Monthly Market Outlook May 2020

113

1 Monthly Market Outlook May 2020

Transcript of Monthly Market Outlook May 2020

1

Monthly Market Outlook May 2020

2

3

Medical Crisis

Financial Crisis

Real Life Crisis

Past Financial Crisis

Unprecedented Times

Past Medical Crisis

SARSAvian influenzaEbolaZika

Harshad Mehta ScamAsian CrisisKetan Parekh ScamSubprime CrisisTaper TantrumDemonetization

3

4 4

5

Sector impact - Revenue Significantly Impacted but Costs continue

• Agricultural Produce• Telecom• FMCG• Food Processing • Online Education• Seeds & Fertilisers• Sugar

• Auto Ancillaries• Consumer Durables• Housing Finance Companies• Automobile OEMs• Logistics• Power• Electronics• Banks• Engineering• Mining• Real Estate ( Residential)• Financial Services• Healthcare &

Pharmaceuticals

• Aviation• Hotels & Tourism• Gems & Jewellery• Multiplexes• Microfinance Institution• Textiles ( Cotton Spinning)• Ports & Seafood• MSME• Retailing

Agility in running business to see through near term without loosing sight of the opportunities in the medium to long term

Please click here for our Sectoral Update Report – March 2020

Low Medium High

6

Economic Implication Of Lockdown

Description In $ ( Approximate)GDP $ 3000 Bn Monthly GDP Loss(a) 100% $ 250 Bn(a) 50% $ 125 Bn+ Cost of restart 45 Days Lockdown ( Assuming 50% activity is shut) $ 190 Bn + Cost of restartSavings Correction in Oil Prices $ 40 - 45 Bn Trade Deficit with China $ 20 Bn

Net Cost $ 130 Bn + Cost of restart

Approximately $130 Bn cost and economy restarting cost could be managed through Fiscal Stimulus + Monetary Stimulus + Foreign Direct Investment

Source: Internal Calculations

7

Nonetheless, India Has Low Leverage Risk Among EM’s

Selected Emerging economies ranked on four measures of financial strength

Source: EIU , JP Morgan , ishares , Economist , Central Banks

8

How The World Responded To Covid-19

Source: Oxford COVID-19 Government response tracker

Data as on 27th April 2020

Stringency index developed at the university of oxford scores the response by the Indian government to combat COVID-19 as ‘100’

9

Current Situation On Coronavirus Treatments Or Vaccines

86 Covid-19 vaccine under development

10

Likely Recovery Scenario

Medical Solution

Low

High V Shaped recovery L Shaped recovery

Reality will be between V and L

Fiscal &

Monetary stimulus

Early Late

11

Benefits for India Economy

Lower Oil Prices

Lower trade deficit with China

Fiscal Stimulus

Monetary Stimulus

- RBI rate cut – credit flow to economy could begin

Higher capital allocation from Global investors

FPI flows due to MSCI & FTSE

FDI through supply chain

Lower Global Interest Rates & Higher Liquidity can bring more capital allocation to India

Supply chain disruption companies coming from China to India

Global Crude Oil Prices Fall Due To COVID-19 Concerns

23.7

10

20

30

40

50

60

70

80

Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

Source: Bloomberg. Data as on 30th April 202012

13

Trade Deficit With China will reduce (~20 bn)

0

11

29

4547

52

58

0

10

20

30

40

50

60

70

2001 2008 2012 2015 2016 2017 2018

Trade Deficit with China ($ bn)

Source: Elara Securities

14

RBI Rate Cut – Credit Flow To Economy Will Begin

Source: Economic Times

15

RBI Takes Measures To Reduce The Cost Of Borrowings And Enhance Liquidity Into The System

Source: RBI, Spark Capital Research

Net liquidity in the system stood at Rs. 7.4 tn as of 29th Apr 20 10-year G-sec yield stood at 6.12% as of Apr’20The yield curve has been steepening led by excess liquidity in the system and fiscal pressure

RBI cuts the reserve repo rate by 25 bps from 3.75% in Apr’20 to 4% in Mar’20

CRR has been cut by 100 bps to 3% of NDTL in Mar’20 from the 4% earlier`

MCLR has increased by 5 bps to 8% in Mar’20 from 7.95% in Feb’20

16

Possible Fiscal Measures To Help Revive Economy

Support to Poor

Credit Guarantee Schemes to insure lending to business

Increase working capital limit for business

Capitalization of banking system

Increased spending on Infrastructure

Tax cuts to spur consumption

Trade off between reviving growth, rating downgrade and ability to raise resources to determine extent of fiscal stimulus

17

Central Bank Stimulus Has Eased Financial Stress To A Great Extent

Source: Bloomberg

Extraordinary central bank stimulus has eased financial stresses

The ECB’s balance sheet growsFed Balance Sheet tops $6tn for 1st time

6.7

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

No

v-0

5

No

v-0

6

Dec

-07

Dec

-08

Dec

-09

Jan

-11

Jan

-12

Jan

-13

Feb

-14

Feb

-15

Mar

-16

Mar

-17

Mar

-18

Ap

r-1

9

Ap

r-2

0

US Condition of All FederalReserve Banks Total Assets

($tn)

5347

0

1000

2000

3000

4000

5000

6000

Ap

r-0

6

Ap

r-0

7

Ap

r-0

8

Ap

r-0

9

Ap

r-1

0

Ap

r-1

1

Ap

r-1

2

Ap

r-1

3

Ap

r-1

4

Ap

r-1

5

Ap

r-1

6

Ap

r-1

7

Ap

r-1

8

Ap

r-1

9

Ap

r-2

0

Asset purchase programme has expanded massively

(Eur bn)

18

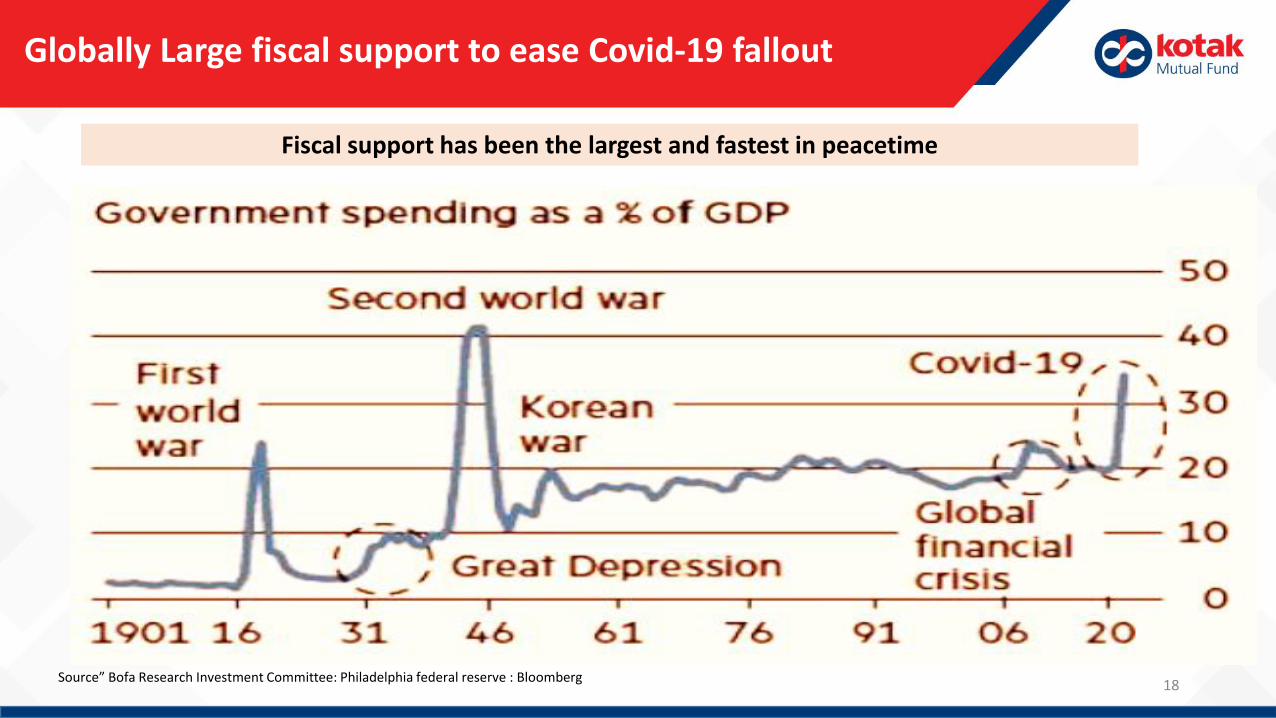

Globally Large fiscal support to ease Covid-19 fallout

Fiscal support has been the largest and fastest in peacetime

Source” Bofa Research Investment Committee: Philadelphia federal reserve : Bloomberg

19

Governments And Central Banks Are Taking Actions To Support The Economy Amid Downside Risks From Covid-19

Source: Kotak Institutional Equities

20

Governments And Central Banks Are Taking Actions To Support The Economy Amid Downside Risks From Covid-19..

Source: Kotak Institutional Equities

21

Indian Exporters Of Chemicals, Engineering Goods, And Marine Products Will Benefit The Most From The Coronavirus Outbreak

Source: Economic Times

22

Exit China Enter India ?

Negative views on China continue to grow in US

23

Recovery Path Ahead Post Lockdown -Lessons From China

China discretionary spend post lockdown remains at sub 50% levels

Source: Eagle Alpha; Chinese transport ministry; Marine Traffic; STR; Economist

24

Valuation

25

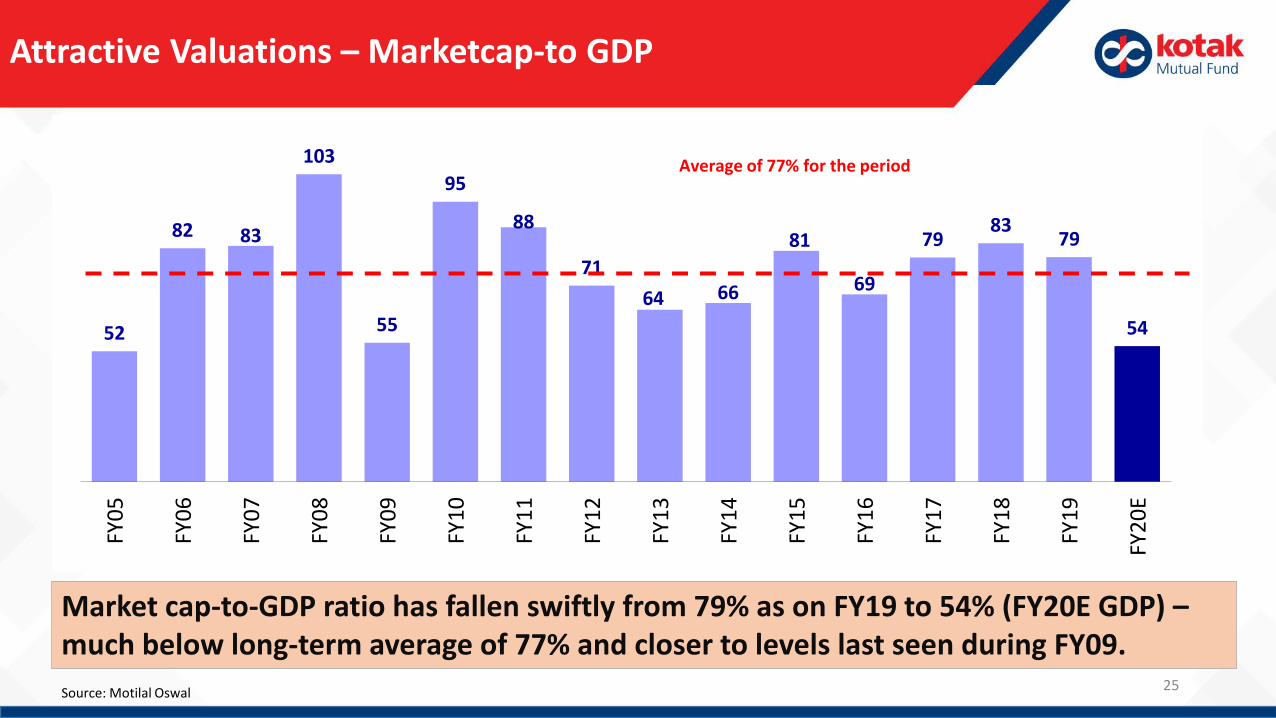

Attractive Valuations – Marketcap-to GDP

Source: Motilal Oswal

Market cap-to-GDP ratio has fallen swiftly from 79% as on FY19 to 54% (FY20E GDP) –much below long-term average of 77% and closer to levels last seen during FY09.

52

82 83

103

55

95

88

71

64 66

81

69

7983

79

54

FY0

5

FY0

6

FY0

7

FY0

8

FY0

9

FY1

0

FY1

1

FY1

2

FY1

3

FY1

4

FY1

5

FY1

6

FY1

7

FY1

8

FY1

9

FY2

0E

Average of 77% for the period

26

Attractive Valuations – P/B

NIFTY P/B (x) - 1 Year Forward NIFTY P/B (x) – Trailing

At 2.4x, the Nifty 12-month trailing P/B is well below the historical average of 3.0x.

