Martins Abolins Economist

15

Baltic economic outlook Martins Abolins Economist September 2020

Transcript of Martins Abolins Economist

Baltic economic outlook

Martins Abolins

Economist

September 2020

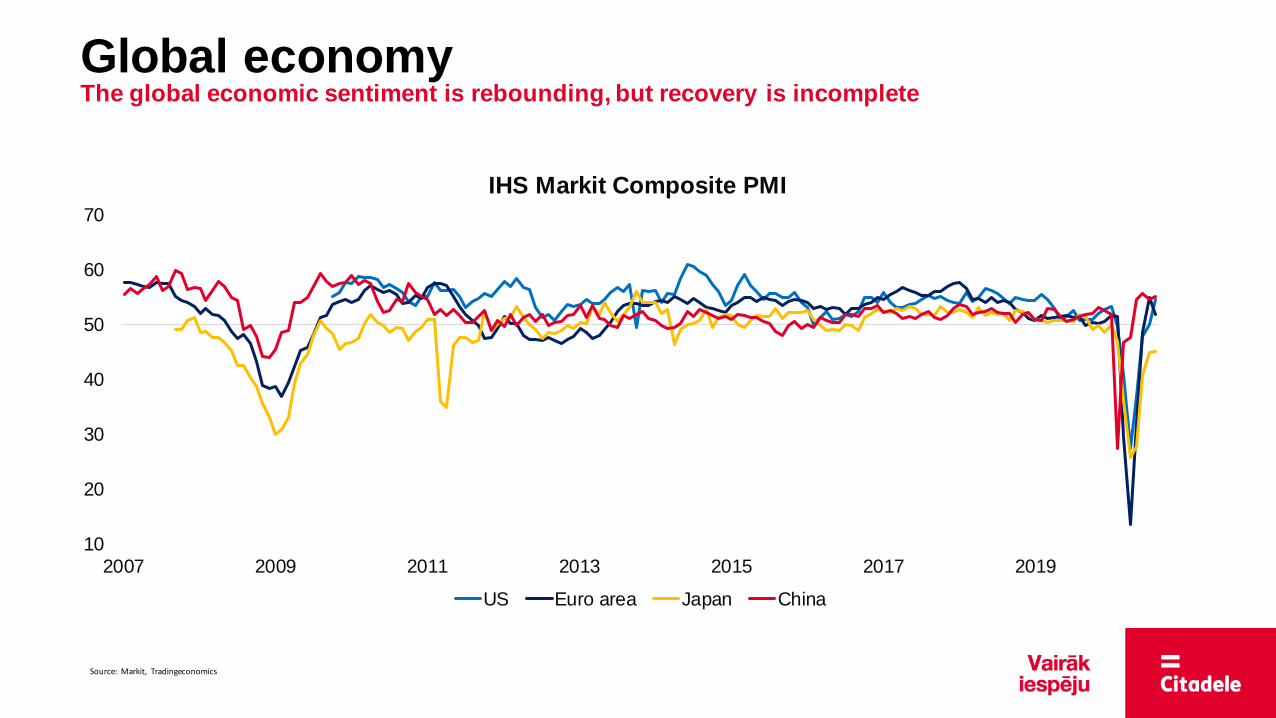

Global economy The global economic sentiment is rebounding, but recovery is incomplete

