Newmarket Gold and Crocodile Gold Combination

38

Establishing a New Platform for Gold Consolidation Combination of Newmarket Gold and Crocodile Gold A First Step In Executing a Gold-Focused Consolidation Strategy May 11, 2015 TSX-V: NGN TSX: CRK

-

Upload

crocodile-gold-corp -

Category

Documents

-

view

59 -

download

2

Transcript of Newmarket Gold and Crocodile Gold Combination

Establishing a New Platform for Gold Consolidation

Combination of Newmarket Gold and Crocodile Gold A First Step In Executing a Gold-Focused Consolidation Strategy

May 11, 2015 TSX-V: NGN

TSX: CRK

Establishing a New Platform for Gold Consolidation 2

Cautionary Disclaimers This presentation contains forward-looking information, including, but not limited to, guidance on estimated annual production and cash costs and information and expectations about the completion of the combination of Newmarket Gold Inc. (“Newmarket” or the

“Company”) and Crocodile Gold Corp. (“Crocodile Gold”) and the offering and the intended participation of management and directors of Newmarket in the offering, the composition of the board of directors of resulting issuer and its senior executive team, future

performance based on current results and past production, expected cash costs and mineral resource estimates. This forward-looking information is not based on historical facts, but rather on current expectations and projections about future events and is subject

to risks and uncertainties. These risks and uncertainties could cause Newmarket, Crocodile or the resulting issuer’s actual results to differ materially from the future results expressed or implied in this presentation. Such risks may include, without limitation: risks

and uncertainties relating to the completion of the transactions as described herein, the ability to successfully integrate operations and realize the anticipated benefits of the Crocodile Gold acquisition; risks and uncertainties relating to foreign currency fluctuations;

risks inherent in mining including environmental hazards, unusual or unexpected geological formations, ground control problems and flooding; liabilities inherent in mine development and production; geological, mining and processing technical problems; risks

associated with the estimation of mineral resources and reserves and the geology, grade and continuity of mineral deposits; the possibility that future exploration, development or mining results will not be consistent with Newmarket’s expectations; ability to obtain

required mine licenses, mine permits and regulatory approvals required in connection with mining and mineral processing operations; competition for, among other things, capital, acquisitions of reserves, undeveloped lands and skilled personnel; incorrect

assessments of the value of acquisitions; changes in commodity prices and exchange rates; various events that could disrupt operations and/or the transportation of mineral products, including labour disputes, shortages or stoppages and severe weather

conditions; the demand for and availability of rail, port and other transportation services; the ability to secure adequate financing, the risk that management and directors of Newmarket may not ultimately participate in the offering to the extent anticipated, and

management's ability to anticipate and manage the foregoing factors and risks. The forward looking information contained in this document is based on a number of assumptions including, but not limited to, the successful completion of the transaction on the

terms as described herein; foreign currency rates; metal prices; estimation of mineral resources and reserves and the geology; grade, tonnage, dilution and metallurgical and other characteristics of ore; production capabilities and cost estimates. Newmarket uses

certain non-GAAP performance measures in this presentation. These performance measures have no meaning under IFRS and, therefore, amounts presented may not be comparable to similar data presented by other mining companies. The data is intended to

provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Operating cash costs per ounce of gold and all-in sustaining costs per ounce of gold (“AISC”) are non-GAAP

measures that Newmarket uses as key performance measures to monitor performance and ability to generate cash flow. Management uses these statistics to assess how well Newmarket’s producing mines are performing compared to plan and to assess overall

efficiency and effectiveness of the mining operations. Newmarket provides operating cash cost and AISC information as it is a key performance indicator required by users of its financial information in order to assess its profit potential and performance relative to

its peers. The operating cash cost figure is calculated by deducting silver sales revenue as a by-product from operating expenses per the consolidated statement of operations, then dividing by the gold ounces sold during the applicable period. Operating expenses

include mine site operating costs such as mining, processing and administration as well as royalties, however excludes depletion and depreciation, share-based payments and rehabilitation costs. AISC reflects all of the expenditures that are required to produce an

ounce of gold from current operations. While there is no standardized meaning of the measure across the industry, Newmarkets’s definition conforms to the AISC definition as set out by the World Gold Council in its guidance dated June 27, 2013. The World Gold

Council is a non-regulatory, non-profit organization established in 1987 whose members include global senior mining companies. Newmarket believes that this measure will be useful to external users in assessing operating performance and the ability to generate

free cash flow from current operations. Newmarket defines AISC as the sum of operating cash costs (per above), sustaining capital (capital required to maintain current operations at existing levels), capital lease repayments, corporate general and administrative

expenses, in-mine exploration expenses and rehabilitation accretion and amortization related to current operations. AISC excludes capital expenditures for significant improvements at existing operations deemed to be expansionary in nature, exploration and

evaluation related to growth projects, rehabilitation accretion and amortization not related to current operations, financing costs, debt repayments, share-based compensation not related to operations, and taxes. The information presented herein was approved by

management of Newmarket on May 11, 2015. For further details of other risks and uncertainties see “Risk Factors” and “Cautionary Statements” in each of Newmarket’s Management’s Discussion and Analysis and Crocodile Gold’s Annual Information Form.

Note: All dollar amounts are in Cdn dollars unless otherwise denoted. The disclosure in this presentation uses mineral reserve and mineral resource classification terms that comply with reporting standards in Canada, and certain mineral resource estimates are

made in accordance with Canadian National Instrument 43-101—Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral

projects. These standards differ significantly from the mineral reserve disclosure requirements of the United States Securities Exchange Commission (the “SEC”) set forth in Industry Guide 7. Consequently, information regarding mineralization contained in this

presentation is not comparable to similar information that would generally be disclosed by U.S. companies in accordance with the rules of the SEC. In particular, the SEC’s Industry Guide 7 applies different standards in order to classify mineralization as a reserve.

As a result, the definitions of proven and probable reserves used in NI 43-101 differ from the definitions used by the SEC in Industry Guide 7. Under SEC standards, mineralization may not be classified as a “reserve” unless the determination has been made that

the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Among other things, all necessary permits would be required to be in hand or issuance imminent in order to classify mineralized material as

reserves under the SEC standards. Accordingly, mineral reserve estimates contained in this presentation may not qualify as “reserves” under SEC standards. In addition, this presentation uses the terms “measured mineral resources,” “indicated mineral resources”

and “inferred mineral resources” to comply with the reporting standards in Canada. The SEC does not recognize mineral resources and U.S. companies are generally not permitted to disclose mineral resources of any category in documents they file with the SEC.

Investors are specifically cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into mineral reserves as defined in NI 43-101 or Industry Guide 7. Further, “inferred mineral resources” have a great amount of

uncertainty as to their existence and as to whether they can be mined legally or economically. Therefore, investors are also cautioned not to assume that all or any part of an inferred resource exists. It cannot be assumed that all or any part of “measured mineral

resources,” “indicated mineral resources,” or “inferred mineral resources” will ever be upgraded to a higher category. Investors are cautioned not to assume that any part of the reported “measured mineral resources,” “indicated mineral resources,” or “inferred

mineral resources” in this presentation is economically or legally mineable. For the above reasons, information contained in this presentation containing descriptions of our mineral reserve and mineral resource estimates is not comparable to similar information

made public by U.S. companies subject to the reporting and disclosure requirements of the SEC.

All scientific and technical information relating to the Cosmo Gold Mine is based on and derived from the NI 43-101 report prepared for Crocodile Gold entitled “Report on the Mineral Resources and Mineral Reserves of the Cosmo Gold Project”, dated effective

December 31, 2014. All scientific and technical information relating to the Fosterville Gold Mine is based on and derived from the NI 43-101 report prepared for Crocodile Gold entitled Report on the Mineral Resources and Mineral Reserves of the Fosterville Gold

Mine Victoria, Australia”, dated effective December 31, 2014. All scientific and technical information relating to the Stawell Gold Mine is based on and derived from the NI 43-101 report prepared for Crocodile Gold entitled “Report on the Mineral Resources and

Mineral Reserves of the Stawell Gold Mine in Victoria, Australia”, dated effective December 31, 2014. All scientific and technical information relating to the Big Hill Enhanced Development Project is based on and derived from the NI 43-101 report prepared for

Crocodile Gold entitled “Big Hill Development Project at Stawell Gold Mine – Mineral Resources & Reserves”, dated effective March 31, 2014.All of the above mentioned technical reports were prepared by “qualified persons” within the meaning of NI 43-101. The

information contained herein is subject to all of the assumptions, qualifications and procedures set out in each of the technical reports and reference should be made to the full details of the technical reports which have been filed with the applicable regulatory

authorities and is available on Crocodile Gold’s profile at www.sedar.com. Mark Edwards, MAusIMM (CP), MAIG, General Manager Exploration and Business Development for Crocodile, is a "qualified person" as such term is defined in NI 43-101 and has reviewed

and approved the technical information and data included in this presentation and has verified that no limitations were imposed on his verification process. See Crocodile Gold’s March 31, 2015 news release for further details with respect to the mineral resource

information contained in this presentation.

This presentation does not constitute an offer to sell or a solicitation of an offer to buy any of the securities in the United States, nor shall there be any sale of these securities in any jurisdiction in which such offer, solicitation or sale would be unlawful. The

securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”) or any state securities laws and may not be offered or sold within the United States or to U.S. Persons unless registered under

the U.S. Securities Act and applicable state securities laws or an exemption from such registration is available. Certain information contained on this presentation with respect to other companies and their business and operation has been obtained or quoted from

publicly available sources, such as continuous disclosure documents, independent publications, media articles, third party websites (collectively, the “Publications”). In certain cases, these sources make no representations as to the reliability of the information they

publish. Further, the analyses and opinions reflected in these Publications are subject to a series of assumptions about future events. There are a number of factors that can cause the results to differ materially from those described in these publications. None of

the Company or its representatives independently verified the accuracy or completeness of the information contained in the Publications or assume any responsibility for the completeness or accuracy of the information derived from these Publications.

Establishing a New Platform for Gold Consolidation

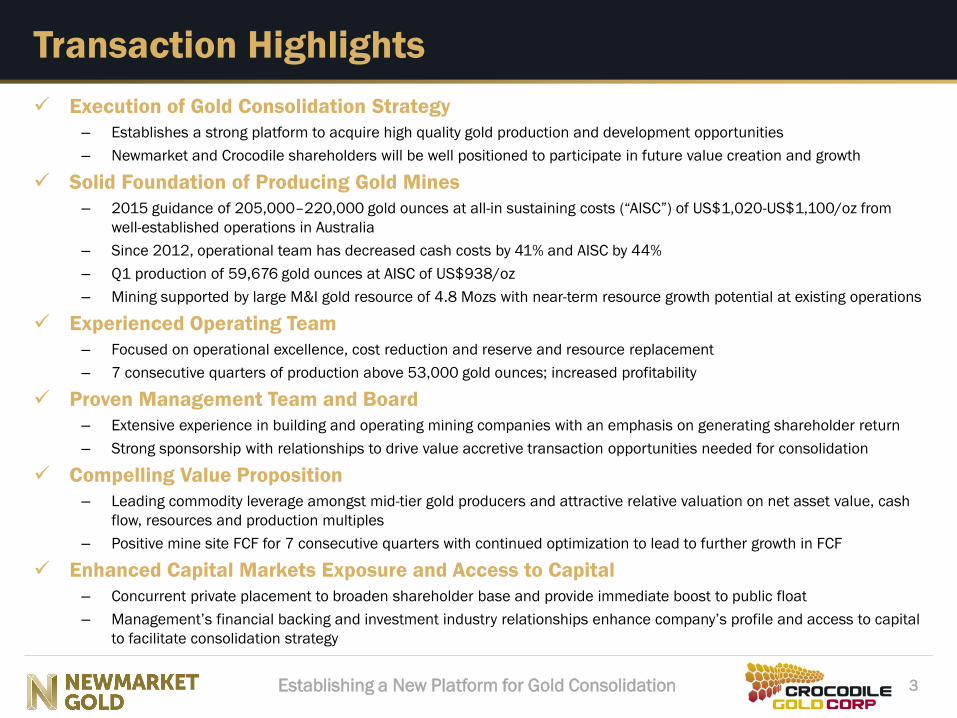

Execution of Gold Consolidation Strategy

– Establishes a strong platform to acquire high quality gold production and development opportunities

– Newmarket and Crocodile shareholders will be well positioned to participate in future value creation and growth

Solid Foundation of Producing Gold Mines

– 2015 guidance of 205,000–220,000 gold ounces at all-in sustaining costs (“AISC”) of US$1,020-US$1,100/oz from

well-established operations in Australia

– Since 2012, operational team has decreased cash costs by 41% and AISC by 44%

– Q1 production of 59,676 gold ounces at AISC of US$938/oz

– Mining supported by large M&I gold resource of 4.8 Mozs with near-term resource growth potential at existing operations

Experienced Operating Team

– Focused on operational excellence, cost reduction and reserve and resource replacement

– 7 consecutive quarters of production above 53,000 gold ounces; increased profitability

Proven Management Team and Board

– Extensive experience in building and operating mining companies with an emphasis on generating shareholder return

– Strong sponsorship with relationships to drive value accretive transaction opportunities needed for consolidation

Compelling Value Proposition

– Leading commodity leverage amongst mid-tier gold producers and attractive relative valuation on net asset value, cash

flow, resources and production multiples

– Positive mine site FCF for 7 consecutive quarters with continued optimization to lead to further growth in FCF

