Most Likely to Succeed | Leadership in the Fund Industry

24

Most Likely to Succeed: Leadership in the Fund Industry Robert Pozen Senior Lecturer, Harvard Business School Senior Fellow, Brookings Institution Theresa Hamacher, CFA President, NICSA November 17, 2011

-

Upload

nicsa -

Category

Economy & Finance

-

view

269 -

download

1

Transcript of Most Likely to Succeed | Leadership in the Fund Industry

Most Likely to Succeed:

Leadership in the Fund Industry

Robert Pozen

Senior Lecturer, Harvard Business School

Senior Fellow, Brookings Institution

Theresa Hamacher, CFA

President, NICSA

November 17, 2011

2

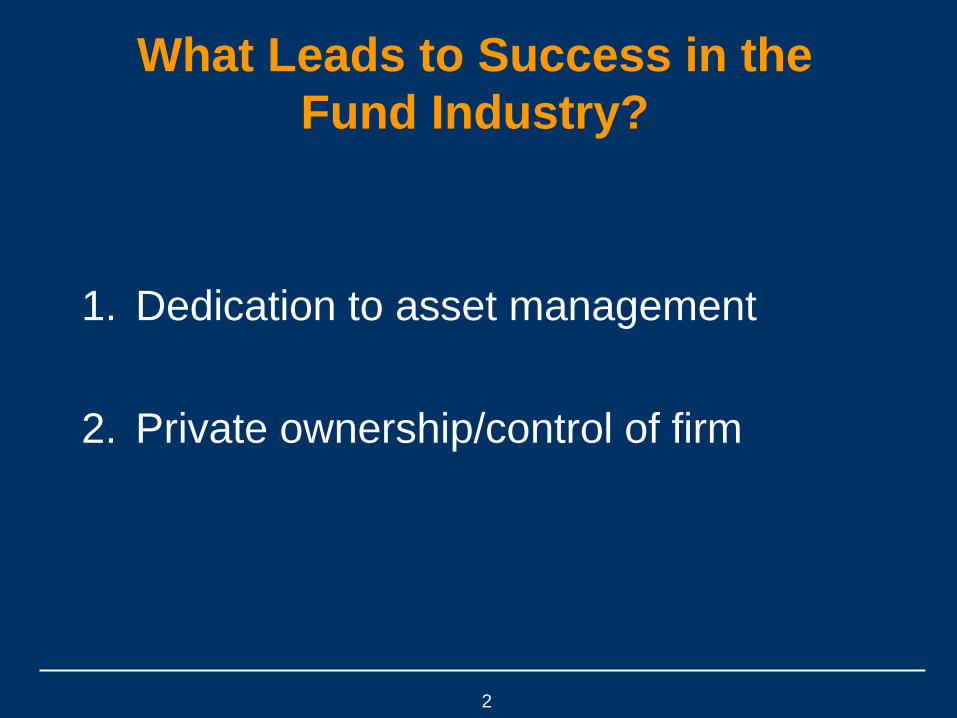

What Leads to Success in the

Fund Industry?

