Outlook for the Mexican Economy Octubre, 2011. Index I.External Conditions II.Macroeconomic...

33

Outlook for the Mexican Economy Octubre, 2011

-

Upload

kenneth-alexander -

Category

Documents

-

view

213 -

download

0

Transcript of Outlook for the Mexican Economy Octubre, 2011. Index I.External Conditions II.Macroeconomic...

Outlook for the Mexican Economy

Octubre, 2011

Index

I. External Conditions

II. Macroeconomic Environment

III. Mexican Competitiveness

I. External Conditions

80

90

100

110

120

130

140

150

160

170

World Advanced Emerging

Industrial Production

Index Jan-2005 = 100*

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

Euro zone Japan U.S.

Real Gross Domestic Product Forecasts for 2011 and 2012 (a)

Percent

*Seasonally adjusted.

Source: CPB Netherlands.

(a) Solid lines refer to the forecast of 2011 and dotted lines correspond to 2012.

Source: Blue Chip.3

Forecast

Forecast

I. External Conditions20

06

2007

2008

2009

2010

2011

2012

2013

2014

2015

-20

-15

-10

-5

0

5

10Brazil ChileU.S. SpainGreece MexicoPortugal Czech Rep.Poland

General Government Balance

Percent of GDP

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

0

20

40

60

80

100

120

140

160

180

200

220

240Brazil ChileU.S. SpainGreece MexicoPortugal Czech Rep.Poland

Gross Public Debt

Percent of GDP

Source: Fiscal Monitor (IMF) and Mexico’s Ministry of Finance (SHCP).

Source: Fiscal Monitor (IMF) and Mexico’s Ministry of Finance (SHCP).

4

Index

I. External Conditions

II. Macroeconomic Environment

III. Mexican Competitiveness

103

108

113

118

123

128

133Total Industrial production Services

Economic Activity Indicators (a)

Index 2003 = 100*

70

80

90

100

110

120

130

140

150

160

170 Total U.S. Others

Manufacturing Exports

by Destination

Index 2007 = 100*

*Seasonally adjusted.

(a) Industrial production data up to August, 2011. Total and Services data up to July, 2011.

Source: INEGI.

*Seasonally adjusted.

Source: Banco de México.

II. Macroeconomic Environment in Mexico

6

85

87

89

91

93

95

97

99

101

103

105Wholesale

Commercial Establishments’ Sales

Index 2008 = 100*

90

100

110

120

130

140

150Total Construction Machinery and equipment

Gross Fixed Investment and Components

Index 2005 = 100*

*Seasonally adjusted.

Source: INEGI.

*Seasonally adjusted.

Source: INEGI.

7

II. Macroeconomic Environment in Mexico

13.4

13.6

13.8

14.0

14.2

14.4

14.6

14.8

15.0

15.2

15.4

15.6 OriginalSeasonally adjusted

3.0

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5 National Urban

I 200

6

IV 2

006

III 20

07

II 200

8

I 200

9

IV 2

009

III 20

10

II 201

1-2

0

2

4

6

8

10

IMSS-insured Workers (a)

Million workers

Unemployment Rate Percent*

Nominal Average Income per Person Employed (a)

Annual change in percent

(a) Permanent and temporary workers in urban areas. Source: IMSS and seasonally adjusted by Banco de México.

*Seasonally adjusted.

Source: INEGI.

(a) Data for 2011 are preliminary and are based on population projections from INEGI.

Source: Calculated by Banco de México with information from ENOE, INEGI.

8

II. Macroeconomic Environment in Mexico

3.0

3.3

3.6

3.9

4.2

4.5

End 2011: Headline End 2011: Core

End 2012: Headline End 2012: Core

Headline and Core Inflation Expectations

Annual Percent

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

End 2011 End 2012End 2013 Next 4 yearsNext 5-8 years Inflation targetVariability interval

Headline Inflation Expectations for Different Time Horizons

Annual Percent

Source: Banco de México’s survey. Source: Banco de México’s survey.

