NoN-Tariff Barriers iN The TraNspor T aNd LogisTics...

120

| RESEARCH REPORT | NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA by Arpita Mukherjee & Smita Miglani August, 2010

Transcript of NoN-Tariff Barriers iN The TraNspor T aNd LogisTics...

| ReseaRch RepoRt |

NoN-Tariff Barriers iN The TraNsporT aNd LogisTics secTors: iNdia

by Arpita Mukherjee & Smita Miglani

August, 2010

contents

acknowledgements i

abbreviations ii

introduction 1

1. coverage of Transport and Logistics services 5

2. Transport and Logistics services in india: an overview 7

2.1 Road Transport 12

2.2 Railways 16

2.3 Air Transport 17

2.4 Maritime Transport 19

2.5 Auxiliary and Logistics Services 21

2.6 Express Delivery and Courier Services 22

3. india-eU Trade, investment and collaboration 25

3.1 Trade in Goods and Services and Investment Flows 26

3.1.1 Trade in Goods 26

3.1.2 Trade in Services 30

3.1.3 Bilateral Investment Flows between India and the EU 32

3.2 The Primary Survey 33

3.3 India-EU Collaboration: Implications for the Transport Sector 43

3.4 Scope for Enhancing Trade, Investment and Collaboration 46

4. Barriers faced by eU companies in india 49

5. addressing Barriers through international Negotiations 63

6. reform requirements in india 69

7. conclusion and the way forward 73

references 77

appendix a 84

appendix B 90

appendix c 108

Non-Tariff Barriers in the Transport and Logistics

sectors: india

List of Tables

Table 2.1: Cumulative FDI Inflows in the Transport Sector: April 2000 – April 2010 8

Table 2.2: FDI Policy in India: Transport and Logistics 11

Table 2.1.1: Automobile Production Trends (Number of Vehicles) 13

Table 3.1.1.1: Leading EU Countries Exporting to India and Products Exported 29

Table 3.1.2.1: Ranking of India and the EU in Global Services 30

Table 3.1.2.2: India’s Trade in Services with the EU in 2008 31

Table 3.1.3.1: FDI Inflows from the EU: January 2000 – November 2008 32

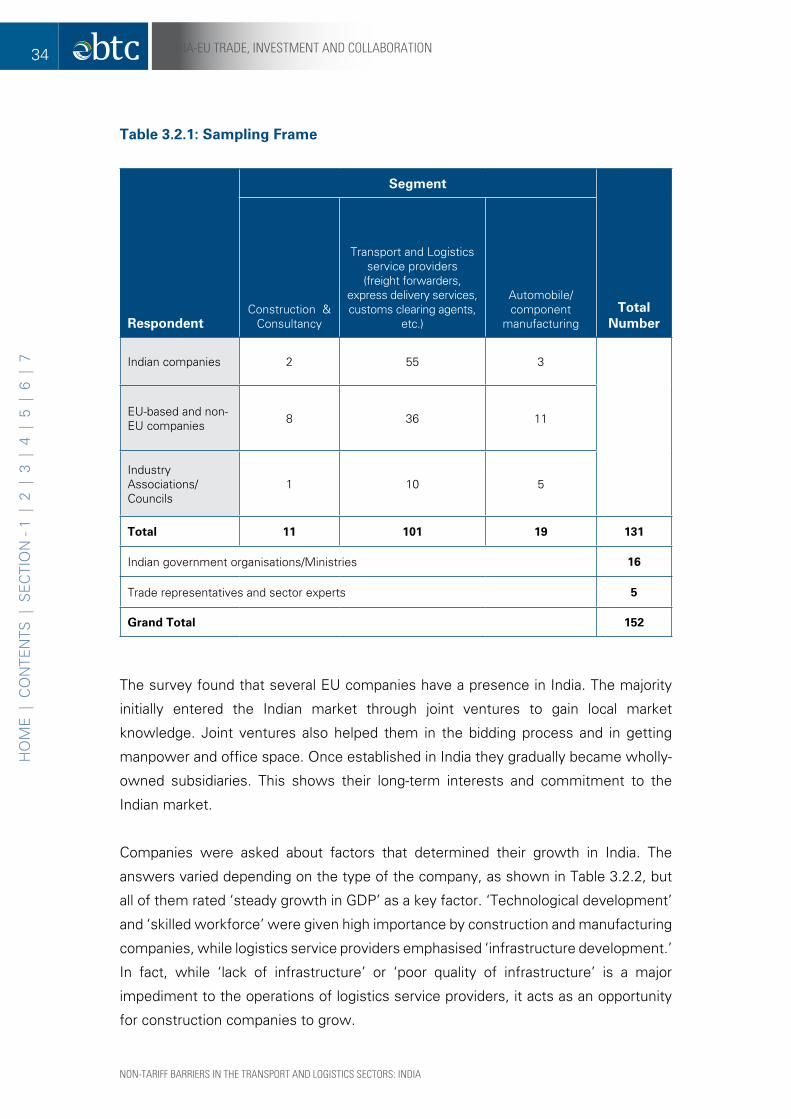

Table 3.2.1: Sampling Frame 34

Table 3.2.2: Perception Ranking of Factors Responsible for Growth in India 35

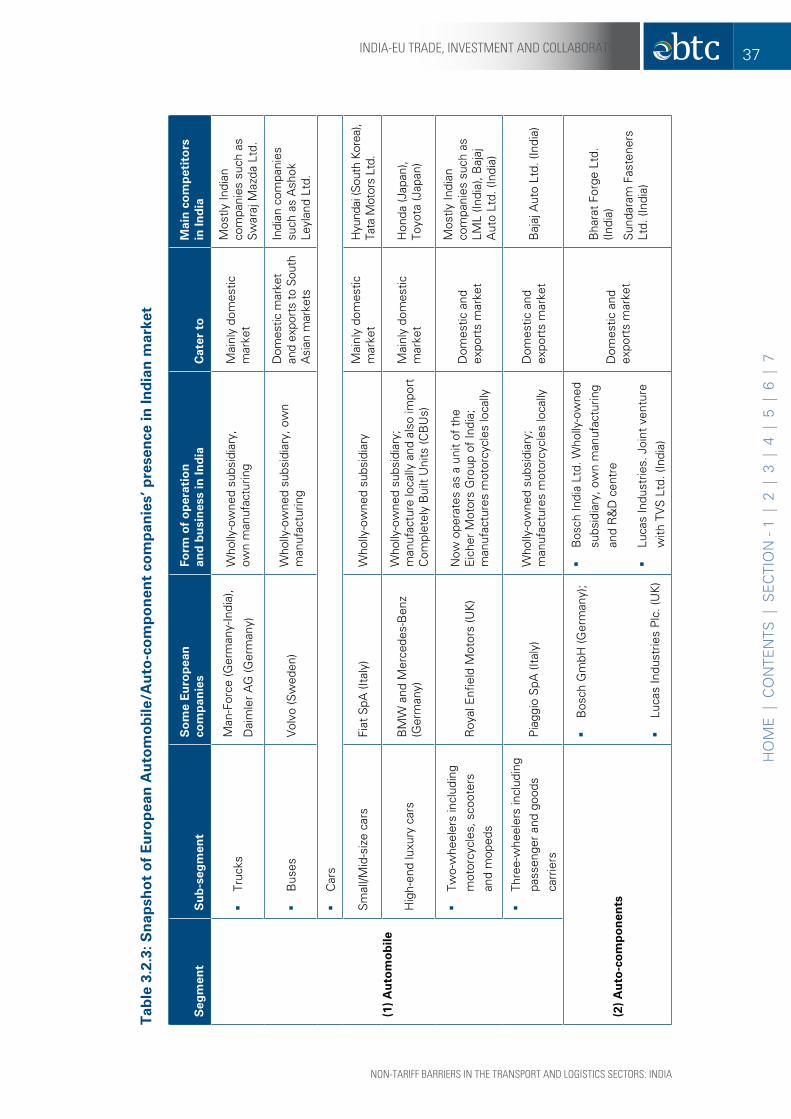

Table 3.2.3: Snapshot of European Automobile/Auto-component companies’ presence in Indian market 37

Table 3.2.4: Snapshot of European Construction and Consultancy (C&C) companies’ presence in the Indian market 39

Table 3.2.5: Snapshot of European Logistics Service Providers (freight forwarders, express delivery services providers, customs clearing agents, etc.) in India 42

Table 3.4.1: Technical Standards for Logistics Sector: India and the EU 47

Table 4.1: Ranking on World Bank’s Doing Business Report (2010) 50

Table 4.2: Rankings for BRIC countries, Germany and Poland on Selected Parameters 51

Table 4.3: World Bank’s Logistics Performance Index (LPI): Ranks of Selected EU Member Countries and India 51

Table 4.4: Barriers Faced by EU companies in India by Nature of Business 53

Table 4.5: Traffic Handled at Major Indian Ports versus Port of Rotterdam 57

Table 4.6: Setting up a Warehouse: Procedures and Days Required 59

Table 5.1: Commitments and Revised Offers in Transport and Logistics: India and the EU 67

List of figures

Figure 2.1: Investment Growth Rates (at constant 1999-00 prices) 10

Figure 3.1.1.1: India’s Major Supplier Countries and Export Destinations for Transportation Equipment (2007-08) 27

Figure 3.1.1.2: India-EU Trade in Transportation Equipment 28

Figure 3.1.1.3: Indian Exports to EU Member States and EU Exports to India in 2007-08 28

