Meridian Words on Wealth - Meridian Credit Union · “talking tax” and making tax, retirement...

8

Words on Wealth Meridian SPRING 2016 INVESTMENTS Getting to know socially responsible investing 3 MARKET UPDATE Whoa, Canada! 2 FINANCIAL ADVICE Benefits of working with your advisor 4 EXPERT’S CORNER What to do with your tax refund 6 It seems like every day we’re hearing something new and gloomy regarding the Canadian economy. But there’s more to the story. This issue kicks off with an economic summary that should help explain the negative and positive effects that a low loonie has on Canadians and Canadian businesses. That is followed by an article about the value of professional advice (hint: it actually contributes more to your savings over the long run!), and we provide you with some helpful tax return advice from a tax expert. We also have information on socially responsible investments that are designed to improve your returns, while allowing you to invest in a more ethical manner. Read on and remember that everyone at Meridian is here to help you. 2016 starts with a whimper

Transcript of Meridian Words on Wealth - Meridian Credit Union · “talking tax” and making tax, retirement...

Words on WealthMeridian

SPRING 2016

INVESTMENTS

Getting to know socially responsible investing

3MARKET UPDATE

Whoa, Canada!2 FINANCIAL ADVICE

Benefits of working with your advisor

4 EXPERT’S CORNER

What to do with your tax refund

6

It seems like every day we’re hearing something

new and gloomy regarding the Canadian

economy. But there’s more to the story. This issue

kicks off with an economic summary that should

help explain the negative and positive effects

that a low loonie has on Canadians and Canadian

businesses.

That is followed by an article about the value of

professional advice (hint: it actually contributes

more to your savings over the long run!), and we

provide you with some helpful tax return advice

from a tax expert. We also have information

on socially responsible investments that are

designed to improve your returns, while allowing

you to invest in a more ethical manner.

Read on and remember that everyone at Meridian

is here to help you.

2016 starts with a whimper

Words on Wealth

2

HOT TOPICS

Whoa, Canada!Ups and downs in our home and native land

similar one by the European Central Bank two years ago with a similar goal – to encourage banks to increase their loans and reduce the costs of borrowing for companies that use this capital to grow.

Closer to home, the U.S. seems to be the one bright spot that continues to keep the global economy growing. With the U.S. Federal Reserve Board planning to increase interest rates again if the U.S. economy continues to grow and many other central banks dropping rates in an effort to stimulate their local economies, the U.S. dollar appears poised to stay relatively strong for some time.

Build a plan and then stick to it

While it seems economic and market uncertainty may persist for some time, the virtues of working with a Meridian Wealth Advisor to create a financial plan that reflects your personal circumstances and long-term goals – and then sticking to that plan – remain. Of course, regular meetings to update your Meridian Wealth Advisor on any changes that may have occurred in your life and to review your plan to ensure it continues to reflect your unique needs and circumstances is always a good idea.

Don’t know where to start? The first step is into your Meridian branch to speak with a Meridian Wealth Advisor today.

The Canadian economy and equity markets were somewhat weak in 2015 and the first few months of 2016 have been more of the same. As we are all reminded when we visit the gas pump, energy prices have hit multi-year lows. Weaker energy prices have had a negative impact on our economy, and could continue to negatively impact Canada’s economy for some time.

That said, it’s not all gloom and doom. Rising interest rates in the U.S. and continued low interest rates in Canada have put downward pressure on the Canadian dollar. Although a weaker loonie makes shopping in the U.S. more expensive, the weaker Canadian dollar actually makes Canadian exports more attractive to buyers outside our borders. Increased sales to the U.S. and elsewhere should contribute to stronger economic growth in the export areas of Canada’s economy, helping to counter the negative impact of the continued weakness in the energy sector.

Most global equity markets have also remained somewhat volatile thus far in 2016, with China’s equity market falling so fast that it was shut down twice earlier in the year in response to selling by local and global investors. Questions about China’s economy have left many people concerned about the strength of the global economy. In Japan, policymakers introduced negative interest rates in an effort to stimulate that country’s economy. This move echoed a

SPRING 2016

3

INVESTMENTS

When you think of socially responsible investing (SRI), you probably think about what not to invest in: tobacco companies, firms that make weapons and big polluters like coal miners, for example.