9

II. Macroeconomic Environment in Mexico

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

19

10

11

12

13

14

15

16

Nominal Exchange Rate

Pesos per dollar

200,000

250,000

300,000

350,000

400,000

450,000

500,000

550,000

600,000

650,000

700,000

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000Bonds CETES

Government Securities Holdings of Foreign Investors

Billions of pesos

Source: Banco de México. Source: Banco de México.

10

II. Macroeconomic Environment in Mexico

Index

I. External Conditions

II. Macroeconomic Environment

III. Mexican Competitiveness

Mexico has a number of comparative advantages that position it as an attractive investment destination:

Excellent location

Market size

Openness

Strong institutions

Competitive infrastructure

Increasingly qualified labor force

Stable macroeconomic environment

III. Competitiveness in Mexico

12

Philip

pine

s

Mex

ico

Mal

aysia

Brazil

Hunga

ry

Turke

y

Argen

tina

Singa

pore

Portu

gal

Taiwan

Hong

Kong

Chile

Thaila

nd

Korea

Polan

d

Indo

nesia

-4

-2

0

2

4

6

8

10

12

Global Competitiveness IndexChange in Ranking Position from 2010 to 2011*

* A positive change represents a better position in the ranking.

Source: World Economic Forum, Global Competitiveness Report 2010-2011, 2011-2012.

III. Competitiveness in Mexico

13

Singa

pore

Hong

Kong

Taiwan

Mal

aysia

Korea

Chile

Thaila

nd

Polan

d

Portu

gal

Indo

nesia

Hunga

ry

Brazil

Mex

ico

Turke

y

Philip

pine

s

Argen

tina

0

10

20

30

40

50

60

70

80

90

100

2010

2011

Global Competitiveness IndexRanking (a)

(a) Rank among 142 countries for 2011 and 139 countries for 2010. A lower value in the rank implies a better position in the ranking. Source: World Economic Forum, Global Competitiveness Report 2010-2011.

III. Competitiveness in Mexico

14

Competitiveness Indicators: Market SizeScore according to World Economic Forum

Source: World Economic Forum, Global Competitiveness Report 2011-2012. Note: Countries are ranked by the WEF according to their score among the 139 evaluated countries. Macroeconomic environment and market size are the two competitiveness pillars (out of 12) in which Mexico performed best. Countries selected in these graphs are those of Mexico's basket of competitors which are Hungary, Thailand, Philippines, South Korea, Turkey, Poland, Portugal, Malaysia, Hong Kong, Taiwan, Indonesia and Singapore. These are the countries with the highest Spearman correlation coefficient of revealed comparative advantage, after dropping China, as calculated in Chiquiar, Fragoso and Ramos-Francia (2007). For comparisson with Latin American countries, Brazil, Chile and Colombia were also included.

III. Competitiveness in Mexico

15

Hunga

ryChi

le

Portu

gal

Singa

pore

Philip

pine

s

Mal

aysia

Hong

Kong

Argen

tina

Thaila

nd

Polan

d

Turke

y

Taiwan

Indo

nesia

Mex

ico

South

Kor

ea

Brasil

China

0

1

2

3

4

5

6

7

8

Free Trade Agreements: *

Mexico is a gateway to more than a billion consumers and 60 percent of world GDP.

Mexico has 11 free trade agreements with 43 countries.

It has 6 Economic Complementation Agreements (ACEs, for its acronym in Spanish), it has signed Promotion and Reciprocal Protection of Investments Agreements (to provide legal protection to productive investments) with 25 countries.

It has Agreements to Avoid Double Taxation with more than 31 countries.

III. Competitiveness in Mexico

16Source: ProMéxico.

III. Competitiveness in Mexico

(a) Since November 19, 2006 only Mexico and Colombia participate in the G3 Free Trade Agreement.

(b) Agreement between Japan and the United Mexican States for the strengthening of the economic partnership. Source: ProMéxico.

