Managing the Impact of CFPB Regulations

7

Managing the Impact of CFPB Regulations Auto lenders must overhaul their IT systems and operations to prepare for increasing scrutiny around their practices and policies. Executive Summary At US$934B, auto-loan debt is the third largest household debt in the U.S., with no signs of decreasing. This shows an increasing demand for vehicles among consumers. The concern is that most of the growth is in the subprime auto loan market. Default rates in auto loans and vehicle repossessions have also increased significantly in recent years. Furthermore, there are indications of discrimination and unfair lending practices, and a lack of transparency. These issues have prompted an intervention by the Consumer Financial Protec- tion Bureau (CFPB), which has taken action in the form of fines, stricter implementation of consumer protection laws, and steps to prevent unfair prac- tices and ensure transparency. In May 2014, the CFPB announced plans to target the auto finance industry for enforcement of fair lending laws. The regulatory body plans to moni- tor the top players in the industry by defining a facing such stringent scrutiny for the first time – posing significant challenges for them. In this white paper, we provide a brief background on the auto finance industry and CFPB laws, and list the major reasons why the CFPB has had to step in. We also touch on existing consumer financial laws that affect the industry. Finally, we will present a high-mid-level analysis of the cur- rent process deficiencies on the lenders’ end, and suggest solutions to overcome these obstacles by improving the performance of supporting pro- cesses, people and technologies. The State of Auto Loan Debt As of Q3 2014, 2 total auto loan debt in the U.S. stood at $0.934T 3 – coming in third after mort- gages ($8.131T) and student loans ($1.126T), and ahead of credit card debt ($0.68T). Banks and other lenders issued $105B in new auto loans in Q3 2014. Banks have the largest share of the auto finance market share, followed by captive finance companies, credit unions, independent finance companies and Buy Here Pay Here (BHPH) lenders. Auto loan debt grew significantly in Q3 2014 – over 10% when compared with Q3 2013, and over 3% when compared with Q2 2014. 4 This growth has not been uniform. Subprime auto loan debt has dou- bled since 2010 (see Figure 1, next page), whereas prime auto debt has increased by only a third. cognizant 20-20 insights | april 2015 • Cognizant 20-20 Insights “Larger Participant” 1 rule, similar to its regula- tion for the student loans sector. Direct lenders (banks) have already gone through several cycles of regulatory changes, such as the Making Home Affordable (MHA) program, CFPB rules, etc., and have managed the impact of regulations on their processes, people and systems. While most of these institutions will find it easier to comply with the new laws, the top indirect lenders will be

Transcript of Managing the Impact of CFPB Regulations

Managing the Impact of CFPB RegulationsAuto lenders must overhaul their IT systems and operations to prepare for increasing scrutiny around their practices and policies.

Executive Summary At US$934B, auto-loan debt is the third largest household debt in the U.S., with no signs of decreasing. This shows an increasing demand for vehicles among consumers. The concern is that most of the growth is in the subprime auto loan market. Default rates in auto loans and vehicle repossessions have also increased significantly in recent years. Furthermore, there are indications of discrimination and unfair lending practices, and a lack of transparency. These issues have prompted an intervention by the Consumer Financial Protec-tion Bureau (CFPB), which has taken action in the form of fines, stricter implementation of consumer protection laws, and steps to prevent unfair prac-tices and ensure transparency.

In May 2014, the CFPB announced plans to target the auto finance industry for enforcement of fair lending laws. The regulatory body plans to moni-tor the top players in the industry by defining a

facing such stringent scrutiny for the first time – posing significant challenges for them.

In this white paper, we provide a brief background on the auto finance industry and CFPB laws, and list the major reasons why the CFPB has had to step in. We also touch on existing consumer financial laws that affect the industry. Finally, we will present a high-mid-level analysis of the cur-rent process deficiencies on the lenders’ end, and suggest solutions to overcome these obstacles by improving the performance of supporting pro-cesses, people and technologies.

