Newmarket Gold Investor Presentation May Metals Investment Forum

Upload

adnet-communicationsCategory

view

408download

4

TSX:NMIFebruary 2016

Exceptional Team, Solid Production,Significant Valuation Upside

2TSX:NMI

Forward-looking StatementsCertain information set forth in this presentation contains “forward-looking statements”, and “forward-lookinginformation under applicable securities laws. Except for statements of historical fact, certain information containedherein constitutes forward-looking statements, which include the Company’s expectations about its business andoperations, and are based on the Company’s current internal expectations, estimates, projections, assumptions andbeliefs, which may prove to be incorrect. Some of the forward-looking statements may be identified by words such as“will”, “expects”, “anticipates”, “believes”, “projects”, “plans”, and similar expressions. These statements are notguarantees of future performance or outcomes and undue reliance should not be placed on them. Forward-lookingstatements are based on the opinions and estimates of management as of the date such statements are made and theyare subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level ofactivity, performance or achievements of the Company to be materially different from those expressed or implied bysuch forward-looking statements or forward-looking information. Although management of the Company hasattempted to identify important factors that could cause actual results to differ materially from those contained inforward-looking statements or forward-looking information, there may be other factors that cause results not to be asanticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate, as actualresults and future events could differ materially from those anticipated in such statements. Accordingly, readers shouldnot place undue reliance on forward-looking statements and forward-looking information. The Company does notundertake to update any forward-looking statements or forward-looking information that are included in thispresentation or incorporated by reference herein, except in accordance with applicable securities laws.

3TSX:NMI

Newmarket Gold Highlights Excellent capital structure US$36.5M cash (A$52.0M equivalent) and US$1.3M debt

Experienced capital markets and operational team with a proven track record of execution and significant value creation

Three 100% owned operating gold mines in Australia with sustainable production of over 200,000 ounces annually with strong cash flow (all production unhedged)

New mine site discoveries leading to organic production growth

Disciplined gold asset consolidation strategy

Highly leveraged to the AUD$ gold price ($A1725, Feb 18,2016)

NEWMARKET OPPORTUNITY

1. All market data is as at Feb 10, 2016, production and cash flow based on 2016 consensus estimates, see peer group details slide 9. Source: public market information and company disclosure as at Feb 10, 2016

$683

$2,492

EV/oz Production EV/oz Production

1.90x

5.70x

Price/2016E CFPS (ratio) Price/2016E CFPS (ratio)

Peer Group1Peer Group1

Newmarket Valuation Newmarket Valuation

4TSX:NMI

NEWMARKET GOLD FOUR PILLARS

SUPERIOR INVESTMENT OPPORTUNITY

PEOPLE

Track record of superior value creation

Board and management aligned with shareholders ($12M invested 8% equity ownership)

Experienced management team

Demonstrated operations excellence

OPERATIONS

Three gold mines in Australia, over 220,000 ounces annual production

Strong cash position (US$36.5M1), record low operating cash costs and AISC, prudent capital allocation

Delivering on guidance, focus on free cash flow and growth

DISCOVERIES

Three new mine site gold discoveries close to current infrastructure

Significant resource expansion opportunities at all mines

New Eagle visible gold discovery at Fosterville traced over 600m x 290m and open

Trend to higher consolidated grades and recoveries

GROWTH

Strong potential for organic production growth and resource expansion

Deep capital markets relationships, patiently targeting accretive production opportunities

1. As at December 31 2015

5TSX:NMI

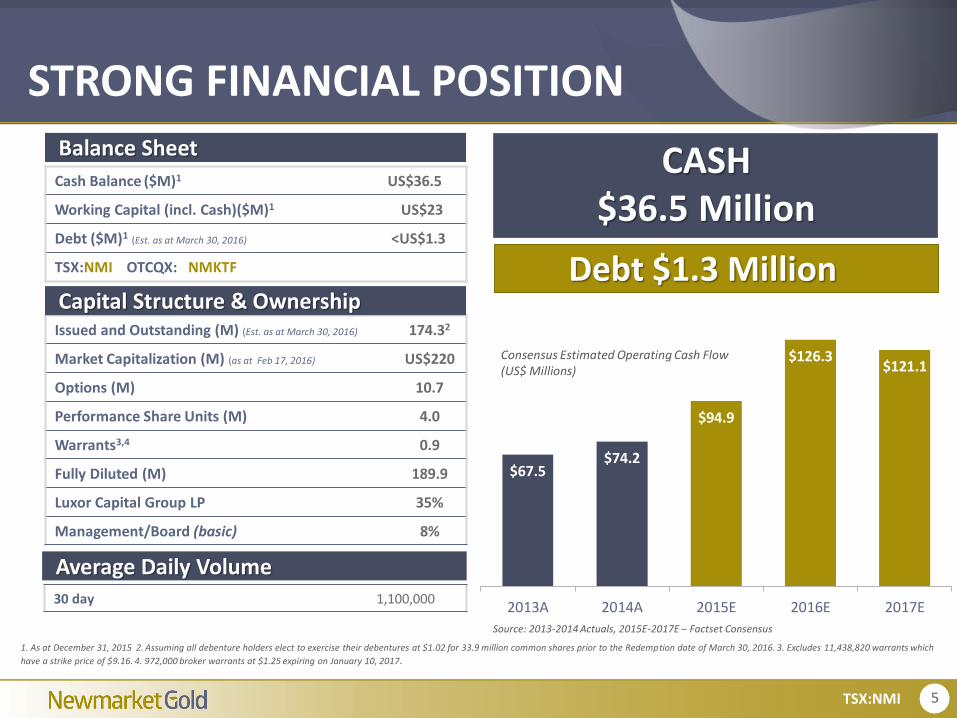

STRONG FINANCIAL POSITION

Cash Balance ($M)1 US$36.5

Working Capital (incl. Cash)($M)1 US$23

Debt ($M)1 (Est. as at March 30, 2016) <US$1.3

TSX:NMI OTCQX: NMKTF

1. As at December 31, 2015 2. Assuming all debenture holders elect to exercise their debentures at $1.02 for 33.9 million common shares prior to the Redemption date of March 30, 2016. 3. Excludes 11,438,820 warrants which

have a strike price of $9.16. 4. 972,000 broker warrants at $1.25 expiring on January 10, 2017.

Balance Sheet

Issued and Outstanding (M) (Est. as at March 30, 2016) 174.32

Market Capitalization (M) (as at Feb 17, 2016) US$220

Options (M) 10.7

Performance Share Units (M) 4.0

Warrants3,4 0.9

Fully Diluted (M) 189.9

Luxor Capital Group LP 35%

Management/Board (basic) 8%

Capital Structure & Ownership

Average Daily Volume30 day 1,100,000

CASH$36.5 Million

$67.5$74.2

$94.9

$126.3$121.1

2013A 2014A 2015E 2016E 2017E

Source: 2013-2014 Actuals, 2015E-2017E – Factset Consensus

Consensus Estimated Operating Cash Flow (US$ Millions)

