Navigating the Bundle Jungle - EY · The Bundle Jungle study is designed to monitor and evaluate...

19

Navigating the Bundle Jungle Content, connectivity and consumer trust September 2016 | second edition | ey.com/bundlejungle A consumer media and telecommunications survey

Transcript of Navigating the Bundle Jungle - EY · The Bundle Jungle study is designed to monitor and evaluate...

Navigating the Bundle JungleContent, connectivity and consumer trustSeptember 2016 | second edition | ey.com/bundlejungle A consumer media and telecommunications survey

93% of UK broadband households now have some form of bundle.

55%would only be interested in a mobile bundle if it offered significant price savings.

28%of respondents say it’s difficult to find a package that meets their needs.

40%of people do not know the advertised speed of their broadband connection.

25%of respondents voice a willingness to switch in 2016, up from 21% in 2013.

Bundle providers’ dreams have in many ways come true, but our study illustrates how they must be careful with what they’ve created: today’s digital households have a diverse set of needs and are more demanding than ever

Much has changed since our last survey of UK broadband households in 2013. A step-change in infrastructure capability means that consumers enjoy ever faster internet speeds at home and on the move. The transition to a digital society is now well underway and households have a wide range of connectivity and content needs. At the same time, service providers are adding new features to their existing packages against a backdrop of industry consolidation.

Our findings very much reflect this converging landscape. Broadband packages that feature TV and mobile options now account for more than half the market and customers of more sophisticated packages are more satisfied than average. Bundle providers’ dreams have in many ways come true, but our study illustrates how they must be careful with what they’ve created: today’s digital households have a diverse set of needs and are more demanding than ever.

Consumers still experience a number of pain points when it comes to taking up bundle packages, from making sense of the vast array of choice on the market to switching between different service providers. Critically, many of these concerns are more pronounced than they were in 2013. Meanwhile, our segmentation reveals a diverse range of consumer behaviors — while digital devotees may respond well to the latest content-rich packages, there is a rump of disgruntled users who are disengaged from a complex landscape of competing offers.

Looking ahead, service providers must take heed of consumer demands for packages that provide simple and trusted value propositions. Consumer willingness to switch providers has risen since our last survey and providers must find new routes to translate customer satisfaction into long-term loyalty. Customers require help navigating the “Bundle Jungle” if they are to respond positively to further service innovations.

Jean-Benoit Berty Sector Lead Partner UK Technology, Media & Telecommunications

32%of households believe there is little difference between the services offered by broadband providers.

The Bundle Jungle 2016 32

The Bundle Jungle study is designed to monitor and evaluate the attitudes of UK consumers toward multi-play packages that incorporate both telecommunications and TV services. It draws on consumer insights generated through an online survey of 2,500 UK consumers conducted in April 2016.

The survey contained 54 attitudinal questions, enabling us to segment respondents into seven groups. Additional analysis and insight have been provided by EY’s team of technology, media and telecommunications professionals.

The Bundle Jungle 2016 updates an earlier study — released in 2013 — that also explored end-user attitudes toward residential bundling. In this edition, we have refreshed our segmentation of customers to give us a better understanding of the shifts in consumer needs and attitudes.

This publication comes at the end of a period of dramatic progress and development in the UK bundle market, a period marked by rapid and continuing evolution and — in recent years — by growing maturity. A number of factors have reshaped the bundle landscape, including the widespread introduction of fiber optic broadband and 4G services, TV rights auctions, the rise of over-the-top (OTT) content and ongoing market consolidation.

Research objectives and methodology

2,500UK consumers

Online survey of

The Bundle Jungle 2016 54

1 2 3 4 5 6

Six key findings

Unpacking the messagesWe’ll now take a closer look at the first four messages before examining the segments identified by our research.

of UK broadband households do not take any form of bundle, including line rental.

The bundle market is now a mature and complex landscape — but also one that’s continuing to evolve.

Some 93% of UK broadband households now have some form of bundle, and TV- and mobile-based bundles have grown since 2013. Yet rather than greater simplicity and clarity, the evolution of the market has resulted in a complex landscape of service combinations with a varying mix of free and pay elements.

Within this landscape, TV and mobile bundles score best in terms of satisfaction and loyalty. Positively, overall satisfaction with bundles has risen since 2013 — from 65% to 70%. Although convenience outscores cost as a take-up driver for bundles, there are signs of apathy towards bundled offerings. Most notably, the leading take-up drivers in 2016 are cited less often by households than they were in 2013.

of respondents disagree that purchasing mobile as part of a broadband bundle is a logical purchasing decision.

Customers exhibit mixed attitudes towards different elements of the bundle.

Customers are increasingly happy with the speed of their broadband services as they upgrade to fiber — but they still regard the reliability of the connection as more important than the need for speed. Although customers recognize the value for money from their pay-TV services, their appetite for more sophisticated content propositions is unclear.

At the same time, attitudes towards bundles containing mobile services are lukewarm at best. Many prospective users do not see mobile bundles as a logical purchasing decision, while 55% would be interested in a mobile bundle only if it offered significant price savings.

of households agree that introductory offers make it difficult to work out which package represents best value.

The digital home is evolving rapidly — but pain points with broadband and bundles remain.

Devices are proliferating within the home in tandem with new forms of content consumption. Even so, households are increasingly concerned about data privacy, and many customers are deeply confused about the services they buy or could buy. Some 28% of respondents say it’s difficult to find a package that meets their needs, while 40% — up from 39% in 2013 — do not know the advertised speed of their broadband connection.

Despite rising overall customer satisfaction and a wider range of packages on the market, 32% of households believe there is little difference between the services offered by broadband providers, another increase from 2013. Our survey also reveals a statistically significant direct link between levels of service understanding and levels of satisfaction, with a lack of understanding essentially impeding satisfaction.

of respondents cite a reputation in good customer service as a reason to switch providers.

The propensity to change providers is rising, with price and trust acting as the top switching triggers.

An overall increase in customer satisfaction is not boosting customers’ loyalty to their providers: 25% of respondents voice a willingness to switch in 2016, up from to 21% in 2013. Trust levels and lower prices are the leading attributes for selecting new providers, cited by 43% of households. Conversely, the offer of new service elements such as TV and mobile as an incentive to change providers is playing a much less pronounced role.

of UK broadband households are identified as disgruntled users in our segmentation.

Our segmentation analysis reveals sharply contrasting attitudes towards bundles and the digital world.

EY’s analysis has defined seven customer segments, each with its own distinct characteristics and needs:

• Digital devotees• Content light bundlers • Serious about sport• Disgruntled users• Bargain hunters• Loyal bundlers• Functional users

Across the segments, the complex interplay of attitudes towards bundle benefits, service consumption and willingness to pay suggests that service providers still have untapped routes to meet customer needs. Cross-segment comparisons can help providers redefine assumptions and unlock counterintuitive insights about customers.

of respondents don’t understand broadband speed and how it relates to using the internet.

Bundle propositions can be refined to help service providers succeed in a complex and evolving marketplace.

Looking ahead, service providers should consider how to bolster trust with their customers to translate satisfaction into loyalty. Accurate and meaningful segmentation of the customer base plays a major role.

Our research makes it clear that simpler, more targeted propositions can help alleviate confusion and frustration. These have remained pronounced since 2013, acting as a continuing brake on satisfaction.

