating Framework

Maximum Exposure per Industry: 45% of the Total Assets Maximum exposure per Asset class: 65% of the Total Assets Maximum Investment per Investee Company: 35% of the Total Assets Minimum Investment Consideration: 5% of the total Assets, when applicable The Capital of Nelion Partners will be divided into Class A and Class B shares (at a par value of USD 1.00 each), which future value will follow the performance of the underlying assets. Governance: (i) The Founding Partners hold Class B shares, granting them the overall responsibility of managing the

investment framework of Nelion Partners (ii) Decision Making Process: Investment Committee comprising of all founding members plus invited

members subject to specific agenda. IC meets every week, with virtual access to proposals in-between committee meetings. Every investment / divestment decision require a 66% approval threshold by the Founding Partners

(ii) Investor Relations: (i) Monthly Report with Portfolio Breakdown & Valuations (ii) Quarterly Macroeconomic Updates (iii) Bi-annually conference calls to provide updates on key performance indicators, structural

updates and strategic initiatives

1

2

3

4

5

6

14

4. The Proposed Investment

15

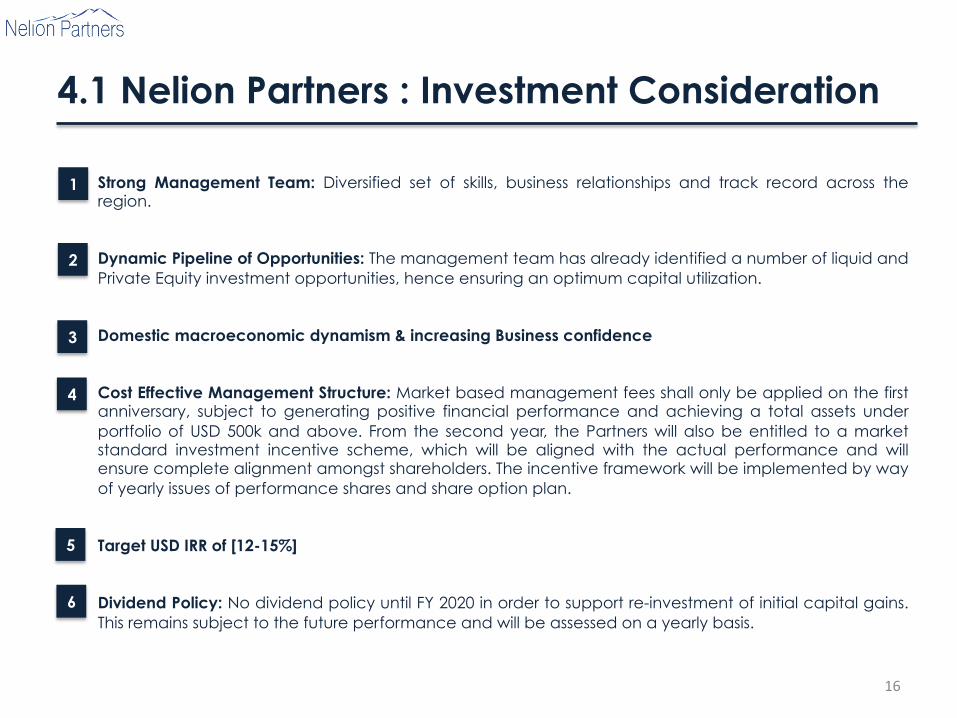

4.1 Nelion Partners : Investment Consideration

Strong Management Team: Diversified set of skills, business relationships and track record across the region. Dynamic Pipeline of Opportunities: The management team has already identified a number of liquid and Private Equity investment opportunities, hence ensuring an optimum capital utilization. Domestic macroeconomic dynamism & increasing Business confidence Cost Effective Management Structure: Market based management fees shall only be applied on the first anniversary, subject to generating positive financial performance and achieving a total assets under portfolio of USD 500k and above. From the second year, the Partners will also be entitled to a market standard investment incentive scheme, which will be aligned with the actual performance and will ensure complete alignment amongst shareholders. The incentive framework will be implemented by way of yearly issues of performance shares and share option plan. Target USD IRR of [12-15%] Dividend Policy: No dividend policy until FY 2020 in order to support re-investment of initial capital gains. This remains subject to the future performance and will be assessed on a yearly basis.