Free Trade Agreements

ALADIMercosur(Marco

Agreement)

ALADICuba

ALADIEcuador

ALADIPanama

ALADIParaguay

ALADIPeru

ALADIBrasil

FTA EFTAIceland

LiechtensteinNorway

Switzerland

FTAChile

FTANicaragua

ALADIUruguay

ALADIArgentina

FTAIsrael

FTAEU

AAE

Japan (b)FTA

Uruguay

ALADIMercosur

(Automotive)

FTA NTGuatemalaHonduras

El Salvador

20041999 2000 2001 2002 2005

NAFTAEUA

Canada

WTO

FTACosta Rica

FTA G3

Colombia (a)

199819951994

OECDMexico's entry into

GATT

1986

ALADIChile

1992

APEC

1993

17

Clusters and Technology Centers

The large size of the country contributes to various cities functioning as service providers, which benefits Mexico in comparison with other countries that depend on labor force concentrated in one city.

III. Competitiveness in Mexico

18

Puebla:Automobile industry

Monterrey-Saltillo:Automobile industry

Queretaro:Aeronautics

Baja California:Tourism

Jalisco: Information Technology

Quintana Roo:Tourism

Mexico: AutomobilesAnd others

Chile

Mex

ico

Hunga

ry

Polan

d

Mal

aysia

Portu

gal

Taiwan

Singa

pore

Hong

Kong

Korea

China

Argen

tina

Philip

pine

s

Thaila

nd

Brazil

Turke

y

Indo

nesia

-8

-6

-4

-2

0

2

4

6

8

10

12

Ease of Doing BusinessChange in Ranking Position from 2010 to 2011

Source: Doing Business 2011 IFC.

III. Competitiveness in Mexico

19

2004

2005

2006

2007

2008

2009

2010

2011

5

6

7

8

9

10

9 9 9

8 8

9

8

6

Mexico

Nicaragua

Panama

Peru

Paraguay

Chile

Dominican Republic

El Salvador

Colombia

Uruguay

Costa Rica

Guatemala

Ecuador

Honduras

Argentina

Bolivia

Brazil

Venezuela

6

6

6

6

7

8

8

8

9

11

12

12

13

13

14

15

15

17

Hong Kong

Singapore

Hungary

Mexico

Portugal

Turkey

Taiwan

Poland

Thailand

South Korea

Malaysia

Indonesia

Philippines

3

3

4

6

6

6

6

6

7

8

9

9

15

Mexico

Number of procedures

Latin American Countries,

2011

Number of procedures

Main Competitors of Mexico in International Markets,

2011

Number of procedures

III. Competitiveness in Mexico: Procedures Required to Register a Firm

Note: A procedure is defined as any interaction of the company founders with external parties (for example, government agencies, lawyers, auditors or notaries).Countries selected are those of Mexico's basket of competitors which are Hungary, Thailand, Philippines, South Korea, Turkey, Poland, Portugal, Malaysia, Hong Kong, Taiwan, Indonesia and Singapore. These are the countries with the highest Spearman correlation coefficient of revealed comparative advantage, after dropping China, as calculated in Chiquiar, Fragoso and Ramos-Francia (2007). The observations for 2011 come from the Global Competitiveness Report 2010-2011, and they correspond to June 2010. Source: World Bank. Doing Business 2011. 20

2004

2005

2006

2007

2008

2009

2010

2011

0

10

20

30

40

50

60

70

58 58 58

27 27 28

13

9

Mexico

Panama

Colombia

Honduras

El Salvador

Dominican Republic

Chile

Argentina

Peru

Paraguay

Guatemala

Nicaragua

Bolivia

Ecuador

Costa Rica

Uruguay

Brazil

Venezuela

9

9

14

14

17

19

22

26

27

35

37

39

50

56

60

65

120

141

Singapore

Hungary

Portugal

Turkey

Hong Kong

Mexico

South Korea

Taiwan

Malaysia

Poland

Thailand

Philippines

Indonesia

3

4

6

6

6

9

14

15

17

32

32

38

47

Mexico

Total number of days

Latin American Countries, 2011

Total number of days

Main Competitors of Mexico in International Markets,

2011

Total number of days

III. Competitiveness in Mexico: Days Required to Register a Firm

Note: The measure captures the median duration that incorporation lawyers indicate is necessary to complete a procedure with minimum follow-up with government agencies and no extra payments.Countries selected are those of Mexico's basket of competitors which are Hungary, Thailand, Philippines, South Korea, Turkey, Poland, Portugal, Malaysia, Hong Kong, Taiwan, Indonesia and Singapore. These are the countries with the highest Spearman correlation coefficient of revealed comparative advantage, after dropping China, as calculated in Chiquiar, Fragoso and Ramos-Francia (2007). The observations for 2011 come from the Global Competitiveness Report 2010-2011, and they correspond to June 2010. Source: World Bank. Doing Business 2011. 21

Competitive Infrastructure:

63 International Airports.

16 deep-sea ports.

