Managed Funds in Australia 2008 - TAFE NSW · Australia’s hedge funds industry has approximately...

56

Managed Funds in Australia 2008 www.austrade.gov.au/financialservices

Transcript of Managed Funds in Australia 2008 - TAFE NSW · Australia’s hedge funds industry has approximately...

Managed Funds in Australia 2008

www.austrade.gov.au/financialservices

Contents

Managed Funds in Australia 3

SizeoftheMarket 3

CharacteristicsoftheMarket 4

AnticipatedGrowth 5

Superannuation 6

GrowthofAustralia’sSuperannuationPool 6

TypesofSuperannuationFundsinAustralia6

BenefitStructures 8

MemberChoice 9

SuperannuationFundAssetAllocation 10

FutureFund 11

Other Fund Management Products 12

PublicUnitTrusts 12

LifeInsuranceProducts 12

IndexFunds 13

ExchangeTradedFunds 13

HedgeFunds 14

PrivateEquityandVentureCapital 15

SociallyResponsibleInvesting 17

StructuredProducts 17

OverlaysandAlphaTransfer 17

The Managed Funds Industry 18

AssetsUnderManagement 18

FundSources 19

AssetAllocation 20

FundManagers 21

WholesaleandRetailAssetsUnder 23Management

LifeInsuranceOffices 24

FundManagementFees 26

Other Industry Participants 28

AssetConsultants 28

TenderConsultants 29

FinancialPlannersandFinancial 29AdvisoryNetworks

Platforms,MasterTrustsand 31WrapAccounts

ThirdPartyRepresentatives 32

Custodians 32

ResearchHousesandRatingAgencies 33

ServiceProviders 33

Regulatory Environment 34

Framework 34

RegulationofFinancialService 35Businesses

RegulationofManagedFundsand 35FundManagers

OtherRegulatorsandIndustryBodies 37

MoneyLaunderingLaw 38

Appendix A: Australia’sRetirementIncomeSystem 39

Appendix B: OfferingSuperannuationProducts 42inAustralia

Appendix C: OperatingaManagedInvestmentScheme 44inAustralia

Appendix D: TaxationTreatmentofManaged 47InvestmentSchemeswhichareUnitTrusts

Appendix E: InternationalTaxationRegime 50

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 1

ManagedFundsTheAustralianfundsmanagementindustryisnowoneofthemajormarketsformanagedfundsintheworld,withtotalfundsundermanagementofA$1.3trillion(1)(US$1.1trillion)(2)inJune2007.Conservativeindustryestimatesforecastthattotal fundsundermanagementwillgrowtoaroundA$2.5trillion (US$2trillion)by2015.(3)

The growth of themanaged funds industry in Australia has been underpinned by a number of factors: asophisticated investor base, maturemarkets, participation by leading global financial institutions, cuttingedgeinvestmentproducts,anefficientregulatoryenvironmentandmost importantly,Australia’s innovativeretirement income (superannuation) system. The Superannuation Guarantee Scheme introduced in 1992requiresthatemployerspayninepercentofanemployee’searningsbase(broadlyequivalenttosalary)intoasuperannuationfundorretirementsavingsaccount.Superannuationfunds(oftenreferredtoaspensionfundsinothercountries)nowdominatethelocalindustry.InJune2007,superannuationinvestments(includingfundsheldwithinlifeoffices)representedapproximately75percentofmanagedfunds(unconsolidated)ataroundA$1.2trillioninassets.

OtherFundManagementProductsInadditiontotraditionalinvestmentmanagementproducts,ariseinthevolumeoffundsundermanagement,together with increasing investor sophistication, has driven a marked increase in demand for alternativeinvestments.Hedgefunds,infrastructureinvestment,listedandunlistedpropertyandprivateequityaresectorswithparticularpotential.

Australia’s hedge funds industry has approximately A$70.3 billion in funds under management. Industryanalystsexpectthistogrowstronglyoverthenextfiveyearsasinstitutionalinvestors,especiallysuperannuationfunds,seektoincreasetheirallocationtothesector.Australiaalsohasathrivingprivateequitysector,spanningde-listingsoflargelistedcompaniesthroughtograssrootsinvestmentinventurecapital.Inrecentyears,theAustralianGovernmenthasintroducedanumberoffarreachingchangestothetaxtreatmentofventurecapitalinvestments,withthegoalofenhancingtheindustry’sinternationalcompetitiveness.

FundManagersThestronggrowthinlocalmanagedfundshasledtoanincreaseinspecialistfundmanagers.Therearecloseto 120 significant fundmanagement firms(4) operating in Australia, aswell as a large number of smallerboutiquefirms.AnumberofglobalfundmanagementorganisationshavechosenAustraliafortheirAsia-Pacificheadquarters,includingVanguard,RussellInvestmentGroupandFidelityInvestments.

ExecutiveSummary

(1) AustralianBureauofStatistics,cat.no.5655.0,Managed Funds,June2007.(2) TheUS$/A$exchangeratewasUS$0.8487asat29June2007(sourcedfromReserveBankofAustraliastatistics).(3) Standard&Poor’sInvestmentConsulting.(4) ManagerswithfundsthathavemorethanA$100millioninfundsundermanagement,InvestorSupermarket,June2007.

PAgE 2 | MAnAgED FunDS In AuSTRAlIA 2008

RegulationAustraliaaspirestoglobalbestpracticeinitsfinancialservicesregulatoryframework.Thiswasamotivatingfactorbehind thesignificant structural changes to regulatoryarrangementsenacted in1997 following theFinancialSystemsInquiry.FurtherreformstotheprudentialframeworkthroughtheFinancial Services Reform Act (FSRA) in 2002 cemented the reputation of Australia’s financial services industry as being among themostefficientlyregulatedintheworld.

The regulation of financial products depends critically on a distinction between superannuation and non-superannuation products. Regulation of superannuation funds generally focuses on prudential standardsandensuringtheproperend-useoffunds.SuperannuationfundsareregulatedbytheAustralianPrudentialRegulationAuthority(APRA)undertheSuperannuation Industry (Supervision) Act 1993 (SIS)andtheAustralianSecurities and InvestmentsCommission (ASIC) under the Corporations Act 2001. The only exception is selfmanaged superannuation funds (SMSFs),which are regulated by the AustralianTaxationOffice (ATO). Thekey regulatory agency for non-superannuation products is ASIC. This agency has supervisory powers overthemanagedfundsindustryandisresponsibleforissuingAustralianFinancialServicesLicences(AFSLs)andregisteringmanagedinvestmentschemes.

TheFutureThecompulsorycontributionsintosuperannuationtogetherwithtaxadvantagedvoluntarycontributionswillcontinuetosupportthestronggrowthofthemanagedfundsindustryinAustraliaandwillbeakeydriverofthehealthandvitalityofthewiderfinancialservicessector.Thehealthymixofdomesticandglobalplayers,aswell as anopen-mindedand innovative culture,helps keepAustraliaat the cuttingedgeofglobal fundmanagement practices. Together with recent tax and regulatory reforms, these factors will help providea competitive and efficientmarket. The Australianmarket should not be assessed purely on its domesticpotential,butasapotentialpowerhouseintheworld’sfastestgrowingregion–theAsia-Pacific.

‘Australianowpunchesaboveitsweightinglobalfinancialservices.Thisisdespiteitsrelativelysmallpopulationof20millionanditsdistancefromthemainEuro-Atlanticmarkets.Astheworld’scentreofgravityshiftstowardsAsiainthe21stcentury,Australiaanditsfinancialsectorappearwellpositionedtoincreaseinstrategicrelevance.’

SunDEEP TuCkER, FInAnCIAl TIMES, SEPTEMBER 6, 2006

0

200

400

600

800

1,000

1,200

1,400

June 1988

June 1989

June 1990

June 1991

June 1992

June 1993

June 1994

June 1995

June 1996

June 1997

June 1998

June 1999

June 2000

June 2001

June 2002

June 2003

June 2004

June 2005

June 2006

June 2007

SizeoftheMarketInJune2007AustraliahadA$1.3trillion(US$1.1trillion)infundsundermanagement.Duringthe1990s,thevolume of funds undermanagement increased almost three-fold, with funds undermanagement almostdoublingoverthesecondhalfofthedecade.ThisperformanceowesmuchtotheintroductionofAustralia’sretirement incomesystemin1992(seeAppendixA),whichhasbeenhailedasoneofthemostprogressiveGovernment-led retirement provision policies in the world. This system has received praise from manyobservers, includingthe InternationalMonetaryFund(IMF)andtheOrganisationforEconomicCooperationandDevelopment(OECD).

TherapidexpansioninfundsundermanagementhasresultedinAustraliahavingoneoftheworld’slargestcontestable investment pools. While differences in coverage and definitions make precise cross countrycomparisonof investmentmarketsdifficult, aglobal surveyofmutual funds conductedby the InvestmentCompanyInstitute(ICI)rankedAustraliaashavingthefourthlargestonshoremanagedfundsmarketintheworldinMarch2007.Australia’sfundsundermanagementhavegrownmorethan460percentsince1992,withacompoundannualgrowthrateof12.2percent.(5)

Sources: Reserve Bank of Australia, Statistical Table, Managed Funds, Table B18; Department of Innovation, Industry, Science and Research (DIISR)

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 3

ManagedFundsinAustralia

(5) CompoundannualgrowthratefromJunequarter1992toJunequarter2007inA$terms.

Australia’s Managed Funds – June 1998 to June 2007

(Consolidated Assets, A$ Million)

CharacteristicsoftheMarketTheAustralianmarkethascometobedominatedbyassetsinvestedinsuperannuationfundsandproducts.Thechartbelowshowsthataround75percentofthetotalassetsundermanagement(unconsolidated) inAustraliaareinvestedinthesuperannuationenvironment.

Source: Reserve Bank of Australia, Statistical Table, Managed Funds, Table B18

TheAustralianmanagedfundsmarketishighlyintermediated.DespitestrongrecentgrowthinSMSFs,mostsuperannuationassetsremaininarelativelysmallnumber(around500)ofretail,publicsector,corporateorindustry-related funds. The rise of investment platforms (includingmaster trusts andwrap accounts) hasalsoseenthenon-superannuationinvestmentsofindividualsmergedintoinstitutionalinvestmentvehicles.Moreover, many individual investors employ the services of a financial planner for advice on investmentstrategy,fundselectionandotherfinancialmatters,particularlyastheynearretirementorencounterotherkeyfinancialdecisionpoints.

Direct holdings of share investments represent a small proportion of total investment assets, howeverprivatisations(e.g.Telstra,Qantas)andthede-mutualisationoflargeinsuranceentities(e.g. IAG,AMP)havewidenedtherangeofdirectshareinvestors.Directshareownershippeakedin2004,whenapproximately44percentofadultAustraliansheldsharesdirectly.Participationdeclinedto38percentby2006,howeverafurthereightpercentheldsharesthroughaSMSF.(6)

Australia’s Managed Funds – June 1998 to June 2007

0

200

400

600

800

1,000

1,200

1,400

1,600

June 1988

June 1989

June 1990

June 1991

June 1992

June 1993

June 1994

June 1995

June 1996

June 1997

June 1998

June 1999

June 2000

June 2001

June 2002

June 2003

June 2004

June 2005

June 2006

June 2007

Superannuation Non-Superannuation

Total unconsolidated Assets, A$ Million

(6) AustralianStockExchange,Australian Share Ownership Report,2006.

