Minnesota Travel Segmentation Study | March 2012 EXPLORE MINNESOTA TOURISM SEGMENTATION FINAL REPORT...

66

esota Travel Segmentation Study | March 2012 EXPLORE MINNESOTA TOURISM SEGMENTATION FINAL REPORT APRIL 11, 2012

-

Upload

jonatan-mullis -

Category

Documents

-

view

214 -

download

1

Transcript of Minnesota Travel Segmentation Study | March 2012 EXPLORE MINNESOTA TOURISM SEGMENTATION FINAL REPORT...

Minnesota Travel Segmentation Study | March 2012

E X P L O R E M I N N E S O TA T O U R I S MS E G M E N TAT I O N F I N A L R E P O R T

APRIL 11 , 2012

Minnesota Travel Segmentation Study | March 2012

SEGMENTATION PURPOSE:

DEEPEN OUR UNDERSTANDING OF CURRENT AND POTENTIAL TARGET AUDIENCES IN ORDER TO DRIVE MORE TRAVEL TO MINNESOTA

Minnesota Travel Segmentation Study | March 2012

TODAY’S GOAL:

RECAP OF F INDINGS

PROFILE OUR PRIORITY SEGMENTS

Minnesota Travel Segmentation Study | March 2012

A G E N D A

OBJECTIVES/METHODOLOGY

PRIORITIZING OUR SEGMENTS

SEGMENT LEARNING

PERSONA OVERVIEW

NEXT STEPS

Nobody’s Unpredictable

Minnesota Travel Segmentation StudyFinal Presentation

April 12, 2012

March 2012

Minnesota Travel Segmentation Study | March 2012 6

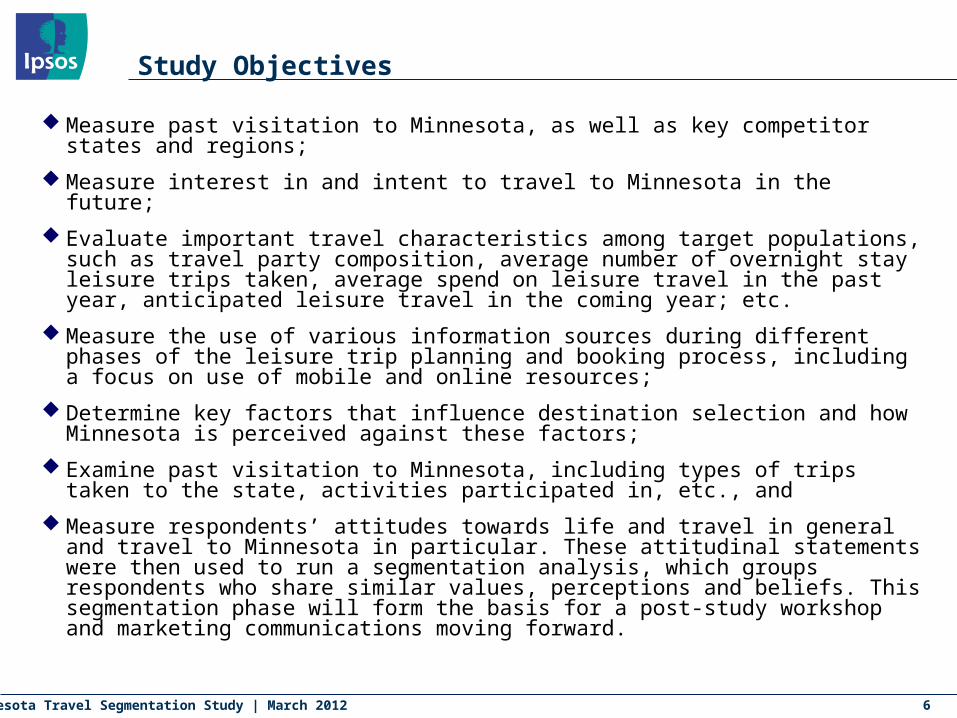

Study Objectives

Measure past visitation to Minnesota, as well as key competitor states and regions; Measure interest in and intent to travel to Minnesota in the future; Evaluate important travel characteristics among target populations, such as travel party

composition, average number of overnight stay leisure trips taken, average spend on leisure travel in the past year, anticipated leisure travel in the coming year; etc.

Measure the use of various information sources during different phases of the leisure trip planning and booking process, including a focus on use of mobile and online resources;

Determine key factors that influence destination selection and how Minnesota is perceived against these factors;

Examine past visitation to Minnesota, including types of trips taken to the state, activities participated in, etc., and

Measure respondents’ attitudes towards life and travel in general and travel to Minnesota in particular. These attitudinal statements were then used to run a segmentation analysis, which groups respondents who share similar values, perceptions and beliefs. This segmentation phase will form the basis for a post-study workshop and marketing communications moving forward.

Minnesota Travel Segmentation Study | March 2012 7

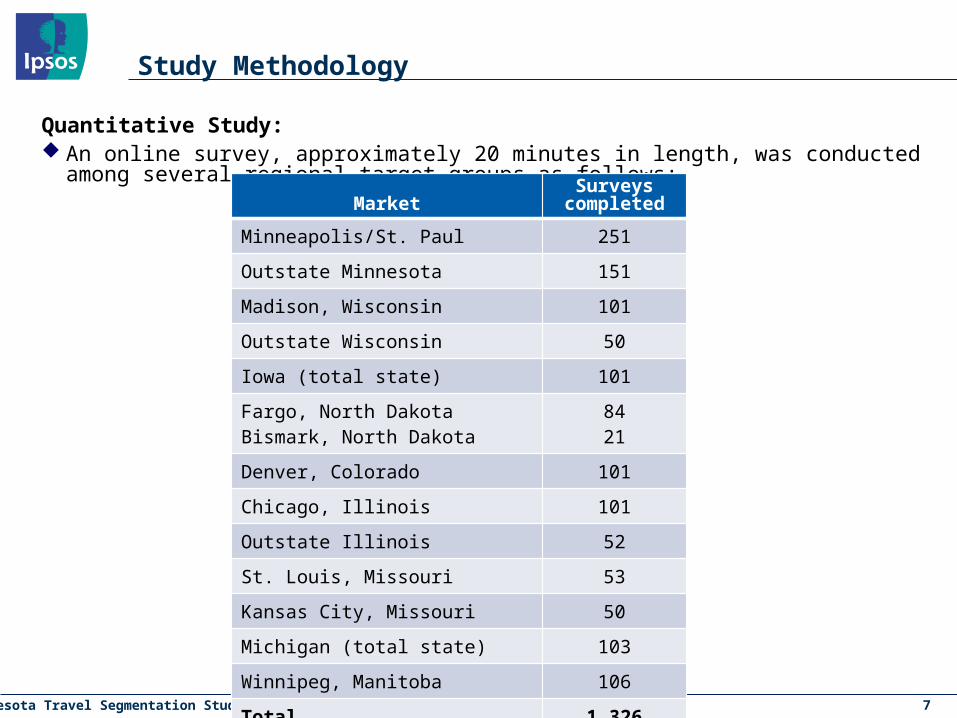

Study Methodology

Quantitative Study: An online survey, approximately 20 minutes in length, was conducted among several regional target

groups as follows:Market

Surveys completed

Minneapolis/St. Paul 251

Outstate Minnesota 151

Madison, Wisconsin 101

Outstate Wisconsin 50

Iowa (total state) 101

Fargo, North DakotaBismark, North Dakota

8421

Denver, Colorado 101

Chicago, Illinois 101

Outstate Illinois 52

St. Louis, Missouri 53

Kansas City, Missouri 50

Michigan (total state) 103

Winnipeg, Manitoba 106

Total 1,326

Minnesota Travel Segmentation Study | March 2012 8

Study Methodology (cont.)

The data were weighted by region, gender and age to reflect the composition of the actual population of the U.S. states and Canadian provinces according to the most recent census data for the United States (through the U.S. Census Data Bureau) and Canada (through Statistics Canada).

The survey was conducted from January 12 - 30, 2012 using Ipsos’ online panel in the United States and Canada.

Qualitative Study: In order to gain further in-depth understanding of the key segments derived from the quantitative

study, a qualitative component was included in the overall study. A total of four focus groups were conducted with respondents who were determined to fit into one

of the two key segments: Cultural Explorers and Spontaneous Spenders. All sessions were recruited using the discriminant analysis from the segmentation study.

There were eight respondents in each focus group session. Four sessions were completed with Cultural Explorers and Spontaneous Spenders – two sessions in

Minneapolis and two in Milwaukee. In each city there was one session completed with each segment. Focus group sessions were held in Minneapolis, MN on March 14, 2012 and in Milwaukee, WI on

March 15, 2012.

Nobody’s Unpredictable

Introducing the Segments

Minnesota Travel Segmentation Study | March 2012 10

Key Segments

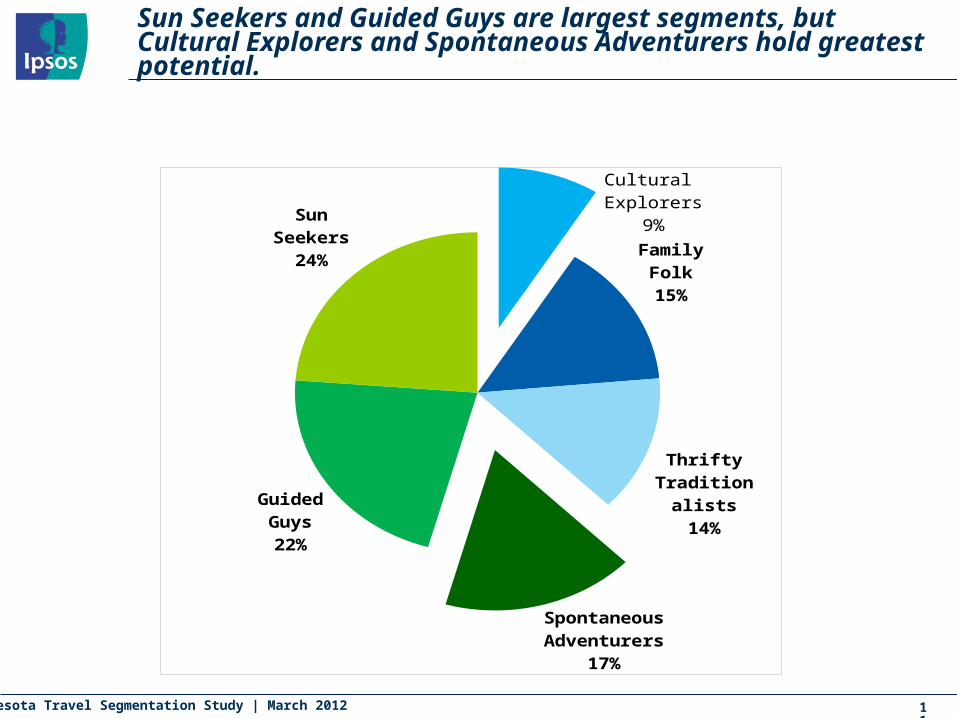

The segmentation analysis produced six different segments. Of these six segments, two were identified as holding the greatest potential for travel to/within Minnesota:

Cultural Explorers Spontaneous Adventurers

These two segments were identified as holding the greatest potential based on: Past travel to/within Minnesota; Leisure spend – both overall and within the state of Minnesota; Anticipated increase in travel spending over the next 12 months; Interest in visiting Minnesota in the future; and Likelihood to visit Minnesota in the next 12 months.

Minnesota Travel Segmentation Study | March 2012

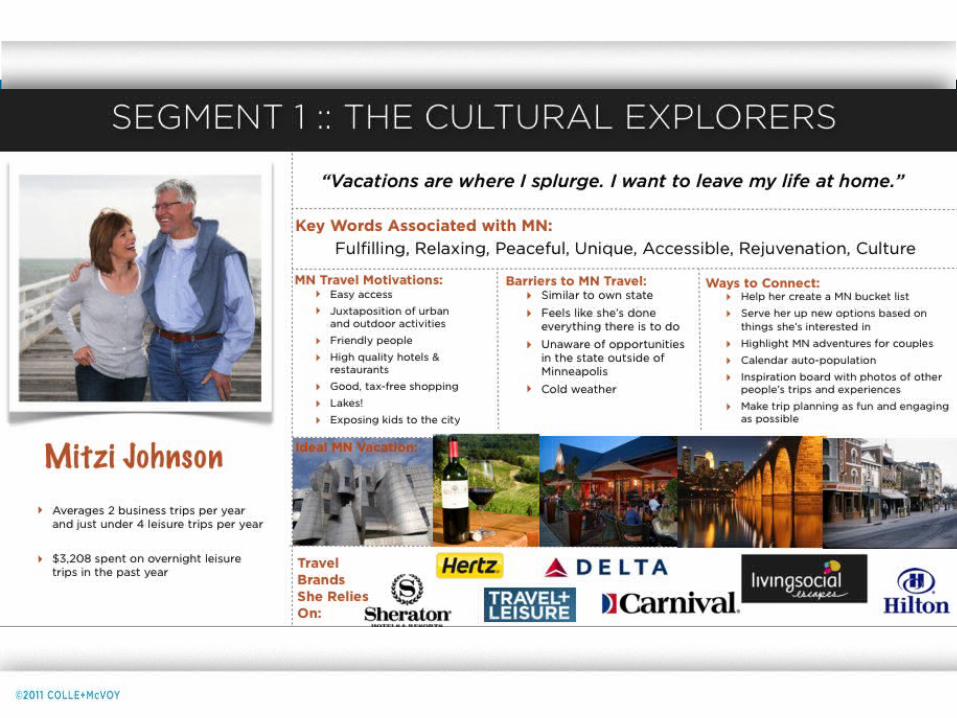

Cultural Explorers

9%

Family Folk15%

Thrifty Tradi-tionalists

14%

Spontaneous Adventurers17%

Guided Guys22%

Sun Seekers24%

11

Sun Seekers and Guided Guys are largest segments, but Cultural Explorers and Spontaneous Adventurers hold greatest potential.

