Managerial Economics - CMRCET

92

Managerial Economics Dr P Alekhya Dr P Alekhya, Associate Professor, MBA, CMRCET

Transcript of Managerial Economics - CMRCET

Managerial Economics

Dr P Alekhya

Dr P Alekhya, Associate Professor, MBA, CMRCET

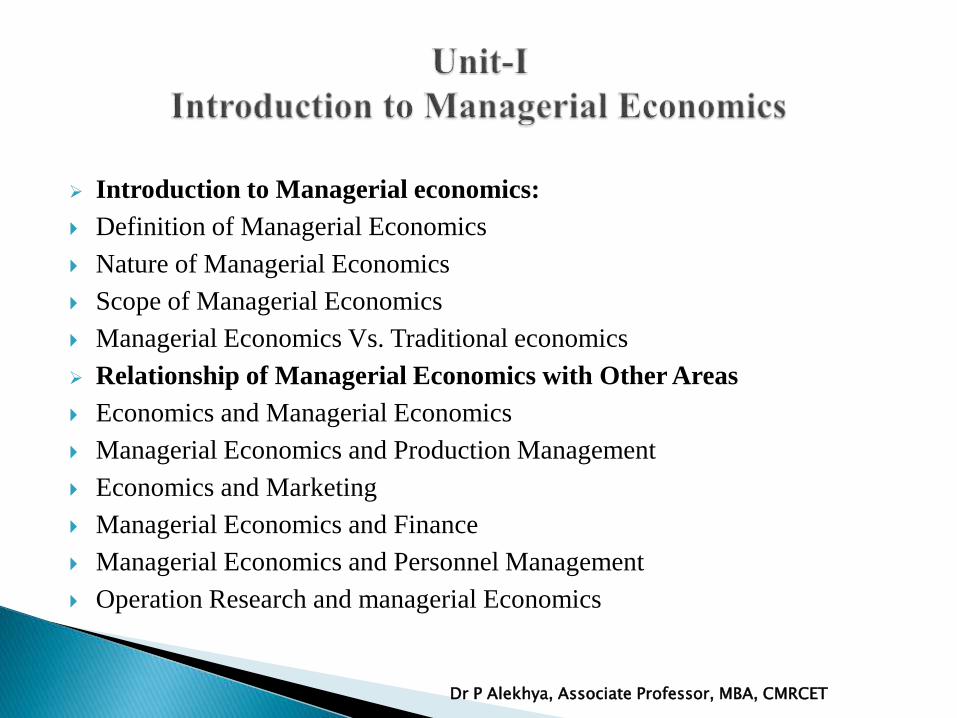

Introduction to Managerial economics:

Definition of Managerial Economics

Nature of Managerial Economics

Scope of Managerial Economics

Managerial Economics Vs. Traditional economics

Relationship of Managerial Economics with Other Areas

Economics and Managerial Economics

Managerial Economics and Production Management

Economics and Marketing

Managerial Economics and Finance

Managerial Economics and Personnel Management

Operation Research and managerial Economics

Dr P Alekhya, Associate Professor, MBA, CMRCET

The Role of Managerial Economist

Responsibility of Managerial Economists

Basic Economic Principles

Opportunity Cost

Incremental Concept

Scarcity

Marginalism

Equi-Marginalism

Time Perspective

Discounting Principle

Risk and Uncertainty

Dr P Alekhya, Associate Professor, MBA, CMRCET

Economics:

Economics is a study of human activity both at individual andnational level. The economists of early age treated economicsmerely as the science of wealth. The reason for this is clear. Everyone of us is involved in efforts aimed at earning money andspending this money to satisfy our wants such as food, Clothing,shelter, and others. Such activities of earning and spending moneyare called “Economic activities”.

According to Adam Smith “Economics as the study of nature anduses of national wealth”.

According to Dr. Alfred Marshall “Economics is a study of man’sactions in the ordinary business of life: it enquires how he gets hisincome and how he uses it”.

Dr P Alekhya, Associate Professor, MBA, CMRCET

Economics

Micro

Economics

Per Capita

Income

Demand of a

Commodity

Macro

Economics

National

Income

Aggregate

Demand

Dr P Alekhya, Associate Professor, MBA, CMRCET

M.H.SPENCER AND L. SIEGELMAN Managerial Economics definedas “the integration of economic theory with business practice for thepurpose of facilitating decision making and forward planning bymanagement”.

BRIGHAMANDPAPPAS believe that managerial economics is “Theapplication of economic theory and methodology to businessadministration practice”.

C.I.SAVAGE AND T.R.SMALL therefore believes that managerialeconomics is concerned with business efficiency.

HAGUE observes that “Managerial Economics is a fundamental academicsubject which seeks to understand and to analyse the problems of businessdecision-making”.

Dr P Alekhya, Associate Professor, MBA, CMRCET

PAPPAS AND HIRSHEY “Managerial Economics applies economictheory and methods to business and administrative decision-making.Because it uses the tools and techniques of economic analysis to solvemanagerial problems, managerial economics links traditional economicswith decision sciences to develop important tools for managerial decision-making”.

MICHAEL R.BAYE defines Managerial Economics as “the study ofhow to direct scarce resources in a way that most efficiently achieves amanagerial goal”.

HAYNES, MOTE AND PAUL define Managerial Economics as“economics applied in decision-making. They consider this as a bridgebetween the abstract theory and the managerial practice”. ManagerialEconomics, therefore, focuses on those tools and techniques, which areuseful in decision-making.

Dr P Alekhya, Associate Professor, MBA, CMRCET

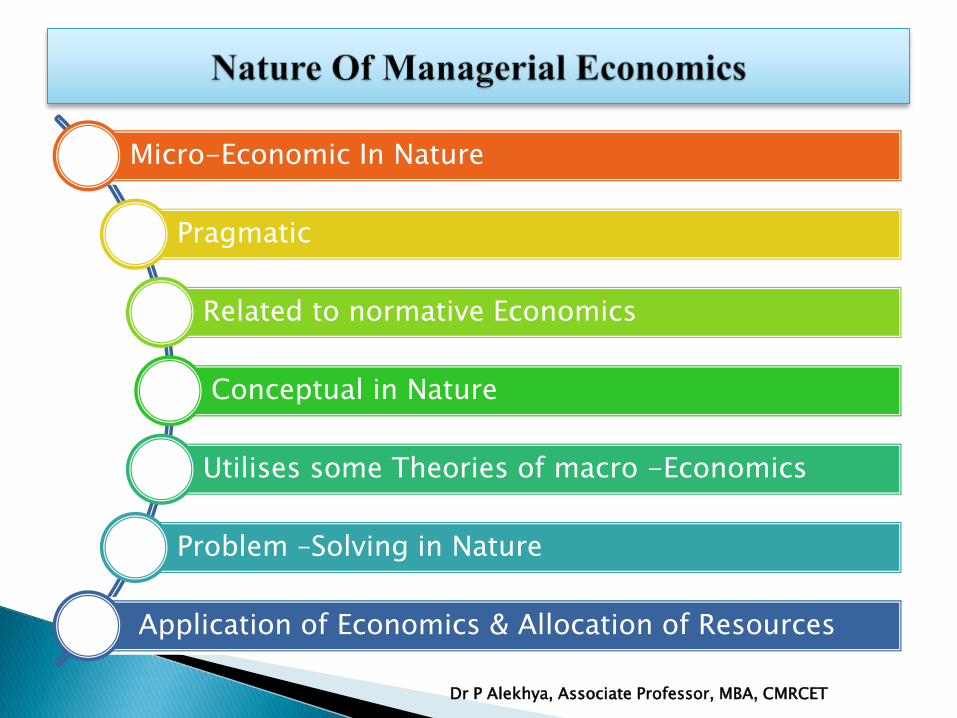

Micro-Economic In Nature

Pragmatic

Related to normative Economics

Conceptual in Nature

Utilises some Theories of macro -Economics

Problem –Solving in Nature

Application of Economics & Allocation of Resources

Dr P Alekhya, Associate Professor, MBA, CMRCET

Demand Decision

Input-Output Decision

Price-Output Decision

Profit-related Decision

Investment Decision

Economic Forecasting and Forward Planning

Dr P Alekhya, Associate Professor, MBA, CMRCET

Concepts and Techniques of

Managerial economics

Managerial Decision Areas:• Production• Reduction or control

of costs• Determination of

Price of a Given Product or service

• Make or buy decision

• Inventory Decision• Capital Management• Profit Planning &

Management• Investment

Decisions

Optimum Solution

Dr P Alekhya, Associate Professor, MBA, CMRCET

Traditional Economics

•Traditional Economics is both Macro and Micro Economics

•It has a wide scope. It deals with each and every aspect of the firm.

•It is both normative and Positive Science.

•It is concerned with Theoretical aspects.

•It considers only the economic aspects of a problem while decision making.

•It deals with both micro and macro problems of a firm.

Managerial Economics:

• Managerial Economics is only micro economic in Nature

• It has a limited scope. It is concerned with decision-making and economic theories that guide the managerial decision making.

• It is a Normative science.

• It deals with practical aspects of the firm.

• It considers both economic and non economic aspects of a problem while decision making.

• It is concerned with decision making of a firm.

