Oklahoma State University Oil & Gas Accounting Conference Nov. 16, 2007 Reserves Estimation in...

74

Oklahoma State University Oklahoma State University Oil & Gas Accounting Conference Oil & Gas Accounting Conference Nov. 16, 2007 Nov. 16, 2007 Reserves Estimation in Reserves Estimation in Accounting and Reporting Accounting and Reporting presented by presented by Don Roesle, Chairman and CEO Don Roesle, Chairman and CEO Ryder Scott Company, L.P. Ryder Scott Company, L.P. www.ryderscott.com www.ryderscott.com

-

Upload

alexandrina-lucas -

Category

Documents

-

view

216 -

download

0

Transcript of Oklahoma State University Oil & Gas Accounting Conference Nov. 16, 2007 Reserves Estimation in...

Oklahoma State UniversityOklahoma State University Oil & Gas Accounting Conference Oil & Gas Accounting Conference

Nov. 16, 2007Nov. 16, 2007

Reserves Estimation in Reserves Estimation in Accounting and ReportingAccounting and Reporting

presented bypresented byDon Roesle, Chairman and CEODon Roesle, Chairman and CEO

Ryder Scott Company, L.P.Ryder Scott Company, L.P.www.ryderscott.comwww.ryderscott.com

Discussion OutlineDiscussion Outline

SEC Compliant ReportSEC Compliant Report Validating a Reserve ReportValidating a Reserve Report SEC Comment LettersSEC Comment Letters SEC Hot Button IssuesSEC Hot Button Issues

The information presented hereinrepresents informed opinions about U.S. SEC

reserves reporting regulations but does not purportto be identical to advice to be obtained from the SEC.

This presentation is offered for information purposes only.

Ryder Scott assumes no liabilityfor the use (or misuse)

of the presented materials.

What does the United States What does the United States Securities and Exchange Securities and Exchange

Commission (SEC) expect in a Commission (SEC) expect in a 10-K Reserves filing?10-K Reserves filing?

SEC 1978SEC 1978 Proved oil and gas reserves are the estimated Proved oil and gas reserves are the estimated

quantities of crude oil, natural gas, and natural gas quantities of crude oil, natural gas, and natural gas liquids which geological and engineering data liquids which geological and engineering data demonstrate with demonstrate with reasonable certaintyreasonable certainty to be to be recoverable in future years from known reservoirs recoverable in future years from known reservoirs under existing economic and operating conditions, under existing economic and operating conditions, i.e., prices and cost as of the date the estimate is i.e., prices and cost as of the date the estimate is made.made.

SPE/WPC 1997 SPE/WPC 1997 Proved reserves are those quantities of petroleum Proved reserves are those quantities of petroleum

which, by analysis of geological and engineering which, by analysis of geological and engineering data, can be estimated with data, can be estimated with reasonable certaintyreasonable certainty to to be commercially recoverable, from a given date be commercially recoverable, from a given date forward, from known reservoirs and under economic forward, from known reservoirs and under economic condition, operating methods, and government condition, operating methods, and government regulations.regulations.

RESERVES DEFINITIONS

SEC GuidelinesSEC Guidelines

“Reasonable Certainty”“Reasonable Certainty” ““The concept of reasonable certainty The concept of reasonable certainty

implies that, as more technical data implies that, as more technical data becomes available, a positive, or becomes available, a positive, or upward, revision is much more likely upward, revision is much more likely than a negative, or downward, than a negative, or downward, revision.”revision.”

SEC GuidelinesSEC Guidelines

Reasonable Certainty RequirementsReasonable Certainty Requirements

Generated by supporting geological and Generated by supporting geological and engineering data.engineering data.

Validation of assumptions are necessary.Validation of assumptions are necessary. Criteria for analogies should be equal to or better Criteria for analogies should be equal to or better

than referenced reservoirs used as analogies.than referenced reservoirs used as analogies. Reasonable certainty is more than just the Reasonable certainty is more than just the

technical considerations that oil and gas is technical considerations that oil and gas is recoverable. It also includes resolution of how recoverable. It also includes resolution of how other barriers such as financial, environmental, other barriers such as financial, environmental, marketing, legal and political will be overcomemarketing, legal and political will be overcome..

What is a SEC “compliant report”?What is a SEC “compliant report”?

An estimate of the reserves and future An estimate of the reserves and future revenues using “existing economic and revenues using “existing economic and operating conditions” (12/31 prices and operating conditions” (12/31 prices and costs).costs).

Recoverable from “known reservoirs” to a Recoverable from “known reservoirs” to a level of “reasonable certainty”.level of “reasonable certainty”.

Revenues limited to that from sale of Revenues limited to that from sale of produced hydrocarbons and not produced hydrocarbons and not associated income from sulphur, CO2, associated income from sulphur, CO2, processing fees, platform rentals, etc.processing fees, platform rentals, etc.

