Minnesota Lottery 18-34 Year Old Segmentation Study

83

© 2016 Ipsos 1 18-34 Year Old Segmentation Study PRESENTATION – JUNE 2016 Minnesota Lottery © 2016 Ipsos. All rights reserved. Contains Ipsos' Confidential and Proprietary information and may not be disclosed or reproduced without the prior written consent of Ipsos.

Transcript of Minnesota Lottery 18-34 Year Old Segmentation Study

© 2016 Ipsos 1

18-34 Year Old Segmentation Study PRESENTATION – JUNE 2016

Minnesota Lottery

© 2016 Ipsos. All rights reserved. Contains Ipsos' Confidential and Proprietary information and may not be disclosed or reproduced without the prior written consent of Ipsos.

© 2016 Ipsos 2

Agenda

What is Happening in Minnesota?

What are the Challenges?

What are the Segments?

How and Where Do We Reach Them?

Discuss the Findings

© 2016 Ipsos 3

What is Happening in Minnesota?

Population

2002

5,019,000 2015

5,489,600

9% Spend

in past 12 months

2002

$377,000,000

2015

$546,900,000

45%

51%

Penetration % played any lottery game

in past 12 months

2002 2015

43% 14%

© 2016 Ipsos 4

Source: Minnesota Lottery SCSU Survey

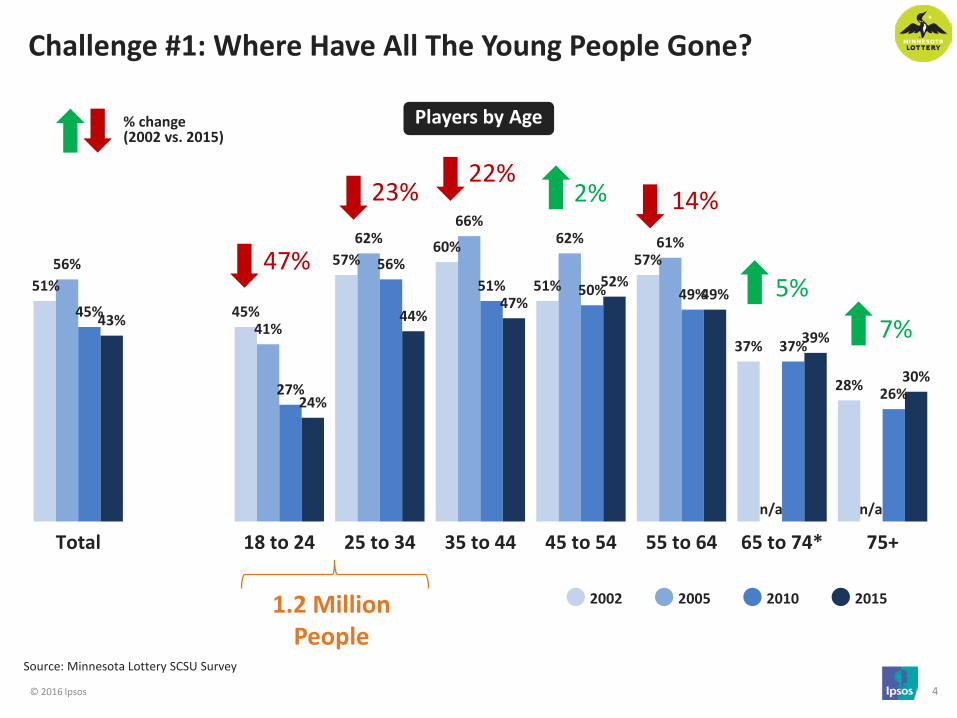

Challenge #1: Where Have All The Young People Gone?

51%

45%

57% 60%

51%

57%

37%

28%

56%

41%

62% 66%

62% 61%

45%

27%

56% 51% 50% 49%

37%

26%

43%

24%

44% 47%

52% 49%

39%

30%

Total 18 to 24 25 to 34 35 to 44 45 to 54 55 to 64 65 to 74* 75+

2002

Players by Age

47%

23% 2% 14%

5%

2005

% change (2002 vs. 2015)

n/a

1.2 Million People

2010 2015

n/a

22%

7%

© 2016 Ipsos 5

Challenge #2: Do Differences Exist?

Are their regional differences?

What are their attitudes towards life?

How they view technology and its role in

their life?

What are they doing for entertainment?

How do they consume news and information?

Where and how do they shop?

.

© 2016 Ipsos 6

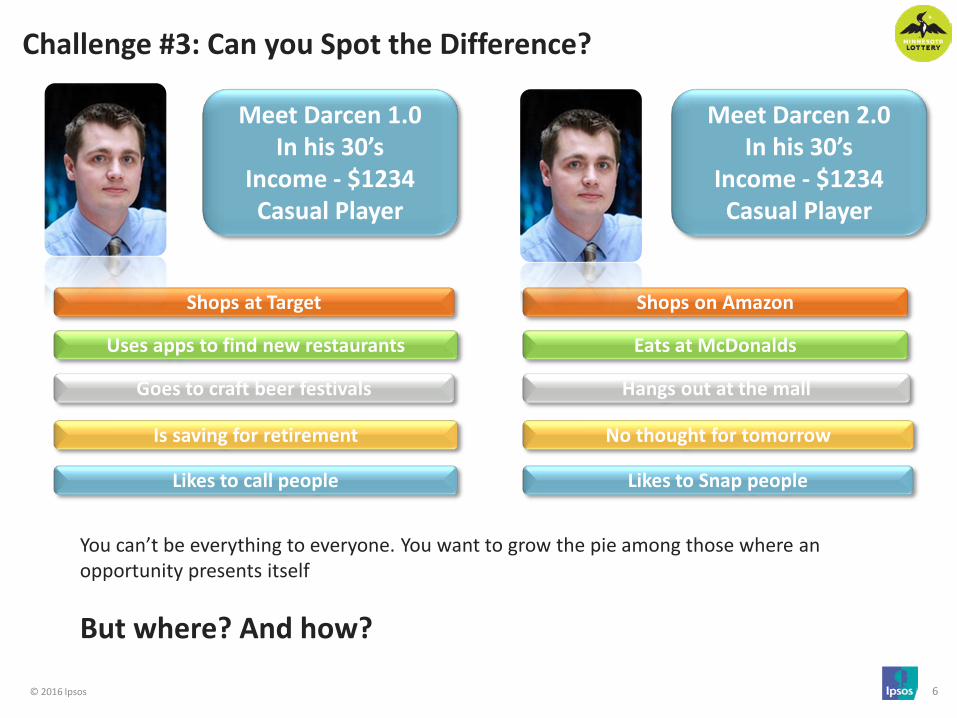

Challenge #3: Can you Spot the Difference?

You can’t be everything to everyone. You want to grow the pie among those where an opportunity presents itself

But where? And how?

Meet Darcen 1.0 In his 30’s

Income - $1234 Casual Player

Meet Darcen 2.0 In his 30’s

Income - $1234 Casual Player

Shops at Target Shops on Amazon

Uses apps to find new restaurants Eats at McDonalds

Goes to craft beer festivals

Is saving for retirement

Likes to call people

Hangs out at the mall

No thought for tomorrow

Likes to Snap people

© 2016 Ipsos 7

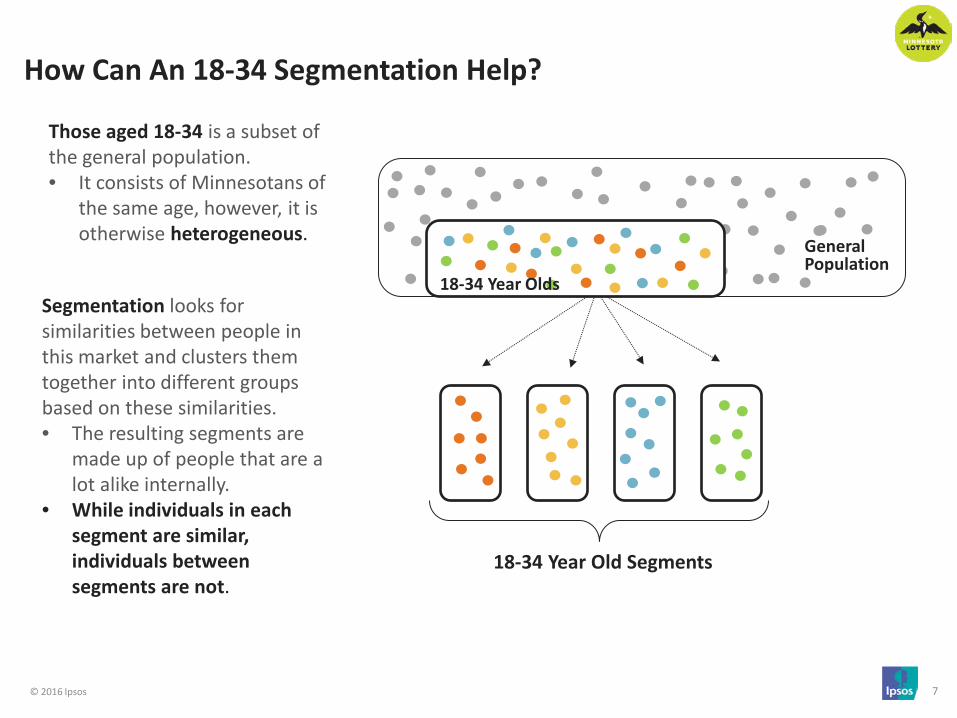

How Can An 18-34 Segmentation Help?

Segmentation looks for similarities between people in this market and clusters them together into different groups based on these similarities. • The resulting segments are

made up of people that are a lot alike internally.

• While individuals in each segment are similar, individuals between segments are not.

Those aged 18-34 is a subset of the general population. • It consists of Minnesotans of

the same age, however, it is otherwise heterogeneous.

18-34 Year Old Segments

18-34 Year Olds

General Population

© 2016 Ipsos 8

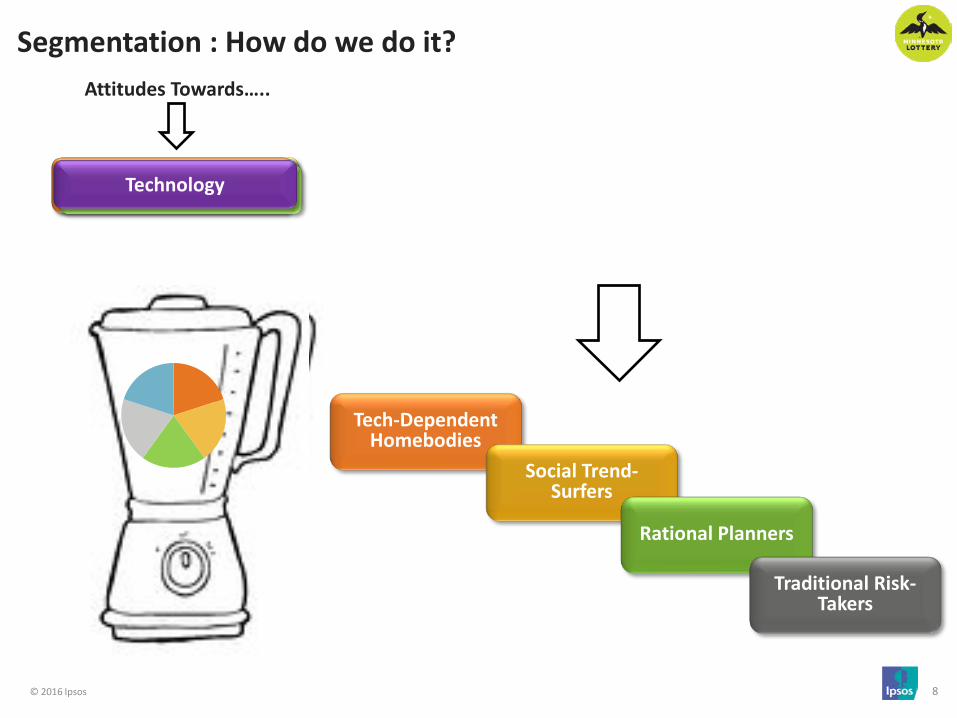

Entertainment Social Media News & Information Shopping Career/Finance Technology

Segmentation : How do we do it?

Tech-Dependent Homebodies

Social Trend-Surfers

Rational Planners

Traditional Risk-Takers

Attitudes Towards…..

© 2016 Ipsos 9

Phase 2: MN 18-34 Online Survey - Quantitative Survey - Segments identified

Phase 3: Qualitative Review and Segment Naming - Qualitative Mini Groups: Deep Dive - Naming the Segments

Phase 1: Qualitative Exploration of 18-34 Attitudes in Minnesota - Mini Groups in Duluth, Minneapolis, Mankato

Phase 4: Consumer Behaviors Study - Understand behaviors of new segments

Addressing the Challenges- The Road Traveled

Phase 5: Presentation and Workshop - Workshopping new segments

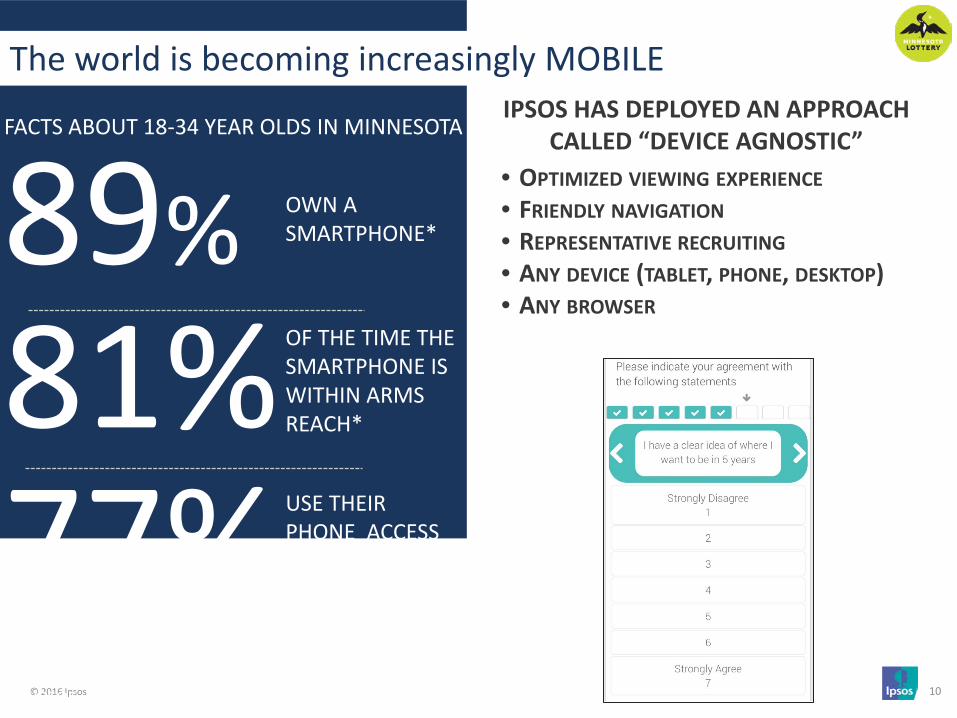

© 2016 Ipsos 10

10

OF THE TIME THE SMARTPHONE IS WITHIN ARMS REACH*

89% 81%

OWN A SMARTPHONE*

• OPTIMIZED VIEWING EXPERIENCE • FRIENDLY NAVIGATION • REPRESENTATIVE RECRUITING • ANY DEVICE (TABLET, PHONE, DESKTOP) • ANY BROWSER

The world is becoming increasingly MOBILE IPSOS HAS DEPLOYED AN APPROACH

CALLED “DEVICE AGNOSTIC”

77% USE THEIR PHONE ACCESS THE INTERNET

EVERY SINGLE DAY*

FACTS ABOUT 18-34 YEAR OLDS IN MINNESOTA

*IPSOS –GAMING WITH MILLENIALS STUDY-2014

© 2016 Ipsos 11

SO WHAT ARE THE CHALLENGES?

18-34 year olds in Minnesota are playing the lottery less than they used to

How do we understand the nuance differences that exist within 18-34 year olds?

How and where do we reach 18-34 year olds in Minnesota?