15,000 miles of railways and 84,000 miles of paved roads, with more than 30,000 miles of federal highways.

Mexico increased its spending in infrastructure from an average of 3% (2001 – 2006) to 5% of its GDP with the National Infrastructure Program 2007-2012.

III. Competitiveness in Mexico

Source: ProMéxico and National Infrastructure Program 2007-2012.

22

0

1

2

3

4

5

6

7

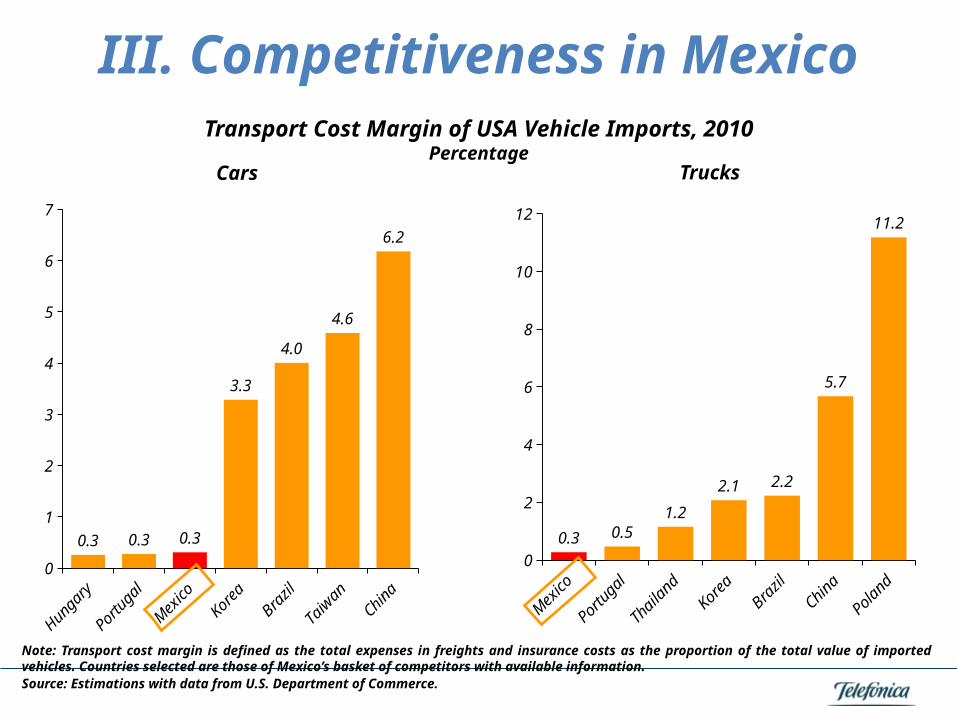

0.3 0.3 0.3

3.3

4.0

4.6

6.2

Mex

ico

Portu

gal

Thaila

nd

Korea

Brazil

China

Polan

d0

2

4

6

8

10

12

0.3 0.51.2

2.1 2.2

5.7

11.2

Cars Trucks

Transport Cost Margin of USA Vehicle Imports, 2010Percentage

Note: Transport cost margin is defined as the total expenses in freights and insurance costs as the proportion of the total value of imported vehicles. Countries selected are those of Mexico’s basket of competitors with available information. Source: Estimations with data from U.S. Department of Commerce.

23

III. Competitiveness in Mexico

U.S.

Mex

ico UK

Turke

y

Portu

gal

Polan

d

Czech

Rep

.

Korea

Hunga

ry0

100

200

300

400

500

600

700

2005

3Q-2009

Natural Gas Prices for IndustryU.S. Dollars (a)

(a) Average price per 107 kcal on a gross calorific value basis.

Source: International Energy Agency.

III. Competitiveness in Mexico

24

Mexico’s labor force has the following advantages:

Population of 112 Million people, with an average age 29 years old.

