Transport of Dendritic Microtubules Establishes Their Nonuniform ...

New York’s Nonuniform Prudent Management ofInstitutional Funds Act: What All New York Nonprofits(and Their Lawyers) Should Know

by David W. Lowden

David W. Lowden

David W. Lowden is aSpecial Counsel in the Corpo-rate and Securities PracticeGroup of Stroock & Stroock &Lavan LLP with a practicefocused on the needs of non-profits. He is currently thechair of the Committee on Non-Profit Organizations of the As-sociation of the Bar of the Cityof New York.

Quotation with attributionis permitted. This memoran-dum offers general information

and should not be taken or used as legal advice for specificsituations, which depend on the evaluation of precise factualcircumstances.

The author wishes to express his appreciation to GordonSiess and Patrick Yu, partners at Holtz Rubenstein ReminickLLP, Certified Public Accountants, Business Advisers, for theiradvice regarding accounting issues.

On September 17, 2010, New York finally enacted aversion1 of the Uniform Prudent Management of Institu-

tional Funds Act (UPMIFA), joining 46 other states, theDistrict of Columbia, and the U.S. Virgin Islands. (OnlyFlorida, Mississippi, and Pennsylvania have not yetenacted it at the state level.)

The New York act imposes new duties on governingboards of all New York-formed nonprofits, imposes newrestrictions on the management of institutional fundsheld by such nonprofits, and liberalizes rules on endow-ment fund spending by such institutions.

The effective date of the New York Prudent Manage-ment of Institutional Funds Act (NYPMIFA)2 and all itsprovisions was September 17. For institutional fundsexisting on the effective date, however, the act onlygoverns decisions made or actions taken on or after thatdate (see section 557).

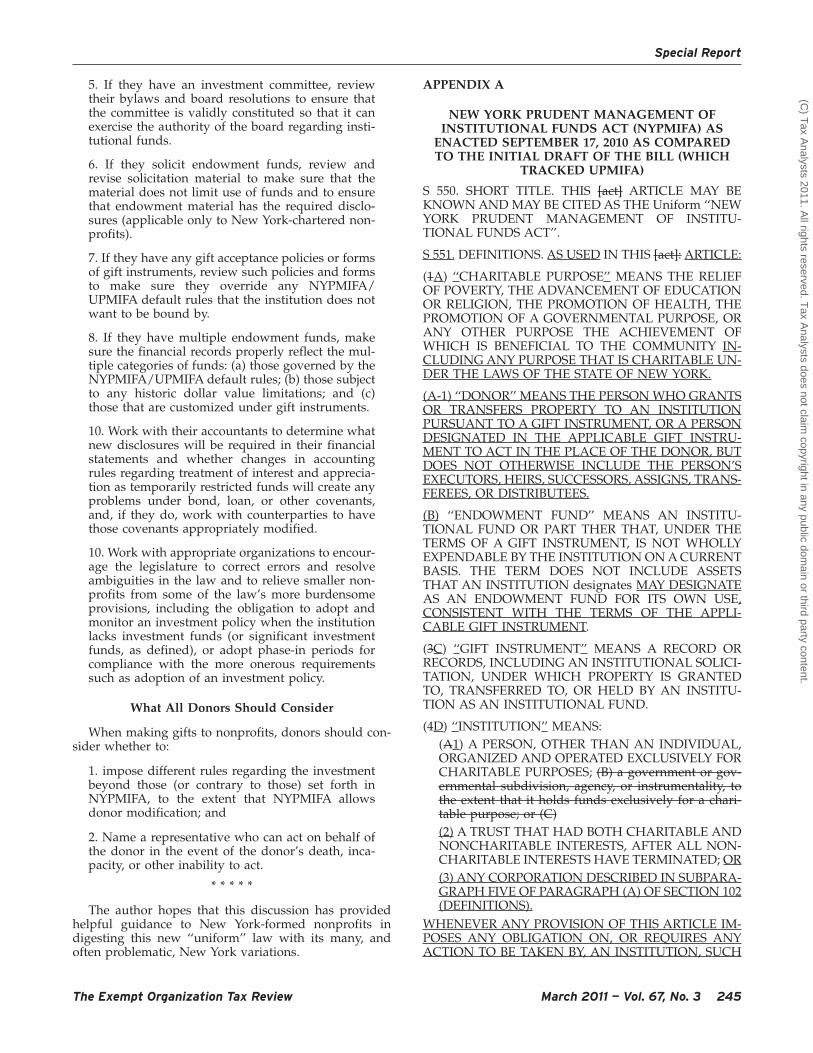

1Assembly bill 7907D (which is the same as Senate bill4778-C) was passed by the Assembly on June 29 and by theSenate on June 30, delivered to the governor on September 7,and signed by the governor on September 17, 2010. See http://assembly.state.ny.us/leg/?default_fld=&bn=A07907%09%09&Summary=Y&Actions=Y&Text=Y. A copy of the enacted billmarked to show the changes from the bill as initially introduced(which generally tracked UPMIFA) is attached as Appendix A.

The new law adds a new article, Article 5-A, to the Not-for-Profit Corporation Law (NPCL), and it amends and repealsother provisions of the NPCL. The amended provisions are theclosing paragraph of paragraph (a); all of paragraph (b); and anew paragraph (e) of section 406 (regarding private founda-tions), paragraph (b) of section 513 (regarding administration ofassets received for specific purposes), paragraph (a) of section514 (regarding delegation of investment management) andparagraph (a) of section 717 (the important provision of theNPCL regarding the duties of officers and directors; the changesto this statement of the duties of directors are several: first, theclause is no longer gender specific, with the ‘‘prudent man’’

standard now changed to a ‘‘prudent person’’ standard; second,the words ‘‘degree of diligence, care and skill’’ are changed tojust ‘‘care;’’ and, third, the words ‘‘in a like position’’ are added.Whether these changes have substantive importance remains tobe seen).

The repealed provisions are subparagraphs 13, 14, and 17 ofparagraph (a) of section 102 (various definitions that are pickedup in the new Article 5-A); paragraphs (c) and (d) of section 513(regarding administration of assets received for specific pur-poses); and section 522 (regarding release of restrictions on useor investment). The law also amends the Religious CorporationLaw (paragraphs (c) and (e) of subdivision of section 2-b), theEstates, Powers and Trust Law (paragraphs (e) and (j) of section8-1.1, section 8-1.7, and subparagraph 1 of paragraph (e) ofsection 11-2.3 to eliminate an ‘‘institutional fund’’ as defined innew Article 5-A from the definition of trustee), the Surrogate’sCourt Procedure Act (subdivision 1 of Section 2115, to authorizejudicial review of the costs of investment authority delegationunder new Article 5-A), and the Executive Law (subdivision 2 ofsection 174-b, to require particular language in solicitationsregarding endowments, discussed below).

2It is telling that the short title for the New York legislation isnot the New York Uniform Prudent Management of InstitutionalFunds Act, as originally proposed. It is, instead, the New YorkPrudent Management of Institutional Funds Act (sometimesabbreviated as NYPMIFA and generally pronounced ‘‘Nip-Mifa’’), dropping the word ‘‘uniform.’’ In truth, it also could becalled the New York Non-Uniform Prudent Management ofInstitutional Funds Act (NYNUPMIFA or pronounced ‘‘Nigh-Nup-Mifa’’).

(Footnote continued in next column.)

The Exempt Organization Tax Review March 2011 — Vol. 67, No. 3 233

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

UPMIFA was proposed by the Uniform Law Commis-sion (also known as the National Conference of Commis-sioners on Uniform State Laws) in 2006 to revise theUniform Management of Institutional Funds Act(UMIFA), the law that was previously in effect in NewYork and most other states.3

UPMIFA primarily changed UMIFA to do three things:• provide guidance for investment decision-making;• provide rules for spending from endowment funds;

and• provide rules for modifying donor restrictions.UPMIFA is good news for nonprofits with underwater

endowments (endowments that have a current dollarvalue below the level of the original grant), which underprior law were precluded from making any distributionsother than from current income (for example, interest,dividends, royalties, and rents).

NYPMIFA, however, differs from UPMIFA in layeringon many provisions unique to New York, some of whichwill prove burdensome, especially to smaller nonprofits:

• First, the New York law applies to all nonprofits, notjust charities.

• Second, it requires all nonprofits to adopt or updateinvestment policies, whether or not they hold en-dowments or other institutional funds.

• Third, it expressly requires that the governing board(or a board committee) assume the duties set forth inthe UPMIFA.

• Fourth, it requires detailed contemporaneous docu-mentation of endowment-related decisions.

Other less onerous changes to UPMIFA were made aswell. The level of added detail found in NYPMIFA is, nodoubt, a response to the perception of lax administrationby nonprofits brought to light by the recent Madoffscandal, which broke after UPMIFA was first proposedby the Uniform Law Commission.

Some NYPMIFA provisions apply to all institutions,some apply to institutions that have institutional funds,and others apply only to institutions that have endow-ment funds.

NYPMIFA, however, should apply only to nonprofitsformed under New York law. The act amends the Not-for-Profit Corporation Law (NPCL). The provisions of theNPCL applicable to foreign corporations (those formedunder the law of another state or jurisdiction) do notinclude these newly amended provisions. (See NPCLArticle 13, especially section 1320.) Further, under theinternal affairs doctrine, governance issues are generallyunderstood to be regulated by the laws of the state offormation. Accordingly, nonprofits formed under thelaws of states other than New York should not be subjectto NYPMIFA.4 The enactment of NYPMIFA gives newnonprofits another reason to consider forming in statesother than New York.