Limited reliance upon 3-D seismic and Limited reliance upon 3-D seismic and other new technology.other new technology.

How does SEC assure that How does SEC assure that companies are in compliance?companies are in compliance?

SEC Review ProcessSEC Review Process

In recent years, the engineering staff In recent years, the engineering staff issues “comment letters” initially asking issues “comment letters” initially asking generic type questions about many issues, generic type questions about many issues, including PUDs, pricing, reliance upon including PUDs, pricing, reliance upon third-party firms, reserves-linked third-party firms, reserves-linked performance bonuses, recovery factors performance bonuses, recovery factors and other matters.and other matters.

How does SEC assure that How does SEC assure that companies are in compliance?companies are in compliance?

SEC Review ProcessSEC Review Process

Upon producer response, SEC then narrows Upon producer response, SEC then narrows remaining relevant questions to specific remaining relevant questions to specific properties and may ask for maps and other properties and may ask for maps and other supporting documentation.supporting documentation.

May result in iteration of several letters back May result in iteration of several letters back and forth until SEC is satisfied or asks producer and forth until SEC is satisfied or asks producer to make modifications (Debooking or to make modifications (Debooking or Restatement)Restatement)

SEC terms related to reserves SEC terms related to reserves compliancecompliance

““De-booking” typically results from SEC De-booking” typically results from SEC request to remove certain reserves from the request to remove certain reserves from the next annual reserves filing. Rather common next annual reserves filing. Rather common but is not typically publicized if the issuer but is not typically publicized if the issuer voluntarily complies in the next annual 10-K voluntarily complies in the next annual 10-K filing.filing.

““Restatement” is a much more serious result, Restatement” is a much more serious result, particularly under SOX, as it requires the particularly under SOX, as it requires the issuer to retroactively “correct” past reserves issuer to retroactively “correct” past reserves disclosures and recalculate earnings.disclosures and recalculate earnings.

U.S. Department of Justice (DOJ) will probably U.S. Department of Justice (DOJ) will probably be involved in any investigation that be involved in any investigation that subsequently leads to a reserves subsequently leads to a reserves restatement.restatement.

What May Cause a Reserves Audit by SECWhat May Cause a Reserves Audit by SEC

Reasons for a Reserves Audits by SEC:Reasons for a Reserves Audits by SEC: History of downward reductions History of downward reductions By press releasesBy press releases Response to Comment LetterResponse to Comment Letter Annual reports that don’t conform to press Annual reports that don’t conform to press

releasesreleases Partner Activity, press releases, or revisions Partner Activity, press releases, or revisions A history of SEC infractionsA history of SEC infractions Negative publicityNegative publicity The Calendar – Every 3 yearsThe Calendar – Every 3 years Unusual Stock Volume or MovementUnusual Stock Volume or Movement ““Whistle blowers” orWhistle blowers” or for several other reasons.for several other reasons.

Reserves TerminologyReserves Terminology

Reviews - Audits - DeterminationsReviews - Audits - Determinations

Two typical types of reviewsTwo typical types of reviews Process review Process review is an analysis of the is an analysis of the

process and procedures established to process and procedures established to ensure that reserves have been estimated ensure that reserves have been estimated using industry accepted practices and in using industry accepted practices and in compliance with relevant standards. May compliance with relevant standards. May involve qualifications and independence of involve qualifications and independence of internal reserves evaluators and auditors. internal reserves evaluators and auditors. Does not address reserves Does not address reserves quantitiesquantities

Reserves reviewReserves review is more typically a is more typically a cursory investigation of client-selected cursory investigation of client-selected properties for various client purposes.properties for various client purposes.

Reserves auditReserves audit A rA reserves audit eserves audit is an examination of the is an examination of the

work of others for the purpose of work of others for the purpose of expressing an opinion that a reserves expressing an opinion that a reserves report is reasonable report is reasonable in the aggregate in the aggregate and and generally conforms to accepted generally conforms to accepted engineering and geological principals and engineering and geological principals and relevant reserves definitions.relevant reserves definitions.

May include all or a portion of the May include all or a portion of the properties of an entity.properties of an entity.

Acceptable tolerances usually within 5 to Acceptable tolerances usually within 5 to 10 percent.10 percent.

May include reserves, production forecasts May include reserves, production forecasts and/or economics.and/or economics.

Reserves determination (reserves report)Reserves determination (reserves report)

A A reserves report reserves report is a “grass roots” is a “grass roots” evaluation in which an evaluator has evaluation in which an evaluator has examined and evaluated all available source examined and evaluated all available source data for the purpose of producing an data for the purpose of producing an independent estimate of reserves and independent estimate of reserves and reserves information in full compliance with reserves information in full compliance with the relevant reserves definitions.the relevant reserves definitions.

