OneMain Direct Auto Receivables Trust 2021-1

19

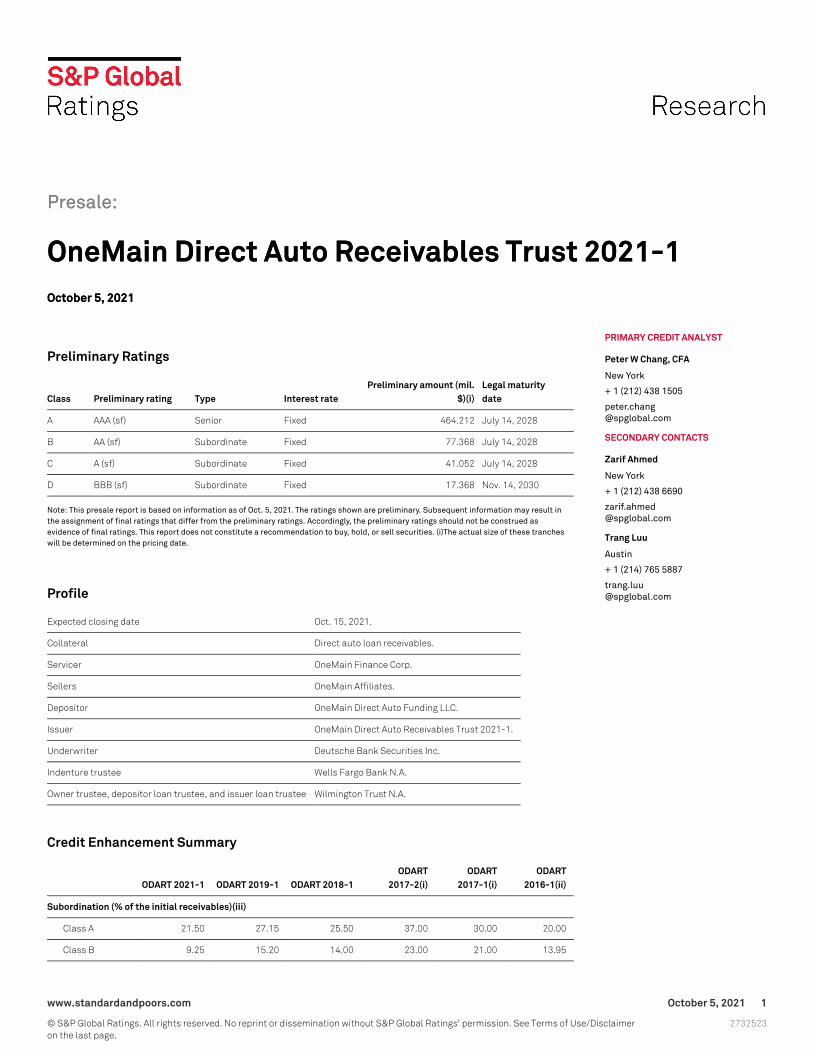

Presale: OneMain Direct Auto Receivables Trust 2021-1 October 5, 2021 Preliminary Ratings Class Preliminary rating Type Interest rate Preliminary amount (mil. $)(i) Legal maturity date A AAA (sf) Senior Fixed 464.212 July 14, 2028 B AA (sf) Subordinate Fixed 77.368 July 14, 2028 C A (sf) Subordinate Fixed 41.052 July 14, 2028 D BBB (sf) Subordinate Fixed 17.368 Nov. 14, 2030 Note: This presale report is based on information as of Oct. 5, 2021. The ratings shown are preliminary. Subsequent information may result in the assignment of final ratings that differ from the preliminary ratings. Accordingly, the preliminary ratings should not be construed as evidence of final ratings. This report does not constitute a recommendation to buy, hold, or sell securities. (i)The actual size of these tranches will be determined on the pricing date. Profile Expected closing date Oct. 15, 2021. Collateral Direct auto loan receivables. Servicer OneMain Finance Corp. Sellers OneMain Affiliates. Depositor OneMain Direct Auto Funding LLC. Issuer OneMain Direct Auto Receivables Trust 2021-1. Underwriter Deutsche Bank Securities Inc. Indenture trustee Wells Fargo Bank N.A. Owner trustee, depositor loan trustee, and issuer loan trustee Wilmington Trust N.A. Credit Enhancement Summary ODART 2021-1 ODART 2019-1 ODART 2018-1 ODART 2017-2(i) ODART 2017-1(i) ODART 2016-1(ii) Subordination (% of the initial receivables)(iii) Class A 21.50 27.15 25.50 37.00 30.00 20.00 Class B 9.25 15.20 14.00 23.00 21.00 13.95 Presale: OneMain Direct Auto Receivables Trust 2021-1 October 5, 2021 PRIMARY CREDIT ANALYST Peter W Chang, CFA New York + 1 (212) 438 1505 peter.chang @spglobal.com SECONDARY CONTACTS Zarif Ahmed New York + 1 (212) 438 6690 zarif.ahmed @spglobal.com Trang Luu Austin + 1 (214) 765 5887 trang.luu @spglobal.com www.standardandpoors.com October 5, 2021 1 © S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimer on the last page. 2732523

Transcript of OneMain Direct Auto Receivables Trust 2021-1

Presale:

OneMain Direct Auto Receivables Trust 2021-1October 5, 2021

Preliminary Ratings

Class Preliminary rating Type Interest ratePreliminary amount (mil.

$)(i)Legal maturitydate

A AAA (sf) Senior Fixed 464.212 July 14, 2028

B AA (sf) Subordinate Fixed 77.368 July 14, 2028

C A (sf) Subordinate Fixed 41.052 July 14, 2028

D BBB (sf) Subordinate Fixed 17.368 Nov. 14, 2030

Note: This presale report is based on information as of Oct. 5, 2021. The ratings shown are preliminary. Subsequent information may result inthe assignment of final ratings that differ from the preliminary ratings. Accordingly, the preliminary ratings should not be construed asevidence of final ratings. This report does not constitute a recommendation to buy, hold, or sell securities. (i)The actual size of these trancheswill be determined on the pricing date.

Profile

Expected closing date Oct. 15, 2021.

Collateral Direct auto loan receivables.

Servicer OneMain Finance Corp.

Sellers OneMain Affiliates.

Depositor OneMain Direct Auto Funding LLC.

Issuer OneMain Direct Auto Receivables Trust 2021-1.

Underwriter Deutsche Bank Securities Inc.

Indenture trustee Wells Fargo Bank N.A.

Owner trustee, depositor loan trustee, and issuer loan trustee Wilmington Trust N.A.

Credit Enhancement Summary

ODART 2021-1 ODART 2019-1 ODART 2018-1ODART

2017-2(i)ODART

2017-1(i)ODART

2016-1(ii)

Subordination (% of the initial receivables)(iii)

Class A 21.50 27.15 25.50 37.00 30.00 20.00

Class B 9.25 15.20 14.00 23.00 21.00 13.95

Presale:

OneMain Direct Auto Receivables Trust 2021-1October 5, 2021

PRIMARY CREDIT ANALYST

Peter W Chang, CFA

New York

+ 1 (212) 438 1505

SECONDARY CONTACTS

Zarif Ahmed

New York

+ 1 (212) 438 6690

Trang Luu

Austin

+ 1 (214) 765 5887

www.standardandpoors.com October 5, 2021 1

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

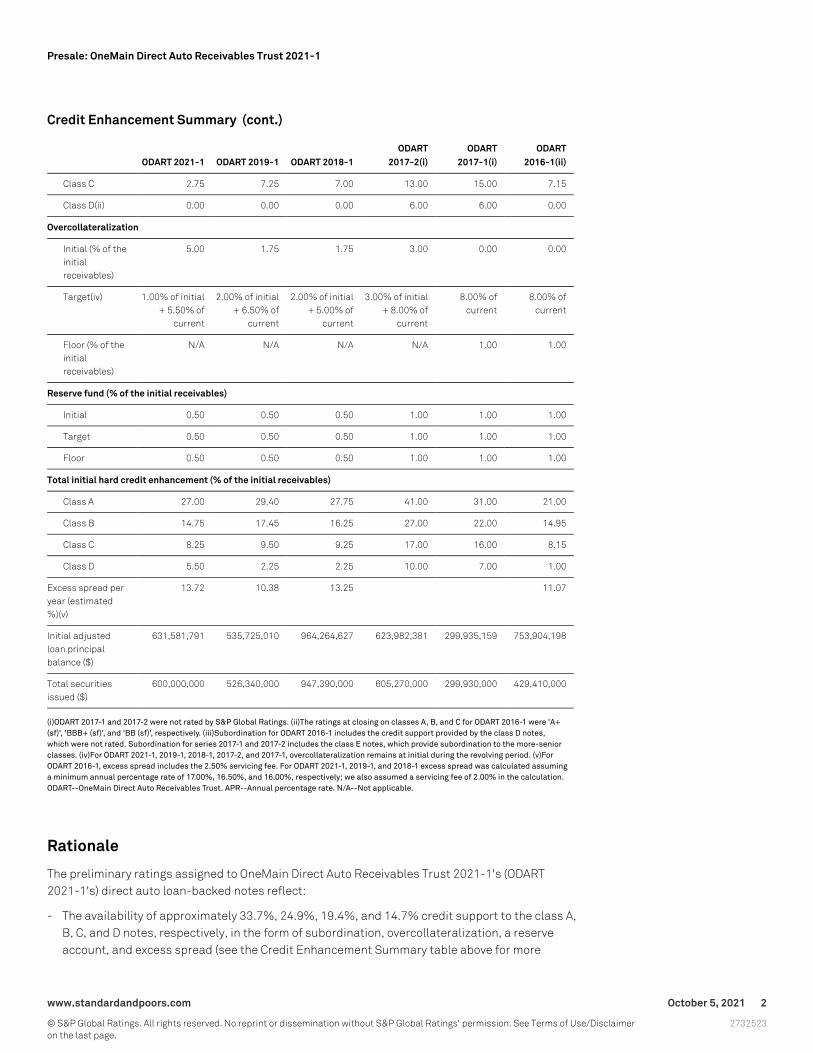

Credit Enhancement Summary (cont.)