10

20

30

40

50

60

70

2007 2009 2011 2013 2015 2017 2019

IHS Markit Composite PMI

US Euro area Japan China

Source: Markit, Tradingeconomics

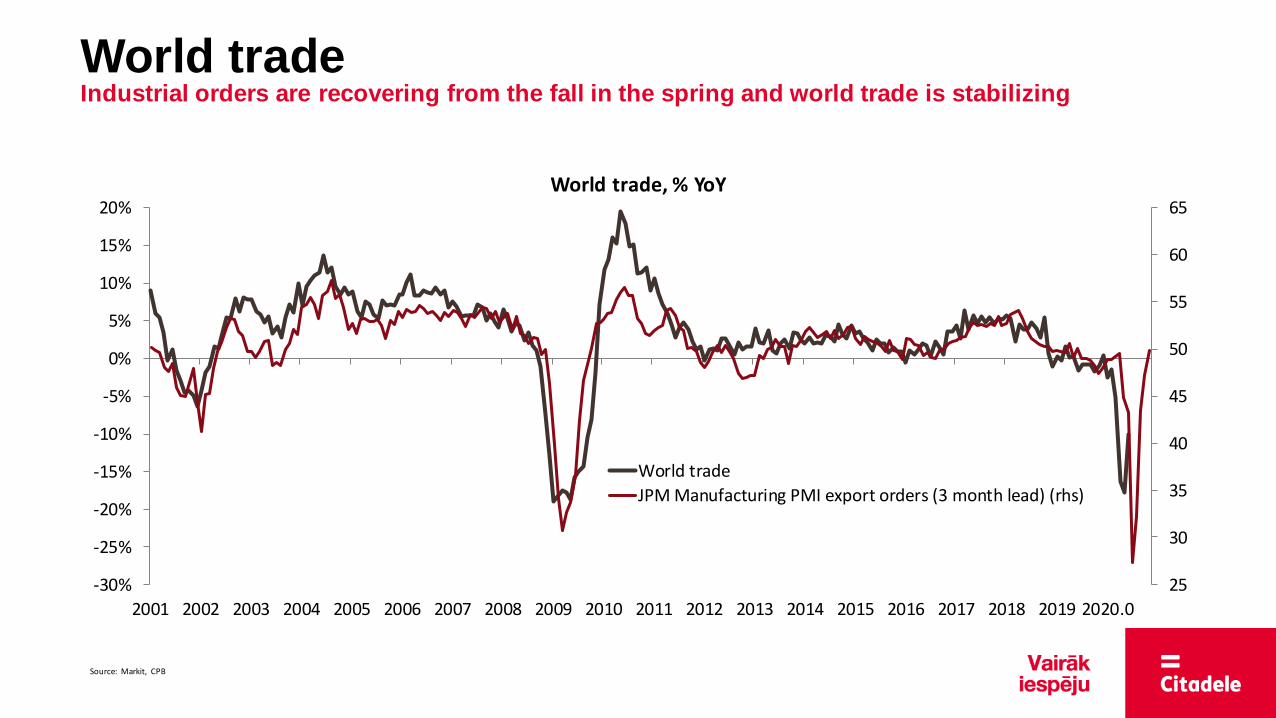

World trade Industrial orders are recovering from the fall in the spring and world trade is stabilizing

25

30

35

40

45

50

55

60

65

-30%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020.0

World trade, % YoY

World trade

JPM Manufacturing PMI export orders (3 month lead) (rhs)

Source: Markit, CPB

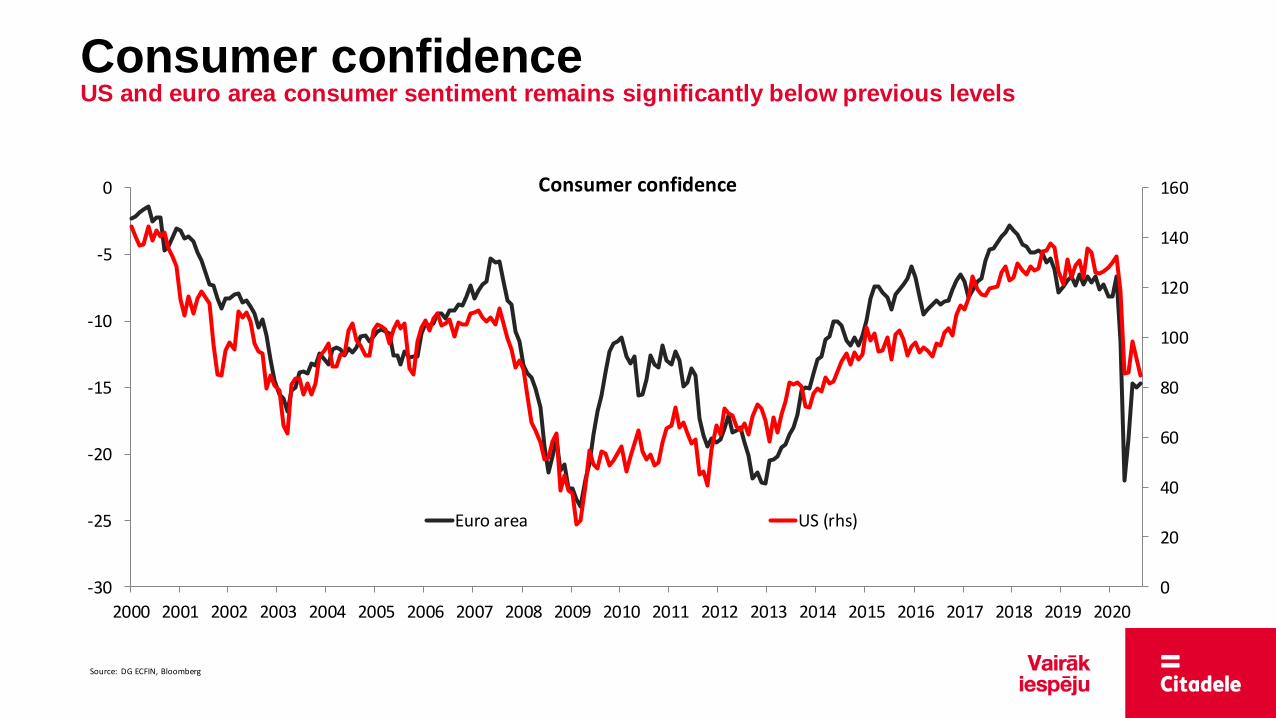

Consumer confidence US and euro area consumer sentiment remains significantly below previous levels

0

20

40

60

80

100

120

140

160

-30

-25

-20

-15

-10

-5

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Consumer confidence

Euro area US (rhs)

