Mid-Con Energy Partners, LP - EnerCom Dallas · Mid-Con Energy Partners, LP EnerCom Dallas March 2,...

24

Mid-Con Energy Partners, LP EnerCom Dallas March 2, 2017 Financial information as of February 28, 2017

Transcript of Mid-Con Energy Partners, LP - EnerCom Dallas · Mid-Con Energy Partners, LP EnerCom Dallas March 2,...

Mid-Con Energy Partners, LP

EnerCom Dallas

March 2, 2017

Financial information as of February 28, 2017

NASDAQ: MCEP ● www.midconenergypartners.com 2

Forward-Looking Statements

This presentation includes "forward-looking statements" — that is, statements related to future, not past, events within the

meaning of the federal securities laws. Forward-looking statements are based on current expectations and include any statement

that does not directly relate to a current or historical fact. In this context, forward-looking statements often address expected future

business and financial performance, and often contain words such as "anticipate," "believe," "estimate," "intend," "expect," "plan,"

"project," "should," "goal," "forecast," "guidance," “could," “may," "continue," "might," "potential," "scheduled," or "will" or other

similar words. These forward-looking statements involve certain risks and uncertainties and ultimately may not prove to be

accurate. Actual results and future events could differ materially from those anticipated in such statements. For further discussion

of risks and uncertainties, you should refer to Mid-Con Energy's filings with the Securities and Exchange Commission (“SEC”)

available at www.midconenergypartners.com or www.sec.gov. Mid-Con Energy undertakes no obligation and does not intend to

update these forward-looking statements to reflect events or circumstances occurring after this presentation. You are cautioned

not to place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. All forward-

looking statements are qualified in their entirety by this cautionary statement and other SEC filings.

These forward–looking statements are subject to a number of risks and uncertainties, many of which are beyond our control,

which may include statements about our:

• business strategies;

• volatility or continued low or further declining commodity

prices;

• future financial and operating results, and our ability to

pay distributions;

• ability to replace the reserves we produce through

acquisitions and the development of our properties;

• revisions to oil and natural gas reserves estimates as a

result of changes in commodity prices;

• future capital requirements and availability of financing;

• technology;

• realized oil and natural gas prices;

• production volumes;

• lease operating expenses;

• general and administrative expenses;

• cash flow and liquidity;

• availability of production equipment;

• availability of oil field labor;

• capital expenditures;

• availability and terms of capital;

• marketing of oil and natural gas;

• general economic conditions;

• competition in the oil and natural gas industry;

• effectiveness of risk management activities;

• environmental liabilities;

• counterparty credit risk;

• governmental regulation and taxation;

• developments in oil producing and natural gas producing

countries; and

• plans, objectives, expectations and intentions.

NASDAQ: MCEP ● www.midconenergypartners.com 3

Mid-Con Energy Partners, LP

Investment Highlights

The

Right

Assets

The

Right

Team

The

Right

Strategy

The

Right

Structure

NASDAQ: MCEP ● www.midconenergypartners.com 4

Mid-Con Energy Partners, LP

Partnership Profile

"The Waterflood Guys"

• Core strength in enhanced oil recovery, focusing on

waterflooding

• Employees have prior experience in over 200

waterflood projects in 12 states

• Expertise focused on maximizing economically

recoverable oil

Straightforward Strategy & Structure

• Waterflood strategy is oil focused and includes both

organic development and acquisitions

• Private equity sponsor, Yorktown Energy Partners

(“Yorktown”), funded new private affiliates as

project incubators and drop-down vehicles

Organic / Acquisition Growth Potential

• Existing properties contain upside potential with

below average capital investment

• Since December 2011, Mid-Con Energy has closed

eleven acquisitions totaling approximately 16.0

MMBoe of estimated total proved reserves

• 19% CAGR in production since IPO

Market Highlights

Symbol / Exchange:

GP / LP Units Outstanding:

Preferred Units Outstanding:

Equity Value:

Debt Outstanding:

Enterprise Value:

MCEP / NASDAQ

30.3MM

11.6MM

$108.1MM

$121.5MM

$229.6MM

1) Based on 30,000,127 limited partner units and 360,000 general

partner units outstanding as of February 28, 2017.