The State of Auto Loan DebtAs of Q3 2014,2 total auto loan debt in the U.S. stood at $0.934T3 – coming in third after mort-gages ($8.131T) and student loans ($1.126T), and ahead of credit card debt ($0.68T). Banks and other lenders issued $105B in new auto loans in Q3 2014. Banks have the largest share of the auto finance market share, followed by captive finance companies, credit unions, independent finance companies and Buy Here Pay Here (BHPH) lenders. Auto loan debt grew significantly in Q3 2014 – over 10% when compared with Q3 2013, and over 3% when compared with Q2 2014.4 This growth has not been uniform. Subprime auto loan debt has dou-bled since 2010 (see Figure 1, next page), whereas prime auto debt has increased by only a third.

cognizant 20-20 insights | april 2015

• Cognizant 20-20 Insights

“Larger Participant”1 rule, similar to its regula-tion for the student loans sector. Direct lenders (banks) have already gone through several cycles of regulatory changes, such as the Making Home Affordable (MHA) program, CFPB rules, etc., and have managed the impact of regulations on their processes, people and systems. While most of these institutions will find it easier to comply with the new laws, the top indirect lenders will be

cognizant 20-20 insights 2

Captive finance companies such as Honda Finance, Toyota Financial Services, Ford Motor Credit and BHPH, for example, have contributed to most of the growth in the subprime market; the dollar value of their subprime loans was almost three times that of banks in Q3 2014.

The Industry StructureThe U.S. auto finance industry encompasses direct lenders, indirect lenders and Buy Here Pay Here (BHPH) lenders. Direct lenders are usually banks and credit unions that lend directly to consumers. In indirect lending, consumers approach dealers, who coordinate with various lenders to obtain auto loans for the consumers. Indirect lenders are made up of captive finance companies, banks, credit unions, independent finance companies and other investors. BHPH lenders generally cater to the subprime market, and finance most of their loans through captive (affiliated) finance companies.

Regulatory ComplianceThe auto finance industry is regulated by broader consumer financial laws that govern other consumer financial industries, such as mort-gages, student loans and credit cards. All auto lenders and dealers have to comply with acts such as the Equal Credit Opportunity Act, the Fair Credit Reporting Act, and the Truth in Lending Act, among others. The Dodd-Frank Act made the Consumer Financial Protection Bureau (CFPB) responsible for enforcing these laws.

Why CFPB IntervenedIn response to the financial and housing crisis of 2008, the Dodd-Frank Wall Street Reform Act and Consumer Protection Act of 2010 (Dodd-Frank Act) was enacted. The Dodd-Frank Act includes

16 titles. The Consumer Financial Protection Bureau (CFPB) was formed as part of Title X. Auto dealers that have an unaffiliated financing source fall under the Federal Trade Commission’s jurisdic-tion and not the CFPB’s. However, CFPB has inves-tigative and enforcement rights over indirect auto lenders and other auto dealers. Direct lenders such as banks are under the CFPB’s jurisdiction.

As shown in Figure 2 (next page), the main drivers behind the CFPB’s intervention in the auto lending industry include:

• Discrimination against consumers due to their sex, color, religion or origin – which violates the ECOA and Fair Lending Act. This is based on reports of dealers selling loans at higher interest rates to consumers from minority groups. Dealers can do this by changing the markup on interest rates offered by lenders.

• An increase in 60+ days past due account volume from $4.07B in Q3 2013 to over $5.38B in Q3 2014. Auto lenders reported $355M in non-performing auto loans in Q3 2014 – stating an increase of 8% YoY. Since March 2012, the CFPB has been accepting customer complaints across various consumer finance categories, including auto loans. The complaint categories specific to auto loans are Billing and Credit Reporting (44%), New Loan and Modifications to Loan Terms (23%), Default Management (22%) and Loan Marketing and Sales (11%).

• Repossession of vehicles was at a record high in 2013.

The total balance of newly originated subprime loans as of Q3 2014 was $81.2B – an eight-year high representing 28% of all new auto loans in 2014.5

Size and Scale Key Players

• $0.934T as of Q3 2014.• Consumers, direct lenders, indirect lenders,

dealers and regulators.

• $105B in new loans in Q3 2014.• Top 20 direct and indirect lenders account

for 47.9% of all retail loans.

• Banks and captive finance companies have a 63.4% share of the auto finance market.