ODART 2021-1 ODART 2019-1 ODART 2018-1ODART

2017-2(i)ODART

2017-1(i)ODART

2016-1(ii)

Class C 2.75 7.25 7.00 13.00 15.00 7.15

Class D(ii) 0.00 0.00 0.00 6.00 6.00 0.00

Overcollateralization

Initial (% of theinitialreceivables)

5.00 1.75 1.75 3.00 0.00 0.00

Target(iv) 1.00% of initial+ 5.50% of

current

2.00% of initial+ 6.50% of

current

2.00% of initial+ 5.00% of

current

3.00% of initial+ 8.00% of

current

8.00% ofcurrent

8.00% ofcurrent

Floor (% of theinitialreceivables)

N/A N/A N/A N/A 1.00 1.00

Reserve fund (% of the initial receivables)

Initial 0.50 0.50 0.50 1.00 1.00 1.00

Target 0.50 0.50 0.50 1.00 1.00 1.00

Floor 0.50 0.50 0.50 1.00 1.00 1.00

Total initial hard credit enhancement (% of the initial receivables)

Class A 27.00 29.40 27.75 41.00 31.00 21.00

Class B 14.75 17.45 16.25 27.00 22.00 14.95

Class C 8.25 9.50 9.25 17.00 16.00 8.15

Class D 5.50 2.25 2.25 10.00 7.00 1.00

Excess spread peryear (estimated%)(v)

13.72 10.38 13.25 11.07

Initial adjustedloan principalbalance ($)

631,581,791 535,725,010 964,264,627 623,982,381 299,935,159 753,904,198

Total securitiesissued ($)

600,000,000 526,340,000 947,390,000 605,270,000 299,930,000 429,410,000

(i)ODART 2017-1 and 2017-2 were not rated by S&P Global Ratings. (ii)The ratings at closing on classes A, B, and C for ODART 2016-1 were 'A+(sf)', 'BBB+ (sf)', and 'BB (sf)', respectively. (iii)Subordination for ODART 2016-1 includes the credit support provided by the class D notes,which were not rated. Subordination for series 2017-1 and 2017-2 includes the class E notes, which provide subordination to the more-seniorclasses. (iv)For ODART 2021-1, 2019-1, 2018-1, 2017-2, and 2017-1, overcollateralization remains at initial during the revolving period. (v)ForODART 2016-1, excess spread includes the 2.50% servicing fee. For ODART 2021-1, 2019-1, and 2018-1 excess spread was calculated assuminga minimum annual percentage rate of 17.00%, 16.50%, and 16.00%, respectively; we also assumed a servicing fee of 2.00% in the calculation.ODART--OneMain Direct Auto Receivables Trust. APR--Annual percentage rate. N/A--Not applicable.

Rationale

The preliminary ratings assigned to OneMain Direct Auto Receivables Trust 2021-1's (ODART2021-1's) direct auto loan-backed notes reflect:

- The availability of approximately 33.7%, 24.9%, 19.4%, and 14.7% credit support to the class A,B, C, and D notes, respectively, in the form of subordination, overcollateralization, a reserveaccount, and excess spread (see the Credit Enhancement Summary table above for more

www.standardandpoors.com October 5, 2021 2

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

information). These credit support levels are sufficient to withstand stresses commensuratewith the assigned preliminary ratings, based on our stressed cash flow scenarios (see the S&PGlobal Ratings' Expected Loss section below for more information).

- Our worst-case weighted average base-case loss for this transaction is 5.56%. This base caseis a function of the transaction-specific reinvestment criteria and actual OneMain Holdings Inc.(OneMain) loan performance to date. Our base case continues to incorporate Direct Autoperformance dating back to 2014.

- Our expectation that, under a moderate ('BBB') stress scenario of 2.32x our expected net losslevel, all else equal, our ratings will be within the credit stability limits specified by section A.4of the Appendix contained in S&P Global Rating Definitions (see "S&P Global RatingsDefinitions," published Jan. 5, 2021).

- The timely interest and full principal payments made under stressed cash flow modelingscenarios appropriate for the assigned preliminary ratings.

- The characteristics of the pool being securitized and the receivables that are expected to bepurchased during the revolving period.

- The transaction's payment and legal structures.

Environmental, Social, And Governance (ESG) Factors

Our rating analysis considers a transaction's potential exposure to ESG credit factors. In our view,the transaction has relatively high exposure to environmental credit factors due to the collateralpool that primarily comprises of vehicles with internal combustion engines (ICEs), which createemissions of pollutants, including greenhouse gases. While the adoption of electric vehicles andfuture regulation could in time lower ICE vehicle values, we believe our current approach toevaluating recovery adequately accounts for vehicle values over the transaction's relatively shortexpected life.

The transaction also has relatively high exposure to social credit factors due to the pool consistingof predominantly subprime obligors with relatively high interest rates. Affordability considerationsfor these subprime borrowers could increase legal and regulatory risks if the validity of the loancontracts or the servicer's collection practices were challenged. We believe this risk is mitigatedby representations made by the issuer that each loan complies with applicable laws when it isoriginated, and that the originator has legal and compliance departments that manage adherenceto applicable laws. In addition, demographic changes and shifts in borrower preferences couldreduce the demand for brick-and-mortar-centric lending models. We believe this risk is mitigatedby the development and growth of multichannel origination platforms, including online and byphone.

We also believe the transaction has relatively high exposure to governance credit factors withrespect to the revolving collateral pool and the originators' active role over the transaction's life,which exposes investors to the risk of loosening underwriting standards or potential adverseselection. To account for this risk, we assumed that the pool's composition will migrate to thelowest credit quality allowable under the transaction's reinvestment criteria tests, resulting in ahigher expected loss than that of a typical amortizing pool.

www.standardandpoors.com October 5, 2021 3

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

Key Rating Considerations

We considered the following factors in analyzing this transaction:

- Centralized servicing centers. OneMain operates four centralized servicing centers, which,along with the branches, operate under a single IT platform (CLASS, the former Springleafproprietary system). The authority for determining and overriding underwriting, servicing, andaccount management parameters are also centralized and highly monitored and controlled.This enables the company to effectively service the portfolio.

- Centralized servicing business continuity plan. OneMain has a business continuity plan in placethat enables the company to centralize servicing for 100% of its operations within 30 days. Thecommon IT platform across the branches also simplifies the process of centralizing servicing.

- Multiyear committed funding. As of June 30, 2021, OneMain had 13 separate revolving conduitfacilities across both legacy platforms, with $7.3 billion of undrawn capacity. OneMain also hasaccess to the securitization market, having issued 29 ABS transactions. The company has alsoissued approximately $14.6 billion in high-yield bonds since 2013.

- Long operating history. OneMain is the combination of two established specialty financecompanies: Springleaf and OneMain Financial Holdings (OMFH) Springleaf (formerly known asAmerican General Finance Inc.) has been in business since 1920, while OMFH has been inbusiness since 1912. The combined OneMain has operated through multiple credit cycles,though under different ownership regimes.

- Leadership experience. The company's executive management team has extensive experiencein the consumer finance industry. In June 2018, an investor group led by fund managers ApolloGlobal Management LLC and Varde Partners Inc. completed its acquisition of FortressInvestment Group LLC's equity interest in OneMain. In July 2018, OneMain announced DougShulman as its president and CEO, succeeding Jay Levine. Effective Dec. 31, 2020, OneMain'sboard of directors elected Mr. Shulman as Chairman of the board. We continue to monitor thecompany's portfolio trends, underwriting policies, and corporate developments.

- Branch operation experience. The company's branch operations are the core of its communitylending business model and are overseen by district managers who averaged 21 years ofexperience at the company.

Key Changes From The ODART 2019-1 Transaction

Credit and structural changes from the ODART 2019-1 transaction include:

- ODART 2021-1 includes a two-year revolving period, while ODART 2019-1 had a five-yearrevolving period. As a result, we removed the additional stress we had applied to our worst-caseweighted average base-case losses in ODART 2019-1 that accounted for the five-year revolvingperiod.

- Hard credit enhancement decreased for classes A, B, and C to 27.00%, 14.75%, 8.25%,respectively, from 29.40%, 17.45%, 9.50%; and it increased for class D to 5.50% from 2.25%.

- Initial overcollateralization increased to 5.00% from 1.75% ODART 2019-1. Meanwhile, theovercollateralization target, which will go into effect once the deal is in amortization, decreasedto 1.00% of initial plus 5.50% of current pool balance from 2.00% of initial plus 6.50% of thecurrent pool balance.

www.standardandpoors.com October 5, 2021 4

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

- Annual unstressed excess spread increased to approximately 13.72% from 10.38%.