Source: DG ECFIN, Bloomberg

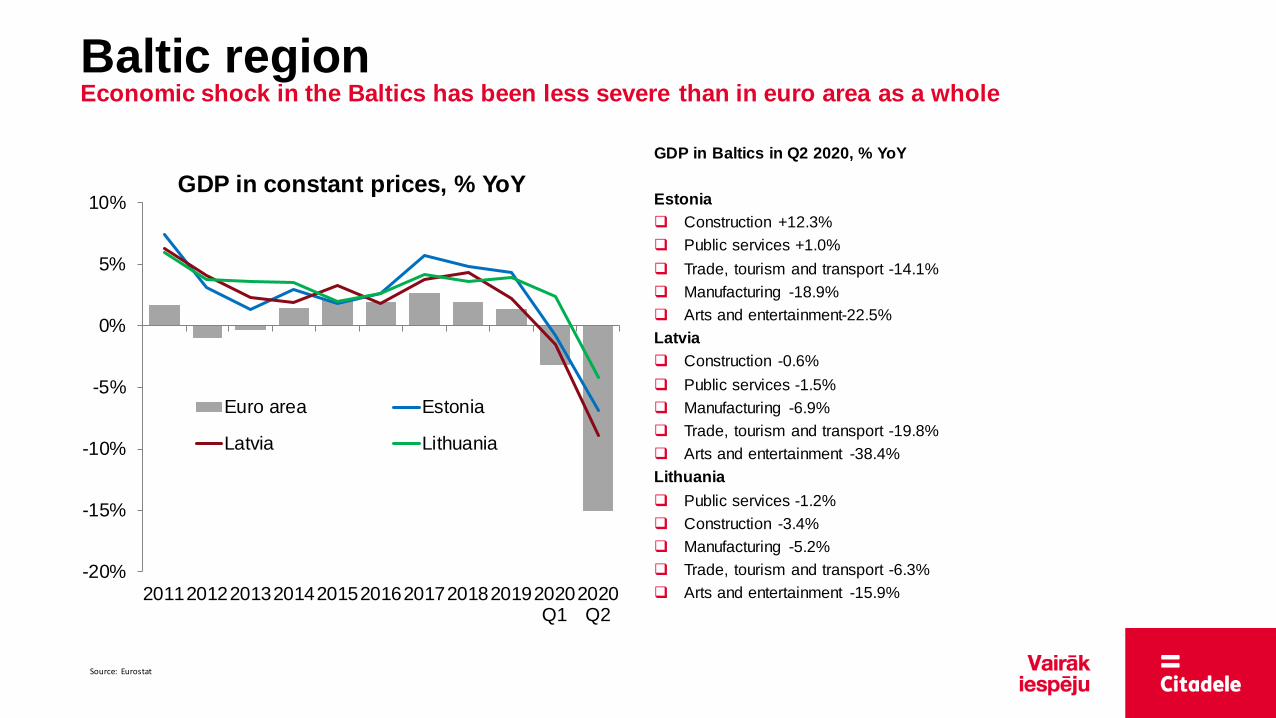

GDP in Baltics in Q2 2020, % YoY

Estonia

Construction +12.3%

Public services +1.0%

Trade, tourism and transport -14.1%

Manufacturing -18.9%

Arts and entertainment-22.5%

Latvia

Construction -0.6%

Public services -1.5%

Manufacturing -6.9%

Trade, tourism and transport -19.8%

Arts and entertainment -38.4%

Lithuania

Public services -1.2%

Construction -3.4%

Manufacturing -5.2%

Trade, tourism and transport -6.3%

Arts and entertainment -15.9%

-20%

-15%

-10%

-5%

0%

5%

10%

2011201220132014201520162017201820192020Q1

2020Q2

GDP in constant prices, % YoY

Euro area Estonia

Latvia Lithuania

Baltic region Economic shock in the Baltics has been less severe than in euro area as a whole

Source: Eurostat

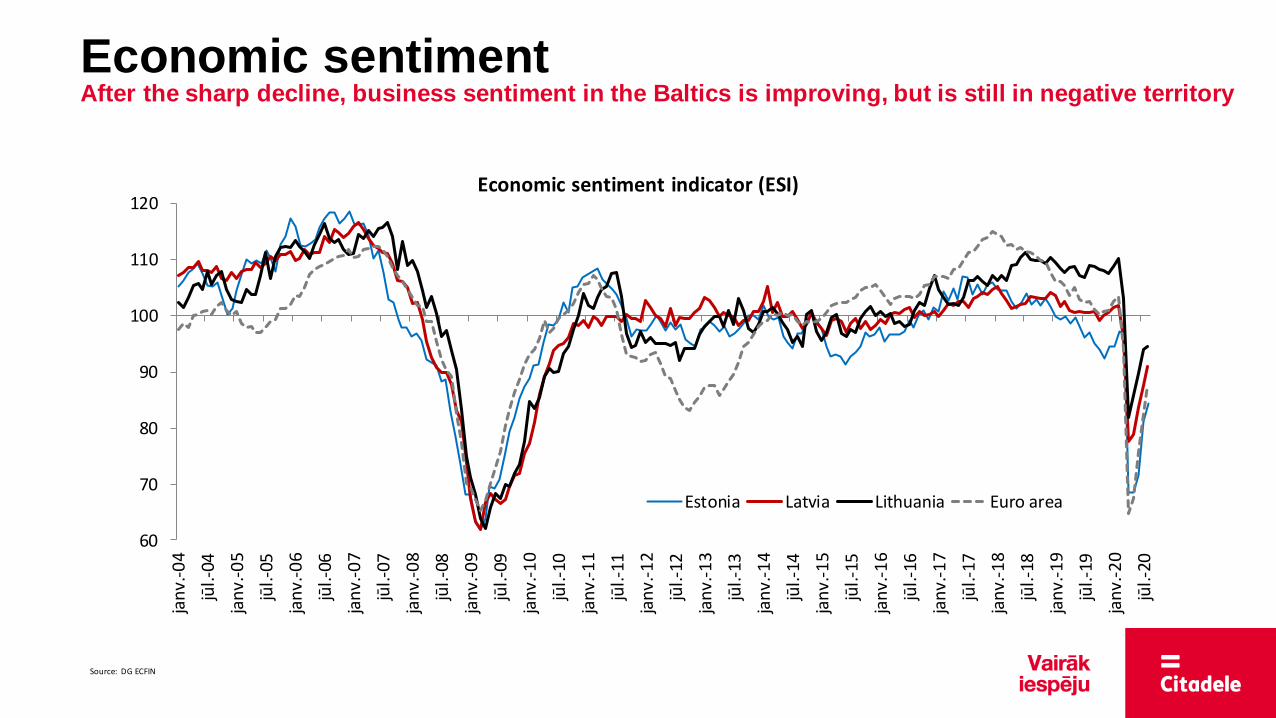

Economic sentiment After the sharp decline, business sentiment in the Baltics is improving, but is still in negative territory

