Medigap 2008

38

NIFS NAYLOR INSURANCE & FINANCIAL SERVICES SUPPLEMENTING MEDICARE

Transcript of Medigap 2008

NIFSNAYLOR INSURANCE & FINANCIAL SERVICES

SUPPLEMENTING MEDICARE

TRAINING OBJECTIVES

Major Gaps in Medicare Coverage

What Type of Insurance Policies Are

Out There?

Consumer Protection

Filing Claims

Illegal Sales Practices

Do and Don’ts in Supplementing Medicare

Why do we need to supplement Medicare?

Major Gaps in Medicare Coverage

Benefit Gaps - services covered by Medicare, but some amounts may still be owed by the beneficiary.

Coverage Gaps - services, supplies, and equipment not covered by Medicare.

What Types Of Insurance Policies Are Out There?

Indemnity Policies

Specific Disease and Specified Accident Policies

Medical-Surgical Expense Policies

Employer Group Plans

Medigap Policies

Indemnity Policies A fixed dollar amount for expenses

covered by the policy.

Some pay added benefits such as part an amount per day while a person is confined to a skilled nursing facility, intensive care unit, or burn unit.

Not tailored to cover the specific gaps in Medicare.

May terminate or reduce benefits after age 65.

Coverage fails to keep pace with inflation.

Specific Disease and Specified Accident Policies

Specified disease policies pay a benefit based on diagnosis of a dread disease, such as cancer, heart attack or stroke.Specified accident policies pay a benefit due to an occurrence of a specific accident.

Pays benefits regardless of other coverages.

Pays only in the event the beneficiary contracts the specified disease or is involved in a specific accident.

Medical-Surgical Expense Policy

Policies pay a defined percentage of the allowable medical or surgical expenses.

The reimbursement is generally based on the “usual and customary” charges or a negotiated rate.

Only covers medical or surgical expenses, not hospital or skilled nursing facility.

Employer Group PlansMany employers offer health benefits to retirees in the

form of a retirement plan.Advantages:• May offer coverage beyond the Medicare-approved amounts

and services.

• May offer limited coverage for prescriptions.

• No health underwriting or waiting periods.

Disadvantages:

• Not subject to federal and state Medicare supplement minimum requirements.

• Some group coverage's automatically becomes like Medicare supplements after retirement. These plans do not cover benefits paid by Medicare, “carve out”.

• May reduce benefits by what Medicare would have paid even if Medicare isn’t elected.

Not all Employer Group Plans are Equal

What type of Employer Group plan do you have?– Fully insured

– Self funded

Why would this be important?– Benefit payments are based on

who is “insuring” the plan.

– Insurance companies are regulated by the state, employer self funded plans are NOT!

Medigap Policies

Also called “MedSup” policies or “Medicare Supplement Policies”

Designed to help fill the gaps in Medicare.

Regulated by federal minimum standards.