Minnesota Travel Segmentation Study | March 2012 12

Non-Key Segments

Outside of the two key segments (Cultural Explorers and Spontaneous Adventurers), there are four other segments that emerged from the segmentation analysis. Below is a brief summary of each and why each is not considered a ‘key’ target:

Family Folk: This segment skews older and male. They are among the most likely of all segments to live in Minnesota. They are among the lower spending segments when it comes to leisure travel, although their share of leisure spending in the state of Minnesota is the highest among all segments. This segment prefers the outdoors to urban oriented activities. In particular, this segment looks for excellent hunting and fishing when choosing a travel destination.

Although this segment is very positive about Minnesota, travels to/within the state and is interested in traveling to Minnesota in the future, this group has an average leisure spend that is lower than the overall average. This segment is already attracted to Minnesota’s outdoor offerings (e.g. fishing and hunting), they already travel to/within Minnesota, thus targeting this segment is somewhat akin to ‘preaching to the converted’.

Minnesota Travel Segmentation Study | March 2012 13

Non-Key Segments

Thrifty Traditionalists: This segment skews female and are highly educated. As this segment’s name indicates, they are thrifty when it comes to leisure travel spending – this group has the lowest average spend among all segments. This segment is also most likely to plan to spend less on travel in the next year. This group considers themselves to be more traditional than experimental. They are among the least likely of all segments to own a Smartphone or tablet and are also among the least likely to say online resources are important when planning or taking a trip.

Given this segment’s low average spend on leisure travel and that they are among the least likely to say they will visit Minnesota in the next year, this segment is not one that holds great potential for travel to Minnesota. Moreover, this group is not particularly positive in their perceptions of the state and are among the least likely to participate in the common activities that Minnesota has to offer.

Minnesota Travel Segmentation Study | March 2012 14

Non-Key Segments

Guided Guys: This segment skews younger and male. They are the most likely of all segments to have young children (five years old or younger) in their home. When it comes to leisure travel spending, this group has the second lowest average level of spend among all segments. When it comes to travel, this segment likes to have things organized/planned for them. They prefer group travel and organized tours . They also like to be in familiar surroundings and are more likely than other segments to feel travel is a hassle and to see no reason to spend money to travel away from home.

Although this is one of the largest segments in terms of its relative size, Guided Guys do not hold strong potential for travel to Minnesota. Given their low average spend on leisure travel and their lower-than-average past two year visitation to Minnesota and likelihood to visit the state in the next 12 months, this segment is not a key group for Minnesota. Moreover, this segment is also more negative in their perceptions of Minnesota than the overall average.

Minnesota Travel Segmentation Study | March 2012 15

Non-Key Segments

Sun Seekers: This segment skews slightly female and are least likely of all segments to be residents of Minnesota; they are also the least likely to have ever traveled to Minnesota. They are the least likely of all segments to say they are interested in travelling to Minnesota in the future. When choosing a travel destination, this group looks for destinations with warm weather. Although this segment is not very positive in their perceptions of Minnesota, they are not overly negative. They hold mostly neutral perceptions of the state, perhaps as a result of this segment’s lack of previous experience in Minnesota.

Like the Guided Guys, this segment is large in size (the largest of all six segments) but they do not hold strong potential for travel to Minnesota. Their lack of familiarity with Minnesota may prove to be a difficult obstacle to overcome in enticing this group to visit the state. Moreover, as their name indicates, this segment identifies warm weather as one of the top factors that influences their decision of a vacation destination; something that Minnesota is not known for.

Nobody’s Unpredictable

What Drove Our Decision On The Segments?

Minnesota Travel Segmentation Study | March 2012

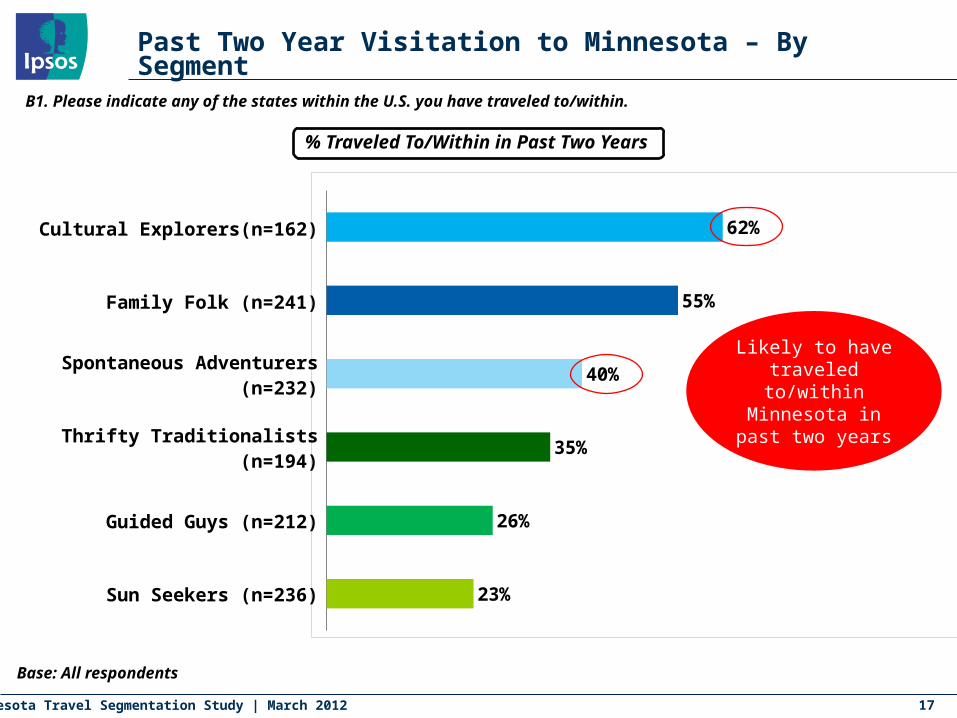

Past Two Year Visitation to Minnesota – By Segment

17

Base: All respondents

% Traveled To/Within in Past Two Years

B1. Please indicate any of the states within the U.S. you have traveled to/within.

62%

55%

40%

35%

26%

23%

Cultural Explorers(n=162)

Family Folk (n=241)

Spontaneous Adventurers (n=232)

Thrifty Traditionalists (n=194)

Guided Guys (n=212)

Sun Seekers (n=236)

Likely to have traveled to/within Minnesota in past

two years

Minnesota Travel Segmentation Study | March 2012

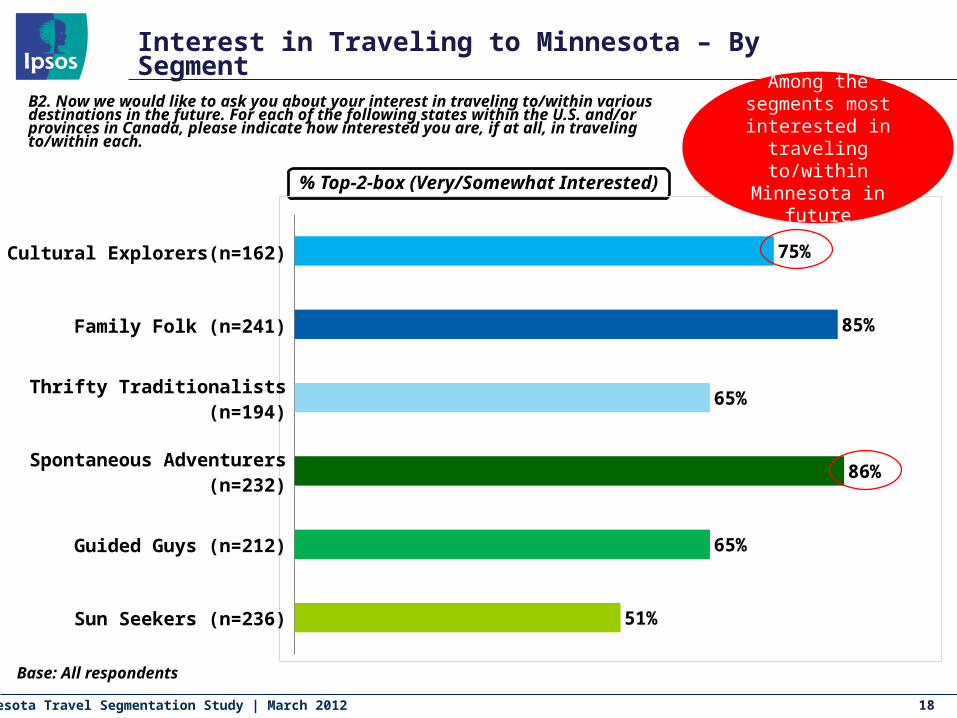

Interest in Traveling to Minnesota – By Segment

18

Base: All respondents

% Top-2-box (Very/Somewhat Interested)

B2. Now we would like to ask you about your interest in traveling to/within various destinations in the future. For each of the following states within the U.S. and/or provinces in Canada, please indicate how interested you are, if at all, in traveling to/within each.

75%

85%

65%

86%

65%

51%

Cultural Explorers(n=162)

Family Folk (n=241)

Thrifty Traditionalists (n=194)

Spontaneous Adventurers (n=232)

Guided Guys (n=212)

Sun Seekers (n=236)

Among the segments most interested in traveling to/within

Minnesota in future

Minnesota Travel Segmentation Study | March 2012

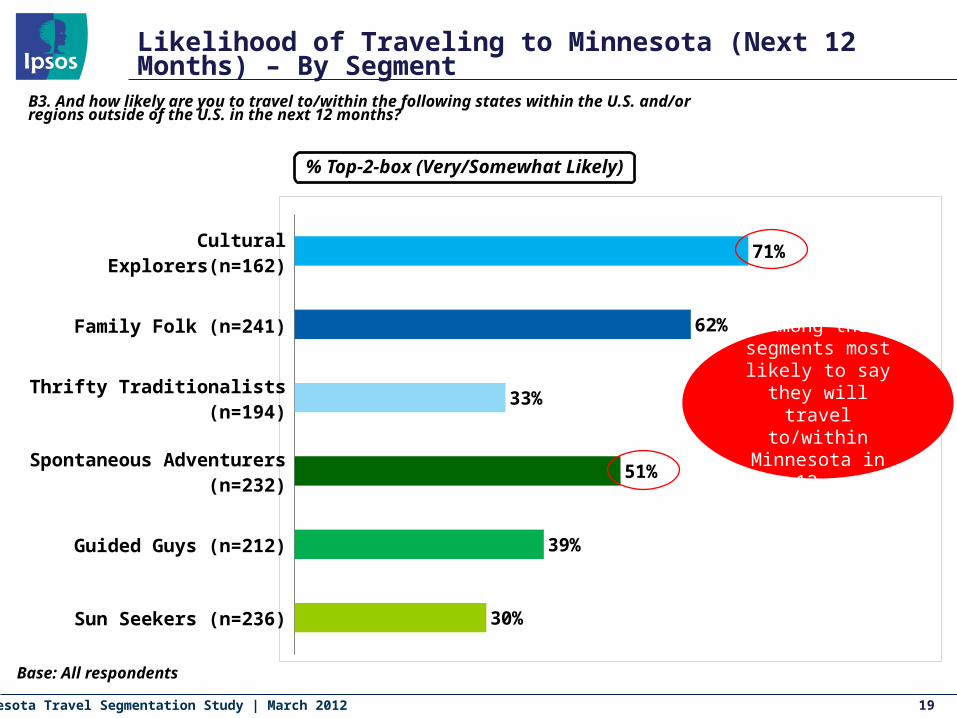

Likelihood of Traveling to Minnesota (Next 12 Months) – By Segment

19

Base: All respondents

% Top-2-box (Very/Somewhat Likely)

B3. And how likely are you to travel to/within the following states within the U.S. and/or regions outside of the U.S. in the next 12 months?

71%

62%

33%

51%

39%

30%

Cultural Explorers(n=162)

Family Folk (n=241)

Thrifty Traditionalists (n=194)

Spontaneous Adventurers (n=232)

Guided Guys (n=212)

Sun Seekers (n=236)

Among the segments most likely to say they

will travel to/within Minnesota in next 12

months

Minnesota Travel Segmentation Study | March 2012

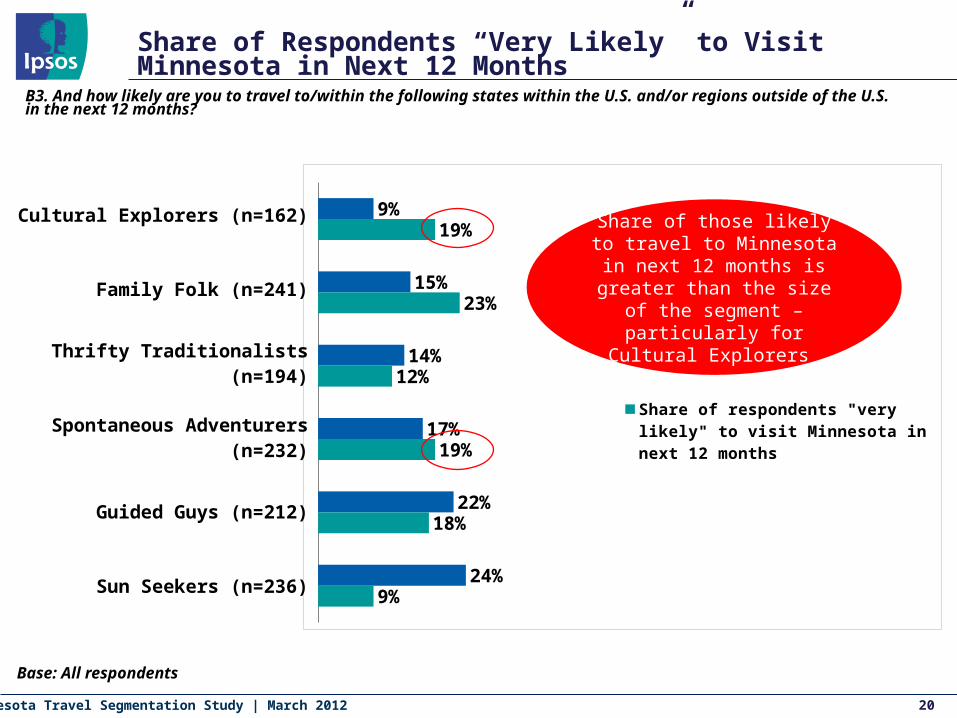

Share of Respondents “Very Likely” to Visit Minnesota in Next 12 Months

20

Base: All respondents

B3. And how likely are you to travel to/within the following states within the U.S. and/or regions outside of the U.S. in the next 12 months?