60

70

80

90

100

110

120

jan

v.-0

4

jūl.-04

jan

v.-0

5

jūl.-05

jan

v.-0

6

jūl.-06

jan

v.-0

7

jūl.-07

jan

v.-0

8

jūl.-08

jan

v.-0

9

jūl.-09

jan

v.-1

0

jūl.-10

jan

v.-1

1

jūl.-11

jan

v.-1

2

jūl.-12

jan

v.-1

3

jūl.-13

jan

v.-1

4

jūl.-14

jan

v.-1

5

jūl.-15

jan

v.-1

6

jūl.-16

jan

v.-1

7

jūl.-17

jan

v.-1

8

jūl.-18

jan

v.-1

9

jūl.-19

jan

v.-2

0

jūl.-20

Economic sentiment indicator (ESI)

Estonia Latvia Lithuania Euro area

Source: DG ECFIN

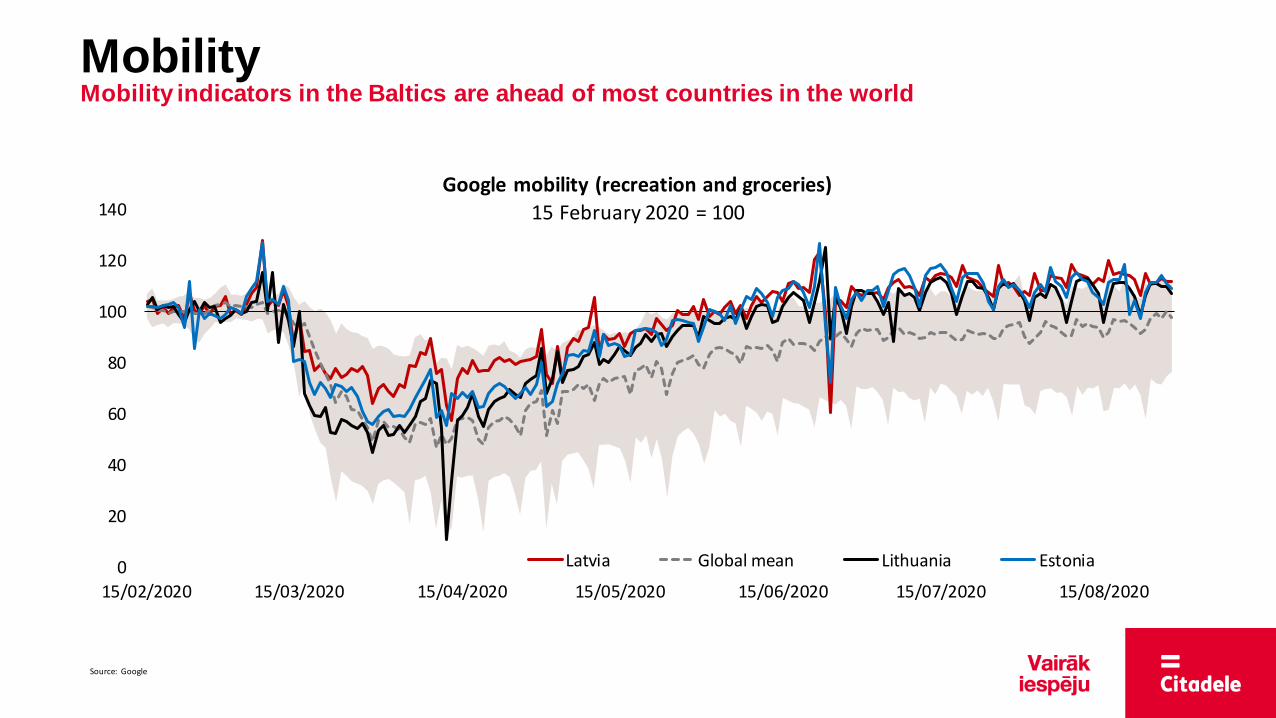

Mobility Mobility indicators in the Baltics are ahead of most countries in the world

0

20

40

60

80

100

120

140

15/02/2020 15/03/2020 15/04/2020 15/05/2020 15/06/2020 15/07/2020 15/08/2020

Google mobility (recreation and groceries)