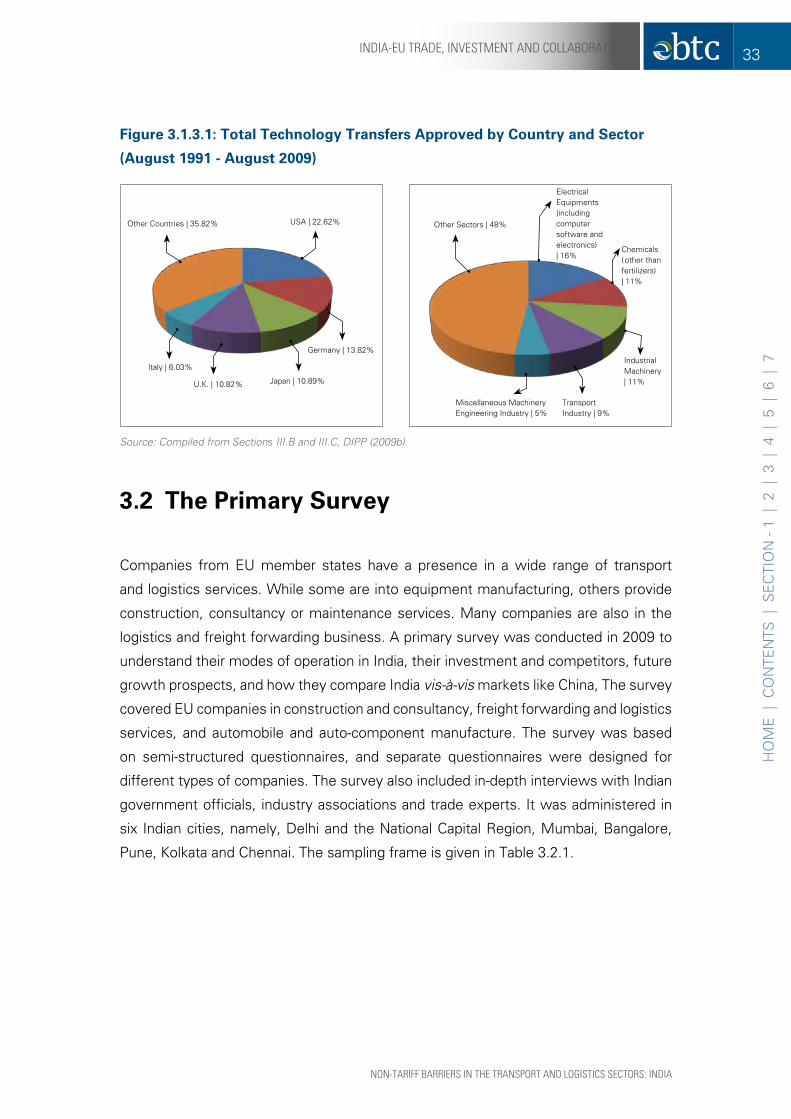

Figure 3.1.3.1: Total Technology Transfers Approved by Country and Sector 33

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

acknowledgements

We are grateful to Dr. Kumar, Director and CE, ICRIER, for giving us the opportunity

to work on the relationship between India and European Union and to our colleague

Ramneet Goswami for her contribution to this paper. Thanks are due to Prasid

Chakraborty of SRG Consultancy Marketing Planning Services and his team for

conducting the survey and R.V. Anuradha for providing the legal input. We would also

like to thank the survey participants for their time and valuable inputs. Dr. Renu Gupta

for copyediting and Anil Kumar for formatting deserve special mention.

For any queries related to this paper, please contact Arpita Mukherjee, Professor,

ICRIER at [email protected] or Smita Miglani, Researcher, ICRIER at smiglani@icrier.

res.in. Tel: (91-11) 43112400, Fax: (91-11) 24620180.

JeL classification: F13, F14, F53, L74, L91, L92, L93, L98, N75

Keywords: Transport, Logistics, Trade, India, EU, Non-Tariff Barriers

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

i

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

abbreviations

3pL Third Party Logistics

4pL Fourth Party Logistics

aai Airports Authority of India

aTf Aviation Turbine Fuel

BoT Build-Operate-Transfer

BTia Broad-based Trade and Investment Agreement

cfs Container Freight Stations

cha Custom House Agents

cii Confederation of Indian Industries

cNg Compressed Natural Gas

coNcor Container Corporation of India

cso Central Statistical Organisation

csT Central Sales Tax

cWc Central Warehousing Corporation

c&f Clearing and Forwarding

dfc Dedicated Freight Corridor

dgca Director General of Civil Aviation

dgfT Director General of Foreign Trade

dgs Director General of Shipping

dipp Department of Industrial Policy and Promotion

edi Electronic Data Interchange

eU European Union

fci Food Corporation of India

fdi Foreign Direct Investment

fipB Foreign Investment Promotion Board

fTa Free Trade Agreement

fTWZ Foreign Trade Warehousing Zones

gaTs General Agreement on Trade in Services

gdp Gross Domestic Product

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

ii

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

gQ Golden Quadrilateral

grT Gross Registered Tonnage

gsT Gross Tonnage

gT Goods and Services Tax

iaTa International Air Transport Association

icd Inland Container Depots

iT Information Technology

JNpT Jawaharlal Nehru Port Trust

LcV Light Commercial Vehicles

MfN Most Favoured Nation

MMTa Million Metric Tonnes per Annum

MT Million Tonnes

MTg Multimodal Transport of Goods

MTo Multimodal Transport Operator

Nhai National Highways Authority of India

NhBf National Highways Builders Federation

Nhdp National Highway Development Programme

ppp Public-Private Partnership

psU Public Sector Undertaking

pWd Public Works Department

r&d Research and Development

rBi Reserve Bank of India

spV Special Purpose Vehicle

TaMp Tariff Authority of Major Ports

TeU Twenty-foot Equivalent Units

TciL Transport Corporation of India Limited

Usa United States of America

UsTr United States Trade Representative

WTo World Trade Organization

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

iii

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

introduction

In an emerging economy like India, transport and logistics services play a crucial role

in boosting economic growth, opening new market opportunities, facilitating trade

and improving the overall competitiveness of the domestic industries. Prior to 1991,

India followed a closed-door policy. During that time, the government was the main

provider of transport services. Although there was some private participation in certain

transport and logistics services such as trucking services and freight forwarding, the

scale of private investment was low and the logistics chain was highly fragmented.

Prolonged government monopoly led to monopoly-induced inefficiencies and low

productivity. In the 1990s, when India embarked on an ambitious reform programme,

trade volumes increased but the transport infrastructure was inadequate to handle it.

Moreover, government funding could no longer support the growing need for transport

and the sector was gradually liberalised to attract private/foreign investment. Thus,

liberalisation and reforms in transport services became an integral part of the overall

reform programme. Increase in trade volumes also led to considerable pressure on the

operating environment of the existing transport infrastructure, forcing it to adopt new,

improved and more reliable technology. Technological developments and innovative

business practices led to a gradual integration of different modes of transport and the

logistics chain.

Post-reforms, India is one of the fastest growing economies of the world, growing at

an average annual rate of over 7 per cent since 2004. It has been estimated that if the

Indian economy grows at around 7 per cent on average, the transport demand will

grow by 10 per cent annually.1 Thus, India is under continuous pressure to upgrade

the transport and logistics infrastructure. Unlike countries like China, government

investment in transport is declining and the share of private investment is increasing.

Foreign investment in the transport and logistics sector also increased significantly.

This sector accounted for around 14 per cent of the cumulative Foreign Direct

Investment (FDI) inflows between April 2000 and April 2010.

The growing Indian market has attracted many European companies that are now

among the major investors in the transport and logistics sectors in India. They

operate across different segments of transport such as transport-related construction,

automobile and component manufacturing, freight forwarding and express delivery,

1 Directorate General of Shipping (2004).

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

1INTRODuCTION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

and maintenance and consultancy services, among others. The modes of operation

vary from wholly-owned subsidiaries to joint ventures and representative offices.

Many of them do projects for the Indian central, state and local governments.

India and the European Union (EU) are currently negotiating a Broad-based Trade

and Investment Agreement (BTIA) which is likely to be signed by the end of the

year 2010. This agreement will cover goods, services, investment, government

procurement, and subsidies, among others and is likely to enhance trade, investment

and collaboration between India and EU member states by removing tariff and non-

tariff barriers. The EU is a major proponent of liberalising transport and logistics

sectors in its multilateral and bilateral agreements and it will put pressure on India to

remove the trade barriers. At present, India’s commitments in transport and logistics

services in the WTO (World Trade Organization) and bilateral agreements (such as the

India-Singapore Comprehensive Economic Co-operation Agreement) is lower than the

level of autonomous liberalisation. This provides opportunities for the EU to secure

liberalisation commitments through the BTIA.

In the above context, this paper examines the non-tariff barriers faced by companies

from EU member states in the transport and logistics sectors of India. The barriers

include market access barriers (such as FDI restrictions), national treatment barriers

(or discriminatory barriers such as subsidies to local companies), regulatory barriers

(i.e., barriers relating to regulation, licensing, technical standards, etc.) and other

barriers (such as anti-competitive practices and pricing). The paper covers railway

transport, road transport, air transport, maritime transport, storage, warehousing

and other auxiliary services, and express delivery services. The paper does not cover

inland waterways since it is not an important mode of transportation in India and the

presence of European companies is limited.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

2 INTRODuCTION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

The structure of the paper is as follows:

�� Section 1 provides the coverage of transport and logistics services.

�� Section 2 provides an overview of the transport and logistics sector in India,

emphasising recent trends and developments, the regulatory framework,

extent of liberalisation and growth prospects.

�� Section 3 analyses India-EU trade, investment and collaboration in transport and

logistics services.

�� Section 4 lists the barriers faced by European companies in India.

�� Section 5 examines how these barriers can be addressed through international

negotiations, specifically the India-EU BTIA.

�� Section 6 discusses the reforms that are required to improve productivity,

efficiency and global competitiveness of the transport and logistics sector in

India and enable the country to benefit from liberalisation under the BTIA.

�� Section 7 draws the main conclusions.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

3INTRODuCTION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

1. coverage of Transport and Logistics services

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

5COvERAGE OF TRANSPORT AND LOGISTICS SERvICES

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

The definition of transport and logistics services and its coverage has evolved over

the years. It broadly covers different forms of transport such as roads, railways,

air, and maritime; transport infrastructure like ports and airports; transport-related

construction like road construction; and services auxiliary to different modes of

transport like storage, warehousing and cargo handling. Logistics can be defined as

“the process of planning, implementing, and controlling the efficient, cost-effective

flow and storage of raw materials, in-process inventory, finished goods and related

information from point of origin to point of consumption so as to meet customer

requirements.”2 With technological developments, emergence of multimodal

transport facilities and development of global supply chains, transport and logistics

services have been integrated with other services such as information technology (IT)

and new transport and logistics services are evolving. For instance, Express Delivery

Services (EDS) have now evolved as a specialised form of logistics services which

include integrated door-to-door transport and quick delivery of time-definite shipments

of documents, samples, parcels, etc.

The EU follows a broad definition of logistics services which includes core logistics

services such as storage and warehousing, related freight logistics services like

maritime freight transport services, and non-core logistics services such as courier/

express delivery services and technical testing services. The EU seeks to get

commitments in a broad range of transport and logistics services from its trading

partners in the WTO and Free Trade Agreements (FTAs) so that companies from EU

member states have wider market access and are able to offer integrated services.

The EU also seeks non-discriminatory access3 to transport infrastructure and facilities

and regulatory certainty and transparency.