Dr P Alekhya, Associate Professor, MBA, CMRCET

Economics

Production Management

Marketing

Finance

Personnel Management

Operations research

Mathematics

Statistics

Psychology

Dr P Alekhya, Associate Professor, MBA, CMRCET

The two Primary Tasks of Managerial economist are:

Processing Information

Making Decisions

a) Specific Decisions: Production Scheduling

Demand Forecasting

Market Research

Economic Analysis of the Industry

Investment Appraisal

Security Management Analysis

Advice on Foreign Exchange Management

Advice on Trade and Public relations

Economic Analysis of competing Companies

Dr P Alekhya, Associate Professor, MBA, CMRCET

Capital Projects

Pricing and Related Decisions

Analyzing and Forecasting

Advice on the Purchase of Raw Materials and inventory Building

Market survey to determine the nature and extent of competition

b) General assignments:

i. External Factors

General Economic condition

Demand for the Product

Input Cost

Market Conditions

Firm’s Share in the Market

Economic Policies

Dr P Alekhya, Associate Professor, MBA, CMRCET

ii.Internal Factors:

Pricing and profit Policies

Investment Decisions

Technological development

Business planning

Statistical Records

Supply of Economic Information

Dr P Alekhya, Associate Professor, MBA, CMRCET

Better Management of Resources

Forecasting

Additional Information

To Maximise Profit

Conceptual as well as Practical

Researcher

Thinking, Discussing and Criticizing

Taking up challenging Tasks

Dr P Alekhya, Associate Professor, MBA, CMRCET

Opportunity Cost Principle

Incremental Principle Concept

Principle of Time Perspective

Discounting Principle

Equi-Marginalism Principle

Marginalism

Risk and uncertainty

Scarcity Principle

Dr P Alekhya, Associate Professor, MBA, CMRCET

Demand Analysis:

Introduction

Meaning & Definition of Demand

Nature Of Demand

Determinants of Demand

Demand Function

Law of Demand

Demand Curve

Reasons for the downward sloping of a demand Curve

Elasticity of Demand

• Different types of Elasticity of Demand

• Significance of Elasticity of Demand

• Methods of Measurement of Elasticity

Dr P Alekhya, Associate Professor, MBA, CMRCET

• Managerial Applications Elasticity of Demand

• Factors Effect the Elasticity of the Demand

Demand Estimation

Stages in Demand Estimation

Marketing Research Approaches to Demand Estimation

Demand Forecasting

Features of Demand Forecasting

Level of Demand Forecasting

Need for Demand Forecasting

Steps Involved in Demand Forecasting

Methods/Techniques of Demand Forecasting

Criteria for Good demand Forecasting

Supply Analysis

Determinants of Supply

Supply Function

Supply Schedule

The Law of Supply

Elasticity of Supply Dr P Alekhya, Associate Professor, MBA, CMRCET

Meaning & Definition of Demand

Demand for a commodity refers to the quantity of the commodity

which an individual consumer or a household is willing to purchase

per unit of time at a particular price. A product or service is said to

have demand when three condition are satisfied.

i. Desire of the consumer to buy the product

ii. Willingness to buy the product

iii. Ability to buy the product

Demand refers to the quantities of commodity that the consumers

are able to buy at each possible price during a given period of time,

other things being equal. ------------------Ferguson

Demand is the ability and willingness to buy specific quantity of a

good at alternative Prices in a given time period. -------B.R Schiller

Dr P Alekhya, Associate Professor, MBA, CMRCET

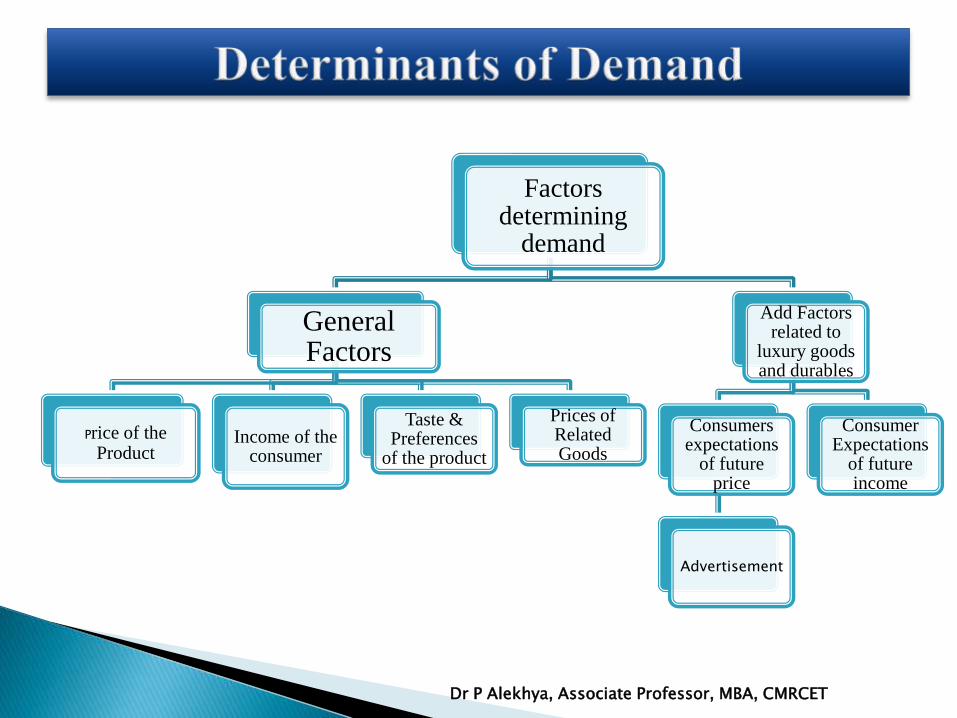

Factors determining

demand

General Factors

Price of the Product

Income of the consumer

Taste & Preferences

of the product

Prices of Related Goods

Add Factors related to

luxury goods and durables

Consumers expectations

of future price

Advertisement

Consumer Expectations

of future income

Dr P Alekhya, Associate Professor, MBA, CMRCET

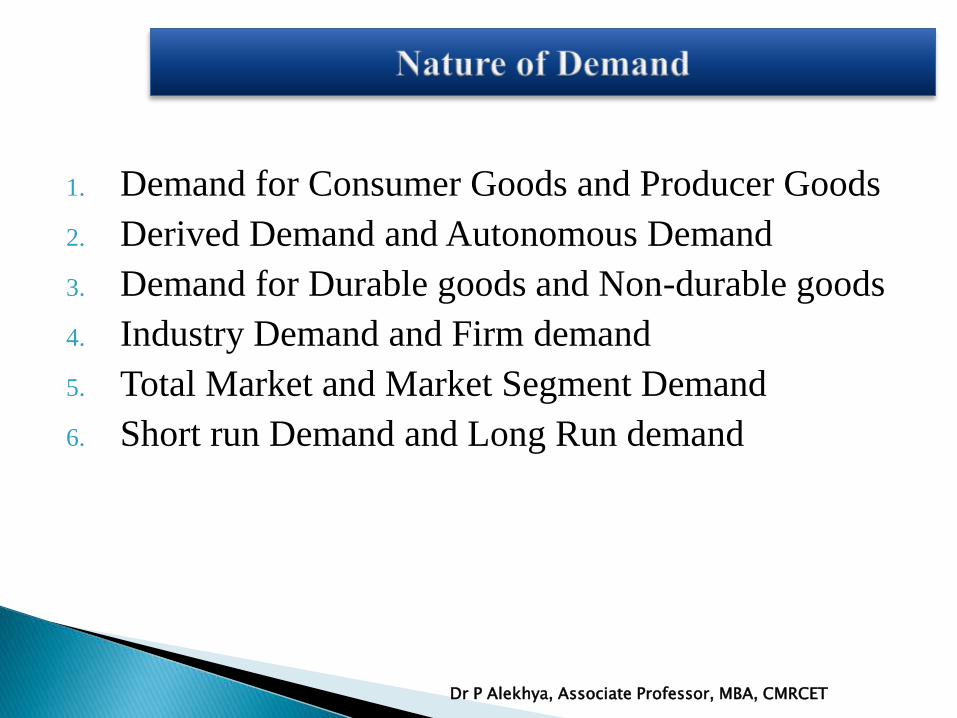

1. Demand for Consumer Goods and Producer Goods

2. Derived Demand and Autonomous Demand

3. Demand for Durable goods and Non-durable goods

4. Industry Demand and Firm demand

5. Total Market and Market Segment Demand

6. Short run Demand and Long Run demand

Dr P Alekhya, Associate Professor, MBA, CMRCET

The demand function is an algebraic expression of the relationshipbetween demand for a commodity and its various determinants thataffect this quantity.

There are two types of demand functions:

Individual Demand Function:An individual’s demand function refers tothe quantities of a commodity demanded at various prices, given hisincome, prices of related goods and tastes. It is expressed as:

Qdx=f(Px,Y,P1….Pn-1,T,A,Ey,Ep,u)

Where:

Qdx- refers to the quantity demande of product X,e.g Ice cream

Px – refers to the price of product X

Y- refers to the level of househld income

P1…Pn-1-refers to all other related products in economy

T-refers to tastes of the consumer

A-refers to advertisement

Ey-refers to consumer’s expected future income

Ep-refers to consumer’s expectations about future prices

U- refers to all those determinants which are not covered in the list of determinantsgiven above.