1

2

3

© 2016 Ipsos 12

THE SEGMENTS

© 2016 Ipsos 13

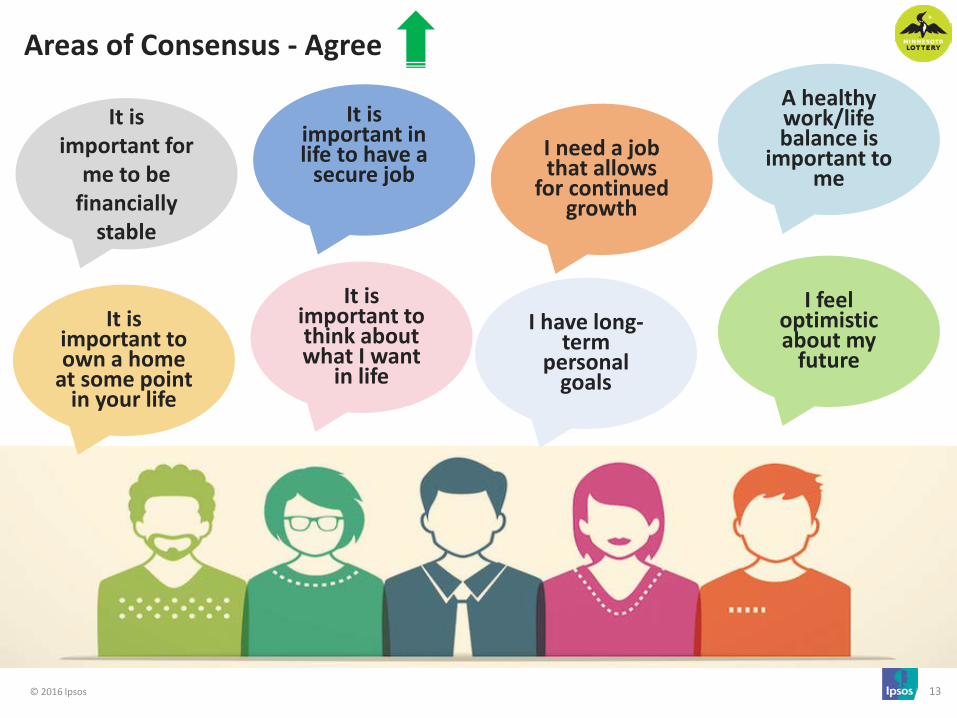

Areas of Consensus - Agree

It is important for

me to be financially

stable

It is important to think about what I want

in life

It is important in life to have a

secure job

It is important to own a home

at some point in your life

A healthy work/life balance is

important to me

I need a job that allows

for continued growth

I feel optimistic about my

future

I have long-term

personal goals

© 2016 Ipsos 14

Areas of Consensus - Agree

Sometimes it is important to stay in on the weekend

to relax

It is important to make time

for just myself

Technology helps me

connect with people I care

about

It is important to budget some

money for “fun”

I believe it is important for me to develop my own world

view

Technology makes my life

more convenient

Entertainment helps me

escape from my day to day

life

It is important to

have a healthy lifestyle

© 2016 Ipsos 15

Areas of Consensus - Disagree

I prefer to stay close to home when I

travel

I consider myself morally

opposed to gambling

I enjoy spending

time in large crowds more than in small

groups

I am more likely to

purchase a product if I see

a celebrity I like actually

using it

I would rather have

lots of casual friends than a

few close friends

I never give out my email

address to companies

Celebrity endorsements

influence what

products I buy

I prefer to communicate

with my friends using short videos or pictures

© 2016 Ipsos 16

SEGMENT SUMMARIES

© 2016 Ipsos 17

Definitions of Segments

Traditional Risk-Takers

Social Trend-Surfers

Tech-Dependent Homebodies

1 2 3

Minnesota Lottery and Ipsos participated in a Segment Naming Workshop on June 2nd to understand the segments and come up with the segment names.

Rational Planners

4

© 2016 Ipsos 18

59%

48%

37%

41%

Proportion of Lottery Game Participation & Spending by Segment SEGMENTATION SUMMARY

21%

29%

22%

27%

26%

32%

21%

22%

% of PY Lottery Players

45%

35%

10%

11%

% of PY Spending on Lotteries

Traditional Risk-Takers

Social Trend-Surfers

Tech-Dependent Homebodies

Rational Planners

% of 18-34 Year Olds

% Other gaming – Ever play

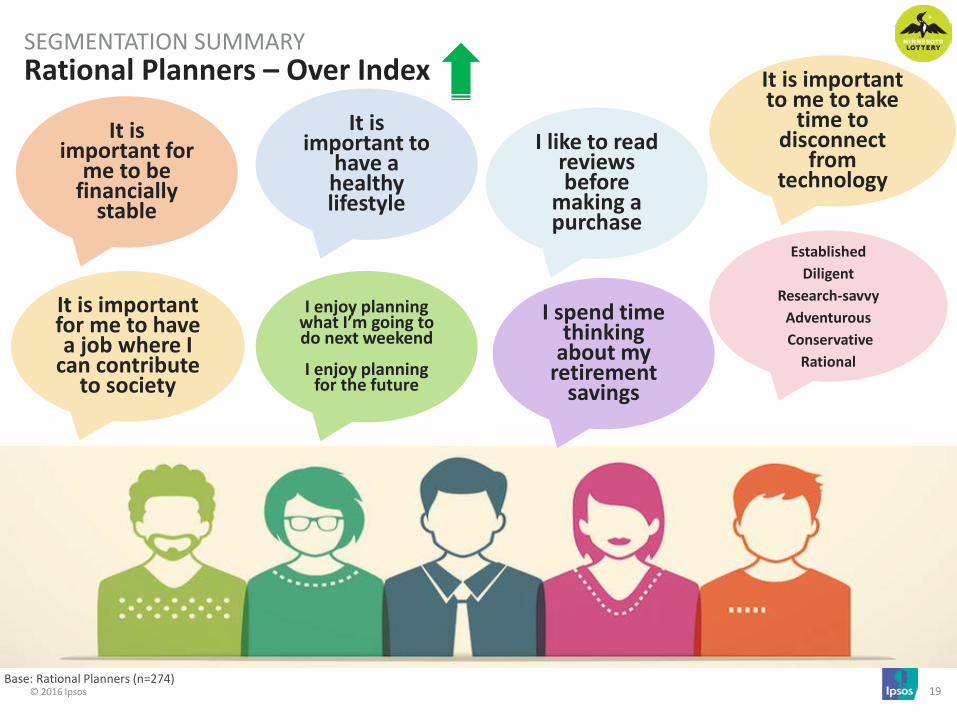

© 2016 Ipsos 19 Base: Rational Planners (n=274)

Rational Planners – Over Index SEGMENTATION SUMMARY

It is important for

me to be financially

stable

It is important to

have a healthy lifestyle

Established Diligent

Research-savvy Adventurous Conservative

Rational

I like to read reviews before

making a purchase

I enjoy planning what I’m going to do next weekend

I enjoy planning

for the future

I spend time thinking

about my retirement

savings

It is important to me to take

time to disconnect

from technology

It is important for me to have a job where I

can contribute to society

© 2016 Ipsos 20 Base: Rational Planners (n=274)

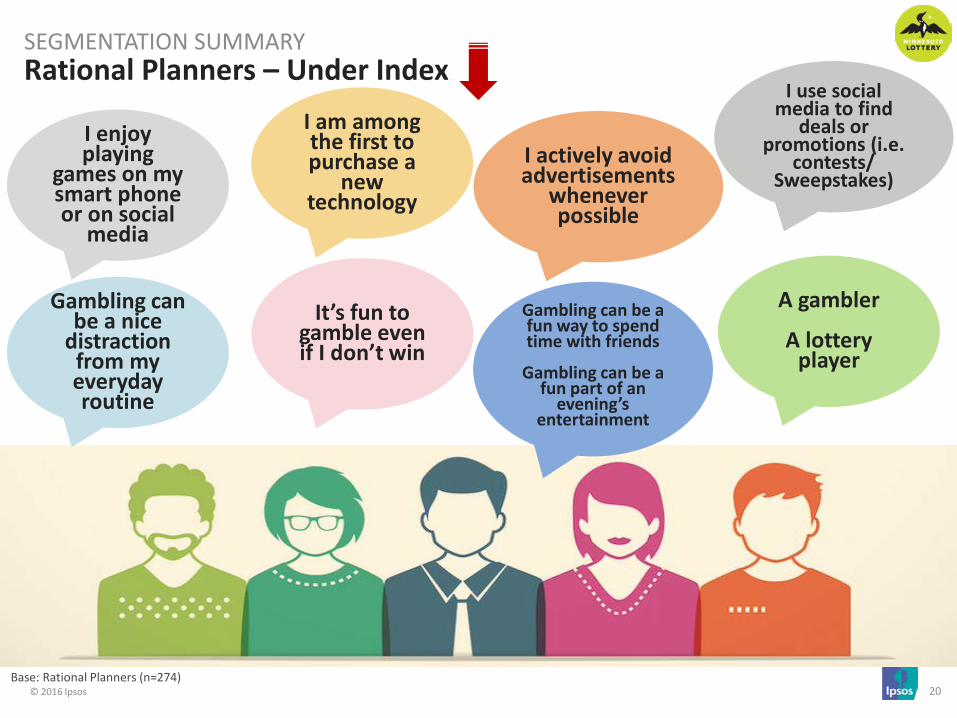

Rational Planners – Under Index SEGMENTATION SUMMARY

I enjoy playing

games on my smart phone or on social

media

It’s fun to gamble even if I don’t win

Gambling can be a fun way to spend time with friends

Gambling can be a

fun part of an evening’s

entertainment

I am among the first to purchase a

new technology

I use social media to find

deals or promotions (i.e.

contests/ Sweepstakes)

I actively avoid advertisements

whenever possible

A gambler

A lottery player

Gambling can be a nice

distraction from my everyday routine

© 2016 Ipsos 21

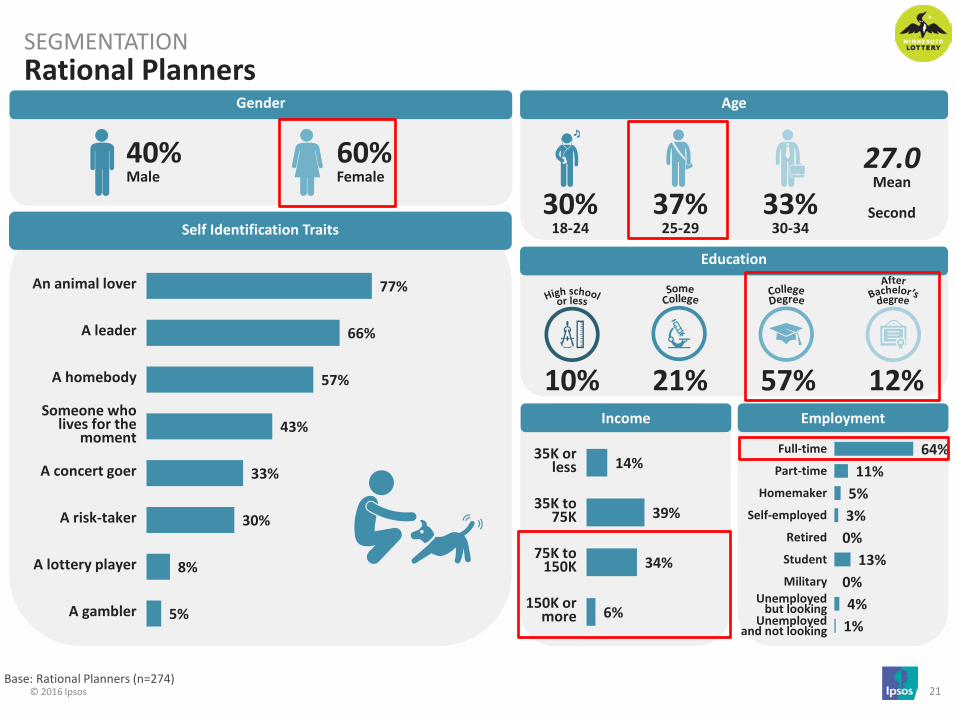

Rational Planners SEGMENTATION

Gender

40% Male

60% Female

Age

Education

33% 30-34

30% 18-24

37% 25-29

27.0 Mean

Second

12% 57% 10% Income Employment

Self Identification Traits

77%

66%

57%

43%

33%

30%

8%

5%

An animal lover

A leader

A homebody

Someone who lives for the

moment

A concert goer

A risk-taker

A lottery player

A gambler

14%

39%

34%

6%

35K or less

35K to 75K

75K to 150K

150K or more

21%

64% 11%

5% 3%

0% 13%

0% 4%

1%

Full-time

Part-time

Homemaker

Self-employed

Retired

Student

Military Unemployed

but looking Unemployed

and not looking

Base: Rational Planners (n=274)

© 2016 Ipsos 22

Rational Planners SEGMENTATION

Past Year/Month Spending (Any Game Mean excl. 0)

17% 34% 18% 30% <[VALUE] Any Game

Participation

I've purchased in the past month

I've purchased in the last 12 months, but not in the past month

I've purchased, but not in the last 12 months

I've heard of this game, but never purchased it

I've never heard of this game

$17.50 $65.50

Past Month Spend

Past Year Spend

Past Year Other Gaming Participation (Top 3 Mentions) Any Game Purchase Frequency

49%

29%

12% 7% 3% 1%

Any Game

Almost every day

Every draw

Weekly

Monthly

Every couple of months

Less than every couple of months

19% Paper

Pulltabs

16% Gambling at casinos

in Minnesota or neighboring states

12% Purchasing

raffle tickets

17%

51%

Past Month

Past Year

Lottery Play

22%

% of Past Year Spend

11%

Past Year Lottery Players

Base: Rational Planners (n=274)

© 2016 Ipsos 23

Tech-Dependent Homebodies – Over Index SEGMENTATION SUMMARY

Technology helps me

connect with people I care

about and keep up with my

friends

Social media is the primary

way I communicate with friends

I would rather do my

shopping online

Homebody Netflix

Introverted Hibernators

When I wake up in the morning, one of the first

things I do is check my social media accounts

I am most likely to get my news

through my phone

I primarily get my news from social

media, like Facebook

I find it easy to hibernate

during winter

I use social media to

follow brands I like or to find deals/ promotions

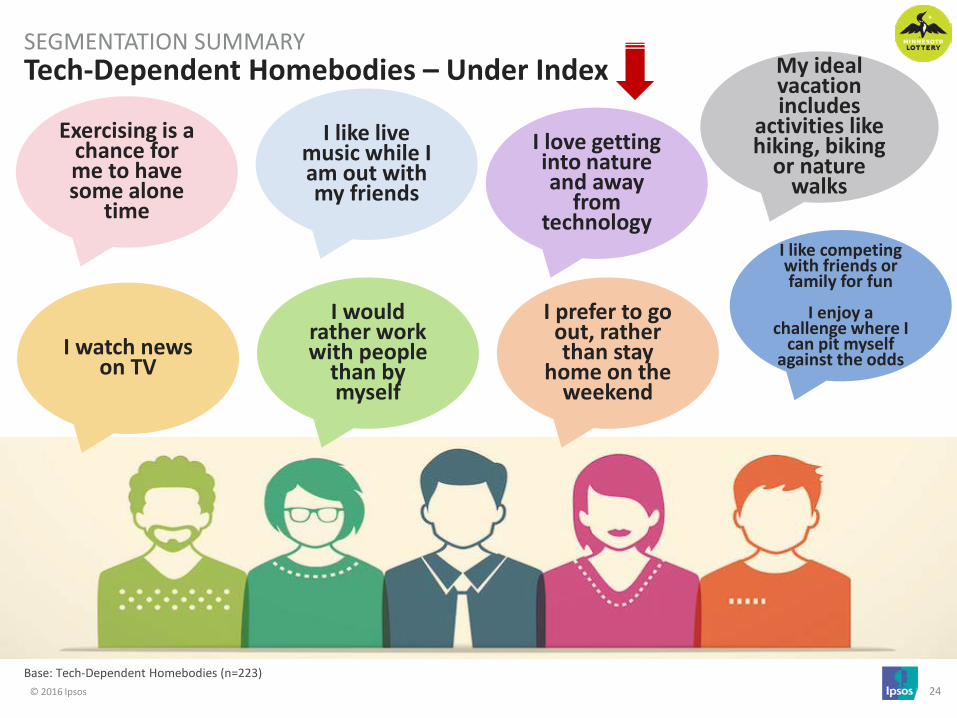

Base: Tech-Dependent Homebodies (n=223)

© 2016 Ipsos 24 Base: Tech-Dependent Homebodies (n=223)

Tech-Dependent Homebodies – Under Index SEGMENTATION SUMMARY

Exercising is a chance for me to have some alone

time

I like live music while I am out with my friends

I like competing with friends or family for fun

I enjoy a

challenge where I can pit myself

against the odds

I love getting into nature and away

from technology

I watch news on TV

I prefer to go out, rather than stay

home on the weekend

My ideal vacation includes

activities like hiking, biking

or nature walks

I would rather work with people

than by myself

© 2016 Ipsos 25

Tech-Dependent Homebodies SEGMENTATION

Gender

29% Male

71% Female

Age

Education

33% 30-34

40% 18-24

26% 25-29

26.3 Mean

Third

6% 40% 28% Income Employment

Self Identification Traits

83%

78%

43%

33%

25%

14%

8%

7%

A homebody

An animal lover

A leader

Someone who lives for the

moment

A concert goer

A risk-taker

A lottery player

A gambler

27%

45%

21%

1%

35K or less

35K to 75K

75K to 150K

150K or more

26%

52% 12% 10%

2% 0%

14% 0%

6% 4%

Full-time

Part-time

Homemaker

Self-employed

Retired

Student

Military Unemployed

but looking Unemployed

and not looking

Base: Tech-Dependent Homebodies (n=223)

© 2016 Ipsos 26

Tech-Dependent Homebodies SEGMENTATION

Past Year/Month Spending (Any Game Mean excl. 0)

20% 41% 16% 23% <[VALUE] Any Game

Participation

I've purchased in the past month

I've purchased in the last 12 months, but not in the past month

I've purchased, but not in the last 12 months

I've heard of this game, but never purchased it

I've never heard of this game

$18.40 $62.80

Past Month Spend

Past Year Spend

Past Year Other Gaming Participation (Top 3 Mentions) Any Game Purchase Frequency

48%

26%

19%

7% 2%

Any Game

Almost every day

Every draw

Weekly

Monthly

Every couple of months

Less than every couple of months

19% Gambling at casinos

in Minnesota or neighboring states

11% Paper

Pulltabs

11% Purchasing

raffle tickets

20%

61%

Past Month

Past Year

Lottery Play

21%

% of Past Year Spend

10%

Past Year Lottery Players

Base: Tech-Dependent Homebodies (n=223)

