Medigap (Medicare Supplement Insurance) Module 3.

56

Medigap (Medicare Supplement Insurance) Module 3

-

Upload

randall-hodge -

Category

Documents

-

view

217 -

download

0

Transcript of Medigap (Medicare Supplement Insurance) Module 3.

Medigap (Medicare Supplement Insurance)

Module 3

Medigap Basics

Module 3—Lesson 1

Lesson 1: Medigap Basics

Lesson 2: Medigap in Detail

04-16-08 3

Session Topics

OverviewMedigap benefitsMedigap plansMedigap costs

04-16-08 4

Session Topics

OverviewMedigap benefitsMedigap plansMedigap costs

04-16-08 5

What Is Medigap?

Health insurance policiesSold by private insurance companiesCover “gaps” in Original Medicare Follow Federal and state laws that protect

youMust say “Medicare Supplement Insurance”

Overview

04-16-08 6

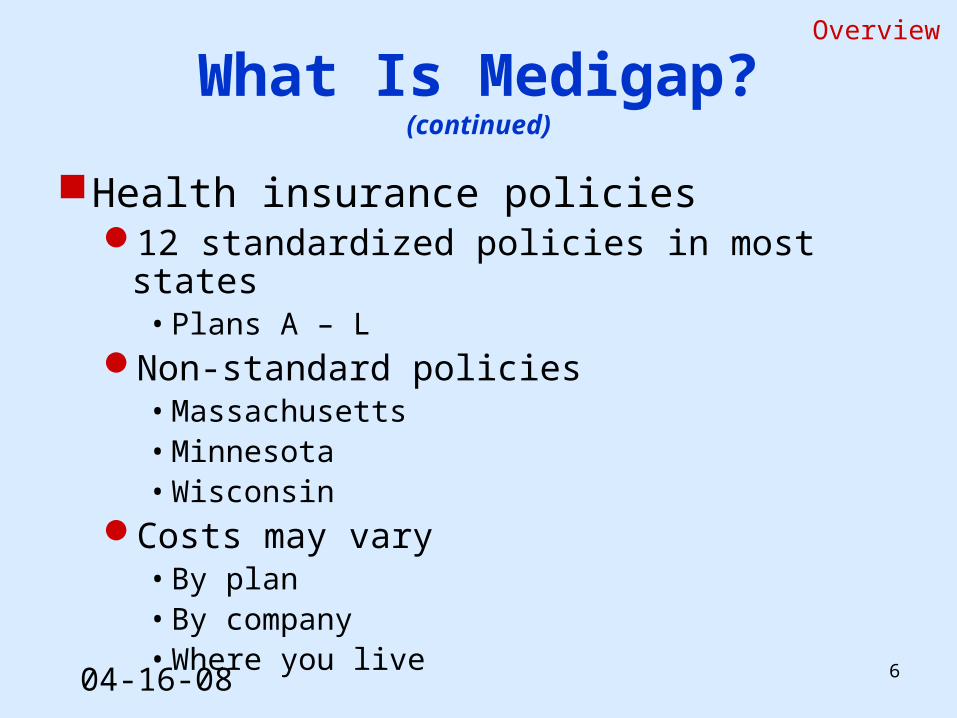

What Is Medigap?(continued)

Health insurance policies12 standardized policies in most states

• Plans A – L Non-standard policies

• Massachusetts• Minnesota• Wisconsin

Costs may vary• By plan• By company• Where you live

Overview

04-16-08 7

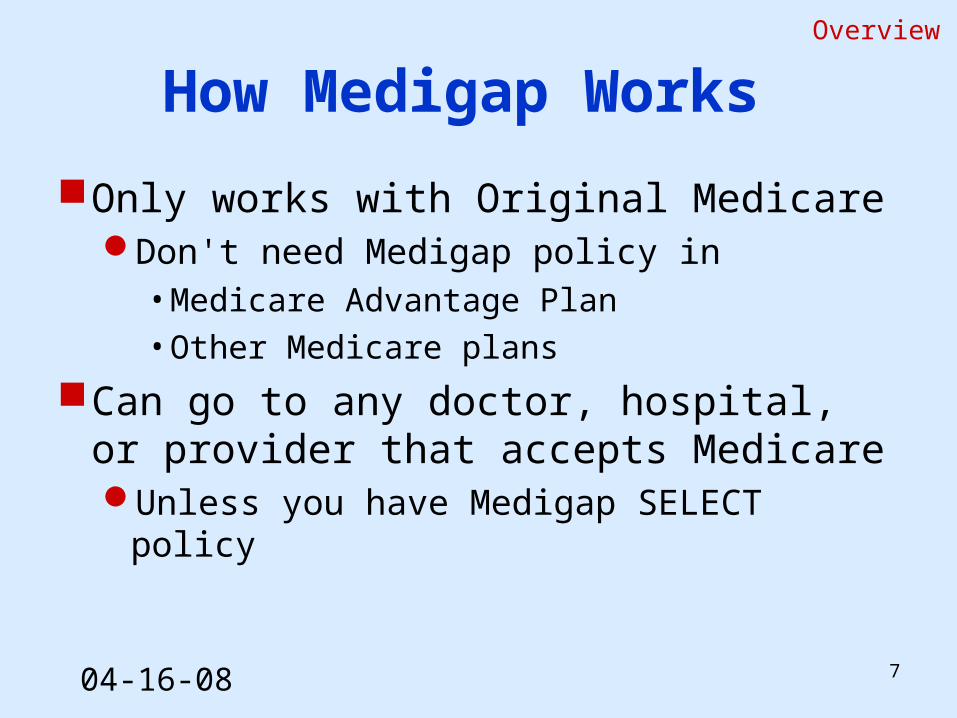

How Medigap Works

Only works with Original MedicareDon't need Medigap policy in

• Medicare Advantage Plan

• Other Medicare plans

Can go to any doctor, hospital, or provider that accepts MedicareUnless you have Medigap SELECT policy