It is interesting to note that the act does not includesection 10 of UPMIFA, which says that consideration‘‘must’’ be given to the need to promote uniformity of thelaw regarding its subject matter among states that enactUPMIFA.

New Procedural Rules Applicable toAll Nonprofits Formed in New York

The act applies to all defined ‘‘institutions,’’5 whichinclude all nonprofit corporations formed in New York,whether or not charitable (including health service cor-porations, social clubs, athletic organizations, social wel-fare organizations, professional and civic organizations,business leagues, and trade associations, as well astraditional charities such as hospitals, educational insti-tutions, and others); whether or not they have endow-ments or other significant institutional funds; and

3The text of UPMIFA is available at http://www.law.upenn.edu/bll/archives/ulc/umoifa/2006final_act.htm. Thetext of UMIFA is available at http://www.law.upenn.edu/bll/archives/ulc/fnact99/1970s/umifa72.htm.

4The New York Attorney General’s Office may take a differ-ent view as to out-of-state nonprofits that are based in New

York. An interesting question is whether a donor could stipulatein a gift instrument that the law of another state would apply,thereby possibly avoiding this statute.

5An institution is defined under the uniform version ofUPMIFA as a person, other than an individual, ‘‘organized andoperated exclusively for charitable purposes,’’ a governmentagency to the extent that it holds funds exclusively for acharitable purpose, and a trust that had both charitable andnon-charitable interests after all non-charitable interests haveterminated. NYPMIFA drops the governmental category forreasons that are unclear but then adds a clause that includes allcorporations as defined under section 102(a)(6) of the NPCL,which means all (or most) nonprofits formed in New Yorkunder the NPCL (whether Type A, B, C, or D) or predecessorlaws or by special act for which a corporation may be formedunder the NPCL as long as the corporation was formed exclu-sively for a purpose or purposes not for pecuniary profit orfinancial gain and no part of the assets, income, or profit isdistributable or inures to the benefit of its members, directors, orofficers except as allowed under the NPCL (as was the case withUMIFA). Although not clear, I assume this also includes corpo-rations formed under the Education Law and Religious Corpo-ration Law (and other legislation that references the NPCL)since they are governed under the NPCL, at least in part. Butthose entities are probably also ‘‘institutions’’ within the mean-ing of NYPMIFA because they are operated for charitablepurposes (in the broad meaning of that word).

However, this definition, with its reference to ‘‘pecuniaryprofit or financial gain,’’ may exclude some Type D corporationsbecause that type of nonprofit includes those formed for ‘‘anybusiness or non-business, or pecuniary or non-pecuniary, pur-pose’’ specified by another law and, if ‘‘business’’ is deemed thesame as ‘‘pecuniary,’’ may also exclude Type C corporations,which are formed for a ‘‘lawful business purpose to achieve alawful public or quasi-public objective.’’ This is one of manyareas where legislative or administrative clarification would bedesirable.

Although the new law does not generally apply to aninstitutional fund held by a charitable trust unless a trustee ofsuch trust is itself a defined institution (see discussion infootnotes 8-10 regarding institutional funds), such trusts stillmay be institutions and therefore subject to the requirement tohave an investment policy, which applies to all defined institu-tions, whether or not they have any institutional fund. It is notclear if this was intended.

Special Report

(Footnote continued in next column.)

234 March 2011 — Vol. 67, No. 3 The Exempt Organization Tax Review

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

whether or not they intend to take advantage of theliberalized rules regarding expenditure of endowmentfunds.

The act imposes burdensome procedural rules on allthose nonprofits. The following is a discussion of some ofthese provisions, including provisions not pertaining toendowments, that impose stringent requirements; a de-tailed discussion of the UPMIFA and NYPMIFA provi-sions applicable to endowments appears later.

The Board Must Adopt or Update Investment Policy

Covered institutions now must adopt, under NPCLsection 552(F), a written investment policy setting forthguidelines on investments and delegation of manage-ment and investment functions ‘‘in accord with thestandards of’’ NYPMIFA, whether or not they holdendowment or any other institutional fund.

The requirement for such a policy is unique to theNew York version of UPMIFA. It has engendered signifi-cant concern among those in the New York nonprofitcommunity who are not used to having such a policy.

It is unfortunate that there is not a phase-in period anda de minimis exception for this rule. It is highly unlikelythat nonprofits that already have investment policies (inother words, those with significant endowments or otherinstitutional funds) have a compliant investment policy,even if they have an otherwise appropriate policy. It iseven more unlikely that the small and midsize nonprofitshave any form of investment policy.6 Generally, small andmidsize institutions have not viewed such policies asnecessary (if they even gave the issue any thought)because they usually do not have any financial assets thatwill be held for a significant period and are generallyliving hand to mouth. Although the number of theseinstitutions is unknown, it is safe to assume that many (ifnot most) of the 50,000-plus nonprofits registered withthe New York Charities Bureau do not have such policies.Furthermore, this 50,000 number does not include manyother nonprofits that do not have to register because theyare not charitable but that are also required to have thispolicy.

It appears unlikely that the attorney general will seekto enforce this provision immediately. In fact, there is nopenalty in the statute for noncompliance, and the statu-tory authority of the attorney general to seek sanctionsfor violations of the requirement is unclear. It appearsmore likely, at least in the early years, that the attorneygeneral will seek to educate the nonprofit communityabout the requirement and seek sanctions only if anonprofit encounters other troubles and ignores its re-sponsibilities or otherwise engages in unwarranted ac-tion or inaction.

The breadth of coverage was not an oversight, andmany practitioners who specialize in nonprofits objectedto it during the short drafting period in the legislativeprocess when the nonuniform provisions were first pro-

posed publicly. The protesters noted that NYPMIFAwould require smaller groups to divert their efforts fromperforming their exempt function to preparing documen-tation that should not be necessary, either because theamount of institutional funds held is small or becauseany institutional funds currently held would be spentsoon.

I understand that the Charities Bureau believes thatalmost all nonprofits have one or more institutionalfunds, whether small or large, and a corporation thatdoes not currently have any institutional fund will mostlikely have one in the future. The Charities Bureau alsohas expressed concern that there has been a general lackof board involvement in asset management. As shown bythe Madoff scandal on nonprofits, many boards were notaware of what they need to do regarding their invest-ments. I assume the Charities Bureau believes the re-quirement to have an investment policy should helpforce organizations pay attention to these matters.

Unless the attorney general seeks to exempt someorganizations from the investment policy requirement ordelay enforcement, either by rulemaking or an an-nounced enforcement policy (for example, ‘‘We will notask New York nonprofits for their investment policiesuntil . . . 20 ___’’),7 all New York-formed nonprofit corpo-rations and other institutions must adopt an investmentpolicy.

It is my understanding that the Charities Bureau doesnot believe it would be wise for it to mandate a defaultform, because every charity is different, although thebureau may be able to offer samples. I understand thatsome nonprofit advisory organizations will be preparingprototype or sample policies for consideration, so thatnonprofits will not have to waste time reinventing thewheel. It is a good idea for small and midsize nonprofitsto wait for sample policies to be issued before theyformulate their own policies.

Obviously, institutions that live hand to mouth, withtheir funds spent day to day, can have a simpler form ofinvestment policy. The policy could be very brief, focus-ing on the need for liquidity and safety. Accordingly, thepolicy might talk about depositing all funds in a checkingaccount, money market, or cash equivalents, or similarliquid forms of investment, interest-bearing if available,maintaining in the account all funds that may be neededto enable the organization’s current bills to be paid, anddepositing in one or more interest-bearing accounts withan appropriate financial institution other funds notneeded to pay current bills. Organizations with fundsthat may not need to be spent currently but that lackother significant investment assets will need to considerwhat other forms of investments are appropriate. Insti-tutions with endowment or other long-term investmentswill need a sophisticated policy.

6For instance, it would be appropriate to exempt all nonprof-its, or at least those with financial assets below a statedthreshold, that have all their funds held in insured bankaccounts.

7The Charities Bureau has announced it will issue guidanceon various issues arising under NYPMIFA. It had not beenissued by February 1.

Special Report

The Exempt Organization Tax Review March 2011 — Vol. 67, No. 3 235

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

Each type of institution will need to review its policyperiodically, with the smaller groups assessing whetherthey have grown to a point that a more sophisticatedpolicy is necessary.

The Board Must Consider General Prudence Rulesand Eight Specific Factors in Determining How toManage and Invest Institutional Funds

The First Question Is ‘‘What Is an Institutional Fund?’’

An institutional fund is defined under the act, incircular fashion, as a ‘‘fund that is held by an institu-tion.’’8 The definition then goes on to exclude: (a) assetsthat are not for investment under the terms of the giftinstrument but are primarily to accomplish a program-matic purpose of the institution; (b) funds that are heldfor an institution by a non-institutional trustee; and (c)funds in which a non-institutional beneficiary has aninterest (other than as a contingent beneficiary).9

There is, however, a fundamental (so to speak) flaw inthe definitions. There is no definition of the word ‘‘fund’’in either UPMIFA or NYPMIFA. (This is less problematicwith UPMIFA since UPMIFA does not impose as manyduties on nonprofits regarding institutional funds, suchas the investment policy requirement.) Does the termapply to all financial assets, including cash in the bank orother liquid assets held for current use, or does it applyonly to investments held in some vehicle that constitutesa ‘‘fund,’’ such as ‘‘in a fund’’ that is specifically managedby the company or an investment adviser? To somereaders ‘‘a fund’’ is not the same as ‘‘funds,’’ whichmeans cash. Instead, a fund is something in which fundsor investments are held. The law is unclear.10

8Under UPMIFA, ‘‘institutional fund’’ is defined as a fundheld by an institution ‘‘exclusively for charitable purposes.’’ Thequoted words were dropped from NYPMIFA.