Dr P Alekhya, Associate Professor, MBA, CMRCET

Market Demand Function: the total demand function is

the basis of demand theory. The market demand function

is the same as Individual demand function.

Dr P Alekhya, Associate Professor, MBA, CMRCET

Law of demand states that higher the price lower the quantity

demanded, and vice versa, other things remaining constant.

Definition of Law of Demand:

According to Marsshell ’’The Law of Demand states that

amount demanded increases with a fall in price and diminishes

when price increases, other things being equal”.

Characteristics of Law of Demand:

Inverse Relationship

Price an Independent Varaiable and Demand of a dependent

variable

Other Things Remain The same

Direction Of Change

Related with the time

Dr P Alekhya, Associate Professor, MBA, CMRCET

Giffen Goods

Veblen Goods

Where there is a shortage of necessities

In case of ignorance of price changes

Demand curve Individual demand Curve

Market demand Curve

Dr P Alekhya, Associate Professor, MBA, CMRCET

Law of Diminishing Marginal Utility

Cumulative Effect

Income Effect

Substitution Effect

Dr P Alekhya, Associate Professor, MBA, CMRCET

The extent of responsiveness of demand with change in the price isnot always the same.

The demand for a product can be elastic or inelastic, depending onthe rate of change in the demand with respect to change in price of aproduct.

Elastic demand is the one when the response of demand is greaterwith a small proportionate change in the price. On the other hand,inelastic demand is the one when there is relatively a less change inthe demand with a greater change in the price.

Dr P Alekhya, Associate Professor, MBA, CMRCET

For better understanding the concepts of elastic and

inelastic demand, the price elasticity of demand has been

divided into five types, which are shown in Figure-1:

Dr P Alekhya, Associate Professor, MBA, CMRCET

1. Perfectly Elastic Demand:

When a small change in price of a product causes a major

change in its demand, it is said to be perfectly elastic demand.

In perfectly elastic demand, a small rise in price results in fall

in demand to zero, while a small fall in price causes increase

in demand to infinity. In such a case, the demand is perfectly

elastic or ep = 00.

Dr P Alekhya, Associate Professor, MBA, CMRCET

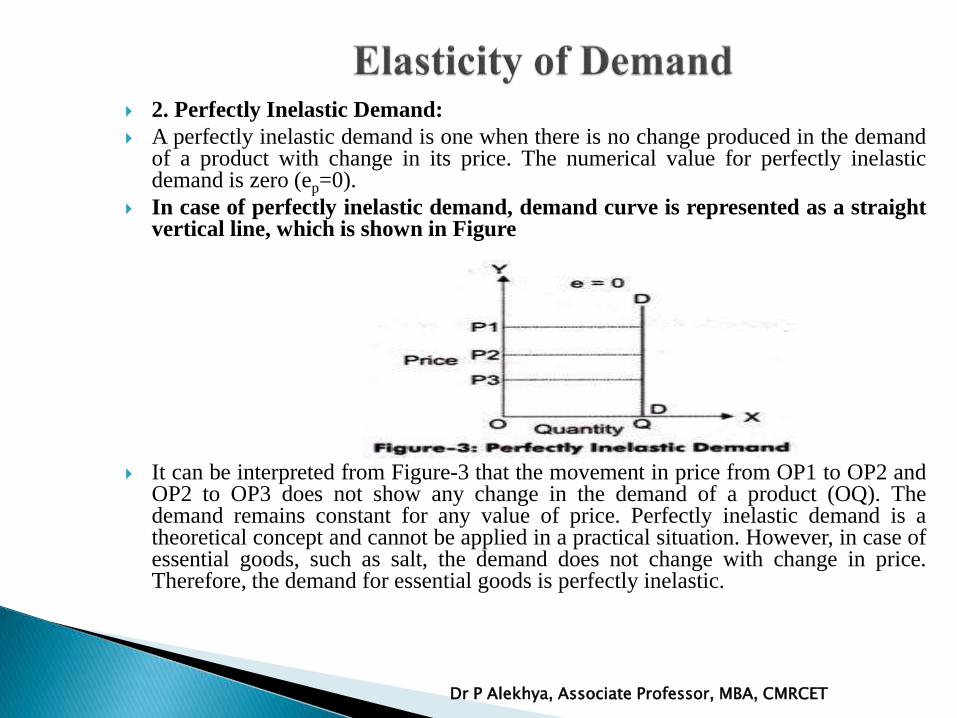

2. Perfectly Inelastic Demand:

A perfectly inelastic demand is one when there is no change produced in the demandof a product with change in its price. The numerical value for perfectly inelasticdemand is zero (ep=0).

In case of perfectly inelastic demand, demand curve is represented as a straightvertical line, which is shown in Figure

It can be interpreted from Figure-3 that the movement in price from OP1 to OP2 andOP2 to OP3 does not show any change in the demand of a product (OQ). Thedemand remains constant for any value of price. Perfectly inelastic demand is atheoretical concept and cannot be applied in a practical situation. However, in case ofessential goods, such as salt, the demand does not change with change in price.Therefore, the demand for essential goods is perfectly inelastic.

Dr P Alekhya, Associate Professor, MBA, CMRCET

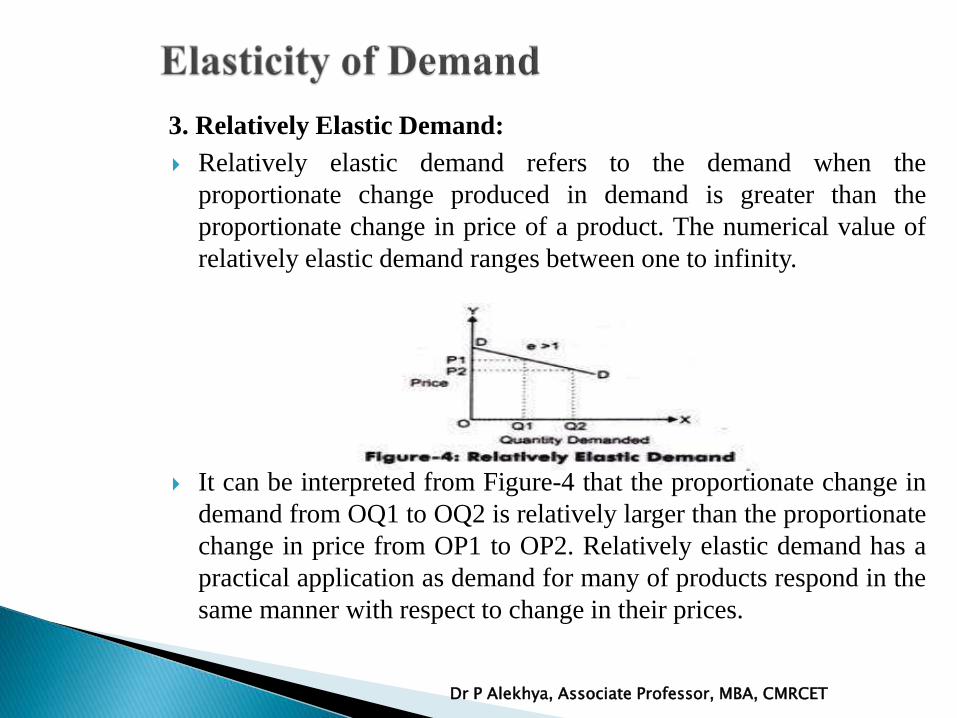

3. Relatively Elastic Demand:

Relatively elastic demand refers to the demand when the

proportionate change produced in demand is greater than the

proportionate change in price of a product. The numerical value of

relatively elastic demand ranges between one to infinity.

It can be interpreted from Figure-4 that the proportionate change in

demand from OQ1 to OQ2 is relatively larger than the proportionate

change in price from OP1 to OP2. Relatively elastic demand has a

practical application as demand for many of products respond in the

same manner with respect to change in their prices.

Dr P Alekhya, Associate Professor, MBA, CMRCET

4. Relatively Inelastic Demand: Relatively inelastic demand is one when the percentage change produced in

demand is less than the percentage change in the price of a product. Forexample, if the price of a product increases by 30% and the demand for theproduct decreases only by 10%, then the demand would be called relativelyinelastic. The numerical value of relatively elastic demand ranges between zeroto one (ep<1). Marshall has termed relatively inelastic demand as elasticitybeing less than unity.

It can be interpreted from Figure-5 that the proportionate change indemand from OQ1 to OQ2 is relatively smaller than the proportionatechange in price from OP1 to OP2. Relatively inelastic demand has apractical application as demand for many of products respond in thesame manner with respect to change in their prices.

Dr P Alekhya, Associate Professor, MBA, CMRCET

5. Unity Elasticity Demand:

When the proportionate change in demand produces the samechange in the price of the product, the demand is referred asunitary elastic demand. The numerical value for unitaryelastic demand is equal to one (ep=1).

The demand curve for unitary elastic demand isrepresented as a rectangular hyperbola, as shown inFigure

From Figure, it can be interpreted that change in price OP1 toOP2 produces the same change in demand from OQ1 to OQ2.Therefore, the demand is unitary elastic.

