October 10, 2017 Rating matrix General Insurance...

19

October 10, 2017 IPO Review ICICI Securities Ltd | Retail Equity Research GIC Re is the largest reinsurance company in India in terms of gross premiums accepted in FY17, and accounted for ~60% of premium ceded by Indian insurers to reinsurers. In addition, the company’s international business accounted for ~30.53% of premium in FY17. According to Crisil Research, GIC Re was ranked 12th largest global reinsurer in 2016 and third largest Asian reinsurer in 2015, in terms of gross premiums accepted. The company provides reinsurance across many key business lines including fire (property), marine, motor, engineering, agriculture, aviation/space, health, liability, credit and financial and life insurance. In FY17, GIC Re had gross premium of | 33741 crore with PAT (on a restated consolidated basis) at | 3140.62 crore. Net worth (including fair value change account) was at | 49550.84 crore. Capital position remains strong with solvency ratio at 183% as on June 30, 2017, against minimum statutory requirement of 150%. As on June 30, 2017, GIC Re Indian investment assets (on a standalone restated basis) had a carrying value of | 41929.85 crore and fair value of | 73902.56 crore. Key business aspects Leader in Indian reinsurance industry GIC Re is the largest Indian reinsurance company in terms of gross premium accepted in FY17 and accounts for ~60% of premium ceded by Indian insurers to reinsurers in FY17, according to Crisil Research. As per Crisil research, reinsurance premiums in India are projected to increase at 11-14% CAGR in the next five years to reach | 70000 crore by FY22. As a trusted brand in the Indian market with 44 years of experience, GIC Re is well positioned to take advantage of this growth. Significant global player with growing international presence As on March 31, 2017, along with India, GIC Re underwrote business from ~162 countries. According to Crisil Research, in terms of gross premiums accepted, GIC Re was ranked 12th largest global reinsurer in 2016 and third largest Asian reinsurer in 2015. In FY15-17, GIC Re’s gross premium from international operation grew at 24.8% CAGR to | 10300.5 crore; representing 30.5% of gross premium in FY17. Diversified investment portfolio generating strong growth, attractive yields Indian investment includes fixed income debt securities, equity securities including exchange traded funds, and other investments. As of June 30, 2017, Indian investment assets had a carrying value of | 41929.8 crore and fair value of | 73902.6 crore. In FY17, FY16 and FY15, yields (without unrealised gains) from Indian investment were at 12.35%, 12.91% and 14.08%, respectively. Concerns Catastrophe business may lead to volatile profits Operate in highly competitive environment, no strong entry barriers Substantial increase in agri reinsurance business in recent years Analytic models as tool to evaluate risk is subject to uncertainty Priced at 3.7x P/B (post issue FY17 BV) on higher band At upper end of price band, the stock is available at P/B multiple of 3.7x FY17 BV (post issue core networth). Including change in fair value of investments made in listed equities and MFs (fair value change account), P/B multiple is at ~1.5x FY17 BV. The company does not have a direct listed peer in India. Given fundamental strength, healthy premium growth and healthy return ratios, we advise investors to SUBSCRIBE to the issue. General Insurance Corporation of India Price band | 855-912 Rating matrix Rating : Subscribe (Apply) Issue Details* Issue Opens 11-Oct-17 Issue Closes 13-Oct-17 Issue Size (| Crore) 11372.64 Price Band (|) 855-912 No of Shares on Offer (crore) 12.47 QIB (%) 50 Non-Institutional (%) 15 Retail (%) 35 Minimum lot size (No. of shares) 16 *Discount of | 45 per share for retail individual bidders and to eligible employees Objects of the Issue The offer consists of fresh issue by the company and offer for sale (OFS). The company will not receive any proceeds from the OFS. Proceeds of IPO will be used for augmenting capital base to support business growth and maintain current solvency levels; and general corporate purposes 1997-98 2001-04 2 HUL acquires 23% stake. Shareholding Pattern Pre-Issue Post-Issue Pre-Issue Post-Issue Promoter & promoter group 100.0% 85.8% Public 0.0% 14.2% Financial Summary | Crore FY14 FY15 FY16 FY17 Premiums earned - Net 13616 13595 15338 26375 Income from Investments 983 1302 1436 1638 Total revenue 2696 3098 3269 3799 PAT 2433 2891 2823 3141 Valuation Summary (at | 912; upper price band) (x) FY14 FY15 FY16 Pre Post P/E 32.2 27.1 27.8 25.0 25.5 P/BV 6.2 5.1 4.5 4.0 3.73 Research Analyst Kajal Gandhi [email protected] Vishal Narnolia [email protected] Vasant Lohiya [email protected]

Transcript of October 10, 2017 Rating matrix General Insurance...

October 10, 2017

IPO Review

ICICI Securities Ltd | Retail Equity Research

GIC Re is the largest reinsurance company in India in terms of gross

premiums accepted in FY17, and accounted for ~60% of premium ceded

by Indian insurers to reinsurers. In addition, the company’s international

business accounted for ~30.53% of premium in FY17. According to Crisil

Research, GIC Re was ranked 12th largest global reinsurer in 2016 and

third largest Asian reinsurer in 2015, in terms of gross premiums

accepted. The company provides reinsurance across many key business

lines including fire (property), marine, motor, engineering, agriculture,

aviation/space, health, liability, credit and financial and life insurance.

In FY17, GIC Re had gross premium of | 33741 crore with PAT (on a

restated consolidated basis) at | 3140.62 crore. Net worth (including fair

value change account) was at | 49550.84 crore. Capital position remains

strong with solvency ratio at 183% as on June 30, 2017, against minimum

statutory requirement of 150%. As on June 30, 2017, GIC Re Indian

investment assets (on a standalone restated basis) had a carrying value of

| 41929.85 crore and fair value of | 73902.56 crore.

Key business aspects

Leader in Indian reinsurance industry

GIC Re is the largest Indian reinsurance company in terms of gross

premium accepted in FY17 and accounts for ~60% of premium ceded by

Indian insurers to reinsurers in FY17, according to Crisil Research. As per

Crisil research, reinsurance premiums in India are projected to increase at

11-14% CAGR in the next five years to reach | 70000 crore by FY22. As a

trusted brand in the Indian market with 44 years of experience, GIC Re is

well positioned to take advantage of this growth.

Significant global player with growing international presence

As on March 31, 2017, along with India, GIC Re underwrote business from

~162 countries. According to Crisil Research, in terms of gross premiums

accepted, GIC Re was ranked 12th largest global reinsurer in 2016 and

third largest Asian reinsurer in 2015. In FY15-17, GIC Re’s gross premium

from international operation grew at 24.8% CAGR to | 10300.5 crore;

representing 30.5% of gross premium in FY17.

Diversified investment portfolio generating strong growth, attractive yields

Indian investment includes fixed income debt securities, equity securities

including exchange traded funds, and other investments. As of June 30,

2017, Indian investment assets had a carrying value of | 41929.8 crore

and fair value of | 73902.6 crore. In FY17, FY16 and FY15, yields (without

unrealised gains) from Indian investment were at 12.35%, 12.91% and

14.08%, respectively.