2 CII-KPMG (2007).

3 Non-discriminatory access means there should not be any preferential treatment to domestic service suppliers (for example, subsidies, lower port/airport charges, cargo reservations, etc.).

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

6 COvERAGE OF TRANSPORT AND LOGISTICS SERvICES

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

2. Transport and Logistics services in india: an overview

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

7TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

The transport and logistics sector in India witnessed significant growth in the post-

liberalisation period. Since 1991, India’s international trade has increased almost

nine-fold, creating a huge demand for transport. This growth was further propelled

by the development of India as a manufacturing hub and the growth of services

sectors like retail. At present, the transport sector contributes significantly to India’s

Gross Domestic Product (GDP) (around 6.4 per cent in 2007-08), employment (about

40 million people in 2007-08)4 and FDI inflows (Table 2.1). The logistics industry is

valued at approximately $90 billion (€63.83 billion),5 employing 45 million people and

growing at the rate of 30-40 per cent per annum.6 It is expected that the demand for

transport and logistics will continue to grow as the Indian economy is on a high growth

trajectory, the domestic market is unsaturated and the country needs investment in

transport infrastructure. The overall logistics market is estimated to reach a size of

over $125 billion (€88.65 billion) by the end of 2010.7

Table 2.1: cumulative fdi inflows in the Transport sector: april 2000 – april 2010

s. No. sector

amount of fdi inflows (in billion) per cent share in

india’s Total fdi inflows(in €) (in $)

1. Construction Activities 5.77 8.14 7.19

2. Automobile Industry 3.27 4.61 4.16

3. Ports 1.15 1.62 1.33

4. Sea transport 0.49 0.69 0.63

5. Air transport (including Air Freight) 0.17 0.24 0.21

6. Earth-moving machinery 0.09 0.13 0.11

7. Railways-related components 0.08 0.11 0.10

Total inflows 11.03 15.55 13.73

india’s Total fdi inflows 79.77 112.47

Source: DIPP Fact Sheet on FDI - From August 1991 to April 2010. Government of India, http://dipp.nic.in/fdi_statistics/india_FDI_April2010.pdf

Note: Figures are calculated using the average exchange rate for fiscal year 2009-10: $1 = Є0.7092. Source: www.oanda.com

4 CSO Statistical Abstracts (2009); CII-KPMG (2007); ADB (2007).

5 This figure is calculated using the average exchange rate for the fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

6 Colliers International (2009).

7 CII-KPMG (2007). This figure is calculated using the average exchange rate for fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

8 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

For domestic transportation, road transport is the dominant mode of transport accounting

for over two-third of the contribution of the transport sector to the GDP. Around 90 per

cent of India’s international trade is through maritime transport, most of the remainder

is through air transport, and less than one per cent is through roads and railways with

neighbouring South Asian Association for Regional Cooperation (SAARC) countries like

Bangladesh, Nepal, Bhutan and Pakistan with whom India shares land borders.

Over the years, the transport industry has been undergoing structural changes and

modernisation. Bulk cargo has been replaced by containerised cargo and multimodal

transportation has developed. Companies now provide integrated logistics services

and the use of Electronic Data Interchange (EDI) and Information Technology (IT)

has improved the operational efficiency of this sector. There has been a decline in

obsolete assets, and improvements in the self-financing capacity of the sector and

commercial management of transport assets and operations. Use of sophisticated

technology requires integrated service providers and skilled personnel, which can

provide services across the value chain. The fragmented market in certain segments

such as trucking is gradually becoming consolidated.

With the development of the logistics industry and just-in-time delivery, the share

of traffic by different modes of transport has changed. The share of road transport

for both passenger and freight traffic has increased, while that of the railways has

decreased.8

Liberalisation in the 1990s brought changes in the transport policy. From being a social

sector, transport is now treated as an economic sector which can facilitate growth

and alleviate poverty. The government’s role gradually changed from a direct provider

to a facilitator. The government has taken various measures to encourage private

participation, including innovative public-private partnership (PPP) models, and allowing

the private sector to charge users and avail of tax concessions. The government

is also taking measures to streamline customs and excise procedures, implement

EDI systems and liberalise the regulatory regime to facilitate private investment. As

a result of these measures, private/foreign participation in the Indian transport and

logistics sector has increased. However, the government is still a major investor in

this sector, especially in transport infrastructure. For instance, in the Eleventh Five-

Year Plan (2007-12), total investment in transport and logistics sectors9 is projected

8 The share of road transport increased from 50 per cent of freight traffic and 80 per cent of passenger traffic in 1990-91 to 65 per cent of freight traffic and 85 per cent of passenger traffic, respectively, by the end of 2006-07.

9 It includes roads and bridges, railways (including metro rail), ports, airports and storage.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

9TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

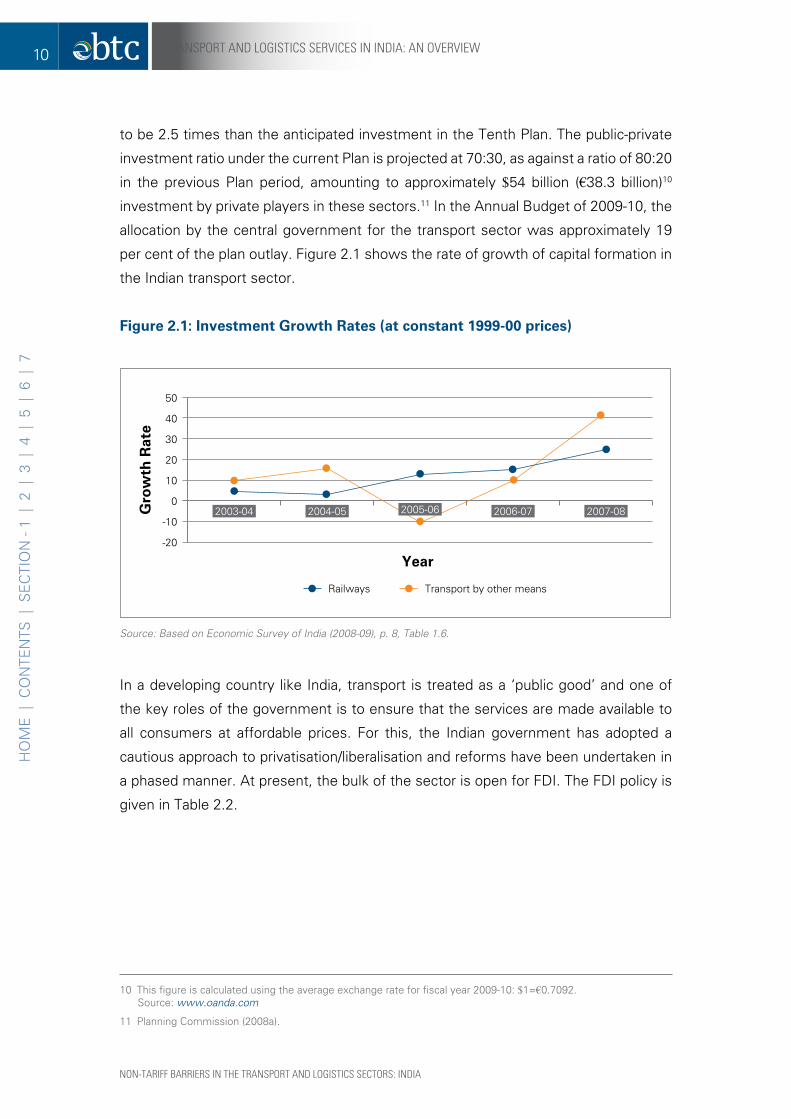

to be 2.5 times than the anticipated investment in the Tenth Plan. The public-private

investment ratio under the current Plan is projected at 70:30, as against a ratio of 80:20

in the previous Plan period, amounting to approximately $54 billion (€38.3 billion)10

investment by private players in these sectors.11 In the Annual Budget of 2009-10, the

allocation by the central government for the transport sector was approximately 19

per cent of the plan outlay. Figure 2.1 shows the rate of growth of capital formation in

the Indian transport sector.

figure 2.1: investment growth rates (at constant 1999-00 prices)

2003-04 2004-05

Year

50

40

30

20

10

0

-10

-20

gro

wth

rat

e

2006-07 2007-082005-06

Railways Transport by other means

Source: Based on Economic Survey of India (2008-09), p. 8, Table 1.6.

In a developing country like India, transport is treated as a ‘public good’ and one of

the key roles of the government is to ensure that the services are made available to

all consumers at affordable prices. For this, the Indian government has adopted a

cautious approach to privatisation/liberalisation and reforms have been undertaken in

a phased manner. At present, the bulk of the sector is open for FDI. The FDI policy is

given in Table 2.2.

10 This figure is calculated using the average exchange rate for fiscal year 2009-10: $1=€0.7092. Source: www.oanda.com

11 Planning Commission (2008a).

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

10 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

Table 2.2: fdi policy in india: Transport and Logistics

sector fdi policy

Road Transport 100 per cent FDI is allowed through the automatic route.

Air Transport (Airlines) �� 49 per cent FDI is allowed in domestic airlines through the automatic route, subject to no direct or indirect equity participation by foreign airlines.

�� Foreign airlines are not allowed to participate directly/ indirectly in the equity of an Air Service Undertaking engaged in operating scheduled, non-scheduled and chartered airlines.

�� FDI up to 74 per cent and investment by Non-Resident Indians (NRIs) up to 100 per cent is allowed in non-scheduled airlines, chartered and cargo airlines through the automatic route. Foreign airlines are allowed to participate in the equity of companies operating cargo airlines.

�� FDI up to 74 per cent and investment by NRIs up to 100 per cent is allowed through the automatic route in ground handling services.

�� 100 per cent FDI is allowed for maintenance and repair organisations.

�� Helicopter services/seaplane services requiring Director General of Civil Aviation (DGCA) approval- FDI up to 100 per cent is allowed through the automatic route.

�� FDI up to 74 per cent is permitted through automatic approvals in existing airports. FIPB approval is required for FDI beyond 74 per cent. 100 per cent FDI allowed for Greenfield projects.

Railways Public monopoly; FDI is not allowed in passenger and freight transportation and pushing and towing services. It is allowed in maintenance and repair of rail transport equipment and supporting services and railway-related components, warehousing, and freight corridors.

Services Auxiliary to all Modes of Transport

100 per cent FDI is allowed through the automatic route in cargo-handling services, storage and warehousing services and freight forwarding services.