• Allys is the largest lender, with a share of 5.56%, followed by Wells Fargo at 5.32% and Toyota FS at 4.49 %.

The Auto Lending Landscape

Source: Experian.com Figure 1

cognizant 20-20 insights 3

In 2014, the CFPB announced that the auto finance industry would be a fair lending enforce-ment target. Both direct and indirect auto lenders had been passing on the onus of complying with various regulations to the dealers. The CFPB’s steps placed the burden back on the lenders to ensure that they are held accountable for the credit processes and practices of the dealers. The regulator has already taken actions against some large auto lenders, and penalized lenders for failure to comply with ECOA and FCRA.

Key Timelines

The CFPB began its campaign in March 2013 – asking indirect auto lenders to comply with ECOA, Regulation B, and the Fair Lending Act, and to ensure controls for dealer markups and

compensation policies. In December 2013, CFPB, along with the Department of Justice (DOJ), imposed a stiff penalty on a top auto lender for discriminatory lending practices.6 In May 2014, CFPB officially confirmed that it would be creat-ing new rules for auto lenders.

Currently, the bureau supervises large banks in auto finance, but not non-bank auto finance companies. CFPB is proposing to extend its super-vision authority to these institutions by defining a “larger participant” rule. This rule is likely to affect 50% of the auto lending market, which could include up to 20 top auto lenders. Similar to the mortgage market, the CFPB plans to impose reporting requirements on auto lenders to spot unfair practices. The regulator also intends to

The CFPB Intervention Timeline

Figure 2

• The rule is likely to impact at least the top 20 auto lenders, including banks and non-banks.

• The CFPB to target auto lenders’ compliance-managing systems or methodologies, as well as their complaint-handling systems.

• The CFPB to present rules for auto lending that would be built around “large participants,” similar to student loan servicing.

• The “large participant“ threshold from the CFPB is expected to include major players in the market, based on market coverage and number of consumers impacted.

March 2013: CFPB on Indirect Auto Lending

• Ensure that lenders comply with ECOA and Regulation B.

• Lenders to set in place controls related to dealer markup and compensation policies.

• Lenders must comply with the Fair Lending Act.

May 2014: CFPB Rule-Making Agenda

• The CFPB officially confirmed it would proceed with creating rules for auto lenders.

• The CFPB began developing a proposal to identify “larger participants” in the market for auto lending. The CFPB had defined larger participants in consumer debt collection, student loan servicing and credit reporting.

December 2013: Action against Ally Bank

• The CFPB and the Department of Justice announced an enforce-ment action and consent order that required Ally Bank to pay $80M in damages to consumers who were harmed by discrimina-tory dealer markups and compensation policies between April 2011–December 2013.

• The discriminatory policy affected 235,000 African-American, Hispanic, Asian and Pacific Island consumers.

• Ally was also required to pay an additional $18M penalty to CFPB’s Penalty Fund.

May-August 2014: CFPB Action Against Auto Lender

• The CFPB took action against six auto lenders, including three banks and three non-banks, for violating fair lending practices.

• American Honda Finance Corp. and Toyota Motor Credit Corp. received notice from the CFPB and the Department of Justice.

• Texas-based First Investor Financial Services Group has been fined $2.75M by the CFPB for knowingly providing inaccurate information to credit-reporting agencies for years.

What to Expect

cognizant 20-20 insights 4

provide advisory services and feedback channels to consumers, similar to home ownership coun-seling for mortgages.

The Impact on the Auto Finance Industry

The CFPB’s actions point to a stronger regula-

tory environment for the auto finance industry.

Through these regulations, the CFPB is looking

to bring greater accountability, improvements

in customer service, a reduction in defaults and

the elimination of unfair practices. The bureau

has not indicated that it plans any amendments

to existing consumer financial laws, or is aiming

to introduce new laws for auto lenders. Rather, it

seems to be focused on ensuring compliance by

all industry participants, several of which were hitherto not covered by the CFPB.

Companies in the auto finance industry will need to make significant changes to their processes and systems, and train associates to comply with the stricter regime. The change will be harder to manage for indirect auto lenders, such as captive finance companies and BHPH lenders, than for banks, since these organizations do not have experience in handling similar regulations.