1

2

3

4

5

16

6

4.2 The Current Opportunity

The Series A Capital Round seeks to open the capital structure of Nelion Partners to selected private investors aiming at developing a long-term exposure to the African investable landscape. Following Terms shall apply to the Extended Series A Capital Round: § Offer Open to a Restricted Number of Investors, invited by the Founding Partners (or “Sponsors”) § Investment Amount : USD 10,000.00 to USD 30,000.00 (for the acquisition of 10,000 to 30,000 Class A shares in

Nelion Partners Limited, the Seychelles holding Company at a price of USD 1.00 per share)

§ Target New Capital: Minimum of USD 250,000

§ Offer Period: Up to 30 June 2015

§ Subscription Method: Transfer of the Subscription Amount as per the final executed subscription form

§ Investment Certificates: Nelion Partners’ investors in the Series A Capital Round will be issued the relevant share certificates, following allocation by the board of Directors.

§ Subscription Fees: a USD 100 fee will be deducted from the respective subscription in order to provide for the underlying administration expenses.

§ Liquidity Framework: an investment into Nelion Partners underpins a long-term holding period with projected liquidity provisions triggered from Year 8 to 10. Envisaged exit avenues include (i) innovative tag along provisions to trigger partial liquidity framework during future capital raising initiatives, (ii) trade sale of portfolio assets and (iii) listing on the Nairobi Securities Exchange to take advantage of the prevailing framework on the Growth Enterprises Market Segment. 17

5. FAQs

18

5. FAQs

19

v Why should I invest in Nelion? Nelion Partners offers a unique Asset Management solution, unlocking high return opportunities into a diversified investments portfolio, taking advantage of an exceptional macro economic dynamism. Plus, Nelion Partners will provide its investors with regular meetings / gatherings to keep them updated with the performance and the prospects on their investments, and also offer tailored networking opportunities for the members. The shares on offer during the extended Series A Capital round are valued at par, hence giving all initial investors the opportunity to acquire shares at the same price paid by the founding Partners.

v Why should I trust the founding Partners? Besides being Africa based business executives with sound understanding of capital deployment strategies, each founding Partner is leveraging his own personal network of family and friends to support the Series A Capital raising, hence making a strong commitment on their ability to deliver the Nelion Partners vision. Furthermore, the international experience gained by the partners will be reflected in the due diligence procedures as we appreciate the comfort our investors require

v What are the tax implications out of an investment into Nelion Partners? Nelion Partners is structured as an International Business Company (IBC) and therefore is totally tax exempt in Seychelles. However, future dividends distributed to shareholders of Nelion Partners will be subject to the applicable Income / Personal tax provisions in their respective jurisdictions. v How and when do I get my investment back? An investment into Nelion Partners needs to be informed by a long-term holding strategy with early opportunity to trigger private sales and / or take advantage of tag and drag provisions to trigger partial exit opportunities alongside the future capital raising efforts. On a long term outlook, the sub-Saharan capital market is likely to offer liquidity avenues via listing on secondary market segments.

5. FAQs (Cont’d)

20

v In which currency will my returns be denominated? The share capital and future returns out of Nelion Partners are USD denominated. v What is the effective currency risk? Nelion Partners will take local currency risks via its Equity and Debt investments in sub-Saharan Africa. The mismatch between the funding currency and the underlying assets denominations trigger an inevitable currency exposure. However, the founding Partners have an investment strategy focusing on currencies with a long-term average yearly depreciation to the USD below 4%. Additionally, the future regional diversification will provide an indirect hedging solution by limiting single currency fluctuations. v What if I want to invest more than the proposed amount? The current extended Series A Capital round intends to achieve a diversity of stakeholders, hence the limitation in maximum investment per shareholder. However, Nelion Partners has a fast growth agenda informed by regional and product diversification. This expansion will be primarily funded by cash calls to shareholders, hence offering regular opportunities to increase financial exposure to the company. v What is the difference between Class A and Class B shares? Class B shareholders have been selected in order to take advantage of their capability to provide a hands-on support to the long-term ambitions of Nelion Partners. They will be responsible to enter into, execute, maintain and/or terminate investment agreements, contracts, undertakings and any and all other instruments, and documents in the name Nelion Partners Ltd. They will also be entitled to a long-term incentive plan, as highlighted in the Memorandum & Articles of Association, in order to create a sustainable alignment between all stakeholders. Class A shareholders will have limited governance rights, as highlighted in the Memorandum & Articles of Association.