Courier and express services (only for carrying packages, parcels and other items which do not come within the ambit of the Indian Post Office Act, 1898)

100 per cent FDI is allowed through the FIPB route subject to existing laws and exclusion of activity relating to distribution of letters, which is exclusively reserved for the state.

Source: Compiled by authors from Manual on FDI. http://dipp.nic.in/manual/FDI_Manual_text_Latest.pdf and http://www.investmentcommission.in/sector.htm

Note: (a) FDI through the automatic route implies that it does not require prior approval either by the Government of India or the Reserve Bank of India (RBI); (b) Foreign Investment Promotion Board (FIPB) is under the jurisdiction of the Indian Ministry of Finance.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

11TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

India has a quasi-federal governance structure – the central, state and local

governments have distinct responsibilities and all of them regulate the transport and

logistics sector. The division of power and responsibilities is outlined in the Indian

Constitution and certain sectors are under the jurisdiction of the central government,

while others are under the jurisdiction of the state government. There are also certain

areas of joint jurisdiction. This has resulted in multi-layered administration systems

and multiple regulations. The central government is responsible for railways, national

highways, major ports, international shipping, civil aviation, and inland waterways.

State governments are responsible for state and rural roads, minor ports and coastal

shipping, inland water transport, urban transport and trucking, inter-city bus services,

etc. In areas such as rural roads, the state governments work closely with the local/

municipal bodies and the central government. Local municipal bodies are responsible

for urban planning and infrastructure. They also sometimes regulate traffic such as

truck entry timings within city limits. The key ministries and departments of the central,

state and local government and regulations relevant for the transport and logistics