Concerns

Catastrophe business may lead to volatile profits

Operate in highly competitive environment, no strong entry barriers

Substantial increase in agri reinsurance business in recent years

Analytic models as tool to evaluate risk is subject to uncertainty

Priced at 3.7x P/B (post issue FY17 BV) on higher band

At upper end of price band, the stock is available at P/B multiple of 3.7x

FY17 BV (post issue core networth). Including change in fair value of

investments made in listed equities and MFs (fair value change account),

P/B multiple is at ~1.5x FY17 BV. The company does not have a direct

listed peer in India. Given fundamental strength, healthy premium growth

and healthy return ratios, we advise investors to SUBSCRIBE to the issue.

General Insurance Corporation of India

Price band | 855-912

Rating matrix

Rating : Subscribe (Apply)

Issue Details*

Issue Opens 11-Oct-17

Issue Closes 13-Oct-17

Issue Size (| Crore) 11372.64

Price Band (|) 855-912

No of Shares on Offer (crore) 12.47

QIB (%) 50

Non-Institutional (%) 15

Retail (%) 35

Minimum lot size (No. of shares) 16

*Discount of | 45 per share for retail individual bidders and to

eligible employees

Objects of the Issue

The offer consists of fresh issue by the company and offer for sale

(OFS). The company will not receive any proceeds from the OFS.

Proceeds of IPO will be used for augmenting capital base to support

business growth and maintain current solvency levels; and general

corporate purposes

1997-98 2001-04 2006

HUL acquires 23% stake.

Shareholding Pattern Pre-Issue Post-Issue

Pre-Issue Post-Issue

Promoter & promoter group 100.0% 85.8%

Public 0.0% 14.2%

Financial Summary

| Crore FY14 FY15 FY16 FY17

Premiums earned - Net 13616 13595 15338 26375

Income from Investments 983 1302 1436 1638

Total revenue 2696 3098 3269 3799

PAT 2433 2891 2823 3141

Valuation Summary (at | 912; upper price band)

(x) FY14 FY15 FY16 Pre Post

P/E 32.2 27.1 27.8 25.0 25.5

P/BV 6.2 5.1 4.5 4.0 3.73

Research Analyst

Kajal Gandhi

Vishal Narnolia

Vasant Lohiya

Page 2 ICICI Securities Ltd | Retail Equity Research

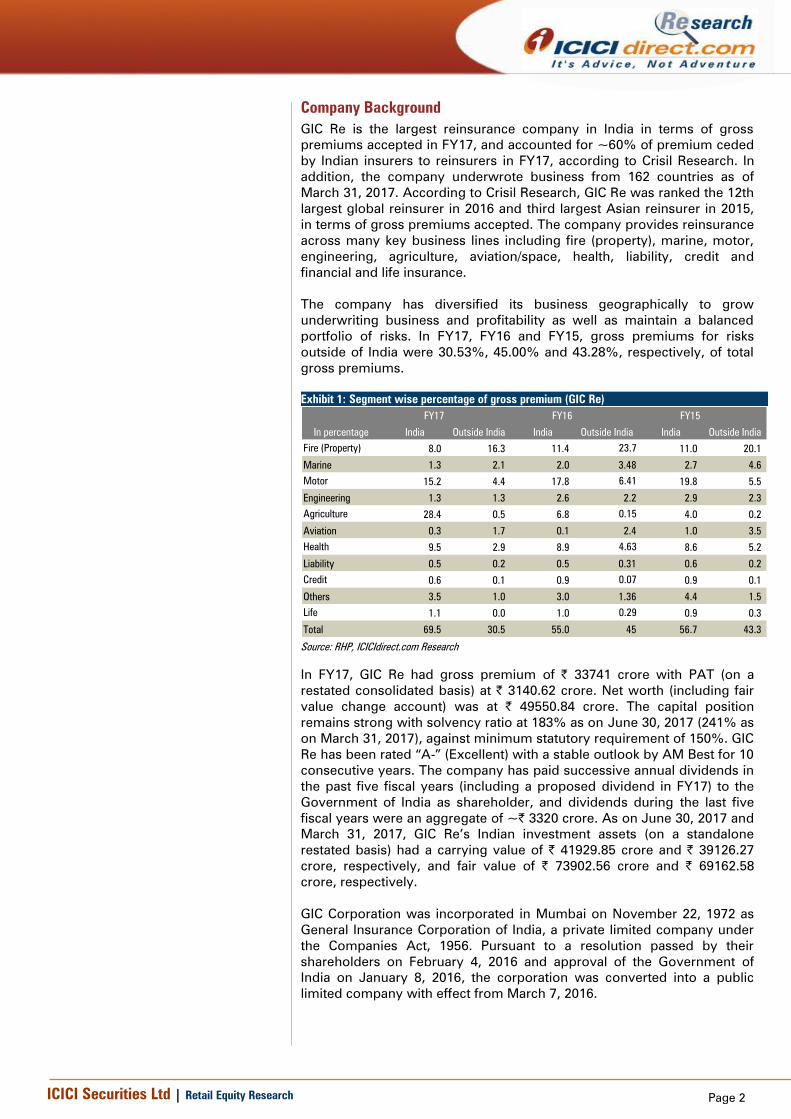

Company Background

GIC Re is the largest reinsurance company in India in terms of gross

premiums accepted in FY17, and accounted for ~60% of premium ceded

by Indian insurers to reinsurers in FY17, according to Crisil Research. In

addition, the company underwrote business from 162 countries as of

March 31, 2017. According to Crisil Research, GIC Re was ranked the 12th

largest global reinsurer in 2016 and third largest Asian reinsurer in 2015,

in terms of gross premiums accepted. The company provides reinsurance

across many key business lines including fire (property), marine, motor,

engineering, agriculture, aviation/space, health, liability, credit and

financial and life insurance.

The company has diversified its business geographically to grow

underwriting business and profitability as well as maintain a balanced

portfolio of risks. In FY17, FY16 and FY15, gross premiums for risks

outside of India were 30.53%, 45.00% and 43.28%, respectively, of total

gross premiums.

Exhibit 1: Segment wise percentage of gross premium (GIC Re)

FY17 FY16 FY15

India Outside India India Outside India India Outside India

Fire (Property) 8.0 16.3 11.4 23.7 11.0 20.1

Marine 1.3 2.1 2.0 3.48 2.7 4.6

Motor 15.2 4.4 17.8 6.41 19.8 5.5

Engineering 1.3 1.3 2.6 2.2 2.9 2.3

Agriculture 28.4 0.5 6.8 0.15 4.0 0.2

Aviation 0.3 1.7 0.1 2.4 1.0 3.5

Health 9.5 2.9 8.9 4.63 8.6 5.2

Liability 0.5 0.2 0.5 0.31 0.6 0.2

Credit 0.6 0.1 0.9 0.07 0.9 0.1

Others 3.5 1.0 3.0 1.36 4.4 1.5

Life 1.1 0.0 1.0 0.29 0.9 0.3

Total 69.5 30.5 55.0 45 56.7 43.3

In percentage

Source: RHP, ICICIdirect.com Research

In FY17, GIC Re had gross premium of | 33741 crore with PAT (on a

restated consolidated basis) at | 3140.62 crore. Net worth (including fair

value change account) was at | 49550.84 crore. The capital position

remains strong with solvency ratio at 183% as on June 30, 2017 (241% as

on March 31, 2017), against minimum statutory requirement of 150%. GIC

Re has been rated “A-” (Excellent) with a stable outlook by AM Best for 10

consecutive years. The company has paid successive annual dividends in

the past five fiscal years (including a proposed dividend in FY17) to the

Government of India as shareholder, and dividends during the last five

fiscal years were an aggregate of ~| 3320 crore. As on June 30, 2017 and

March 31, 2017, GIC Re’s Indian investment assets (on a standalone

restated basis) had a carrying value of | 41929.85 crore and | 39126.27

crore, respectively, and fair value of | 73902.56 crore and | 69162.58

crore, respectively.