Includes projections of production, revenues, Includes projections of production, revenues, costs ( Capex, Opex, Taxes, Abandonment ) costs ( Capex, Opex, Taxes, Abandonment ) and future net income discounted at 10%.and future net income discounted at 10%.

A reserves report may be internally or A reserves report may be internally or externally prepared.externally prepared.

Creation of “auditable” data and Creation of “auditable” data and workproduct filesworkproduct files

Personnel should be trained in industry Personnel should be trained in industry “best practices” regarding (1) acceptable “best practices” regarding (1) acceptable geological interpretations and reservoir geological interpretations and reservoir description (2) basic understanding of description (2) basic understanding of reservoir mechanics and fluid flow (3) reservoir mechanics and fluid flow (3) comprehension of pertinent reserves comprehension of pertinent reserves definitions and (4) ethics.definitions and (4) ethics.

Evaluators should establish “real time” Evaluators should establish “real time” access to data from employer-operated access to data from employer-operated properties and “ASAP” data from partner-properties and “ASAP” data from partner-operated assets.operated assets.

Creation of “auditable” data and workproduct filesCreation of “auditable” data and workproduct files

Partners should be wary of accepting operator-supplied Partners should be wary of accepting operator-supplied reserves estimates.reserves estimates.

Attention must be given to documentation of all Attention must be given to documentation of all interpretative data steps, including narrative descriptions of interpretative data steps, including narrative descriptions of critical decisions.critical decisions.

All data and information related to a reserves report, All data and information related to a reserves report, including geological maps, must be archived in a form that including geological maps, must be archived in a form that can be accessed and reviewed by authorized parties at any can be accessed and reviewed by authorized parties at any time. time.

General Reserves DeterminationGeneral Reserves DeterminationProblems Identified by the SECProblems Identified by the SEC

Some abuses of the proved classification (in no particular order)Some abuses of the proved classification (in no particular order) Spacing violations for PUDsSpacing violations for PUDs PUDs which are too optimistic based on supporting dataPUDs which are too optimistic based on supporting data Seismic amplitudes for down dip limitsSeismic amplitudes for down dip limits Use of non-hydrocarbon revenue streamsUse of non-hydrocarbon revenue streams Misuse of reservoir simulation resultsMisuse of reservoir simulation results Field level decline curve analysisField level decline curve analysis Declining operating costs with declining well countDeclining operating costs with declining well count Allocation of development costs to probable category to Allocation of development costs to probable category to justify proved reserves economicsjustify proved reserves economics Justification of proved reserves by analogy with non-analogous Justification of proved reserves by analogy with non-analogous properties properties Misuse of statistical analysisMisuse of statistical analysis Reserves being declared proved when no sales market existsReserves being declared proved when no sales market exists Scheduling of reserves which extend beyond the term of Scheduling of reserves which extend beyond the term of foreign concessions foreign concessions

Validating a Reserve Report

Series of questions that should be askedto help assess the degreeof reserve risk associated

with a company’s reservesand their reserve report.

Who did the underlying reserve evaluation?

internal engineeringor

independent engineering firm

1.

Is the independent engineering firm or company engineering staff knowledgeable of

SEC reserve definitions and the appropriate reporting requirement ?

2.

How long has the independent engineering firm been doing the company’s reserves ?

Is the engineering firm familiar with special issues that might be involved with the company’s properties ?

3.

4.

Where are the reserves located ?

How knowledgeable is the company of the areas where the reserves are located ?

Are they in an area where assessment of reserves carries greater risk(I.e. Gulf Coast vs. Mid-Continent) ?

Are the reserves concentrated in specific areas, or are they widely scattered (I.e. do they have core areas of competency) ?

Are the reserves in areas that require higher operating and development costs (I.e. profit margin is smaller and expenditure demands are higher

on the company) ?

Are the reserves in areas that are environmentally very sensitive ?

Are the reserves all domestic,or do they include international properties ?

5.

Is the independent engineering firm familiar with the areas where the reserves are located ?

6.

Does the independent engineering firm look at all of the company reserves or just a

percentage ?

Does the engineering firm do a detailed studyor an audit ?

7.

Are the company’s reserves concentrated in a small number of properties, or is the portfolio

of properties more diverse ?

What type of interest position does the company hold in its different properties ?

8.

Are the reserves mature,or relatively new with minimal production ?

Is the reserve analysis primarily based on performance methods or volumetrics ?

Are the reserves strictly primary, or do they include secondary and EOR projects ?

9.

Are most of the properties operatedor non-operated ?

If a high percentage of the company’s reserves are non-operated, what is known about the operators ?

Are the various operators substantial from a technical and business standpoint ?

Do the operators have an established track recordof operations in the areas where the

reserves are located ?

10.