© 2016 Ipsos 27 Base: Social Trend-Surfers (n=295)

Social Trend-Surfers – Over Index SEGMENTATION SUMMARY

I prefer to go out, rather than stay

home on the weekend

I like online ads that are targeted specifically to me

I am more likely to view ads that

show up in one of my social media

feeds

I enjoy playing

games on social media

Celebrity endorsements influence what products I buy

I am more likely to purchase a product if I see a celebrity I like actually using it

I trust social media

websites with my personal information

I am among the first to purchase

a new technology

Socialites Trendy

Brand /Image conscious

FOMO - want to be able to/ confidence

to contribute to conversation

I enjoy spending

time in large crowds more than in small

groups

© 2016 Ipsos 28 Base: Social Trend-Surfers (n=295)

Social Trend-Surfers – Under Index SEGMENTATION SUMMARY

It is important for

me to be financially

stable

It is important to think about what I want

in life

Gambling is wasteful Sometimes it

is important to stay in on the weekend

to relax

I actively avoid advertisements

whenever possible

A healthy work/life balance is

important to me

I find it easy to hibernate

during winter

It is important to

build/improve my credit

rating

© 2016 Ipsos 29

Social Trend-Surfers SEGMENTATION

Gender

61% Male

39% Female

Age

Education

24% 30-34

45% 18-24

32% 25-29

25.4 Mean

Youngest

10% 37% 26% Income Employment

Self Identification Traits

69%

57%

53%

42%

41%

38%

22%

15%

An animal lover

A leader

Someone who lives for the

moment

A homebody

A concert goer

A risk-taker

A lottery player

A gambler

33%

32%

25%

4%

35K or less

35K to 75K

75K to 150K

150K or more

27%

50% 19%

4% 3%

<1% 15%

<1% 6%

1%

Full-time

Part-time

Homemaker

Self-employed

Retired

Student

Military Unemployed

but looking Unemployed

and not looking

Base: Social Trend-Surfers (n=295)

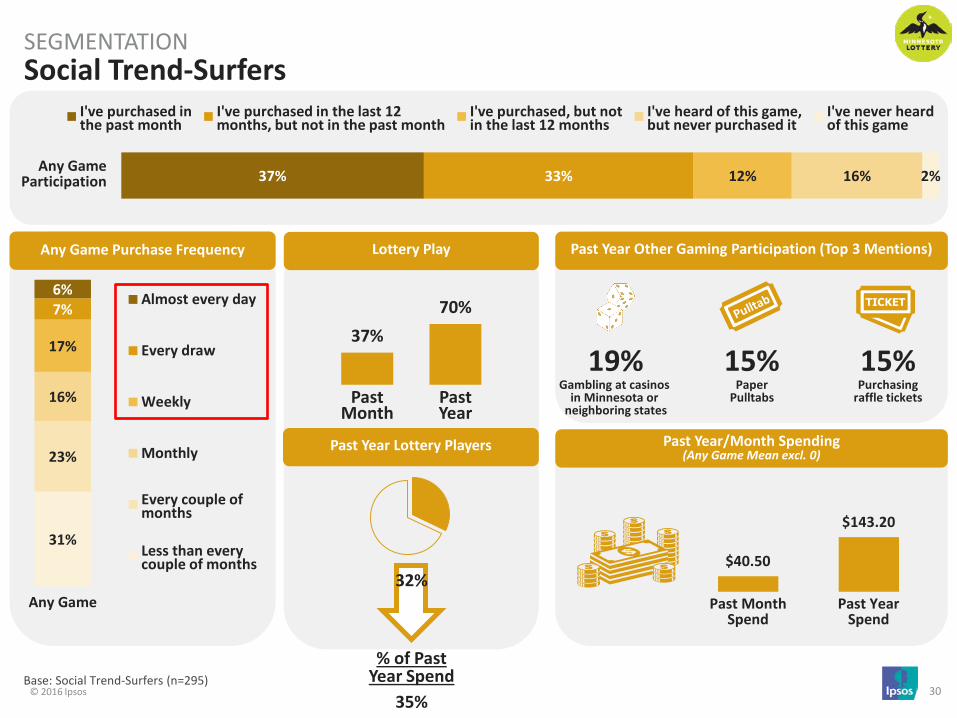

© 2016 Ipsos 30

Social Trend-Surfers SEGMENTATION

Past Year/Month Spending (Any Game Mean excl. 0)

37% 33% 12% 16% 2% Any Game

Participation

I've purchased in the past month

I've purchased in the last 12 months, but not in the past month

I've purchased, but not in the last 12 months

I've heard of this game, but never purchased it

I've never heard of this game

$40.50

$143.20

Past Month Spend

Past Year Spend

Past Year Other Gaming Participation (Top 3 Mentions) Any Game Purchase Frequency

31%

23%

16%

17%

7% 6%

Any Game

Almost every day

Every draw

Weekly

Monthly

Every couple of months

Less than every couple of months

19% Gambling at casinos

in Minnesota or neighboring states

15% Paper

Pulltabs

15% Purchasing

raffle tickets

37% 70%

Past Month

Past Year

Lottery Play

32%

% of Past Year Spend

35%

Past Year Lottery Players

Base: Social Trend-Surfers (n=295)

© 2016 Ipsos 31 Base: Traditional Risk-Takers (n=209)

Traditional Risk-Takers – Over Index SEGMENTATION SUMMARY

Hunting and fishing is a

fun source of recreation –

ideal vacation

Someone who lives for the moment

I prefer to pay with cash over debit or credit

Gambling can be a fun part of an

evening’s entertainment, a fun way to spend

time with friends or a nice distraction from my everyday

routine

I enjoy a challenge

where I can pit myself

against the odds

I actively follow at least one

Minnesota pro sports team

When I pay, I prefer to

interact with a store clerk over a machine

I enjoy the interaction with a clerk at a store

I feel comfortable asking

store staff about promotions and deals

It’s fun to gamble even if I don’t win

© 2016 Ipsos 32

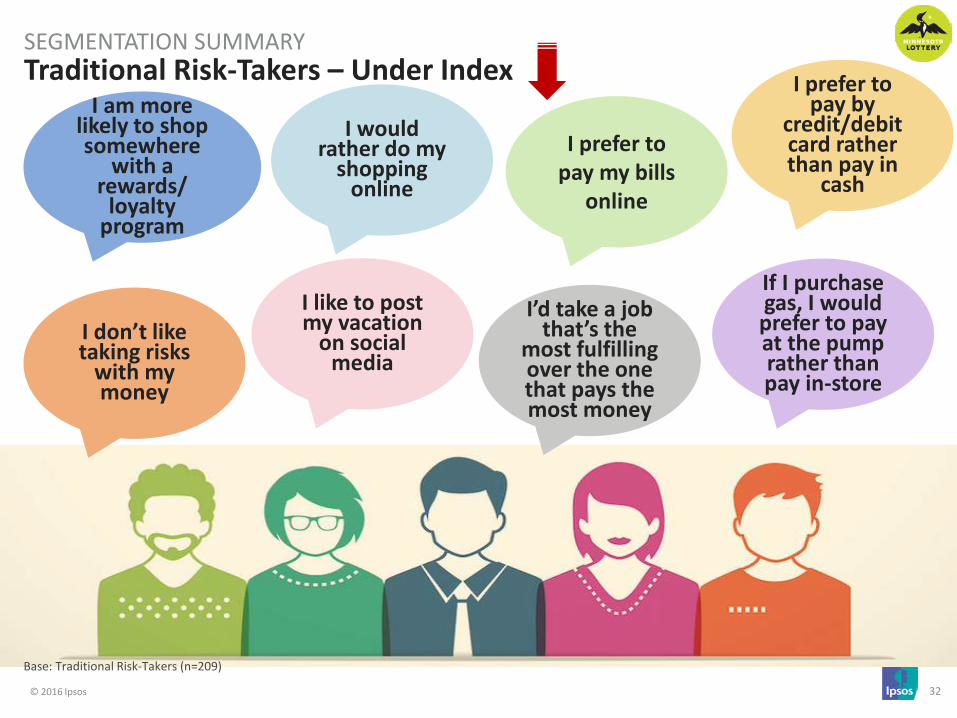

Traditional Risk-Takers – Under Index SEGMENTATION SUMMARY

I prefer to pay my bills

online

I like to post my vacation

on social media

I am more likely to shop somewhere

with a rewards/

loyalty program

I prefer to pay by

credit/debit card rather than pay in

cash

I’d take a job that’s the

most fulfilling over the one that pays the most money

I don’t like taking risks

with my money

If I purchase gas, I would prefer to pay at the pump rather than pay in-store

I would rather do my

shopping online

Base: Traditional Risk-Takers (n=209)

© 2016 Ipsos 33

Traditional Risk-Takers SEGMENTATION

Gender

71% Male

29% Female

Age

Education

39% 30-34

33% 18-24

28% 25-29

27.1 Mean

Oldest

4% 35% 28% Income Employment

Self Identification Traits

80%

69%

67%

63%

43%

41%

39%

33%

An animal lover

A leader

Someone who lives for the

moment

A risk-taker

A homebody

A lottery player

A gambler

A concert goer

36%

39%

19%

2%

35K or less

35K to 75K

75K to 150K

150K or more

34%

55% 17%

4% 4%

0% 8%

<1% 8%

2%

Full-time

Part-time

Homemaker

Self-employed

Retired

Student

Military Unemployed

but looking Unemployed

and not looking

Base: Traditional Risk-Takers (n=209)

© 2016 Ipsos 34

Traditional Risk-Takers SEGMENTATION

Past Year/Month Spending (Any Game Mean excl. 0)

51% 31% 7% 9% 3% Any Game

Participation

I've purchased in the past month

I've purchased in the last 12 months, but not in the past month

I've purchased, but not in the last 12 months

I've heard of this game, but never purchased it

I've never heard of this game

$48.90

$221.80

Past Month Spend

Past Year Spend

Past Year Other Gaming Participation (Top 3 Mentions) Any Game Purchase Frequency

20%

26%

17%

24%

2% 11%

Any Game

Almost every day

Every draw

Weekly

Monthly

Every couple of months

Less than every couple of months

37% Gambling at casinos

in Minnesota or neighboring states

30% Paper

Pulltabs

18% Purchasing

raffle tickets

51% 82%

Past Month

Past Year

Lottery Play

26%

% of Past Year Spend

45%

Past Year Lottery Players

Base: Traditional Risk-Takers (n=209)

© 2016 Ipsos 35

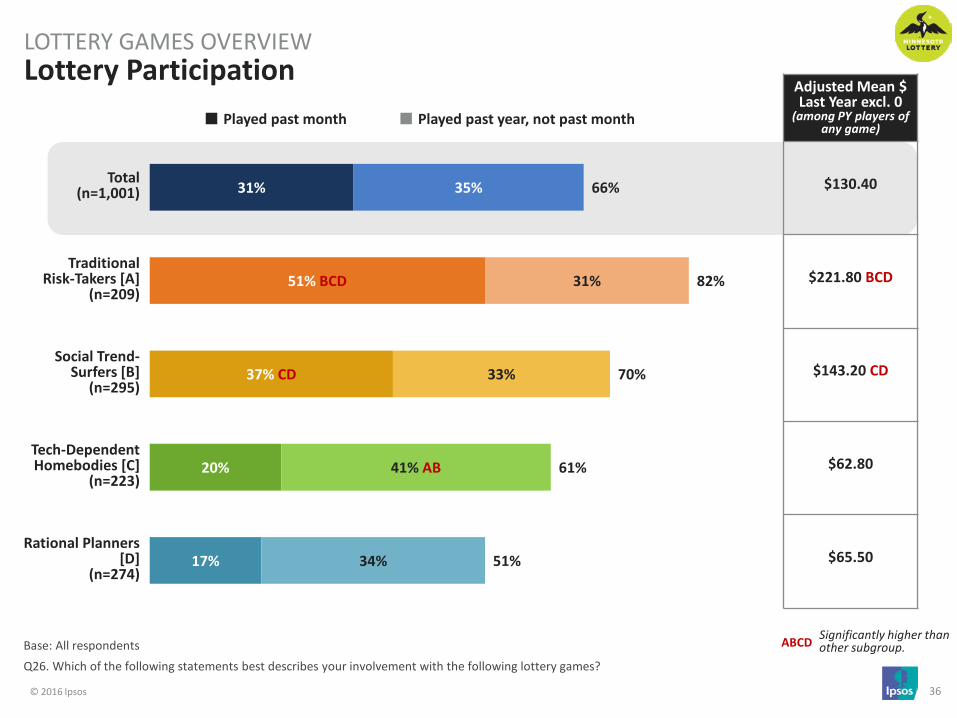

LOTTERY GAMES OVERVIEW

© 2016 Ipsos 36

Base: All respondents Q26. Which of the following statements best describes your involvement with the following lottery games?

Lottery Participation LOTTERY GAMES OVERVIEW

31%

51% BCD

37% CD

20%

17%

35%

31%

33%

41% AB

34%

66%

82%

70%

61%

51%

Total (n=1,001)

Traditional Risk-Takers [A]

(n=209)

Social Trend- Surfers [B]

(n=295)

Tech-Dependent Homebodies [C]

(n=223)

Rational Planners [D]

(n=274)

Played past month Played past year, not past month

ABCD Significantly higher than other subgroup.

Adjusted Mean $ Last Year excl. 0

(among PY players of any game)

$130.40

$221.80 BCD

$143.20 CD

$62.80

$65.50

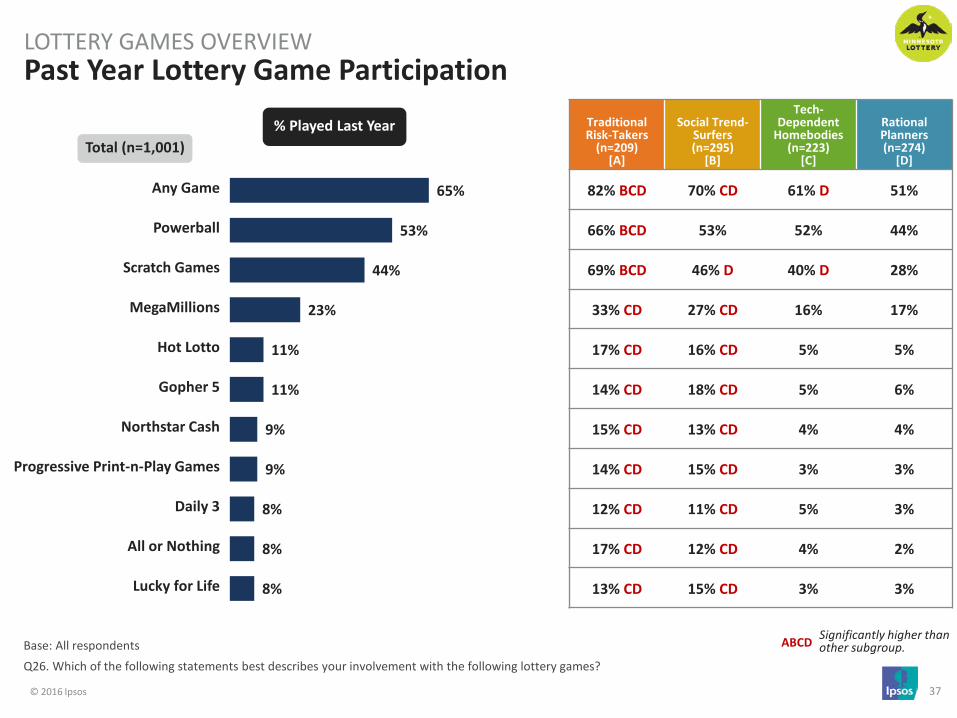

© 2016 Ipsos 37

65%

53%

44%

23%

11%

11%

9%

9%

8%

8%

8%

Any Game

Powerball

Scratch Games

MegaMillions

Hot Lotto

Gopher 5

Northstar Cash

Progressive Print-n-Play Games

Daily 3

All or Nothing

Lucky for Life

Base: All respondents Q26. Which of the following statements best describes your involvement with the following lottery games?

Past Year Lottery Game Participation LOTTERY GAMES OVERVIEW

Traditional Risk-Takers

(n=209) [A]

Social Trend-Surfers (n=295)

[B]

Tech-Dependent

Homebodies (n=223)

[C]

Rational Planners (n=274)

[D]

82% BCD 70% CD 61% D 51%

66% BCD 53% 52% 44%

69% BCD 46% D 40% D 28%

33% CD 27% CD 16% 17%

17% CD 16% CD 5% 5%

14% CD 18% CD 5% 6%

15% CD 13% CD 4% 4%

14% CD 15% CD 3% 3%

12% CD 11% CD 5% 3%

17% CD 12% CD 4% 2%

13% CD 15% CD 3% 3%

ABCD Significantly higher than other subgroup.

% Played Last Year Total (n=1,001)

© 2016 Ipsos 38

How Do We Reach

Them?