GIC Corporation was incorporated in Mumbai on November 22, 1972 as

General Insurance Corporation of India, a private limited company under

the Companies Act, 1956. Pursuant to a resolution passed by their

shareholders on February 4, 2016 and approval of the Government of

India on January 8, 2016, the corporation was converted into a public

limited company with effect from March 7, 2016.

Page 3 ICICI Securities Ltd | Retail Equity Research

Types of reinsurance

There are two main types of reinsurance: treaty and facultative

reinsurance;

Treaty reinsurance: In treaty reinsurance, the cedent seeks reinsurance

for certain type of insurance or class of risks insured under a direct

contract of insurance or specific risks within a certain period. Once the

treaty is in place, the cedent is obliged to cede while the reinsurer is

obliged to reinsure all businesses that come within the scope of the terms

and conditions under the treaty. Generally, under a treaty arrangement,

the reinsurer does not separately evaluate each individual risk assumed

under the contract. They follow the original underwriting decision made

by the cedent.

Facultative reinsurance: Facultative reinsurance constitutes a separately

negotiated contract of reinsurance with respect to each original contract

of insurance. This permits the reinsurer to decide in each case whether to

underwrite each risk and to more accurately price the reinsurance to

reflect the risks. Facultative reinsurance is usually sought by cedents for

risks that are not covered by their treaty reinsurance arrangements, for

amounts exceeding the sum insured of their treaty arrangements and for

complex or unusual risks.

Reinsurance is written on either a proportional basis or a non-proportional

basis;

Proportional (quota-share): In proportional reinsurance arrangements, the

retention amount of cedent and liability of reinsurer are determined

according to the sum insured. The cedent and the reinsurer share the risk

on a proportional basis. Premium and losses are allocated according to

the agreed percentage of the sum insured. Facultative reinsurance

contracts are usually proportional.

Non-proportional (excess): In non-proportional insurance, the liabilities of

the cedent and the reinsurer are calculated based on losses. Once the

losses incurred by the cedent exceed the agreed amount the reinsurer

will be liable for a specified portion or all the excess loss. These are

known as excess of loss agreements.

Alternative capital

In recent years, alternative capital products have emerged as a substitute

for traditional reinsurance contracts. Alternative capital refers to a source

of reinsurance capacity, which is based on investors directly investing

into certain reinsurance risks such as catastrophe bonds, collaterised

reinsurance, and insurance-linked securities. The underlying risk covered

relates to the various of insurance relating to fire, marine, health,

property, life, etc, written by the direct insurers as well as re- insurers.

Page 4 ICICI Securities Ltd | Retail Equity Research

Financial Performance

GIC Re’s gross premiums have grown at healthy pace of 48.65% CAGR

from | 15270.1 crore in FY15 to | 33740.79 crore in FY17. In FY15-17, PAT

grew at 4.23% CAGR from | 2890.97 crore in FY15 to | 3140.62 crore in

FY17. As on March 31, 2017, total assets were at | 97079.43 crore. The

capital position remains strong with solvency ratio at 183% as on June

30, 2017 (241% as on March 31, 2017), against minimum statutory

requirement of 150%.

Exhibit 2: Gross premium growth surges in FY17 led by crop insurance

14680.0 15270.2

18534.2

33740.8

17325.4

4.0%

21.4%

82.0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

0

5000

10000

15000

20000

25000

30000

35000

40000

FY14 FY15 FY16 FY17 Q1FY18

|crore

Premiums earned - Net YoY growth (RHS)

Source: RHP, ICICIdirect.com Research

Exhibit 3: Trend in net worth

15237

1741419514

20,143.21

14.3%

12.1%

10%

20%

0

5000

10000

15000

20000

25000

FY15 FY16 FY17 Q1FY18

(%)

| b

illion

Net worth YoY growth (RHS)

Source: RHP, ICICIdirect.com, Research

Exhibit 4: PAT growth trend

2253

2891 2823

3141

629

-20%

0%

20%

40%

0

500

1000

1500

2000

2500

3000

3500

FY14 FY15 FY16 FY17 Q1FY18

| c

rore

PAT YoY growth (RHS)

Source: RHP, ICICIdirect.com, Research

Exhibit 5: Return on net worth above 16%

19.1 19.0

16.2 16.1

3.1

0

10

20

30

FY14 FY15 FY16 FY17 Q1FY18

(%

)

Source: RHP, ICICIdirect.com, Research

Exhibit 6: Solvency ratio remains prudent (%)

293

332

380

241

183

0

100

200

300

400

FY14 FY15 FY16 FY17 Q1FY18

(%

)

Source: RHP, ICICIdirect.com, Research

Page 5 ICICI Securities Ltd | Retail Equity Research

Indian reinsurance industry landscape

Reinsurance refers to the arrangement whereby insurers transfer part of

the risks and liabilities written to one or more insurers or reinsurers by

entering reinsurance contracts. Reinsurance is considered the insurance

of insurance. Reinsurance allows direct insurers to manage capacity, ease

surplus strain, minimise fluctuations in claim payments and lapse

exposure and manage their portfolios. The reinsurance industry also

provides insurance companies with access to important industry

information and expertise.

Global size and growth

The size of the global reinsurance market is estimated to be around

US$230 billion in 2016, with the non-life segment accounting for 70% of

the market (source: Crisil Report). According to Crisil Research, the

reinsurance industry is in a deep soft market cycle, which began in 2013.

The troika of weak underlying demand growth, low interest rates and the

expansion of alternative capital has impacted the global reinsurance

market over the past few years. With the supply of capital far exceeding

demand, the market has been extremely soft (source: Crisil Report).

Primary insurance premiums in emerging markets are growing faster than

in advanced economies, providing opportunities for global reinsurance

players. The share of emerging markets in the life reinsurance segment is

expected to increase from the current 14% (source: Crisil Report). In non-

life reinsurance, the share of business from emerging markets is higher

than that in the life segment at about 26% (source: Crisil Report).

