Initiating Coverage Analysts’ Name Ravi Sodah Indian Cement...

87

1 ICICIdirect.com | Equity Research April 20, 2009 | Cement Initiating Coverage Indian Cement Sector Near term macros improve… With softening interest rates, sharp correction in coal and petcoke prices and firming up of cement prices due to strong demand, we believe the near term macroeconomic conditions for the cement industry have improved significantly. We believe that due to healthier balance sheets, moderate consolidation, use of more cost efficient technology and change in the macro environment over the last two quarters cement players will be better off compared to the earlier down cycle. We are initiating coverage on the cement sector with a positive view on Shree Cement, Orient Paper, JK Cement and UltraTech Cement, neutral on India Cement and negative view on ACC, Ambuja and Dalmia Cement. Demand growth accelerates After reporting cement dispatch growth of merely 6.7% in the first seven months of FY09 (April-October ’08), cement growth has accelerated to 10.5% in November ’08-March ’09. We believe the Indian cement industry will continue to grow by 1.2x GDP growth in FY10. Oversupply is inevitable About 62 million tonnes (MT) of cement capacity is scheduled to come on stream by the end of FY10. We expect the capacity utilisation of the industry to drop from 88% in FY09 and further to 79% in FY10. Thus, cement prices are likely to come under pressure with the beginning of the monsoon season. Subsiding cost pressure to cushion margins in near term A 4% cut in excise duty, sharp correction in imported coal, petcoke and crude prices by 67.8%, 49% and 66% respectively from their peak levels have reduced cost pressures for the cement industry. Apart from this, softening of interest rates would reduce the interest burden of smaller cement players, who have funded their capex by debt and cushion their PAT margins. However, we believe that in the long run, the demand-supply situation will force cement players to cut prices and pass on the benefits. Recommendation Some of the cement stocks are currently trading at valuations lower than the value given to loss making cement companies in the last 10 years. This is despite the fact that replacement cost for cement companies has increased significantly over the last decade. We believe that long-term value has emerged in select cement stocks. We also believe that companies that have completed a majority of their capacity addition, undertaken cost cutting measures or have low cost structure with lower earning sensitivity to price declines will be better off compared to their peers. Timely capacity addition will reduce the payback period while a low cost structure will enable them to cut prices and push volumes in a down cycle. We prefer UltraTech Cement among large caps, Shree Cement in the mid cap space and JK Cement and Orient Paper in small caps. Analysts’ Name Ravi Sodah [email protected] Vijay Goel [email protected] Ambuja Cement (GUJAMB) CMP 80 TP 64 Rating Underperformer Dalmia Cements (DALCEM) CMP 95 TP 81 Rating Underperformer India Cements (INDCEM) CMP 120 TP 110 Rating Hold Orient Paper & Ind. (ORIPAP) CMP 28 TP 36.2 Rating Outperformer ACC (ACC) CMP 617 TP 500 Rating Underperformer JK Cements (JKCEME) CMP 54 TP 62 Rating Performer Shree Cement (SHRCEM) CMP 796 TP 900 Rating Performer UltraTech Cement (ULTCEM) CMP 546 TP 630 Rating Performer CMIE Cement Stock Index 1200 2200 3200 4200 Mar'08 Apr'08 May'08 Jun'08 July'08 Aug'08 Sep'08 Oct'08 Nov'08 Dec'08 Jan'09 Feb'09 Mar'09

Transcript of Initiating Coverage Analysts’ Name Ravi Sodah Indian Cement...

1

ICICIdirect.com | Equity Research

April 20, 2009 | Cement

Initiating Coverage

Indian Cement Sector

Near term macros improve…

With softening interest rates, sharp correction in coal and petcoke prices and firming up of cement prices due to strong demand, we believe the near term macroeconomic conditions for the cement industry have improved significantly. We believe that due to healthier balance sheets, moderate consolidation, use of more cost efficient technology and change in the macro environment over the last two quarters cement players will be better off compared to the earlier down cycle. We are initiating coverage on the cement sector with a positive view on Shree Cement, Orient Paper, JK Cement and UltraTech Cement, neutral on India Cement and negative view on ACC, Ambuja and Dalmia Cement.

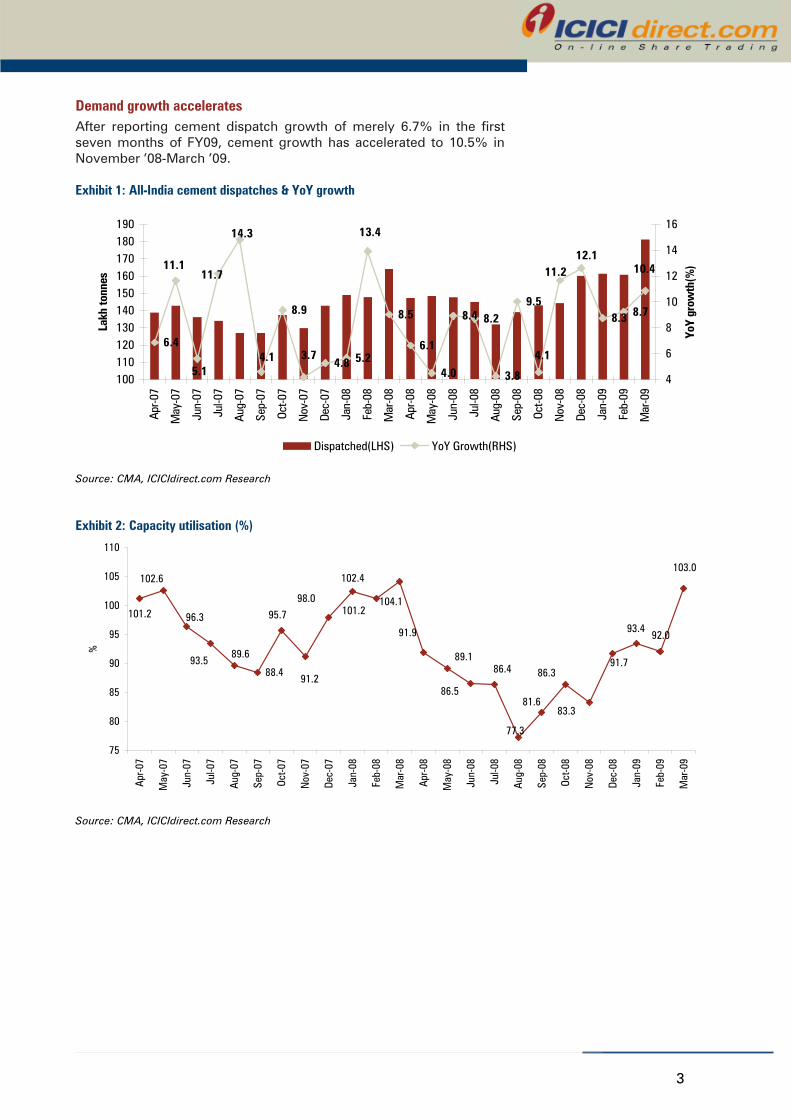

Demand growth accelerates After reporting cement dispatch growth of merely 6.7% in the first seven months of FY09 (April-October ’08), cement growth has accelerated to 10.5% in November ’08-March ’09. We believe the Indian cement industry will continue to grow by 1.2x GDP growth in FY10.

Oversupply is inevitable About 62 million tonnes (MT) of cement capacity is scheduled to come on stream by the end of FY10. We expect the capacity utilisation of the industry to drop from 88% in FY09 and further to 79% in FY10. Thus, cement prices are likely to come under pressure with the beginning of the monsoon season.

Subsiding cost pressure to cushion margins in near term A 4% cut in excise duty, sharp correction in imported coal, petcoke and crude prices by 67.8%, 49% and 66% respectively from their peak levels have reduced cost pressures for the cement industry. Apart from this, softening of interest rates would reduce the interest burden of smaller cement players, who have funded their capex by debt and cushion their PAT margins. However, we believe that in the long run, the demand-supply situation will force cement players to cut prices and pass on the benefits.

Recommendation Some of the cement stocks are currently trading at valuations lower than the value given to loss making cement companies in the last 10 years. This is despite the fact that replacement cost for cement companies has increased significantly over the last decade. We believe that long-term value has emerged in select cement stocks. We also believe that companies that have completed a majority of their capacity addition, undertaken cost cutting measures or have low cost structure with lower earning sensitivity to price declines will be better off compared to their peers. Timely capacity addition will reduce the payback period while a low cost structure will enable them to cut prices and push volumes in a down cycle. We prefer UltraTech Cement among large caps, Shree Cement in the mid cap space and JK Cement and Orient Paper in small caps.

Analysts’ Name

Ravi Sodah [email protected] Vijay Goel [email protected]

Ambuja Cement (GUJAMB)CMP 80TP 64Rating Underperformer

Dalmia Cements (DALCEM)CMP 95TP 81Rating Underperformer

India Cements (INDCEM)CMP 120TP 110Rating Hold

Orient Paper & Ind. (ORIPAP)CMP 28TP 36.2Rating Outperformer

ACC (ACC)CMP 617TP 500Rating Underperformer

JK Cements (JKCEME)CMP 54TP 62Rating Performer

Shree Cement (SHRCEM)CMP 796TP 900Rating Performer

UltraTech Cement (ULTCEM)CMP 546TP 630Rating Performer

CMIE Cement Stock Index

1200

2200

3200

4200

Mar

'08

Apr

'08

May

'08

Jun'

08

July

'08

Aug

'08

Sep'

08

Oct'0

8

Nov

'08

Dec'

08

Jan'

09

Feb'

09

Mar

'09

2

Content

• Demand growth accelerates 3

• Oversupply unavoidable 7

• Subsiding cost pressure to cushion margins in near term 12

• Recommendation 19

Companies Section

Initiating Coverages

• Ambuja Cement 23

• Dalmia Cement 32

• India Cements 42

• Orient Paper & Industries 54

Company Updates

• ACC 68

• JK Cements 73

• Shree Cements 78

• Ultratech Cements 82

Page No.

3

Demand growth accelerates After reporting cement dispatch growth of merely 6.7% in the first seven months of FY09, cement growth has accelerated to 10.5% in November ’08-March ’09.