Social Media

Television

Radio /Music

Shopping

Entertainment / Events

© 2016 Ipsos 39

SOCIAL MEDIA USAGE

© 2016 Ipsos 40

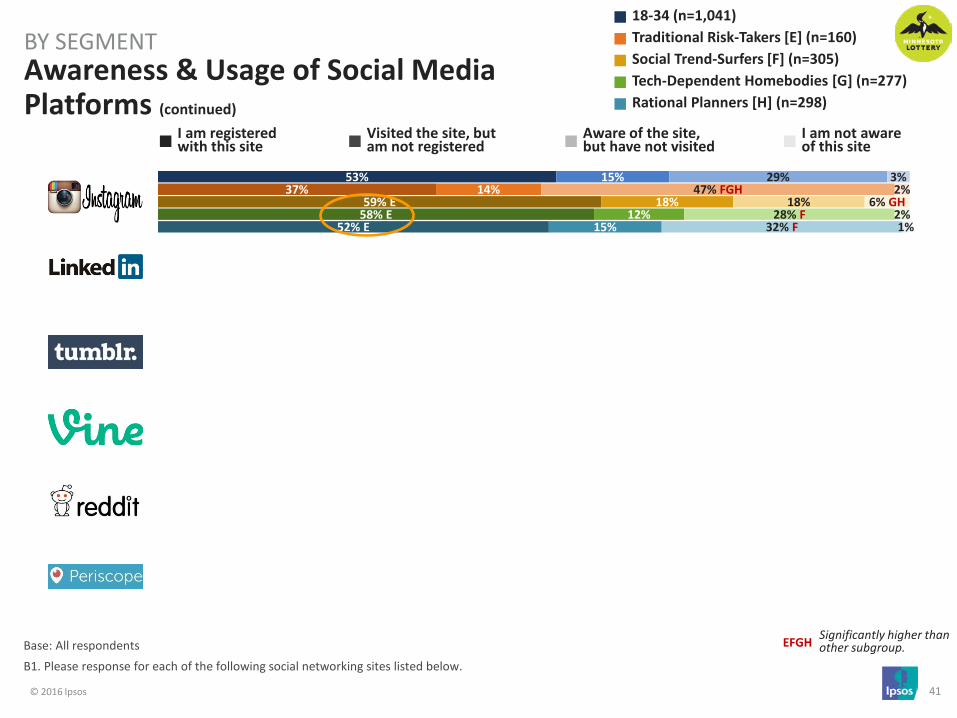

Base: All respondents B1. Please response for each of the following social networking sites listed below.

Awareness & Usage of Social Media Platforms

BY SEGMENT

91%

73%

58%

57%

56%

54%

86%

74% H

48%

53%

44%

39%

88%

78% H

63% E

61%

47%

63% EH

96% EFH

76% H

60% E

58%

68% EFH

61% EH

91%

63%

58%

53%

59% EF

47%

EFGH Significantly higher than other subgroup.

I am registered with this site

Visited the site, but am not registered

Aware of the site, but have not visited

I am not aware of this site

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

4%

24%

8%

19%

19%

20%

5% G

24%

8%

21%

20%

21%

6% G

17%

12% H

19%

22%

17%

1%

23%

8%

17%

16%

17%

4% G

34% EFG

5%

19%

18%

23%

5%

3%

31%

23%

23%

26%

8% G

2%

42% FG

23%

33% FGH

40% FGH

5%

4%

21%

20%

24% G

18%

2%

2%

30% F

23%

15%

21%

5%

2%

36% F

26%

23% G

30% FG

3%

2%

3%

1%

2%

3%

2%

1%

1%

1%

4%

1%

8% EGH

2%

2%

2%

1%

1%

2%

3%

1%

© 2016 Ipsos 41

Base: All respondents B1. Please response for each of the following social networking sites listed below.

Awareness & Usage of Social Media Platforms (continued)

BY SEGMENT

53%

45%

19%

17%

11%

5%

37%

35%

11%

13%

9%

4%

59% E

35%

23% EH

27% EGH

10%

5%

58% E

50% EF

26% EH

15%

14%

8% H

52% E

57% EF

12%

10%

9%

3%

I am registered with this site

Visited the site, but am not registered

Aware of the site, but have not visited

I am not aware of this site

EFGH Significantly higher than other subgroup.

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

15%

16%

25%

23%

30%

9%

14%

14%

27%

26%

30%

6%

18%

23% EGH

24%

26%

32%

14% EGH

12%

13%

20%

21%

29%

6%

15%

12%

27%

21%

28%

7%

29%

30%

47%

44%

44%

36%

47% FGH

37%

51% F

44% F

42%

29%

18%

28%

37%

31%

36%

36%

28% F

29%

47% F

46% F

46% F

37%

32% F

29%

53% F

54% F

50% F

39% E

3%

9%

10%

17%

16%

50%

2%

15% GH

11%

18%

19% G

62% FGH

6% GH

14% GH

15% GH

17%

21% GH

44%

2%

8% H

7%

18%

12%

50%

1%

2%

7%

16%

13%

51%

© 2016 Ipsos 42

64%

17%

17%

17%

16%

61%

16%

11%

19%

13%

56%

26%

23%

22%

26%

76%

18%

21%

19%

15%

62%

8%

9%

9%

10%

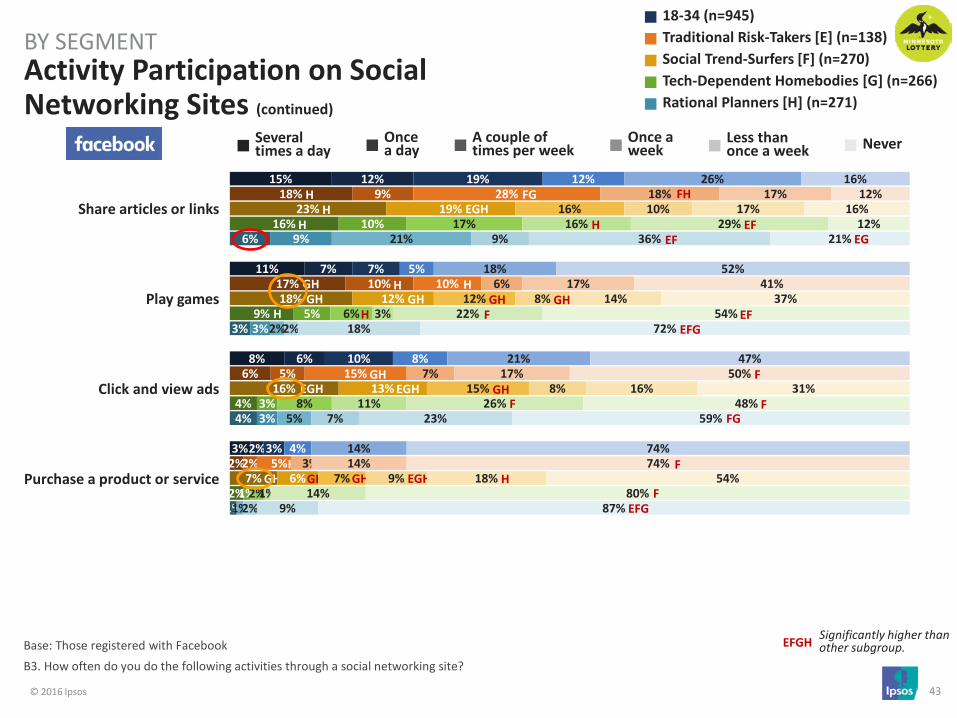

Base: Those registered with Facebook B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites (continued)

BY SEGMENT

Browsing my feed to see what's new

Share pictures or videos

Follow brands, celebrities or companies I'm interested in

learning about

Searching the site for specific news

Participate in a group chat or message

EFGH Significantly higher than other subgroup.

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

18-34 (n=945) Traditional Risk-Takers [E] (n=138) Social Trend-Surfers [F] (n=270) Tech-Dependent Homebodies [G] (n=266) Rational Planners [H] (n=271)

H EGH

H

EGH H

GH GH

EFH

H H

H

18%

11%

12%

15%

12%

16%

15%

9%

12%

10%

20%

16%

17%

18%

16%

15%

7%

11%

15%

11%

18%

7%

9%

14%

8%

H

GH GH

GH

7%

23%

17%

17%

17%

7%

30%

14%

17%

17%

10%

22%

20%

23%

17%

4%

26%

19%

15%

14%

8%

17%

15%

14%

19%

H

H

G

GH

4%

13%

10%

10%

12%

6%

9%

11%

14%

14%

5%

11%

11%

9%

12%

1%

13%

8%

10%

14%

4%

19%

12%

11%

9%

EF

G G

G

4%

28%

22%

18%

27%

4%

23%

24%

16%

23%

4%

16%

17%

13%

15%

3%

29%

21%

20%

30%

5%

43%

26%

21%

38%

F EFG

EF F

F

F F

4%

8%

22%

23%

17%

6%

8%

31%

23%

22%

6%

10%

13%

16%

15%

2%

7%

21%

21%

16%

3%

7%

29%

31%

17%

FG

FG F

G G

FG

© 2016 Ipsos 43

15%

11%

8%

3%

18%

17%

6%

2%

23%

18%

16%

7%

16%

9%

4%

2%

6%

3%

4%

1%

Base: Those registered with Facebook B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites (continued)

BY SEGMENT

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

Share articles or links

Play games

Click and view ads

Purchase a product or service

EFGH Significantly higher than other subgroup.

EGH

GH

GH GH

H

H H

H

18-34 (n=945) Traditional Risk-Takers [E] (n=138) Social Trend-Surfers [F] (n=270) Tech-Dependent Homebodies [G] (n=266) Rational Planners [H] (n=271)

12%

7%

6%

2%

9%

10%

5%

2%

19%

12%

13%

6%

10%

5%

3%

1%

9%

3%

3%

EGH

GH H

H GH

EGH

19%

7%

10%

3%

28%

10%

15%

5%

16%

12%

15%

7%

17%

6%

8%

2%

21%

2%

5%

1%

GH GH

GH H

H GH

H

FG 12%

5%

8%

4%

18%

6%

7%

3%

10%

8%

8%

9%

16%

3%

11%

1%

9%

2%

7%

2%

EGH

GH

FH

H

26%

18%

21%

14%

17%

17%

17%

14%

17%

14%

16%

18%

29%

22%

26%

14%

36%

18%

23%

9%

F

H

F

EF EF

16%

52%

47%

74%

12%

41%

50%

74%

16%

37%

31%

54%

12%

54%

48%

80%

21%

72%

59%

87%

F

F FG

F

F EFG

EF EFG

EG

© 2016 Ipsos 44

19%

11%

11%

6%

6%

19%

15%

13%

6%

4%

24%

15%

15%

9%

12%

21%

11%

11%

5%

4%

10%

4%

6%

1%

1%

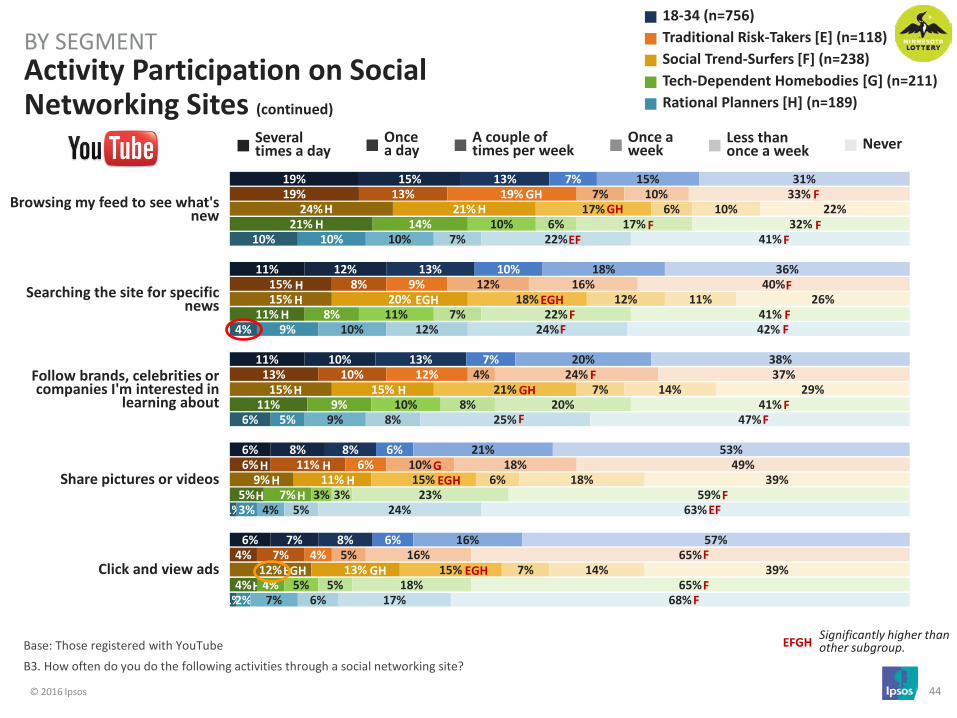

Base: Those registered with YouTube B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites (continued)

BY SEGMENT

Browsing my feed to see what's new

Searching the site for specific news

Follow brands, celebrities or companies I'm interested in

learning about

Share pictures or videos

Click and view ads

18-34 (n=756) Traditional Risk-Takers [E] (n=118) Social Trend-Surfers [F] (n=238) Tech-Dependent Homebodies [G] (n=211) Rational Planners [H] (n=189)

EFGH Significantly higher than other subgroup.

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

H H

H

EGH H

H

H H

H H

H

15%

12%

10%

8%

7%

13%

8%

10%

11%

7%

21%

20%

15%

11%

13%

14%

8%

9%

7%

4%

10%

9%

5%

3%

2%

H H

H

GH

H

H

EGH

13%

13%

13%

8%

8%

19%

9%

12%

6%

4%

17%

18%

21%

15%

15%

10%

11%

10%

3%

5%

10%

10%

9%

4%

7%

EGH

EGH

GH

GH GH

EGH

7%

10%

7%

6%

6%

7%

12%

4%

10%

5%

6%

12%

7%

6%

7%

6%

7%

8%

3%

5%

7%

12%

8%

5%

6%

G

15%

18%

20%

21%

16%

10%

16%

24%

18%

16%

10%

11%

14%

18%

14%

17%

22%

20%

23%

18%

22%

24%

25%

24%

17%

F

F

F EF

F F

31%

36%

38%

53%

57%

33%

40%

37%

49%

65%

22%

26%

29%

39%

39%

32%

41%

41%

59%

65%

41%

42%

47%

63%

68%

F EF

F

F F

F F

F

F F

F

F F

© 2016 Ipsos 45

5%

4%

4%

3%

5%

7%

7%

4%

8%

6%

8%

6%

4%

2%

3%

1%

1%

1%

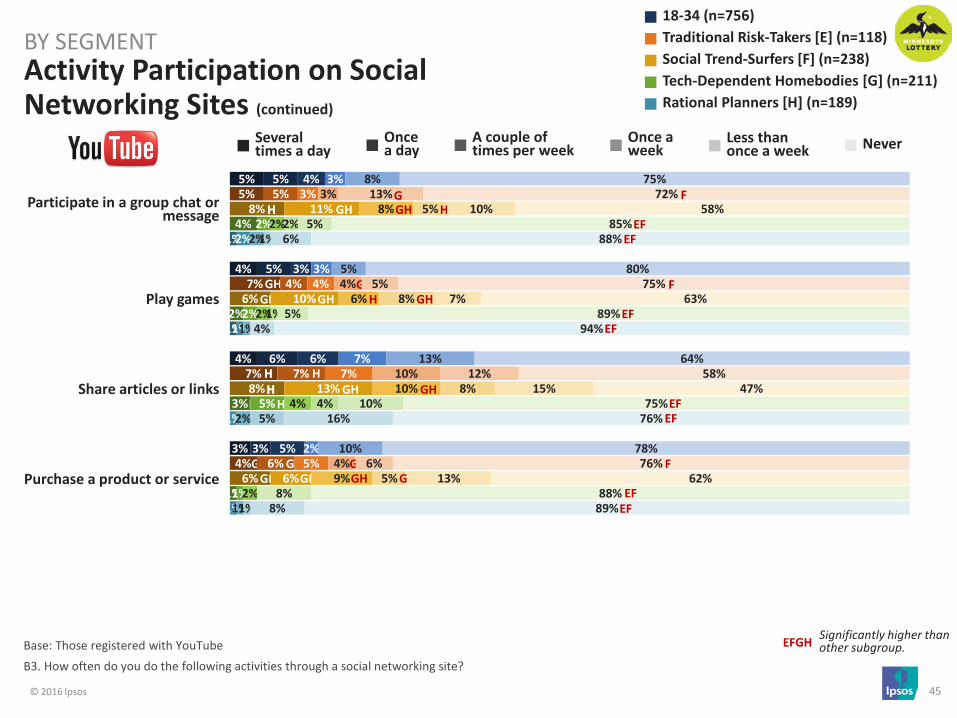

Base: Those registered with YouTube B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites (continued)

BY SEGMENT

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

Participate in a group chat or message

Play games

Share articles or links

Purchase a product or service

EFGH Significantly higher than other subgroup.

18-34 (n=756) Traditional Risk-Takers [E] (n=118) Social Trend-Surfers [F] (n=238) Tech-Dependent Homebodies [G] (n=211) Rational Planners [H] (n=189)

GH GH

GH GH

H H

H

H

5%

5%

6%

3%

5%

4%

7%

6%

11%

10%

13%

6%

2%

2%

5%

1%

2%

1%

1%

1%

H H

H

GH GH

GH

GH H

H

GH

4%

3%

6%

5%

3%

4%

7%

5%

8%

6%

10%

9%

2%

2%

4%

2%

2%

1%

2%

1%

GH

H

GH

GH

3%

3%

7%

2%

3%

4%

10%

4%

5%

8%

8%

5%

2%

1%

4%

1%

5%

1%

GH GH

GH GH

H

8%

5%

13%

10%

13%

5%

12%

6%

10%

7%

15%

13%

5%

5%

10%

8%

6%

4%

16%

8%

G 75%

80%

64%

78%

72%

75%

58%

76%

58%

63%

47%

62%

85%

89%

75%

88%

88%

94%

76%

89%

F

EF EF

F

EF EF

EF EF

F

EF EF

© 2016 Ipsos 46

39%

33%

15%

12%

7%

29%

19%

10%

7%

8%

46%

40%

21%

18%

14%

38%

31%

12%

13%

5%

37%

33%

12%

6%

2%

Base: Those registered with Snapchat * Small base size, interpret with caution. B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites (continued)

BY SEGMENT

Browsing my feed to see what's new

Share pictures or videos

Participate in a group chat or message

Follow brands, celebrities or companies I'm interested in

learning about

Searching the site for specific news

18-34 (n=607) Traditional Risk-Takers [E] (n=76)* Social Trend-Surfers [F] (n=192) Tech-Dependent Homebodies [G] (n=166) Rational Planners [H] (n=172)

EFGH Significantly higher than other subgroup.