However, there’s more to SRI than avoiding “bad” companies or seeking out the next big player in the wind turbine market. It’s about investing in financially sound companies that you can feel good about owning. It’s also about aligning your values with your investment portfolio. There is a growing consumer trend that points to thoughtful spending habits, from knowing where your meat and veggies come from (think local and organic) to understanding the impact of socially conscious business practices. SRI gives Members the opportunity to incorporate these values into their investment and retirement accounts.

Why SRI matters to you

A company responsible for a major environmental or human rights disaster will feel the impact on their reputation and their bottom line. These issues are costly and may even ruin a company financially, but they also hurt your portfolio performance. SRI attempts to remove that type of risk from an investment portfolio.

The ESG of SRI

SRI Funds focus on companies with strong financial performance that also have limited environmental, social and governance (ESG) risks. What does that mean?

Make a difference with socially responsible investingUnderstanding a different investment discipline

• Environmental risks have an actual or potential negative impact on our environment, so SRI Funds look for practices that could cause species extinction, pollution and climate change, among other things;

• Social risks are things like human rights practices, supply chains, worker safety and aboriginal rights;

• Governance risks have to do with the way companies are run. A few factors that SRI Funds look for include board diversity, corporate risk management practices and high executive compensation.

How SRI can make a difference

SRI Funds do more than screen for ESG risks. They can actively challenge companies to improve their ESG practices and become sustainability leaders in their industries. Ethical Funds research emerging trends, issues and risks that could affect the companies they own. They also work with policymakers to promote change on a broader scale.

Socially responsible investing can also help you diversify your portfolio by including Canadian, U.S. and global equity as well as fixed income funds.

If you’re interested in learning more, visit your local Meridian branch or speak to your Meridian Wealth Advisor.

