Market History and Forecast for Downtown Chicago, August 2014

12

Market History and Forecast for Downtown Chicago, August 2014

-

Upload

aileen-sargent -

Category

Documents

-

view

29 -

download

0

description

Market History and Forecast for Downtown Chicago, August 2014. What’s Changed in 2014?. Chicago itself is doing as well as it ever has in occupancy. Rate is getting better. There are over 109,000 rooms in the metro area. An extra 10,000 rooms would be an increase of only 9% over 5 years. - PowerPoint PPT Presentation

Transcript of Market History and Forecast for Downtown Chicago, August 2014

Market History and Forecast for Downtown Chicago,

August 2014

What’s Changed in 2014?

• Chicago itself is doing as well as it ever has in occupancy. Rate is getting better.

• There are over 109,000 rooms in the metro area. An extra 10,000 rooms would be an increase of only 9% over 5 years.

• Almost all the proposed hotels are in Chicago, which only has 36,000 rooms, meaning it would be a 28% increase in downtown rooms!

• Historically, Chicago sent over 500,000 rooms into the suburbs per year, or around 120 days.

• Now it’s less than 100,000, or 10-20 days.

Changes in the Traveler

• People now stay where they want to.– Corporations are more flexible– There are way more rooms to choose from– The consumer is more informed

• Thanks primarily to the internet

• There are more travelers– Convention has stayed the same, but they’re a smaller

percent (used to be 60%, now 45%). People don’t always stay in the HQ hotel anymore.

– Leisure is a larger percentage (used to be 10% or less, now it’s 15% and growing)

Regional Markets

Why do we think Chicago is going to lose occupancy?

• It’s all room count.

• We’re going to add 20% more rooms to the supply in the next 5 years.

• Demand is still going up, but not fast enough.

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 201830,000

32,000

34,000

36,000

38,000

40,000

42,000

44,000

46,000

50%

55%

60%

65%

70%

75%

80%

85%

90%

95%

100%Room Count Vs. Occupancy 2008-2018

Rooms Occupancy

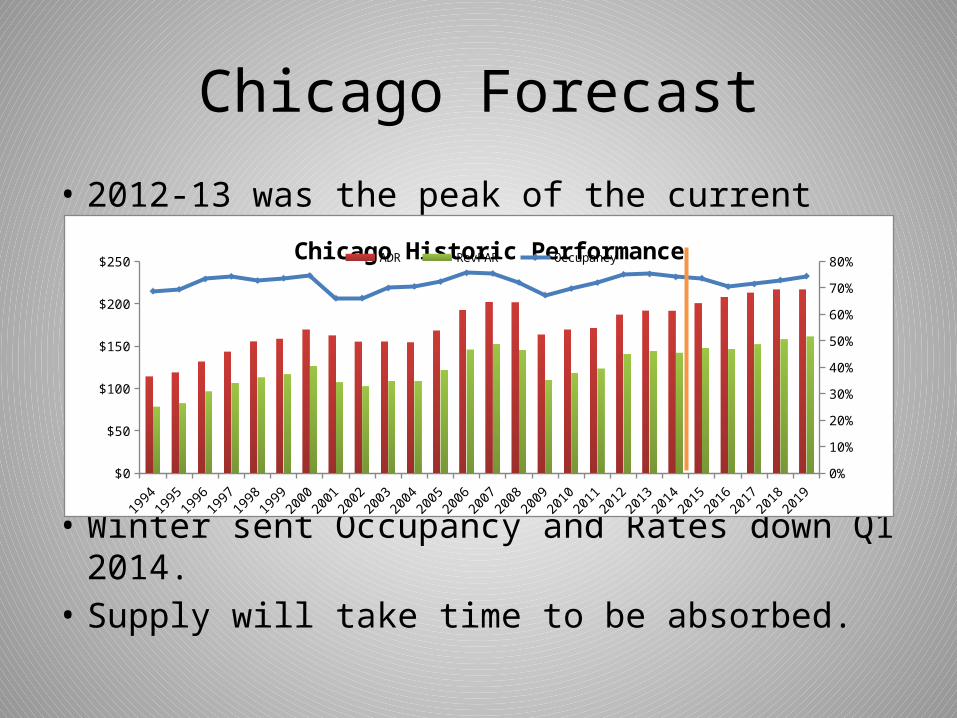

Chicago Forecast

• 2012-13 was the peak of the current cycle.

• Winter sent Occupancy and Rates down Q1 2014.• Supply will take time to be absorbed.

$0

$50

$100

$150

$200

$250

0%

10%

20%

30%

40%

50%

60%

70%

80%Chicago Historic Performance

ADR RevPAR Occupancy

Weekly data

• Tuesday is the highest rate day, Saturday is the highest occupancy day.– Tuesday is usually corporate and group, at full rack

and is less price conscious.– Weekends are usually packaged rates and

discounts.– This change happened about 5 years ago during

the recession.

Monthly Data

• Historically consistent. May-October are the busy months. November-April are slow.

Jan Feb

March

April

May

June

July

Aug

Sept

Oct Nov

Dec

Jan Feb

March

April

May

June

July

Aug

Sept

Oct Nov

Dec

Jan Feb

March

April

May

June

July

Aug

Sept

Oct Nov

Dec

Jan Feb

March

April

May

June

$0

$50

$100

$150

$200

$250

$300

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Chicago CBD Market Monthly 2011 - 2014ADR RevPAR

Recent SalesDate

Hotel Name/ Buyer

Year Built/ # Units

Price in mil. /CPR

Pending Intercontinental Chicago O'Hare 2008 $120

Loews Hotels 556 units $215,827

Pending Homewood Suites 1999 $53

ARC Hospitality Trust 233 units $226,156

May'14 Howard Johnson Inn Chicago Downtown 1968 $15

MAC Management Co JV Magellan Development Group JV 71 units $214,789

Feb'14 Warwick Allerton Hotel 1923 $82

Warwick Int'l Hotels 443 units $184,989

Feb'14 Hotel Burnham 1895 $35

Lone Star Funds 122 units $288,525

Jan'14 Drake Hotel (Land Only) 1920 $150

Lodging Capital Partners JV

Dec'13 Belden Stratford 1923 $87

Prudential RE Investors 297 units $292,088

Nov'13 Hotel Monaco Chicago 1912 $56

Inland American REIT 192 units $291,667

Oct'13 Tokyo Hotel* 1928 $14

Sydell Group Ltd 190 units $71,053

Sep'13 Hotel Lincoln 1928 $49

Walton Street CapitalJV 184 units $263,587

Aug'13 Hotel Blake (Bulk Condo)* 1986 $5

Bluegreen Corp 12 units* $407,625

Average CPR: $247,204

This YTD is Rough• April

– Occupancy down 2.5%– ADR down 4.5%– RevPAR down 6.9%

• YTD– Occupancy down 4.9%– ADR down 3.8%– RevPAR down 8.4%

• Supply up 5.6% YTD• Demand up 0.4% YTD

New Supply

• 2,800 rooms recently opened or about to open.

• Another 4,800 in the planning stage. More are added almost weekly at this point.

• A lot of conversion from old office buildings.• Neighborhoods are starting to get their own

hotels, generally boutique properties.

New, U C and Proposed HotelsOpened

Early Planning

Advancing