At 2.2x, the Nifty 12-month forward P/B is also well below thehistorical average of 2.6x

Source: Motilal Oswal

2.4

1.5

2.5

3.5

4.5

5.5

Ap

r-0

5

Ap

r-0

6

Ap

r-0

7

Ap

r-0

8

Ap

r-0

9

Ap

r-1

0

Ap

r-1

1

Ap

r-1

2

Ap

r-1

3

Ap

r-1

4

Ap

r-1

5

Ap

r-1

6

Ap

r-1

7

Ap

r-1

8

Ap

r-1

9

Ap

r-2

0

Average: 3x

2.2

1.5

2.3

3.0

3.8

4.5

Ap

r-0

5

Ap

r-0

6

Ap

r-0

7

Ap

r-0

8

Ap

r-0

9

Ap

r-1

0

Ap

r-1

1

Ap

r-1

2

Ap

r-1

3

Ap

r-1

4

Ap

r-1

5

Ap

r-1

6

Ap

r-1

7

Ap

r-1

8

Ap

r-1

9

Ap

r-2

0

Average: 2.6x

27

Attractive Valuations – P/B

Source: Bloomberg, Internal Calculations

% of Top 1000 stocks by market cap trading below 1x P/B

74%

49%41%

43%

36%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Apr 00 Apr 02 Apr 04 Apr 06 Apr 08 Apr 10 Apr 12 Apr 14 Apr 16 Apr 18 Apr 20

28

Equity Markets Are Doing A Time Travel To Past

Source: Capital Line , Internal Calculations

9860

13502

4078

0

5000

10000

15000

20000

25000

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Jul-

13

Oct

-13

Jan

-14

Ap

r-1

4

Jul-

14

Oct

-14

Jan

-15

Ap

r-1

5

Jul-

15

Oct

-15

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

Jan

-17

Ap

r-1

7

Jul-

17

Oct

-17

Jan

-18

Ap

r-1

8

Jul-

18

Oct

-18

Jan

-19

Ap

r-1

9

Jul-

19

Oct

-19

Jan

-20

Ap

r-2

0

Nifty 50 Nifty Midcap 100 Nifty Smallcap 100

Nifty50 at 2017 levelsNifty Midcap100 at 2015 LevelsNifty Smalcap100 at 2010 Levels

Market Performance

29

Market Snapshot

Source: Axis Capital , Bloomberg,

Dec-07 May-13 Apr-20 Dec-07 May-13 Apr-20

Macro Indicators 10-Year Govt Bond Yield

Capacity Utilisation (Dec 19) 91.7% 71.6% (Jun-13) 68.6% India 7.8% 7.2% 6.1%

Credit Growth (as on Mar 20) 22.0% 14.4% 6.1% USA 4.0% 2.1% 0.6%

ROE Nifty 50 (Apr 20) 25.5% 17.1% (Mar-13) 14.0% Japan 1.5% 0.9% 0.0%

Net FII Flows (12M - Rs. Cr – Apr 20) 71,952 125,110 -21,015 Europe 4.3% 1.5% -0.6%

IIP – Feb 20 13.5% 1.0% 4.5% China 4.5% 3.4% 2.5%

GDP Growth (Oct – Dec 19) 9.6% 6.4% 4.7%

Dec-07 May-13 Apr-20 Dec-07 May-13 Apr-20

Valuations Returns of Nifty 50 (CAGR)

Trailing P/E Nifty 50 27.6 18.0 22.4 Last 1 Yr Return 54.8% 21.6% -16.1%

Trailing P/B Nifty 50 6.4 3.2 2.8 Last 2 Yr Return 47.1% 3.8% -4.2%

Last 3 Yr Return 43.4% 5.6% 2.0%

30

*As on 30 April 2020, Source: Axis Capital, Bloomberg, Past Performance may or may not sustain in the future

Performance Across Market Cap

31

32

Gauge To View Market Sentiment

15

46

54

49

40 1 0 0

2

54

9

0

40

29

13

3

23

48

36

66

40

40 0 0

36

21 22

63

5

0 0

65

47

81

40 0 0 0 0 0 0

13

57

7

0 00

10

20

30

40

50

60

70

80

90

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Nifty Index NSE Midcap 100 NSE Smallcap 100

Number of New All Time Highs

Source: Axis Capital

Drawdown from 52 Week HighNo. of Stocks

% of Top 1000

stocks

Less than 10% 40 4%

Between 10% and 20% 66 7%

Between 20% and 30% 128 13%

Between 30% and 50% 427 43%

More than 50% 328 34%

Median Correction from 52 Week High by Market Cap

Top 10 -20%

10 to 100 -30%

100 to 500 -39%

500 to 1000 -48%

Overall : Top 1000 -28%

Small And Mid Cap Corrected Significantly

Source: Axis Capital, Bloomberg, As on 30 April2 020 33

Drawdown fromDrawdown from

52 week highDrawdown

from Jan 2018

Nifty 50 -21% -11%

Nifty Midcap 100 -27% -35%

Nifty Smallcap 100 -39% -54%

34

FPI Flows Trend May Reverse - Post MSCI And FTSE Russel Index Rejig

Source: Morgan Stanley

MSCI + FTSE India Potential Passive Inflow of US$6.4 bn this year

Possible index impact for FTSE is likely in June 2020 and MSCI is likely in August 2020

Earliest possible flows impact ( US$ bn)

Jun-20 Aug-20 Sep-20 Nov-20 Dec-20 Total

MSCI - net - 3.09 - 0.51 - 3.6

FTSE - net 2.16 - 0.6 - 0.04 2.8

Total - net 2.16 3.09 0.6 0.51 0.04 6.4

MSCI - gross - 5.09 - 0.51 - 5.6

FTSE - gross 2.66 - 0.60 - 0.04 3.26

Total - gross 2.66 5.09 0.60 0.51 0.04 8.86

Time to Be Over Weight on Equities in staggered manner

35

36

Buying Into The Mayhem Made Sense In The Past

Source: Motilal Oswal & Internal analysis

Past performance may or may not be sustained in future

Nifty50 Performance (%)

Date (MM-YY) Peak Trough Peak to Trough +1M +3M +6M +12M

Jun 96 -Dec 96 13/06/1996 04/12/1996 -33% 18% 42% 35% 28%

Aug97-Jan 98 05/08/1997 29/01/1998 -26% 13% 22% -3% 3%

Apr98-Nov 98 02/04/1998 28/11/1998 -30% 9% 16% 35% 73%

Feb 00-May 2000 11/02/2000 23/05/2000 -30% 22% 12% 1% -4%

Feb 01-Sep 01 15/02/2001 21/09/2001 -40% 14% 24% 35% 14%

Jan04-May 04 14/01/2004 17/05/2004 -30% 8% 15% 35% 43%

May06-June 06 10/05/2006 14/06/2006 -30% 19% 29% 46% 58%

Jan 08-Oct 08 08/01/2008 27/10/2008 -60% 9% 6% 38% 92%

Nov 10-Dec 11 05/11/2010 20/12/2011 -28% 10% 16% 13% 30%

May- Aug 2013 17/05/2013 28/08/2013 -15% 10% 15% 17% 51%

Mar 15 to Feb 16 03/03/2015 25/02/2016 -23% 11% 14% 24% 28%

Aug 18 to Oct 18 28/08/2018 26/10/2018 -15% 5% 8% 17% 15%

Jan 20 to Mar 20 14/01/2020 23/03/2020 -38% 22% ? ? ?

37

Earlier Epidemics Such As SARS, EBOLA And ZICA Does Suggest That Medical Science Will Find Out A Solution Sooner Than Later

Source : Bloomberg , Mint Research and Intrenal Calculations

Do Not Convert Notional Loss To Real Loss

Virus OutbreakEstimated Period of

OutbreakReturns during

Outbreak1-Year return post

outbreak

SARS Jan to Mar 2003 -10.07 83.38

Avian influenza Jan to Aug 2004 -12.23 50.33

Ebola Dec 2013 to Feb 2014 1.58 39.02

Zika Nov 2015 to Feb 2016 -13.14 24.14

Covid-19 14 Jan 20 to 23 Mar 20 -38.44 ?

38

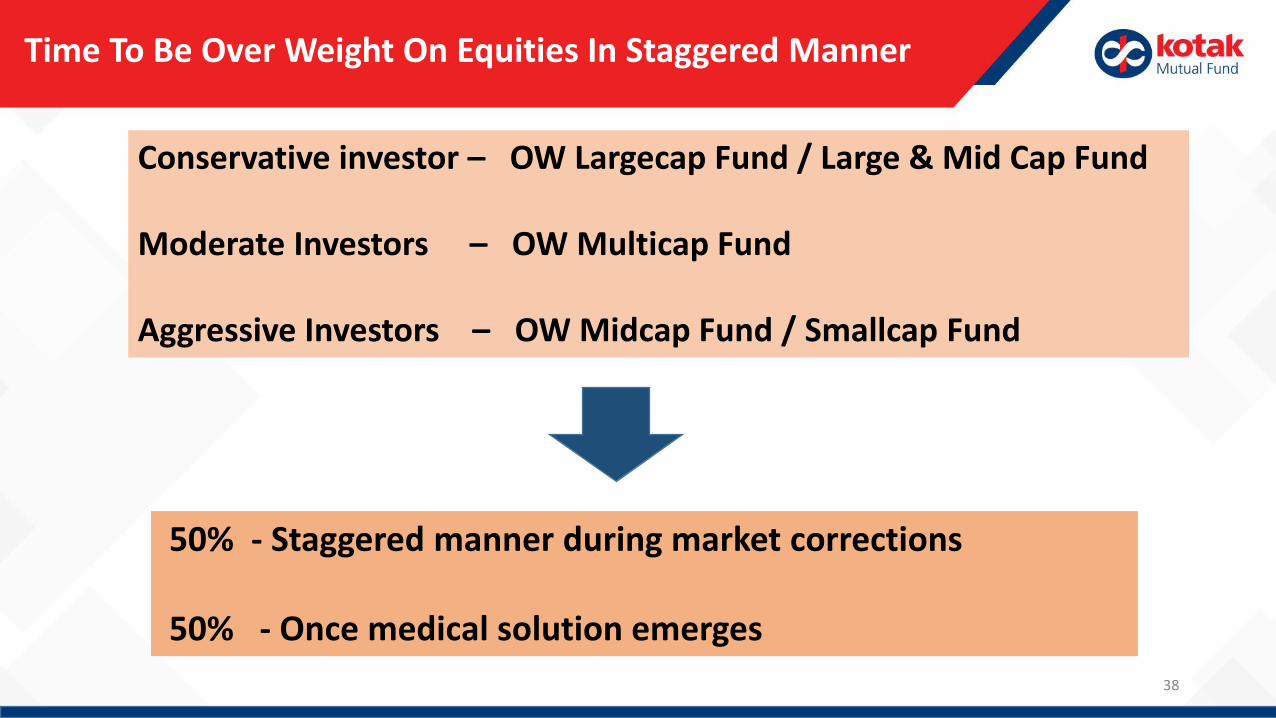

Time To Be Over Weight On Equities In Staggered Manner

Conservative investor – OW Largecap Fund / Large & Mid Cap Fund

Moderate Investors – OW Multicap Fund

Aggressive Investors – OW Midcap Fund / Smallcap Fund

50% - Staggered manner during market corrections

50% - Once medical solution emerges

Equity Hybrid Fund

Largecap Fund

Multicap Fund

Midcap Fund

Smallcap Fund

Time To Play On Front Foot ( Cautiously)

39Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Please consult your financial advisor or investment professional for investment decisions.

Time To Notch Up The Risk Appetite One At A Time

• It has been our long ongoing call that Mid & Small Cap category positioned better in terms of valuation over Large Cap

• With the recent Coronavirus scare, some of the valuations in Mid & Small cap has become more attractive, both in relation to the largecaps and vis-à-vis its own historical average.

• Thus, a portfolio with a mix exposure of large & mid is better suited to gain from this upside than an only large cap portfolio.

• For an investor with a moderately high risk appetite, one can choose to invest in:

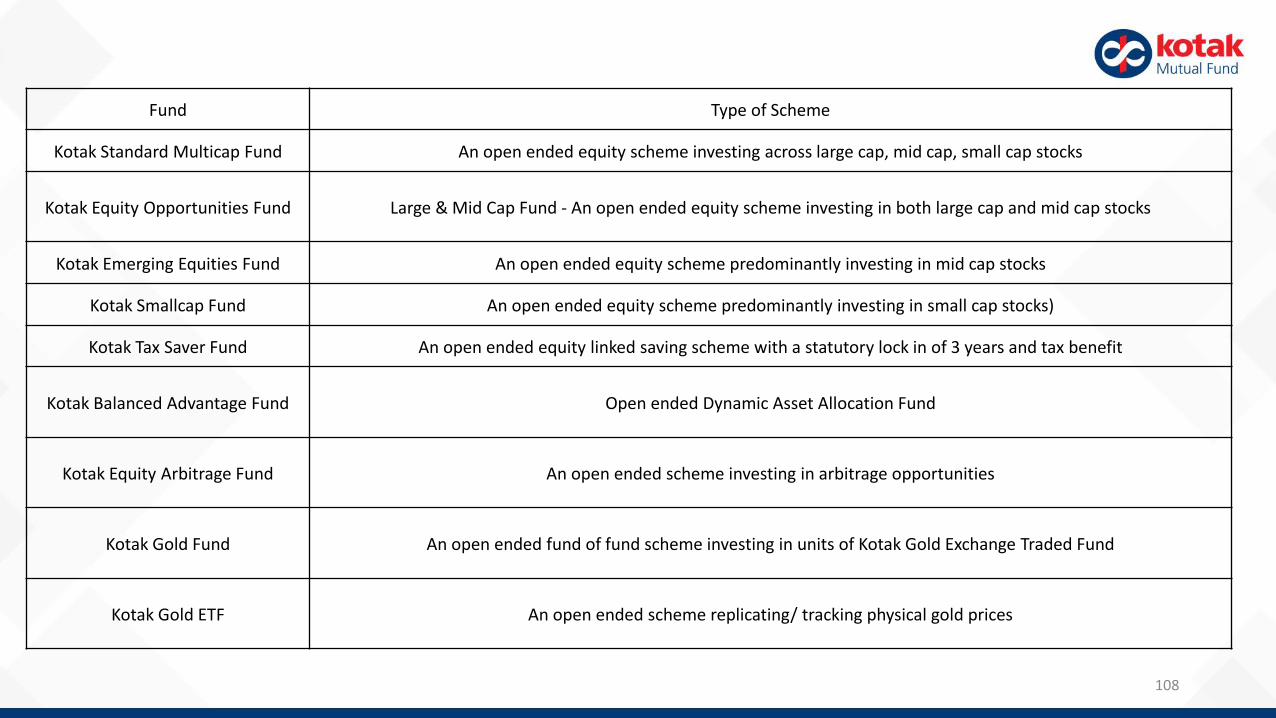

• Kotak Equity Opportunities Fund - Large & Mid Cap Fund - An open ended equity scheme investing in both large cap and mid cap stocks

• Kotak Equity Opportunities Fund has increased its exposure in mid-cap category to take advantage of attractive valuations

Latest Valuation Estimates Nifty 50 Nifty Midcap 50

Price to Book Ratio 2.38 1.53Price to Sales Ratio 1.73 1.34

Price Earnings Ratio (P/E) 19.42 21.65

Historical Valuation Average* Nifty 50 Nifty Midcap 50

Price to Book Ratio 2.60 1.86

Price to Sales Ratio 1.96 1.64

Price Earnings Ratio (P/E) 21.91 27.09

* Average of last 10 years data until Feb 2020Source: Bloomberg

Market Correction Provides Opportunity to Upgrade from Largecap to Large & Midcap

Date Large Cap Mid Cap Small Cap

Apr-20 46.61% 42.08% 4%

Mar-20 46.90% 41.42% 4.45%

Source: MFi Explorer51

40

41

Is It Time To Switch From Value/Contra Category To Mid & Small?