Enhanced Capital Markets Exposure and Access to Capital

– Concurrent private placement to broaden shareholder base and provide immediate boost to public float

– Management’s financial backing and investment industry relationships enhance company’s profile and access to capital

to facilitate consolidation strategy

3

Transaction Highlights

Establishing a New Platform for Gold Consolidation

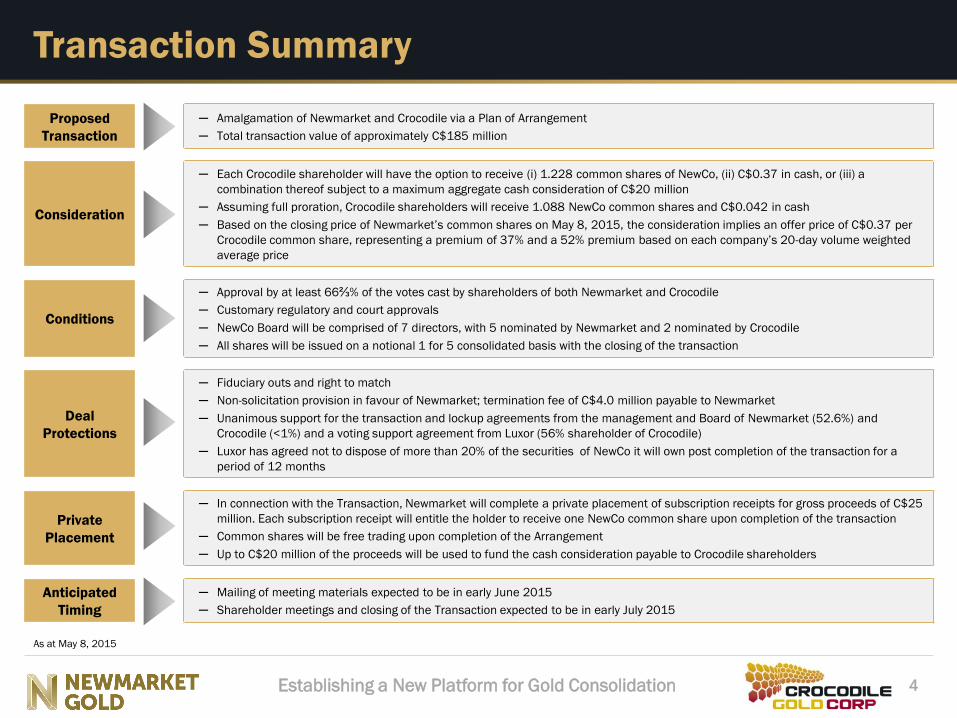

Proposed

Transaction

─ Amalgamation of Newmarket and Crocodile via a Plan of Arrangement

─ Total transaction value of approximately C$185 million

Consideration

─ Each Crocodile shareholder will have the option to receive (i) 1.228 common shares of NewCo, (ii) C$0.37 in cash, or (iii) a

combination thereof subject to a maximum aggregate cash consideration of C$20 million

─ Assuming full proration, Crocodile shareholders will receive 1.088 NewCo common shares and C$0.042 in cash

─ Based on the closing price of Newmarket’s common shares on May 8, 2015, the consideration implies an offer price of C$0.37 per

Crocodile common share, representing a premium of 37% and a 52% premium based on each company’s 20-day volume weighted

average price

Conditions

─ Approval by at least 66⅔% of the votes cast by shareholders of both Newmarket and Crocodile

─ Customary regulatory and court approvals

─ NewCo Board will be comprised of 7 directors, with 5 nominated by Newmarket and 2 nominated by Crocodile

─ All shares will be issued on a notional 1 for 5 consolidated basis with the closing of the transaction

Deal

Protections

─ Fiduciary outs and right to match

─ Non-solicitation provision in favour of Newmarket; termination fee of C$4.0 million payable to Newmarket

─ Unanimous support for the transaction and lockup agreements from the management and Board of Newmarket (52.6%) and

Crocodile (<1%) and a voting support agreement from Luxor (56% shareholder of Crocodile)

─ Luxor has agreed not to dispose of more than 20% of the securities of NewCo it will own post completion of the transaction for a

period of 12 months

Private

Placement

─ In connection with the Transaction, Newmarket will complete a private placement of subscription receipts for gross proceeds of C$25

million. Each subscription receipt will entitle the holder to receive one NewCo common share upon completion of the transaction

─ Common shares will be free trading upon completion of the Arrangement

─ Up to C$20 million of the proceeds will be used to fund the cash consideration payable to Crocodile shareholders

Anticipated

Timing

─ Mailing of meeting materials expected to be in early June 2015

─ Shareholder meetings and closing of the Transaction expected to be in early July 2015

4

Transaction Summary

As at May 8, 2015

Establishing a New Platform for Gold Consolidation

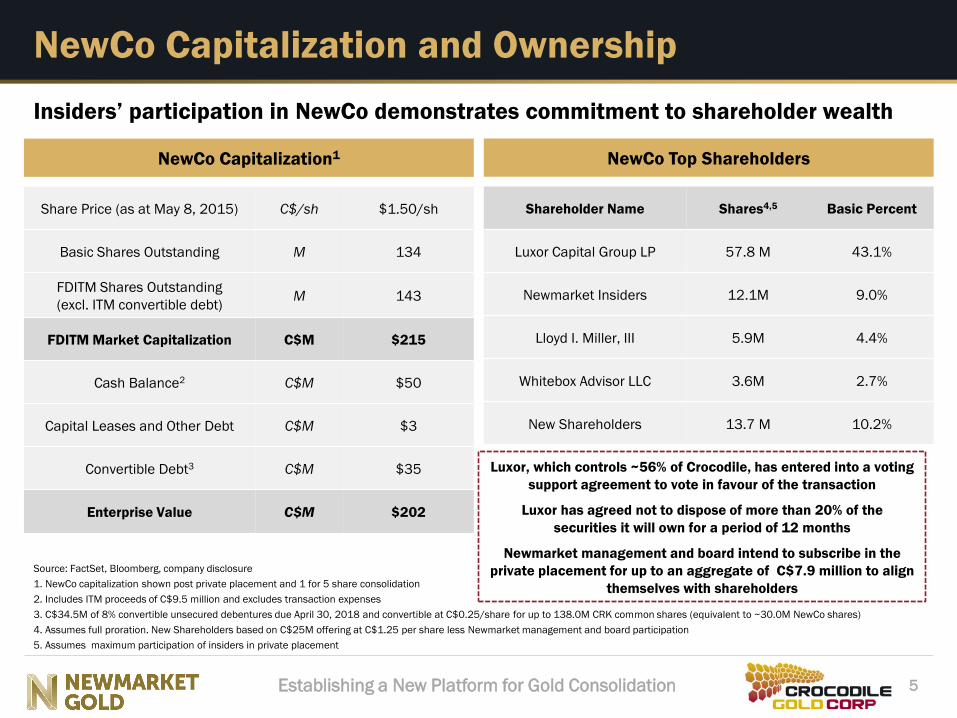

Share Price (as at May 8, 2015) C$/sh $1.50/sh

Basic Shares Outstanding M 134

FDITM Shares Outstanding

(excl. ITM convertible debt) M 143

FDITM Market Capitalization C$M $215

Cash Balance2 C$M $50

Capital Leases and Other Debt C$M $3

Convertible Debt3 C$M $35

Enterprise Value C$M $202

5

NewCo Capitalization and Ownership

Source: FactSet, Bloomberg, company disclosure

1. NewCo capitalization shown post private placement and 1 for 5 share consolidation

2. Includes ITM proceeds of C$9.5 million and excludes transaction expenses

3. C$34.5M of 8% convertible unsecured debentures due April 30, 2018 and convertible at C$0.25/share for up to 138.0M CRK common shares (equivalent to ~30.0M NewCo shares)

4. Assumes full proration. New Shareholders based on C$25M offering at C$1.25 per share less Newmarket management and board participation

5. Assumes maximum participation of insiders in private placement

NewCo Top Shareholders NewCo Capitalization1

Shareholder Name Shares4,5 Basic Percent

Luxor Capital Group LP 57.8 M 43.1%

Newmarket Insiders 12.1M 9.0%

Lloyd I. Miller, III 5.9M 4.4%

Whitebox Advisor LLC 3.6M 2.7%

New Shareholders 13.7 M 10.2%

Insiders’ participation in NewCo demonstrates commitment to shareholder wealth

Luxor, which controls ~56% of Crocodile, has entered into a voting

support agreement to vote in favour of the transaction

Luxor has agreed not to dispose of more than 20% of the

securities it will own for a period of 12 months

Newmarket management and board intend to subscribe in the

private placement for up to an aggregate of C$7.9 million to align

themselves with shareholders

Establishing a New Platform for Gold Consolidation

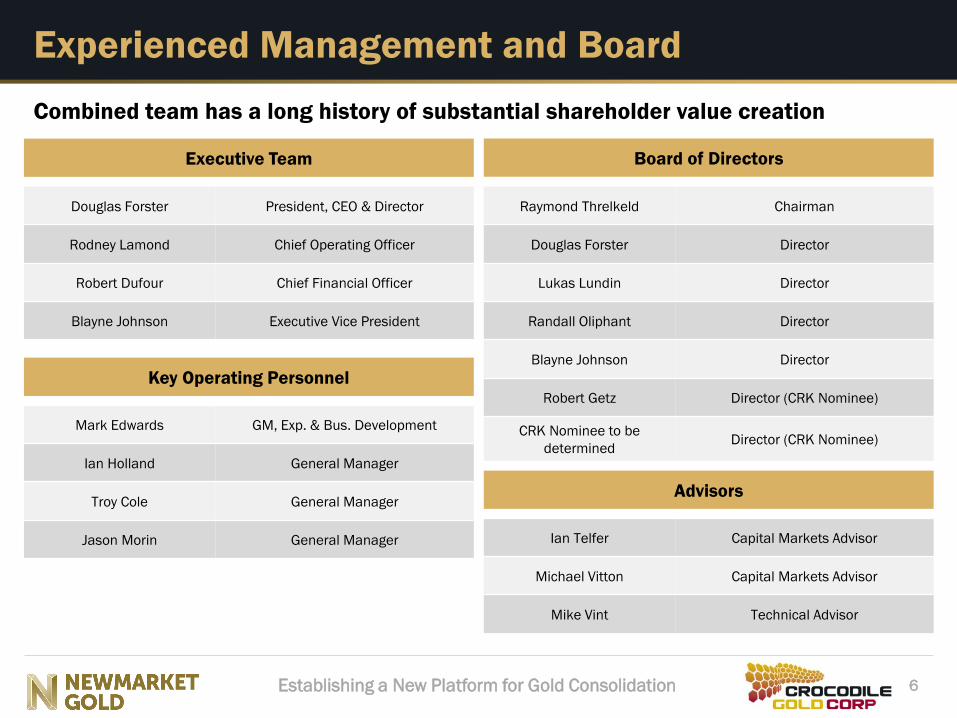

Executive Team

Douglas Forster President, CEO & Director

Rodney Lamond Chief Operating Officer

Robert Dufour Chief Financial Officer

Blayne Johnson Executive Vice President

6

Experienced Management and Board

Board of Directors

Raymond Threlkeld Chairman

Douglas Forster Director

Lukas Lundin Director

Randall Oliphant Director

Blayne Johnson Director

Robert Getz Director (CRK Nominee)

CRK Nominee to be

determined Director (CRK Nominee)

Combined team has a long history of substantial shareholder value creation

Advisors

Ian Telfer Capital Markets Advisor

Michael Vitton Capital Markets Advisor

Mike Vint Technical Advisor

Mark Edwards GM, Exp. & Bus. Development

Ian Holland General Manager

Troy Cole General Manager

Jason Morin General Manager

Key Operating Personnel

Establishing a New Platform for Gold Consolidation 7

Newmarket’s Proven Track Record of Execution

Principals have founded, managed and sold mining companies with a combined

market value of approximately $30 billion

“Newmarket Gold Inc.’s mission is to deliver exceptional shareholder value through a

disciplined approach to acquiring quality, gold production assets and outstanding

development opportunities in politically stable jurisdictions worldwide”

Public Sold

Establishing a New Platform for Gold Consolidation

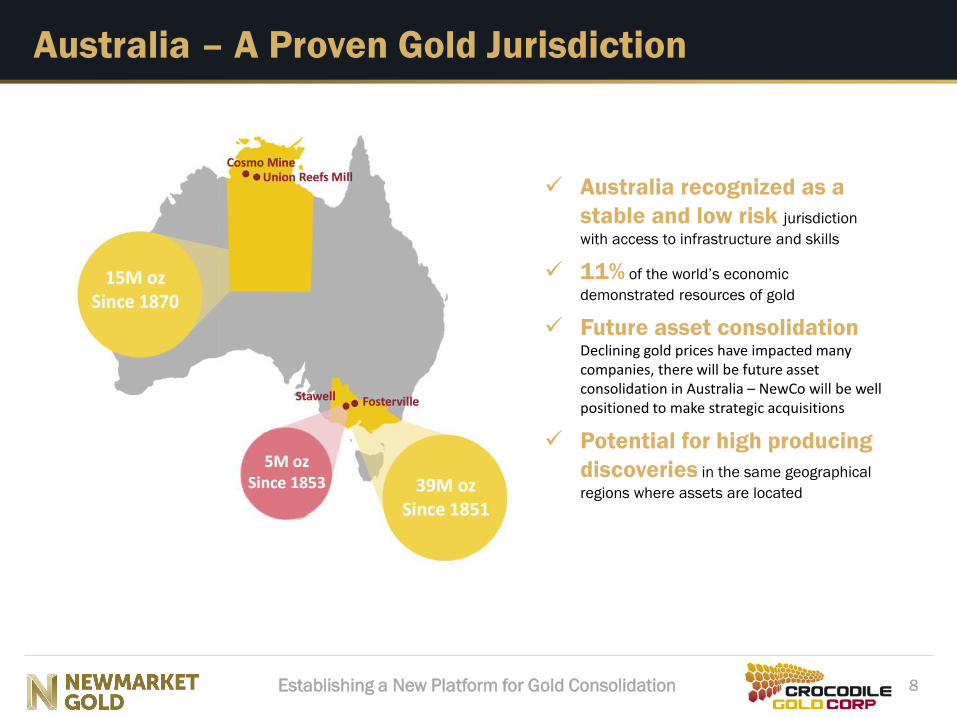

Australia – A Proven Gold Jurisdiction

8

Australia recognized as a

stable and low risk jurisdiction

with access to infrastructure and skills

11% of the world’s economic

demonstrated resources of gold

Future asset consolidation Declining gold prices have impacted many companies, there will be future asset consolidation in Australia – NewCo will be well positioned to make strategic acquisitions