Exhibit 1: All-India cement dispatches & YoY growth

6.4

8.9

4.8 5.2

8.5

6.1

4.0

8.4 8.2

3.8

9.58.3 8.7

10.4

3.7

14.3

11.7

5.1

11.1 11.2

4.14.1

12.1

13.4

100110120130140150160170180190

Apr-0

7

May

-07

Jun-

07

Jul-0

7

Aug-

07

Sep-

07

Oct-0

7

Nov

-07

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-0

8

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

Lakh

tonn

es

4

6

8

10

12

14

16

YoY

grow

th(%

)

Dispatched(LHS) YoY Growth(RHS)

Source: CMA, ICICIdirect.com Research

Exhibit 2: Capacity utilisation (%)

88.4

103.0

81.6

104.198.0

91.2

95.7

89.693.5

96.3

102.6

101.2

102.4

101.2

91.9

89.1

86.5

77.3

86.4 86.3

83.3

91.7

93.492.0

75

80

85

90

95

100

105

110

Apr-0

7

May

-07

Jun-

07

Jul-0

7

Aug-

07

Sep-

07

Oct-0

7

Nov

-07

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-0

8

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

%

Source: CMA, ICICIdirect.com Research

4

Increased plan expenditure in the fiscal stimulus package by Rs 20,000 crore, pre-election spending led increase in demand from the infrastructure sector coupled with capacity additions have driven the volumes of the industry. Also, cooling off of raw material prices and softening interest rates have increased the viability of infrastructure projects that had turned unviable. We have determined that individual housing demand in rural and semi-urban areas has revived due to the following factors: • Efforts by the government to boost the demand for houses in the

below Rs 20-lakh category in stimulus packages • Cooling off of land prices and steel prices • Good agricultural harvest • Increase in minimum support price (MSP) (wheat's MSP has risen

to Rs 1,080 per quintal in 2008-09 from Rs 750 per quintal in 2006-07 while the figure for rice in the corresponding period has jumped to Rs 850 per quintal from Rs 580 per quintal),

• Increase in pay for workers under the flagship rural job guarantee scheme

• Implementation of debt waiver scheme and • Implementation of the Sixth Pay Commission All-India cement dispatches grew by 6.7% in April-October ’08, mainly driven by the southern region, which had reported growth of 11.5% (Andhra Pradesh had been the main contributor in the southern region with growth of 15.7% mainly driven by higher spending on irrigation projects) as compared to just 4.4% for the rest of India, which forced players like ACC and Shree Cement to shut down their plants. In November ’08-March ’09, cement demand accelerated in other regions with the central region growing at 8.8% due to higher cement demand on part of the UP government on low-cost housing and demand from infrastructure projects such as Yamuna (Taj) Express Highway. In the northern region the growth was 18.7% due to incremental demand from major projects, viz Commonwealth Games, sewerage line project in Punjab, national irrigation project in Haryana and Delhi Metro, fly-over & Delhi Airport and re-imposition of countervailing duty (CVD) of 8% and Special CVD (special additional duty of customs) of 4%, which has dried up cement imports. Demand in the western region has continued to be muted as the organised real estate sector, which contributes a significant chunk in overall demand, has witnessed a slowdown.

Exhibit 3: Region wise cement dispatches growth in FY09(in Lakh tonnes)

Regions Apr-Oct'08 Apr-Oct'07 Var.(%) Nov-Mar'09 Nov-Mar'08 Var.(%)

North 222.2 205.2 8.3 189.2 159.4 18.7

East 139.5 128.7 8.4 120.5 103.5 16.5

West 156.7 159 -1.4 127.9 127.8 0.1

Central 140.1 138 1.5 116.8 107.4 8.8

South 343.9 308.3 11.5 253.2 233.2 8.6

All India Ex South 658.5 630.9 4.4 554.4 498.0 11.3

All India Inc South 1002.4 939.2 6.7 807.6 731.2 10.5

Source: CMA, ICICIdirect.com Research

5

Cement demand had grown at 8.1% CAGR during FY94-FY08 and at 10% CAGR during FY06-FY08. In the near future, cement consumption has been growing in line with the GDP growth rate with the correlation being close to 97%. We believe that in the long run, the cement industry will continue to grow by 1.2x GDP. With a consensus estimate of 5.9% GDP growth, we expect cement demand to grow at 7% in FY10. We are expecting around 59 MT of demand to be generated by the infrastructure sector and 11 MT by real estate projects in Tier-I cities. Exhibit 4: Cement consumption growth, GDP growth and cement to GDP multiple

-4

-2

0

2

4

6

8

10

12

14

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

Grow

th(%

)

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Cem

ent c

onsu

mpt

ion

to G

DP

Mul

tiple

Cement consumption growth(%) (LHS) Cement consumption to GDP Multiple (RHS) GDP growth(%) (LHS)

Source: Bloomberg, CMA, ICICIdirect.com Research

Exhibit 5: Per capita consumption of cement of major countries

777

522

348 342 301

131

0

250

500

750

1000

China Europe WorldAverage

USA Asia (exchina)

India

Per c

apita

con

sum

ptio

n (K

g)

Source: ICICIdirect.com Research

Average GDP to cement consumption growth multiple of last 15 years is 1.2x

r =0.97

6

Exhibit 6: Estimated cement demand from infrastructure sector

11th Five year Plan Roads/ Railways Urban Irrigation Ports *PowerBridges Infra

Investment expected from 11th Plan (Rs. Bn) 3142 2618 1661 2533 880 1760

Assumed that 70% will be spent 2199 1833 1163 1773 616 1232

Civil Construction (%) 100 42 60 45 45

Cement Component(%) 25 20 33 12 30

Total Cement (Rs. Bn) 550 154 230 96 83

Cement Prices Rs/Tonne 4200 4200 4200 4200 4200

Total cement required (Mn Tonnes) 131 37 55 23 20 30

Total Cement for 11th Five year Plan (Mn Tonnes) 295

Average annual Cement consumption (Mn Tonnes) 59*Cement demand as estimated by "White Paper on strategy for 11th Plan"

Source: Planning Commission, ICICIdirect.com Research

Exhibit 7: Year-wise planned expenditure

3892.7

4791.2

5959.1

2702.7

3215.8

6.06.5

7.3

8.29.3

2000

2500

3000

3500

4000

4500

5000

5500

6000

6500

FY08 FY09 FY10 FY11 FY12

Inve

stm

ent i

n Rs

Bill

ion

0

1

2

3

4

5

6

7

8

9

10

as a

% o

f GD

P

Investment in infrastructure (Rs Crore) (LHS) Investment as % of GDP (RHS)

Source: Planning Commission, ICICIdirect.com Research

Exhibit 8: Estimated cement demand from real estate projects in Tier-I cities

Residential(Mn.Sq.Ft.)

Commercial(Mn.Sq.Ft.) Retail (Mn.Sq.Ft.)

City Supply Supply SupplyMumbai 19.2 6.2 NAPune 14.5 3.6 NAChennai 28.4 5 NADelhi NCR 164.8 8 NABangalore 59.0 9.1 NAHyderabad 58.7 1.1 NAKolkata 31.9 1.25 NATotal 376.6 34.3 143.0

553.80.0422.211.1

Total developable area Cement consumptions per sq ft per tonneCement demand over next two years (Mn Tonnes)Average annual cement consumption (Mn Tonnes)

Source: Industry, ICICIdirect.com Research

7

Oversupply unavoidable About 62 MT of cement capacity is scheduled to come on stream by the end of FY10. We expect the capacity utilisation of the industry to drop from 95% in FY08 to 87% in FY09 and further to 79% in FY10. Thus, cement prices are likely to come under pressure from the beginning of the monsoon season. Exhibit 9: Demand-Supply scenario; Capacity Utilisation to drop Million Tonnes FY05 FY06 FY07 FY08 FY09 FY10EEffective Capacity 153.6 158.1 166.7 175.7 206.5 246.0Production 127.6 141.8 155.7 168.3 181.4 195.6Capacity Utilisation (%) 83 90 93 95 88 79Domestic consumption 121.1 135.6 149.0 164.0 177.0 189.8*Export 10.1 9.2 9.0 6.0 6.1 5.8Import 0.4 0.7 0.0

Source: CMA, ICICIdirect.com Research

*Cement and clinker

Exhibit 10: Region wise capacity addition in FY10

47%

30%

11%

12%

South North East West

Source: Industry, ICICIdirect.com Research

8

Exhibit 11: Capacity addition in FY09 Capacity at the beginning of the year 2008-2009 was 198.30 Mn.T.

Month of CapacityCommissioning Existing

(a) NewOCL India-Kapilas (G) Orissa May-09 - 0.9Rain Comdt. Unit-II Line 2 A.P. Jun-09 - 2.0India Cements-Vallur (G) T.N. Aug-09 - 1.1UltraTech-Ginigera (G) KAR Sep-09 - 1.3Lakshmi Cmt-Kalol (G) GUJ Feb-09 - 0.6Madras Cmts-Ariyalur T.N. Mar-09 - 2.0Chettinad-Ariyalur T.N. Mar-09 - 2.0Total – (a) 9.9(b) ExpansionMadras Cements - R.S. Raja Nagar TN Apr-09 1.2 0.6Vasvadatta Cement KAR Apr-09 3.7 0.5Rain Comdt. Unit-1 A.P. Jun-09 1.0 0.4Rain Comdt. Unit-II Line 1 A.P. Jun-09 0.5 0.1My Home Indus. Ltd. A.P. Jun-09 2.8 0.4Mangalam Cement RAJ Sep-09 0.5 0.5J.K. Gotan RAJ Sep-09 0.1 0.4Kesoram Cement A.P. Nov-09 1.2 0.3Dalmia Cement T.N. Dec-09 3.5 0.5Total – (b) 3.7Total – (a+b) 13.5Capacity as on 31st March 2009 – 211.81 Mn.T.