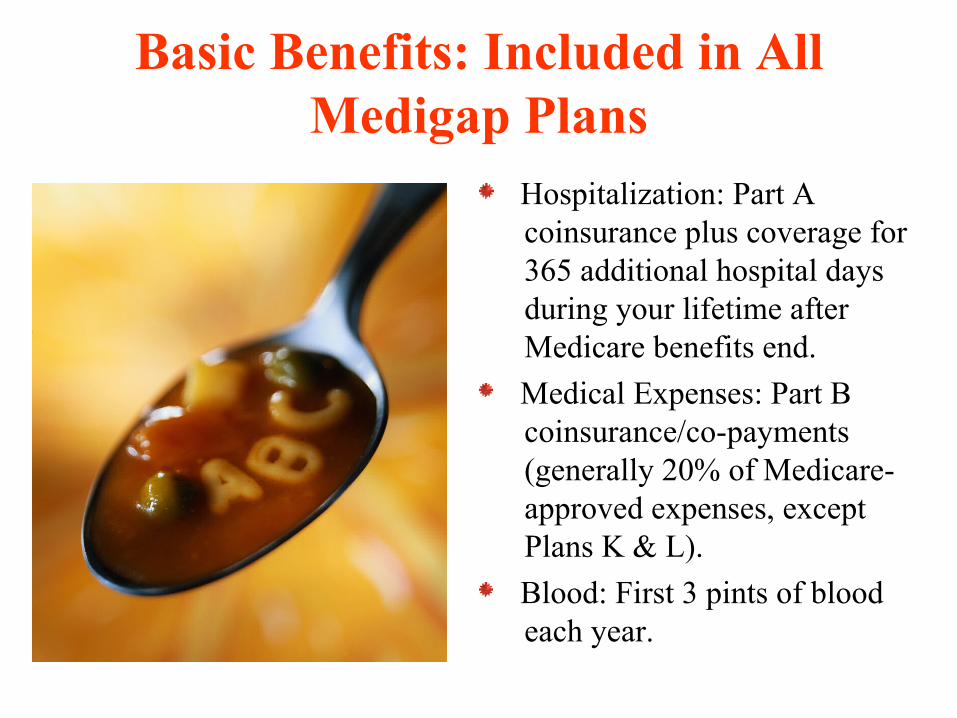

Basic Benefits: Included in All Medigap Plans

Hospitalization: Part A coinsurance plus coverage for 365 additional hospital days during your lifetime after Medicare benefits end.

Medical Expenses: Part B coinsurance/co-payments (generally 20% of Medicare-approved expenses, except Plans K & L).

Blood: First 3 pints of blood each year.

MEDIGAP STANDARD MEDICARE SUPPLEMENT PLANS

ADDITIONAL BENEFITS A B C D E F G H I J K* L**

SNF coinsurance: Days 21 to 100 - $119 per day in 2006

? ? ? ? ? ? ? ? 50% 75%

Part A Hospital Deductible: $952 in 2006 ? ? ? ? ? ? ? ? ? 50% 75%

Part B Annual Deductible: $124 in 2006 ? ? ?

Part B Excess Charges: Coverage for up to 115% percent of Medicare's approved charge (Medigap policy will either pay 80% or 100% of excess charge)

100% 80% 100% 100%

CORE BENEFITS A B C D E F G H I J K* L** Hospital coinsurance: Days 61 to 91 ? ? ? ? ? ? ? ? ? ? ? ?

Hospital coinsurance: Days 91 to 150 ? ? ? ? ? ? ? ? ? ? ? ?

Hospital Payment in full: 365 additional days ? ? ? ? ? ? ? ? ? ? ? ?

Part A and Part B blood deductible: First three pints of blood

? ? ? ? ? ? ? ? ? ? 50% 75%

Part B 20% coinsurance: Physician and other services ? ? ? ? ? ? ? ? ? ? 50% 75%

Foreign Travel Emergency: $250 deductible, 80% of the cost of emergency care during the first two months of the trip, $50,000 lifetime limit

? ? ? ? ? ? ? ?

At-Home Recovery: Maximum benefit of $1,600 annually

? ? ? ?

* Plan K covers 100% of cost sharing for Medicare Part B preventive services and 100% of all cost sharing under Medicare Parts A and B for the balance of the calendar year once an individual has

reached the out-of-pocket limit on annual expenditures of $4,620 in 2009.

** Plan L covers 100% of cost sharing for Medicare Part B preventive services and 100% of all cost sharing under Medicare Parts A and B for the balance of the calendar year once an individual has

reached the out-of-pocket limit on annual expenditures of $2,310 in 2009.