9%

15%

14%

17%

22%

24%

19%

23%

12%

19%

18%

9%

Share of respondents "very likely" to visit Minnesota in next 12 months

Size of Segment

Cultural Explorers (n=162)

Family Folk (n=241)

Thrifty Traditionalists (n=194)

Spontaneous Adventurers (n=232)

Guided Guys (n=212)

Sun Seekers (n=236)

Share of those likely to travel to Minnesota in next 12 months is

greater than the size of the segment – particularly for

Cultural Explorers

Minnesota Travel Segmentation Study | March 2012

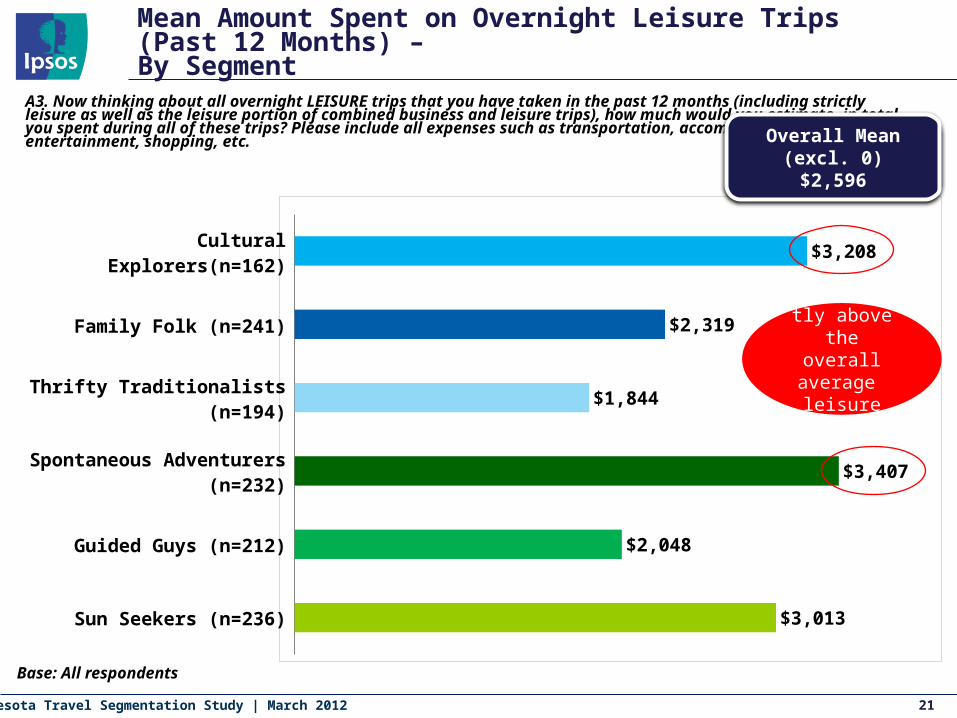

Mean Amount Spent on Overnight Leisure Trips (Past 12 Months) – By Segment

21

Base: All respondents

$3,208

$2,319

$1,844

$3,407

$2,048

$3,013

A3. Now thinking about all overnight LEISURE trips that you have taken in the past 12 months (including strictly leisure as well as the leisure portion of combined business and leisure trips), how much would you estimate, in total, you spent during all of these trips? Please include all expenses such as transportation, accommodation, food, entertainment, shopping, etc.

Cultural Explorers(n=162)

Family Folk (n=241)

Thrifty Traditionalists (n=194)

Spontaneous Adventurers (n=232)

Guided Guys (n=212)

Sun Seekers (n=236)

Overall Mean (excl. 0)$2,596

Significantly above the

overall average leisure spend

Minnesota Travel Segmentation Study | March 2012

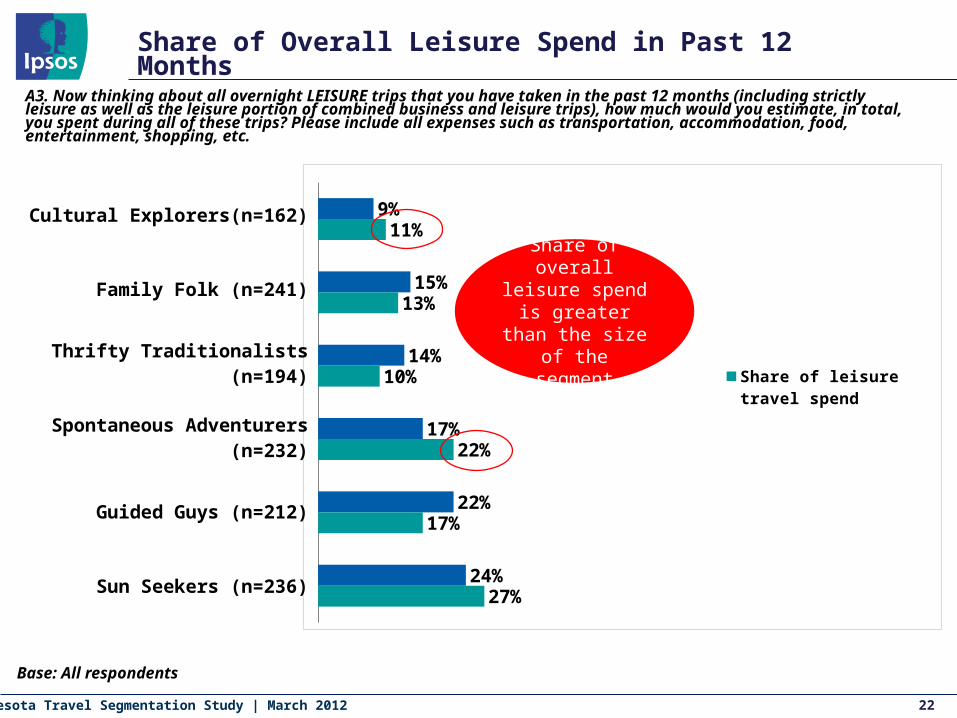

Share of Overall Leisure Spend in Past 12 Months

22

Base: All respondents

A3. Now thinking about all overnight LEISURE trips that you have taken in the past 12 months (including strictly leisure as well as the leisure portion of combined business and leisure trips), how much would you estimate, in total, you spent during all of these trips? Please include all expenses such as transportation, accommodation, food, entertainment, shopping, etc.

9%

15%

14%

17%

22%

24%

11%

13%

10%

22%

17%

27%

Share of leisure travel spendSize of Segment

Cultural Explorers(n=162)

Family Folk (n=241)

Thrifty Traditionalists (n=194)

Spontaneous Adventurers (n=232)

Guided Guys (n=212)

Sun Seekers (n=236)

Share of overall leisure spend is greater than the

size of the segment

Minnesota Travel Segmentation Study | March 2012

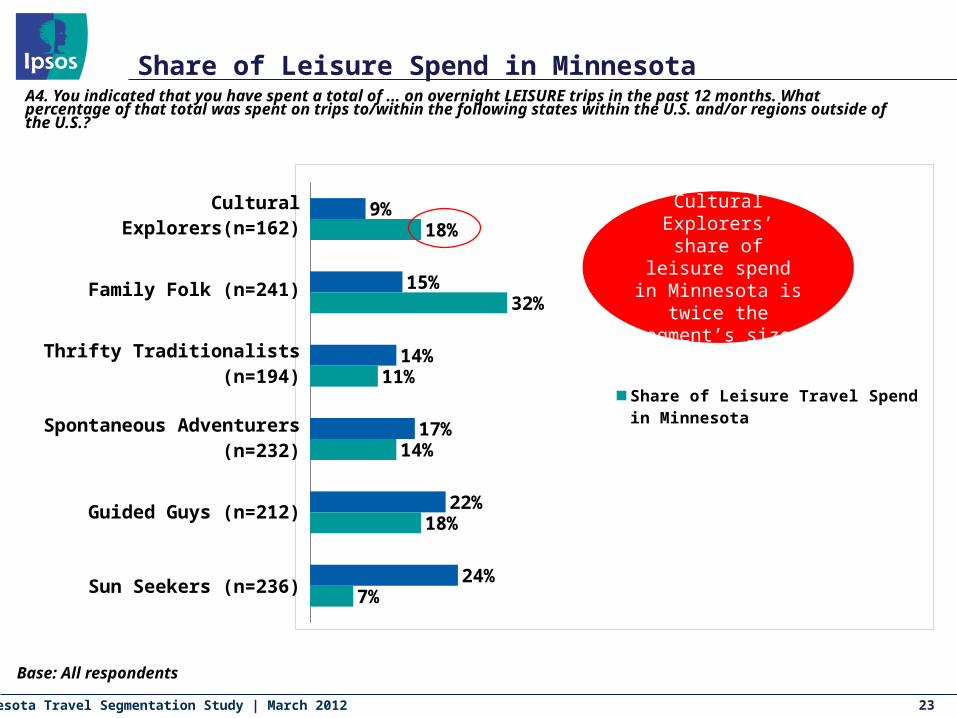

Share of Leisure Spend in Minnesota

23

Base: All respondents

A4. You indicated that you have spent a total of ... on overnight LEISURE trips in the past 12 months. What percentage of that total was spent on trips to/within the following states within the U.S. and/or regions outside of the U.S.?

9%

15%

14%

17%

22%

24%

18%

32%

11%

14%

18%

7%

Share of Leisure Travel Spend in MinnesotaSize of Segment

Cultural Explorers(n=162)

Family Folk (n=241)

Thrifty Traditionalists (n=194)

Spontaneous Adventurers (n=232)

Guided Guys (n=212)

Sun Seekers (n=236)

Cultural Explorers’ share of leisure spend in Minnesota is twice

the segment’s size

Minnesota Travel Segmentation Study | March 2012

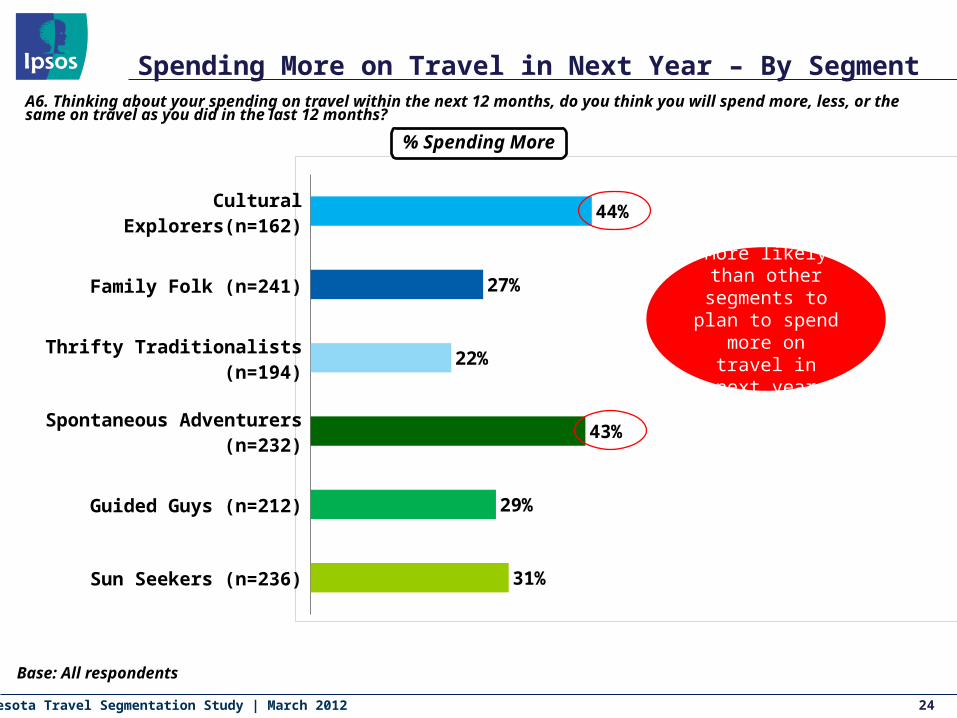

Spending More on Travel in Next Year – By Segment

24

Base: All respondents

44%

27%

22%

43%

29%

31%

Cultural Explorers(n=162)

Family Folk (n=241)

Thrifty Traditionalists (n=194)

Spontaneous Adventurers (n=232)

Guided Guys (n=212)

Sun Seekers (n=236)

A6. Thinking about your spending on travel within the next 12 months, do you think you will spend more, less, or the same on travel as you did in the last 12 months?

