Outline - World Bankpubdocs.worldbank.org/en/787691505799074026/092017-CMO...Broad commodity price...

42

Transcript of Outline - World Bankpubdocs.worldbank.org/en/787691505799074026/092017-CMO...Broad commodity price...

Outline

Broad commodity price trends

30

60

90

120

150

180

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Index, nominal terms, 2010 = 100

Source: World BankNote: Last observation is August 2017.

Energy

AgricultureMetals

Prices are still higher than the 1985-2004 average

0

40

80

120

160

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015Source: World Bank.

Agriculture

Metals

Energy

Index, constant US$ (2010 = 100)

Changes (%) in real prices to 2016 from:1986-2004 1998

Agriculture: +38 +35Energy: +65 +147Metals: +38 +63

0 3 6 9 12 15 18

Turkey

India

Brazil

China

EU-12

Canada

US

SSA

DEVELOPING

HIGH INCOME

WORLD

Manufacture

Agriculture

Cost of energy

Source: Author’s calculations based on the GTAP database (2007 release) and Baffes (2007), Resources Policy, vol.32, pp. 126-134.Notes: Elasticity estimates are based on OLS regression of nominal prices on oil price, deflator, time trend, annual data, 1960-2005.

Agriculture is an energy intensive industry

0.160.18 0.19

0.17

0.04

0.11

0.33

0.00

0.10

0.20

0.30

0.40

Non-energy Grains Oils andmeals

Other food Rawmaterials

Metals Fertilizers

Elasticity estimates

Energy intensity Transmission elasticities

Outline

20

40

60

80

100

120

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17

“Old” versus “new” oil price equilibrium

Source: World Bank.Note: Weekly data. Volatility is defined as standard deviation of logarithmic changes times 100. Last observation is July 7, 2017.

US$/bbl

January 2011 - August 2014Average price: $104/bbl

Volatility: 2.95

December 2014 - August 2017Average price: $48/bbl

Volatility: 5.05

-70 -60 -50 -40 -30 -20 -10 0 10

Crude oilWheatTeaGoldCocoaSoybeansZincPlatinumLeadTinRiceMaizeCoffee (arabica)AluminumPalmoilCopperNickelSilverCoalCottonNatural rubber

All commodity prices declined during 2011Q1-2014Q2, but oil

Source: World Bank

Price change from 2011Q1 to 2014Q2 (percent)

Downward revisions to EMDE growth

6.16.0

5.7

5.55.45.5

5.3

4.85.0

5.4

5.0

4.3

3

4

5

6

7

2012 2013 2014 2015

Forecast in January of previous year Forecast in January of current year Actual growth

Percent

Source: World Bank, Global Economic ProspectsNotes: EMDE denotes Emerging Markets and Developing Economies.

-

2

4

6

8

10

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US shale Canadian oil sands Biofurels

Unconventional oil productionmb/d

Source: International Energy Agency and World Bank

7

8

9

10

11

12

13

J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D

2010 2011 2012 2013 2014 2015

The U.S. shale oil expansion sursprized marketsmb/d

2011

2012

2013

2014

2015

Source: International Energy Agency and World BankNote: U.S. oil output includes biofuels. Solid lines denote annual oil production and diamonds denote IEA projections on the specific month.

Solid lines: Actual production for the yearDiamonds: IEA projection for the year on the specific month

-3.0

-1.5

0.0

1.5

3.0

4.5

2010Q1 2010Q3 2011Q1 2011Q3 2012Q1 2012Q3 2013Q1 2013Q3 2014Q1 2014Q3 2015Q1 2015Q3 2016Q1 2016Q3 2017Q1

Iran Libya Syria Yemen United States Net Change

mb/d, cumulative changes since 2010Q4

Surplus conditions became apparent in 2014Q2

Source: International Energy Agency and World BankNote: Last observation 2017Q1.

Source: IEA

Trigger I: Geopolitical concerns dissipate

3.09

3.60 3.26 3.32 3.42

3.17 3.15 3.11 3.36 3.32 3.41

3.70

0.50

0.36

0.22 0.220.22

0.24 0.42 0.53

0.78 0.87 0.690.44

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

Iraq's oil production during 2014 Libya's oil production during 2015

70

75

80

85

90

95

100

20

40

60

80

100

120

Jan-14 May-14 Sep-14 Jan-15 May-15 Sep-15 Jan-16 May-16 Sep-16 Jan-17 May-17

Trigger II: The U.S. dollar begins appreciating

Source: World Bank and FRED.Note: Oil refers to WTI and US$ is the trade weighted U.S. dollar index against major currencies, not seasonally adjusted (DTWEXM), both daily frequency.