7% 32% 49% 23% 17% 21%

The Bundle Jungle 2016 76

With 93% of UK broadband households now having some form of bundle, our research shows that TV- and mobile-based packages are gaining popularity against a backdrop of ongoing infrastructure rollout and rising availability. However, as Chart 1 illustrates, today’s bundle landscape is not only growing but also becoming increasingly complex as the distinction between categories blurs. This trend is challenging traditional notions of double-, triple- and quad-play service packages.

Taken together, bundles that include mobile or TV options now account for 51% of UK consumer bundles, up from 44% in 2013. Correspondingly, the market share of more basic bundles that feature some combination of broadband, line rental and inclusive call package/options has fallen back. And overall, the bundle market is in a mature phase — absolute bundle penetration has increased by only one percentage point over the past three years.

Convenience trumps price as a take-up driverAs in 2013, our study finds that the convenience of having a single point of customer service and a single bill is more influential than cost savings as a take-up driver (see Chart 2). However, the availability of lower introductory pricing has increased its score from 2013, reflecting greater competitive intensity in a more crowded marketplace. That said, signs of consumer apathy have emerged as the bundle market matures. All take-up drivers are less pronounced than in 2013, and the top three in 2016 all score lower than three years ago. Other data points also suggest a lack of engagement — particularly in terms of the perceived lack of differentiation between suppliers.

Chart 2: Ranking of factors influencing bundle take-up

Buy services individually

Broadband and line rental*

Broadband, line rental and fixed telephony

Broadband and TV

Broadband and mobile

Broadband, fixed telephony and mobile

Broadband, fixed telephony and TV

Broadband, TV and mobile

Broadband, fixed telephony, TV and mobile* Including or excluding free calls

Chart 1: Breakdown of UK bundle packages, April 2016

Free TV Free TV

Basic TV

Basic TV

Premium TV

Premium TV

Perc

enta

ge o

f bro

adba

nd h

ouse

hold

s

35

30

25

20

15

10

5

0

Four servicesThree servicesTwo services

A bundle is very important for the convenience of having a single point

of contact for customer service53%

53%

52%

51%

43%

29%

60%

60%

57%

51%

40%

32%

1. The bundle market is now a mature and complex landscape — but one that’s continuing to evolve

A bundle is very important for the convenience of a single bill

A bundle from a single provider is very important to save costs

The quality of equipment that comes with a broadband service played a

significant role in my choice of provider

The introductory pricing offer played a significant role in my

choice of provider

Recommendations from family or friends played a significant role in

my choice of provider

2016 2013

Our study shows that overall levels of satisfaction have risen in the last three years. The aggregate proportion of respondents who are “very” or “quite” satisfied has increased from 65% in 2013 to 70% in 2016. However, the proportion of very satisfied households has slipped from 30% to 27%. As Chart 3 shows, composite bundles with

more service elements tend to generate higher satisfaction: TV bundles score best on loyalty. But, as illustrated by the respective proportions likely to switch providers, the positive correlation between number of services taken and “stickiness” doesn’t always hold true.

Reliable broadband outscores the need for speedAgainst the backdrop of an ongoing rollout of higher-speed fiber networks, households are marginally happier with their broadband speeds in 2016 than in 2013 (see Chart 4). Yet, with 62% of households now having services above 25Mbps, compared with 33% in 2013, the increase in satisfaction seems to have been held back by rising expectations. As the chart also shows, the reliability of broadband services is seen as more important than speed: only 19% of users say they would sacrifice some customer service for lower broadband prices.

Broadband, fixed telephony, TV and mobile

Broadband, TV and mobile

Broadband, fixed telephony and TV

Broadband and TV

Broadband, line rental and fixed telephony

Broadband and line rental

No bundle Broadband and mobile telephony

Chart 3: Customer satisfaction and switching propensity by bundle type

Chart 4: Views on broadband speeds, satisfaction and reliability — percentage of respondents

Perc

enta

ge o

f bro

adba

nd h

ouse

hold

s

90

80

70

60

50

40

30

20

10

0

2016

2016

38

19 18

6762

35 32

332013

2013

82%

74% 73% 70%66%

62%55%

82%

37%

24% 23% 26% 26% 28%

12%

23%

2. Customers exhibit mixed attitudes towards different elements of the bundle

Very or quite satisfied with bundle Very or quite likely to switch providers

Strongly agree Slightly agree

Up to 24Mbps 24Mbps

20% Strongly agree41% Slightly agree33% Neither agree nor

disagree5% Slightly disagree1% Strongly disagree

TV-based bundles

What is the advertised maximum speed of your broadband connection? (excludes don’t knows)

“ I’m very happy with my broadband speed and don’t think my household needs a faster connection.”

“ The reliability of my household’s broadband connection is more important than a broadband speed.”

Q:

2016

The Bundle Jungle 2016 98

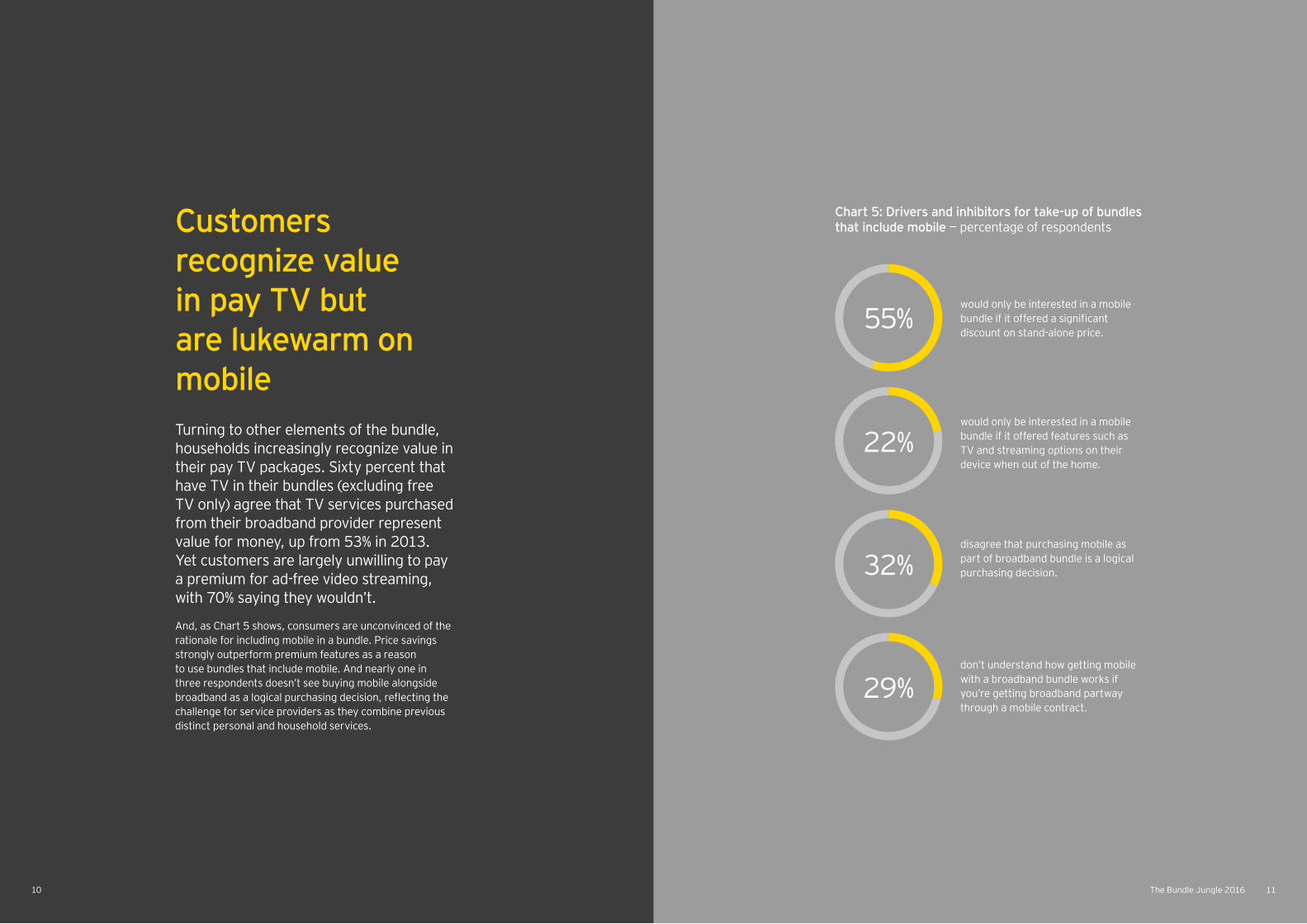

Customers recognize value in pay TV but are lukewarm on mobile

Chart 5: Drivers and inhibitors for take-up of bundles that include mobile — percentage of respondents

would only be interested in a mobile bundle if it offered a significant discount on stand-alone price.

would only be interested in a mobile bundle if it offered features such as TV and streaming options on their device when out of the home.

disagree that purchasing mobile as part of broadband bundle is a logical purchasing decision.

don’t understand how getting mobile with a broadband bundle works if you’re getting broadband partway through a mobile contract.

55%

22%

32%

29%

Turning to other elements of the bundle, households increasingly recognize value in their pay TV packages. Sixty percent that have TV in their bundles (excluding free TV only) agree that TV services purchased from their broadband provider represent value for money, up from 53% in 2013. Yet customers are largely unwilling to pay a premium for ad-free video streaming, with 70% saying they wouldn’t.

And, as Chart 5 shows, consumers are unconvinced of the rationale for including mobile in a bundle. Price savings strongly outperform premium features as a reason to use bundles that include mobile. And nearly one in three respondents doesn’t see buying mobile alongside broadband as a logical purchasing decision, reflecting the challenge for service providers as they combine previous distinct personal and household services.

The Bundle Jungle 2016 1110

New types of devices and content consumption are proliferating in the home, with one in six respondents now using tablets or smartphones as the primary internet access device, over two-thirds having high-definition (HD) TV and over a third having internet-enabled TV. Although consumption of streamed and catch-up content is on the rise, legacy forms remain prominent. Forty-six percent said their household watches TV on the five traditional channels, surprisingly up from 43% in 2013. Even as consumers grow ever more technology-centric and become empowered by a digital lifestyle, their concerns over data privacy are rising. And they remain unconvinced by the emerging generation of “smart home” services (see Chart 6).

The caution over digital privacy is mirrored by a lack of understanding about the connectivity services that consumers receive. Despite marketing campaigns focused on broadband speeds and capabilities, the proportion of users unaware of advertised speeds has actually increased since 2013 (see Chart 7). Also, 21% still don’t really understand how broadband speeds relate to using the internet; 28% say it’s hard to find a package that meets their needs; and a growing proportion find it difficult to switch packages, even with their existing provider. All of this underlines continued confusion and areas of frustration in the broadband and bundle arena.

3. The digital home is evolving rapidly — but pain points with broadband and bundles remain

Chart 6: Attitudes toward online data privacy and “smart home” services — percentage of respondents

Chart 7: Consumer pain points with broadband services and service providers — percentage of respondents

2016 61 28 11 2013

Agree Neither agree nor disagree Disagree

“ I am very cautious about disclosing personal and financial information on the internet, even if the website is from a brand I know or trust.”

Likelihood of using or purchasing smart home products and services in next five years

52 33 15

Smart heating

Smart security

Smart lighting

Connected car

53%

54%

57%

61%

26%

25%

23%

18%

Unlikely Likely

Don’t know the speed of my broadband connection*

Communication services are hard to understand and it is difficult to

find a package that meets my needs

It is difficult to change broadband provider

It is difficult to upgrade or downgrade my broadband package

with my provider

Don’t understand broadband speed and how it relates to using

the internet

39%

28%

24%

15%

21%

40%

28%

24%

19%

21%

2013 2016

* This answer does not refer to an agree or disagree statement, but represents the proportion of don’t know to the multiple-choice question referring to broadband speed (see p. 9).

The overall picture that emerges is of a marketplace where the complexity of bundle offerings and the resulting customer confusion are undermining the opportunity for providers to add value. Put simply, consumers are struggling to navigate the bundle jungle. As Chart 8 shows, introductory offers create confusion rather than clarity, and consumers are increasingly turning to price comparison sites to navigate to the right offerings.

Reflecting these issues, our survey highlights a direct correlation between a lack of understanding and lower overall satisfaction: of the 49% of customers who agree that introductory offers make it difficult to work out which broadband package represents the best value, 24% are very satisfied with their current broadband service compared to 52% for those who strongly disagreed with this statement.

Households that agree introductory offers played a role in their choice of broadband service provider

2013 2016

Chart 8: Consumers’ attitudes toward introductory offers and price comparison sites

43%

34%agree

38%agree

49%

Households that agree that introductory offers make it difficult to work out which package represents best value

“ I use comparison websites (e.g., uswitch, broadband choices) when choosing a broadband.”

Complexity and confusion are undermining value add — and a lack of understanding is impeding satisfaction.

The Bundle Jungle 2016 1312

Despite rising top-line satisfaction, the propensity for households to switch bundle providers has increased since 2013 (see Chart 9). Thus, the customer confusion and lack of understanding we have highlighted are preventing higher satisfaction from feeding through into enhanced customer loyalty.

4. The propensity to switch providers is rising, with price and trust acting as the top triggers

Chart 9: Household propensity to switch providers in 2013 and 2016 — percentage of respondents

Reasons to switch: price and trust outweigh convenience and quality.Considering the reasons why customers switch providers, our research shows that price and brand trust significantly outscore the attraction of more sophisticated packages (see Chart 10). While cost savings rank third as a bundle take-up driver, lower prices rank first as a reason to switch providers. Broadband speed and reliability emerge as more significant factors informing switching than the quality of other bundle elements, such as TV, while introductory offers and equipment quality outweigh customer service. The concern for the industry is that although it seeks to differentiate on the availability of content and service quality, customers are more focused on price, underlying brand trust and broadband performance.

Chart 10: Factors driving switching decisions — percentage of respondents

Low price

Trust in the brand

Reliability of broadband connection

Speed of broadband connection

Quality of introductory offersQuality of equipment (Wi-Fi router, TV box)

that comes with the broadband service Reputation for good

customer serviceQuality of TV offering

Recommendation from friends or family

Have previously got broadband service from them

Availability of free TV contentAlready have some services from that

supplier (e.g., TV, mobile phone)Ability to include mobile with my

broadband bundleAvailability of premium TV content

Availability of “on-demand” TV or video services

43%

43%

38%

38%

28%

24%

23%

16%

13%

11%

11%

10%

9%

9%

6%

Percentage slightly or strongly agree

If you were forced to switch broadband provider, which of the following reasons are applicable for choosing a new provider?

