Mega-Trends Influencing the Future of Auto Insurance National Auto Insurance ExecuSummit Uncasville,...

57

Mega-Trends Influencing the Future of Auto Insurance National Auto Insurance ExecuSummit Uncasville, CT October 19, 2010 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information Institute 110 William Street New York, NY 10038

-

Upload

deanna-starlin -

Category

Documents

-

view

217 -

download

1

Transcript of Mega-Trends Influencing the Future of Auto Insurance National Auto Insurance ExecuSummit Uncasville,...

Mega-Trends Influencing the Future of Auto

InsuranceNational Auto Insurance ExecuSummit

Uncasville, CTOctober 19, 2010

Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038Office: 212.346.5540 Cell: (917) 494-5945 [email protected] www.iii.org

2

Competition in the Auto Insurance Market

3

In Many States, the PP Auto Marketin 2009 was Highly Competitive

5

0

3

8

1110

7

4

2

0

2

4

6

8

10

12

under 700 700-799 800-899 900-999 1000-1099

1100-1199

1200-1299

1300-1399

1400 andover

*Herfindahl-Hirschman Index, a standard measure of market concentrationSources: Insurance Information Institute research from SNL Financial.

Number of States with HHI* in Indicated Range

An HHI Under 1000 is Generally Considered a Highly Competitive Market; HHIs Between 1000 and 1800 Indicate a Moderately Competitive Market;

Over 1800 Suggests a Concentrated Market

HHI Range

Highly Competitive Moderately Competitive

What HHIs of 775 and 1200 Look Like

Sources: SNL Financial; Insurance Information Institute

In the Highly Competitive Market, The Top 10 Carriers Have 77.8% Market Share; In the Moderately Competitive Market, the Top 10 Have 97.8%

The bar segments show the market share of the top 10 insurers in the state’s market plus(far right, light gray) the combined share of rest of the companies in that state’s market

5

PP Auto Competitive Environment Varies by State and Region*

1490

.614

28.9

1176

.511

63.7

1139

.611

23.2

1121

.111

11.9

1059

.410

03.1

983.

196

0.2

1265

.512

52.0

1184

.710

01.4

944.

2

1285

.789

9.3

731.

871

6.2

689.

464

5.7

1628

.1

1254

.7

600

800

1000

1200

1400

1600

1800

LA WV SC AL

MS TN KY FL AR

VA

GA

NC DE

MD NY

PA NJ

MA RI

NH CT

VT

ME

AK HI

*Data for 2009

Sources: SNL Financial; Insurance Information Institute.

Southeast Mid-Atlantic New EnglandHHI

6

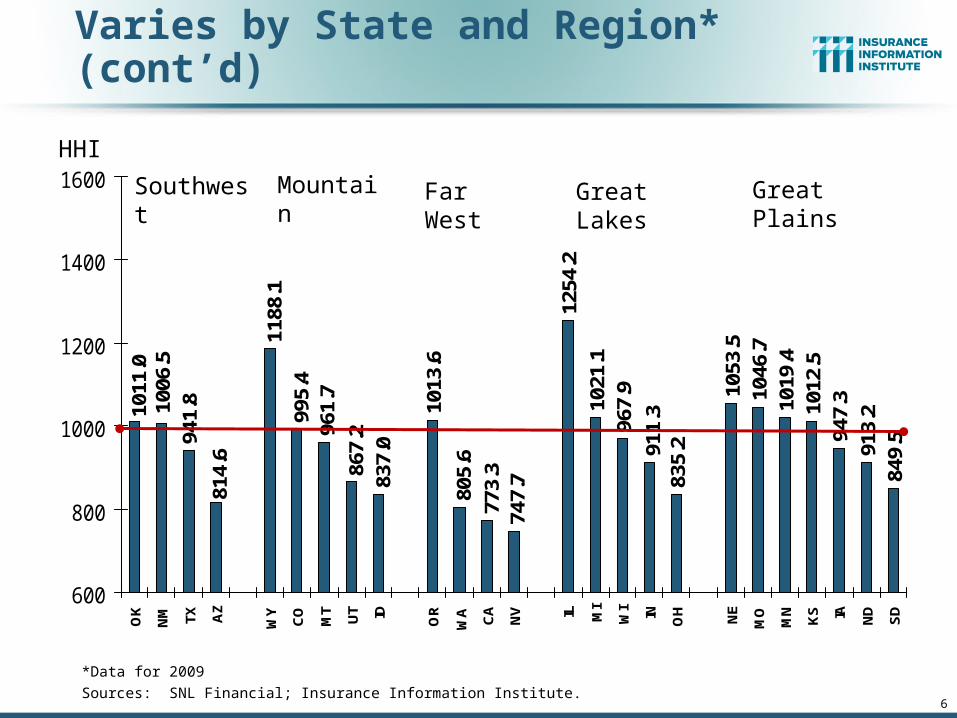

PP Auto Competitive EnvironmentVaries by State and Region* (cont’d)

1013

.6

1254

.2

1012

.594

7.3

913.

284

9.5

747.

777

3.3

805.

6 911.

383

5.2

1019

.4

967.

9 1046

.710

53.5

1021

.1

995.

4

837.

086

7.296

1.7

1188

.1

1006

.594

1.8

814.

6

1011

.0

600

800

1000

1200

1400

1600

OK

NM TX AZ

WY

CO

MT

UT ID OR

WA CA

NV IL MI

WI IN O

H NE

MO

MN

KS IA ND

SD

*Data for 2009

Sources: SNL Financial; Insurance Information Institute.

Southwest Mountain Far West Great PlainsGreat Lakes

HHI

7

Profitabilityin the Auto Insurance Market

8

Auto Insurance Return on Net Worth, 2008, Varies by Line, State and Region

9.7%

-0.7

%

7.4% 8.0%

7.9%

2.1%

5.5% 6.

3%

4.7%

3.4%

5.5%

2.1%

6.3%

4.7%

4.4%

1.5%

0.0%

13.1

%

12.2

%

12.3

%

6.5%

8.9%

7.8% 9.

5%

20.1

%

3.9%

7.5%

9.8%

5.8%

1.4%

8.0%

6.9%

6.9% 8.

5%

5.3%

8.5%

13.2

%

9.7%

7.2%

4.6%

12.2

%

12.5

%

16.3

%

15.2

%

14.0

%

12.9

%

22.1

%

20.1

%

13.0

%

13.8

%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

21%

24%

AL AR SC MS VA LA WV TN NC KY GA FL PA MD NY DE NJ ME NH VT MA RI CT AK HI

PP Auto Total Commercial Auto Total

Sources: NAIC Report on Profitability by Line by State in 2008, pp. 103-104, 109-110; Insurance Information Institute.

Southeast Mid-Atlantic New England

9

Auto Insurance Return on Net Worth, 2008, Varies by Line, State and Region

8.6%

7.9%

0.8% 1.2%

3.7%

9.5% 10

.1%

5.0%

5.1%

12.8

% 15.9

%

13.2

%

2.9%

8.0%

15.6

%

9.8%

-8.9

%

15.4

%

12.1

%

7.0% 7.