PAgE 4 | MAnAgED FunDS In AuSTRAlIA 2008

AnticipatedGrowthSubstantialandsustainedgrowthinthemanagedfundsindustryisexpected,withanalystspredictingaverageannualgrowthofmorethan10percent.Bi-partisansupportfortheAustralianGovernment’sretirementincomesystem, includingpreferentialtaxtreatmentofsuperannuation,willencouragecontinuedstrongflows intosuperannuationproducts.Inaddition,agrowingawarenessoftheadvantagesoffundmanagementproductsovermoretraditionalsavingsvehicleswillcontinuetodrivegrowthinthebroaderindustry.Averageannualgrowthof10percentwouldtaketheinvestmentpooltooverA$2.5trillion(US$2trillion)by2015.ThiswillputpressureonlocalinvestorstofindnewwaystoemploytheircapitalprofitablybutequallyrepresentsanunprecedentedopportunityforentrantstotheAustralianmarkettoattractcapitalandgrow.(7)

RecognitionoftheopportunitiescreatedbythegrowthinfundsundermanagementisthekeydriverfortheincreasednumberofglobalindustryparticipantsseekingtoestablishandbuildfundsmanagementoperationsinAustralia.Thesizeofthedomestic industry,togetherwiththeavailabilityofahighlyskilled,multilingualworkforce, the strategic time zone and access toworld class infrastructure, have proven critical factors inthe decision by global investment houses and service providers to establish regional fund managementoperationsinAustralia.

(7) DEXX&R,Market Projections Report,2006;Standard&Poor’sInvestmentConsulting;AssumptionA$1=US$0.80.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 5

‘AsiaandAustraliawillaccountforthemajorityofnetnewbusinessinfundsmanagement by 2012, representing 30 per cent of global assets undermanagement.’

BEnJAMIn F. PHIllIPS, MAnAgIng DIRECTOR, FIg STRATEgIC AnAlYSIS, DECEMBER 2007

GrowthofAustralia’sSuperannuationPool‘Superannuation’ is the term used in Australia to describe the setting aside of income for retirement.‘Superannuationfund’isatermthatincludesinvestmentvehiclesmorecommonlyknowninothercountriesas ‘pension funds’, aswell as certain funds directed at the retail segment of the superannuationmarket.The increasingly important role played by superannuation in the managed funds industry over the pastfifteenyearsisadirectresultofthesignificantrestructuringofAustralia’sretirementincomesystembytheAustralianGovernmentinthemid-1980sandearly1990s(seeAppendixA).

The introductionoftheSuperannuationGuaranteeSchemehasbeen largelyresponsibleforthe increase insuperannuation contributions by employees from around 40 per centwho contributed to superannuationin themid-1980s toover90per cent today.Australiaposted thehighestgrowth rate in assets invested insuperannuationinaWatsonWyattsurveyofmajorpensionmarketsfrom1996to2006.

TypesofSuperannuationFundsinAustraliaTherearemanytypesofsuperannuationfundsinAustralia:

nCorporate fundsaresponsoredbyasingleemployerorgroupofrelatedemployersandoftenprovidejointmemberandemployercontrol.Contributionsaremadebytheemployersandemployeesofrelatedfirms.

nIndustry funds are sponsored by unions and employer organisations. Many originated from industrialworkplacearrangements,butnowhaveabroaderrole,andinmanycaseshaveopenedfundmembershiptothegeneralpublic.

nPublic sector funds providebenefitsforgovernmentemployees.Theyaresponsoredbyagovernmentagencyoragovernmentcontrolledbusinessenterprise(atAustralian,StateorLocalgovernmentlevel).

nSmall APRA Funds(SAFs)arefundswithfewerthanfivemembersthathaveanAPRAlicensedtrustee.

n Self managed superannuation fundsmust alsohave fewer thanfivemembers.They are typically usedbyindividualsorfamilymemberswhodesiregreatercontrolovertheirsuperannuationinvestmentsandgreaterflexibilityintaxplanning.Allmembersarerequiredtobetrustees.ManySMSFsaretaxplanningvehiclesadvisedbyaccountantsandfinancialplanners.Inlate1999,theATOtookovertheregulationofthesefundsfromAPRA.

Superannuation

Total Australian Funds under Management – Type of Institution (A$ Million)

Superannuation life Public Cash Common Friendly Funds Insurance unit Management Funds Societies unconsolidated ConsolidatedAt the end of Offices(a) Trusts Trusts

Jun-1992 101,587 103,124 25,599 5,344 4,373 8,988 249,015 238,478

Jun-1997 205,062 145,494 66,449 15,028 6,252 7,262 445,547 397,960

Jun-2002 372,737 201,698 153,572 33,023 7,941 6,034 775,005 649,959

Jun-2007 933,400 263,740 300,648 46,745 12,093 7,185 1,563,811 1,334,673

CAGR–%Since1992 15.9 6.5 17.8 15.6 7.0 -1.5 13.0 12.2

CAGR=CompoundAnnualGrowthRate

(a)Figuresincludesuperannuationfundsheldinthestatutoryfundsoflifeinsuranceoffices.

Sources: Reserve Bank of Australia, Statistical Table, Managed Funds, Table B18; DIISR

TOTAl OF All FunDS

PAgE 6 | MAnAgED FunDS In AuSTRAlIA 2008

nRetail fundsarepubliclyofferedsuperannuationfundsthatmembersjoineitherthroughgrouparrangementsestablished by employers or by purchasing investment units or policies that are distributed throughintermediaries,suchaslifeinsuranceagentsorfinancialplanners.

nRetirement Savings Accounts(RSAs),firstintroducedin1997,arecapital-guaranteedsuperannuationproductsofferedtoindividualsbyfinancialinstitutions.Theyaresubjecttothesameretirementincomestandardsasothersuperannuationproducts.

Source: Australian Prudential Regulation Authority, Statistics, Quarterly Superannuation Performance, June 2007

The classification of superannuation funds by fund type has become somewhat blurred in recent years.Legislationnow requiresmost employers to offer their employees choice overwhere their superannuationcontributionsare invested.Thishasseenanumberof larger fundsacquireanAFSL,orbecomepublicofferfunds competing for newmembers in thismore openmarketplace. At the same time, the introduction ofstringentlicensingarrangementsandanassociatedtighteningofprudentialrequirementshaveencouragedarationalisationinthenumberofmediumandsmallcorporatefundsinthepastthreeyears.Itisestimatedthatthenumberofcorporatefundshasfallenfromalmost4,000inJune1998toaround1,400inJune2004andlessthan300inJune2007,withmanyemployerschoosingtonominateanindustryfundoraretailfundasthedefaultfundfortheiremployees.Thenumberofindustryandpublicsectorfundshasalsofallen.Inmostcasesthishasbeendrivenbyfundmergersor,inthecaseofsomepublicsectorfunds,byfundclosuresresultingfromprivatisationorotherchangestotheemployerorganisation.Muchofthisrationalisationhasoccurredamongtheranksofthesmallercorporate,industryandretailfunds,whichhavesoughtscaleinordertocompetemoreeffectivelyformembers.ThusthenumberoffundswithassetsgreaterthanA$50millionhasremainedrelativelystableoverthepastfiveyears.(8)

Distribution of Superannuation Funds by Fund Type – June 2007

Assets A$ Billion number of Entities

By Fund Type

Corporate 71.9 290

Industry 198.1 75

PublicSector 177.5 39

Retail 372.0 171

Sub Total 819.5 575

PooledSuperannuationTrusts 81.1 101

SmallAPRAFunds 3.3 6,017

Single-memberApprovedDepositFunds(ADFs) 0.2 150

SelfManagedSuperannuationFunds 287.7 359,370

BalanceofLifeOfficeStatutoryFunds 42.6 –

Total 1153.3 366,213

(8) AustralianPrudentialRegulationAuthoritystatistics,supplementedbyR.Clare,AssociationofSuperannuationFundsofAustralia,The Shape of Things to Come,presentationto14thColloquiumofSuperannuationResearchers,UniversityofNewSouthWales2006.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 7

Anumberoflargepublicsectorandindustrysuperannuationfundshavedevelopedin-houseinvestmentteamsoverthepastdecade.Insomecasestheseteamsmanageassetsdirectly,butmostoutsourcemanagementofthemajorityofassetstoexternalfundmanagementfirms.Theselargesuperannuationfundsoftenactivelybenchmarktheirprocessesagainstlarge-scalepeersinothermarketssuchastheUSandEurope.

BenefitStructuresIncreasinglythe investmentriskassociatedwithsuperannuation isbeingborneby individuals.Upuntil theearly1980s,a largeproportionof individualswithsuperannuationwere indefinedbenefitschemes,whereanemployerpromisestofundadefinedbenefituponretirement–usuallyrelatedtofinalsalaryandyearsofemployment.Essentially,theemployerwouldbeartheinvestmentrisk,increasingcontributionsifinvestmentreturnswerelowanddecreasingthemifinvestmentreturnswerehigh.However,overthepastdecadetherehasbeenadeliberateandsignificantmovetowardaccumulationfundstructures,wherethemembersbeartheriskandbenefitsofbeingexposedtovariationsininvestmentreturns.BytheendofJune2006,around45percentoftheassetsinAPRA-regulatedsuperannuationfundswithmorethanfourmemberswereinaccumulation-typefunds.Afurther46percentwereinfundswithahybridstructure,inwhichmembersbearinvestmentrisktoeitherpartoralloftheirsuperannuationbalance.(9)Somehybridfundshaverelativelysmalldefinedbenefitdivisionswhichareclosedtonewmembers,withmostmembersinaccumulationarrangements.

Bothemployersandemployeeshavefoundaccumulationschemesamoreattractiveoption.Foremployers,there isareluctancetocontributemorethanthesuperannuationguaranteeminimumanddefinedbenefitschemescanexceedthisminimum.EmployersarealsobecomingwaryoftheimpactofvolatilityinthefundingleveloftheirdefinedbenefitplanontheircorporatefinancialaccountsasaresultofaccountingstandardAASB119(10),whichissimilar(butnotidentical)toIAS19(11).Theseaccountingstandardsdefinethewayasponsoringemployermustaccountforthecompany’sfinancialobligationstoanydefinedbenefitsuperannuationplansitsponsorsforitsemployees.

For employees, accumulation schemeshaveprovedapractical option fornewentrants to superannuation,especiallythosewhoregularlymovebetweenjobs.Employeesalsobenefitfromthesimplertaxationtreatmentofaccumulationschemes.