2) Based on 11,627,906 Class A Convertible Preferred Units (“Preferred

Units”) as of February 28, 2017.

3) Based on February 28, 2017 market close price of $2.77 per common

unit and previously announced Unit Purchase Price of $2.15 per

Preferred Unit.

4) $121.5 million debt outstanding as of February 28, 2017.

(1)

(2)

(3)

(4)

NASDAQ: MCEP ● www.midconenergypartners.com 5

Primary Production – 10 to 25%

• Initial production from the reservoir typically recovered as a

result of expansion of reservoir fluids which are naturally

pressured within the producing formation

Secondary Production – 10 to 20%

• Waterflooding is the most commonly used method

• Additional oil is recovered by injecting water into the

reservoir, which displaces oil to producing wellbores

Tertiary Potential

• This type of recovery seeks to alter the properties of oil in

ways that facilitate additional production

• Examples include chemical flooding, thermal recovery

(steamfloods) and CO2 injection

• At this time, no estimated reserves or production associated

with potential tertiary recovery projects are assigned to Mid-

Con Energy’s properties

Original Oil In Place "OOIP"

The Right Strategy

Oil Recovery Overview

NASDAQ: MCEP ● www.midconenergypartners.com 6

The Right Strategy

Waterflooding Overview

• Waterflooding increases production and recovery of oil in place by displacing oil

from injection wells to producing wells

• Historically, the success of waterfloods has been attributable to the quality of the

reservoir rock, favorable reservoir fluid characteristics, availability of water for

injection and ease with which it can be injected

Surface

Waterflood

Target

Water Injected To Displace OilTypical Waterflood "5-Spot" Pattern

Injector

Producer

NASDAQ: MCEP ● www.midconenergypartners.com 7

The Right Assets

Core Area Summary

(1) Production volumes in Boe equivalents calculated at a rate of six Mcf per Bbl.

(2) Proved reserves based on SEC pricing for the twelve months ended December 31, 2016 of $42.75 per Bbl for oil and $2.49 per MMBtu for natural gas.

12/31/16 Proved Reserves (MBoe) 19,231

% Proved Developed 65%

December 2016 Net Production Boe/d 3,760

12/31/16 Proved Reserves (MBoe) 8,366

% Proved Developed 66%

December 2016 Net Production Boe/d 1,274

12/31/16 Proved Reserves (MBoe) 7,766

% Proved Developed 59%

December 2016 Net Production Boe/d 1,789

12/31/16 Proved Reserves (MBoe) 2,720

% Proved Developed 74%

December 2016 Net Production Boe/d 652

12/31/16 Proved Reserves (MBoe) 379

% Proved Developed 76%

December 2016 Net Production Boe/d 45

Total Mid-Con Energy Partners, LP(1)(2)

Northeastern Oklahoma

Permian

Southern Oklahoma

Other

NASDAQ: MCEP ● www.midconenergypartners.com 8

• Seek to acquire properties with low decline rates and upside potential

• Seek to acquire mature "drop-down" properties from Mid-Con Energy’s private

affiliates

• Capitalize on relationship with Yorktown

Exploit Potential

Of Existing

Property Base

Maintain Operational

Control and Cost

Effectiveness

Acquire High Quality

Properties For

EOR Development

Improve Liquidity

and Financial Flexibility

• Targeting a low Debt to EBITDA ratio

• Live within operating cash flow and focus on enhancing liquidity under revolver

• Hedged to help stabilize revenues against fluctuations in commodity prices

while maintaining some ability to participate in upside to current strip pricing

• Increase production and recovery from existing reserve portfolio (~95% Oil)