Exhibit 7: Five year CAGR for life and non-life insurance business worldwide

2.80%

1.50%

9.40%

3%

1.90%

8.50%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

World Advanced markets Emerging markets

(%)

Source: RHP, ICICIdirect.com Research

Total premiums in the Indian life and non-life insurance markets were

around | 4.18 trillion and | 1.28 trillion, respectively, in FY17. According

to Crisil Research, the size of the Indian reinsurance market was estimated

to be ~| 388 billion in FY17. Reinsurance of non-life insurance business

accounted for ~95% of the total premium ceded in FY17 (source: Crisil

Report). Currently, GIC Re is the only publicly owned reinsurance

company in India. There is one privately owned reinsurance company

which has been registered by the IRDAI - ITI Reinsurance Ltd. Subject to

IRDAI regulation, foreign reinsurance companies are permitted to sell

reinsurance coverage in India. As of June 30, 2017, eight foreign

reinsurance companies and Lloyds of London have been registered by

IRDAI, which allows them to operate branches in India.

Under the IRDA (General Insurance-Reinsurance) Regulations, 2016,

general insurers are required to make a minimum level of cessions to

Indian reinsurers. Previously, IRDAI had prescribed that all general

insurers should compulsorily cede 20% of their gross premium to Indian

Page 6 ICICI Securities Ltd | Retail Equity Research

reinsurers (currently only GIC Re). As the size of the general insurance

industry increased, this limit has been progressively reduced to 15% in

2007, 10% in 2008 and 5% in 2013 and same till now.

Reinsurance sector growth in India

According to Crisil Research, the size of the Indian reinsurance market

was estimated to be ~| 388 billion in FY17. The reinsurance market in

India grew at a healthy 15% CAGR in 10 fiscal years ending FY17. In FY17,

premiums ceded to reinsurers increased 73%, as non-life insurance

premiums grew 32% YoY and retention ratios declined close to 9%

(source: Crisil Report). GIC Re, the largest reinsurance company in India

in terms of gross premiums accepted in FY17, accounted for close to 60%

of premiums ceded by Indian insurers to reinsurers in FY17, according to

Crisil Research. Approximately 30% of the reinsurance ceded by Indian

non-life insurance companies in FY16 was ceded to foreign reinsurance

companies.

Exhibit 8: Indian reinsurance market

Source: RHP, ICICIdirect.com Research

According to Crisil Research, fire (property), motor, health were the

largest market segments in terms of non-life gross premiums ceded in

FY16. These segments combined contributed ~60% of non-life gross

premium ceded in FY16. However, according to Crisil, crop insurance

premiums ceded to reinsurers quadrupled in FY17, and, typically, a large

portion of premiums from crop reinsurance tends to be ceded to

reinsurers. The following pie chart shows the composition of premium

ceded to reinsurers in India by segment in FY16.

Page 7 ICICI Securities Ltd | Retail Equity Research

Exhibit 9: Non-life premium ceded to reinsurers segment-wise (FY16)

18%

12%

3%

27%

6%

9%

25%

Motor Health Liability Fire Marine Engineering Others

Source: RHP, ICICIdirect.com Research

Given that most reinsurance premiums written in India come from the

non-life segment (an average 95% in the past five years ending FY17),

future growth in reinsurance premiums will be driven by growth in the

non-life insurance segment as well as percentage of non-life premiums to

reinsurers. According to Crisil Research, reinsurance premiums in India

are projected to increase at 11-14% CAGR over the next five fiscal years

to touch | 700 billion by FY22. New business opportunities may also

emerge in areas like cyber security, big data and smart city infrastructure

(Source: Crisil Report). The contribution of this new business to overall

premiums, however, would be insignificant.

Reinsurance growth - derivative of direct growth in non-life insurance….

The Indian non-life insurance size was at | 1.28 trillion on a GDPI basis as

of March 31, 2017, making it the 15th largest non-life insurance market in

the world and fourth largest in Asia (source: Swiss Re and Crisil Research,

Analysis of general insurance industry in India, July 2017). In FY01-17,

Indian non-life insurance GDPI grew at a healthy pace of ~17.4% CAGR.

India was also among the fastest growing non-life insurance markets over

2011-16, growing at 14.5% (Source: Swiss Re). Despite this, India

continues to be an under penetrated market with a non-life insurance

penetration (insurance penetration refers to premiums as a percentage of

GDP) of 0.77% in 2016, compared to 1.81% in China, 1.70% in Thailand,

1.67% in Singapore and 1.62% in Malaysia and a global average of 2.81%

in 2016. Similarly, insurance density (per capita premium or premium per

person) also remains very low compared to other developed and

emerging market economies at US$13.2 in 2016.

Page 8 ICICI Securities Ltd | Retail Equity Research

Exhibit 10: Insurance penetration (as percentage of GDP) - 2016

4.29

2.742.58

2.37

1.81 1.76

1.36

0.77

0.51

0

1

1

2

2

3

3

4

4

5

5

US South

Africa

UK Japan China Brazil Russia India Indonesia

(%)

Source: ICICI Lombard RHP, ICICIdirect.com Research

Exhibit 11: Non-Life Insurance density (2016)

2449

1031928

147 151 147 10018 13

0

500

1000

1500

2000

2500

3000

US UK Japan S.Africa Brazil China Russia Indonesia India

(U

SD

)

Source: ICICI Lombard RHP, ICICIdirect.com Research

The Indian non-life insurance sector offers different products such as

motor, health, crop, fire, marine, liability, travel, aviation and home

insurance aimed at meeting different protection needs of retail customers,

government as well as corporate customers. The industry operates under

a “cash before cover” model under which insurers are not required to

assume underwriting risk until premiums are received except in the case

of government sponsored schemes such as mass health and crop

insurance.

The Indian non-life insurance sector has significant growth potential due

to its under-penetration and low insurance density compared with other

economies. According to Crisil Research, GDPI for non-life insurers are

projected to grow at 15-20% CAGR in FY17-22. India’s large working

population, rising affluence, rapid urbanisation and rising awareness of

risk with higher disposable incomes is expected to continue to propel the

growth of the non-life insurance industry in India. In addition, improving

economic growth, emergence of new risks such as cyber frauds and a

strong regulatory focus on improving insurance coverage are expected

be the key catalysts among others for this growth.

Recent catastrophic events have also highlighted the importance of

insurance in India. With only around 10% of economic losses being

insured in India, significant market potential exists for insurance as people

seek to obtain protection to reduce the impact of uninsured losses in the

event of a catastrophe.