9Both UPMIFA and NYPMIFA exclude from the term ‘‘insti-tutional fund’’ the following assets:

(a) ‘‘program-related assets’’ (a program-related asset isdefined as ‘‘an asset held by an institution [New Yorkadded, ‘‘not for investment under the terms of a giftinstrument, but’’] primarily to accomplish a charitable[New York changed to ‘‘programmatic,’’ which was ne-cessitated by the elimination of the requirement that aninstitutional fund be held for charitable purposes] pur-pose of the institution’’).(b) ‘‘a fund held for an institution by a trustee that is notan institution’’ (i.e., a fund held by individual or for-profitcorporate trustees); and(c) ‘‘a fund in which a beneficiary that is not an institutionhas an interest, other than an interest that could ariseupon violation or failure of the purposes of the fund.’’

For a discussion by the drafting committee which wroteUPMIFA as to the meaning of program-related assets, seeUPMIFA Program Related Assets, available at http://www.upmifa.org/Uploads/UPMIFA_ProgramRelatedAssets.pdf.This commentary makes clear that the term usually applies onlyto tangible or real assets, such as buildings and equipment, notcash or other funds generally held to carry out the charity’spurposes, such as a fund to pay for scholarships or to buy foodto distribute to those in need. It does acknowledge, however,that a fund used by a micro-finance charity to make low-interestloans would be a program-related asset, presumably becausethe fund must be available on a moment’s notice. Presumablythe same standard would apply to actual loans once made, suchas student loans, which would be judged on the basis ofwhether making the loan is an appropriate educational decision,not whether making the loan is an appropriate investmentdecision.

Note that the decision to exclude any fund managed byindividual and corporate trustees was one to which the draftersof UPMIFA gave extensive consideration. UMIFA similarlyexcepted them as most states have their own set of rulesapplicable to trusts. The UPMIFA standards, however, generallytrack those applicable to trustees under the Uniform PrudentInvestor Act (UPIA). In New York the rules applicable to suchtrusts are set forth in section 11-2.3 of the Estates, Powers and

Trust Law. The UPMIFA rules applicable to endowment spend-ing and the modification rules applicable to older, smaller fundsthrough which changes can be done without court approval arenot found in the UPIA, however. See Revisions to the UniformManagement of Institutional Funds Act by Susan N. Gary, Re-porter, Drafting Committee Decisions Made January 22, 2004,available at http://www.abanet.org/rppt/meetings_cle/2005/spring/pt/UniformManagementUMIFA/GARY_hand.pdf.

10Some language in the statute implies that ‘‘a fund’’ shouldnot be viewed as synonymous with ‘‘funds.’’ For instance,section 552(D) says a nonprofit ‘‘may pool two or more institu-tional funds,’’ and numerous sections, such as those containingthe definition of institutional fund, refer to ‘‘an’’ institutionalfund or ‘‘a fund’’ (‘‘an’’ and ‘‘a’’ are not appropriate terms forcash or cash equivalents).

The supporting material on the UPMIFA website (http://www.upmifa.org/DesktopDefault.aspx) does not provide muchguidance as to what is meant by the term ‘‘fund.’’ Revisions to theUniform Management of Institutional Funds Act, by Susan N. Gary,Reporting, Drafting Committee Decisions Made January 22, 2004(available at http://www.abanet.org/rppt/meetings_cle/2005/spring/pt/UniformManagementUMIFA/GARY_hand.pdf)states that ‘‘as under UMIFA (1972), Revised UMIFA [i.e.,UPMIFA] covers all funds held and managed by a charity for itscharitable purposes.’’

Financial Accounting Standards Board Statement of Finan-cial Accounting Standards No. 117, ‘‘Financial Statements ofNot-for-Profit Organizations,’’ June 1993, available at http://www.fasb.org/pdf/fas117.pdf, also does not define fund (al-though it does define endowment fund as ‘‘an established fundof cash, securities, or other assets to provide income for themaintenance of a not-for-profit organization’’).

The drafting committee’s memorandum UPMIFA ProgramRelated Assets, cited above in footnote 9, however, says, ‘‘Nearlyall funds held by a charity are governed by UPMIFA. The fundsmay be used for operating expenses, may serve as an endow-ment for scholarships, or may be a development fund to be usedto pay for a new building. All of these funds are institutionalfunds under UPMIFA.’’

In an e-mail exchange with the reporter for UPMIFA, SusanGary, this writer has been advised that although the word‘‘fund’’ covers only assets held for investment purposes, currentoperating funds are still an institutional fund even though heldfor only a short-term period. Gary notes that the prudentinvestment rules applicable to such short-term funds will bedifferent than those applicable to long-term funds, focusingmore on safety and availability (presumably as part of factor (G)in NPCL section 552: ‘‘The needs of the institution and the fundto make distributions’’).

Special Report

(Footnote continued in next column.) (Footnote continued on next page.)

236 March 2011 — Vol. 67, No. 3 The Exempt Organization Tax Review

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

The distinction may not be important for a charity thatreceives funds from gifts and earnings on its investments;one can say that all its funds are held in one or morefunds. However, the distinction is important to otherNew York nonprofits that do not solicit or receive giftsbut operate businesses, such as some health insurancecompanies and nonprofit hospital corporations. It makesno sense to apply the statute to their operating funds,such as their cash or cash equivalents, which are sup-posed to be spent soon.

Although it appears that the word ‘‘fund’’ is intendedto apply only to assets held for investment purposes, thereporter for UPMIFA has said that current operatingfunds are still an institutional fund even though held foronly a short term, since they are being held for invest-ment until spent. If that is correct, ‘‘institutional funds’’would include all cash and other liquid assets — regard-less of how small or how soon they will be spent — aswell as more traditional investments. This is one of manyprovisions in the law that would benefit from clarifica-tion or guidance from the attorney general’s office,especially since NYPMIFA covers non-charitable institu-tions, the only nonprofits covered by UPMIFA. Until it isclarified, it is safest to assume that the term ‘‘fund’’practically applies to all financial assets other than asspecifically exempted from the law.

How Are Institutional Funds to Be Managed?

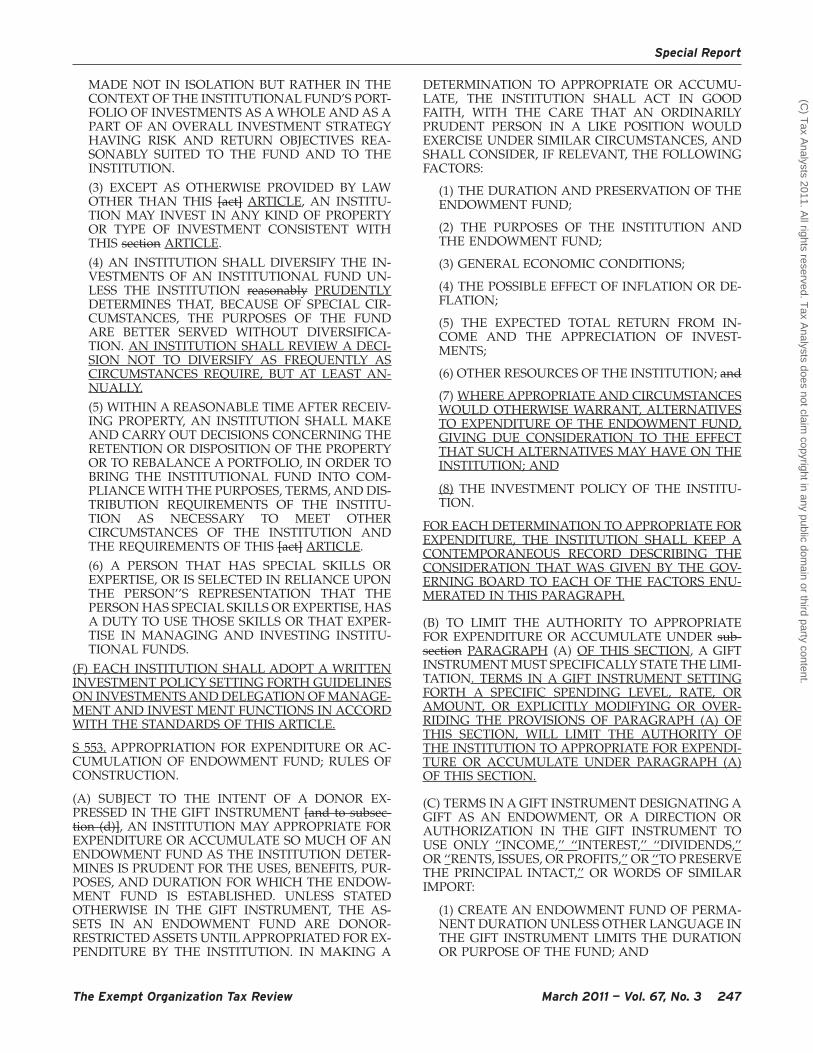

In managing and investing any institutional fund,NPCL section 552(E)(1) of the act requires an institutionto assess at least eight statutorily enumerated factors, ifrelevant:

(A) general economic conditions;

(B) the possible effects of inflation or deflation;

(C) the expected tax consequences, if any, of invest-ment decisions or strategies;

(D) the role that each investment or course of actionplays within the overall investment portfolio of thefund;

(E) the expected total return from income and theappreciation of investments;

(F) other resources of the institution;

(G) the need of the institution and the fund to makedistributions and to preserve capital; and

(H) an asset’s special relationship or special value,if any, to the purposes of the institution.