Name of the Plant State Capacity Added

Source: CMA, ICICIdirect.com Research

Over the last 13 years, the steepest annual fall in cement WPI has been 3.4% as the quantum and timing of the decline has historically been different for different regions. Historically, the southern region has reported the highest decline in cement prices (due to its larger size and presence of a number of players) while the western region has shown least price declines. Exhibit 12: Cement WPI

120

140

160

180

200

220

240

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

WPI

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

Chan

ge(%

)

Change(%) (RHS) WPI (LHS)

Base Year 1992-93=100 Note: Cement WPI indicates movement of average cement prices in India

Source: MOSPI, ICICIdirect.com Research

9

We believe that moderate concentration of the industry and low leverage will prevent a very sharp decline in prices. It should be noted that in the last down cycle, the cement sector was not consolidated as ACC and Ambuja were not under one group and UltraTech was not a part of the AV Birla group. The top five players now control about 52% (38% by combined Holcim and AV Birla group) of the total capacity. Exhibit 14: Debt equity ratio of cement industry

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

Deb

t equ

ity ra

tio (x

)

Source: Capitaline, ICICIdirect.com Research

Exhibit 13: Cement price changes in major cities

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

Delhi Mumbai Chennai Kolkata

Unlike other regions, prices in South had declined by 10% for 2 consecutive years

Source: CMA, ICICIdirect.com Research

1 0

Exhibit 15: Herfindahl -Hirschman Index

Source: ICICIdirect.com Research

Note: HH Index is calculated by adding square of market share of industry players. The Indian cement industry has HHI of approx. 0.1, which indicates moderate concentration

An increase in the level of coordination in the industry was seen in the recent past in the northern region, which witnessed oversupply in the initial part of FY09. During April-November ’08, when cement consumption grew by 6.3% in Rajasthan and only by 2.3% in the northern region, cement players were able to maintain retail cement prices on a YoY basis despite the fact that Rajasthan added 9.2 MT (38%) capacity while the northern region added 12.1 MT (33%) capacity during the period. However, prices had declined in the bulk cement segment. North-based players, having a presence in the bulk cement segment, reported a decline in net realisations of 6.5% YoY in Q3FY09 on account of their inability to pass on the higher excise duty on bulk cement due to weak demand. Exhibit 16: Installed capacity (million tonne) and consumption growth (%)

Consumption Growth (%)

Nov'08 Nov'07 Capacity additions Apr-Nov'08

Rajasthan 33.2 24 9.2 6.3Northern region 48.3 36.3 12.1 2.3

Installed Capacity

Source: CMA, ICICIdirect.com Research

Exhibit 17: Cement prices in major northern cities Rs/Bag Nov'08 Nov'07 Var.(%)Delhi 233 232 0%Jaipur 220 213 4%Ludhiana 241 231 4%Chandigarh 237 229 3%Jammu 296 285 4% Source: CMA, ICICIdirect.com Research

Un-concentrated Moderately concentrated Highly concentrated

0 0.1 0.18 1.0

India Cement Industry

1 1

In order to recover cost of capital, a cement company should earn EBITDA per tonne of Rs 700 on a Greenfield plant and Rs 490 on a brownfield plant. Thus, even with 10% price correction and over Q3FY09 levels, cement industry will be able to recover its cost of capital. The actual price decline will also be a function of the decline in average cost of production of the industry. Exhibit 18: Sustainable EBITDA per tonne for cement industry

(a) Average Realisations 3493(b) Average EBITDA Per tonne 946(c) Capex For Greenfield 5000(d) Cost of capital 14%(e) Required EBITDA per tonne (c*d) 700(f) Decline in EBITDA per tonne (b-e) 246(g) Implied decline in cement price( f/a) 7%(h) Capex For Brownfield 3500(i) Required EBITDA per tonne (h*d) 490(j) Decline in EBITDA per tonne (b-i) 456(k) Implied decline in cement price (j/a) 13%(h) *Average Implied decline in cement price((k+g/2)) 10%*assuming cost structure remain same and no capacity is added by debottlenecking Source: ICICIdirect.com Research

Exhibit 19: Cement stock price index and major developments

0

1000

2000

3000

4000

5000

6000

Jan-

07

Feb-

07

Mar

-07

Apr-0

7

May

-07

Jun-

07

Jul-0

7

Aug-

07

Sep-

07

Oct-0

7

Nov

-07

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-0

8

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

Import duty withdrawn

Dual excise duty on cement introduced

Cement players agreed to hold prices

Abolition of CVD & SAD

Ad valorem duty introduced

Liberalisation in imports from Pakistan

Excise duty on clinker increased to Rs 450/tn and on bulk cement increased to Rs 400/tn or 14%

Export ban

Cement clinker ban onexport to Nepal lifted

Export allowed from Gujarat ports Cenvat duty cut

of 4%

Excise duty on bulk cement decreased to Rs 230/tn or 8%

Source: CMIE, ICICIdirect.com Research

1 2

Subsiding cost pressure to cushion margins in near term Power & fuel constitutes 30-35% of the total expenditure for cement manufacturers. Companies mainly use coal and petcoke as fuel for power plants and kilns during the process of making cement. Due to worsening of the macroeconomics scenario, international coal and domestic petcoke prices have corrected by 67.8% and 49%, respectively, from their peak levels. The correction in sea freight has further reduced the landed cost of imported coal. The benchmark index for sea freights, the Baltic Dry Index is 80.8% down from its peak level. However, part of the benefit of softening of international coal prices has been taken away by a weaker rupee, which has deprecated 31% YoY. Exhibit 20: Baltic Dry Index & international coal prices

0

2000

4000

6000

8000

10000

12000

14000

Mar

-09

Feb-

09

Jan-

09

Dec-

08

Nov

-08

Oct-

08

Sep-

08

Aug-

08

Jul-0

8

Jun-

08

May

-08

May

-08

Apr-

08

Mar

-08

Feb-

08

Jan-

08

Dec-

07

Nov

-07

Oct-

07

Sep-

07

Aug-

07

0

25

50

75

100

125

150

175

200

USD

per T

onne

Baltic dry Index (RHS) Coal price Richards Bay, South Africa (LHS)

$57/Tonne

67.8% decline from peak of $177/tonne

80.8% decline from peak of 11612 2225

Note: Baltic Dry Index indicates the movement of sea freight rate

Source: Bloomberg, ICICIdirect.com Research

Exhibit 21: Rupee – US dollar exchange rate

38

40

42

44

46

48

50

52

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-0

8

May

-08

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

Rupee has depreciated nearly 31% from its peak of 39.8, which has partly neutralised the benefits of decline in international coal prices.

Source: Reuters, ICICIdirect.com Research

1 3

Exhibit 22: Thermal coal prices spot prices, NCDEX

3000

3300

3600

3900

4200

4500

4800

Sep- 08 Oct- 08 Oct- 08

Nov

-08

Dec- 08

Dec- 08 Jan- 09

Feb- 09

Mar

-09

Rs

per

Ton

ne

Rs 3430/tonne

33% decline from its Sept high of Rs 4560/tonne

Source: NCDEX, ICICIdirect.com Research

Exhibit 23: Domestic petcoke prices

6073 5956

6343

58076073

63666065

4793

4053

3271

3000

4000

5000

6000

7000

Apr-0

8

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov-

08

Dec-

08

Jan-

09

Rs p

er to

nne

Source: Industry, ICICIdirect.com Research

1 4

As far as domestic linkage of coal prices is concerned, it was last revised in Q3FY08 by 10-15%. Players, who depend on domestic coal, are unlikely to see a sharp decline in their average coal cost per tonne due to a decline in incremental coal linkages. Exhibit 24: Fuel receipts by cement industry (in million tonne)

Year Coal linkage Receipts against

linkageCoal

production

Coal Receipts as % of Coal

production

1992-93 15.6 10.5 238.3 4.4

1993-94 15.7 10.3 246.0 4.2

1994-95 17.0 10.3 253.8 4.1

1995-96 18.0 10.1 270.1 3.7

1996-97 16.9 10.5 285.7 3.7

1997-98 17.1 9.6 296.1 3.2

1998-99 14.1 8.2 290.8 2.8

1999-00 13.8 9.0 299.3 3.0

2000-01 13.5 9.7 309.8 3.1

2001-02 15.1 11.1 323.0 3.4

2002-03 15.7 12.4 324.2 3.8

2003-04 16.1 13.3 356.2 3.7

2004-05 17.1 14.8 376.6 3.9

2005-06 17.1 14.8 407.0 3.6

2006-07 15.5 14.4 430.9 3.3

2007-08 16.4 14.6 457.0 3.2 Source: CMA, Crisil, Coal India, ICICIdirect.com Research

Exhibit 25: Pithead coal prices

0

200

400

600

800

1000

1200

Dec-

91Ju

n-92

Dec-

92Ju

n-93

Dec-

93Ju

n-94

Dec-

94Ju

n-95

Dec-

95Ju

n-96

Dec-

96Ju

n-97

Dec-

97Ju

n-98

Dec-

98Ju

n-99

Dec-

99Ju

n-00

Dec-

00Ju

n-01

Dec-

01Ju

n-02

Dec-

02Ju

n-03

Dec-

03Ju

n-04

Dec-

04Ju

n-05

Dec-

05Ju

n-06

Dec-

06Ju

n-07

Dec-

07

Rs p

er to

nne

Note: Coal prices are for D-grade coal from Singareni Collieries.

Source: Crisil, ICICIdirect.com Research

1 5

Exhibit 26: Fuel mix of ICICIdirect.com cement universe Company Domestic Coal(%) Imported Coal(%) Petcoke(%)ACC 85 15 0Ultra Tech Cement 57 43 0Shree Cement 0 0 100Dalmia Cement 0 100 0India Cement 30 70 0JK Cement 10 0 90Orient Paper 100 0 0Ambuja Cement 70 30 0 Source: Company, ICICIdirect.com Research

Exhibit 27: Fuel and power cost of major players for FY08/CY07 Average per tonne coal of Fuel in last FY08/CY07

Company Rate/tonne for coal used in Klin CPP cost per unitGrid cost per unit

ACC 2580 2.44 3.55 59#Ambuja Cement - 2.06 3.62 52#India Cement 3863 NA 3.22 NA#Ultra Tech 3017 1.73 4.69 23*Shree cement 4587 2.16 5.38 95*JK Cement 4118 3.12 4.33 52Orient Paper 2018 NA 3.1 0Dalmia 4349 3.9 2.5 25Average 3586 2.6 3.8 52*Use Petoke# Imported Coal

Power cost per unit

% of power requirement met through CPP(Coal

&pet coke based)

Source: Company, ICICIdirect.com Research

Exhibit 28: Electricity consumption per tonne of cement

8985

8985

79

93

80.774

01020

3040506070

8090

100

ACC AmbujaCement

IndiaCement

Ultra Tech Shreecement

*JK cement Orient paper Dalmia

KWH/

tonn

e

*Including white cement

Source: Company, ICICIdirect.com Research

1 6

Crude oil prices have also corrected by 66% from their peak. This, in turn, has led to a saving in packing cost (decline of about Rs 4 per bag) and cut in domestic diesel prices by Rs 2 per litre each in December ’08 and January ’09. However, Indian Railways has changed the product classification for cement and coal in December ’08, which has resulted in an increase of 7-8% in freight charges. Apart from this, Railways has continued to levy a busy season surcharge of 7%. About 38% of the total industry volumes are dispatched by rail. With a worsening of the demand-supply situation, the lead distance to market is also expected to increase. Thus, we do not expect any significant saving in freight cost for the cement industry, which constitutes 25-30% of the total expenditure for cement manufactures. Exhibit 29: Transport mix Company Road Rail SeaACC 50 50 0Ultratech Cement 56 37 7Shree Cement 70 30 0JK Cement 78 22 0Dalima Cement 70 30 0Orient Paper 60 40 0Ambuja Cement 65 6 29 Source: Company, ICICIdirect.com Research