• Properties consist of interests in mature fields in Oklahoma and Texas with

well-understood geologic features, relatively predictable production profiles

and modest capital requirements

• Our affiliate, Mid-Con Energy Operating, operates ~100% of our properties

• Continue to maintain this level of control and favor acquisitions of operated

properties

• Realize certain service operating efficiencies from our third-party affiliate

The Right Strategy

Operating Strategy

NASDAQ: MCEP ● www.midconenergypartners.com 9

2016 Strategic Objectives

Transformational Year In Review

• Reduced 2016 total cash expenses of $25.36 per Boe (LOE, production

taxes, cash G&A, cash interest expense) 11.7% YoY

• 2016 LOE of $15.35 per Boe declined 21.5% YoY due to field-level cost

savings initiatives, Hugoton divestiture, and Permian Bolt-On acquisition

• 2016 total cash G&A of $5.7 million declined 8.1% YoY due to lower payroll

expense, professional fees, and discretionary G&A categories

• Reduced debt by $58.0 million, or 32.2%, during 2016 after investing over

$7.0 million in capital expenditures

• Debt outstanding of $122.0 million and Compliance Total Leverage of

2.59x, as calculated by our credit agreement, as of December 31, 2016

• Completed $25.0 million private offering of Class A Convertible Preferred

Units (“Preferred Units”) in August 2016 to fund Permian Bolt-On acquisition

Improve Efficiencies

& Cut Costs

Lower cash break-even levels, widen

margins

Live Within Cash Flow

Cash from operations to fund CAPEX

and debt reduction in 2016, fund

acquisitions with incremental equity-

weighted capital

Maintain Flexibility

In Uncertain TimesBalance short-term needs with long-term

objectives, protect balance sheet

• Increased conforming borrowing base to $140.0 million from $105.0 million

per August 2016 non-scheduled redetermination

• Subsequently reaffirmed conforming borrowing base of $140.0 million by

lender group in October 2016 during the fall redetermination

• Total liquidity of $20.4 million as of December 31, 2016, included $2.4 million

in cash and $18.0 million in accessible revolver borrowings

NASDAQ: MCEP ● www.midconenergypartners.com 10

Annual Cash Expenses Per Boe(1)

Reducing Costs In Response To Lower Prices

2014 2015 2016

LOE $22.93 $19.55 $15.35

Production taxes $5.56 $2.03 $1.96

Cash G&A $6.08 $3.61 $3.86

Cash interest expense $4.04 $3.53 $4.19

Total cash expenses $38.61 $28.72 $25.36

$22.93 $19.55

$15.35

$5.56

$2.03

$1.96

$6.08

$3.61

$3.86

$4.04

$3.53

$4.19

$38.61

$28.72

$25.36

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

2014 2015 2016

$/B

oe

LOE

Production taxes

Cash G&A

Cash interest expense

Total cash expenses

Total Cash Expense per Boe decreased 34.3% since 2014

Total LOE per Boe decreased 33.1% since 2014

Total Cash Expense per Boe decreased 11.7% since 2015

Total LOE per Boe decreased 21.5% since 2015

(1) Production volumes in Boe equivalents calculated at a rate of six Mcf per Bbl.