15 February 2020 = 100

Latvia Global mean Lithuania Estonia

Source: Google

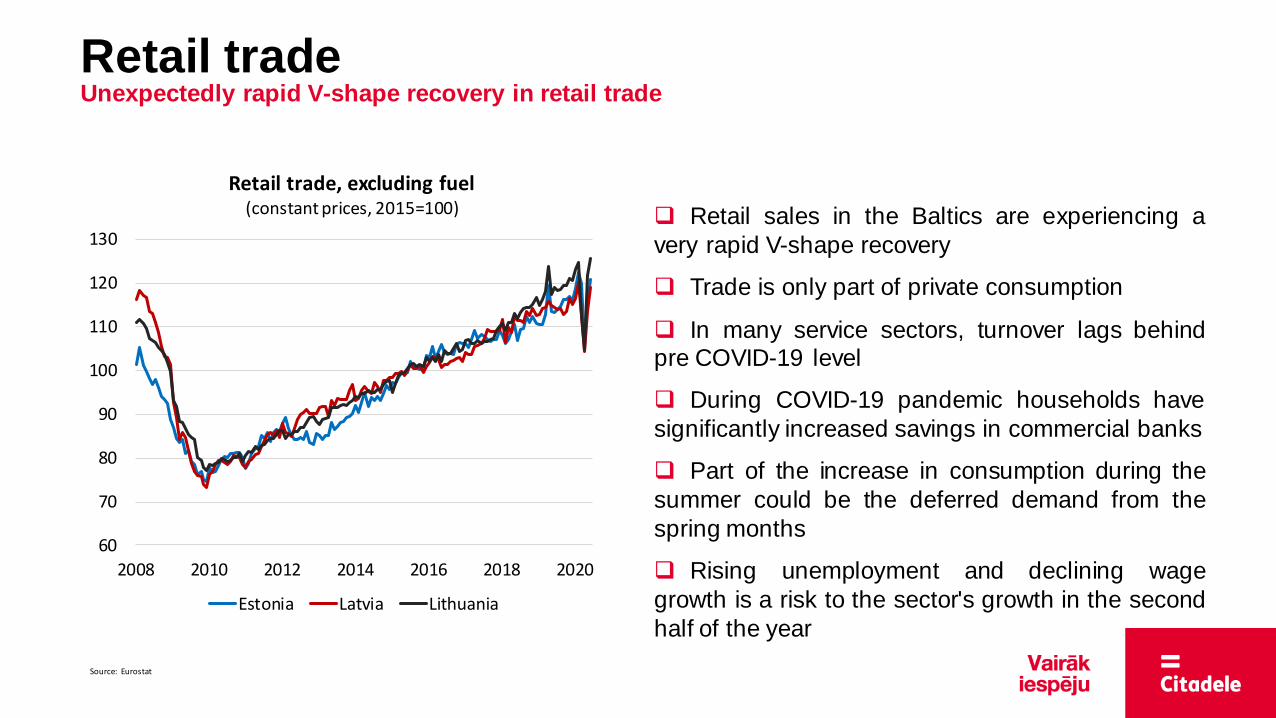

Retail trade Unexpectedly rapid V-shape recovery in retail trade

Retail sales in the Baltics are experiencing a

very rapid V-shape recovery

Trade is only part of private consumption

In many service sectors, turnover lags behind pre COVID-19 level

During COVID-19 pandemic households have

significantly increased savings in commercial banks

Part of the increase in consumption during the

summer could be the deferred demand from the

spring months

Rising unemployment and declining wage

growth is a risk to the sector's growth in the second

half of the year

60

70

80

90

100

110

120

130

2008 2010 2012 2014 2016 2018 2020

Retail trade, excluding fuel (constant prices, 2015=100)