Market Size of Two Categories (Rs in Cr as of Mar 2020)Net Inflows in the mutual Fund Category (in Rs Cr as of Mar 20)

Old investments are Flowing Out of Contra-Value Segment. Midcap & Small-cap segment may provide an alternative for this money

Data Source: Morningstar.

Kotak Balanced Advantage Fund – Asset AllocationEpisodes in last 21 months where we have demonstrated discipline and agility

Kotak Balanced Advantage Fund benefitted by investing when cheap and selling when expensive. Thus, when Nifty was flat, asset allocation helped earn returns.

Source: Internal Analysis. As on 30th April 2020. Disclaimer: Past Performance is not a guarantee for future return. Mutual fund investments are subject to market risks, read all scheme related documents carefully. Please refer to slide number 106, 107 and 108 for detailed performance of the fund. . Please click here for performance disclaimers

42

84

101

60

70

80

90

100

110

Nifty 50 Index Value( Rebased to100) K-BAF NAV (Rebased to 100)

K-BAF NAV (Rebased to 100)

Nifty 50 Index Value (Rebased to 100)

10198

1064111157

11597 11600

12053

7610.25

9859.9

51.2

35.8 34.6 29.9

48.9

37.9

79.0 74.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

7000

8000

9000

10000

11000

12000

Aug-18 Oct-18 Nov-18 Dec-18 Feb-19 Mar-19 Apr-19 Jun-19 Jul-19 Aug-19 Oct-19 Nov-19 Dec-19 Feb-20 Mar-20 Apr-20

Nifty 50 KBAF Net Equity

Nifty 50 Index Value (LHS)

K-BAF Net Equity (RHS)

42

Kotak Equity Arbitrage – Market Volatility May Help Performance Potential

• The roll spread (annualized) on the arbitrage book is approximately 5.40%. We have increased our proportion incash future Arbitrage to 70.86% as rollover spreads were better than average. The rest 29.14% of corpus is investedin FDs, debt and money market instruments.

• On the last day of April series, market-wide rollovers stands high at 90% (vs. average rollovers of 84% seen in lastthree series). Stock futures rollovers also stands high at 93% (vs. average rollovers of 88% seen in last three series).

• Going forward allocation to Arbitrage book may remain high as post the rate cuts arbitrage book may offer a betterreturn compared to debt.

• On the debt side, we continue to run a conservative portfolio as far as credit and duration are concerned. Investorsneed to analyze the debt component of arbitrage funds and evaluate if higher returns are a function of credit orduration risk.

43

30

61

0

10

20

30

40

50

60

70

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Jan-1

0

Jan-1

1

Jan-1

2

Dec-1

2

Dec-1

3

Dec-1

4

Dec-1

5

Dec-1

6

Dec-1

7

Dec-1

8

Dec-1

9

SIPS stopped at Mkt Falls Simple SIP

Even with Assumption of Perfect Information, SIP Start-Stop Strategy may be Sub-optimal vis-à-vis Regular SIP

Regular SIP Investor Stopping SIP at FAlls

SIP amount 5000/- 5000/-

Total money invested through SIP 12,00,000 6,95,000

Amount saved by stopping SIP in market Falls N.A 5,05,000

Corpus at end of Dec-19 Rs 60.83 lakhs Rs 29.67 lakhs

Performance in XIRR (%) 14.29% 13.12%

There were 15 cycles market cycles when the index fell by 10% or more since 2000-19. Above assumes the Investors stops SIP at the cycle beginning and restarts at cycle bottom. 44

Volatile Market Conditions Impact Your SIP Returns In the Short-Term, Generally Over the Long-Term SIP investments deliver returns

Ups & Downs in the market helps to reduce the overall cost of SIP investments

For A SIP Investor, Volatility Is Your Friend

Please consult your financial advisor or other professionals before acting on any information in this communication.

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

45

Kotak Emerging Equity Fund SIP Returns

Source: MFi Explorer. As on 30 April 2020. Returns are for regular plan. Nifty Midcap 100 TRI is the benchmark for Kotak Emerging Equity FundDisclaimer: SIP is an optional feature offered by Kotak Mutual Fund. This feature does not in any way give assurance of the performance of any of the Funds of Kotak Mutual. Past performance may or may not be sustained in the future. The returns are calculated by XIRR approach assuming investment of Rs. 10,000/- on the 1st working day of every month. XIRR helps in calculating return on investments given an initial and final value and a series of cash inflows and outflows and taking the time of investment into consideration. Since inception returns are assumed to be starting from the beginning of the subsequent month from the date of inception. Please consult your financial advisor or other professionals before acting on any information in this communication. 46

Kotak Emerging Equity Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 16.59 16.78 16.46 14.71 14.37 15.25 15.63 15.81 15.74 16.77 15.67 9.24 11.38

7 Yr 17.15 17.50 16.94 14.24 13.62 14.85 15.33 15.53 15.33 16.81 15.06 5.29 8.31

5 yr 10.76 11.06 10.25 6.50 5.73 7.69 8.52 8.97 8.88 11.19 8.89 -4.54 0.16

3 yr 5.21 6.34 5.38 -0.41 -1.13 2.53 4.31 5.38 5.28 9.10 5.26 -16.04 -8.23

1 yr 2.31 9.04 8.37 -6.96 -6.68 6.33 11.66 14.23 13.93 26.63 13.16 -41.26 -21.05

Benchmark Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 12.50 12.60 12.09 9.97 9.50 9.77 10.52 10.81 10.52 11.34 9.91 2.89 5.56

7 Yr 12.88 13.18 12.35 9.19 8.43 8.76 9.83 10.20 9.70 10.87 8.67 -1.76 2.03

5 yr 7.98 8.28 7.19 2.83 1.88 2.57 4.20 4.87 4.32 6.11 3.17 -11.05 -5.43

3 yr 2.39 3.25 1.47 -5.49 -6.64 -5.17 -2.13 -0.74 -1.56 1.39 -3.33 -24.95 -15.87

1 yr -4.93 1.10 -1.65 -18.41 -18.53 -11.19 -1.38 3.44 2.42 13.11 -0.97 -51.01 -28.60

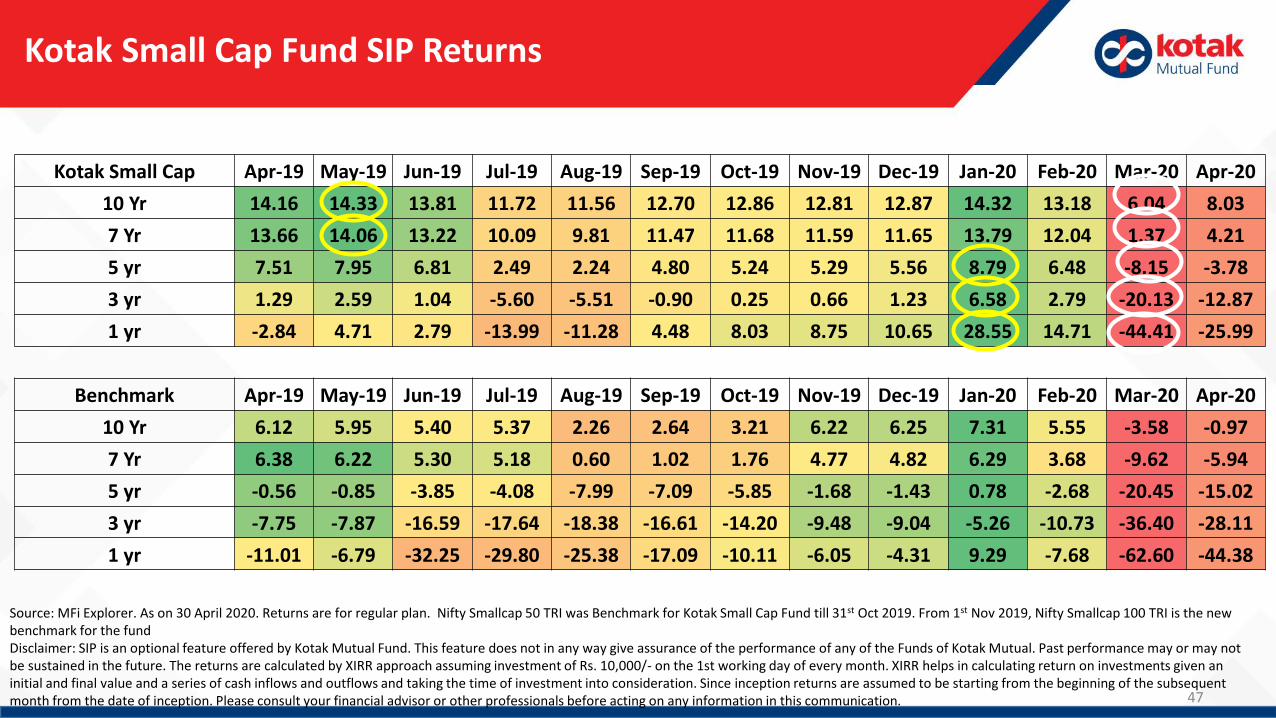

Kotak Small Cap Fund SIP Returns

Source: MFi Explorer. As on 30 April 2020. Returns are for regular plan. Nifty Smallcap 50 TRI was Benchmark for Kotak Small Cap Fund till 31st Oct 2019. From 1st Nov 2019, Nifty Smallcap 100 TRI is the new benchmark for the fundDisclaimer: SIP is an optional feature offered by Kotak Mutual Fund. This feature does not in any way give assurance of the performance of any of the Funds of Kotak Mutual. Past performance may or may not be sustained in the future. The returns are calculated by XIRR approach assuming investment of Rs. 10,000/- on the 1st working day of every month. XIRR helps in calculating return on investments given an initial and final value and a series of cash inflows and outflows and taking the time of investment into consideration. Since inception returns are assumed to be starting from the beginning of the subsequent month from the date of inception. Please consult your financial advisor or other professionals before acting on any information in this communication. 47

Kotak Small Cap Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 14.16 14.33 13.81 11.72 11.56 12.70 12.86 12.81 12.87 14.32 13.18 6.04 8.03

7 Yr 13.66 14.06 13.22 10.09 9.81 11.47 11.68 11.59 11.65 13.79 12.04 1.37 4.21

5 yr 7.51 7.95 6.81 2.49 2.24 4.80 5.24 5.29 5.56 8.79 6.48 -8.15 -3.78

3 yr 1.29 2.59 1.04 -5.60 -5.51 -0.90 0.25 0.66 1.23 6.58 2.79 -20.13 -12.87

1 yr -2.84 4.71 2.79 -13.99 -11.28 4.48 8.03 8.75 10.65 28.55 14.71 -44.41 -25.99

Benchmark Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 6.12 5.95 5.40 5.37 2.26 2.64 3.21 6.22 6.25 7.31 5.55 -3.58 -0.97

7 Yr 6.38 6.22 5.30 5.18 0.60 1.02 1.76 4.77 4.82 6.29 3.68 -9.62 -5.94

5 yr -0.56 -0.85 -3.85 -4.08 -7.99 -7.09 -5.85 -1.68 -1.43 0.78 -2.68 -20.45 -15.02

3 yr -7.75 -7.87 -16.59 -17.64 -18.38 -16.61 -14.20 -9.48 -9.04 -5.26 -10.73 -36.40 -28.11

1 yr -11.01 -6.79 -32.25 -29.80 -25.38 -17.09 -10.11 -6.05 -4.31 9.29 -7.68 -62.60 -44.38