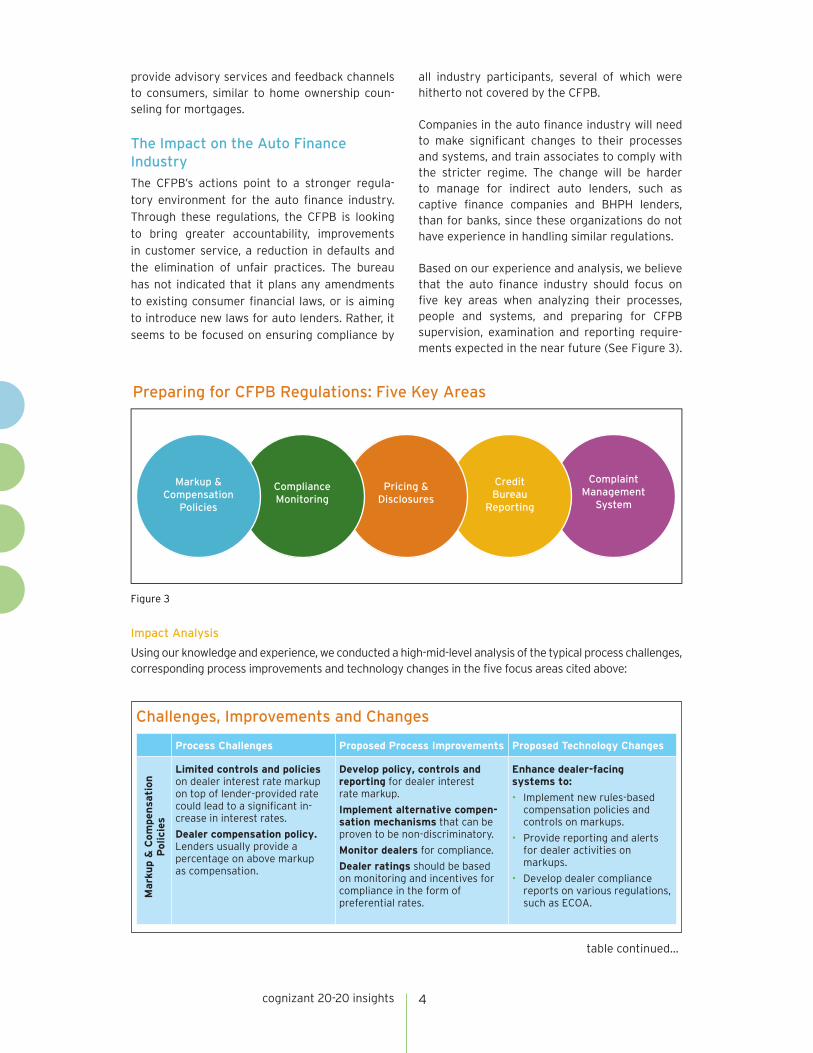

Based on our experience and analysis, we believe that the auto finance industry should focus on five key areas when analyzing their processes, people and systems, and preparing for CFPB supervision, examination and reporting require-ments expected in the near future (See Figure 3).