What is the breakdown on proved reserve status categories

(I.e. producing, shut-in, behind pipe and undeveloped) ?

Are the reserves fairly well split between categories, or is there a high percentage in the non-producing and

particularly in the undeveloped ?

11.

What kind of reserve life index is there for the proved producing reserves ?

Is this realistic for the type of proved producing reserves stated in the SEC filing ?

Is this realistic taking into account the current production of the company ?

12.

What kind of reserve life index is there for the total proved reserves ?

What level of producing rates will have to be added by non-producing and undeveloped reserves to make a

reasonable life index ?

Does this seem attainable for the types ofreserves involved ?

13.

Are the reported reserves based on the appropriate economic parameters

as specified by theSecurities and Exchange Commission ?

Did the reserve appraiser use currenteconomic conditions ?

14.

Historical Checks

Do future revenue projections appear reasonable considering recent historical

company revenues ?

15.Historical Checks

Do future cost projections appear reasonable considering recent historical company

expenditures ?

Have the appropriate operating costs been applied againstthe reserve projections ?

Does the company have sufficient cashflow to carry their burden of operating costs and service other necessary company expenditures ?

Have sufficient development costs been included to develop the stated non-producing and undeveloped reserves ?

Does the company have an established track record and the financial stability to spend the amounts of capital dollars

necessary to fund the development ?

16.Company Performance

How does the company look over the years in regards to “revisions of previous estimates” ?

Have the revisions consistently been significantin size in relation to the company’s base reserves ?

Are the revisions consistently negative ?

Are the negative revisions consistently associatedwith the non-producing and undeveloped

reserve categories ?

17.Company Performance

“Extensions, discoveries, other additions”are an indicator of how well the company is moving proved undeveloped and probable reserves into the developed reserve base

of the company.Is the company historically demonstrating an

ability to do so ?

How well is the company finding new reserves through the drill bit ?

Does the company have an active exploration and development drilling program ?

Does the company have a good acreage position around its developing properties ?

What kind of exploratory acreage position does the company hold ?

18.Company Performance

Does the company typically grow through acquisitions or the drill bit ?Is there a good mix of both ?

Does “purchase of reserves in place” contribute significantly to the company’s reserve base ?

If the company traditionally grows through acquisitions, is the company paying an appropriate

amount for reserves ?

Could too much success with competitive bids mean they are over-paying for the reserves ?

19.

Company Performance

Does the company “sell reserves in place”to divest themselves

of non-strategic reserves ?

Is the company burdened with a large number of low margin wells in non-core areas ?

20.

How recent is the reserve evaluationthat is the source of the company’s reserves

in the public filing ?

Based on the answers to some of the previous questions, are the reserves of a nature

that significant changes in reserve quantities can occur over a limited period of time ?

Is the reserve evaluation a recent study or a prior study that has been mechanically adjusted to a

specific as-of date for public reporting purposes ?

SEC Comment & Audit LettersSEC Comment & Audit Letters A series of questions posed by accountants, lawyers, A series of questions posed by accountants, lawyers,

and engineers designed to test the compliance of the and engineers designed to test the compliance of the company with SEC regulations regarding technical and company with SEC regulations regarding technical and commercial issues.commercial issues.

The first producer answers are typically followed by a The first producer answers are typically followed by a shorter list of questions, which typically are more shorter list of questions, which typically are more specific and ask for more detail. SEC may request specific and ask for more detail. SEC may request maps, logs, test data, copies of contracts, market maps, logs, test data, copies of contracts, market studies, etc.studies, etc.

Iteration of letters may lead to request to restate Iteration of letters may lead to request to restate previous filings, "de-booking" of reserves in previous filings, "de-booking" of reserves in subsequent reports or, simply, no more letters.subsequent reports or, simply, no more letters.

Most favorable response from SEC is “ We have no Most favorable response from SEC is “ We have no more questions at this time”.more questions at this time”.

SEC Comment & Audit LettersSEC Comment & Audit Letters

Typical SEC Staff questionTypical SEC Staff question : :

Please inform us of Please inform us of anyany circumstance circumstance where you have reported proved where you have reported proved reserves located structurally reserves located structurally below the below the lowest-knownlowest-known hydrocarbons as hydrocarbons as established through well logsestablished through well logs and if and if these additional reserves have not been these additional reserves have not been confirmed through performance history.confirmed through performance history.

SEC Comment & Audit LettersSEC Comment & Audit Letters

Another question may be:Another question may be:

Please inform us of any circumstances Please inform us of any circumstances where your reported reserves and future where your reported reserves and future income were estimated using prices income were estimated using prices other than those in effect on the last day other than those in effect on the last day of the year. of the year.

SEC Comment & Audit LettersSEC Comment & Audit Letters

Another common question asksAnother common question asks::

Have you reported Have you reported anyany undeveloped undeveloped reserves attributable to well locations reserves attributable to well locations more than one offset locationmore than one offset location (“legal (“legal location”) away from a commercial well?location”) away from a commercial well?