- The backup servicer was removed from the transaction. We reviewed this change with respectto our operational risk criteria and determined that this does not have any material impact.

Changes in the pool from ODART 2019-1 at closing include:

- The age limit for the vehicles securing the loans increased to up to 10 years old from up to eightyears old. These types of loans were included in the static pool data and were considered in ouranalysis.

- The weighted average annual percentage rate (APR) of the initial pool decreased to 19.66%from 19.71%.

- The percent of the initial pool with an original term greater than 60 months decreased to16.72% from 18.31%.

Despite the somewhat comparable collateral characteristics of the initial pools, each transactionincludes a revolving period where the proceeds from principal payments on loans can be used topurchase new loans for the pool during the revolving period--as long as the reinvestment criteriais met. That said, the pool characteristics are expected to change over time. To account for anypotential weakening, we assume the worst-case pool in our assumptions, given the reinvestmentcriteria. We believe the reinvestment criteria by risk tier for ODART 2021-1 is slightly weaker thanthat for ODART 2019-1: The minimum percentage of the pool that can be in the best risk tier (tier S)decreased to 15% from 20%, though this is somewhat offset by the combined limit of the twoworst tiers declining to 2.0% from 2.50%. Overall, our worst-case weighted average base-caselosses remain comparable, given that OneMain's direct auto managed portfolio continues togenerally perform in-line with our expected loss performance. However, given the shorter revolvingperiod, we decreased our overall base-case loss proxy slightly (see the S&P Global Ratings'Expected Loss section below for additional info).

Transaction Overview

This transaction is OneMain's sixth direct auto loan term ABS transaction and its first in 2021. It isthe fourth OneMain direct auto transaction rated by S&P Global Ratings. We also have currentratings on 13 OneMain transactions backed by unsecured personal and hard-secured loans:OneMain Financial Issuance Trust (OMFIT) 2015-3, 2016-1, 2016-3, 2017-1, 2018-1, 2018-2 and2019-1, 2019-2, 2020-1, 2020-2, and 2012-1; and two Springleaf consumer loan transactions:Springleaf Funding Trust (SLFT) 2015-B and 2017-A.

www.standardandpoors.com October 5, 2021 5

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

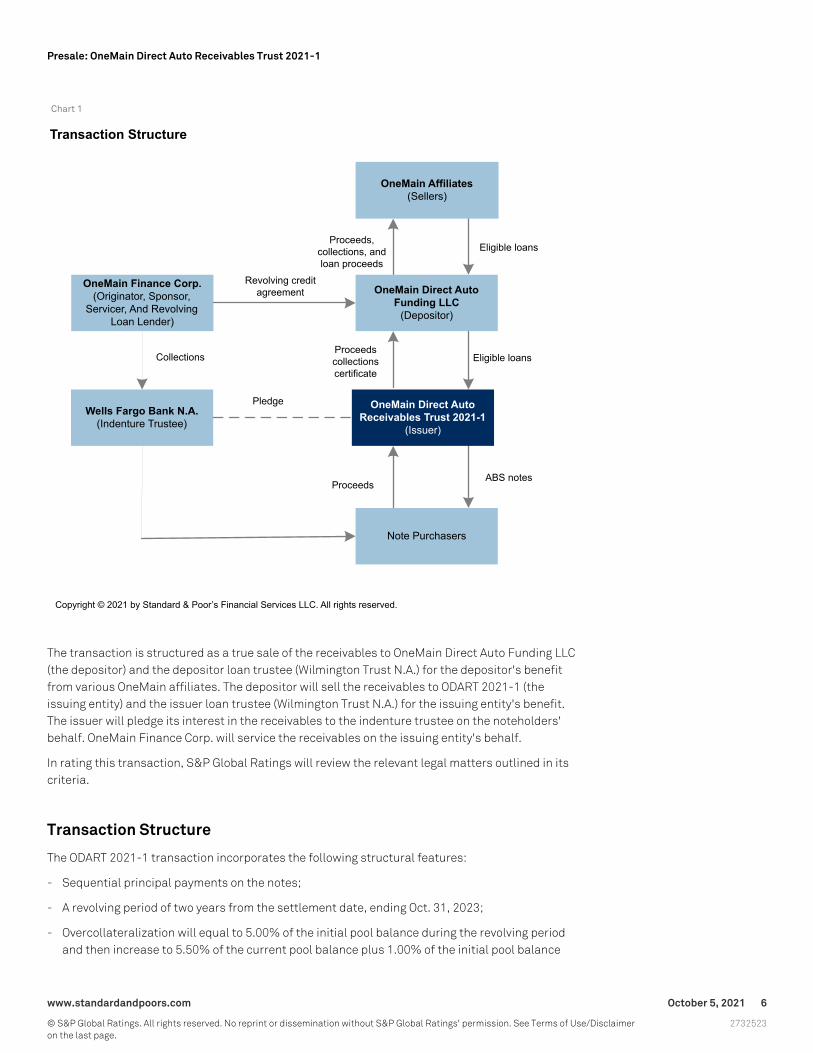

Chart 1

The transaction is structured as a true sale of the receivables to OneMain Direct Auto Funding LLC(the depositor) and the depositor loan trustee (Wilmington Trust N.A.) for the depositor's benefitfrom various OneMain affiliates. The depositor will sell the receivables to ODART 2021-1 (theissuing entity) and the issuer loan trustee (Wilmington Trust N.A.) for the issuing entity's benefit.The issuer will pledge its interest in the receivables to the indenture trustee on the noteholders'behalf. OneMain Finance Corp. will service the receivables on the issuing entity's behalf.

In rating this transaction, S&P Global Ratings will review the relevant legal matters outlined in itscriteria.

Transaction Structure

The ODART 2021-1 transaction incorporates the following structural features:

- Sequential principal payments on the notes;

- A revolving period of two years from the settlement date, ending Oct. 31, 2023;

- Overcollateralization will equal to 5.00% of the initial pool balance during the revolving periodand then increase to 5.50% of the current pool balance plus 1.00% of the initial pool balance

www.standardandpoors.com October 5, 2021 6

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

during the amortization period.

- A nondeclining 0.50% reserve account;

- Performance-based early amortization triggers linked to a three-month average monthly netloss percentage measured on or after the payment date in January 2022, or anovercollateralization test; and

- Early amortization triggers linked to pool composition or a servicer default.

Payment Structure

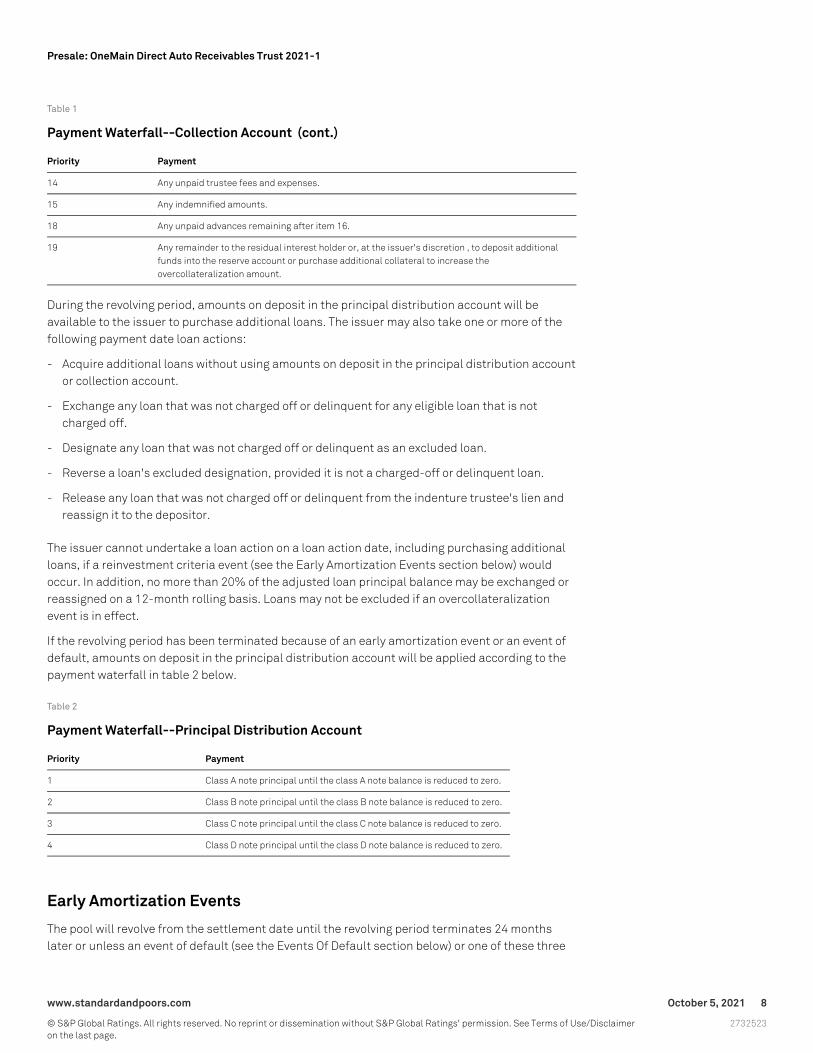

The servicer will deposit interest and principal collections for the receivables pool into thecollection account no later than two business days after processing. Priority and regular principalpayments made in items 4, 6, 8, 10, and 13 of the collection account's payment waterfall (seetable 1) will be deposited into the principal distribution account, which is subject to its ownpayment waterfall. The class A, B, C, and D notes will receive interest payments on each monthlypayment date and no principal during the revolving period. Principal payments on the notes will bemade upon the revolving period's termination in a sequential order of priority. Funds may bewithdrawn from the reserve account each month to make payments in items 1-10 of the collectionaccount's payment waterfall to the extent that collections are not sufficient.