Dr P Alekhya, Associate Professor, MBA, CMRCET

Income Elasticity of Demand:

The income elasticity of demand measures the responsiveness of the

quantity demanded of a good to the change in the income of the people

demanding the good. It is calculated as the ratio of the change in

quantity demanded to the percent change in income. For eg. If in

response to a 10% increase in income, the quantity of a good

demanded increased by 20%, the income elasticity of demand would

be 2% 10%=2 .

Dr P Alekhya, Associate Professor, MBA, CMRCET

Cross elasticity of demand: Cross elasticity of demand refers to the

quantity demanded of a commodity in response to a change in the

price of a related good, which may be substitute or complement.

Advertising Elasticity of Demand: The Degree of responsiveness

of quantity demanded to the change in the advertisement expenses

of expenditure

Dr P Alekhya, Associate Professor, MBA, CMRCET

Nature of Product

Time Frame

Degree of postponement

Number of alternative uses

Tastes and preferences of the consumer

Availability of close substitutes

Incase of complementaries or joint goods

Level of prices

Availability of subsidies

Expectation of prices

Durability of the product

Government Policy

Dr P Alekhya, Associate Professor, MBA, CMRCET

Prices of factors of production

Price Fixation

Government Policies

• Tax Policies

• Raising Bank Deposits

• Public Utilities

• Revaluation or devaluation of currencies

• Formulate government policy

Forecasting demand

Planning the levels of output and price

Dr P Alekhya, Associate Professor, MBA, CMRCET

Demand estimation is a process that involves coming up

with an estimate of the amount of demand for a product

or service. The estimate of demand is typically confined

to a particular period of time, such as a month, quarter or

year. While this is definitely not a way to predict the

future for your business, it can be used to come up with

fairly accurate estimates if the assumptions made are

correct.

Dr P Alekhya, Associate Professor, MBA, CMRCET

The Important methods of demand Estimation as follows:

1. Market Experiment Method

a) Actual Market method

b) Market simulation Method

2. Survey of consumer’s Future Plans

a) Census Method

b) Samples Survey method

3. Regression Analysis

a) Simple Regression Analysis

b) Multiple Regression Analysis

Dr P Alekhya, Associate Professor, MBA, CMRCET

Forecasting means predicting the future from the informationavailable in the present. Demand forecasting is done to estimatefuture market demand. Information with regard to future demand isuseful to firm in planning and scheduling production, purchase orraw materials and advertisement.

Demand forecasting can be done for short –term and long-term.Short term forecasting is done for a period not exceeding a year andlong-term forecasting is done for period of 3 to 5 years.

Forecasts can broadly be Classified into two categories:

o Passive forecasts

o Active Forecasts

Levels of Demand Forecasting:

o Firm Level

o Industry Level

o National Level

o International Level

Dr P Alekhya, Associate Professor, MBA, CMRCET

Purpose of forecasting Demand:

1) Short Run

Production Planning

Helps to formulate right purchase policy

Helps to frame realistic pricing policy

Sales forecasting

Helps in estimating short run financial requirements

Reduce the dependence on chances

Helps to evolve a suitable labour policy

2) Long Run

Business Planning

Financial Planning

Manpower Planning

Business Control

Dr P Alekhya, Associate Professor, MBA, CMRCET

Steps involved in Forecasting:

Step-1.Identification of objective

Step-II. Determining the nature of goods under

consideration

Step-III. Selecting a proper method of forecasting

Step-IV. Interpretation of results

Dr P Alekhya, Associate Professor, MBA, CMRCET

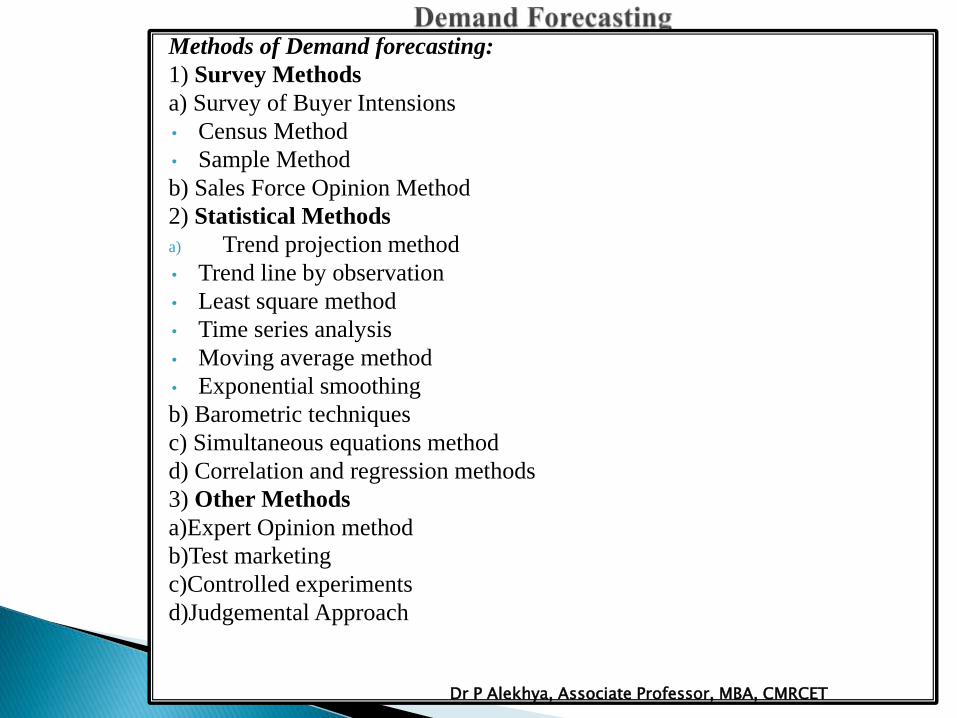

Methods of Demand forecasting:

1) Survey Methods

a) Survey of Buyer Intensions

• Census Method

• Sample Method

b) Sales Force Opinion Method

2) Statistical Methods

a) Trend projection method

• Trend line by observation

• Least square method

• Time series analysis

• Moving average method

• Exponential smoothing

b) Barometric techniques

c) Simultaneous equations method

d) Correlation and regression methods

3) Other Methods

a)Expert Opinion method

b)Test marketing

c)Controlled experiments

d)Judgemental Approach

Dr P Alekhya, Associate Professor, MBA, CMRCET

Accuracy

Plausibility

Simplicity

Durability

Flexibility

Availability of data

Economy

Quickness

Dr P Alekhya, Associate Professor, MBA, CMRCET

Supply of a commodity is the amount of its which the seller is willing to offer for sale at price during a certain period of time.supply is a relative term related to price and time. Market supply means the total quantity of a commodity that all the firms are willing to sell at a given

Dr P Alekhya, Associate Professor, MBA, CMRCET

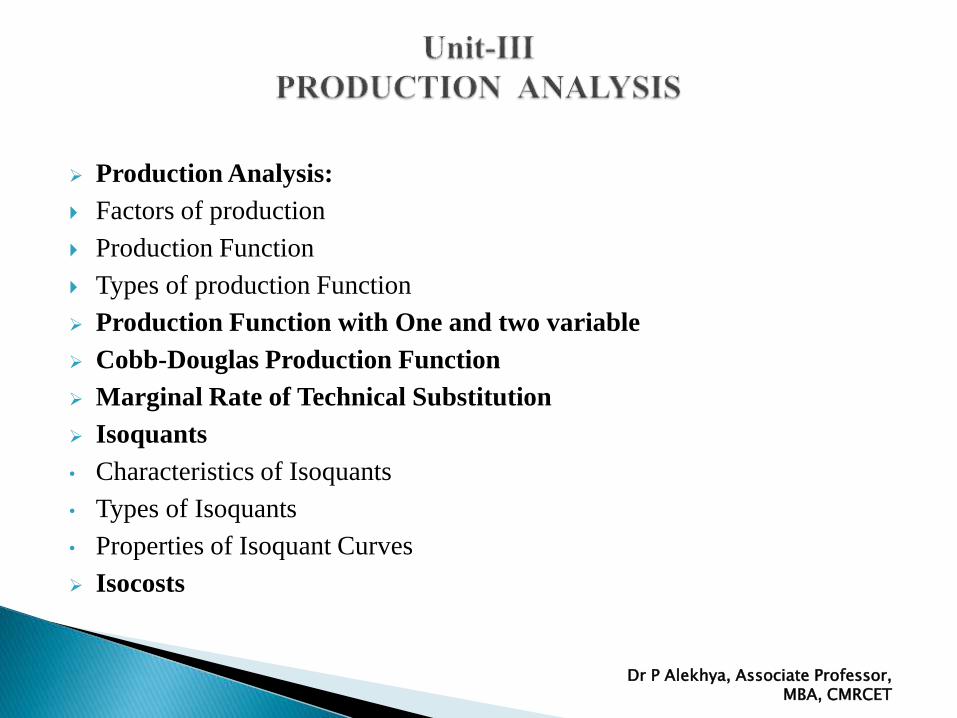

Production Analysis:

Factors of production

Production Function

Types of production Function

Production Function with One and two variable

Cobb-Douglas Production Function

Marginal Rate of Technical Substitution

Isoquants

• Characteristics of Isoquants

• Types of Isoquants

• Properties of Isoquant Curves

Isocosts

Dr P Alekhya, Associate Professor, MBA, CMRCET

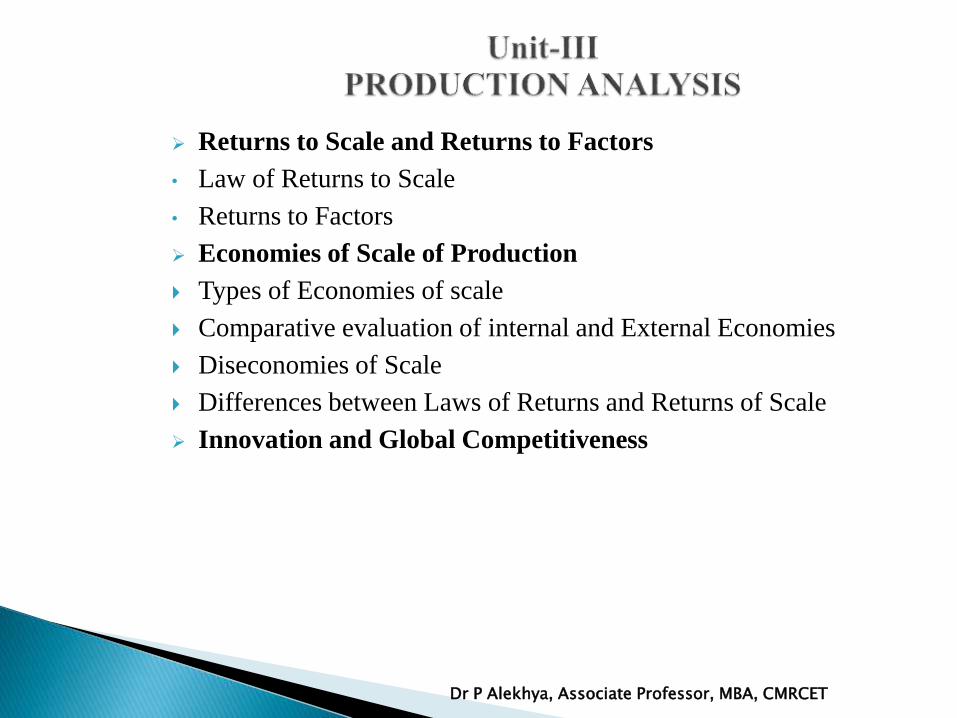

Returns to Scale and Returns to Factors

• Law of Returns to Scale

• Returns to Factors

Economies of Scale of Production

Types of Economies of scale

Comparative evaluation of internal and External Economies

Diseconomies of Scale

Differences between Laws of Returns and Returns of Scale

Innovation and Global Competitiveness

Dr P Alekhya, Associate Professor, MBA, CMRCET

During1900–1947, Charles Cobb and Paul Douglasformulated and tested the Cobb–Douglasproduction function through various statisticalevidence.

The Cobb–Douglas functional form of production functions is widely used to represent the relationship of an output and two inputs.

Dr P Alekhya, Associate Professor, MBA, CMRCET

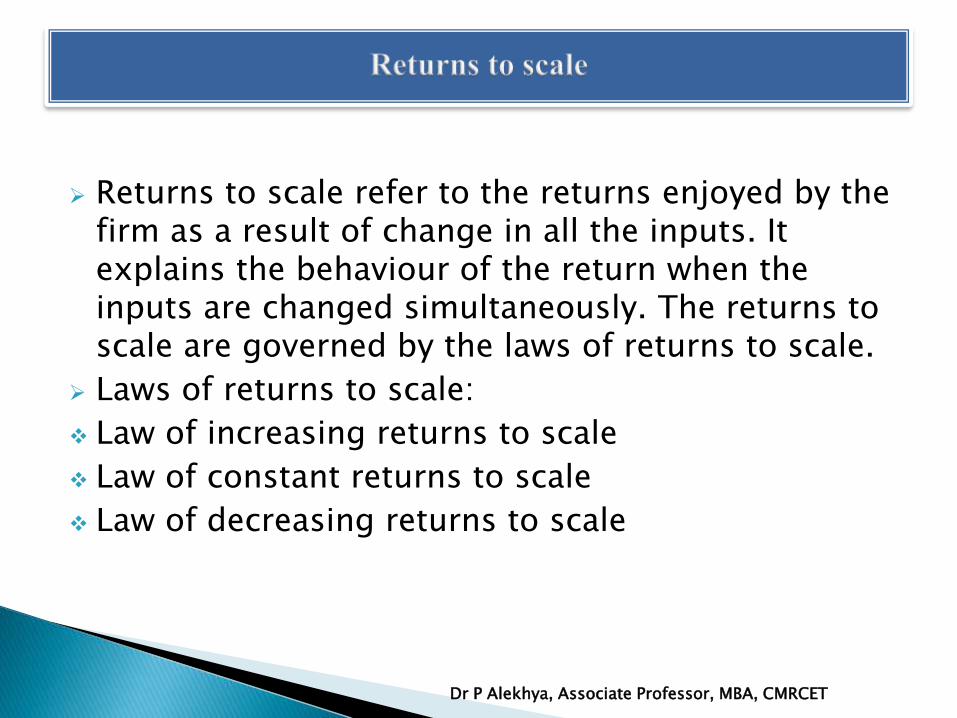

Returns to scale refer to the returns enjoyed by the firm as a result of change in all the inputs. It explains the behaviour of the return when the inputs are changed simultaneously. The returns to scale are governed by the laws of returns to scale.

Laws of returns to scale:

Law of increasing returns to scale

Law of constant returns to scale

Law of decreasing returns to scale

Dr P Alekhya, Associate Professor, MBA, CMRCET

Returns to Factors: Returns to factors are also called factor

productiveness. Productivity is the ratio of output to the input.

Factor productivity rears to the short-run relationship of input and

out-put. The productivity of one unit of a factor of production will

be equal to the output it can generate. The productivity of a

particular factor is measured with the assumption that the other

factors are not changed or remain unchanged. Only that particulars

factor under study changed.

Returns to factors refer to the output or return generated as a result

of change in one or more factors, keeping the other factors

unchanged. Given a percentage of increase or decrease in a

particular factor such as labor, is it yielding proporionate increase or

decrease in production. This is analysed in returns to factors.

Dr P Alekhya, Associate Professor, MBA, CMRCET

The Change in productivity can be measured in terms of

Total Productivity

Average Productivity

Marginal Productivity

Dr P Alekhya, Associate Professor, MBA, CMRCET

According to porter, Economies of scale is the declines in the

units cost of Production.

According to Pratten, Economies of scale is “The reduction in

average unit costs attributable to increase in the scale of

output”.

According to spencer, Economies of scale is a curvilinear

relationship between average cost and the number of units

produced.”