These requirements must be met unless the gift instru-ment says otherwise. This duty is in addition to thegeneral requirement set forth in NYPMIFA to act ‘‘in

good faith and with the care an ordinarily prudentperson in a like position would exercise under similarcircumstances.’’

The act tracks UPMIFA. However, UPMIFA does notsay who should make such decisions, whereas NYPMIFAincludes language stating that all obligations imposed onthe institution are imposed on, and shall be authorizedby, the governing board.

Although management of the nonprofit will no doubttake the leading oar in recommending where and how toinvest, the act makes clear that any decisions have to bemade by the board or a board committee. The act doesnot require that these decisions be documented, in con-trast to other decisions discussed below, but to protect thedirectors from fiduciary liability it would be appropriateto have such decisions memorialized in board minutes orother corporate records.

The Board Must Consider Eight Factors WhenDetermining Whether to Appropriate EndowmentFunds for Expenditure

In determining whether to appropriate endowmentfunds for current use,11 new NPCL section 553 requiresthat a governing board assess the following eight factors:

(1) the duration and preservation of the endow-ment fund;

(2) the purposes of the institution and the endow-ment fund;

(3) general economic conditions;

(4) the possible effect of inflation or deflation;

Accordingly, if such view is correct, an institutional fundappears to include all cash and other non-programmatic liquidassets regardless of how small they are or how soon they will bespent, as well as more traditional investment funds. The boardshould consider all eight factors enumerated in section 552, tothe extent relevant, in determining how to invest such fund, andthe New York-mandated investment policy must include con-siderations appropriate to such short-term needs.

11When money in an endowment fund is to be spent, theboard must first appropriate it — i.e., determine that it isavailable for current expenditure. It is then spent in due course.The time of appropriation and the time of expenditure are rarelythe same. While it would be prudent for the board resolutionthat is intended to appropriate endowment funds to specificallyuse the term ‘‘appropriate,’’ alternative steps may serve toappropriate funds. For instance, FASB Staff Position FAS 117-1(discussed more fully in footnote 28) indicates that in theabsence of interpretations of the term ‘‘appropriated for expen-diture’’ by legal or regulatory authorities, such appropriation isdeemed to occur on approval of an expenditure (e.g., byapproval of a formal annual budget or by separate spendingauthorization as unexpected developments occur) unless ap-proval is for a future period, in which case such appropriationis deemed to occur when that period is reached. For instance, ifa budget is approved in November for the fiscal year startingthe following January, appropriation by means of such budget isdeemed to occur on January 1. Further, if there is a purposerestriction on the fund, such reclassification does not occur untilthat purpose restriction has also been met. See FAS 117-1,paragraph 9.

Many nonprofits, especially smaller ones, are lax in approv-ing annual budgets (and in approving deviations from suchbudgets); this law will require that such organizations withendowment funds follow better budgeting practices or be clearwhen appropriating endowment funds. This difference in tim-ing has led to some questions regarding the applicability of theNYPMIFA provisions to funds appropriated before enactmentbut only to be expended after enactment.

Special Report

The Exempt Organization Tax Review March 2011 — Vol. 67, No. 3 237

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

(5) the expected total return from income and theappreciation of investments;(6) other resources of the institution;(7) when appropriate and when circumstanceswould otherwise warrant, alternatives to expendi-ture of the endowment fund, giving due consider-ation to the effect that such alternatives may haveon the institution (this seventh factor does notappear in UPMIFA; while consideration of thisfactor may be appropriate for nonprofits in finan-cial trouble, it does not seem warranted when theinstitution is solvent and the appropriation is fromcurrent income); and(8) the investment policy of the institution.12

The board must also keep a contemporaneous recorddescribing the consideration that it gave to each factor.

The requirement for contemporaneous documentation(generally assumed to be satisfied by board meetingminutes) is unique to New York; the law does not definethe term ‘‘contemporaneous.’’13

Traditionally, there was no requirement for formalizeddocumentation regarding these types of decisions. In fact,the decision-making was often delegated by the board tostaff (sometimes the decisions were made by staff with-out board delegation) or made by default through ap-proval of annual budgets.

Now, the act requires that this decision be taken by theboard (or a validly constituted board committee), ratherthan by its delegates; that in making these decisions, agreater number of issues must be considered; and thatthe decision-making process be documented with a for-mality rarely seen in prior years. We understand that theCharities Bureau does not want such documentation tobe boilerplate, rote, or merely conclusory (for example,‘‘the eight factors were considered’’). How much detailwill have to be included in the minutes or other docu-mentation remains to be seen.

The Board Must Diversify Its Investments in AlmostAll Cases

Diversification of all investments is now requiredunless the institution prudently determines that specialcircumstances warrant non-diversification. In the samespirit, when the organization receives specific assets froma donor, it must promptly assess whether the assets can

be kept or should be sold to satisfy the organization’sinvestment criteria and to maintain investment diversity.

NYPMIFA changed the word ‘‘reasonably,’’ which is inUPMIFA, to ‘‘prudently’’ and added a requirement thatthe determination be reviewed as frequently as ‘‘circum-stances require,’’ but at least annually.

The act does not describe what actions are necessaryfor diversification, but in light of recent experiences ofnonprofits with fraudulent investment managers, inwhich institutional funds have been significant, suchdiversification must be of asset type and class and ofmanagers. If an institution keeps all its funds in achecking account or in other accounts with a single bankand the amount of such funds exceeds the limits ofinsurance available, care will need to be taken to ensurethat the prudence of the decision is reassessed anddocumented as required. Keeping funds in non-interest-bearing accounts is probably not prudent, although ex-ceptions may be appropriate when funds are held inshort-term escrows.

Why Was UPMIFA Proposed and What Does It DoRegarding Endowments?

Many larger and some smaller nonprofits are luckyenough to have endowment funds, in other words,monies that are invested to generate income or apprecia-tion that can be used in yearly operations. The beauty ofa large endowment fund is that an organization (ordesignated programs) can live off the income or appre-ciation.

But in the recent troubled economic environmentmany nonprofits found that their endowments wereunderwater, meaning that the current principal amountin the endowment was less than the historic dollar value(in other words, the amount contributed to the endow-ment by the original donor without any inflation factor).Under UMIFA, the law previously in effect in New York,such charities could no longer take distributions ofappreciation from underwater endowments.

Although an institution might still have been able touse any interest, dividends, royalties, and rents generatedby the underwater endowment property, the inability touse realized or unrealized appreciation could place it in aprecarious financial situation. Under UPMIFA, whichsucceeded UMIFA, the trustees have greater flexibility inusing the principal in the endowment funds for currentneeds.

The provisions of UMIFA (and what precededUMIFA), UPMIFA, and NYPMIFA are discussed below.

What Is an Endowment Fund?

First, we need a word of clarification. Under New Yorklaw, endowment funds are funds in the nonprofit’sinvestment portfolio that cannot be ‘‘wholly expend-able . . . on a current basis’’ under the specific terms of thegift instrument (see section 102, subd. (a)(13) of the NewYork Not-for-Profit Corporation Law; the prior provisionremains intact with only modest changes under NYP-MIFA). In most cases the term applies to a fund set upunder the terms of a specific gift instrument, but it alsocould refer to a fund set up by the nonprofit that isfunded by multiple gifts from different individuals.

12Donors can require consideration of additional factors; it isnot clear whether they could eliminate the need to consider anyof these enumerated factors.

13But that term is now defined under IRS instructions forForm 990, ‘‘Return of Organization Exempt From Income Tax,’’applicable to the question whether such meetings were contem-poraneously documented by means of minutes or other writ-ings valid under state law to document board or committeeaction. Under such instructions, ‘‘contemporaneous’’ means ‘‘bythe later of (1) the next meeting of the governing body orcommittee (such as approving the minutes of the prior meeting)or (2) 60 days after the date of the meeting or written action.’’ SeeInstructions to Form 990 for 2009, Part IV, section B, Line 8,available at, http://www.irs.gov/pub/irs-pdf/i990.pdf.Whether such IRS definition will apply to NYPMIFA is not clear.

Special Report

238 March 2011 — Vol. 67, No. 3 The Exempt Organization Tax Review

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

While a nonprofit could have many endowment fundsthat are managed collectively, separate accounting foreach fund is required.14

Pre-UMIFA Standards Allowed Distribution ofIncome Only

Historically, under trust accounting rules (which mostnonprofits assumed applied), nonprofits could use onlythe dividends, interest, rent, or royalties received fromendowment funds for current operations; any increase inthe value of investments (stocks, bonds, etc.) could not bespent.

When endowment assets were sold, all of the proceedshad to be rolled over into similar forms of investment.Additionally, each investment had to meet the applicableinvestment standard; in other words, risk was analyzedon an asset-by-asset basis, rather than by looking at theentire portfolio. Furthermore, trust law did not allowdelegation of investment authority.

UMIFA Changes

In the 1970s commentators realized that many fundswere investing solely for income instead of growth (inother words, capital appreciation) in order to generatethe necessary significant income for day-to-day opera-tions. The funds were less likely to invest in stocks thatmight grow in value because the appreciation could beused only to increase the principal of the endowment. Inthe market conditions that existed in that and subsequentperiods, many stocks that were increasing in value werenot paying dividends; rather, the amounts that couldhave been paid out as dividends were used to grow thebusiness. Consequently, endowments from which it wasnecessary to generate current income were, as a practicalmatter, precluded from investing in such stocks.