Kotak Equity Opportunities Fund SIP Returns

Source: MFi Explorer. As on 30 April 2020. Returns are for regular plan. Nifty 200 TRI is the benchmark for Kotak Equity Opportunities FundDisclaimer: SIP is an optional feature offered by Kotak Mutual Fund. This feature does not in any way give assurance of the performance of any of the Funds of Kotak Mutual. Past performance may or may not be sustained in the future. The returns are calculated by XIRR approach assuming investment of Rs. 10,000/- on the 1st working day of every month. XIRR helps in calculating return on investments given an initial and final value and a series of cash inflows and outflows and taking the time of investment into consideration. Since inception returns are assumed to be starting from the beginning of the subsequent month from the date of inception. Please consult your financial advisor or other professionals before acting on any information in this communication. 48

Kotak Equity Opportunities

Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 13.64 13.72 13.18 11.96 11.76 12.36 12.80 13.07 13.15 13.71 12.42 7.09 9.26

7 Yr 14.46 14.63 13.70 11.80 11.41 12.23 12.80 13.14 13.18 13.93 11.92 3.91 7.00

5 yr 11.36 11.53 10.30 7.67 7.21 8.55 9.48 10.11 10.32 11.54 8.85 -2.20 2.49

3 yr 9.55 10.02 7.92 3.60 3.07 5.49 7.24 8.38 8.58 10.47 5.82 -12.05 -4.31

1 yr 12.24 15.51 10.16 -1.69 -1.32 7.66 13.03 15.73 16.31 22.39 7.20 -37.53 -16.86

Benchmark Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 12.22 12.26 11.91 10.60 10.36 10.93 11.52 11.61 11.57 11.29 9.92 4.66 7.20

7 Yr 13.23 13.33 12.68 10.67 10.22 10.98 11.78 11.87 11.73 11.25 9.15 1.34 4.99

5 yr 11.46 11.59 10.79 8.04 7.53 8.82 10.07 10.35 10.29 9.69 6.86 -3.91 1.47

3 yr 11.68 11.83 10.31 5.51 4.69 6.85 8.94 9.26 8.83 7.51 2.56 -14.70 -6.02

1 yr 10.29 12.44 8.75 -4.04 -4.17 4.45 11.66 12.40 11.89 8.82 -4.78 -43.76 -21.21

Kotak Standard Multicap Fund SIP Returns

Source: MFi Explorer. As on 30 April 2020. Returns are for regular plan. Nifty 200 TRI is the benchmark for Kotak Standard Multicap FundDisclaimer: SIP is an optional feature offered by Kotak Mutual Fund. This feature does not in any way give assurance of the performance of any of the Funds of Kotak Mutual. Past performance may or may not be sustained in the future. The returns are calculated by XIRR approach assuming investment of Rs. 10,000/- on the 1st working day of every month. XIRR helps in calculating return on investments given an initial and final value and a series of cash inflows and outflows and taking the time of investment into consideration. Since inception returns are assumed to be starting from the beginning of the subsequent month from the date of inception. Please consult your financial advisor or other professionals before acting on any information in this communication. 49

Kotak Standard Multicap

Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr NA NA NA NA NA 14.43 14.80 14.90 14.78 14.81 13.53 8.10 10.20

7 Yr 16.47 16.97 16.14 13.97 13.41 14.31 14.76 14.84 14.54 14.50 12.50 4.31 7.31

5 yr 13.01 13.66 12.58 9.57 8.88 10.38 11.16 11.45 11.22 11.33 8.70 -2.56 2.02

3 yr 11.51 12.81 10.97 5.97 5.06 7.76 9.24 9.76 9.18 9.16 4.62 -13.46 -5.92

1 yr 12.77 18.36 13.52 -0.52 -1.10 8.90 13.69 14.67 13.18 13.62 0.14 -42.26 -22.50

Benchmark Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 12.22 12.26 11.91 10.60 10.36 10.93 11.52 11.61 11.57 11.29 9.92 4.66 7.20

7 Yr 13.23 13.33 12.68 10.67 10.22 10.98 11.78 11.87 11.73 11.25 9.15 1.34 4.99

5 yr 11.46 11.59 10.79 8.04 7.53 8.82 10.07 10.35 10.29 9.69 6.86 -3.91 1.47

3 yr 11.68 11.83 10.31 5.51 4.69 6.85 8.94 9.26 8.83 7.51 2.56 -14.70 -6.02

1 yr 10.29 12.44 8.75 -4.04 -4.17 4.45 11.66 12.40 11.89 8.82 -4.78 -43.76 -21.21

Kotak Tax Saver Fund SIP Returns

Source: MFi Explorer. As on 30 April 2020. Returns are for regular plan. Nifty 500 TRI is the benchmark for Kotak Tax Saver FundDisclaimer: SIP is an optional feature offered by Kotak Mutual Fund. This feature does not in any way give assurance of the performance of any of the Funds of Kotak Mutual. Past performance may or may not be sustained in the future. The returns are calculated by XIRR approach assuming investment of Rs. 10,000/- on the 1st working day of every month. XIRR helps in calculating return on investments given an initial and final value and a series of cash inflows and outflows and taking the time of investment into consideration. Since inception returns are assumed to be starting from the beginning of the subsequent month from the date of inception. Please consult your financial advisor or other professionals before acting on any information in this communication. 50

Kotak Tax Saver Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 12.84 13.14 12.94 11.42 10.99 11.74 12.13 12.33 12.37 12.84 11.59 6.12 8.30

7 Yr 13.99 14.48 14.09 11.77 11.06 12.10 12.63 12.90 12.89 13.55 11.63 3.47 6.59

5 yr 11.32 11.89 11.35 8.04 7.04 8.64 9.43 9.92 10.03 11.06 8.46 -2.82 1.87

3 yr 10.16 11.32 10.42 4.90 3.49 6.36 7.88 8.78 8.77 10.28 5.74 -12.52 -4.82

1 yr 13.78 18.82 16.53 0.18 -2.23 7.98 12.57 14.30 14.38 19.27 4.80 -39.77 -19.67

Benchmark Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20

10 Yr 12.18 12.23 11.83 10.45 10.20 10.80 11.37 11.46 11.42 11.27 9.92 4.52 7.03

7 Yr 13.19 13.30 12.58 10.47 10.01 10.81 11.59 11.67 11.54 11.24 9.16 1.14 4.74

5 yr 11.11 11.24 10.35 7.46 6.94 8.27 9.50 9.75 9.71 9.38 6.58 -4.47 0.84

3 yr 10.71 10.91 9.23 4.25 3.43 5.69 7.76 8.09 7.73 6.87 2.01 -15.61 -7.02

1 yr 8.86 11.44 7.56 -5.51 -5.51 3.50 10.63 11.43 11.16 9.53 -3.97 -44.09 -21.81

51

Should We Invest In Gold ?

Gold Corrected In 2008 From June To Sept 2008 And Than Rallied To Life Time High As Central Banks Cut Interest Rates And Pumped Liquidity

Gold correction

in 2008

Fall in Gold

prices

Life time High

Source: Bloomberg 52

53

Debt Market Outlook April 2020

54

Whatever It Takes From RBI– Measures Will Keep Coming Till Economy Stabilizes. Have Patience For Medicine To Work

Monetary Initiatives Measures Impact

Rate Cut75bps repo cut to 4.40%

Bring down short term yield starting from Sov and gradually gets transmitted to Credits, leading to spread compression

Cut the reverse repo rate by 115 bps to 3.75%Disincentive banks from parking the surplus liquidity with the RBI

TLTRO (1.0)Targeted long-term repo operations for securities up to three years for a total amount of Rs 1 lakh crore. These will be issued at a floating rate linked to the benchmark repo rate

This could help in offsetting in part the adverse impact of the fiscal slippage in the offing

TLTRO (2.0)

Conduct targeted long-term repo operations (TLTRO 2.0) for an aggregate amount of Rs500 bn in tranches of appropriate sizes. The funds availed by banks under TLTRO 2.0 should be invested in investment grade bonds, commercial paper, and non-convertible debentures of NBFCs, with atleast50% of the total amount availed going to small and mid-sized NBFCs and MFI

Very Positive for NBFC and MFI. This will create demand for assets thus arrest the sharp spike in yields. It will also create demand for other assets in credit markets but it takes time for demand response from banks.

Mutual Fund Liquidity Support

RBI to open Rs 50,000-cr special liquidity window to support mutual fundsHelp boost confidence and reduce volatility seen in corporate debt market

Operation Twist Rs. 10,000 cr operation twist announced on 28 April 2020

The sov curve has a tendency to steepen in such time and we have steepest curve 1 yr at 3.70% and 30 yr at 6.90%. This will help some flattening of the curve hence positive for duration investors.

Refinancing Facilities for All India Financial Institutions (AIFIs

Provide special refinance facilities for a total amount of Rs500 bn to NABARD, SIDBI and NHB to enable them to meet sectoral credit needs. Advances under this facility will be charged at the RBI’s policy repo rate at the time of availment

This will remove some supply of bonds from PSU category thereby will creates space for yields coming down.

55

Monetary Initiatives Measures Impact

CRR100 bps CRR cut to 3% for 1 year. Also, a 1- time dispensation - reduced the requirement of minimum daily CRR balance maintenance from 90% to 80%

Immediate infusion of liquidity into the banking system to help in rate transmission. Reduction to release liquidity worth Rs1.37 tn. Bring down short term yield starting from Sov and gradually gets transmitted to Credits leading to spread compression

Liquidity Coverage RatioReduced LCR requirement for Scheduled Commercial Banks from 100% to 80% with immediate effect

Pressure for managing balance sheet eases hence provides liquidity comfort at individual institution level

MSF

Accommodation of Marginal Standing Facility to be increased from 2% SLR to 3%. Banks can dip into their mandated pool of government securities or the ‘statutory liquidity ratio’ to borrow from the RBI’s marginal standing facility.

The ability of banks to obtain funds from RBI on MSF rate increases by as much. This will provide additional liquidity potential to the debt market. Allows banks to avail an additional Rs1.37 tn of liquidity under the LAF window in times of stress at the MSF rate

OMO Purchases Conducted OMO purchases worth Rs400 bnCreates demand for long bonds hence help rate transmission

USD-INR sell-buy swap Conducted US$4bn worth of USD-INR sell buy swap Providing dollar liquidity

WMA limit for the central govt

Increased the limits for Ways and Means Advances (WMA) for 1HFY21 to Rs1.2 tn (earlier Rs750 bn)

Govt can manage better as supply of bonds will ease in primary markt hence yields come down.

WMA limit for the state govt

Increased the limits for Ways and Means Advances (WMA) for states 1HFY21 by 60%

Govt can manage better as supply of bonds will ease in primary markt hence yields come down.

Whatever It Takes From RBI– Measures Will Keep Coming Till Economy Stabilizes. Have Patience For Medicine To Work

56

A Step Towards Inclusion of Indian Bonds in Global Indices

Measures To Attract FPI Investment Implication

RBI has opened a new window “Fully Accessible Route” wherein specified govt. securities shall be eligible for investment by foreign investors

• This will ease access of foreign investors to the Indian Bond Market and facilitate inclusion in global bond indices

• Indian Bond Market has a huge scope of incremental flows by FPIs. This will have a downward pressure on interest ratesIncreased FPI Limit For Corporate Bonds

• Increased FPI limits for corporate bonds to 15% from 9% for 2020-21

Source: RBI Documents

57

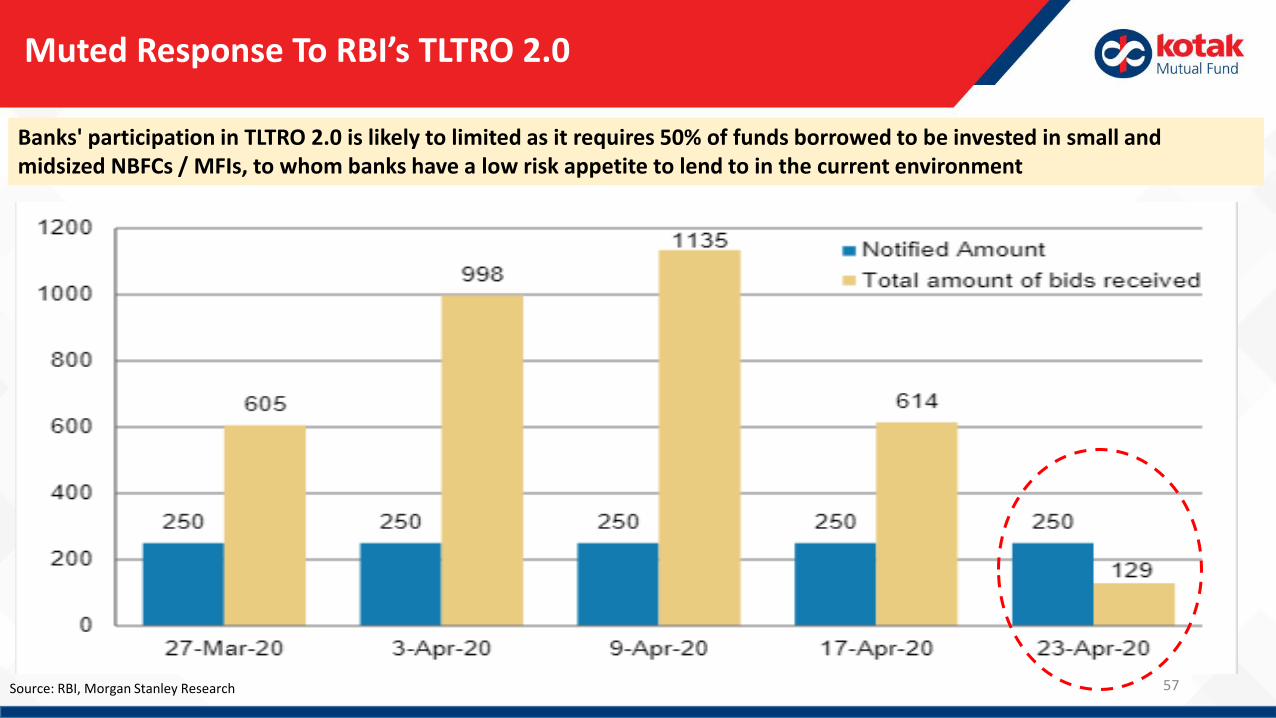

Muted Response To RBI’s TLTRO 2.0

Source: RBI, Morgan Stanley Research

Banks' participation in TLTRO 2.0 is likely to limited as it requires 50% of funds borrowed to be invested in small and midsized NBFCs / MFIs, to whom banks have a low risk appetite to lend to in the current environment