Source: Australian Prudential Regulation Authority, Annual Superannuation Bulletin, Table 13, June 2006

(9) AustralianPrudentialRegulationAuthority,SuperannuationBulletin,Table13,June2006.(10) AustralianAccountingStandardsBoardAASB119Employee Benefits.Theobjectiveofthisstandardistoprescribetheaccountinganddisclosure

requirementsforemployeebenefits.Furtherinformationisavailableatwww.aasb.com.au.(11)InternationalAccountingStandardsBoardIAS19Employee Benefits.Furtherinformationisavailableatwww.iasb.org.(12)AustralianPrudentialRegulationAuthority–regulatedsuperannuationfundswithgreaterthanfourmembers.

Distribution of Superannuation Funds by Benefit Structure – Year End 2006(12)

Entities Members Assets 000’s A$ Billion

Accumulation 573 16,745 297.1

DefinedBenefit 57 792 56.4

Hybrid 242 10,734 299.9

Total 872 28,271 653.4

PAgE 8 | MAnAgED FunDS In AuSTRAlIA 2008

Accumulation fundsaresuperannuationfundswheremembersmakedefinedcontributionswhichaccumulatetotheirbenefit.Theassetsofthefundareinvestedandanyearnings(orlosses)arecredited(ordebited)tothemember’saccount less any charges suchas administration fees and insurancepremiums.Membersbear the full effect offluctuationininvestmentearnings.Thesefundsarealsoreferredtoasdefinedcontribution(DC)funds.

Defined benefit fundsaresuperannuationfundswherethemember’sbenefitisbasedonaformulaspecifiedinthetrustdeed.Usuallythemember’sfinalbenefitdependsontheyearsofservicewithanemployer(ortheyearsofmembershipofthefund)andthelevelofsalarynearretirement.Theemployerpayswhateverisrequiredtofundthemember’sretirementbenefit.

Hybrid fundsaresuperannuationfundsthathaveacombinationofbothaccumulationanddefinedbenefitmembers.(13)

MemberChoiceTherearetwotypesofmemberchoiceintheAustraliansuperannuationsystem:‘choiceoffund’and‘investmentchoice’.

Choice of Fund

TheSuperannuation Legislation Amendment (Choice of Superannuation Funds) Act 2004requiresmostemployerstoprovidetheiremployeeswitha‘Choice’forminwhichtheemployeecannominateacomplyingfundofchoicefortheemployertodirecthisorhersuperannuationcontributions.Intheabsenceofanomination,theemployercandirectthecontributiontoacomplyingfundofitschoosing,oftenaretailmastertrustoranindustryfund.(14)TheseprovisionscameintoforceinJuly2005.Researchtodatesuggeststhatonly10-15percentofmembershaveelectedtore-directtheirsuperannuationbalancesfromthefundnominatedbytheiremployer.(15)

Investment Choice

Superannuationfundshavebeenabletoofferinvestmentchoiceformembersforsometime.Thisreflectsthedesiretogivemembersgreatercontroloverthemanagementoftheirsuperannuationinvestmentsand,morerecently,thedesireoffundtrusteestoensuretheirfundstayscompetitiveinanenvironmentoffundchoice.Thedeclineofdefinedbenefitplans,inwhichmemberinvestmentchoiceislessrelevant,hasfurtherinfluencedthistrend.Corporate,industryandpublicsectorfundstypicallyofferamoreconstrainedchoice,oftenlimitedtolessthansixoptionswithdifferentassetmixesreflectingdifferentriskprofiles.Sometimes,however,theyincludemorespecialisedstrategiesand/orinvestmentinspecifiedcompanyshares.Todaymorethan70percentofthesetypesoffundsofferinvestmentchoicetotheirmembers,withatrendtowardsgreaterdiversity.Notsurprisingly,retailfundstypicallyoffermembersawiderangeofinvestmentchoicesfrommanydifferentunderlyingfundmanagers.This‘openarchitecture’modeldemonstratesthesophisticationandspecialisationoftheAustralianmanagedfundsindustry.

APRAhasexpressedsomeconcernsabouttheofferofunrestrictedchoicetomemberswithlimitedfinancialliteracy.AreportbytheParliamentaryJointCommitteeonCorporationsandFinancialServiceshasrecommendedfurtherattentiontothisissue.(16)Interestingly,themajorityofsuperannuationcontributionsareinvestedinthe‘default’option,whichisforthecontributionsofthosememberswhohavenotchosenaninvestmentoption.Mostdefaultoptionsaremanagedona‘balanced’basisthatincludesexposuretoawiderangeofinvestmentmarketsandassetclasses.

(13)DefinitionsfromtheAustralianPrudentialRegulationAuthority,Annual Superannuation Bulletin,June2006.(14) Currentemployeescanchangetheirnominationsatanytime,thoughemployersarenotrequiredtoprovidemorethanone‘Choice’formtoan

individualemployeeinanytwelvemonthperiod.Theycandomoreattheirdiscretion.(15) InvestmentLinkpressrelease,Leading Industry and Retail Funds Dominate Choice,February2007.(16)ParliamentaryJointCommitteeonCorporationsandFinancialServices,The Structure and Operation of the Superannuation Industry,August2007.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 9

SuperannuationFundAssetAllocationAustralian superannuation funds have a broadly-based portfolio of investments in aggregate, generallyconcentratingingrowthassets.

Asset Allocation of Default Investment Strategy – Year End June 2006

Corporate Industry Public Sector Retail Total

AustralianShares 11,947 37,404 29,750 21,789 100,889

InternationalShares 7,519 28,312 25,100 16,223 77,153

ListedProperty 993 2,957 2,962 3,937 10,848

UnlistedProperty 1,185 8,387 6,092 1,115 16,779

AustralianFixedInterest 4,067 10,165 6,017 15,710 35,959

InternationalFixedInterest 1,880 5,088 6,067 3,834 16,869

Cash 1,396 5,550 7,065 11,152 25,163

Other(a) 1,463 13,005 9,205 11,373 35,046

TotalDefaultStrategyAssets 30,449 110,867 92,256 85,133 318,706

Total Assets 52,423 150,475 151,990 298,445 653,333

Entities with More than Four Members, (A$ Million)

Corporate Industry Public Sector Retail Total

AustralianShares 39 34 32 26 32

InternationalShares 25 26 27 19 24

ListedProperty 3 3 3 5 3

UnlistedProperty 4 8 7 1 5

AustralianFixedInterest 13 9 7 18 11

InternationalFixedInterest 6 5 7 5 5

Cash 5 5 8 13 8

Other(a) 5 12 10 13 11

Total 100 100 100 100 100

Proportion of Assets as a Percentage

Note:Notallsuperannuationentitiesarerequiredtohaveadefaultinvestmentstrategy.Wherethereisnodefaultstrategy,thestrategyofthelargestoptionisreportedforthefundstrategyasawhole.

(a)Otherincludesassetsinalternativeinvestmentssuchashedgefundsandassetsnotincludedinanyothercategory.

Source: Australian Prudential Regulation Authority, Annual Superannuation Bulletin, Table 16, June 2006.

PAgE 10 | MAnAgED FunDS In AuSTRAlIA 2008

Thepercentageofsuperannuationfundassetsinvestedoverseashasincreasedovertime.Thisisparticularlyevidentintherisingallocationtointernationalshares.Theothermajordevelopmenthasbeentheincreasingappetiteforprivateequity,hedgefundsandotheralternativeassets.ThesetrendsoverlaptotheextentthatsomeofthealternativeassetspurchasedbyAustralianfundshavebeensourcedoverseas.Thisisparticularlytrue inthehedgefundssector.Bothtrendsreflectthegrowingsizeofthesuperannuationindustryrelativeto local listedmarkets and the desire of trustees to diversify their investments away from the traditionalassetclasses.

FutureFundTheFutureFundwasestablishedin2006tomanageassetscontributedbytheFederalGovernmenttomeetunfunded superannuation liabilities arising from the superannuation entitlements payable to somepublicservantsanddefencepersonnel.TheseliabilitiescurrentlyamounttooverA$100billionandinAugust2007werematchedbyfinancialassetsofapproximatelyA$60billion.TheliabilitiesareexpectedtogrowtoaroundA$148billionby2019-20andtomorethanA$200billionby2046-47.

TheFutureFundisoverseenbyanindependentBoardofGuardians.MembersoftheBoardareappointedbytheTreasurerandtheMinisterforFinanceandDeregulationandareappointedforuptofiveyears.TheFund’sfinancial assets are typicallymanaged by investmentmanagers selected from the private sector, althoughcashholdingsarecurrentlymanagedbytheReserveBankofAustralia(RBA).TheFundalsohas2.1billionsharesinTelstra,whichareheldinescrowuntil2008.NorthernTrustwasappointedasanindependentcustodianoftheFundinMay2007.

TheFundcurrentlyhasatargetreturnofbetween4.5and5.5percentabovetheConsumerPriceIndex(CPI)measureofinflationoverthelongterm.TheBoardhasinterpretedthisasanobjectivetoprovideareturn(netofcosts)ofatleast5percentabovetheCPIoverrolling10yearperiods.

Moreinformationcanbefoundatwww.futurefund.gov.au.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 11

PublicUnitTrustsPublicunittrustsareinvestmentfundsopentothepublic.InAustralia,aunittrust’soperationsareadministeredby a single Responsible Entity (RE), which has responsibility for both investment strategy and custodialarrangements.Thesetrustsallowunitholderstodisposeoftheirunitsrelativelyquickly.Theymaysellthembacktothemanagerifthetrustisunlisted,orsellthemontheAustralianSecuritiesExchange(ASX)ifthetrustislisted.Thereisenormousdiversityintherangeandsizeofunittrusts.TheyincludeAustralianandinternationalproperty,infrastructure,shares,fixedincomeandcashmanagementtrusts.

LifeInsuranceProductsWith the rapid increase in superannuation funds over the past decade, life insurance offices have becomeincreasinglyinvolvedintheprovisionofsuperannuationproductsandservices.Non-superannuationbusinessnowaccountsforjust16percentofstatutoryfundsoflifeoffices.

Sources: Reserve Bank of Australia, Managed Funds, Table B18; DIISR

OtherFundManagementProducts

life Offices Statutory Funds – June 1998 to June 2007

0

40

80

120

160

200

240

280

June 1988

June 1989

June 1990

June 1991

June 1992

June 1993

June 1994

June 1995

June 1996

June 1997

June 1998

June 1999

June 2000

June 2001

June 2002

June 2003

June 2004

June 2005

June 2006

June 2007

Superannuation Business Ordinary Business

PAgE 12 | MAnAgED FunDS In AuSTRAlIA 2008

IndexFundsIndexfundsaimtoprovidemarketreturnsand,unlikeactivelymanagedfunds,donotattempttopickstocksormarketcycles.Anindexmanagerconstructsaportfoliothatcloselytracksaspecificmarketindexandaimstocapturethemarketreturnoftheassetsmakingupthetargetindex.Thephilosophybehindindexfundsisthatitisdifficulttooutperformthemarketoverthelong-termthroughactiveinvesting.