% Spending More

More likely than other segments to

plan to spend more on travel in next

year

Minnesota Travel Segmentation Study | March 2012

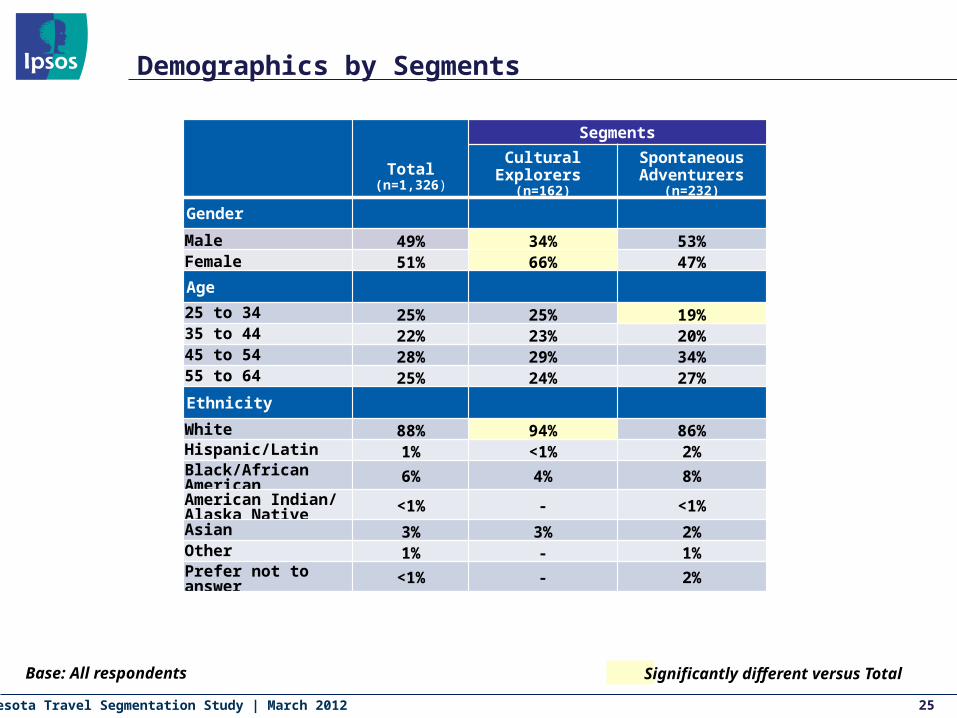

Demographics by Segments

25

Base: All respondents Significantly different versus Total

Total(n=1,326)

Segments

Cultural Explorers (n=162)

Spontaneous Adventurers

(n=232)

Gender

Male 49% 34% 53%Female 51% 66% 47%

Age

25 to 34 25% 25% 19%35 to 44 22% 23% 20%45 to 54 28% 29% 34%55 to 64 25% 24% 27%

Ethnicity

White 88% 94% 86%Hispanic/Latin 1% <1% 2%Black/African American 6% 4% 8%American Indian/Alaska Native <1% - <1%

Asian 3% 3% 2%Other 1% - 1%Prefer not to answer <1% - 2%

Minnesota Travel Segmentation Study | March 2012

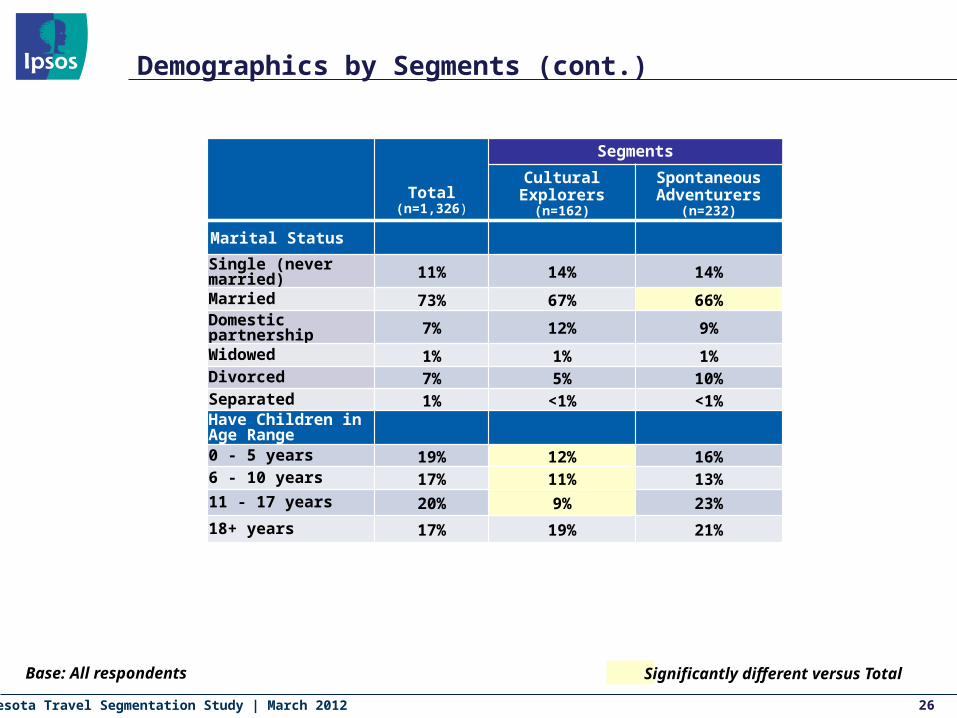

Demographics by Segments (cont.)

26

Base: All respondents

Total(n=1,326)

Segments

Cultural Explorers(n=162)

Spontaneous Adventurers

(n=232)

Marital Status

Single (never married) 11% 14% 14%

Married 73% 67% 66%

Domestic partnership 7% 12% 9%

Widowed 1% 1% 1%Divorced 7% 5% 10%Separated 1% <1% <1%Have Children in Age Range0 - 5 years 19% 12% 16%6 - 10 years 17% 11% 13%11 - 17 years 20% 9% 23%

18+ years 17% 19% 21%

Significantly different versus Total

Minnesota Travel Segmentation Study | March 2012

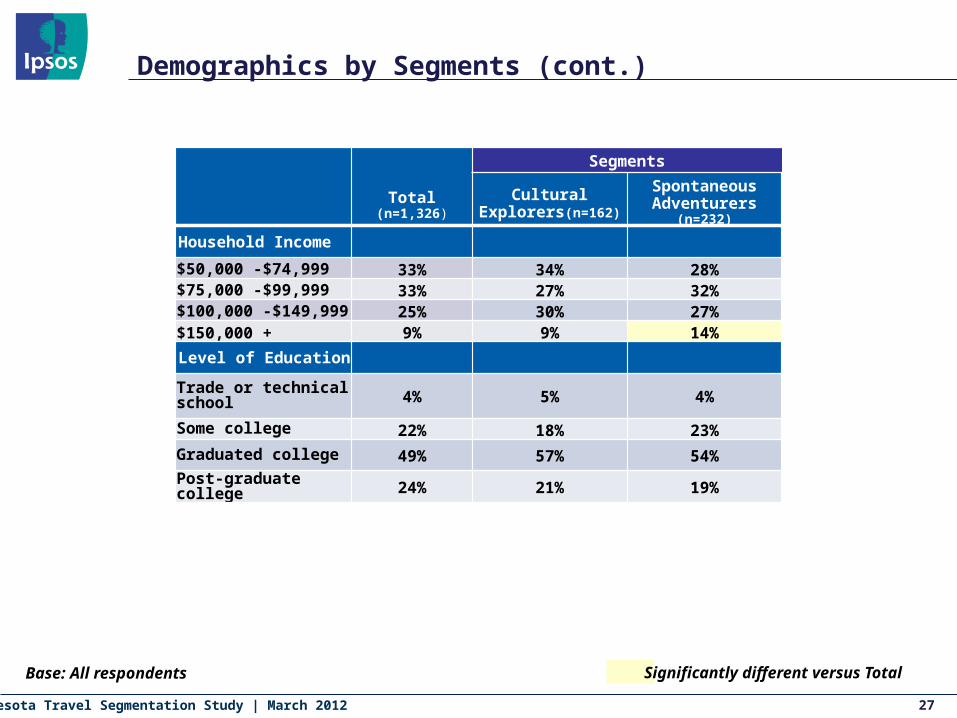

Demographics by Segments (cont.)

27

Base: All respondents

Total(n=1,326)

Segments

Cultural Explorers(n=162)

Spontaneous Adventurers

(n=232)

Household Income

$50,000 -$74,999 33% 34% 28%$75,000 -$99,999 33% 27% 32%$100,000 -$149,999 25% 30% 27%$150,000 + 9% 9% 14%

Level of Education

Trade or technical school 4% 5% 4%

Some college 22% 18% 23%

Graduated college 49% 57% 54%

Post-graduate college 24% 21% 19%

Significantly different versus Total

Nobody’s Unpredictable

What Factors Drive The Segmentation?

Minnesota Travel Segmentation Study | March 2012 29

Key Segments

Cultural Explorers and Spontaneous Adventurers offer significant potential as key segments based on:

Annual Household Income: Spontaneous Adventurers are more likely than the total to have an annual household income of $150,000 or more. Cultural Explorers have more than one-third (39%) within this group who earn at least $100,000 per year.

Travel Spend: Both segments have the highest average spend on leisure travel in the past 12 months among all six segments (Spontaneous Adventurers followed by Cultural Explorers).

Interest in Travel to Minnesota: Both segments are among the most likely of all six segments to say they are interested in traveling to/within Minnesota in the future – at least three-quarters within each segment says they are ‘very’ or ‘somewhat’ interested in traveling to Minnesota.

Minnesota Travel Segmentation Study | March 2012

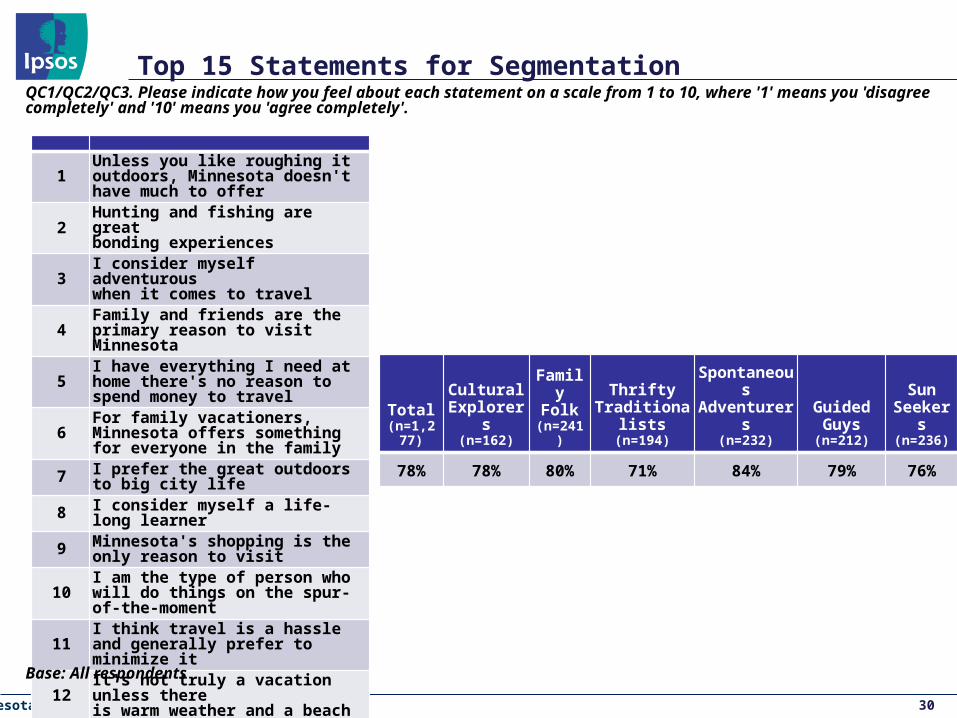

Top 15 Statements for Segmentation

1 Unless you like roughing it outdoors, Minnesota doesn't have much to offer

2 Hunting and fishing are great bonding experiences

3 I consider myself adventurous when it comes to travel

4 Family and friends are the primary reason to visit Minnesota

5 I have everything I need at home there's no reason to spend money to travel

6 For family vacationers, Minnesota offers something for everyone in the family

7 I prefer the great outdoors to big city life

8 I consider myself a life-long learner

9 Minnesota's shopping is the only reason to visit

10 I am the type of person who will do things on the spur-of-the-moment

11 I think travel is a hassle and generally prefer to minimize it

12 It's not truly a vacation unless there is warm weather and a beach

13 I like to be the first among my friends to try something new

14 Minnesota has a rich history and interesting historical sites

15 For a truly romantic getaway, you need to leave the city

30

QC1/QC2/QC3. Please indicate how you feel about each statement on a scale from 1 to 10, where '1' means you 'disagree completely' and '10' means you 'agree completely'.

Base: All respondents

Total(n=1,277)

Cultural Explorers

(n=162)

Family Folk

(n=241)

Thrifty Traditionalists

(n=194)

Spontaneous Adventurers

(n=232)

Guided Guys

(n=212)

Sun Seekers(n=236)

78% 78% 80% 71% 84% 79% 76%

Minnesota Travel Segmentation Study | March 2012

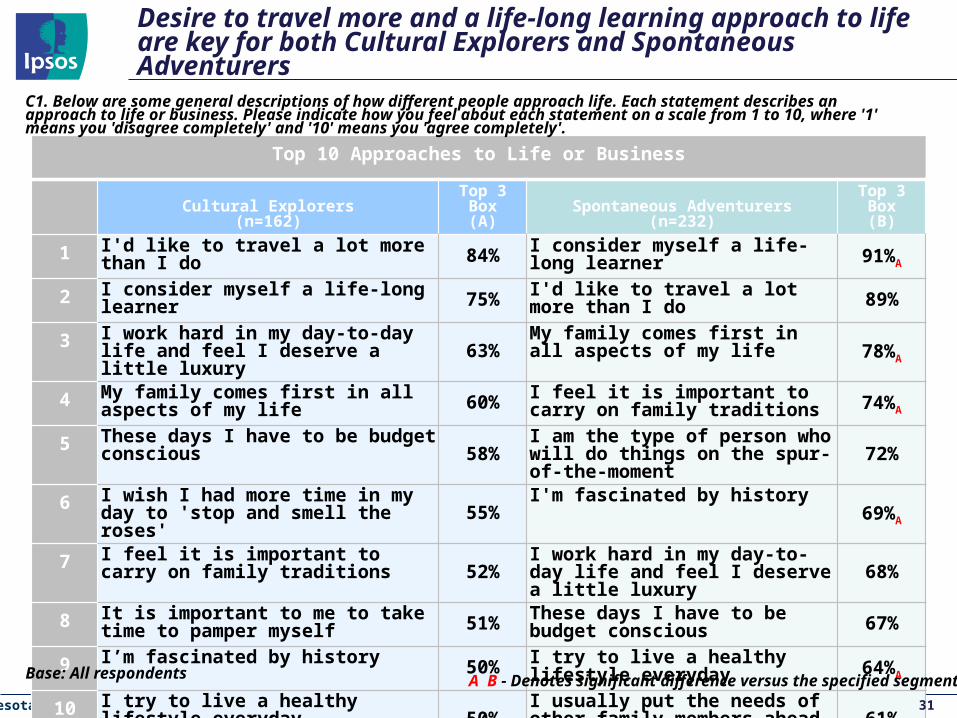

Desire to travel more and a life-long learning approach to life are key for both Cultural Explorers and Spontaneous Adventurers

Top 10 Approaches to Life or Business

Cultural Explorers(n=162)

Top 3 Box(A)

Spontaneous Adventurers(n=232)

Top 3 Box(B)

1 I'd like to travel a lot more than I do84%

I consider myself a life-long learner91%A

2 I consider myself a life-long learner75%

I'd like to travel a lot more than I do89%

3 I work hard in my day-to-day life and feel I deserve a little luxury 63%

My family comes first in all aspects of my life 78%A

4 My family comes first in all aspects of my life 60%

I feel it is important to carry on family traditions 74%A

5 These days I have to be budget conscious58%

I am the type of person who will do things on the spur-of-the-moment 72%

6 I wish I had more time in my day to 'stop and smell the roses' 55%

I'm fascinated by history69%A

7 I feel it is important to carry on family traditions 52%

I work hard in my day-to-day life and feel I deserve a little luxury 68%

8 It is important to me to take time to pamper myself 51%

These days I have to be budget conscious 67%

9 I’m fascinated by history50%

I try to live a healthy lifestyle everyday64%A

10 I try to live a healthy lifestyle everyday50%

I usually put the needs of other family members ahead of my own 61%

31

Base: All respondents

C1. Below are some general descriptions of how different people approach life. Each statement describes an approach to life or business. Please indicate how you feel about each statement on a scale from 1 to 10, where '1' means you 'disagree completely' and '10' means you 'agree completely'.