1. Dedication to asset management

2. Private ownership/control of firm

Agenda

• The evidence

─ Market share trends

─ M&A trends

• The limits of the financial supermarket

• The example of the Big Three

• The public–private model

3

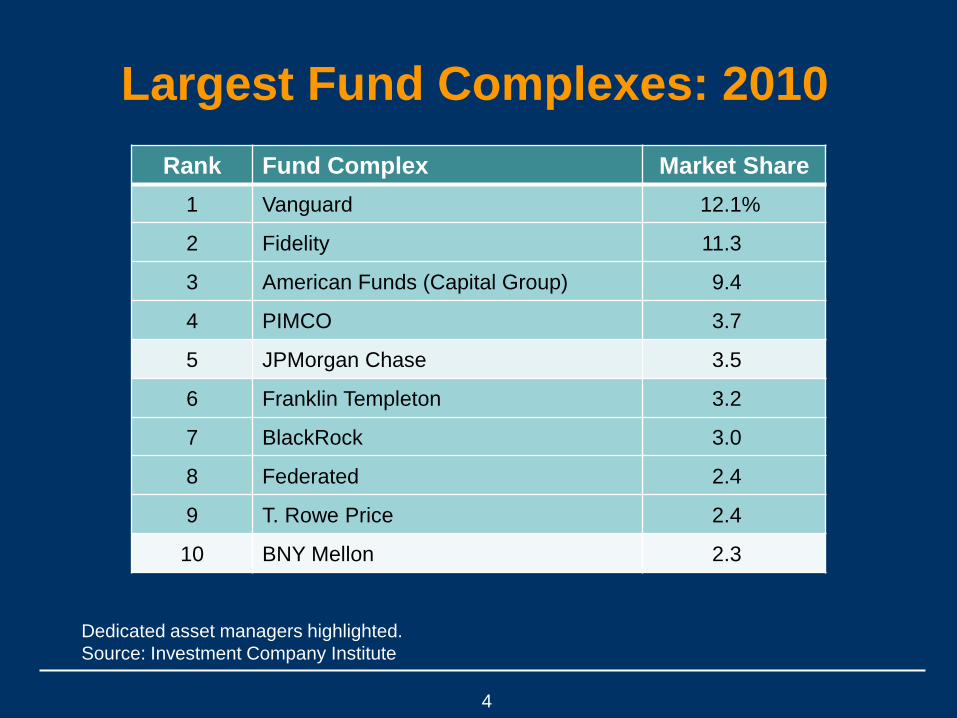

Largest Fund Complexes: 2010

4

Rank Fund Complex Market Share

1 Vanguard 12.1%

2 Fidelity 11.3

3 American Funds (Capital Group) 9.4

4 PIMCO 3.7

5 JPMorgan Chase 3.5

6 Franklin Templeton 3.2

7 BlackRock 3.0

8 Federated 2.4

9 T. Rowe Price 2.4

10 BNY Mellon 2.3

Dedicated asset managers highlighted.

Source: Investment Company Institute

Top 25 Fund Complexes

5

Source: Investment Company Institute

1990 2000 2010

Dedicated asset managers

Market share 39.8% 43.2% 55.3%

Number of firms 13 11 14

Total top 25 market share 76.2% 71.0% 73.6%

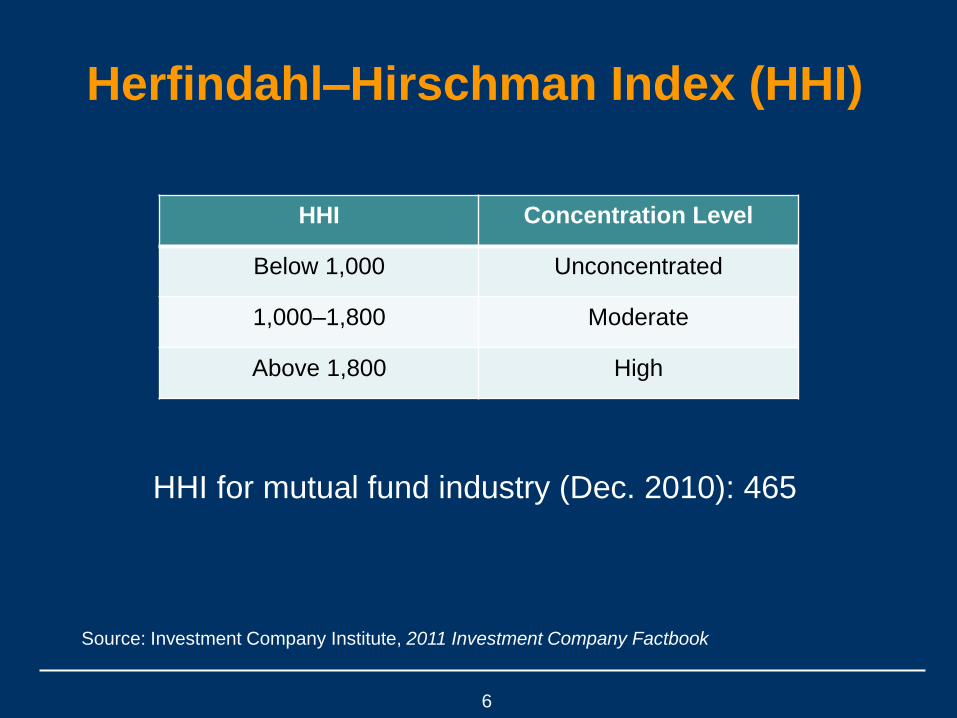

Herfindahl–Hirschman Index (HHI)