UMIFA was first approved in 1972 by what was thenknown as the National Conference of Commissioners onUniform State Laws, and 47 states and the District of

Columbia eventually adopted UMIFA. It was adopted inNew York as sections 512, 514, and 522 (and somedefinitions in section 102) of the NPCL.15

UMIFA allowed the prudence of any one investmentto be determined by looking at the entire portfolio (ratherthan having to analyze whether each separate investmentwas prudent),16 allowed endowments to invest in anytype of assets, allowed the pooling of endowment funds,and allowed nonprofits to delegate management to pro-fessional investment advisers as long as the charity ineach case exercised ordinary business care and wasprudent in making its choices.

In addition to any classic income (for example, inter-est, dividends, royalties, and rents) under UMIFA, theboard was now able to spend on a current basis anyrealized appreciation in the endowment fund (in otherwords, gains on the sale of securities) and any unrealizedappreciation regarding readily marketable assets (gainsin the quoted value for the investment, such as exchange-traded stocks) as long as the board determined that suchexpenditure was prudent, after considering the charity’spurposes, and provided that no expenditures of appre-ciation would cause the fund to go below the historicdollar value (HDV) of the fund (in other words, theoriginal principal amount, unadjusted for inflation).Whether there has been appreciation was determined, atleast in New York state, on a fund-by-fund, not anaggregate, basis.17

Donors can, of course, impose or allow other spendingarrangements, being limited only by the creativity of thedonee or donor, the willingness of the donee organizationto live with any restrictions imposed by the donor (notethat donee organizations are now often not willing toaccept unusual donor restrictions), and the willingness ofthe donor to make the donation if it does not like theconditions required by the donee. For example, the giftinstrument could allow the board to spend according to aspending rate policy prudently adopted by the board that

14Many organizations have funds that they call ‘‘endow-ments’’ that are not endowments subject to UPMIFA. Althougha true endowment is a gift that a donor designates in a writteninstrument to be not wholly expendable by the organization ona current basis, sometimes the board sets aside other funds thatthe nonprofit otherwise has available to it (for instance, pro-ceeds from unusual sales) on which the board has imposedparticular spending restrictions and which it refers to as anendowment. For instance, it could set up a rainy day fund, forwhich money is set aside not to be touched unless a need arises,in which case the full amount of the fund would be available. Orthe board could treat it like a donor-restricted endowment fund,of which the nonprofit can regularly use only the income orappreciation but not the principal. These funds are what issometimes called a ‘‘board-designated endowment fund’’ butthey are not classic endowment funds since the board can, atany time, lift such restrictions. Board-designated funds are notsubject to the endowment limitations of NYPMIFA or UPMIFAand therefore are not as problematic as are endowments com-posed of gifts from donors. While temporarily restricted byboard action, for accounting purposes, such board-designatedfunds are considered unrestricted, whereas true endowmentfunds, for accounting purposes, are restricted.

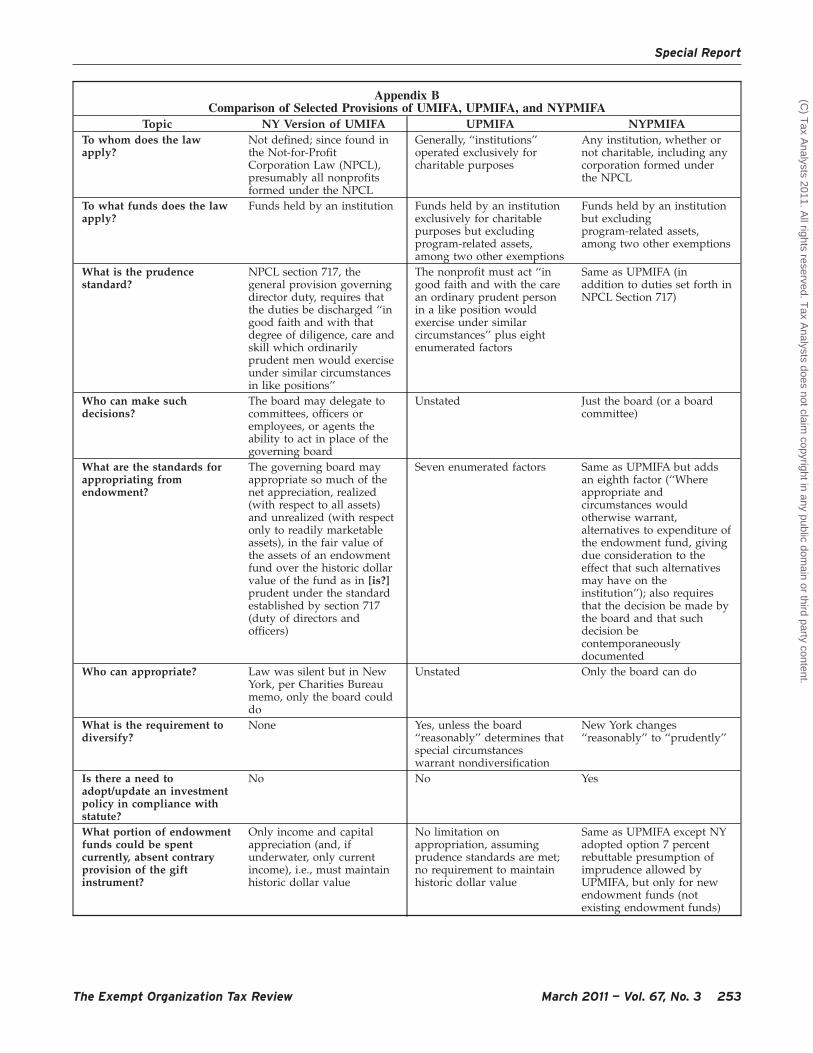

15A chart showing specific provisions under UMIFA, UP-MIFA, and NYPMIFA is attached as Appendix B.

16This is sometimes called ‘‘total return investing.’’ It wasrecognized that having multiple riskier investments does notnecessarily increase the total risk if the nature of the risksbetween the different investments were different. In fact, havingvarying risks may reduce the total risk of the overall invest-ments rather than increase the risk.

17See Advice for Not-For-Profit Corporations on the Appropriationof Endowment Fund Appreciation — the ‘‘Endowment Memo’’ —published by the Charities Bureau of the New York AttorneyGeneral’s Office, available at http://www.oag.state.ny.us/bureaus/charities/pdfs/endowment.pdf. The EndowmentMemo required that appropriation of endowment appreciationhad to be done at the board level instead of the staff level.Whether or not such formal board appropriation process wasalways done in the past, the new NYPMIFA makes the require-ment explicit. The treasurer of each nonprofit is also requiredunder sections 513(b) and 519(a)(2) of the NPCL as existingbefore and after the adoption of NYPMIFA to make an annualreport to the members, or if there are none, to the board ofdirectors concerning the administration and use of the assets ineach endowment fund held for specific purposes and theincome from such assets.

Special Report

The Exempt Organization Tax Review March 2011 — Vol. 67, No. 3 239

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

specifies the percentage (for example, 5 percent of theinvestment principal calculated over a three-year period)to be appropriated for spending each year, whether ornot the income or gain equaled that rate.

UPMIFA Changes

Although UMIFA was a vast improvement over theold rule, times and the needs of charities have changedsince 1972. In 2006 the Uniform Law Commission ap-proved a revised approach, the Uniform Prudent Man-agement of Institutional Funds Act. UPMIFA updates theprudence standard applicable to management and in-vestment of charitable funds, revises the rules governingexpenditures, and includes provisions governing therelease and modification of existing restrictions. Onemotivation for UPMIFA was a fear that nonprofits withunderwater endowments might return to the pre-UMIFAera policy of investing in income-producing investmentsonly.

Prudence Standard

The prudence standard in UPMIFA says managersmust act ‘‘in good faith and with the care an ordinarilyprudent person in a like position would exercise undersimilar circumstances.’’ UPMIFA then sets forth an articu-lated prudence standard (which is more detailed thanthat found in UMIFA) requiring a review of the eightcriteria enumerated in NPCL section 553. As underUMIFA, funds can be pooled.

Diversification

UPMIFA says a charity must diversify its investmentsunless it reasonably determines that special circum-stances dictate otherwise. New York changed ‘‘reason-ably’’ to ‘‘prudently’’ and, as noted above, added aperiodic review requirement. Under NYPMIFA, newinvestments received by an organization must be re-viewed ‘‘within a reasonable time after receiving [the]property’’ to determine if they conform to the charity’sinvestment strategy and fund objectives and whether theinvestments can be retained and whether the portfoliomight need to be rebalanced. Although not expresslynoted in the act, such diversification should be both as toasset type and class and as to managers, especially if theamount of funds under management is significant.

Donors often ask that their donated funds be investedin specific types of investments (such as treasuries) ormaybe even in a specific stock, or require that thedonated funds be managed by a specific manager.Whether such restrictions on the ability to diversify orother such restrictions are enforceable is debatable.

Many institutions take a very cautious approach totheir investments, maintaining them in treasuries orother low-risk liquid investments; whether that approachsatisfies the diversification requirement is also question-able. It is generally assumed that it is imprudent to investthe funds in non-interest-bearing accounts.

No Need to Maintain Historic Dollar Value;Requirements for Appropriation

The biggest change with UPMIFA involves the abilityto spend endowment funds. Under UPMIFA, a charity is

not obliged to maintain the historic dollar value of thefund (unless contractually obligated to do so by the termsof the original gift instrument18 or if so instructed by thedonor under a notice procedure described below), andthe charity can appropriate for expenditure or accumu-lation ‘‘so much of the endowment fund as the institutiondetermines is prudent for the uses, benefits, purpose, andduration for which the endowment fund is established.’’