Table 1

Payment Waterfall--Collection Account

Priority Payment

1 Indenture trustee and owner trustee fees and expenses, capped at $200,000 per year (providedthat the cap will not apply if an event of default or servicer default occurs and continues). To thesuccessor servicer, if any, the transition expenses incurred from it becoming the successorservicer--to the extent not previously paid by the predecessor servicer and capped at $250,000.

2 Servicing fee of 2.00% per year.

3 Class A note interest.

4 First-priority principal payment (if the class A notes' balance is greater than the adjusted loanprincipal balance).

5 Class B note interest

6 Second-priority principal payment (if the class A and B notes' balance is greater than the adjustedloan principal balance after any first-priority principal payments are made).

7 Class C note interest.

8 Third-priority principal payment (if the class A, B, and C notes' balance is greater than theadjusted loan principal balance after any first- and second-priority principal payments are made).

91 Class D note interest.

10 Fourth-priority principal payment (if the class A, B, C, and D notes' balance is greater than theadjusted loan principal balance after any first-, second-, and third-priority principal payments aremade).

11 Restore the reserve account to its required amount (the lesser of the reserve account requiredamount for that payment date and all funds remaining after items 1 through 11 above).

12 Any unpaid advances to the servicer.

13 Regular principal payment (the excess, if any, of the class A, B, C, and D notes' balance over thedifference between the adjusted loan principal balance and the required overcollateralizationamount after any priority principal payments are made).

www.standardandpoors.com October 5, 2021 7

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

Table 1

Payment Waterfall--Collection Account (cont.)

Priority Payment

14 Any unpaid trustee fees and expenses.

15 Any indemnified amounts.

18 Any unpaid advances remaining after item 16.

19 Any remainder to the residual interest holder or, at the issuer's discretion , to deposit additionalfunds into the reserve account or purchase additional collateral to increase theovercollateralization amount.

During the revolving period, amounts on deposit in the principal distribution account will beavailable to the issuer to purchase additional loans. The issuer may also take one or more of thefollowing payment date loan actions:

- Acquire additional loans without using amounts on deposit in the principal distribution accountor collection account.

- Exchange any loan that was not charged off or delinquent for any eligible loan that is notcharged off.

- Designate any loan that was not charged off or delinquent as an excluded loan.

- Reverse a loan's excluded designation, provided it is not a charged-off or delinquent loan.

- Release any loan that was not charged off or delinquent from the indenture trustee's lien andreassign it to the depositor.

The issuer cannot undertake a loan action on a loan action date, including purchasing additionalloans, if a reinvestment criteria event (see the Early Amortization Events section below) wouldoccur. In addition, no more than 20% of the adjusted loan principal balance may be exchanged orreassigned on a 12-month rolling basis. Loans may not be excluded if an overcollateralizationevent is in effect.

If the revolving period has been terminated because of an early amortization event or an event ofdefault, amounts on deposit in the principal distribution account will be applied according to thepayment waterfall in table 2 below.

Table 2

Payment Waterfall--Principal Distribution Account

Priority Payment

1 Class A note principal until the class A note balance is reduced to zero.

2 Class B note principal until the class B note balance is reduced to zero.

3 Class C note principal until the class C note balance is reduced to zero.

4 Class D note principal until the class D note balance is reduced to zero.

Early Amortization Events

The pool will revolve from the settlement date until the revolving period terminates 24 monthslater or unless an event of default (see the Events Of Default section below) or one of these three

www.standardandpoors.com October 5, 2021 8

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

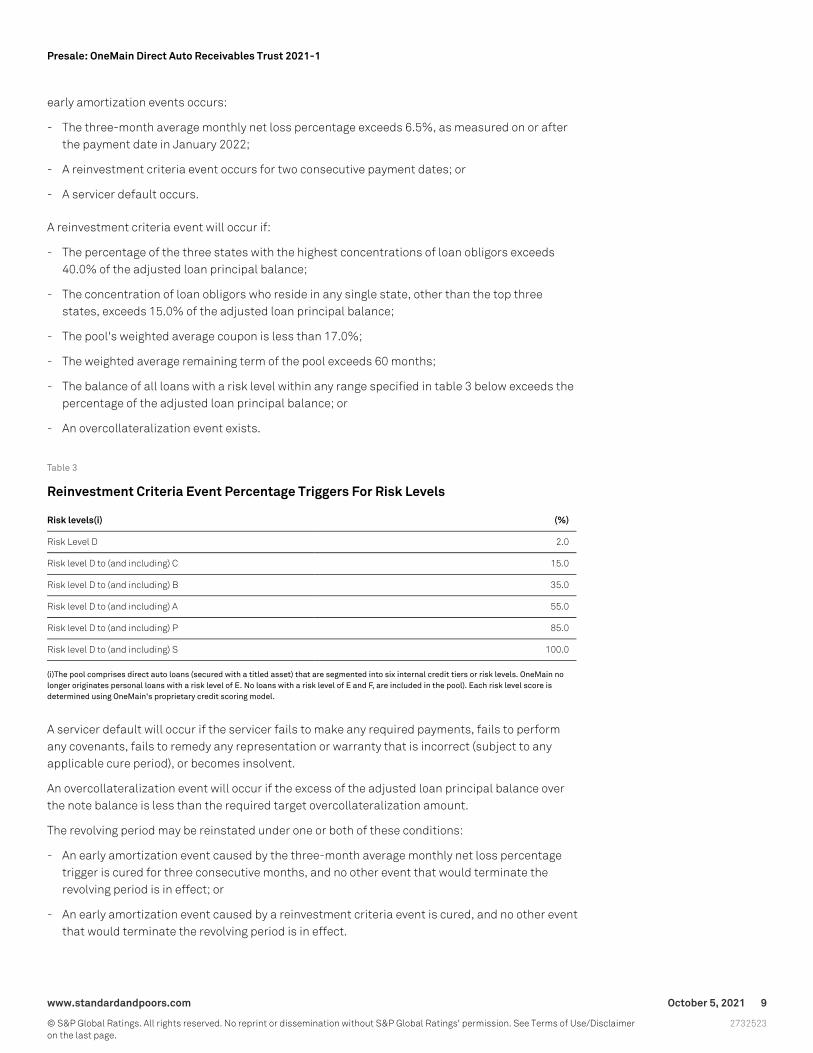

early amortization events occurs:

- The three-month average monthly net loss percentage exceeds 6.5%, as measured on or afterthe payment date in January 2022;

- A reinvestment criteria event occurs for two consecutive payment dates; or

- A servicer default occurs.

A reinvestment criteria event will occur if:

- The percentage of the three states with the highest concentrations of loan obligors exceeds40.0% of the adjusted loan principal balance;

- The concentration of loan obligors who reside in any single state, other than the top threestates, exceeds 15.0% of the adjusted loan principal balance;

- The pool's weighted average coupon is less than 17.0%;

- The weighted average remaining term of the pool exceeds 60 months;

- The balance of all loans with a risk level within any range specified in table 3 below exceeds thepercentage of the adjusted loan principal balance; or

- An overcollateralization event exists.

Table 3

Reinvestment Criteria Event Percentage Triggers For Risk Levels

Risk levels(i) (%)

Risk Level D 2.0

Risk level D to (and including) C 15.0

Risk level D to (and including) B 35.0

Risk level D to (and including) A 55.0

Risk level D to (and including) P 85.0

Risk level D to (and including) S 100.0

(i)The pool comprises direct auto loans (secured with a titled asset) that are segmented into six internal credit tiers or risk levels. OneMain nolonger originates personal loans with a risk level of E. No loans with a risk level of E and F, are included in the pool). Each risk level score isdetermined using OneMain's proprietary credit scoring model.

A servicer default will occur if the servicer fails to make any required payments, fails to performany covenants, fails to remedy any representation or warranty that is incorrect (subject to anyapplicable cure period), or becomes insolvent.

An overcollateralization event will occur if the excess of the adjusted loan principal balance overthe note balance is less than the required target overcollateralization amount.