Exhibit 30: International crude oil prices & domestic diesel price

32

33

34

35

36

37

38

39

40

Dec-

07

Jan-

08

Feb-

08

Mar

-08

Apr-0

8

May

-08

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

Rs p

er li

tre

0

20

40

60

80

100

120

140

160

US$

per

bar

rel

Diesel (LHS) Crude Oil (RHS)

Source: Bloomberg, ICICIdirect.com Research

Govt has cut diesel prices by Rs 4 per ltr

1 7

Exhibit 31: Indian road freight index

171

173

172

171171171171

172

172

172

172

170

171

171

172

172

173

173

174M

ay-0

8

Jun-

08

Jul-0

8

Aug-

08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

Source: TCIL, ICICIdirect.com Research

Exhibit 32: HDPE prices (packing material)

0

500

1000

1500

2000

2500

Mar

-08

Apr

-08

May

-08

Jun-

08

Jul-0

8

Aug

-08

Sep-

08

Oct-0

8

Nov

-08

Dec-

08

Jan-

09

Feb-

09

Mar

-09

USD

per

tonn

e

USD 970 Per tonne

Source: Bloomberg, ICICIdirect.com Research

1 8

In Q3FY09, the impact of receding cost pressures was already visible in the form of sequential improvement in financials of some of the cement companies. It should be noted that high cost inventories and contracts that cement players had entered into, have prevented major cost relief in Q3FY09. Q3FY09 Result review Exhibit 33: QoQ (Q3FY09 vs. Q2FY09) change in OPM (in bps)

-10

-420

520

-680

510 520

270

-100

-800

-600

-400

-200

0

200

400

600

ACC AmbujaCement

UltraTechCement

IndiaCement

ShreeCement

JKCement

OrientPaper

DalmiaCement

bps

Source: Company, ICICIdirect.com Research

Exhibit 34: QoQ (Q3FY09 vs. Q2FY09) % change in net profit and operating profit

22

0

61

13

-41

70

11

-14

24

45

-45

38

10

45

-38

-60

-40

-20

0

20

40

60

80

ACC AmbujaCement

UltraTechCement

IndiaCement

ShreeCement

JKCement

OrientPaper

DalmiaCement

QoQ

grow

th(%

)

Net Profit Growth Q0Q (%) Operating Profit growth QoQ (%)

Source: Company, ICICIdirect.com Research

1 9

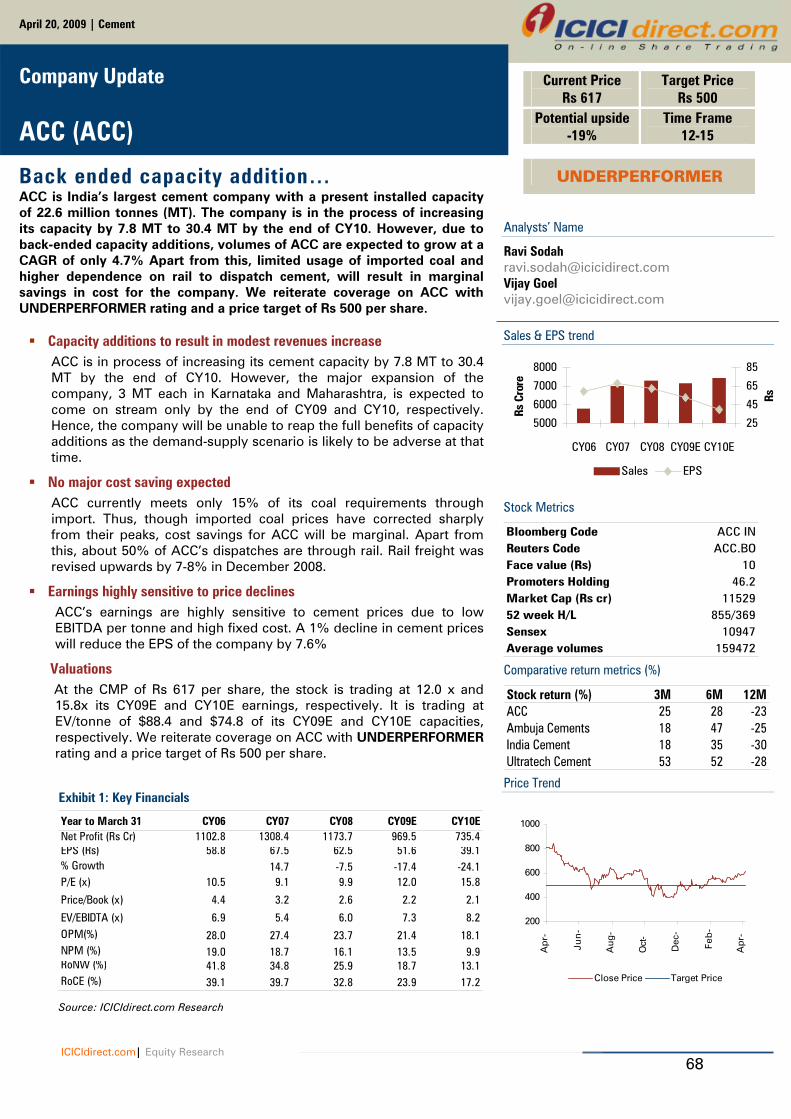

Recommendation Some of the cement stocks are currently trading at valuations lower than the value given to loss making cement companies in the last 10 years. This is despite the fact that the replacement cost for cement companies has increased significantly over the last decade. We believe that long-term value has emerged in select cement stocks and companies that have completed a majority of their capex, undertaken cost-cutting measures or have a low cost structure and have lower earning sensitivity to price declines. These companies will be better off than their peers. Timely capex will reduce the payback period while low cost structure will enable them to cut prices and push volumes in a down cycle. We prefer UltraTech in large caps, Shree Cement in mid caps and JK Cement and Orient Paper in small caps. Our rating rationale is based on P/E & earnings risk, RoNW, EBITDA margins & EV per tonne and normalised P/E & RoNW matrix. We believe that as the cement sector is expected to witness a surplus in the near future, earnings risk will be key rather than CAGR of earnings (PEG). We have estimated the earning risk of cement companies by estimating the impact of cement price decline on earnings. Cement being a cyclical industry, we have also considered EV per tonne and normalized P/E as during a downturn, earnings contract significantly on account of the companies high earnings sensitivity to cement prices. We have calculated normalised earnings of cement companies by multiplying book value with normalized RoNW (average of business cycle RoNW). Cyclical industry stocks normally have a low P/E at the end of boom and a high P/E at the end of a down cycle. Use of normalized P/E reduces this anomaly. We have used this valuation methodology for pure cement companies having a long history. It is inappropriate to use it for diversified companies as the portion of capital employed in a cement division changes over a period of time. Exhibit 35: Some past M&A deals

Year Acquirer Target Capacity (mt) EV/tonne (US$)1998 Guj Ambuja Modi 2 421998 Grasim Sri Digvijay 1.1 41

1999 Ambuja ACC 12 1442003 Grasim L&T cement 17 822005 Holcim ACC 18 1102006 Holcim Guj Ambuja 13.4 1952007 Cimphor Sri Digvijay 1 1522008 CRH My Home 3 2202008 Vicat Sagar 2.5 105

Source: ICICIdirect.com Research

2 0

Exhibit 36: RoNW vs. EV/tonne

0

10

20

30

40

50

0 20 40 60 80 100 120

EV/Tonne (US$)

RoN

W (%

)

ACC Ambuja UltraTech Shree Cem

India Cem JK Cem Orient Paper Dalmia Cem

Source: ICICIdirect.com Research

Note: The size of the bubble indicates FY10E/CY09E OPM (%) Exhibit 37: FY10 P/E vs. earnings risk

0

2

4

6

8

10

1.0 3.0 5.0 7.0 9.0 11.0

P/E

Earn

ings

risk

(%)

ACC Ambuja UltraTech Shree Cem

India Cem JK Cem Orient Paper Dalmia Cem

Source: ICICIdirect.com Research

2 1

Exhibit 38: FY10 Normalised P/E & normalised RoNW (%)

4

8

12

16

20

24

6 7 8 9 10 11 12 13

Normalized RoNW(%)

Nor

mal

ized

P/E

ACC Ambuja Shree India Cem

Source: ICICIdirect.com Research

Exhibit 39: Earnings yield (%) & Earnings CAGR (%)

-40

-20

0

20

5 10 15 20 25 30 35 40 45

Earning yield(%)

Earn

ing

CAGR

(%)

ACC Ambuja Shree Cem India Cem

JK Cem Orient Paper Dalmia Cem UltraTech

As ACC and Ambuja has a negative earning CAGR with earning yield close to AAA bond, investors have no reward for bearing systematic risk in these stocks

AAA bond yield

Source: ICICIdirect.com Research

2 2

Exhibit 40: Q3FY09 cost structure of cement industry

-150

350

850

1350

1850

2350

2850

3350

ACC Ambuja Cement India Cement Ultra Tech Shree Cement *JK cement

Rs P

er to

nne

Stock Adj Raw material Employee cost Power and Fuel Freight Other Expenditure EBIDTA

*includes White Cement

Source: Company, ICICIdirect.com Research

Exhibit 41: Valuation matrix

FY08 FY09 FY10 FY08 FY09 FY10 FY08 FY09 FY10 FY08 FY09 FY10 FY08 FY09 FY10 FY08 FY09 FY10ACC 67.5 62.5 51.6 9.1 9.9 12.0 5.4 6.0 7.3 94.8 94.9 88.4 34.8 25.9 18.7 39.7 32.8 23.9Ambuja 8.3 7.4 7.2 9.7 10.7 11.1 5.2 6.6 6.2 121.7 109.1 106.3 30.8 21.9 18.0 39.6 27.7 23.1UltraTech 80.4 75.9 68.7 6.8 7.2 8.0 4.8 5.1 4.6 94.1 76.1 61.7 45.2 30.4 21.8 40.7 28.9 23.4Shree Cem 82.6 152.2 131.6 9.6 5.2 6.0 3.5 2.9 2.4 69.0 60.2 45.0 51.1 59.1 34.7 26.6 35.5 26.9India Cem 23.5 18.6 19.0 5.2 6.5 6.4 4.2 3.9 3.6 105.7 86.8 59.4 32.9 18.8 16.8 24.3 18.6 17.4JK Cem 37.9 18.4 22.3 1.4 2.9 2.4 1.8 5.4 3.3 34.8 67.6 36.1 41.5 15.7 16.3 26.0 12.5 13.5Orient Paper 10.9 12.2 9.3 2.6 2.5 3.0 1.9 1.8 1.7 33.6 33.5 17.7 66.9 38.5 24.3 59.7 39.7 27.0Dalmia Cem 43.0 18.2 17.4 2.2 5.2 5.5 3.5 5.7 4.4 79.8 115.8 59.9 36.6 12.1 10.3 22.9 10.7 10.0