Overview

04-16-08 8

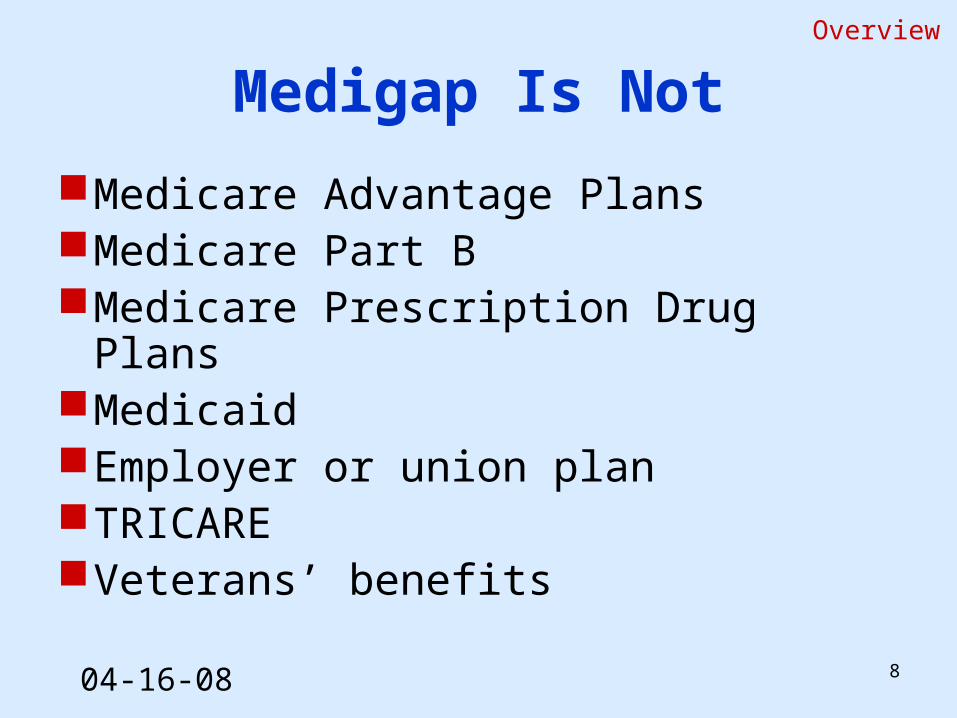

Medigap Is Not

Medicare Advantage PlansMedicare Part BMedicare Prescription Drug PlansMedicaidEmployer or union planTRICAREVeterans’ benefits

Overview

04-16-08 9

Who Can Buy Medigap?

Must have Medicare Parts A and BMay not be able to buy Medigap under 65

People with a disabilityPeople with End-Stage Renal Disease

Guaranteed right to buy a Medigap policyIn your Medigap open enrollment periodCovered under a Medigap protection

Overview

04-16-08 10

Session Topics

Overview

Medigap benefitsMedigap plansMedigap costs

04-16-08 11

Why Buy Medigap?

Original Medicare does not pay all costsMedigap policy may help you

Lower your out-of-pocket costsGet more health insurance coverage

Medigap Benefits

04-16-08 12

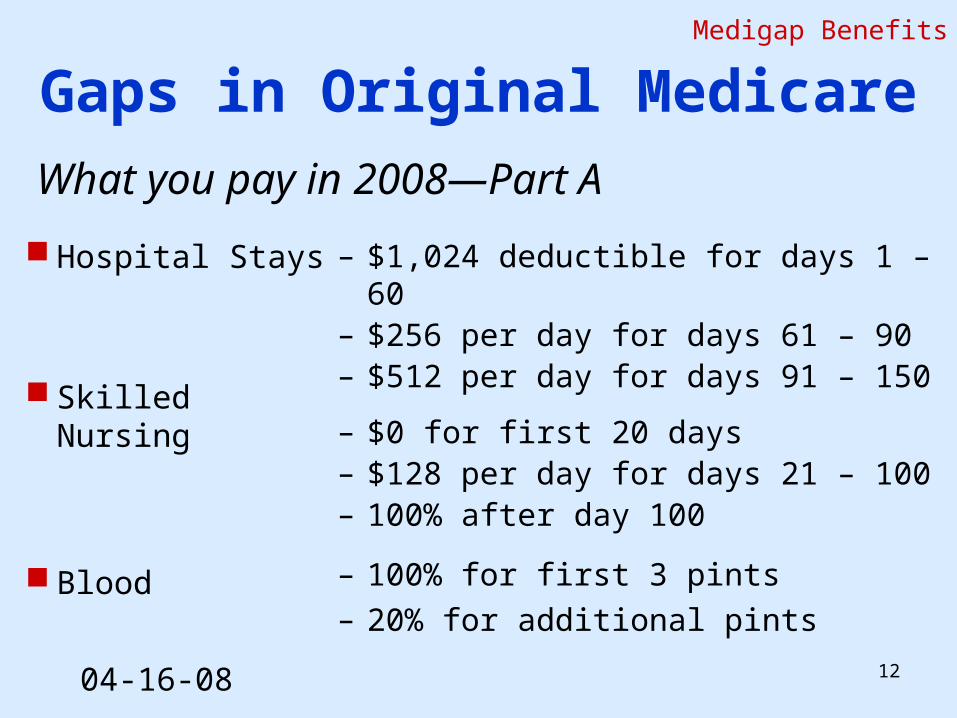

Gaps in Original Medicare

Hospital Stays

Skilled Nursing

Blood

– $1,024 deductible for days 1 – 60 – $256 per day for days 61 – 90 – $512 per day for days 91 – 150