6

HHI Concentration Level

Below 1,000 Unconcentrated

1,000–1,800 Moderate

Above 1,800 High

HHI for mutual fund industry (Dec. 2010): 465

Source: Investment Company Institute, 2011 Investment Company Factbook

Top 10 Fund Complexes

Rank 1990 2000 2010

1 Fidelity Fidelity Vanguard

2 Merrill Lynch Vanguard Fidelity

3 IDS/Shearson American Funds American Funds

4 Dreyfus Putnam Funds PIMCO

5 Vanguard Morgan Stanley JPMorgan Chase

6 Franklin Janus Franklin Templeton

7 Federated Invesco BlackRock

8 Dean Witter Merrill Lynch Federated

9 Kemper Franklin Templeton T. Rowe Price

10 American Funds Smith Barney/Citi BNY Mellon

7

Firms new to the top 10 in 2000 and 2010 are highlighted.

Source: Investment Company Institute

Life Cycle of an Asset Manager

• Lots of new entrants

─ Low barriers to entry

─ Niche fund products

─ Other companies market and service

• Many new entrants close shop or stay small over the

next decade

• Successful firms get to tipping point

─ Develop full product line

─ Own marketing/servicing

─ Enter retirement space

• Or choose to be acquired

8

U.S. Fund Sponsor M&A($ billions)

9

Deals with a publicly disclosed value of $50 million or greater. Data for 2000–2010 are for all

asset managers, not just fund sponsors.

Sources: Merrill Lynch; Thomson Reuters information provided by Goldman Sachs.

Deal Valuations

10

Deals with a publicly disclosed value of $50 million or greater. Data are for all asset managers,

not just fund sponsors.

Source: Thomson Reuters information provided by Goldman Sachs.