NASDAQ: MCEP ● www.midconenergypartners.com 11

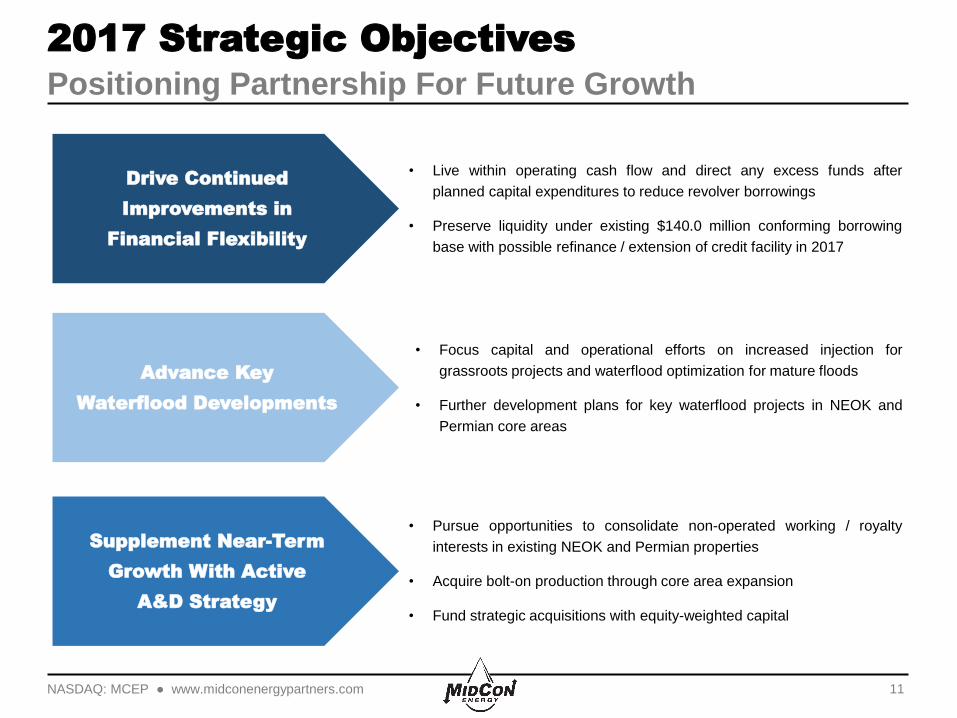

2017 Strategic Objectives

Positioning Partnership For Future Growth

• Live within operating cash flow and direct any excess funds after

planned capital expenditures to reduce revolver borrowings

• Preserve liquidity under existing $140.0 million conforming borrowing

base with possible refinance / extension of credit facility in 2017

• Focus capital and operational efforts on increased injection for

grassroots projects and waterflood optimization for mature floods

• Further development plans for key waterflood projects in NEOK and

Permian core areas

Drive Continued

Improvements in

Financial Flexibility

Advance Key

Waterflood Developments

Supplement Near-Term

Growth With Active

A&D Strategy

• Pursue opportunities to consolidate non-operated working / royalty

interests in existing NEOK and Permian properties

• Acquire bolt-on production through core area expansion

• Fund strategic acquisitions with equity-weighted capital

NASDAQ: MCEP ● www.midconenergypartners.com 12

Cash Margins Before Hedges

Cash Surplus, Inclusive of Total CAPEX, Above ~$34/Boe

$44.31 $30.00 $40.00 $50.00 $60.00 $70.00 $80.00

($/Boe) 4Q16

Oil & natural gas sales revenues $44.31 $30.00 $40.00 $50.00 $60.00 $70.00 $80.00

LOE(1)$14.56 $15.50 $15.50 $15.50 $15.50 $15.50 $15.50

Production taxes(2)$2.31 $1.59 $2.12 $2.65 $3.18 $3.71 $4.24

Cash G&A(3)$3.93 $4.23 $4.23 $4.23 $4.23 $4.23 $4.23

Cash interest expense(4)$3.21 $3.16 $3.16 $3.16 $3.16 $3.16 $3.16

Cash expenses $24.01 $24.48 $25.01 $25.54 $26.07 $26.60 $27.13

Cash margin excluding hedges $20.30 $5.52 $14.99 $24.46 $33.93 $43.40 $52.87

Less Total CAPEX(5)$6.70 $9.63 $9.63 $9.63 $9.63 $9.63 $9.63

Cash surplus/(shortfall) $13.60 ($4.11) $5.36 $14.83 $24.30 $33.77 $43.24

Oil price scenarios, realized $/Boe excluding hedges

$24.01 $24.48 $25.01 $25.54 $26.07 $26.60 $27.13

$6.70 $9.63 $9.63 $9.63 $9.63 $9.63 $9.63

$13.60

$(4.11)

$5.36 $14.83

$24.30

$33.77

$43.24

-$10

$0

$10

$20

$30

$40

$50

$60

$70

$80

$44.31 $30.00 $40.00 $50.00 $60.00 $70.00 $80.00

$/B

oe

Oil price scenarios, realized $/Boe

Cash surplus/(shortfall)

Total CAPEX

Cash expenses

Breakeven Operating

Cash Flows

4Q16Results

(1) Projections for LOE based on the mid-point of FY2017 guidance.

(2) Projections for production taxes calculated at 5.3% of total oil and gas revenues based on the mid-point of FY2017 guidance.

(3) Projections for G&A based on FY2016 cash G&A expenses divided by the mid-point of FY2017 Boe production guidance.

(4) Projections for cash interest based on $122MM in borrowings outstanding at December 31, 2016 at a rate of 3.5% divided by the mid-point of FY2017 Boe production guidance.

(5) Projections based on FY2017 capital budget of $13MM divided by the mid-point of FY2017 Boe production guidance.