A B - Denotes significant difference versus the specified segment

Minnesota Travel Segmentation Study | March 2012

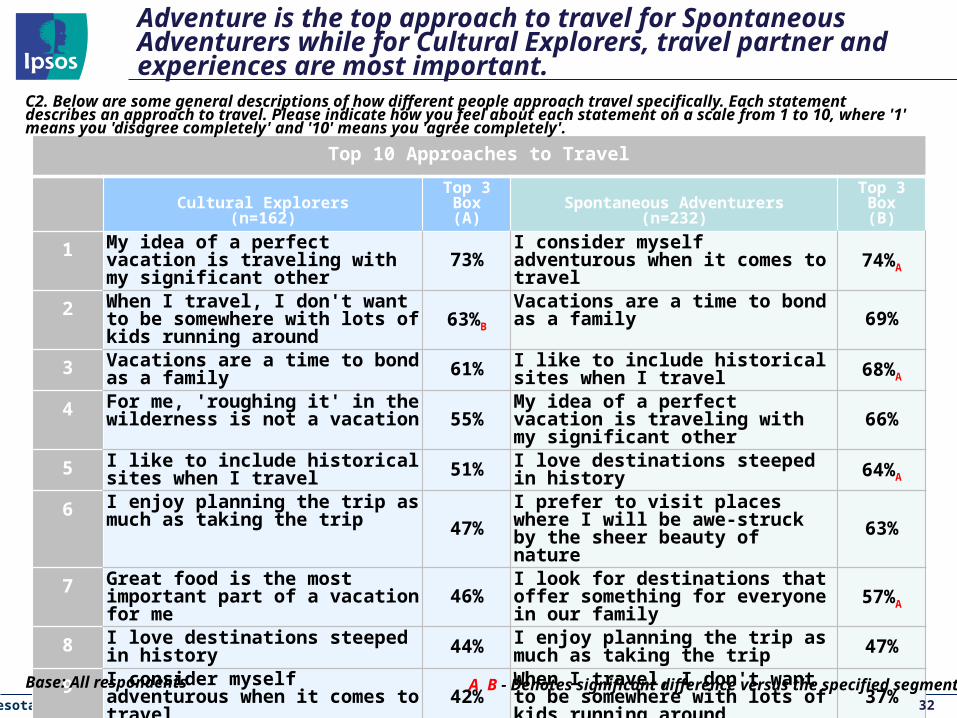

Adventure is the top approach to travel for Spontaneous Adventurers while for Cultural Explorers, travel partner and experiences are most important.

Top 10 Approaches to Travel

Cultural Explorers(n=162)

Top 3 Box(A)

Spontaneous Adventurers(n=232)

Top 3 Box(B)

1 My idea of a perfect vacation is traveling with my significant other 73% I consider myself adventurous when it

comes to travel 74%A

2 When I travel, I don't want to be somewhere with lots of kids running around 63%B

Vacations are a time to bond as a family69%

3 Vacations are a time to bond as a family 61% I like to include historical sites when I travel 68%A

4 For me, 'roughing it' in the wilderness is not a vacation 55% My idea of a perfect vacation is traveling

with my significant other 66%

5 I like to include historical sites when I travel 51% I love destinations steeped in history

64%A

6 I enjoy planning the trip as much as taking the trip 47%

I prefer to visit places where I will be awe-struck by the sheer beauty of nature 63%

7 Great food is the most important part of a vacation for me 46% I look for destinations that offer

something for everyone in our family 57%A

8 I love destinations steeped in history 44% I enjoy planning the trip as much as taking the trip 47%

9 I consider myself adventurous when it comes to travel 42%

When I travel, I don't want to be somewhere with lots of kids running around 37%

10 I look for destinations that offer something for everyone in our family 40% I generally plan travel around

opportunities to visit family and friends 36%

32

Base: All respondents

C2. Below are some general descriptions of how different people approach travel specifically. Each statement describes an approach to travel. Please indicate how you feel about each statement on a scale from 1 to 10, where '1' means you 'disagree completely' and '10' means you 'agree completely'.

A B - Denotes significant difference versus the specified segment

Minnesota Travel Segmentation Study | March 2012

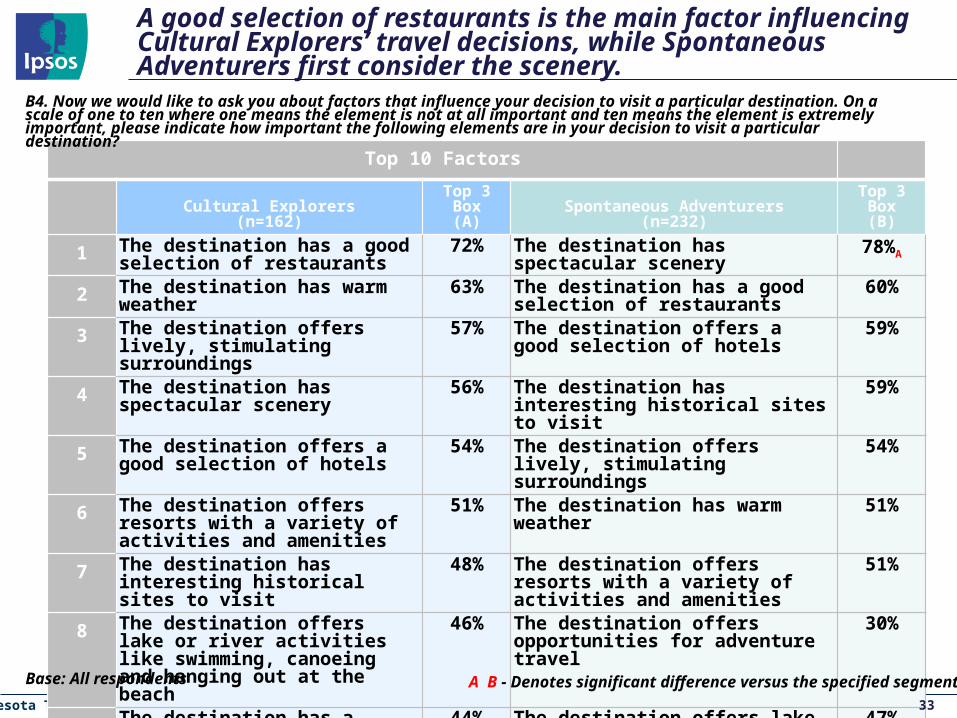

A good selection of restaurants is the main factor influencing Cultural Explorers’ travel decisions, while Spontaneous Adventurers first consider the scenery.

Top 10 Factors

Cultural Explorers(n=162)

Top 3 Box(A)

Spontaneous Adventurers(n=232)

Top 3 Box(B)

1 The destination has a good selection of restaurants

72% The destination has spectacular scenery 78%A

2 The destination has warm weather 63% The destination has a good selection of restaurants

60%

3 The destination offers lively, stimulating surroundings

57% The destination offers a good selection of hotels

59%

4 The destination has spectacular scenery

56% The destination has interesting historical sites to visit

59%

5 The destination offers a good selection of hotels

54% The destination offers lively, stimulating surroundings

54%

6 The destination offers resorts with a variety of activities and amenities

51% The destination has warm weather 51%

7 The destination has interesting historical sites to visit

48% The destination offers resorts with a variety of activities and amenities

51%

8 The destination offers lake or river activities like swimming, canoeing and hanging out at the beach

46% The destination offers opportunities for adventure travel

30%

9 The destination has a variety of arts and cultural events (theater, museums, plays)

44% The destination offers lake or river activities like swimming, canoeing and hanging out at the beach

47%

10 The destination offers fine dining 44% The destination offers a variety of outdoor recreational activities (such as hiking, biking, golfing)

46%

33

Base: All respondents

B4. Now we would like to ask you about factors that influence your decision to visit a particular destination. On a scale of one to ten where one means the element is not at all important and ten means the element is extremely important, please indicate how important the following elements are in your decision to visit a particular destination?

A B - Denotes significant difference versus the specified segment

Minnesota Travel Segmentation Study | March 2012 34

Focus Group Findings – Approaches to Life and TravelCultural Explorers described their approach to life and travel in the following

ways, showing they place importance on travel as an opportunity to ‘splurge’ and indulge themselves, as well as an escape from the day-to-day routine. “Vacations are where I splurge” “We look for quality” “We’re not cheap” “We’re not lower class. We are spending a good amount of money on travel,

but we look on Priceline for value…we’re educated” “Splurge more…vacation is your time to be different than you normally are” “More selfish on vacation because you don’t have to tend to your regular

duties in life” “I want to leave my life at home”

This group is also looking for the opportunity to experience new and exciting things:

“I look at vacations as an opportunity to get away and explore. If I want a vacation that’s relaxing I go to a place I’ve already been”.

“I’m looking for something different and memorable. I don’t want to just be stuck in my own world”.

Minnesota Travel Segmentation Study | March 2012 35

Focus Group Findings – Approaches to Life and Travel

Cultural Explorers in both Milwaukee and Minneapolis also noted that they enjoyed the trip planning phase: “I love planning a trip…it’s lots of fun” “If you can enjoy the planning, it’s almost like spreading out the vacation. It

extends the fun”

Minnesota Travel Segmentation Study | March 2012 36

Focus Group Findings – Approaches to Life and Travel

Spontaneous Adventurers also mentioned ‘splurging’ on travel, while many in this segment mentioned family as playing a role: “I’m blue collar with caviar dreams…we like to splurge on vacation” “Frugal in everyday life so I can travel” “I’m into rugged sophistication” “I’m family oriented” “I want to make memories with the family that are fun”

Spontaneous Adventurers also noted their attraction to the adventurous side of travel: “I’m looking for an experience” “Looking to expand our horizons” and “Versatile, adaptable and curious”

This group also highlighted their overall penchant for travel/getaways: “I go on vacation a lot more frequently than other people I know” “I get away a lot more than my friends do, even if it’s just for the weekend”.

Minnesota Travel Segmentation Study | March 2012

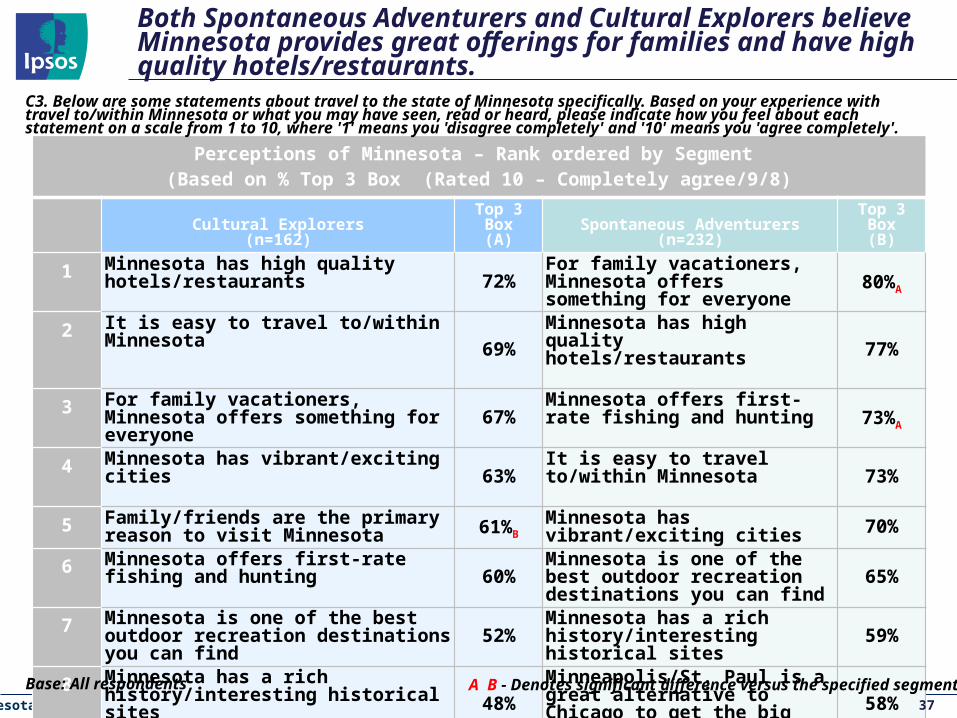

Both Spontaneous Adventurers and Cultural Explorers believe Minnesota provides great offerings for families and have high quality hotels/restaurants.