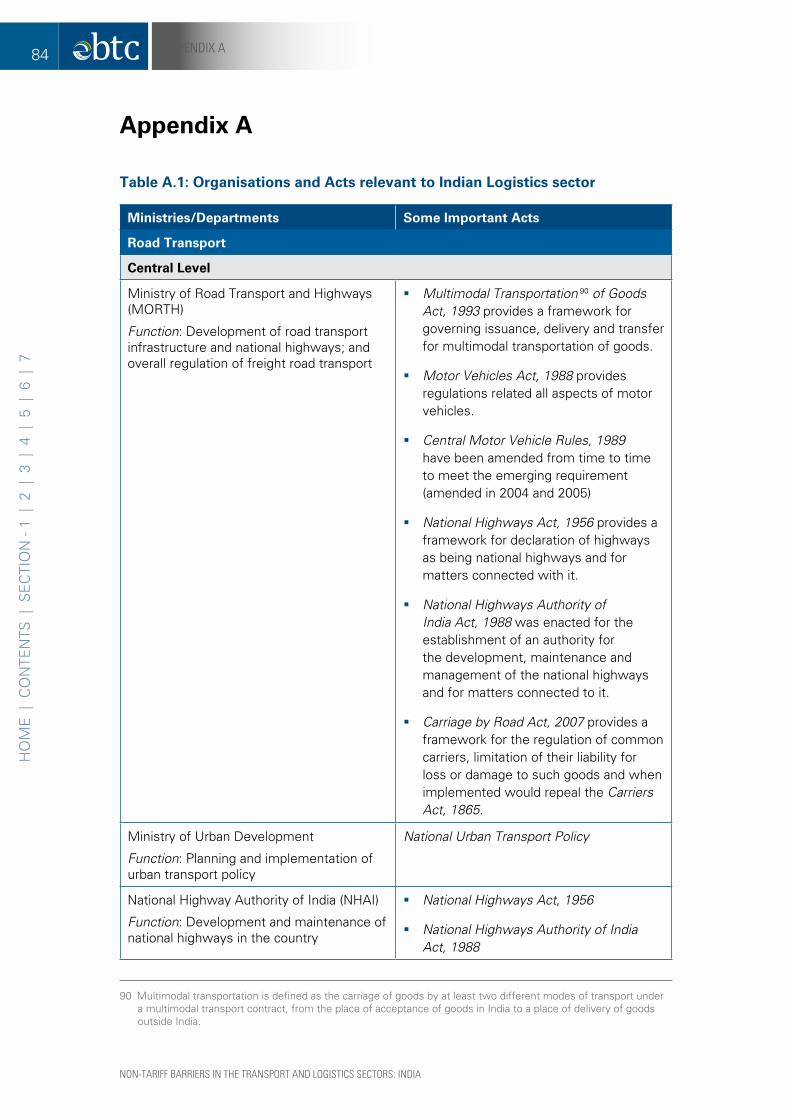

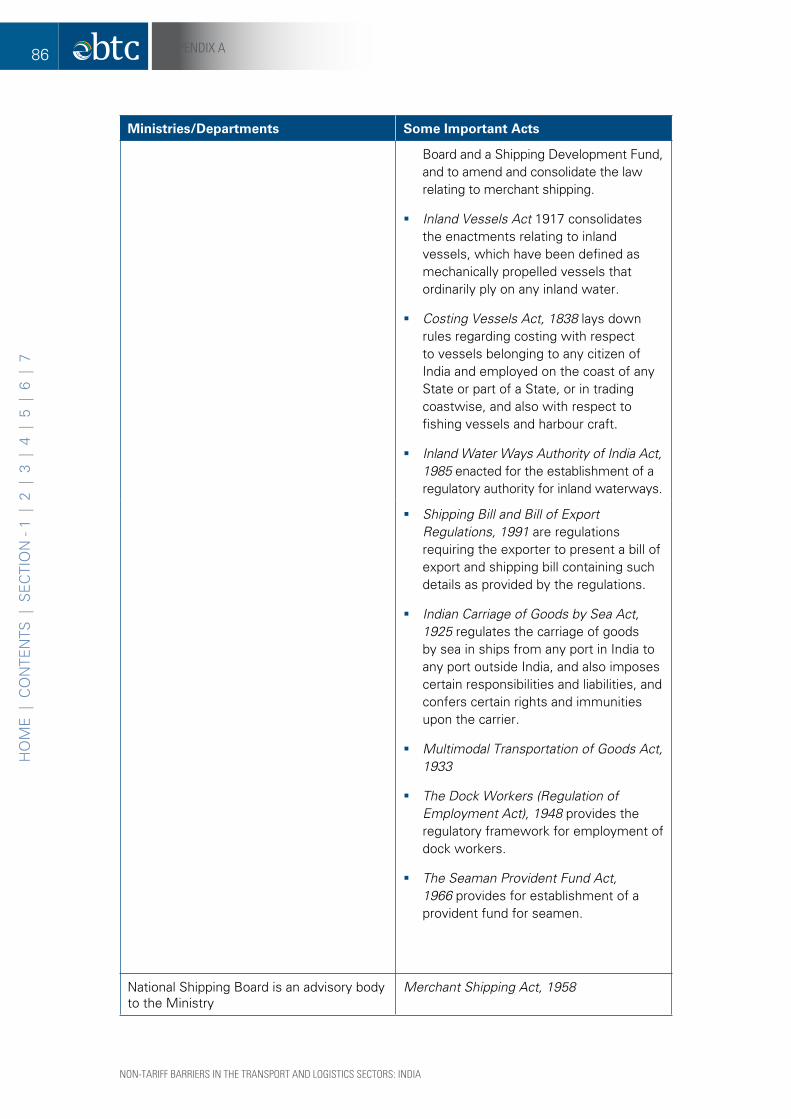

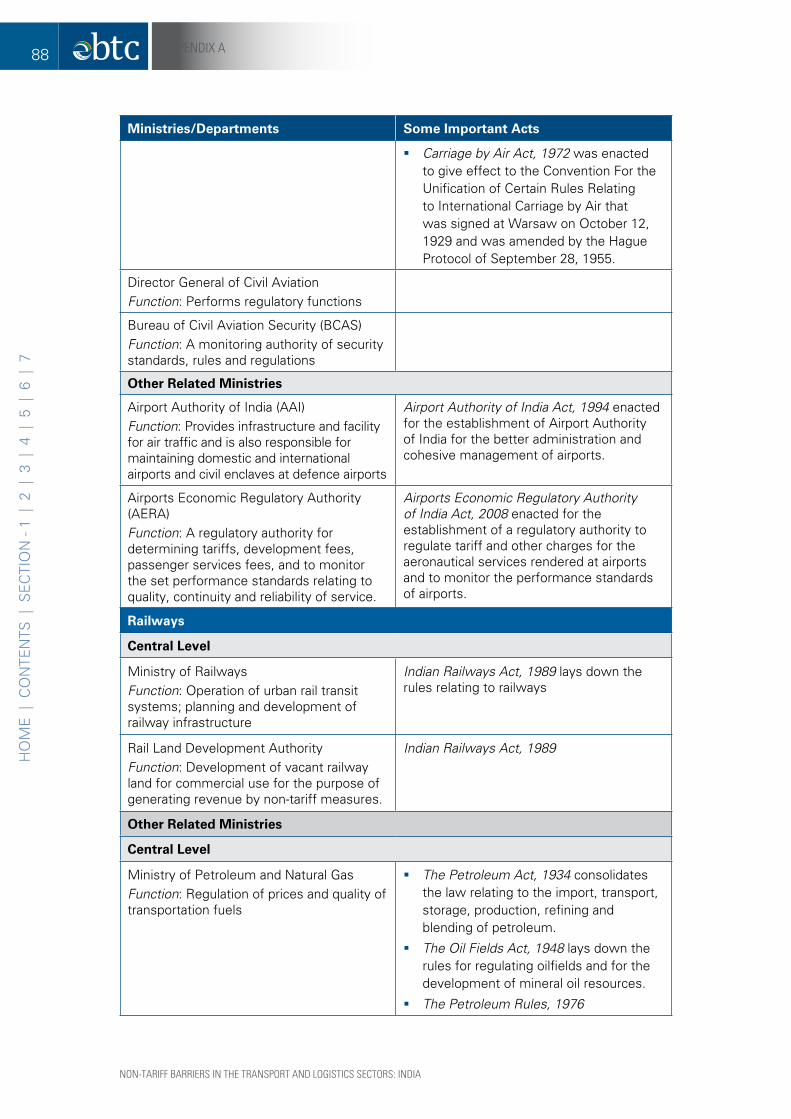

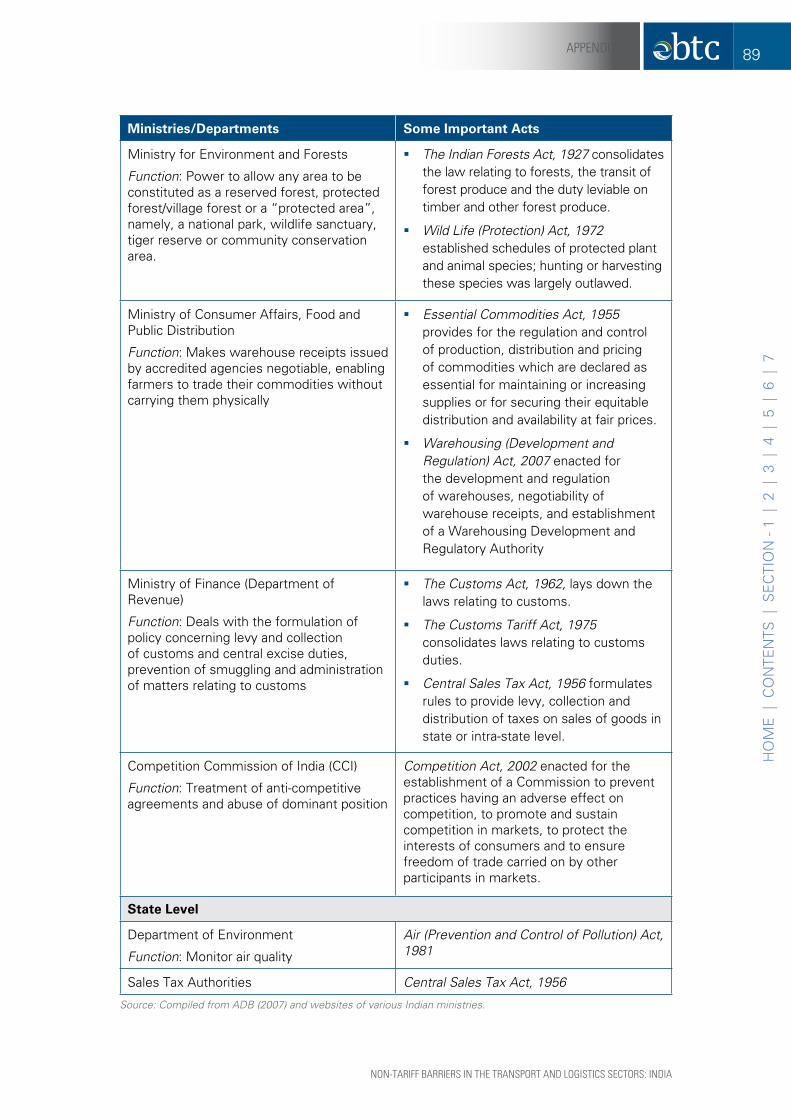

sector are given in Table A.1 of Appendix A. The table shows that apart from transport

ministries and departments, a number of other ministries such as the Ministry of

Finance, the Ministry of Environment and Forests and the Ministry of Consumer

Affairs, Food and Public Distribution (which regulates inter-state movement of goods)

regulate this sector directly or indirectly.

Recent changes and developments in different segments of transport logistics are

discussed below:

2.1 road Transport

India has the second largest road network in the world (after the US). The network

increased from around 2 million kilometres in 1990-91 to over 3.3 million kilometres

in 2008-09. Traffic on Indian roads is growing at the rate of 7-10 per cent per annum,

while the vehicle population is growing at 12 per cent per annum.

India is a manufacturing hub for automobile and auto-component companies. The

figures for compound annual growth rate (CAGR) in different segments of automobile

production between 2002-03 and 2008-09 are given in Table 2.1.1.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

12 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

Table 2.1.1: automobile production Trends (Number of Vehicles)

category 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09cagr (in %)

Passenger Vehicles 723,330 989,560 1,209,876 1,309,300 1,545,223 1,777,583 1,838,697 16.82

Commercial Vehicles 203,697 275,040 353,703 391,083 519,982 549,006 417,126 12.69

Three- Wheelers 276,719 356,223 374,445 434,423 556,126 500,660 501,030 10.40

Two- Wheelers 5,076,221 5,622,741 6,529,829 7,608,697 8,466,666 8,026,681 8,418,626 8.80

Grand Total 6,279,967 7,243,564 8,467,853 9,743,503 11,087,997 10,853,930 11,175,479 10.08

Source: SIAM, http://www.siamindia.com/scripts/production-trend.aspx

Road is the main mode of domestic transport and carries about 65 per cent of freight

and 85 per cent of passenger traffic in India.12 However, road infrastructure is not well-

developed. The national highways/expressways which connect different states constitute

around 65,569 kilometres or 2 per cent of the road network and carry 40 per cent of the

road traffic; state highways have a network of 1,30,000 kilometres; and rural, district

and urban roads are 3.14 million kilometres in length.13 However, the national highways

are often congested. On average, a commercial vehicle in India runs at a speed of 32

kilometres (20 miles) per hour compared to over 97 kilometres (60 miles) per hour in

the mature logistics markets of Western Europe and the US.14 Moreover, many national

highways are two-lane and are not properly linked to major economic centres.

To enhance the capacity of the national highways, the National Highway Act, 1956

was amended in 1995 to encourage private participation. In 1998-99 the government

launched the National Highway Development Project (NHDP) which comprised 5,846

kilometres (3632.53 miles) of Golden Quadrilateral (GQ) connecting four metro cities,

7,300 kilometres of North-South and East-West corridors, 1,133 kilometres of port

connectivity and other projects at an investment of $12 billion (€8.51 billion).15 Innovative

methods of financing through Build, Operate and Transfer (BOT), annuity-based BOT and

Special Purpose Vehicles (SPV) were adopted to attract the private sector. The FDI regime

was liberalised to attract foreign investment and FDI up to 100 per cent is now allowed

through the automatic route in all road development projects including construction and

12 http://morth.nic.in/writereaddata/sublinkimages/overview_NH3244795788.htm

13 http://www.investmentcommission.in/roads.htm and the Department of Road Transport and Highways Annual Report (2007-08).

14 Data Monitor (2007).

15 This figure was calculated using the average exchange rate for fiscal year 2009-10: $1=€0.7092. Source: www.oanda.com

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

13TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

maintenance of roads, highways, bridges and tunnels; all sub-sectors of road transport,

namely, passenger, freight, rental of commercial vehicles with operators, maintenance

and repair of road transport equipment and supporting services; and all sub-sectors of

services auxiliary to all modes of transport, i.e., cargo handling services, storage and

warehousing, freight transport agency and other services. The private sector has been

allowed to collect user charges, and they have been given incentives in the form of

100 per cent income tax exemption for a period of 10 years, cheaper loans, duty-free

import of road building equipment and machinery, and permission to develop rest areas

along roads entrusted to them, among others. To meet the funding requirements for all

categories of roads, the government created a Central Road Fund and levied cess on

petrol and high-speed diesel. Fifty per cent of this duty is allocated to rural roads and the

remainder is given to national highways and other roads.

With private and foreign investments, the total length of national highways increased

from 16,200 kilometres in the early 1990s to 70,548 km in 2009-10. However, private

investment has been largely concentrated in national highways, while the government

has focused on rural road development. In the Eleventh Five-Year Plan (2007-12),

the government aims to consolidate the existing road network and integrate state

highways and district roads with rural roads. In more recent years, road development

projects have gained momentum; the Ministry of Road Transport and Highways

(MORTH) has announced plans to build 12-13 kilometres of road network each day

in the fiscal year 2010-11.16 Allocation for the road transport sector increased by over

13 per cent, from approximately Rs. 1,75,200 million (€2,628 million) in Union Budget

2009-10 to Rs. 1,98,940 million (€2,984 million) in the Budget of 2010-11.17

Road freight transport has seen significant growth in recent years, but this sector is still

highly fragmented – only 15 per cent of the logistics service providers operate in the

corporate sector. Transporters with fleets of fewer than five trucks account for over

two-third of the owned and operated trucks, and 80 per cent of the total revenue.18

Small truck operators have been mainly engaged in haulage and depend on a large

number of intermediaries (brokers, booking agents, etc.). With liberalisation, the sector

is becoming corporatised and the market is becoming consolidated. Individual truckers

are being replaced by integrated logistics providers. A number of foreign players

16 http://www.livemint.com/2010/04/26145432/India-long-way-off-from-20km.html

17 The Union Budget of India 2010-11, Speech by the Minister of Finance (February 26, 2010), http://indiabudget.nic.in/ub2010-11/bs/speecha.htm. This figure was calculated using the average exchange rate for fiscal year 2009-10: Re.1 = €0.015. Source: www.oanda.com

18 Data Monitor (2007).

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

14 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

including DHL19 (Germany), Kühne & Nagel International AG (Switzerland) and Thomas

Nationwide Transport (TNT) N.V (Netherlands) operate in the road freight segment.

These integrated logistics providers have reduced the need for intermediaries and the

skills of the workforce are improving. Better road conditions have also facilitated the

use of multi-axle vehicles which are gradually replacing single-axle vehicles/trucks.

In India, public transport has not been able to keep pace with the growing population

and demand. The share of buses in total registered vehicles declined from 11.1 per

cent in 1951 to 1.1 per cent in 2004.20 In the past, the government was the main

provider of public transport, but with liberalisation, passenger transport is no longer

a government monopoly. Since public transport is not adequate, personal transport,

especially two-wheelers and small cars, have become an important mode of transport.

India is the second fastest growing automobile market after China. The contribution of

the automotive industry to GDP increased from 2.8 per cent in 1992-93 to 5 per cent in

2006-07. The Indian automobile market is dominated by small-sized cars. At present,

the market for luxury cars is small - only one per cent of the Indian population can afford

luxury cars. With sustained growth in GDP and rising incomes, the market for luxury

cars is expected to grow. Many Indian corporate companies and foreign players have

entered the automobile and auto-component manufacturing segment. FDI up to 100

per cent is allowed in the automobile and auto-component manufacturing sector and

India has emerged as a major exporting country for auto- components. International

companies such as Ford Motor Company (USA), General Motors Company (USA) and

Volkswagen AG (Germany) have established manufacturing bases in India because of

conducive policies and the availability of cheap labour.

Due to increases in energy prices and the shortage of fossil fuels, the Indian government

(both at the centre and state levels) is now focusing on environment-friendly public

transportation modes like metro rail and fuel-efficient vehicles.