How likely are you to change your home broadband provider in the next 12 months?

Q:

Q:

2016 10 15 31 18 26

Very likely Quite likely Neither likely nor unlikely

Quite likely Very unlikely

2013 10 11 27 16 36

Our analysis has enabled us to identify seven customer segments that make up the UK residential market, each demonstrating a unique combination

of traits. The seven segments and their main characteristics are summarized in chart 11. We’ll now examine each segment in turn.

5. Our segmentation analysis reveals sharply contrasting attitudes toward bundles and the digital world

When we look across the seven segments, it’s useful to put their characteristics side by side to highlight differences and support the creation of strategies to target particular groups of consumers. Providers can then redefine their assumptions and unlock counterintuitive insights about customers, helping to build trust and translate satisfaction into loyalty.

To help providers do all this, we’ve ranked the seven customer segments from one to seven according to their relative attitudes and characteristics around levels of understanding, choice of broadband service and bundle package, media usage, mobile usage; and customer satisfaction and loyalty. These rankings are summarized in chart 12.

Chart 11: Seven customer segments in the UK bundle market

1. Digital devotees• Young, affluent and

tech-savvy• Consume a lot of content

and willing to pay for it• Mobile centric but not

high adopters of mobile bundles

2. Content light bundlers

• High affinity for bundled services

• Tech-savvy and want fast broadband

• Low propensity for premium content and not willing to pay for sport

• High propensity to switch

3. Serious about sport• Love watching sport and

willing to pay for it• High adopters of

premium TV bundles and mobile packages

• Loyal customers with low propensity to switch

7. Functional users• Internet is not essential • Late adopters and lowest

broadband usage• Not interested in new

technology — and low levels of service awareness

6. Loyal bundlers• Late adopters and light

internet users• Most loyal segment with

longest average tenure• Low propensity for

premium content• Oldest segment

5. Bargain hunters• Price-sensitive,

knowledgeable and value-focused

• Regularly switch to get best deal

• Low propensity for latest tech and premium content

UK broadband households

17.2%

13.5%

11.7%

10.7% 15.6%

14.1%

17.2%

4. Disgruntled users• Above average internet usage• Low satisfaction levels• Very low understanding

— they find it difficult to select packages and switch providers

The Bundle Jungle 2016 1514

Chart 12: Relative ranking of the seven segments on various criteria

Customer understanding

Communication services are very difficult to understand and find it hard to choose services or a package that suits my needs 4 6 3 1 7 5 2

Introductory broadband or bundle offers make it difficult to work out which broadband package represents the best value 5 7 6 2 4 3 1

Don’t understand what broadband speed really means and now it relates to using the internet 5 6 4 2 7 3 1

Complicated or very difficult to change broadband provider 3 6 4 1 5 7 2

Don’t know advertised speed of home broadband 7 5 4 3 6 1 2

Choice of broadband and bundle

Very little or no difference between the service offered by the different broadband providers 6 7 5 2 3 4 1

Household tries to spend as little as possible on communication services 7 4 5 6 1 3 2

Household has regularly switched broadband provider to ensure we get the best deal 1 3 4 6 2 7 5

Introductory pricing offer played a significant role in choice of broadband provider 1 2 4 7 3 5 6

Bundling seen as important (average of three relevant statements) 4 2 3 5 6 1 7

Very happy with broadband speed and don’t think my household needs faster broadband 4 3 2 7 5 1 6

Reliability of broadband more important than broadband speed 5 4 2 7 6 1 3

Willing to put up with inferior customer service for lower prices 1 6 4 5 2 7 3

Household is very interested in new technology and “gadgets” and tends to get them before everyone else 1 2 3 4 5 7 6

The internet is fundamental to my social life 1 2 4 3 5 6 7

The internet is very important for my household for working from home or running a business from home 1 3 5 2 4 7 6

Have fibre broadband 1 2 3 4 5 6 7

Media usage

Household mainly watches TV programs on the five traditional TV channels 7 6 5 4 3 2 1

Household tends to watch TV programs on ‘catchup TV’ or recorded on a PVT rather than when they are broadcast 1 2 3 4 5 7 6

Household is willing to pay to watch sport on TV on a subscription basis 2 7 1 4 5 6 3

Some members of household spend a lot more time on the internet than watching traditional TV 1 2 5 3 4 6 7

I am often online whilst doing something else, e.g., watching TV 1 3 4 2 5 6 7

Household often streams online video content on multiple devices (mobile devices or TVs) at the same time 1 3 4 2 5 7 6

Would pay a premium to stream catchup TV without adverts 1 5 2 4 7 6 3

Mobile attitudes

Purchasing mobile as part of a broadband bundle is a logical purchase decision 1 3 2 4 7 6 5

People in my household like to have the most up-to-date smartphones 1 2 4 3 5 7 6

I need to access the internet when I am on the move (i.e., not at home or at work) 1 2 4 3 5 7 6

Like to watch TV programs or movies on a mobile device when on the move (i.e., not at home or at work) 1 5 3 2 6 7 4

Willing to pay a premium for an unlimited mobile data allowance 1 4 2 3 6 7 5

Satisfaction and loyalty

Very satisfied with home broadband service 4 3 2 7 6 1 5

Been with supplier for more than four years 7 5 4 2 6 1 3

Very likely to switch provider in next 12 months 2 6 4 3 1 7 5

Dig

ital

Dev

otee

s

Cont

ent L

ight

B

undl

ers

Seri

ous

Abo

ut

Spor

ts

Dis

grun

tled

Usr

es

Bar

gain

H

unte

rs

Loya

l B

undl

ers

Func

tiona

l U

sers

Myriad contrasts and insights related to various segments can be drawn from this comparison. Here are some that leapt out at us:

• Digital devotees regularly shop around for the best deal despite being highly affluent — yet rank only fourth when it comes to viewing service bundles as important.

• Content light bundlers are well-informed about bundles and less frustrated than other segments — and they also prize customer service more highly than five of the other segments.

• Bargain hunters are knowledgeable about different bundle offers and the broadband speeds offered yet are the third-likeliest to agree that they perceive very little difference between providers.

• Disgruntled users are relatively sophisticated in terms of usage, ranking second in content streaming across multiple devices, but find it difficult to select bundle packages and switch providers.

• Serious about sport is an attractive segment for premium TV bundles — and also ranks second in viewing mobile and broadband packages as a logical purchasing decision.

• Loyal bundlers are the least likely to switch suppliers, but they also have a low affinity for mobile technology in general — and do not see mobile and broadband packages as a logical purchasing decision.

6. Bundle propositions can be refined to help service providers succeed in a complex and evolving marketplace

By using cross-segment insights, bundle providers can adapt and create propositions to meet each group’s unique needs. For example, if a provider is looking to upsell and upgrade customers from a triple-play to a quad-play bundle that includes mobile, then targeting serious about sport users would be a good place to start.

At the same time, digital devotees represent a promising market for mobile bundles, yet service providers should be mindful of their unique switching triggers. For other segments, such as disgruntled users and functional users, clearer communication about service benefits and simpler value propositions could translate into more meaningful and satisfied customer relationships in the long term.