Potential for high producing

discoveries in the same geographical

regions where assets are located

Establishing a New Platform for Gold Consolidation

Fosterville

9

Strong Operating Platform

Cosmo

Stawell Union Reefs Mill

[NTD: Insert asset image]

Three process facilities, 787 employees and contractors

Establishing a New Platform for Gold Consolidation

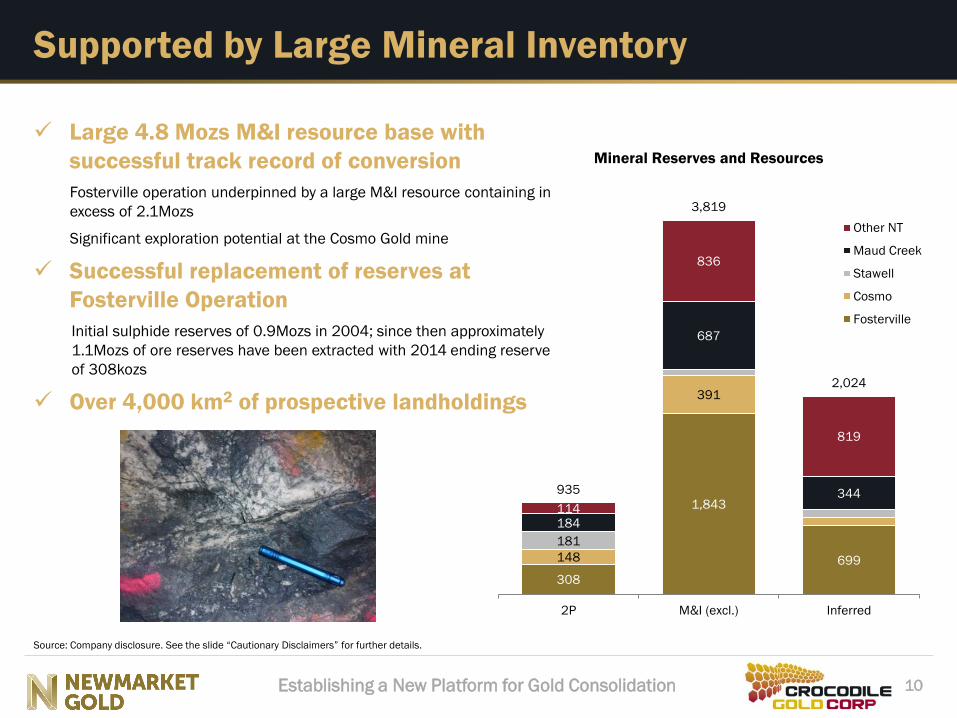

308

1,843

699 148

391

181

184

687

344

114

836

819

935

3,819

2,024

2P M&I (excl.) Inferred

Mineral Reserves and Resources

Other NT

Maud Creek

Stawell

Cosmo

Fosterville

10

Supported by Large Mineral Inventory

Source: Company disclosure. See the slide “Cautionary Disclaimers” for further details.

Large 4.8 Mozs M&I resource base with

successful track record of conversion

Fosterville operation underpinned by a large M&I resource containing in

excess of 2.1Mozs

Significant exploration potential at the Cosmo Gold mine

Successful replacement of reserves at

Fosterville Operation

Initial sulphide reserves of 0.9Mozs in 2004; since then approximately

1.1Mozs of ore reserves have been extracted with 2014 ending reserve

of 308kozs

Over 4,000 km2 of prospective landholdings

Establishing a New Platform for Gold Consolidation

Fosterville:

64 kozs

Fosterville:

98 kozs

Fosterville:

105 kozs

Fosterville:

100 - 105 kozs

Cosmo:

41 kozs

Cosmo:

74 kozs

Cosmo:

78 kozs

Cosmo:

75 - 85 kozs Stawell:

50 kozs

Stawell:

38 kozs

Stawell:

39 kozs

Stawell:

~30 kozsCurrent

Production:

Base:

205 - 220 kozs

Organic

Growth

External

Growth

156 kozs

211 kozs222 kozs 205 - 220 kozs

2012A 2013A 2014A 2015E 2016E+

Go

ld P

rod

uc

tio

n (

ko

zs)

11

Historical Growth and Sustainable Production

Source: Company disclosure. See the slide “Cautionary Disclaimers” for further details.

Record production in 2014 of 222,312 ozs, up 5.5% from 2013

Achieved second consecutive year of production above 210,000 ozs

Execute consolidation strategy of high quality gold assets

Seek growth opportunities through both organic and external initiatives

Q1 2015 production of 59,676 ozs, ahead of guidance Esmeralda

Wonga

Maud Creek

Big Hill

2P: 298kozs

M&I: 1,821kozs

Establishing a New Platform for Gold Consolidation 12

Demonstrated Ability to Decrease Costs

Source: Company disclosure

$1,680/oz

$1,386/oz

$1,236/oz

$1,020 -

$1,100/oz

$938/oz

$1,167/oz

$1,027/oz

$905/oz $780 -

$860/oz

$683/oz

2012A 2013A 2014A 2015E Q1 2015A

Co

st

Pe

r O

un

ce

(U

S$

/o

z)

All-in sustaining costs per oz Operating costs per oz

Consistent decrease in

operating costs and AISC

Operating cash costs have decreased 41%

since 2012

All-in sustaining costs have decreased 44%

since 2012

Further cost reductions

expected in 2015 and beyond

Q1 cash costs of US$683/oz and AISC of

US$938/oz, significantly below guidance

Management expects continued optimization

efforts to lead to further declines in operating

costs and AISC

Decreasing Costs

Establishing a New Platform for Gold Consolidation 13

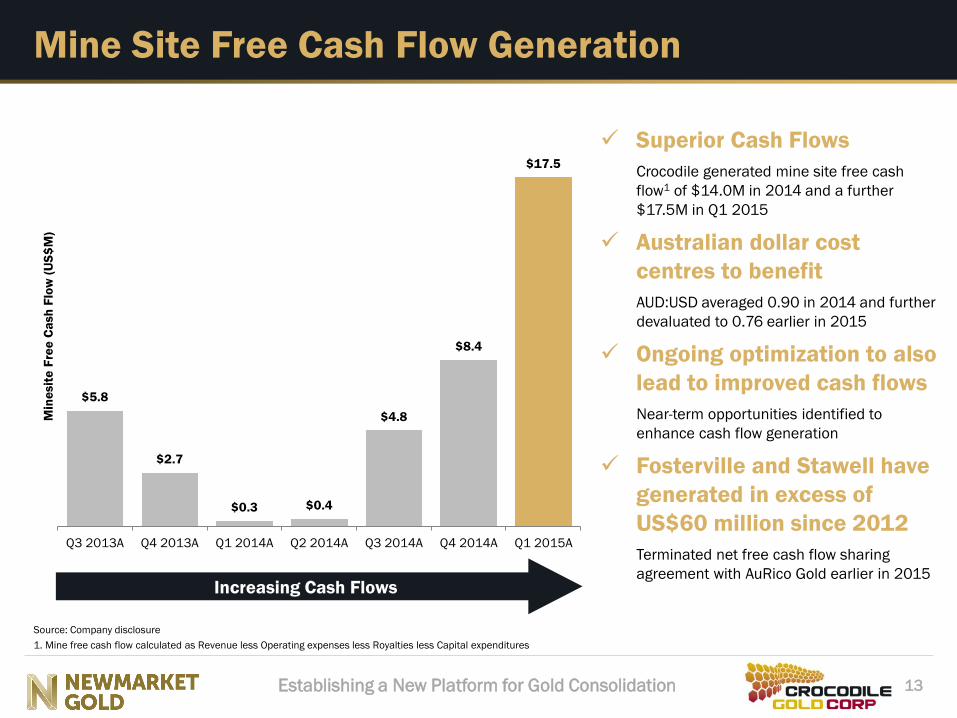

Mine Site Free Cash Flow Generation

Source: Company disclosure

1. Mine free cash flow calculated as Revenue less Operating expenses less Royalties less Capital expenditures

$5.8

$2.7

$0.3 $0.4

$4.8

$8.4

$17.5

Q3 2013A Q4 2013A Q1 2014A Q2 2014A Q3 2014A Q4 2014A Q1 2015A

Min

esit

e F

ree

Ca

sh

Flo

w (

US

$M

)

Superior Cash Flows

Crocodile generated mine site free cash

flow1 of $14.0M in 2014 and a further

$17.5M in Q1 2015

Australian dollar cost

centres to benefit

AUD:USD averaged 0.90 in 2014 and further

devaluated to 0.76 earlier in 2015

Ongoing optimization to also

lead to improved cash flows

Near-term opportunities identified to

enhance cash flow generation

Fosterville and Stawell have

generated in excess of

US$60 million since 2012

Terminated net free cash flow sharing

agreement with AuRico Gold earlier in 2015 Increasing Cash Flows

Establishing a New Platform for Gold Consolidation 14

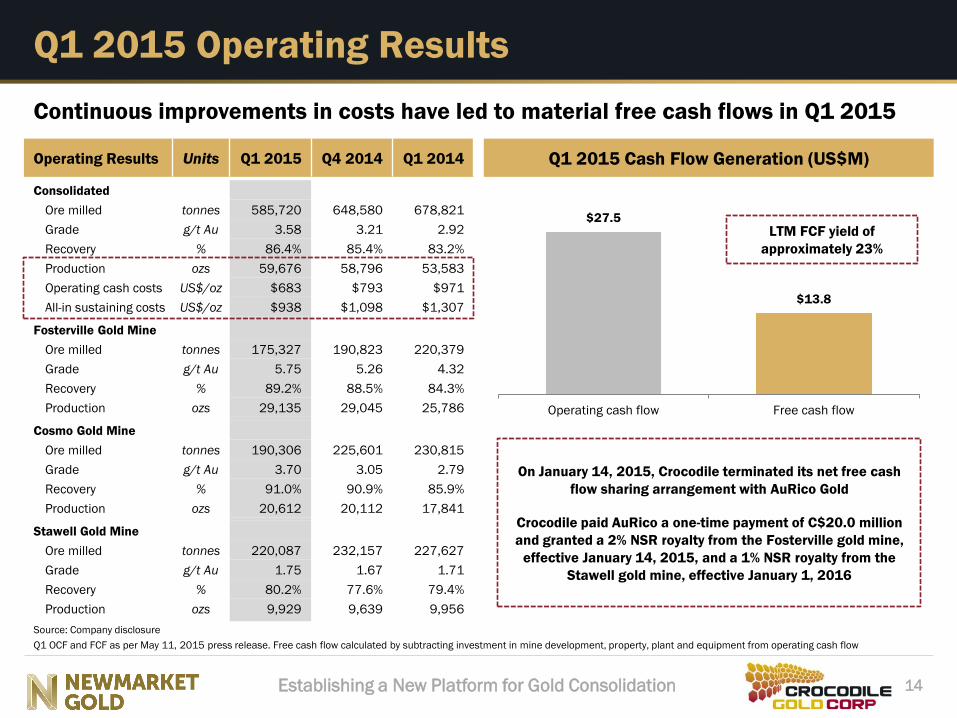

Q1 2015 Operating Results

Source: Company disclosure

Q1 OCF and FCF as per May 11, 2015 press release. Free cash flow calculated by subtracting investment in mine development, property, plant and equipment from operating cash flow

Continuous improvements in costs have led to material free cash flows in Q1 2015

Operating Results Units Q1 2015 Q4 2014 Q1 2014

Consolidated

Ore milled tonnes 585,720 648,580 678,821

Grade g/t Au 3.58 3.21 2.92

Recovery % 86.4% 85.4% 83.2%

Production ozs 59,676 58,796 53,583

Operating cash costs US$/oz $683 $793 $971

All-in sustaining costs US$/oz $938 $1,098 $1,307

Fosterville Gold Mine

Ore milled tonnes 175,327 190,823 220,379

Grade g/t Au 5.75 5.26 4.32

Recovery % 89.2% 88.5% 84.3%

Production ozs 29,135 29,045 25,786

Cosmo Gold Mine

Ore milled tonnes 190,306 225,601 230,815

Grade g/t Au 3.70 3.05 2.79

Recovery % 91.0% 90.9% 85.9%

Production ozs 20,612 20,112 17,841

Stawell Gold Mine

Ore milled tonnes 220,087 232,157 227,627

Grade g/t Au 1.75 1.67 1.71

Recovery % 80.2% 77.6% 79.4%

Production ozs 9,929 9,639 9,956

Q1 2015 Cash Flow Generation (US$M)