Overall, road development has been recognised as a key infrastructure sector for

sustaining India’s economic growth. It is estimated that with the growth of the

population and economic development, both road freight and passenger volumes will

grow. The road freight industry will grow at a CAGR of 9.9 per cent from 2007-08 to

2011-12,21 while passenger traffic is projected to grow at 12-15 per cent per annum.22

19 DHL is named after its founders –Adrian Dalsey, Larry Hillblom and Robert Lynn of Germany.

20 National Highways Builders Federation (NHBF), http://nhbf.in/national_road_polocy.htm

21 Information provided by the Planning Commission.

22 http://www.investmentcommission.in/roads.htm

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

15TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

Investment in the road sector is expected to grow at 19 per cent per annum and

the government plans to spend about $10 billion (€7.09 billion) per annum on road

development over the next five years.23

2.2 railways

Indian Railways (spanning a length of 81,511 route kilometres) is the world’s fourth

largest rail network and the second largest in Asia. It is also the world’s fourth largest

freight carrier. It accounts for about 1.2 per cent of GDP and employed about 1.4

million people directly and 0.7 million indirectly (through support services) in 2006-07.

It is the principal mode of transport for inland bulk cargo and long-distance passenger

traffic. It carries more than 13 million passengers and 1.25 million tonnes of freight

every day.24 In 2008, there were over 7,000 railway stations in India.

The railways are one of the few sectors in India in which the government still has a

monopoly. With liberalisation, the demand for value-added transport services increased

and it was realised that the railways face capacity constraints in high-density corridors

and suffer from monopoly-induced inefficiencies and a maintenance backlog. Another

problem area identified was that the freight rates subsidise passenger transport. This

has led to a shift in freight traffic from rail to road transport over the years. There has

also been a shift in passenger traffic from the railways to airlines, especially to no-frill

private airlines. To reduce inefficiencies, the railways took various measures in the

1990s and in early 2000 to re-balance tariffs and involve the private sector in non-core

activities. However, the sector continued to be supported by budgetary grants and

suffered operational losses.

In 2005-06, the Ministry of Railways formulated an integrated modernisation plan

for 2005–2006 to 2009–2010, to upgrade operations (both passenger and freight

services) to global standards. The total expenditure was estimated to be $5.5 billion

(€3.9 billion).25 Private players were allowed to participate through the PPP route in

operating container trains on designated routes and developing rail-side warehouses,

logistics parks, budget hotels, etc. They can now participate in strengthening rail-port

connectivity, and developing dedicated freight corridors. Non-core activities such as

23 This was pointed out by the Investment Commission of India.

24 http://www.asiatradehub.com/India/railways.asp and http://www.indianrailways.gov.in/evolution/ rail-network.htm

25 This figure was calculated using the average exchange rate for fiscal year 2009-10: $1=€0.7092. Source: www.oanda.com

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

16 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

product manufacturing have been opened up for FDI and corporate management

practices have been introduced. After the adoption of these measures, the Indian

Railways started recording impressive rates of growth. In the past four years, the

railways generated a cumulative cash surplus before dividend of approximately $16.94

billion (€12.01 billion).26 The operating ratio of the railways, which was 83.72 per cent

in 2005-06, came down to 75.94 per cent in 2007-0827 and is expected to drop further.

The Indian Railways is also a major equipment manufacturer. It meets most of the

requirements through domestic production in factories like Chittaranjan Locomotive

Works (Chittaranjan, West Bengal) and Diesel-Loco Modernisation Works (Patiala,

Punjab). The Ministry of Railways is focused on developing its industrial capacity to

meet most of the country’s locomotive, passenger-car and ancillary equipment needs

domestically and to export locomotives to other countries. The total value of exports

of rolling stock/ spares during 2008-09 was Rs. 1,501.5 million (€22.52 million).28

In recent years, there has been an increase in freight and passenger traffic due to

improved service quality and increases in route length. Also, unlike road transport,

the railways are not subjected to inter-state border checks that are time-consuming.

In 1990-91, freight traffic was around 3.3 billion tonnes which increased to 7.9 million

tonnes in 2007-08. In future, private investment in this sector is likely to increase due

to PPP initiatives. The government has already signed agreements with companies

from countries such as Japan, Russia, Germany and France for high-speed passenger

corridors, and manufacturing and consultancy services. The Indian Railways is also

setting up two Greenfield electric and diesel locomotive factories in joint ventures

with foreign manufacturers. Although private participation in the sector is increasing,

Indian Railways is unlikely to be privatised in the near future.

2.3 air Transport

Air transport is the fastest mode of transport for long-distance passengers and

high-value cargo. Post-liberalisation, with the development of services (financial,

telecommunications, IT, etc.) and growth in exports in sectors such as gems and

26 This figure was calculated using the average exchange rate for fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

27 http://www.ibef.org/Archives/ViewArticles.aspx?art_id=17585&cat_id=808 and Indian Railways (2008)

28 This figure is calculated using the average exchange rate for fiscal year 2008-09: Re. 1 = €0.015. Source: www.oanda.com. Exports included new Cape Gauge diesel locomotives, lease-cum-maintenance of YDM4 diesel locomotives, new MG coaches/chair cars (non-AC), diesel loco spares, and MG diesel locomotive axles to developing countries such as Angola, Sudan, Mozambique, Senegal, Tanzania, Malaysia and Sri Lanka.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

17TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

jewellery and pharmaceuticals, this sector has witnessed a rapid rate of growth.

According to the International Air Transport Association (IATA), India has one of the

fastest growing aviation industries and the country’s rank in the world’s aviation market

rose from 12 in 2006 to 9 in 2008. The market grew at a CAGR of 18 per cent and

was worth approximately $5.6 billion (€3.94 billion)29 in 2008. Indian carriers currently

have a fleet size of 310 aircraft.30 Passenger traffic (both domestic and international)

almost doubled between 2004 and 2007, while cargo traffic increased by 33.8 per

cent between 2004-05 and 2007-08.31

The air transport sector has been liberalised in a phased manner. In 1994, the

government monopoly in airline operations ended and private players were allowed

to enter the market. In 2007, private operators catered to nearly 82 per cent of the

market. In 2009, the proportion of passenger and freight carried by national and private

carriers was in the ratio of 1:4 and 1:2, respectively, for domestic operations and 4:1

and 2:1 for international operations.

Competition among private operators brought down prices and no-frill airlines have made

air travel affordable for a large number of people. The number of domestic passengers

using private air services (both scheduled and non-scheduled) increased from 15 million

in 1990 to 35.16 million in 2006-07.32 Important policy changes include an open sky

policy for cargo and Indian private airlines are allowed to fly on designated international

routes. There are still, however, some FDI restrictions on ownership by foreign airlines.

With the growth in demand, airports have started facing capacity constraints and the

government is now encouraging private investment in development and maintenance

of airports. For Greenfield airports, up to 100 per cent FDI is allowed through the

automatic route, while for other airports clearances are required for FDI beyond

74 per cent. FDI up to 100 per cent is allowed in ground handling services (74 per

cent through the automatic route), maintenance and repairs, and flying training and

technical training institutes. Private developers are allowed to set up captive airstrips

and general airports 150 kilometres away from an existing airport, and they can avail

100 per cent tax exemption for airport projects for a period of 10 years. There are no

caps on investment in maintenance and repairs, flying training institutes and technical

training institutes; and helicopter/seaplane services.

29 This figure was calculated using the average exchange rate for fiscal year 2008-09: $1 = €0.7042. Source: www.oanda.com

30 http://www.ibef.org/industry/aviation.aspx

31 Figures taken from the Airport Authority of India, http://www.airportsindia.org.in/AAI/main.jsp

32 http://indiabudget.nic.in/es2000-01/chap99.pdf; www.indiastat.com

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

18 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

With the privatisation of airports, the need for regulatory changes has been felt. The

government enacted the Airports Economic Regulatory Authority of India Act, 2008 that

established a regulatory authority called the Airports Economic Regulatory Authority of

India (AERA) in May 2009.33 The objectives of AERA are to foster healthy competition

among all major airports (government-owned, PPP-based, and private);34 encourage

investment in the sector; regulate tariffs of aeronautical services; protect reasonable

interests of users; and operate efficient, economic and viable airports. As a transparent

entity, AERA published its “White Paper on Regulatory Objectives and Philosophy in

Economic Regulation of Airports and Air Navigation Services” in December 2009, listing

major issues that impact the formulation of its regulatory philosophy.

The Indian air transport sector will continue to grow at a rapid pace. The Vision

2020 statement announced by the Ministry of Civil Aviation projected investment

opportunities of approximately $110 billion (€78.01 billion)35 in the Indian civil aviation

sector ($80 billion or €56.5 billion in new aircraft and $30 billion or €21.5 billion in the

development of airport infrastructure); air cargo traffic will grow at over 11.4 per cent

per annum and exceed 2.8 million tonnes by end-2010.36

2.4 Maritime Transport

India is strategically located in the global shipping routes and has a long coastline

which makes it an important maritime nation. Maritime transport caters to over 90 per

cent of the country’s trade in terms of volume and 70 per cent in terms of value. India

has 13 major ports which are regulated by the central government and 187 minor ports

which are under the jurisdiction of state governments. Major ports handle over three-

fourth of the sea-borne traffic. The quantity of cargo handled and container traffic in the

major ports increased from 152.6 million tonnes and 7.9 million tonnes, respectively,

in 1990-91 to 519.1 million tonnes and 92.13 million tonnes, respectively, in 2007-08.37

India’s shipping industry is ranked 17th among the world’s maritime nations in terms

of Gross Tonnage (GT) and 15th in terms of Dead Weight Tonnage (DWT).38 It has the

33 Ministry of Civil Aviation (2009).

34 Major airports have been defined under the Act as follows: “Major airport means an airport which has, or is designated to have annual passenger throughput in excess of one and a half million or any other airport as the Central Government may, by notification, specify as such.”