Diversified Firms as Buyers1993–2001

• Banks and insurers acquire asset managers

─ Mellon/Dreyfus

─ Higher growth of earnings

─ Diversification of income

• European firms particularly active

─ Deutsche Bank/Zurich Scudder

─ Seeking global diversification

─ Most did not achieve major U.S. presence

─ Though there were exceptions: Invesco

11

Diversified Firms as Buyers1993–2001

• Brokerage firms expand proprietary fund families

─ Morgan Stanley acquires Van Kampen and MAS

─ Lehman/Neuberger

─ American Express/Threadneedle

• U.S. asset managers buy high-net-worth managers

─ Franklin/Fiduciary Trust, Alliance/Sanford Bernstein

─ Leverage investment skills

─ Add customized services

─ Invesco’s acquisition of AIM is an exception

12

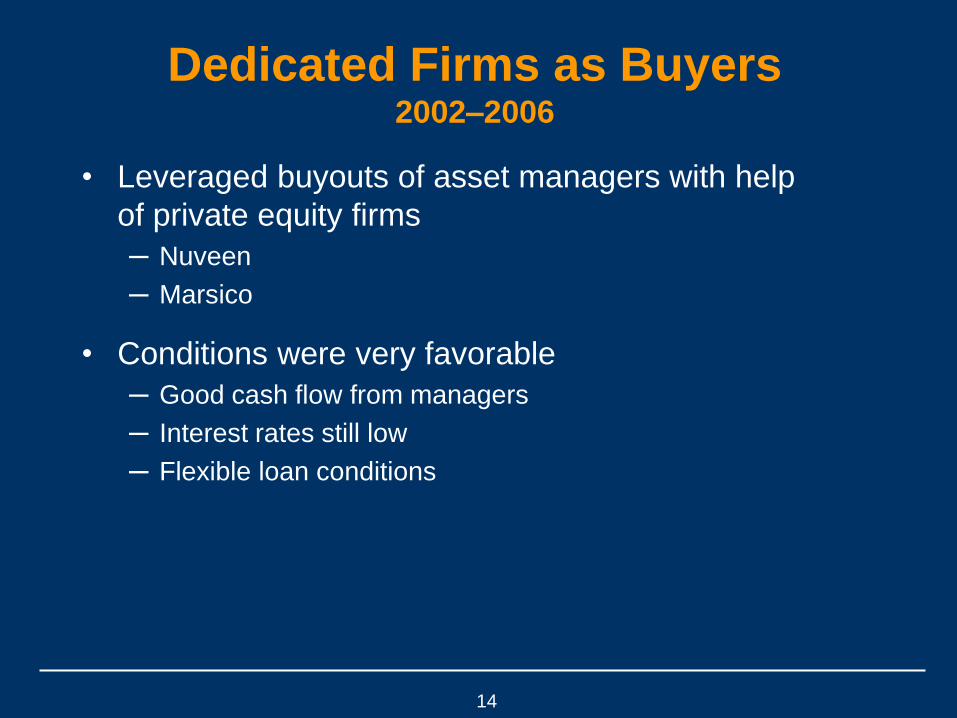

Dedicated Firms as Buyers2002–2006

• BlackRock and Legg Mason key buyers

─ BlackRock buys State Street Research, Quellos, and Merrill

Lynch unit

─ Legg Mason bought Private Capital, Permal, and Salomon

Smith Barney unit

• Focus on distribution by Merrill Lynch and Smith

Barney, not on fund management

─ Clients want choice of best funds

─ Regulatory scrutiny of conflicts

13

Dedicated Firms as Buyers2002–2006

• Leveraged buyouts of asset managers with help

of private equity firms

─ Nuveen

─ Marsico

• Conditions were very favorable

─ Good cash flow from managers

─ Interest rates still low

─ Flexible loan conditions

14

Credit Crisis–Driven Divestitures2007–2010

• Insurers in trouble sold asset managers

─ Marsh McLennan sold Putnam to Great West of Canada

─ AIG sold asset management arms to Bridge Partners

─ Lincoln National Life sold Delaware Management

to Macquarie (Australia)

• Brokers in trouble also sold asset management units

─ Lehman sold Neuberger Berman

─ Morgan Stanley sold Van Kampen to Invesco

15

Credit Crisis–Driven Divestitures2007–2010

• In U.S. and U.K., Treasury put heavy pressure on

large banks to accept federal capital along with

restrictions on dividends and executive

compensation

─ To help redeem federal capital, Bank of America

sold Columbia Management to Ameriprise

─ To help avoid taking government capital, Barclays

sold BGI, its asset management business, to BlackRock

16

Top 10: Dedicated vs. Diversified

2010

RankDedicated

1 Vanguard

2 Fidelity

3 American Funds

4 PIMCO

6 Franklin Templeton

7 BlackRock

8 Federated

9 T. Rowe Price

17

Highlighted firms have a strong money market fund base.

Source: Investment Company Institute

2010

RankDiversified

5 JPMorgan Chase

10 BNY Mellon

Limitations of the Financial

Supermarket

• Open architecture

─ Client demand

─ Regulatory scrutiny

• Challenges of cross-selling

─ Divergent customer bases

─ Training demands

• Retention of investment professionals

─ Culture

─ Compensation

• Volatility of investment performance

─ Difficult for public firms

18

The Big Three

19

Rank 1990 2000 2010

1 Fidelity Fidelity Vanguard

2 Vanguard Fidelity

3 American Funds American Funds

5 Vanguard

10 American Funds

Combined

share18.7% 25.1% 32.8%

Source: Investment Company Institute

The Example of the Big Three

• Organization

─ Non-hierarchical

─ Informal voice in key issues

• Compensation

─ Partners get stake in asset management business

─ Executives comfortable with PM compensation

• Privately held

─ No public reporting

─ Continuity of ownership (vs. generational transfers)

20

The Public–Private Hybrid

• Various forms

─ Dual share class: Federated

─ Concentrated ownership: Franklin Templeton, BlackRock,

T. Rowe Price

• Advantages

─ Valuation of stock options

─ Currency for acquisitions

─ Controlled by management

─ Long-term, investor culture

21

Top 10: Private and Hybrid

2010

RankPrivate

1 Vanguard

2 Fidelity

3 American Funds

22

2010

RankPublic–Private Hybrid

6 Franklin Templeton

7 BlackRock

8 Federated

9 T. Rowe Price

Role Reversal

1990–2000

From outsiders. . .

Diversified financial

firms

Banks

Insurers

Brokers

23

2010

. . . to insiders

Dedicated asset

managers

Majority of top 25

complexes

With majority of fund

assets

24

www.nicsa.org/thefundindustry