Multi-Factor asset pricing And more on the homework.

25

Multi-Factor asset pricing And more on the homework

-

Upload

myah-skerritt -

Category

Documents

-

view

219 -

download

0

Transcript of Multi-Factor asset pricing And more on the homework.

Multi-Factor asset pricing

And more on the homework

Review item

Define beta.

Answer

2)(

),(

M

jM

M

Mjj RVar

RRCov

Rate of return on asset j isRate of return on the marketportfolio is

jR

MR

My project: AOL

Regression: y = a + bx + e

where a and b are constants y is to be explained x is an explanatory variable e is a random error term

For Beta

Rj = a + bRM + e

e = idiosyncratic risk (diversifiable risk) b = beta a = alpha = sample average advantage

over the market if statistically significant

Components of risk

Diversifiable risk is unique, idiosyncratic, or unsystematic risk

Market risk is systematic or portfolio risk

Diversifiable risk

It is eliminated by buying other assets, i.e.,

can be "diversified away."

Arbitrage pricing theory

Side-issue: Arbitrage is interesting in options, bonds, CAPM, and this course.

Notion: There are several factors (indexes). They are found by regression analysis. More notion: Each factor has its own beta. Risk unrelated to the factors can be

diversified away, leaving only systematic risk.

The K-Factor Model

Surprise in factors: F1, F2, … ,Fk

Ri = E(Ri) + i1F1 + i2F2 + … + iKFk + i

The unexpected systematic return is explained bysurprise in “factors.”

Arbitrage pricing theory is like CAPM, …

Factor risk (previously market risk) remains even when the portfolio is fully diversified.

Factor risk is undiversifiable. For any asset, the betas of factors

measure factor risk. Required return is linear in the factor

betas.

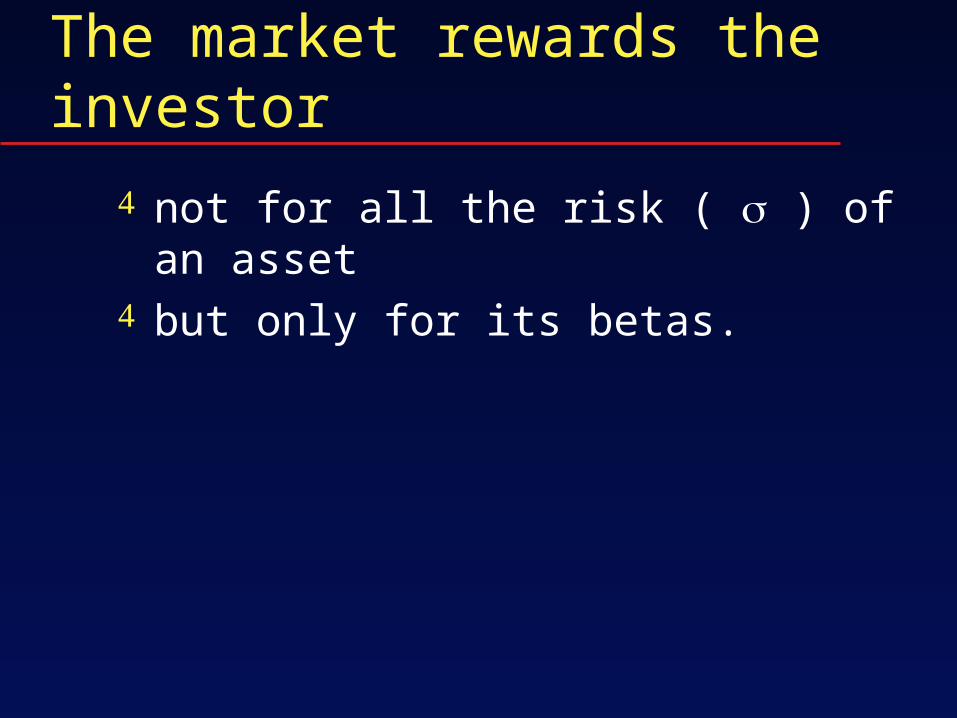

The market rewards the investor

not for bearing diversifiable risk but only for bearing factor (or market) risk.

The market rewards the investor

not for all the risk ( ) of an asset but only for its betas.