Note that UMIFA only allowed any such appropria-tion of appreciation to be from any realized appreciationor any unrealized appreciation regarding readily market-able assets; UPMIFA, however, literally allows appropria-tion of unrealized appreciation from assets that are notreadily marketable (but such appropriation would stillhave to satisfy the general prudence standard). The boardmust act in good faith with the care that an ordinarilyprudent person in a like position would exercise undersimilar circumstances and ‘‘shall consider, if relevant,’’the eight factors in the text associated with footnote 12,UPMIFA says. As noted above, NYPMIFA adds an eighthfactor19 and also requires contemporaneous documenta-tion of any such decision.

A charity must follow any limitation on expendituresor accumulation specifically set forth in the gift instru-ment; accordingly, donors could impose caps such as anannual limit on expenditures of a stated percentage of theamount of the endowed fund. NYPMIFA clarifies thatterms setting forth a specific spending level, rate, oramount, or explicitly modifying or overriding the right toappropriate, will limit the authority of the institution.However, if the grant instrument restricts spending toincome, interest, dividends, or rents, issues, or profits, orrequires the institution to preserve the principal intact (orwords of similar import), the charity can use the UPMIFAstandard, the act says.

The UPMIFA standard would apply to all grant instru-ments, even those that predate adoption of UPMIFA,unless contrary grant language is clear. For any giftinstrument executed before the effective date of the act,however, NYPMIFA provides that before the first of anyappropriations for expenditure or accumulation, the in-stitution must provide at least 90 days advance written

18A gift instrument is defined as a record or records, includ-ing an institutional solicitation under which property is grantedto, transferred to, or held by an institution as an institutionalfund. It includes any deed of gift or will bequest.

19This new factor is: ‘‘Where appropriate and circumstanceswould otherwise warrant, alternatives to expenditure of theendowment fund, giving due consideration to the effect thatsuch alternatives may have on the institution.’’ In other words,the nonprofit needs to consider such alternatives to appropria-tion as making substantial layoffs or taking other drastic actionsto reduce costs. Those considerations may be appropriate if thenonprofit is facing financial difficulties, but they seem inappro-priate if the nonprofit is acting routinely. Questions have beenraised as to whether this consideration should only apply if thenonprofit wishes to appropriate any appreciation, which wouldthen cause the fund to drop below historic dollar value (ormaybe inflation-adjusted historic dollar value).

Special Report

240 March 2011 — Vol. 67, No. 3 The Exempt Organization Tax Review

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

notice to the donor — if the donor is then available.20 Adonor is available if he or she is still alive if a naturalperson, or ‘‘in existence and conducting activities’’ if nota natural person and can be identified and located withreasonable efforts. (See text below captioned ‘‘Who is theDonor’’ regarding the ability of a donor to appoint adesignee, who or which would be entitled to receive suchnotice after the donor’s death.)

The act sets forth a form of notice; the form that thenonprofit uses must contain language substantially as setforth in the form.21 During the 90-day period, the donormay, by checking one of two boxes, specifically allow theinstitution to spend ‘‘as much of’’ his gift ‘‘as may beprudent’’ or require that the institution not spend belowthe original dollar value (assumed by most commenta-tors to be the same as historic dollar value). Failure torespond allows the nonprofit to spend according to theUPMIFA prudence standards.

No such notice must be given if the gift instrumentpermits appropriation without regard to historic dollarvalue, the instrument limits the institution’s authority toappropriate for expenditure, or the gift consists of fundsas a result of an institutional solicitation without anyseparate statement by the donor restricting the use offunds. An institution must keep records of all actionstaken under these provisions. It is wise for each institu-tion to issue such notices as soon as possible and beforeit may need to access the endowment funds.

The decision to appropriate should be made simulta-neously for different, similarly situated endowmentfunds by, for example, applying a spending rate to allsuch funds, subject to appropriate documentation re-quirements. When a spending rate is applied acrossmultiple funds, the minutes should nevertheless note theconsideration of all the factors for each of the variousfunds to the extent that factors may vary by fund.

Delegation

Unless otherwise required by the gift instrument, aninstitution may delegate to an external agent22 the man-agement and investment of an institutional fund if suchdecision is made in good faith as would a prudent personin a like position. Such a good faith standard applies to:(a) the selection and, under NYPMIFA, continuance ortermination of the agent; (b) the determination of thescope of delegation (and, in New York, compensation),and (c) the ‘‘periodic review’’ (or, in New York, the‘‘monitoring’’) of the agent’s performance.

NYPMIFA says the agent owes the institution theduties of skill and caution in addition to the duty ofreasonable care as set forth in UPMIFA. NYPMIFAuniquely requires that all conflicts of interest that theagent ‘‘has or may have’’ must be so assessed.23 It alsouniquely requires that all contracts with agents be termi-nable at any time on not more than 60 days notice. Asunder UPMIFA, the act says the agent submits to NewYork jurisdiction.

Following the Madoff scandal, it is especially impor-tant, in making such delegation, for an institution toconduct due diligence regarding the manager. Though itis not required by the statute, all engagements should bememorialized in written agreements, and the experience,track record, employees, and proposed compensationarrangements of all potential agents should be reviewedand compared.

NYPMIFA requires that the engagement be periodi-cally assessed using the same criteria. Although notexpressly required by the NYPMIFA, to carry out thegeneral fiduciary duty of care, all reports from the agentsshould be reviewed regularly by appropriate staff andboard (or committee) members.

While paragraph (c) of NPCL section 554 says aninstitution that complies with the provisions of NYP-MIFA regarding delegation is not liable for the actions ofdecisions of such agent, unique-to-New York paragraph

20The law now requires such notice before any appropria-tion. It is generally assumed that if an appropriation hadoccurred before enactment of the law, such notice is not requirednow even if the appropriated funds had not been spent at thetime the act was enacted. Many practitioners also think that anappropriation from the endowment could be made during the90-day notice period as long as the appropriation does not causethe fund to fall below historic dollar value as allowed underUMIFA, but this is not clear in the statute.

One issue that may surface in the future is whether there isany duty to give notice sooner, rather than later, to avoid theincreased likelihood that a donor may die without havingappointed a designee and therefore no longer be available (andthus notice would not be required). Whether a donor’s estatewould have a cause of action if the institution waited until afterthe donor’s death, or even have standing to assert a claim, is anopen question.

21Many practitioners have noted deficiencies in the languageof the notice as set forth in the statute. For example, if box 2 ischecked, does the prudence standard noted in box 1 still apply(in addition to the box 2 prohibitions)? One would think so, butthe notice language literally indicates otherwise. Also, do thewords ‘‘original dollar value’’ have the same meaning as thewords, under UMIFA, ‘‘historic dollar value’’? The notice alsouses the word ‘‘expenditure,’’ but the statute properly focuseson the time of appropriation, not the time of expenditure. Thisis another area in which guidance or legislative change wouldbe appropriate. Because the statute requires that the notice shall‘‘contain language substantially as’’ appears in the statutorynotice language, it may be safe to tweak the language; however,the extent to which such changes can be safely made is not clear.The act is also unclear on how much effort must be undertakento identify and locate a donor and the consequences if a locateddonor is incompetent.

22This is another definition unique to the New Yorkmeasure.It means independent investment adviser, investment counselor manager, bank, or trust company.

23NYPMIFA is unclear, however, as to the scope of suchconflict assessment — whether it is limited to conflicts with theinstitution and its managers, directors, and officers, or whetherit also extends to conflicts relating to the investments that theagent recommends for the institution. It is wise to require agentsto disclose any investments in products with which the agent orhis or her firm, family members, business partners, or affiliatesmay have a conflict. For example, the agent should not investthe institution’s funds in the business the agent’s cousin unlessfull disclosure is made to the nonprofit and the investment isapproved after disclosure.

Special Report

The Exempt Organization Tax Review March 2011 — Vol. 67, No. 3 241

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

(g) of such section says that nothing in the act shallimpair the operation of section 717 of the NPCL (the basicfiduciary duty statement). So the exculpation language inthe UPMIFA may not have the same practical effect underthe NYPMIFA.

Also, applicable law allows delegation of managementand investment functions to board committees, officers,or employees. In New York, section 514 of the NPCL asamended by NYPMIFA continued the UMIFA provisionthat allows such delegation to committees, officers, oremployees. But section 551(d) of the revised NPCL saysthe duties under the act are imposed on the governingboard. From a drafting standpoint, it is not clear thatsection 551(d) controls, but it is clear that the CharitiesBureau views such language as controlling. Section 712allows the governing board to designate board commit-tees that have the authority of the board except asotherwise set forth in section 712. That section does notlimit the ability of committees to make investment-typedecisions. Accordingly, it appears to be safe to delegatesuch NYPMIFA board duties to a board committee, but itis not clear that they could be delegated to an officer oremployee.24 This analysis is also supported by the gen-eral view that boards work better when they have activecommittees that can focus on topics germane to eachcommittee. Any such delegation in New York does notimpair the obligation of NPCL section 717 regarding theduty of directors and officers.