NASDAQ: MCEP ● www.midconenergypartners.com 13

Debt & Liquidity Update

2.59x Total Leverage(1) and $140MM Borrowing Base

$203 $200 $194 $180 $169 $162 $128 $122

$37 $20$26

$8

$11

$12$18

$240

$220 $220

$188 $180

$163

$140 $140

2.77x

3.15x

3.47x3.27x

2.77x 2.71x

2.21x

2.59x

0.00x

1.00x

2.00x

3.00x

4.00x

5.00x

6.00x

$0

$40

$80

$120

$160

$200

$240

1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

Debt

/ E

BIT

DA

$M

M

Borrowings Available Debt Outstanding Borrowing Base Debt / EBITDA (Compliance TTM PF)

$140 Borrowing Base

Reaffirmed During

Fall-16 Redetermination

(1) Debt to EBITDA calculated on a trailing twelve month basis, as defined per the credit agreement, and includes pro forma adjustments for acquisitions and divestitures.

NASDAQ: MCEP ● www.midconenergypartners.com 14

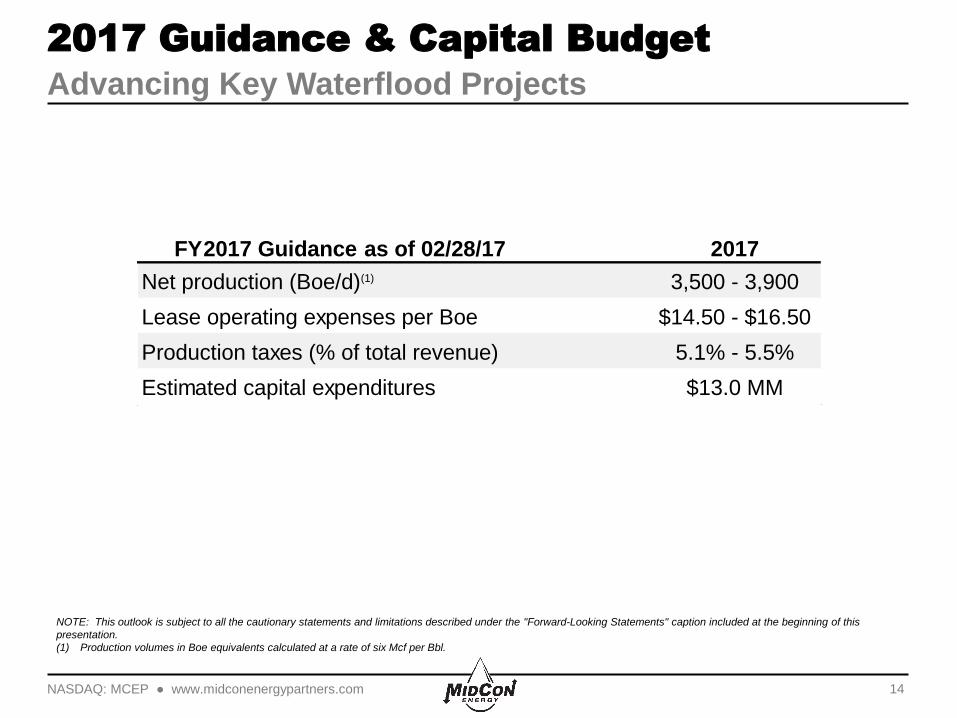

2017 Guidance & Capital Budget

Advancing Key Waterflood Projects

NOTE: This outlook is subject to all the cautionary statements and limitations described under the "Forward-Looking Statements" caption included at the beginning of this

presentation.

(1) Production volumes in Boe equivalents calculated at a rate of six Mcf per Bbl.

FY2017 Guidance as of 02/28/17 2017

Net production (Boe/d)(1) 3,500 - 3,900

Lease operating expenses per Boe $14.50 - $16.50

Production taxes (% of total revenue) 5.1% - 5.5%

Estimated capital expenditures $13.0 MM

NASDAQ: MCEP ● www.midconenergypartners.com 15

Mid-Con Energy Partners, LP

Investment Highlights

The

Right

Assets

The

Right

Team

The

Right

Strategy

The

Right

Structure

Appendix

NASDAQ: MCEP ● www.midconenergypartners.com 17

Commodity Derivatives

Summary Positions as of February 28, 2017

(1) Deferred premium puts include premiums that are to be paid monthly as the contracts settle (refer to our SEC filing for additional details). Total deferred put premiums by

calendar year: 2017 ($5.0MM) and 2018 ($0.4MM).