Page 9 ICICI Securities Ltd | Retail Equity Research

Exhibit 12: Extent of uninsured losses in recent catastrophe events in India

Date Event Place of event

Economic

Losses

(USD bn)

Insured

Losses

(USD bn)

Un-insured

loss of

total loss

Dec, 2015 Floods Tamil Nadu and Andhra Pradesh 2.2 0.8 66%

Oct, 2014 Cyclone Hudhud Odisha and Andhra Pradesh 7.1 0.6 91%

Sept, 2014 Severe Monsoon Floods Jammu and Kashmir 6.0 0.2 96%

Sept, 2014 Severe Monsoon Floods

Assam, Bihar, Meghalaya, Uttar

Pradesh and West Bengal 6.1 0.2 96%

Oct, 2013 Cyclone Phailin Odisha 4.5 0.1 98%

Jun, 2013 Floods Uttarakhand 1.1 0.5 54%

Sept, 2009 Floods Andhra Pradesh and Karnataka 5.3 0.1 99%

Source: ICICI Lombard RHP, ICICIdirect.com Research

Exhibit 13: GDPI by product segment and insurer (FY17) in direct non life insurers

Source: ICICI Lombard RHP, ICICIdirect.com Research

Impact of entry of more players

Subsequent to the decision to allow foreign reinsurers to set up branch

offices in India, IRDAI has granted certificates of registration to eight

foreign reinsurers to open Indian branches. This includes Munich Re,

Swiss Re, SCOR, Hannover Re, RGA Life Reinsurance Company of

Canada, Gen Re, XL Catlin and Axa Re. In addition, in the global specialist

insurance and reinsurance market, Lloyd’s has also been granted a

license. Prior to being allowed to set up branches in India, these players

sourced business from India without domestic branches. Setting up a

branch will bring them closer to customers and help build stronger

relationships. However, these branches also entail these companies to

commit capital to their Indian business. All nine companies are currently

recruiting professional teams to run their India operations. In addition to

foreign players, IRDAI has also granted a certificate of registration to ITI

Reinsurance Ltd (ITI) so that it can function as a domestic reinsurer

alongside GIC Re. Crisil Research believes the Indian insurance industry

will benefit from international reinsurers’ experience, their capability to

develop new products, and global pricing and marketing experience.

Page 10 ICICI Securities Ltd | Retail Equity Research

Exhibit 14: Comparison of Global Reinsurance Companies

Parameter GIC Re

Everest

Re Group

Ltd

Partner

Re MAPFRE

China

Reinsuran

ce Group

Corporatio

n

Renaissan

ce Re

Headquarters India Bermuda Bermuda Spain China Bermuda

Market cap $ billion as on 5/7/2017 N/A 10.8 N/A 11.0 9.3 5.7

Non-life gross reinsurance premium earned

(USD mn) 4,946 4,247 4,189 3,979 3,682 2,375

Share of non-life gross reinsurance premium (as

% of total gross premium) 98.9% 70.4% 78.2% 84.7% 28.2% 100.0%

3 year CAGR growth (USD) – Non-life gross

reinsurance premium 27.1% 2.6% -3.0% 2.1% n.a. 13.9%

3 year CAGR growth (local currency) - Non-life

gross reinsurance premium 31.7% 2.6% -3.0% 8.2% n.a. 13.9%

Net retention ratio for non-life reinsurance

business 89.8% 91.5% 91.6% 61.1% 97.7% 64.7%

Management expense ratio (Non-life

reinsurance business) 0.8% 3.1% 9.3% 0.8% 1.6% 16.8%

Commission ratio (Non-life reinsurance

business) 20.4% 24.4% 27.4% 28.5% 36.2% 20.6%

Net expense ratio (Non-life reinsurance

business) 21.3% 27.5% 36.7% 29.3% 37.8% 37.4%

Loss/claims ratio (Non-life reinsurance

business) 80.4% 50.0% 60.2% 65.0% 62.0% 37.8%

Combined ratio (Non-life reinsurance business) 101.7% 77.6% 97.0% 94.2% 99.8% 75.2%

Net investment yield based on book value 7.8% 2.8% 2.7% 5.0% 5.1% 3.4%

Return on equity 17.4% 12.7% 6.6% 15.2% 7.4% 10.0%

Source: RHP, ICICIdirect.com Research

Exhibit 15: Extent of uninsured losses in recent catastrophe events in India

Date Event Place of event

Economic

Losses

(USD bn)

Insured

Losses

(USD bn)

Un-insured

loss of

total loss

Dec, 2015 Floods Tamil Nadu and Andhra Pradesh 2.2 0.8 66%

Oct, 2014 Cyclone Hudhud Odisha and Andhra Pradesh 7.1 0.6 91%

Sept, 2014 Severe Monsoon Floods Jammu and Kashmir 6.0 0.2 96%

Sept, 2014 Severe Monsoon Floods

Assam, Bihar, Meghalaya, Uttar

Pradesh and West Bengal 6.1 0.2 96%

Oct, 2013 Cyclone Phailin Odisha 4.5 0.1 98%

Jun, 2013 Floods Uttarakhand 1.1 0.5 54%

Sept, 2009 Floods Andhra Pradesh and Karnataka 5.3 0.1 99%

Source: RHP, ICICIdirect.com Research

Page 11 ICICI Securities Ltd | Retail Equity Research

Key strengths and strategies:

Leader in Indian reinsurance industry

GIC Re writes reinsurance for every non-life and over half of the life

insurance companies in India and has long-term business relationships

with almost all these domestic insurance companies. GIC Re is the largest

reinsurance company in India in terms of gross premiums accepted in

FY17, and accounts for ~60% of the premium ceded by Indian insurers to

reinsurers in FY17, according to Crisil Research.

As per Crisil research, reinsurance premiums in India are projected to

increase at 11-14% CAGR over the next five years to reach | 70000 crore

by FY22. As a trusted brand in the Indian market with 44 years of

experience, GIC Re is well positioned to take advantage of this industry

growth.

Exhibit 16: Market share of Indian reinsurance industry (FY17)

60%

40%

GIC Re Others

Source: RHP, ICICIdirect.com Research

Exhibit 17: Segment-wise percentage of gross premium (GIC Re)

FY17 FY16 FY15

India Outside India India Outside India India Outside India

Fire (Property) 8.0 16.3 11.4 23.7 11.0 20.1

Marine 1.3 2.1 2.0 3.48 2.7 4.6

Motor 15.2 4.4 17.8 6.41 19.8 5.5

Engineering 1.3 1.3 2.6 2.2 2.9 2.3

Agriculture 28.4 0.5 6.8 0.15 4.0 0.2

Aviation 0.3 1.7 0.1 2.4 1.0 3.5

Health 9.5 2.9 8.9 4.63 8.6 5.2

Liability 0.5 0.2 0.5 0.31 0.6 0.2

Credit 0.6 0.1 0.9 0.07 0.9 0.1

Others 3.5 1.0 3.0 1.36 4.4 1.5

Life 1.1 0.0 1.0 0.29 0.9 0.3

Total 69.5 30.5 55.0 45 56.7 43.3

In percentage

Source: RHP, ICICIdirect.com Research

Page 12 ICICI Securities Ltd | Retail Equity Research

Significant global player with growing international presence

GIC Re is an international reinsurer that underwrote business from India

and 162 countries as at March 31, 2017. According to Crisil Research, in

terms of gross premiums accepted, GIC Re was ranked 12th largest global

reinsurer in 2016 and third largest Asian reinsurer in 2015. Geographic

diversity has been important to the growth of the company’s underwriting

business, profitability and also allowed it to maintain a geographically

balanced portfolio of risks.

In FY15-17, GIC Re has grown gross premium from international

operations at 24.84% CAGR to | 10300.45 crore in FY17, representing

30.53% of total gross premium in FY17. The company has developed

business by establishing relationships with insurers and reinsurers

globally and has a robust network of brokers, which assists in sourcing

business. The overseas business is written through home office in

Mumbai, branch offices in London, Dubai and Kuala Lumpur, a

representative office in Moscow, a subsidiary in South Africa and a

subsidiary in the UK that is a member of Lloyd’s of London. In addition,

the company has recently established an International Financial Services

Centre (IFSC) Insurance Office in Gujarat International Finance Tec-City

(GIFT), which has begun accepting reinsurance from international clients

in India from FY18.