As the bundle marketplace evolves and matures, and as competition intensifies, the ability to understand the attitudes — and thereby the likely buying behavior — of different consumer segments will become increasingly critical to success. We believe our behavioral and attitudinal segmentation of the entire UK consumer population provides a great basis for gaining this understanding, thus opening the way to winning strategies. As our research underlines, every consumer perceives the value of the bundle differently — and the winning providers will be those equipped to cater to those perceptions of value across all segments.

The Bundle Jungle 2016 1716

Like our 2013 report, this Bundle Jungle study uses statistical market segmentation to differentiate various groupings of consumers. Segmentation has enabled us to develop a unique perspective on the UK broadband market, further informed by our telecommunications and analytical teams.

To make the analysis as accurate and actionable as possible, we’ve conducted an attitudinal segmentation. This reflects our view that understanding customers’ attitudes is a much better predictor of their future behavior and preferences than purely behavioral segmentation.

EY has also chosen a segmentation framework that we feel has the most meaningful structure for the current UK broadband market dynamics and that provides the most practicable segment diversity to support the development of distinct propositions.

Our method splits the market into seven segments. Our profiling for each segment looks at bundling behavior, current and future household broadband usage, current and future ownership of fiber broadband, usage of online services and online video services, and usage of mobile telephony services.

Segmenting the UK consumer base

Segmentationoffers a unique perspective on the UK broadband market.

The Bundle Jungle 2016 1918

Digital devotees 22Content light bundlers 24Serious about sport 26Disgruntled users 28Bargain hunters 30Loyal bundlers 32Functional users 34

49%aged 18—39 years

Digital devotees is the youngest segment, with

18—39

Drill-down into the seven customer segments

The Bundle Jungle 2016 2120

This segment is composed of sophisticated, technology-savvy users who understand what they are purchasing. Some 65% agree that they are very interested in new technology and gadgets and are the first to adopt them, the highest of all segments.

Demographic profile:

• The youngest segment — 49% are aged 18–34; 12% are over 55

• The smallest proportion of households without children — 50% (against 70% overall)

• The largest families — 31% have two or more children under 18 (ahead of 18% for the next-highest segment)

• The highest-income segment — 14% have a household income under £20,000 annually;

• 30% exceed £50,000• 19% are from the London area

(against 12% of the overall sample)

Digi

tal d

evot

ees

15.6%

Heavy internet usersDigital devotees have the highest take-up of fiber broadband, and 75% agree that people in their household like to have the most up-to-date smartphones. They spend much of their time on the internet and have a high propensity to purchase additional content — both movies and sport — to watch at home or on the move.

33%9%

43%12%

57%17%

55%18%

56%18%

46%17%

65%21%

64%25%

47%16%

75%29%

Digital devotees Other segments Percentage slightly or strongly agree

Would pay a premium to stream catch-up TV without adverts

Like to watch TV programs or movies on a mobile device when on the move

(i.e., not at home or at work)

Willing to pay a premium for an unlimited mobile data allowance

Household is willing to pay to watch movies on TV on a pay-as-you-use basis

Household is willing to pay to watch movies on TV on a subscription basis

Offers providing free access to content play an important role

in mobile decision makingHousehold is willing to pay to watch

sport on TV on a pay-as-you-use basisHousehold often streams online video

content on multiple devices (mobile devices or TVs) at the same time

Household is willing to pay to watch sport on TV on a subscription basis

People in my household like to have the most up-to-date smartphones

Chart 13: Digital devotees — top 10 differential attitudes

of UK householdsthe third largest segment

Hungry for mobile data Digital devotees strongly agree that being able to access the internet on the move is important. And they are hungry for mobile data, with 37% saying that data usage allowances are insufficient for their needs. Similar to content light bundlers, 45% of digital devotees would be interested in taking mobile as part of a broadband bundle only if a new handset came with it. But 46% agree that purchasing mobile as part of a broadband bundle is a logical decision.

Hard to please — and likely to switchThis segment’s eagerness to consume content is reflected in the 34% who take triple play with premium TV, the second-highest proportion across all segments. However, digital devotees are difficult to keep loyal and have a high propensity to switch. Their satisfaction levels are above the average of the other six segments, ranking third overall. Despite these reasonably healthy satisfaction levels, 33% state they are likely to switch providers in the next 12 months — the highest of any segment.

56%61%

25%28%

18%21%

36%49%

40%50%

14%23%

23%31%

27%49%

25%34%

17%32%

15%17%

34%

22%

11%

28%

18%

31%

13%10%

Digital devotees Other segments

Digital devotees Other segments

Percentage slightly or strongly agree

Chart 14: Digital devotees — bottom 10 differential attitudes

Chart 15: Digital devotees — likelihood of switching in the next 12 months

Very cautious about disclosing personal details or financial information on the internet

Communication services are very difficult to understand and find it hard to choose services

or a package that suits my needsI only use the internet when I have

a specific reason to do soIntroductory broadband or bundle offers

make if difficult to work out which broadband package represents the best value

I only ever use a small number of websites that I am familiar with

Very little or no difference between the service offered by the different

broadband providersHousehold tries to spend as little as possible

on communication services

Don’t understand what broadband speed really means and how it relates to using the internet

Household mainly watches TV programs on the five traditional TV channels

Don’t understand how mobile or broadband bundle works if getting broadband pathway

through a mobile contract

Very unlikely Quite unlikely Neither likely nor unlikely

Quite likely Very likely

The Bundle Jungle 2016 2322

Satisfied triple- or quad-play customersThis segment’s propensity for bundling is demonstrated by the high proportion that take TV-based ‘triple-play’ packages, with some TV and mobile ‘quad-play’ packages. Reflecting their good understanding of the services they buy, they have the highest overall satisfaction rates of any segment, although only the third-highest proportion saying they are very satisfied. They are also generally less likely to change providers, with the second-lowest propensity to switch in the next 12 months.

36%

45%

14%

3%1%

25%

43%

23%

5%3%

Very satisfied Quite satisfied Neither satisfied nor dissatisfied

Quite dissatisfied

Very dissatisfied

Chart 18: Content light bundlers — overall satisfaction with broadband provider

This segment is composed of sophisticated users who understand what they are buying. They rank second behind the digital devotees in their interest in new technology, wanting the most up-to-date smartphones and fiber broadband ownership.

Demographic profile:

• Slightly younger than the population average — with 29% aged 18–34 (in line with 29% overall) and 29% over 55 (against 36% overall)

• 66% have no children under 18, while 18% have two or more children under 18

• The lowest proportion of single-adult households (18%)

• Income profile very close to the population average: 26% have a household income under £20,000 annually; 17% exceed £50,000

Cont

ent l

ight

bun

dler

s

Content light bundlers Other segments Percentage slightly or strongly agree

of UK householdsthe largest segment

Eager to bundleBundling is very important to this segment, for both convenience and cost. Customer service is also highly influential, with this segment unwilling to trade off customer service for lower prices. Key differences from the digital devotees include an unwillingness to pay for sport and a preference for free/basic TV as part of the bundle rather than premium TV packages.

Keen on catch-up content Content light bundlers embrace nontraditional TV viewing habits, are high users of catch-up TV and services, and like to stream content over multiple devices at the same time. Of the seven segments, Content light bundlers have the second-highest proportion of customers taking mobile as part of the bundle. And 32% agree that purchasing mobile as part of a bundle is a logical decision, the third-highest of any segment. However, the bundled mobile package would need to include a discount, and 42% are interested only if a handset comes with it.