(2) Calculated estimated percent hedged based on the mid-point of FY2017 Boe production guidance multiplied by a 93% oil weighting based on fourth quarter 2016 reported

production volumes.

Oil Hedges 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Collar Volume (Bbl/d) 667 659 652 652 1,500 1,484 1,141 1,141 433 429 424 424

Call Strike Price ($/Bbl) 49.00$ 50.15$ 51.22$ 52.35$ 57.39$ 57.91$ 52.42$ 53.13$ 60.52$ 60.52$ 60.52$ 60.52$

Put Strike Price ($/Bbl) 40.00$ 45.00$ 45.00$ 45.00$ 45.00$ 45.00$ 43.57$ 43.57$ 50.00$ 50.00$ 50.00$ 50.00$

Put Volume (Bbl/d)(1)

2,000 1,978 1,957 1,793 - - 326 326 - - - -

Put Strike Price ($/Bbl)(1)

50.00$ 50.00$ 50.00$ 50.00$ -$ -$ 45.00$ 45.00$ -$ -$ -$ -$

Total Hedged Volume (Bbl/d) 2,667 2,637 2,609 2,446 1,500 1,484 1,467 1,467 433 429 424 424

Floor Strike Price ($/Bbl) 47.50$ 48.75$ 48.75$ 48.67$ 45.00$ 45.00$ 43.89$ 43.89$ 50.00$ 50.00$ 50.00$ 50.00$

% Hedged(2) 77% 77% 76% 71% 44% 43% 43% 43% 13% 12% 12% 12%

2,667 2,637 2,609

2,446

1,500 1,484 1,467 1,467

433 429 424 424

$30

$40

$50

$60

$70

$80

$90

0

500

1,000

1,500

2,000

2,500

3,000

1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19

Avera

ge F

loo

r P

rice (

$/B

bl)

Bb

l/d

Hed

ged

Put Volume (Bbl/d)(1)

Collar (% Hedged, LHS)

Total Hedge Volume

Floor Price ($/Bbl, RHS)

WTI Futures ($/Bbl, RHS)

NASDAQ: MCEP ● www.midconenergypartners.com 18

Operating and Financial Results

Sequential and YoY Variance Analysis

(1) Production volumes in Boe equivalents calculated at a rate of six Mcf per Bbl.

(2) Three months ended September 30, 2016 cash settlements from matured derivatives exclude $5.8 million received and the $1.5 million of deferred premiums paid upon early termination of previous oil

derivative contracts in July 2016.

(3) General and administrative include non-cash equity-based compensation expense of approximately $0.2 million in 4Q16, $0.3 million in 3Q16, and $0.2 million in 4Q15.

(4) This presentation includes "EBITDA", "Adjusted EBITDA" , and "Distributable Cash Flow", each of which are non-generally accepted accounting principles ("Non-GAAP") measures, and should not be

considered an alternative to net income (loss), net cash provided by operating activities or any other measure of financial performance or liquidity presented in accordance with GAAP.

Three Months Ended Variance Analysis

December 31, September 30, December 31, Quarter-over-quarter Year-over-year

(unaudited, in thousands, except per Boe data) 2016 2016 2015 # % # %

Select Operating Results

Oil (MBbl) 329 339 413 (10) -2.8% (84) -20.2%

Natural gas (MMcf) 144 149 154 (5) -3.2% (10) -6.4%

Total production (MBoe) (1)

353 364 439 (11) -3.0% (86) -19.6%

Average daily production (Boe/d) 3,837 3,957 4,772 (120) -3.0% (935) -19.6%

Select Financial Results

Oil sales 15,208$ 14,012$ 15,845$ 1,196$ 8.5% (637)$ -4.0%

Natural gas sales 434$ 398$ 394$ 36$ 9.0% 40$ 10.2%

Cash settlements from matured derivatives, inclusive of net premiums (2)