SEC Comment & Audit LettersSEC Comment & Audit Letters

A recent letter also posed the A recent letter also posed the followingfollowing::

Are Are performance bonusesperformance bonuses linked to linked to reserves increases?reserves increases?

SEC Comment & Audit LettersSEC Comment & Audit Letters

In the same letter:In the same letter:

Who has the authority to engage third Who has the authority to engage third party engineers and who do they report party engineers and who do they report to?to?

SEC Comment & Audit LettersSEC Comment & Audit Letters

Interesting Questions – One recent SEC Interesting Questions – One recent SEC comment letter asked for the following:comment letter asked for the following:

Identify all independent engineering firms used Identify all independent engineering firms used over last 5 years.over last 5 years.

What properties were reviewed?What properties were reviewed?

How much the firms were paid for work on How much the firms were paid for work on projects other than year-end type work?projects other than year-end type work?

If the firms were discharged, reason(s) why?If the firms were discharged, reason(s) why?

SEC Comment & Audit LettersSEC Comment & Audit Letters

Another common question asksAnother common question asks::

Have you reported proved reserves in Have you reported proved reserves in untesteduntested fault blocks, structures, or fault blocks, structures, or seismic amplitudes?seismic amplitudes?

(Untested here refers to the drilling of a (Untested here refers to the drilling of a well confirming presence of oil and/or well confirming presence of oil and/or gas)gas)

SEC Comment & Audit LettersSEC Comment & Audit Letters

November 9November 9thth, 2004, the SEC sent a 9 page, 23 , 2004, the SEC sent a 9 page, 23 question inquiry to an independent US oil companyquestion inquiry to an independent US oil company

Among other items, the SEC asked for:Among other items, the SEC asked for:

A one line summary for each proved reserve entry on the A one line summary for each proved reserve entry on the books as of 12/31/2002 and 12/31/2003books as of 12/31/2002 and 12/31/2003

Narratives, engineering and geological exhibits for the Narratives, engineering and geological exhibits for the three largest reserve extensions or discoveries during three largest reserve extensions or discoveries during 20032003

SEC Comment & Audit LettersSEC Comment & Audit Letters

Hindsight analysis of 5 largest PUD locations Hindsight analysis of 5 largest PUD locations booked as of 12/31/2002 drilled during 2003booked as of 12/31/2002 drilled during 2003

““Include the engineering and geological Include the engineering and geological exhibits used to justify the reserve booking at exhibits used to justify the reserve booking at each year end and a brief narrative reconciling each year end and a brief narrative reconciling the differences between the two estimates.”the differences between the two estimates.”

““Address corporate methodology for Address corporate methodology for eliminating future discrepancies between the eliminating future discrepancies between the estimates”estimates”

SEC Comment & Audit LettersSEC Comment & Audit Letters

““Narratives, engineering and geological exhibits for Narratives, engineering and geological exhibits for the 3 largest reserve revisions – both positive and the 3 largest reserve revisions – both positive and negative – not caused by economics”negative – not caused by economics”

““Supplementally, tell us all the estimated Supplementally, tell us all the estimated hydrocarbon volumes, if any, you have claimed as hydrocarbon volumes, if any, you have claimed as proved reserves;proved reserves;

A) In undrilled fault blocksA) In undrilled fault blocks B) Below the LKH – penetrated or assessed – B) Below the LKH – penetrated or assessed –

structural occurrence of hydrocarbons”structural occurrence of hydrocarbons”

SEC Comment & Audit LettersSEC Comment & Audit Letters

““For the PUD locations as of 12/31/2002 drilled For the PUD locations as of 12/31/2002 drilled during 2003, provide a comparison table of during 2003, provide a comparison table of projected capital expenditures and actual projected capital expenditures and actual expenditures for each well. Explain any expenditures for each well. Explain any variances over 1%.” (This is not a typo)variances over 1%.” (This is not a typo)

““Prepare a list of the PUD wells as of 12/31/2002 Prepare a list of the PUD wells as of 12/31/2002 projected to be drilled during 2003 but were not projected to be drilled during 2003 but were not drilled. Provide an explanation as to why the drilled. Provide an explanation as to why the wells were not drilled, if they are still carried as wells were not drilled, if they are still carried as PUD locations as of 12/31/2003 and why they PUD locations as of 12/31/2003 and why they still qualify as PUD locations.”still qualify as PUD locations.”

SEC Comment & Audit LettersSEC Comment & Audit Letters

Discuss the internal controls you have in Discuss the internal controls you have in place to assure consistency and conservatism place to assure consistency and conservatism in your proved reserve estimations.in your proved reserve estimations.