Preparing for CFPB Regulations: Five Key Areas

Figure 3

ComplaintManagement

System

Credit Bureau

Reporting

Pricing &Disclosures

ComplianceMonitoring

Markup &Compensation

Policies

Impact Analysis

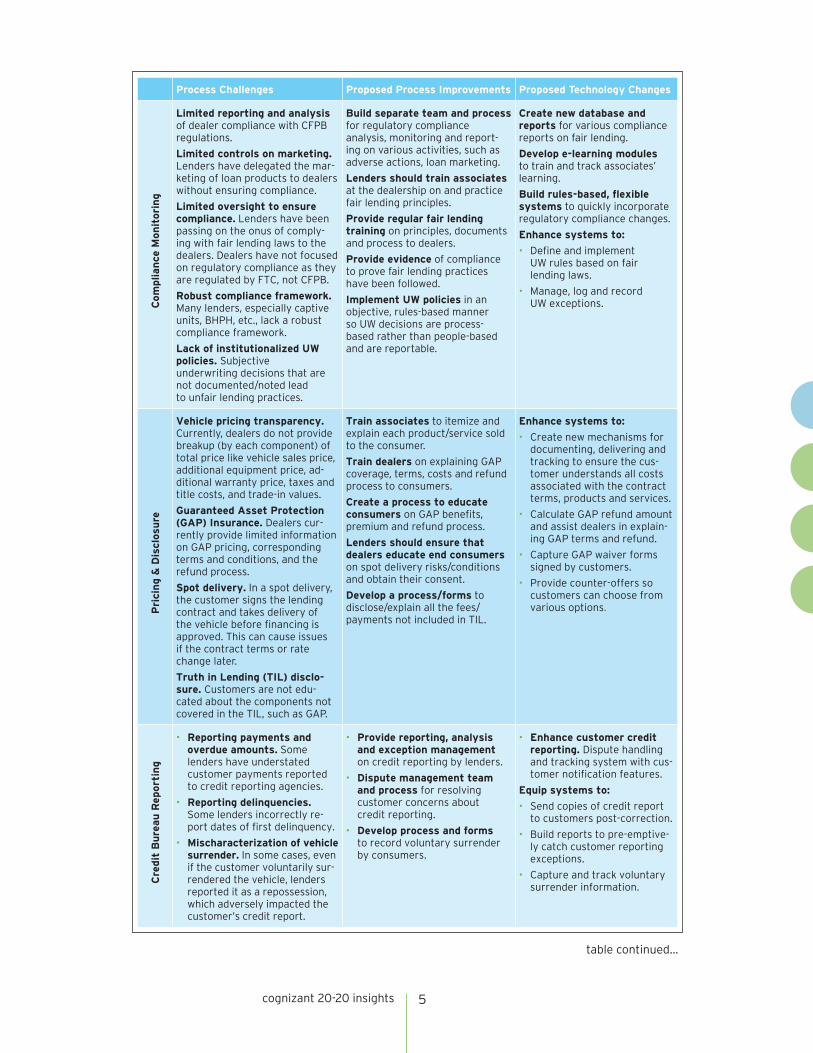

Using our knowledge and experience, we conducted a high-mid-level analysis of the typical process challenges, corresponding process improvements and technology changes in the five focus areas cited above:

table continued...

Process Challenges Proposed Process Improvements Proposed Technology Changes

Mark

up &

Com

pen

sati

on

P

olici

es

Limited controls and policies on dealer interest rate markup on top of lender-provided rate could lead to a significant in-crease in interest rates.

Dealer compensation policy. Lenders usually provide a percentage on above markup as compensation.

Develop policy, controls and reporting for dealer interest rate markup.

Implement alternative compen-sation mechanisms that can be proven to be non-discriminatory.

Monitor dealers for compliance.

Dealer ratings should be based on monitoring and incentives for compliance in the form of preferential rates.

Enhance dealer-facing systems to:

• Implement new rules-based compensation policies and controls on markups.

• Provide reporting and alerts for dealer activities on markups.

• Develop dealer compliance reports on various regulations, such as ECOA.

Challenges, Improvements and Changes

cognizant 20-20 insights 5

Process Challenges Proposed Process Improvements Proposed Technology Changes

Com

plian

ce M

on

itori

ng

Limited reporting and analysis of dealer compliance with CFPB regulations.

Limited controls on marketing. Lenders have delegated the mar-keting of loan products to dealers without ensuring compliance.

Limited oversight to ensure compliance. Lenders have been passing on the onus of comply-ing with fair lending laws to the dealers. Dealers have not focused on regulatory compliance as they are regulated by FTC, not CFPB.

Robust compliance framework. Many lenders, especially captive units, BHPH, etc., lack a robust compliance framework.

Lack of institutionalized UW policies. Subjective underwriting decisions that are not documented/noted lead to unfair lending practices.

Build separate team and process for regulatory compliance analysis, monitoring and report-ing on various activities, such as adverse actions, loan marketing.

Lenders should train associates at the dealership on and practice fair lending principles.

Provide regular fair lending training on principles, documents and process to dealers.