Debt $1.3 Million

6TSX:NMI

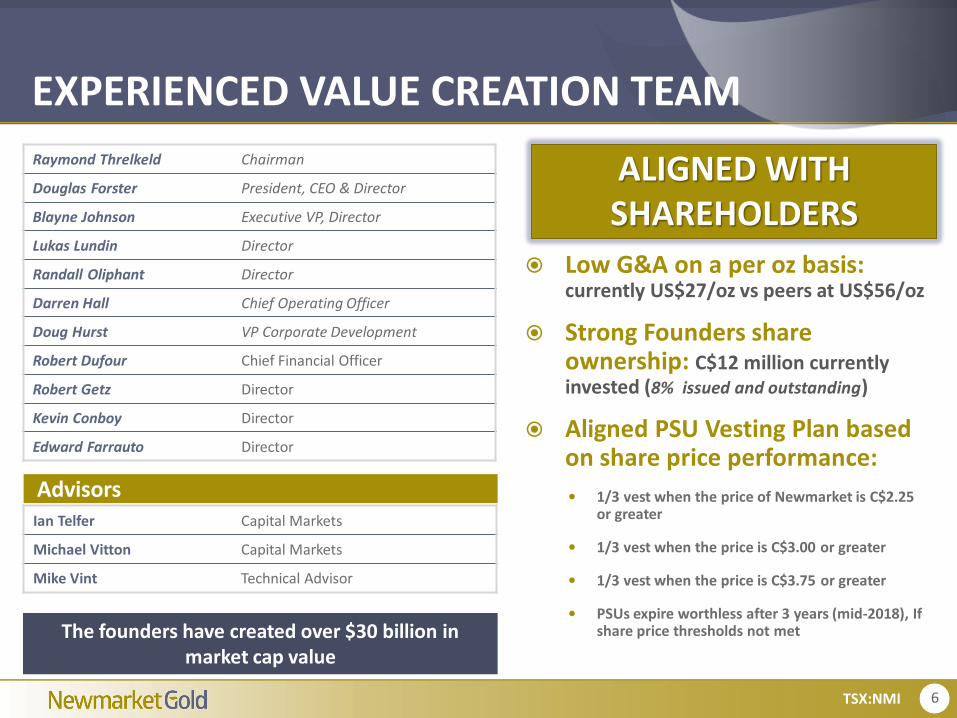

Low G&A on a per oz basis: currently US$27/oz vs peers at US$56/oz

Strong Founders share ownership: C$12 million currently invested (8% issued and outstanding)

Aligned PSU Vesting Plan based on share price performance:

1/3 vest when the price of Newmarket is C$2.25 or greater

1/3 vest when the price is C$3.00 or greater

1/3 vest when the price is C$3.75 or greater

PSUs expire worthless after 3 years (mid-2018), If share price thresholds not met

EXPERIENCED VALUE CREATION TEAM

Raymond Threlkeld Chairman

Douglas Forster President, CEO & Director

Blayne Johnson Executive VP, Director

Lukas Lundin Director

Randall Oliphant Director

Darren Hall Chief Operating Officer

Doug Hurst VP Corporate Development

Robert Dufour Chief Financial Officer

Robert Getz Director

Kevin Conboy Director

Edward Farrauto Director

AdvisorsIan Telfer Capital Markets

Michael Vitton Capital Markets

Mike Vint Technical Advisor

The founders have created over $30 billion in market cap value

ALIGNED WITH SHAREHOLDERS

7TSX:NMI

SUSTAINABLE PRODUCER WITH A STRATEGY FOR LONG-TERM GROWTH

RECORD 222,671 oz

FLAGSHIP FOSTERVILLE GOLD MINE

3 AustralianCONSOLIDATED GOLD PRODUCTION

2015 RECORD YEAR

RECORD PRODUCTION 123,095RECORD GRADE 6.11 g/t AuRECORD RECOVERY 88.5%RECORD DRILL INTERCEPT 645g/t Au over 3.5m

CONSOLIDATED COSTS

OPERATING CASH COSTS $US 704/ozALL-IN SUSTAINING COSTS $US 987/oz

Gold Mines

THREE NEW MINE SITE DISCOVERIES

ROBUST AUD$ GOLD PRICE

8TSX:NMI

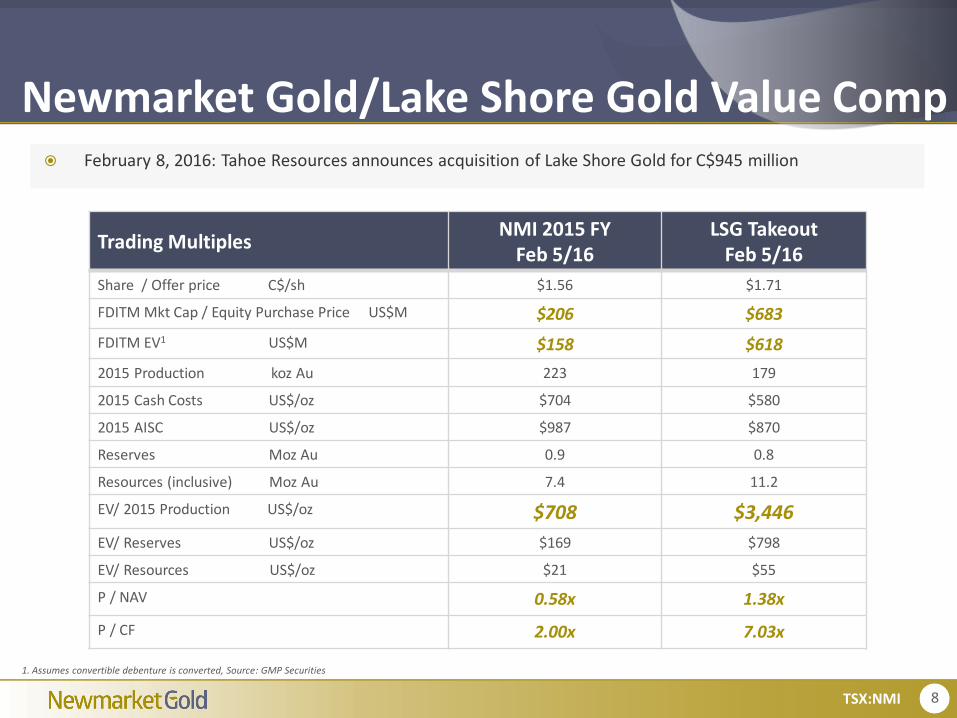

Newmarket Gold/Lake Shore Gold Value Comp

Trading MultiplesNMI 2015 FY

Feb 5/16LSG Takeout

Feb 5/16

Share / Offer price C$/sh $1.56 $1.71

FDITM Mkt Cap / Equity Purchase Price US$M $206 $683

FDITM EV1 US$M $158 $618

2015 Production koz Au 223 179

2015 Cash Costs US$/oz $704 $580

2015 AISC US$/oz $987 $870

Reserves Moz Au 0.9 0.8

Resources (inclusive) Moz Au 7.4 11.2

EV/ 2015 Production US$/oz $708 $3,446

EV/ Reserves US$/oz $169 $798

EV/ Resources US$/oz $21 $55

P / NAV 0.58x 1.38x

P / CF 2.00x 7.03x

1. Assumes convertible debenture is converted, Source: GMP Securities

February 8, 2016: Tahoe Resources announces acquisition of Lake Shore Gold for C$945 million