19%32%

19%35%

11%20%

12%27%

13%23%

8%21%

16%30%

5%28%

12%26%

6%36%

Chart 17: Content light bundlers — bottom 10 differential attitudes

Don’t understand how a mobile or broadband bundle works if getting broadband part way

through a mobile contractVery little or no difference between the service

offered by the different broadband providers

Willing to put up with inferior customer service for lower prices

Don’t understand what broadband speed really means and now it relates to using the internet

Communication services are very difficult to understand and find it hard to choose services

or a package that suits my needsMy household got home internet access

later than many people I know

Complicated or very difficult to change broadband provider

Complicated or very difficult to upgrade or downgrade broadband package with

mycurrent providerHousehold is willing to pay to watch sport

on TV on a pay-as-you-use basis

Household is willing to pay to watch sport on TV on a subscription basis

17.2%

Bundling very important for the convenience of having a single point of

contact for customer servicesBundling very important for the

convenience of getting a single billQuality or functionality of the

equipment (Wi-Fi router, TV box) played a significant role in choice

of broadband providerPrefer to stream mobile content over

Wi-Fi or my mobile network rather than download contact and watch later

Bundling very important in order to save costs

Household is very interested in new technology and “gadgets” and tends to

get them before everyone else

People in my household like to have the most up-to-date smartphones

Some members of household spend a lot more time on the internet than

watching traditional TVIntroductory pricing offer played

a significant role in choice of broadband provider

Only interested in getting mobile as part of a broadband bundle if it came with option of a new mobile handset

75%49%

74%49%

70%47%

47%34%

38%26%

64%46%

70%48%

56%40%

45%31%

42%31%

Chart 16: Content light bundlers — top 10 differential attitudes

Content light bundlers Other segments Percentage slightly or strongly agree

Content light bundlers Other segments

The Bundle Jungle 2016 2524

Relatively satisfied and loyalThis segment’s propensity for bundling and for buying sport content is demonstrated by the high proportion who take triple- and quad-play packages with premium TV. Although 38% of serious about sport consumers do not appear to know their broadband speed, 82% are satisfied with their speed vs. that advertised, with the highest proportion of very happy users among all segments. They also more loyal than average, with the second-highest proportion saying they are very unlikely to switch providers in the next 12 months.

These consumers are focused on being able to watch sport — and they are willing to pay for it. To a lesser extent, they are also willing to pay for other content.

Demographic profile:

• Age profile close to the population average — 27% are aged 18–34 (against 29% overall); 40% over 55 (against 36% overall)

• 66% have no children under 18; 18% have two or more children under 18

• The second-highest income segment — 23% have a household income under £20,000 annually; 21% exceed £50,000

Serio

us a

bout

spo

rt of UK householdsthe fourth-largest segment

Reliability over speedBundling is important to this segment, particularly for cost and convenience.

A reliable connection is a higher priority than speed, with 65% saying they are happy with their broadband speed, the second-highest of any segment.

Furthermore, 61% agree that the quality and functionality of the equipment that comes with a broadband service played a significant role in the choice of broadband provider. These consumers rank third among all segments in being interested in new technology and gadgets, although they have a high proportion of HD and internet-enabled TVs — possibly reflecting their interest in sport content.

Highest take-up of mobile bundles Serious about sport consumers exhibit the highest take-up of mobile as part of their bundle, and 37% — the second-highest — agree that buying mobile as part of a bundle is a logical decision. When choosing a mobile package, 27% agree that gaining free access to content would play an important role in their decision.

14.1%

37%39%

20%

3% 2%

26%

44%

22%

5%3%

Very satisfied Quite satisfied Neither satisfied nor dissatisfied

Quite dissatisfied

Very dissatisfied

Chart 21: Serious about sport — overall satisfaction

Serious about sport Other segments Percentage slightly or strongly agree

38%47%

14%17%

39%49%

19%25%

22%28%

15%19%

31%39%

35%51%

39%50%

15%22%

Chart 20: Serious about sport — bottom 10 differential attitudes

Household mainly watches TV programs on the five traditional TV channels

Like to watch programs or movies on a mobile device when on the move

(i.e., not at home or at work)Household tries to spend as little as

possible on communication servicesPrefer to stream mobile content over

Wi-Fi or my mobile network rather than download content and watch later

Use comparison websites (e.g., uswitch, broadband choices) when choosing

a broadband providerIntroductory broadband or bundle offers make

it difficult to work out which broadband package represents the best value

Complicated or very difficult to upgrade or downgrade broadband provider

Complicated or very difficult to upgrade or downgrade broadband package

with my current providerSome members of household spend a lot more

time on the internet than watching traditional TVHousehold often streams online video

content on multiple devices (mobile devices or TVs) at the same time

Household is willing to pay to watch sport on TV on a subscription basis

Household is willing to pay to watch sport on TV on a pay-as-you-go basis

Household is willing to pay to watch movies on TV on a subscription basis

Household is willing to pay to watch movies on TV on a pay-as-you-go basis

Purchasing mobile as part of a broadband bundle is a logical purchse decision

Offers provding free access to content play an important role

in mobile decision-making The internet should be very tightly

regulated to restrict what people can access online

Only interested in getting mobile as part of a broadband bundle if it came with option

of a new mobile handsetBundling very important in order

to save costs

Don’t understand what broadband speed really means and how it

relates to using the internet

81%22%

59%18%

42%26%

53%39%

33%23%

42%31%

37%27%

65%49%

27%20%

27%20%

Chart 19: Serious about sport — top 10 differential attitudes

Serious about sport Other segments Percentage slightly or strongly agree

Serious about sport Other segments

The Bundle Jungle 2016 2726

Disgruntled users Other segments Percentage slightly or strongly agree

38%15%

47%19%

46%24%

35%26%

67%45%

38%28%

29%20%

51%39%

29%20%

61%47%

Chart 22: Disgruntled users — top 10 differential attitudes

Complicated or very difficult to upgrade or downgrade broadband package

with my current providerComplicated or very difficult to

change broadband providerCommunication services are very difficult

to understand and find it hard to choose services or a package that suits my needs

Introductory broadband or bundle offers make it difficult to work out which broadband package

represents the best valueDon’t believe it is possible to meet my household’s mobile needs through a

broadband or mobile phone bundleDon’t understand what broadband

speed really means and how it relates to using the internet

Prefer to stream mobile content over Wi-Fi or my mobile network rather than

download content and watch laterDon’t understand how a mobile or broadband

bundle works if getting broadband part way through a mobile contract

The internet is very important for my household for working from home or running a business from home

Some members of household spend a lot more time on the internet than

watching traditional TV

Disg

runt

led

user

s 38%56%

17%25%

35%55%

8%14%

21%33%

26%46%

25%41%

13%23%

16%26%

10%23%

Chart 23: Disgruntled users — bottom 10 differential attitudes

Bundling very important for the convenience of getting a single bill

Household got home internet access later than many people I know

Bundling very important in order to save costs

Household is willing to pay to watch sport on TV on a subscription basis

Use comparison websites (e.g., uswitch, broadband choices) when

choosing a broadband provider

Household is willing to pay to watch sport on TV on a pay as you go basis

I could happily go for a month without internet access in my home

Introductory pricing offered played a significant role in choice of broadband provider

I only use internet when I have a specific reason to do so

Household has regularly switched broadband provider to ensure we get the best deal

Disgruntled users Other segments Percentage slightly or strongly agree

47%

41%

Buy services

individually

Broadband and line rental or

calls

Triple play with free or

basic TV

Triple play with premium

TV

Quad play with free or

basic TV

Quad play with premium

TV

Other bundles

including mobile

11%

6%

23% 24%

12%

20%

2% 3%

Chart 24: Disgruntled users — bundle ownership

Disgruntled users Other segments

2% 3% 2% 3%

A low tendency to buy bundles — or switch providersWell over half — 58% — of these consumers either purchase just broadband and line rental (with or without calls) or buy broadband and line rental from separate suppliers. Their take-up of premium packages is also below average. Their confusion around purchasing communication services seems to strongly affect their happiness: they are the least likely to say they are very satisfied with their broadband service or speed.