On January 14, 2015, Crocodile terminated its net free cash

flow sharing arrangement with AuRico Gold

Crocodile paid AuRico a one-time payment of C$20.0 million

and granted a 2% NSR royalty from the Fosterville gold mine,

effective January 14, 2015, and a 1% NSR royalty from the

Stawell gold mine, effective January 1, 2016

$27.5

$13.8

Operating cash flow Free cash flow

LTM FCF yield of

approximately 23%

Establishing a New Platform for Gold Consolidation

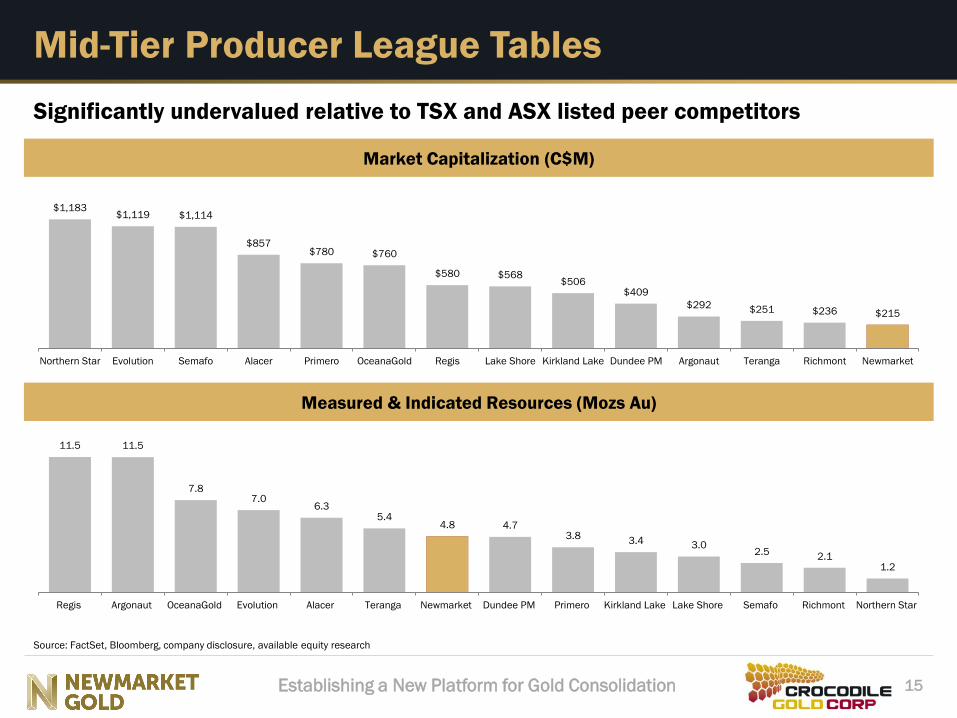

Market Capitalization (C$M)

15

Mid-Tier Producer League Tables

Source: FactSet, Bloomberg, company disclosure, available equity research

Significantly undervalued relative to TSX and ASX listed peer competitors

Measured & Indicated Resources (Mozs Au)

$1,183 $1,119 $1,114

$857 $780 $760

$580 $568 $506

$409

$292 $251 $236 $215

Northern Star Evolution Semafo Alacer Primero OceanaGold Regis Lake Shore Kirkland Lake Dundee PM Argonaut Teranga Richmont Newmarket

11.5 11.5

7.8 7.0

6.3 5.4

4.8 4.7 3.8

3.4 3.0 2.5

2.1 1.2

Regis Argonaut OceanaGold Evolution Alacer Teranga Newmarket Dundee PM Primero Kirkland Lake Lake Shore Semafo Richmont Northern Star

Establishing a New Platform for Gold Consolidation

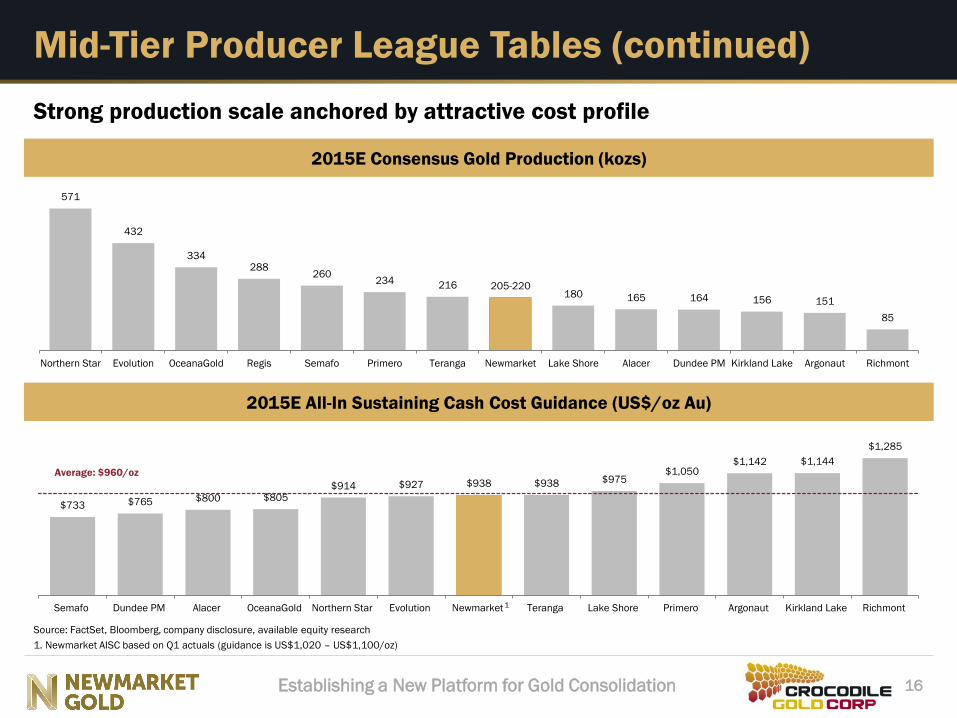

2015E Consensus Gold Production (kozs)

16

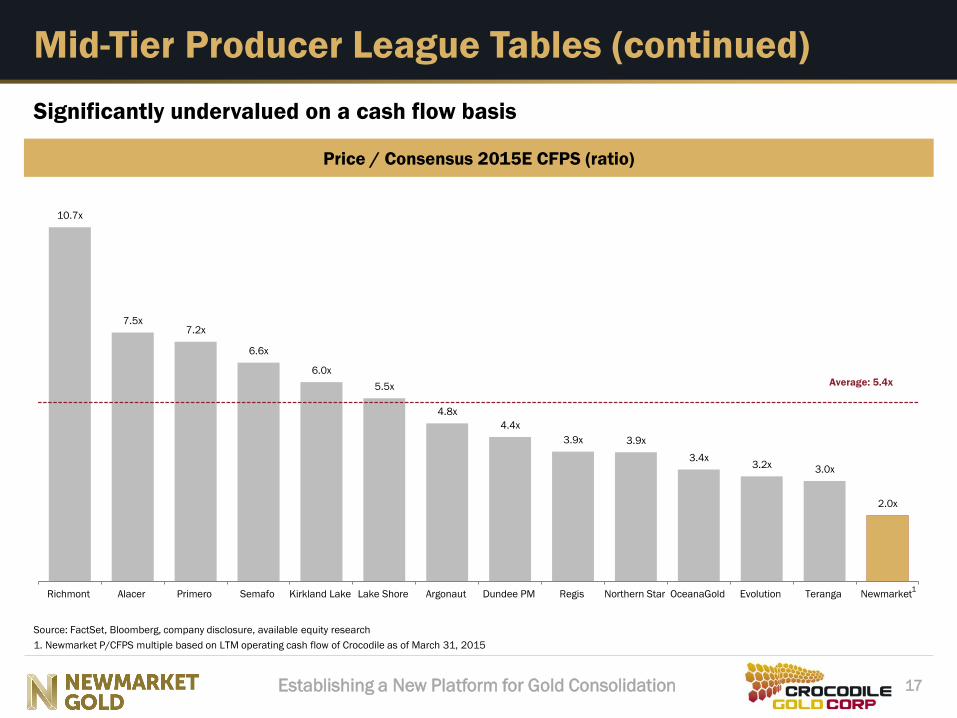

Mid-Tier Producer League Tables (continued)

Source: FactSet, Bloomberg, company disclosure, available equity research

1. Newmarket AISC based on Q1 actuals (guidance is US$1,020 – US$1,100/oz)

Strong production scale anchored by attractive cost profile

2015E All-In Sustaining Cash Cost Guidance (US$/oz Au)

571

432

334 288

260 234 216 205-220

180 165 164 156 151

85

Northern Star Evolution OceanaGold Regis Semafo Primero Teranga Newmarket Lake Shore Alacer Dundee PM Kirkland Lake Argonaut Richmont

$733 $765 $800 $805 $914 $927 $938 $938 $975

$1,050 $1,142 $1,144

$1,285

Semafo Dundee PM Alacer OceanaGold Northern Star Evolution Newmarket Teranga Lake Shore Primero Argonaut Kirkland Lake Richmont

Average: $960/oz

1

Establishing a New Platform for Gold Consolidation 17

Mid-Tier Producer League Tables (continued)

Source: FactSet, Bloomberg, company disclosure, available equity research

1. Newmarket P/CFPS multiple based on LTM operating cash flow of Crocodile as of March 31, 2015

Significantly undervalued on a cash flow basis

Price / Consensus 2015E CFPS (ratio)

10.7x

7.5x 7.2x

6.6x

6.0x

5.5x

4.8x

4.4x

3.9x 3.9x

3.4x 3.2x 3.0x

2.0x

Richmont Alacer Primero Semafo Kirkland Lake Lake Shore Argonaut Dundee PM Regis Northern Star OceanaGold Evolution Teranga Newmarket

Average: 5.4x

1

Establishing a New Platform for Gold Consolidation

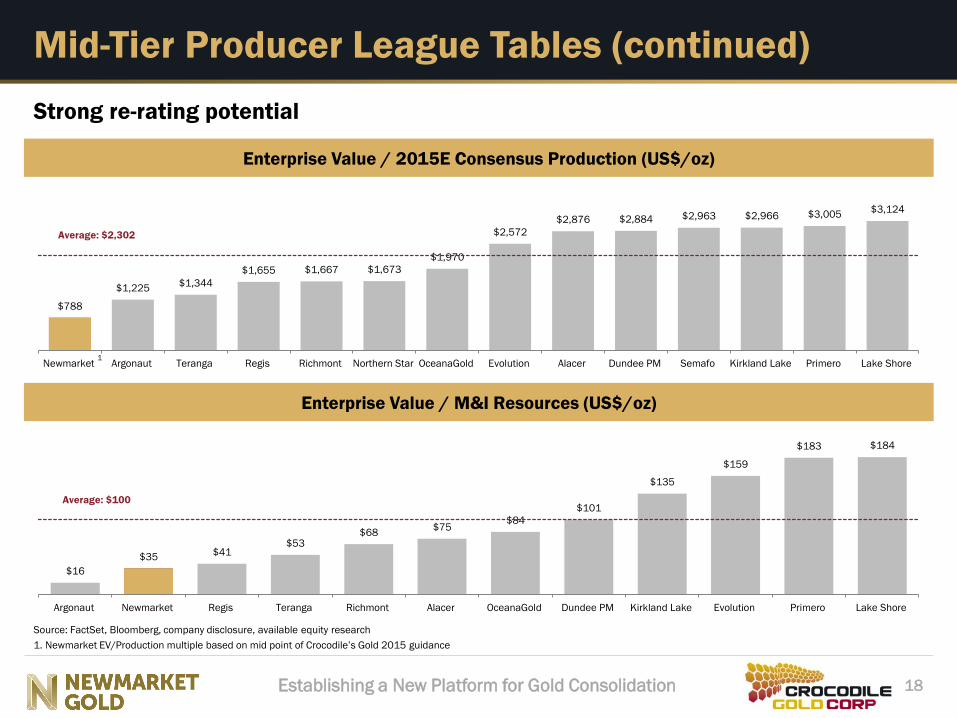

Enterprise Value / M&I Resources (US$/oz)

18

Mid-Tier Producer League Tables (continued)

Source: FactSet, Bloomberg, company disclosure, available equity research

1. Newmarket EV/Production multiple based on mid point of Crocodile’s Gold 2015 guidance

Strong re-rating potential

Enterprise Value / 2015E Consensus Production (US$/oz)

$788

$1,225 $1,344

$1,655 $1,667 $1,673

$1,970

$2,572

$2,876 $2,884 $2,963 $2,966 $3,005 $3,124

Newmarket Argonaut Teranga Regis Richmont Northern Star OceanaGold Evolution Alacer Dundee PM Semafo Kirkland Lake Primero Lake Shore

Average: $2,302

$16

$35 $41 $53

$68 $75

$84

$101

$135

$159

$183 $184

Argonaut Newmarket Regis Teranga Richmont Alacer OceanaGold Dundee PM Kirkland Lake Evolution Primero Lake Shore