Dr P Alekhya, Associate Professor, MBA, CMRCET

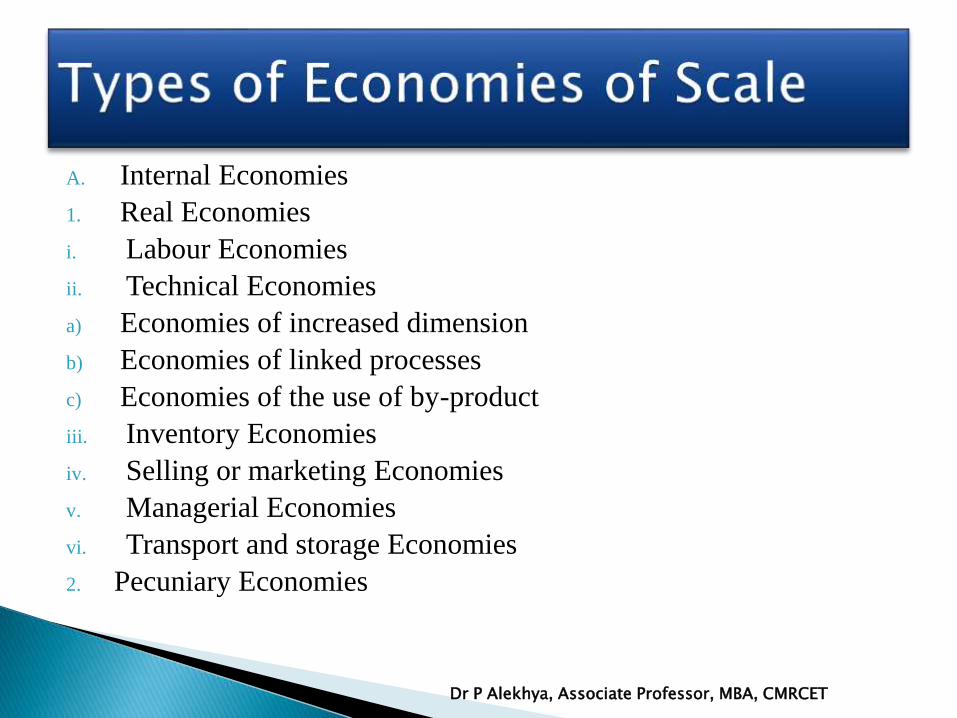

A. Internal Economies

1. Real Economies

i. Labour Economies

ii. Technical Economies

a) Economies of increased dimension

b) Economies of linked processes

c) Economies of the use of by-product

iii. Inventory Economies

iv. Selling or marketing Economies

v. Managerial Economies

vi. Transport and storage Economies

2. Pecuniary Economies

Dr P Alekhya, Associate Professor, MBA, CMRCET

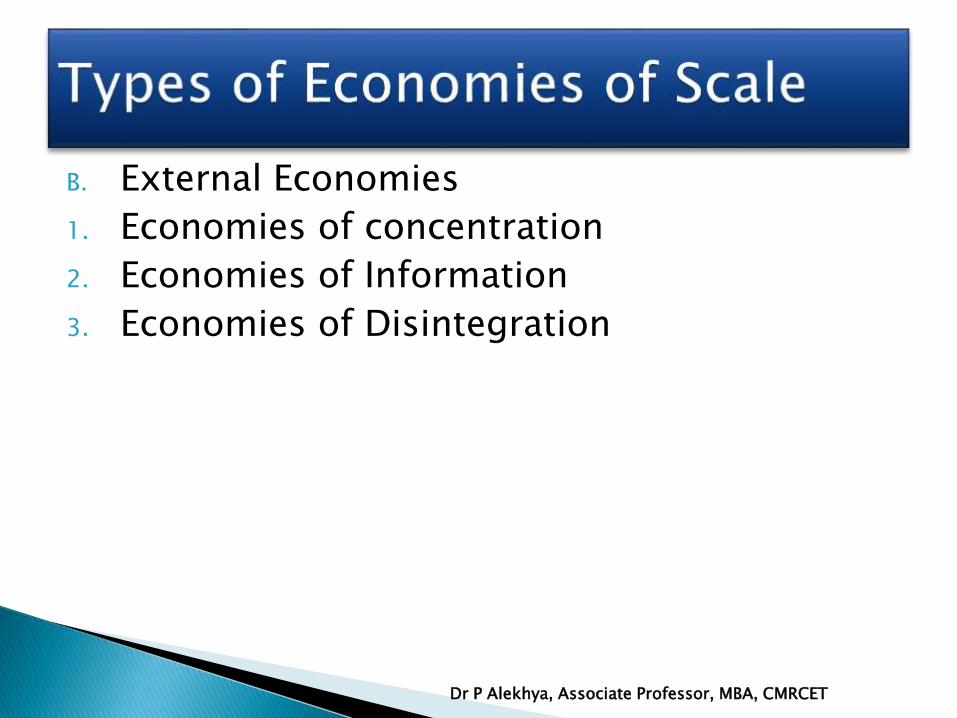

B. External Economies

1. Economies of concentration

2. Economies of Information

3. Economies of Disintegration

Dr P Alekhya, Associate Professor, MBA, CMRCET

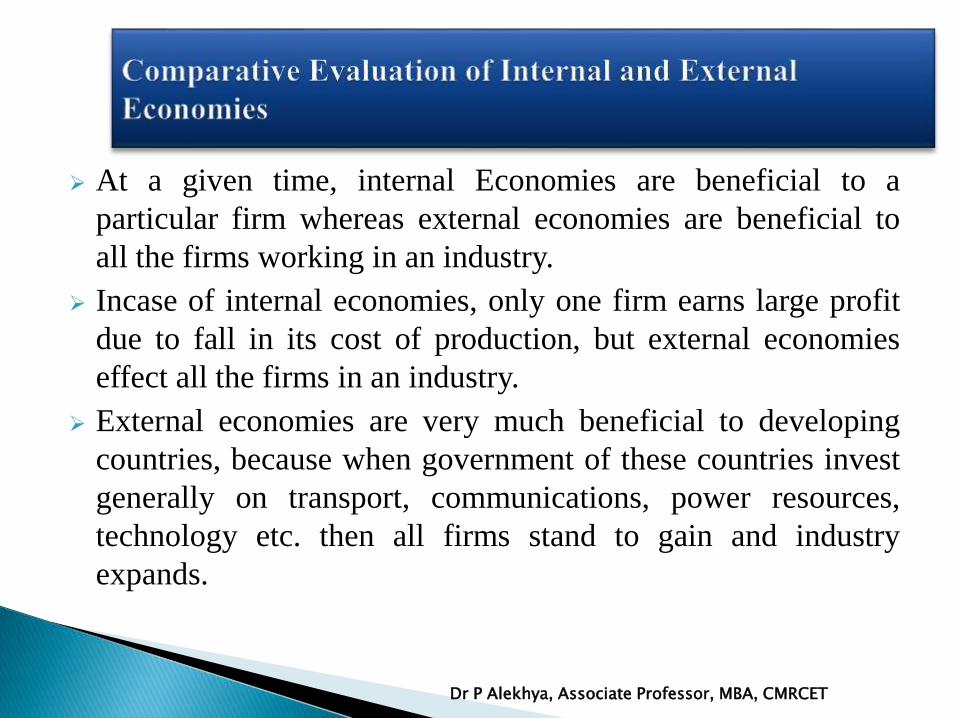

At a given time, internal Economies are beneficial to a

particular firm whereas external economies are beneficial to

all the firms working in an industry.

Incase of internal economies, only one firm earns large profit

due to fall in its cost of production, but external economies

effect all the firms in an industry.

External economies are very much beneficial to developing

countries, because when government of these countries invest

generally on transport, communications, power resources,

technology etc. then all firms stand to gain and industry

expands.

Dr P Alekhya, Associate Professor, MBA, CMRCET

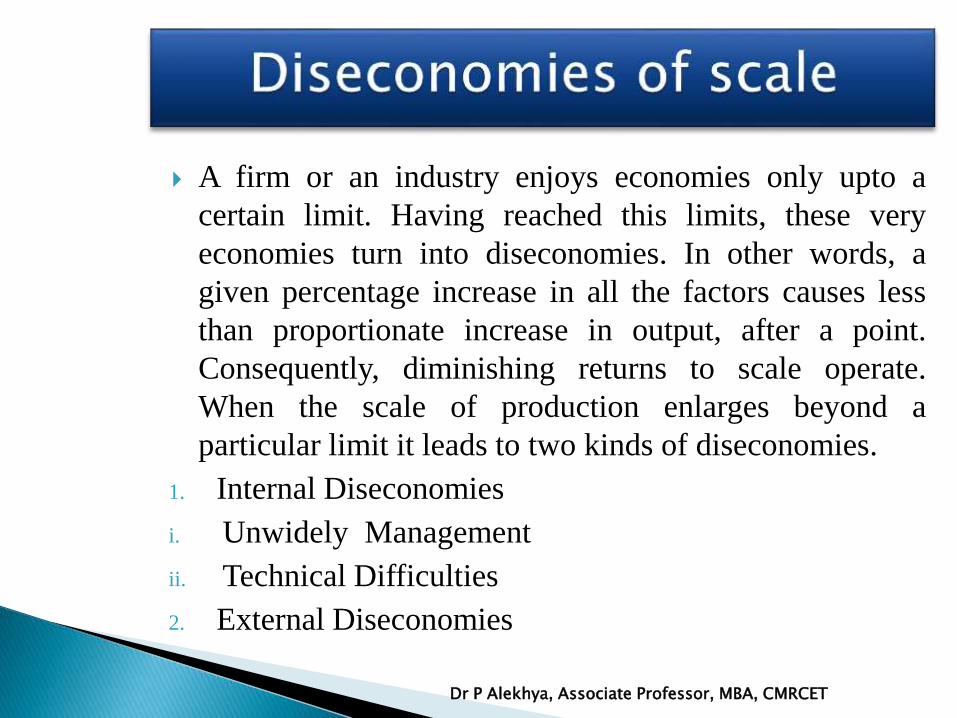

A firm or an industry enjoys economies only upto a

certain limit. Having reached this limits, these very

economies turn into diseconomies. In other words, a

given percentage increase in all the factors causes less

than proportionate increase in output, after a point.

Consequently, diminishing returns to scale operate.

When the scale of production enlarges beyond a

particular limit it leads to two kinds of diseconomies.

1. Internal Diseconomies

i. Unwidely Management

ii. Technical Difficulties

2. External Diseconomies

Dr P Alekhya, Associate Professor, MBA, CMRCET

Laws of returns Returns to scale

It applies in short period It applies in the long period

It applies when only one factor is variable and all other factors are fixed.