RoNW (%) RoCE (%)EPS P/E EV/EBITDA EV/Tonne

Source: Company, ICICIdirect.com Research

Note: ACC’s and Ambuja’s numbers are for CY07, CY08 and CY09

2 3

Exhibit 1: Key Financials

CY06 CY07 CY08 CY09E CY10ENet Profit 1,461.5 1,256.5 1,133.5 1,093.6 868.8EPS 9.6 8.3 7.4 7.2 5.7% Growth -14.3 -9.8 -3.5 -20.6P/E (x) 8.3 9.7 10.7 11.1 14.0P/BV (x) 3.5 2.6 2.1 1.9 1.7EV/EBITDA (x) 5.4 5.2 6.6 6.2 6.7OPM% 34.0 35.8 27.4 29.7 25.2NPM % 23.3 22.0 18.2 17.7 13.9RoNW % 51.6 30.8 21.9 18.0 12.8RoCE % 45.2 39.6 27.7 23.1 16.9 Source: Company, ICICIdirect.com Research

Analysts’ Name

Ravi Sodah [email protected] Vijay Goel [email protected]

Sales & EPS trend

5,4005,6005,8006,0006,2006,400

CY06 CY07 CY08 CY09E CY10E

Rs

Cror

e

0

5

10

15

Rs

Net Sales EPS

Stock Metrics

Bloomberg Code ACEM INReuters Code ABUJ.BOFace value (Rs) 2Promoters Holding 46%Market Cap (Rs cr) 1306452 week H/L 119 / 43Sensex 10947Average volumes 335798 Comparative return metrics

Stock return(%) 3M 6M 12MAmbuja Cements 18 47 -25ACC 25 28 -23India Cement 18 35 -30Ultratech Cement 53 52 -28 Price Trend

40

60

80

100

120

140

Apr-

Jun-

Aug-

Oct-

Dec-

Feb-

Apr-

Close Price Target Price

April 20, 2009 | Cement

Initiating Coverage

Ambuja Cements (GUJAMB)

Unjustified premium… Ambuja Cements (ACL) is trading at steep premium to its peers despite not having best return ratios and margins in the industry. Also, company is adding 4.5 million tonnes (MT) of new capacity by CY11, the time by which the demand-supply situation will turn adverse. With realisation and capacity utilisation set to fall, we expect EPS to decline by 12.5% CAGR (CY08-CY10). Hence, we are initiating coverage on the stock with an UNDERPERFORMER rating on account of its expensive valuations.

Capacity addition to bring modest volume growth

Ambuja has expanded its capacity to 22 MT by adding 3.5 MT in CY08. The company is planning to further add 4.5 MT, which will take its capacity to 26.5 MT by CY11. 4.5 MT of capacity is scheduled to come on stream after mid CY09, the time by which the demand-supply situation will turn adverse.

Industry to face demand-supply mismatch; pricing pressure ahead

With 62 MT of capacity addition in FY10 and an expected slowdown in construction activities, we expect the demand-supply scenario to worsen. We have seen demand growth in the last couple of months on the back of pre-election spending and the government’s stimulus packages. However, we believe this is a temporary relief for the players. We expect a decline in realisations and capacity utilisation.

Cement exports to come under pressure Ambuja has exported 0.8 MT of cement (4.7% of the total sales volume) in CY08. The company mainly exports to Middle East countries. As the infrastructure and real estate projects around the Middle East slow down, Ambuja will find it difficult to divert higher volumes to export.

Valuations At the CMP of Rs 80, Ambuja Cement is trading at 11.1x and 14.0x its CY09E and CY10E earnings, respectively. On an EV/tonne basis, it is trading at $106/tonne and $94/tonne of its CY09E and CY10E capacities, respectively. Thus, we are initiating coverage on Ambuja Cement with an UNDERPERFORMER rating and a target price of Rs 64.

Current Price Rs 80

Target Price Rs 64

Potential upside -20%

Time Frame 12 months

UNDERPERFORMER

ICICIdirect.com | Equity Research

2 4

Company Background

Ambuja Cements was set up in 1986. The company is controlled by the Holcim group, which owns 45.68% of the company. The total capacity of the company, as on CY08, is 22 MT. Ambuja has a presence in the north, east and western regions of India. Its plants are situated in Gujarat, Maharashtra, Himachal Pradesh, Punjab, Rajasthan, Uttarakhand, Chhattisgarh and West Bengal. Ambuja has bulk cement terminals at Muldwarka (Gujarat), Panvel, Navi Mumbai and Surat. Ambuja is the largest exporter of cement in India. The company largely exports to the Middle East. The company was one of the first to be equipped with a shipping fleet and make use of the sea as a medium to transport cement across the globe. It has a port terminal at Muldwarka, Gujarat that handles ships with 40,000 DWT. Exhibit 2: Region wise capacity break up(as on Mar’09)

35%

43%

22%

North West East

Source: Company, ICICIdirect.com Research

Share holding pattern (Q4CY08)

Shareholder % holdingPromoters 46.47Institutional investors 37.91Other investors 11.00General public 4.62

Promoter & Institutional holding trend (%)

46% 46% 46% 46%37%37%37%38%

0%

20%

40%60%

80%

100%

Q1 Q2 Q3 Q4

Promoter Holding Institutional Holding

2 5

Investment Concerns

Capacity addition to bring modest volume growth Ambuja has expanded its capacity to 22 MT by adding 3.5 MT in CY08. The company is planning to further add 4.5 MT, which will take its capacity to 26.5 MT by CY11. 4.5 MT of capacity is scheduled to come on stream after mid CY09, the time by which the demand-supply situation will turn adverse. Thus, the sales volume of Ambuja is expected to grow at a CAGR of only 5.7% (CY08-CY10) while the end of the year installed capacity is expected to grow at 8% CAGR during the same period. Exhibit 3: Capacities commissioned in CY08 (million tonnes) Location Caoacity Completion

Surat (GJ) 1 CY08

Bhatapara (CG) 1 CY08

Maratha (Chandrapur) 1.5 CY08

Total 3.5

Source: Company, ICICIdirect.com Research

Exhibit 4: Capex plan (million tonnes) Location Grinding Clinker Expected Completion

Bhatapara (CG) - 2.2 Mid 2009

Ahemdabad (GJ) 1.5 - First half of 2011

Rauri (HP) - 2.2 End of 2009

Dadri (UP) 1.5 - Mid 2009

Nalagarh (HP) 1.5 - First half of 2010

Total 4.5 4.4 Source: Company, ICICIdirect.com Research

Industry to face demand-supply mismatch; pricing pressure ahead

With around 62 MT of capacity addition in FY10, we expect the demand-supply scenario to worsen. We have seen demand growth in the last couple of months on the back of pre-election spending and government’s stimulus packages. However, we believe this is a temporary relief for the players. We expect a decline in realisations and capacity utilisation. Cement exports in difficulty; gulf region faces oversupply Ambuja has exported 0.8 MT of cement (4.7% of the total sales volume) in CY08. The company mainly exports to Middle East countries. As infrastructure and real estate projects around the Middle East slow down, Ambuja will find it difficult to divert higher volumes to exports.

2 6

Financials

Earnings to decline During CY08-CY10, Ambuja’s net sales are expected to remain flat, a CAGR of 0.1% to Rs 6243 crore in CY10 from Rs 6235 crore in CY08 on account of 5.3% CAGR decline in realisation in the next two years. However, the sales volume is expected to grow at a CAGR of only 5.6% (CY08-CY10). Exhibit 5: Revenue to remain flat; volume to grow by 5.6% CAGR

0

1000

2000

3000

4000

5000

6000

7000

CY05 CY06 CY07 CY08 CY09E CY10E0

5

10

15

20

25

Sales Sales Volume

Source: Company, ICICIdirect.com Research

The operating profit is expected to decline by 4.0% CAGR to Rs 1573.2 crore in CY10 from Rs 1708.7 crore in CY08 on account of a decline in operating margin. Exhibit 6: Margins to decline

25.2

29.727.4

35.834.0

23.3 22.0

18.2

13.9

17.7

10

15

20

25

30

35

40

CY06 CY07 CY08 CY09E CY10E

EBITDA margin (%) NPM %

Source: Company, ICICIdirect.com Research

2 7

The reported net profit is expected to decline by 21.3% CAGR to Rs 869 crore in CY10 from Rs 1402 crore in CY08 as Ambuja had a high base in CY08. The company had a net extraordinary income on account of sale of investments, change in inventory policy and one-time retirement benefits charges. Thus, the adjusted PAT is expected to decline by 12.5% CAGR to Rs 869 crore in CY10 from Rs 1134 crore in CY08.

Return ratios to decline

Exhibit 7: RoNW & RoCE

16.9%

12.8%

30.8%

21.9%18.0%

27.7%23.1%

39.6%

0%

10%

20%

30%

40%

50%

CY07 CY08 CY09E CY10E

RoNW ROCE

Source: Company, ICICIdirect.com Research

2 8

Risks to our call

Captive power usage Ambuja sources around 64% of its power requirements from captive power generation. During 2008, one new 18.7 MW power plant was commissioned at the Rabriyawas plant. Additional captive power projects are in progress at Ambujanagar, Bhatapara and Maratha. These will add approximately another 90 MW, most commissioned in 2009 and taking the total capacity to more than 400 MW. For CY08, the average cost of power generation from coal-based CPP was Rs 2.60/Kwh as against Rs 3.86/Kwh for the power purchased from grid. Strong balance sheet Ambuja has cash and bank balance of Rs 852 crore and investments of Rs 332 crore at the end of CY08. It has a debt/equity ratio of 0.05 at the end of CY08. We expect it to further reduce to 0.03 by CY10 as the company’s total capex plan of Rs 3500 crore will be funded totally through internal accruals. Cost pressure eases The company meets 30% of its fuel requirement through imported coal. As international coal prices have dropped sharply by 67.8% from their peak, the company is expected to benefit from the March quarter only because it had been consuming high-cost coal inventory till now. With a worsening of the demand-supply scenario, the lead distance of the company to the markets is expected to increase. However, the cut in diesel prices by Rs 4/litre would enable the company to maintain its freight cost at current levels on a per tonne basis. Quantum of clinker purchase to decline in future Ambuja purchased 7.04 lakh tonnes of clinker (Rs 231.7 crore) in CY08 accounting for 38% of the total raw material cost. With new clinker capacities coming up, the company is likely to reduce clinker purchase in CY09 and CY10. The impact on the EBITDA margin of using purchased clinker rather than own produced clinker is approximately 260 bps.