Average: $100

1

Establishing a New Platform for Gold Consolidation 19

Targeted Growth Plans

Production

2015 production guidance of 205-220koz at AISC of

US$1,020 – US$1,100/oz

Increase pace of resource conversion

Exploit significant mineral inventory of 4.8Moz in M&I

resources to increase mine life

Operational

Enhancements

& Optimization

Increase underground productivity and mill recoveries to expand

current production levels

Continue ongoing cost optimization efforts

Exploration

Commence growth exploration program

Focus on resource potential at or near mine sites

Significant land package with over 4,000km2 of prospective landholdings

in known gold fields with brownfield development capability

Big Hill &

Maud Creek

Maintain permitting efforts at Big Hill (160koz in M&I gold resources; decision

expected in 2015 on revised mine plan)

Initiate Feasibility Study at Maud Creek Gold Project (871koz in M&I gold

resources)

Corporate/

Asset

Acquisitions

Stronger and more diversified platform with the critical scale and enhanced capital

markets presence to pursue further high quality acquisitions

Excellent access to capital increases ability to compete

Establishing a New Platform for Gold Consolidation

Strong platform to execute Newmarket Gold’s accretive growth consolidation

strategy

Portfolio of well-established producing mines with free cash flow and an

improving cost profile

Proven management team and Board with extensive experience in building and

operating mining companies focused on generating shareholder return

Compelling value proposition with attractive re-rate potential

Enhanced capital markets profile to improve access to capital, market liquidity

and broaden investor interest globally

Material ownership of management and board; aligned with shareholders in goal

of creating significant shareholder wealth

20

Winning Combination to Drive Shareholder Returns

Establishing a New Platform for Gold Consolidation

Douglas Forster President & CEO, Director T: 604-559-8040

May 11, 2015 TSX-V: NGN

TSX: CRK

“The People, The Commodity, The Time”

Contact Us

www.newmarketgoldinc.com

Rodney Lamond President & CEO, Director T: 416-847-1847

www.crocgold.com

Establishing a New Platform for Gold Consolidation

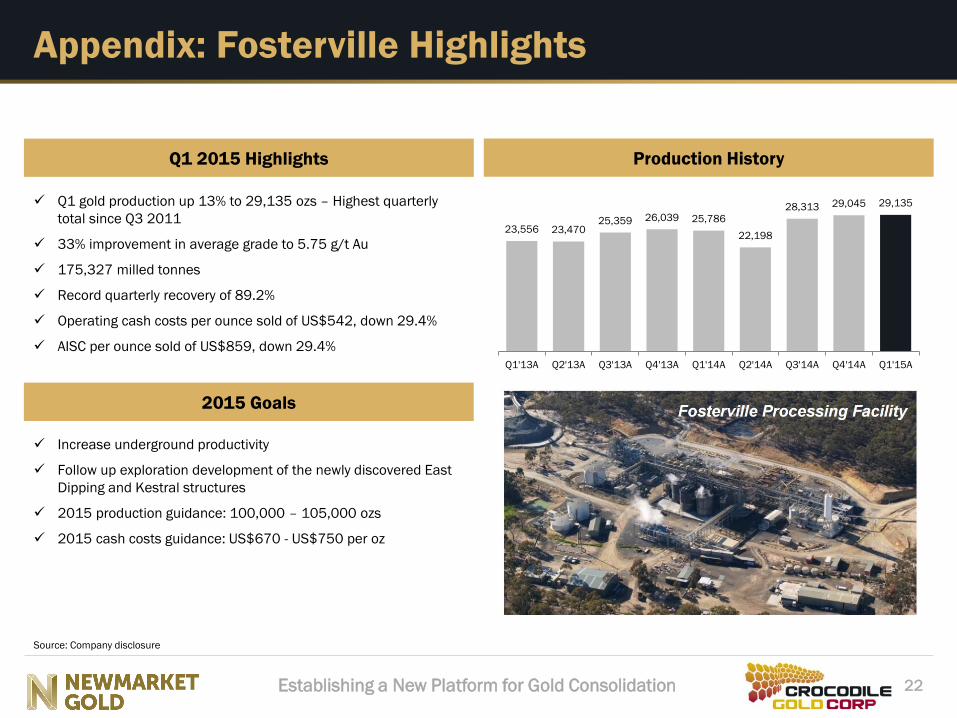

Q1 2015 Highlights

Q1 gold production up 13% to 29,135 ozs – Highest quarterly

total since Q3 2011

33% improvement in average grade to 5.75 g/t Au

175,327 milled tonnes

Record quarterly recovery of 89.2%

Operating cash costs per ounce sold of US$542, down 29.4%

AISC per ounce sold of US$859, down 29.4%

22

Appendix: Fosterville Highlights

Source: Company disclosure

Production History

2015 Goals

Increase underground productivity

Follow up exploration development of the newly discovered East

Dipping and Kestral structures

2015 production guidance: 100,000 – 105,000 ozs

2015 cash costs guidance: US$670 - US$750 per oz

23,556 23,470 25,359 26,039 25,786

22,198

28,313 29,045 29,135

Q1'13A Q2'13A Q3'13A Q4'13A Q1'14A Q2'14A Q3'14A Q4'14A Q1'15A

Establishing a New Platform for Gold Consolidation

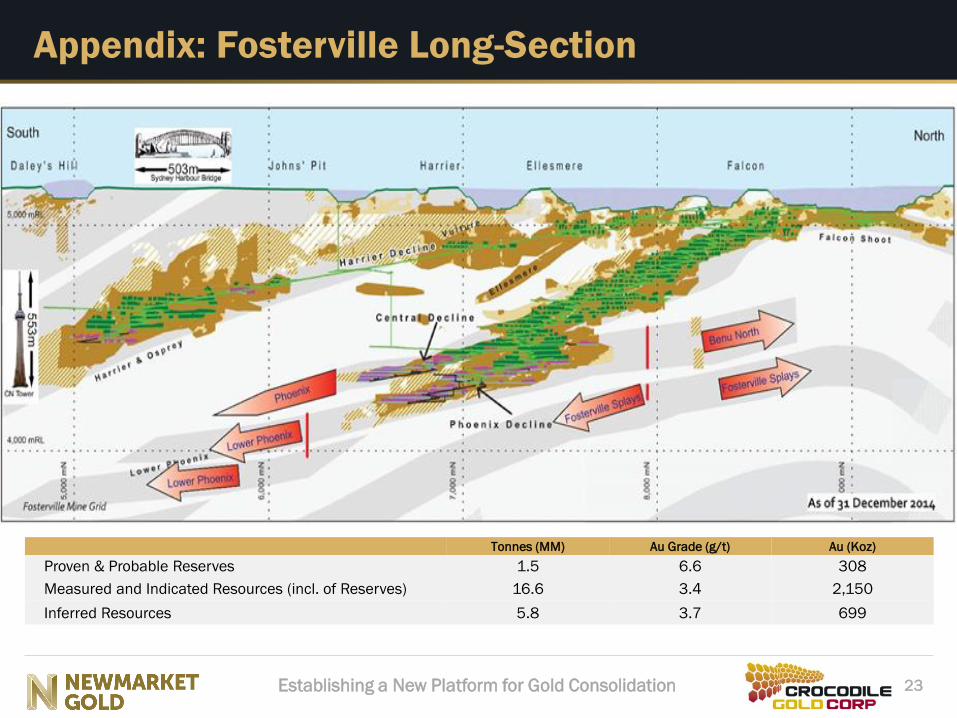

Appendix: Fosterville Long-Section

23

Tonnes (MM) Au Grade (g/t) Au (Koz)

Proven & Probable Reserves 1.5 6.6 308

Measured and Indicated Resources (incl. of Reserves) 16.6 3.4 2,150

Inferred Resources 5.8 3.7 699

Establishing a New Platform for Gold Consolidation

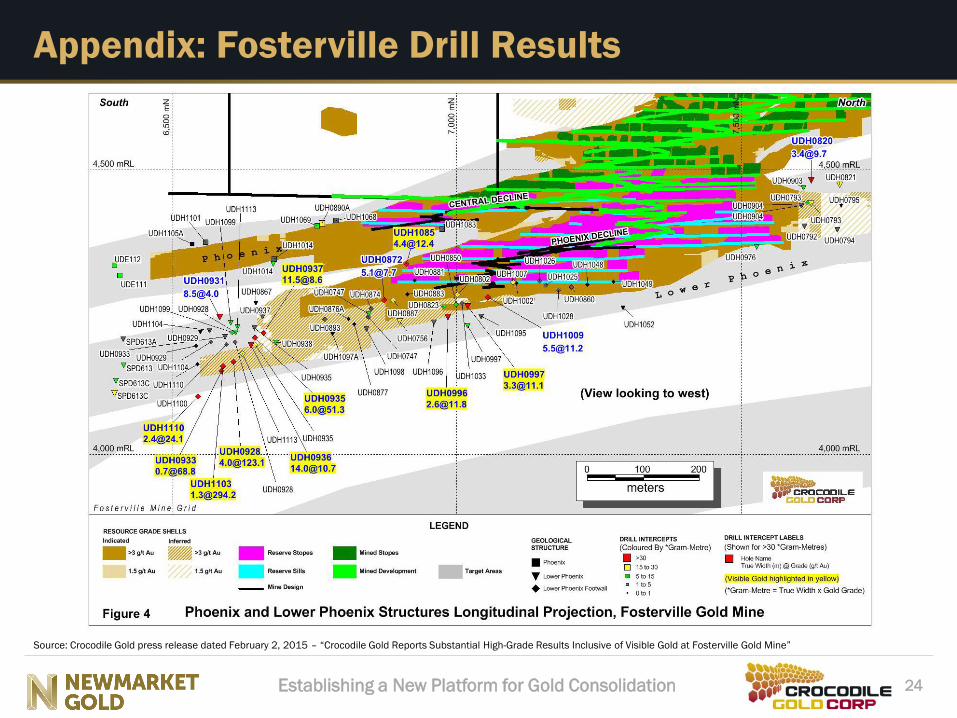

Appendix: Fosterville Drill Results

24

Source: Crocodile Gold press release dated February 2, 2015 – “Crocodile Gold Reports Substantial High-Grade Results Inclusive of Visible Gold at Fosterville Gold Mine”