However, they don’t see their dissatisfaction as a reason to switch providers. Nearly half of these consumers (49%) have spent over four years with their current providers, the second-highest. Their reluctance to change appears to result from inertia caused by perceived barriers to switching.

These users are moderately interested in new technology but feel that purchasing communication services is complicated and confusing. Consequently, they find changing providers or packages difficult.

Demographic profile:

• The second-youngest segment — 36% are aged 18–34; 27% are over 55

• 67% have no children under 18; 15% have two or more children under 18

• The highest proportion of households with three or more adults over 18 (26%)

• Slightly more affluent than the population average — 24% have a household income under £20,000 annually; 20% exceed £50,000

of UK householdsthe second-largest segment

Spending a lot of time online …Bundling is important to Access to the internet is important to disgruntled users. These households rank second for time spent online and have the second-highest proportion who agree that the internet is important for working from home or running a business from home. They also score highly (75%) when asked whether they are often online while doing something else, such as watching TV.

… but confused by offers People in this segment find introductory offers confusing, and their responses suggest they struggle to understand the value proposition of services they have bought or would be willing to buy. This confusion leads to the lowest satisfaction levels of any segment.

Disgruntled users — along with serious about sport and digital devotees — are much less price-sensitive than other segments. They rank fourth in agreeing that they try to spend as little as possible on communication services. Consequently, they do not view bundling as important for either convenience or cost. For example, only 21% agree that it is logical to buy mobile as part of a broadband bundle.

17.2%

The Bundle Jungle 2016 2928

35%18%

64%34%

71%44%

37%31%

61%43%

61%54%

51%42%

22%21%

22%18%

30%30%

Bargain hunters Other segments Percentage slightly or strongly agree

Household has regularly switched broadband provider to ensure

we get the best dealUse comparison websites (e.g., uswitch,

broadband choices) when choosing a broadband provider

Household tries to spend as little as possible on communication services

Household mainly watches TV programs on the five traditional TV channels

Introductory pricing offered played a significant role in

choice of broadband providerWilling to put up with inferior

service for lower pricesVery little or no difference between

the service offered by different broadband providers

Only interested in getting mobile as part of a broadband bundle if it meant a

significant price discountDon’t believe it is possible to meet my

household’s mobile needs through a broadband or mobile phone bundle

Don’t understand how a mobile or broadband bundle works if getting broadband part way

through a mobile contract

Chart 25: Bargain hunters — top 10 differential attitudes

25%58%

10%25%

9%24%

10%34%

8%22%

7%24%

5%14%

7%31%

9%27%

5%27%

Bargain hunters Other segments Percentage slightly or strongly agree

Chart 26: Bargain hunters — bottom 10 differential attitudes

Bundling very important for the convenience of getting a single bill

Willing to pay premium for an unlimited mobile data allowance

Only interested in mobile or broadband bundle if it included added features such as TV

and streaming options on my device

Offers providing free access to content play an important role in mobile decision-making

Would pay premium to stream catch-up TV without adverts

Household is willing to pay to watch sport on TV on a pay-as-you-go basis

Household is willing to pay to watch sport on TV on a subscription basis

Don’t understand what broadband speed really means and how it

relates to using the internet

Household is willing to pay to watch movies on TV on a subscription basis

Household is willing to pay to watch movies on TV on a pay-as-you-go basis

18%14%

37%

12%

18%

28%

18%

30%

15%

9%

Bargain hunters Other segments

Chart 27: Bargain hunters — likelihood of switching in the next 12 months

Very unlikely Quite unlikely Neither likely nor unlikely

Quite likely Very likely

Relatively dissatisfied — and likeliest to switchThis segment has a high propensity to limit services with a provider, with the majority having just broadband and line rental (with or without a call package). Uptake of premium packages is also low. These consumers are most likely to have been with their current provider for less than two years, and only the Disgruntled and Functional User segments voice lower overall satisfaction. Despite having a good understanding of the package they have purchased, 18% of bargain hunters say they are very likely to switch in the next 12 months, compared with 11% for the next-highest segment, digital devotees.

As their name suggests, bargain hunters are knowledgeable, highly price-sensitive and very value-focused. This segment has the highest proportion of those agreeing that their household spends as little as possible on communication services, at 71%.

Demographic profile:

• Slightly older than the population average — 26% are aged 18–34 (against 29% overall); 39% are over 55 (against 36% overall)

• 75% have no children under 18, while 13% have two or more children under 18

• These tend to be middle-income households — 23% have a household income under £20,000 annually (lower than the overall average of 26%), but 14% have a household income over £50,000 (lower than the overall average of 18%)

Barg

ain

hunt

ers of UK

householdsthe fifth-largest segment

Comparing and switching regularlyIn line with their price sensitivity, these consumers rank second for agreeing that they have regularly switched providers to get the best deal (35%), and they are the most likely to use comparison websites, with 64% doing this when choosing a provider. They also have the highest propensity to switch providers in the next 12 months.

A taste for the traditional Bargain hunters are not willing to pay for premium content, with 61% agreeing that they prefer to watch the five traditional TV channels. Bundling is much less important than the overall cost, and they are more willing to trade off customer service for lower prices. They are also not especially interested in new technology or gadgets and have the third-lowest take-up of fiber broadband.

13.5%

The Bundle Jungle 2016 3130

48%27%

36%22%

80%50%

63%43%

60%39%

70%49%

43%28%

28%20%

76%50%

27%20%

Loyal bundlers Other segments Percentage slightly or strongly agree

I only ever use a small number of websites that I am familiar with

My household got home internet access later than many people I know

Bundling very important for the convenience of getting a single bill

The internet should be very tightly regulated to restrict what

people can access onlineDon’t understand how a mobile or broadband

bundle works if getting broadband part way through a mobile contract

Bundling very important for convenience of having a single point of contact

for customer servicesHousehold mainly watches

TV programs on the five traditional TV channels

Bundling very important in order to save costs

Don’t understand what broadband speed really means and how it

relates to using the internet

I only use the internet when I have a specific reason to do so

Chart 28: Loyal bundlers — top 10 differential attitudes

7%30%

8%34%

6%27%

4%23%

9%40%

5%31%

5%22%

6%42%

8%37%

3%24%

Loyal bundlers Other segments Percentage slightly or strongly agree

Chart 29: Loyal bundlers — bottom 10 differential attitudes

Prefer to stream mobile content over Wi-Fi or my mobile network rather than

download content and watch laterHousehold is willing to pay to watch sport on TV on a subscription basis

Household is willing to pay to watch sport on TV on a pay-as-you-go basis

People in my household like to have the most up-to-date smartphones

Household has regularly switched broadband provider to ensure we get the best deal

Household is very interested in new technology and ‘gadgets’ and tends to

get them before everyone else

Offers provding free access to content play an important role in mobile decision-making

Household is willing to pay to watch sport on TV on a subscription basis

I need to access the internet when I am on the move (i.e., not at home or at work)Household often streams online video

content on multiple devices (mobile devices or TVs at the same time

Loyal bundlers Other segments

Chart 30: Loyal bundlers — bundle ownership

42% 42%

Buy services

individually

Broadband and line rental or

calls

Triple play with free or

basic TV

Triple play with

premium TV

Quad play with free or

basic TV

Quad play with

premium TV

Other bundles

including mobile

2%

7%

37%

23%

10%

20%

4%2% 1%

3% 3% 2%

As its name implies, this segment is highly loyal, with the highest average tenure with current providers and the lowest switching propensity. Similar to functional users, these consumers are relatively light users of the internet — using it when they have a specific reason and restricting themselves to familiar websites.