35 This figure was calculated using the average exchange rate for the fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

36 Mukherjee (2009) and http://www.ibef.org/artdispview.aspx?cat_id=503&art_id=21353&in=5

37 http://indiabudget.nic.in/es1990-91/4%20Infrastructure.pdf

38 http://pib.nic.in/archieve/image/2005/r2005111704.pdf and http://www.imaritime.com/knowledge-center/shipping.php

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

19TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

largest merchant shipping fleet among the developing countries; the fleet consisted

of 912 ships of 9.3 million GT in 2008.39 However, coastal shipping and inland water

transport is limited. Apart from ports and shipping, the maritime sector also consists

of other facilities such as shipbuilding, ship repair and maintenance, and training of

seafarers. India is a global supplier of seafarers and accounts for around 6 per cent of

the total seafarers in the world.40

With the increase in trade after liberalisation, it became necessary to enhance

port capacities. FDI up to 100 per cent is now allowed in port development projects

(construction and maintenance). The private sector has been offered other incentives such

as 100 per cent income tax exemption for port development for a period of 10 years. As a

result, several global port operators have established operations in India through BOT and

other modes. These include the Maersk Line Group in the Jawaharlal Nehru Port Trust

(JNPT), Mumbai; P & O Ports in JNPT, Mumbai and Chennai; Dubai Ports International

in Cochin and Visakhapatnam; and PSA Singapore in Tuticorin. In the shipping sector,

foreign ships calling at Indian ports no longer require a licence for overseas trade; the

cargo reservation policy has been relaxed to allow foreign vessels on a case-by-case

basis. This has increased the share of foreign shipping in total trade. Foreign shipping

companies now control most of the container traffic and the share of Indian shipping in

international trade declined from 36.7 per cent in 1991-92 to 13.7 per cent in 2005-06.41

Despite these developments, government policy is geared towards promoting national

shipping for strategic reasons and self-reliance. For instance, the government introduced

the Tonnage Tax42 in 2004, which boosted the growth of the Indian merchant fleet.

It has been estimated that the cargo-handling capacity of Indian ports will increase to

1,855 MT by 2012 with an investment of about $20.61 billion or €14.62 billion; over

60 per cent of this will be from the private sector.43 The Indian ship-building industry

accounts for 1.7 per cent of the global ship-building market. The share is expected to

increase to 15 per cent by 2020 and this industry is expected to grow at a CAGR of 30

per cent to reach $22 billion (€15.6 billion) in 2020.44

39 This comprises around 282 overseas vessels with 7.89 million GT and 13.55 million DWT and 590 coastal vessels with 0.5 million GT and 0.99 million DWT.

Source: http://www.thehindubusinessline.com/2009/01/27/stories/2009012750181000.htm

40 CII-KPMG (2007), Gaps in the Indian Logistics Sector: A White Paper, September 2007.

41 In fact, while the world cargo fleet grew from 464.99 million GT in 1995 to 687.98 million GT in 2006, India was still witnessing slow growth in its fleet size during this period. Source: Planning Commission (2008b).

42 Under this system, ship-owners can opt for tonnage tax, whereby income tax is levied on the basis of presumptive income of the Net Tonnage (NT) of each ship owned by Indian ship-owners determined according to a fixed scale.

43 This figure was calculated using the average exchange rate for fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

44 http://www.thehindubusinessline.com/2008/03/24/stories/2008032450570600.htm. This figure was calculated using the average exchange rate for fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

20 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

2.5 auxiliary and Logistics services

The term ‘logistics services’ is defined as the management of goods and resources

between the ‘point of origin’ and the ‘point of consumption’, so as to meet customer

requirements. Thus, transportation is a key component of logistics services. Such

services help to integrate different modes of transport. It also includes other services

such as storage and warehousing, inventory management, and packaging. The logistics

sector started modernising and globalising after India began integrating into the global

value chain. Indian industries such as automobiles and auto-components, IT hardware,

electronics, textiles, Fast Moving Consumer Goods (FMCG) and retail are some

main users of logistics services. Most Indian companies now concentrate on their

core businesses and have outsourced the non-core business to specialised logistics

service providers. The Indian Third Party Logistics (3PL) service providers’ market was

estimated at about $890.3 million (€631.42 million) in 2005 and is expected to grow

at a CAGR of 21.9 per cent to reach around $3,557 million (€2523 million) in 2012.45

Although the current size of the Fourth Party Logistics (4PL) service providers’ market

is small, it is expected to grow at a rate of over 20 per cent in the next five years.

The total warehousing space in India was estimated to be 1,800 million sq ft in

2006.46 A large part of the warehousing business is in the unorganised sector and

organised players accounted for only 8 per cent of the segment in 2006.47 Among

the organised players, public sector enterprises such as the Central Warehousing

Corporation (CWC) and Food Corporation of India (FCI) have the majority share. The

government is encouraging foreign investment in warehousing and FDI up to 100 per

cent is allowed. In recent years, a large number of Indian companies such as the Tata

Group and foreign players such as the Maersk Logistics Group (Denmark), ProLogis

(USA) and Jebel Ali Free Zone (Jafza) International (Dubai) have entered the storage

and warehousing business. The need for warehousing and storage is likely to grow as

the Indian economy is growing and businesses are integrating into global value chains.

It is estimated that the Indian warehousing sector will grow from $20 billion (€14.18

billion) in 2007-08 to about $55 billion (€39.01 billion) by 2010-11, growing at a rate of

35-40 per cent every year.48

45 http://www.frost.com/prod/servlet/market-insight-top.pag?docid=74102578. This figure was calculated using the average exchange rate for fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

46 CII-KPMG (2007).

47 The main reason is India’s indirect tax structure. Since taxes paid on cross-border sales are higher than local tax charges, most companies prefer to set up small warehouses across different states rather than large centralised set-ups.

48 Colliers International (2009). The figures were calculated using the average exchange rate for fiscal year 2009-10: $1 = €0.7092. Source: www.oanda.com

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

21TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

With increased containerisation, the demand for container-handling services in India is

growing. In 2009, India had 133 container freight stations and inland container depots, the

majority of which are privately owned. The Planning Commission of India has projected

that these facilities should double in the next two years to support the growth in container

traffic. The different transport ministries such as the Ministry of Railways have taken

initiatives to develop container-handling facilities through private partnerships. In 2007,

the Indian Railways allowed private players in rail container transportation. By 2009, 16

companies including many private players have acquired licences to run container trains.

Due to such incentives, although India’s present container handling capacity is low, it

will grow at a rapid pace in the near future. For instance, Frost & Sullivan in the report,

“Strategic Assessment of Containerization Trends in India”, pointed out that India’s

container handling capacity for international and domestic traffic is expected to reach 21

million Twenty-foot Equivalent Units (TEU) in 2014 from 9.1 million TEU in 2008.

Customs brokers, Clearing and Forwarding (C&F) agents and freight forwarders

are some important players in the logistics chain. Some of them have integrated

operations and offer a wide variety of services to customers, while others provide

specialised services. In the past, the logistics chain in India was highly fragmented

with a large number of intermediaries. With the integration of the logistics chain, the

need for a large number of intermediaries is decreasing. Automated systems, on-line

documentation filing, etc., have also reduced the need for multiple agents.

Since Indian companies cater to global clients who demand time-bound high quality

services in product consumption, the segment of reverse logistics49 is growing. About

7 per cent of an enterprise’s gross sales are captured by return costs. This is a new

area of operations in India and most reverse logistics contracts are customised to fit

the size and type of companies that contract them.

2.6 express delivery and courier services

Express Delivery Services (EDS) facilitate the transportation of documents, samples,

gifts and other high-value time-bound items. EDS companies also handle customs

clearances and reduce the need for multiple agents such as freight forwarders and

customs clearance agents. Courier companies offer similar services but generally

49 The term ‘Reverse Logistics’ stands for all operations related to the resources getting at least one step back in the supply chain for the purpose of value addition, proper disposal or re-manufacturing. Mostly, it is seen as the flow of goods from the point of consumption to the point of origin and also involves planning and managing (collection, disassembly and processing) the efficient flow of and/or reuse of surplus inventory.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

22 TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

the EDS companies provide more value-added services. Since the logistics chain in

India is fragmented and delivery time is high, Indian companies often use EDS/courier

services instead of general logistics services to save time. The growth of this industry

has been propelled by the development of India as a business process outsourcing

hub, the growth of services such as telecommunications and financial services, and

exports of products like auto-components and textiles.

At present, the size of the EDS industry is estimated at around Rs. 90 billion (€1.33

billion)50 and this sector is growing at around 20-25 per cent per annum.51 According

to industry estimates, the courier/EDS industry is expected to grow at around 30 per

cent in the next five years. There are more than 2,500 EDS/courier companies in

India that employ close to 1 million people either directly or indirectly; of these, only

20 or 30 companies belong to the organised/ corporate sector but they account for

70 per cent of the total revenue. Global integrators, namely, Federal Express (FedEx)

and United Parcel Service Inc. (UPS) from the USA, DP-DHL (Germany), and TNT N.V

(Netherlands) have a presence in India. They have expanded their domestic operations

through local partnerships. For instance, DHL has partnered with the Indian company,

Blue Dart, and also entered into partnership with India Post (i.e., the Department of

Posts of the Government of India) for international mail services.

Up to 100 per cent FDI is allowed in the courier/EDS business, but according to the

present regulations (i.e., Indian Post Office Act, 1898), ‘letters’ are reserved for India

Post. However, this act does not define the term ‘letter’ and the Department of Posts

is in the process of designing new regulations for this sector.

Overall, the transport and logistics sector in India has undergone significant changes

in the past 15 years. Private participation has increased and there have been mergers

and acquisitions and consolidation. With growing GDP and trade, India is an important

market for transport and logistics service providers, and several EU companies have

already established a presence in India. The next section discusses India-EU trade,

investment and collaboration in this sector.

50 This figure is calculated using the average exchange rate for fiscal year 2009-10: Re. 1 = €0.015. Source: www.oanda.com

51 Express Industry Council of India (EICI), http://www.eiciindia.org/FrontSite/aboutus.aspx

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

23TRANSPORT AND LOGISTICS SERvICES IN INDIA: AN OvERvIEw

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

3. india-eU Trade, investment and collaboration

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

25INDIA-Eu TRADE, INvESTmENT AND COLLABORATION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

India-EU trade, investment and collaboration in transport and logistics constitute trade

in goods, trade in services, investment by EU companies in India, joint ventures and

other forms of collaboration. This study does not address Indian investments in the

EU. Section 3.1 discusses trade in goods between India and the EU, using bilateral

trade flow data; it also shows the comparative positions of both India and the EU in

transport services. A primary survey was conducted to understand the pattern of trade

in goods and services, areas in which EU companies are investing in India, their views

on future growth potential, and factors determining their success in India. These are

discussed in Section 3.2.52 Section 3.3 discusses on-going and past collaborations

at the government-to-government level that have implications for enhancing trade

and collaboration between India and EU. Section 3.4 examines areas for future trade,

collaboration and investment.