Exhibit 18: Geography-wise break-up of premium (GIC Re)

69.47

55 56.72

30.53

45 43.28

0

20

40

60

80

100

120

FY15 FY16 FY17

(%)

India Outside India

Source: RHP, ICICIdirect.com Research

With a goal of achieving a balance of international and India business in

terms of premiums, following are business plans for overseas expansion;

Establishing a syndicate at Lloyds of London, which will write a

variety of classes of business from different parts of the world;

Expanding relationships with insurers in the US (the largest

market globally) and accepting more US insurance related risks;

Establishing representative offices in China and expanding

reinsurance business written in China;

Establishing a representative office in Brazil to expand Latin

American business;

Converting Moscow representative office into a wholly owned

subsidiary and expanding reinsurance business in Russia and CIS

countries from Moscow and

Establishing a strategic relationship for reinsurance business in

Myanmar and establishing a representative office in Bangladesh

Page 13 ICICI Securities Ltd | Retail Equity Research

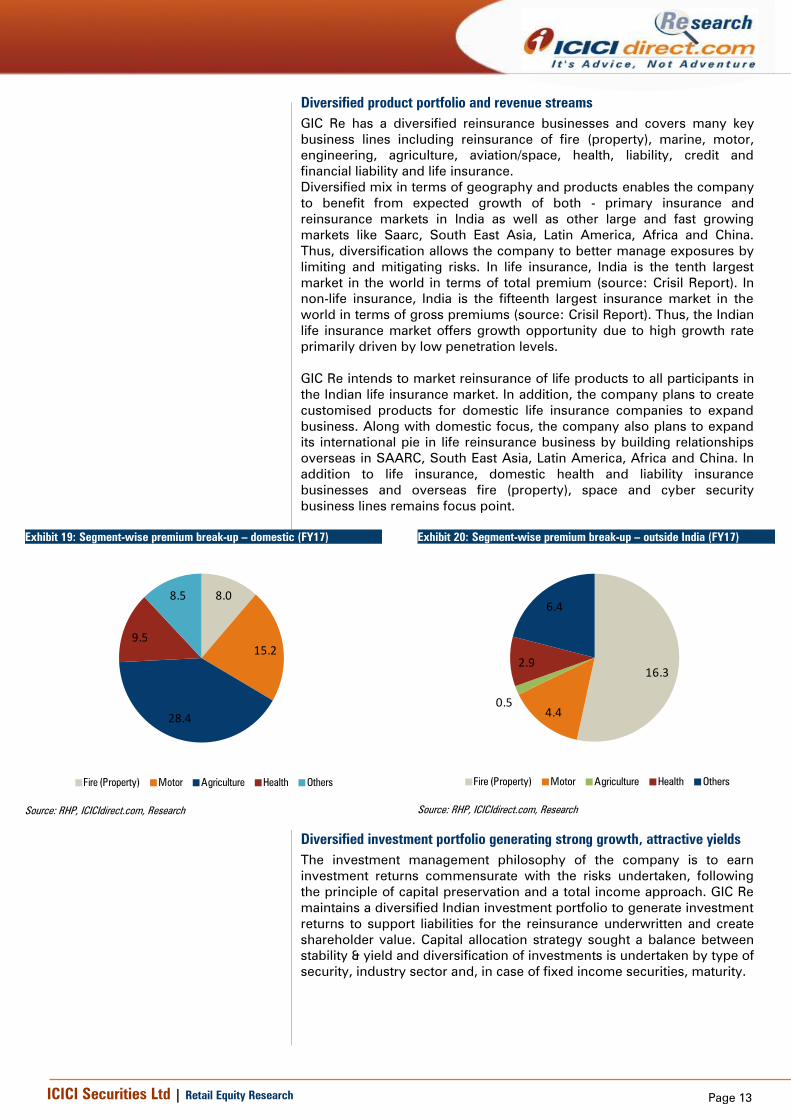

Diversified product portfolio and revenue streams

GIC Re has a diversified reinsurance businesses and covers many key

business lines including reinsurance of fire (property), marine, motor,

engineering, agriculture, aviation/space, health, liability, credit and

financial liability and life insurance.

Diversified mix in terms of geography and products enables the company

to benefit from expected growth of both - primary insurance and

reinsurance markets in India as well as other large and fast growing

markets like Saarc, South East Asia, Latin America, Africa and China.

Thus, diversification allows the company to better manage exposures by

limiting and mitigating risks. In life insurance, India is the tenth largest

market in the world in terms of total premium (source: Crisil Report). In

non-life insurance, India is the fifteenth largest insurance market in the

world in terms of gross premiums (source: Crisil Report). Thus, the Indian

life insurance market offers growth opportunity due to high growth rate

primarily driven by low penetration levels.

GIC Re intends to market reinsurance of life products to all participants in

the Indian life insurance market. In addition, the company plans to create

customised products for domestic life insurance companies to expand

business. Along with domestic focus, the company also plans to expand

its international pie in life reinsurance business by building relationships

overseas in SAARC, South East Asia, Latin America, Africa and China. In

addition to life insurance, domestic health and liability insurance

businesses and overseas fire (property), space and cyber security

business lines remains focus point.

Exhibit 19: Segment-wise premium break-up – domestic (FY17)

8.0

15.2

28.4

9.5

8.5

Fire (Property) Motor Agriculture Health Others

Source: RHP, ICICIdirect.com, Research

Exhibit 20: Segment-wise premium break-up – outside India (FY17)

16.3

4.4 0.5

2.9

6.4

Fire (Property) Motor Agriculture Health Others

Source: RHP, ICICIdirect.com, Research

Diversified investment portfolio generating strong growth, attractive yields

The investment management philosophy of the company is to earn

investment returns commensurate with the risks undertaken, following

the principle of capital preservation and a total income approach. GIC Re

maintains a diversified Indian investment portfolio to generate investment

returns to support liabilities for the reinsurance underwritten and create

shareholder value. Capital allocation strategy sought a balance between

stability & yield and diversification of investments is undertaken by type of

security, industry sector and, in case of fixed income securities, maturity.

Page 14 ICICI Securities Ltd | Retail Equity Research

Exhibit 21: Geography-wise break-up of premium (GIC Re)

Investment Carrying Value % of total invt Market Value % of total invt Yield

Equity 7970.413 20.37 37931.132 54.84 27.9%

Fixed Income Securities - -

... Central Govt Securities 8343.947 21.33 8343.947 12.06 8.1%

…State Govt Securities 4,831.0 12.4 4,831.0 7.0 8.5%

…Other Approved Securities 338.171 0.86 338.171 0.49 7.7%

...Debentures and Bonds 11,164.7 28.5 11,164.7 16.2 9.1%

...Money Market Instruments 5957.051 15.23 6032.645 8.72 5.0%

Loans 319.7 0.8 319.7 0.5 10.3%

Venture Capital Funds 174.448 0.45 174.448 0.25 5.8%

Preference Shares 6.9 0.0 6.9 0.0 6.1%

Application Money 20 0.05 20 0.03

Total Investments 39,126.3 100.0 69,162.6 100.0 12.3%

Source: RHP, ICICIdirect.com Research

The Indian investment portfolio includes fixed income debt securities,

equity securities including exchange traded funds, and other investments.