Perceptions of Minnesota – Rank ordered by Segment (Based on % Top 3 Box (Rated 10 – Completely agree/9/8)

Cultural Explorers(n=162)

Top 3 Box(A)

Spontaneous Adventurers(n=232)

Top 3 Box(B)

1 Minnesota has high quality hotels/restaurants 72% For family vacationers, Minnesota

offers something for everyone 80%A

2 It is easy to travel to/within Minnesota69%

Minnesota has high quality hotels/restaurants 77%

3 For family vacationers, Minnesota offers something for everyone 67% Minnesota offers first-rate fishing

and hunting 73%A

4 Minnesota has vibrant/exciting cities63%

It is easy to travel to/within Minnesota 73%

5 Family/friends are the primary reason to visit Minnesota 61%B

Minnesota has vibrant/exciting cities 70%

6 Minnesota offers first-rate fishing and hunting 60% Minnesota is one of the best outdoor

recreation destinations you can find 65%

7 Minnesota is one of the best outdoor recreation destinations you can find 52% Minnesota has a rich

history/interesting historical sites 59%

8 Minnesota has a rich history/interesting historical sites 48%

Minneapolis/St. Paul is a great alternative to Chicago to get the big city experience

58%

9 Minneapolis/St. Paul is a great alternative to Chicago to get the big city experience 45% What makes Minnesota unique is

found in its small towns 28%

10 What makes Minnesota unique is found in its small towns 24% Family/friends are the primary

reason to visit Minnesota 23%

37

Base: All respondents

C3. Below are some statements about travel to the state of Minnesota specifically. Based on your experience with travel to/within Minnesota or what you may have seen, read or heard, please indicate how you feel about each statement on a scale from 1 to 10, where '1' means you 'disagree completely' and '10' means you 'agree completely'.

A B - Denotes significant difference versus the specified segment

Minnesota Travel Segmentation Study | March 2012

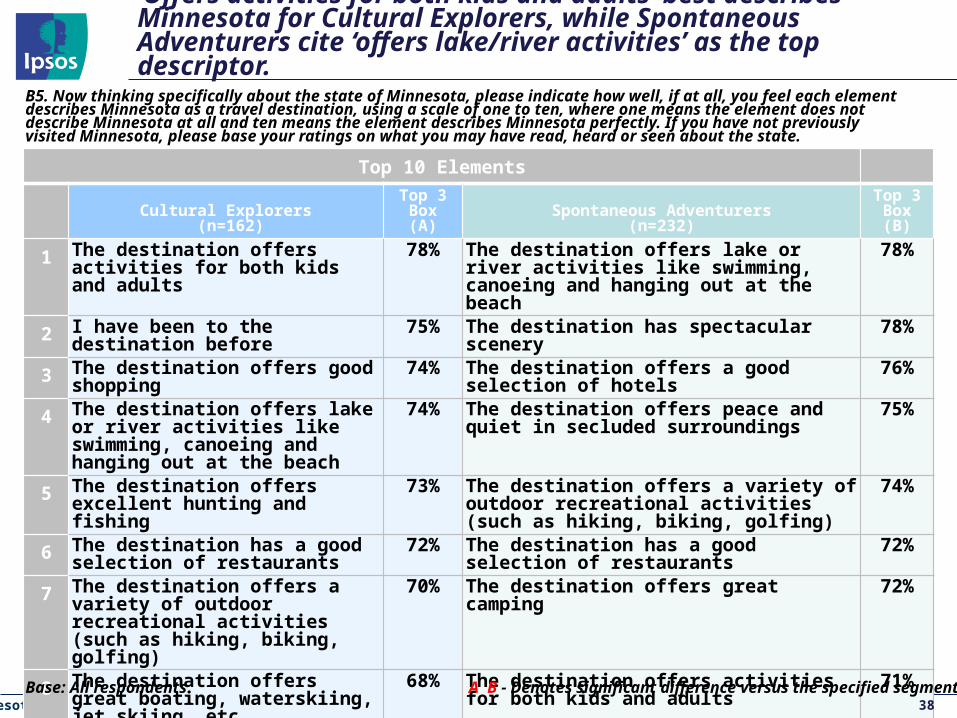

‘Offers activities for both kids and adults’ best describes Minnesota for Cultural Explorers, while Spontaneous Adventurers cite ‘offers lake/river activities’ as the top descriptor.

Top 10 Elements

Cultural Explorers (n=162)

Top 3 Box(A)

Spontaneous Adventurers(n=232)

Top 3 Box(B)

1 The destination offers activities for both kids and adults

78% The destination offers lake or river activities like swimming, canoeing and hanging out at the beach

78%

2 I have been to the destination before 75% The destination has spectacular scenery 78%

3 The destination offers good shopping 74% The destination offers a good selection of hotels 76%

4 The destination offers lake or river activities like swimming, canoeing and hanging out at the beach

74% The destination offers peace and quiet in secluded surroundings

75%

5 The destination offers excellent hunting and fishing

73% The destination offers a variety of outdoor recreational activities (such as hiking, biking, golfing)

74%

6 The destination has a good selection of restaurants

72% The destination has a good selection of restaurants

72%

7 The destination offers a variety of outdoor recreational activities (such as hiking, biking, golfing)

70% The destination offers great camping 72%

8 The destination offers great boating, waterskiing, jet skiing, etc.

68% The destination offers activities for both kids and adults

71%

9 The destination offers great camping 64% The destination offers great boating, waterskiing, jet skiing, etc.

69%

10 The destination is within a reasonable driving distance

63% The destination offers excellent hunting and fishing

68%

38Base: All respondents

B5. Now thinking specifically about the state of Minnesota, please indicate how well, if at all, you feel each element describes Minnesota as a travel destination, using a scale of one to ten, where one means the element does not describe Minnesota at all and ten means the element describes Minnesota perfectly. If you have not previously visited Minnesota, please base your ratings on what you may have read, heard or seen about the state.

A B - Denotes significant difference versus the specified segment

Minnesota Travel Segmentation Study | March 2012 39

Focus Group Findings – Perceptions of MinnesotaCultural Explorers in Milwaukee described their perceptions of Minnesota in the

following ways: “You have the excitement of the city, and the relaxation in terms of lakes and

parks and natural beauty” “I think the twin cities and I just can’t think of anything else” “I don’t ever feel threatened by the city, because it feels like Milwaukee” “Minnesota is comfortable, but a little not comfortable. Minnesota isn’t

intimidating, you’re not spending a lot of money, but it’s a little different, stuff you don’t ordinarily see”.

“…Balanced and entertained. There’s so much to do and something for everyone”

“You can have an adventure. It’s an attractive city and we travel with family and friends..”

Cultural Explorers in Minneapolis described Minnesota in the following ways: “Minnesota is nice” (people are nice, sincere) “Minnesota is our outdoor getaway” (For their urban getaways, this group

mentioned destinations like Chicago, New York and Los Angeles) Several Cultural Explorers in Minnesota noted they had done a ‘couples

weekend’ in Minneapolis.

Minnesota Travel Segmentation Study | March 2012 40

Focus Group Findings – Perceptions of MinnesotaSpontaneous Adventurers in Milwaukee also described Minnesota in terms of its

feeling of safety and warm atmosphere: “I know I’m going to be safe even if I’m in the city” “I think it’s a relaxing place. The times I’ve gone there’s the museum, it’s so

beautiful and it’s easy to get around” “It’s laid back and Midwest…I didn’t have to spend a lot to get there so now I can

spend on my activities” “It’s not commercial attractions, it’s not like Disney…it’s smaller towns and areas.

It’s inviting. There’s a close knit feel to it”Other Spontaneous Adventurers noted the variety that Minnesota has to offer:

“It’s spontaneous – I could be going to a water park one minute, walking downtown the next”.

Spontaneous Adventurers in Minneapolis described Minnesota in the following ways, reinforcing this segment’s sense of adventure: “Exploring together” “Exploring, learning new things, family time, peaceful”

Many in this segment also mention the beauty and scenery: “Four seasons” “Beauty everywhere” “Lots of lakes”.

Minnesota Travel Segmentation Study | March 2012

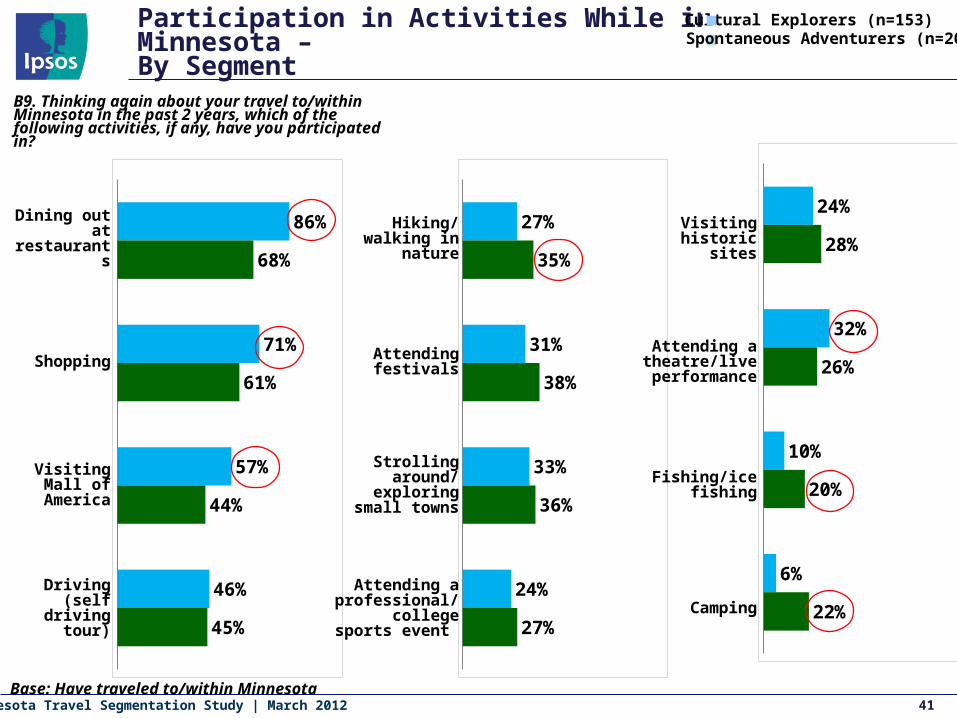

Participation in Activities While in Minnesota – By Segment

41Base: Have traveled to/within Minnesota

86%

71%

57%

46%

68%

61%

44%

45%

Dining out at restaurants

Shopping

Visiting Mall of America

Driving (self driving tour)

Cultural Explorers (n=153)Spontaneous Adventurers (n=202)

27%

31%

33%

24%

35%

38%

36%

27%

Hiking/walking in nature

Attending festivals

Strolling around/ exploring small

towns

Attending a professional/ college sports

event

24%

32%

10%

6%

28%

26%

20%

22%

Visiting historic sites

Attending a theatre/live

performance

Fishing/ice fishing

Camping

B9. Thinking again about your travel to/within Minnesota in the past 2 years, which of the following activities, if any, have you participated in?

Nobody’s Unpredictable

Finding Opportunities for Minnesota

Minnesota Travel Segmentation Study | March 2012

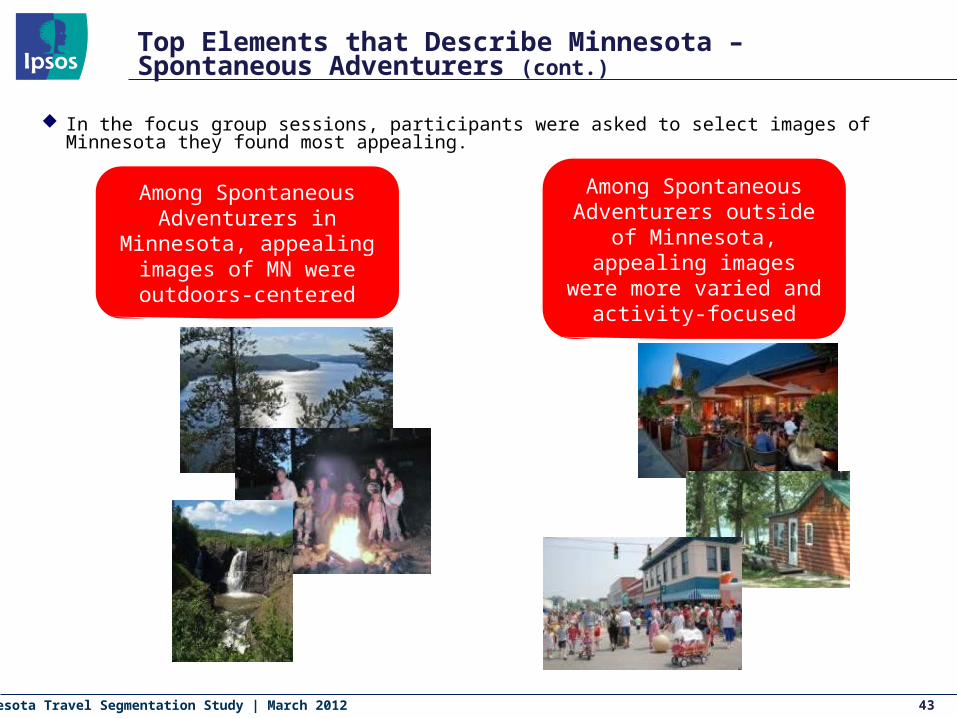

Top Elements that Describe Minnesota – Spontaneous Adventurers (cont.)

43

In the focus group sessions, participants were asked to select images of Minnesota they found most appealing.

Among Spontaneous Adventurers in Minnesota,

appealing images of MN were outdoors-centered

Among Spontaneous Adventurers outside of

Minnesota, appealing images were more varied and activity-

focused

Minnesota Travel Segmentation Study | March 2012

Top Elements that Describe Minnesota – Cultural Explorers (cont.)