9TSX:NMI

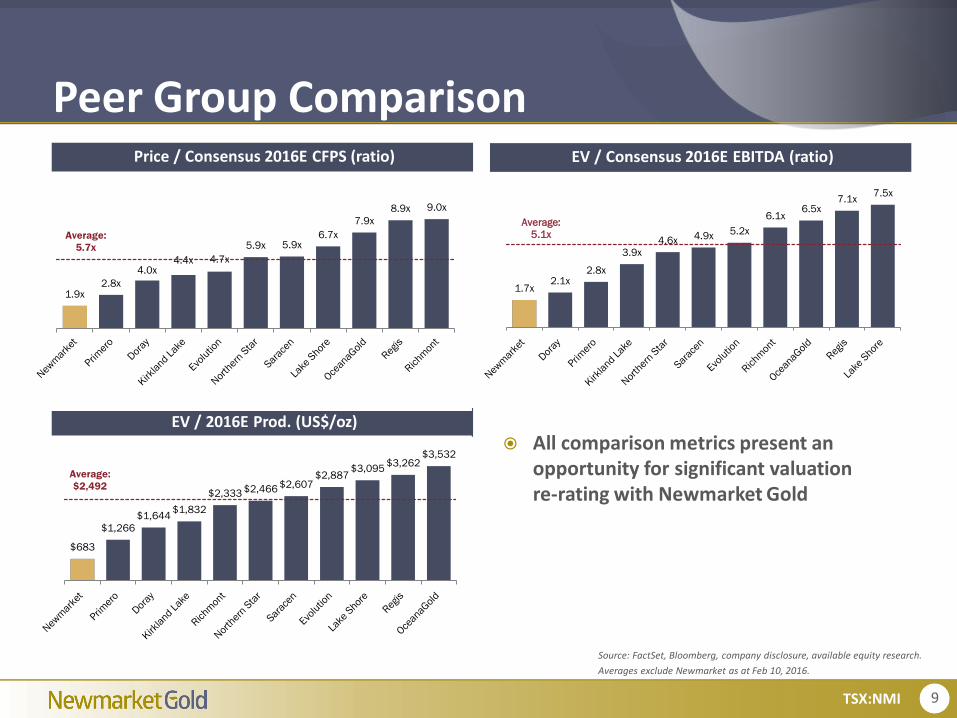

Source: FactSet, Bloomberg, company disclosure, available equity research.

Averages exclude Newmarket as at Feb 10, 2016.

Peer Group Comparison

All comparison metrics present an opportunity for significant valuation re-rating with Newmarket Gold

EV / 2016E Prod. (US$/oz)

Price / Consensus 2016E CFPS (ratio) EV / Consensus 2016E EBITDA (ratio)

$683

$1,266

$1,644 $1,832

$2,333 $2,466 $2,607 $2,887

$3,095 $3,262

$3,532

Average:

$2,492

1.9x 2.8x

4.0x 4.4x 4.7x

5.9x 5.9x 6.7x

7.9x

8.9x 9.0x

Average:

5.7x

1.7x 2.1x

2.8x

3.9x

4.6x 4.9x 5.2x

6.1x 6.5x

7.1x 7.5x

Average:

5.1x

10TSX:NMI

PRODUCING IN A TOP MINING JURISDICTIONCOSMO/UNION REEF

Location Northern TerritoryOwnership 100%Metals GoldMining UndergroundCapacity 2.0Mtpa Yrs in Production 2.5 Prod. Guidance 60k – 65k ouncesDiscovery Western Lodes Discovery

MAUD CREEK GOLD PROJECT

Location Northern TerritoryOwnership 100%Metals GoldMining Open Pit + UndergroundStage PEAM&I Resources 871,000 ozs @ 3.5 g/t1

1. See slide 25 for details on Mineral Resource and Reserve details 2. see Non-IFRS Disclosure p.32

FOSTERVILLE GOLD MINE

Location Bendigo, VictoriaOwnership 100% (2% Royalty)Metals GoldMining UndergroundCapacity 850Ktpa Yrs in Production +10 Prod. Guidance 110k – 120k ouncesDiscovery Eagle Fault Zone

STAWELL GOLD MINE

Location Stawell, VictoriaOwnership 100% (1% Royalty)Metals GoldMining UndergroundCapacity 1.0Mtpa Yrs in Production +30Prod. Guidance ~35k ouncesDiscovery Aurora B Gold Zone

2016E CONSOLIDATED GUIDANCE

Production: 205,000 - 220,000 ouncesOperating Cash Cost2: US$650 - US$725 per ounceAll-in sustaining costs2: US$950 - US$1,025 per ounce

AUSTRALIA

BIG HILL GOLD PROJECT

Location VictoriaOwnership 100%Metals GoldMining Open PitStage PermittingM&I Resources 160,000 ozs @ 1.68 g/t1

Producing Mine

Development Project

Mine site Discovery

11TSX:NMI

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

Feb 2011 Feb 2012 Feb 2013 Feb 2014 Feb 2015 Feb 2016

Gold

Pri

ce (

$/o

z)

Gold (US$/oz) (LHS) Gold (A$/oz) (LHS)

Source: Capital IQ as of February 11, 2016

AUSTRALIAN ADVANTAGE

A$1725/oz(Feb 18, 2016)

12TSX:NMI

2015 Record Production 123,095 oz

2015 Record Grade 6.11 g/t Au

Q3/15 Record Production 32,793

Q3/15 Record Grade 6.42g/t Au

Q3/15 Record Recoveries 89.7%

Q3/15 Operating Cash Costs per ounce $481

Q3/15 All-In Sustaining Costs per ounce $7971

Flagship Fosterville Mine – Low Cost Producer

U.S. Dollars unless stated otherwise 1. excludes corporate G&A

Eagle Fault discovery traced 600m along strike by 290m vertical height, open for expansion in all directions

Highlight drill intercepts include; 161g/t gold over 4.9m & 645g/t gold over 3.5m

Good continuity and mill reconciliation on Eagle fault ore

DISCOVERY

13TSX:NMI

Fosterville Mine (Longitudinal Projection)

Harrier Drill Drive

14TSX:NMI

LegendDrill InterceptsColoured by Gram-Metre

Mined Stopes Reserves Mineralization >30 5 - 15

Mined Development Mine Design Target Trend 15 – 20 1 - 5

12.8 g/t Gold over 8.5m

24.8 g/t Gold over 2.5m

16.4 g/t Gold (Visible Gold) over 16.5m

73.2 g/t Gold (Visible Gold) over 7.8m

385 g/t Gold (Visible Gold) over 3.4m

Fosterville Mine (Eagle Gold Zone) (DRILLING ONGOING)