58

Hopes of More RBI Measures Leads To a Fall In 10 Year Gilt

Source: Bloomberg; Data as on 30 April 2020

6.31

6.11

6.00

6.10

6.20

6.30

6.40

6.50

6.60

3-A

pr-

20

4-A

pr-

20

5-A

pr-

20

6-A

pr-

20

7-A

pr-

20

8-A

pr-

20

9-A

pr-

20

10

-Ap

r-2

0

11

-Ap

r-2

0

12

-Ap

r-2

0

13

-Ap

r-2

0

14

-Ap

r-2

0

15

-Ap

r-2

0

16

-Ap

r-2

0

17

-Ap

r-2

0

18

-Ap

r-2

0

19

-Ap

r-2

0

20

-Ap

r-2

0

21

-Ap

r-2

0

22

-Ap

r-2

0

23

-Ap

r-2

0

24

-Ap

r-2

0

25

-Ap

r-2

0

26

-Ap

r-2

0

27

-Ap

r-2

0

28

-Ap

r-2

0

29

-Ap

r-2

0

30

-Ap

r-2

0

Disappointing April-Sept Borrowing Plan and weak demand expectation at auction

Headline Inflation eases to 5.91%

Hopes on the RBI to announce more steps such as open market purchases of dated securities and liquidity infusion to improve the transmission of interest rates,

Improved appetite for dated securities as the Reserve Bank of India set better-than-expected cutoffs at today's 200-bln-rupee debt sale

Anticipation Of Fiscal Stimulus

Hopes of more rounds of special open market operations by the Reserve Bank of India were offset by fears of fiscal slippage and additional market borrowing

RBI likely placed bids at the 200-bln-rupee auction boosted investor sentiment.

59

Super Surplus Liquidity In The System To Support The Economy

Inr Bn

Source: RBI, Data as on 30 April 2020

Liquidity Surplus is here to stay for longer than what market is pricing 5,035.83

(3,000.00)

(2,000.00)

(1,000.00)

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

6,000.00

Au

g-1

8

Sep

-18

Oct

-18

No

v-1

8

Dec

-18

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

System Borrowing

Source: MOSPI, ICRA

• Consumer price inflation declined to 5.91% in Mar 2020, from 6.6% in Feb 2020

• Core inflation eased to 4.03% in Mar 2020, from 4.08% in Feb 2020

• Inflation in food and beverages segment softened to 7.82% in Mar 2020, from 9.45% in Feb 2020

• Urban CPI inflation softened to 5.66% in Mar 2020, from 6.7% in Feb 2020

• Rural CPI inflation declined to 6.09% in Mar 2020, from 6.7% in Feb 2020

Source: Bloomberg 60

CPI Inflation Eases To 5.91% In Mar 2020

5.91%

4.03%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Oct-13 May-14 Dec-14 Jul-15 Feb-16 Sep-16 Apr-17 Nov-17 Jun-18 Jan-19 Aug-19 Mar-20

CPI Core CPI

61

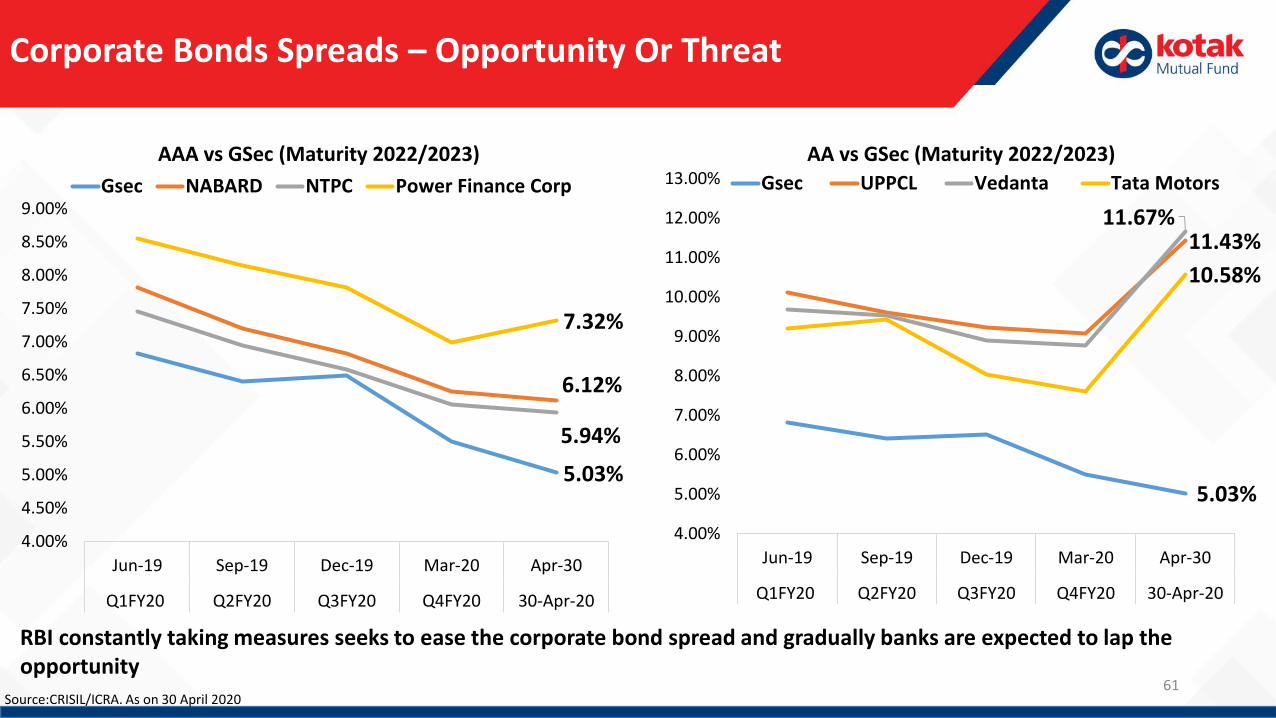

Corporate Bonds Spreads – Opportunity Or Threat

Source:CRISIL/ICRA. As on 30 April 2020

5.03%

6.12%

5.94%

7.32%

4.00%

4.50%

5.00%

5.50%

6.00%

6.50%

7.00%

7.50%

8.00%

8.50%

9.00%

Jun-19 Sep-19 Dec-19 Mar-20 Apr-30

Q1FY20 Q2FY20 Q3FY20 Q4FY20 30-Apr-20

AAA vs GSec (Maturity 2022/2023)

Gsec NABARD NTPC Power Finance Corp

5.03%

11.43%11.67%

10.58%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

10.00%

11.00%

12.00%

13.00%

Jun-19 Sep-19 Dec-19 Mar-20 Apr-30

Q1FY20 Q2FY20 Q3FY20 Q4FY20 30-Apr-20

AA vs GSec (Maturity 2022/2023)

Gsec UPPCL Vedanta Tata Motors

RBI constantly taking measures seeks to ease the corporate bond spread and gradually banks are expected to lap the opportunity

62

Bank Perp Spread- Opportunity Or Threat

5.03%

12.63%

9.14%

12.64%

10.50%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

Jun-19 Sep-19 Dec-19 Mar-20 Apr-30

Q1FY20 Q2FY20 Q3FY20 Q4FY20 30-Apr-20

Perpetual Bonds vs GSec (Call Date 2022/2023)

Gsec PNB SBI Union Bank Bank of Baroda

Source:CRISIL/ICRA. As on 30 April 2020

• When a bank buys a perp of other bank it means the bank is straight lending capital to other bank. Despite that, banks are queuing up to take this opportunity.

• Banks understand banks more than any one • Its often quoted “Don’t go by what they say, but watch what they do” • Almost all banks are buying these assets, this says some thing about the quality of the assets and future too.

63

FII Debt Flows

Source: Axis Capital, SEBI

Trend In Monthly FII Flows (Debt) – USD mn

(367)(1,158)

2,213

(846)

537 1,199 1,226

1,593

(274)

713

(442) (756)(1,494)

381

(8,680)

(1,129)

(10,500)

(9,000)

(7,500)

(6,000)

(4,500)

(3,000)

(1,500)

0

1,500

3,000

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

Debt Outlook

64

• RBI Policy Measures were a reasonably strong boost in terms of action across the market.

• The falling commodity prices especially Brent and the bond rally globally will help lower Indian rates. This may reduce the trade deficit. However due to equityselloff INR will remain under pressure. However, this is manageable as RBI has enough reserves to fight the same.

• Govt has announced H1 borrowing programme of Rs 4.88 tn worth of bonds and Rs 3 tn T bill for Q1. This is on expected lines but given low tradingvolumes/risk appetite, it may find difficulty to absorb 20k of weekly duration supply.

• We need some strong Demand side measures for bonds more than 5 yr. However given over all global environment with zero and negative sovereign rates inworld major economies, India 30 yr bonds ~7.30% (currently at 6.80%~)and 12-15 SDL at 7.60-7.90% (Currently at 7.20-7.30%) may emerge as great valuecreator for the coming year

The large liquidity infusion and rate cut may lower short term rates.

The Cut in Small savings rate and low bank deposit rate may lead to chase for high yielding assets through flow in MF this may aid spread compression

Expect corporate bonds to now outperform government bonds as the spreads may ease in weeks ahead

We prefer low to mid duration strategies on risk adjusted basis.

SDL spreads are attractive bet at ~100-120 bps on a 10 year curve. We may see a good compression in these spreads over the year. Therefore investors whohave appetite for volatility and who are looking for duration gains, can look to invest in the Gilt and Bond Funds space.

We believe that opportunities in the 1-3yr yield curve space are a potent option for investors. For this reason, investors with 6 month plus investmenthorizon may consider investing in corporate bond space.

In the same vein, the investment opportunity in short duration bond funds, banking and PSU funds, credit funds and dynamically managed duration fundsis still present and becoming more attractive. Investors may look to invest in the funds depending on the scale of risk appetite and the investment horizon.

65

Kotak MF Mantra: ‘Return of Capital’ is more important than ‘Return on Capital’

Strong Promoters, Cashflow backed business, Liquidity, and Asset Security are key to our investment ideas

Rating & Category Breakup Across Kotak MF Debt Assets

Credit Rating % of Total AUM

Tbill/G-Sec/SDL/AAA/A1+/Cash/NCA 90.99%

AA+ 1.58%

AA 4.12%

AA- 1.52%

Below AA- 1.78%

Grand Total (AUM) (INR Cr) 82,305

Category Breakup% of Total

AUM

Non-Credit Risk Funds 95%

Credit Risk Funds 5%

Grand Total (AUM) (INR Cr) 82,305

Data As on 30 April 2020

• In these challenging times, we reassure you that we always follow our investment process of focussing on credit quality and liquidity profile of our debt funds and maintain high degree of transparency for investors. Debt Funds can be broadly divided in two categories -Credit Risk Funds and Non Credit Risk Funds.

• Kotak MF has zero borrowing across all our schemes as on 30 April 2020.

We reassure you that we always follow our investment process of focussing on credit quality and liquidity profile of our debt funds and maintain high degree of transparency for investors.

Mutual fund investment are subject to market risks, read all scheme related documents carefully. This communication isn't solicitation for investments and is only meant for Kotak MF’s distributors and investors

• Liquidity, Maturity profile and Credit quality for Non Credit Risk Funds which constitutes ~ 95% of our debt AUM as on April 30, 2020 is substantially superior to credit risk funds.

66

67

• Our Liquidity profile remains robust

We reassure you that we follow our investment process of focusing on credit quality and liquidity profile of our debt funds and maintain high degree of transparency for investor.

Mutual fund investments are subject to market risks, read all scheme related documents carefully.

Liquidity Position Of Kotak MF Debt Funds As on 30 April 2020

Scheme Category Name of Scheme% of AUM in AAA (Long Term) or A1+ (Short

Term), Sovereign Debt, Cash & NCANon-Credit Strategies

Liquid Fund Kotak Liquid Fund 100

Money Market Fund Kotak Money Market Fund 100

Corporate Bond Fund Kotak Corporate Bond Fund 100

Short Duration Fund Kotak Bond Short Term Fund 100

Ultra Short Duration Fund Kotak Savings Fund 87.05Dynamic Bond Fund Kotak Dynamic Bond Fund 84.96

Medium to Long Duration Fund Kotak Bond Fund 84.14Banking and PSU Fund Kotak Banking and PSU Debt Fund 78.93

Low Duration Fund Kotak Low Duration Fund 54.91

Credit Strategies Medium Duration Fund Kotak Medium Term Fund 49.63Credit Risk Fund Kotak Credit Risk Fund 26.58

68

Kotak MF Debt Funds Are Well Equipped To Meet Redemption Requirements & Contingencies

We request for rationality and level-headed approach. Our portfolios are well provided-for normal redemption

requirements, as also for some level of contingencies.