Words on Wealth

4

FINANCIAL ADVICE

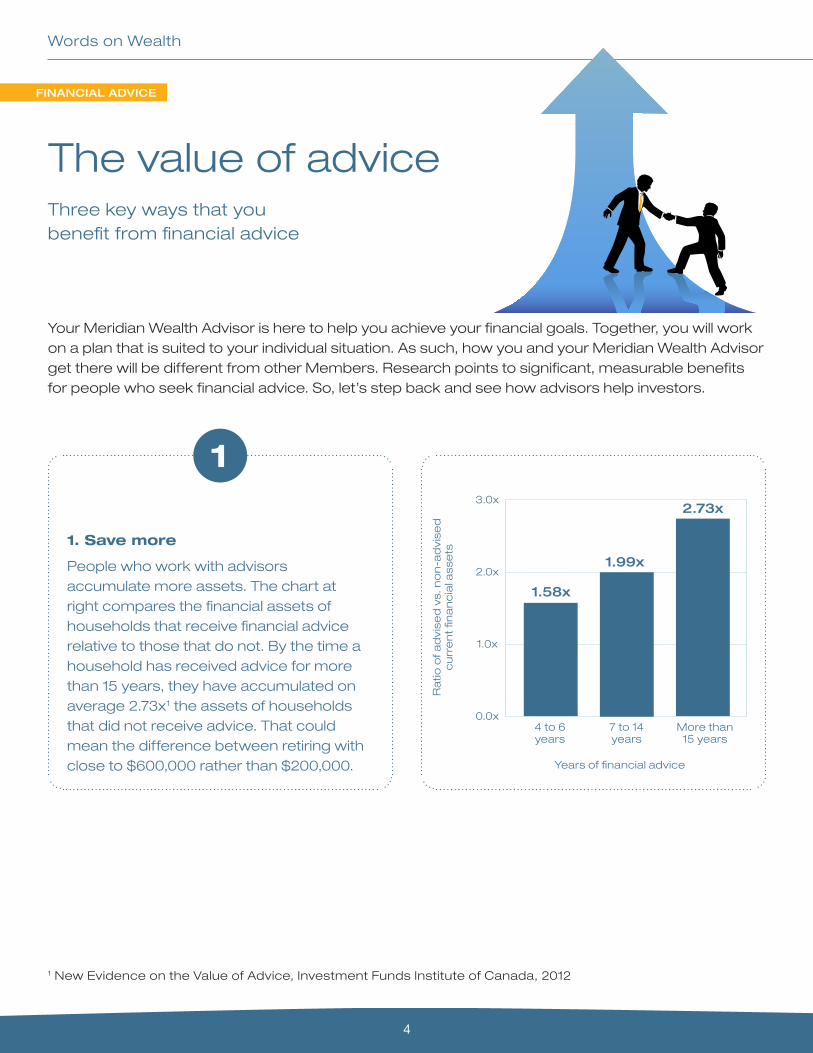

The value of adviceThree key ways that you benefit from financial advice

1. Save more

People who work with advisors accumulate more assets. The chart at right compares the financial assets of households that receive financial advice relative to those that do not. By the time a household has received advice for more than 15 years, they have accumulated on average 2.73x1 the assets of households that did not receive advice. That could mean the difference between retiring with close to $600,000 rather than $200,000.

1

1 New Evidence on the Value of Advice, Investment Funds Institute of Canada, 2012

Your Meridian Wealth Advisor is here to help you achieve your financial goals. Together, you will work on a plan that is suited to your individual situation. As such, how you and your Meridian Wealth Advisor get there will be different from other Members. Research points to significant, measurable benefits for people who seek financial advice. So, let’s step back and see how advisors help investors.

Years of financial advice

Ra

tio o

f a

dvi

sed

vs.

no

n-a

dvi

sed

c

urr

en

t fin

an

cia

l as

sets

2.73x

1.99x

1.58x

4 to 6 years

7 to 14 years

More than 15 years

3.0x

2.0x

1.0x

0.0x

SPRING 2016

5

Please contact your local branch or Meridian Wealth Advisor to discuss your bottom line.

2 The Value of Advice Report, Investment Funds Institute of Canada, 2012

2. Invest with discipline

Picking the right investments is essential but it goes much further. Greater wealth also comes from improved savings discipline. When investing, your Meridian Wealth Advisor helps you stay disciplined in three key ways:

• Helping you control your emotions – e.g., if stock markets fell 25%, some investors would sell their investments and consider themselves lucky. Stock markets, however, go up and down, and it helps to be reassured that short-term weakness is temporary and often an opportunity;

• Getting you to invest regularly – paying yourself first is an excellent strategy for building financial security through pre-authorized contributions;

• Appropriately allocating your assets – many Canadian investors suffer from “home country bias,” in which they invest the majority of their portfolio in Canadian securities. A portfolio like this is highly susceptible to the strength (and weakness) of the Canadian economy.

3. Be more confident

Besides a larger portfolio, what’s another result of long-term disciplined investing? Confidence. The confidence that comes from knowing you will have enough savings to live a comfortable retirement. Households that receive advice are 13%2 more likely to say that they are ready for retirement (compared to non-advised households).

The bottom line: the value of advice has a positive impact on the size of your portfolio and your peace of mind.

2 3

SIMPLE

SAFE SMART

Index-Linked GICsWe just put safety in the stock market with Index-Linked GICs.

All our Index-Linked GICs offer:

• Higher potential returns through the stock markets• 100% principal guarantee• No fees or commissions

To find out more, visit your branch today to speak with aMeridian Financial Advisor or call us at 1-866-592-2226.

Words on Wealth

6

Here’s some advice from an expert about what to do with it

EXPERT’S CORNER

If a Member wants to invest their tax refund, is an RRSP the best destination?

As all good advisors like to say, “It depends.” I am a firm believer in flexible financial planning. There isn’t one “financial planning solution” that meets the needs of all Members. If a Member doesn’t have “bad” debt, such as a credit card balance with high interest and their lifestyle needs are being met, than reinvesting a tax refund would be a prudent choice.

Is there a rule of thumb to decide if a tax refund should pay down debt or be invested?

If the Member has bad debt, for example a credit card balance being charged 19.99% or an unsecured line of credit with interest of about 8% or more, the tax refund should be used to pay either of these balances down first, as it’s unlikely the tax refund will generate a greater return if invested.

Getting a tax refund is a great feeling

Michelle Connolly, CPA, CA, CFP, TEPVice President, Tax, Retirement and Estate Planning, CI Investments

Michelle is a frequent speaker at CI and other financial industry events. She enjoys

“talking tax” and making tax, retirement and estate planning topics understandable

for advisors and clients, small to medium corporate enterprise owners and

incorporated professionals. Michelle is a graduate of Brock University’s Co-op

Accounting program.