View looking North

West East

5.3 g/t Gold over 5.9m

Schematic Cross Section

286 g/t Gold (Visible Gold) over 2.8m

11.1 g/t Gold over 4.9m

42.9 g/t Gold over 3.7m

161 g/t Gold over 4.9m645 g/t Gold over 3.5m

Total Strike 600m x 290m vertical height, open for expansion as at Jan/16

15TSX:NMI

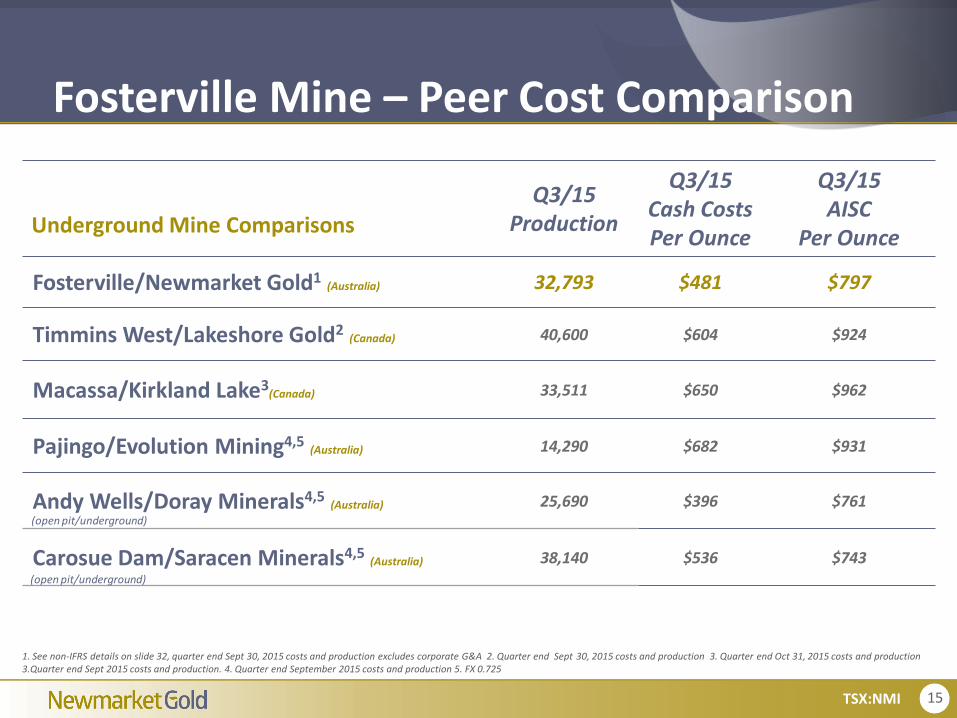

Fosterville Mine – Peer Cost Comparison

Q3/15Production

Q3/15Cash CostsPer Ounce

Q3/15 AISC

Per Ounce

Fosterville/Newmarket Gold1(Australia) 32,793 $481 $797

Timmins West/Lakeshore Gold2(Canada) 40,600 $604 $924

Macassa/Kirkland Lake3(Canada) 33,511 $650 $962

Pajingo/Evolution Mining4,5(Australia) 14,290 $682 $931

Andy Wells/Doray Minerals4,5(Australia) 25,690 $396 $761

Carosue Dam/Saracen Minerals4,5(Australia) 38,140 $536 $743

1. See non-IFRS details on slide 32, quarter end Sept 30, 2015 costs and production excludes corporate G&A 2. Quarter end Sept 30, 2015 costs and production 3. Quarter end Oct 31, 2015 costs and production 3.Quarter end Sept 2015 costs and production. 4. Quarter end September 2015 costs and production 5. FX 0.725

(open pit/underground)

(open pit/underground)

Underground Mine Comparisons

16TSX:NMI

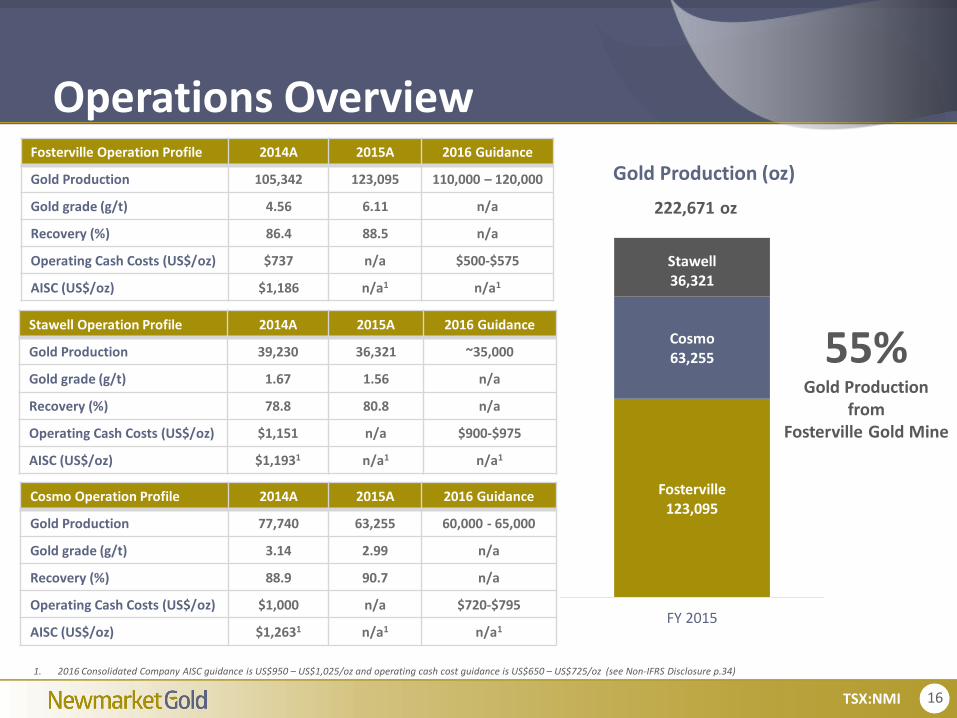

Fosterville123,095

Cosmo63,255

Stawell36,321

FY 2015

Gold Production (oz)

222,671 oz

Fosterville Operation Profile 2014A 2015A 2016 Guidance

Gold Production 105,342 123,095 110,000 – 120,000

Gold grade (g/t) 4.56 6.11 n/a

Recovery (%) 86.4 88.5 n/a

Operating Cash Costs (US$/oz) $737 n/a $500-$575

AISC (US$/oz) $1,186 n/a1 n/a1

Operations Overview

1. 2016 Consolidated Company AISC guidance is US$950 – US$1,025/oz and operating cash cost guidance is US$650 – US$725/oz (see Non-IFRS Disclosure p.34)

Cosmo Operation Profile 2014A 2015A 2016 Guidance

Gold Production 77,740 63,255 60,000 - 65,000

Gold grade (g/t) 3.14 2.99 n/a

Recovery (%) 88.9 90.7 n/a

Operating Cash Costs (US$/oz) $1,000 n/a $720-$795

AISC (US$/oz) $1,2631 n/a1 n/a1

Stawell Operation Profile 2014A 2015A 2016 Guidance

Gold Production 39,230 36,321 ~35,000

Gold grade (g/t) 1.67 1.56 n/a

Recovery (%) 78.8 80.8 n/a

Operating Cash Costs (US$/oz) $1,151 n/a $900-$975

AISC (US$/oz) $1,1931 n/a1 n/a1

55% Gold Production

from Fosterville Gold Mine

17TSX:NMI

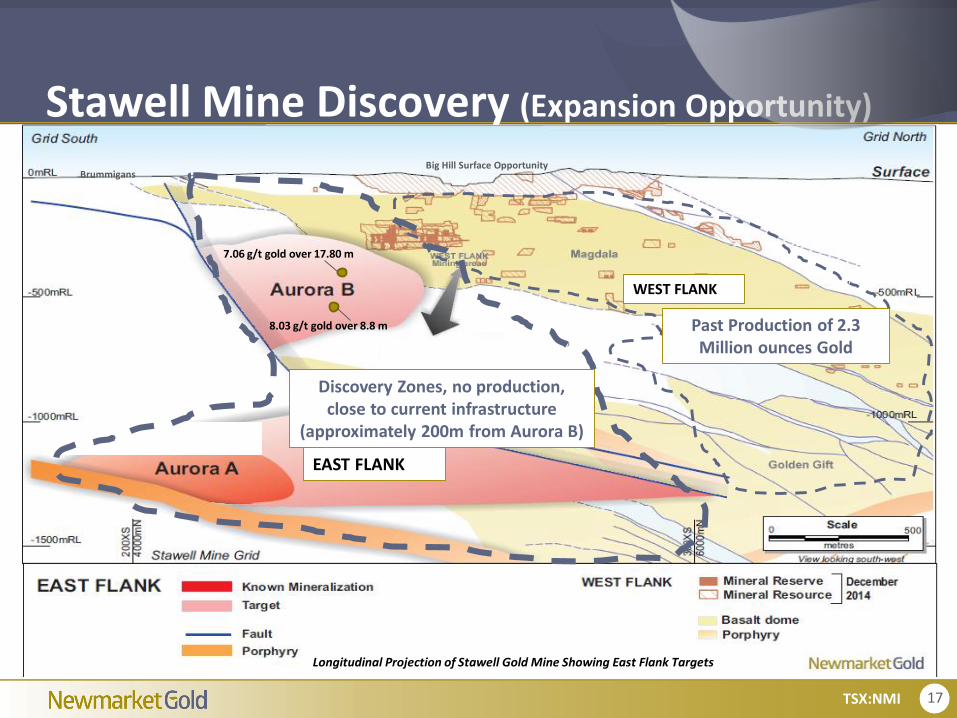

Stawell Mine Discovery (Expansion Opportunity)