SEBI regulation allow borrowing up to 20% of net assets of a fund to meet redemption requirements. But when does a

fund need to borrow? - At times due to redemption pressure, yields rise so high that it is more sensible to borrow at

lower cost and meet the redemption rather than to sell.

Thankfully, none of our funds have had to borrow to meet redemptions currently. We do have multiple credit lines if

needed. This also shows the quality of our fund and its liquidity profile even in stressful times.

We have done stress test of our portfolio’s to see what is the level of portfolio that we will be able to liquate quickly

and meet redemptions without borrowing in a worst case scenario and the found it encouraging. The liquidity profile of

debt funds have been given in the end of this minutes.

Having said that we may endeavour to reward the patient investor and share risk with the panicky investor.

Thus, if we face high redemption requirements, then we may endeavour to sell low credit rating / high credit risk papers.

This way, early redeemers may have to exit at lower NAVs. Additionally, the incremental proceeds would be invested in higher quality assets. Thus patient investors will see their investment portfolio improve rather than deteriorate

Mutual fund investment are subject to market risks, read all scheme related documents carefully.

69

Kotak MF – Our Past Experience

In past, we had chosen to defer payment rather than have knee-jerk reaction and hurt investors’

interest. Case in point: the issue surrounding delayed payment from Essel group.

o Our six FMPs got affected due to this issue in 2019. Then, we chose to delay marginal redemption

amount, rather than exercise the stock selling of Essel.

o We coordinated with Essel to arrange both capital and late payment interest for our investors.

Had we sold stocks instead, then the under-realization would have resulted in irrecoverable loss

of investors.

o We believe we have a fire proof house. We have done fire drills regularly, but we still don’t want

to see even a spark fly.

In any case, investors’ interests will be primary

Mutual fund investment are subject to market risks, read all scheme related documents carefully.

70

Investment Opportunity

71

Reality Check – Emerging Trends

Market Factors Pre-COVID-19 Post-COVID-19

31-Jan-20 31-Mar-20 30-Apr-20

Liquidity (System Borrowing) (Inr Bn) 3409.64 4841.78 5035.83

Weighted Avg Overnight Rate (RBI) 4.56% 0.85% 3.30%

India 10 Year Gilt 6.60% 6.14% 6.11%

Corporate Bond AAA 3 Year 6.83% 6.54% 6.42%

NBFC AAA 3 Year 7.19% 7.24% 6.95%

Corporate Bond AA 3 Year 7.51% 7.19% 7.12%

Corporate Bond AA 1 Year 6.89% 6.48% 6.71%

US 10 Year Gilt 1.51% 0.67% 0.63%

• Yields have fallen sharply all across the markets i.e Overnight, OIS, G Sec, AAA while yields in short term credit has shot up significantly

• Due to recent event supply in secondary of sub AAA rated bonds in market has increase which has lead to sharp increase in yields of sub AAA credit assets in particular

• Owing to COVID-19 and Lockdown, markets have become thin and if supply of bonds increase sharply irrsepticve of the quality then yield spikes up significantly – trader misery is investor delight

• Surplus liquidity in the system has increased further indicating that it’s a matter of time for an increase in the demand for the assets

Source: RBI, Bloomberg

72

Yield Across The Segment – Sanity Will Prevail

3.94

4.73

6.41

7.12

3.50

4.50

5.50

6.50

7.50

8.50

9.50

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

3 Year OIS 3 Year G-Sec 3 Year AAA 3 Year AA

Fund YTM (As on 30 April 2020) Respective Segment YieldsIncremental Earnings%

(Spread)Kotak Banking & PSU Fund 7.13% 3 Year AAA 6.41% 0.72%Kotak Low Duration Fund 9.47% 1 Year OIS 3.94% 5.53%

Kotak Credit Risk Fund 11.16% 3 Year AA 7.12% 4.04%

Kotak Medium Term Fund 10.51% 3 Year AA 7.12% 3.39%

Source: Bloomberg. Data as on 30 April 2020. Past performance may or may not sustain in the future

Mutual fund investment are subject to market risks, read all scheme related documents carefully.

73

Kotak Low Duration Fund: Yield Valuation Matrix – More Attractive Now

• If overnight return is ~3.5% and OIS is telling us this will remain here for about 2-3 year

• YTM of Kotak Low Duration Fund is ~10% and the same is for Kotak Credit Risk Fund

• This implies interest income for this risk is almost 250%-300% more

• This was 20-50% a year back

• Rs. 1 cr investment will earn ~9-10 lac of income vs ~3.5-3.7 lac in overnight which is a good incentive to take advantage of all the volatility in between

• Hence it is just a matter of time the demand from banks will come for these assets

9.47

6.10

4

5

6

7

8

9

10

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

No

v-1

9

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

Kotak Low Duration Fund (YTM) vs 1 Year AAA

Kotak Low Duration Fund - Std - Growth

1 Year AAA

Source: Bloomberg, MFi Explorer. Data as on 30 April 2020

Mutual fund investment are subject to market risks, read all scheme related documents carefully.

74

Kotak Credit Risk & Kotak Medium Term Fund: Yield Valuation Matrix – More Attractive Now

• This is an investor market and it is time to take contra bets when trader is willing to give steep discount for liquidity• All regulators are taking measure to bring sanity and we need to take advantage of this anomaly created due to

impatience of others

9.08 8.71

11.16

2.05 1.88

4.75

0

2

4

6

8

10

12

Oct-19 Jan-20 Apr-20

Kotak Credit Risk Fund

Kotak Credit Risk Fund (YTM)

Spread (Kotak Credit Risk vs 3 Year AAA)

9.24 8.79

10.51

2.21

1.96

4.10

0

2

4

6

8

10

12

Oct-19 Jan-20 Apr-20

Kotak Medium Term Fund

Kotak Medium Term Fund(YTM)

Spread (Kotak Medium Term vs 3 year AAA)

Source: MFi Explorer, Bloomberg. Data as on 30 April 2020 Mutual fund investment are subject to market risks, read all scheme related documents carefully.

75

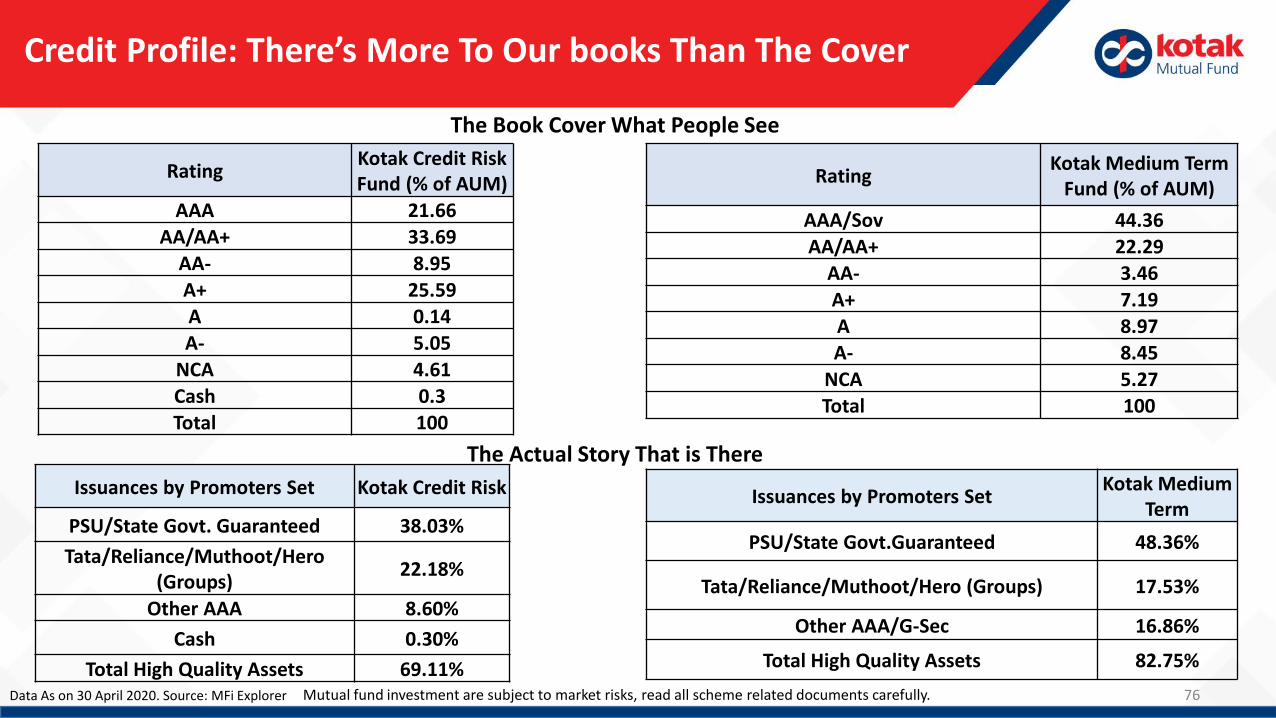

Our Credit Funds – Rating Profile

Rating Profile (% of AUM)

Mutual fund investment are subject to market risks, read all scheme related documents carefully.

Kotak Credit Risk Fund 30-Apr-20 15-Apr-20 31-Mar-20

AAA/Cash/NCA 26.57 25.67 29.32

AA/AA+ 33.69 31.45 29.75

AA- & Below 39.73 42.87 40.93

Kotak Medium Term Fund 30-Apr-20 15-Apr-20 31-Mar-20

AAA/A1+/Cash/NCA/Sov 49.63 47.59 51.04

AA/AA+ 22.29 29.00 26.84

AA- & Below 28.07 23.41 22.12

Credit Profile: There’s More To Our books Than The Cover

76

RatingKotak Credit Risk Fund (% of AUM)

AAA 21.66AA/AA+ 33.69

AA- 8.95A+ 25.59A 0.14A- 5.05

NCA 4.61

Cash 0.3Total 100

RatingKotak Medium Term

Fund (% of AUM)

AAA/Sov 44.36

AA/AA+ 22.29AA- 3.46

A+ 7.19A 8.97

A- 8.45NCA 5.27Total 100

Issuances by Promoters Set Kotak Credit Risk

PSU/State Govt. Guaranteed 38.03%

Tata/Reliance/Muthoot/Hero (Groups)

22.18%

Other AAA 8.60%

Cash 0.30%

Total High Quality Assets 69.11%

Issuances by Promoters SetKotak Medium

Term

PSU/State Govt.Guaranteed 48.36%

Tata/Reliance/Muthoot/Hero (Groups) 17.53%

Other AAA/G-Sec 16.86%

Total High Quality Assets 82.75%

The Book Cover What People See

The Actual Story That is There

Data As on 30 April 2020. Source: MFi Explorer Mutual fund investment are subject to market risks, read all scheme related documents carefully.

77

YTM At Elevated Levels Despite Better Rating Profile NowH

igh

Qu

alit

y A

sse

t A

s P

erc

en

tage

of

Po

rtfo

lio (

LHS)

Source: Internal Research; High Quality – Sov, A1+, AAA,AA+, & Cash.

YTM

Kotak Credit Risk Fund

29.15

11.16

8

8.5

9

9.5

10

10.5

11

11.5

5

10

15

20

25

30

35

40

45

50

Sep-1

8

Oct-1

8

No

v-18

Dec-1

8

Jan-1

9

Feb-1

9

Mar-1

9

Ap

r-19

May-1

9

Jun

-19

Jul-1

9

Au

g-19

Sep-1

9

Oct-1

9

No

v-19

Dec-1

9

Jan-2

0

Feb-2

0

Mar-2

0

Ap

r-20

High Quality (LHS) YTM (RHS)

78

Kotak Dynamic Bond Fund Has Outperformed Over Long-Term Since 2017

Credit funds carry credit risk and duration/ dynamic funds carry interest rate risk

Hence our advice to IFA/ distributors is that they allocate clients money in both dynamic and accrual funds from a 3 year

perspectiveSource: ICRA. As on 30th April 2020. The above returns is daily rolling returns for last 36months. Past Performance is not a guarantee for future return. Mutual fund investments are subject to market risks, read all scheme related documents carefully.