Estonia Latvia Lithuania

Source: Eurostat

-10%

-5%

0%

5%

10%

15%

20%

2004 2006 2008 2010 2012 2014 2016 2018 2020

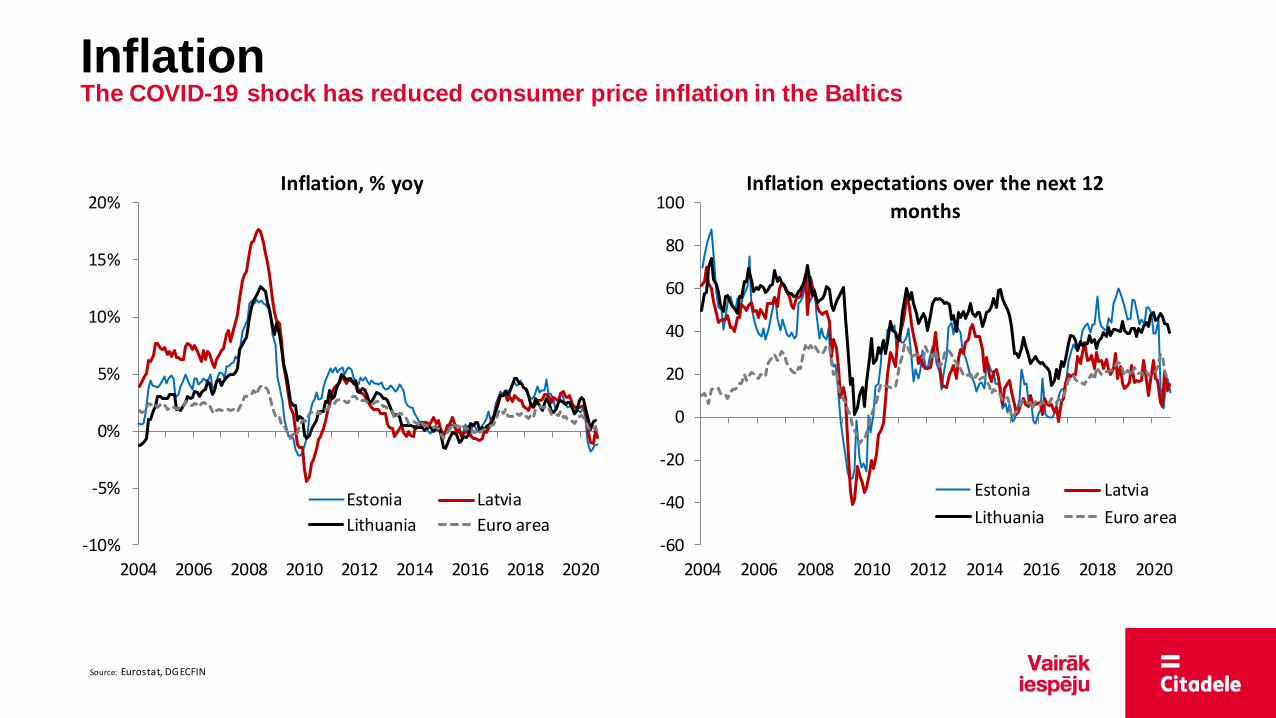

Inflation, % yoy

Estonia Latvia

Lithuania Euro area-60

-40

-20

0

20

40

60

80

100

2004 2006 2008 2010 2012 2014 2016 2018 2020

Inflation expectations over the next 12

months

Estonia Latvia

Lithuania Euro area

Inflation The COVID-19 shock has reduced consumer price inflation in the Baltics

Source: Eurostat, DG ECFIN

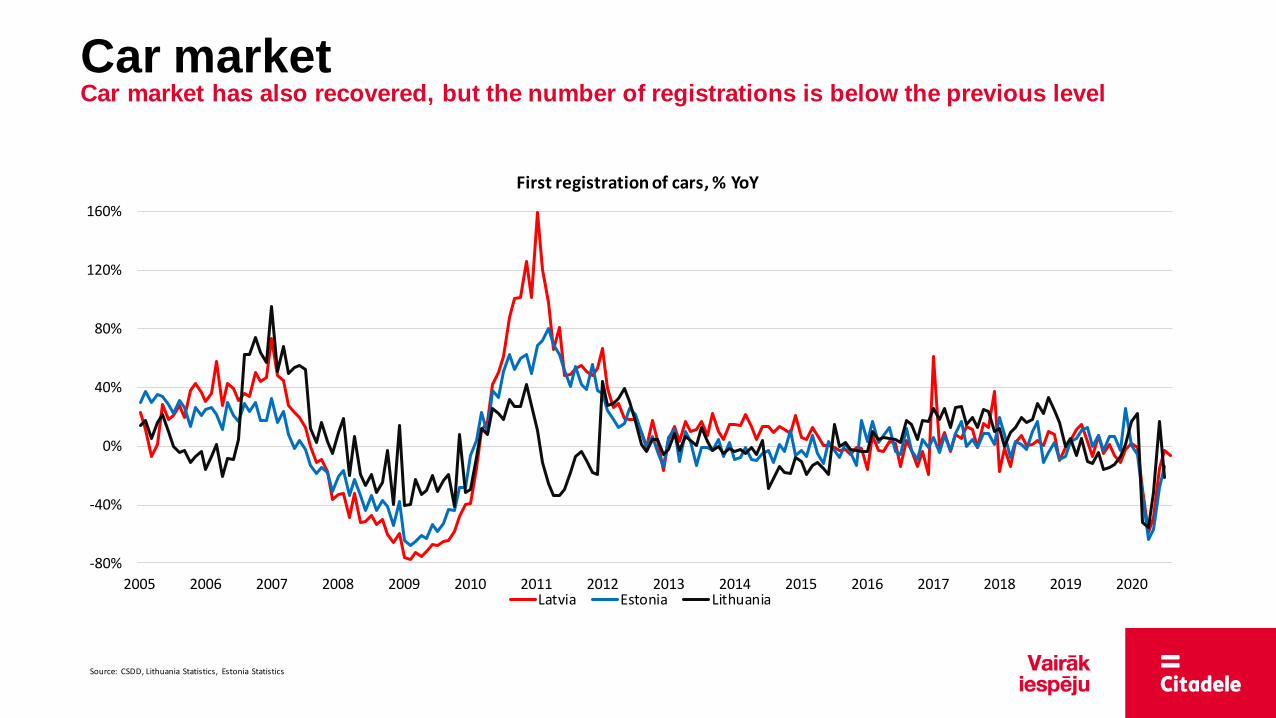

Car market Car market has also recovered, but the number of registrations is below the previous level