2 9

Valuations

On an EV/tonne basis, Ambuja is trading at a steep premium to its peers despite the fact that it does not have the best return ratios and best margins in the industry. Even on a P/E basis, it is trading at richer valuations to its peers despite the fact that it does not have the lowest earnings risk in the industry. At the CMP of Rs 80, Ambuja Cement is trading at 11.1x and 14.0x its CY09E and CY10E earnings, respectively. On an EV/tonne basis, it is trading at $106/tonne and $94/tonne its CY09E and CY10E capacities, respectively. Thus, we are initiating coverage on Ambuja Cement with an UNDERPERFORMER rating and a target price of Rs 64. Exhibit 8: Movement of EV/tonne with change in RoE and RoCE

0

50

100

150

200

250

300

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

CY07

CY08

E

CY09

E

CY10

E

EV/t

onne

($)

-5

5

15

25

35

45

55

%

EV/Tonne ($) (RHS) ROE(%) (LHS) ROCE (%) (LHS)

Source: Company, ICICIdirect.com Research

Exhibit 9: P/BV, Market cap to sales, P/CEPS, EV/EBITDA

0

1

2

3

4

5

6

7

FY93

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

CY07

CY08

E

CY09

E

CY10

E

P/BV

& M

cap/

Sal

es

0

5

10

15

20

25

P/CE

PS &

EV/

EBIT

A

P/BV (LHS) M Cap/Sales (LHS) P/CEPS (RHS) EV/EBIDTA (RHS)

Source: Company, ICICIdirect.com Research

3 0

Profit and Loss Account Rs Crore Year Ending March 31 CY06 CY07 CY08 CY09E CY10E Net Sales 6,274.5 5,704.8 6,234.7 6,187.8 6,243.0 % Growth -9.1 9.3 -0.8 0.9 Total Expenditure 4138.1 3659.7 4456.7 4348.4 4669.8 EBITDA 2136.4 2045.1 1708.7 1839.4 1573.2 Other income 94.1 193.5 175.4 114.0 91.0 Depreciation 326.1 236.3 259.8 398.3 413.3 Interest 113.2 75.9 32.1 14.9 9.8 Extra ordinary items 47.5 785.9 377.6 0.0 0.0 PBT 1838.7 2712.4 1969.9 1540.3 1241.1 Taxation 338.4 943.3 567.6 446.7 372.3 Reported PAT 1500.3 1769.1 1402.3 1093.6 868.8 Extra ordinary items(net of tax) 38.8 512.6 268.8 0.0 0.0 Adjusted PAT 1461.5 1256.5 1133.5 1093.6 868.8 EBITDA margin (%) 34.0 35.8 27.4 29.7 25.2 NPM % 23.3 22.0 18.2 17.7 13.9 Shares O/S (crore) 151.7 152.2 152.3 152.3 152.3 EPS (Rs) 9.6 8.3 7.4 7.2 5.7

Balance Sheet Rs Crore Year Ending March 31 CY06 CY07 CY08 CY09E CY10E Sources of funds Equity Share Capital 304.5 304.9 304.9 304.9 304.9 Reserves & Surplus 3,187.2 4,356.4 5,368.0 6,156.0 6,782.0 Secured Loans 317.8 100.0 100.0 100.0 100.0 Unsecured Loans 547.6 230.4 188.7 158.7 128.7 Deferred Tax Liability 383.9 378.4 380.8 380.8 380.8 Total Liability 4,741.0 5,370.1 6,342.3 7,100.3 7,696.3 Application of Funds Net Block 2,489.2 2,959.9 3,192.8 5,902.8 5,821.3 Capital WIP 634.9 696.8 1,947.2 112.7 0.0 Investments 1,133.1 1,288.9 332.4 332.4 332.4 Cash 378.1 642.6 851.8 736.9 1,526.7 Sundry Debtors 90.0 145.7 224.6 222.9 224.9 Inventories 408.8 581.6 939.8 916.9 984.7 Loans & Advances 295.7 205.4 299.9 297.6 300.3 Current Liabilities & Provisions 701.6 1,169.1 1,473.8 1,449.4 1,521.8 Miscellaneous Expenditure 12.8 18.3 27.7 27.5 27.7 Total Asset 4,741.0 5,370.1 6,342.3 7,100.3 7,696.3

3 1

Cash Flow Statement Rs Crore Year Ending March 31 CY06 CY07 CY08 CY09E CY10E Profit Before Tax 1,841.6 2,712.4 1,969.9 1,540.3 1,241.1 Depreciation 326.1 236.3 259.8 398.3 413.3 Changes In working Capital 46.3 (117.9) (261.2) 2.6 (0.3) Others (412.3) (1,279.1) (1,002.2) (511.2) (418.9) Cash Flow from Operating activities 1,801.7 1,551.8 966.2 1,429.9 1,235.2 Inc/Dec in Investment 87.8 266.8 1,241.7 0.0 0.0 Capex (756.4) (521.5) (1,641.5) (1,273.8) (219.1) others 36.0 91.8 125.0 79.4 56.3 Cash Flow from Investing activities (632.7) (162.9) (274.9) (1,194.4) (162.8) Inc/Dec in capital 48.1 32.3 1.2 0.0 0.0 Inc/Dec in Loan Funds (340.2) (525.3) (43.4) (30.0) (30.0) Others (596.7) (631.4) (439.9) (320.5) (252.5) Cash Flow from Financing activities (888.9) (1,124.4) (482.1) (350.5) (282.5) Net Inc/dec in cash 280.2 264.4 209.3 (115.0) 789.9 Opening Balance of Cash 98.0 378.2 642.6 851.8 736.9 Closing Balance of Cash 378.1 642.6 851.8 736.9 1,526.7

Ratios Year Ending March 31 CY06 CY07 CY08 CY09E CY10E EPS 9.6 8.3 7.4 7.2 5.7 Cash EPS 12.0 13.2 10.9 9.8 8.4 OPM (%) 34.0 35.8 27.4 29.7 25.2 NPM (%) 23.3 22.0 18.2 17.7 13.9 Debt/Equity 0.25 0.07 0.05 0.04 0.03 RoCE (%) 45.2 39.6 27.7 23.1 16.9 RoNW (%) 51.6 30.8 21.9 18.0 12.8 Valuation Ratios P/E (x) 8.3 9.7 10.7 11.1 14.0 P/BV (x) 3.5 2.6 2.1 1.9 1.7 EV/EBITDA (x) 5.4 5.2 6.6 6.2 6.7 EV/Tonne (US$) 150.0 121.7 109.1 106.3 93.7 Turnover Ratios Fixed asset turnover ratio 1.4 1.1 1.1 0.7 0.7 inventory turnover ratio 10.1 6.3 4.7 4.7 4.7 Debtors turnover ratio 92.4 48.4 33.7 27.7 27.9

-

32

Exhibit 1: Key financials

FY07 FY08 FY09E FY10E FY11ENet Profit 230.2 348.0 147.3 140.5 105.2EPS 53.8 43.0 18.2 17.4 13.0% Growth -20.1 -57.7 -4.6 -25.2P/E (x) 1.8 2.2 5.2 5.5 7.3P/BV (x) 0.5 0.7 0.6 0.5 0.5EV/EBITDA (x) 3.7 3.5 5.7 4.4 4.5OPM% 25.0 32.0 25.0 22.0 18.0NPM % 23.0 23.0 8.0 6.0 4.0RoNW % 39.0 36.6 12.0 10.0 7.0RoCE % 22.8 22.9 11.0 10.0 9.0 Source: Company, ICICIdirect.com Research

Analysts’ Name

Ravi Sodah [email protected] Vijay Goel [email protected]

Sales & EPS trend

0

500

1000

1500

2000

2500

3000

FY07 FY08 FY09E FY10E FY11E

Rs C

rore

0

10

20

30

40

50

60

Rs

Net Sales EPS (Rs) Stock Metrics

Bloomberg Code DCB INReuters Code DLMI.BOFace value (Rs) 2Promoters Holding 54.8%Market Cap (Rs cr) 79252 week H/L 355 / 67.2Sensex 10947Average volumes 21736 Comparative return metrics

Stock return(%) 3M 6M 12MDalmia Cem 28 1 -65Jk Cem 36 -18 -62Shree Cem 69 74 -24Orient Paper 56 46 -33 Price Trend

3080

130180230280330

Mar

-

May

-

Jul-

Sep-

Nov

-

Jan-

Mar

-

Close Price Target Price

April 20, 2009 | Cement

Initiating Coverage

Dalmia Cement (DALCEM)

Caught in equity market woes… Dalmia Cement (Bharat) (DCBL) is expanding its capacity from 3.5 million tonnes (MT) to 8 MT. All plants of the company will be located in the southern region, which is expected to have surplus supplies in the next financial year. This will lead to deterioration in the return ratio below WACC. Apart from this, DCBL has had notional loss on its investments and has highest leverage in our coverage universe. Hence, we are initiating coverage on the stock with an UNDERPERFORMER rating and one-year target price of Rs 81 per share.

Regional player The company has presence only in southern markets. Out of the expected 62 MT capacity addition at an all-India level in FY10, around 47% is coming up in the southern region, which will lead to a worsening

High debt to equity DCBL has total capex of around Rs 1250 crore and is funded by debt of Rs 1100 crore and balance through internal accruals. The company has debt equity ratio of 1.9 for FY09E, highest among our coverage universe.

High exposure to equity investments DCBL has exposure to equity market investments on which it had a notional loss of Rs 160 crore on its investment books as on December 31 2008.