Longitudinal Projection of Stawell Gold Mine Showing East Flank Targets

BrummigansBig Hill Surface Opportunity

WEST FLANK

Past Production of 2.3 Million ounces Gold

Past old

8.03 g/t gold over 8.8 m

EAST FLANK

7.06 g/t gold over 17.80 m

Discovery Zones, no production, close to current infrastructure

(approximately 200m from Aurora B)

18TSX:NMI

Stawell Mine Aurora B Discovery Section

East Flank TargetAurora B

East Flank TargetAurora A

Traditionally mined West Flank

Total production to date 2.3 million ounces

8.03 g/t gold over 8.8 m

7.06 g/t gold over 17.80 m

Magdala

19TSX:NMI

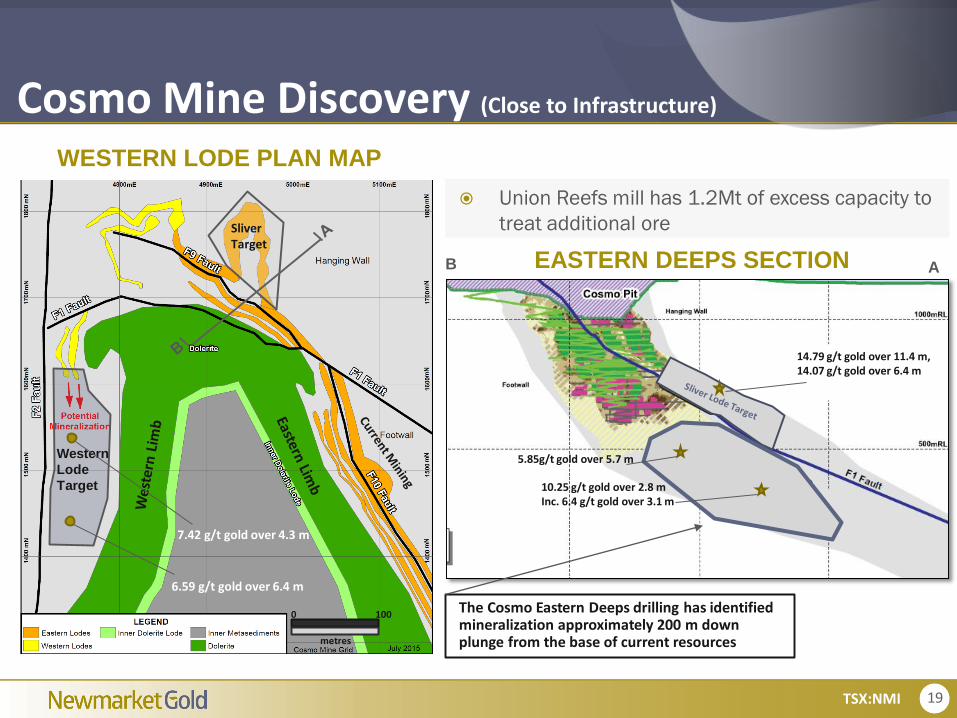

Cosmo Mine Discovery (Close to Infrastructure)

0 100

metres

Western

Lode

Target

SliverTarget

7.42 g/t gold over 4.3 m

6.59 g/t gold over 6.4 m

Cosmo Long Section

14.79 g/t gold over 11.4 m, 14.07 g/t gold over 6.4 m

5.85g/t gold over 5.7 m

10.25 g/t gold over 2.8 mInc. 6.4 g/t gold over 3.1 m

The Cosmo Eastern Deeps drilling has identified mineralization approximately 200 m down plunge from the base of current resources

WESTERN LODE PLAN MAP

EASTERN DEEPS SECTION

Union Reefs mill has 1.2Mt of excess capacity to

treat additional ore

AB

20TSX:NMI

0.56x

1.06x

1.35x

P/NAV NMI P/NAV top 25% quartile P/NAV Mean Mid-Tier

M&A Strategy Prudently acquire quality gold production to grow to 500,000 ounces of annual production

Targeting Australia and North America as preferred jurisdictions

Focus on operating cash costs below US$800 and All-in-costs below US$1000

Targeting +100,000 oz annual production opportunities and increased life of mine reserves

Accretive to CFPS, All-Sustaining costs, operating cash costs and market cap per share

NMI Opportunity

Source: company disclosure, Factset, Bloomberg, Peer Averages exclude Newmarket Gold, as at Feb 16, 2016

Top 1.42x

Top 1.26x

Australia Junior Gold Producers Australia Mid-tier Gold Producers

< 200,000 ounces

> 300,000 ounces

Newmarket Gold Valuation

21TSX:NMI

PEOPLEFounders have created over $30 billion of shareholder value Shareholder alignment C$12M invested, 8% equity ownership, performance share units vest based on share price performance

Demonstrated operational excellence

OPERATIONSThree operating mines in Australia with over 220,000 ounces of annual gold production, strong cash position, (US$36.5M) with 2015 consolidated record low operating cash costs $704 and AISC $987

Trend to higher consolidated grades and recoveries

GROWTHNewmarket’s vision is to become the next quality intermediate gold producer with annual production of 400-500kozs

Focusing on internal organic growth and a prudent accretive acquisition strategy

Newmarket Gold Advantage

DISCOVERIESThree new mine site gold discoveries close to current infrastructure with significant resource expansion opportunity – extensive drilling underway

New Eagle visible gold discovery at Fosterville traced over 600m x 290m open down plunge

Douglas ForsterPresident & CEO, Director

T: 604-559-8040E: [email protected]

www.newmarketgoldinc.com

Contact Us

Ryan KingVice President, Corporate Communications

T: 778-998-3700E: [email protected]

Laura LeporeDirector, Investor Relations

T: 416-728-3707E: [email protected]