– $0 for first 20 days– $128 per day for days 21 – 100– 100% after day 100

– 100% for first 3 pints– 20% for additional pints

What you pay in 2008—Part A

Medigap Benefits

04-16-08 13

Gaps in Original Medicare

Home Health Care

Hospice Care

– $0 for home health care services

– 20% for durable medical equipment

– Up to $5 copayments for outpatient prescription drugs

– 5% for inpatient respite care – Room and board, in some

cases

What you pay in 2008—Part A

Medigap Benefits

04-16-08 14

Gaps in Original Medicare

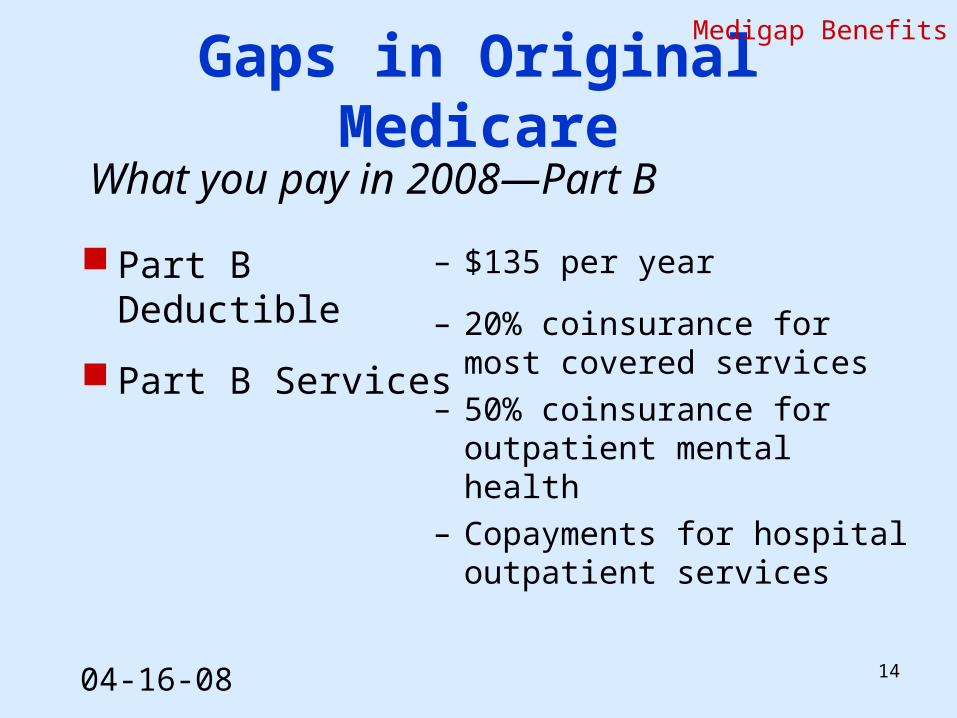

Part B Deductible

Part B Services

– $135 per year

– 20% coinsurance for most covered services

– 50% coinsurance for outpatient mental health

– Copayments for hospital outpatient services

What you pay in 2008—Part B

Medigap Benefits

04-16-08 15

Medigap Coverage

Plans A – JAll cover basic benefits

• Part A coinsurance for inpatient hospital care

• Cost of 365 extra days of inpatient hospital care

• Part B coinsurance after deductible• First 3 pints of blood each year

Some plans cover more

Medigap Benefits

04-16-08 16

Other Medigap Benefits

Most plans have extra benefitsSome Medigap policies cover

Part A deductiblePart B deductibleAt-home recoveryMedicare Part B excess charges

• Subject to the “limiting charge”Other services

Medigap Benefits

04-16-08 17

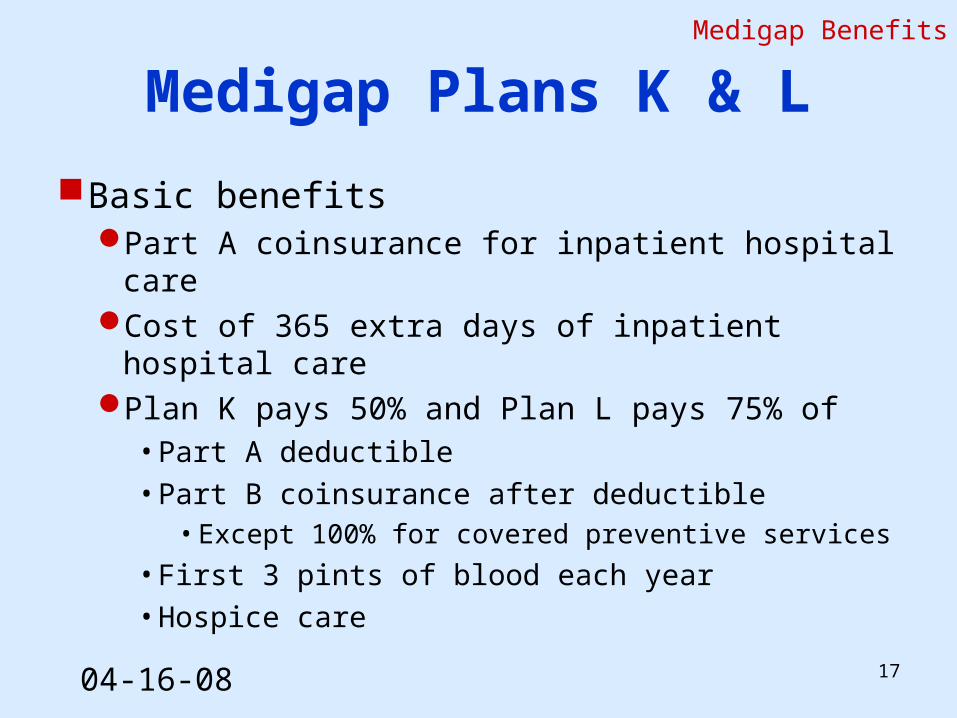

Medigap Plans K & L

Basic benefitsPart A coinsurance for inpatient hospital careCost of 365 extra days of inpatient hospital carePlan K pays 50% and Plan L pays 75% of

• Part A deductible• Part B coinsurance after deductible

• Except 100% for covered preventive services

• First 3 pints of blood each year• Hospice care

Medigap Benefits

04-16-0802-13-08 18

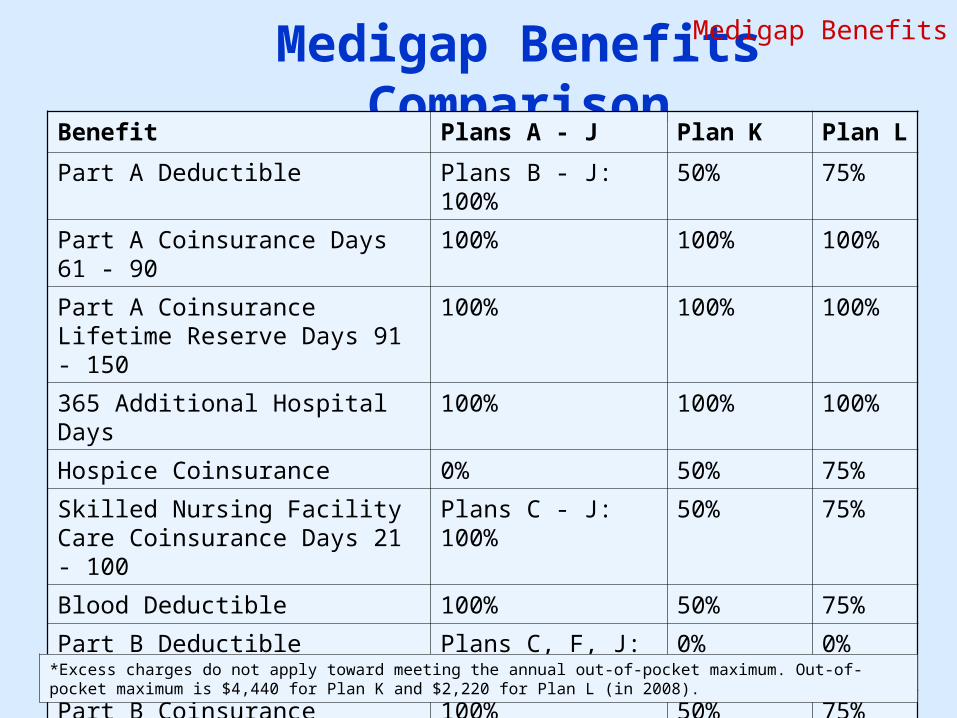

Medigap Benefits ComparisonBenefit Plans A - J Plan K Plan L

Part A Deductible Plans B - J: 100% 50% 75%

Part A Coinsurance Days 61 - 90 100% 100% 100%

Part A Coinsurance Lifetime Reserve Days 91 - 150

100% 100% 100%

365 Additional Hospital Days 100% 100% 100%

Hospice Coinsurance 0% 50% 75%

Skilled Nursing Facility Care Coinsurance Days 21 - 100

Plans C - J: 100% 50% 75%

Blood Deductible 100% 50% 75%

Part B Deductible Plans C, F, J: 100% 0% 0%

Part B Coinsurance 100% 50% 75%

Part B Excess Charges Plans F, I, J: 100%

Plan G: 80%

0%* 0%*

*Excess charges do not apply toward meeting the annual out-of-pocket maximum. Out-of-pocket maximum is $4,440 for Plan K and $2,220 for Plan L (in 2008).