Discuss how the effectiveness of these Discuss how the effectiveness of these controls is reflected in your history of proved controls is reflected in your history of proved reserve revisions over the past 3 yearsreserve revisions over the past 3 years

Identify the personnel in your company who Identify the personnel in your company who have final authority over your proved have final authority over your proved reservesreserves

SEC Red Flags and Hot Button TopicsSEC Red Flags and Hot Button Topics

Technical IssuesTechnical Issues Validation of proved undeveloped locations (PUDS)Validation of proved undeveloped locations (PUDS) Proper use of analogiesProper use of analogies Determination of down dip limits/LKHDetermination of down dip limits/LKH Application of seismic interpretationsApplication of seismic interpretations Recovery factorsRecovery factors Application of reservoir simulationApplication of reservoir simulation Flow testing/Data comprising a conclusive formation testFlow testing/Data comprising a conclusive formation test Undrilled fault blocks Undrilled fault blocks • Commercial IssuesCommercial Issues SEC year-end pricingSEC year-end pricing Costs – Capex and OpexCosts – Capex and Opex Non-hydrocarbon revenuesNon-hydrocarbon revenues Financial commitment to develop/project stagnationFinancial commitment to develop/project stagnation Project sanctioningProject sanctioning Commerciality – lack of marketCommerciality – lack of market Booking under PSC’SBooking under PSC’S

A) SEC year-end pricingA) SEC year-end pricing SPE/WPC – allow some latitude, average SPE/WPC – allow some latitude, average

period OKperiod OK SEC – no interpretation. Must use price on SEC – no interpretation. Must use price on

effective dateeffective date SEC position reflects its dated origins (1978)SEC position reflects its dated origins (1978)

A time with less volatility in O&G marketsA time with less volatility in O&G markets Now O&G sold on spot marketsNow O&G sold on spot markets

Year-end price to be used for rev. projections Year-end price to be used for rev. projections and economic limitsand economic limits

Can lead to abnormally high (or low) economic Can lead to abnormally high (or low) economic well liveswell lives