9% 9.7% 11

.2%

6.8% 8.

3%

1.8%

4.8%

13.9

%

3.6%

7.0%7.6%

2.8%

5.9%

3.9%

2.4%

5.2%

9.9%

5.1%

9.3%

3.1%4.

6%8.

0%

12.2

%

9.1%

0.9%

-4.1

%

10.8

%

6.7%

-12%

-9%

-6%

-3%

0%

3%

6%

9%

12%

15%

18%

21%

NM AZ TX OK ID CO WY UT MT CA OR WA NV OH WI IN IL MI SD ND IA MN KS NE MO

PP Auto Total Commercial Auto Total

Sources: NAIC Report on Profitability by Line by State in 2008, pp. 103-104, 109-110; Insurance Information Institute.

Southwest Mountain Far West Great PlainsGreat Lakes

10

Premium Growth Trendsin Auto Insurance

They’re Not In SyncWith the Economy

11

Monthly Change* in Auto Insurance Prices, 2005-2010

(Percent Changefrom same month,prior year)

* Percentage change from same month in prior year, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute

3.4%

3.3%

3.0%

2.9%

2.4%

2.2%

2.0%

1.9%

1.3%

0.6% 0.

9%0.

5%0.

2% 0.4%

0.4% 0.5%

0.3%

0.2%

0.2%

1.0%

1.6%

1.1%

0.8%

0.7% 0.8%

0.6%

0.4%

-0.2

%0.

3% 0.6%

0.6%

0.4%

0.1% 0.2% 0.

5%0.

9% 1.1% 1.

4% 1.7%

2.6%

2.6% 2.7% 3.

0% 3.1% 3.

4%3.

8% 4.0%

4.0% 4.

3% 4.4% 4.

6%4.

6% 4.7%

4.6%

4.6%

4.6%

4.6%

4.6% 4.7%

4.7% 4.

9%5.

3%5.

3%5.

3%5.

1% 5.3%

5.1%

0.9%

-1%

0%

1%

2%

3%

4%

5%

6%

Jan

05F

eb 0

5M

ar 0

5A

pr 0

5M

ay 0

5Ju

n 05

Jul 0

5A

ug 0

5S

ep 0

5O

ct 0

5N

ov 0

5D

ec 0

5Ja

n 06

Feb

06

Mar

06

Apr

06

May

06

Jun

06Ju

l 06

Aug

06

Sep

06

Oct

06

Nov

06

Dec

06

Jan

07F

eb 0

7M

ar 0

7A

pr 0

7M

ay 0

7Ju

n 07

Jul 0

7A

ug 0

7S

ep 0

7O

ct 0

7N

ov 0

7D

ec 0

7Ja

n 08

Feb

08

Mar

08

Apr

08

May

08

Jun

08

Jul 0

8A

ug 0

8S

ep 0

8O

ct 0

8N

ov 0

8D

ec 0

8Ja

n 09

Feb

09

Mar

09

Apr

09

May

09

Jun

09Ju

l 09

Aug

09

Sep

09

Oct

09

Nov

09

Dec

09

Jan

10F

eb 1

0M

ar 1

0A

pr 1

0M

ay 1

0Ju

n 10

Jul 1

0A

ug 1

0

Auto Insurance Price Increases Have Averaged About 5% in 2010 over 2009, After

Averaging About 4.5% in 2009 over 2008

A Really Soft Market for Auto Insurance Lasted From Oct 2005 Through Dec

2007 (When the Great Recession Began!)

12

Average Expenditures on Auto Insurance

$651$668

$691$705

$726

$786

$830$842

$831$816

$795$816

$853

$895

$690$685$703

$600

$650

$700

$750

$800

$850

$900

$950

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08* 09* 10*

Countrywide Auto Insurance Expenditures Increased2.6% in 2008 and 4.5% Pace in 2009 (est.) and 5% in 2010 (est.)

* Insurance Information Institute Estimates/ForecastsSources: NAIC, Insurance Information Institute estimates 2008-2010 based on CPI data for Auto Insurance.

13

Private Passenger Auto InsuranceNet Written Premium, 2000–2009

$110

$120

$130

$140

$150

$160

$170

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Sources: A.M. Best; Insurance Information Institute.

$ Billion

14

Commercial Auto InsuranceNet Written Premium, 2000–2009

$25.43

$23.72

$21.80

$26.73

$21.77

$25.52

$26.68$26.62

$24.57

$19.53

$18

$20

$22

$24

$26

$28

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Sources: A.M. Best; Insurance Information Institute.

$ Billion

15

Exposure Driversin Auto Insurance

16

Registered Passenger Carsand Other 2-axle, 4-tire Vehicles

181.

97

181.

33

183.

60

187.

32

190.

78

194.

13 198.

86

199.

97

203.

17 207.

79 212.

70

221.

82

220.

93

222.

86 228.

28

231.

91

234.

52

237.

40

238.

31

175

200

225

250

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

It is likely that the number of vehicles dropped during and following the “Great Recession.” Recovery depends on employment and lending trends.

Sources: http://www.bts.gov/publications/national_transportation_statistics/html/table_01_11.html Insurance Information Institute

Millions

Recession years in gold

17

16.9

16.5

16.1

13.1

10.3

11.5

12.7

16.9

16.617

.117.5

17.8

17.4

9

10

11

12

13

14

15

16

17

18

19

99 00 01 02 03 04 05 06 07 08 09 10F 11F

(Millions of Units)

Auto/Light Truck Sales, 1999-2011F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (9/10); Insurance Information Institute.

Car/Light Truck Sales Will Recover from the 2009 Low Point, but High Unemployment, Tight Credit Are Still Restraining Sales;

Gas Prices Could Once Again Become a Factor Too

New auto/light truck sales fell to the lowest level since the late 1960s. Forecast for 2010-11 is still far below 1999-2007 yearly

average of 17 million units

Sharply lower auto sales will have a smaller effect on auto insurance

exposure level than problems in the housing market will on home insurers

“Cash for Clunkers” generated about $300M in net new personal auto premiums

18

Miles Driven*, 1990–2010**

*Moving 12-month total **Most recent month is July 2010. Note: Recessions indicated by gray shaded columns.Sources: Federal Highway Administration (http://www.fhwa.dot.gov/ohim/tvtw/tvtpage.cfm ); National Bureau of Economic Research (recession dates); Insurance Information Institute.

Billions

2,100

2,200

2,300

2,400

2,500

2,600

2,700

2,800

2,900

3,000

3,100

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10

Sharp rise in gas prices, then pullback

Two of the past three recessions temporarily slowed the rise in miles driven.

Will the trend toward hybrid and non-gasoline-powered vehicles affect

miles driven? What about the aging and

retirement of the baby boomers?

Growth per Decade1999 vs. 1989: 27.2%2009 vs. 1999: 9.4%

Do Changes in Miles Driven AffectAuto Collision Claim Frequency? No.