IndexfundshavebeenpopularwithAustralianinvestorsforsometime.MajorglobalplayerssuchasStateStreetGlobalAdvisors,BarclaysGlobalInvestorsandVanguardInvestmentsAustraliahavejoinedlocalplayerssuchasMacquarieandAMPinofferingindexfundstoinstitutionalandretailinvestors.RecentestimatesputtheassetsundermanagementinindexfundsatapproximatelyA$120billion.(17)

ExchangeTradedFundsExchangeTradedFunds(ETFs)arearecentadditiontotheAustralianmarket,withthefirstfundestablishedbyStateStreetGlobalAdvisorsin2001.ETFsareahybridformofinvestment,combiningthecharacteristicsofshareswiththoseofunittrusts.Theyhavethreemainattributes:

n Theyareopen-endfundsratherthanclosed-end.ThismeansthatthenumberofunitsonissueandavailabletobetradedontheASXwillfluctuateaccordingtodemand.

n Theyhaveaprimarymarket(forongoingunitcreationandredemption)andasecondarymarket.

n Theyaredesignedtoensurethattheunitpriceonthesecondarymarketdoesnotdivergetoofarfromthenetassetvalueoftheunits.

TherewerethreeindexedETFslistedontheASXasat30June2007.TheyweremanagedbyStateStreetGlobalAdvisorsandhadamarketcapitalisationofapproximatelyA$770millionasat31December2006.Duringthesecondhalfof2007afurther14ETFswerelistedontheASXbyBarclaysGlobalInvestors.(18)Whilegrowing,theAustralianmarket isstillsmallrelativetotheglobalmarket,whichisestimatedtobeworthmorethanA$550billion.Theslowtake-upisrelatedtoavarietyoffactors,including:

n Thefactthatmanyfinancialplannersdonotprovideadviceondirectholdingsinlistedsecurities.

n ThefactthatAustraliandomiciledactivefundmanagershaveagoodrecordofbeingableto‘beatthemarket’(outperformtheindex)inAustralianshares.

(17) VanguardInvestmentsAustralia,http://www.vanguard.com.au/Institutional_Investors/Our_approach/Why_index/index.aspx(18) On10October2007,BarclaysGlobalInvestorslaunchedeightnewETFsontheASXprovidingdirectaccesstotheUS,European,Japanese,

FarEasternandemergingmarkets.Thefirmlaunchedafurther6ETFson15November2007toprovidedirectaccesstoAsianmarketsincludingChina,TaiwanandSouthKorea.KnownasiShares,eachETFtracksanestablishedmarketindex.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 13

HedgeFundsThehedgefundsindustryinAustraliaisexpanding,withagrowingfundspoolandanincreasinglysophisticatedlocalinvestorbaseseekingnewwaystodiversifytheirinvestments.Inthepastfewyearsvolatileanduncertainmarketshavealsoincreasedtheattractivenessof‘absolute’returns(19),leadingtomoreinterestinalternativeproductssuchashedgefunds.ManyinstitutionalinvestorsinAustraliahavechosentouseforeign-domiciledhedge funds to build up their hedge fund portfolio. Nevertheless, as the table below shows, Australia’sdomestichedgefundindustryhasgrownstronglyinrecentyears,fromaroundA$2billioninJune2000tooverA$70billioninJune2007,whichisspreadacrossroughly200funds.Thenumberofhedgefundmanagershasalsogrown.

Approximately65percentoftotalassetsaresourcedfromlocalhighnetworthandretail investors,20percentfromsuperannuationfundsand15percentfromoffshoresources.Muchofthemoneyinvestedinfundofhedgefunds,comesfromindividualinvestors.However,institutionalinvestorshavealsoshownastrongdesiretoallocatetohedgefunds(especiallyfundofhedgefunds)inmorerecenttimes.Thisseemslikelytocontinue.Industryresearchsuggeststhattheinstitutionalallocationtohedgefundsisexpectedtoincreasebyaround50percentoverthecomingtwotofiveyears.(20)Atthesametime,thelocalindustryappearstobeoperatingatapproximately60percentofcurrentsingleandmulti-strategyproductcapacity,indicatingthepotentialforgrowthinbothcurrentandnewproductlines.(21)

(19) Absolutereturnsorhedgefundsaremanagedfundsthataimtoproducereturnsinbothrisingandfallingmarkets.Theinvestmenttechniquesadoptedbyanabsolutereturnfundmaybedifferenttomethodsemployedbyatraditionalfundmanager.Ratherthanthetraditional‘buyandhold’approach,absolutereturnfundshavegreaterscopetousesophisticatedtradingstrategiestobenefitfromopportunitiesinthemarket,ASXAbsolute Return Funds LMI Fact Sheet,2007.

(20) AlternativeInvestmentManagementAssociation,Australian Hedge Fund Survey 2006,April2006.(21) Rainmaker Hedge Fund Report,2007.

Year Asset under Management A$ Billion (as at 30 June)

2000 2(1)

2001 4(1)

2002 10

2003 18

2004 26

2005 45

2006 60.1

2007 70.3

(1)Estimates

Source: LCA Group, as at 30 June 2007

growth in Assets under Management of the Australian Hedge Funds Industry

PAgE 14 | MAnAgED FunDS In AuSTRAlIA 2008

TheprofileoftheAustralianindustryhasbeenhelpedwiththeentryofmany‘traditional’fundmanagementfirmsintothehedgefundarena.Currently,therearemorethan70hedgefundmanagersand24fundofhedgefundmanagersinAustralia. Inaddition,it isestimatedthattherearemorethan150potentialandstart-uphedgefundsandboutique‘long-only’sharefundsinAustralia.AsarecentRainmakerreportnotes,mostplayersintheAustralianmarkethaveonlyoneortwoproductsandlessthanA$500millionundermanagement.(22)

Australian-basedhedgefundmanagersincludelong/shortAustralian,AsianandGlobalequityfunds,AustralianandAsianfixedincomeandconvertiblearbitragefunds,andGlobalmanagedfuturesfunds.Inaddition,manyinternationalhedgefundserviceproviders,suchashedgefundassetconsultants,primebrokers,administratorsandcustodians,haveestablishedlocalorregionalofficesinAustralia.Thishasledtoa‘clusteringeffect’,providingasolidnetworkofserviceprovidersfortheindustry.

PrivateEquityandVentureCapitalAustralia’sprivateequityandventurecapitalindustryhasexperiencedstronggrowthoverthepastfiveyearsandisnowoneofthemostsophisticatedanddevelopedintheAsia-Pacificregion.Bylate2006,theAustralianprivateequityandventurecapital industry included139investmentfirms.ThesefirmshadinvestedcapitalofA$9billionandavailable capital ofover$A8billionwith total capitalundermanagementofmore than$A17billion.(23)Thegrowingmaturityofthemarketishighlightedbytheincreasingsizeoffunds(therearesevencurrentfundsinexcessofA$500million)andtheindustry’sinvestmentinover1,000underlyingcompanies.(24)

Growthintheindustryhasbeendrivenby:

ndemandforfundingfromemergingandexpandingbusinesses

nincreasedallocationofinstitutionalfunding

ngrowthinthefundsmanagementindustry

nthegrowinginterestofinternationalfirmsintheAustralianindustry.

number of Single Strategy Hedge Fund number of Fund of number of Managers number of ManagersYear (as at 30 June) Products Hedge Fund Products Hedge Funds Fund of Hedge Funds

2002 45 22 27 13

2003 65 28 42 15

2004 86 40 49 15

2005 115 46 59 16

2006 130 58 66 17

2007 139 61 71 24

Source: LCA Group, as at 30 June 2007

growth in Australian-Based Products and Managers for Hedge Funds and Fund of Hedge Funds

(22)Rainmaker Hedge Fund Report,2007.(23)PrivateEquityMedia, Australian Venture Capital Guide 2007.(24)ThomsonFinancial,asat3May2007.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 15

The Australian Government has introduced a number of changes to the tax treatment of venture capitalinvestments.

Keychangesinclude:

n VentureCapitalLimitedPartnerships(VCLP)introducedthroughtheVenture Capital Act 2002.AVCLPisaninvestmentvehiclewithaflow-throughtaxstructurethatallowsinternationalinvestorsanexemptiononAustralianCapitalGainsTax(CGT).ThisisparticularlyusefulforpensionandendowmentfundswhosehomecountryhaslowerCGT,ordoesnothaveCGT.Additionally,thereisanAustralianVentureCapitalFundofFunds(AFOF)investmentvehiclewhichhassimilartaxbenefits.

n EarlyStageVentureCapitalLimitedPartnerships (ESVCLP)arenewinvestmentvehicleseffectivefromthe2007-08 income year(25), allowing flow-through income tax treatment and no tax liability for investors,whetherinternationalorAustralian.

n Allowancesthatpermitforeigninvestorswhoaretax-exemptresidentsofspecifiedjurisdictions,orpartnersinflow-throughlimitedpartnerships(thatsatisfycertainconditions),tobeexemptfromtaxonprofitsmadefromthedisposalofinvestmentsineligibleinvesteecompanies.

Source: Private Equity Media, Australian Venture Capital Guide 2007

NumberofFirms 139

TotalCapital A$17.1billion

InvestedCapital A$9.3billion

AvailableCapital A$8.9billion

TotalNumberofInvestments 1,837

ComprisingCurrentPortfolioCompanies 1,097

CompletedDivestments 740

ProfessionalStaff 835

Australian Private Equity and Venture Capital Industry – 2007

(25) IncomeYearasdefinedundertheIncome Tax Assessment Act 1997.

PAgE 16 | MAnAgED FunDS In AuSTRAlIA 2008

SociallyResponsibleInvestingSocially Responsible Investment (SRI) funds aim to build a portfolio on stated environmental and/or socialandethicalcriteria,recognisingagrowingtrendamonginvestorstolookatacompany’s‘triplebottomline’offinancial,environmentalandsocialperformance.ThesizeofthesectorinAustraliawasestimatedtobealmostA$12billioninJune2006,havinggrownbyover50percentovertheyear.Ofthisgrowth,someA$1.5billionwasgeneratedbynetcashflowintoretailandinstitutionalfundsandmandates.(26)RetailassetsundermanagementnowamounttoapproximatelyA$1.4billion,whilewholesaleassetshavegrowntoapproximatelyA$7.8billion.

InvestorfocusonpotentiallyadverseenvironmentalissueshasspurredthegrowthinSRI.Manysuperannuationfunds, includingover120publicoffersuperannuationfunds,nowofferSRIoptionsaspartof theirsuiteofinvestmentoptions.

Increasing investor awareness of SRIs is also being recognised under the Australian financial regulatoryframework.ASIChasdevelopedapolicyundertheFSRAthatstates it isgoodpracticetoascertainwhetherenvironmental,socialorethicalconsiderationsareimportanttoclientsbeforerecommendinginvestmentsandproductstothem.(27)

StructuredProductsStructuredproducts(28) areavailable toAustralian retail investors through themajorbanking,advisoryandprivatebankingnetworks.Theyarealsousedtoalimitedextentbyinstitutionalinvestors.IndustryestimatesplacedassetsinstructuredproductsataroundA$2billionin2002andaroundA$6billionbytheendof2005(29),thoughderivingaccuratestatisticsforthissectorisextremelydifficult.