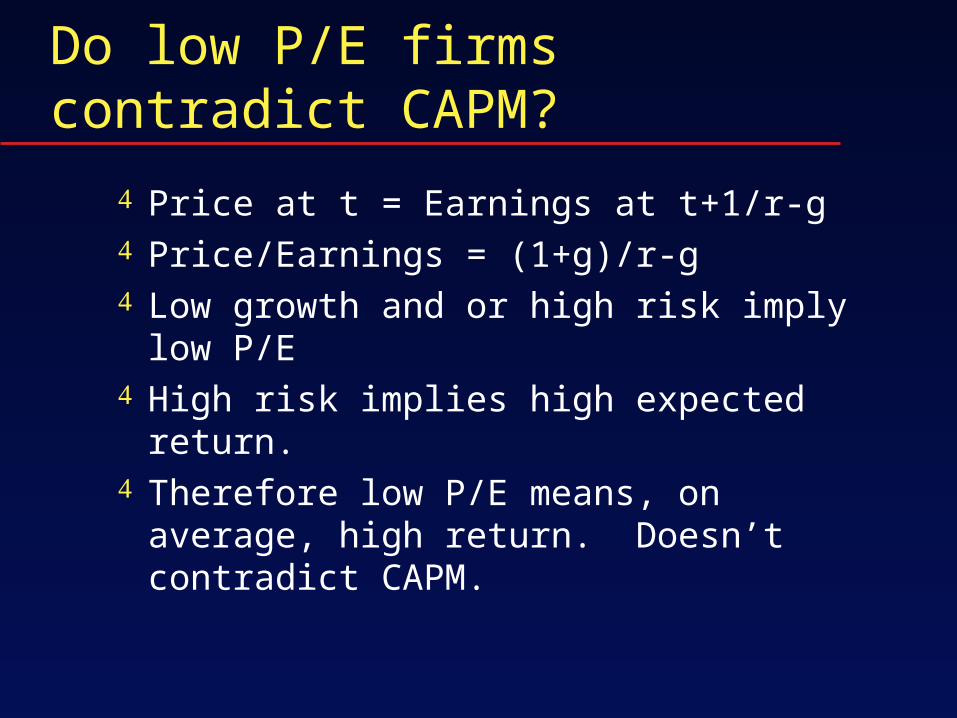

Do low P/E firms contradict CAPM?

Price at t = Earnings at t+1/r-g Price/Earnings = (1+g)/r-g Low growth and or high risk imply low

P/E High risk implies high expected return. Therefore low P/E means, on average,

high return. Doesn’t contradict CAPM.

How many assets in a diversified portfolio?

Not many. About 30 well-chosen ones.

Statman JFQA Sept 87

Diversification for an Equally Weighted Portfolio

Number of Securities

Systematicrisk

Total risk2

P

Unsystematicrisk

Investors need only two funds.

Figures 10.4, 10.5, and 10.6.

Diversification, minimum variance

E(R)

0 1

A

B

1

1MV

MV

MV

Diversification with a risk-free asset

E(R)

A=risk-free

asset

B

MV

Diversification, minimumvariance

E(R)

0 1

A

B

1

1MV

MV

MV

Capital Market LineExpected return

of portfolio

Standarddeviation of

portfolio’s return.

Risk-freerate (Rf )

M..

.Capital market line

.X

Y.

.In

diffe

renc

e cu

rve

preferred

Argument for the security market line

Only beta matters A mix of T-Bills and the market can

produce any beta. An asset with that beta is no better or

worse than the two-fund counterpart Hence it has the same return.

Security Market LineExpected returnon security (%)

Beta ofsecurity

Rm

Rf

1

M.

0.8

S.

Security market line (SML)

S is overvalued.Its price falls

T is undervalued.Its price rises

.T.

Review item

Asset A has a beta of .8. Asset B has a beta of 1.5. Consider a portfolio with weights .4 on

asset A and .6 on asset B. What is the beta of the portfolio?

Answer

Portfolio beta is .4*.8+.6*1.5 = 1.22. Work it out this way: DevP = .4 DevA + .6 Dev B E[DevP*DevM] = .4 E[DevA*DevM]

+ .6*E[DevB*DevM]. Divide by E[DevP squared].