It is operative when all factors are variable

Dr P Alekhya, Associate Professor, MBA, CMRCET

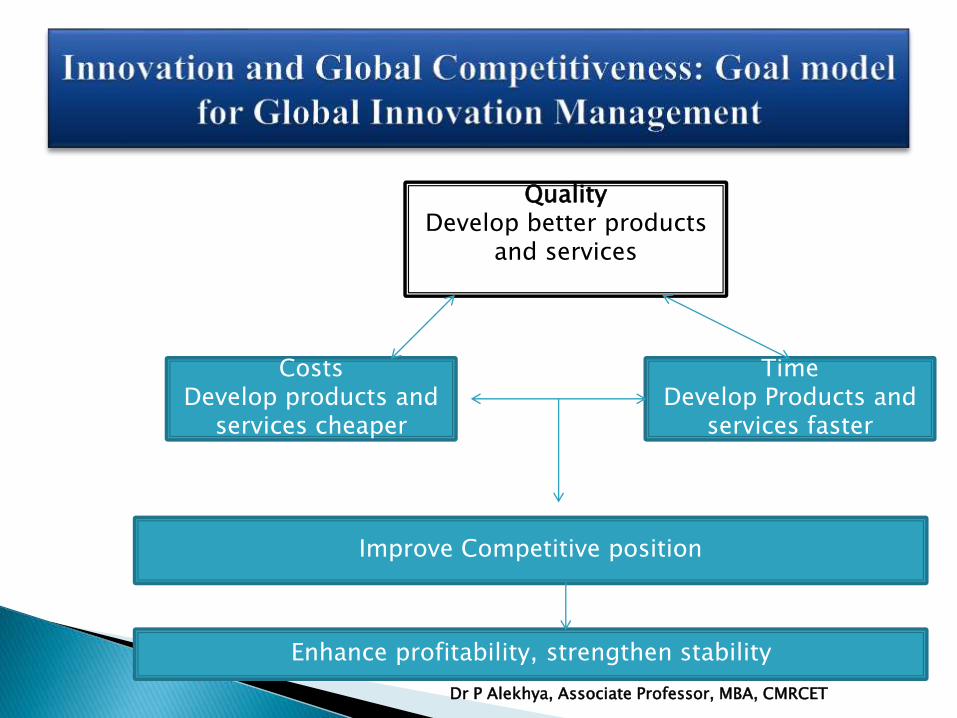

QualityDevelop better products

and services

Costs Develop products and

services cheaper

TimeDevelop Products and

services faster

Improve Competitive position

Enhance profitability, strengthen stability

Dr P Alekhya, Associate Professor, MBA, CMRCET

Access to knowledge(Getting access

to skilled Knowledge resources and

specialised know-how in clusters

and lead markets)

Local adaptation ( addressing the needs and

aspirations of a target market: global product

with local flair)

Financial incentives(general resources

by international business

development while reducing costs of the R&D efforts

Global Innovation Activities

Stable Innovation Capacity and Global Competitiveness

Dr P Alekhya, Associate Professor, MBA, CMRCET

Cost Theory and estimation:

Cost Concept

Types of Cost

Determinants of Cost

Cost Function

Factors Effecting Cost

Importance of Cost Analysis in Managerial Decision Making

Cost –Output Relationship in the short run and long run

Cost Output Relation under short-run

Cost-Output Relation under long-run

Dr P Alekhya, Associate Professor, MBA, CMRCET

Short Run Vs. Long Run Costs

Average Cost Curves

Importance of Cost curve

Why is LAC Curve U-shaped

Overall cost Leadership

Cost Estimation

Methods of Cost Estimation

Problems of cost Estimation

Dr P Alekhya, Associate Professor, MBA, CMRCET

In managerial economics, usually cost is taken into consideration

from the producer’s or firm’s perspective. While producing a

commodity or service, a firm would need a collection of different

factors of production i.e land, labour, capital and organisation. These

factors are rewarded by the firm in return of their efforts or their

contribution made in producing the products. This reward is known as

cost. Therefore, the cost of production of a commodity is the total of

price which is being paid for the factors of production which are used

in producing that product.

Cost of production indicates the value of the factors of production

that are used. Hence, the value of inputs needed in the production of a

good determines its cost of output. The term “cost” involves different

concepts like,

Real cost

Opportunity Cost

Money CostDr P Alekhya, Associate Professor, MBA, CMRCET

Cost is defined as those expenses faced by a business in the process

of supplying goods and services to consumers. In economics, the

cost of production is the value that the price of an object or

condition is determined by the sum of the cost of the resources that

went into making it. The cost can compose any of the factors of

production (including labour,capital,land or entrepreneur) and

Taxation.

According to campbell, “Production costs are those which must be

received by resource owners in order to assume that they will

continue to supply them in a particular time of production.”

Dr P Alekhya, Associate Professor, MBA, CMRCET

1. Actual Cost

2. Opportunity Cost

3. Sunk Cost

4. Incremental Cost

5. Explicit Cost

6. Implicit Cost or Imputed Costs

7. Book Cost

8. Out-of-Pocket costs

9. Accounting Costs

10. Economic Costs

Dr P Alekhya, Associate Professor, MBA, CMRCET

11. Direct Cost

12. Indirect Cost

13. Controllable Costs

14. Non-Controllable Costs

15. Historical Cost and Replacement Cost

16. Abandonment Costs

17. Urgent Costs and Postponable costs

18. Business Cost and Full Cost

19. Fixed Costs

20. Variable Costs

Dr P Alekhya, Associate Professor, MBA, CMRCET

Level of Output

Price of input Factors

Productivities of Factors of Production

Size of Plant

Output Stability

Lost Size

Laws of returns

Levels of capacity Utilisation

Time Period

Technology

Experience

Process of range of Products

Supply Chain and logistics

Government Incentives

Dr P Alekhya, Associate Professor, MBA, CMRCET

The concept cost function refers to the mathematical relation betweencost of a product and the various determinants of costs. In costfunction the dependent variable is unit cost or total cost and theindependent variables are the price of a factor, the size of the output orany other relevant phenomenon, which has a bearing on cost.symbolically we may state the function as:

C= f (O,S,T,U,P……)

Where,

C=Cost

O=Level of Output

S=size of Plant

T=Time under consideration

P=prices of factors of production

Dr P Alekhya, Associate Professor, MBA, CMRCET

Law of returns Operating

Size of the plant

Period

Capacity Utilisation

Prices of Factors of Production

Technology

Efficiency in the use of inputs

Lot size of the product

Output is stable and constant

Dr P Alekhya, Associate Professor, MBA, CMRCET

Product costing and pricing decisions

Costs Management

Profit Planning

Capital Investment Decisions

Marketing Decisions

Dr P Alekhya, Associate Professor, MBA, CMRCET

The theory of cost deals with the behaviour of cost in relation to a

change in output. In other words, the cost theory, deals with cost

output relations.The basic principle of the cost behaviour is that the

total cost increases with increase in output.This simple statement of an

observed fact is of little theoretical and practical importance. What is

of importance from theoritical and managerial point of view is not the

absolute increase in the total cost but the direction of change in the

average cost and the managerial cost.

Cost-output Relation under short-run

Cost-output Relation under Long-run

Dr P Alekhya, Associate Professor, MBA, CMRCET

Basis of Difference Short Run Costs Long Run Costs

Time period The short run is a period of

time in which output can be

increased or decreased by

changing only variable cost

The long run is defined as a

period in which quantities of

all factors are variable. No

factor is fixed

Expansion No increase in short run output

can be made by expanding the

existing plants and equipments

In the long run output can be

expanded not only by

increasing labour and raw

materials but also by

expanding the size of plants

and equipments

Produce output In short run a firm produces

output at a higher point on its

short run marginal cost curve.

The firms under long run

produce at another cost curve

called long period curve. In

long period a firm is at will to

produce or to leave the

industry

Technology In short run costs production

technology is given

Long run can adopt production

technology in marketDr P Alekhya, Associate Professor, MBA, CMRCET

1. Decision regarding production

2. Choice of plants

3. Equilibrium Output

4. Estimate of profit and loss

Dr P Alekhya, Associate Professor, MBA, CMRCET

1. Economies of Scale

i. Division and specialisation of labour

ii. Technical Economies

iii. Economies of indivisibility

2. Diseconomies of Scale

Dr P Alekhya, Associate Professor, MBA, CMRCET

In an Industry, cost leadership position would be achieved a competitive firm with the help of the following.

1. Cost control measures

2. Avoiding wastages

3. Better supervision on the workers

4. Use of less expensive/Costly source of capital and required finance. Financial management at low-cost.

5. Emphasis on quantitative targets for the business expansion by assuring that the cost is maintained at the minimum level

Porter suggested two generic level strategies in the modern business

Product Differentiation

Cost Leadership

Dr P Alekhya, Associate Professor, MBA, CMRCET

Economies of scale

Learning curve Effect

Internationalisation

Technological Acquisition and Improvement

Access to low cost Inputs

Knowledge Management

Cost conscious organisational culture

Threat of new entry

Threat of rivalry

Threat of substitutes

Threat of suppliers

Threat of buyers

Dr P Alekhya, Associate Professor, MBA, CMRCET

Meaning Of Cost Estimation

Methods of cost Estimation

Accounting Method

Statistical Techniques

Econometric Models

Statistical Models

Survivorship Method

Engineering Method

Dr P Alekhya, Associate Professor, MBA, CMRCET

1. Time Period

i. Normality

ii. Variety

iii. Recent Period

iv. Units of Observation

2. Technical Homogeneity

3. Cost Adjustments

i. Selection of Cost data

ii. Cost Deflation

4. Economic versus Accounting cost data

5. Changing in Accounting Practices

Dr P Alekhya, Associate Professor, MBA, CMRCET

Market:

Meaning & Definition of Market

Features of Market

Classification of Market

Market Structure

• Determinants of Market Structure

• Types of Market Structure

Perfect Competition

Features of Assumptions of Perfect Competition

Advantages and Disadvantages of Perfect Market

Price output Determination in Perfect Competition

Monopoly

• Characteristics of Monopoly

• Sources of Monopoly Power

• Price-Output Determination under Monopoly

Dr P Alekhya, Associate Professor, MBA, CMRCET

Advantages and Disadvantages of Monopoly

Comparison between Perfect Competition and Monopoly

Monopolistic Competition

• Features of Monopolistic Competition

• Product Differentiation

• Price-Output Determination in Monopolistic Competition

• Advantages and Disadvantages of Monopolistic Competition

Oligopoly

• Features of Oligopoly

• Classification of Oligopoly

• Price and Output Determination in Oligopoly

The Kinked Demand curve Market

Price Determination Under Collusive Oligopoly

• Price Leadership Model of Oligopoly

• Evil of Oligopoly

• Price of Determination types under oligopoly

Dr P Alekhya, Associate Professor, MBA, CMRCET

• Limit Pricing Models of Oligopoly

• Emergence of Oligopoly

Comparison of Various Market Structure

Pricing Philosophy

Pricing Objectives

Steps for Developing the Pricing

Price Discounts Types

Methods of Pricing

Factors Involved in Pricing Policy

Price as a weapon of Competition

Price Discrimination

Pricing of Multiple Products

Dr P Alekhya, Associate Professor, MBA, CMRCET

Meaning & Definition of monopoly

According to D. Salvatore, “Monopoly is the form of market

organisation in which there is a single firm selling a commodity for

which there are no close substitutes”.