OverlaysandAlphaTransferAustralianinvestorshavetraditionallybeenveryinnovative.Theyhaveactivelypursuedspecialtyproductssuchastacticalassetallocation(30),currencymanagementandalphatransfer.(31)

Inpart,thisopennesstonewproductsstemsfromthehighallocationbymostinstitutionalinvestors(andmanyretailinvestors)tonon-Australianassetsbearingcurrencyrisk.Italsoreflectsthegenuinelyglobalperspective,cultureofinnovationandhightechnicalcompetenceofthelocalinvestingcommunity.

(26) EthicalInvestmentAssociation,Sustainable Responsible Investment in Australia,BenchmarkingSurvey,2006.(27) AustralianSecuritiesandInvestmentsCommission,Regulatory Guide 175 Licensing: Financial Product Advisers – Conduct and Disclosure,RG

175.110,May2007.(28) Structuredproductsaresyntheticinvestmentinstrumentstailoredorpackagedtomeettheindividualfinancialgoalsofinvestors,offeringboth

capitalprotectionandincome.(29) BarclaysCapital,Australia Prepares for Take-off,www.structuredproductsonline.com.(30) Tacticalassetallocationisanactivemanagementportfoliostrategythatrebalancesthepercentageofassetsheldinvariouscategoriesinorderto

takeadvantageofmarketpricinganomaliesorstrongmarketsectors.(31) Alphatransferistheprocessofusingderivativestomodifythemarket(‘beta’)exposureofaportfolioandsocreateaninvestmentwiththeactively

managed(‘alpha’)componentofreturnsdrawnfromonemarket(orsetofmarkets)andthemarket(‘beta’)exposurefromanother.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 17

TheManagedFundsIndustry

AssetsUnderManagementAccording to the Australian Bureau of Statistics, assets placed with professional investment managers inAustraliareachedA$1.2trillioninJune2007,upfromA$771billionthreeyearsago.

Note:Notallassetsheldbycollectiveinvestmentinstitutionsareplacedwithprofessionalinvestmentmanagers.HencethefigureofA$1.2trillionislowerthanthetotalfundsundermanagementfigurereportedonpage1ofA$1.3trillion.

Source: Australian Bureau of Statistics, cat. no. 5655.0, Managed Funds, Australia, June 2007

Total Assets Held by Investment Managers (A$ Million)

June Quarter June QuarterSource of Funds 2003-04 2004-05 2006 2007

Funds from Australian Sources 743,521 851,543 983,846 1,166,459

Total Managed Funds 531,461 607,379 708,937 852,122

LifeInsuranceOffices 124,181 136,657 138,462 148,017

SuperannuationFunds 278,760 337,588 418,428 529,078

PublicUnitTrusts 94,235 96,857 112,261 127,018

FriendlySocieties 2,408 2,329 2,378 2,096

CommonFunds 3,961 4,250 4,516 4,033

CashManagementTrusts 27,916 29,698 32,892 41,880

Other Domestic Sources 212,060 244,164 274,909 314,337

Government 17,307 19,978 24,800 22,915

Charities 2,332 2,133 2,492 3,174

OtherTrusts 97,137 119,821 145,176 174,189

GeneralInsurance 27,297 30,629 33,571 34,391

OtherInvestmentManagers 44,040 37,472 27,589 30,250

OtherSources 23,947 34,131 41,281 49,418

Funds from Overseas Sources 27,963 32,861 42,900 59,590

TOTAl SOuRCE OF FunDS 771,484 884,404 1,026,746 1,226,049

PAgE 18 | MAnAgED FunDS In AuSTRAlIA 2008

FundSourcesThe share of total (consolidated) assets of managed funds outsourced to investment managers throughsuperannuationfunds,lifeinsuranceoffices,publicunittrusts,cashmanagementtrusts,commonfunds,andfriendlysocietieswasaround64percentinJune2007.Thebulkoffundsoutsourcedintheinstitutionalarenaareawardedinacompetitive,transparentandarms-lengthprocess.

(a)Figuresincludesuperannuationfundsheldinthestatutoryfundsoflifeinsuranceoffices.

Sources: Australian Bureau of Statistics, cat no. 5655.0, Managed Funds, Australia, June 2007; DIISR

Masterfunds,whichoutsourcetheinvestmentfunctiontospecialistmanagers,havebecomecommonintheretailinvestmentandsuperannuationsectors.Manyfinancialinstitutionswithstrongdistributioncapabilities,suchasbanks,nowofferretailinvestorsamenuofspecialistmanagers,oftencomplementingthedistributor’sin-house fundsmanagement services.Dealergroups typically employanaverageof5.3platforms,withanaverageof2.4preferredplatformspergroup.(32)ThesevehicleshaveenabledspecialistinvestmentmanagerstogainafootholdintheAustralianretailmarketwithoutdevelopingtheirowndistributioncapability.Thishasbeenfurtherfacilitatedbytheuseofthirdpartymarketingrepresentatives.

Currently, fundsundermanagement fromoffshoresources representasmallelementof total fundsundermanagementinAustralia,conservativelyestimatedataroundA$60billioninJune2007.(33)However,recentreformstoAustralia’sinternationaltaxarrangements(34)meanthevolumeofoffshorefundsmanagedfromAustraliaisexpectedtorise.

Assets Placed with Investment Managers – June 2007

Placed with Investment Share of Assets Consolidated Assets Managers Placed A$ Million A$ Million %

SuperannuationFunds 780,735 529,078 68

LifeInsuranceOffices(a) 224,546 148,017 66

PublicUnitTrusts 266,980 127,018 48

CashManagementTrusts 46,745 41,880 90

CommonFunds 11,421 4,033 35

FriendlySocieties 4,245 2,096 49

OtherDomesticSources N/A 314,337 –

OvereasSources N/A 59,590 –

Total 1,334,672 1,226,049 –

(32) InvestorSupermarket,Top 100 Dealer Groups Survey,June2007.(33)AustralianBureauofStatistics,cat.no.5655.0,Managed Funds Australia,June2007.Someindustryestimatessuggestthiscouldbeashighas

A$400billion.(34) ReferAppendixD.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 19

AssetAllocationThemostmarked change in asset allocation throughout the industryhasbeen thegrowth indemand foralternativeassets,suchashedgefunds,infrastructureandprivateequity(35),whichhasmostlybeenfundedoutofnewmonies.Themainexceptiontothisistheinclusionofdomesticandoverseasprivateequitytoportfolios,whereinmanycasestheallocationisreplacingAustralianshares.TheindustryhasalsoseenadecreaseintheallocationoffundstoAustralianfixedinterestandcash.

Asset Breakdown of Fund Managers – 2002 to 2006

Asset Breakdown December 2002

Australian Shares 28%

Alternative Investments 1%Miscellaneous 1%

International Shares 21%

Australian Fixed Interest 17%

Cash 12%

Property 11%

Tactical AssetAllocation/Currency 5%

International FixedInterest 4%

Asset Breakdown December 2006

Australian Shares 28%

Alternative Investments 6%Miscellaneous 0%

International Shares 23%

Australian Fixed Interest 13%

Cash 9%

Property 11%

Tactical AssetAllocation/Currency 5%

International FixedInterest 5%

Source: InvestorSupermarket Market Wrap, December 2002-2006

(35) InvestorSupermarket Market Wrap,December2002-06.

PAgE 20 | MAnAgED FunDS In AuSTRAlIA 2008

FundManagersTherearecloseto120significantfundmanagementfirmsoperatinginAustralia,including17ofthe20largestglobalassetmanagementfirms.(36)ThefundsmanagementmarketinAustraliaisdominatedbythesubsidiariesof larger institutions, suchas internationalfinancial groups, domesticbanksand life insurance companies.The10largestinvestmentmanagers(rankedbyassetsundermanagement)controlledapproximately48percentofthemarketinJune2007andthenext10managersheld18percentofthemarket.The30largestfundscontrolledaround80percentofthefundsundermanagementinthemarket.

Recently,therehasbeenconsolidationinthenumberofmedium-sizedfundmanagementfirmsinAustralia.Thisisnotonlyafunctionofthegrowingmaturityoftheindustrybutalsoreflectsthedesireamongparticipantstobecomebothmanufacturersanddistributorsofproduct.Theneedtocaptureopportunitiesintheretailsectorhasbeenacatalystforthisconsolidation.

Despiteconsolidationoccurringattheinstitutionalendofthemarket,therehasbeensignificantgrowthinthenumberofsmall‘boutique’fundmanagers.Manyofthesefirmsareinvolvedinemergingproducts,suchasprivateequity,hedgefundsandproperty,butthereareatleast30boutiqueplayersmanagingtraditionalAustralian share products.(37) These have been assisted by the development of ‘incubator’ organisationsestablishedtoprovidebackofficeandcompliancesupporttostart-upboutiquemanagers.

EstablishedinvestmentmanagersinAustraliacanenjoyrobustprofitability.PricewaterhouseCoopers’researchindicatesthatover40percentofAustralianinvestmentmanagersenjoycost/incomeratiosthatarelowerthan30percent.(38)Thisreflectsacombinationofhealthyfeelevelsandclosemanagementattentiontooperationalefficiencyandriskmanagement.

(36) Pensions&Investments,2006 Data Book,25December2006;InvestorSupermarket;DIISR.(37) PricewaterhouseCoopers, Australian Investment Management Survey 2006.(38) Ibid.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 21

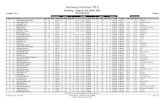

Australian Sourced Total Funds under Management (Consolidated) largest 30 Managers by Market Share – June 2007

Notes:Columnsmaynotaddupduetorounding.ManagerssuchasMLC,VFMCandRussellInvestmentGroupdonotappearduetoconsolidation.