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

E

E

EGH

EH H

E

H GH

20%

14%

9%

14%

7%

27%

12%

7%

5%

6%

20%

18%

13%

26%

11%

17%

15%

4%

10%

3%

18%

10%

11%

9%

6%

G

G

EGH

G

11%

19%

10%

11%

6%

18%

32%

13%

15%

12%

10%

15%

14%

12%

9%

12%

14%

10%

9%

3%

10%

22%

6%

9%

3%

G

FG

H

GH GH

4%

8%

6%

5%

5%

5%

15%

9%

5%

3%

5%

9%

5%

6%

9%

5%

5%

6%

7%

3%

3%

8%

7%

3%

2%

G

GH

8%

14%

13%

12%

8%

9%

15%

12%

11%

9%

5%

9%

9%

10%

8%

15%

19%

17%

15%

8%

6%

13%

13%

12%

7%

F

F

FH

17%

13%

47%

47%

68%

13%

9%

50%

57%

63%

13%

10%

39%

29%

50%

14%

17%

51%

47%

78%

26%

14%

51%

62%

80%

F F

F

F FG

EFG

EF EF

© 2016 Ipsos 47

5%

5%

5%

2%

8%

7%

3%

4%

8%

10%

10%

4%

4%

4%

3%

1%

1%

2%

2%

Base: Those registered with Snapchat * Small base size, interpret with caution. B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites (continued)

BY SEGMENT

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

Play games

Share articles or links

Click and view ads

Purchase a product or service

EFGH Significantly higher than other subgroup.

18-34 (n=607) Traditional Risk-Takers [E] (n=76)* Social Trend-Surfers [F] (n=192) Tech-Dependent Homebodies [G] (n=166) Rational Planners [H] (n=172)

GH

3%

4%

4%

3%

2%

1%

3%

8%

9%

10%

8%

1%

2%

1%

1%

1%

3%

2%

1%

GH

EGH

GH

EGH

3%

5%

5%

4%

3%

11%

3%

5%

6%

8%

10%

8%

2%

2%

2%

1%

1%

3%

2%

2%

GH

GH

3%

5%

4%

2%

3%

7%

5%

1%

5%

6%

6%

6%

1%

2%

2%

1%

3%

4%

2%

1%

GH

G

4%

8%

8%

6%

6%

3%

5%

9%

4%

10%

8%

7%

5%

10%

9%

4%

2%

7%

7%

6%

E

82%

72%

75%

83%

77%

71%

81%

81%

69%

57%

56%

68%

88%

80%

83%

93%

93%

81%

85%

91%

F

F F

F

EF EF

EF EF

F

F F

© 2016 Ipsos 48

20%

9%

8%

8%

8%

17%

6%

9%

7%

7%

26%

16% GH

13% H

15% GH

10%

17%

7%

8%

6%

7%

19%

5%

4%

6%

7%

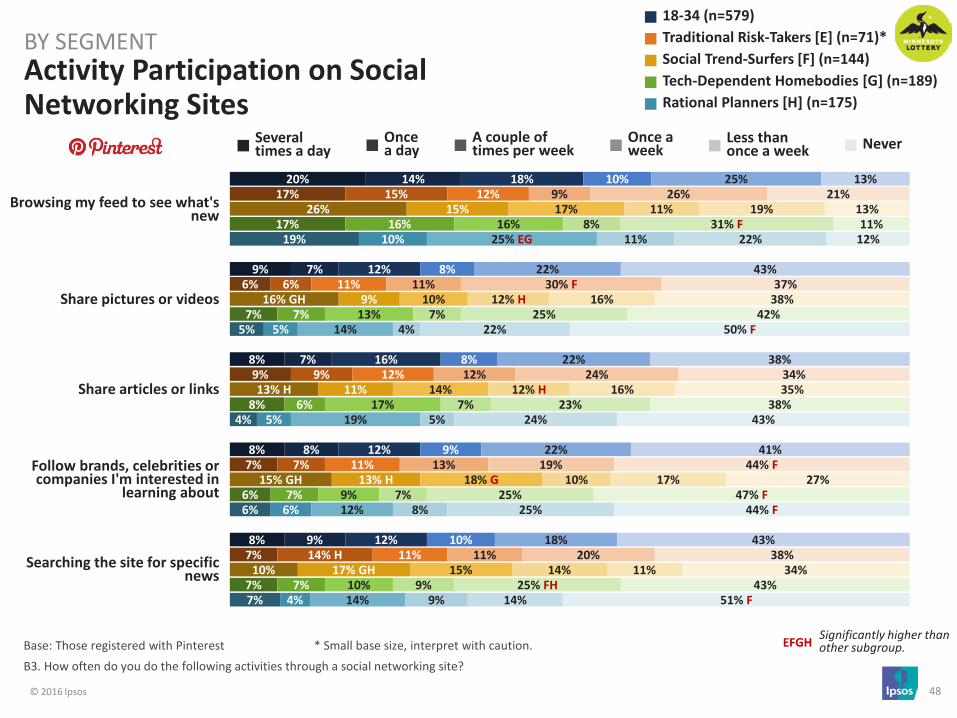

Base: Those registered with Pinterest * Small base size, interpret with caution. B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites

BY SEGMENT

Browsing my feed to see what's new

Share pictures or videos

Share articles or links

Follow brands, celebrities or companies I'm interested in

learning about

Searching the site for specific news

18-34 (n=579) Traditional Risk-Takers [E] (n=71)* Social Trend-Surfers [F] (n=144) Tech-Dependent Homebodies [G] (n=189) Rational Planners [H] (n=175)

EFGH Significantly higher than other subgroup.

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

14%

7%

7%

8%

9%

15%

6%

9%

7%

14% H

15%

9%

11%

13% H

17% GH

16%

7%

6%

7%

7%

10%

5%

5%

6%

4%

18%

12%

16%

12%

12%

12%

11%

12%

11%

11%

17%

10%

14%

18% G

15%

16%

13%

17%

9%

10%

25% EG

14%

19%

12%

14%

10%

8%

8%

9%

10%

9%

11%

12%

13%

11%

11%

12% H

12% H

10%

14%

8%

7%

7%

7%

9%

11%

4%

5%

8%

9%

25%

22%

22%

22%

18%

26%

30% F

24%

19%

20%

19%

16%

16%

17%

11%

31% F

25%

23%

25%

25% FH

22%

22%

24%

25%

14%

13%

43%

38%

41%

43%

21%

37%

34%

44% F

38%

13%

38%

35%

27%

34%

11%

42%

38%

47% F

43%

12%

50% F

43%

44% F

51% F

© 2016 Ipsos 49

5%

4%

3%

3%

10% GH

6%

5% H

5%

10% GH

7% GH

6% H

6% H

3%

2%

2%

3%

2%

2%

1%

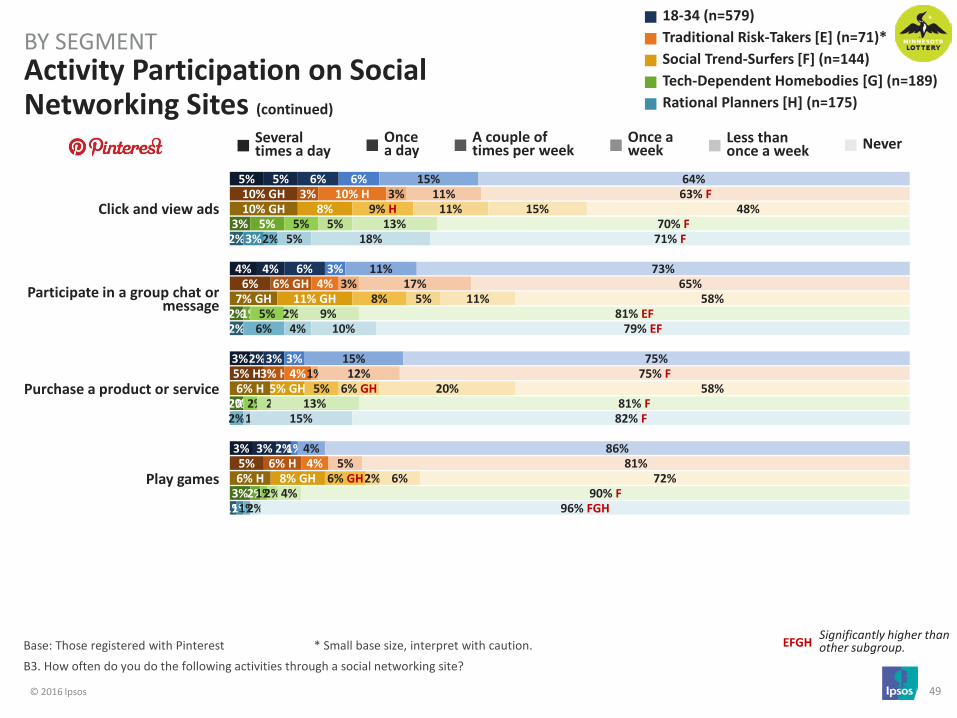

Base: Those registered with Pinterest * Small base size, interpret with caution. B3. How often do you do the following activities through a social networking site?

Activity Participation on Social Networking Sites (continued)

BY SEGMENT

Several times a day

Once a day

A couple of times per week

Once a week

Less than once a week Never

Click and view ads

Participate in a group chat or message

Purchase a product or service

Play games

EFGH Significantly higher than other subgroup.

18-34 (n=579) Traditional Risk-Takers [E] (n=71)* Social Trend-Surfers [F] (n=144) Tech-Dependent Homebodies [G] (n=189) Rational Planners [H] (n=175)

5%

4%

2%

3%

3%

6% GH

3% H

6% H

8%

11% GH

5% GH

8% GH

5%

1%

0%

2%

3%

1%

6%

6%

3%

2%

10% H

4%

4%

4%

9% H

8%

5%

6% GH

5%

5%

2%

1%

2%

6%

2%

1%

6%

3%

3%

1%

3%

3%

1%

11%

5%

6% GH

2%

5%

2%

2%

2%

5%

4%

1%

15%

11%

15%

4%

11%

17%

12%

5%

15%

11%

20%

6%

13%

9%

13%

4%

18%

10%

15%

2%

64%

73%

75%

86%

63% F

65%

75% F

81%

48%

58%

58%

72%

70% F

81% EF

81% F

90% F

71% F

79% EF

82% F

96% FGH

© 2016 Ipsos 50

TELEVISION

© 2016 Ipsos 51

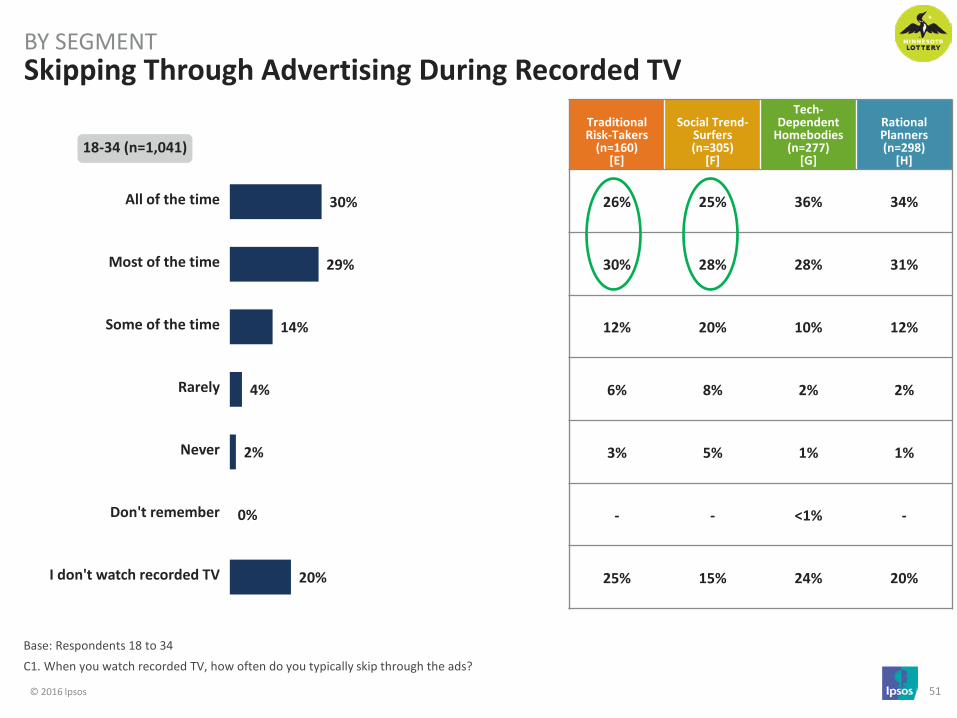

30%

29%

14%

4%

2%

0%

20%

All of the time

Most of the time

Some of the time

Rarely

Never

Don't remember

I don't watch recorded TV

Base: Respondents 18 to 34 C1. When you watch recorded TV, how often do you typically skip through the ads?

Skipping Through Advertising During Recorded TV BY SEGMENT

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

26% 25% 36% 34%

30% 28% 28% 31%

12% 20% 10% 12%

6% 8% 2% 2%

3% 5% 1% 1%

- - <1% -

25% 15% 24% 20%

18-34 (n=1,041)

© 2016 Ipsos 52

30%

29%

22%

19%

19%

41% GH

30% G

19%

22%

18%

35% GH

38% G

33% EGH

22% H

21%

21%

15%

21% H

21%

19%

27%

32% G

13%

14%

17%

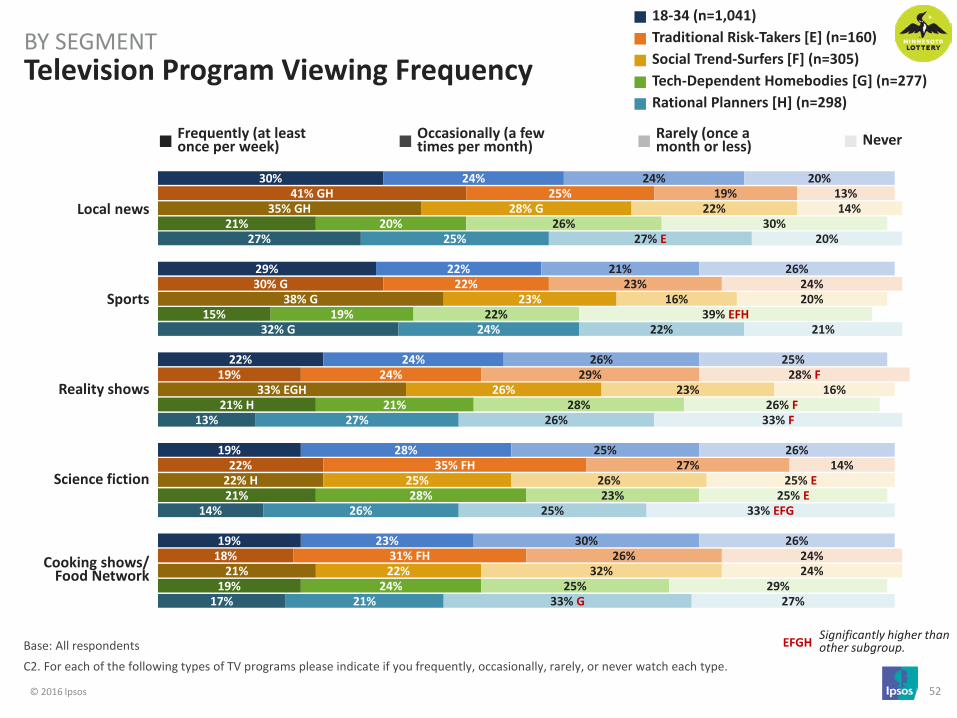

Base: All respondents C2. For each of the following types of TV programs please indicate if you frequently, occasionally, rarely, or never watch each type.

Television Program Viewing Frequency BY SEGMENT

Frequently (at least once per week)

Occasionally (a few times per month)

Rarely (once a month or less) Never

EFGH Significantly higher than other subgroup.