Medigap Benefits

04-16-08 19

Items Not Covered

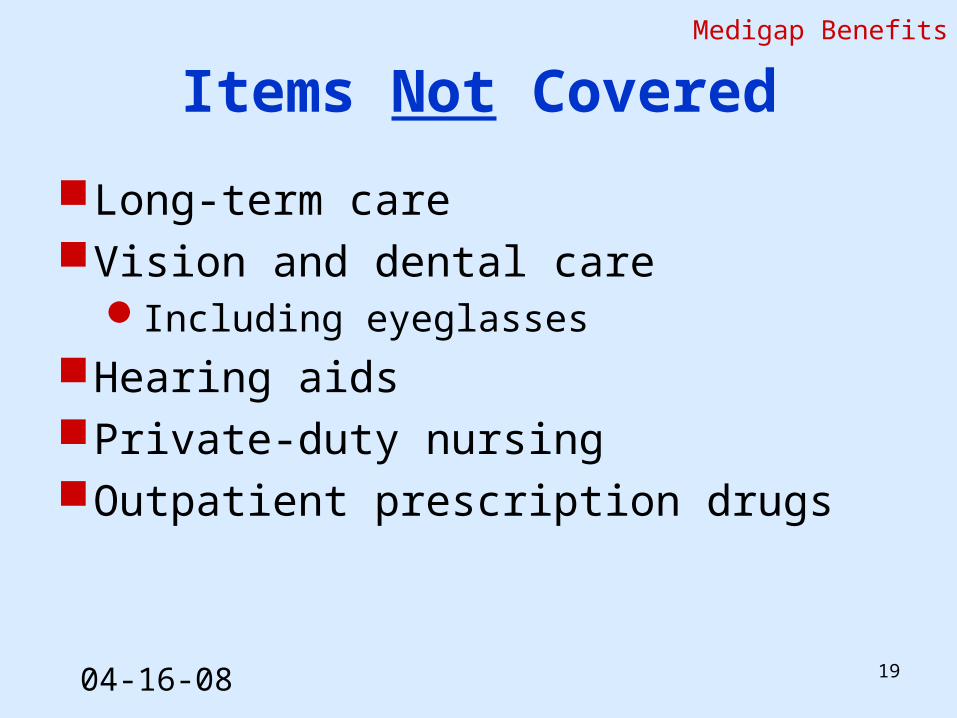

Long-term careVision and dental care

Including eyeglasses

Hearing aidsPrivate-duty nursingOutpatient prescription drugs

Medigap Benefits

04-16-08 20

Session Topics

OverviewMedigap benefits

Medigap plansMedigap costs

04-16-08 21

Special Types of Medigap Plans

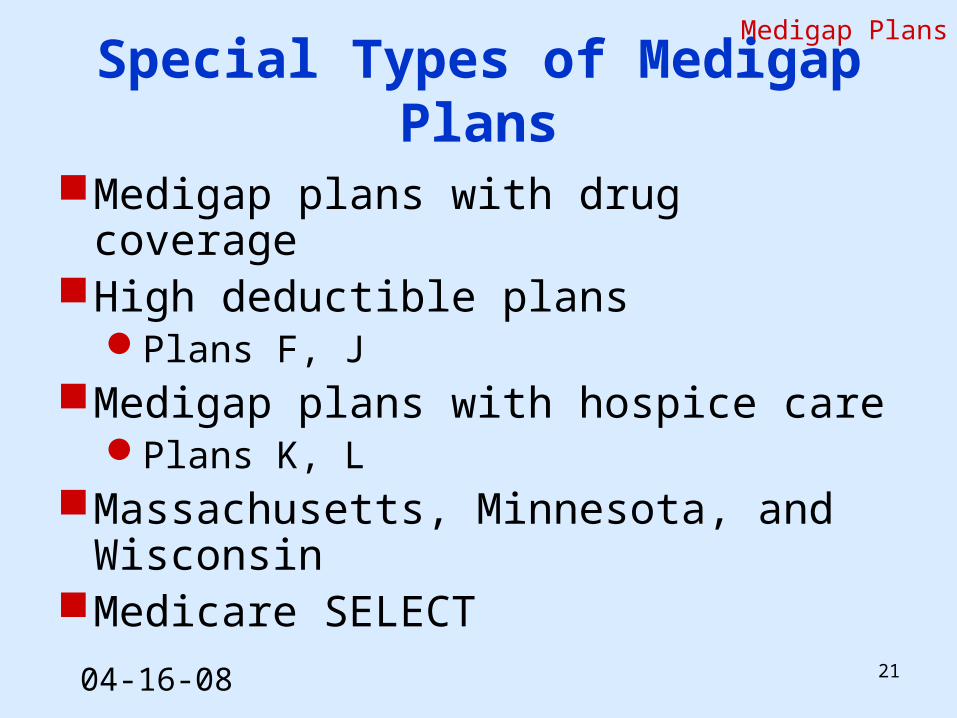

Medigap plans with drug coverageHigh deductible plans

Plans F, JMedigap plans with hospice care

Plans K, LMassachusetts, Minnesota, and WisconsinMedicare SELECT

Medigap Plans

04-16-08 22

Drug Coverage and Medigap

Medigap policies covering prescription drugsMay not be sold after January 1, 2006Same policies may be sold without drug coverage

If your Medigap policy covers drugsShould have received information from company

• Explains how drug coverage affects your policy

Medigap Plans

04-16-08 23

Medigap Plans With Drug Coverage

Standardized plans H, I, JSold before January 1, 2006

Some policiesMassachusettsMinnesotaWisconsin

Some pre-standardized plansOthers

Medigap Plans

04-16-08 24

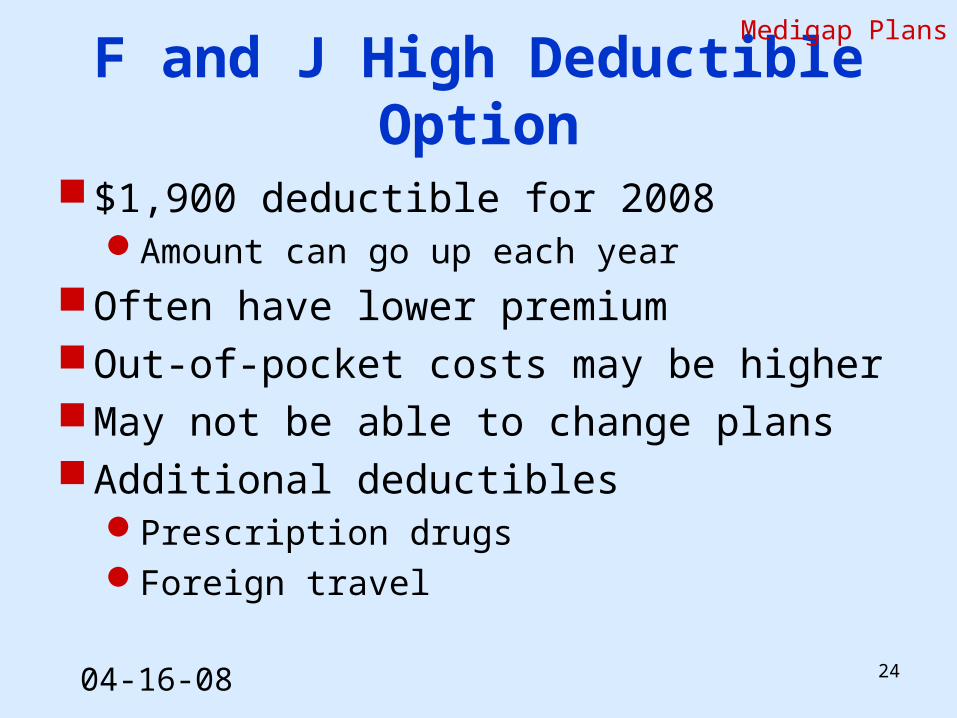

F and J High Deductible Option

$1,900 deductible for 2008Amount can go up each year

Often have lower premiumOut-of-pocket costs may be higherMay not be able to change plansAdditional deductibles