-80%

-40%

0%

40%

80%

120%

160%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

First registration of cars, % YoY

Latvia Estonia Lithuania

Source: CSDD, Lithuania Statistics, Estonia Statistics

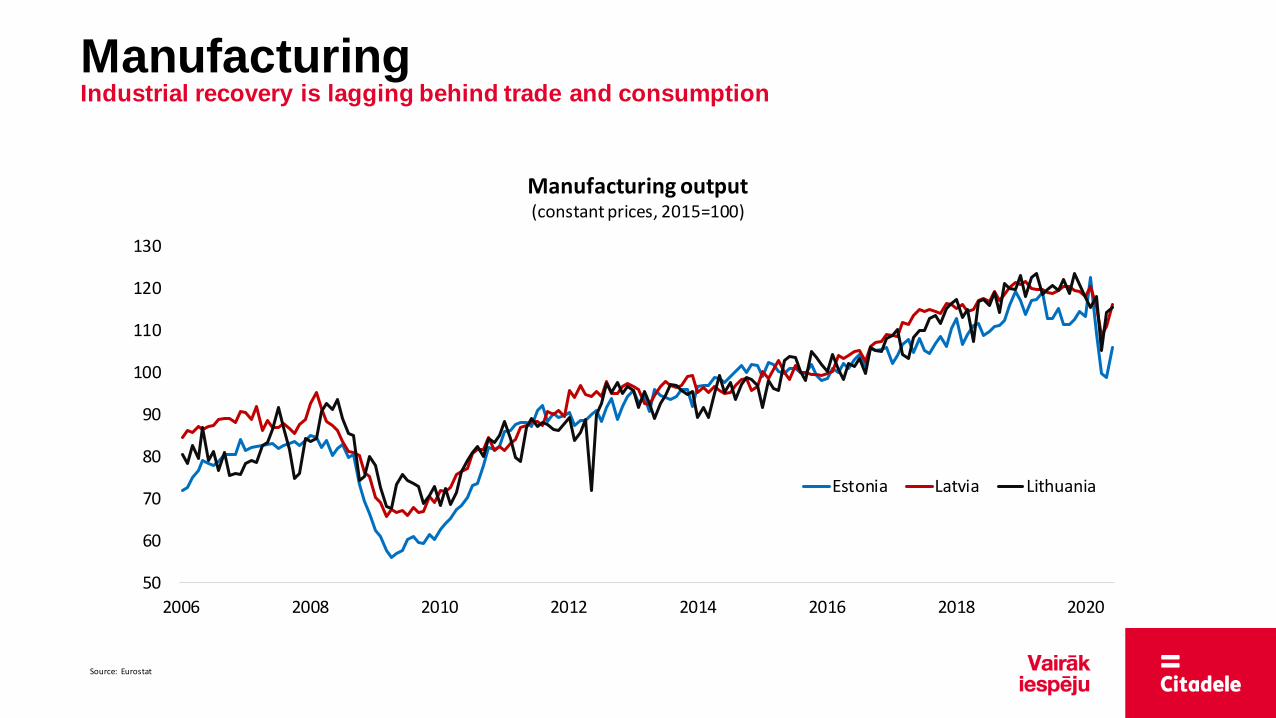

Manufacturing Industrial recovery is lagging behind trade and consumption

50

60

70

80

90

100

110

120

130

2006 2008 2010 2012 2014 2016 2018 2020

Manufacturing output (constant prices, 2015=100)

Estonia Latvia Lithuania

Source: Eurostat

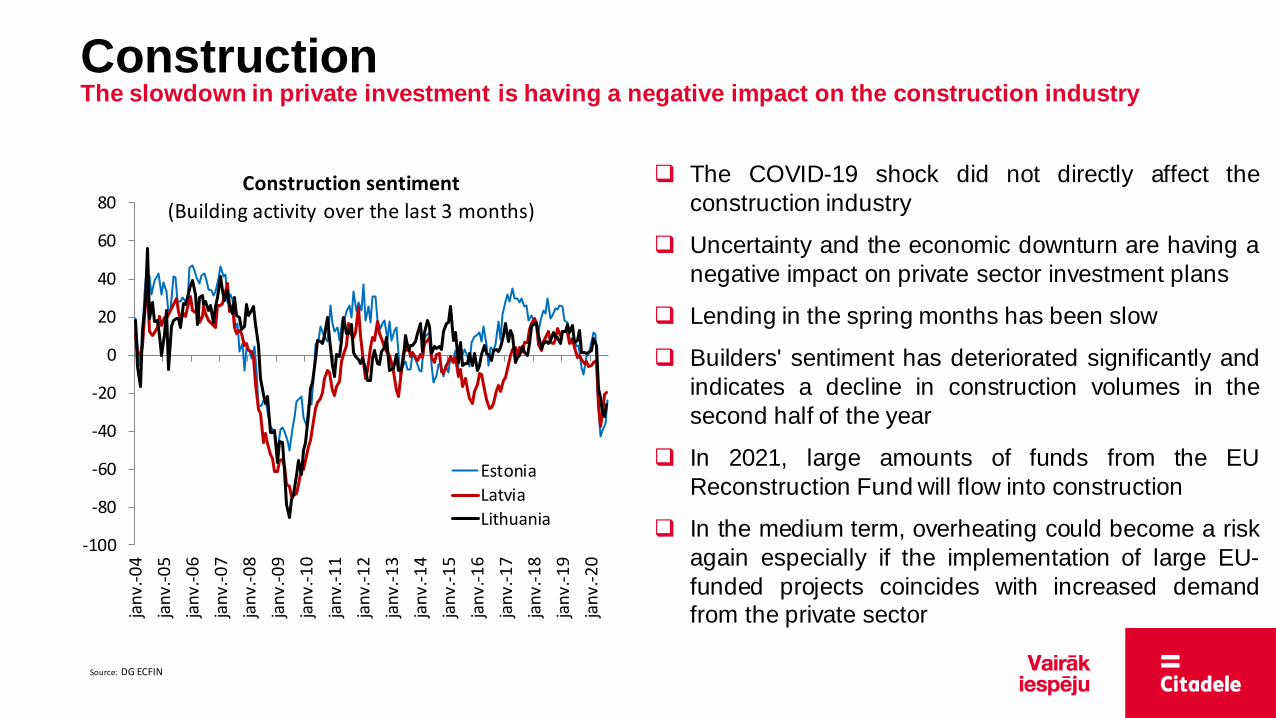

The COVID-19 shock did not directly affect the

construction industry

Uncertainty and the economic downturn are having a

negative impact on private sector investment plans

Lending in the spring months has been slow

Builders' sentiment has deteriorated significantly and

indicates a decline in construction volumes in the

second half of the year

In 2021, large amounts of funds from the EU

Reconstruction Fund will flow into construction

In the medium term, overheating could become a risk

again especially if the implementation of large EU-

funded projects coincides with increased demand from the private sector

-100

-80

-60

-40

-20

0

20

40

60

80

jan

v.-0

4

jan

v.-0

5

jan

v.-0

6

jan

v.-0

7

jan

v.-0

8

jan

v.-0

9

jan

v.-1

0

jan

v.-1

1

jan

v.-1

2

jan

v.-1

3

jan

v.-1

4

jan

v.-1

5

jan

v.-1

6

jan

v.-1

7

jan

v.-1

8

jan

v.-1

9

jan

v.-2

0

Construction sentiment

(Building activity over the last 3 months)