TSX:NMI

23TSX:NMI

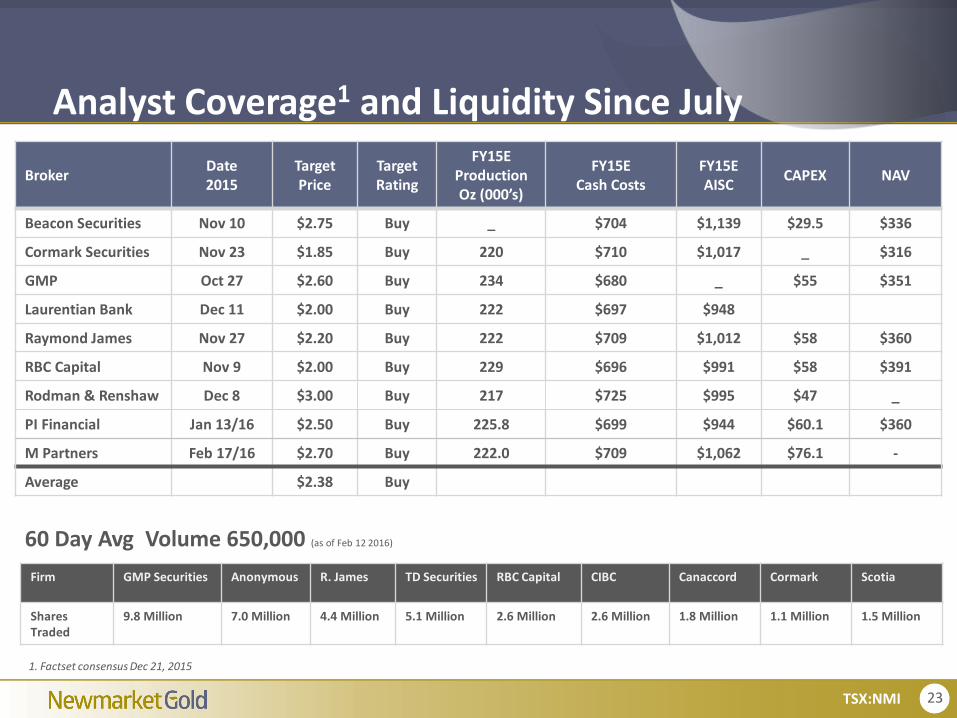

Analyst Coverage1 and Liquidity Since July

Firm GMP Securities Anonymous R. James TD Securities RBC Capital CIBC Canaccord Cormark Scotia

Shares Traded

9.8 Million 7.0 Million 4.4 Million 5.1 Million 2.6 Million 2.6 Million 1.8 Million 1.1 Million 1.5 Million

60 Day Avg Volume 650,000 (as of Feb 12 2016)

BrokerDate2015

Target Price

TargetRating

FY15EProductionOz (000’s)

FY15ECash Costs

FY15EAISC

CAPEX NAV

Beacon Securities Nov 10 $2.75 Buy _ $704 $1,139 $29.5 $336

Cormark Securities Nov 23 $1.85 Buy 220 $710 $1,017 _ $316

GMP Oct 27 $2.60 Buy 234 $680 _ $55 $351

Laurentian Bank Dec 11 $2.00 Buy 222 $697 $948

Raymond James Nov 27 $2.20 Buy 222 $709 $1,012 $58 $360

RBC Capital Nov 9 $2.00 Buy 229 $696 $991 $58 $391

Rodman & Renshaw Dec 8 $3.00 Buy 217 $725 $995 $47 _

PI Financial Jan 13/16 $2.50 Buy 225.8 $699 $944 $60.1 $360

M Partners Feb 17/16 $2.70 Buy 222.0 $709 $1,062 $76.1 -

Average $2.38 Buy

1. Factset consensus Dec 21, 2015

24TSX:NMI

$400

$800

$1,200

$1,600

$2,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Go

ld S

po

t (i

n A

UD

$)

Historical Gold Price (in AUD$)

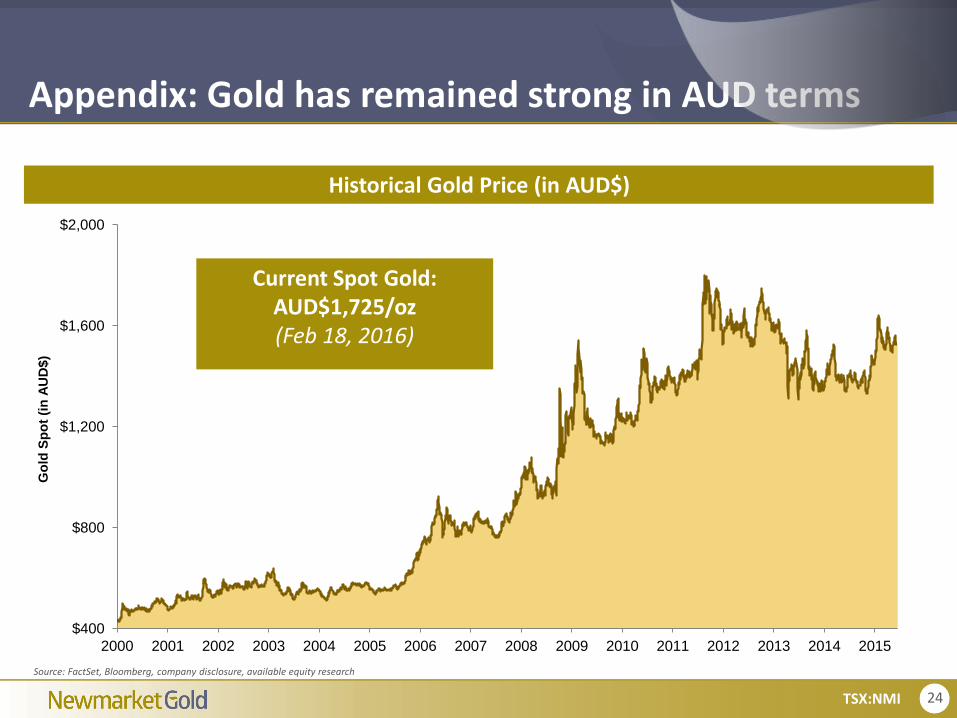

Appendix: Gold has remained strong in AUD terms

Source: FactSet, Bloomberg, company disclosure, available equity research

Current Spot Gold:AUD$1,725/oz(Feb 18, 2016)

25TSX:NMI

Appendix: Mineral Reserves and Resources

Inferred Resources Tonnes (Mt) Grade Au (g/t) Au (kozs)

Fosterville 5.8 3.72 699

Cosmo 1.0 2.72 84

Stawell 0.8 3.07 77

Burnside 6.9 1.47 323

Maud Creek 4.2 2.55 344

Union Reefs 4.3 2.23 305

Pine Creek 2.5 2.34 191

Inferred Resources 31.3 2.48 2,024

M&I Resources (incl.) Tonnes (Mt) Grade Au (g/t) Au (kozs)

Fosterville 16.6 4.18 2,151

Cosmo 5.0 3.35 539

Stawell 4.2 1.80 243

Burnside 7.5 1.38 335

Maud Creek 7.7 3.50 871

Union Reefs 3.0 2.43 236

Pine Creek 8.4 1.41 379

M&I Resources (incl.) 52.5 2.82 4,754Source: Crocodile Gold March 31, 2015 press release announcing 2014 year-end mineral reserves and mineral resources

2P Reserves Tonnes (Mt) Grade Au (g/t) Au (kozs)