The revolving period may be reinstated under one or both of these conditions:

- An early amortization event caused by the three-month average monthly net loss percentagetrigger is cured for three consecutive months, and no other event that would terminate therevolving period is in effect; or

- An early amortization event caused by a reinvestment criteria event is cured, and no other eventthat would terminate the revolving period is in effect.

www.standardandpoors.com October 5, 2021 9

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

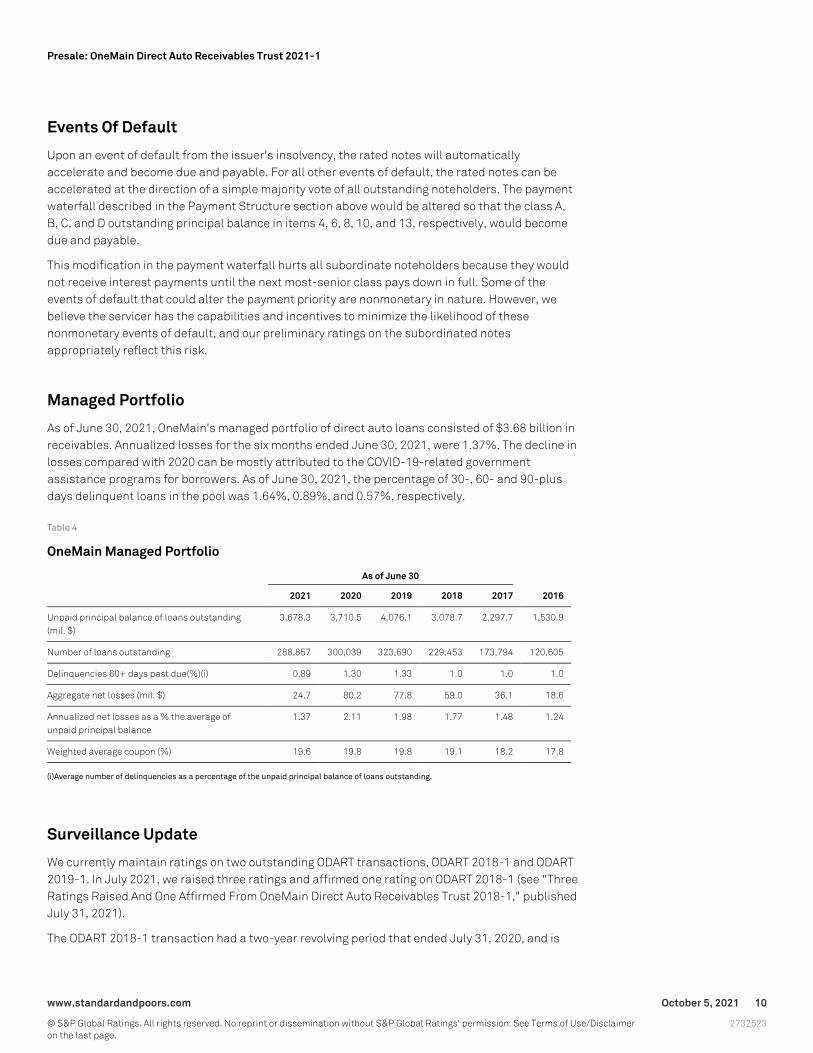

Events Of Default

Upon an event of default from the issuer's insolvency, the rated notes will automaticallyaccelerate and become due and payable. For all other events of default, the rated notes can beaccelerated at the direction of a simple majority vote of all outstanding noteholders. The paymentwaterfall described in the Payment Structure section above would be altered so that the class A,B, C, and D outstanding principal balance in items 4, 6, 8, 10, and 13, respectively, would becomedue and payable.

This modification in the payment waterfall hurts all subordinate noteholders because they wouldnot receive interest payments until the next most-senior class pays down in full. Some of theevents of default that could alter the payment priority are nonmonetary in nature. However, webelieve the servicer has the capabilities and incentives to minimize the likelihood of thesenonmonetary events of default, and our preliminary ratings on the subordinated notesappropriately reflect this risk.

Managed Portfolio

As of June 30, 2021, OneMain's managed portfolio of direct auto loans consisted of $3.68 billion inreceivables. Annualized losses for the six months ended June 30, 2021, were 1.37%. The decline inlosses compared with 2020 can be mostly attributed to the COVID-19-related governmentassistance programs for borrowers. As of June 30, 2021, the percentage of 30-, 60- and 90-plusdays delinquent loans in the pool was 1.64%, 0.89%, and 0.57%, respectively.

Table 4

OneMain Managed Portfolio

As of June 30

2021 2020 2019 2018 2017 2016

Unpaid principal balance of loans outstanding(mil. $)

3,678.3 3,710.5 4,076.1 3,078.7 2,297.7 1,530.9

Number of loans outstanding 288,857 300,039 323,690 229,453 173,794 120,605

Delinquencies 60+ days past due(%)(i) 0.89 1.30 1.33 1.0 1.0 1.0

Aggregate net losses (mil. $) 24.7 80.2 77.8 59.0 36.1 18.6

Annualized net losses as a % the average ofunpaid principal balance

1.37 2.11 1.98 1.77 1.48 1.24

Weighted average coupon (%) 19.6 19.8 19.8 19.1 18.2 17.8

(i)Average number of delinquencies as a percentage of the unpaid principal balance of loans outstanding.

Surveillance Update

We currently maintain ratings on two outstanding ODART transactions, ODART 2018-1 and ODART2019-1. In July 2021, we raised three ratings and affirmed one rating on ODART 2018-1 (see "ThreeRatings Raised And One Affirmed From OneMain Direct Auto Receivables Trust 2018-1," publishedJuly 31, 2021).

The ODART 2018-1 transaction had a two-year revolving period that ended July 31, 2020, and is

www.standardandpoors.com October 5, 2021 10

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

currently in amortization. As of the September 2021 distribution date, the transaction has beenoutstanding 38 months, with a pool factor of 39.66% for the last 14 months in amortization andcumulative net losses of 1.31% since the start of amortization. The transaction is performingbetter than our initial expectations, which were based on the pool migrating to a worst-case poolcomposition. We currently expect cumulative net losses, measured from the start of amortization,of up to 2.50%.

The ODART 2019-1 transaction has 30 months of performance and is still in its revolving period asof the September 2021 distribution date.

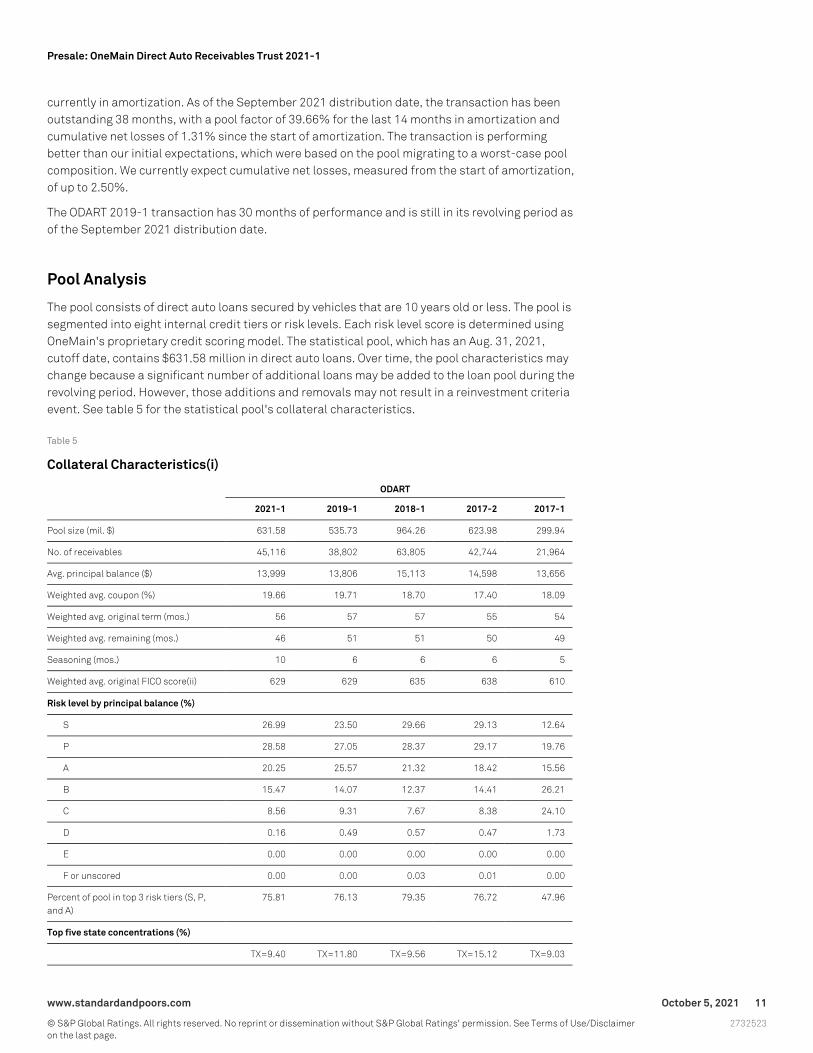

Pool Analysis

The pool consists of direct auto loans secured by vehicles that are 10 years old or less. The pool issegmented into eight internal credit tiers or risk levels. Each risk level score is determined usingOneMain's proprietary credit scoring model. The statistical pool, which has an Aug. 31, 2021,cutoff date, contains $631.58 million in direct auto loans. Over time, the pool characteristics maychange because a significant number of additional loans may be added to the loan pool during therevolving period. However, those additions and removals may not result in a reinvestment criteriaevent. See table 5 for the statistical pool's collateral characteristics.