High debt to increase payoff period The company is adding capacity at nearly Rs 2778/tonne. 80% of the capex has been funded through debt. The payoff period for the company after accounting for interest expense and interest accrued during the moratorium period will be close to six years. Valuations At the CMP of Rs 95, DCBL is trading at 5.2x and 5.5x its FY09E and FY10E earnings, respectively. On an EV/tonne basis, it is trading at $116/tonne and $60/tonne its FY09E and FY10E capacities, respectively. We are initiating coverage on the stock with an UNDERPERFORMER rating and a target price of Rs 81.

Current Price Rs 95

Target Price Rs 81

Potential upside -15%

Time Frame 12-15 months

UNDERPERFORMER

ICICIdirect.com | Equity Research

-

33

Company Background

Dalmia Cements (Bharat) Ltd (DCBL) was established in 1935. DCBL has two major business segments — cement and sugar. The company started its cement operations in 1939. DCBL has a presence only in the southern region. The company’s other product profile includes power, refractories and refractory products, multilayer ceramic chip capacitors, industrial alcohol and others. DCBL has a current cement capacity of 3.5 MT with a plant in Tamil Nadu. The company is in the process of expanding its cement capacity by 4.5 MT by setting up plants at Kadapa, Andhra Pradesh and Ariyalur, Tamil Nadu of 2.25 MT each. DCBL has expanded its sugar business to 22500 TCD at three locations of Uttar Pradesh with cogeneration power plant capacity of 79 MW and ethanol plant with a capacity of 80 KL per day. The company also has a 16-MW wind farm power generation unit. The power generated from this unit is utilised for consumption at the cement unit by wheeling through the state electricity grid. Exhibit 2: Revenue mix (FY08)

77%

18%

5%

Cement Sugar Others

Source: Company, ICICIdirect.com Research

Exhibit 3: Cement geographical mix (FY08)

60%27%

9%4%

Tamil Nadu Kerala Karnataka Others

Source: Company, ICICIdirect.com Research

Share holding pattern (Q3FY09)

Shareholder % holdingPromoters 54.79Institutional investors 5.06Other investors 11.00General public 29.15

Promoter & Institutional holding trend (%)

55% 55% 55% 55%

5% 5% 5% 6%

0%

20%

40%60%

80%

100%

Q4 Q1 Q2 Q3

Promoter Holding Institutional Holding

-

34

Investment concerns

Regional player The company has 100% presence in the southern markets. Out of the expected 62 MT capacity addition at an all-India level, around 47% is coming up in the southern region in FY10. This will lead to a worsening of the demand-supply scenario.

High debt to equity DCBL has a total capex of around Rs 1250 crore and is funded by debt of Rs 1100 crore with the balance through internal accruals. The company has a debt equity ratio of 1.9 for FY09E. This is the highest in our coverage universe. However, the debt repayment will start after two years. Thus, we do not expect the company to face a cash crunch for two years.

High debt to increase payoff period The company is adding capacity at nearly Rs 2778/tonne. 80% of the capex has been funded through debt. The payoff period for the company after accounting for interest expense and interest accrued during the moratorium period will be close to six years.

High exposure to equity investments The company has exposure to equity market investments on which it had notional loss of Rs 160 crore on its investment books as on December 31 2008.

High-cost coal inventories procurement till Q4FY09 Dalmia had procured imported coal at nearly $190 per tonne. We expect these high-cost coal inventories to be consumed by Q4FY09. Thus, it will depress the Q4FY09 earnings of the company. We expect the company to only benefit in terms of coal cost from Q1FY10 as imported coal prices have corrected by nearly 67.8% from their peak.

-

35

Financials

Topline to grow at 22% CAGR (FY08-FY11) Net sales is expected to grow at 23.1% CAGR (FY08-FY11) to Rs 2762.7 crore in FY11 from Rs 1482 crore in FY08 on the back of 25.2% CAGR increase in cement sales volume during the same period. Exhibit 4: Revenue to grow at 23% CAGR (FY08-FY11)

0

500

1000

1500

2000

2500

3000

FY08 FY09E FY10E FY11E

Rs c

rore

0%

10%

20%

30%

40%

50%

60%

Net Sales % Growth

Source: Company, ICICIdirect.com Research

Exhibit 5: Revenue mix

0

500

1000

1500

2000

2500

3000

FY08 FY09E FY10E FY11E

Rs c

rore

Cement Sugar Others

Source: Company, ICICIdirect.com Research

-

36

Margins The OPM is expected to decline to 17.9% in FY11 from 31.8% in FY08 on the back of a fall in cement realisations. Exhibit 6: OPM of cement and sugar business

44%

36%32%

27%

11% 11% 10%6%

0%

10%

20%

30%

40%

50%

FY08 FY09E FY10E FY11E

Cement Sugar

Source: Company, ICICIdirect.com Research

Exhibit 7: OPM & NPM

17.9%

23.5%

3.8%

31.8%

21.6%25.2%25.4%

8.4%5.9%

23.3%

0%

5%

10%

15%

20%

25%

30%

35%

FY07 FY08 FY09E FY10E FY11E

OPM% NPM %

Source: Company, ICICIdirect.com Research

Exhibit 8: EBITDA per tonne of cement and sugar business

15191389

1129920

2125 2240 2145

1181

0

500

1000

1500

2000

2500

FY08 FY09E FY10E FY11E

Rs p

er to

nne

Cement Sugar

Source: Company, ICICIdirect.com Research

-

37

Net profit The net profit is expected to decline by 33% CAGR (FY08-FY11) to Rs 105.2 crore from Rs 348 crore on account of the lower operating margin and high interest cost. Exhibit 9: Net profit to decline by 33% CAGR (FY08-FY11)

230.17

348.02

147.34 140.50105.15

050

100150200250300350400

FY07 FY08 FY09E FY10E FY11E

Rs

Net Profit

Source: Company, ICICIdirect.com Research

Return ratios to decline RoNW and RoCE are expected to decline to 7.1% and 8.9% in FY11 from 36.6% and 22.9% in FY08, respectively. Exhibit 10: RoNW & RoCE

36.6%

22.9%

7.1%10.3%

39.0%

12.1%8.9%10.0%

22.8%

10.7%

0%

10%

20%

30%

40%

FY07 FY08 FY09E FY10E FY11E

RoNW % RoCE %

Source: Company, ICICIdirect.com Research

-

38

Risks to our call

Capacity addition to drive cement volume growth by 25% CAGR (FY08-FY10) DCBL is expanding its cement capacity by 4.5 MT to 8 MT by adding two units of 2.25 MT each. Clinker production from the AP plant has already been commissioned in December 2008 whereas production from the Tamil Nadu plant is expected from July 2009. We expect the cement sales volume of DCBL to grow at 25% CAGR (FY08-FY10). This would enable the company to maintain its bottomline in FY10 despite a fall in cement prices. Location Capacity (Million Tonnes) Expected CompletionKadapa, Andhra Pradesh * 2.25 Mar-09Ariyalur, Tamil Nadu 2.25 Jul-09* Clinker unit commisioned in Dec'08 Presence in highly priced markets The company has a presence in the highly priced southern region markets, viz. Tamil Nadu, Kerala, Karnataka and Andhra Pradesh. On account of its market mix, DCBL has the highest realisations in our coverage universe. The net realisation of the company for Q3FY09 was Rs 3891/tonne and for 9MFY09 was Rs 3758/tonne. Exhibit 11: Net realisation of our coverage as of Dec 08 quarter

3455 3606 3765 35683049

36542952

3891

0

1000

2000

3000

4000

5000

ACC

Am

buja

Indi

aCe

m

Ultr

atec

h

Shre

eCe

m

JK C

em

Orie

ntPa

per

Dal

mia

Rs p

er to

nne

Source: Company, ICICIdirect.com Research

Meets entire fuel requirement through imported coal The company meets its entire fuel requirement through imported coal for its kiln and power plant operations. As imported coal prices have corrected by nearly 67.8% from their peak, the company is likely to benefit in terms of coal cost from Q1FY10. Firm sugar prices to drive sugar revenue India’s sugar inventory has declined to 4.6 MT in 2009 from 9.1 MT in 2008. The current favourable demand-supply scenario has led to a surge in sugar prices to Rs 23 per kg (ex-factory). In the short to medium term, sugar prices are likely to remain firm on the back of tight supply in India and a global deficit.

-

39

Valuations

At the CMP of Rs 95, DCBL is trading at 5.2x and 5.5x its FY09E and FY10E earnings, respectively. On an EV/tonne basis, it is trading at $116/tonne and $60/tonne its FY09E and FY10E capacities, respectively. We believe Dalmia Cement being a regional player having high debt/equity is more vulnerable to its peers in a down cycle. Also we expect the return ratios of DCBL to decline below WACC in the current down cycle. Factoring in concerns like lower return ratios, high leverage and presence in price sensitive markets of southern India, we expect Dalmia Cement to continue to trade at a steep discount to its replacement cost. Thus, we are initiating coverage on Dalmia Cement with an UNDERPERFORMER rating and a target price of Rs 81. Exhibit 12: Historical Valuations

0

2

4

6

8

10

12

FY94

FY95

FY96

FY97

FY98

FY99

FY00

FY01

FY02

FY03

FY04

FY05

FY06

FY07

FY08

FY09

FY10

FY11

P/C

EPS,

EV/

EBIT

DA

0

0.5

1

1.5

2

2.5

3

3.5

P/BV

, MCa

p/Sa

lesP/CEPS (LHS) EV/EBIDTA (LHS) P/BV (RHS) M Cap/Sales (RHS)

Source: Company, ICICIdirect.com Research

-

40

Profit and Loss Account Rs Crore Year Ending March 31 FY07 FY08 FY09E FY10E FY11E

Net Sales 986.5 1,482.0 1,752.8 2,395.6 2,762.7 % Growth 50.2 18.3 36.7 15.3 Total Expenditure 735.9 1011.0 1311.9 1879.1 2269.2 EBITDA 250.6 471.0 440.9 516.6 493.5 Other income 156.1 164.0 14.0 14.0 15.4 Depreciation 55.1 87.1 92.5 129.3 131.3 Interest 54.0 112.9 141.8 206.1 231.5 Extra ordinary items 0.0 0.0 0.0 0.0 0.0 PBT 297.6 435.0 220.5 195.1 146.0 Taxation 67.5 86.9 73.2 54.6 40.9 Reported PAT 230.2 348.0 147.3 140.5 105.2 Extra ordinary items(net of tax) 0.0 0.0 0.0 0.0 0.0 Adjusted PAT 230.2 348.0 147.3 140.5 105.2 EBITDA margin (%) 25.4 31.8 25.2 21.6 17.9 NPM % 23.3 23.5 8.4 5.9 3.8 Shares O/S (crore) 4.3 8.1 8.1 8.1 8.1 EPS (Rs) 53.8 43.0 18.2 17.4 13.0