Establishing a New Platform for Gold Consolidation 25

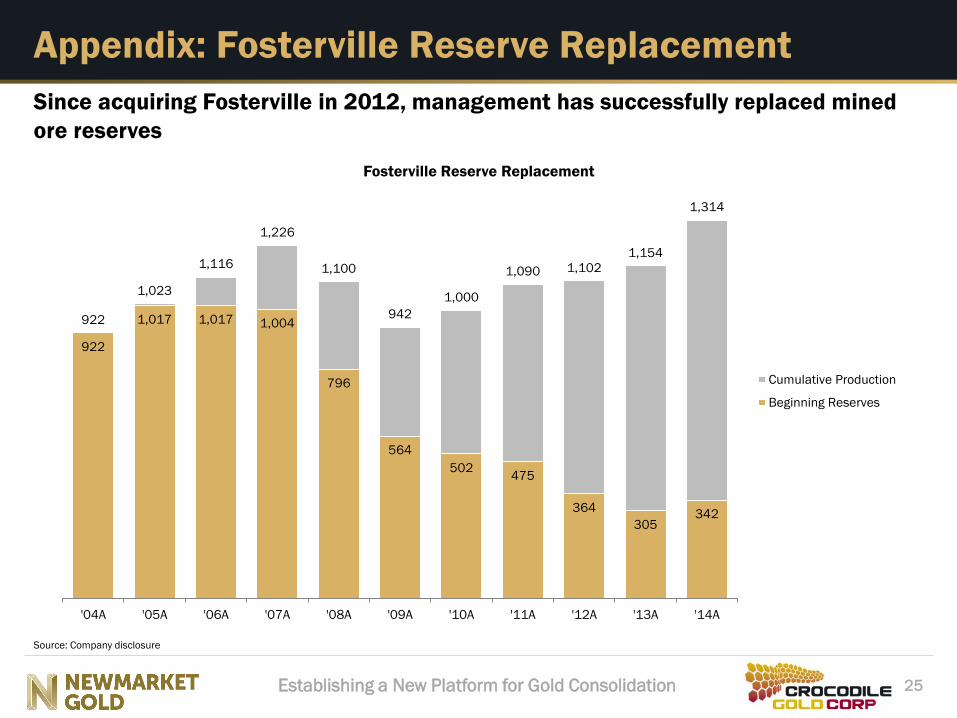

Appendix: Fosterville Reserve Replacement

Source: Company disclosure

Since acquiring Fosterville in 2012, management has successfully replaced mined

ore reserves

922

1,017 1,017 1,004

796

564

502 475

364

305 342

922

1,023

1,116

1,226

1,100

942

1,000

1,090 1,102

1,154

1,314

'04A '05A '06A '07A '08A '09A '10A '11A '12A '13A '14A

Fosterville Reserve Replacement

Cumulative Production

Beginning Reserves

Establishing a New Platform for Gold Consolidation

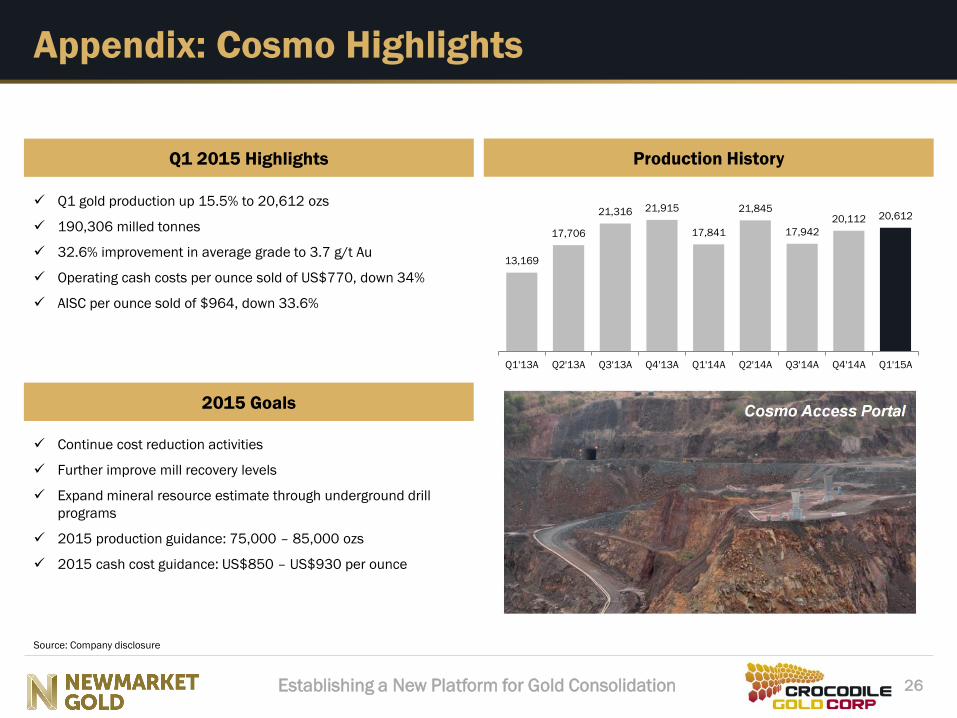

Q1 2015 Highlights

Q1 gold production up 15.5% to 20,612 ozs

190,306 milled tonnes

32.6% improvement in average grade to 3.7 g/t Au

Operating cash costs per ounce sold of US$770, down 34%

AISC per ounce sold of $964, down 33.6%

26

Appendix: Cosmo Highlights

Source: Company disclosure

Production History

2015 Goals

Continue cost reduction activities

Further improve mill recovery levels

Expand mineral resource estimate through underground drill

programs

2015 production guidance: 75,000 – 85,000 ozs

2015 cash cost guidance: US$850 – US$930 per ounce

13,169

17,706

21,316 21,915

17,841

21,845

17,942

20,112 20,612

Q1'13A Q2'13A Q3'13A Q4'13A Q1'14A Q2'14A Q3'14A Q4'14A Q1'15A

Establishing a New Platform for Gold Consolidation

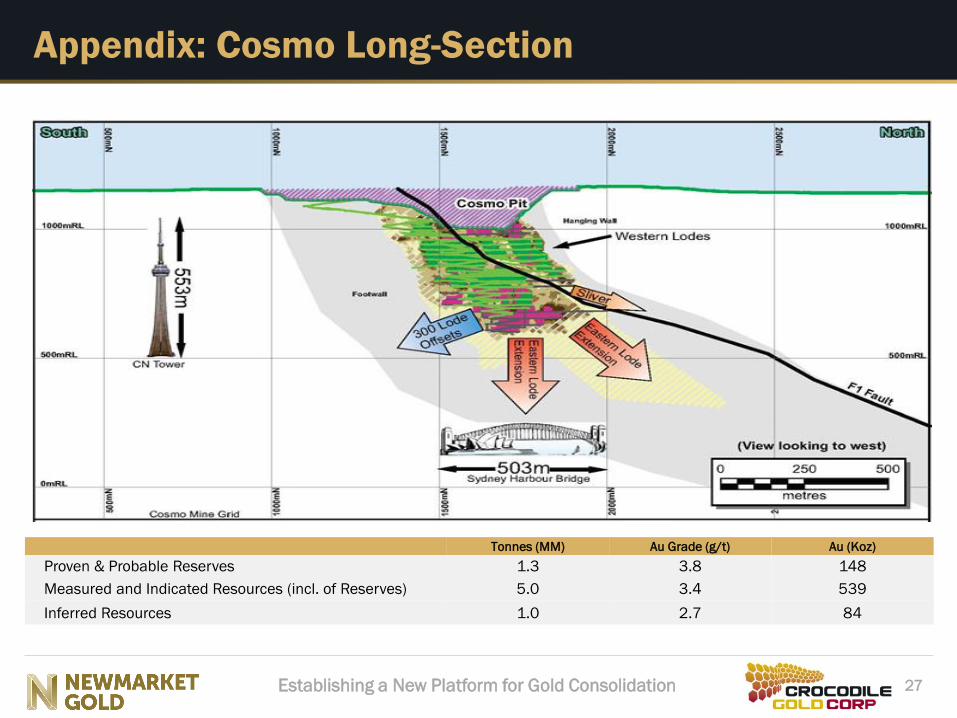

Appendix: Cosmo Long-Section

27

Tonnes (MM) Au Grade (g/t) Au (Koz)

Proven & Probable Reserves 1.3 3.8 148

Measured and Indicated Resources (incl. of Reserves) 5.0 3.4 539

Inferred Resources 1.0 2.7 84

Establishing a New Platform for Gold Consolidation

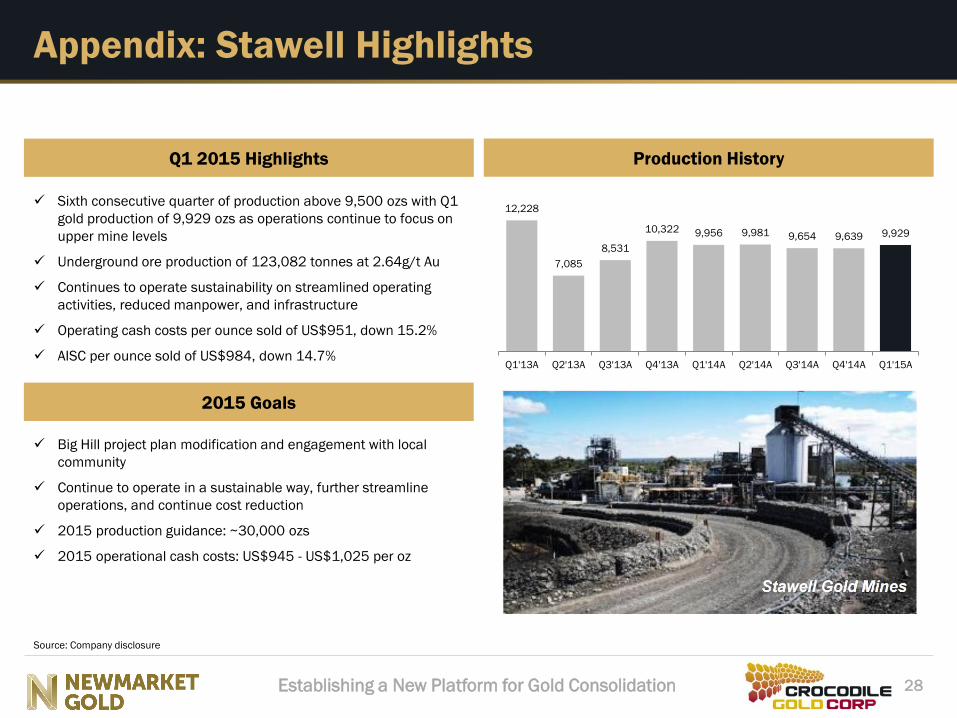

Q1 2015 Highlights

Sixth consecutive quarter of production above 9,500 ozs with Q1

gold production of 9,929 ozs as operations continue to focus on

upper mine levels

Underground ore production of 123,082 tonnes at 2.64g/t Au

Continues to operate sustainability on streamlined operating

activities, reduced manpower, and infrastructure

Operating cash costs per ounce sold of US$951, down 15.2%

AISC per ounce sold of US$984, down 14.7%

28

Appendix: Stawell Highlights

Source: Company disclosure

Production History

2015 Goals

Big Hill project plan modification and engagement with local

community

Continue to operate in a sustainable way, further streamline

operations, and continue cost reduction

2015 production guidance: ~30,000 ozs

2015 operational cash costs: US$945 - US$1,025 per oz

12,228

7,085

8,531

10,322 9,956 9,981 9,654 9,639 9,929

Q1'13A Q2'13A Q3'13A Q4'13A Q1'14A Q2'14A Q3'14A Q4'14A Q1'15A

Establishing a New Platform for Gold Consolidation

Appendix: Stawell Long-Section

29

Tonnes (MM) Au Grade (g/t) Au (Koz)

Proven & Probable Reserves 3.9 3.4 181

Measured and Indicated Resources (incl. of Reserves) 4.1 1.8 243

Inferred Resources 0.8 3.1 77

End of May 2015

Current Mine Plan C4350 level commence access Apr / May

End of May at Ore C4440 DD Extent

728L

Development

(460m)

343L Development

(250m)

180L Development

(500m)

Establishing a New Platform for Gold Consolidation

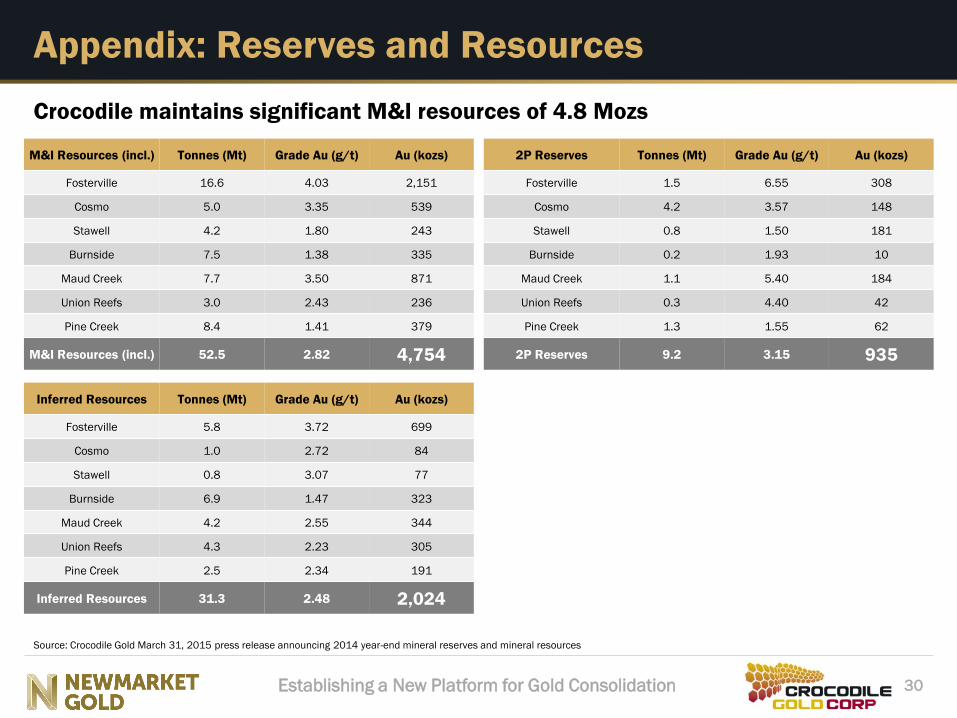

Appendix: Reserves and Resources

30

Inferred Resources Tonnes (Mt) Grade Au (g/t) Au (kozs)

Fosterville 5.8 3.72 699

Cosmo 1.0 2.72 84

Stawell 0.8 3.07 77

Burnside 6.9 1.47 323

Maud Creek 4.2 2.55 344

Union Reefs 4.3 2.23 305

Pine Creek 2.5 2.34 191

Inferred Resources 31.3 2.48 2,024

M&I Resources (incl.) Tonnes (Mt) Grade Au (g/t) Au (kozs)

Fosterville 16.6 4.03 2,151

Cosmo 5.0 3.35 539

Stawell 4.2 1.80 243

Burnside 7.5 1.38 335

Maud Creek 7.7 3.50 871

Union Reefs 3.0 2.43 236

Pine Creek 8.4 1.41 379

M&I Resources (incl.) 52.5 2.82 4,754

Source: Crocodile Gold March 31, 2015 press release announcing 2014 year-end mineral reserves and mineral resources

2P Reserves Tonnes (Mt) Grade Au (g/t) Au (kozs)

Fosterville 1.5 6.55 308

Cosmo 4.2 3.57 148

Stawell 0.8 1.50 181

Burnside 0.2 1.93 10

Maud Creek 1.1 5.40 184

Union Reefs 0.3 4.40 42

Pine Creek 1.3 1.55 62

2P Reserves 9.2 3.15 935

Crocodile maintains significant M&I resources of 4.8 Mozs

Establishing a New Platform for Gold Consolidation

This investor presentation is considered to be an “offering memorandum” for the purposes of Canadian securities laws. Securities legislation in the provinces of Canada in which the offering is being made provides

purchasers, in addition to any other rights they may have at law, with a remedy for rescission or damages, or both, where the offering memorandum (the “Offering Memorandum”), or any amendment to the Offering

Memorandum, contains a misrepresentation. A “misrepresentation” is generally defined under applicable securities laws as an untrue statement of a material fact, or an omission to state a material fact that is

required to be stated or that is necessary to make any statement not misleading in light of the circumstances in which it was made. These remedies, or notice with respect thereto, must be exercised or delivered, as

the case may be, by the purchaser within the time limit prescribed, and are subject to the defences contained, in the applicable securities legislation. Purchasers should refer to the provisions of the applicable

securities legislation for the particulars of these rights or consult with a legal advisor. The following is a summary of the rights of rescission or rights to damages available to purchasers.