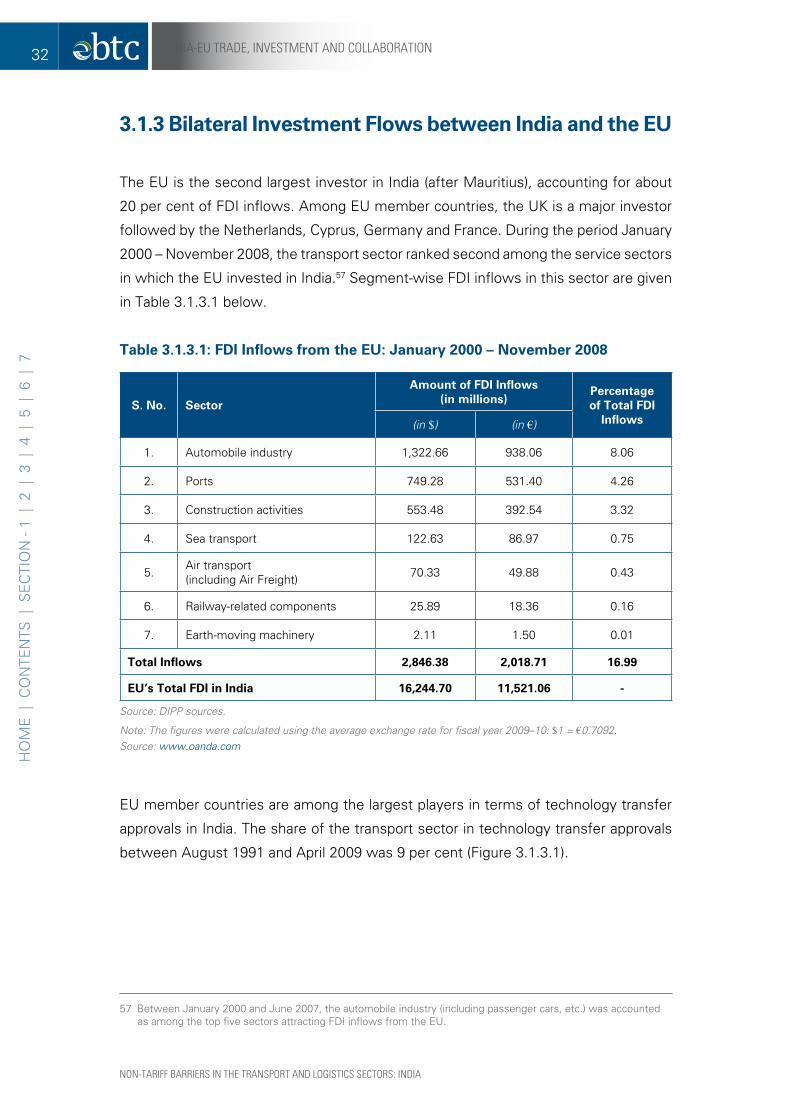

3.1 Trade in goods and services and investment flows

3.1.1 Trade in goods

The EU is the largest player in global trade but more than half of this is intra-EU. In 2008,

the EU (extra-EU) contributed 15.9 per cent and 18.3 per cent in global merchandise

exports and imports, respectively. India’s ranking among WTO member countries has

also improved in the past few years, but its share remains low. In 2008, India ranked

19th among merchandise exporters (1.5 per cent share) and 10th among importers in

the world.53

The EU is India’s largest trading partner in goods. In the past few years, merchandise

trade between India and the EU has shown impressive growth. In 2008, the total trade

between India and the EU reached $79 billion (€55.63 billion) compared to only $19.7

billion (€17.43 billion) in 1998, and witnessed a CAGR of 14 per cent over the past 10

years. India has a negative trade balance with the EU.54

India’s trade in transport equipment includes import and export of different types of

vehicles, vehicle parts, aircraft and aircraft parts, cruise ships, and boats. Transport

52 The barriers faced by EU companies in India are discussed in Section 4.

53 WTO (2009)

54 Balance of Payments, IMF. This figure was calculated using the average exchange rate for fiscal year 2008–09 ($1 = €0.7042) and 1998–99 ($1 = €0.8849). (Source: http://www.oanda.com/)

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

26 INDIA-Eu TRADE, INvESTmENT AND COLLABORATION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

equipment holds an important place in India’s trade basket and India’s global trade in

this sector was €19 billion in 2007-08, of which exports accounted for €4.9 billion. India

is a major importer of transport equipment and the EU is one of the largest suppliers of

transport equipment to India (Figure 3.1.1.1). India also exports transport equipment

to the EU.

figure 3.1.1.1: india’s Major supplier countries and export destinations for

Transportation equipment (2007-08)

EU | 20.8%Others | 35.8%Singapore | 10.2%

UAE | 8%

USA | 9.7%Bangladesh | 2%

Egypt | 2.7%

Algeria | 2.1%

South Africa | 3.4%Sri Lanka | 5.3%

export destinations of indiasupplier countries to india

Japan | 3.1%

China | 3.7%

Others | 10.2% EU | 35.5%

Singapore | 4.2%

USA | 43.3%

Source: Authors’ calculations from Export-Import Databank, Director General of Foreign Trade (DGFT), Government of India.

Over time, India-EU trade in transportation equipment has increased. As in the

case of total merchandise trade, India has a negative trade balance with the EU in

transportation equipment. Figure 3.1.1.2 shows an increase in trade in 2005-06. This

is due to an increase in imports of aeroplane and other aircraft (the HS codes for

transportation equipment at the 6-digit level are given in Table B.1 of Appendix B). In

2007-08, transportation equipment was the 8th largest commodity in India’s export

basket to the EU, accounting for 4.2 per cent of total exports. It was the second

largest commodity in imports from the EU, with a share of 5.8 per cent. In 2008, India

was the 15th largest trading partner for the EU in this sector, accounting for 1.6 per

cent of the total EU trade in transportation equipment.55 This clearly shows that while

India is a major importer of transport equipment and imports from the EU are rising,

there is scope for further increase in trade between India and the EU.

55 http://exporthelp.europa.eu

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

27INDIA-Eu TRADE, INvESTmENT AND COLLABORATION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

figure 3.1.1.2: india-eU Trade in Transportation equipment

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

1997-98 2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 (Apr- Dec)

Valu

e in

€B

illio

ns

Years

0.390.56

0.27 0.33 0.250.42 0.29

0.55 0.60 0.63

1.01

3.13 3.04

4.29

1.25

0.79 0.761.02

1.61

0.68

Exports Imports

Source: Authors’ calculations from Export-Import Databank, DGFT, Government of India.

Note: Exchange rates are as follows: For 1997, Є1 = Rs.20.9613; for 2000, Rupee 1 = Є0.0241; for 2001, Rupee 1 = Є0.0237; for 2002, Rupee 1 = Є0.0207; for 2003, Rupee 1 = Є0.0185; for 2004, Rupee 1 = Є0.0176; for 2005, Rupee 1 = Є0.0185; for 2006, Rupee 1 = Є0.0172; for 2007, Rupee 1 = Є0.0175; for 2008 (Apr–Dec), Rupee 1 = Є0.0153. (Source: RBI and Foreign Exchange Dealers’ Association of India, http://www.fedai.org.in/)

The top 10 items of India’s exports and imports to and from the EU are given in Table

B.2 and Table B.3 in Appendix B. The two tables show that the major export items

constitute vehicles parts and accessories, while imports largely constitute aeroplanes

and other aircraft. There has been a change in both the import and export baskets over

time. India’s major export destinations and the major EU member countries exporting

to India in 2007-08 are given in Figure 3.1.1.3.

figure 3.1.1.3: indian exports to eU Member states and eU exports to india

in 2007-08

France | 65.3%

Germany | 12.7%

EU-19 | 5.7%

Italy | 1.6%

Czech Republic | 2.3%

Cyprus | 2.3%

Sweden | 2.9%

Netherlands | 3.1%

UK | 4.1%

eU’s exports to indiaindia’s exports to eU countries

Belgium | 4.3%EU-19 | 14.4% Italy | 23.6%

UK | 13.9%France | 12.1%

Germany | 14.3%

Spain | 6.2%

Greece | 4.5% Netherlands

| 6.7%

Source: Authors’ calculations from Export-Import Databank, DGFT, Government of India.

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

28 INDIA-Eu TRADE, INvESTmENT AND COLLABORATION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

The types of products exported by different EU member states are listed in Table 3.1.1.1.

Table 3.1.1.1: Leading eU countries exporting to india and products exported

eU countries Top 5 Transportation products

france

Aeroplanes & other aircraft, of an unladen weight >2000 kg but not excluding 15000 kg (880230)

Aeroplanes & other aircraft, of an unladen weight not exceeding 2000 kg (880220)

Aeroplanes & other aircraft, of an unladen weight exceeding 15000 kg (880240)

Other parts of aeroplanes/helicopters (880330)

Dredgers (890510)

germany

Aeroplanes & other aircraft, of an unladen weight >2000 kg but not excluding 15000 kg (880230)

Other parts & accessories of vehicles of heading 8701-8705 (870899)

Other parts of aeroplanes/helicopters (880330)

Other motor cars & motor vehicles principally for the transport of persons, including station wagon etc (870390)

Vehicle with spark ignition internal combustion reciprocating piston engine of cylinder capacity>3000 cc (870324)

UK

Other parts of aeroplanes/helicopters (880330)

Other vessels, fire floats etc (890590)

Other parts of goods of heading 8801 or 8802 (880390)

Other vessels for transport of goods & other vessels for transport of persons & goods (890190)

Cruise ships, excursion boats & similar vessels principally designed for transport of persons, ferry-boats of all kinds (890110)

Netherlands

Dredgers (890510)

Cruise ships, excursion boats & similar vessels principally designed for transport of persons, ferry-boats of all kinds (890110)

Other vessels for transport of goods & other vessels for transport of persons & goods (890190)

Tugs and pusher craft (890400)

Other vessels, fire floats etc (890590)

sweden

Other vessels, fire floats etc (890590)

Other parts & accessories of vehicles of heading 8701-8705 (870899)

Other vessels for transport of goods & other vessels for transport of persons & goods (890190)

Drive axles with differential w/n provided with other transmission components (870850)

Dumpers designed for off-highway use (870410)

Source: Compiled from Export-Import Databank, DGFT, Government of India. http://dgftcom.nic.in/

NON-TARIFF BARRIERS IN THE TRANSPORT AND LOGISTICS SECTORS: INDIA

29INDIA-Eu TRADE, INvESTmENT AND COLLABORATION

HO

ME

| C

ON

TEN

TS |

SE

CTI

ON

- 1

| 2

| 3

| 4

| 5

| 6

| 7

3.1.2 Trade in services

The global services trade has seen significant growth in the past decade from $2.7

trillion (€2.3 trillion) in 1998 to $7.3 trillion (€5 trillion) in 2008.56 In 2008, the world’s