7.00

6.81

6.59

6.80 6.786.91

6.65

6.32

6.025.92

5.71

5.85

5.705.62

5.55

5.0

5.5

6.0

6.5

7.0

96 97 98 99 00 01 02 03 04 05 06 07 08 09 10*

Pa

id C

laim

Fre

q

2400

2500

2600

2700

2800

2900

3000

3100

Bil

lio

ns

of

Mil

es D

rive

n

Collision Claim FrequencyBillions of Vehicle Miles

Sources: Federal Highway Administration (http://www.fhwa.dot.gov/ohim/tvtw/09dectvt/page2.cfm; ISO Fast Track Monitoring System, Private Passenger Automobile Fast Track Data: 2nd Qtr. 2010, published Sep. 30, 2010 and earlier reports. *2010 FHWA and ISO figures are for 12 months ending 6/30/2010.

Paid Claim Frequency = (No. of paid claims)/(Earned Car Years) x 100

Source: ISO, US DOT.

Oct. 17, 1973: Arab oil

embargo begins

Frequency Effects of the Embargo:Collision: -7.7%

PD: -9.5%BI: -13.3%

March 17, 1974: Arab oil states announce end

to embargo

Driving StatsGas prices rose

35-40%Miles driven fell

6.7% in 1974

Collision frequency began

to rebound almost immediately after

the embargo ended and reached

pre-embargo levels within 9

months

Auto Insurance: Claim Frequency Impacts of Energy Crisis/Recession of 1973/74

Liability claim frequency

remained below pre-embargo levels for 2

years

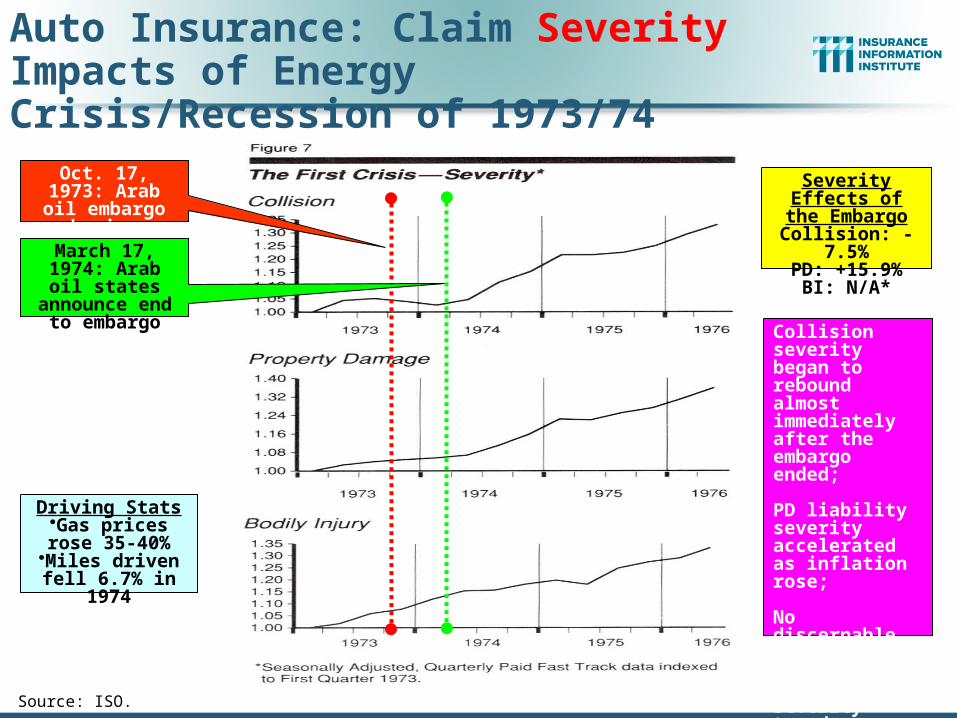

Source: ISO.

Severity Effects of the EmbargoCollision: -7.5%

PD: +15.9%BI: N/A*

Driving StatsGas prices rose

35-40%Miles driven fell

6.7% in 1974

Oct. 17, 1973: Arab oil

embargo begins

March 17, 1974: Arab oil states

announce end to embargo

Collision severity began to rebound almost immediately after the embargo ended;

PD liability severity accelerated as inflation rose;

No discernable trend change in BI liability severity trend.

Auto Insurance: Claim Severity Impacts of Energy Crisis/Recession of 1973/74

Commercial Auto Will Also

See Slow Growth

23

Real GDP Growth,Yearly, 1970-2014F

Estimates/Forecasts from Blue Chip Economic Indicators, 10/2010 issue.Sources: (GDP) U.S. Department of Commerce at http://www.bea.gov/national/xls/gdpchg.xls.

-3%

0%

3%

6%

9%

Real GDP Growth (%)

The “consensus” forecast is for several years of real yearly GDP growth around 3%--weaker than

following most recent recessions

66%

68%

70%

72%

74%

76%

78%

80%

82%

Ma

r 0

1

Ju

n 0

1

Se

p 0

1

De

c 0

1

Ma

r 0

2

Ju

n 0

2

Se

p 0

2

De

c 0

2

Ma

r 0

3

Ju

n 0

3

Se

p 0

3

De

c 0

3

Ma

r 0

4

Ju

n 0

4

Se

p 0

4

De

c 0

4

Ma

r 0

5

Ju

n 0

5

Se

p 0

5

De

c 0

5

Ma

r 0

6

Ju

n 0

6

Se

p 0

6

De

c 0

6

Ma

r 0

7

Ju

n 0

7

Se

p 0

7

De

c 0

7

Ma

r 0

8

Ju

n 0

8

Se

p 0

8

De

c 0

8

Ma

r 0

9

Ju

n 0

9

Se

p 0

9

De

c 0

9

Ma

r 1

0

Ju

n 1

0

Recovery in Capacity Utilization is a Positive Sign for Commercial Exposures

Source: Federal Reserve Board statistical releases at http://www.federalreserve.gov/releases/g17/Current/default.htm. 24

Percent of Manufacturing Capacity

Hurricane Katrina

March 2001-November 2001

recession

“Full Capacity”