Ontario

Ontario Securities Commission Rule 45-501 — Ontario Prospectus and Registration Exemptions provides that when an offering memorandum, such as this Offering Memorandum, is delivered to an purchaser to

whom securities are distributed in reliance upon the “accredited investor” prospectus exemption in Section 73.3 of the Securities Act (Ontario) (the “Ontario Act”), the right of action referred to in Section 130.1

(“Section 130.1”) of the Ontario Act is applicable, unless the prospective purchaser is:

i. an association governed by the Cooperative Credit Associations Act (Canada) or a central cooperative credit society for which an order has been made under section 473(1) of that Act;

ii. a bank, loan corporation, trust company, trust corporation, insurance company, treasury branch, credit union, caisse populaire, financial services corporation, or league that, in each case, is

authorized by an enactment of Canada or a jurisdiction of Canada to carry on business in Canada or a jurisdiction in Canada;

i. a Schedule III bank, meaning an authorized foreign bank named in Schedule III of the Bank Act (Canada);

i. the Business Development Bank of Canada incorporated under the Business Development Bank of Canada Act (Canada); or

i. a subsidiary of any person referred to in paragraphs (a) through (d), if the person owns all of the voting securities of the subsidiary, except the voting securities required by law to be owned by the

directors of the subsidiary.

The right of action referred to in Section 130.1 is also applicable to a purchaser to whom securities are distributed in reliance upon the “minimum amount investment” prospectus exemption in Section 2.10

National Instrument 45-106 Prospectus Exemptions (“NI 45-106”).

Section 130.1 provides such purchasers who purchase securities offered by an offering memorandum with a statutory right of action against the issuer of securities for rescission or damages in the event that the

offering memorandum and any amendment to it contains a “misrepresentation”. In Ontario, the term “misrepresentation” means an untrue statement of a material fact or an omission to state a material fact that is

required to be stated or that is necessary to make any statement not misleading or false in the light of the circumstances in which it was made. These remedies, or notice with respect to these remedies, must be

exercised or delivered, as the case may be, by the purchaser within the time limits prescribed by applicable securities laws.

Where this Offering Memorandum is delivered to a prospective purchaser of securities in connection with a trade made in reliance on either Section 73.3 of the Ontario Act or Section 2.10 of NI 45-106, and this

Offering Memorandum contains a misrepresentation, the purchaser will have, without regard to whether the purchaser relied on the misrepresentation, a statutory right of action against the Company for damages

or, while still the owner of the securities, for rescission, in which case, if the purchaser elects to exercise the right of rescission, the purchaser will have no right of action for damages, provided that the right of action

for rescission will be exercisable by the purchaser only if the purchaser gives notice to the Company, not more than 180 days after the date of the transaction that gave rise to the cause of action, that the purchaser

is exercising such right; or, in the case of any action other than an action for rescission, the earlier of: (i) 180 days after the plaintiff first had knowledge of the facts giving rise to the cause of action, or (ii) three years

after the date of the transaction that gave rise to the cause of action.

The Company will not be liable for a misrepresentation if it proves that the purchaser purchased securities with knowledge of a misrepresentation. In an action for damages, the Company will not be liable for all or

any portion of the damages that the Company proves do not represent the depreciation in value of securities as a result of a misrepresentation relied upon. In no case will the amount recoverable for a

misrepresentation exceed the price at which the securities were offered. The foregoing statutory right of action for rescission or damages conferred is in addition to and without derogation from any other right the

purchaser may have at law. This summary is subject to the express provisions of the Ontario Act and the regulations and rules made under it, and prospective purchasers should refer to the complete text of those

provisions.

31

Legal Matters

Establishing a New Platform for Gold Consolidation 32

Legal Matters Saskatchewan

Section 138 of The Securities Act, 1988 (Saskatchewan), as amended (the “Saskatchewan Act”) provides that where an offering memorandum, such as this Offering Memorandum, or any amendment to it is sent or delivered to a purchaser and it contains a misrepresentation (as defined in the Saskatchewan Act), a purchaser who purchases a security covered by the offering memorandum or any amendment to it has, without regard to whether the purchaser relied on the misrepresentation, a right of action for rescission against the issuer or a selling security holder on whose behalf the distribution is made or has a right of action for damages against:

(a)the issuer or a selling security holder on whose behalf the distribution is made;

(b)every promoter and director of the issuer or the selling security holder, as the case may be, at the time the offering memorandum or any amendment to it was sent or delivered;

(c)every person or company whose consent has been filed respecting the offering, but only with respect to reports, opinions or statements that have been made by them;

(d)every person who or company that, in addition to the persons or companies mentioned in (a) to (c) above, signed the offering memorandum or the amendment to the offering memorandum; and

(e)every person who or company that sells securities on behalf of the issuer or selling security holder under the offering memorandum or amendment to the offering memorandum.

Such rights of rescission and damages are subject to certain limitations including the following:

(a)if the purchaser elects to exercise its right of rescission against the issuer or selling security holder, it will have no right of action for damages against that party;

(b)in an action for damages, a defendant will not be liable for all or any portion of the damages that he, she or it proves do not represent the depreciation in value of the securities resulting from the

misrepresentation relied on;

(c)no person or company, other than the issuer or a selling security holder, will be liable for any part of the offering memorandum or any amendment to it not purporting to be made on the authority of an

expert and not purporting to be a copy of, or an extract from, a report, opinion or statement of an expert, unless the person or company failed to conduct a reasonable investigation sufficient to provide

reasonable grounds for a belief that there had been no misrepresentation or believed that there had been a misrepresentation;

(d)in no case will the amount recoverable exceed the price at which the securities were offered; and

(e)no person or company is liable in an action for rescission or damages if that person or company proves that the purchaser purchased the securities with knowledge of the misrepresentation.

In addition, no person or company, other than the issuer or selling security holder, will be liable if the person or company proves that:

(a)the offering memorandum or any amendment to it was sent or delivered without the person’s or company’s knowledge or consent and that, on becoming aware of it being sent or delivered, that person or

company immediately gave reasonable general notice that it was so sent or delivered; or

(b)after the filing of the offering memorandum or the amendment to the offering memorandum and before the purchase of the securities by the purchaser, on becoming aware of any misrepresentation in the

offering memorandum or the amendment to the offering memorandum, the person or company withdrew the person’s or company’ s consent to it and gave reasonable general notice of the person’s or

company’s withdrawal and the reason for it;

(c)with respect to any part of the offering memorandum or any amendment to it purporting to be made on the authority of an expert, or purporting to be a copy of, or an extract from, a report, an opinion or a

statement of an expert, that person or company had no reasonable grounds to believe and did not believe that there had been a misrepresentation, the part of the offering memorandum or any amendment

to it did not fairly represent the report, opinion or statement of the expert, or was not a fair copy of, or an extract from, the report, opinion or statement of the expert.

Not all defences upon which the Company or others may rely are described herein. Please refer to the full text of the Saskatchewan Act for a complete listing.

Similar rights of action for damages and rescission are provided in section 138.1 of the Saskatchewan Act in respect of a misrepresentation in advertising and sales literature disseminated in connection with an

offering of securities.

Section 138.2 of the Saskatchewan Act also provides that where an individual makes a verbal statement to a prospective purchaser that contains a misrepresentation relating to the security purchased and the verbal

statement is made either before or contemporaneously with the purchase of the security, the purchaser has, without regard to whether the purchaser relied on the misrepresentation, a right of action for damages

against the individual who made the verbal statement.

Section 141(1) of the Saskatchewan Act provides a purchaser with the right to void the purchase agreement and to recover all money and other consideration paid by the purchaser for the securities if the securities

are purchased from a vendor who is trading in Saskatchewan in contravention of the Saskatchewan Act, the regulations to the Saskatchewan Act or a decision of the Saskatchewan Financial Services Commission.

Establishing a New Platform for Gold Consolidation 33

Legal Matters

Section 141(2) of the Saskatchewan Act also provides a right of action for rescission or damages to a purchaser of securities to whom an offering memorandum or any amendment to it was

not sent or delivered prior to or at the same time as the purchaser enters into an agreement to purchase the securities, as r equired by Section 80.1 of the Saskatchewan Act. The rights of

action for damages or rescission under the Saskatchewan Act are in addition to and do not derogate from any other right which a purchaser may have at law. Section 147 of the Saskatchewan

Act provides that no action will be commenced to enforce any of the foregoing rights more than:

(a)in the case of an action for rescission, 180 days after the date of the transaction that gave rise to the cause of action; or

(b)in the case of any other action, other than an action for rescission, the earlier of:

(i)one year after the plaintiff first had knowledge of the facts giving rise to the cause of action; or

(ii)six years after the date of the transaction that gave rise to the cause of action.

The Saskatchewan Act also provides a purchaser who has received an amended offering memorandum delivered in accordance with s ubsection 80.1(3) of the Saskatchewan Act has a right to

withdraw from the agreement to purchase the securities by delivering a notice to the person who or company that is selling th e securities, indicating the purchaser’s intention not to be bound

by the purchase agreement, provided such notice is delivered by the purchaser within two business days of receiving the amend ed offering memorandum. This summary is subject to the

express provisions of the Saskatchewan Act and the regulations and rules made under it, and prospective purchasers should ref er to the complete text of those provisions.

Manitoba

Pursuant to section 141.1(1) of The Securities Act (Manitoba) (the “Manitoba Act”), where an offering memorandum, such as thi s Offering Memorandum, or any amendment to an offering

memorandum, is sent or delivered to a purchaser in the Province of Manitoba and such document contains a misrepresentation, a purchaser to whom the offering memorandum has been

delivered and who purchases securities in the offering contemplated by this document or any amendment to this document is dee med to have relied on that misrepresentation, if it was a

misrepresentation at the time of purchase and, subject to the defences described in the Manitoba Act, has:

(a) a right of action for damages against:

(i)the Company;

(ii)every director of the Company at the date of this document or any amendment to this document; and

(iii)every person or company who signed this document or any amendment to this document; and

(b) a right of rescission against the Company;

provided that:

(a)no person or company is liable if the person or company proves that the purchaser purchased securities with knowledge of the misrepresentation;

(b)in an action for damages, the defendant is not liable for all or any part of the damages that he, she or it proves do not rep resent the depreciation in value of securities resulting from

the misrepresentation relied on; and

(c)in no case will the amount recovered exceed the price at which securities were offered under this document or any amendment t o this document.

Where a purchaser elects to exercise a right of rescission against the Company, the purchaser will have no right of action fo r damages against the Company or against a person or company

referred to in (a)(ii) or (iii) above. No person or company is liable:

(a)if the person or company proves that this document or any amendment to this document was sent without the person’s or company ’s knowledge or consent and that, after becoming

aware of its being sent, the person or company promptly gave reasonable notice to the Company that it was sent without the pe rson’s or company’s knowledge and consent;

(b)if the person or company proves that, after becoming aware of any misrepresentation in this document or any amendment to this document, the person or company withdrew the person’s or company’s

consent to it and gave reasonable notice to the Company of the person’s or company’s withdrawal and the reason for it;

(c)if the person or company proves that with respect to any part of this document or of any amendment to this document purportin g to be made on the authority of an expert or

purporting to be a copy of, or an extract from, a report, opinion or statement of an expert, the person or company had no rea sonable grounds to believe and did not believe that:

(i)there had been a misrepresentation; or

(ii)the relevant part of this document or of the amendment to this document:

(i)did not fairly represent the report, opinion or statement of the expert; or

(ii)was not a fair copy of, or extract from, the report, opinion or statement of the expert; or

Establishing a New Platform for Gold Consolidation 34

Legal Matters

(d) with respect to any part of this document or of any amendment to this document not purporting to be made on an expert’s autho rity and not purporting to be a copy of, or an extract from, the

expert’s report, opinion or statement, unless the person or company:

(i) did not conduct an investigation, sufficient to provide reasonable grounds for a belief that there had been no misrepresentation; or

(ii) believed that there had been a misrepresentation.

If a misrepresentation is contained in a record incorporated by reference in, or that is deemed incorporated into, this docum ent or any amendment to this document, the misrepresentation is deemed to be

contained in this document or any amendment to this document.

Pursuant to section 141.4 of the Manitoba Act, but subject to the other provisions thereof, no action shall be commenced to e nforce any of the foregoing rights more than:

(a) in the case of an action for rescission, 180 days from the date of the transaction that gave rise to the cause of action, or

(b) in the case of an action for damages, the earlier of:

(i) 180 days after the date that the plaintiff first had knowledge of the facts giving rise to the cause of action, or

(ii) two years after the date of the transaction that gave rise to the cause of action.

The rights of action for rescission or damages under the Manitoba Act are in addition to and do not derogate from any other r ight that the purchaser may have at law. This summary is subject to the

express provisions of the Manitoba Act and the regulations and rules made under it, and prospective purchasers should refer t o the complete text of those provisions.