SEC HOT-BUTTON TOPICS

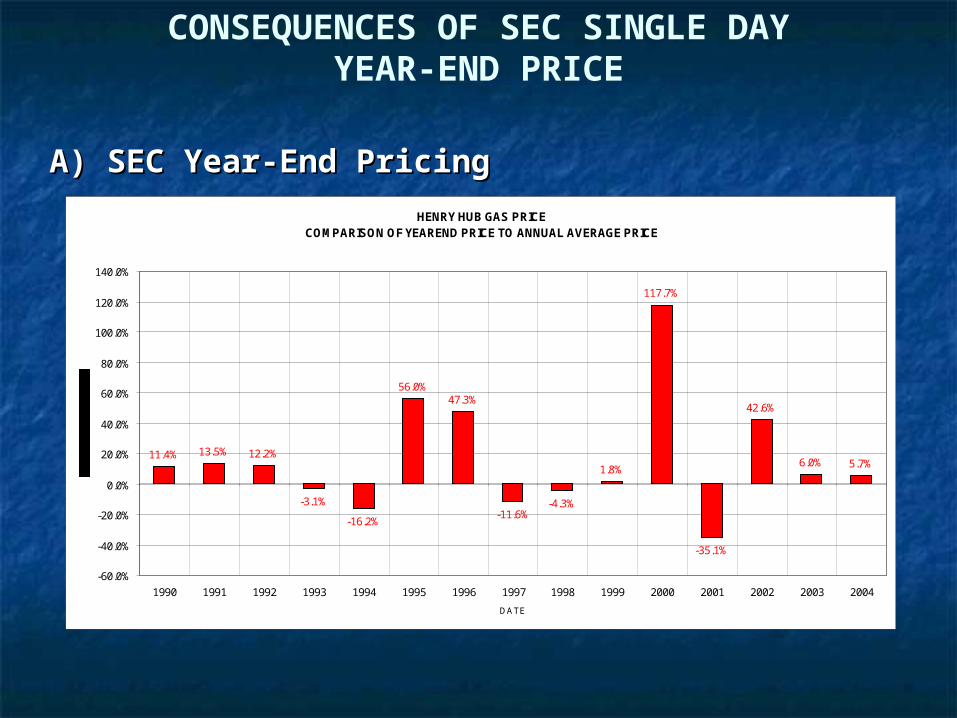

CONSEQUENCES OF SEC SINGLE DAYYEAR-END PRICE

WTI OIL PRICESCOMPARISON OF YEAREND PRICE TO ANNUAL AVERAGE PRICE

16.8%

-12.3%

-4.1%

-24.7%

3.9%7.2%

17.8%

-15.2% -16.3%

33.5%

-11.5%

-23.7%

23.3%

4.5% 4.8%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

DATE

A) SEC Year-End PricingA) SEC Year-End Pricing

A) SEC Year-End PricingA) SEC Year-End Pricing

CONSEQUENCES OF SEC SINGLE DAYYEAR-END PRICE

HENRY HUB GAS PRICECOMPARISON OF YEAREND PRICE TO ANNUAL AVERAGE PRICE

11.4% 13.5% 12.2%

-3.1%

-16.2%

56.0%47.3%

-11.6%-4.3%

1.8%

117.7%

-35.1%

42.6%

6.0% 5.7%

-60.0%

-40.0%

-20.0%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

DATE

B) Recovery factorsB) Recovery factors

SEC increasing scrutinySEC increasing scrutiny

Staff pressing for hard evidence for recovery Staff pressing for hard evidence for recovery factor’s higher than low-side of rangefactor’s higher than low-side of range

May ask for supporting documentation of May ask for supporting documentation of assumptionsassumptions

Examples: Examples: water drive for oilwater drive for oil absence of water drive for gasabsence of water drive for gas

SEC HOT-BUTTON TOPICS

C) PUD’sC) PUD’s

One offset “rule” (regulatory spacing)One offset “rule” (regulatory spacing)

Website – “certainty” beyond one locationWebsite – “certainty” beyond one location

Rule also applies to CBMRule also applies to CBM

Large percentage of PUDsLarge percentage of PUDs

““Stale” PUDsStale” PUDs

PUDs remain undrilledPUDs remain undrilled

Analogy for PUDs no longer valid Analogy for PUDs no longer valid

SEC HOT-BUTTON TOPICS

D) Reliance upon seismic interpretationsD) Reliance upon seismic interpretations

Historically SEC has dismissed as too uncertain for Historically SEC has dismissed as too uncertain for proved reservesproved reserves

Extension of lowest known hydrocarbonsExtension of lowest known hydrocarbons Proving up nearby untested analog structuresProving up nearby untested analog structures

SEC HOT-BUTTON TOPICS

E) Booking reserves under PSC’sE) Booking reserves under PSC’s

Necessary ElementsNecessary Elements Right to develop and extractRight to develop and extract Reasonable certainty of productionReasonable certainty of production Intent and commitment to developIntent and commitment to develop Capital at riskCapital at risk Legal right to produce at the date of the estimateLegal right to produce at the date of the estimate

SEC Position – after foreign government declaration of SEC Position – after foreign government declaration of commerciality or government approval of development plancommerciality or government approval of development plan

Exceptions if “Compelling Case” made to SECExceptions if “Compelling Case” made to SEC

SEC HOT-BUTTON TOPICS

F) Determination of LKH – SEC - well logs onlyF) Determination of LKH – SEC - well logs only

SEC position can lead to significant differences SEC position can lead to significant differences relative to SPE/WPC reservesrelative to SPE/WPC reserves

Reversal of 2000 SPEE forum position – “compelling Reversal of 2000 SPEE forum position – “compelling case”case”

SEC HOT-BUTTON TOPICS

Determination of lowest-known hydrocarbonsDetermination of lowest-known hydrocarbons

SPE and SEC definitions read similarlySPE and SEC definitions read similarly

SEC – “SEC – “in the absence of information on fluid in the absence of information on fluid contacts, the lowest known structural occurrence contacts, the lowest known structural occurrence of hydrocarbons control the lower proved limit of of hydrocarbons control the lower proved limit of the reservoirthe reservoir.”.”

SPE – “SPE – “lowest known occurrence of hydrocarbons lowest known occurrence of hydrocarbons controls the proved limit unless otherwise controls the proved limit unless otherwise indicated by definitive geological, engineering or indicated by definitive geological, engineering or performance dataperformance data.”.”

SIGNIFICANT DIFFERENCES IN SEC ANDSPE / WPC RESERVES DEFINITIONS

Determination of Lowest-Known Determination of Lowest-Known HydrocarbonsHydrocarbons

Well A Well B

O = 31.1%K = 1100 md LKO Log

SPE Proved VolumeIncrement

OWC (RFT)

Reservoir cross section through wells A and B

O = 32.4%K = 1600 md

SIGNIFICANT DIFFERENCES IN SEC ANDSPE / WPC RESERVES DEFINITIONS

Formation Pressures

Wireline test data established

Pressure PSIA

Base of sand

Top of sand

Base of sand

Top of sand

MDT

DepthTVDSS

8100

8200

8300

8400

8500

8600

8700

8800

4880 4920 4960 5000 5040 5080 5120 5160 5200

Well BMDT Pressures

Calculated OWC

Well AMDT Pressures

SIGNIFICANT DIFFERENCES IN SEC ANDSPE / WPC RESERVES DEFINITIONS

Determination of Lowest-Known Determination of Lowest-Known HydrocarbonsHydrocarbons