As of June 30, 2017 and March 31, 2017, Indian investment assets had a

carrying value of | 41929.85 crore and | 39126.27 crore, respectively and

fair value of | 73902.56 crore and | 69162.58 crore, respectively. In

addition, as of June 30, 2017 and March 31, 2017, the company had fixed

term deposits for non-Indian business (written outside of India) of

| 8062.19 crore and | 7610.99 crore, respectively, held at various

overseas financial institutions. Investment assets outside India of

subsidiaries amounted to | 307.22 crore and | 287.44 crore, as of June

30, 2017 and March 31, 2017, respectively. Accounted portion of

investments in associate companies amounted to | 1391.02 crore and

| 1320.33 crore, respectively.

Indian investment assets are managed centrally, using appropriate risk

management and investment parameters to guide investment team within

prescribed regulatory guidelines. In FY17, FY16 and FY15, investment

income from Indian investment assets was | 4515.61 crore, | 4174.99

crore and | 4176.06 crore, respectively, with a CAGR of 3.99% from FY15-

17. Yields (without unrealised gains) from Indian investment assets were

at 12.35%, 12.91% and 14.08% in FY17, FY16 and FY15, respectively. In

addition to investment income on Indian investment portfolio, in FY17,

interest income on foreign short term deposits for overseas business

(written outside of India at our branches) stood at | 99.76 crore.

Page 15 ICICI Securities Ltd | Retail Equity Research

Key risks and concerns

Catastrophe business may lead to volatile profits

Catastrophic losses result from events such as windstorms, hurricanes,

tsunamis, earthquakes, floods, hailstorms, tornadoes, etc and other

natural and man-made disasters, the incidence and severity of which are

inherently unpredictable. Since catastrophe reinsurance accumulates

large aggregate exposures to man-made and natural disasters, GIC Re’s

loss experience in catastrophe reinsurance can be characterised as low

frequency and high severity. This may result in substantial volatility in

their financial results for any fiscal quarter or fiscal year.

Operate in highly competitive environment, no strong entry barriers

The reinsurance industry is highly competitive and the company

competes with a number of worldwide reinsurance companies, many of

which have greater financial resources and industry experience.

In India, IRDAI regulations now permit private Indian reinsurers to be

licensed, foreign reinsurers to open branches and Lloyd’s syndicates to

operate in India. The lack of strong barriers to entry into the reinsurance

business means that new companies in India and internationally may be

formed to enter reinsurance markets and compete with GIC Re. In

addition, the company may experience increased competition as a result

of the consolidation in the reinsurance industry.

Cyclical nature of reinsurance industry with excess underwriting capacity

and unfavourable premium rates

Historically, the reinsurance industry has been cyclical. Demand for

reinsurance is influenced significantly by underwriting results of primary

insurers. The supply of reinsurance is related directly to prevailing prices

and levels of capacity that, in turn, may fluctuate in response to changes

in rates of return on investments being realised in the reinsurance

industry. If any of these factors were to result in a decline in the demand

for reinsurance or an overall increase in reinsurance capacity, the

profitability of the company may be impacted. In recent years, they have

experienced a soft market cycle, with increased competition, surplus

underwriting capacity, deteriorating rates and less favourable terms and

conditions all having an impact on our ability to write business.

Foreign currency fluctuations can reduce net income & capital levels

GIC Re has multinational reinsurance operations. They conduct business

in a variety of foreign (non-rupee) currencies including but not limited to

US dollar, Euro and British pound. Assets and liabilities denominated in

foreign currencies are exposed to changes in currency exchange rates,

which may be material. Their reporting currency is the Indian rupee, and

exchange rate fluctuations relative to the Indian rupee may materially

impact their results of operation and financial position

Usefulness of analytic models as tool to evaluate risk is subject to high

degree of uncertainty

The company’s success is dependent upon its ability to assess accurately

the risks associated with the businesses that they insure and reinsure.

They use their own and third-party vendor analytic and modelling

capabilities to provide objective risk assessment relating to risks in

reinsurance portfolio. They use these models to help them control risk

accumulation, assess capital requirements and to improve the risk/return

profile. However, given the inherent uncertainty of modelling techniques

and application of such techniques, these models and databases may not

accurately address a variety of matters, which might impact certain

reinsurance coverage that they write. The models may not accurately

represent loss potential to reinsurance.

Page 16 ICICI Securities Ltd | Retail Equity Research

Substantial increase in agriculture reinsurance business in recent years

The company has substantially increased its agriculture reinsurance

business by reinsuring crop insurance under the GoI’s Pradhan Mantri

Fasal Bima Yojana insurance scheme (PMFBY). Gross premiums in

agriculture reinsurance segment have increased from | 644.2 crore in

FY15 to | 1291.7 crore in FY16 and further to | 9752.3 crore in FY17. Even

gross premiums in agriculture reinsurance segment were | 9925.2 crore

in the three months ended June 30, 2017. The GoI is looking for

Corporation to provide technical support for PMFBY.

GIC Re has not operated at this level of exposure in agriculture segment

before. Such substantial growth in the agriculture business exposes it to

risks, losses, uncertainties and challenges peculiar to this segment.

Reputational risk

GIC re is exposed to risks arising due to improper business practices such

as inadequate due diligence, including client verification, non-adherence

to anti-money laundering guidelines and client’s needs analysis, in the

sales process. Any fraud, sales misrepresentation, money laundering and

other misconduct committed by its employees, intermediaries and any

other business partners may result in violation of laws and regulations

and subject to regulatory sanctions. Even if such instances of misconduct

do not result in any legal liabilities on their part, they could cause serious

reputational or financial harm to GIC Re.