Nova Scotia

The right of action for rescission or damages described herein is conferred by section 138 of the Securities Act (Nova Scotia) (the “Nova Scotia Act”). Section 138 provides, in the relevant part, that in the

event that an offering memorandum, such as this Offering Memorandum, together with any amendments hereto, or any advertising or sales literature (as defined in the Nova Scotia Act) contains an untrue

statement of material fact or omits to state a material fact that is required to be stated or that is necessary in order to m ake any statements contained herein or therein not misleading in light of the

circumstances in which it was made (in Nova Scotia, a “misrepresentation”), a purchaser of securities is deemed to have relied upon such misrepresentation if it was a misrepresentation at the time of

purchase and has, subject to certain limitations and defences, a statutory right of action for damages against the seller of such securities, the directors of the seller at the date of t he offering

memorandum and the persons who have signed the offering memorandum or, alternatively, while still the owner of such securitie s, may elect instead to exercise a statutory right of rescission against the

seller, in which case the purchaser will have no right of action for damages against the seller, the directors of the seller at the date of the offering memorandum or the persons who have signed the

offering memorandum, provided that, among other limitations:

(a) no action will be commenced to enforce the right of action for rescission or damages by a purchaser resident in Nova Scotia l ater than 120 days after the date payment was made for the securities

(or after the date on which initial payment was made for the securities where payments subsequent to the initial payment are made pursuant to a contractual commitment assumed prior to, or

concurrently with, the initial payment);

(b) no person will be liable if it proves that the purchaser purchased the securities with knowledge of the misrepresentation;

(c) in the case of an action for damages, no person will be liable for all or any portion of the damages that it proves do not re present the depreciation in value of the securities; and

(d) in no case will the amount recoverable in any action exceed the price at which the securities were offered to the purchaser.

In addition, no person or company (other than the issuer if it is the seller) will be liable if such person or company proves that:

(a) the offering memorandum or the amendment to the offering memorandum was sent or delivered to the purchaser without the person ’ s or company’ s knowledge or consent and that, on becoming

aware of its delivery, the person or company gave reasonable general notice that it was delivered without the person’ s or co mpany’ s knowledge or consent;

(b) after delivery of the offering memorandum or the amendment to the offering memorandum and before the purchase of the securiti es by the purchaser, on becoming aware of any misrepresentation

in the offering memorandum, or amendment to the offering memorandum, the person or company withdrew the person’ s or company’ s consent to the offering memorandum, or amendment to the

offering memorandum, and gave reasonable general notice of the withdrawal and the reason for it; or

(c) with respect to any part of the offering memorandum or amendment to the offering memorandum purporting

Establishing a New Platform for Gold Consolidation 35

Legal Matters

(i) to be made on the authority of an expert, or

(ii) to be a copy of, or an extract from, a report, an opinion or a statement of an expert, the person or company had no reasonable grounds to believe and did not believe that

(i) there had been a misrepresentation, or

(ii) the relevant part of the offering memorandum or amendment to the offering memorandum did not fairly represent the report, opinion or statement of the expert, or was not a fair copy of, or an

extract from, the report, opinion or statement of the expert.

Furthermore, no person or company (other than the issuer if it is the seller) will be liable under section 138 of the Securities Act (Nova Scotia) with respect to any part of the offering memorandum or amendment to

the offering memorandum not purporting

(i) to be made on the authority of an expert; or

(ii) to be a copy of, or an extract from, a report, opinion or statement of an expert, unless the person or company

(i) failed to conduct a reasonable investigation to provide reasonable grounds for a belief that there had been no misrepresentation; or

(ii) believed that there had been a misrepresentation.

If a misrepresentation is contained in a record incorporated by reference in, or deemed incorporated into, the offering memorandum or amendment to the offering memorandum, the misrepresentation is deemed to

be contained in the offering memorandum or amendment to the offering memorandum. The liability of all persons or companies referred to above is joint and several with respect to the same cause of action. A

defendant who is found liable to pay a sum in damages may recover a contribution, in whole or in part, from a person or company who is jointly and severally liable to make the same payment in the same cause of

action unless, in all the circumstances of the case, the court is satisfied that it would not be just and equitable. This summary is subject to the express provisions of the Nova Scotia Act and the regulations and rules

made under it, and prospective purchasers should refer to the complete text of those provisions. New Brunswick

New Brunswick Securities Commission Rule 45-802 provides that the statutory rights of action in rescission or damages referred to in Section 150 (“Section 150”) of the Securities Act (New Brunswick) (the “New

Brunswick Act”) apply to information relating to an offering memorandum, such as this Offering Memorandum, that is provided to a purchaser of securities in connection with a distribution made in reliance on either

the “accredited investor” prospectus exemption in Section 2.3 of NI 45-106 or the “minimum amount investment” exemption in Section 2.10 of NI 45-106. Section 150 provides purchasers who purchase securities

offered for sale in reliance on an exemption from the prospectus requirements of the New Brunswick Act with a statutory right of action against the issuer of securities for rescission or damages in the event that an

offering memorandum provided to the purchaser contains a “misrepresentation”. In New Brunswick, “misrepresentation” means an untrue statement of a material fact or an omission to state a material fact that is

required to be stated or that is necessary to make a statement not misleading in the light of the circumstances in which it was made.

Where this document is delivered to a prospective purchaser of securities in connection with a trade made in reliance on either Section 2.3 of NI 45-106 or Section 2.10 of NI 45-106, and this document contains a

misrepresentation, a purchaser who purchases securities will be deemed to have relied on the misrepresentation and will have, subject to certain limitations and defences, a statutory right of action against the

Company for damages or, while still the owner of securities, for rescission, in which case, if the purchaser elects to exercise the right of rescission, the purchaser will have no right of action for damages, provided that

the right of action for rescission will be exercisable by the purchaser only if the purchaser commences an action against the defendant, not more than 180 days after the date of the transaction that gave rise to the

cause of action, or, in the case of any action other than an action for rescission, the earlier of: (i) one year after the plaintiff first had knowledge of the facts giving rise to the cause of action, or (ii) six years after the

date of the transaction that gave rise to the cause of action.

The Company shall not be liable where it is not receiving any proceeds from the distribution of the securities being distributed and the misrepresentation was not based on information provided by the Company unless

the misrepresentation (i) was based on information that was previously publicly disclosed by the Company, (ii) was a misrepresentation at the time of its previous public disclosure, and (iii) was not subsequently

publicly corrected or superseded by the Company before the completion of the distribution of the securities being distributed.

In addition, if advertising or sales literature is relied upon by a purchaser in connection with a purchase of securities of the Company and such advertising or sales literature contains a misrepresentation, the

purchaser shall also have a right of action for damages or rescission against every promoter or director of the Company at the time the advertising or sales literature was disseminated.

In addition, where an individual makes a verbal statement to a prospective purchaser that contains a misrepresentation relating to the securities of the Company and the verbal statement is made either before or

contemporaneously with the purchase of the securities of the Company, the purchaser shall be deemed to have relied upon the misrepresentation if it was a misrepresentation at the time of purchase, and has a right

of action for damages against the individual who made the verbal statement. No such individual will be liable if:

Establishing a New Platform for Gold Consolidation 36

Legal Matters

(a) that individual can establish that he or she cannot reasonably be expected to have known that his or her statement contained a misrepresentation; or

(b) prior to the purchase of the securities by the purchaser, that individual notified the purchaser that the individual’s statem ent contained a misrepresentation.

Neither the Company nor any other person referred to above will be liable, whether for misrepresentations in this Offering Me morandum, any advertising or sales literature or in a verbal

statement:

(a) if the Company or such other person proves that the purchaser purchased the securities of the Company with knowledge of the misrepresentation; or

(b) in an action for damages, for all or any portion of the damages that the Company or such other person proves do not represent the depreciation in value of the securities of the

Company as a result of the misrepresentation relied on.

No person, other than the Company, is liable for misrepresentations in any advertising or sales literature if the person prov es:

(a) that the advertising or sales literature was disseminated without the person’s knowledge or consent and that, on becoming awa re of its dissemination, the person gave reasonable

general notice that it was so disseminated,

(b) that, after the dissemination of the advertising or sales literature and before the purchase of the securities by the purchas er, on becoming aware of any misrepresentation in the

advertising or sales literature the person withdrew the person’s consent to it and gave reasonable general notice of the with drawal and the reason for the withdrawal, or

(c) that, with respect to a false statement purporting to be a statement made by an official person or contained in what purports to be a copy of, or an extract from, a public official

document, it was a correct and fair representation of the statement or copy of, or extract from, the document, and the person had reasonable grounds to believe and did believe that

the statement was true.

No person, other than the Company, is liable with respect to any part of the advertising or sales literature not purporting t o be made on the authority of an expert and not purporting to be a

copy of or, an extract from, a report, opinion or statement of an expert unless the person:

(a) failed to conduct such reasonable investigation as to provide reasonable grounds for a belief that there had been no misrepre sentation; or

(b) believed there had been a misrepresentation.

Any person who at the time the advertising or sales literature was disseminated, sells securities on behalf of the Company wi th respect to which the advertising or sales literature was

disseminated is not liable if that person can establish that the person cannot reasonably be expected to have had knowledge t hat the advertising or sales literature was disseminated or

contained a misrepresentation. In no case will the amount recoverable for the misrepresentation exceed the price at which sec urities were offered. The foregoing statutory right of action for

rescission or damages conferred is in addition to and without derogation from any other right the purchaser may have at law. This summary is subject to the express provisions of the New

Brunswick Act and the regulations and rules made under it, and prospective purchasers should refer to the complete text of th ose provisions.

Prince Edward Island

The right of action for rescission or damages described herein is conferred by Section 112 of the Securities Act (Prince Edward Island) (the “PEI Act”). Section 112 provides, that in the event

that an offering memorandum, such as this Offering Memorandum, contains a “misrepresentation”, a purchaser who purchased secu rities during the period of distribution, without regard to

whether the purchaser relied upon such misrepresentation, has a statutory right of action for damages against the issuer, the selling security holder on whose behalf the distribution is made,

every director of the issuer at the date of the offering memorandum, and every person who signed the offering memorandum. Alt ernatively, the purchaser while still the owner of securities may

elect to exercise a statutory right of action for rescission against the issuer, or the selling security holder on whose beha lf the distribution is made. Under the PEI Act, “misrepresentation”

means an untrue statement of material fact, or an omission to state a material fact that is required to be stated by the PEI Act, or an omission to state a material fact that needs to be stated

so that a statement is not false or misleading in light of the circumstances in which it is made. Statutory rights of action for rescission or damages by a purchaser are subject to the following

limitations:

(a) no action will be commenced to enforce the right of action for rescission by a purchaser, resident in Prince Edward Island, l ater than 180 days after the date of the transaction that

gave rise to the cause of action;

(b) in the case of any action other than an action for rescission;

(i) 180 days after the purchaser first had knowledge of the facts given rise to the cause of action; or

(ii) three years after the date of the transaction giving rise to the cause of action or whichever period expires first;

(c) no person will be liable if the person proves that the purchaser purchased the security with knowledge of the misrepresentati on;

(d) no person other than the issuer and selling securityholder will be liable if the person proves that:

Establishing a New Platform for Gold Consolidation 37

Legal Matters

(i) the offering memorandum was sent to the purchaser without the person’s knowledge or consent and that, on becoming aware of it being sent, the person had promptly given reasonable notice to the issuer

that it had been sent without the knowledge and consent of the person;

(ii) the person, on becoming aware of the misrepresentation in the offering memorandum, had withdrawn the person’s consent to the offering memorandum and had given reasonable notice to the issuer of the

withdrawal and the reason for it; or

(iii) (with respect to any part of the offering memorandum purporting to be made on the authority of an expert or purporting to be a copy of, or an extract from, a report, statement or opinion of an expert, the

person had no reasonable grounds to believe, and did not believe that;

(A) there had been a misrepresentation; or

(B) the relevant part of the offering memorandum:

I. did not fairly represent the report, statement or opinion of the expert, or

II. was not a fair copy of, or an extract from, the report, statement, or opinion of the expert.

If the purchaser elects to exercise a right of action for rescission, the purchaser will have no right of action for damages.

In no case will the amount recoverable in any action exceed the price at which securities were offered to the purchaser.

In an action for damages, the defendant will not be liable for any damages that the defendant proves do not represent the depreciation in value of securities as a result of the misrepresentation. The foregoing

statutory right of action for rescission or damages conferred is in addition to and without derogation from any other right the purchaser may have at law. This summary is subject to the express conditions of the PEI Act

and the regulations and rules made under it, and prospective purchasers should refer to the complete text of those provisions.

Newfoundland and Labrador

The right of action for damages or rescission described herein is conferred by section 130.1 of the Securities Act (Newfoundland and Labrador) (the “Newfoundland Act”). The Newfoundland Act provides, in relevant

part, that where an offering memorandum, such as this Offering Memorandum, contains a misrepresentation, as defined in the Newfoundland Act, a purchaser who purchases securities offered by the offering

memorandum during the period of distribution has, without regard to whether the purchaser relied upon the misrepresentation, (a) a statutory right of action for damages against (i) the issuer, (ii) every director of the

issuer at the date of the offering memorandum, and (iii) every person or company who signed the offering memorandum and (b) for rescission against the issuer.

The Newfoundland Act provides a number of limitations and defences in respect of such rights. Where a misrepresentation is contained in an offering memorandum, a person or company shall not be liable for

damages or rescission:

(a) where the person or company proves that the purchaser purchased the securities with knowledge of the misrepresentation;

(b) where the person or company proves that the offering memorandum was sent to the purchaser without the person’s or company’s knowledge or consent and that, on becoming aware of its being sent, the

person or company promptly gave reasonable notice to the issuer that it was sent without the knowledge and consent of the person or company;

(c) if the person or company proves that the person or company, on becoming aware of the misrepresentation in the offering memorandum, withdrew the person’s or company’s consent to the offering

memorandum and gave reasonable notice to the issuer of the withdrawal and the reason for it;

(d) if, with respect to any part of the offering memorandum purporting to be made on the authority of an expert or purporting to be a copy of, or an extract from, a report, opinion or statement of an expert, the