The closer the economy is to operating at “full

capacity,” the greater the inflationary pressure

The US operated at 74.7% of industrial

capacity in August 2010,

above the June 2009 low of

68.3%

Recession began December 2007

27

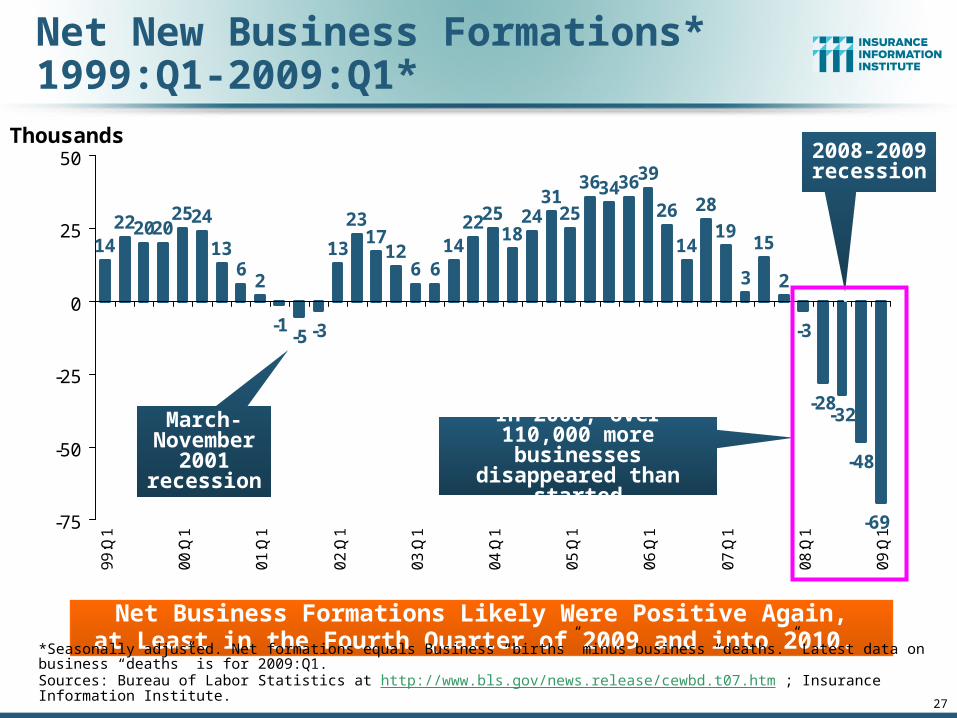

Net New Business Formations*1999:Q1-2009:Q1*

14222020

2524

136

2

-1-5 -3

13

2317

126 6

142225

1824

3125

36343639

26

14

28

19

3

15

2

-3

-28-32

-48

-69-75

-50

-25

0

25

50

99

:Q1

00

:Q1

01

:Q1

02

:Q1

03

:Q1

04

:Q1

05

:Q1

06

:Q1

07

:Q1

08

:Q1

09

:Q1

Net Business Formations Likely Were Positive Again,at Least in the Fourth Quarter of 2009 and into 2010.

*Seasonally adjusted. Net formations equals Business “births” minus business “deaths.” Latest data on business “deaths” is for 2009:Q1.Sources: Bureau of Labor Statistics at http://www.bls.gov/news.release/cewbd.t07.htm ; Insurance Information Institute.

Thousands

March-November

2001 recession

2008-2009 recession

In 2008, over 110,000 more businesses

disappeared than started

28

Unemployment and UnderemploymentRates: Is the Worst Over?

2

4

6

8

10

12

14

16

18

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Traditional Unemployment Rate U-3

Unemployment + Underemployment Rate U-6

September 2010 unemployment rate (U-3) was

9.6%. Peak rate in the last 30

years: 10.8% in Nov - Dec 1982

Source: U.S. Bureau of Labor Statistics; Insurance Information Institute.

U-6 hit 17.5% in Oct 2009 but is now

17.1%

January 2000 through September 2010, Seasonally Adjusted (%)

Recession ended in

November 2001

Unemployment kept rising

slightly for 19 months more

Recession began in

December 2007

Recession ended in

June 2009

Gap between U-3 and U-6 is

normally 4 percentage

points but is now 7.5 points

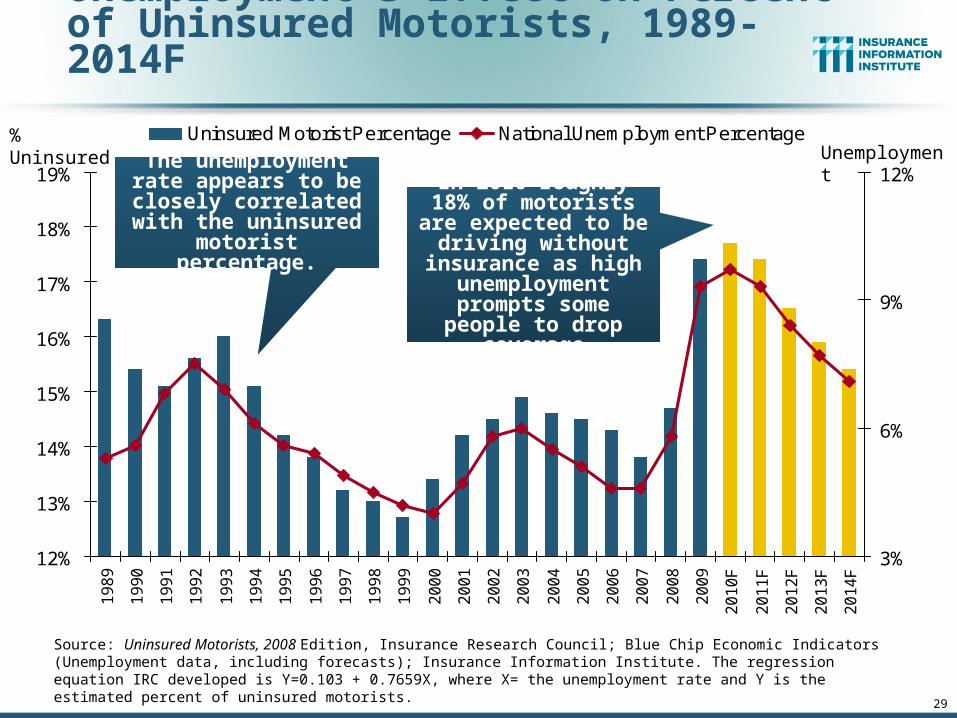

Unemployment’s Effect on Percent of Uninsured Motorists, 1989-2014F

12%

13%

14%

15%

16%

17%

18%

19%

19

89

19

90

19

91

19

92

19

93

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

F

20

11

F

20

12

F

20

13

F

20

14

F

3%

6%

9%

12%

Uninsured Motorist Percentage National Unemployment Percentage

Source: Uninsured Motorists, 2008 Edition, Insurance Research Council; Blue Chip Economic Indicators (Unemployment data, including forecasts); Insurance Information Institute. The regression equation IRC developed is Y=0.103 + 0.7659X, where X= the unemployment rate and Y is the estimated percent of uninsured motorists.

Unemployment% Uninsured

The unemployment rate appears to be closely

correlated with the uninsured motorist

percentage.