2010 Medigap E,H and I are going away.

2010 MedigapWelcomes

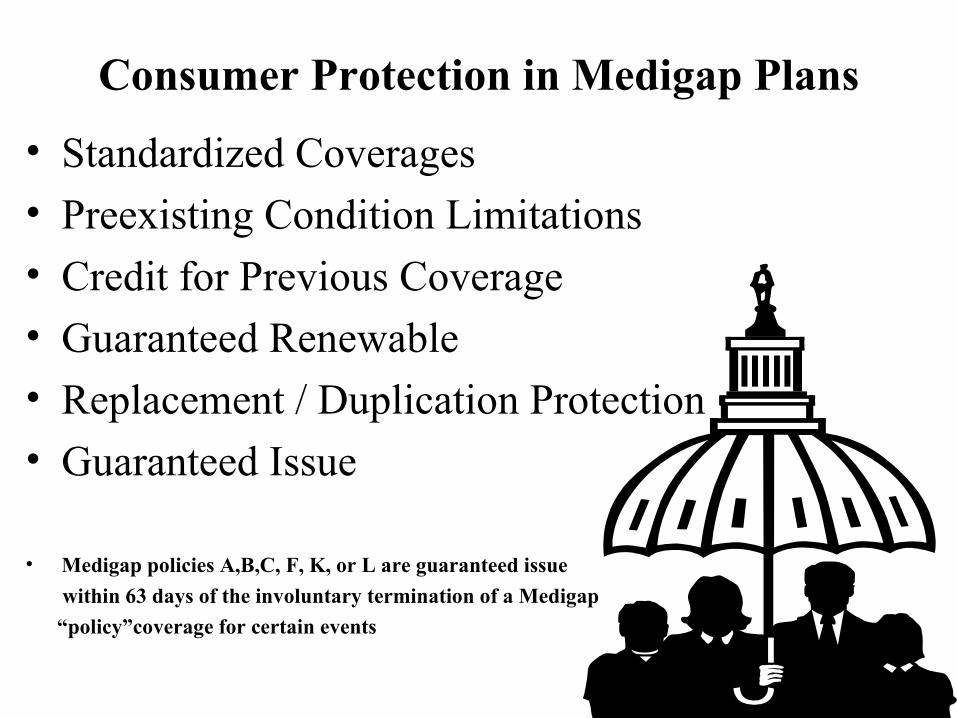

Consumer Protection in Medigap Plans

• Standardized Coverages

• Preexisting Condition Limitations

• Credit for Previous Coverage

• Guaranteed Renewable

• Replacement / Duplication Protection

• Guaranteed Issue

• Medigap policies A,B,C, F, K, or L are guaranteed issue

within 63 days of the involuntary termination of a Medigap

“policy”coverage for certain events

How are Premiums Calculated?

Attained Age. Premiums increase automatically as you get older.

Issue Age. Premium is set when you buy the policy. Premiums will not increase due to age.

No Age Rating. Premium are all the same. Not based on age.

Consumer Protection in Medigap Plans

Rating Requirements

Must pay out 65 cents for every $1 dollar of premium received for individual policies.

Must pay out 75 cents for every $1 dollar of premium received for group policies.

WARNING !!!Open enrollment for a supplement plan hinges on when you take out Medicare Part B.

Filing ClaimsSome insurers and plans have made arrangements for Medicare to file claims directly with the plan or carrier.If not, you can complete box #13 on the claim form which instructs the carrier to directly forward to the Medigap carrier.Keep an accurate record of all health care expenses.

Illegal Sales Practices

Wolf in Sheep’s Clothing

Twisting or Rollover

Pie in the Sky

Duplicate Sales

“Make the Check Out to Me”

Scare Tactics

Clean Sheeting

Unauthorized Insurance

Wolf in Sheep’s Clothing

The producer/agent fails on initial contact with clients to disclose that he or she represents a for-profit insurance company.

The producer/agent may say he or she is from Medicare and wants to help seniors.

Twisting or Rollover

New is BetterThe producer/agent encourages the client to cancel or enhance an existing policy so that additional

commission payments will be made.

Pie in the Sky

The producer/agent misrepresents the policy, “this policy will pay for everything.”

Read your policy! Know what it does cover and what it doesn’t cover.

Duplicate Sales

The producer/agent sells the client additional policies, which in effect duplicates the coverage of the existing policy.

Clients are ultimately responsible to make sure their prior policy is cancelled.

“Make the Check Out To Me”

The producer/agent ask the client to make the check out to him or her.

No policy has been issued and no money is given to the insurance company.

Scare Tactics

The producer/agent uses scary language to make the sale, or suggest the client’s current insurance company is not financially sound or their current policy is insufficient.

“I won’t leave unless you sign the form!”

Clean Sheeting

The producer/agent offers to complete the application, and then fails to fully report the applicant’s health conditions on the application, or tells the client not to put a condition on the application.

When a claim is filed the insurer investigates the statements made on the application. If the application has not been properly completed, the insurer may accuse the client of fraud and the policy may be rescinded.

Unauthorized Insurance

The client should verify if the policy and the insurance company exist.

Before purchasing insurance that seems too good to be true call the Utah Insurance Department.

DO’s in Supplementing Medicare

Do read the policy CAREFULLY!!!– 30 Day Free Look

Period.

Do compare the costs and benefits of plans offered by several insurance companies before buying any insurance policy.

Do’s Continued

Do understand how your employer’s plan will supplement Medicare.Do read the current Guide to Health Insurance for People with Medicare.Do look at eligible providers (Are your doctors and hospital part of the plan?)

Do understand that after 30 days a pre paid premium may not be returned.

Don’ts in Supplementing Medicare

DON’T BELIEVE a producer who says a policy offers coverage that is not listed.

DON’T DROP an existing insurance policy until the new one is issued. However, don’t forget to cancel when new policy is issued.

DON’T PAY CASH for a policy.

DON’T let a producer tell you they represent a government agency.

Naylor Insurance & Financial Services

For any questions or additional information, please call:

ALLEN C NAYLOR

1-888-222-8115Or

801-638-3141

SHOP FOR INSURANCE?

INFORMATION FOR SENIORS.

Questions?