Estonia

Latvia

Lithuania

Construction The slowdown in private investment is having a negative impact on the construction industry

Source: DG ECFIN

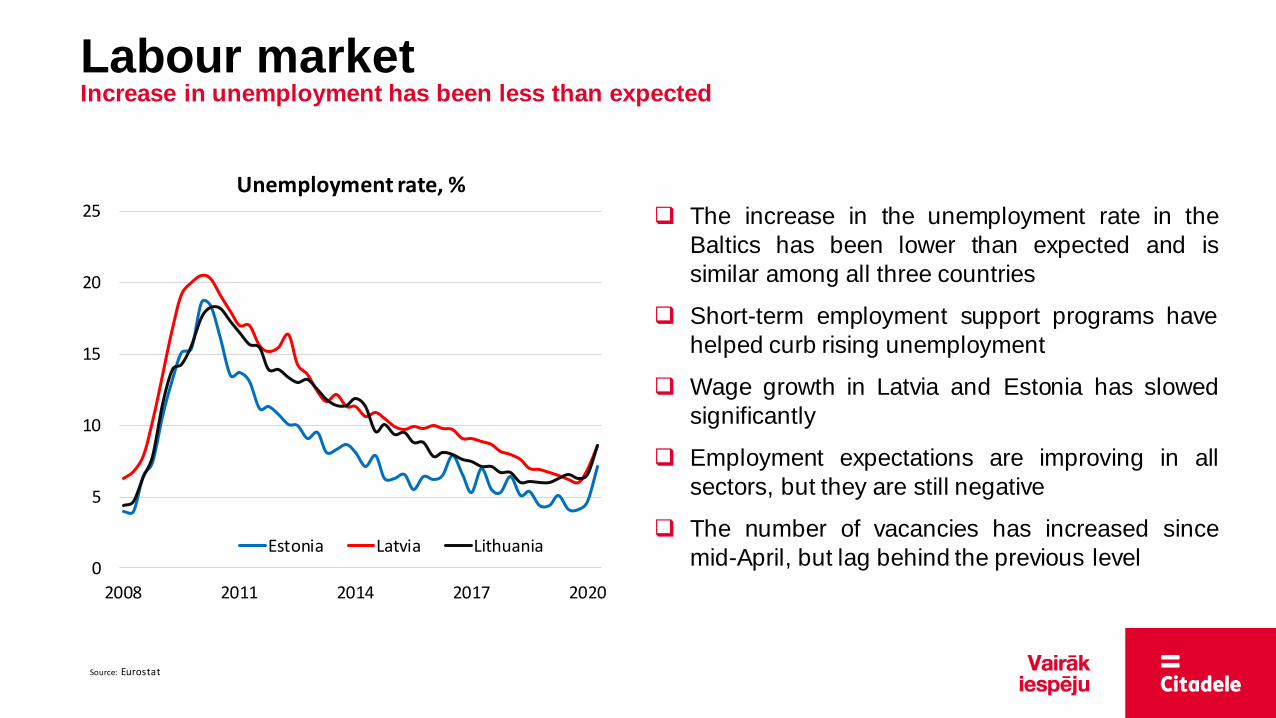

Labour market Increase in unemployment has been less than expected

The increase in the unemployment rate in the

Baltics has been lower than expected and is

similar among all three countries

Short-term employment support programs have

helped curb rising unemployment

Wage growth in Latvia and Estonia has slowed

significantly

Employment expectations are improving in all

sectors, but they are still negative

The number of vacancies has increased since

mid-April, but lag behind the previous level 0

5

10

15

20

25

2008 2011 2014 2017 2020

Unemployment rate, %

Estonia Latvia Lithuania

Source: Eurostat

The Baltic economy reached its lowest point in mid-April.

The economic recovery has so far been much stronger than expected.

Domestic consumption is leading economic recovery.

Retail sales returned to positive growth in June, but the situation in the services sector is less encouraging.

Exports and production lag behind consumption, but the situation in foreign markets is improving.

In the second quarter, the decline in GDP in the Baltics was significantly smaller than in the euro area as a whole.

The key to the Baltic's success was rapid virus containment, strong public finances, timely support for the economy and

balanced economic development in previous years.

The sectors hardest hit, tourism and leisure, will only be able to return to previous levels when a vaccine or effective

treatment for COVID-19 is available.

The decline in GDP in the Baltic region in 2020 will not exceed 5% and economic losses will be lower than in other

countries.

Economic growth in the Baltics in 2021 will be in the range of 3-5%.

The economic recovery both in the world and in the Baltics is still incomplete.

Since June, improvements in short-term economic performance have slowed significantly.

Strong fiscal and monetary stimulus measures continue to support the economy. Financial markets remain optimistic.

The eurozone has slipped into deflation and consumers do not expect inflation to rise in the near future.

The biggest risk to economic recovery is the possible second wave of COVID-19.

Conclusions The Baltic region is recovering from the COVID-19 shock, but uncertainty remains

AS “Citadele banka”

Republikas laukums 2A

Rīga, Latvija

![INDEX [martins-supermarkets.com]](https://static.fdocuments.us/doc/165x107/61d44a57b48a9f17f2484734/index-martins-.jpg)