Page 17 ICICI Securities Ltd | Retail Equity Research

Financial Summary

Exhibit 22: Shareholders Account

(| Crore) FY14 FY15 FY16 FY17

Fire Insurance 3668.3 3981.7 4637.2 5595.9

Miscellaneous Insurance 8846.1 8548.7 9541.0 19629.3

Marine Insurance 995.7 924.9 918.9 910.4

Life Insurance 106.0 139.5 241.1 239.1

Premiums earned - Net 13,616.0 13,594.8 15,338.2 26374.688

Operating Profit/(Loss) 1603.4 1561.3 1590.2 2251.8

Income from Investments 982.7 1302.1 1436.4 1638.4

Other income 110.0 234.8 242.6 -91.5

Total revenue 2,696.1 3,098.1 3,269.2 3,798.67

Provisions 124.9 110.7 42.0 260.0

Other expenses 268.7 156.9 205.7 122.2

Profit before tax 2302.4 2830.5 3021.4 3416.5

Tax -130.6 -60.5 198.0 275.9

PAT 2,433.1 2,891.0 2,823.4 3,140.6

Source: RHP, ICICIdirect.com Research

Exhibit 23: Balance Sheet

(| Crore) FY14 FY15 FY16 FY17

Sources of Funds

Share capital 430 430 430 430

Reserves and Surplus 13224 15594 17988 19539

Net worth 13654 16024.18 18417.78 19968.7

Borrowings - - - -

Deferred Tax Liability - - - -

Fair Value Change Account 20532 28148 23457 30037

Total Liabilities 34186 44172 41875 50006

Applications of Funds

Investments 46679 56758 55686 66212

Loans 424 394 366 322

Fixed assets 118 143 176 169

Goodwill on Consolidation 0 38 38 38

Deferred tax asset 24 9 11 16

Net current assets -13059 -13169 -14402 -16752

Miscellaneous Expenditure 0 0 0 0

Total 34186 44172 41875 50006

Source: RHP, ICICIdirect.com Research

Exhibit 24: Key Ratios

(Year-end March) FY14 FY15 FY16 FY17

Valuation

No. of Equity Shares (Crore) 86.0 86.0 86.0 86.0

Diluted EPS (|) 28.3 33.6 32.8 36.5

BVPS (|) 148.0 177.2 202.5 226.9

P/E 32.2 27.1 27.8 25.0

P/B 6.2 5.1 4.5 4.0

Efficiency Ratios (%)Expense of Management to Net Written

Premium Ratio 1.3 1.2 1.2 0.8

Net Incurred Claims to Net Earned Premium 88.9 87.6 84.5 81.6

Combined ratio 108.9 108.9 107.0 100.2

Operating Profit Ratio 12.1 11.2 9.7 7.1

Return Ratios and capital (%)

Return on Net worth 19.1 19.0 16.2 16.1

Solvency Ratio 293 332 380 241

Source: RHP, ICICIdirect.com Research

Page 18 ICICI Securities Ltd | Retail Equity Research

RATING RATIONALE

ICICIdirect.com endeavours to provide objective opinions and recommendations. ICICIdirect.com assigns ratings to its

stocks according to their notional target price vs. current market price and then categorises them as Strong Buy, Buy, Hold

and Sell. The performance horizon is two years unless specified and the notional target price is defined as the analysts'

valuation for a stock.

Subscribe: Apply for the IPO

Avoid: Do not apply for the IPO

Pankaj Pandey Head – Research [email protected]

ICICIdirect.com Research Desk,

ICICI Securities Limited,

1st Floor, Akruti Trade Centre,

Road No 7, MIDC,

Andheri (East)

Mumbai – 400 093

Page 19 ICICI Securities Ltd | Retail Equity Research

ANALYST CERTIFICATION

We /I, Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA, Research Analysts, authors and the names subscribed to this report, hereby certify that all of the views expressed in this research

report accurately reflect our views about the subject issuer(s) or securities. We also certify that no part of our compensation was, is, or will be directly or indirectly related to the specific recommendation(s)

or view(s) in this report.

Terms & conditions and other disclosures:

ICICI Securities Limited (ICICI Securities) is a full-service, integrated investment banking and is, inter alia, engaged in the business of stock brokering and distribution of financial products. ICICI Securities

Limited is a Sebi registered Research Analyst with Sebi Registration Number – INH000000990. ICICI Securities is a wholly-owned subsidiary of ICICI Bank which is India’s largest private sector bank and has

its various subsidiaries engaged in businesses of housing finance, asset management, life insurance, general insurance, venture capital fund management, etc. (“associates”), the details in respect of which

are available on www.icicibank.com.

ICICI Securities is one of the leading merchant bankers/ underwriters of securities and participate in virtually all securities trading markets in India. We and our associates might have investment banking

and other business relationship with a significant percentage of companies covered by our Investment Research Department. ICICI Securities generally prohibits its analysts, persons reporting to analysts

and their relatives from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover.

The information and opinions in this report have been prepared by ICICI Securities and are subject to change without any notice. The report and information contained herein is strictly confidential and

meant solely for the selected recipient and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without

prior written consent of ICICI Securities. While we would endeavour to update the information herein on a reasonable basis, ICICI Securities is under no obligation to update or keep the information current.

Also, there may be regulatory, compliance or other reasons that may prevent ICICI Securities from doing so. Non-rated securities indicate that rating on a particular security has been suspended

temporarily and such suspension is in compliance with applicable regulations and/or ICICI Securities policies, in circumstances where ICICI Securities might be acting in an advisory capacity to this

company, or in certain other circumstances.

This report is based on information obtained from public sources and sources believed to be reliable, but no independent verification has been made nor is its accuracy or completeness guaranteed. This

report and information herein is solely for informational purpose and shall not be used or considered as an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial

instruments. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ICICI Securities will not treat recipients as customers by virtue of their

receiving this report. Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to your specific

circumstances. The securities discussed and opinions expressed in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment

objectives, financial positions and needs of specific recipient. This may not be taken in substitution for the exercise of independent judgment by any recipient. The recipient should independently evaluate

the investment risks. The value and return on investment may vary because of changes in interest rates, foreign exchange rates or any other reason. ICICI Securities accepts no liabilities whatsoever for any

loss or damage of any kind arising out of the use of this report. Past performance is not necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the

risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to

change without notice.

ICICI Securities or its associates might have managed or co-managed public offering of securities for the subject company or might have been mandated by the subject company for any other assignment

in the past twelve months.

ICICI Securities or its associates might have received any compensation from the companies mentioned in the report during the period preceding twelve months from the date of this report for services in

respect of managing or co-managing public offerings, corporate finance, investment banking or merchant banking, brokerage services or other advisory service in a merger or specific transaction.

ICICI Securities or its associates might have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the companies mentioned

in the report in the past twelve months.

ICICI Securities encourages independence in research report preparation and strives to minimize conflict in preparation of research report. ICICI Securities or its associates or its analysts did not receive any

compensation or other benefits from the companies mentioned in the report or third party in connection with preparation of the research report. Accordingly, neither ICICI Securities nor Research Analysts

and their relatives have any material conflict of interest at the time of publication of this report.

It is confirmed that Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA Research Analysts of this report have not received any compensation from the companies mentioned in the report in the

preceding twelve months.

Compensation of our Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions.

ICICI Securities or its subsidiaries collectively or Research Analysts or their relatives do not own 1% or more of the equity securities of the Company mentioned in the report as of the last day of the month

preceding the publication of the research report.

Since associates of ICICI Securities are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject

company/companies mentioned in this report.

It is confirmed that Kajal Gandhi, CA, Vasant Lohiya, CA and Vishal Narnolia, MBA, Research Analysts do not serve as an officer, director or employee of the companies mentioned in the report.

ICICI Securities may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report.

Neither the Research Analysts nor ICICI Securities have been engaged in market making activity for the companies mentioned in the report.

We submit that no material disciplinary action has been taken on ICICI Securities by any Regulatory Authority impacting Equity Research Analysis activities.

This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution,

publication, availability or use would be contrary to law, regulation or which would subject ICICI Securities and affiliates to any registration or licensing requirement within such jurisdiction. The securities

described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. Persons in whose possession this document may come are required to inform themselves of and

to observe such restriction.