Local news

Sports

Reality shows

Science fiction

Cooking shows/ Food Network

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

24%

22%

24%

28%

23%

25%

22%

24%

35% FH

31% FH

28% G

23%

26%

25%

22%

20%

19%

21%

28%

24%

25%

24%

27%

26%

21%

24%

21%

26%

25%

30%

19%

23%

29%

27%

26%

22%

16%

23%

26%

32%

26%

22%

28%

23%

25%

27% E

22%

26%

25%

33% G

20%

26%

25%

26%

26%

13%

24%

28% F

14%

24%

14%

20%

16%

25% E

24%

30%

39% EFH

26% F

25% E

29%

20%

21%

33% F

33% EFG

27%

© 2016 Ipsos 53

18%

16%

12%

11%

22%

21% GH

14%

10%

21% H

21% GH

19% GH

20% EGH

15%

13%

8%

9%

15%

11%

8%

6%

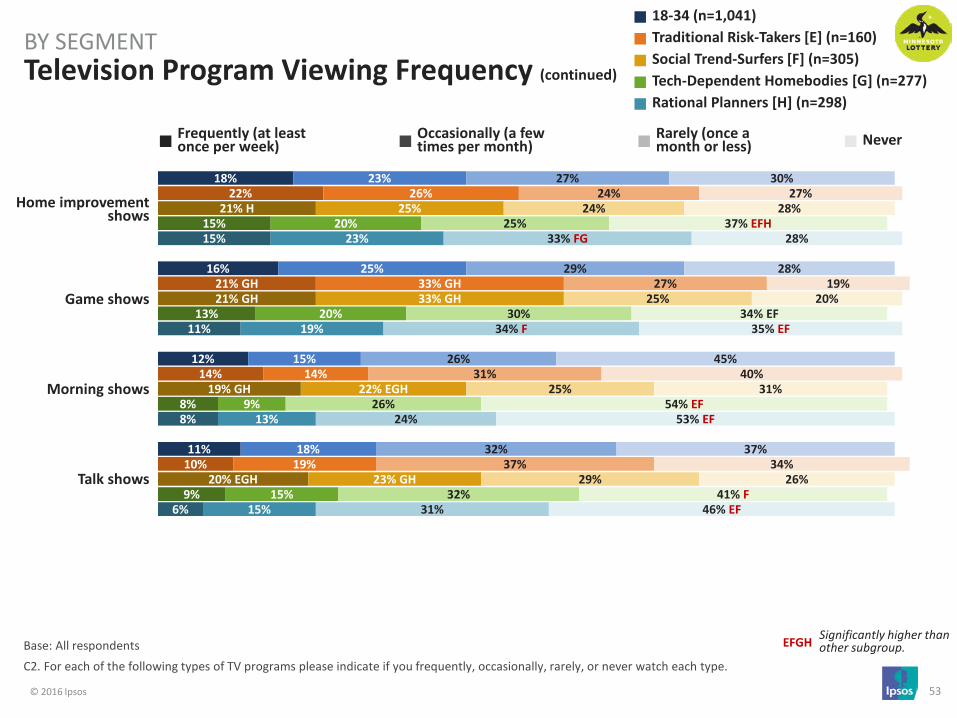

Base: All respondents C2. For each of the following types of TV programs please indicate if you frequently, occasionally, rarely, or never watch each type.

Television Program Viewing Frequency (continued)

BY SEGMENT

EFGH Significantly higher than other subgroup.

Home improvement shows

Game shows

Morning shows

Talk shows

Frequently (at least once per week)

Occasionally (a few times per month)

Rarely (once a month or less) Never

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

23%

25%

15%

18%

26%

33% GH

14%

19%

25%

33% GH

22% EGH

23% GH

20%

20%

9%

15%

23%

19%

13%

15%

27%

29%

26%

32%

24%

27%

31%

37%

24%

25%

25%

29%

25%

30%

26%

32%

33% FG

34% F

24%

31%

30%

28%

45%

37%

27%

19%

40%

34%

28%

20%

31%

26%

37% EFH

34% EF

54% EF

41% F

28%

35% EF

53% EF

46% EF

© 2016 Ipsos 54

RADIO / MUSIC

© 2016 Ipsos 55

14%

20%

67%

74%

9%

24%

75% F

72% F

13%

18%

55%

59%

18% E

24% H

72% F

82% EF

13%

16%

70% F

84% EF

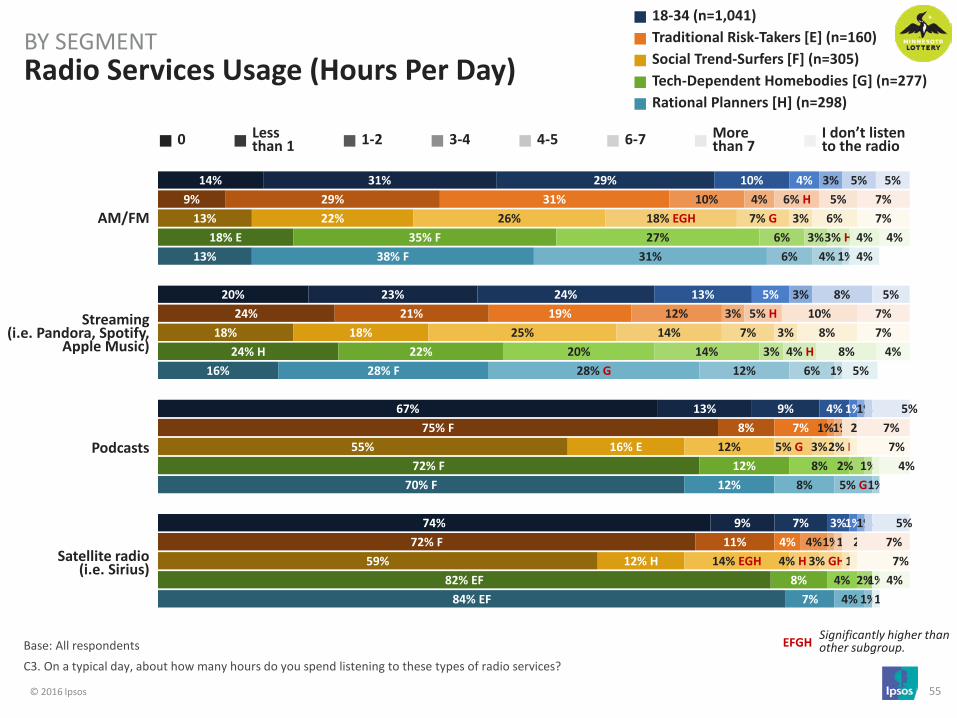

Base: All respondents C3. On a typical day, about how many hours do you spend listening to these types of radio services?

Radio Services Usage (Hours Per Day) BY SEGMENT

0 Less than 1 1-2 3-4 4-5 6-7 More

than 7 I don’t listen to the radio

AM/FM

Streaming (i.e. Pandora, Spotify,

Apple Music)

Podcasts

Satellite radio (i.e. Sirius)

EFGH Significantly higher than other subgroup.

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

31%

23%

13%

9%

29%

21%

8%

11%

22%

18%

16% E

12% H

35% F

22%

12%

8%

38% F

28% F

12%

7%

29%

24%

9%

7%

31%

19%

7%

4%

26%

25%

12%

14% EGH

27%

20%

8%

4%

31%

28% G

8%

4%

10%

13%

4%

3%

10%

12%

1%

4%

18% EGH

14%

5% G

4% H

6%

14%

2%

2%

6%

12%

5% G

1%

4%

5%

1%

1%

4%

3%

1%

1%

7% G

7%

3%

3% GH

3%

3%

1%

4%

6%

1%

3%

3%

1%

1%

6% H

5% H

1%

3%

3%

2% H

1%

3% H

4% H

1%

1%

5%

8%

1%

1%

5%

10%

2%

2%

6%

8%

1%

1%

4%

8%

1%

1%

4%

5%

1%

5%

5%

5%

5%

7%

7%

7%

7%

7%

7%

7%

7%

4%

4%

4%

4%

4%

4%

4%

4%

© 2016 Ipsos 56

75%

50%

24%

18%

3%

3%

79%

34%

15%

20%

2%

6%

75%

57%

37%

26%

1%

2%

66%

51%

17%

11%

4%

4%

79%

48%

21%

15%

5%

3%

45%

30%

7%

5%

3%

2%

57%

14%

5%

9%

2%

3%

38%

34%

11%

6%

1%

1%

42%

31%

8%

4%

4%

2%

50%

32%

4%

4%

4%

2%

Base: Listen to radio streaming services C4. Which of the following online music services do you currently use? Then, please indicate which service you most prefer to use.

Online Music Services Current Use and Preference BY SEGMENT

Pandora

Spotify

Apple Music

Google Play Music All Access

Amazon/ Amazon Prime

Music

iHeartRadio

Currently Use Prefer To Use

18-34 (n=780) Traditional Risk-Takers [E] (n=112) Social Trend-Surfers [F] (n=230) Tech-Dependent Homebodies [G] (n=200) Rational Planners [H] (n=238)

© 2016 Ipsos 57

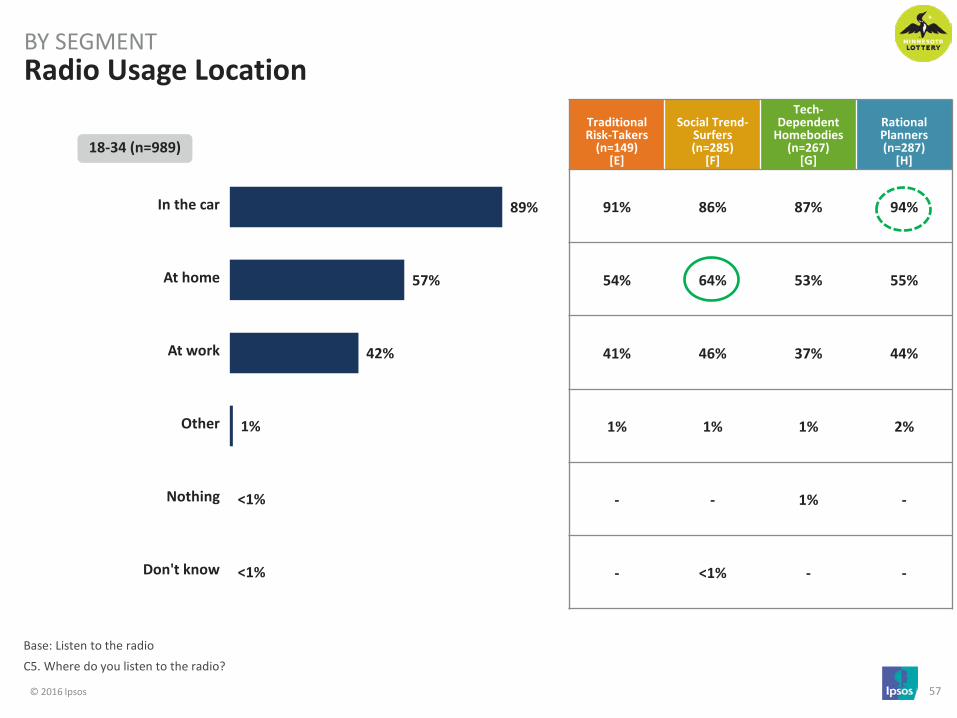

89%

57%

42%

1%

<1%

<1%

In the car

At home

At work

Other

Nothing

Don't know

Base: Listen to the radio C5. Where do you listen to the radio?

Radio Usage Location BY SEGMENT

Traditional Risk-Takers

(n=149) [E]

Social Trend-Surfers (n=285)

[F]

Tech-Dependent

Homebodies (n=267)

[G]

Rational Planners (n=287)

[H]

91% 86% 87% 94%

54% 64% 53% 55%

41% 46% 37% 44%

1% 1% 1% 2%

- - 1% -

- <1% - -

18-34 (n=989)

© 2016 Ipsos 58

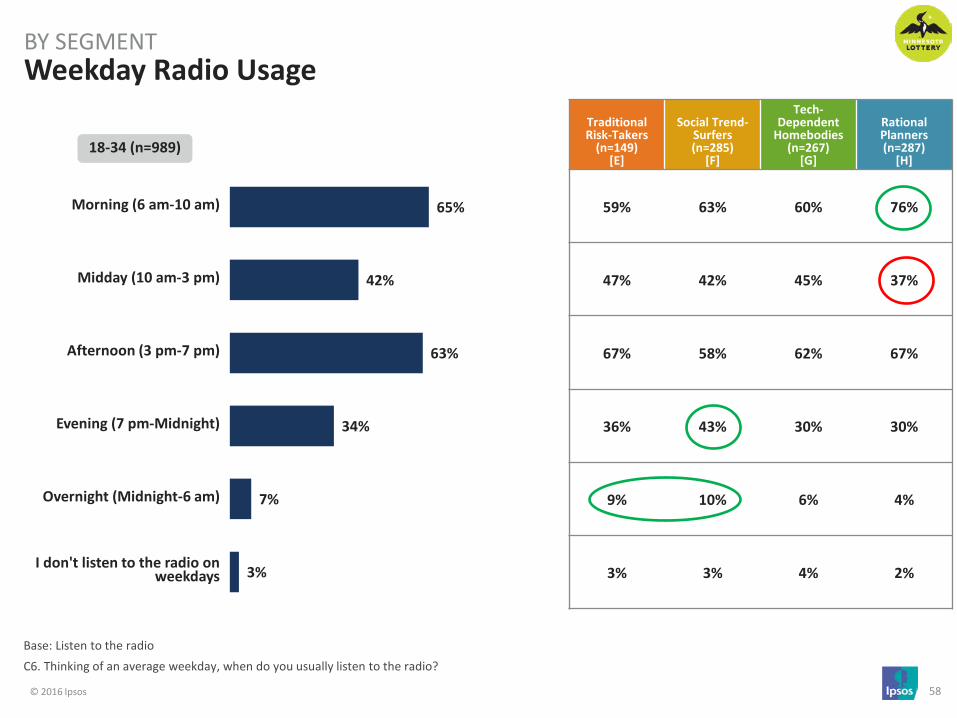

65%

42%

63%

34%

7%

3%

Morning (6 am-10 am)

Midday (10 am-3 pm)

Afternoon (3 pm-7 pm)

Evening (7 pm-Midnight)

Overnight (Midnight-6 am)

I don't listen to the radio on weekdays

Base: Listen to the radio C6. Thinking of an average weekday, when do you usually listen to the radio?

Weekday Radio Usage BY SEGMENT

Traditional Risk-Takers

(n=149) [E]

Social Trend-Surfers (n=285)

[F]

Tech-Dependent

Homebodies (n=267)

[G]

Rational Planners (n=287)

[H]

59% 63% 60% 76%

47% 42% 45% 37%

67% 58% 62% 67%

36% 43% 30% 30%

9% 10% 6% 4%

3% 3% 4% 2%

18-34 (n=989)

© 2016 Ipsos 59

23%

46%

51%

39%

10%

18%

Morning (6 am-10 am)

Midday (10 am-3 pm)

Afternoon (3 pm-7 pm)

Evening (7 pm-Midnight)

Overnight (Midnight-6 am)

I don't listen to the radio on weekends

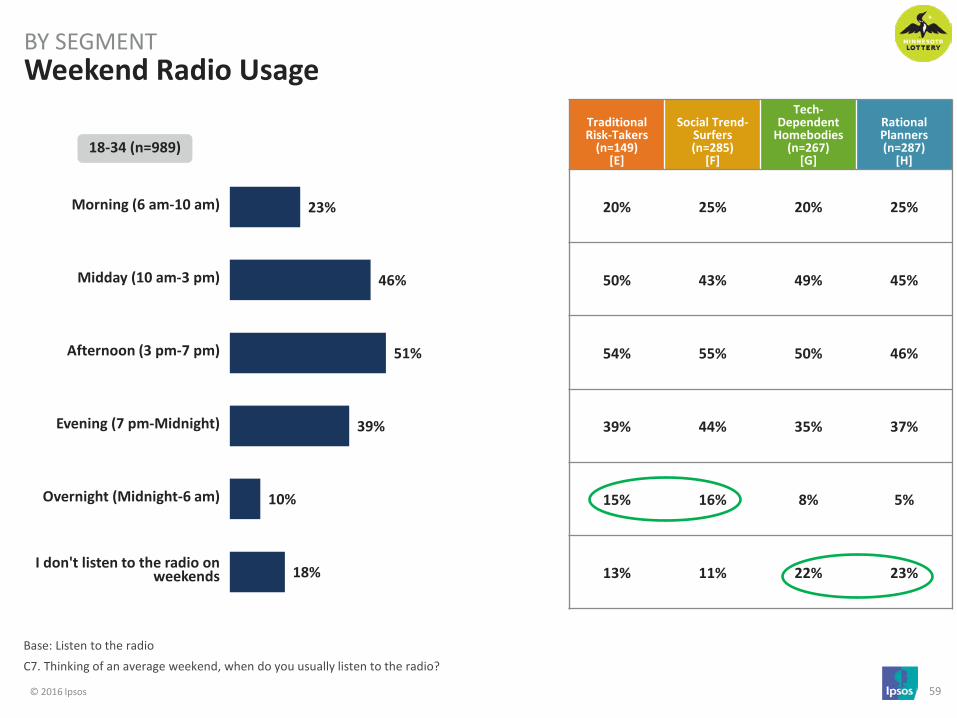

Base: Listen to the radio C7. Thinking of an average weekend, when do you usually listen to the radio?