Oil price [left] U.S. $ [right]

US$/bbl Index, 1973 = 100

Outline

5

6

7

8

9

Jul-14 Sep-14 Nov-14 Jan-15 Mar-15 May-15 Jul-15 Sep-15 Nov-15 Jan-16 Mar-16 May-16 Jul-16 Sep-16 Nov-16

mb/dMb/d

Source: International Energy Agency

Iran, Iraq, and Libya added 2.6 mb/d during Jul ’14-Dec ’16

Oil prices in a longer term perspective

Source: World BankNote: World Bank crude oil average. Last observation is August 2017.

0

30

60

90

120

150

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

US$/bbl, deflated by U.S. CPI (2014 terms)

1965-2017 average: $48.32/bbl

Prior to 1985/86: (i) Alaska, (ii) North Sea, and (iii) Gulf of Mexico (brought 5 mb/d in the 8 years prior to the collapse, 9% of world total). The real oil price during 1978-86 averaged $82/bbl.

Prior to 2014/15: (i) Biofuels, (ii) Canadian oil sands, and (iii) U.S. shale oil (brought 7 mb/d in the decade prior to the collapse, 8% of world total). The real oil price during 2004-14 averaged $92/bbl.

OPEC: Changed its policy in both 1986 and 2014.

36-yr average (excluding the 2 spike periods): $29/bbl.

-1,000

-500

0

500

1,000

1,500

2,000

Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16 Jul-16 Jan-17 Jul-17 Jan-18 Jul-18

U.S. shale oil: Slow to get out but quick to come backy-o-y monthly changes, thousand bbl

IEA Forecast

Source: International Energy Agency.Notes: U.S. crude oil production. Last actual observation is August 2017. September 2017 to December 2018 is forecast.

The plunge begins

0

300

600

900

1,200

1,500

1,800

0

30

60

90

120

150

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Rig countUS$/bbl

It only takes 3 months for active drilling to respond

Source: Baker Hughes, Bloomberg, and World Bank.Note: Weekly data, last observation is September 1, 2017.

Oil price, WTI [LHS]

Rig count [RHS]

0

200

400

600

800

1,000

1,200

1,400

1,600

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

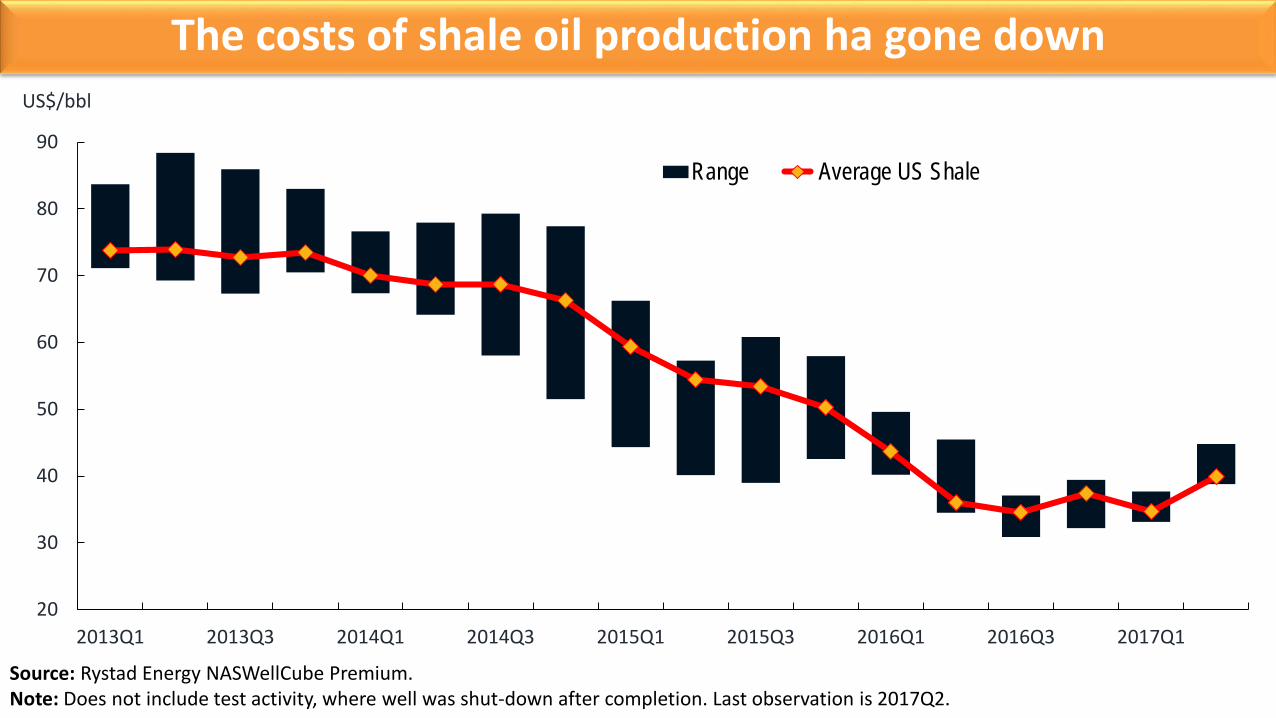

b/d per well

Bakken Eagle Ford Niobrara Utica Permian

Source: Rystad Energy NASWellCube Premium.

There have been large productivity increases in shale oil

20

30

40

50

60

70

80

90

2013Q1 2013Q3 2014Q1 2014Q3 2015Q1 2015Q3 2016Q1 2016Q3 2017Q1

US$/bbl

Range Average US Shale

Source: Rystad Energy NASWellCube Premium. Note: Does not include test activity, where well was shut-down after completion. Last observation is 2017Q2.

The costs of shale oil production ha gone down

55

58

61

64

67

70

J J A S O N D J F M A M J J A S O N D J F M A M J J A S O N D J F M A M

2016-17 2016-17 2016-17

2020

Evolution of Consensus on Brent before/after December 2016

2018 2019US$/bbl

Source: Consensus Economics and World Bank.Note: Median Brent oil price forecasts reported from June 2016 through May 2017 for 2018, 2019, and 2020.

Red diamonds: Price forecast reported prior to the December 2016 announcement of the OPEC/non-OPEC cuts.Blue diamonds: Price forecast reported after the December 2016 announcement of the OPEC/non-OPEC cuts.Horizontal lines: Forecasts averaged over the specific year.

50

60

70

80

90

100

110

Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug Feb Apr Jun Aug Oct Dec Feb Apr Jun Aug

2014-15 2014-15 2014-15

2018

Evolution of Consensus on Brent before/after November 2014

2016 2017US$/bbl

Source: Consensus Economics and World Bank.Note: Median Brent oil price forecasts reported from February 2014 through August 2015 for 2016, 2017, and 2018.

Red diamonds: Price forecast reported prior to the November 2014 OPEC’s disengagement.Blue diamonds: Price forecast reported after the November 2014 OPEC’s disengagement.Horizontal lines: Forecasts averaged over the specific year (illustration purposes only).

U.S. oil announcements drive prices more than other events

Source: Bloomberg, US Energy Information Administration, World Bank, and various media sources.Notes: Price refers to the World Bank average

June 14, 21Inventory buildup

June 8UK

election

June 5Qatar

isolation

June 7Iran

attack

June 7Inventory buildup

May 22Manchester

attack

May 15Cut extension

announcement

May 25OPEC

meeting

June 3London attack

June 1U.S. withdraws

from Paris

May 4Inventory buildup

May 19Expectations of deeper cut

May 31Surging U.S. oil imports

Blue bars denote increases and red bars denote declines in oil price (from the previous trading day). Arrows point to oil price changes in excess of $ 1/bbl.

Outline

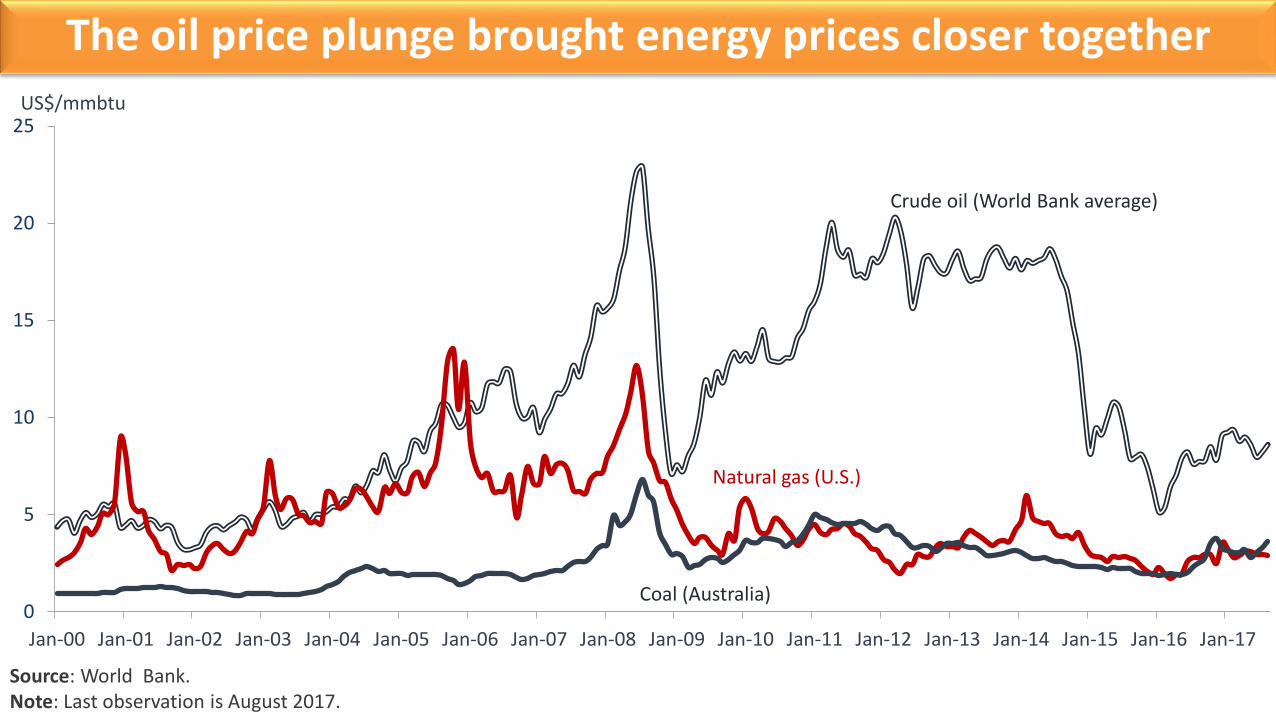

The oil price plunge brought energy prices closer together

0

5

10

15

20

25

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

US$/mmbtu

Source: World Bank.Note: Last observation is August 2017.

Coal (Australia)

Natural gas (U.S.)

Crude oil (World Bank average)

Natural gas prices follow suit

Source: World Bank.Note: Last observation is August 2017.

0

5

10

15

20

Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

US$/mmbtu

Japan (LNG)

Europe

U.S.

Outline

Agricultural prices have weakened as well

60

80

100

120

140

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Beverages Food Raw materials

Index, nominal terms, 2010 = 100

Source: World Bank.Note: Last observation is August 2017.

The S/U ratios have recovered relative to their 2006-07 lows

0.10

0.15

0.20

0.25

0.30

0.35

0.40

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016

Maize Rice Wheat

Source: U.S. Department of Agriculture.Notes: Update based on the U.S. Department of Agriculture August, 2017 data release.

Ratio

Outline

Metals prices have picked up

0

40

80

120

160

200

2,000

4,000

6,000

8,000

10,000

Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17

Copper [LHS] Iron ore [RHS]$/mt $/mt

Source: World BankNote: Last observation is August 2017.

China is still the key driver of metal consumption

Source: World Bank and World Bureau of Metal StatisticsNotes: Last observation is June 2017.

0

1

2

3

4

5

6

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09 Jan-11 Jan-13 Jan-15 Jan-17

Million metric tons

Rest of the world

China

Outline

Where are commodity prices heading?

0

40

80

120

160

1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

Source: World Bank.Note: The period 2017-30 refers to forecasts, as of September 2017.

Agriculture

Metals

Energy

Index, real (2010 = 100)

2015 2016 2017F 2018F 2019F

Crude oil price ($/bbl) 51 43 52 54 57

Gold price ($/toz) 1,161 1,249 1,250 1,229 1,208

Agriculture index (2010 = 100) 89 89 88 89 91

Metals index (2010 = 100) 67 63 77 76 76

Global growth (%) 2.7 2.4 2.7 2.9 2.9

Emerging economy growth (%) 3.6 3.5 4.1 4.5 4.7

Commodity and global economy forecasts (nominal)

Source: World BankNote: 2017 onwards denote forecasts.

0

1

2

3

4

5

6

7

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Consumption Net Exportsmb/d

Iran’s emergence after sanctions: Perhaps a downside risk?

Source: BP Statistical Review, International Energy Agency.Note: Production includes crude oil and liquids.

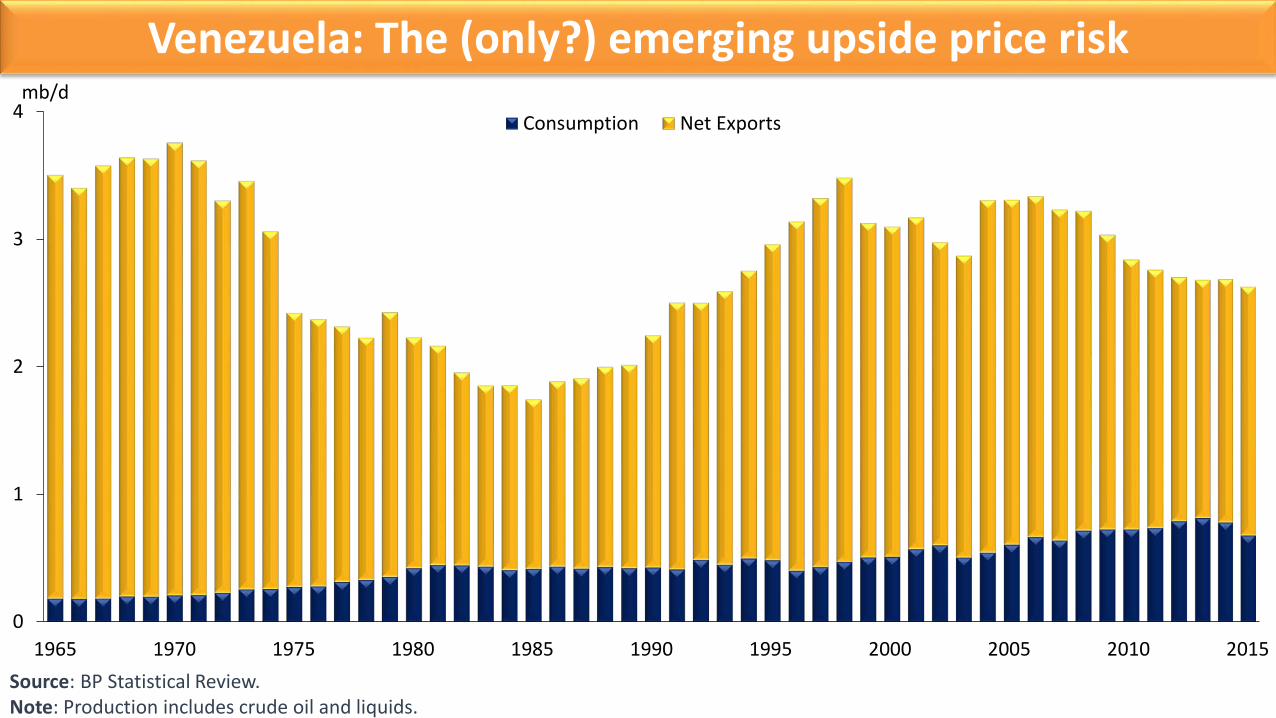

0

1

2

3

4

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Consumption Net Exports

Venezuela: The (only?) emerging upside price risk

Source: BP Statistical Review.Note: Production includes crude oil and liquids.

mb/d

20

30

40

50

60

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

OECD, actual Non-OECD, actual OECD, projected in 2005 Non-OECD, projected in 2005

Oil consumption: History and (2005) prospects

Source: International Energy Agency and World Bank.Note: The projection was taken from the 2005 Outlook.

mb/d

2

4

6

8

10

12

14

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

World OECD Non-OECD

Energy intensity has been declining

Source: BP Statistical Review and World Bank.

bbl/$10,000 of GDP

5

10

15

20

25

30

35

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

World OECD Non-OECD

bbl of oil equivalent/$10,000 of GDP

Oil intensity Energy intensity

2.4

21.4

11.3

22.6

5.7

8.6

24.8

3.7

12.0

18.7

22.2

21.8

50.4

49.4

50.5

12.5

- 15 30 45 60

GDP

Population

Edible oils

Grains

Base metals

Iron ore

Coal

Crude oil

Share of world total (percent)

2014-16

1990-92

China’s and India’s share of global commodity consumption

Source: World Bank, BP Statistical Review of World Energy, World Bureau of Metals Statistics, U.S. Department of Agriculture

1.2

16.5

9.3

9.9

1.8

1.9

5.2

1.9

3.0

17.8

13.5

9.7

3.0

5.4

10.5

4.4

- 15 30 45 60

GDP

Population

Edible oils

Grains

Base metals

Iron ore

Coal

Crude oil

Share of world total (percent)

2014-16

1990-92

China India