Demographics Bonus:

• By 2030 Mexico will reach its lowest Dependency ratio (Children and seniors / EAP).

More than 90,000 engineers graduate every year.

• 3 times higher than the US in per capita terms.

9th largest talent pool of Information Technology (IT) Professionals in the World.

III. Competitiveness in Mexico

Source: ProMéxico.

25

Phillip

ines

Mex

ico

Polan

d

Taiwan

Brazil

Hunga

ry

Estoni

a

Argen

tina

Czech

Rep

.

Eslova

quia

Portu

gal

Korea

New Z

eala

nd

Singa

pore

Israe

l

Canad

aU.S

.0

5

10

15

20

25

30

35

40

2000

2009

Hourly Compensation Costs in ManufacturingU.S. Dollars

Source: BLS.

III. Competitiveness in Mexico

26

III. Competitiveness in Mexico

U.S.

Mex

ico

Brazil

Jam

aica

Belize

Colom

bia

Venez

uela

South

Afri

ca

El Sal

vado

r0

10

20

30

40

50

60

70

Homicide Rate 2010Per 100,000 Population

Sources: United Nations Office on Drugs and Crime; FBI, US; Ministry of Security, Mexico; and Secretaria Nal de Seguranca Publica, Brazil.

27

Source: World Economic Forum, Global Competitiveness Report 2011-2012. Note: Countries are ranked by the WEF according to their score among the 139 evaluated countries. Macroeconomic environment and market size are the two competitiveness pillars (out of 12) in which Mexico performed best. Countries selected in these graphs are those of Mexico's basket of competitors which are Hungary, Thailand, Philippines, South Korea, Turkey, Poland, Portugal, Malaysia, Hong Kong, Taiwan, Indonesia and Singapore. These are the countries with the highest Spearman correlation coefficient of revealed comparative advantage, after dropping China, as calculated in Chiquiar, Fragoso and Ramos-Francia (2007). For comparisson with Latin American countries, Brazil, Chile and Colombia were also included.

Competitiveness Indicators: Macroeconomic Environment Score according to World Economic Forum

III. Competitiveness in Mexico

28

Brasil

Portu

gal

Polan

d

Turke

y

Hunga

ry

Argen

tina

Philip

pine

s

Mex

ico

Mal

aysia

Thaila

nd

Indo

nesia

Taiwan

Chile

Singa

pore

China

Hong

Kong

South

Kor

ea0

1

2

3

4

5

6

7

III. Competitiveness in Mexico

Jun-

07

Nov-0

7

Apr-0

8

Sep-0

8

Feb-0

9

Jul-0

9

Dec-0

9

May

-10

Oct-10

Mar

-11

Aug-1

170

80

90

100

110

120

130Argentina Brazil Chile Mexico Peru

Effective Real Exchange Rate (a)

Index June-2007 =100

(a) An increase means a depreciation. For comparison only Latin American countries were selected.

Source: Bank of International Settlements.

Recent Exchange-rate-induced Changes in Competitiveness

29

III. Competitiveness in Mexico

8.4

9.3

9.9

10.4

10.7

11.2

11.5

11.6

11.0

10.6

10.2

10.7

10.8

10.3

11.3

12.0

6.2 6.4 7.

2 7.8 8.

0

8.2 9.0 10

.8

12.1 13

.4 14.5 15

.5 16.4

16.1

19.0

19.1

15.0

13.9

13.9

14.0

13.7

13.7

12.7

12.4

11.7

11.4

10.4

10.1

9.4

8.7 9.2

9.1

ChinaMexican competi-tors without China

Mexico

Mexican, Chinese and other Mexico’s Competitors Exports Share in Total US Imports

Percent

Source: Banco de MéxicoNote: Mexican competitors are Hungary, Thailand, Philippines, South Korea, Turkey, Poland, Portugal, Malaysia, Hong Kong, Taiwan, Indonesia and Singapore. These are the countries with the highest Spearman correlation coefficient of revealed comparative advantage, after dropping China, as calculated in Chiquiar, Fragoso and Ramos-Francia

(2007). 30

III. Competitiveness in Mexico

8.1

9.1

9.7

10.2

10.6

11.0

11.4

11.4

10.7

10.3

9.8

10.3

10.5

10.2

11.3

12.1

6.5

6.7 7.5 8.