Weekend Radio Usage BY SEGMENT

Traditional Risk-Takers

(n=149) [E]

Social Trend-Surfers (n=285)

[F]

Tech-Dependent

Homebodies (n=267)

[G]

Rational Planners (n=287)

[H]

20% 25% 20% 25%

50% 43% 49% 45%

54% 55% 50% 46%

39% 44% 35% 37%

15% 16% 8% 5%

13% 11% 22% 23%

18-34 (n=989)

© 2016 Ipsos 60

45%

35%

31%

28%

27%

34%

45% FG

38% GH

31% G

23%

53% EH

33%

39% GH

34% G

28%

46% E

32%

24%

20%

27%

43%

36%

26%

28% G

29%

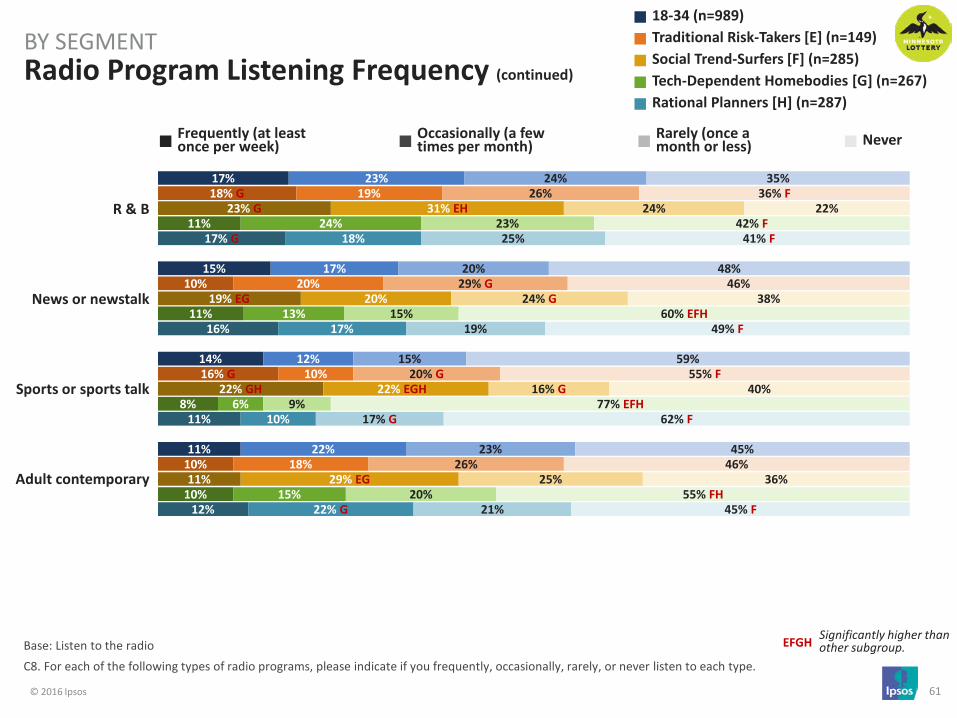

Base: Listen to the radio C8. For each of the following types of radio programs, please indicate if you frequently, occasionally, rarely, or never listen to each type.

Radio Program Listening Frequency BY SEGMENT

Frequently (at least once per week)

Occasionally (a few times per month)

Rarely (once a month or less) Never

EFGH Significantly higher than other subgroup.

Pop

Rock

Country

Hip hop/rap

Alternative

18-34 (n=989) Traditional Risk-Takers [E] (n=149) Social Trend-Surfers [F] (n=285) Tech-Dependent Homebodies [G] (n=267) Rational Planners [H] (n=287)

28%

26%

15%

25%

28%

31%

24%

14%

20%

26%

27%

32% G

21% GH

30% EG

31% G

29%

22%

12%

22%

23%

26%

26%

14%

24%

30%

12%

20%

16%

22%

20%

13%

17%

12%

22%

24%

9%

19%

15%

19%

20%

11%

23%

19%

27% F

18%

16% F

19%

16%

20%

19%

15%

19%

38%

25%

26%

21% F

14%

36% F

27%

27%

12%

17%

26%

17%

22%

14%

23% E

45% F

31%

33% FH

15%

20%

44% F

27%

22%

© 2016 Ipsos 61

17%

15%

14%

11%

18% G

10%

16% G

10%

23% G

19% EG

22% GH

11%

11%

11%

8%

10%

17% G

16%

11%

12%

Base: Listen to the radio C8. For each of the following types of radio programs, please indicate if you frequently, occasionally, rarely, or never listen to each type.

Radio Program Listening Frequency (continued)

BY SEGMENT

EFGH Significantly higher than other subgroup.

R & B

News or newstalk

Sports or sports talk

Adult contemporary

Frequently (at least once per week)

Occasionally (a few times per month)

Rarely (once a month or less) Never

18-34 (n=989) Traditional Risk-Takers [E] (n=149) Social Trend-Surfers [F] (n=285)

Rational Planners [H] (n=287) Tech-Dependent Homebodies [G] (n=267)

23%

17%

12%

22%

19%

20%

10%

18%

31% EH

20%

22% EGH

29% EG

24%

13%

6%

15%

18%

17%

10%

22% G

24%

20%

15%

23%

26%

29% G

20% G

26%

24%

24% G

16% G

25%

23%

15%

9%

20%

25%

19%

17% G

21%

35%

48%

59%

45%

36% F

46%

55% F

46%

22%

38%

40%

36%

42% F

60% EFH

77% EFH

55% FH

41% F

49% F

62% F

45% F

© 2016 Ipsos 62

SHOPPING

© 2016 Ipsos 63

4%

3%

2%

1%

9%

5%

3%

3%

6%

5%

3%

3%

2%

3%

2%

1%

1%

Base: All respondents D1. Thinking of the various products you use around your home, such as groceries, snacks, and various household items, how often do you shop at each of the following types of stores?

Store Type Shop Frequency BY SEGMENT

Daily Several times a week

Once a week

A few times a month

Once a month

Less than once a month Never

EFGH Significantly higher than other subgroup.

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

Convenience stores

Big box stores such as Target or Wal-Mart

Supermarkets

Independently owned local businesses

H H

GH GH

GH H

H

16%

24%

17%

6%

25%

19%

18%

7%

17%

25%

21%

7%

15%

29%

14%

4%

9%

20%

15%

7%

G

FGH H

H

20%

34%

35%

12%

26%

29%

29%

10%

27%

35%

36%

17%

17%

30%

32%

8%

13%

39%

38%

11%

EG

GH

GH GH

25%

26%

25%

23%

19%

32%

25%

25%

25%

22%

22%

25%

26%

28%

26%

18%

27%

25%

29%

24%

F

G

10%

8%

11%

18%

6%

9%

16%

19%

10%

10%

9%

16%

12%

6%

12%

17%

12%

9%

9%

19%

FH

E

18%

4%

7%

26%

12%

5%

5%

24%

9%

2%

7%

17%

20%

5%

9%

37%

29%

5%

6%

28%

F

F F

EFH F

EF EFG

7%

1%

4%

15%

4%

1%

5%

14%

7%

2%

3%

15%

7%

6%

18%

10%

1%

2%

12%

H

E

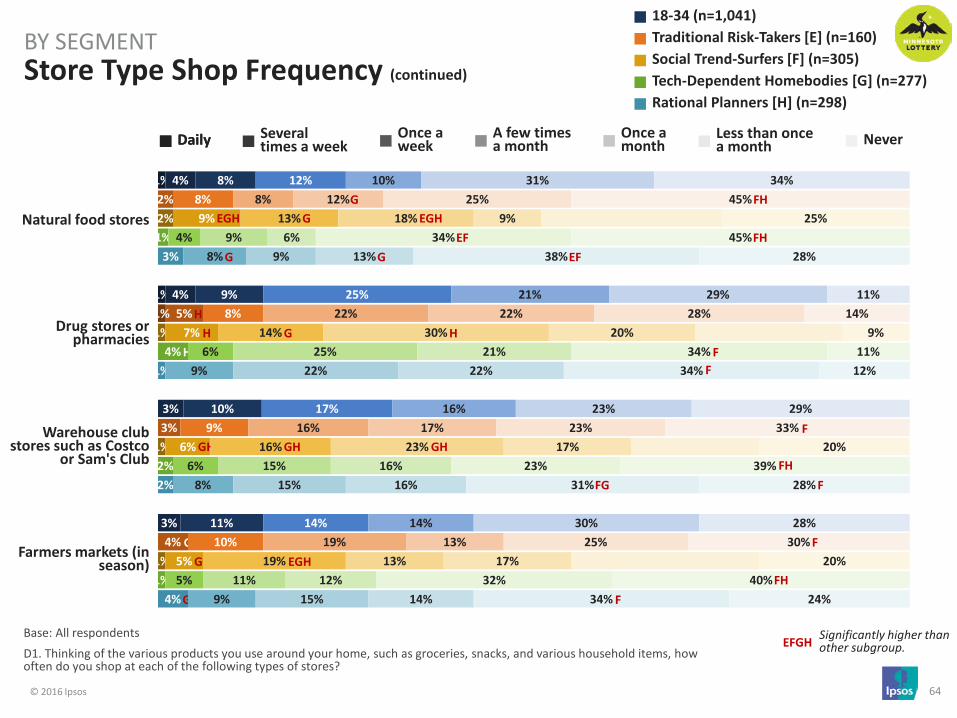

© 2016 Ipsos 64

1%

1% 1%

2%

1%

1%

1%

Base: All respondents D1. Thinking of the various products you use around your home, such as groceries, snacks, and various household items, how often do you shop at each of the following types of stores?

Store Type Shop Frequency (continued)

BY SEGMENT

Daily Several times a week

Once a week

A few times a month

Once a month

Less than once a month Never

EFGH Significantly higher than other subgroup.

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

Natural food stores

Drug stores or pharmacies

Warehouse club stores such as Costco

or Sam's Club

Farmers markets (in season)

H

4%

4%

3%

3%

1%

2%

5%

3%

4%

9%

7%

6%

5%

1%

4%

2%

1%

3%

1%

2%

4%

Daily

GH

EGH

H H

H

G G

G

8%

9%

10%

11%

8%

8%

9%

10%

13%

14%

16%

19%

4%

6%

6%

5%

8%

9%

8%

9%

GH

G

G

G

EGH

12%

25%

17%

14%

8%

22%

16%

19%

18%

30%

23%

13%

9%

25%

15%

11%

9%

22%

15%

15%

GH

EGH

H

10%

21%

16%

14%

12%

22%

17%

13%

9%

20%

17%

17%

6%

21%

16%

12%

13%

22%

16%

14%

G

G

31%

29%

23%

30%

25%

28%

23%

25%

24%

20%

17%

25%

34%

34%

23%

32%

38%

34%

31%

34%

FG

EF EF

F F

F

34%

11%

29%

28%

45%

14%

33%

30%

25%

9%

20%

20%

45%

11%

39%

40%

28%

12%

28%

24%

F

FH F

FH

FH

F

FH

© 2016 Ipsos 65

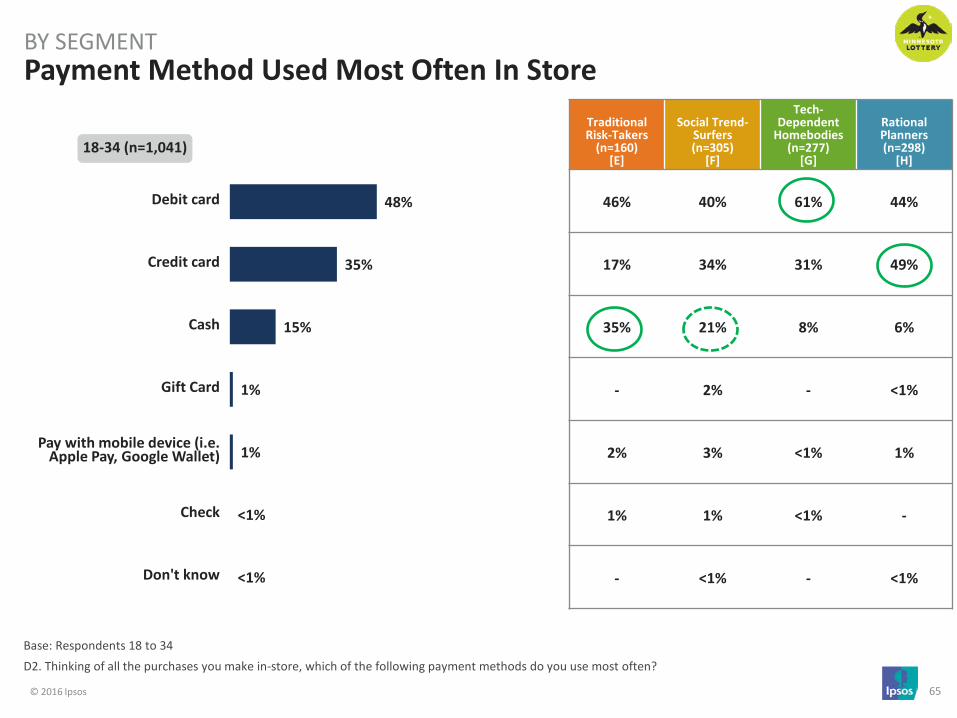

48%

35%

15%

1%

1%

<1%

<1%

Debit card

Credit card

Cash

Gift Card

Pay with mobile device (i.e. Apple Pay, Google Wallet)

Check

Don't know

Base: Respondents 18 to 34 D2. Thinking of all the purchases you make in-store, which of the following payment methods do you use most often?

Payment Method Used Most Often In Store BY SEGMENT

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

46% 40% 61% 44%

17% 34% 31% 49%

35% 21% 8% 6%

- 2% - <1%

2% 3% <1% 1%

1% 1% <1% -

- <1% - <1%

18-34 (n=1,041)

© 2016 Ipsos 66

73%

29%

In-store

Online

Base: Respondents 18 to 34 D3. Of all the shopping you do, what proportion do you do online vs. in-store?

Online vs. In-Store Shopping BY SEGMENT

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

77% 69% 75% 74%

27% 33% 27% 27%

Proportion (Mean excl. 0)

18-34 (n=1,041)

© 2016 Ipsos 67

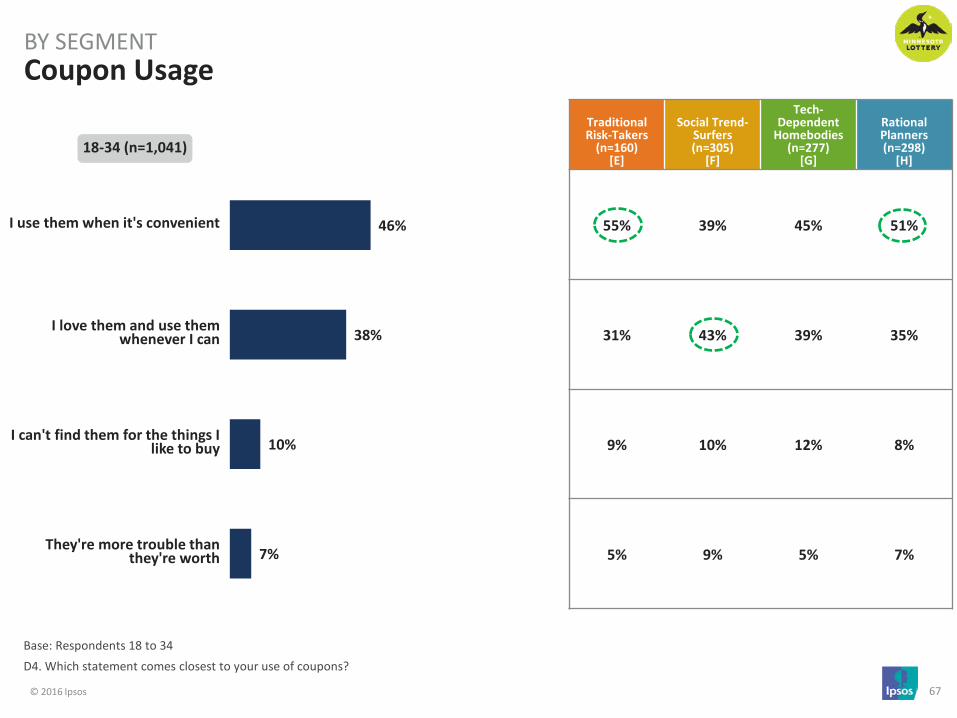

46%

38%

10%

7%

I use them when it's convenient

I love them and use them whenever I can

I can't find them for the things I like to buy

They're more trouble than they're worth

Base: Respondents 18 to 34 D4. Which statement comes closest to your use of coupons?

Coupon Usage BY SEGMENT

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

55% 39% 45% 51%

31% 43% 39% 35%

9% 10% 12% 8%

5% 9% 5% 7%

18-34 (n=1,041)

© 2016 Ipsos 68

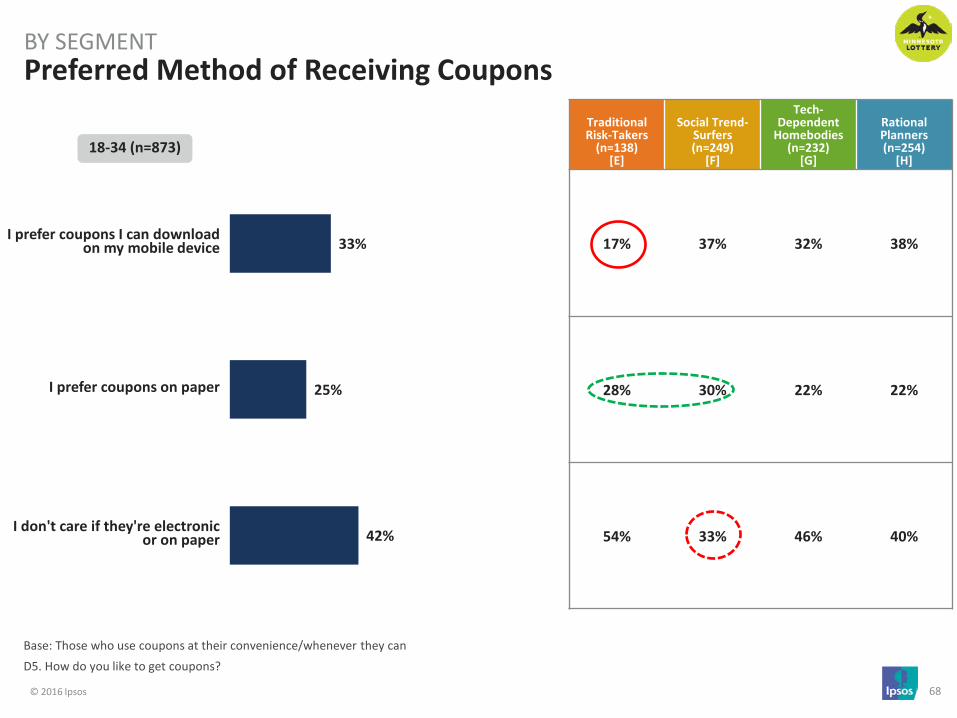

33%

25%

42%

I prefer coupons I can download on my mobile device

I prefer coupons on paper

I don't care if they're electronic or on paper

Base: Those who use coupons at their convenience/whenever they can D5. How do you like to get coupons?