Determination of Lowest-Known Determination of Lowest-Known HydrocarbonsHydrocarbons

SIGNIFICANT DIFFERENCES IN SEC ANDSPE / WPC RESERVES DEFINITIONS

G) Simulation-derived reserves estimatesG) Simulation-derived reserves estimates

Model in-place volumes limited by SECModel in-place volumes limited by SEC

LKH limitationsLKH limitations

Flow test requirementsFlow test requirements

SEC recognizes models often represent expected SEC recognizes models often represent expected casecase

SEC requires “good history match”SEC requires “good history match”

SEC HOT-BUTTON TOPICS

H) Revenue from Sale of Non-HydrocarbonsH) Revenue from Sale of Non-Hydrocarbons

SEC Prohibits All Non-Hydrocarbon Reserves SEC Prohibits All Non-Hydrocarbon Reserves (including Sulphur , CO(including Sulphur , CO22 , and Helium), and Helium)

Third Party Processing Revenue excludedThird Party Processing Revenue excluded

Cannot use non-hydrocarbon income to offset or Cannot use non-hydrocarbon income to offset or reduce operating costsreduce operating costs

SEC HOT-BUTTON TOPICS

I) Flow Test RequirementsI) Flow Test Requirements

SEC – “SEC – “Reserves are considered proved if Reserves are considered proved if economic producibility is supported by either economic producibility is supported by either actual production or conclusive formation test.actual production or conclusive formation test.””

SEC Survey on Booking Practices in GOMSEC Survey on Booking Practices in GOM SEC “Special Project”SEC “Special Project” Inquiry concerning booking proved reserves without Inquiry concerning booking proved reserves without

conventional flow testconventional flow test Addressed in 2002 SPEE Forum with SECAddressed in 2002 SPEE Forum with SEC

SEC HOT-BUTTON TOPICS

I)I) Flow Test RequirementsFlow Test Requirements

Significant Unresolved Issue – SEC Definition of Significant Unresolved Issue – SEC Definition of ““conclusive formation testconclusive formation test” ”

In certain areas- GOM -not seen as necessary or feasibleIn certain areas- GOM -not seen as necessary or feasible

Producers reasons for no flow test in deepwater GOMProducers reasons for no flow test in deepwater GOM Redundancy to calculated test ratesRedundancy to calculated test rates Costs often exceed $10MMCosts often exceed $10MM Delays of up to two yearsDelays of up to two years Environmental concerns and permitting requirementsEnvironmental concerns and permitting requirements

SEC HOT-BUTTON TOPICS

I)I) Flow Test RequirementsFlow Test Requirements Potential Impact of SEC Decision – If Position EnforcedPotential Impact of SEC Decision – If Position Enforced

Producers will be required to under report reservesProducers will be required to under report reserves Impact will be greater on smaller independentsImpact will be greater on smaller independents SEC’s mandate of full disclosure may not be metSEC’s mandate of full disclosure may not be met

Deepwater GOM rulingDeepwater GOM ruling

Collaboration of logs, cores, seismic and MDTs Collaboration of logs, cores, seismic and MDTs

SEC HOT-BUTTON TOPICS

J) Net Profits Interest (NPI)J) Net Profits Interest (NPI)

For properties subject to payment of net profits, For properties subject to payment of net profits, SEC requires property owner to deduct NPI SEC requires property owner to deduct NPI “reserves” from owned reserves“reserves” from owned reserves

SPE/WPC definitions – silent, but tradition SPE/WPC definitions – silent, but tradition considers NPI’s to be financial transaction without considers NPI’s to be financial transaction without reserves ownershipreserves ownership

SEC HOT-BUTTON TOPICS

What’s on the HorizonWhat’s on the Horizon SPE is revising its petroleum reserves definitions and will SPE is revising its petroleum reserves definitions and will

issue new ones in 2006-2007.issue new ones in 2006-2007. The United Nations has integrated the SPE/World The United Nations has integrated the SPE/World

Petroleum Congress reserves definitions into its Petroleum Congress reserves definitions into its framework with an aim to fully align both.framework with an aim to fully align both.

SPE is working with the International Accounting SPE is working with the International Accounting Standards Board and other organizations, including the Standards Board and other organizations, including the UN, to ensure the adequacy of reserves standards.UN, to ensure the adequacy of reserves standards.

The IASB and FASB have agreed to work towards the The IASB and FASB have agreed to work towards the convergence of existing U.S. and international financial convergence of existing U.S. and international financial accounting practices and the joint development of future accounting practices and the joint development of future standards.standards.

According to Roger Schwall, assistant director for the According to Roger Schwall, assistant director for the Division of Corporate Finance - the SEC has no current Division of Corporate Finance - the SEC has no current plans to change their definitions or guidelines.plans to change their definitions or guidelines.

Thank You for ListeningThank You for Listening