Marketing Incentives and Mutual Fund Portfolio Choicewebuser.bus.umich.edu/dsosyura/Research...

34

Marketing Incentives and Mutual Fund Portfolio Choice* Denis Sosyura Ross School of Business University of Michigan [email protected] Abstract This paper studies the effect of funds’ marketing incentives on their choice of portfolio holdings. I argue that open-end funds exploit the familiarity bias of small investors by establishing salient positions in stocks with abnormally high positive media coverage. The loading on positive news is more pronounced for the widely-reported top 10 holdings. The strategy of holding stocks with positive media coverage at reporting dates is more prevalent among funds that charge a load, spend more on marketing, and have somewhat weaker and less stable past performance. This tactic has a significant positive effect on fund flows, controlling for other holdings’ and funds’ characteristics. Overall, the article shows the importance of media coverage in investors’ evaluation of fund holdings and demonstrates the strategic response of money managers to this investor behavior. *I am grateful to Arturo Bris and Huseyin Gulen for their data on mutual fund closures. I would also like to thank Nick Barberis, Darwin Choi, William Goetzmann, Dong Lou, Antti Petajisto, Paul Tetlock, Geert Rouwenhorst, Frank Zhang, as well as seminar participants at Georgetown University, Northwestern University, New York University, Penn State University, Rice University, the University of Michigan, the University of Notre Dame, the University of Southern California, the University of Toronto, Yale University, and Washington University in St. Louis for comments.

Transcript of Marketing Incentives and Mutual Fund Portfolio Choicewebuser.bus.umich.edu/dsosyura/Research...

Marketing Incentives and Mutual Fund Portfolio Choice*

Denis Sosyura

Ross School of Business

University of Michigan

Abstract

This paper studies the effect of funds’ marketing incentives on their choice of portfolio holdings. I argue that open-end

funds exploit the familiarity bias of small investors by establishing salient positions in stocks with abnormally high

positive media coverage. The loading on positive news is more pronounced for the widely-reported top 10 holdings.

The strategy of holding stocks with positive media coverage at reporting dates is more prevalent among funds that

charge a load, spend more on marketing, and have somewhat weaker and less stable past performance. This tactic has

a significant positive effect on fund flows, controlling for other holdings’ and funds’ characteristics. Overall, the

article shows the importance of media coverage in investors’ evaluation of fund holdings and demonstrates the

strategic response of money managers to this investor behavior.

*I am grateful to Arturo Bris and Huseyin Gulen for their data on mutual fund closures. I would also like to thank

Nick Barberis, Darwin Choi, William Goetzmann, Dong Lou, Antti Petajisto, Paul Tetlock, Geert Rouwenhorst, Frank

Zhang, as well as seminar participants at Georgetown University, Northwestern University, New York University,

Penn State University, Rice University, the University of Michigan, the University of Notre Dame, the University of

Southern California, the University of Toronto, Yale University, and Washington University in St. Louis for

comments.

2

Introduction

By 2010, the amount of capital in actively-managed mutual funds has reached a staggering $11.5

trillion. Yet portfolios of fund managers generally fail to outperform their passive benchmarks.1 In

addition, the extra fees associated with managing and marketing mutual funds impose an

additional burden on investor returns. If actively managed funds show bleak performance and

charge significant fees, how do they attract new capital?

In this paper, I examine the role of funds’ portfolio holdings in attracting capital flows. The

conjecture that fund holdings matter in investors’ capital allocation decisions is plausible for

several reasons. First, previous research has shown that funds strategically adjust their holdings

before reporting them to investors, a tactic known as window dressing (e.g., Lakonishok et al,

1991; Musto, 1999). Second, fund marketing materials typically provide a snapshot of top

portfolio holdings. Finally, the largest investor research services such as Morningstar, Yahoo-

Finance, and Lipper offer investors free access to information about fund portfolio holdings as part

of the key attributes of the fund.

If fund holdings play a role in investor decisions, what kind of stocks would generate a

favorable investor response? Prior research suggests that individual investors show preference for

companies with positive news coverage, even if this news conveys little new information (e.g.,

Huberman and Regev, 2001; Tetlock 2010). As a result, fund managers, whose compensation is

usually tied to assets under management, may have an incentive to include stocks with favorable

media exposure among their reported holdings. First, investors are more likely to be familiar with

these stocks and their recent performance. Second, stocks in the news may enable fund brokers to

pitch more effective stories about fund’s portfolio strategy and its winning picks, making them

more salient to potential investors. Both storytelling and the appeal to familiarity are extensively

used in other areas of mutual fund marketing, as shown in Cronqvist (2006) and Mullainathan and

Shleifer (2005). Moreover, anecdotal evidence from fund managers and investment consultants

also confirms the incentives for holding “hot” stocks and even acknowledges investors’ pressure

on some fund managers to establish these positions.2

To test the effect of media coverage on portfolio decisions of fund managers and

investment decisions of their investors, I construct a comprehensive media dataset, which includes

the text of nearly 700,000 daily news articles in major print publications and electronic sources

from 2000 to 2008. Using these data, I introduce several measures of stock salience, which

1 For example, Malkiel (1995) and Carhart (1997), among many others. 2 For instance, McDonald (2000) reports several quotes from fund managers regarding these incentives.

3

capture both the breadth of news coverage (i.e., number of articles) and the positive or negative

tone of each article. As a proxy for article tone, I compute the number of positive and negative

words defined according to the classification of words in an economic context developed in

Loughran and McDonald (2010). To capture the effect of positive news incremental to stock

returns, I also use orthogonalized measures of media coverage with respect to past performance

and other firm fundamentals.

My empirical results indicate that marketing incentives have a significant impact on

portfolio decisions of open-end funds. Stocks with more positive media coverage and greater

number of articles are more likely to be held by fund managers at reporting dates, controlling for

others stock fundamentals. On average, an increase of 10 percentile points (e.g., from 50th

percentile rank to 60th percentile rank) in the positive media coverage of a stock (measured as the

difference between the number of positive and negative articles about a firm in a quarter) increases

the odds ratio of a stock being held at a reporting date in a randomly chosen fund by 1.6%. The

preference for positive news is stronger at year-end, consistent with greater marketing incentives

at the end of the fiscal year – the most salient reporting date.

The positive media coverage of a stock is also associated with a higher probability of its

inclusion in the fund’s top 10 holdings – the subset of portfolio positions that is most widely

reported to investors and represents the most salient part of a fund’s portfolio. An increase of 10

percentile points in the positive media coverage rank of a stock increases the odds ratio of the

stock appearing among the fund’s top 10 holdings (vs. the rest of the portfolio) by 2.5%. In the

cross-section, the loadings on positive news are more prevalent among funds with a more

extensive marketing effort, as proxied by distribution expenses and load fees. By interacting fund

performance level and persistence, I find that funds with weaker or unstable past performance

have a greater preference for showing off stocks with positive media coverage.

Loadings on media-favored stocks have a significant positive impact on fund flows,

controlling for fund performance and other fund characteristics. However, the relationship

between portfolio tone and future flows appears to be concave and implies diminishing benefit of

this marketing strategy at higher levels of positive news. Moreover, media coverage of fund

holdings has a significant positive effect on flows over holdings’ past returns, suggesting that my

findings are unlikely to be explained by a momentum strategy followed by professional money

managers (Grinblatt, Titman, and Wermers 1995; Carhart 1997). To illustrate, for tone levels

below (above) the median, an increase in momentum-orthogonalized tone rank by 10 percentile

points results in an increase in the next-quarter flow by 45.5 (20.5) basis points. I further

4

distinguish between the effect of media tone and breadth of coverage. The evidence suggests that

the association between the positive media coverage of portfolio holdings and future flows is

approximately twice as strong (an increase in flows by 45.5 basis points vs. 22.3 basis points) if

the tone is measured by the difference between the number of positive and negative articles rather

than by their ratio. One possible interpretation of this evidence is that the breadth of news

coverage is critical for the positive articles to get noticed by investors.

While my empirical evidence is consistent with funds’ strategic behavior aimed at

increasing the appeal of their holdings to individual investors, I consider several alternative

explanations that could account for my results. First, it is possible that fund managers purchased

media-favored stocks before the release of positive news. In this case, loading on the stocks with

positive media coverage may reflect managerial skill in security selection rather than a strategic

response to investor preferences. Under this hypothesis, funds with a higher propensity to holding

stocks with positive media coverage should have higher returns in the concurrent quarter relative

to funds with a lower tilt toward stocks with positive news. However, the empirical evidence is

inconsistent with this interpretation, and, if anything, difference in performance between these two

groups goes in the opposite direction.