Preferred Method of Receiving Coupons BY SEGMENT

Traditional Risk-Takers

(n=138) [E]

Social Trend-Surfers (n=249)

[F]

Tech-Dependent

Homebodies (n=232)

[G]

Rational Planners (n=254)

[H]

17% 37% 32% 38%

28% 30% 22% 22%

54% 33% 46% 40%

18-34 (n=873)

© 2016 Ipsos 69

66%

25%

2%

7%

Pay at pump

Pay clerk inside

Pay clerk outside at walk-up window

I don't usually purchase gas

Base: Respondents 18 to 34 D6. When buying gasoline, what is your primary method of payment?

Primary Payment Method When Purchasing Gasoline BY SEGMENT

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

27% 62% 71% 87%

59% 27% 21% 10%

2% 3% <1% <1%

12% 8% 8% 3%

18-34 (n=1,041)

© 2016 Ipsos 70

EVENTS & ENTERTAINMENT OPTIONS

© 2016 Ipsos 71

65%

65%

62%

46%

40%

30%

17%

17%

10%

10%

1%

<1%

Social Media

From friends or family

Online (i.e. own personal search)

Television

Radio

Online (websites that notify you of upcoming events)

At an event

Coupons

Billboard

Direct mail

Other

Don't know

Base: Respondents 18 to 34 E1. Where do you look to find out about entertainment options?

Source(s) of Information Regarding Entertainment Options BY SEGMENT

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

58% 63% 74% 62%

66% 53% 68% 72%

54% 55% 68% 67%

53% 51% 41% 43%

47% 39% 34% 41%

27% 27% 29% 35%

15% 19% 12% 19%

16% 22% 11% 16%

15% 14% 6% 8%

7% 15% 7% 8%

2% <1% - 1%

- <1% <1% -

18-34 (n=1,041)

© 2016 Ipsos 72

64%

48%

14%

7%

6%

61%

46%

17%

5%

5%

61%

54%

18%

12%

9%

65%

38%

11%

3%

3%

69%

54%

12%

6%

5%

Base: All respondents E2. Below you'll see a list of events that take place in Minnesota during the year. For each one, please select the response that best represents your experience with that event.

Minnesota Event Participation BY SEGMENT

I attended this event in the past year

I’ve attended this event, but not in the past year

I’d like to attend this event, but haven’t had the chance

I’m not interested in this event

I’m not familiar with this event

EFGH Significantly higher than other subgroup.

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

Mall of America

Minnesota State Fair

Minnesota Renaissance Festival

Red Bull Crushed Ice

Uptown Art Fair

G

G

G

G

EGH

G

24%

33%

30%

9%

13%

26%

32%

29%

7%

5%

20%

26%

23%

11%

15%

27%

42%

32%

3%

10%

24%

31%

36%

11%

18%

EFH

F F

E

EG

G

G

F

5%

12%

30%

31%

22%

9%

18%

37%

34%

22%

9%

12%

28%

31%

23%

4%

13%

28%

24%

18%

1%

9%

28%

36%

25%

H

G

G G

GH GH

5%

5%

21%

21%

18%

4%

4%

14%

18%

21%

4%

4%

19%

16%

15%

4%

7%

24%

29%

22%

6%

6%

22%

21%

17%

E E

F

EFH

2%

2%

6%

33%

41%

1%

4%

36%

48%

6%

5%

12%

29%

38%

1%

5%

42%

48%

1%

2%

26%

35%

EGH

H

FH

H

FH

EGH

© 2016 Ipsos 73

5%

3%

3%

2%

1%

1%

4%

5%

0%

1%

6%

6%

6%

6%

2%

2%

1%

1%

0%

1%

7%

2%

1%

1%

2%

Base: All respondents E2. Below you'll see a list of events that take place in Minnesota during the year. For each one, please select the response that best represents your experience with that event.

Minnesota Event Participation (continued)

BY SEGMENT

I attended this event in the past year

I’ve attended this event, but not in the past year

I’d like to attend this event, but haven’t had the chance

I’m not interested in this event

I’m not familiar with this event

EFGH Significantly higher than other subgroup.

18-34 (n=1,041) Traditional Risk-Takers [E] (n=160) Social Trend-Surfers [F] (n=305) Tech-Dependent Homebodies [G] (n=277) Rational Planners [H] (n=298)

Basilica Block Party

WE Fest

Soundset

Rock the Garden

Bayfront Blues Festival

G GH

EG

EG

GH GH

EGH

9%

9%

7%

5%

4%

9%

10%

6%

3%

2%

10%

14%

11%

8%

6%

6%

4%

3%

2%

2%

9%

7%

7%

6%

4%

G GH

EG

G

G

G

G

33%

31%

25%

24%

16%

30%

43%

26%

22%

18%

36%

34%

30%

25%

21%

25%

25%

22%

17%

7%

39%

26%

22%

30%

19%

GH GH

G G

G

G

G

GH

G

G

18%

34%

18%

14%

20%

14%

23%

16%

13%

21%

18%

25%

15%

16%

21%

20%

41%

21%

16%

21%

16%

44%

20%

11%

17%

EF EF

37%

23%

47%

55%

60%

47%

19%

47%

62%

59%

29%

21%

37%

45%

51%

47%

30%

53%

65%

71%

29%

22%

50%

52%

59%

EFH

EFH

FH

FH

F

F F

F

FH

© 2016 Ipsos 74

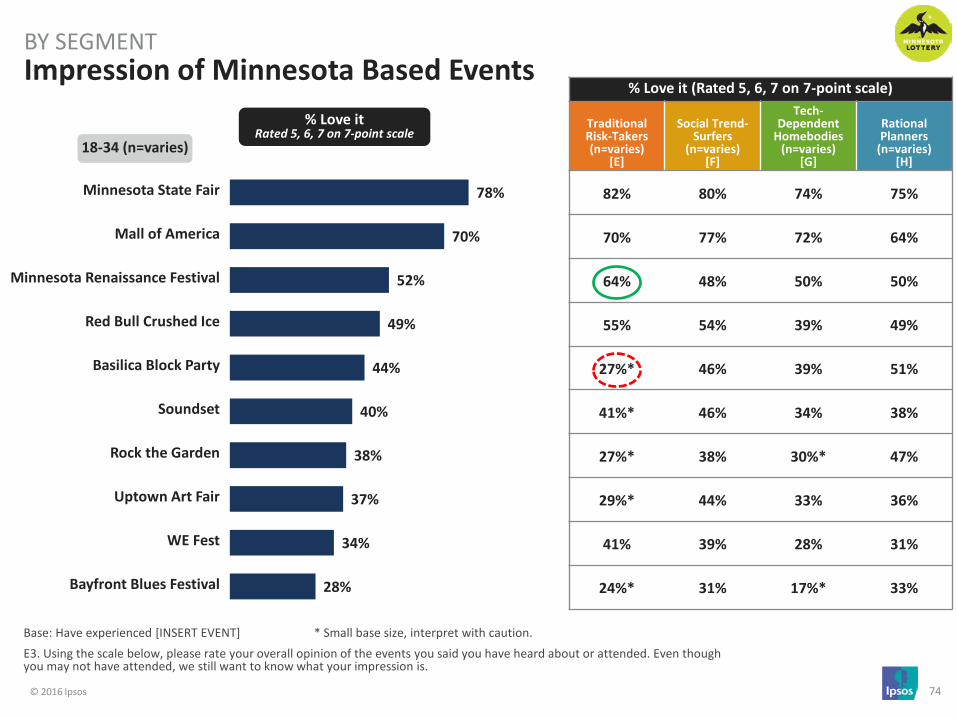

78%

70%

52%

49%

44%

40%

38%

37%

34%

28%

Minnesota State Fair

Mall of America

Minnesota Renaissance Festival

Red Bull Crushed Ice

Basilica Block Party

Soundset

Rock the Garden

Uptown Art Fair

WE Fest

Bayfront Blues Festival

Base: Have experienced [INSERT EVENT] * Small base size, interpret with caution. E3. Using the scale below, please rate your overall opinion of the events you said you have heard about or attended. Even though you may not have attended, we still want to know what your impression is.

Impression of Minnesota Based Events BY SEGMENT

18-34 (n=varies)

% Love it (Rated 5, 6, 7 on 7-point scale)

Traditional Risk-Takers (n=varies)

[E]

Social Trend-Surfers

(n=varies) [F]

Tech-Dependent

Homebodies (n=varies)

[G]

Rational Planners

(n=varies) [H]

82% 80% 74% 75%

70% 77% 72% 64%

64% 48% 50% 50%

55% 54% 39% 49%

27%* 46% 39% 51%

41%* 46% 34% 38%

27%* 38% 30%* 47%

29%* 44% 33% 36%

41% 39% 28% 31%

24%* 31% 17%* 33%

% Love it Rated 5, 6, 7 on 7-point scale

© 2016 Ipsos 75

34%

19%

16%

14%

12%

7%

5%

4%

4%

Minnesota Twins

Minnesota Wild

Minnesota Vikings

University of Minnesota sports

Minnesota Timberwolves

A rodeo

Minnesota auto racing

Minnesota Lynx

Minnesota United Soccer

Base: All respondents E4. For each item indicate (a) if you have attended a game in the past year, (b) if you've watched a game on TV in the past year, and (c) if you regularly follow news articles/stories for that team.

Sports Entertainment Participation BY SEGMENT

% Attended a Game in the Past Year

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

31% 40% 21% 43%

21% 23% 8% 25%

18% 20% 9% 16%

15% 21% 4% 16%

8% 20% 4% 14%

8% 11% 5% 4%

9% 11% 1% 2%

4% 7% 2% 3%

3% 9% 1% 3%

18-34 (n=1,041)

% Attended a Game in the Past Year

© 2016 Ipsos 76

51%

41%

40%

26%

25%

13%

7%

6%

6%

Minnesota Vikings

Minnesota Wild

Minnesota Twins

Minnesota Timberwolves

University of Minnesota sports

Minnesota Lynx

Minnesota United Soccer

Minnesota auto racing

A rodeo

Base: All respondents E4. For each item indicate (a) if you have attended a game in the past year, (b) if you've watched a game on TV in the past year, and (c) if you regularly follow news articles/stories for that team.

Sports Entertainment Participation (continued)

BY SEGMENT

% Watched a Game on TV in the Past Year

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

57% 50% 44% 56%

47% 43% 27% 48%

45% 45% 30% 42%

28% 35% 15% 25%

28% 31% 15% 25%

17% 16% 9% 11%

8% 11% 3% 7%

8% 12% 2% 4%

7% 11% 1% 5%

18-34 (n=1,041)

% Watched a Game on TV in the Past Year

© 2016 Ipsos 77

23%

20%

20%

15%

14%

10%

8%

6%

5%

Minnesota Vikings

Minnesota Twins

Minnesota Wild

University of Minnesota sports

Minnesota Timberwolves

Minnesota Lynx

Minnesota United Soccer

Minnesota auto racing

A rodeo

Base: All respondents E4. For each item indicate (a) if you have attended a game in the past year, (b) if you've watched a game on TV in the past year, and (c) if you regularly follow news articles/stories for that team.

Sports Entertainment Participation (continued)

BY SEGMENT

% Regularly Follow News Articles/Stories

Traditional Risk-Takers

(n=160) [E]

Social Trend-Surfers (n=305)

[F]

Tech-Dependent

Homebodies (n=277)

[G]

Rational Planners (n=298)

[H]

26% 26% 17% 24%

23% 21% 15% 24%

24% 24% 12% 23%

16% 20% 8% 16%

16% 22% 9% 12%

7% 16% 7% 10%

6% 13% 3% 8%

9% 9% 2% 4%

5% 12% - 3%

18-34 (n=1,041)

% Regularly Follow News Articles/Stories

© 2016 Ipsos 78

KEY TAKEAWAYS

© 2016 Ipsos 79

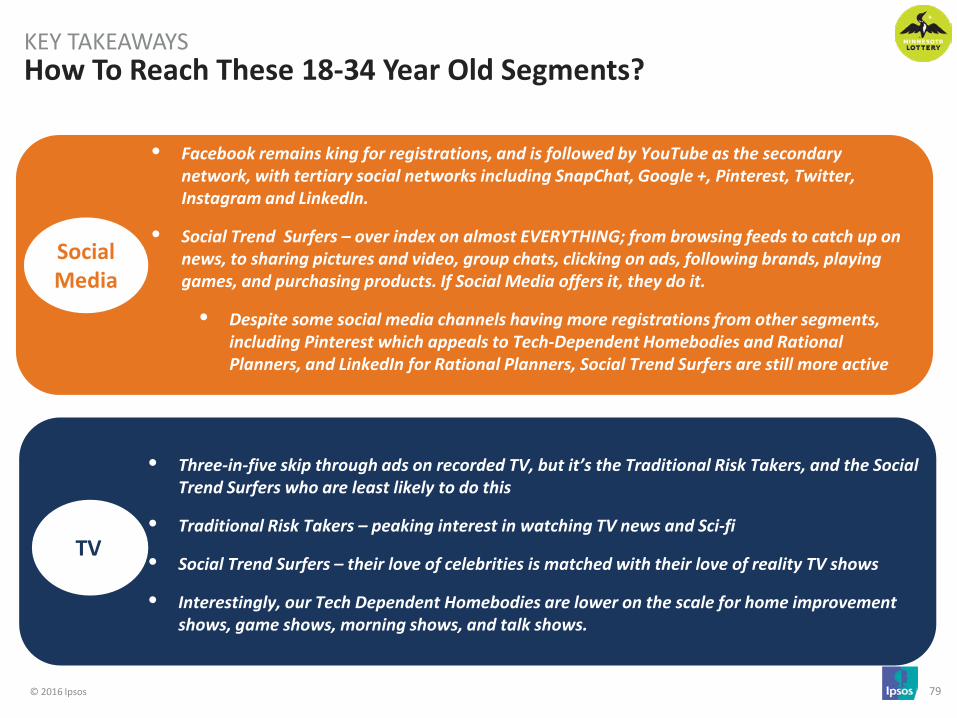

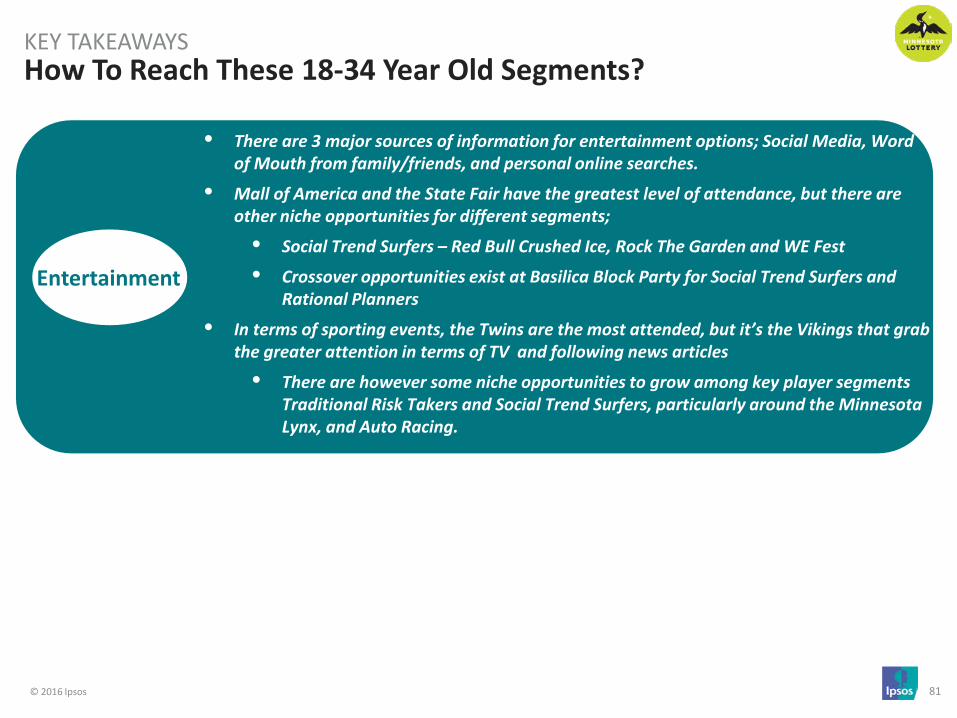

How To Reach These 18-34 Year Old Segments? KEY TAKEAWAYS

• Three-in-five skip through ads on recorded TV, but it’s the Traditional Risk Takers, and the Social Trend Surfers who are least likely to do this

• Traditional Risk Takers – peaking interest in watching TV news and Sci-fi