Fosterville (Under Ground) 1.02 5.55 182

Fosterville (CIL Residues) 0.4 8.89 126

Cosmo 1.3 3.57 148

Stawell 0.8 2.80 36

Big Hill 2.9 1.54 145

Burnside 0.2 1.93 10

Maud Creek 1.1 5.40 184

Union Reefs 0.3 4.40 42

Pine Creek 1.3 1.55 62

2P Reserves 9.2 3.15 935

26TSX:NMI

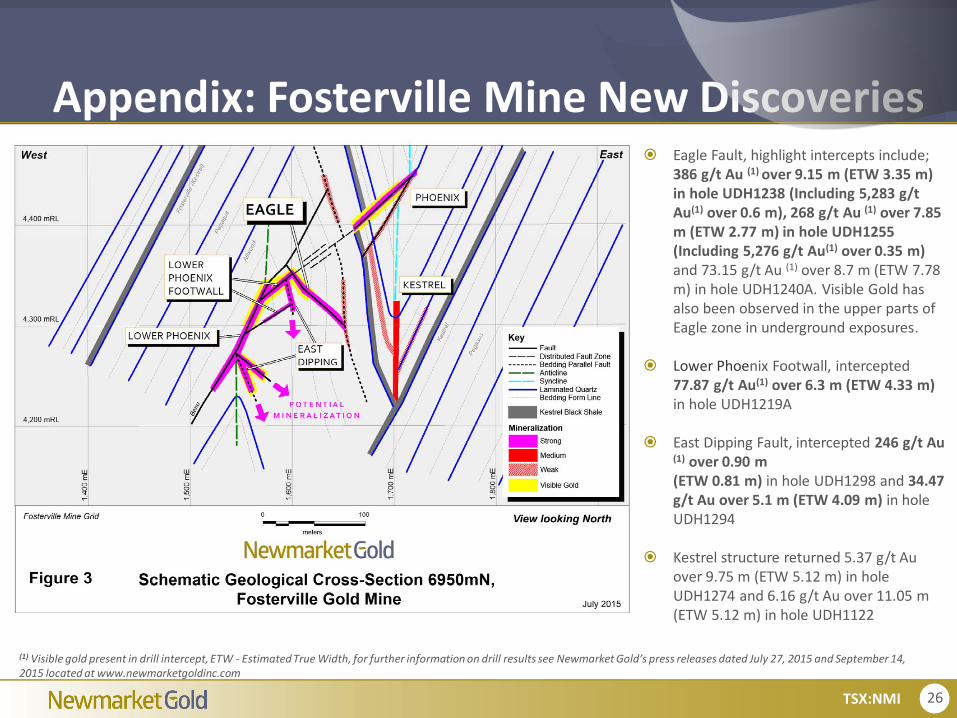

Appendix: Fosterville Mine New Discoveries Eagle Fault, highlight intercepts include;

386 g/t Au (1) over 9.15 m (ETW 3.35 m) in hole UDH1238 (Including 5,283 g/t Au(1) over 0.6 m), 268 g/t Au (1) over 7.85 m (ETW 2.77 m) in hole UDH1255 (Including 5,276 g/t Au(1) over 0.35 m)and 73.15 g/t Au (1) over 8.7 m (ETW 7.78 m) in hole UDH1240A. Visible Gold has also been observed in the upper parts of Eagle zone in underground exposures.

Lower Phoenix Footwall, intercepted 77.87 g/t Au(1) over 6.3 m (ETW 4.33 m)in hole UDH1219A

East Dipping Fault, intercepted 246 g/t Au (1) over 0.90 m (ETW 0.81 m) in hole UDH1298 and 34.47 g/t Au over 5.1 m (ETW 4.09 m) in hole UDH1294

Kestrel structure returned 5.37 g/t Au over 9.75 m (ETW 5.12 m) in hole UDH1274 and 6.16 g/t Au over 11.05 m (ETW 5.12 m) in hole UDH1122

(1) Visible gold present in drill intercept, ETW - Estimated True Width, for further information on drill results see Newmarket Gold’s press releases dated July 27, 2015 and September 14, 2015 located at www.newmarketgoldinc.com

27TSX:NMI

Appendix: Fosterville Mine (Eagle Zone - Visible Gold)

28TSX:NMI

Appendix: Cosmo Mine Western Lodes

A number of drill holes have now penetrated the Western Lodes Target.

Drill results for the Cosmo Western Lodes which are outside of the current mine plan include 7.42 g/t gold over 4.3 m (estimated true width 2.85 m) and 6.59 g/t gold over 6.4 m (estimate true width 1.65 m).

Work continues to fully define the potential of the Western Lodes

Target is located only 160 m from current development and has the potential to increase resources at Cosmo and expand the current mine plan to alternative mining areas.

Note: For further information on drill results see Newmarket Gold’s press release dated July 22, 2015 located at www.newmarketgoldinc.com

29TSX:NMI

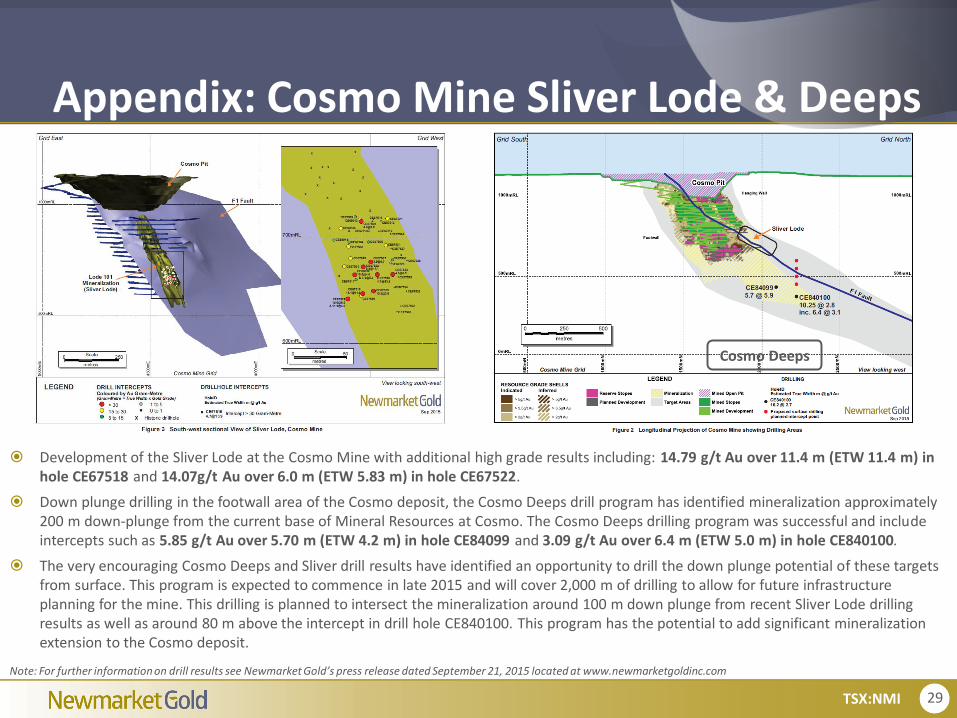

Appendix: Cosmo Mine Sliver Lode & Deeps

Development of the Sliver Lode at the Cosmo Mine with additional high grade results including: 14.79 g/t Au over 11.4 m (ETW 11.4 m) in hole CE67518 and 14.07g/t Au over 6.0 m (ETW 5.83 m) in hole CE67522.

Down plunge drilling in the footwall area of the Cosmo deposit, the Cosmo Deeps drill program has identified mineralization approximately 200 m down-plunge from the current base of Mineral Resources at Cosmo. The Cosmo Deeps drilling program was successful and include intercepts such as 5.85 g/t Au over 5.70 m (ETW 4.2 m) in hole CE84099 and 3.09 g/t Au over 6.4 m (ETW 5.0 m) in hole CE840100.

The very encouraging Cosmo Deeps and Sliver drill results have identified an opportunity to drill the down plunge potential of these targets from surface. This program is expected to commence in late 2015 and will cover 2,000 m of drilling to allow for future infrastructure planning for the mine. This drilling is planned to intersect the mineralization around 100 m down plunge from recent Sliver Lode drilling results as well as around 80 m above the intercept in drill hole CE840100. This program has the potential to add significant mineralization extension to the Cosmo deposit.