Second, it is possible that fund managers choose stocks with richer information flow to

minimize their search costs in portfolio construction (for example, as in Kacperczyk and Seru,

2007). Alternatively, fund managers may be subject to a similar bias toward attention-grabbing

stocks as that documented for retail investors in Barber and Odean (2008). To test these

alternatives, I evaluate the fraction of capital allocated to the most salient part of fund holdings –

the top 10 portfolio positions. If the loadings on media-covered stocks represent an effort of fund

managers to reduce their search costs, then the fraction of assets in the top 10 holdings (fund’s

largest positions) should be positively related to the amount of media coverage received by these

holdings, as managers establish larger positions in stocks where they have the lowest search costs.

In contrast, if loadings on media-covered stocks represent a strategic response to investor

preferences at reporting dates (and if establishing these positions is costly for the fund), we should

expect the opposite pattern for funds exploiting this strategy – namely, we should observe a

smaller fraction of assets concentrated in the top 10 holdings, just enough to push them over this

salience threshold. The empirical results show the latter pattern, in which the fraction of assets in

the top 10 holdings is negatively related to the loadings of the fund on media-covered stocks.

A third alternative hypothesis is a possible reverse causality between a fund manager’s

choice of stocks and stock media coverage. Under this interpretation, the selection of a stock by

some portfolio managers may induce additional media coverage of these stocks, particularly if

5

they are selected by high-profile fund managers whose stock picks are closely followed. To test

this explanation, I eliminate any qualified articles containing the words “holding”, “pick”,

“position”, and “fund manager”, as well as their variations. Overall, only about 1.4% of the

articles in my sample fit this criterion, and their elimination has no effect on quantitative or

qualitative results, suggesting that this explanation is unlikely to account for my findings.

The results of this study have several implications. First, the article provides one of the

first pieces of evidence on the role of media in mutual fund portfolio choice and documents the

importance of news coverage of fund holdings for attracting flows. Second, it appears that the

potentially irrational preferences of small investors have a tangible impact on the trading decisions

of professional money managers. Third, my results provide one possible explanation for the

tendency of mutual funds to deviate from market indexes – an explanation focused on increasing a

fund’s appeal to investors rather than improving performance.

The evidence in this paper is related to several areas of research. First, my results help

reconcile and connect two pieces of evidence in prior studies. In particular, Falkenstein (1996) has

shown that fund portfolios hold stocks with greater news coverage, and Chae and Lewellen (2004)

find that portfolio managers follow momentum strategies in foreign markets where momentum is

not profitable. My findings indicate that funds likely hold stocks with recent positive media

coverage in order to increase their appeal to investors rather than just follow momentum and that

this strategy has a significant positive effect on capital flows beyond that of holdings’ returns.

Second, this paper extends the literature on mutual fund portfolio disclosure and shows

that portfolio reporting can act as an effective marketing mechanism. Ge and Zheng (2006) find

that more frequent portfolio disclosure increases capital flows for funds with mediocre

performance, but has no effect on flows for well-performing funds. The results in my paper

provide a plausible explanation for this asymmetric relation. In particular, if the best-performing

funds have lower loadings on attention-grabbing stocks, the disclosure of their holdings is likely to

have lower incremental effect on flows beyond fund performance.

Third, this study contributes to the literature on information processing by mutual fund

investors. Previous research indicates that information salience has a strong impact on the

decisions of mutual fund investors. Klibanoff, Lamont, and Wizman (1998) find that a release of

salient information, such as a front-page article in The New York Times, dramatically increases

investors’ reaction to the changes in net asset values of closed-end funds. In another paper, Barber,

Odean, and Zheng (2005) show that mutual fund clients are sensitive to funds’ salient fees, such as

loads and commissions, but tend to overlook their less prominent characteristics, such as operating

6

expenses. My paper demonstrates the role of information salience in a new context – portfolio

holdings – and quantifies its impact on investment decisions of fund managers and their investors.

Finally, this study contributes to the research on financial media and mutual fund

marketing. Several papers have shown that advertising and media coverage of mutual funds have a

strong positive effect on fund flows (Jain and Wu, 2000; Gallaher et al., 2006; Kaniel et al.,

2007).3 However, these marketing techniques are often unavailable to the average fund manager

for two reasons. First, advertising decisions are made at the fund family level, and most families

advertise only one or two flagship funds. Second, only a small fraction of mutual funds receive

any media attention.4 This paper uncovers a new marketing mechanism employed at the level of

fund managers. It also demonstrates an alternative strategy used by mutual funds to benefit from

media exposure – establishing salient positions in stocks with positive news coverage.

The rest of this paper is organized as follows. Section 1 provides an overview of mutual

fund marketing. Section 2 describes the dataset and major variables. Section 3 presents empirical

results. Section 4 offers additional tests and robustness checks. The paper concludes with a brief

summary and a discussion of directions for future research.

1. Mutual Fund Marketing and Distribution

1.1 Overview and Prior Evidence

Open-end fund shares are typically distributed via one of the two main channels: (1) direct sales

from the mutual fund, and (2) sales through a broker or dealer (Bergstresser, Chalmers, and

Tufano, 2009).5 In my sample, broker-channel funds account for 43.2% of all assets under

management, 47.2% of all funds, and 76.4% of all share classes. Over the past decade, the portion

of broker-channel funds has somewhat declined, with 59.8% of new funds offered via the direct

channel. Nowadays, these two groups of funds divide the mutual fund universe into two roughly

equal parts according to the number of existing funds.

While some funds can be distributed via multiple channels and have more complex

distribution arrangements, the presence of a sales load generally serves as a good proxy for the

distribution model, with no-load funds distributed primarily via the direct channel and load funds

3 In particular, Jain and Wu (2000) and Gallaher et al. (2006) document a strong positive effect of advertising on fund flows, and Kaniel et al. (2007) show that funds featured in the media receive substantially greater capital inflows. 4 Kaniel et al. (2007) estimate that only about 19% of mutual funds receive any mentioning in the media in a given month. 5 This is a simplified classification that aggregates some smaller distribution channels with similar attributes. For example, the supermarket channel (online brokerages) and the institutional channel (direct transactions between funds and institutional investors) are included in the direct channel.

7

distributed largely via the broker channel (Gallaher, Kaniel, and Starks 2006). This is the proxy I

follow throughout the rest of this paper. I define no-load funds as funds whose shares have neither

a front nor a back load and which charge a 12b-1 fee of less than 50 basis points. The remaining

funds are classified as load funds.

No-load funds offered via the direct channel cater primarily to investors, who generally

know the type of the fund they are seeking. Correspondingly, direct-channel funds rely primarily

on advertising as their main marketing strategy, attempting to expose themselves to prospective

investors and thus enter their selection set. In this channel, investors carry out transactions directly

with mutual funds by mail, phone, or via customer service centers. As an example, Vanguard and

Fidelity are among representative fund families relying primarily on the direct channel.

In contrast, broker-channel funds are marketed to a somewhat less sophisticated clientele.

For example, according to the Investment Company Institute survey of mutual fund shareholders

(ICI 2004), customers purchasing funds through the broker channel tend to have lower median

income, smaller financial assets, and less education, with nearly half (43%) of the clients without a

four-year college degree. These clients often decide to purchase fund shares based on factors less

tangible than a fund’s expenses, manager’s alpha, or other common evaluation criteria. To

illustrate, Bergstresser, Chalmers, and Tufano (2009) find that investors in broker-channel funds

pay fees that are about twice as large as the fees of direct-channel funds, incur higher expense

ratios in excess of any load fees, and, most importantly, purchase funds that underperform direct-

channel funds even before fees. If these funds provide few tangible benefits, what strategies do

they use to attract new investors?

1.2 Fund Holdings and Salience Threshold

From the marketing perspective, the top holdings of open-end funds have two distinct features.

First, a fund’s top 10 portfolio positions (as measured by their weight in the portfolio) are

prominently displayed to prospective investors. To illustrate, many investor research services

focus on the top 10 positions of mutual fund portfolios. A similar emphasis in disclosure is

followed by mutual funds, which typically list their top ten holdings more prominently or even

separately on their web sites. Second, the information on the top holdings is often more up-to-date

than that on the remaining portfolio. The vast majority of the largest fund families update the list

of their top holdings once or twice a month, while their remaining portfolios are reported only

quarterly. 6 Therefore, the top 10 holdings often serve as the only source of the most up-to-date

6 For evidence in the financial press, see Dietz and McDonald (2000).

8

information on a fund’s portfolio available to a retail investor. Moreover, even when the full list of

holdings is disclosed by a fund, many funds provide the list of the top 10 positions in addition to

the full list of investments. As a result, while the difference in portfolio weights between, for

example, position 10 and position 11 may be marginal, the former is more salient to the

investment public.