In 2010 roughly 18% of motorists are expected

to be driving without insurance as high

unemployment prompts some people

to drop coverage

29

30

Underwriting Trends in Auto Insurance

31

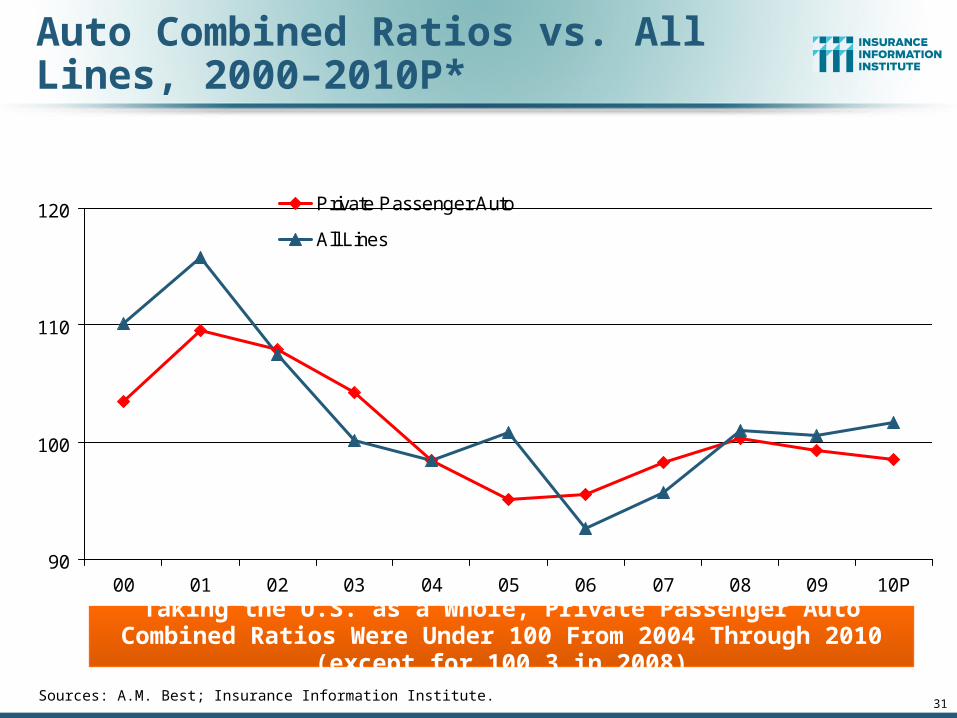

Auto Combined Ratios vs. All Lines, 2000–2010P*

90

100

110

120

00 01 02 03 04 05 06 07 08 09 10P

Month Recession Started

Private Passenger Auto

All Lines

Sources: A.M. Best; Insurance Information Institute.

Taking the U.S. as a Whole, Private Passenger Auto Combined Ratios Were Under 100 From 2004 Through 2010 (except for 100.3 in 2008)

32

Reduction in Combined Ratio Necessary to Offset 1% Decline in Investment Yield to Maintain Constant ROE, by Line*

*Based on 2008 Invested Assets and Earned PremiumsSource: A.M. Best; Insurance Information Institute.

Lower Investment Earnings Place a Greater Burden on Underwriting and Pricing Discipline

-1.8%

-1.9%-1.9%

-1.9%

-1.9%

-1.9%

-1.8%

-1.8%

-1.8%

-1.8%

-1.8%

-1.7%Pvt Pass Auto Comml Auto

33

Claim Trends

Rising Severity Held in Checkby Falling Frequency:

Can That Pattern Be Sustained?

34

PPAuto Bodily Injury Liability: Severity Trends Offset the Decline in Frequency

-5.4%

-3.8%-5.0%

-3.1% -3.2%-2.2%

2.9%

4.7%5.9% 6.1%

2.1%1.2%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2005 2006 2007 2008 2009 2010*

Severity Frequency

*For 2010, data are for the 4 quarters ending with 2010:Q2.Source: ISO/PCI Fast Track data; Insurance Information Institute

Annual Change, 2005 through 2010*

Cost Pressures Will Increase if BI Severity Increases Outpace Declines in Frequency

35

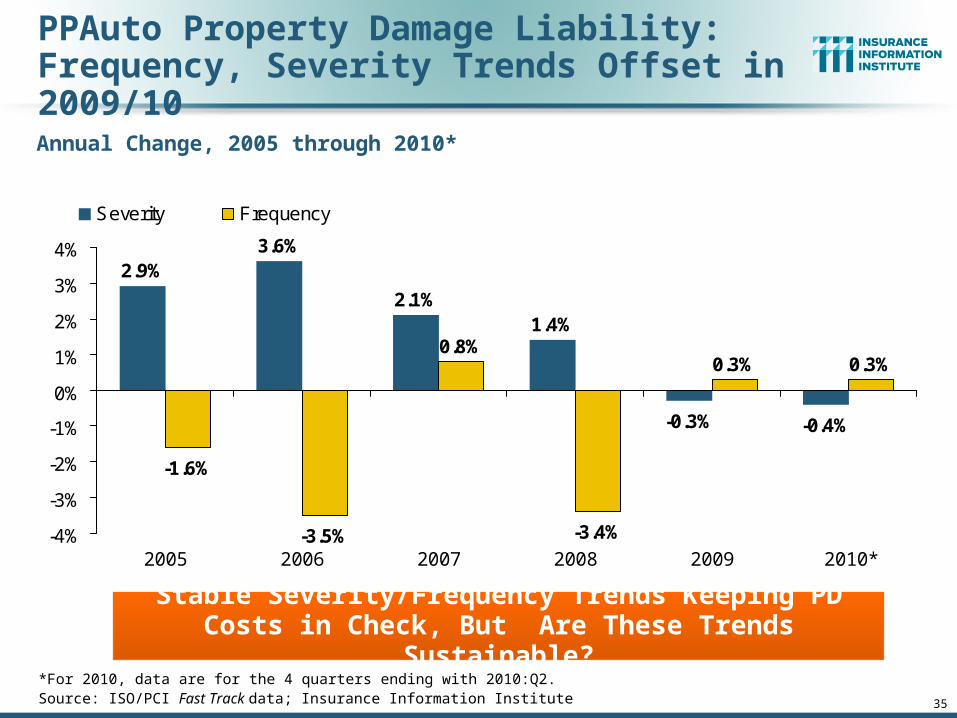

PPAuto Property Damage Liability:Frequency, Severity Trends Offset in 2009/10

-1.6%

-3.5%

0.8%

-3.4%

0.3% 0.3%

2.9%3.6%

2.1%1.4%

-0.3% -0.4%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

2005 2006 2007 2008 2009 2010*

Severity Frequency

Annual Change, 2005 through 2010*

Stable Severity/Frequency Trends Keeping PD Costs in Check, But Are These Trends Sustainable?