Prescription drugsForeign travel

Medigap Plans

04-16-08 25

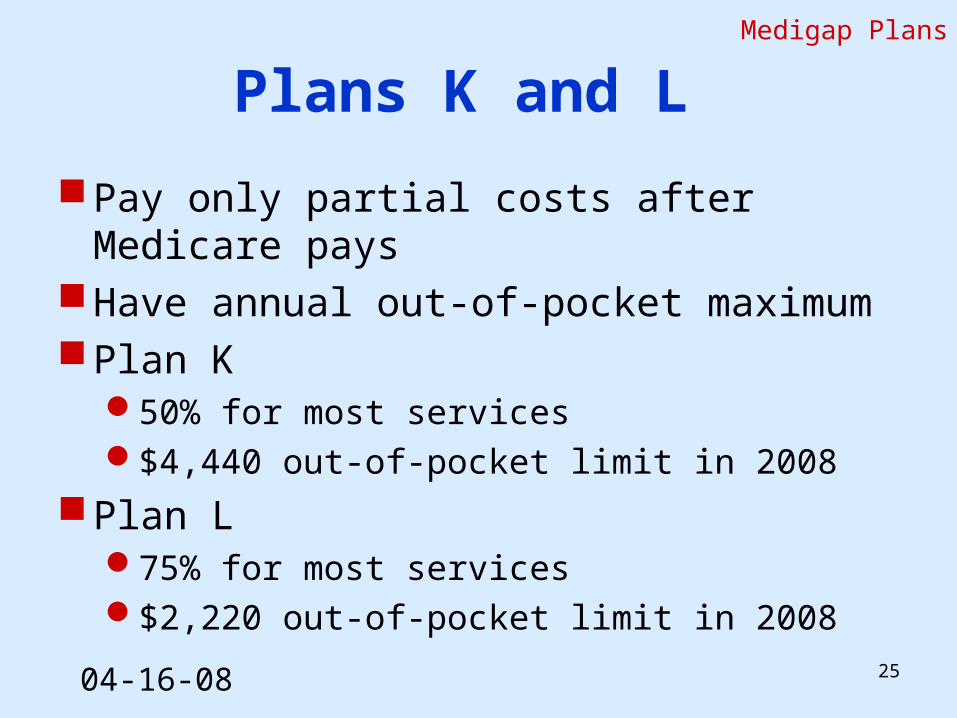

Plans K and L

Pay only partial costs after Medicare paysHave annual out-of-pocket maximumPlan K

50% for most services$4,440 out-of-pocket limit in 2008

Plan L 75% for most services$2,220 out-of-pocket limit in 2008

Medigap Plans

04-16-08 26

Session Topics

OverviewMedigap benefitsMedigap plans

Medigap costs

04-16-08 27

How Much Does Medigap Cost?

Depends onYour age (in some states)Where you liveCompany selling the policy

Can be big differences in premiumsFor exactly the same coverage

Compare the same Medigap policies

Medigap Costs

04-16-08 28

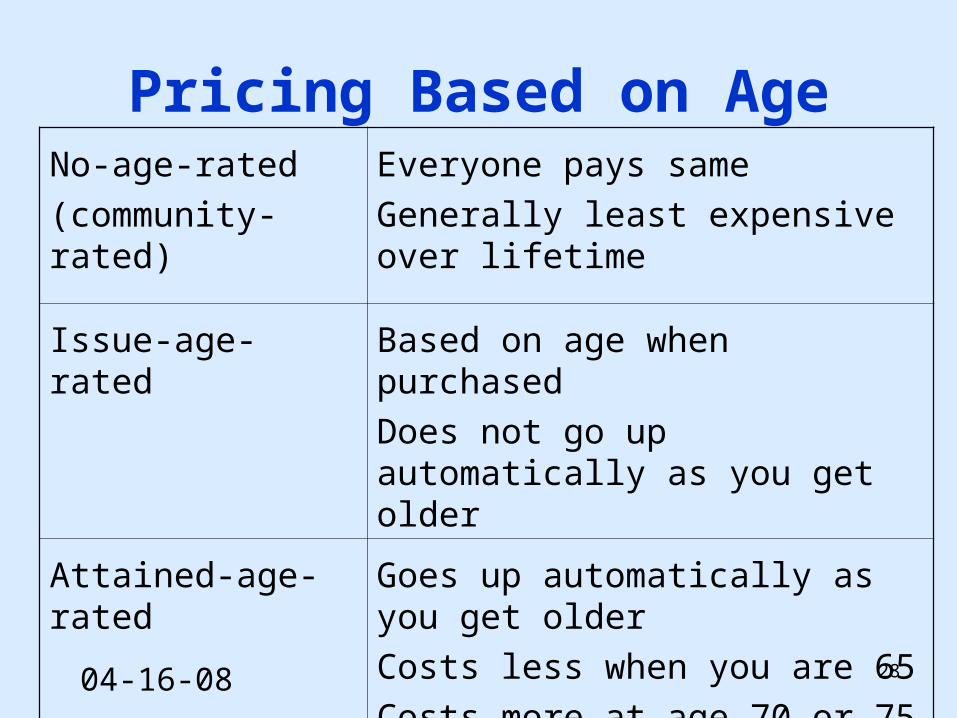

Pricing Based on AgeNo-age-rated

(community-rated)

Everyone pays same

Generally least expensive over lifetime

Issue-age-rated Based on age when purchased

Does not go up automatically as you get older

Attained-age-rated Goes up automatically as you get older

Costs less when you are 65

Costs more at age 70 or 75

04-16-08 29

What is Underwriting?

ReviewHealth statusMedical history

Insurance company determinesWhether to accept your applicationHow much to charge youWhether to make you wait for some benefits

ApplicationUsually includes medical questions Fill out carefully

Medigap Costs

04-16-08 30

Buying a Medigap Policy

May be able to buy a policy any timeBest time is during open enrollment period

Lasts for 6 monthsStarts on first day of the month you are

• Age 65 or older AND

• Enrolled in Medicare Part B

Once 6-month Medigap open enrollment period starts, it can't be changed

Medigap Costs

04-16-08 31

Open Enrollment Period

Insurance company can’tDeny you coverageMake you wait for coverage to start

• But may make you wait for coverage of pre-existing conditions

– Unless you have creditable coverage

Charge you more for a policy• Because of your health problems

Medigap Costs

04-16-08 32

Let’s look at a case study…

It is October 1, 2008, and Sam (who is 65) wants to buy a Medigap policy. He needs to know if he is in his open enrollment period. He looks at his Medicare card. His Medicare Part B coverage started August 1, 2008.Is Sam in his Medigap open enrollment period?Can the company deny him coverage?