Given the distinction in salience between the top ten holdings and the rest of a fund’s

portfolio, I conduct my analysis in two stages. First, I study the effect of positive media coverage

on the likelihood of a stock being included in fund portfolio at a reporting date. Second, for stocks

included in a fund portfolio, I examine the relation between media coverage and the inclusion of a

holding among in the more salient portfolio group – the top ten portfolio positions.

Previous research indicates that information salience has a strong impact on the decisions

of mutual fund investors in evaluating fund fees (Barber, Odean, and Zheng, 2005) and net asset

values (Klibanoff, Lamont, and Wizman, 1998). If prospective investors react to funds’ salient

features, does information salience matter for portfolio holdings? Do fund managers respond to

these incentives? These are the primary questions that motivate my empirical analysis.

2. Data and Variables

2.1 Open-End Funds

The data on the fund characteristics and performance come from the CRSP Mutual Funds

Database, and the data on fund holdings are collected from the Thompson/CDA Spectrum

database. To construct my sample of funds, I begin by excluding all non-equity funds (including

balanced and asset allocation classes), international funds, and index funds. Index funds are

excluded to eliminate the funds where portfolio managers have little discretion over active

allocation decisions. International funds are omitted because most foreign securities receive

relatively little media coverage in the U.S.

To address the incubation bias, I also exclude fund observations before the starting year

reported in CRSP, as well as any funds with a missing name or total net assets below $10 million.

Finally, I retain only funds focusing on large-cap stocks, as indicated by funds’ Morningstar

classification7. This restriction is imposed by the scope of my media dataset, which covers only

the S&P 500 stocks, a proxy for the stock universe for large-cap domestic equity funds. The time

period in my sample begins in 2000 and ends in 2008, also to match the duration of the data on

media coverage.

7 Specifically, Morningstar equity style is one the three: “Large Growth”, “Large Blend” or “Large Value”.

9

My final sample consists of 1,553 large-cap domestic equity funds, whose combined assets

under management in 2008 totaled $1.9 trillion. Of the 1,553 funds in my sample, 524 were

initiated between 2000 and 2008. During this sample period, an average (median) fund managed

$1.8 billion ($0.25 billion) in assets, charged an expense ratio of 1.27% (1.22%), and held 109

(70) stocks. Panel A of Table 1 provides summary statistics for the mutual fund sample.

I also collect a series of data about individual stocks in fund portfolios. Share price,

volume, stock returns, and other fundamentals are retrieved from CRSP. News coverage data are

collected from the Factiva Database.

2.2 Media Coverage

I start my media sample in 2000 to ensure sufficient coverage of media articles in the Factiva

database, which tends to be significantly sparser in earlier years. To collect articles and match

them to firms, I use a system of Intelligent Indexing Codes assigned by Factiva. In particular, if a

news article discusses a firm in sufficient detail, Factiva matches this article to the firm’s

intelligent indexing code. This approach ensures a more accurate match and higher relevance of

article content compared to key word searches. As an additional filter for article substance, I omit

articles with fewer than 50 words.

My list of news sources includes four U.S. newspapers with wide circulation: USA Today,

The Wall Street Journal, The New York Times, and The Washington Post (as in Fang and Peress,

2009), and one of the most popular electronic news wires – the Dow Jones News Wire. This set of

media sources is intended to provide a proxy for the information available to a typical U.S. mutual

fund investor both in print and online, since many web-based investor services offer free access to

the Dow Jones News Wire. All media coverage is measured at quarterly intervals to control for the

coverage of standard quarterly disclosures, such as earnings or dividends, and to match the

frequency of mutual fund portfolio reporting.

Panel B of Table 1 provides summary statistics on the news sources and stock media

coverage. My sample of news stories includes 673,187 articles, of which 78.5% appear in the Dow

Jones News Wire and 21.5% in print publications. Among the newspapers, the largest number of

stories (73,774 articles or 11.0% of the sample) come from The Wall Street Journal, followed by

The New York Times (40,085 articles or 6.0% of the sample). An average (median) firm in my

sample appears in 34.5 (12.0) articles per quarter. The amount of quarterly media coverage is

significantly right-skewed, and ranges from 1 to 1934 articles, with a standard deviation of 76.84.

10

Given the significant skewness in media coverage, I use the logarithmic transformation of the

number of media articles in regression analysis.

2.3 Measuring Media Coverage: Tone and Breadth

Previous research has shown that the positive or negative tone of news coverage has a significant

impact on investors’ perception of news (e.g., Tetlock 2007; Engelberg 2008; Tetlock et al. 2008;

Demers and Vega, 2010). To measure the tone of news coverage, I begin by identifying positive

and negative words in each article according to the classification of Loughran and McDonald

(2010) who provide a comprehensive list of words that are perceived as positive or negative in a

business setting. I then classify each article as either positive or negative based on the ratio of

positive to negative words in this article relative to the sample average in that quarter. More

specifically, for every article (articles are indexed by s, companies (stocks) are indexed by i, funds

are indexed by j, and time periods are indexed by t) I define the following dummy variable:

POSDUMMYs = 1 if (POSNEGRATIOs – mean POSNEGRATIO across all articles from the

same source in that quarter about other firms) > 0 and 0 if it is < 0, where POSNEGRATIOs

is the number of positive words divided by the number of negative words in article s.

The above variable is a relative measure of article tone, given the set of articles about all

firms in a specific quarter. This dummy variable is intended to provide a simple and replicable

proxy that addresses potential measurement issues associated with semantic analysis. For example,

it is unlikely that a particular article with a ratio of positive to negative words twice as high as that

in another article can be considered twice as favorable.

Next, I calculate measures of article tone for each company-quarter by introducing a

variable, which captures the fraction of positive news stories about the firm relative to all news

coverage of the company in that quarter. The variable is constructed as follows:

POSPERCit = NUMPOSARTICLESit / (NUMPOSARTICLESit + NUMNEGARTICLESit)

where NUMPOSARTICLESit (NUMNEGARTICLESit) is the number of positive (negative) articles

about company i in quarter t.

In addition to the fraction of positive articles, I also introduce a variable, which

incorporates the number of articles – a proxy for the visibility of a firm. This variable is motivated

11

by the assumption that a greater number of articles increase the salience of a firm to potential

investors and extend the reach of positive or negative news about a given stock. This measure is

constructed as the difference between the total number of positive and negative articles about a

firm in a given quarter:

POSNUMit = NUMPOSARTICLESit – NUMNEGARTICLESit

To specify an appropriate set of controls in measuring media coverage, I begin by estimating a

panel regression of media coverage variables on an array of firm characteristics. The model is

estimated over the period from 2000 to 2008 for the stocks, which were included in the S&P 500

index in any year during the sample period. The dependent variables include measures of media

tone, POSPERC and POSNUM, as defined above. The independent variables include firm size,

quarterly return, market-to-book ratio, stock illiquidity, firm age, and volatility:

POSPERCit (logPOSNUMit) = β1logSIZEit + β2MOMit + β3logMTBit + β4logILLIQit +

β5logAGEit + β6VOLATILit +

T...1t

tt DUMMYT + εit (1)

where logPOSNUMit is defined as sign(POSNUMit)*log(1+|POSNUMit|) to reduce the skewness of the

original variable, logSIZEit is the natural log of the company’s market capitalization at the end of

quarter t, MOMit is the market-adjusted stock return over quarter t, logMTBit is the natural log of

the market-to-book ratio at the end of quarter t, logILLIQit is the natural log of the Amihud

illiquidity measure for the stock multiplied by 1,000, logAGEit is the natural log of the time (in

years) since the initial listing of the stock, and VOLATILit is the monthly volatility of stock returns

estimated over the last 36 months.

The estimation results are summarized in Table 2. The evidence indicates that both tone

measures are negatively related to size, suggesting that smaller companies tend to receive more

favorable coverage. One interpretation of this result is that smaller companies find it easier to

conceal bad news from the public. An alternative interpretation is that media sources are more

likely to report scandalous or infamous news about larger firms. As expected, the relation between

momentum and the tone of media coverage is always positive and highly significant in all

specifications, indicating that favorable news is strongly positively associated with past stock

returns. The association between the market-to-book ratio and media tone is also positive and

significant, suggesting that companies with higher growth prospects tend to have more positive

12

news coverage. Finally, stock illiquidity and firm age do not appear to be significantly related to

the tone of news.