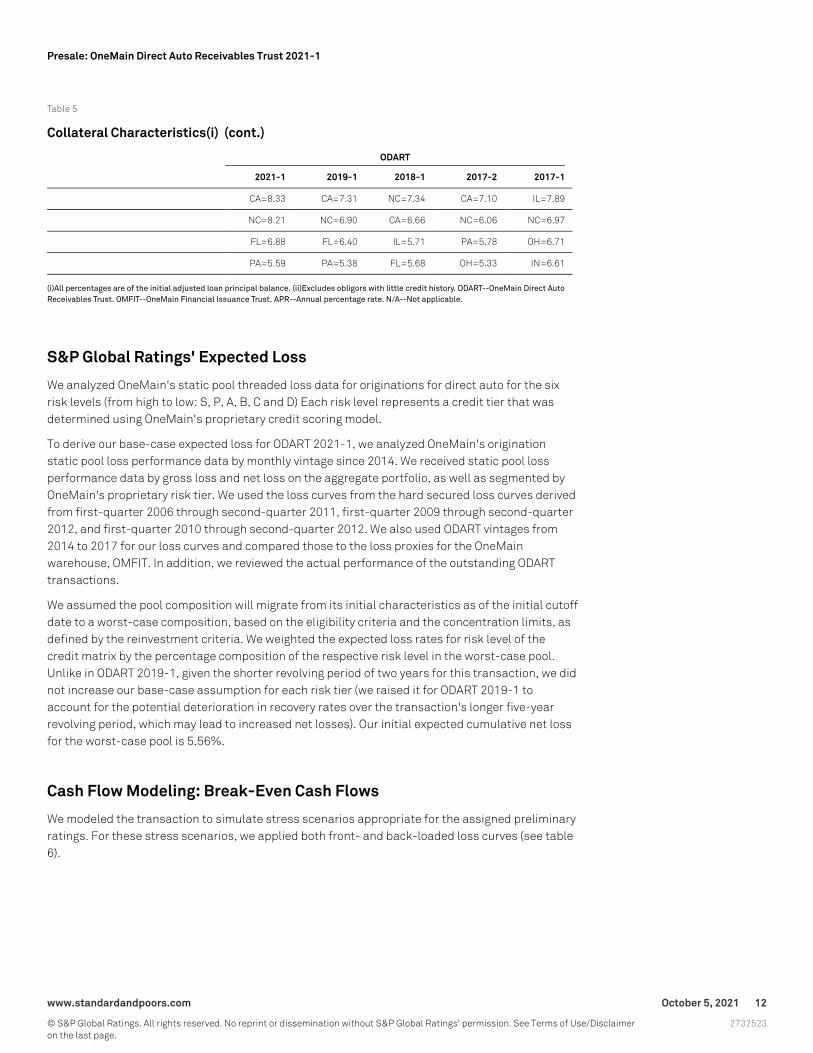

Table 5

Collateral Characteristics(i)

ODART

2021-1 2019-1 2018-1 2017-2 2017-1

Pool size (mil. $) 631.58 535.73 964.26 623.98 299.94

No. of receivables 45,116 38,802 63,805 42,744 21,964

Avg. principal balance ($) 13,999 13,806 15,113 14,598 13,656

Weighted avg. coupon (%) 19.66 19.71 18.70 17.40 18.09

Weighted avg. original term (mos.) 56 57 57 55 54

Weighted avg. remaining (mos.) 46 51 51 50 49

Seasoning (mos.) 10 6 6 6 5

Weighted avg. original FICO score(ii) 629 629 635 638 610

Risk level by principal balance (%)

S 26.99 23.50 29.66 29.13 12.64

P 28.58 27.05 28.37 29.17 19.76

A 20.25 25.57 21.32 18.42 15.56

B 15.47 14.07 12.37 14.41 26.21

C 8.56 9.31 7.67 8.38 24.10

D 0.16 0.49 0.57 0.47 1.73

E 0.00 0.00 0.00 0.00 0.00

F or unscored 0.00 0.00 0.03 0.01 0.00

Percent of pool in top 3 risk tiers (S, P,and A)

75.81 76.13 79.35 76.72 47.96

Top five state concentrations (%)

TX=9.40 TX=11.80 TX=9.56 TX=15.12 TX=9.03

www.standardandpoors.com October 5, 2021 11

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

Table 5

Collateral Characteristics(i) (cont.)

ODART

2021-1 2019-1 2018-1 2017-2 2017-1

CA=8.33 CA=7.31 NC=7.34 CA=7.10 IL=7.89

NC=8.21 NC=6.90 CA=6.66 NC=6.06 NC=6.97

FL=6.88 FL=6.40 IL=5.71 PA=5.78 OH=6.71

PA=5.59 PA=5.38 FL=5.68 OH=5.33 IN=6.61

(i)All percentages are of the initial adjusted loan principal balance. (ii)Excludes obligors with little credit history. ODART--OneMain Direct AutoReceivables Trust. OMFIT--OneMain Financial Issuance Trust. APR--Annual percentage rate. N/A--Not applicable.

S&P Global Ratings' Expected Loss

We analyzed OneMain's static pool threaded loss data for originations for direct auto for the sixrisk levels (from high to low: S, P, A, B, C and D) Each risk level represents a credit tier that wasdetermined using OneMain's proprietary credit scoring model.

To derive our base-case expected loss for ODART 2021-1, we analyzed OneMain's originationstatic pool loss performance data by monthly vintage since 2014. We received static pool lossperformance data by gross loss and net loss on the aggregate portfolio, as well as segmented byOneMain's proprietary risk tier. We used the loss curves from the hard secured loss curves derivedfrom first-quarter 2006 through second-quarter 2011, first-quarter 2009 through second-quarter2012, and first-quarter 2010 through second-quarter 2012. We also used ODART vintages from2014 to 2017 for our loss curves and compared those to the loss proxies for the OneMainwarehouse, OMFIT. In addition, we reviewed the actual performance of the outstanding ODARTtransactions.

We assumed the pool composition will migrate from its initial characteristics as of the initial cutoffdate to a worst-case composition, based on the eligibility criteria and the concentration limits, asdefined by the reinvestment criteria. We weighted the expected loss rates for risk level of thecredit matrix by the percentage composition of the respective risk level in the worst-case pool.Unlike in ODART 2019-1, given the shorter revolving period of two years for this transaction, we didnot increase our base-case assumption for each risk tier (we raised it for ODART 2019-1 toaccount for the potential deterioration in recovery rates over the transaction's longer five-yearrevolving period, which may lead to increased net losses). Our initial expected cumulative net lossfor the worst-case pool is 5.56%.

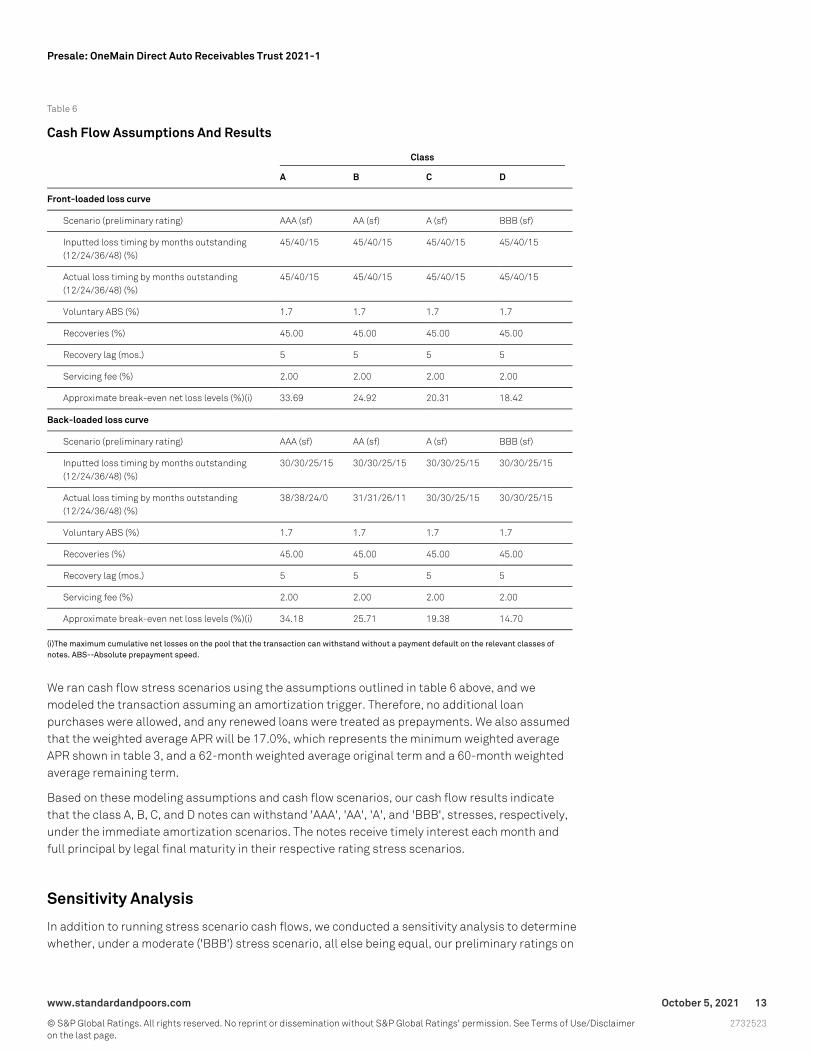

Cash Flow Modeling: Break-Even Cash Flows

We modeled the transaction to simulate stress scenarios appropriate for the assigned preliminaryratings. For these stress scenarios, we applied both front- and back-loaded loss curves (see table6).

www.standardandpoors.com October 5, 2021 12

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

Table 6

Cash Flow Assumptions And Results

Class

A B C D

Front-loaded loss curve

Scenario (preliminary rating) AAA (sf) AA (sf) A (sf) BBB (sf)

Inputted loss timing by months outstanding(12/24/36/48) (%)

45/40/15 45/40/15 45/40/15 45/40/15

Actual loss timing by months outstanding(12/24/36/48) (%)

45/40/15 45/40/15 45/40/15 45/40/15

Voluntary ABS (%) 1.7 1.7 1.7 1.7

Recoveries (%) 45.00 45.00 45.00 45.00

Recovery lag (mos.) 5 5 5 5

Servicing fee (%) 2.00 2.00 2.00 2.00

Approximate break-even net loss levels (%)(i) 33.69 24.92 20.31 18.42

Back-loaded loss curve

Scenario (preliminary rating) AAA (sf) AA (sf) A (sf) BBB (sf)

Inputted loss timing by months outstanding(12/24/36/48) (%)

30/30/25/15 30/30/25/15 30/30/25/15 30/30/25/15

Actual loss timing by months outstanding(12/24/36/48) (%)

38/38/24/0 31/31/26/11 30/30/25/15 30/30/25/15

Voluntary ABS (%) 1.7 1.7 1.7 1.7

Recoveries (%) 45.00 45.00 45.00 45.00

Recovery lag (mos.) 5 5 5 5

Servicing fee (%) 2.00 2.00 2.00 2.00

Approximate break-even net loss levels (%)(i) 34.18 25.71 19.38 14.70

(i)The maximum cumulative net losses on the pool that the transaction can withstand without a payment default on the relevant classes ofnotes. ABS--Absolute prepayment speed.