5. FAQs (Cont’d)

21

v Why the need for an extended Series A round? The recent currency and capital market evolutions across the continent have unlocked tremendous investment opportunities which need to be funded promptly. The founding partners have identified a number of Equities and Real Estate investment avenues and the most pragmatic and immediate way of raising more capital is to extend the duration of the initial Series A round, and therefore to offer new investors the same terms and conditions as previously applied. v What has Nelion invested in so far? Nelion has managed to complete a number of pre-IPO and mid-cap Equity trades in Kenya and Nigeria. The portfolio stocks comprise of: (i) UAP Group: an East African General and Life Insurance Company present in Kenya, Uganda, Rwanda

and South Sudan (ii) NIC Bank: a Tier 2 Banking institution with a regional presence in Kenya, Tanzania and Uganda (iii) National Bank of Kenya: a leading retail and Corporate bank in Kenya which successfully undertook a

turnaround strategy in 2012. (iv) Kenya Re: a leading reinsurance company with a pan-African presence; (v) Centum: a diversified investment holding company with significant interests in East African Real Estate and

Financial Institution (vi) Seplat: an independent indigenous Nigerian upstream exploration and production company with a focus

on Nigeria (vii) Diamond Bank of Nigeria: a leading retail financial institution in Nigeria

Appendix

22

A1 - Partnership with SBG Securities and Standard Bank Group A2 - The Greater Opportunity: Africa A3 - The Proposed Partners Incentive Scheme

A1, Why SBG Securities as trading Partner?

23

v We obtained the best rates available: While the average fee in the market is around 1.5%, Nelion partners negotiated 0.95% inclusive of all taxes in order to maximize the performance of the fund and future returns.

v Their Global footprint: Standard Bank Group is a leading African bank with global emerging markets reach, with Africa Equity platforms in place in Lagos (Nigeria, Ghana & Côte d'Ivoire), Nairobi (Kenya, Uganda, Rwanda & Tanzania) and Johannesburg (South Africa); as well as Global Equity platforms in place in New York and London. v Their research department: SBGS has a fully fledged and independent equity, macroeconomic and fixed income research department which produce regular market, sector and listed company reports across Africa. v 2013 Stock Broker of the Year – Winner, SBG Securities

v Transparency of transactions as some of Nelion Partners are involved in the Kenyan Investment Banking industry

A2. Africa by Numbers

24

Current Figures

v Population: 1.1 Bn

v GDP: $2,392 Bn

v GDP per Capita: $2,106

v Population density: 33/km²

v Real GDP Growth (2013): 4.7%

v Net FDI (2013): $43 Bn

v Population (2050): > 1.8 Bn

v GDP (2020): $3,392Bn

v GDP/Capita (2020): $2,552

v Population density(2050): 60/km²

v Real GDP Growth (2014-20): 4.9%

v Net FDI (2017): >$80 Bn

Future Projections

Source| IMF World Economic Outlook, United Nations; BMI, World Bank

A3. Incentive Scheme

25

Notwithstanding any other rights accruing to the holders of Class B Shares, Class B Shareholders will be entitled to a performance incentive scheme which will comprise of the following: A Share Ownership Plan: on the 1st anniversary of the Series A Capital Round Closing Date, each Class B Shareholder will be entitled, for a period of 3 years, to an option to acquire a certain number of Class A shares, upon final recommendation by the Board. The applicable price per share shall be validated by the Board and will be fixed until termination of the option. The beneficiary of such option will exercise his right to acquire all or some of the optional shares at any time during the applicability period of such option. All payments for the underlying consideration will have to be made prior to the issue of the relevant certificates. Performance Shares: Each Class B Shareholder will be entitled, upon recommendation by the Board to performance shares issued by the Company subject to the yearly financial performance and appreciation of the NAV per share. The “hurdle rate” has been defined at 8% (in USD terms) and the proposed incentive scheme will assess, on a yearly basis, the organic growth (exclude recapitalization initiatives) of the NAV and offer Class B shareholders the following carried interest into future capital appreciation:

Contacts

26

Contacts

Samy Ghannam Email: [email protected] Tel: +254-712-211-017 / +254-713-847-328 Skype: samghannam

27

Clément Martineau Email: [email protected] Tel: +254-775-741-151 / +254-717-118-704 Skype: clems1100

Stanley Gabriel Email: [email protected] Tel: +234-810-599-2030 / +27-799-201-202 Skype: stanley.gabriel

Guy Brennan Email: [email protected] Tel: +254-704-101-100 Skype: brennanguy