The results in Table 2 demonstrate that the tone of a firm’s news coverage is significantly

related to stock characteristics. To distill the effect of media coverage from firm fundamentals, I

develop several measures of news tone based on the residuals generated from cross-sectional

regressions. In each quarter, a positive or negative residual for a particular stock provides an

estimate of the relatively positive or negative media coverage of this firm compared to the

predicted value based on the stock’s fundamental characteristics. To standardize these values and

to limit the impact of outliers, I measure the tone of a firm’s news exposure as a percentile rank of

its residual from model (1) relative to the residuals of all other stocks in the S&P 500 in that

quarter. The tone rank ranges from 0 to 1, such that the firm with the highest ε (most positive

media tone) is assigned 1 and the company with the lowest ε (most negative media tone) is

assigned 0. The measure thus defined possesses several desirable attributes. First, it is largely

independent of the residual distribution, a property that helps to address the skewness in raw

media coverage and standardizes the aggregation of results from funds with different investment

styles (e.g. large-growth vs. large-value). Second, the percentile rank accounts for the time-series

variation in the overall tone of media articles across all stocks in my sample. Finally, this measure

facilitates the intuitive interpretation of results and their economic significance.

To perform orthogonalization, I consider two sets of independent variables. One set

includes all stock characteristics that came out significant for at least one measure of tone: size,

momentum, MTB, and volatility. The second set of variables excludes stock returns. It can be

argued that stock returns are a sufficient statistic for positive or negative news, since all relevant

public news should be reflected in stock prices. On the other hand, it is possible that the tone of

financial media has an impact on investment decisions that is incremental to the information

contained in stock prices (for example, as in Tetlock 2007; Tetlock et al. 2008; and Demers and

Vega, 2010). This distinction is important, since previous research has shown that mutual funds

tend to follow momentum strategies (e.g., Grinblatt, Titman, and Wermers 1995; Carhart 1997).

Therefore, I consider tone measures incorporating and independent of returns to capture the role of

media sentiment on mutual fund portfolio choice, if any, over and above these well-documented

investment strategies.

Formally, I introduced the following measures of media tone and coverage orthogonalized

with respect to stock fundamentals:

13

POSPERCRANKPUREit = ranked POSPERCit orthogonalized wrt to {size, MTB,

volatility, past return}

POSNUMRANKPUREit = ranked POSNUMit orthogonalized wrt to {size, MTB, volatility,

past return}

POSPERCRANKMOMit = ranked POSPERCit orthogonalized wrt to {size, MTB,

volatility}

POSNUMRANKMOMit = ranked POSNUMit orthogonalized wrt to {size, MTB, volatility}

3. Empirical Evidence

In this section, I analyze the relationship between a firm’s news coverage, portfolio decisions of

fund managers, and investment decisions of mutual fund investors. There are several possible

reasons why news coverage may be important in portfolio decisions.

First, it is possible that fund managers possess skills in security selection and pick stocks

with the sole objective of creating value for their investors. In each period, these managers identify

underpriced stocks, purchase them before they appreciate, and hold them until the reporting date.

As these stocks grow in value, they attract positive media coverage. As a result, the end-of-period

portfolios appear to be loaded on positive-tone stocks, although the media coverage itself was not

a factor in the selection of these securities. Under this hypothesis, a fund’s tilt toward stocks with

high media coverage should be positively related to fund returns in the quarter of observation.

Second, it is possible that fund managers do not possess superior stock-picking skills, but

rather follow news from the media when deciding on their portfolio composition. Under this

interpretation, fund managers select securities with higher media coverage to minimize their

information search costs rather than to cater to their investors. In this case, it is unlikely for the

relationship between the tilt toward media-favored stocks and future fund flows to be strong. If

funds do not incorporate preferences of their clientele into their investment decisions, investors are

unlikely to respond to this strategy with additional flows.

Finally, I consider an explanation rooted in marketing incentives of mutual funds. Fund

managers might recognize media sentiment as irrelevant for future stock returns but still regard

positive-tone stocks as desirable investments. As long as individuals are willing to invest more

into funds holding stocks with favorable coverage, loading up on stocks with positive news is a

viable marketing strategy that can increase future flows. Another prediction generated by this

hypothesis concerns the salience of different positions in the fund portfolio. If managers’ goal is to

emphasize the presence of favorably described stocks in their portfolios, they are more likely to

14

include these stocks among the holdings that are widely reported to the investment public. As a

result, we should expect a strong positive association between the positive media coverage of a

stock and the probability that this stock is included in a fund’s top 10 holdings.

3.1 Media Coverage and Stock Position in the Portfolio

I begin by studying how the variables of media coverage affect funds’ decisions to hold stocks at

the end of the concurrent quarter. To this effect, I run a logit regression across stock-fund-quarters

where the dependent variable HOLDijt is a dummy equal to 1 if fund j held stock i at the end of

quarter t. The estimated model is as follows:

Prob(HOLDijt) =F(β1TONEit + β2HOLDijt-1 +

Tt

tt DUMMYT...1

+ εijt) (2a)

The results of this regression are reported in Table 3, Panel A. The evidence indicates that

all four measures of tone are positively related to the probability that the stock is held by a

randomly chosen fund. However, the results for the measures based on the fraction of positive

articles (POSPERCRANKPUREit and POSPERCRANKMOMit) are marginally significant, while

those for the measures based on the difference between positive and negative articles are much

stronger. This pattern suggests that funds base their decisions to hold the stock not only on how

favorably the company is described by the media but also on how widely this stock is covered.

This result is consistent with the marketing-based explanation for funds’ preference for stocks

with positive media coverage since positive news is more likely to be known to a larger number of

potential investors. On the other hand, if funds simply relied on the tips from the media to pick

stocks, we would expect the fraction of positive articles to work just as well or better than the

difference.

Furthermore, the results are stronger for tone measures not orthogonal to momentum.

Improvement in the POSNUMRANKMOM (momentum-dependent tone) of the stock by 10

percentiles increases the odds ratio of the stock appearing in the portfolio by a factor of 1.028

(exp(0.2749*0.1)) or by 2.8%. To compare, improvement in the POSNUMRANKPURE (tone

orthogonal to momentum) of the stock by 10 percentiles increases the odds ratio by a factor of

1.016 (exp(0.1583*0.1)) or by 1.6%. These results suggest that part of the marketing strategy

involves picking stocks with high past returns, although the residual predictive power of

momentum-orthogonalized measures is also significant. Since past return cannot fully explain why

funds are more likely to invest in stocks that received positive coverage, the observed preference

15

for tone is not a mechanical by-product of the funds’ timing of trades. If portfolio tone only

reflected the fact that funds had invested in the stock before it appreciated, the orthogonalized

measure would not matter for the probability of the stock appearing in the portfolio.

In Table 3, Panel B, I test whether more positive news coverage of a stock is associated

with a higher probability of the stock’s inclusion in the top 10 holdings. Since the top 10 positions

of funds are reported more saliently to prospective investors, the marketing-based hypothesis

would predict that favorably-covered stocks are more likely to be included in this portfolio subset.

This analysis is performed conditionally on the stock being held in the portfolio. In other words, I

consider stock-fund pairs in which the fund held the stock at the end of the quarter. I define

variable TOP10ijt to equal 1 if stock i’s rank (based on portfolio weight) among all the stocks in

fund j’s portfolio was between 1 and 10 at the end of quarter t and 0 otherwise. In the end, I

estimate the following model:

Prob(TOP10ijt) =F(β1TONEit + β2TOP10ijt-1 +

Tt

tt DUMMYT...1

+ εijt) (2b)

Comparing the results from Panel A and Panel B, we observe that the top 10 effect is

stronger than the holding effect for three of the four measures. To illustrate, an increase in the

POSNUMRANKPURE by 10 percentile points increases the odds ratio of the stock appearing in

the top 10 positions by a factor of 1.025 (exp(0.2502*0.1)) or by 2.5%. This is larger than the

increase in the odds ratio of the stock appearing in the portfolio (1.6%). In other words, funds

prefer to include favorably covered stocks in their portfolios. Moreover, conditional on a stock

being purchased by a fund manager, the stock’s positive news coverage has an even stronger effect

on the probability of inclusion in the most salient part of a fund’s portfolio. This propensity of

funds to report media-favored stock among their most salient holdings speaks in favor of the

marketing hypothesis.