*For 2010, data are for the 4 quarters ending with 2010:Q2.Source: ISO/PCI Fast Track data; Insurance Information Institute

36

No-Fault (PIP) Liability: Frequency & Severity Trends Are Adverse*

-4.8%-5.7%

-2.7%

-6.9%

5.9%6.6%

4.7%

2.4%

6.3% 6.4% 6.5%5.2%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

2005 2006 2007 2008 2009 2010*

Severity Frequency

*No-fault states included are: FL, HI, KS, KY, MA, MI, MN, NY, ND and UT; 2010 data are for the 4 quarters ending 2010:Q2.Source: ISO/PCI Fast Track data; Insurance Information Institute

Annual Change, 2005 through 2010*

Multiple States Are Experiencing Severe Fraud and Abuse Problems in their No-Fault Systems, Especially FL, MI, NY and NJ

37

Collision Coverage: Frequency and Severity Trends Have Been Favorable

-1.8%

-3.5%

2.3%

-2.4%-1.6% -1.4%

3.9%3.1%

0.7% 0.4%

-2.3%-1.6%

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

2005 2006 2007 2008 2009 2010*

Severity Frequency

Annual Change, 2005 through 2010*

The Recession, High Fuel Prices Have Helped Push Down Frequency and Temper Severity, But this Trend Will Likely Be

Reversed Based on Evidence from Past Recoveries*For 2010, data are for the 4 quarters ending with 2010:Q2.Source: ISO/PCI Fast Track data; Insurance Information Institute

38

Comprehensive Coverage: Severity Trends Very Favorable in 2009/2010

-3.1%

-9.8%-6.6%

1.6% 1.5%

6.6%

15.5%

-1.4% -1.4%

13.0%

-8.3%-10.3%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2005 2006 2007 2008 2009 2010*

Severity Frequency

Annual Change, 2005 through 2010*

Weather Creates Volatility for Comprehensive Coverage; Recession Has Helped Push Down Frequency and Temper

Severity, But This Factors Will Weaken as Economy Recovers*For 2010, data are for the 4 quarters ending with 2010:Q2.Source: ISO/PCI Fast Track data; Insurance Information Institute

Hurricane Katrina

39

Subdued Inflation Doesn’t Reflect P/C Cost Pressures

Inflation

40

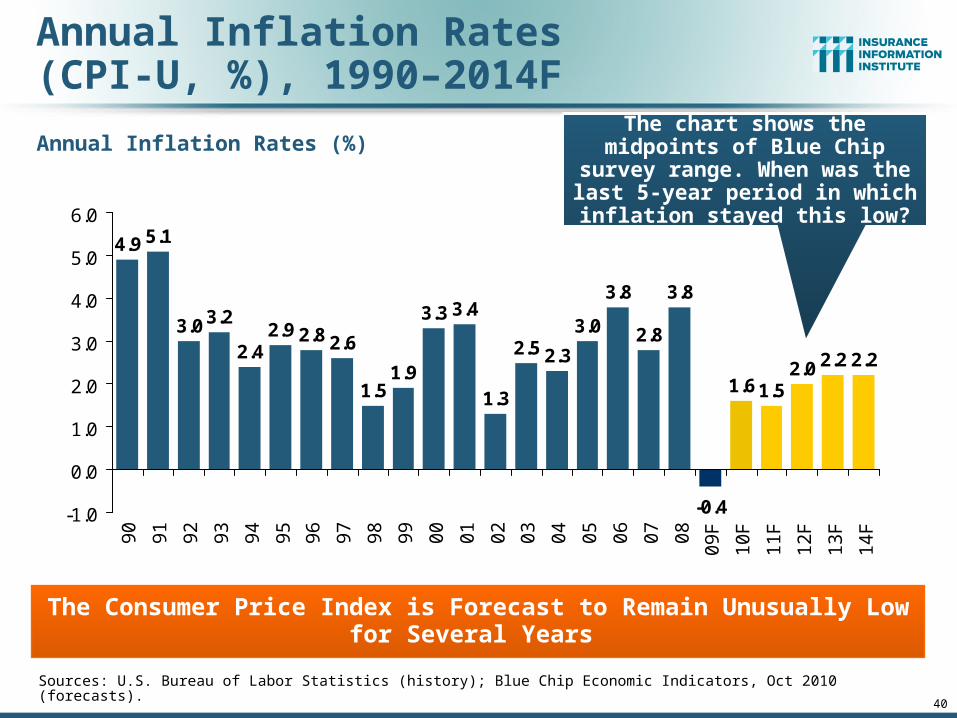

Annual Inflation Rates(CPI-U, %), 1990–2014F

2.8 2.6

1.51.9

3.3 3.4

1.3

2.5 2.3

3.0

3.8

2.8

3.8

-0.4

1.6 1.52.0 2.2 2.2

2.92.4

3.23.0

5.14.9

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

F

10

F

11

F

12

F

13

F

14

F

Sources: U.S. Bureau of Labor Statistics (history); Blue Chip Economic Indicators, Oct 2010 (forecasts).

The Consumer Price Index is Forecast to Remain Unusually Low for Several Years

Annual Inflation Rates (%) The chart shows the midpoints of Blue Chip survey range. When was the last 5-year period in

which inflation stayed this low?

Auto BI Liability Insurers Feel Higher Inflation than the CPI Measures

Source: Bureau of Labor Statistics; Insurance Information Institute.

1.1% 0.9%

6.9%

3.3%2.8%

4.2%

3.0%2.5%

0%

2%

4%

6%

8%

Overall CPI "Core" CPI HospitalServices

Physicians'Services

DentalServices

PrescriptionDrugs

Medical CareCommodities

Other MedicalProfessional

Services

(Percent increase Aug 09 to Aug 10)

Healthcare Costs Are a Major Auto BI Liability Insurance Cost Driver. They Are Likely to Increase Faster than the CPI for the Next Few Years, at Least

41

Excludes Food and Energy

Inpatient Services Rose 7.7%;

Outpatient Services Rose 5.0%

Auto Physical Damage Insurers Feel Higher Inflation than the CPI Measures

Sources: U.S. Dept of Labor, Bureau of Labor Statistics; Insurance Information Institute

1.1%0.9%

4.3%

2.7%2.4%

0%

1%

2%

3%

4%

5%

Overall CPI "Core" CPI Legal Services Motor VehicleBody Work

Motor VehicleRepair

(Percent increase Aug 09 to Aug 10)

Legal/Tort Costs and Auto Repair Costs Are Major Auto Physical Damage Insurance Cost Drivers That Are Expected to Increase Above the Inflation Rate Indefinitely

42

All Segments of French Motor Insurance CostsHave Grown Faster than the CPI for Over 20 Years

Source : Fédération Française des Sociétés d’Assurance

Average cost of motor insurance

100

120

140

160

180

200

220

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

100

= 1

987

Liability for materials

Theft & FireGlass breakage

Accidental damagesCPI

44

Top Risks for Auto Insurersif Inflation Is Reignited

Source: Insurance Information Institute.

Rising Claim SeveritiesCost of claims settlement rises across the board (property and

liability)

Rate InadequacyRates inadequate due to low trend assumptions arising from use of

historical data

Reserve InadequacyReserves may develop adversely and become inadequate

(deficient)

Burn Through on RetentionsRetentions, deductibles burned through more quickly

Reinsurance Penetration/ExhaustionHigher costs risks burn through their retentions more quickly,

tapping into reinsurance more quickly and potentially exhausting their reinsurance more quickly

45

We Can Have InflationDespite High Unemployment

We can “import” inflation.

For example, China is raising interest rates to tame a growing inflation rate. If the prices of things we import rise, importers will try to pass these increases along to buyers.