We ran cash flow stress scenarios using the assumptions outlined in table 6 above, and wemodeled the transaction assuming an amortization trigger. Therefore, no additional loanpurchases were allowed, and any renewed loans were treated as prepayments. We also assumedthat the weighted average APR will be 17.0%, which represents the minimum weighted averageAPR shown in table 3, and a 62-month weighted average original term and a 60-month weightedaverage remaining term.

Based on these modeling assumptions and cash flow scenarios, our cash flow results indicatethat the class A, B, C, and D notes can withstand 'AAA', 'AA', 'A', and 'BBB', stresses, respectively,under the immediate amortization scenarios. The notes receive timely interest each month andfull principal by legal final maturity in their respective rating stress scenarios.

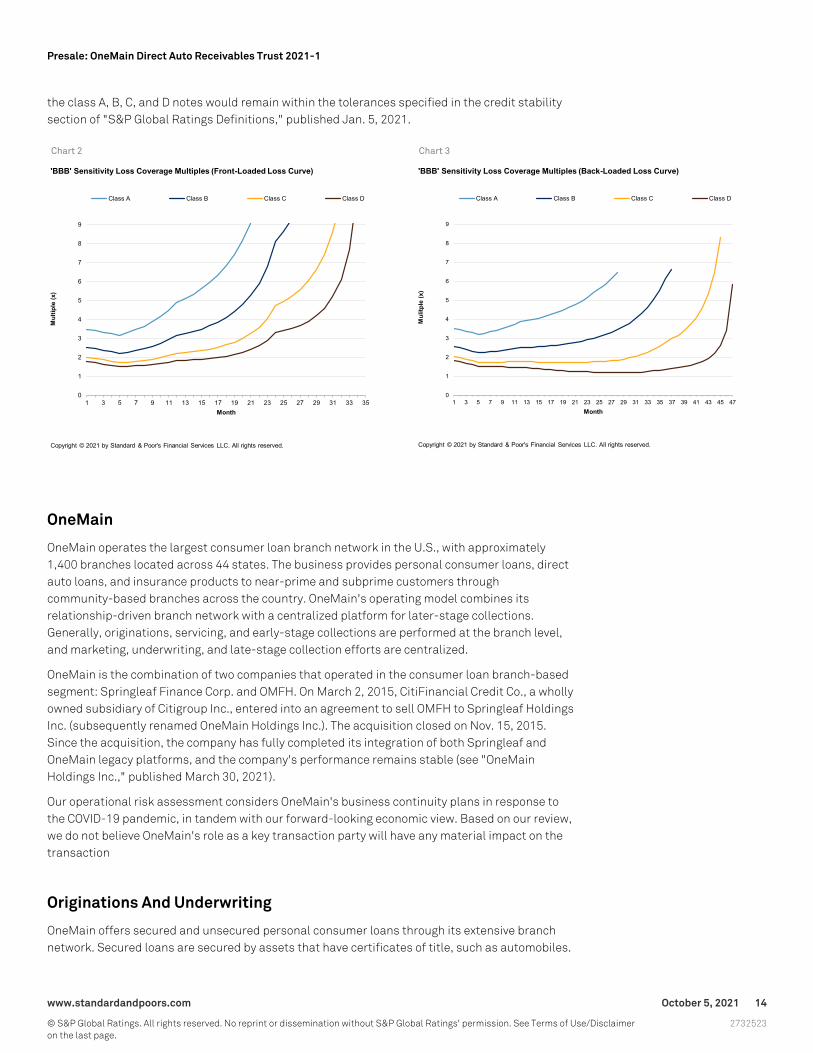

Sensitivity Analysis

In addition to running stress scenario cash flows, we conducted a sensitivity analysis to determinewhether, under a moderate ('BBB') stress scenario, all else being equal, our preliminary ratings on

www.standardandpoors.com October 5, 2021 13

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

the class A, B, C, and D notes would remain within the tolerances specified in the credit stabilitysection of "S&P Global Ratings Definitions," published Jan. 5, 2021.

Chart 2 Chart 3

OneMain

OneMain operates the largest consumer loan branch network in the U.S., with approximately1,400 branches located across 44 states. The business provides personal consumer loans, directauto loans, and insurance products to near-prime and subprime customers throughcommunity-based branches across the country. OneMain's operating model combines itsrelationship-driven branch network with a centralized platform for later-stage collections.Generally, originations, servicing, and early-stage collections are performed at the branch level,and marketing, underwriting, and late-stage collection efforts are centralized.

OneMain is the combination of two companies that operated in the consumer loan branch-basedsegment: Springleaf Finance Corp. and OMFH. On March 2, 2015, CitiFinancial Credit Co., a whollyowned subsidiary of Citigroup Inc., entered into an agreement to sell OMFH to Springleaf HoldingsInc. (subsequently renamed OneMain Holdings Inc.). The acquisition closed on Nov. 15, 2015.Since the acquisition, the company has fully completed its integration of both Springleaf andOneMain legacy platforms, and the company's performance remains stable (see "OneMainHoldings Inc.," published March 30, 2021).

Our operational risk assessment considers OneMain's business continuity plans in response tothe COVID-19 pandemic, in tandem with our forward-looking economic view. Based on our review,we do not believe OneMain's role as a key transaction party will have any material impact on thetransaction

Originations And Underwriting

OneMain offers secured and unsecured personal consumer loans through its extensive branchnetwork. Secured loans are secured by assets that have certificates of title, such as automobiles.

www.standardandpoors.com October 5, 2021 14

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

OneMain holds a first lien in the secured collateral that is pledged in this pool, and, in most cases,the assets serve as collateral for a personal loan rather than the loan proceeds being used tofinance the asset purchase. Unsecured loans include loans that are not secured by any collateralor secured by nontitled assets.

OneMain launched a direct auto loan business in 2014 as an extension of its personal consumerloan secured business. The direct auto loan business allows OneMain to offer its customers largerloan amounts with lower interest rates, on average, than its traditional secured personal loanproduct. OneMain originates direct auto loans through the same branch network directly withcustomers that typically already own the vehicle, rather than indirectly through automobiledealers at the point of sale.

The direct auto loans are nonrevolving with fixed interest rates, an average original principalbalance of $15,000, and a fixed, original term. The direct auto loans are secured by new and usedautomobiles, light-duty trucks, and other vehicles. The direct auto loans have loan-to-value ratiosranging from a maximum of 90% for the highest risk borrowers to a maximum of 250% for thelowest risk borrowers, based on OneMain's proprietary risk-scoring model and the model year ofthe financed vehicles, though some exceptions may be made.

OneMain's target demographic has an average FICO score in the high-500s to mid-600s range. Thetypical customer is employed full-time at origination and has a long and consistent employmenthistory, in the company's view. Borrowers typically take out loans to address a specific financingneed, such as debt consolidation, auto repair, medical bills, home repair, or household bills;borrowers use 78% of the direct auto loans to refinance existing auto loans. OneMain's direct autoprogram allows the qualifying borrower to get a loan with better terms than the personal loan orhard-secured program in return for collateral in a newer, better-quality vehicle. OneMain'saverage customer is 48 years old, has an average household income of $45,000 (based oncombined personal loan portfolio data as of March 31, 2021).

The company employs a marketing strategy that prioritizes the acquisition of profitable newcustomers while retaining and growing relationships with profitable existing customers. Customeracquisition can be broken down into three main segments: present, former, and new borrowers.The company acquires customers through several channels, including branch solicitation, directmail, retail, and the internet. Loan applications are either processed by the branch network withinscope of the centralized platform parameters or on a centralized basis. There has been anincrease in remote and online closings, since the COVID-19 pandemic. Before this, almost allcustomers completed their applications in person at the branches (even if the application beganonline).

OneMain's underwriting decision-making reflects two primary inputs: its proprietary risk-scoringmodel (which is a centralized process that assigns a risk level) and the individual borrower netcash flow analysis (which is performed at the branch or on a centralized basis). According toOneMain, all loans are underwritten with full verification and documentation of the borrower'sinformation, including identity, income, employment, and residence. The loans may be closed in abranch, at a centralized location, or remotely through the internet. The branch staff itself, ratherthan a third party, conducts collateral inspection.