3.2 Fund Characteristics and Loadings on Stocks with Positive News

After providing evidence on the relation between a stock’s media coverage and its position in a

fund’s portfolio, I investigate the cross-sectional determinants of the strength of this relationship.

To capture the preference of fund j for stocks with a positive tone of media coverage in quarter t, I

define portfolio tone as the weighted average of tone measures of stocks that compose the

portfolio:

16

∑∈ji

itijtTONEwTONEjt =

where wijt is the weight of stock i in portfolio j at the end of quarter t and TONEit is one of the four

stock tone measures defined above.

The set of independent variables includes an array of fund characteristics, such as measures

of size, performance, investment style, and fund family attributes. In addition to these standard

variables, I also include several measures that proxy for the fund’s marketing effort. If the

inclusion of stocks with positive media coverage is motivated by marketing incentives, this

strategy may be more important for funds with greater expenditures on marketing and distribution.

On the other hand, a tilt toward media-favored stocks may serve as a substitute for other marketing

tactics. To distinguish between these hypotheses, I include 12b-1 fees and load dummies among

the independent variables.

Further, if managers’ allocations to high-visibility stocks are driven by marketing motives

rather than stock fundamentals, funds with the strongest tilt towards attention-grabbing stocks

would likely have a smaller concentration of assets in their top holdings in an effort to minimize

the constraints of this strategy on their portfolio choice and reduce the costs associated with

establishing these positions. In contrast, according to the alternative hypotheses, managers should

allocate larger weights to their top picks if these holdings are selected based on skill (i.e.

purchased before positive news is released) or if these stocks are purchased to minimize overall

search costs for portfolio holdings (since holding more concentrated portfolios would reduce the

number of stocks that need to be researched). To test these predictions, I include the percentage of

fund assets in the top 10 holdings as one of the independent variables. Finally, the marketing

hypothesis predicts that the loading on stocks with positive media coverage is likely to be stronger

at the end of the year – the most salient reporting date. In contrast, there seems to be no clear

reason this prediction should hold under any alternative explanations. Formally, I test the

following regression model:

TONEjt = βXjt +

Tt

tt DUMMYT...1

+ εjt (3)

Vector Xjt of independent variables includes RETjt (fund j’s net-of-fees return in quarter t),

LOADj (dummy variable equal to 1 if fund j charges a front-end or a back-end load in any of its

share classes), GROWTHj (dummy variable equal to 1 if fund j is assigned the Morningstar style of

Large Growth), VALUEj (a dummy variable equal to 1 if fund j is assigned the Morningstar style

17

of Large Value), DISTRFEEj (the 12b-1 fee proxying for the fund’s marketing expenses),

TOP10FRACTIONjt (the aggregate weight (reported in decimals) of the top 10 positions in fund j’s

portfolio at the end of quarter t), YEARENDt (dummy variable equal to 1 if quarter t is the last

quarter of the year), PERFRANKYEARjt (rank of fund j in the year-to-date in-style tournament in

which funds compete on raw net-of-fees returns; the rank is normalized to between 0 and 1 where

1 corresponds to the winner fund), PERFRANKPASTjt (average quarterly rank of fund j in the in-

style tournament over the last 12 quarters), PERFPERSISTjt (minus standard deviation of fund j’s

quarterly in-style ranks over the last 12 quarters), FAMAGEjt (dummy variable equal to 1 if fund

j’s family’s age at the end of quarter t is above the median among all mutual fund families),

FAMSIZEjt (dummy variable equal to 1 if fund j’s family TNA at the end of quarter t is above the

median TNA among all mutual fund families), and STARFAMjt (dummy variable equal to 1 if fund

j’s family has at least one fund with a three-year aggregate net return in the top 5% of its

Morningstar style). I also interact PERFRANKPASTjt and PERFRANKPASTjt to check if funds

with stable history of strong performance have a weaker preference for tone.

The results of this regression are reported in Table 4. Most of the results consistent with

the marketing hypothesis are concentrated in the two measures of tone that are based on the

difference between the number of positive and negative articles. As expected, for tone variables

not orthogonal to momentum, portfolio tone is positively related to fund return in the observation

quarter. This finding suggests that high portfolio tone is partially a result of well-timed trades.

However, for tone measures independent of past return, I observe the opposite effect: the portfolio

tone is higher if the fund return is lower. A 1% drop in fund quarterly return increases the portfolio

tone by 1.5 percentiles. In other words, if a stock is portrayed optimistically by the media but does

not experience growth, it remains a desirable investment, more so for funds with weaker

performance.

I further investigate the relationship between fund past performance and tone by

considering each fund’s year-to-date in-style rank as well as its average tournament rank over the

last three years. The year-to-date performance doesn’t appear to have a sizable effect on tone

while the level effect of the long-run performance is weakly negative. However, performance

persistence amplifies the effect of the average rank on portfolio tone: among funds with low

volatility of rank those that have high performance have low portfolio tone. A reduction of 10

basis points in the standard deviation of fund monthly return increases the effect of past ranking

by 0.374. To compare, the raw effect of past ranking at zero fund return volatility is 0.525. This

18

result is consistent with the intuition that skilled managers who deliver stable results are unlikely

to engage in portfolio-based marketing.

Controlling for the performance effect, a tilt toward stocks with positive media coverage is

higher for funds charging a load and for funds with higher distribution expenses – funds with a

more aggressive marketing strategy. Notably, the aggregate weight of the top 10 positions of a

high-tone fund is smaller than that of a low-tone fund. This result is inconsistent with the

alternative hypothesis that stocks with favorable coverage represent fund managers’ best bets and

are selected for their growth potential. I also find that portfolio tone is generally higher at the end

of the year. This result provides indirect evidence in support of the marketing hypothesis since

more investor attention is directed at fund year-end reports than at interim quarterly reports.

Finally, family-level variables do not appear to have a significant impact on the funds’ tilt toward

media-favored stocks.

Overall, my findings support the conjecture that funds hold stocks with more positive (less

negative) portrayal by the media to make their portfolios more appealing to individual investors.

In the next section, I analyze the efficacy of this strategy for attracting capital flows.

3.3 Capital Flows and Media Coverage of Fund Holdings

It is likely that the relationship between media coverage of fund holdings and capital flows is non-

linear. Indeed, the incremental effect of media-based marketing may diminish at higher loadings,

when most investors become aware of the firms’ recent news, key developments, and

performance. It is also possible that at high loadings on media-favored stocks, this strategy

imposes significant costs, both explicit (such as trading expenses), and implicit (such as possible

reputation damage). To test for possible non-linearity, I estimate the following continuous piece-

wise linear regression:

FLOWjt = βLTONELOWjt-1 + βHTONEHIGHjt-1 + βCXjt +

Tt

tt DUMMYT...1

+ εjt (4)

The main dependent variable is FLOWjt defined as

FLOWjt = (TNAjt+1 – (1+RETjt) * TNAjt-1) / TNAjt-1

19

To ensure against outliers and rogue observations, I exclude all fund-quarters for which the

value of this variable is lower than -0.9 or higher than 3.0. The main independent variables of

interest are TONELOWjt-1 and TONEHIGHjt-1 defined as follows for each of the four measures of

portfolio tone:

TONELOWjt-1 = TONE jt-1, if TONE jt-1 ≤ MTONEt-1; MTONEt-1, if TONE jt-1 >

MTONEt-1

TONEHIGHjt-1 = 0, if TONE jt-1 ≤ MTONEt-1; TONE jt-1 – MTONEt-1, if TONE jt-1 >

MTONEt-1

where MTONEt-1 is the median TONE jt-1 in quarter t-1 of all funds in my sample. By defining the

two components of tone in this way, I force OLS to fit a continuous piece-wise linear

specification.

Vector of control variables Xjt includes: RETLOW jt-1 and RETHIGH jt-1 (to account for the

convexity in the flow-performance relationship, these variables are defined as follows: each fund

is assigned a rank between 0 and 1 on the basis of its net return in quarter t-1 among all the funds

from the same Morningstar style, this rank is then transformed into piece-wise linear components

to account for non-linearity in the flow-performance relationship: RETLOW = {RETRANK, if

RETRANK ≤ 0.5; 0.5, if RETRANK > 0} and RETHIGH = {0, if RETRANK ≤ 0.5; RETRANK –

0.5, if RETRANK > 0}), STDEVjt (standard deviation of fund j’s monthly net return over the last

36 months), logFUNDTNAjt (natural log of fund j’s TNA at the end of quarter t), NEWFUNDjt

(dummy variable equal to 1 if there is less than 365 days between the end of quarter t and fund j’s

initiation date), DISTRFEEj (the 12b-1 fee proxying for the fund’s marketing expenses),

logFAMILYTNAjt (natural log of aggregate TNA of fund j’s family at the end of quarter t),

logFAMILYAGEjt (natural log of the age (in years) of fund j’s family at the end of quarter t),

STARFAMjt (dummy variable equal to 1 if fund j’s family has at least one fund with a three-year

aggregate net return in the top 5% of its Morningstar style), STYLEFLOWjt (weighted average of

FLOWjt across all funds belonging to the same Morningstar style as fund j), and FLOWjt-1 (fund j’s

flow over the previous quarter).