And if the dollar depreciates vs. currencies of nations from which we import, the dollar price of imports will rise.

We had high inflation during the 1980 and 1981-82 recessions.

The Aging Population

46

47

6.468

10.110

14.575

0

2

4

6

8

10

12

14

16

Under 18 18-64 65+

Increase in Population by Age Category, 2010 to 2020

(Millions)

Source: US Census Bureau

Over the next decade, the demand for personal lines

insurance will be driven by an increasingly older population

Claim Trends in Personal Lines Will Shift With Demographics; Insurers Must Adapt

Labor Force Participation Rate, Ages 55-64, Quarterly, 1998-2010:Q3

61.0% 61.5%

61.5%

61.8%62.9%

62.6%

62.3% 63.0%

62.8%

61.9%

61.8% 62.7%

62.6%

62.9%

62.9%63.3%

63.5%

63.7%

63.6%

64.0%

63.8%

63.5%

63.8%

64.1% 64.8%

64.1%

64.0%65.3%

65.3%

64.5%

64.5%

64.4% 65.0%65.4%

64.9%

61.8%

59.2%

59.2%

59.5%

59.8%

58.8%

59.2%

59.3%

59.4%

59.7%

58.9%

59.0%59.4% 60.1%

60.3%

60.2%

56%

58%

60%

62%

64%

66%

68%

1998.1

1998.2

1998.3

1998.4

1999.1

1999.2

1999.3

1999.4

2000.1

2000.2

2000.3

2000.4

2001.1

2001.2

2001.3

2001.4

2002.1

2002.2

2002.3

2002.4

2003.1

2003.2

2003.3

2003.4

2004.1

2004.2

2004.3

2004.4

2005.1

2005.2

2005.3

2005.4

2006.1

2006.2

2006.3

2006.4

2007.1

2007.2

2007.3

2007.4

2008.1

2008.2

2008.3

2008.4

2009.1

2009.2

2009.3

2009.4

2010.1

2010.2

2010.3

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

The brown bars indicate recessions.

Labor Force participation rate

This percent is forecast to grow to 68.1% by 2018

The labor force participation rate for workers 55-64 grew from about 59% in 2000to 64% by 2006 and then flattened, but might be inching up again.

Labor Force Participation Rate, Ages 55-64, Quarterly, 1998-2018P

61.0% 61.5%

61.5%

61.8%62.9%

62.6%

62.3% 63.0%

62.8%

61.9%

61.8% 62.7%

62.6%

62.9%

62.9%

63.3%

63.5%

63.7%

63.6%

64.0%

63.8%

63.5%

63.8%

64.1% 64.8%

64.1%

64.0%65.3%

65.3%

64.5%

64.5%

64.4% 65.0%65.4%

64.9%

65.0%

65.1%

65.2%

65.3%

65.4%

65.5%

65.6%

65.7%

65.8%

65.9%

66.0%

66.1%

66.2%

66.3%

66.4%

66.5%

66.6%

66.7%

66.8%

66.9%

67.0%

67.1%

67.2%

67.3%

67.4%

67.5%

67.6%

67.7%

67.8%

67.9%

61.8%

59.2%

59.2%

59.5%

59.8%

58.8%

59.2%

59.3%

59.4%

59.7%

58.9%

59.0%59.4% 60.1%

60.3%

60.2%

56%

58%

60%

62%

64%

66%

68%

1998

.1

1999

.1

2000

.1

2001

.1

2002

.1

2003

.1

2004

.1

2005

.1

2006

.1

2007

.1

2008

.1

2009

.1

2010

.1

2011

.1

2012

.1

2013

.1

2014

.1

2015

.1

2016

.1

2017

.1

2018

.1

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

Labor Force participation rate

This is what happens if the labor force

participation rate for this group grows by 0.1% per

quarter

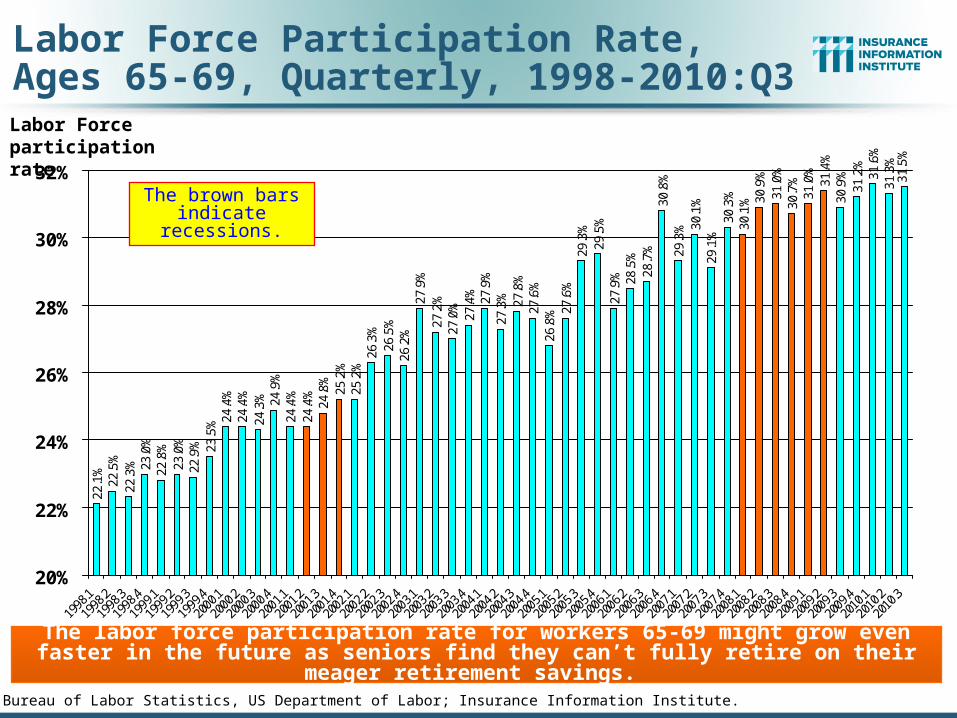

Labor Force Participation Rate, Ages 65-69, Quarterly, 1998-2010:Q3

25.2%

25.2%26.3%

26.5%

26.2%

27.9%

27.2%

27.4% 27.9%

27.3% 27.8%

27.6%

26.8% 27.6%

29.3%

29.5%

27.9% 28.5%

28.7%

30.8%

29.3% 30.1%

29.1%30.3%

30.1% 30.9%

31.0%

30.7%

31.0%

31.4%

30.9%

31.2%

31.6%

31.3%

31.5%

27.0%

22.9%

23.0%

22.8%

23.0%

22.3%

22.5%

22.1%

23.5% 24.4%

24.4%

24.3% 24.9%

24.4%

24.4%24.8%

20%

22%

24%

26%

28%

30%

32%

1998.1

1998.2

1998.3

1998.4

1999.1

1999.2

1999.3

1999.4

2000.1

2000.2

2000.3

2000.4

2001.1

2001.2

2001.3

2001.4

2002.1

2002.2

2002.3

2002.4

2003.1

2003.2

2003.3

2003.4

2004.1

2004.2

2004.3

2004.4

2005.1

2005.2

2005.3

2005.4

2006.1

2006.2

2006.3

2006.4

2007.1

2007.2

2007.3

2007.4

2008.1

2008.2

2008.3

2008.4

2009.1

2009.2

2009.3

2009.4

2010.1

2010.2

2010.3

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

The brown bars indicate recessions.