Medigap Costs

Medigap in Detail

Module 3—Lesson 2

Lesson 1: Medigap Basics

Lesson 2: Medigap in Detail

04-16-08 34

Session Topics

Prior creditable coverageUnder age 65Medigap and MedicaidGuaranteed issueMore information

04-16-08 35

Session Topics

Prior creditable coverageUnder age 65Medigap and MedicaidGuaranteed issueMore information

04-16-08 36

Pre-Existing Condition

Health problem before new policy startsMedigap company can refuse to cover

that conditionIf diagnosed or treated during the 6 months

before the policy startsFor up to 6 months in some casesCalled “pre-existing condition waiting period”

Medigap Coverage

04-16-08 37

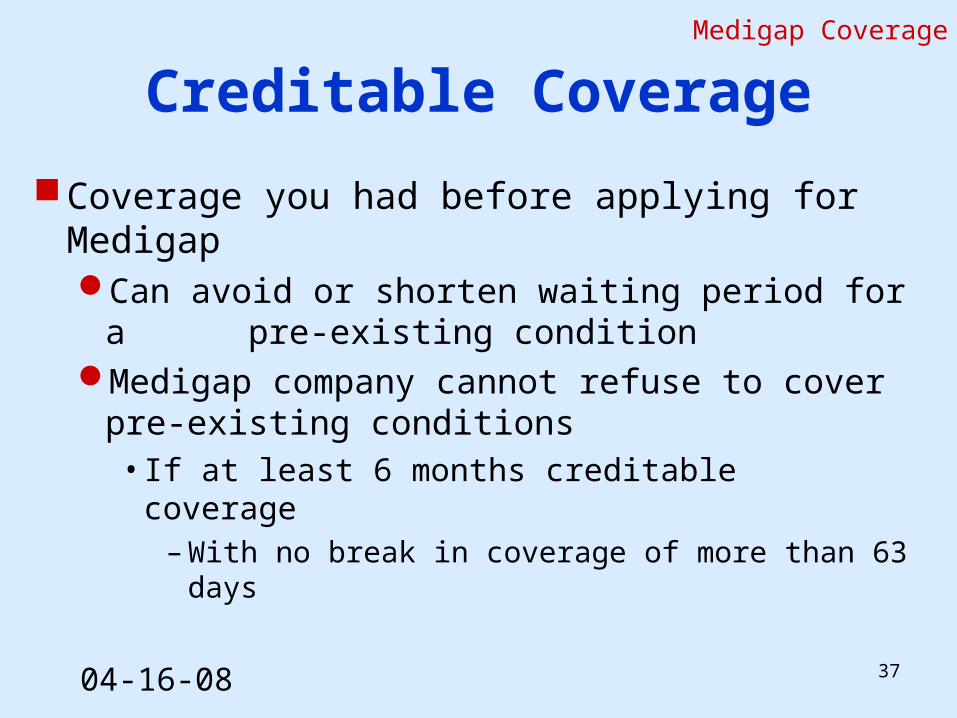

Creditable Coverage

Coverage you had before applying for MedigapCan avoid or shorten waiting period for a

pre-existing conditionMedigap company cannot refuse to cover

pre-existing conditions• If at least 6 months creditable coverage

– With no break in coverage of more than 63 days

Medigap Coverage

04-16-08 38

Examples of Creditable Coverage

Union/employer group health plan

Some health insurance policies

Medicare Part A or B Medicaid IHS or tribal organization A state health benefits

risk pool

TRICARE FEHBP Public health plan Health plan under the

Peace Corps Act COBRA SCHIP

Medigap Coverage

04-16-08 39

Not Creditable Coverage

Hospital indemnity insuranceSpecified disease insurance

For example, cancer insurance

Vision or dental policiesLong-term care policies

Medigap Coverage

04-16-08 40

Let’s look at a case study…

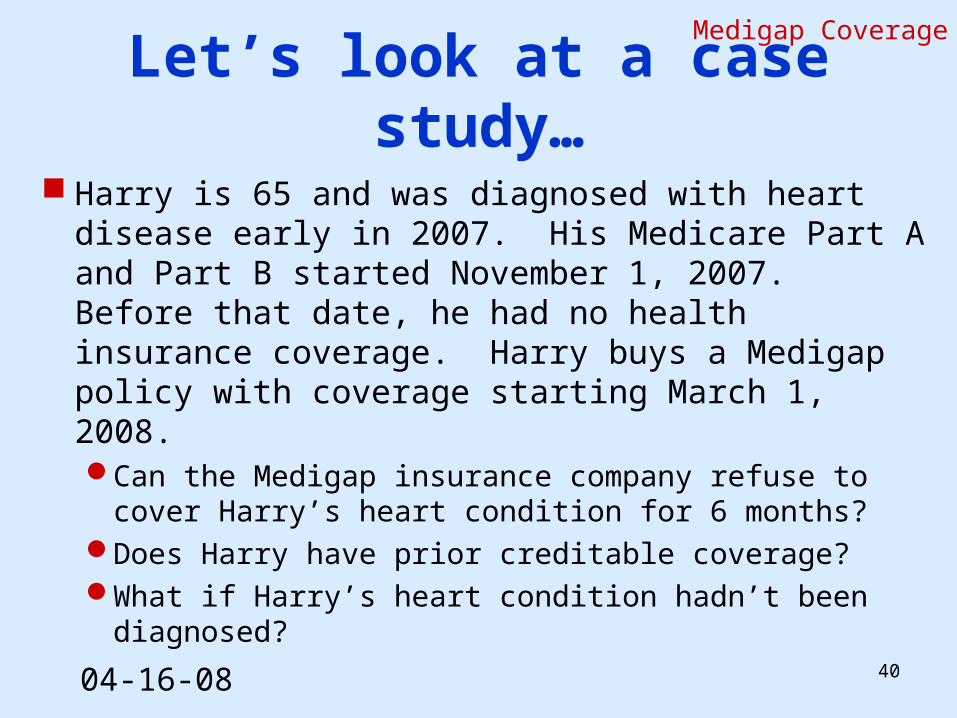

Harry is 65 and was diagnosed with heart disease early in 2007. His Medicare Part A and Part B started November 1, 2007. Before that date, he had no health insurance coverage. Harry buys a Medigap policy with coverage starting March 1, 2008.Can the Medigap insurance company refuse to cover

Harry’s heart condition for 6 months?Does Harry have prior creditable coverage?What if Harry’s heart condition hadn’t been diagnosed?