Table 5 contains the results. Controlling for the effect of past performance on flows (which

is always positive), I observe that funds loading up on stocks with positive tone experience higher

future flows but that the efficacy of this strategy levels off as the portfolio becomes more loaded

on stocks with positive news. For two out of four measures, coefficient on TONEHIGH is

20

insignificant while the coefficient on TONELOW is significant across all specification. The results

are stronger for the measures based on the net number rather than the percentage of positive

articles. To illustrate, at below-median tone level, an increase in TONEPOSPERCRANKPURE by

10 percentiles increases next-quarter flow by 22.3 basis points. Correspondingly, an increase in

TONEPOSNUMRANKPURE by 10 percentiles causes next-quarter flow to go up by 45.5 basis

points. In this analysis, I see little difference between the measures clean and not clean of

momentum. This is unsurprising, since the component of flows attributable to past performance as

well as the non-linearity of this relationship are effectively captured by the piece-wise linear

controls for past return.

Overall, I observe that more positive (less negative) portfolio tone is associated with higher

future flows and that this effect diminishes as the portfolio tone increases. As discussed, this result

may indicate explicit and implicit costs of displaying holdings with positive news. Alternatively, it

is possible that this strategy becomes less credible at high levels, unless supported by the actual

fund performance.

3.4 Media Coverage of Fund Holdings and Future Performance

In this section, I test whether a tilt toward stocks with positive news coverage has any predictions

for future fund performance. There are several possible reasons why this strategy may affect fund

performance.

First, media tone can signal that the stock is fundamentally good and has high growth

potential. In this case, there is no conflict between the marketing-based choice of holdings and the

value creation objectives, and funds with stronger preference for stocks with positive media

coverage should exhibit higher future returns. Second, it is possible that favorable press induces an

overreaction in the market, which causes prices of some high-tone stocks to rise above their

fundamental values and experience a correction thereafter (e.g., Huberman and Regev, 2001;

Barber and Odean 2008). In this case, holding these stocks is detrimental to fund future

performance. However, given the well-established convex relationship between fund performance

and flows (e.g., Sirri and Tufano, 1998), funds may still pursue this strategy, if the flows generated

by this strategy exceed the capital attrition from its cost on performance. Finally, the tilt toward

media-favored stocks may have no relationship with performance, unless media coverage can

predict future performance.

In this section, I use portfolio analysis to investigate the relationship between a tilt toward

media-covered stocks and future fund performance. Each quarter, I sort funds into four bins by

21

each of the tone measures and consider equal-weighted bin portfolios as well as the long-short

portfolio. In all cases, bin 1 corresponds to low values of tone, while the long-short portfolio goes

long in bin 4 and short in bin1.

Table 6 reports average monthly return and four-factor alphas for each of the portfolios.

The relationships between funds’ loadings on media-covered stocks and fund future returns are

generally weak, at least for my measures of media coverage. Loading up on momentum-dependent

(independent) tone seems to be associated with weak positive (negative) return but this result is

neither statistically nor economically significant.

4. Robustness and Alternative Measures

4.1 Positive vs. Negative News Coverage

In the previous sections I documented that 1) funds can increase their future flows by holding

more (less) stocks with optimistic (pessimistic) coverage, and 2) the tone matters more if it is

measured by the net number of positive articles rather than the percentage. Notably, since all my

tone measures have been defined in relative terms via the net positive effect, these results can be

interpreted as being driven both by more optimistic tone and less pessimistic tone. In this section, I

attempt to distinguish the two effects by considering positive and negative tone separately. In both

cases I focus on the number of articles as it appears to play a significant role in managers’

incentives and their portfolio composition decisions

I begin by orthogonalizing NUMPOSARTICLESit and NUMNEGARTICLESit with respect

to size, market-to-book, volatility, and momentum and ranking the residuals as before. This way I

arrive at the two measures: POSTONEit and NEGTONEit. Next, I rerun the logit analysis (2a) and

(2b) separately for each of these measures. To facilitate the interpretation of the results, I include

variable NEGTONE with a minus so that an increase in this variable would correspond to an

improvement in tone.

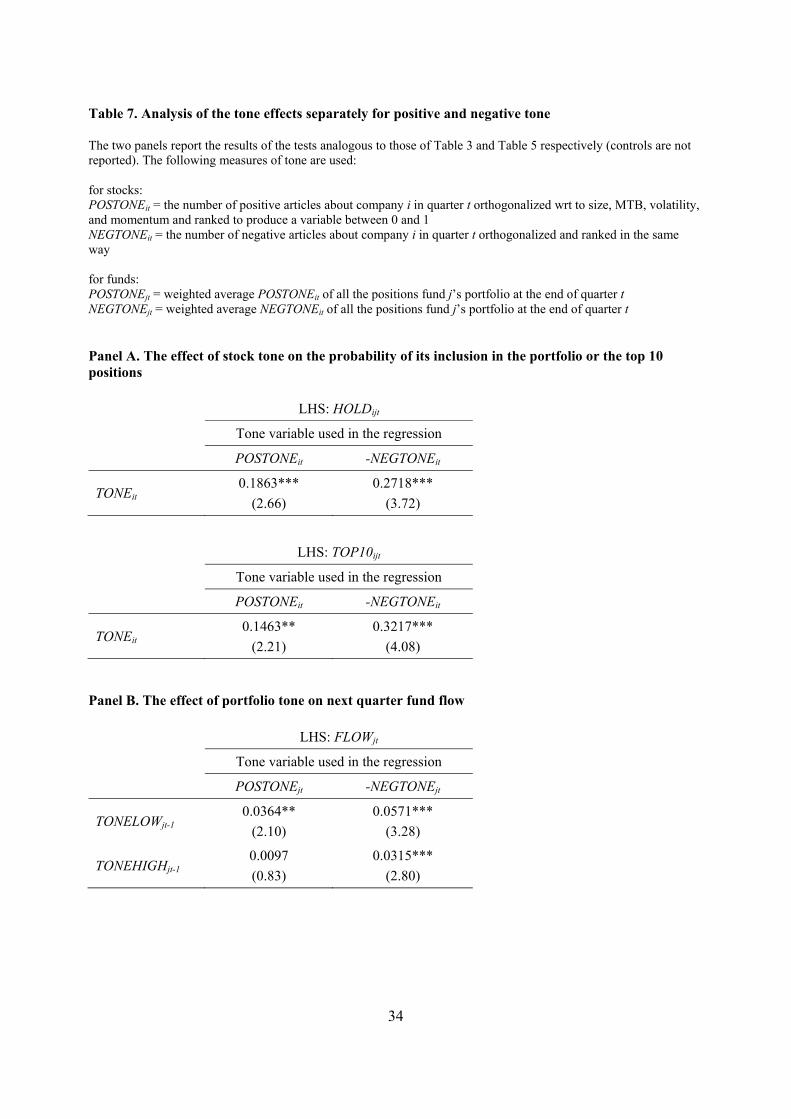

Table 7, Panel A contains the results from the logit regressions. Compared to an increase in

positive tone, a reduction in negative tone has a stronger effect both on the inclusion of the stock

in the fund’s portfolio and on its appearance in the fund’s top 10 holdings. The difference is more

apparent for the top 10 effect, i.e. funds benefit significantly from excluding stocks with bad

publicity from the most salient fraction of their portfolios. Increase (decrease) in the positive

(negative) tone rank of the stock by 10 percentiles increases the odds ratio of the stock appearing

in the top 10 positions by 1.46% (3.21%).

22

I also rerun the flow regression (4) separately for positive and negative portfolio tone

calculated, respectively, as the weighted averages of POSTONEit and NEGTONEit of stocks held

by the fund. The results of this analysis, reported in the Panel B of Table 7, prompt two

conclusions. First, a reduction in negative tone has a stronger effect on future flows than an

increase in positive tone. Second, increasing positive tone becomes ineffective at higher levels (as

the portfolio becomes saturated with optimistically viewed stocks) while reducing negative tone

remains an effective device even when the portfolio already contains few pessimistically viewed

stocks. At below-median (above-median) level, the reduction in negative tone rank of 10

percentiles results in an increase in the fund’s next-quarter flow of 31.5 (57.1) basis points.

4.2 Alternative Measure of Holdings Media Coverage

In Section 3.2, I defined a measure of portfolio tone as the weighted average of tones of stocks

held in the portfolio. One potential issue with this measure is that some funds can exhibit stronger

preference for media-covered stocks as a result of fund-specific trading strategies correlated with

media coverage, but unrelated to marketing incentives.

In this section, I consider a fund-specific measure that controls for fund style and exploits

only the variation in the salience of fund holdings. Specifically, I define portfolio tone tilt as the

difference between the average tone of the top 10 positions and the average tone of the rest of the

portfolio. This measure compares the preference for stocks with positive media coverage at

reporting dates between the more salient and less salient part of the portfolio.

If the tilt toward media-favored stocks reflects a marketing strategy employed by mutual

funds, we should expect the salient top 10 holdings to have more positive media tone (i.e. a

positive value of the tilt). In contrast, if preference for media-covered stocks is a result of an

omitted variable correlated with a fund’s trading strategy, there is little reason to expect a

significant difference between the positivity of the news coverage of top holdings and the rest of

the portfolio, controlling for other factors. Even if the control variables are imperfect, if anything,

we should see a negative tilt, since larger stocks tend to have a smaller fraction of positive news

(as shown in Table 2). Formally, I define an alternative measure of portfolio tilt as follows:

TONETILTjt = average TONEit of positions 1 to 10 – average TONEit of positions 11 to Njt,

where Njt is the number of stocks in the portfolio of fund j in quarter t

23

Next, I rerun regression (3) using portfolio tone tilt on the left-hand side. The results (not

tabulated) are qualitatively similar for the main variables as those to those for the weighted

average tone, with two notable differences. First, the results for the tone measures based on the

percentage of positive articles are weaker, while those for the measures based on the number of

articles are stronger. Second, the effect of the average historical tournament rank is significant at

1%, while its interaction with the performance persistence is not. With respect to the association

between fund’s marketing incentives and other fund characteristics, this variable generates the

similar qualitative conclusions.

24

Conclusion

I examine the impact of marketing incentives on mutual fund portfolios and argue that mutual

funds capitalize on the limited attention of small investors by establishing positions in stocks with

high visibility and positive news coverage to increase funds’ appeal to retail clientele. This

strategy has a positive effect on flows, controlling for fund characteristics and holdings’ past

returns. The extent of loading on media-covered stocks varies across the fund universe and is more

pronounced among funds that charge a load, spend more on direct marketing, and do not show a

stable pattern of strong performance.

Overall, the evidence in this paper suggests that the emphasis of investor research services

on portfolio disclosure does not always paint an accurate picture of a fund’s trading strategy.

Furthermore, this emphasis itself generates a strategic response from funds seeking to increase

their marketing appeal.

The results in this study could be extended in several directions. First, I do not distinguish

between the content of media stories and rely on an arguably noisy classification of news based on

textual analysis. In future research, it would be useful to analyze how investor reaction varies with

the subject matter of the article and what kind of news coverage generates the strongest investor

response. Second, it is promising to explore whether the pursuit of stocks with positive news

coverage before reporting dates contributes to fund herding behavior documented in the literature

(e.g. Wermers, 1999, among others). These directions offer new avenues for expanding our

understanding of the connection between the incentives of mutual fund managers and their

investment decisions.

25

References

Amihud, Yakov, 2002, “Illiquidity and Stock Returns”, cross-section and time-series effects, Journal of Financial Markets, 5, 31-56. Barber, Brad and Terrance Odean, 2008, “All that Glitters: The Effect of Attention and News on the Buying Behavior of Individual and Institutional Investors”, Review of Financial Studies, 21, 785-818. Barber, Brad, Terrance Odean, and Ning Zhu, 2010, “Do Noise Traders Move Markets?”, Review of Financial Studies, forthcoming. Barber, Brad, Terrance Odean, and Lu Zheng, 2005, “Out of Sight, Out of Mind: The Effects of Expenses on Mutual Fund Flows," Journal of Business, 60, 1983-2011. Bergstresser, Daniel, John Chalmers and Peter Tufano, 2009, “Assessing the Costs and Benefits of Brokers in the Mutual Fund Industry,” Review of Financial Studies, 22, 4129-4156. Bris, Arturo, Huseyin Gulen, Padma Kadiyala, and Raghavendra Rau, 2007, “Good Stewards, Cheap Talkers, or Family Men? The Impact of Mutual Fund Closures on Fund Managers, Flows, Fees, and Performance”, Review of Financial Studies, 20, 953-982. Carhart, Mark, 1997, “On Persistence in Mutual Fund Performance”, Journal of Finance, 52, 57 – 82. Chae, Joon and Jonathan Lewellen, 2005, “Herding, Feedback Trading, and Stock Returns: Evidence from Korea”, working paper, Dartmouth College. Cronqvist, Henrik, 2006, “Advertising and Portfolio Choice”, working paper, Claremont McKenna College. Del Guercio, Diane, and Paula Tkac, 2002, “The Determinants of the Flows of Funds of Managed Portfolios: Mutual Funds vs Pension Funds”, Journal of Financial and Quantitative Analysis, 37, 523-558. Del Guercio, Diane, and Paula Tkac, 2008, “The Star power: the effect of Morningstar Ratings on Mutual Fund Flows”, Journal of Financial and Quantitative Analysis, 43, 907-936. Demers, Elizabeth A., and Clara Vega, 2010, “Soft Information in Earnings Announcements: News or noise?” working paper, INSEAD and Federal Reserve Board. Dietz, David and Ian MacDonald, “What's the Big Secret About Mutual Fund Holdings?”, The Street.com, April 26, 2000. Ellison, Glenn and Judith Chevalier, 1997, “Risk Taking by Mutual Funds as a Response to Incentives”, Journal of Political Economy, 105, 1167-1200. Engelberg, Joseph E., 2008, “Costly Information Processing: Evidence from Earnings Announcements”, working paper, University of North Carolina. Fang, Lily and Joel Peress, 2009, “Media Coverage and the Cross-Section of Stock Returns”, Journal of Finance, 64, 2023-2052. Falkenstein, Eric, 1996, “Preferences for Stock Characteristics as Revealed by Mutual Fund Portfolio Holdings,” Journal of Finance, 51, 111-135.

26

Ge, Weili, and Lu Zheng, 2006, "The Frequency of Mutual Fund Portfolio Disclosure," working paper, the University of Michigan. Gallaher, Steven, Ron Daniel, and Laura Starks, 2006, “Madison Avenue Meets Wall Street: Mutual Fund Families, Competition, and Advertising”, working paper, University of Texas at Austin and Duke University. Grinblatt, Mark and Tobias Moskowitz, 1999, “Do Industries Explain Momentum? Journal of Finance, 54, 1249–1290. Grullon, Gustavo, George Kanatas, and James P. Weston, 2004, “Advertising, Breadth of Ownership, and Liquidity”, Review of Financial Studies 17, 439–461. Huberman, Gur, 2001, “Familiarity Breeds Investment”, Review of Financial Studies, 14, 659–680. Huberman, Gur and Tomer Regev, 2001, “Contagious Speculation and a Cure for Cancer: A Non-Event that Made Stock Prices Soar,” Journal of Finance, 56, 387-396. Investment Company Institute, 2004. Profile of Mutual Fund Shareholders, Investment Company Institute Research Series. Jain, Prem and Joanna Shuang Wu, 2000. “Truth in Mutual Fund Advertising: Evidence on Future Performance and Fund Flows“, Journal of Finance, 55, 937–958. Kaniel, Ron, Laura Starks, and Vasudha Vasudevan, 2007. “Headlines and Bottom Lines: Attention and Learning Effects from Media Coverage of Mutual Funds”, working paper, Duke University and the University of Texas at Austin. Kacperczyk, Marcin and Amit Seru, 2007. “Fund Manager Use of Public Information: New Evidence on Managerial Skills”, Journal of Finance, 62, 485-528. Kacperczyk, Marcin, Clemens Sialm, and Lu Zheng, 2008, “Unobserved Actions of Mutual Funds”, Review of Financial Studies, 21, 2379-2416. Klibanoff, Peter, Owen Lamont, and Thierry Wizman, 1998 “Investor Reaction to Salient News in Closed-End Country Funds”, Journal of Finance, 53, 673-699. Lakonishok, Josef, Andrei Shleifer, Richard Thaler, and Robert Vishny, 1991, “Window Dressing by Pension Fund Managers,” American Economic Review, Papers and Proceedings, 81, 227-231. Loughran, Tim and Bill McDonald, 2010, “When is a Liability not a Liability? Textual Analysis, Dictionaries, and 10-Ks”, Journal of Finance, forthcoming. Malkiel, Burton G., 1995, “Returns from Investing in Equity Mutual Funds 1971 to 1991,” Journal of Finance, 50, 549-72. McDonald, Ian, 2000, "A Must to a Bust: Scores of Funds Get Burned on Big Qualcomm Bets", The Street.com, June 15, 2000. Moeller, Steven, 1999, Effort-Less Marketing for Financial Advisors, Business Visions Publishing. Mullainathan, Sendhil and Andrei Shleifer, 2005, “Persuasion in Finance”, working paper, Harvard University.