Optional Provisions

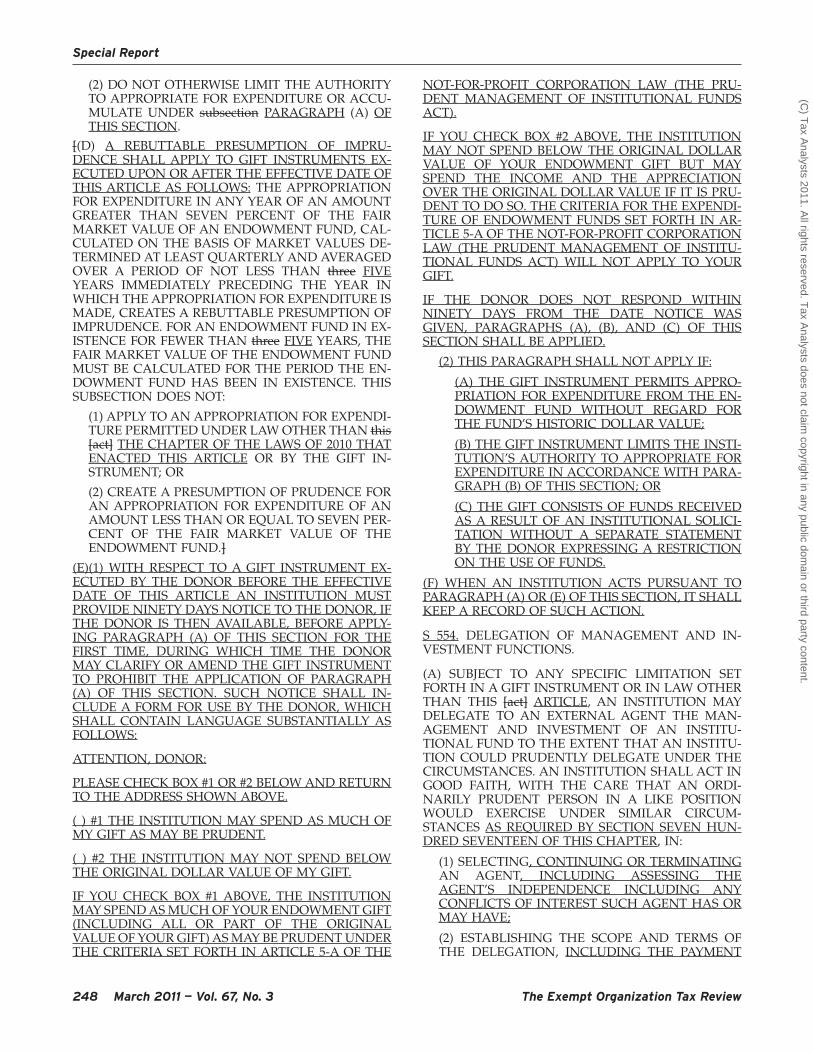

UPMIFA includes several optional provisions thatstates may adopt. One gives the attorney general 60 daysto review the actions of all charities with endowmentsthat aggregate less than $2 million if the value wouldthereby drop below historic dollar value. New York didnot adopt this provision.25

A second optional provision, which New York didadopt, creates a rebuttable presumption of imprudence ifspending from an endowment fund exceeds more than 7percent of the endowment in any year (valuation deter-mined quarterly on the basis of not less than a multiyearrolling average — three years under UPMIFA and fiveyears under NYPMIFA, or the life of the fund ifshorter).26 This presumption presumably would apply

even if the income or appreciation generated by anendowment fund exceeded 7 percent and the fund wasnot underwater. (Note that the presumption does not runthe other way; appropriation of less than 7 percent is notpresumptively prudent.)

Although not expressly required by the act, any deci-sion to exceed the 7 percent threshold should be docu-mented carefully in the minutes of the meetings at whichthat decision was made. The New York presumptionapplies only to gift instruments signed after adoption ofthe act. If an instrument was signed before adoption ofNYPMIFA, the prudence standard (with the eight factors)is the only standard, as such standard may be modifiedby the gift instrument.

According to the Uniform Law Commission commen-tary to UPMIFA, this burden is one of production, not ofpersuasion. It is not clear, however, that New Yorkautomatically would follow this commentary. If NewYork follows the commentary on this issue, the nonprofitneed only show some evidence (whether it is sufficient toproduce a scintilla of evidence or whether the evidencehas to be substantial is not certain) as to why the 7percent threshold was exceeded. A court then wouldrequire the attorney general to carry the burden of proofto show that the appropriation was imprudent. It alsoshould be noted that calculations as to whether or not the7 percent rate was exceeded could be made using severaldifferent standards, because the act only requires that thenumber of years assessed be no less than three (or, inNew York, five) years.

Nonprofits might wish to modify their standard loanforms to override this presumption.

Release of Restrictions

UPMIFA also changes the rules on obtaining donor orlegal consent to the release of restrictions. Under UMIFA,if the donor was living, only he or she could consent tochanges to any restriction (for a foundation or otherdonor that is not an individual, the right of consent lastedas long as the donor entity legally existed). If suchconsent could not be obtained because of the donor’s‘‘death, disability, unavailability, or impossibility of iden-tification,’’ the charity’s governing board could seekcourt approval, on notice to the attorney general, for suchchange, without needing to satisfy cy-pres standards.(Under cy-pres procedures, a charity can seek to haverestrictions lifted only if the restrictions are ‘‘impossibleof performance’’ or illegal, with more practical restric-tions being substituted for the now-superseded restric-tions). Such change could be authorized only if the courtfound that the restriction was obsolete, inappropriate, orimpracticable.

24Care must be taken, however, to ensure that the committeeis validly formed. For example, under NPCL section 712, theonly members of ‘‘such committee can be other directors, and amajority of the entire board’’ (not just a majority of a quorum)must approve the formation of the committee (unless thecommittee was formed under the by-laws), the size of thecommittee (of which there must be at least three members), andthe names of the members appointed.

25This, or a similar, provision was adopted by Maine andNew Hampshire, according to a chart published effective No-vember 6, 2009, available at http://www.arnoldporter.com/resources/documents/UPMIFA%20chart%20(Nov.%206,%202009).pdf.

26This or a similar provision was adopted by at least 13 otherstates: California, Maine, Maryland, Montana, Nevada, NewHampshire, North Dakota, Oregon, Rhode Island, Tennessee,Texas, Utah, and Wyoming. One state, Ohio, adopted a 5 percent

irrebuttable presumption of prudence, and two states (Texasand Wyoming) lowered the presumption of imprudence to 5percent, at least for smaller endowments. Some of these stateshave separate rules for different educational systems. Thesedata come from a chart published effective November 6, 2009,available at http://www.arnoldporter.com/resources/documents/UPMIFA%20chart%20(Nov.%206,%202009).pdf.

Special Report

(Footnote continued in next column.)

242 March 2011 — Vol. 67, No. 3 The Exempt Organization Tax Review

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

The UPMIFA procedure now allows this court proce-dure to lift restrictions even if the donor is alive orexisting. In New York, the application can be made to theSupreme Court in the judicial district where the nonprofithas its office or principal place of carrying out itspurposes or, if the gift instrument is a will, to theSurrogate’s Court where the will was probated. Query:What if the donor to a New York-formed nonprofit wasfrom out-of-state and thus his will was not probated inNew York?

The UPMIFA procedure applies if the restriction ‘‘hasbecome impracticable or wasteful,’’ if it ‘‘impairs themanagement or investment of funds,’’ or if, ‘‘because ofcircumstances not anticipated by the donor, modifica-tion . . . will further the purpose of the fund,’’ with allchanges needing to be consistent, ‘‘to the extent practi-cable, ‘‘with the donor’s ‘‘probable intention.’’ The insti-tution must notify the attorney general and, in New York,the donor if available, and give such parties an opportu-nity to be heard at the hearing. NYPMIFA added lan-guage that says the provisions in the act related to releaseof restrictions does not limit the applicability of thedoctrine of cy-pres.

One other change will help smaller charities. If thefund is at least 20 years old and contains no more than$25,000 in the standard version of UPMIFA ($100,000under NYPMIFA), the restriction can be lifted solely onapproval by the attorney general (or with no approvalother than that of the nonprofit’s board, if there has beenno action by the attorney general after 60 days (90 days inNew York) following notice) instead of needing to obtaincourt approval if the institution determines under NPCLsection 555(d) that the restriction is ‘‘unlawful, impracti-cable, impossible to achieve or wasteful.’’

Under UPMIFA, no notice is required to the donor inthe case of these proceedings, although such notice maybe useful from a public relations standpoint. UnderNYPMIFA, however, notice is required if the donor isavailable. Such notice must include an explanation ofhow the current restriction is inappropriate, the proposedrelease or modification, a copy of the record of theinstitution’s approval of the release or modification, anda statement of the proposed use after such release ormodification.

Who Is the Donor?

Although UPMIFA does not include a definition ofdonor, NYPMIFA does. NYPMIFA defines a donor as the‘‘person who grants or transfers property to an institutionpursuant to a gift instrument, or a person designated inthe applicable gift instrument to act in the place of thedonor, but does not otherwise include the person’sexecutors, heirs, successors, assigns, transferees or dis-tributees’’ (emphasis added). Under this language, if agift is made under a will through a gift instrument signedby the executor, the donor is presumably the decedent,not the executor. However, this interpretation is nottotally clear. It is therefore prudent to include in all giftinstruments the language giving donor rights to a namedindividual.