Medigap Coverage

04-16-08 41

Session Topics

Prior creditable coverage

Under age 65Medigap and MedicaidGuaranteed issueMore information

04-16-08 42

Medigap for People Under 65

Federal law does not require coverageMay not be able to buy a Medigap policySome state laws are differentAt age 65

Can choose and buy any Medigap policyCompanies cannot refuse to sell Medigap6-month open enrollment periodAlready have Medigap

• May reapply to get a better rate

Under Age 65

04-16-08 43

Medigap for People Under 65

Some companies sell to people under 65Policies may cost more

Some states require Medigap be offeredSee Guide to Health Insurance for People

with Medicare

Another open enrollment period at 65

Under Age 65

04-16-08 44

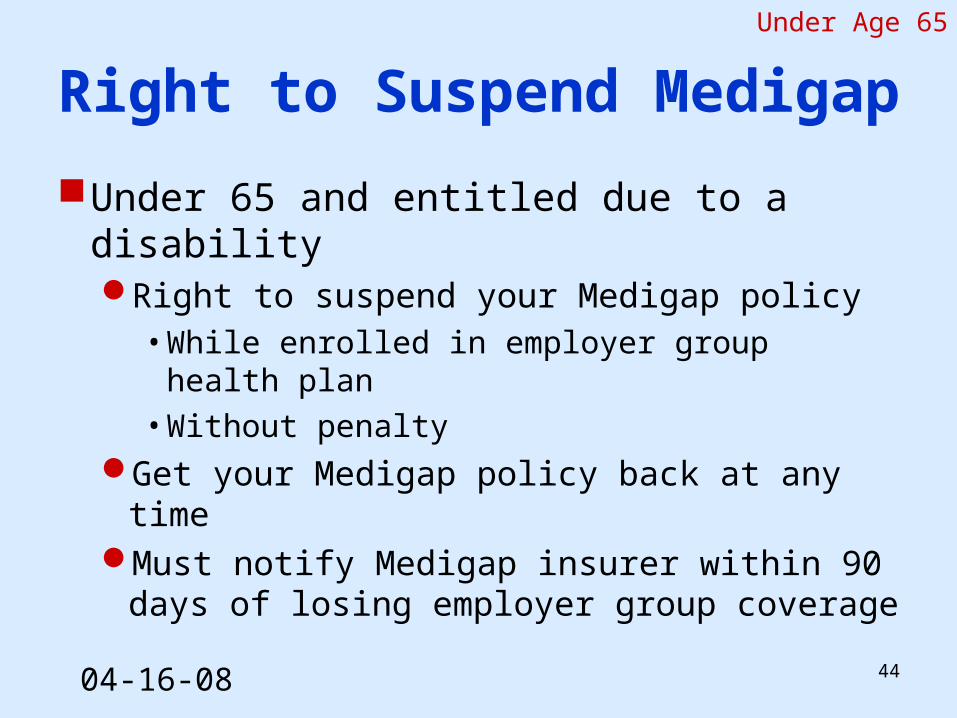

Right to Suspend Medigap

Under 65 and entitled due to a disabilityRight to suspend your Medigap policy

• While enrolled in employer group health plan

• Without penaltyGet your Medigap policy back at any timeMust notify Medigap insurer within 90 days of

losing employer group coverage

Under Age 65

04-16-08 45

Session Topics

Prior creditable coverageUnder age 65

Medigap and MedicaidGuaranteed issueMore information

04-16-08 46

Medigap and Medicaid

If you have both Medicare and MedicaidMost health care costs are coveredCan suspend Medigap policy for up to 2

yearsAn insurance company can sell you a

Medigap policy only in certain situations

For information, call state Medicaid office

Medigap and Medicaid

04-16-08 47

Suspending Medigap

Right to suspend MedigapWithin 90 days of getting MedicaidDo not pay premiumsPolicy will not pay benefitsCan suspend policy for up to 2 yearsCan start it up again

• No new medical underwriting• No pre-existing condition waiting periods

Call state Medicaid office

Medigap and Medicaid

04-16-08 48

Session Topics

Prior creditable coverageUnder age 65Medigap and Medicaid

Guaranteed issue rightsMore information

04-16-08 49

Medigap Rights and Protections

Also called “guaranteed issue rights”Special rights to buy MedigapKeep

LettersClaim denialsPostmarked envelopes

Protections are in Federal lawMany states provide more Medigap protectionsCall your SHIP or state insurance department

Guaranteed Issue Rights

04-16-08 50

Summary of Medigap Protections

Guaranteed issue rights in some situationsRight to buy a Medigap policyApply within 63 days from other coverage

ending

In these situations, an insurance companyMust sell you a Medigap policyMust cover all pre-existing conditionsCan’t charge more because of past or present

health problems

Guaranteed Issue Rights

04-16-08 51

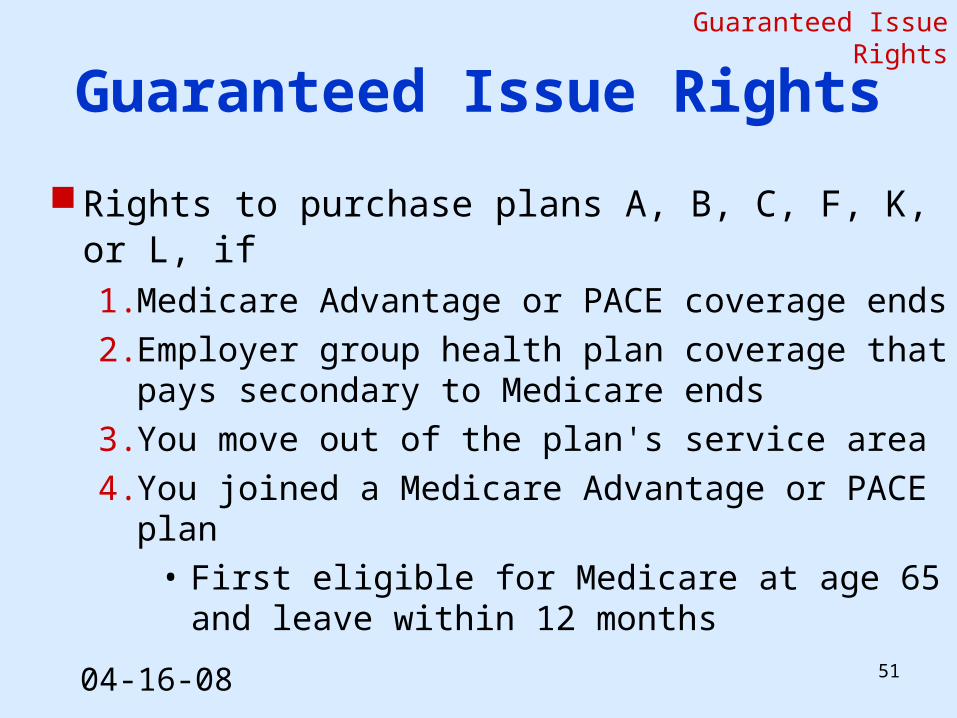

Guaranteed Issue Rights

Rights to purchase plans A, B, C, F, K, or L, if 1. Medicare Advantage or PACE coverage ends