27

Murray, Nick, 1991, “Serious Money: The Art of Marketing Mutual Funds”, Robert a Stanger & Co. Publising, 330 pages. Musto, David, 1999, “Investment Decisions Depend on Portfolio Disclosures”, Journal of Finance, 54(3), 935-952. Odean, Terrance, 1999, “Do Investors Trade Too Much?”, American Economic Review, 89, 1279-1298. Petersen, Mithchell, 2009, “Estimating Standard Errors in Finance Panel Data Sets: Comparing Approaches”, Review of Financial Studies, 22, 435-480. Sias, Richard, 2004, "Institutional Herding", Review of Financial Studies, 17, 165-206. Sirri, Erik and Peter Tufano, 1998, "Costly Search and Mutual Fund Flows", Journal of Finance, 1589-1622. Tetlock, Paul C., 2007, "Giving Content to Investor Sentiment: The Role of Media in the Stock Market," Journal of Finance, 62, 1139-1168. Tetlock, Paul C., 2010, “All the News That's Fit to Reprint: Do Investors React to Stale Information?”, Review of Financial Studies, forthcoming. Tetlock, Paul C., Maytal Saar-Tsechansky, and Sofus Macskassy, 2008, “More Than Words: Quantifying Language to Firms' Fundamentals”, Journal of Finance 63, 1437-1467. Wermers, Russ, 1999, “Mutual Fund Herding and the Impact on Stock Prices”, Journal of Finance, 54, 581-622. Wermers, Russ, 2001, “The Potential Effects of More Frequent Portfolio Disclosure on Mutual Fund Performance”, Investment Company Institute Perspective, June. Zheng, Lu, Vikram Nanda, and Jay Wang, 2004, “Family Values and the Star Phenomenon,” Review of Financial Studies 17, 667-698.

28

Table 1. Summary Statistics: Mutual Funds and Financial Media This table reports summary statistics for the sample of U.S. open-end domestic large-cap equity funds and the sample of media coverage of stocks in the S&P 500 index. Both samples start in 2000 and end in 2008. Panel A. Open-end U.S. equity funds

Number of funds in the sample 1,553

Total assets under mgmt, $ bil, in 2000 (2008) 1,840.5 (1,909.4)

Number of fund initiations during sample period 524

Mean (median) number of fund starts per year 25.9 (29.0)

Mean (median) fund size, $ mil 1,804.5 (250.0)

Mean (median) expense ratio, % 1.27 (1.22)

Mean (median) turnover, % 88.1 (59.0)

Mean (median) number of stocks in portfolio 109.2 (70.0)

Mean (median) % of assets in top 10 stocks 44.0 (35.9)

Panel B. Media data

Number of articles in the sample 673,187

Distribution of articles by source:

Dow Jones Newswire 528,199 (78.5%)

Wall Street Journal 73,774 (11.0%)

New York Times 40,085 (6.0%)

Washington Post 22,674 (3.4%)

USA Today 8,455 (1.3%)

Mean (median) number of articles in a company-quarter 34.54 (12.00)

Min (max) number of articles in a company-quarter 1 (1924)

Standard deviation of the number of articles in a company-quarter 76.84

29

Table 2. Media Coverage and Stock Characteristics This table reports the results of the regression of raw tone measures on stock characteristics. The dependent variables are: POSPERCit (defined as a fraction of the number of positive articles to the total number of qualifying articles about company i in quarter t) and logPOSNUMit (defined as sign(POSNUMit)*log(1+|POSNUMit|) to reduce the skewness, where POSNUMit is the number of positive minus the number of negative articles about company i in quarter t). The independent variables are: logSIZEit is the natural log of the company’s market capitalization at the end of quarter t, MOMit is the stock market-adjusted return over quarter t, logMTBit is the natural log of the stock market-to-book ratio at the end of quarter t, logILLIQit is the natural log of the Amihud illiquidity measure for the stock multiplied by 1000, logAGEit is the natural log of the time (in years) since the stock IPO, and VOLATILit is the monthly volatility of stock returns estimated over the last 36 months. T-statistics are reported in parentheses.

POSPERCit logPOSNUMit

logSIZEit -0.0062** (-2.54)

-0.0044* (-1.79)

-0.3866*** (-45.92)

-0.3984*** (-47.09)

MOMit 0.0822*** (6.35)

0.1053*** (7.10)

0.5072*** (11.99)

0.6078*** (12.77)

logMTBit 0.0780*** (14.18)

0.0793*** (14.35)

0.5512*** (29.15)

0.5385*** (28.47)

logILLIQit 0.0000 (-0.56)

0.0000 (-0.66)

-0.0002 (-1.50)

-0.0003 (-1.62)

logAGEit -0.0041 (-1.25)

-0.0053 (-1.39)

0.0035 (0.29)

-0.0030 (-0.25)

VOLATILit -0.1911*** (-4.05)

-0.3276*** (-6.25)

-2.9950*** (-18.56)

-3.5541*** (-19.94)

Fixed Effects quarter quarter

Number of obs. 16,820 16,820 16,408 16,408

R-sq 2.05% 3.07% 15.82% 17.43%

30

Table 3. Media Coverage and Mutual Fund Portfolio Choice This table reports the results of the logit regression of dummies HOLDijt (equal to 1 if stock i is held by fund j at the end of quarter t and 0 otherwise) and TOP10ijt (equal to 1 if stock i is among the top 10 positions of fund j’s portfolio at the end of quarter t, equal to 0 if it is held by the funds but is outside of the top 10 positions, and undefined otherwise) on different tone measures. The tone measures considered are: POSPERCRANKPUREit (the fraction of positive articles about company i in quarter t orthogonalized with respect to size, MTB, volatility, and stock quarterly return and then ranked to produce a variable between 0 and 1), POSNUMRANKPUREit (the difference between the number of positive and negative articles about company i in quarter t orthogonalized and ranked in the same way), POSPERCRANKMOMit (the fraction of positive articles about company i in quarter t orthogonalized with respect to size, MTB, and volatility and then ranked to produce a variable between 0 and 1), and POSNUMRANKMOMit (the

difference between the number of positive and negative articles about company i in quarter t orthogonalized and ranked in the same way). In all regressions, the dependent variable lagged by 1 quarter is included as a control. The regressions are estimated with quarter fixed effects. T-statistics are reported in parentheses. Panel A. Probability of stock being held in the portfolio

Tone variable used in the regression

POSPERCRANKPUREit POSNUMRANKPUREit POSPERCRANKMOMit POSNUMRANKMOMit

TONEit 0.1034*

(1.77)

0.2314***

(3.15)

0.1583**

(2.18)

0.2749***

(3.41)

HOLDijt-1 0.7122***

(15.20)

0.6943***

(14.44)

0.6335***

(12.17)

0.6201***

(11.23)

Number of obs.

24,645,812 25,256,510 24,645,812 25,256,510

Nagelkerke R-sq

20.66% 26.16% 22.73% 28.13%

Panel B. Probability of stock being held in the top 10 conditional on it being held in the portfolio

Tone variable used in the regression

POSPERCRANKPUREi

t POSNUMRANKPUREi

t POSPERCRANKMOMi

t POSNUMRANKMOMi

t

TONEit 0.1439**

(2.18)

0.2502***

(3.37)

0.1872***

(2.75)

0.2554***

(2.94)

TOP10ijt-1 0.4853***

(8.21)

0.4149***

(7.73)

0.3861***

(6.52)

0.3985***

(6.94)

Number of obs.

4,211,518 4,603,420 4,211,518 4,603,420

Nagelkerke R-sq

14.73% 16.31% 15.11% 16.84%

31

Table 4. Fund Characteristics and Loadings on Media-Favored Stocks