THE EXPERT

If the Member has no bad debt, it would be prudent to invest the tax refund. We all recognize it’s more difficult to save than spend a windfall such as a tax refund, but life happens and being prepared and having a little extra saved for unplanned emergencies can reduce stress and allow Members to focus on what’s important.

Can a Member invest their tax refund in an RESP? A TFSA?

Absolutely! A Member can invest their tax refund in a RESP, TFSA, this year’s RRSP or an open account. A tax refund represents excess after-tax dollars paid to CRA – Members are free to invest or spend their tax refund as they see fit.

SPRING 2016

7

I might also recommend that John and Mary open up a Family RESP with $10,000 – $5,000 for 2016 and a make-up for 2015 to obtain a Canada Education Savings Grant of $2,000 ($500 for each child for two years).

For the remaining $5,000, a RRSP contribution for John or Mary might be a good idea, depending on their contribution room.

For more information on any of the ideas or accounts named in the article, or for a plan that is specific to your needs, contact your Meridian Wealth advisor today!

Important financial details

• $100,000 in an open account• $180,000 in RRSPs• No Tax Free Savings Accounts• No Registered Education Savings Plan

(RESP) investments• Their house is worth $600,000• Mortgage is $200,000, 3.5 years

remaining at 2.8%• John and Mary’s 2015 tax refunds

totalled $8,000

Can you share a case study with us that illustrates what Members could do?

Yes. Taking the time to determine what to do with a tax refund is also a good time to look at your entire portfolio. So, let’s consider John and Mary, both aged 42, and long-time Members. John is an executive earning $140,000 and Mary has recently returned to work as a part-time administrator in a dental practice earning $25,000. They have 10-year-old twins.

Providing John has been maxing out his RRSPs and Mary has little or no RRSP contribution room from the last 10 years, what should they consider?

I would recommend John and Mary each open a TFSA with $46,500* transferred from their open account to shelter any future income earned or capital gains from income tax. Having the TFSA available will let them access cash flow and provide flexibility for any unplanned lifestyle needs, such as braces for the twins, sports, a new car, or house repairs.

The math behind the plan

-

$108,000 (open acct + refund)

$46,500 (John’s TFSA)

$15,000 (remaining)=

- $10,000 (family RESP)

$46,500 (Mary’s TFSA)

$5,000 (John or Mary’s RRSP)-

-

Words on Wealth

meridiancu.ca

* Mutual funds are offered through Credential Asset Management Inc. Mutual funds, financial planning and other securities are offered through Credential Securities Inc. Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Unless otherwise stated, mutual fund securities, other securities and cash balances are not insured or guaranteed and are not covered by the Canada Deposit Insurance Corporation or by any other government deposit insurer that insures deposits in credit unions. Mutual funds and other securities are not guaranteed, their values change frequently and past performance may not be repeated. The information contained in this report was obtained from sources believed to be reliable; however, we cannot guarantee that it is accurate or complete and it should not be considered personal taxation advice. We are not tax advisors and we recommend that clients seek independent advice from a professional advisor on tax related matters. Credential Securities Inc. is a Member of the Canadian Investor Protection Fund.

™Trademarks of Meridian Credit Union Limited. 04/16;

As your trusted Meridian Wealth Advisor and your neighbour, I take the time to build a strong relationship for the long term, as well as to understand your unique needs. My goal is to translate where you want to go into an effective and achievable roadmap and to find the right investment solutions to help you save, protect and grow your financial assets.

Here is how I look forward to building our relationship and your trust:

✔ I provide an unbiased, honest perspective and my decisions are based only on your best interests. I have no bias toward any particular solution apart from the one that most effectively helps you meet your objectives;

✔ I ensure you clearly understand your wealth planning options and align your portfolio with the right solutions to help you reach your goals. We will review your finances together on a regular basis and I will keep you well informed so you always feel knowledgeable and comfortable.

As a Meridian Wealth Advisor and your neighbour, I am committed to working with you to create and build the right approach – tailored to your needs, your objectives and your values – to ensure your family's security.

What does wealth management mean at Meridian?

Words to Ponder"The difference between winning and losing is most often not quitting."

Walt Disney

WHY MERIDIAN WEALTH

It means: Trust. Advice. Planning.