44

Among Cultural Explorers in Minnesota, the most appealing

images focused heavily on urban

Outside of Minnesota, Cultural Explorers view the state as

more of a mix of urban and outdoor settings.

In the focus group sessions, participants were asked to select images that they felt represented Minnesota.

Minnesota Travel Segmentation Study | March 2012 45

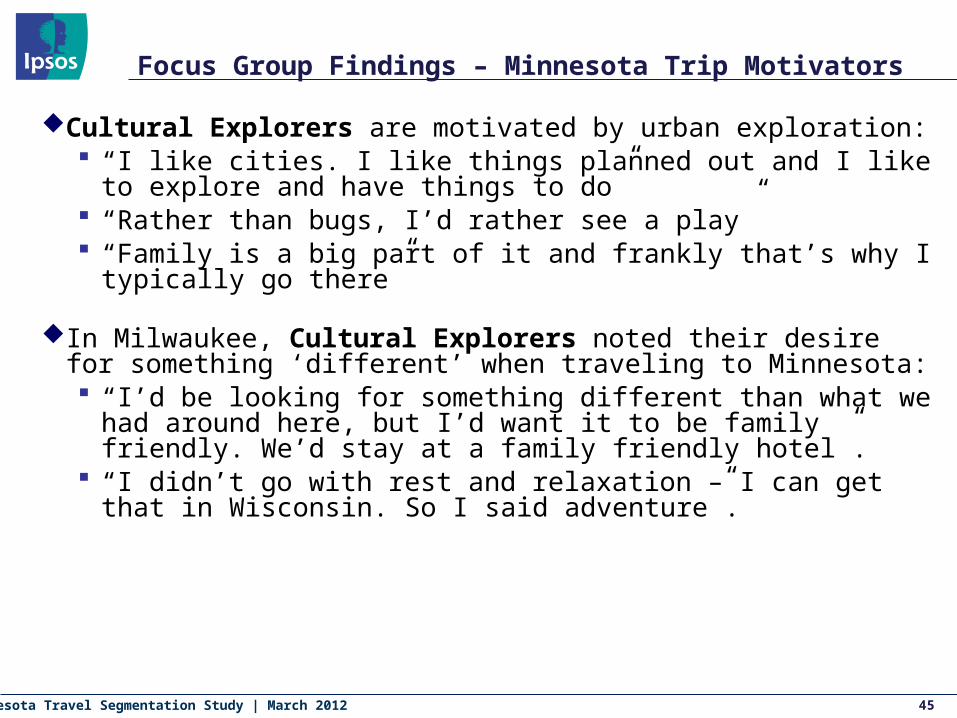

Focus Group Findings – Minnesota Trip Motivators

Cultural Explorers are motivated by urban exploration: “I like cities. I like things planned out and I like to explore and have things to

do” “Rather than bugs, I’d rather see a play” “Family is a big part of it and frankly that’s why I typically go there”

In Milwaukee, Cultural Explorers noted their desire for something ‘different’ when traveling to Minnesota: “I’d be looking for something different than what we had around here, but

I’d want it to be family friendly. We’d stay at a family friendly hotel”. “I didn’t go with rest and relaxation – I can get that in Wisconsin. So I said

adventure”.

Minnesota Travel Segmentation Study | March 2012

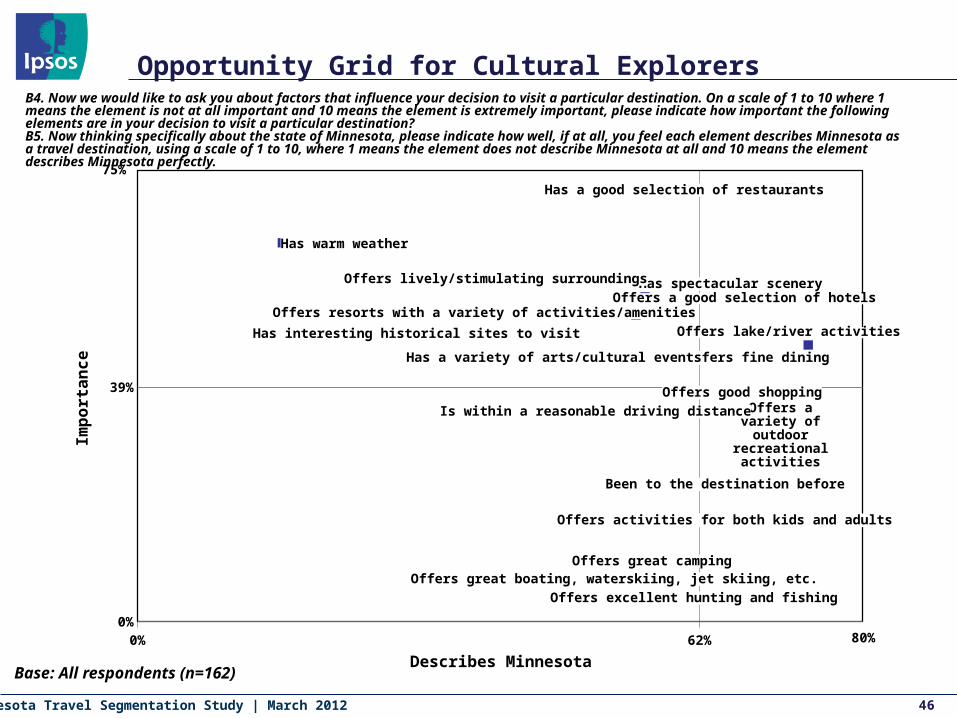

Opportunity Grid for Cultural Explorers

46

Base: All respondents (n=162)

B4. Now we would like to ask you about factors that influence your decision to visit a particular destination. On a scale of 1 to 10 where 1 means the element is not at all important and 10 means the element is extremely important, please indicate how important the following elements are in your decision to visit a particular destination?B5. Now thinking specifically about the state of Minnesota, please indicate how well, if at all, you feel each element describes Minnesota as a travel destination, using a scale of 1 to 10, where 1 means the element does not describe Minnesota at all and 10 means the element describes Minnesota perfectly.

0% 62%0%

39%

Describes Minnesota

Impo

rtan

ce

80%

Offers lake/river activities

Has spectacular sceneryOffers a good selection of hotels

Has a good selection of restaurants

Offers resorts with a variety of activities/amenities

Offers lively/stimulating surroundings

Offers fine diningHas a variety of arts/cultural events

Has interesting historical sites to visit

Has warm weather

Offers activities for both kids and adults

Been to the destination before

Offers good shopping

Offers excellent hunting and fishing

Offers a variety of outdoor recreational

activities

Offers great boating, waterskiing, jet skiing, etc.Offers great camping

Is within a reasonable driving distance

75%

Minnesota Travel Segmentation Study | March 2012 47

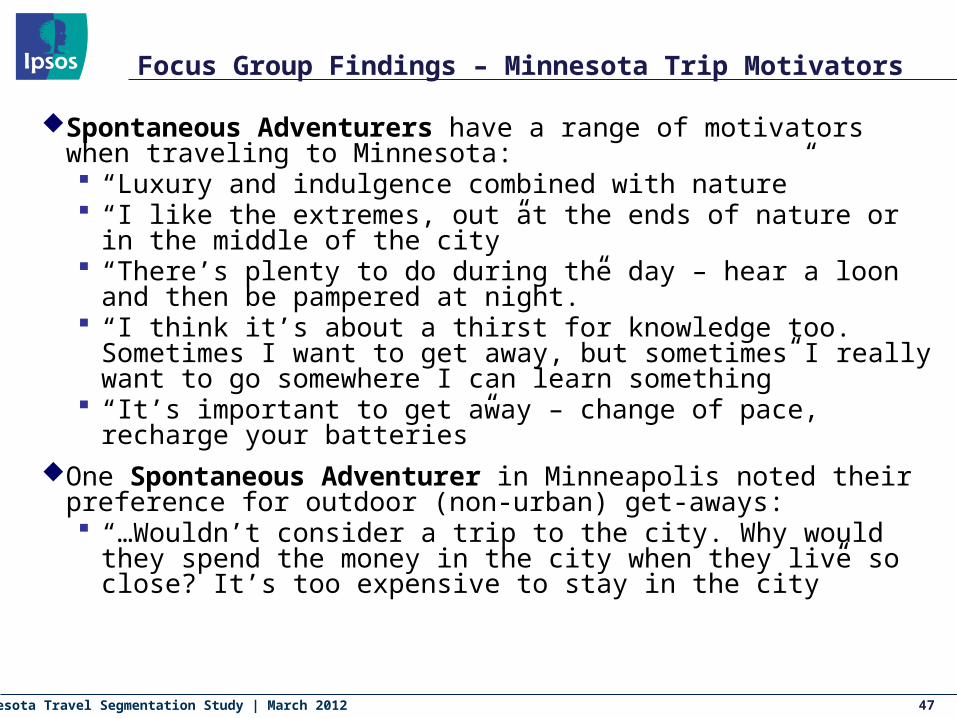

Focus Group Findings – Minnesota Trip Motivators

Spontaneous Adventurers have a range of motivators when traveling to Minnesota: “Luxury and indulgence combined with nature” “I like the extremes, out at the ends of nature or in the middle of the city” “There’s plenty to do during the day – hear a loon and then be pampered at

night.” “I think it’s about a thirst for knowledge too. Sometimes I want to get away,

but sometimes I really want to go somewhere I can learn something” “It’s important to get away – change of pace, recharge your batteries”

One Spontaneous Adventurer in Minneapolis noted their preference for outdoor (non-urban) get-aways: “…Wouldn’t consider a trip to the city. Why would they spend the money in

the city when they live so close? It’s too expensive to stay in the city”

Minnesota Travel Segmentation Study | March 2012

Opportunity Grid for Spontaneous Adventurers

48

Base: All respondents (n=232)

B4. Now we would like to ask you about factors that influence your decision to visit a particular destination. On a scale of 1 to 10 where 1 means the element is not at all important and 10 means the element is extremely important, please indicate how important the following elements are in your decision to visit a particular destination?B5. Now thinking specifically about the state of Minnesota, please indicate how well, if at all, you feel each element describes Minnesota as a travel destination, using a scale of 1 to 10, where 1 means the element does not describe Minnesota at all and 10 means the element describes Minnesota perfectly.

20% 66%10%

45%

80%

Describes Minnesota

Impo

rtan

ce

80%

Offers lake/river activities

Has spectacular scenery

Offers a good selection of hotelsHas a good selection of restaurants

Offers resorts with a variety of activities/amenitiesOffers lively/stimulating surroundings

Offers variety of outdoor recreational activitiesOffers opportunities for adventure travel

Has interesting historical sites to visit

Has warm weather

Offers peace and quiet

Offers great camping

Offers activities for both kids and adults

Offers great boating, waterskiing, jet skiing, etc.

Offers excellent hunting and fishing

Nobody’s Unpredictable

How Does Minnesota Attract and Communicate With These Segments?

Minnesota Travel Segmentation Study | March 2012 50

Communicating with the Key Segments

There appears to be tremendous opportunity, particularly in markets outside of Minnesota to communicate all that the state has to offer visitors. Numerous focus group participants in Milwaukee stated that they had not heard much/any marketing or communications about the state of Minnesota, especially compared to advertising they have seen for other states.

In terms of messaging, communications that focus on all that the urban center of Minneapolis/St. Paul has to offer (great restaurants, cultural activities, vibrant city life, etc.) should appeal to both Cultural Explorers and Spontaneous Adventurers alike as both segments find urban-oriented, exciting activities appealing.

In addition to showing a Minnesota vacation as “fun,” positioning the vacation as relaxing is important as well as both segments showed a propensity to choose ‘relaxation’ to describe their ideal Minnesota vacation.

Historical elements of a destination also appeal to both segments. Highlighting Minnesota’s historical sites, particularly ones located in urban centers, will help position the state as a destination of interest in this area.

Minnesota Travel Segmentation Study | March 2012 51

Communicating with the Key Segments

Cultural Explorers:Any communications targeting this group should focus on the urban setting of

Minneapolis/St. Paul and the ‘first class’ offerings (e.g. restaurants, hotels, nightlife) that can be found there. Cultural Explorers are looking for these elements in a travel destination, along with vibrant, lively surroundings.

This segment wants to be entertained and enriched. The activities they choose are for their entertainment – cities, theater, etc… Any communication will need to emphasize that Minnesota is a destination where they can get away from their stressful lives and let life come to them.

Minnesota Travel Segmentation Study | March 2012 52

Communicating with the Key Segments

Spontaneous Adventurers:This segment likes to escape the city and enjoy outdoor adventures, but are

also drawn to urban settings and activities. As a result, communications that center on getaways in the great outdoors (e.g. cabin or lakeside retreat) or small town excursions should be included when targeting this group.

Highlighting the dichotomy of activities that Minnesota has to offer will be key in connecting with Spontaneous Adventurers as these travelers look to experience different activities and engage in a wide range of experiences when they have the opportunity.

Communications should also reinforce the idea that getaways can be had for weekends/long weekends – a long vacation is not necessary to experience what Minnesota has to offer, as Spontaneous Adventurers like to take short getaways and do things ‘spur-of-the-moment’.

Minnesota Travel Segmentation Study | March 2012 53

Communicating with the Key Segments

Communication vehicles:Both Spontaneous Adventurers and Cultural Explorers say online resources are

‘very important’ when planning or taking a trip, particularly search engines such as Google. Moreover, both segments show a strong likelihood to own a Smartphone. As a result, online communications, such as sponsored ads on Google, would be an effective way to reach both segments.

Also it is critical to guarantee that Minnesota destinations appear on Google key word searches.

Official State Tourism Agency websites, group discount sites (such as groupon.com) and lodging websites are also important online resources for the Spontaneous Adventurers. Marketing through these channels should be more tailored towards the wants and needs of this particular segment.

Outside of online resources, friends and family and word-of-mouth are also important resources for both segments when considering or choosing a destination. By reaching out to Spontaneous Adventurers and Cultural Explorers and making Minnesota ‘top of mind’ as a vacation destination, friends and family may become advocates for travel to/within Minnesota.