Provide evidence of compliance to prove fair lending practices have been followed.

Implement UW policies in an objective, rules-based manner so UW decisions are process-based rather than people-based and are reportable.

Create new database and reports for various compliance reports on fair lending.

Develop e-learning modules to train and track associates’ learning.

Build rules-based, flexible systems to quickly incorporate regulatory compliance changes.

Enhance systems to:

• Define and implement UW rules based on fair lending laws.

• Manage, log and record UW exceptions.

Pri

cin

g &

Dis

clos

ure

Vehicle pricing transparency. Currently, dealers do not provide breakup (by each component) of total price like vehicle sales price, additional equipment price, ad-ditional warranty price, taxes and title costs, and trade-in values.

Guaranteed Asset Protection (GAP) Insurance. Dealers cur-rently provide limited information on GAP pricing, corresponding terms and conditions, and the refund process.

Spot delivery. In a spot delivery, the customer signs the lending contract and takes delivery of the vehicle before financing is approved. This can cause issues if the contract terms or rate change later.

Truth in Lending (TIL) disclo-sure. Customers are not edu-cated about the components not covered in the TIL, such as GAP.

Train associates to itemize and explain each product/service sold to the consumer.

Train dealers on explaining GAP coverage, terms, costs and refund process to consumers.

Create a process to educate consumers on GAP benefits, premium and refund process.

Lenders should ensure that dealers educate end consumers on spot delivery risks/conditions and obtain their consent.

Develop a process/forms to disclose/explain all the fees/ payments not included in TIL.

Enhance systems to:

• Create new mechanisms for documenting, delivering and tracking to ensure the cus-tomer understands all costs associated with the contract terms, products and services.

• Calculate GAP refund amount and assist dealers in explain-ing GAP terms and refund.

• Capture GAP waiver forms signed by customers.

• Provide counter-offers so customers can choose from various options.

Cre

dit

Bu

reau

Rep

ort

ing

• Reporting payments and overdue amounts. Some lenders have understated customer payments reported to credit reporting agencies.

• Reporting delinquencies. Some lenders incorrectly re-port dates of first delinquency.

• Mischaracterization of vehicle surrender. In some cases, even if the customer voluntarily sur-rendered the vehicle, lenders reported it as a repossession, which adversely impacted the customer’s credit report.

• Provide reporting, analysis and exception management on credit reporting by lenders.

• Dispute management team and process for resolving customer concerns about credit reporting.

• Develop process and forms to record voluntary surrender by consumers.

• Enhance customer credit reporting. Dispute handling and tracking system with cus-tomer notification features.

Equip systems to:

• Send copies of credit report to customers post-correction.

• Build reports to pre-emptive-ly catch customer reporting exceptions.

• Capture and track voluntary surrender information.

table continued...

cognizant 20-20 insights 6

ConclusionWhile auto loan debt in the U.S. has increased rapidly in recent years, most of this growth is in the subprime segment. There is also a noticeable surge in defaults and repossessions, and evidence of unfair lending practices. Consumer complaints to the CFPB related to auto finance are lower compared to complaints related to mortgages, student loans and credit cards. However, the CFPB believes the auto-lending sector should be better monitored to prevent another subprime crisis and protect consumers from unfair lending practices. In fact, in 2014 the bureau fined some auto lenders and announced that auto finance was its target for enforcing fair lending in 2014.

The CFPB plans to define a “Larger Participant” rule similar to the one it specified for student loan servicers, and bring most large auto lend-ers under its domain. If the rule for the student loan servicing market is any indicator, the new directive for auto lenders could at the very least impact the top 20 players.

To manage regulatory monitoring, oversight and reporting, direct and indirect auto lenders need

to focus on and invest in retooling processes, improving employee training, and enhancing and building new systems and reports that can handle compliance requirements. Lenders will not only need to remain compliant; they will also have to provide evidence of such with various fair lend-ing laws, and supply data/reports on compliance, non-compliance and actions taken to ensure compliance – even for their dealers. CFPB’s moni-toring of auto lenders will test the latter’s resil-ience. The adaptation and upgrade process, which could take several months, will strengthen auto lenders’ capabilities to meet future regulatory requirements.