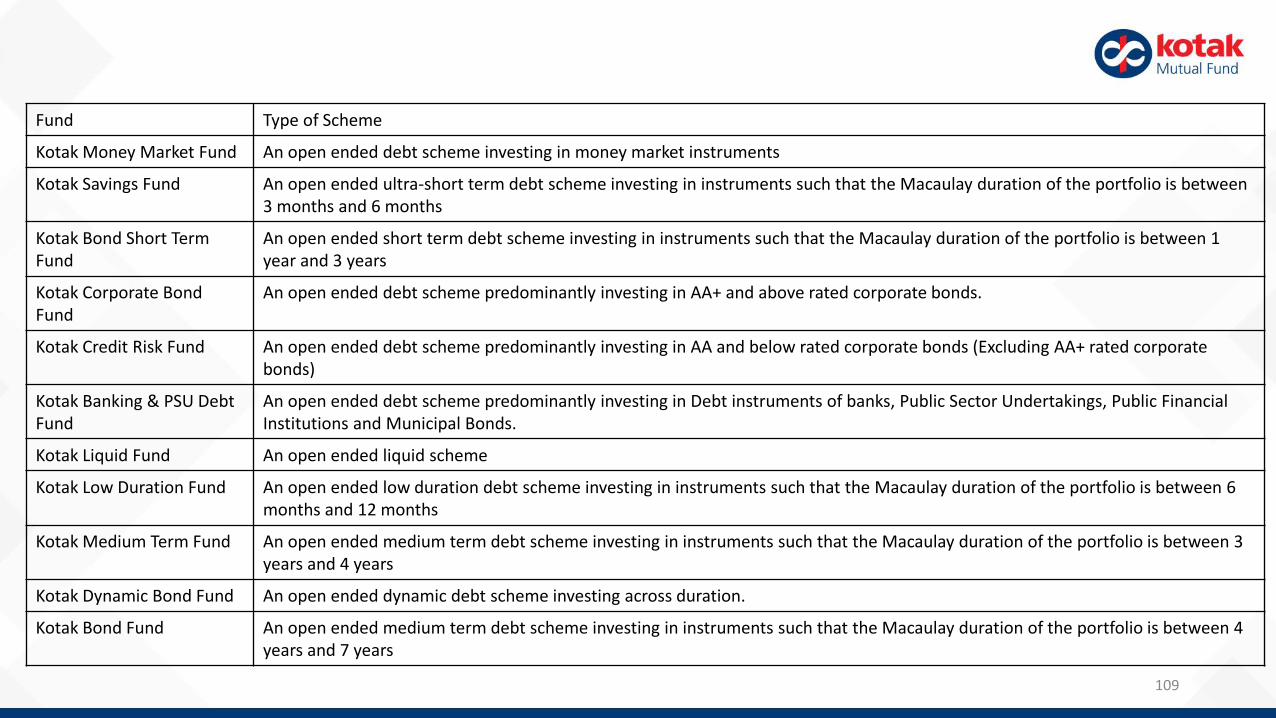

Liquid Funds

Ultra Short Term Debt Funds

Short Duration Funds

Credit Risk/Dynamic Debt/Medium Term

Long Duration Funds

Time To Play On Front Foot (Cautiously)

79Mutual Fund investments are subject to market risks, read all scheme related documents carefully. Please consult your financial advisor or investment professional for investment decisions.

Time To Notch Up The Risk Appetite One At A Time

80

Declining Trend In Net Redemptions in Credit Risk Funds

81

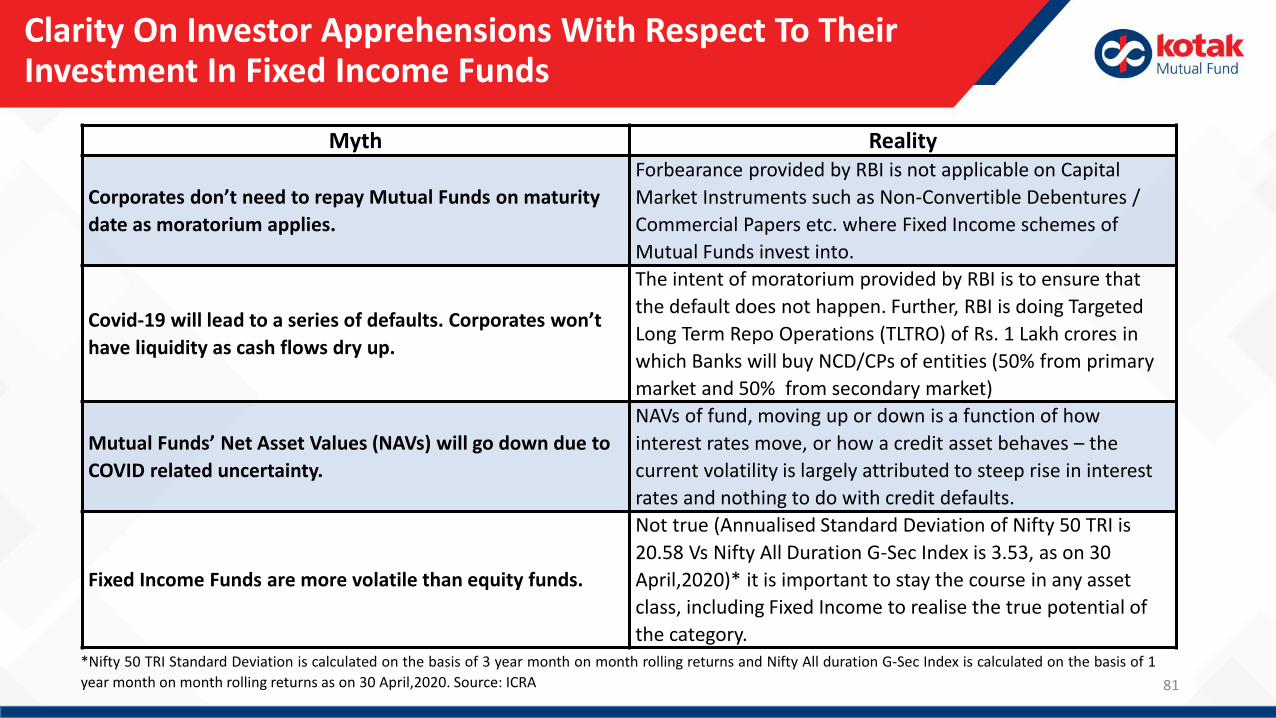

Clarity On Investor Apprehensions With Respect To Their Investment In Fixed Income Funds

Myth Reality

Corporates don’t need to repay Mutual Funds on maturity

date as moratorium applies.

Forbearance provided by RBI is not applicable on Capital

Market Instruments such as Non-Convertible Debentures /

Commercial Papers etc. where Fixed Income schemes of

Mutual Funds invest into.

Covid-19 will lead to a series of defaults. Corporates won’t

have liquidity as cash flows dry up.

The intent of moratorium provided by RBI is to ensure that

the default does not happen. Further, RBI is doing Targeted

Long Term Repo Operations (TLTRO) of Rs. 1 Lakh crores in

which Banks will buy NCD/CPs of entities (50% from primary

market and 50% from secondary market)

Mutual Funds’ Net Asset Values (NAVs) will go down due to

COVID related uncertainty.

NAVs of fund, moving up or down is a function of how

interest rates move, or how a credit asset behaves – the

current volatility is largely attributed to steep rise in interest

rates and nothing to do with credit defaults.

Fixed Income Funds are more volatile than equity funds.

Not true (Annualised Standard Deviation of Nifty 50 TRI is

20.58 Vs Nifty All Duration G-Sec Index is 3.53, as on 30

April,2020)* it is important to stay the course in any asset

class, including Fixed Income to realise the true potential of

the category.*Nifty 50 TRI Standard Deviation is calculated on the basis of 3 year month on month rolling returns and Nifty All duration G-Sec Index is calculated on the basis of 1

year month on month rolling returns as on 30 April,2020. Source: ICRA

Key Recommendations

Segment Scheme Rationale

Accrual

PlayKotak Credit Risk Fund /

Kotak Medium Term Fund

Investment for higher

accrual

Asset Allocation Kotak Debt Hybrid FundInvestment for asset

allocation

Short Term Parking of

Funds

Kotak Savings Fund / Kotak Low Duration Fund /

Kotak Corporate Bond Fund

Parking of surplus

cash

Kotak Equity Arbitrage Fund

Parking of surplus

cash with equity

taxation status

Duration Play

Kotak Dynamic Bond FundInvestment for Active

Duration Management

Kotak Bond Short Term FundInvestment for shorter

maturities

Kotak Bond FundInvestment for longer

maturities

82

ANNEXURES

83

84

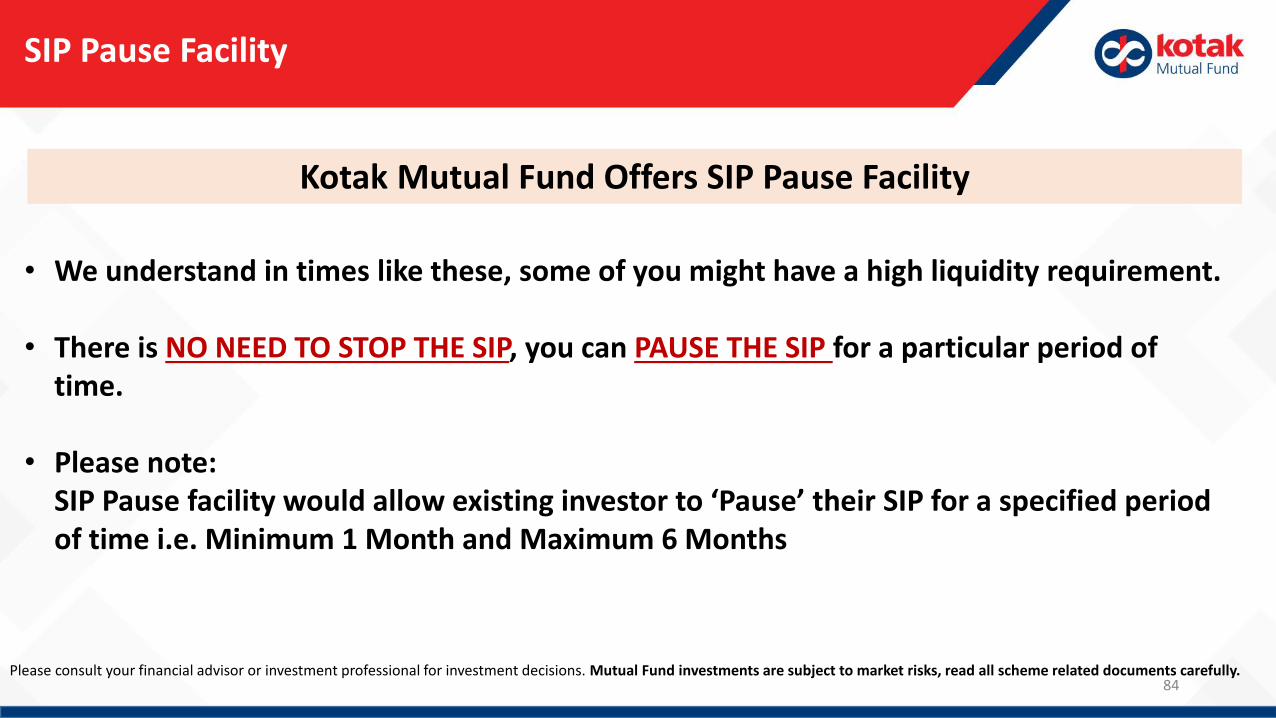

SIP Pause Facility

Kotak Mutual Fund Offers SIP Pause Facility

• We understand in times like these, some of you might have a high liquidity requirement.

• There is NO NEED TO STOP THE SIP, you can PAUSE THE SIP for a particular period of time.

• Please note: SIP Pause facility would allow existing investor to ‘Pause’ their SIP for a specified periodof time i.e. Minimum 1 Month and Maximum 6 Months

Please consult your financial advisor or investment professional for investment decisions. Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

SIP Pause and Cancellation Facility

85

SIP Pause or Cancellation facility is provided to Investors in their post login section of Kotak Mutual Fund App and

Website.

Steps to Pause SIP

Logon to Kotak Mutual fund Website/App

Choose SIP Pause option from Menu

Select the Folio number

Choose the SIP that you would like to pause

You can Pause your SIP for a Maximum period

of 6 Installments

Steps to Cancel SIP

Logon to Kotak Mutual fund Website/App

Choose Systematic Transaction from Menu

Choose Cancellation of Systematic registration

Choose Systematic Investment Plan

Select the mode of SIP (Online/Offline)

Choose the SIP that you would like to Cancel

Business Hub

An Initiative by Kotak Mutual Fund to Support Distributor's to Improve the efficiency in their Business

Logon to https://kotakmfadvisor.comKey Features of Business Hub Include

Initiate Transaction

Existing Investors

Lumpsum Switch Redeem SIP STP SWP

New Investors

Lumpsum SIP Zero Balance Folio

Business Opportunity

SIP Ceased

Inactive Investors

SIP Upcoming Maturity

Zero Balance Investor

Equity Only Investor

Debt Only Investor

ELSS Opportunity

Liquid Investor

And much more business data

86

87

Stay Home, Stay Safe And Learn From The Comfort Of Your Home With Prostart

Log on to www.kotakmfadvisor.com

VIEW ALL 10 VIDEOS Excel Based Financial Calculators on email PLUS

Course Completion Certificate

In case you are unable to log in kindly send a message to

Tejas Thakur (9619510328) – Kotak AMC.

“FINANCIAL PLANNING - VIDEO MODULE” was a grand success

VIEWERSHIP CROSSED 22,000+ 1500+ UNIQUE USERS 215+ CERTIFCATES AWARDED

Click here For Process of ProStart Video Learning Login

88

Debt Market Outlook – Mar 2020

Stay Updated ! Follow us at Kotak Mutual Fund Click here to visit our Youtube Channel

All About Kotak Tax SaverInvestor Education

Product VideoEquity Market Outlook – April 2020

Opportunity in Mid and Small cap spaceWhy invest in Small and Midcap fund now?

Key Variables & Their Impact On Equities

Key VariablesShort -term

Medium –term

Remarks

EconomyNear-term growth to get impacted due to Coronavirus scare, but many reforms like IBC, GST, RERA to improve longer term growth trajectory

Corporate Earnings

Near-term earning growth to get impacted. Strong medium term earning growth trajectory, as previous cycle of NPA ends and capacity utilization improves. Will also be aided by recent tax cuts

FII Flow

Flows to turn negative in short term. Strong long term growth as India stands out among global asset classes with prospects of long term growth given favorable demographics

DII Flow Long runaway of growth in financialization of savings

Supply of paperNear term supply will be impacted. Higher disinvestment target and repair of leveraged balance sheet to create supply in markets.