The language about a donor designee is significant.Since the designee could be a corporation or other entity

(since the definition of person in section 551(g) is exten-sive) with a perpetual legal life, the obligations to notifythe donor set forth in the act could go on long after thedonor’s death. One commentator suggested that theestate fund the likely expenses of enforcement by a donordesignee.27

Notifications Required When Soliciting EndowmentFunds

UPMIFA does not require any specific disclosureswhen soliciting endowment contributions. In New York,however, NYPMIFA changed the Executive Law to re-quire that any institution soliciting donations for anendowment fund now include a statement that ‘‘unlessotherwise restricted by the gift instrument pursuant toparagraph (b) of Section Five Hundred Fifty Three of theNot-for-Profit Corporation Law, the institution may ex-pend so much of an endowment fund as it deemsprudent after considering the factors set forth in para-graph (a) of Section Five Hundred Fifty Three of theNot-for-Profit Corporation Law.’’ Presumably it will beacceptable to simplify this disclosure by using referencesto the statutory provisions using numbers rather thanspelled-out forms and shorthand references to the statute(for example, the NPCL).

Can the Donor and Donee Agree on AlternativeProvisions?

Under NYPMIFA, nonprofits that are holding institu-tional funds are bound to abide by express limitationsimposed by the donors of those funds. Many of theUPMIFA and NYPMIFA provisions are default rules thatapply if the donors and the nonprofits that they give todon’t agree on specific provisions on how the donatedfunds may be spent. Accordingly, many of the statutoryprovisions may be made more or less onerous by expressagreement of the donor and donee. Whether all theprovisions of NYPMIFA applicable to a donated fund,such as diversification and documentation requirements,can be modified by such agreement remains to be re-solved.

Accounting Issues

The adoption of UPMIFA and NYPMIFA will requireall nonprofits to consult with their accountants to addressissues related to the treatment of restricted funds. Underthe accounting rules applicable under UMIFA, earningson endowment funds were considered to be unrestricted;under UPMIFA and NYPMIFA, however, they are classi-fied as temporarily restricted until appropriated. Thischange arises from the wording of UPMIFA, which says,

27See William Josephson, ‘‘New Prudent Management ofInstitutional Funds Act,’’ New York Law Journal, Dec. 3, 2010,page 4. Josephson’s article, along with prior articles appearingin the New York Law Journal on June 11, 2009 and March 30, 2010,praises the legislature for adding many of the provisions uniqueto New York, which he views as protecting the interests ofdonors, a group that he views as generally underrepresentedamong lobbyists.

Special Report

The Exempt Organization Tax Review March 2011 — Vol. 67, No. 3 243

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

‘‘Unless stated otherwise in the gift instrument, the assetsin an endowment fund [meaning all assets, both princi-pal and income] are donor-restricted assets until appro-priated.’’

This may affect some debt covenants and have otherfinancial implications that should be coordinated with anonprofit’s accountants, and may require that the partiesrenegotiate such covenants. For guidance on how theaccounting profession reacted to UPMIFA, see FASB StaffPosition No. FAS 117-1, issued August 6, 2008, effectivefor fiscal years that ended after December 15, 2008.28

Unauthorized Practice of Law Issues

Nonprofits should be careful not to engage in theunauthorized practice of law in advising donors to aninstitution as to the meaning of the law. Although it issafe to repeat the language of the statute, donors shouldseek the counsel of their own lawyers for more detailedanswers to their questions.

What All Nonprofits Should Do

All nonprofits should:

1. educate their board members and investmentstaff on their duties under NYPMIFA/UPMIFA,especially duties regarding:

(a) the eight factors applicable to managingand investing funds and the eight factorsapplicable to any decision to appropriate en-dowment funds (and ensure that any suchdecisions are appropriately memorialized incontemporaneous records);

(b) delegation of investment management,including the need to be diligent at the time ofinitial delegation and periodically thereafter;

(c) diversification, including the need to re-view at least once each year the need todiversify and whether adequate diversifica-tion has been achieved; and

(d) any decision to exceed the 7 percent rateabove which an appropriation from the en-dowment is considered presumptively im-prudent (applicable only to nonprofitsformed in New York and other states thatadopt this optimal provision).

2. Whether or not they have institutional funds,adopt the required investment policy, or amendtheir existing policy to comply with the terms ofNYPMIFA (applicable only to New York-formednonprofits).

3. If they have delegated investment responsibility,review their conflicts policies to make sure financialmanager conflicts at the board and officer level areaddressed and include a provision in the invest-ment policy applicable to the financial manager’sselection of investments.

4. If they have existing endowment funds, give the90-day notice to donors (applicable only to NewYork-formed nonprofits).

28Under FASB Staff Position, FAS 117-1, ‘‘Endowments ofNot-for-Profit Organizations: Net Asset Classification of FundsSubject to an Enacted Version of the Uniform Prudent Manage-ment of Institutional Funds Act, and Enhanced Disclosures forAll Endowment Funds,’’ available at http://www.fasb.org/pdf/fsp_fas117-1.pdf, all nonprofits subject to UPMIFA (or itspredecessor, UMIFA) must classify a portion of each donor-restricted endowment fund of perpetual duration as perma-nently restricted net assets. This must include all portions to beretained permanently in accordance with explicit donor restric-tions or, in the absence of such stipulations, such portion as thegoverning board determines must be retained permanently. Thebalance of the fund is classified as temporarily restricted netassets (time restricted) until appropriated. Many nonprofits willopt to characterize the historic dollar value of the funds (or,alternatively, the inflation-adjusted historic dollar value) aspermanently restricted, leaving the balance as temporarilyrestricted (see FAS 117-1, paragraphs 5 and 8).

All nonprofits with endowment funds, whether or notsubject to UPMIFA, now must disclose in their audited finan-cials more information in order to enable readers to understandthe net asset classification, net asset composition, changes in netasset composition, spending policies, and investment policies ofthe endowment fund, whether it be a classic donor-restrictedfund or a board-designated fund. See FAS 117-1, paragraphs 10,11, and 12. Such description must include:

• a description of the governing board’s interpretation ofthe laws that underlies the organization’s net assetclassification of donor-restricted endowment funds;

• a description of the organization’s policies for theappropriation of endowment assets for expenditure(i.e., its endowment spending policies);

• a description of the organization’s endowment invest-ment policies, which shall include the organization’sreturn objectives and risk limits, how those objectivesrelate to the organization’s endowment spending poli-cies, and the strategies employed for achieving thoseobjectives;

• the composition of the organization’s endowment bynet asset class at the end of the period, in total and bytype of endowment fund, showing donor-restrictedendowment funds separately from board-designatedendowment funds;

• a reconciliation of the beginning and ending balance ofthe organization’s endowment, in total and by net assetclass, including, at a minimum, the following line items(as applicable): investment return, separated into in-vestment income (for example, interest, dividends,rents) and net appreciation or depreciation of invest-ments; contributions; amounts appropriated for expen-diture; reclassifications; and other changes;

• the nature and types of permanent restrictions ortemporary restrictions; and

• the aggregate amount of the deficiencies for all donor-restricted endowment funds for which the fair value ofthe assets at the reporting date is less than the levelrequired by donor stipulations or law.

For the first fiscal year in which UPMIFA is effective in thestate where the nonprofit was formed, the organization mustreport any net reclassification in a separate line item within itsstatement of activities. See FAS 117-1, paragraph 16. FAS 117-1includes illustrative examples of endowment disclosures, bothtabular and footnote.

Special Report

(Footnote continued in next column.)

244 March 2011 — Vol. 67, No. 3 The Exempt Organization Tax Review

(C) T

ax Analysts 2011. A

ll rights reserved. Tax A

nalysts does not claim copyright in any public dom

ain or third party content.

5. If they have an investment committee, reviewtheir bylaws and board resolutions to ensure thatthe committee is validly constituted so that it canexercise the authority of the board regarding insti-tutional funds.

6. If they solicit endowment funds, review andrevise solicitation material to make sure that thematerial does not limit use of funds and to ensurethat endowment material has the required disclo-sures (applicable only to New York-chartered non-profits).

7. If they have any gift acceptance policies or formsof gift instruments, review such policies and formsto make sure they override any NYPMIFA/UPMIFA default rules that the institution does notwant to be bound by.

8. If they have multiple endowment funds, makesure the financial records properly reflect the mul-tiple categories of funds: (a) those governed by theNYPMIFA/UPMIFA default rules; (b) those subjectto any historic dollar value limitations; and (c)those that are customized under gift instruments.

10. Work with their accountants to determine whatnew disclosures will be required in their financialstatements and whether changes in accountingrules regarding treatment of interest and apprecia-tion as temporarily restricted funds will create anyproblems under bond, loan, or other covenants,and, if they do, work with counterparties to havethose covenants appropriately modified.

10. Work with appropriate organizations to encour-age the legislature to correct errors and resolveambiguities in the law and to relieve smaller non-profits from some of the law’s more burdensomeprovisions, including the obligation to adopt andmonitor an investment policy when the institutionlacks investment funds (or significant investmentfunds, as defined), or adopt phase-in periods forcompliance with the more onerous requirementssuch as adoption of an investment policy.

What All Donors Should Consider

When making gifts to nonprofits, donors should con-sider whether to:

1. impose different rules regarding the investmentbeyond those (or contrary to those) set forth inNYPMIFA, to the extent that NYPMIFA allowsdonor modification; and

2. Name a representative who can act on behalf ofthe donor in the event of the donor’s death, inca-pacity, or other inability to act.

* * * * *

The author hopes that this discussion has providedhelpful guidance to New York-formed nonprofits indigesting this new ‘‘uniform’’ law with its many, andoften problematic, New York variations.

APPENDIX A

NEW YORK PRUDENT MANAGEMENT OFINSTITUTIONAL FUNDS ACT (NYPMIFA) AS

ENACTED SEPTEMBER 17, 2010 AS COMPAREDTO THE INITIAL DRAFT OF THE BILL (WHICH

TRACKED UPMIFA)