1 8.4 8.

8 9.6 11

.5

13.2 14

.7 16.2 17

.6 18.7 19

.1

21.6

22.0

15.8

14.6

14.6

14.5

14.3

14.7

13.6

13.3

12.7

12.5

11.6

11.4

10.7

10.3

10.4

10.

4

Mexico

Mexican competitors wi-thout China

China

Mexican, Chinese and other Mexico’s Competitors Exports Share in Non-oil USA Imports

Percent

Source: Banco de México.

Note: Mexican competitors are Hungary, Thailand, Philippines, South Korea, Turkey, Poland, Portugal, Malaysia, Hong Kong, Taiwan, Indonesia and Singapore. These are the countries with the highest Spearman correlation coefficient of revealed comparative advantage, after dropping China, as calculated in Chiquiar, Fragoso and Ramos-Francia

(2007).

31

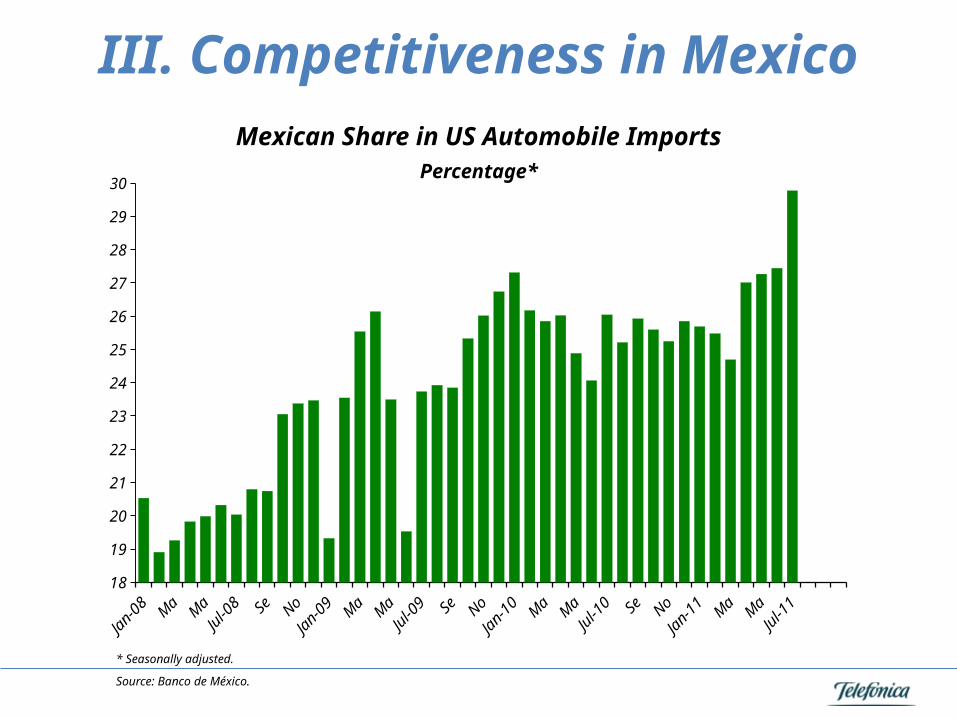

18

19

20

21

22

23

24

25

26

27

28

29

30

Mexican Share in US Automobile ImportsPercentage*

* Seasonally adjusted.

Source: Banco de México.

III. Competitiveness in Mexico

32

III. Competitiveness in Mexico

JPM

X/12/11

July. INEGI gross-fixed inv 9.3% driven by purchases of machinery and equipment. JPM “Even though GFI figure came in lower than expected it continues to reflect investments announced months ago to reallocate from other countries to Mexico. The weaker peso, higher global transport costs, and lower wage differential between Mexico and Asian countries has increased Mexico’s competitiveness. This has created incentives for investors to reallocate production to Mexico or enhance existing operations. Investment continues to expand at a healthy pace, after lagging the externally-driven recovery over the last year. A more promising investment outlook is likely to support better employment conditions in addition to a significant credit expansion.