Demographic profile:

• The oldest segment — with 9% aged 18–34 and 68% over 55

• 90% have no children under 18• The joint-highest proportion of

single-adult households (33%) and the highest proportion of retired respondents (12%)

• The lowest-income segment — 42% have a household income under £20,000 annually, and only 4% exceed

Loya

l bun

dler

s of UK householdsthe second-smallest segment

Latecomers to the internet … In general, loyal bundlers are late adopters of technology: 36% agree that they got home internet access later than other people; only 8% agree that they are interested in new technology and gadgets; and only 9% agree that they like to have the most up-to-date smartphones. Although their understanding of broadband services is limited, they do think that bundling is important for both convenience and cost.

11.7%

An affinity for triple play with basic TVLoyal bundlers tend to purchase more than one service from their provider, and they have a relatively high proportion of triple-play bundles with basic TV. Although they have low understanding of their broadband speed, they have the highest proportion saying they are very satisfied with their service. This segment is much less likely to switch, having the highest proportion of users who have been with their current provider for over five years.

… who see little benefit in mobile internet access People in this segment tend not to use the internet on the move, with only 6% agreeing that they need mobile internet access — by far the lowest of any segment. This group also has the second-highest proportion of prepaid mobile customers, at 49%. And even though they view bundling as important, only 19% agree that purchasing mobile as part of a broadband bundle is logical. Almost two-thirds — 63% — agree that they mainly watch TV on the five traditional channels, and they are very unlikely to be willing to pay for content.

The Bundle Jungle 2016 3332

46%18%

28%11%

43%21%

45%26%

39%19%

71%43%

42%22%

49%30%

31%17%

45%28%

Functional users Other segments Percentage slightly or strongly agree

I only use the internet when I have a specific reason to do so

I could happily go for a month without internet access in my home

My household got home internet access later than many people I know

Don’t understand what broadband speed really means and how it

relates to using the internet

Complicated or very difficult to change broadband provider

Complicated or very difficult to upgrade or downgrade broadband package

with my current providerCommunication services are very difficult

to understand and find it hard to choose services or a package that suits my needs

Household mainly watches TV programs on the five traditional TV channels

Very little or no difference between the service offered by the different

broadband providers

I only ever use a small number of websites that I am familiar with

Chart 31: Functional users — top 10 differential attitudes Chart 33: Functional users — overall satisfaction with broadband provider

10%22%

30%64%

25%56%

16%40%

25%57%

22%55%

22%55%

11%36%

16%39%

15%51%

20%

33%35%

9%

3%

28%

44%

20%

5%3%

Functional users Other segments

Functional users Other segments

Percentage slightly or strongly agree

Chart 32: Functional users — bottom 10 differential attitudesHousehold often streams online video

content on multiple devices (mobile devices or TVs) at the same time

I am often online whilst doing something else e.g., watching TV

Bundling very importantfor the convenience of getting a single bill

Bundling very important for the convenience of having a single point

of contact for customer servicesQuality or functionality of equipment (Wi-Fi

router, TV box) played a significant role in choice of broadband provider

People in my household like to have the most up-to-date smartphones

I need to access the internet when I am on the move (i.e., not at home or at work)

Bundling very important in order to save costs

Household is very interested in new technology and ‘gadgets’ and tends to

get them before everyone else

The internet is fundamental to my social life

Very satisfied Quite satisfied Neither satisfied nor dissatisfied

Quite dissatisfied

Very dissatisfied

These consumers are light users of the internet —using it only when they have a specific reason and restricting themselves to familiar websites. They find purchasing communication services difficult and don’t understand broadband speed or how it relates to the internet, with 39% — the highest of any segment — agreeing with this statement.

Demographic profile:

• The second-oldest segment — 18% are aged 18–34, and 58% are over 55

• 82% have no children under 18• The joint-highest proportion of

single-adult households (33%)• The second-lowest segment in

income — 32% have a household income under £20,000 annually; 14% exceed £50,000

Func

tiona

l use

rs of UK householdsthe smallest segment

Confused late adopters …Like the disgruntled users, functional users do not perceive the value of bundling, a perspective that reflects their view that communication services are difficult to understand. They are late adopters of technology — with only 16% agreeing that people in their household like having the most up-to-date smartphones.

Fragmented buying patterns and low satisfactionThis group has the highest proportion of customers purchasing broadband and line rental from different suppliers. Their understanding of broadband speeds is poor, and they’re less satisfied than the other segments with their current speed vs. the advertised speed. This segment has also the lowest overall satisfaction — only 53%. However, compared with disgruntled users, functional users have a higher proportion of people who say they’re very satisfied. Only 25% of functional users agree they’re likely to switch providers in the next 12 months, and 48% have been with their current provider for more than four years.

… who are unwilling to pay for content Functional users have the highest proportion of people who mainly watch the five traditional TV channels. Consequently, they are less likely to pay for content. This segment also has the highest number of prepaid mobile customers. Only 14% of functional users agree that they would pay a premium for unlimited data for their mobile, and only 20% agree that buying mobile as part of a broadband bundle is a logical decision.

10.7%

The Bundle Jungle 2016 3534

About EYEY is a global leader in assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities.EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legal entity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients. For more information about our organization, please visit ey.com.

© 2016 Ernst & Young LLP. Published in the UK. All Rights Reserved.

EYG no: 02919-164GBL

In line with Ernst & Young’s commitment to minimize its impact on the environment, this document has been printed on paper with a high recycled content.

Information in this publication is intended to provide only a general outline of the subjects covered. It should neither be regarded as comprehensive nor sufficient for making decisions, nor should it be used in place of professional advice. Ernst & Young LLP accepts no responsibility for any loss arising from any action taken or not taken by anyone using this material.

ey.com/UK

EY | Assurance | Tax | Transactions | Advisory

EY key contactsJB BertySector Lead Partner, UK Technology, Media & Telecommunications, Ernst & Young [email protected]

Adrian BaschnongaLead Analyst, Global Telecommunications Centre, Ernst & Young [email protected]

Stuart OrrPartner, UK Telecommunications and Media & Entertainment, Ernst & Young [email protected]

Rahul GautamAdvisory Leader, UK Media & Entertainment, Ernst & Young [email protected]

Olivier WolfPartner, UK Transaction Advisory Services, Ernst & Young [email protected]

For Media and Marketing enquiries, please contact [email protected].