Source: InvestorSupermarket, Market Wrap, 30 June 2007

Cumulative Market Market Share ShareRank Investment Manager A$ Million % %

1 MacquarieBankingGroup 100,948.0 8.2

2 ColonialFirstStateInvestmentsLtd 78,561.3 6.4

3 StateStreetGlobalAdvisors 75,933.7 6.2

4 AMPCapitalInvestors 71,228.9 5.8

5 AXAAustralia 62,888.0 5.1

6 BarclaysGlobalInvestors 47,044.0 3.8

7 VanguardInvestmentsAustralia 42,557.4 3.5

8 QIC 40,072.7 3.3

9 PerpetualInvestments 39,608.0 3.2 Top 10

10 UBSGlobalAssetManagement 33,646.0 2.7 48.3

11 INGInvestmentManagement 32,414.0 2.6

12 BTFinancialGroup 31,947.3 2.6

13 PerennialInvestmentPartners 22,397.2 1.8

14 DeutscheAssetManagement 21,739.0 1.8

15 ChallengerFinancialServicesGroup 21,712.2 1.8

16 PIMCO 21,365.0 1.7

17 BlackRockInvestmentManagement(Australia)Limited 17,550.4 1.4

18 MapleBrownAbbott 17,330.4 1.4

19 PlatinumAssetManagement 16,951.0 1.4 Top 20

20 GMOAustraliaLimited 16,526.0 1.3 66.3

21 CapitalInternational,Inc. 16,439.0 1.3

22 MellonGlobalInvestments 15,751.8 1.3

23 TacticalGlobalManagementLimited 15,639.4 1.3

24 CreditSuisseAssetManagement 15,628.0 1.3

25 WellingtonInternationalMangementCo 15,482.0 1.3

26 LazardAssetManagement 14,749.5 1.2

27 IndustryFundsManagement 14,503.0 1.2

28 SuncorpInvestmentManagement 13,542.7 1.1

29 CentroMCS 13,500.0 1.1 Top 30

30 SchroderInvestmentManagement 13,089.8 1.1 78.4

Top 30 960,746 78.4

Other Industry Participants 264,787 21.6

Industry Total 1,225,533 100

PAgE 22 | MAnAgED FunDS In AuSTRAlIA 2008

WholesaleandRetailAssetsUnderManagementDatacollectedbyInvestorSupermarketindicatesthatfundsfromwholesale(institutional)sourcesaccountedforaround75percentofaggregateassetsundermanagementinJune2007.Wholesaleassetsareassuminganincreasingshareofmanagers’totalassets.

Therelativegrowthinwholesaleassetsundermanagementisnotentirelyindependentofincreasingactivityintheretailmarket.Thegrowthinmastertrustsandwrapaccounts–wholesaleproductsthattaptheretailmarket – have boostedwholesale numbers. The increasing use of specialistmanagers as sub-advisors byretailsuperannuationfundshashadthesameeffect.

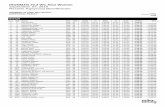

Wholesale and Retail Funds under Management (unconsolidated)

Notes:Columnsmaynotaddupduetorounding.Thewholesaleandretailbreakdownsdonotadduptothetotalassetsundermanagementonthepreviouspageasthisbreakdownisdoneonanunconsolidatedbasis.

Source: InvestorSupermarket, Market Wrap, 30 June 2007

CumulativeRank largest 30 Wholesale Australian Market Market Investment Managers Sourced Share Share as at 30 June 2007 A$ Million % %

1 StateStreetGlobalAdvisors 75,181 6.32 MacquarieBankingGroup 68,794 5.83 QIC 64,419 5.44 AllianceBernstein 61,456 5.15 AXAAustralia 54,814 4.66 AMPCapitalInvestors 47,408 4.07 BarclaysGlobalInvestors 47,044 3.98 ColonialFirstStateInvestmentsLtd 44,497 3.7 9 VictorianFundsManagementCorp 41,306 3.5 Top 1010 VanguardInvestmentsAustralia 35,610 3.0 45.3

11 PerpetualInvestments 29,315 2.512 DeutscheAssetManagement 25,964 2.213 MLCInvestmentManagement 25,166 2.114 UBSGlobalAssetManagement 24,160 2.015 PerennialInvestmentPartners 22,710 1.916 PIMCO 21,365 1.817 MapleBrownAbbott 19,449 1.618 RussellInvestmentGroup 19,120 1.619 BNPParibasInvestmentMgmt 15,857 1.3 Top 2020 MellonGlobalInvestments 15,752 1.3 63.6

21 TacticalGlobalManagementLtd 15,639 1.322 GMOAustraliaLimited 15,576 1.323 WellingtonInternational 15,482 1.324 BTFinancialGroup 15,399 1.325 LazardAssetManagement 14,750 1.226 IndustryFundsManagement 14,503 1.227 ChallengerFinancialServicesGroup 14,263 1.228 CreditSuisseAssetManagement 14,158 1.229 IAGAssetManagement 13,447 1.1 Top 3030 FundsSA 13,103 1.1 75.8 OtherManagers 288,010 24.2

Total 1,193,716 100

Cumulativelargest 30 Retail Australian Market MarketInvestment Managers Sourced Share Shareas at 30 June 2007 A$ Million % %

MLCInvestmentManagement 57,757 13.2 ColonialFirstStateInvestmentsLtd 56,511 12.9 AMPCapitalInvestors 49,339 11.2 MacquarieBankingGroup 33,533 7.6 INGInvestmentManagement 31,938 7.3 AXAAustralia 27,707 6.3 BTFinancialGroup 24,904 5.7 PerpetualInvestments 10,293 2.3 UBSGlobalAssetManagement 9,486 2.2 Top 10ChallengerFinancialServicesGroup 9,433 2.1 70.8

CentroMCS 8,700 2.0 BlackRockInvestmentManagement 7,865 1.8 CapitalInternational,Inc. 7,203 1.6 VanguardInvestmentsAustralia 6,947 1.6 CreditSuisseAssetManagement 6,720 1.5 GoldmanSachsJBWereAssetMgmt 6,322 1.4 SuncorpInvestmentManagement 6,178 1.4 InvestorsMutual 5,160 1.2 RubiconAssetManagementLimited 4,928 1.1 Top 20RussellInvestmentGroup 4,926 1.1 85.5

APNFundsManagementLimited 4,729 1.1 PlatinumAssetManagement 4,035 0.9 DFAAustraliaLtd 3,923 0.9 AustralianUnityInvestments 3,618 0.8 AberdeenAssetManagement 3,481 0.8 IOOFFundsManagement 3,403 0.8 PMCapital 3,301 0.8 ZurichFinancialServices 2,967 0.7 TOWERAustraliaLimited 2,892 0.7 Top 30TyndallInvestmentManagement 2,339 0.5 93.5

OtherManagers 28,350 6.5

Total 438,888 100

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 23

ThedataonassetsundermanagementobscuresoneofthekeythemesinthemanagedfundsmarketplaceinAustralia,namelytheproliferationofretailproducts,whichistheresultofanincreasedfocusofvendorsondistributingproducttotheretailsector.Currentestimatessuggestthereareapproximately10,000productsavailabletoinvestors,about8,500intheretailmarketand1,500inthewholesalemarket.Thefocusontheretailendofthemarketisbeingdrivenbyexpectationsofcontinuedstronggrowthinthismarketsegment.

Thistrendplaystothoseinstitutionswithhighprofilebrands,highlydevelopeddistributionchannelsandthescaletosupportarangeofretailproducts.Itisoneofthedriversbehindtheexpansionofbanksandthelargerfundmanagersinthemarket(throughmergersandacquisitions).Considerableresourcesarealsobeingdevotedtobuildingfinancialplanningcapabilities,boththroughalliancesandin-house.Withintheretailsector,financialplannersperformarolesimilartothatprovidedbyassetconsultantsinthewholesalemarket.

LifeInsuranceOfficesWith the rapid increase in superannuation funds over the past decade, life insurance offices have becomeincreasinglyinvolvedintheprovisionofinvestmentandsuperannuationproductsandservices.Lifeinsuranceofficesprovidesuperannuationandrelatedproductsviatheirownsuperannuationplansandmastertrusts,aswellasarangeofservicestoothersuperannuationfundsincludinglifeinsurance,fundsmanagementandadministrativeservices.

At the end of June 2007, life insurance offices were the second largest holder of managed fund assets(A$264billion),withthemajority(84percent)ofthesebeingsuperannuation-based(aroundA$220billion).Agreaterfocusonthesuperannuationindustryhasledtoanincreaseinsuperannuation-basedbusinessasaproportionofthetotalbusinessoflifeinsurancecompanies.Around20percentofallsuperannuationassetsareheldinlifeinsurancepolicies.(39)

AttheendofJune2007,therewere34registeredlifeinsurancecompaniesoperatinginAustralia,withforeign-ownedlifeinsurancecompaniesaccountingfor27percentofassetsand29percentoftotalAustralianbusinesspremiumsreceived.Bank-owned life insurancecompaniesaccounted for37percentofassetsmanagedbythelifeinsuranceindustryand37percentofallAustralianbusinesspremiums.Themarketishighlyconcentrated,withthethree largest life insurancecompaniesmanagingaround64percentof the industry’s totalassetsand the 10 largestmanaging around 94 per cent of these assets.(40) The past decade has seen a numberof de-mutualisations and rationalisations in the sector due to mergers and increased capital adequacyrequirements.

(39) ReserveBankofAustralia,Bulletin Statistical Tables, B18-Managed Funds.(40) AustraliaPrudentialRegulationAuthority,Life Office Market Report,June2007.

PAgE 24 | MAnAgED FunDS In AuSTRAlIA 2008

Ten largest life Insurance Companies – June 2007

Statutory Fund Assets^

Backing Australian liabilities Backing Total liabilities

group A$ Billion Industry Share % A$ Billion Industry Share %

1 AMP 75.5 30 77.9 30

2 NationalAustralia 55.4 22 55.4 22Bank/MLC

3 ING/ANZ 31 12 31 12

4 Colonial/CBA 21 8 21.3 8

5 NationalMutual/ 17.7 7 20 8AXA

6 Westpac 14.5 6 14.5 6

7 SuncorpLifeandSuper 8.9 4 8.9 3

8 Aviva 5.6 2 5.6 2

9 ZurichLife 4.2 2 4.2 2

10 TowerLife 3.2 1 3.2 1

Topthreegroups 162 64 164.3 64

Toptengroups 237.1 94 242 94

Foreignownedgroups 68.1 27 70.7 28

Bankownedgroups 94.1 37 94.4 37

Total Industry 251.3 256.6 of which overseas assets = 32.6 13 37.7 15

Total Premiums – Australian Business^^

Industry group A$ Million Share %

1 AMP 11,515 28

2 NationalAustralia 9,120 22 Bank/MLC

3 ING/ANZ 7,449 18

4 Colonial/CBA 2,503 6

5 NationalMutual/ 2,177 5 AXA

6 Westpac 1,726 4

7 SuncorpLifeandSuper 1,521 4

8 Aviva 1,398 3

9 ZurichLife 853 2

10 TowerLife 785 2

Topthreegroups 28,084 68

Toptengroups 39,048 94

Foreignownedgroups 12,133 29

Bankownedgroups 15,355 37

Total Industry 41,505

^ Statutoryfundassetsarereportedatfairvalue. ^^ Summationofregularinforcepremiumsatendofperiodandnewsinglepremiums.

Note:Detailsonthetablemaynotadduptototalsduetoroundingoffigures.

Source: Australian Prudential Regulation Authority, Life Office Market Report, June 2007; DIISR

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 25

FundManagementFeesTherehasbeendownwardpressureonfeesfortraditionalfundmanagementproductsoverthepastdecade.Thisreflectschangestothestructureoftheindustry,particularlytheriseofwrapaccounts,aswellasnaturalcompetition between fundmanagers. Economies of scale arising from the strong growth in assets undermanagementhasenabledfundmanagerstoofferlowerfeeswithlessimpactontheiroperatingmarginsthanwouldotherwisehavebeenthecase.

*ExcludesemployerplanswithlessthanA$5millioninassets.#EmployerplanswithlessthanA$5millioninassets.