2. Employer group health plan coverage that pays secondary to Medicare ends

3. You move out of the plan's service area

4. You joined a Medicare Advantage or PACE plan• First eligible for Medicare at age 65 and

leave within 12 months

Guaranteed Issue Rights

04-16-08 52

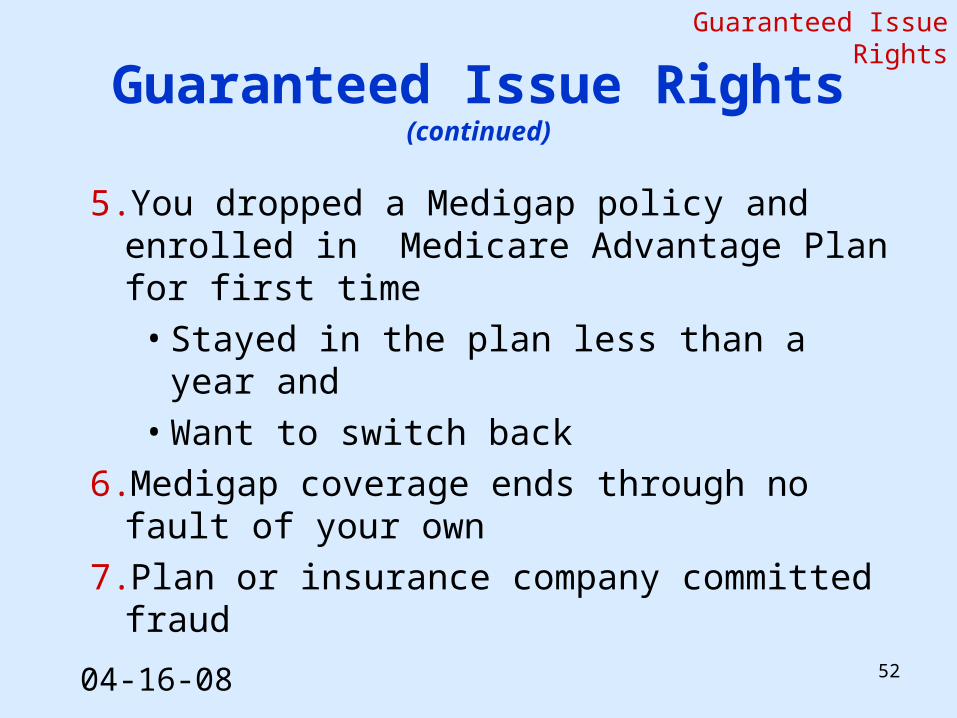

Guaranteed Issue Rights(continued)

5. You dropped a Medigap policy and enrolled in Medicare Advantage Plan for first time• Stayed in the plan less than a year and• Want to switch back

6. Medigap coverage ends through no fault of your own

7. Plan or insurance company committed fraud

Guaranteed Issue Rights

04-16-08 53

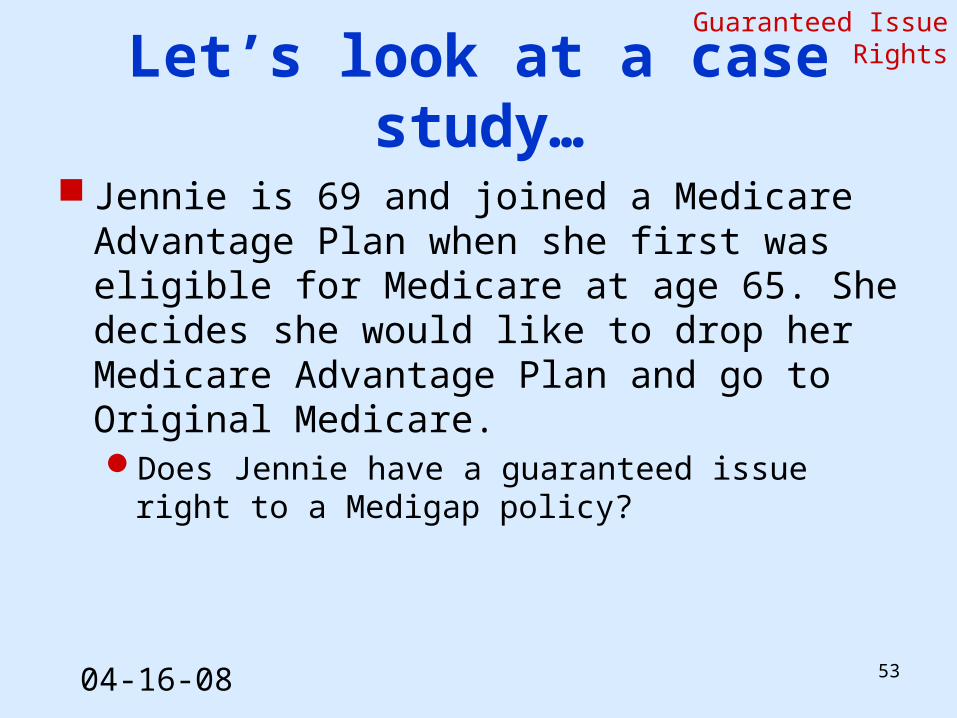

Let’s look at a case study…

Jennie is 69 and joined a Medicare Advantage Plan when she first was eligible for Medicare at age 65. She decides she would like to drop her Medicare Advantage Plan and go to Original Medicare.Does Jennie have a guaranteed issue right to a

Medigap policy?

Guaranteed Issue Rights

04-16-08 54

Session Topics

Prior creditable coverageUnder age 65Medigap and MedicaidGuaranteed issue

More information

04-16-08 55

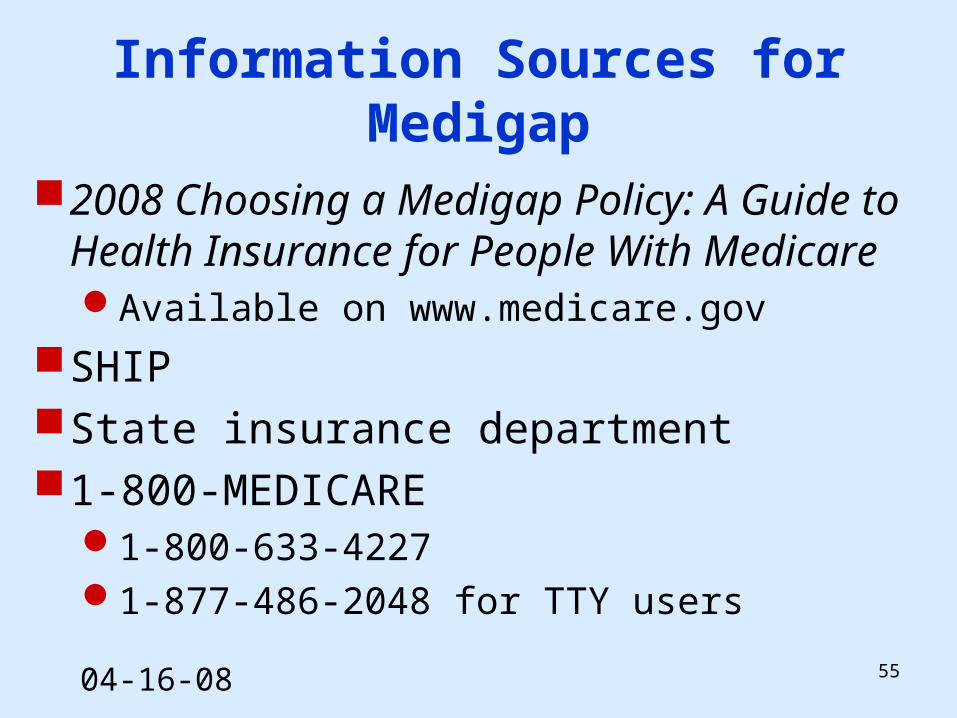

Information Sources for Medigap

2008 Choosing a Medigap Policy: A Guide to Health Insurance for People With MedicareAvailable on www.medicare.gov

SHIPState insurance department1-800-MEDICARE

1-800-633-42271-877-486-2048 for TTY users

This training module provided by the

For questions about training products, email [email protected]

To view all available NMTP materials or to subscribe to our listserv, visit

www.cms.hhs.gov/NationalMedicareTrainingProgram