In the words of Baumol, “ a pure monopoly is defined as the firm

that is also an industry. It is the only supplier of some particular

commodity for which there exists no close substitute.”

Dr P Alekhya, Associate Professor, MBA, CMRCET

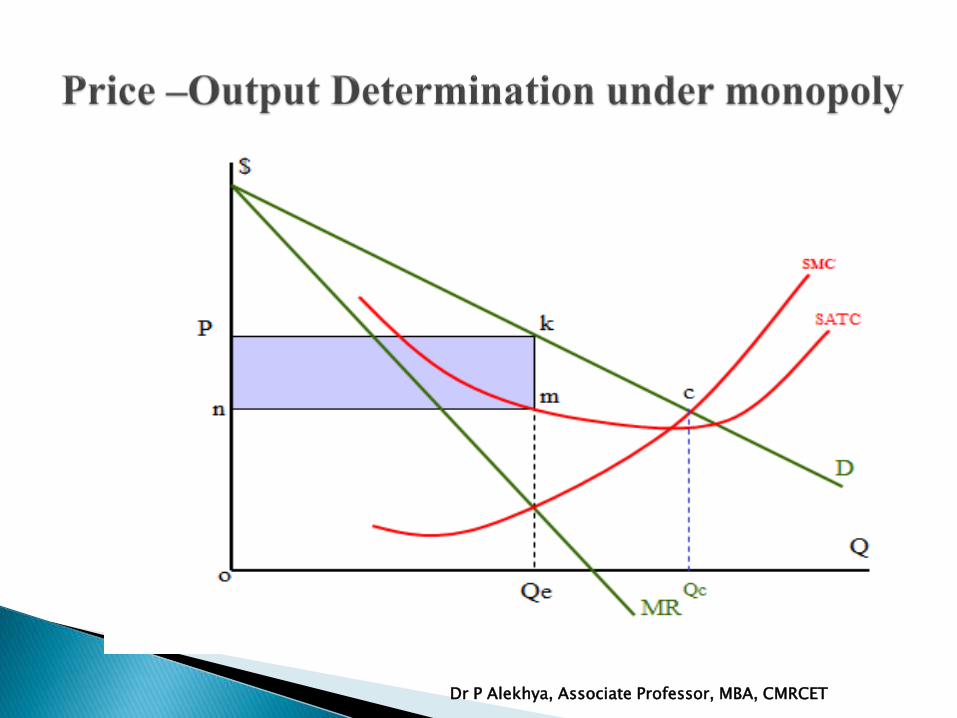

Single seller

No close Substitutes

No Entry for New firms

Profit in the Long Run

Losses in the short period

Nature of Demand curve

Price Discrimination

Firm is a Price –Maker

Average and Marginal Revenue Curves

Dr P Alekhya, Associate Professor, MBA, CMRCET

Patent rights for the products or production processes give legal monopoly rights to firms.

Government Policies such as granting licencesor imposing foreign trade restrictions (like quotas.,)result in limiting the number of sellers.

Ownership and control of some strategic raw materials

Exclusive knowledge of technology by the firm.

Technological Superiority

Economic Barriers

Dr P Alekhya, Associate Professor, MBA, CMRCET

Dr P Alekhya, Associate Professor, MBA, CMRCET

Advantages

• Research and Development

• Economies of Scale

• Competition for corporate control

• Stability of prices

• Sources of Revenue for the Government

• Massive Profits

Disadvantages

•Exploitation of consumers

•Dissatisfied Consumers

•High Prices

•Price Discrimination

• Inferior Goods and services

•Prices and Costs

Dr P Alekhya, Associate Professor, MBA, CMRCET

Comparison Perfect Competition Monopoly

Relation between AR AR=MR AR>MR

Profits in the Long run

Normal profits in the long run

Supernormal Profits in the long run

Number of Sellers Large number of sellers

Single seller

Barriers to entry and Exit

Free entry and Exit, as there are no barriers

There are strong barriers

Control on price taker

The seller is only the price inelastic

Monopolist is the price maker

Nature of demand curve

Perfectly elastic Inelastic

Relationship Between firm and Industry

Each firm is a part of the industry

Firm and industry are one and the same.

Dr P Alekhya, Associate Professor, MBA, CMRCET

According to J.S Bains, “Monopolistic competition

is market structure where there is a long number of

sellers, selling differentiated but close substitute

products”.

According to Buemoul, The term monopolistic

competition refers to the market structure in which

the sellers do have a monopoly of their own

products, but they are also subject to substantial

competitive pressures from sellers of substitute

product.”

Dr P Alekhya, Associate Professor, MBA, CMRCET

Large Number

Close Substitutes

Group

Product Differentiation

Selling Cost

Dr P Alekhya, Associate Professor, MBA, CMRCET

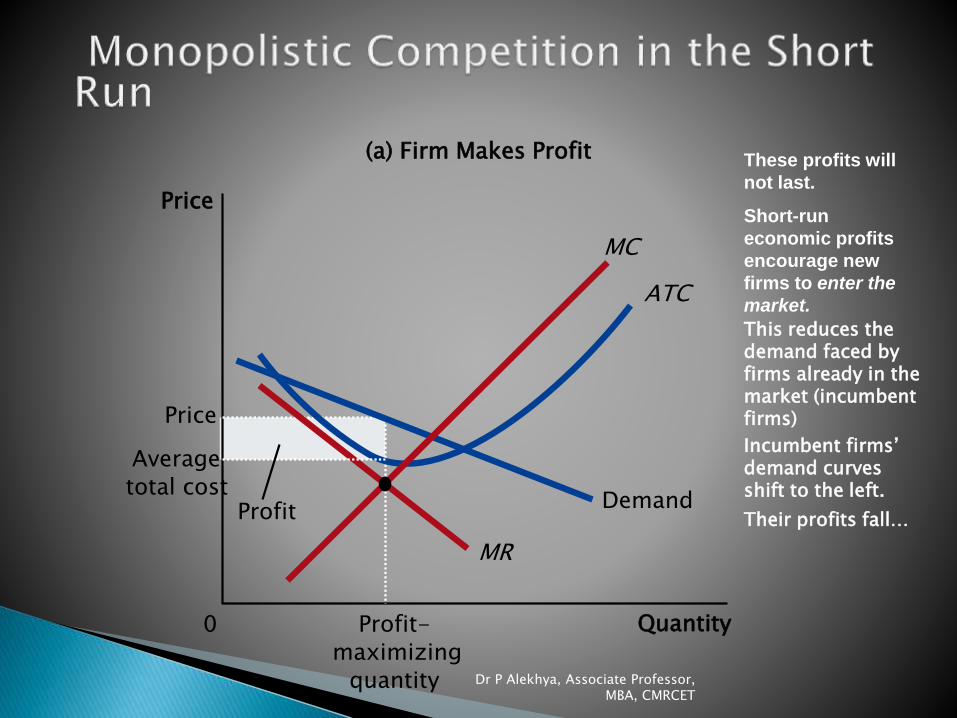

Quantity0

Price

Profit-

maximizing

quantity

Price

Demand

MR

ATC

(a) Firm Makes Profit

Average

total costProfit

MC

These profits will

not last.

Short-run

economic profits

encourage new

firms to enter the

market.

This reduces the demand faced by firms already in the market (incumbent firms)

Incumbent firms’ demand curves shift to the left.

Their profits fall…

Dr P Alekhya, Associate Professor, MBA, CMRCET

Quantity0

Price

Profit-

maximizing

quantity

Demand

MR

ATC

(a3) Firm Makes No Profit

Price = ATC

MC

Zero profit

Dr P Alekhya, Associate Professor, MBA, CMRCET

Advantages

•Promotion of Competition(Lack of

barriers to entry)

•Differentiation brings greater

consumer choice and variety

•Product and service Quality

development

•Consumers become more

knowledgeable of products

Disadvantages

•Liable of Excess capacity

•Allocatively Inefficient

•Higher Prices

•Advertising

Dr P Alekhya, Associate Professor, MBA, CMRCET