Source: Investment and Financial Services Association/Rice Warner, Superannuation Fees Report, May 2007

Feestructuresintheretailcomponentofthefundsmanagementindustryarequitedifferentfromthoseinthewholesalecomponent.Intheretailmarket,feesmayincludethreeelements:entry,exitandongoingfees.Insomecases‘nilentryfee’productsamortisetheentryfeeoveranumberofyears.Inthewholesalemarket,entryandexitfeesarerare.Wrapaccounts,whichallowretailinvestorstopurchaseproductsatwholesalerates,typicallycarryanentryfee,anannualaccountkeepingfeeandanannualinvestmentmanagementfee.

TheProductDisclosureStatement(PDS)applyingtoretailmanagedinvestmentsorsuperannuationproductsmustincludeprescribedfeeinformation.Thisincludesastandardisedfeetemplateandanillustrativeworkedexample.Thesearedesignedtoimprovetransparencyandtoaidcomparisonacrossfunds.(41)

Foravarietyofreasons,feesinthewholesalemarketarelesstransparent.Ascanbeseeninthetablebelow,estimatesinthesuperannuationmarketsuggestthattheinvestmentmanagementfeeforanoverallportfolioofA$10millionoraboveislikelytositintherangeof0.4-0.7percentperannum,dependingonthesizeandnatureoftheportfolio,withadditionalfeesforcustodyandotherinvestment-relatedservices.(42)Withinthatrange,somespecialistsectorswillclearlybemuchmoreexpensive(e.g.smallcaporemergingmarketsequity)andothersmuchcheaper(e.g.cashmanagement).Inpracticemostwholesaleinvestmentmanagementfeesarenegotiated.

Expense Expense Expense Rate Rate Rate 2006 2004 2002Sector Segment % % %

Wholesale Corporate 0.78 0.75 0.86

CorporateSuperMasterTrust*(large) 0.81 1.14 1.24

Industry 1.13 1.18* 1.23

PublicSector 0.70 0.66* 0.63*

Retail CorporateSuperMasterTrust#(small) 2.01 2.11 2.36

PersonalSuperannuation 2.12 2.30 2.41

PostRetirement 1.79 2.04 2.02

RetirementSavingsAccounts 2.30 2.30 2.30

EligibleRolloverFunds 2.53 2.53* 2.53*

Small Funds SelfManagedSuperFunds 0.87 1.01 1.08

Total (%) 1.26 1.30* 1.37*

(41) AustralianSecuritiesandInvestmentsCommission,RegulatoryGuide168:Disclosure:ProductDisclosureStatements,May2007.(42) InvestmentandFinancialServicesAssociation/RiceWarner,Superannuation Fees Report,May2007.

PAgE 26 | MAnAgED FunDS In AuSTRAlIA 2008

Fund Management Fees – 2002 to 2006

*ExcludesemployerplanswithlessthanA$5millioninassets.

#EmployerplanswithlessthanA$5millioninassets

Source: Investment and Financial Services Association/Rice Warner, Superannuation Fees Report, May 2007

Theincreasingpopularityofproductssuchashedgefundsandprivateequity,whichcarrymuchhigherfeesthanaretypicalwithmoretraditionalassetclasses,hastosomeextentoffsetthefallingleveloffeesininvestors’portfolios.Furthermore,theemergenceofperformance-basedfees inbothalternative investments,suchashedgefunds,andinmoretraditionalmanagedinvestmentsisintroducingavariablecomponenttothefeespaidbyinvestors.Thesefeesarebecomingincreasinglycommoninbothretailandwholesaleproducts.

Fees and Expenses By Superannuation Segment – Year to 30 June 2006

Investment Administration Cost of Total Administration Management & Investment Advice Expenses Sector Segment % % Management % % %

Wholesale Corporate 0.30 0.48 0.78 – 0.78

CorporateSuperMasterTrust*(large) 0.23 0.56 0.79 0.02 0.81

Industry 0.49 0.64 1.13 – 1.13

PublicSector 0.25 0.45 0.70 – 0.70

Retail CorporateSuperMasterTrust#(small) 0.78 0.77 1.55 0.46 2.01

PersonalSuperannuation 0.80 0.77 1.57 0.55 2.12

RetirementIncome 0.60 0.66 1.26 0.53 1.79

RetirementSavingsAccounts 0.60 1.70 2.30 – 2.30

EligibleRolloverFunds 2.08 0.45 2.53 – 2.53

Small Funds SelfManagedSuperFunds 0.47 0.26 0.73 0.15 0.87

Total (%) 0.52 0.54 1.06 0.21 1.26

Variation within Segments

Source: Investment and Financial Services Association/Rice Warner, Superannuation Fees Report, May 2007

3.50

3.00

2.50

2.00

1.50

1.00

0.50

0.00Corporate Industry Public Sector Corporate Super

Master TrustPersonal

SuperannuationRetail PostRetirement

Mean

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 27

OtherIndustryParticipants

AssetConsultantsAssetconsultantsadvise institutional investorsonawide rangeofmatters, fromgovernanceandstrategicissues, through setting, documenting and implementing an investment strategy, to investment managerselectionandfinallyperformanceappraisalandriskmanagement.TheassetconsultingsectorhasgrownrapidlyinAustraliawiththegrowthinsuperannuationfundsandtheincreasingattentionongovernanceissuesbylocalinstitutionalinvestors.MostofthelargerplayersareforeignownedbuthavewellresourcedofficesinatleastMelbourneandSydney.Inanumberofcasestheassetconsultingfirmsmanagetheirownfundoffundproductswhichgounderthetitleof‘implementedconsulting’services.Severalleadinginstitutionsalsoofferfundof fundproducts.Themainparticipants in themarkethadapproximatelyA$575billionunderadviceandA$215billionundermanagementinMarch2007.

N/A=NotApplicable

Note:MorningstarandStandard&Poor’sprovideconsultingadviceinrelationtodealergroupapprovedproductlists.

Source: Chant West Financial Services, March 2007

Main Asset Consultants and Implemented Providers in Australia

Consultant/Institution Owner Funds under Funds under Advice Management A$ Billion A$ Billion

AccessCapitalAdvisers Independent 10 N/A

AMP ASXlisted N/A 20

AonConsulting NYSElisted 5 N/A

ASGARD StGeorge N/A 5

AVIVA AVIVA N/A 2

BT Westpac N/A 2

ColonialFirstState CommonwealthBank N/A 15

FrontierInvestmentConsulting IndustryFunds(4) 85 N/A

Intech OldMutual 20 9

ING INGGroup N/A 8

IPAC AXAGroup N/A 15

JANAInvestmentAdvisers NationalAustraliaBank 115 6

Mercer Marsh&McLennan 100 12

MLC NationalAustraliaBank N/A 78

QIC QLDGovernment N/A 19

RussellInvestmentGroup NorthwesternMutual 100 22

WatsonWyatt NYSElisted 100 N/A

vanEykResearch Independent 40 2

Total 575 215

PAgE 28 | MAnAgED FunDS In AuSTRAlIA 2008

TenderConsultantsThe rise in ‘implemented consulting’ services, where traditional consulting firms offer pooled investmentproductstotheirclients,hasspurredthedevelopmentofanewtypeof‘independent’adviserinthewholesalemarket.Tenderconsultantsareretainedbywholesale investorstoguidetheirselectionofserviceproviders,especially in choosing implementedconsulting relationshipswhen the investors’ownconsultantwouldbeconflicted.Tenderconsultantsarealsosometimesusedbywholesaleinvestorstochoosetraditionalconsultingserviceproviders,fundadministratorsandinsuranceproviders.(43)

FinancialPlannersandFinancialAdvisoryNetworksFinancialplannersadviseindividualsonsuitableformsofinvestmentfortheirassets,aswellasriskmanagement,insurance,taxation,retirementandestateplanningissues.

AfinancialplannermustholdeitheranAFSLorbeanauthorisedrepresentativeofanAFSLholderinordertoprovideadvicetoclients.Giventheapplicationrequirementsandtheongoing licenceconditions, individualplannersfrequentlyformorjoinafinancialadvisorynetwork(alsoknownasadealergrouporfinancialplanninggroup.)Aswiththefundsmanagementindustry,manyofthelargerfinancialplanninggroupsareaffiliatedwithlargefinancialinstitutions,suchasbanks,insurancecompaniesand,increasingly,largesuperannuationfunds.TheyprovidesupportservicestofinancialplannersintheformofITsystems,clientmanagementplatforms,complianceprocessesandproductresearch.Undersection932AoftheCorporations Act 2001,suchadviserscannotcallthemselves‘independent’whenadvisingonproductissuedbyrelatedparties.

AccordingtotheFinancialPlanningAssociation,thereareapproximately16,000financialplannersinAustraliaandindustryestimatesindicatethatthelargerdealergroupsareexperiencingnetgrowthofabout10percentayearintermsofplannernumbers.

(43) SuperfundsOctober2004,Human Resources Magazine,October2003.

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 29

FUA=FundsUnderAdvice

N/A=NotApplicable

Source: InvestorSupermarket, Top 100 Dealer Groups Survey, 30 June 2007

Top 50 Dealer groups in Australia

Rank Dealer group number of Total FuA Advisers $A Million

1 ProfessionalInvestmentServ’s 1,465 16,800

2 AMPFinancialPlanning 1,216 42,825

3 CountFinancial 895 12,410

4 CommonwealthFinancial 702 25,540Planning

5 WestpacFinancialPlanning 594 24,147

6 Millennium3Financial 517 4,200 Services

7 MLC/GarvanFP 481 11,022

8 NABFinancialPlanning 464 13,000

9 ABNAMROMorgansLimited 447 30,000

10 CharterFinancialPlanning 429 N/A

11 Securitor 418 N/A

12 FinancialWisdomLtd 416 9,632

13 ANZFinancialPlanning 408 11,995

14 AXAFinancialPlanning 406 N/A

15 GenesysWealthAdvisers 390 12,200

16 HillrossFinancialServicesLtd 285 11,800

17 LonsdaleFinancialGroup 256 8,500

18 RetireInvest 224 12,500

19 SuncorpFinancialPlanningP/L 216 3,230

20 BridgesFinancialServicesP/L 213 8,930

21 AustralianFinancialServices 199 6,000

22 GodfreyPembrokeFinancial 181 5,276Consultants

23 WealthsureFinancialServices 181 1,800

24 FinancialLifestyleSolutions 177 n/a

25 ApogeeFinancialPlanning 174 3,120

Rank Dealer group number of Total FuA Advisers $A Million

26 AonFinancialPlanning 163 2,100 andProtectionLtd

27 AFGFinancialPlanningP/L 153 N/A

28 GuardianFinancialPlanning 150 1,350

29 FinancialServicesPartners 141 3,000

30 AAAFinancialIntelligence 131 N/A

31 UBSWealthManagement 120 N/A

32 LifespanFinancialPlanning 119 1,369

33 ConsultumFinancialAdvisers 104 2,000

34 TotalFinancialSolutions 102 1,500 Australia

35 StGeorgeFinancialPlanning 97 3,510

36 WHKGroupLimited 93 8,000

37 BongiornoFinancialAdvisers 91 1,600

38 SnowballGroup 82 4,250

39 MeritumFinancialGroupP/L 81 2,300

40 MacquarieWealthMgmt 77 4,700

41 MatrixPlanningSolutions 77 2,200

42 MadisonFinancialGroupP/L 75 2,500

43 TandemFinancialAdvice 74 2,500

44 MyAdviser 74 N/A

45 FinancialPlanningServices 68 N/A Australia

46 MercerWealthSolutions 65 4,127

47 CapstoneFinancialPlanning 64 2,100

48 FuturoFinancialServicesP/L 57 1,200

49 IndustryFundServicesP/L 56 1,900

50 PremiumWealthManagement 55 1,500

PAgE 30 | MAnAgED FunDS In AuSTRAlIA 2008

Platforms,MasterTrustsandWrapAccountsOneofthemost importantfeaturesofthemanagedfundsmarket inrecentyearshasbeentheincreaseinthe use ofmaster trusts andwrap accounts(44). Bothmaster trusts andwrap accounts are platforms thatgive investors access to a ‘supermarket’ of investment andfinancial services products through a ‘gateway’thatpromotesconsumerconvenienceanddiversityofinvestment.Theseplatformsareadministrativeinthatthe platformprovider bundles a range of investment products and services (supported by technology andadministrativeexpertise)thatcanbesoldtomeettheconsumer’sneeds.