Minnesota Travel Segmentation Study | March 2012

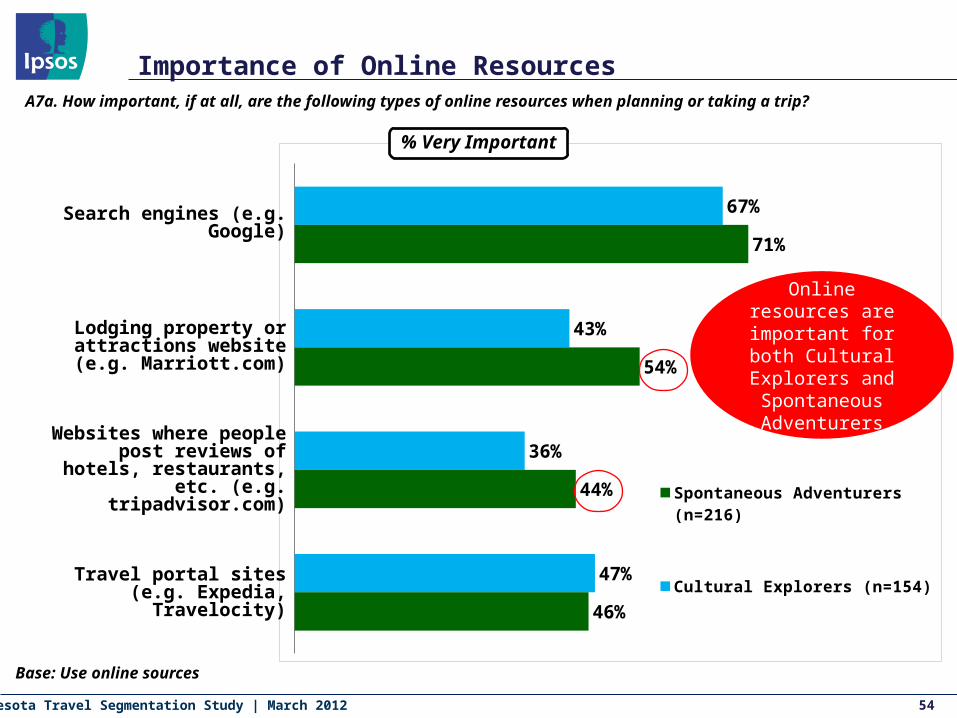

Importance of Online Resources

54

Base: Use online sources

67%

43%

36%

47%

71%

54%

44%

46%

Spontaneous Adventurers (n=216)

Cultural Explorers (n=154)

A7a. How important, if at all, are the following types of online resources when planning or taking a trip?

% Very Important

Search engines (e.g. Google)

Lodging property or attractions website (e.g. Marriott.com)

Websites where people post reviews of hotels, restaurants,

etc. (e.g. tripadvisor.com)

Travel portal sites (e.g. Expedia, Travelocity)

Online resources are important for both

Cultural Explorers and Spontaneous Adventurers

Minnesota Travel Segmentation Study | March 2012

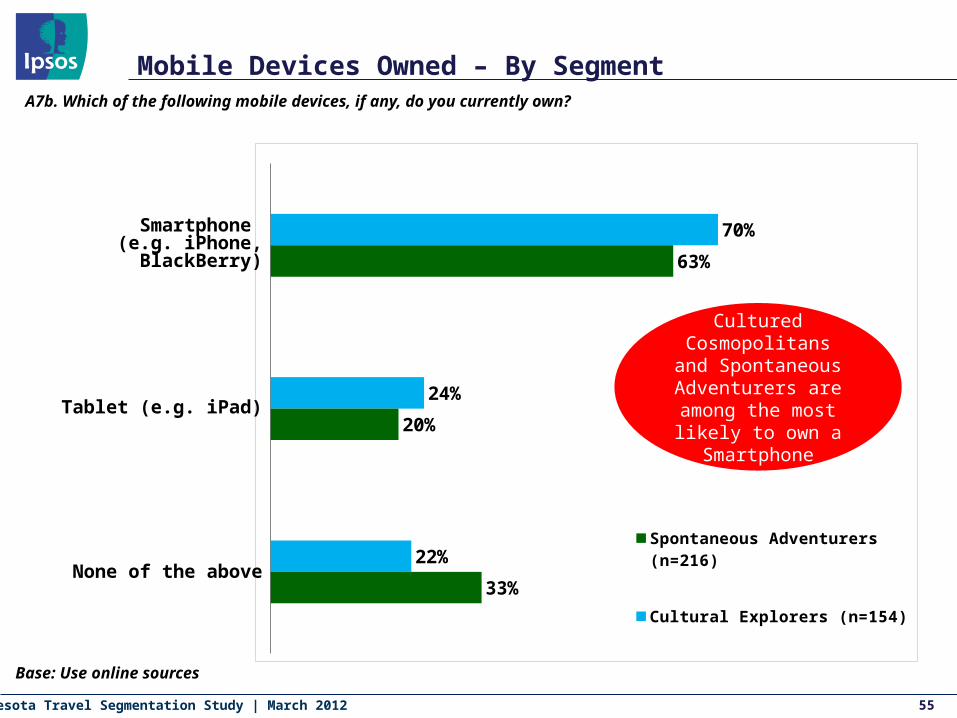

Mobile Devices Owned – By Segment

55

Base: Use online sources

70%

24%

22%

63%

20%

33%

Spontaneous Adventurers (n=216)

Cultural Explorers (n=154)

Smartphone (e.g. iPhone, BlackBerry)

Tablet (e.g. iPad)

None of the above

A7b. Which of the following mobile devices, if any, do you currently own?

Cultured Cosmopolitans and Spontaneous

Adventurers are among the most likely to own a

Smartphone

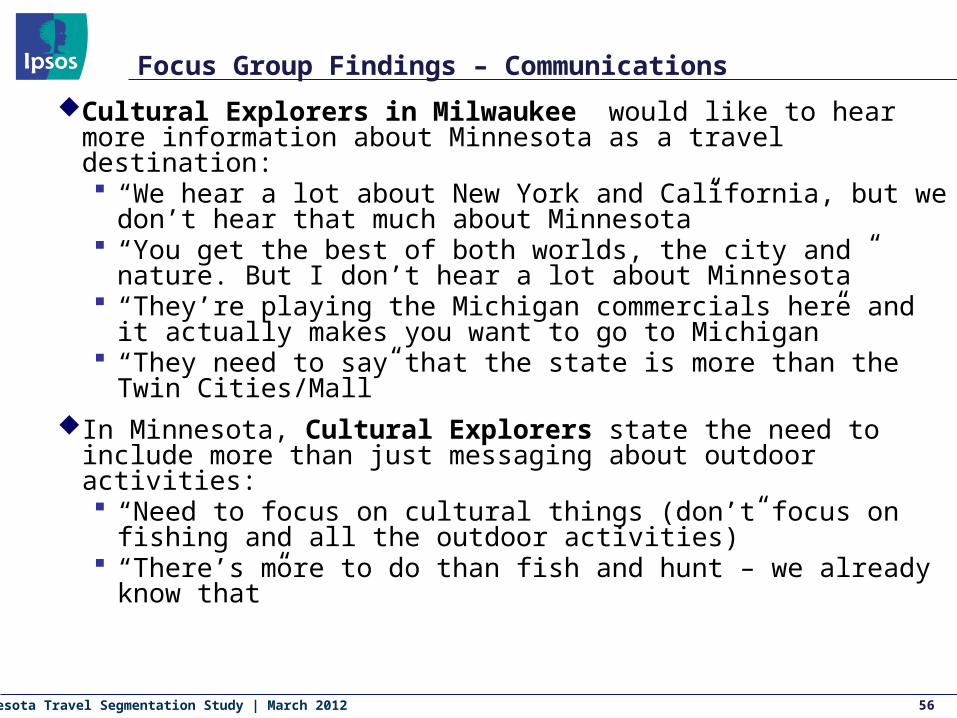

Minnesota Travel Segmentation Study | March 2012 56

Focus Group Findings – CommunicationsCultural Explorers in Milwaukee would like to hear more information about

Minnesota as a travel destination: “We hear a lot about New York and California, but we don’t hear that much

about Minnesota” “You get the best of both worlds, the city and nature. But I don’t hear a lot

about Minnesota” “They’re playing the Michigan commercials here and it actually makes you

want to go to Michigan” “They need to say that the state is more than the Twin Cities/Mall”

In Minnesota, Cultural Explorers state the need to include more than just messaging about outdoor activities: “Need to focus on cultural things (don’t focus on fishing and all the outdoor

activities)” “There’s more to do than fish and hunt – we already know that”

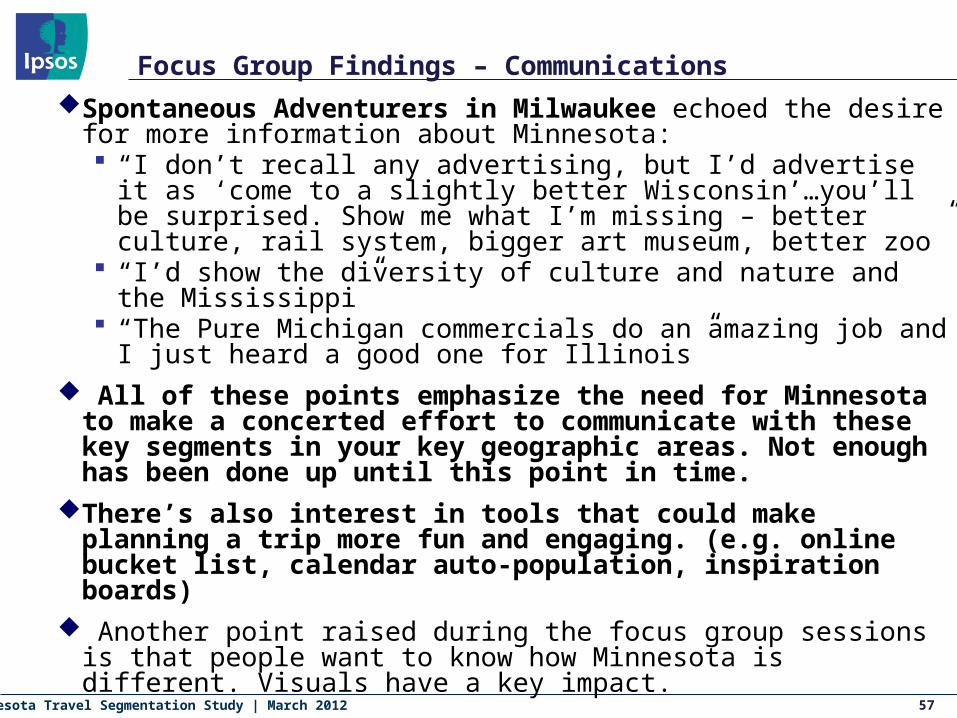

Minnesota Travel Segmentation Study | March 2012 57

Focus Group Findings – CommunicationsSpontaneous Adventurers in Milwaukee echoed the desire for more

information about Minnesota: “I don’t recall any advertising, but I’d advertise it as ‘come to a slightly better

Wisconsin’…you’ll be surprised. Show me what I’m missing – better culture, rail system, bigger art museum, better zoo”

“I’d show the diversity of culture and nature and the Mississippi” “The Pure Michigan commercials do an amazing job and I just heard a good

one for Illinois” All of these points emphasize the need for Minnesota to make a concerted

effort to communicate with these key segments in your key geographic areas. Not enough has been done up until this point in time.

There’s also interest in tools that could make planning a trip more fun and engaging. (e.g. online bucket list, calendar auto-population, inspiration boards)

Another point raised during the focus group sessions is that people want to know how Minnesota is different. Visuals have a key impact.

Minnesota Travel Segmentation Study | March 2012

SUMMARY OF KEY SEGMENTS

Minnesota Travel Segmentation Study | March 2012

Q UA N T I TAT I V E

Q UA L I TAT I V E

S I M M O N S

VA LU E SL I F E S T Y L E S

D E M O G R A P H I C SB R A N D P R E F E R E N C E S

Minnesota Travel Segmentation Study | March 201260

+ IPSOS quantitative report

+Qualitative focus groups (Minnesota and Milwaukee)

+Simmons research

Minnesota Travel Segmentation Study | March 201261

+ IPSOS quantitative report

+Qualitative focus groups (Minnesota and Milwaukee)

+Simmons research

Minnesota Travel Segmentation Study | March 201262

+ IPSOS quantitative report

+Qualitative focus groups (Minnesota and Milwaukee)

+Simmons research

Minnesota Travel Segmentation Study | March 201263

+ IPSOS quantitative report

+Qualitative focus groups (Minnesota and Milwaukee)

+Simmons research

Minnesota Travel Segmentation Study | March 201264

K E Y C O N C L U S I O N S

+ Considerable opportunities exist to tailor messages to motivate our priority segments: The Cultural Explorers and The Spontaneous Adventurers

• Key ways to motivate the Cultural Explorers include:• Highlighting luxurious experiences that stimulate all her senses

• Helping her get away from the grind of her daily life

• Highlighting opportunities in Minnesota outside of the Twin Cities

• Refreshing her interest in Minnesota by continuously serving up new experiences

• Making trip planning fun and engaging

• Key ways to motivate the Spontaneous Adventurers include:• Focusing on recreational experiences

• Showcasing trip options that include both urban and outdoors activities

• Highlighting great vacation options for families

• Promoting fun, instant, spur-of-the moment deals

• Leveraging Minnesota’s four distinct seasons

+ Regardless of segment, promoting what makes Minnesota truly different and unique from other destinations is key. People from other geographical areas are interested in learning more about Minnesota.

Minnesota Travel Segmentation Study | March 201265

N E X T S T E P S

+Segments will be incorporated into 2013 media planning, as well as overall strategy for the year

+Presentation :: May 2nd

Minnesota Travel Segmentation Study | March 2012

T H A N K Y O U