Balance Sheet Rs Crore Year Ending March 31 FY07 FY08 FY09E FY10E FY11E Sources of funds Equity Share Capital 8.6 16.2 16.2 16.2 16.2 Reserves & Surplus 745.0 1,131.0 1,278.3 1,418.8 1,524.0 Secured Loans 930.6 1,050.1 1,700.1 1,798.1 1,918.1 Unsecured Loans 84.0 533.3 733.3 733.3 733.3 Deferred Tax Liability 129.3 163.0 163.0 163.0 163.0 Total Liability 1,897.4 2,893.5 3,890.8 4,129.3 4,354.5 Application of Funds Net Block 1,227.1 1,324.7 2,082.2 2,453.0 2,371.7 Capital WIP 116.5 501.3 673.7 0.0 0.0 Investments 378.6 613.8 613.8 613.8 613.8 Cash 103.8 87.0 73.1 412.8 607.8 Sundry Debtors 82.1 105.1 124.3 169.8 195.9 Inventories 197.5 491.6 637.9 913.7 1,103.4 Loans & Advances 292.2 433.2 512.4 700.3 807.6 Current Liabilities & Provisions 500.3 663.3 826.5 1,134.0 1,345.7 Miscellaneous Expenditure 0.0 0.0 0.0 0.0 0.0 Total Asset 1,897.4 2,893.5 3,890.8 4,129.3 4,354.5

-

41

Cash Flow Statement Rs Crore Year Ending March 31 FY07 FY08 FY09E FY10E FY11E Profit Before Tax 296.4 434.1 220.5 195.1 146.0 Depreciation 55.4 87.3 92.5 129.3 131.3 Changes In working Capital 123.1 (299.2) (81.5) (201.6) (111.4) Others (120.8) (88.8) 54.6 137.5 175.2 Cash Flow from Operating activities 354.2 133.4 286.2 260.3 341.1 Inc/Dec in Investment (66.9) 250.3 0.0 0.0 0.0 Capex (611.5) (575.2) (1,022.4) 173.5 (50.0) others (0.1) (345.3) 14.0 14.0 15.4 Cash Flow from Investing activities (678.5) (670.2) (1,008.4) 187.5 (34.6) Inc/Dec in capital 117.3 90.6 0.0 0.0 0.0 Inc/Dec in Loan Funds 333.1 569.3 850.0 98.0 120.0 Others (81.2) (139.8) (141.8) (206.1) (231.5) Cash Flow from Financing activities 369.2 520.1 708.2 (108.1) (111.5) Net Inc/dec in cash 44.8 (16.7) (14.0) 339.7 195.0 Opening Balance of Cash 58.9 103.7 87.0 73.0 412.7 Closing Balance of Cash 103.7 87.0 73.0 412.7 607.8

Ratios Year Ending March 31 FY07 FY08 FY09E FY10E FY11E EPS 53.8 43.0 18.2 17.4 13.0 Cash EPS 66.7 53.8 29.7 33.4 29.2 OPM (%) 25.4 31.8 25.2 21.6 17.9 NPM (%) 23.3 23.5 8.4 5.9 3.8 Debt/Equity 1.3 1.4 1.9 1.8 1.7 RoCE (%) 22.8 22.9 10.7 10.0 8.9 RoNW (%) 39.0 36.6 12.1 10.3 7.1 Valuation Ratios P/E (x) 1.8 2.2 5.2 5.5 7.3 P/BV (x) 0.5 0.7 0.6 0.5 0.5 EV/EBITDA (x) 3.7 3.5 5.7 4.4 4.5 Turnover ratios Fixed asset turnover ratio 0.6 0.8 0.6 0.7 0.8 inventory turnover ratio 3.7 2.1 2.1 2.1 2.1 Debtors turnover ratio 9.0 9.6 10.6 11.1 11.6

42

Analysts’ Name

Ravi Sodah [email protected] Vijay Goel [email protected]

Sales & EPS trend

1000

2000

3000

4000

FY07

FY08

FY09

E

FY10

E

FY11

E

Rs C

rore

15

20

25

R

Sales EPS Stock Metrics

Bloomberg Code ICEM IN Reuters Code ICMN.BO Face value (Rs) 10 Promoters Holding 28 Market Cap (Rs cr) 3680 52 week H/L 195 / 68 Sensex 10947 Average volumes 252982

Comparative return metrics

Stock return (%) 3M 6M 12MIndia Cement 18 35 -30ACC 25 28 -23Ambuja Cements 18 47 -25Ultratech Cement 53 52 -28 Price Trend

40

90

140

190

Apr-0

8

Jun-

08

Aug-

08

Oct-0

8

Dec-

08

Feb-

09

Apr-0

9

Close Price Target Price

April 20, 2009 | Cement

Initiating Coverage

India Cement (INDCEM)

Fairly valued… India Cement (ICL) is currently trading at lower valuations on EV/tonne and EV/EBIDTA basis than the last down-cycle, in which it incurred losses due to higher leverage. However, in terms of P/BV, Mcap/sales and normalised P/E it is still trading at a premium to the last down cycle. Even on a relative valuations basis, it is richly valued compared to north-based players. Thus, we are initiating coverage on the stock with a HOLD rating and price target of Rs 110 per share.

To benefit from decline in coal prices Imported coal meets approximately 70% of ICL’s fuel requirement. The prices of imported coal have declined by 67.6% to $57 per tonne from their peak of $177 per tonne. The benefit of the decline in coal prices is likely to be visible from Q4FY09.

Dependence on grid power India Cement (ICL) does not have captive power plants (CPPs) at any of its unit except for a waste heat recovery power plant (of 8 MW), wind power (of 10 MW) and DG sets. However, it has power supply arrangement with APGPCL and Coromondel Power Company for the rest of the requirement.

FCCB may require Rs 575 crore cash outflow in FY12 ICL has outstanding foreign currency convertible bonds (FCCBs) of US475 million, which are to be converted at the price of Rs 305 or are redeemable at 147.7% of its face value. Thus, this could result in a cash outgo of Rs 575 crore (i.e. approximately half of the reported EBITDA of FY08) in May 2011.

Valuations At the CMP of Rs 120 per share, the stock is trading at 6.5x and 6.4x its FY09E and FY10E earnings, respectively. It is trading at an EV/tonne of $87 and $60 its FY09E and FY10E capacities, respectively. We are initiating coverage on the stock with a HOLD rating and a price target of Rs 110 per share.

Current Price Rs 120

Target Price Rs 110

Potential upside -9%

Time Frame 12 months

HOLD

Exhibit 1: Key Financials

Year Ending March 31 FY07 FY08 FY09E FY10E FY11E

Net Profit (Rs Cr) 478.8 661.3 523.8 535.7 527.1

EPS (Rs) 18.4 23.5 18.6 19.0 18.7

% Growth 27.6 -20.8 2.3 -1.6

P/E (x) 6.6 5.2 6.5 6.4 6.5

P/BV (x) 2.2 1.3 1.1 1.0 0.9

EV/ 6.6 4.2 3.9 3.6 3.2 OPM(%) 32.6 35.4 30.4 27.8 25.2

NPM (%) 21.2 21.7 15.4 14.5 13.2

RoNW (%) 37.4 32.9 18.8 16.8 14.6

RoCE (%) 20.2 24.3 18.6 17.4 15.8 Source: Company, ICICIdirect.com Research

ICICIdirect.com| Equity Research

43

Company background Established in 1946, India Cement (ICL) is among the largest players in South India, with a cement capacity of 10.8 million tonnes (MT). The company has seven plants of which four are in Andhra Pradesh and three are in Tamil Nadu. India Cement’s key markets are Andhra Pradesh, Tamil Nadu, Kerala, parts of Karnataka and Maharashtra. ICL has historically been a south-based player. However, going forward, it is in the process of diversifying its presence by venturing into North India.

India Cement sells its cement under the brand name of ’Sankar Super Power’, ‘Coromandel Super Power’ and ‘Raasi Super Power’.

India Cement has acquired the Chennai franchisee in the Indian Premier League (IPL), the 20:20 format tournament started by the Board of Control of Cricket in India (BCCI) for US$91 million in January 2008. The investment in IPL was done by the company from the point of view of advertising its brands all across the country.

Exhibit 2: Volume break up

36%

24%

16%

15%

7% 2%

Tamil Nadu Andhra Pradesh Kerala

Karnataka Maharashtra Others

Source: Company, ICICIdirect.com Research

Shareholding pattern (Q3FY09)

Shareholder % holdingPromoters 28.0Institutional investors 46.9Other investors 17.9General public 7.2

Promoter & Institutional holding trend (%)

35% 36% 37% 37%

28%28%27% 28%

0%

20%

40%

Q4 Q1 Q2 Q3

Promoter Holding Institutional Holding

44

Investment Rationale

To benefit from decline in coal prices Imported coal meets approximately 70% of ICL’s coal requirements. The prices of imported coal have declined by 66% to $57 per tonne from their peak of $177 per tonne. The benefit of decline in coal prices is likely to be visible from Q4FY09. India Cement has also acquired two second-hand dry bulk carriers of about 40,000 tonne each to transport coal from international markets. However, due to sharp corrections in sea freights (benchmark index Baltic Dry Index has corrected around 80% from its peak), we do not expect any significant saving in transportation cost of coal. Nevertheless, it will hedge the company from the volatility in sea freights.

Capacity additions to contribute to volume growth

ICL is in the process of increasing its cement capacity from 10.8 MT to 14.3 MT through debottlenecking and brownfield expansions. India Cement will be further adding 1.5 MT in Rajasthan. The company has deferred its 2 MT greenfield plant in Himachal Pradesh for the time being. On account of capacity additions, we expect India Cement’s volumes to grow at a CAGR of 10.7% between FY08 - FY11 period.

Exhibit 3: Power & fuel cost per tonne

600

750

900

1050

FY06

FY07

FY08

FY09

E

FY10

E

FY11

E

Rs p

er to

nne

Source: Company, ICICIdirect.com Research

Exhibit 4: Cement sales volumes (in million tonnes)

9.2 9.1

11.012.5

0

2

4

6

8

10

12

14

FY08 FY09E FY10E FY11E

Cem

ent S

ales

vol

umes

Source: Company, ICICIdirect.com Research

45