Thetypesofplatformsofferedinthemarketinclude:

n Discretionary funds–wheretheinvestorsselecttheunderlyingfunds.

n Fund of funds–wheretheplatformproviderselectstheunderlyingfunds.

n Personal master trusts–wheretheinvestorselectstheindividualassetsintheirportfolio.

AccordingtofiguresfromresearchhouseMorningstar,inJune2007approximatelyA$420billionwasheldinmastertrustsandwrapaccounts.(45)Liketheretailmanagedfundssector,thisareaisdominatedbydomesticbankinginstitutions,withthelargestfiveplayersaccountingforaround60percentoftotalassets.Industrysourcesagreethatmarginpressurewillforcesomelevelofconsolidationinthissectoroverthenextthreeyears.(46)

Mastertrustshavebeen,andcontinuetobe,animportantforceforchangeintheindustry.Theyhaveblurredthedistinctionbetweentheretailandwholesalesectorsoftheindustrybyprovidingretailinvestorswithaccesstowholesaleinvestmentproducts(andfees).Moreover,financialplannershaveusedmastertruststostreamlinetheirbackofficefunctionsandre-orienttheadvicetheyprovideawayfromcommission-basedfundsales.MastertrustsarealsousedbyindividualstoprovideaplatformforSMSFs.

Source: Morningstar, Market Share Report, June 2007

(44) Themaindifferencebetweenamastertrustandawrapaccountisthelegalstructure.Inamastertrustthetrusteeholdstitletotheassetsonbehalfoftheinvestor,butinawrapaccounttheinvestorholdstheassetsdirectly.Inbothcases,theinvestoristhebeneficialowneroftheassets.

(45) Morningstar,Market Share Report,June2007.(46) PricewaterhouseCoopers,Australian Investment Management Survey,2006.

Funds under Administration – Retail Platforms – June 2007

Administrator A$ Billion

1 National/MLCGroup 70.5

2 BT/WestpacGroup 54.2

3 AMP 47.7

4 StGeorgeGroup 43.8

5 Commonwealth/ColonialGroup 36.5

6 ING/ANZGroup 36.4

7 MacquarieBankGroup 29.6

8 AXAGroup 28.0

9 Navigator 18.7

10 AustralianWealthManagementLimited 16.0

Top 10 Total 381.6

Industry Total 419.6

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 31

ThirdPartyRepresentativesThirdpartymarketingrepresentativesarequitecommonincertainnichesoftheAustralianmarket,includinghedgefunds,privateequityandspecialistequitiesmanagement.Theseorganisationstypicallycompriseasmallnumberofkeyindividualswhocoordinatesales,marketing,clientserviceactivitiesandinsomecasesdistributiononbehalfofoverseasinvestmentfirmsandprovidealocalpointofcontactformasterfunds,assetconsultants,localinvestmentmanagersandothers.Insomecases,overseasfirmshaveusedthirdpartyrepresentativesasawaytoentertheAustralianmarketpriortocommittingdedicatedresourcesonthegroundinAustralia.

CustodiansAustraliahasasophisticatedandfullservicecustodysector(47).Typicaloftheglobalmodel,thecustodianholdsassetsonbehalfoftheinvestor,suchasasuperannuationfundormanagedfund.Thecustodianthereforehasthetitletothefundassetsbutthepowersofinvestmentmanagementremainwiththetrustees.Themainbenefitofacustodianisadministrativeefficiency.Itwillbringtogetherafund’sinvestmentportfolios,enablingacloserwatchoninvestments.Itcollectsincome,reportsonthevalueofassets,providesregisteredaddressesoffshoreand,ifthetrusteesofaplanareindividuals,eliminatesthenecessitytotransfertheownershipofassetstothenewtrusteeseachtimethereisachange.Amastercustodianaggregatesaseriesofportfoliosandaglobalcustodianholdsassetsforclientsinanumberofdifferentcountries.Usuallyacustodianisacompany(e.g.trusteecompany,bankorspecialistcustodiancompany).

Source: Invest Australia, The Custody Industry in Australia, 2006

(47) Forfurtherinformation,seeInvestAustralia’s,The Custody Industry in Australia,2006.

key Providers in the Australian Custody Industry

Investment Domestic global Master Manager Custody Custody Custody Outsourcing

ANZCustodians n

BankofNewYork n

BNPParibas n n n

Citigroup n n

HSBCCustodyNominees n

JPMorganWorldwideSecurities n n n n

NationalCustodialServices n n n

NorthernTrust n

RBCDexiaInvestorServices n n n n

StateStreet n n n

WestpacCustodialServices n

PAgE 32 | MAnAgED FunDS In AuSTRAlIA 2008

AssetsUnderAdministration(MasterCustody) A$1,363.8billion

GlobalCustodyAssets A$448.6billion

DomesticCustodyAssets A$1,649.3billion

NumberofCustodians 12

NumberofGlobalCustodians 8

NumberofEmployees Morethan2,500

Source: Australian Custodial Services Association

ResearchHousesandRatingAgenciesResearchhousesprovidequantitativeandqualitativeinvestmentinformationtosubscribersand,inareducedform,tothepublicviawebsites.Mostprovidelistsofrecommendedfundsand/orfundratings.Intermediariessuchasdealergroups,financialplanners,superannuationfundsandsomeinstitutionsusetheresearchtoguidetheirclientrecommendations.

ThemainprovidersoffundresearchintheAustralianmarketare:

n ChantWest

n DEXX&R

n InTechResearchPtyLtd

n LonsecResearch

n MorningstarResearch

n RainmakerInformation

n Standard&Poor’s

n SuperRatings

n vanEykResearch.

ServiceProvidersService providers supply software and/or IT support for fund managers. The industry has grown rapidlyinAustralia, not only becauseof the growth in superannuation funds, but alsodue to the fact thatmanyinternationalserviceprovidershavechosentomoveoperationstoAustraliatocapitaliseonitshighlyskilledworkforceandrelativelylow-costenvironment.Bloomberg,ReutersandBravuraareamongtheglobalfirmswithasignificantpresenceintheAustralianmarket.

Australian Custody Market – June 2007

MAnAgED FunDS In AuSTRAlIA 2008 | PAgE 33

FrameworkAustraliaaspirestoglobalbestpractice in itsfinancialservicesregulatoryframework.Thisobjectivewasanimportantmotivationforthesignificantstructuralchangestotheregulatoryarrangementsenactedsince1997.ThesechangeshavecementedthereputationofAustralia’sfinancialservicesindustryasbeingamongthemostefficientlyregulatedintheworld.

Supervisionofthesectorisnoworganisedalongfunctionalinsteadofinstitutionallines.WhiletheRBAplaysamajorroleintheoperationandefficiencyofthefinancialsystem,therearetwomajorregulatorybodiesrelevanttotheinvestmentmanagementindustryinAustralia;APRAandASIC.Thesestatutorybodieshaveoperationalindependence,whichmeanstheGovernmentprovidesguidanceintheformofobjectives,valuesandpolicies,butdoesnotinterfereinday-to-daymatters.RecentreviewsofthesystemhavestressedtheimportanceofAPRAandASICworkingcloselytogethertominimiseoverlap,inefficiencyorotherproblemsthatwouldadverselyimpactontheachievementofcompetitiveneutrality,cost-effectiveness,transparency,flexibilityandaccountability.(48)

(a) The Australian Prudential Regulation Authority (APRA)

APRAisAustralia’sprudentialregulatorofbanks,insurancecompanies,superannuationfunds(otherthanselfmanagedsuperannuationfunds),creditunionsandbuildingandfriendlysocieties.APRAhelpstoensuretheefficiencyandeffectivenessoftheAustralianfinancialsystem.Itsmissionistoestablishandenforceprudentialstandardsandpracticestoensurethatfinancialpromisesmadebyinstitutionsaremetwithinastable,efficientandcompetitivefinancialsystem.InformationaboutAPRAanditsoperationscanbefoundatwww.apra.gov.au.

(b) The Australian Securities and Investments Commission (ASIC)

ASICenforcescompanyandfinancialserviceslawstoprotectconsumers,investorsandcreditors.ItregulatesandinformsthepublicaboutAustraliancompanies,financialmarkets,financialserviceorganisationsandprofessionalswhodealandadvise in investments,superannuation, insurance,deposittakingandcredit. In1998itbecameresponsibleforconsumerprotectioninsuperannuation,insurance,deposittakingand(from2002)credit.ASICisresponsibleforissuingAFSLsandregisteringmanagedinvestmentsschemes.InformationaboutASICanditsoperationscanbefoundatwww.asic.gov.au.ASICalsomaintainsaconsumer-focusedwebsiteatwww.fido.gov.au.

RegulatoryEnvironment

(48) AustralianPrudentialRegulationAuthority/AustralianSecuritiesandInvestmentsCommission,IR 07-03 APRA ASIC Working Group Status Report,5February2007.

PAgE 34 | MAnAgED FunDS In AuSTRAlIA 2008

TREASuRER

ReserveBankofAustralia

(RBA)

AustralianPrudentialRegulationAuthority

(APRA)

AustralianSecuritiesandInvestmentsCommission

(ASIC)

nMonetaryPolicynSystemicstabilitynPaymentssystemsregulation

nPrudentialregulationof:–Deposit-takinginstitutions–Lifeandgeneralinsurance–Superannuationfunds

nMarketintegritynConsumerprotectionnCorporations

COunCIl OF FInAnCIAl REgulATORS

Note:MembershipoftheCouncilofFinancialRegulatorsalsoincludestheCommonwealthTreasury.

Source: KPMG 1998 Financial Institutions Performance Survey

PaymentSystemsBoard