Note: For further information on drill results see Newmarket Gold’s press release dated September 21, 2015 located at www.newmarketgoldinc.com

Cosmo Deeps

30TSX:NMI

Appendix: Stawell Aurora B East Flank

New discovery of Aurora B East Flank mineralization is a significant event in the long history of the Stawell mine.

West Flank at Stawell has produced 2.3 million oz gold whereas the East Flank, where the Aurora B discovery has been made has no recorded production.

Drilling on the Aurora B discovery returned high-grade intercepts containing visible gold including: 7.06 g/t gold over 17.80 m (estimate true width 8.3 m).

Additional drilling on this new discovery is on-going.

Note: For further information on drill results see Newmarket Gold’s press release dated July 22, 2015 located at www.newmarketgoldinc.com

31TSX:NMI

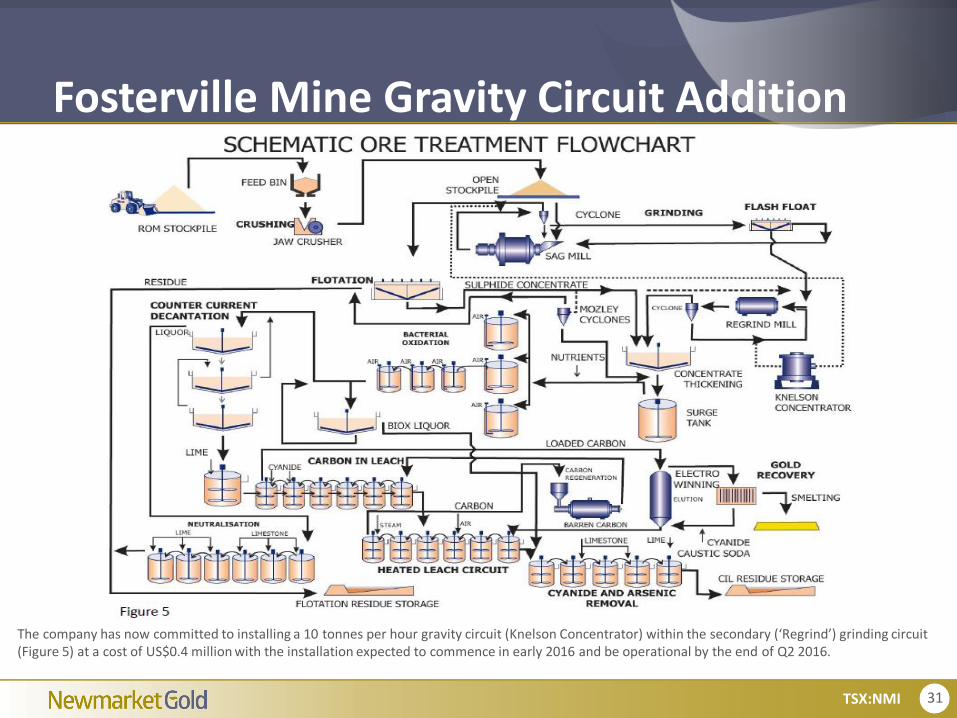

Fosterville Mine Gravity Circuit Addition

The company has now committed to installing a 10 tonnes per hour gravity circuit (Knelson Concentrator) within the secondary (‘Regrind’) grinding circuit (Figure 5) at a cost of US$0.4 million with the installation expected to commence in early 2016 and be operational by the end of Q2 2016.

32TSX:NMI

Appendix: Non-IFRS and Additional InformationNon-IFRS MeasuresNewmarket Gold believes that investors use certain indicators to assess gold mining companies. The indicators are intended to provide additional information and should not beconsidered in isolation or as a substitute for measures of performance in accordance with the International Financial Reporting Standards.“OperationalCash Costs perOunce” is a non-IFRS performance measure which could provide an indication of the mining and processing efficiency at the operations.The Company calculates operating cash costs per ounce by deducting silver sales revenue as a by-product from operating expenses per the consolidated statement ofoperations, then dividing by the gold ounces sold during the applicable period. Operating expenses include mine site operating costs such as mining, processing andadministration as well as royalties, however excludes depletion and depreciation, share-based payments and rehabilitation costs. There are variations in the method ofcomputation of “operational cash costs per ounce” as determined by the Company compared with other mining companies. For more detail on the operational cash costs perounce determination for Crocodile Gold, please visit www.sedar.com or www.newmarketgoldinc.com and review the latest Annual Financial Statements issued on March 19,2014.

“All-In Sustaining Costs per Ounce of Gold (“AISC”) Effective December 31, 2013, the Company has adopted an all-in sustaining cost (“AISC”) performance measure that reflectsall of the expenditures that are required to produce an ounce of gold from current operations. While there is no standardized meaning of the measure across the industry, theCompany’s definition conforms to the AISC definition as set out by the World Gold Council in its guidance dated June 27, 2013. The World Gold Council is a non-regulatory, non-profit organization established in 1987 whose members include global senior mining companies. The Company believes that this measure will be useful to external users inassessing operating performance and the ability to generate free cash flow from current operations. The Company defines AISC as the sum of operating cash costs (per above),sustaining capital (capital required to maintain current operations at existing levels), capital lease repayments, corporate general and administrative expenses, mine explorationwithin the known resources and rehabilitation accretion and amortization related to current operations. AISC excludes capital expenditures for significant improvements atexisting operations deemed to be expansionary in nature, exploration and evaluation related to growth projects, rehabilitation accretion and amortization not related to currentoperations, financing costs, debt repayments, share-based compensation not related to operations, and taxes.

Additional InformationNotes for Page 25: For information regarding mineral resource and reserve estimates, including parameters used to generate the estimates and depletion, please see thetechnical reports titled: NI43-101 TECHNICAL REPORT FOSTERVILLE GOLD MINE, VICTORIA, AUSTRALIA PREPARED FOR CROCODILE GOLD CORP dated March 31, 2015 and;NI43-101 TECHNICAL REPORT – BIG HILL ENHANCED DEVELOPMENT PROJECT AT STAWELL GOLD MINE MINERAL RESOURCES & RESERVES PREPARED FOR CROCODILE GOLDCORP dated June 6, 2014. For the Northern Territory Mineral Reserve Estimates please refer to the technical reports titled: REPORT ON THE MINERAL RESOURCES & MINERALRESERVES OF THE COSMO DEEPS GOLD PROJECT dated March 31, 2015; NI 43-101 TECHNICAL REPORT STAWELL GOLD MINE, VICTORIA, AUSTRALIA PREPARED FOR CROCODILEGOLD CORP dated March 31, 2015; REPORT ON THE MINERAL RESOURCES & MINERAL RESERVES OF THE UNION REEFS GOLD PROJECT dated December 31, 2012; REPORT ONTHE MINERAL RESOURCES & MINERAL RESERVES OF THE PINE CREEK GOLD PROJECT dated December 31, 2012; REPORT ON THE MINERAL RESOURCES & MINERAL RESERVES OFTHE MAUD CREEK GOLD PROJECT dated December 31, 2012 and; REPORT ON THE MINERAL RESOURCES & MINERAL RESERVES OF THE BURNSIDE GOLD AND BASE METALPROJECT dated December 12, 2013.Mineral resources that are not mineral reserves do not have demonstrated economic viability.

Qualified PersonMark Edwards, MAusIMM (CP), MAIG, General Manager, Exploration, Newmarket Gold, is a "qualified person" as such term is defined in National Instrument 43-101 and hasreviewed and approved the technical information and data included in this presentation.