770$ 1,182$ 5,834$ (412)$ -34.9% (5,064)$ -86.8%

Oil & natural gas sales plus cash settlements from matured derivatives,

inclusive of premiums, net 16,412$ 15,592$ 22,073$ 820$ 5.3% (5,661)$ -25.6%

Lease operating expenses 5,141$ 5,709$ 8,298$ (568)$ -9.9% (3,157)$ -38.0%

Oil and gas production taxes 816$ 753$ 853$ 63$ 8.4% (37)$ -4.3%

General and administrative (3)

1,609$ 1,715$ 1,880$ (106)$ -6.2% (271)$ -14.4%

Select Non-GAAP Measures (4)

0 0.0%

Adjusted EBITDA 9,002$ 11,873$ 18,993$ (2,871)$ -24.2% (9,991)$ -52.6%

Distributable Cash Flow 6,242$ 9,104$ 15,462$ (2,862)$ -31.4% (9,220)$ -59.6%

Select Financial Results per Boe

Oil sales 43.08$ 38.49$ 36.09$ 4.59$ 11.9% 6.99$ 19.4%

Natural gas sales price 1.23$ 1.09$ 0.90$ 0.14$ 12.4% 0.33$ 37.0%

Cash settlements from matured derivatives, inclusive of net premiums (2)

2.18$ 3.25$ 13.29$ (1.07)$ -32.8% (11.11)$ -83.6%

Oil & natural gas sales plus cash settlements from matured derivatives,

inclusive of premiums, net 46.49$ 42.84$ 50.28$ 3.66$ 8.5% (3.79)$ -7.5%

Lease operating expenses 14.56$ 15.68$ 18.90$ (1.12)$ -7.1% (4.34)$ -23.0%

Oil and gas production taxes 2.31$ 2.07$ 1.94$ 0.24$ 11.7% 0.37$ 19.0%

General and administrative (3)

4.56$ 4.71$ 4.28$ (0.15)$ -3.3% 0.28$ 6.4%

Select Non-GAAP Measures (4)

Adjusted EBITDA 25.50$ 32.62$ 43.26$ (7.12)$ -21.8% (18)$ -41.1%

Distributable Cash Flow 17.68$ 25.01$ 35.22$ (7.33)$ -29.3% (18)$ -49.8%

NASDAQ: MCEP ● www.midconenergypartners.com 19

Appendix

Non-GAAP Summary(1)

(1) This presentation includes "EBITDA", "Adjusted EBITDA" , and "Distributable Cash Flow", each of which are non-generally accepted accounting principles ("Non-GAAP")

measures, and should not be considered an alternative to net income (loss), net cash provided by operating activities or any other measure of financial performance or

liquidity presented in accordance with GAAP.

(2) Full year 2016 reflects cash distributions to holders of Preferred units payable on November 14, 2016 and February 14, 2017, according to terms of the Partnership

Agreement, and attributable to the periods from August 11, 2016 to September 30, 2016 and October 1, 2016 to December 31, 2016, respectively.

December 31, December 31, December 31, December 31,

($ in thousands) 2016 2015 2016 2015

Reconciliation of Net Loss to Adjusted EBITDA and Distributable Cash Flow

Net loss (3,311) (57,961) (24,814) (95,495)

Interest expense, net 1,502 1,895 7,475 7,248

Depreciation, depletion and amortization 5,524 8,482 23,074 34,174

Accretion of discount on asset retirement obligations 134 156 577 432

Loss (gain) on derivatives, net 4,238 (9,822) 12,202 (22,366)

Cash settlements received for matured derivatives, net 2,044 12,977 20,511 28,543

Cash settlements received for early termination and modifications of

derivatives, net - - 5,820 11,069

Cash premiums received (paid) upon settlement for derivatives, net (1,274) 1 (5,040) (1,701)

Cash premiums paid at inception of derivatives, net (121) - (121) (14,064)

Impairment of proved oil and natural gas properties - 63,018 895 103,938

Impairment of proved oil and natural gas properties sold - - 3,578 -

Non-cash equity-based compensation 223 247 1,184 3,204

Loss on sales of oil and natural gas properties, net 43 - 560 -

Adjusted EBITDA 9,002 18,993 45,901 54,982

Less:

Cash interest expense 1,135 1,464 6,198 6,070

Estimated maintenance capital expenditures 1,123 1,520 4,473 8,473

Other non-operating cash income - 547 34 547

Distributions to preferred unitholders (2)

502 - 779 -

Distributable Cash Flow 6,242 15,462 34,417 39,892

Three Months Ended Year Ended

NASDAQ: MCEP ● www.midconenergypartners.com 20

Quarterly Cash Expenses Per Boe(1)

Continued Downtrend Through Fourth Quarter 2016

4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

LOE $21.56 $21.62 $18.14 $19.60 $18.90 $15.55 $15.57 $15.68 $14.56

Production taxes $4.42 $2.69 $3.14 $0.46 $1.94 $1.52 $1.97 $2.07 $2.31

Cash G&A $5.04 $4.12 $3.01 $3.61 $3.72 $4.35 $3.28 $3.86 $3.93

Cash interest expense $3.90 $3.50 $3.80 $3.51 $3.47 $4.96 $4.75 $3.74 $3.21

Total cash expenses $34.92 $31.93 $28.09 $27.18 $28.03 $26.38 $25.57 $25.35 $24.01

$21.56 $21.62 $18.14

$19.60 $18.90 $15.55 $15.57 $15.68 $14.56

$4.42 $2.69

$3.14 $0.46 $1.94

$1.52 $1.97 $2.07 $2.31

$5.04

$4.12

$3.01 $3.61

$3.72

$4.35 $3.28 $3.86 $3.93

$3.90

$3.50

$3.80 $3.51

$3.47

$4.96 $4.75 $3.74 $3.21

$34.92

$31.93

$28.09 $27.18 $28.03

$26.38 $25.57 $25.35 $24.01

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16

$/B

oe

LOE

Production taxes

Cash G&A

Cash interest expense

Total cash expenses

Total Cash Expense per Boe decreased 31.2% since 4Q14

Total LOE per Boe decreased 32.5% since 4Q14

Total Cash Expense per Boe decreased 14.3% since 4Q15

Total LOE per Boe decreased 23.0% since 4Q15

(1) Production volumes in Boe equivalents calculated at a rate of six Mcf per Bbl.

NASDAQ: MCEP ● www.midconenergypartners.com 21

Capital Expenditures

Fourth Quarter 2016 Activity

53%

47%

Growth Maintenance

$2.4MM

4Q16 CAPEX

$2.4 Million in 4Q16 Total CAPEX

• Maintenance: $1.1 million

• Growth $1.3: million

Initiated 6 conversions to injection(1)

• Permian: 5 conversions

• SOK: 1 conversion

Spud 3 producing wells

• Permian: 1 producing wells

• NEOK: 2 producing wells

Initiated 15 recompletions

• Permian: 4 recompletions

• NEOK: 8 recompletions

• SOK: 3 recompletions

MCEP Comments on Maintenance CAPEX: Maintenance CAPEX reflects the total amount of spending required to

maintain proper injection pressure and flood fronts across each individual unit.

(1) Does not include modification of target injection formation of two wells during the quarter.

NASDAQ: MCEP ● www.midconenergypartners.com 22

44%

40%

14%

2%

Permian NEOK SOK Other

2016 Proved Reserves(1)

Year End 2016 Audited SEC(2) Reserves

19.2

MMBoe

65%

35%

Proved Developed Proved Undeveloped

(1) Production volumes in Boe equivalents calculated at a rate of six Mcf per Bbl.

(2) SEC pricing for the twelve months ended December 31, 2016 of $42.75 per Bbl for oil and $2.49 per MMBtu for natural gas.

(3) Reserve-to-production ratio calculated based on dividing estimated net proved reserves as of December 31, 2016 by average net production for the month ended December

31, 2016 of 3,760 Boe/d.

Core Area Summary Reserve Category Summary

~14 Year

R/P Ratio(3)

NASDAQ: MCEP ● www.midconenergypartners.com 23

2017 Capital Budget

Core Area Summary

55%

29%

15%

1%

Permian NEOK SOK Other

$13.0MM

2017 CAPEX

Mid-Con Energy Partners, LP Investor Relations

2431 E. 61st Street, Suite 850

Tulsa, Oklahoma 74136

918.743.7575