Renewals are new loans made to existing customers who undergo a complete re-underwritingprocess. In addition, the borrower's credit history and performance with OneMain is consideredduring the re-underwriting process. In most cases, the renewed loan balance is incrementallyhigher than the outstanding balance of the loan being replaced, and part of the renewed loan'sproceeds are used to retire the replaced loan. The renewed loan's terms may differ materially fromthose of the replaced loan because the borrower may be assigned a new risk level or change froman unsecured loan to a secured loan. Renewals are an important source of new loan volume for

www.standardandpoors.com October 5, 2021 15

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

OneMain, as historically about half of customers have renewed their loan at least once during theloan's life.

During the two-year revolving period for ODART 2021-1, principal collections from the existingloans can be used to purchase new and renewed loans subject to eligibility parameters.

Servicing And Collections

OneMain generally employs a hybrid servicing model that leverages branch and centralizedcapabilities. All branches service and collect on loans, and they work to build relationships withcustomers through frequent personal interaction.

OneMain generally services each loan at the individual branch office location where the loan wasoriginated or at a central location. When a loan reaches three payments past due, OneMainFinance Corp., as servicer, transfers servicing to one of its four centralized servicing facilitieslocated in Evansville, Ind.; London, Ky.; Fort Mill, S.C.; or Tempe, Ariz. Servicing may be centralizedbefore 60 days past due if an account has been referred for litigation, bankruptcy, orrepossession. If an account has a pending insurance claim, it may not be centralized for up to 90days past due. OneMain may determine that loans that are fewer than 60 days past due shouldalso be serviced on a centralized basis if it determines centralized servicing is more effective andefficient. Although OneMain maintains a hybrid servicing platform, the risk of a servicinginterruption because of significant branch closures is partially mitigated by its practice ofcentralizing the servicing for later-stage delinquency accounts.

Branch payments are important in OneMain maintaining close contact with its customers forservicing purposes and future solicitation opportunities. These payments (i.e., cash, check, ormoney order) accounted for approximately 4.3% of all payment receipts on OneMain loans as ofthe three months ended March 31, 2021. As of June 2019, OneMain ceased accepting in-branchcash payments. In addition, a portion of payments were made by checks mailed to OneMainbranches. Centralized payment options (i.e., internet, ACH, and phone) account for the remainder.Branch-collected payments are transferred to a central account daily. The trend amongcustomers to make payments at branches has been steadily decreasing, replaced with paymentsby mail or electronic payment channels.

OneMain uses various loss mitigation techniques, such as deferment, curing, and modifications ofthe loans (of which modifications and curing must be approved centrally by OneMain's riskdepartment) in cases where consistent payment activity has been demonstrated. Deferment is apartial payment that extends an account's term. Customers are generally limited to twodeferments during a 12-month rolling period and are typically not offered a deferment if they aregreater than one payment past due, though the credit and collection policy permits deferments forborrowers who are two payments past due. Delinquent accounts may be brought back to currentstatus (i.e., a cure) if customers can demonstrate that they have rehabilitated from a temporaryevent that caused the delinquency, and if they have made two qualified payments in full duringconsecutive months. No payment or interest amounts are forgiven in this process. A modificationfor any payment is provided to customers to address ongoing or higher severity issues. Themodification involves changed loan terms (rate and/or tenor) and modifies the loan to meet theborrower's new financial situation and is offered on a short-term or permanent basis. Ashort-term modification reduces the rate and payment for a three- or six-month duration, with theability to extend to 12 months. A permanent modification leverages a term extension and/or ratereduction to meet a borrower's payment need.

OneMain's policy is generally not to renew delinquent accounts to mitigate loss. Accounts that aremore than 30 days delinquent are only renewed if the re-underwriting is successful and the cause

www.standardandpoors.com October 5, 2021 16

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

of the delinquency was temporary and will not, in OneMain's view, affect the customer's ability torepay the new loan. Enrollment for these borrower-assistance tools peaked in April 2020 atapproximately 8.0% of loans in the managed portfolio, but has since normalized to pre-pandemiclevels. Historically, borrower assistance enrollment has been approximately 2.0% per month ofoutstanding loans.

Wells Fargo Bank N.A. will act as the indenture trustee. In the event of a servicer default, servicingwill be transferred to a successor servicer.

Related Criteria

- Criteria | Structured Finance | General: Global Framework For Payment Structure And CashFlow Analysis Of Structured Finance Securities, Dec. 22, 2020

- Criteria | Structured Finance | Legal: U.S. Structured Finance Asset Isolation AndSpecial-Purpose Entity Criteria, May 15, 2019

- Criteria | Structured Finance | General: Counterparty Risk Framework: Methodology AndAssumptions, March 8, 2019

- Criteria | Structured Finance | General: Incorporating Sovereign Risk In Rating StructuredFinance Securities: Methodology And Assumptions, Jan. 30, 2019

- Criteria | Structured Finance | General: Global Framework For Assessing Operational Risk InStructured Finance Transactions, Oct. 9, 2014

- Criteria | Structured Finance | ABS: Global Methodology And Assumptions For Assessing TheCredit Quality Of Securitized Consumer Receivables, Oct. 9, 2014

- General Criteria: Global Investment Criteria For Temporary Investments In TransactionAccounts, May 31, 2012

- General Criteria: Principles Of Credit Ratings, Feb. 16, 2011

- Criteria | Structured Finance | General: Methodology For Servicer Risk Assessment, May 28,2009

Related Research

- Economic Outlook U.S. Q4 2021: The Rocket Is Leveling Off, Sept. 23, 2021

- U.S. Real-Time Data: The Economy Hits A Speed Bump, Sept. 13, 2021

- U.S. Real-Time Data: Consumers Are Wary Of A COVID Resurgence Amid A Recovering LaborMarket, Aug. 134, 2021

- U.S. Biweekly Economic Roundup: A Medal Performance for Jobs Eases Fears About ASlowdown In The Recovery, Aug. 6, 2021

- Economic Research: The Financial Fragility Of U.S. Households And Businesses Hit A DecadeLow In The First Quarter, July 30, 2021

- Three Ratings Raised And One Affirmed From OneMain Direct Auto Receivables Trust 2018-1,July 30, 2021

- U.S. Real-Time Data: Growth Is Still On Track Despite Rising COVID-19 Cases, July 23, 2021

www.standardandpoors.com October 5, 2021 17

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

- U.S. Biweekly Economic Roundup: Auto Sector Problems Leave Imprints Throughout MajorEconomic Data, July 16, 2021

- U.S. Real-Time Data: In A Sweet Spot, July 9, 2021

- Auto Loan ABS COVID-19 Loss Adjustment Reassessed After Better-Than-ExpectedPerformance, July 8, 2021

- Economic Outlook U.S. Q3 2021: Sun, Sun, Sun, Here It Comes, June 24, 2021

- U.S. Real-Time Data: Job And Mobility Trends Improve As Rising Prices Dampen ConsumerEnthusiasm, June 12, 2021

- U.S. Biweekly Economic Roundup: A Long Way Back To Full Employment, June 4, 2021

- OneMain Holdings Inc., March 30, 2021

- S&P Global Ratings Definitions, Jan. 5, 2021

www.standardandpoors.com October 5, 2021 18

© S&P Global Ratings. All rights reserved. No reprint or dissemination without S&P Global Ratings' permission. See Terms of Use/Disclaimeron the last page.

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1

S&P may receive compensation for its ratings and certain credit-related analyses, normally from issuers or underwriters of securities or from obligors.S&P reserves the right to disseminate its opinions and analyses. S&P's public ratings and analyses are made available on its Web sites,www.standardandpoors.com (free of charge), and www.ratingsdirect.com and www.globalcreditportal.com (subscription), and may be distributedthrough other means, including via S&P publications and third-party redistributors. Additional information about our ratings fees is available atwww.standardandpoors.com/usratingsfees.

S&P keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respectiveactivities. As a result, certain business units of S&P may have information that is not available to other S&P business units. S&P has establishedpolicies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed andnot statements of fact. S&P's opinions, analyses and rating acknowledgment decisions (described below) are not recommendations to purchase,hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P assumes no obligation toupdate the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment andexperience of the user, its management, employees, advisors and/or clients when making investment and other business decisions. S&P does not actas a fiduciary or an investment advisor except where registered as such. While S&P has obtained information from sources it believes to be reliable,S&P does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-relatedpublications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limitedto, the publication of a periodic update on a credit rating and related analyses.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certainregulatory purposes, S&P reserves the right to assign, withdraw or suspend such acknowledgment at any time and in its sole discretion. S&P Partiesdisclaim any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damagealleged to have been suffered on account thereof.

Copyright © 2021 Standard & Poor's Financial Services LLC. All rights reserved.

No content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any partthereof (Content) may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrievalsystem, without the prior written permission of Standard & Poor's Financial Services LLC or its affiliates (collectively, S&P). The Content shall not beused for any unlawful or unauthorized purposes. S&P and any third-party providers, as well as their directors, officers, shareholders, employees oragents (collectively S&P Parties) do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are notresponsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or forthe security or maintenance of any data input by the user. The Content is provided on an “as is” basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESSOR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE ORUSE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THECONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct,indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, withoutlimitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advisedof the possibility of such damages.

Standard & Poor’s | Research | October 5, 2021 19

2732523

Presale: OneMain Direct Auto Receivables Trust 2021-1