Policy/Reform Initiative Expect improved policy measures reform momentum

Signify Growth 89

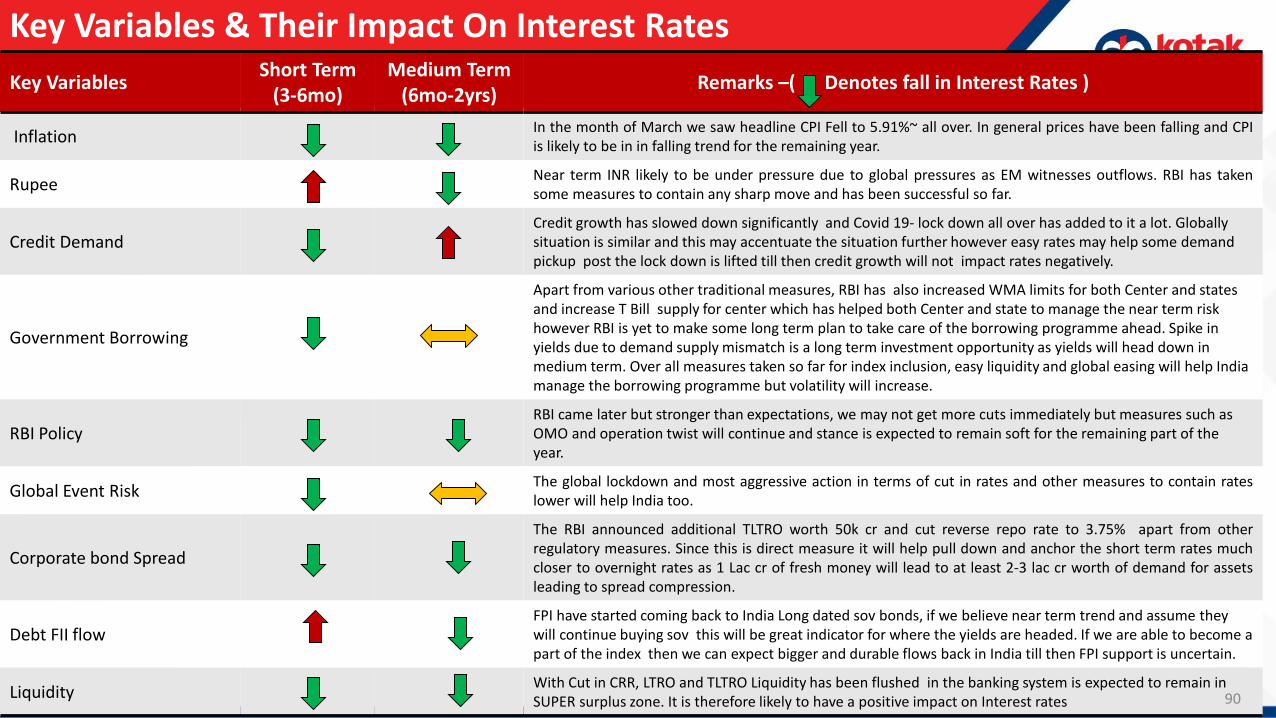

Key Variables & Their Impact On Interest Rates

Key VariablesShort Term

(3-6mo)Medium Term

(6mo-2yrs)Remarks –( Denotes fall in Interest Rates )

InflationIn the month of March we saw headline CPI Fell to 5.91%~ all over. In general prices have been falling and CPIis likely to be in in falling trend for the remaining year.

RupeeNear term INR likely to be under pressure due to global pressures as EM witnesses outflows. RBI has takensome measures to contain any sharp move and has been successful so far.

Credit DemandCredit growth has slowed down significantly and Covid 19- lock down all over has added to it a lot. Globally situation is similar and this may accentuate the situation further however easy rates may help some demand pickup post the lock down is lifted till then credit growth will not impact rates negatively.

Government Borrowing

Apart from various other traditional measures, RBI has also increased WMA limits for both Center and states and increase T Bill supply for center which has helped both Center and state to manage the near term risk however RBI is yet to make some long term plan to take care of the borrowing programme ahead. Spike in yields due to demand supply mismatch is a long term investment opportunity as yields will head down in medium term. Over all measures taken so far for index inclusion, easy liquidity and global easing will help India manage the borrowing programme but volatility will increase.

RBI PolicyRBI came later but stronger than expectations, we may not get more cuts immediately but measures such as OMO and operation twist will continue and stance is expected to remain soft for the remaining part of the year.

Global Event RiskThe global lockdown and most aggressive action in terms of cut in rates and other measures to contain rateslower will help India too.

Corporate bond Spread

The RBI announced additional TLTRO worth 50k cr and cut reverse repo rate to 3.75% apart from otherregulatory measures. Since this is direct measure it will help pull down and anchor the short term rates muchcloser to overnight rates as 1 Lac cr of fresh money will lead to at least 2-3 lac cr worth of demand for assetsleading to spread compression.

Debt FII flowFPI have started coming back to India Long dated sov bonds, if we believe near term trend and assume they will continue buying sov this will be great indicator for where the yields are headed. If we are able to become a part of the index then we can expect bigger and durable flows back in India till then FPI support is uncertain.

LiquidityWith Cut in CRR, LTRO and TLTRO Liquidity has been flushed in the banking system is expected to remain in SUPER surplus zone. It is therefore likely to have a positive impact on Interest rates 90

12-month Forward Sensex P/E (X)

Sensex in ‘Fair Value Plus’ Range in P/E Terms

Source: Axis Capital , Internal Estimates91

11000

15000

19000

23000

27000

31000

35000

39000

43000

May

-17

Jun

-17

Jul-

17

Au

g-1

7

Sep

-17

Oct

-17

No

v-1

7

Dec

-17

Jan

-18

Feb

-18

Mar

-18

Ap

r-1

8

May

-18

Jun

-18

Jul-

18

Au

g-1

8

Sep

-18

No

v-1

8

Dec

-18

Jan

-19

Feb

-19

Mar

-19

Ap

r-1

9

May

-19

Jun

-19

Jul-

19

Au

g-1

9

Sep

-19

Oct

-19

Dec

-19

Jan

-20

Feb

-20

Mar

-20

Ap

r-2

0

Cheap 8x - 10x

Attractive 10x - 13x

Fair 13x - 17x

Fair Value Plus 17x - 20x

Stretched 20x - 24x

92

Performance Of Sensex And Nifty Indices

Source: Bloomberg, Kotak Institutional Equities

Disclaimers & Disclosures

93

The information contained in this (document) is extracted from different public sources. All reasonable care has been taken to ensure that the information contained hereinis not misleading or untrue at the time of publication. This is for the information of the person to whom it is provided without any liability whatsoever on the part of KotakMahindra Asset Management Co Ltd or any associated companies or any employee thereof.We are not soliciting any action based on this material and is for generalinformation only. Investors should consult their financial advisors if in doubt about whether the product is suitable for them before investing

These materials are not intended for distribution to or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Thedistribution of this document in certain jurisdictions may be restricted or totally prohibited and accordingly, persons who come into possession of this document arerequired to inform themselves about, and to observe, any such restrictions

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Disclaimers & Risk Factors

94

95

Kotak Dynamic Bond Fund

Scheme Inception date is 26/05/2008. Mr. Deepak Agrawal has been managing the fund since 25/11/2012. Different plans have different expense structure. The performance details provided herein are of regular plan ^Past performance may or may not be sustained in future.*All payouts during the period have been reinvested in the units of the scheme at the then prevailing NAV. Returns >= 1 year: CAGR (Compounded Annualised Growth Rate). N.A stands for data not available. Note: Point to Point (PTP) Returns in INR shows the value of 10,000/- investment made at inception. Source: ICRA MFI Explorer. # Name of Scheme Benchmark. ## Name of Additional Benchmark. The performance of the scheme is benchmarked to the Total Return variant (TRI) of the Benchmark. Alpha is difference of scheme return with benchmark return.

Kotak Dynamic Bond Fund As on 30 April 2020

May 26, 2008Kotak Dynamic Bond Fund -

GrowthNIFTY Composite Debt

Index# ALPHACRISIL 1 Year

Tbill##Kotak Dynamic Bond Fund -

GrowthNIFTY Composite Debt

Index# CRISIL 1 Year Tbill##

Since Inception 8.63% 8.51% 0.12% 6.68% 26,869 26,503 21,645

Last 1 Year 10.77% 13.05% -2.28% 8.37% 11,077 11,305 10,837

Last 3 Years 8.38% 8.10% 0.28% 7.27% 12,740 12,641 12,351

Last 5 Years 9.11% 8.41% 0.69% 7.29% 15,470 14,983 14,220

Kotak Dynamic Bond Fund

Systematic Investment Plan (SIP) If you had invested Rs 10,000 every month

Monthly SIP of Rs 10000 Since Inception 10 years 7 years 5 years 3 years 1 year

Total amount invested (Rs) 1,440,000 1,200,000 840,000 600,000 360,000 120,000

Total Value as on Apr 30, 2020 (Rs) 2,520,450 1,918,226 1,157,089 750,896 413,170 125,163

Scheme Returns (%) 8.93 9.08 9.01 8.92 9.17 8.12

Nifty Composite Debt Index Returns (%) 8.55 8.68 8.77 8.62 9.53 10.73

Alpha* 0.38 0.39 0.24 0.30 -0.36 -2.60

Nifty Composite Debt Index (Rs)# 2,443,106 1,866,159 1,139,528 740,368 412,358 125,826

CRISIL 1 Year T-Bill Index (Rs)^ 2,242,911 1,751,175 1,093,188 722,827 405,434 125,696

CRISIL 1 Year T-Bill Index Returns (%) 7.11 7.34 7.41 7.39 7.89 8.97

Scheme Inception : - May 26, 2008. The returns are calculated by XIRR approach assuming investment of Rs. 10,000/- on the 1st working day of every month. XIRR helps in calculating return on investments given an initial and final value and a series of cash inflows and outflows and taking the time of investment into consideration. Since inception returns are assumed to be starting from the beginning of the subsequent month from the date of inception. # Benchmark ; ^ Additional Benchmark. Alpha is difference of scheme return with benchmark return.

96

Kotak Credit Risk Fund

Scheme Inception date is 11/05/2010. Mr. Deepak Agrawal has been managing the fund since 12/04/2010. Different plans have different expense structure. The performance details provided herein are of regular plan ^Past performance may or may not be sustained in future.*All payouts during the period have been reinvested in the units of the scheme at the then prevailing NAV. Returns >= 1 year: CAGR (Compounded Annualised Growth Rate). N.A stands for data not available. Note: Point to Point (PTP) Returns in INR shows the value of 10,000/- investment made at inception. Source: ICRA MFI Explorer. # Name of Scheme Benchmark. ## Name of Additional Benchmark. The performance of the scheme is benchmarked to the Total Return variant (TRI) of the Benchmark. Alpha is difference of scheme return with benchmark return

Kotak Credit Risk Fund Performance As on 30 April 2020

May 11, 2010 Kotak Credit Risk Fund - GrowthNIFTY Credit Risk Bond

Index# ALPHACRISIL 1 Year

Tbill##Kotak Credit Risk Fund -

GrowthNIFTY Credit Risk Bond

Index# CRISIL 1 Year Tbill##Since Inception 7.90% 9.08% -1.17% 6.97% 21,364 23,799 19,586Last 1 Year 4.72% 8.43% -3.71% 8.37% 10,472 10,843 10,837Last 3 Years 5.80% 7.61% -1.82% 7.27% 11,847 12,469 12,351Last 5 Years 7.28% 8.50% -1.22% 7.29% 14,215 15,046 14,220

Kotak Credit Risk Fund

Systematic Investment Plan (SIP) If you had invested Rs 10,000 every month

Monthly SIP of Rs 10000 Since Inception 10 years 7 years 5 years 3 years 1 year

Total amount invested (Rs) 1,200,000 NA 840,000 600,000 360,000 120,000

Total Value as on Apr 30, 2020 (Rs) 1,776,527 NA 1,077,939 701,054 388,685 120,295

Scheme Returns (%) 7.62 NA 7.02 6.17 5.05 0.46

NIFTY Credit Risk Bond Index Returns (%) 8.92 NA 8.49 8.00 7.70 6.71

Alpha* -1.30 NA -1.47 -1.83 -2.65 -6.25

NIFTY Credit Risk Bond Index (Rs)# 1,902,151 NA 1,136,163 733,870 404,324 124,279

CRISIL 1 Year T-Bill Index (Rs)^ 1,751,118 NA 1,093,188 722,827 405,434 125,696

CRISIL 1 Year T-Bill Index (%) 7.34 NA 7.41 7.39 7.89 8.97

Scheme Inception : - May 11, 2010. The returns are calculated by XIRR approach assuming investment of Rs. 10,000/- on the 1st working day of every month. XIRR helps in calculating return on investments given an initial and final value and a series of cash inflows and outflows and taking the time of investment into consideration. Since inception returns are assumed to be starting from the beginning of the subsequent month from the date of inception. # Benchmark ; ^ Additional Benchmark. Alpha is difference of scheme return with benchmark return.

Kotak Emerging Equity Fund Performance As on 30 April 2020

97

Scheme Inception date is 30/03/2007. Mr. Pankaj Tibrewal has been managing the fund since 27/05/2010. Different plans have different expense structure. The performance details provided herein are of regular plan ^Past performance may or may not be sustained in future.*All payouts during the period have been reinvested in the units of the scheme at the then prevailing NAV. Returns >= 1 year: CAGR (Compounded Annualised Growth Rate). N.A stands for data not available. Note: Point to Point (PTP) Returns in INR shows the value of 10,000/- investment made at inception. Source: ICRA MFI Explorer. # Name of Scheme Benchmark. ## Name of Additional Benchmark. TRI Total Return Index, In terms of SEBI circular dated January 4, 2018, the performance of the scheme is benchmarked to the Total Return variant (TRI) of the Benchmark Index instead of Price Return Variant (PRI). Alpha is difference of scheme return with benchmark return.