Based on our research, we believe that com-panies that adopt a proactive, comprehensive approach to CFPB compliance will learn how to make the most of their internal resources (peo-ple, processes and technologies). They will also look to external resources, such as the Software as a Service (SaaS) model, and call on consulting and technology organizations with the expertise to needed to successfully manage the impact of CFPB regulations on a sustainable basis.

Process Challenges Proposed Process Improvements Proposed Technology Changes

Com

pla

int

Man

agem

ent

Syst

em

Complaint handling. Lack of well-defined process, SLAs, dedicated resources and system to handle customer complaints.

Recordkeeping. Maintain audit trail of all complaints handled.

Build a strong complaints- management process with SLAs and infrastructure.

Set up a complaints- management team that will identify, monitor, analyze and resolve complaints.

Use SPOC concept for complaints management and resolution.

Develop a multi-channel complaint system to streamline the complaint intake process. The system should be able to record, categorize, track and manage customer complaints.

Figure 4

Footnotes1 http://www.consumerfinance.gov/newsroom/cfpb-proposes-new-federal-oversight-of-nonbank-

auto-finance-companies/

2 http://www.newyorkfed.org/householdcredit/2014-q3/data/pdf/HHDC_2014Q3.pdf

3 www.ycharts.com

4 http://www.experian.com/assets/automotive/white-papers/experian-auto-2014-q3-presentation.pdf?WT.srch=Auto_Q22014FinanceTrends_PD

5 http://www.consumerfinance.gov/newsroom/cfpb-and-doj-order-ally-to-pay-80-million-to-consumers-harmed-by-discriminatory-auto-loan-pricing/

World Headquarters

500 Frank W. Burr Blvd.Teaneck, NJ 07666 USAPhone: +1 201 801 0233Fax: +1 201 801 0243Toll Free: +1 888 937 3277Email: [email protected]

European Headquarters

1 Kingdom StreetPaddington CentralLondon W2 6BDPhone: +44 (0) 207 297 7600Fax: +44 (0) 207 121 0102Email: [email protected]

India Operations Headquarters

#5/535, Old Mahabalipuram RoadOkkiyam Pettai, ThoraipakkamChennai, 600 096 IndiaPhone: +91 (0) 44 4209 6000Fax: +91 (0) 44 4209 6060Email: [email protected]

© Copyright 2015, Cognizant. All rights reserved. No part of this document may be reproduced, stored in a retrieval system, transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the express written permission from Cognizant. The information contained herein is subject to change without notice. All other trademarks mentioned herein are the property of their respective owners.

About Cognizant

Cognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process outsourcing services, dedicated to helping the world's leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 75 development and delivery centers worldwide and approximately 211,500 employees as of December 31, 2014, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top performing and fastest growing companies in the world.

Visit us online at www.cognizant.com or follow us on Twitter: Cognizant.

References

• http://www.consumerfinance.gov/

• http://www.cfpbmonitor.com/

• http://www.treasury.gov/

• http://www.autonews.com/

• http://www.experian.com/

• http://www.ibisworld.com/

• http://www.mortgagenewsdaily.com/

About the AuthorsSaurabh Parakh is a Consultant with Cognizant Business Consulting. He has over seven years of experience working with leading banks in product management and business process optimization across geographies. He can be reached at [email protected].

Sivaraj Lakshmanan is a Senior Consultant with Cognizant Business Consulting. He has over 10 years of experience working with leading banks in project management, product management, and business process optimization. He can be reached at [email protected].

Ashish Shreni is a Principal Consultant with Cognizant Business Consulting and has worked for over 14 years in the banking and insurance space on projects spanning business and IT strategy, business process optimization and complex project execution. His core focus area is Consumer Finance. He can be reached at [email protected].

http://www.consumerfinance.gov/newsroom/consumer-financial-protection-bureau-to-hold-auto-lenders-accountable-for-illegal-discriminatory-markup/

6 http://www.consumerfinance.gov/newsroom/consumer-financial-protection-bureau-to-hold-auto-lenders-accountable-for-illegal-discriminatory-markup/