Labor Force participation rate

The labor force participation rate for workers 65-69 might grow even faster in the future as seniors find they can’t fully retire on their meager retirement savings.

Labor Force Participation Rate,Ages 70-74, Quarterly, 1998-2010:Q3

14.2%

13.8%14.2%

14.0%

14.0%14.4%

14.4% 14.9%

14.9% 15.4%

15.6%

15.3%

16.4% 17.0%

15.8%16.2% 16.7%

16.9%

17.2%

17.0%

16.7%

16.8%

18.0%

17.5%

17.3%

16.9%

18.6%

18.2%

17.7%

17.9%18.9%

19.2%

18.0%

18.1%

17.4%

14.6%

13.1%13.6%

12.4%12.9%

12.4%

12.2%

12.5% 13.1%

13.3%

13.5%

13.6%

13.8% 14.4%

13.7% 14.2%

10%

12%

14%

16%

18%

20%

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

Labor Force participation rate

The labor force participation rate for workers 70-74 grew by about 50% since 1998,but growth has stalled since the Great Recession began.

Labor Force Participation Rate,Ages 75 & over, Quarterly, 1998-2010:Q3

5.4%

5.1%5.1% 5.2%

5.0%

5.5%

5.9%

5.8% 5.9% 6.0% 6.1%

6.5%

6.1%

6.6%

6.3%

6.7%

6.4%6.6%

6.0%

6.5%6.5%

7.1%

7.0%

6.9%6.9%

7.2%7.4%7.6%7.6%

7.0%7.2% 7.3%7.3%

6.9%

7.7%

5.8%

5.4%

5.1%

4.8%5.0%

4.6%4.6%

4.5%

5.2%5.4%

5.3%

5.2% 5.3%

5.2%5.2%

5.1%

4%

5%

6%

7%

8%

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

Labor Force participation rate

These people were born before 1935

This percent is forecast to grow to

10.3% by 2018

The labor force participation rate for workers 70-74 grew by about 50% since 2002,but growth has stalled since the Great Recession began.

Younger and Older Drivers Are Over- Represented in Fatal Crashes

Share of Drivers in Age Group

Sources: US DOT, NHTSA, Federal Highway Administration; Insurance Information Institute

0.1%

6.3% 6.7%

17.4%19.2%

15.2%

8.6%6.5%

20.0%

21.37

17.10

19.28

29.89

52.80

24.93

21.86

45.06

0%

5%

10%

15%

20%

25%

Under 16 16 to 20 21 to 24 25 to 34 35 to 44 45 to 54 55 to 64 65 to 74 75+0

10

20

30

40

50

60

Percent of Licensed Total Drivers in Age GroupInvolvement Rate in Fatal Crashes

Immigration and High Birth Rates in Some Demographic Groups, Combined With Baby Boomers Aging Creates Challenges for Insurers and Auto Safety Experts

Involvement Rate per 100,000 Drivers

Motor Vehicle Deaths per 100,000 Persons by Age, 2008

Problem: How to Keep the Elderly Safe in Cars (Not Just When They’re Behind the Wheel)

Sources: Insurance Institute for Highway Safety; Insurance Information Institute

The elderly are almost as likely to be killed in a motor vehicle

accident as a teenager. As the Baby Boomers age, this is a looming public health crisis

55

Fraud & Abuse in Private Passenger Auto Insurance

Skyrocketing No-Fault (PIP) Claim Costs Are a Major Concern in

Several States

56

Increase in No-Fault Claim Severity: 2004-2010*

*2010 figure is for the 4 quarters ending 2010:Q2. Sources: Insurance Information Institute research from ISO/PCI Fast Track data.

$34,364

$16,640

$8,807 $7,711 $6,887$5,212$6,674$5,871

$12,136

$24,385

$0$5,000

$10,000$15,000$20,000$25,000$30,000$35,000$40,000

Michigan New Jersey New York Florida Minnesota

2004 2010

The no-fault systems in MI, NJ, NY, FL, and MN are under stressdue to rising fraud and abuse

which will ultimately lead to higher premiums for drivers

+36.8%

+37.1%

+50.0% +15.5% +32.1%

57

New York State No-Fault Claim Severity, 2001:Q1–2010:Q2

Sources: ISO/PCI Fast Track data; Insurance Information Institute.

$8,3

27

$7,8

88

$7,5

07

$8,2

34

$9,2

35

$8,7

27$8

,577

$7,7

73

$7,3

11

$6,9

58

$6,8

70

$6,1

56

$6,0

52

$5,8

20

$5,9

91

$5,6

15

$6,0

94

$5,9

14 $6,2

50$6

,269 $6

,530

$6,6

06

$7,0

63 $7,3

23

$7,3

78

$7,2

97 $7,6

70

$7,7

40

$8,4

43

$8,1

77 $8,5

07$8

,025

$8,5

62

$8,7

48

$8,6

90

$8,8

62

$8,6

66 $9,0

07

$5,000

$5,500

$6,000

$6,500

$7,000

$7,500

$8,000

$8,500

$9,000

$9,500

1:01

1:03

2:01

2:03

3:01

3:03

4:01

4:03

5:01

5:03

6:01

6:03

7:01

7:03

8:01

8:03

9:01

9:03

10:0

1

1.4%

1.6%

1.8%

2.0%

2.2%

2.4%Avg. Claim Severity

Frequency

About 20% of No-Fault Claim Costs Are Attributable to Fraud and Abuse

No-Fault Claim Severity No-Fault Claim Frequency

Avg. Claim Severity Rose 63% in 5 years

after 1997 Presbyterian

Decision

58

$12

$504

$875

$1,390

$1,561$1,644

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

2005 2006 2007 2008 2009** 2010F

Estimated Per-Claim Cost of No-Fault Fraud in New York State, 2005-2010F*

*No-fault severity reached a post-reform low in 2004 before, hence selection of 2005 as the first year of analysis. Actual no-fault losses in 2005 and beyond are higher than estimates indicate due to baselevel of fraud imbedded in 2004 data.**2009 figure is estimated based on 4 quarters ending 2009:Q3 (latest available).Source: Insurance Information Institute analysis and research.

No-fault fraud costs per claim could rise

to $1,644 in 2010 without reform

The estimated per claim cost of no-fault fraud (a.k.a. Fraud Tax) in NY state was $1,561 in 2009, up 12.3% from 2008 and

78.4% from 2007

www.iii.org

Thank you for your timeand your attention!

Insurance Information Institute Online: