Macquarie Private Wealth Australia · Macquarie Private Wealth Australia Independent Risk Culture...

59

Macquarie Private Wealth Australia Independent Risk Culture Review Final Report May 2013 Confidential & Commercially Sensitive MGL.0001.0003.0187

Transcript of Macquarie Private Wealth Australia · Macquarie Private Wealth Australia Independent Risk Culture...

Macquarie Private Wealth Australia

Independent Risk Culture Review

Final Report

May 2013

Confidential & Commercially Sensitive

MGL.0001.0003.0187

2

Contents

Executive Summary 3

Areas of Strength 11

Theme 1 – Inertia 13

Theme 2 – Risk insight clouded 21

Theme 3 – Freedom without boundaries 29

Theme 4 – Short-term focus 35

Theme 5 – Sidelined risk function 45

Appendix 1 – Data sources 49

Appendix 2 – Tier 1 Analysis 53

Confidential & Commercially Sensitive

MGL.0001.0003.0188

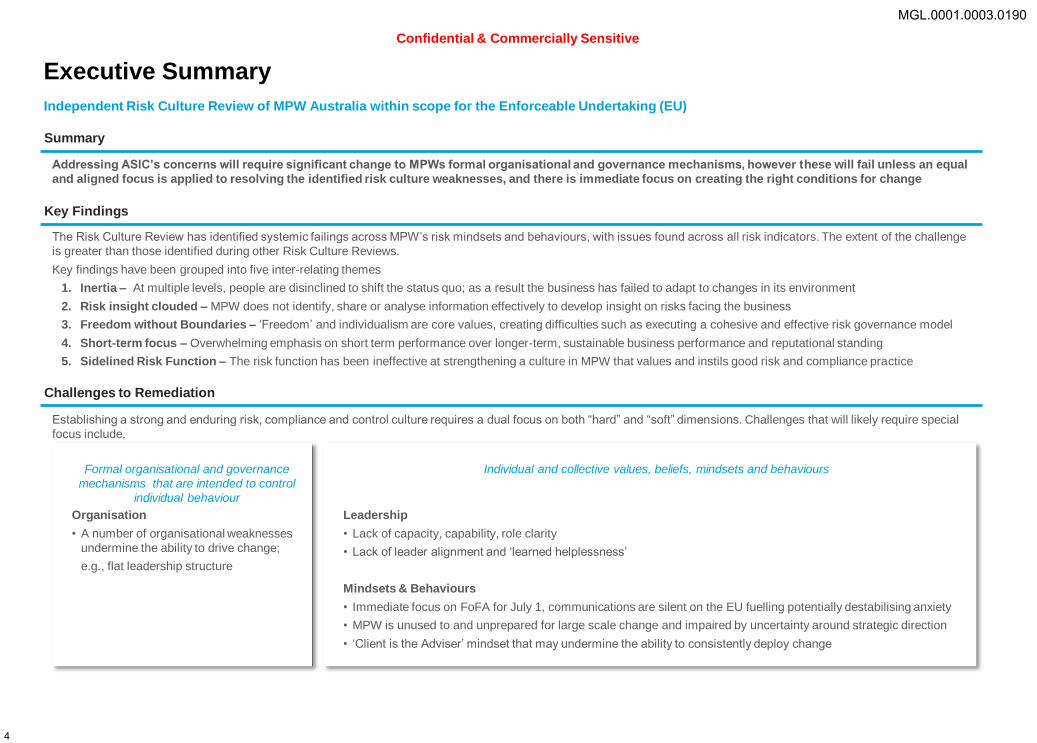

Executive Summary

MGL.0001.0003.0189

4

Establishing a strong and enduring risk, compliance and control culture requires a dual focus on both “hard” and “soft” dimensions. Challenges that will likely require special

focus include.

‘Hardware’ ‘Software’

Executive Summary

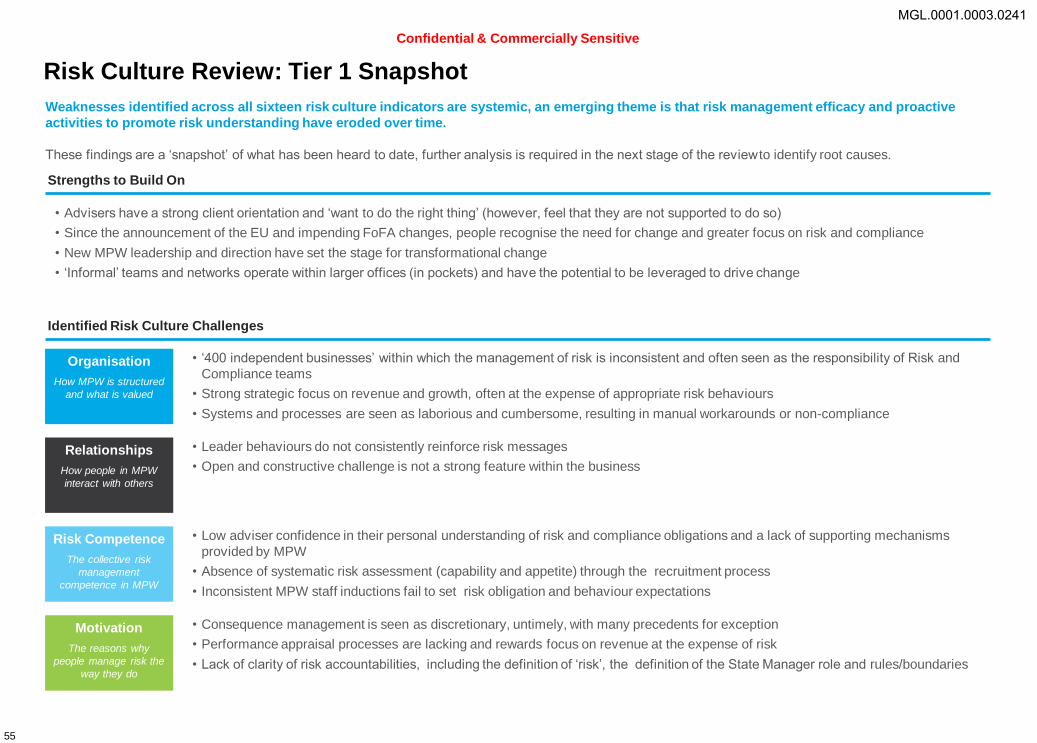

The Risk Culture Review has identified systemic failings across MPW’s risk mindsets and behaviours, with issues found across all risk indicators. The extent of the challenge

is greater than those identified during other Risk Culture Reviews.

Key findings have been grouped into five inter-relating themes

1. Inertia – At multiple levels, people are disinclined to shift the status quo; as a result the business has failed to adapt to changes in its environment

2. Risk insight clouded – MPW does not identify, share or analyse information effectively to develop insight on risks facing the business

3. Freedom without Boundaries – ‘Freedom’ and individualism are core values, creating difficulties such as executing a cohesive and effective risk governance model

4. Short-term focus – Overwhelming emphasis on short term performance over longer-term, sustainable business performance and reputational standing

5. Sidelined Risk Function – The risk function has been ineffective at strengthening a culture in MPW that values and instils good risk and compliance practice

Key Findings

Challenges to Remediation

Addressing ASIC’s concerns will require significant change to MPWs formal organisational and governance mechanisms, however these will fail unless an equal

and aligned focus is applied to resolving the identified risk culture weaknesses, and there is immediate focus on creating the right conditions for change

Organisation

• A number of organisational weaknesses

undermine the ability to drive change;

e.g., flat leadership structure

Leadership

• Lack of capacity, capability, role clarity

• Lack of leader alignment and ‘learned helplessness’

Mindsets & Behaviours

• Immediate focus on FoFA for July 1, communications are silent on the EU fuelling potentially destabilising anxiety

• MPW is unused to and unprepared for large scale change and impaired by uncertainty around strategic direction

• ‘Client is the Adviser’ mindset that may undermine the ability to consistently deploy change

Formal organisational and governance

mechanisms that are intended to control

individual behaviour

Individual and collective values, beliefs, mindsets and behaviours

Independent Risk Culture Review of MPW Australia within scope for the Enforceable Undertaking (EU)

Summary

Confidential & Commercially Sensitive

MGL.0001.0003.0190

5

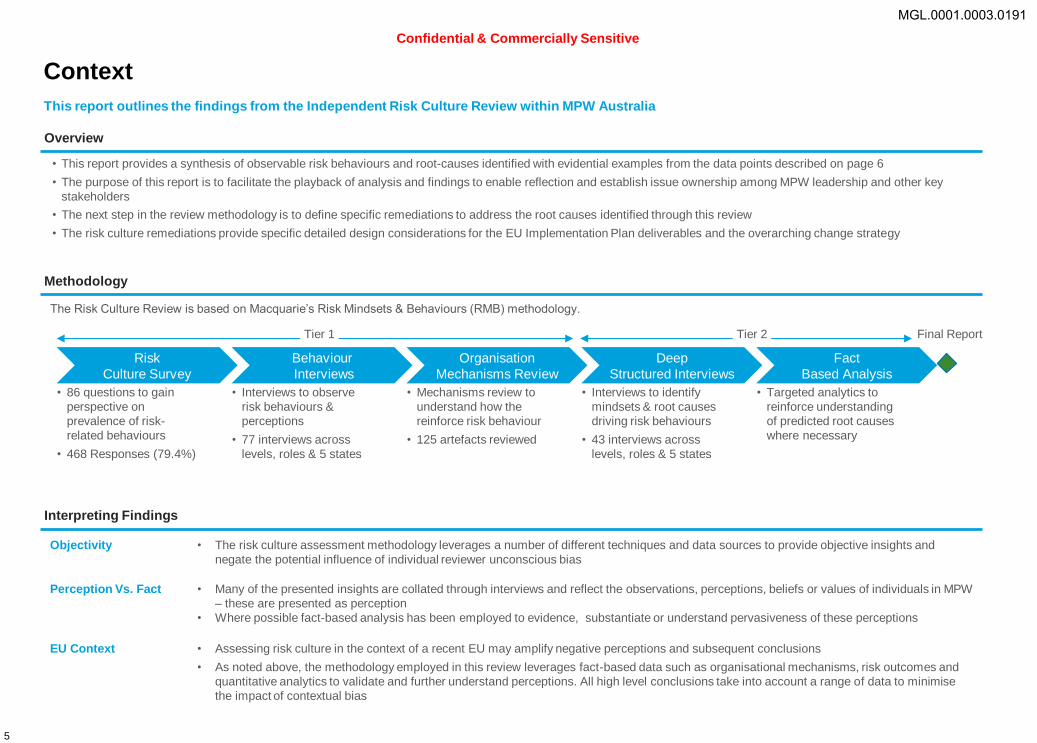

Context

The Risk Culture Review is based on Macquarie’s Risk Mindsets & Behaviours (RMB) methodology.

This report outlines the findings from the Independent Risk Culture Review within MPW Australia

Methodology

Risk

Culture Survey

• 86 questions to gain

perspective on

prevalence of risk-

related behaviours

• 468 Responses (79.4%)

Behaviour

Interviews

• Interviews to observe

risk behaviours &

perceptions

• 77 interviews across

levels, roles & 5 states

Organisation

Mechanisms Review

• Mechanisms review to

understand how the

reinforce risk behaviour

• 125 artefacts reviewed

Deep

Structured Interviews

• Interviews to identify

mindsets & root causes

driving risk behaviours

• 43 interviews across

levels, roles & 5 states

Fact

Based Analysis

• Targeted analytics to

reinforce understanding

of predicted root causes

where necessary

Tier 1 Tier 2

• This report provides a synthesis of observable risk behaviours and root-causes identified with evidential examples from the data points described on page 6

• The purpose of this report is to facilitate the playback of analysis and findings to enable reflection and establish issue ownership among MPW leadership and other key

stakeholders

• The next step in the review methodology is to define specific remediations to address the root causes identified through this review

• The risk culture remediations provide specific detailed design considerations for the EU Implementation Plan deliverables and the overarching change strategy

Overview

Interpreting Findings

Final Report

Objectivity • The risk culture assessment methodology leverages a number of different techniques and data sources to provide objective insights and

negate the potential influence of individual reviewer unconscious bias

Perception Vs. Fact • Many of the presented insights are collated through interviews and reflect the observations, perceptions, beliefs or values of individuals in MPW

– these are presented as perception

• Where possible fact-based analysis has been employed to evidence, substantiate or understand pervasiveness of these perceptions

EU Context • Assessing risk culture in the context of a recent EU may amplify negative perceptions and subsequent conclusions

• As noted above, the methodology employed in this review leverages fact-based data such as organisational mechanisms, risk outcomes and

quantitative analytics to validate and further understand perceptions. All high level conclusions take into account a range of data to minimise

the impact of contextual bias

Confidential & Commercially Sensitive

MGL.0001.0003.0191

6

Data Sources

26 52 22

The report uses a number of tools and evidential examples from the data sources to support conclusions

Overview of Data Sources*

*A more detailed explanation of data points is included in the Appendix 1

Organisation Mechanism Reviews

• A review of MPW business policies, processes,

procedures and enabling systems has been

conducted to understand how these reinforce a

clear expectation of behaviour

• Artefacts were evaluated against the Risk Mindsets

& Behaviours Framework

That’s where it helps when you work

with a planner – they can do the

compliance and planning.

Risk Culture Survey

• Numbers represent percentage distribution of

responses, excluding the responses of those who

answered ‘N/A’.

• Unless otherwise stated, the graph relates to all

respondents

People in MPW are inclined to take excessive risk

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Behaviour Interview Analysis

• Numbers represent the different categories of risk

behaviours identified (detrimental, developing and

desirable) as ‘more like MPW’ when an

interviewee was questioned on a given Risk

indicator

Interview Comments

• Quotes from the survey, behaviour, and deep

structured Interviews have been illustrated in

speech bubbles

• These verbatim quotes have been extracted from

notes taken during interviews

• Demographic information has not been provided to

protect the confidentiality of interviews

23 29 28

“Behaviours relating to incentives and consequences”

Desirable Developing Detrimental

%

distribution

%

distribution

Fact Based Analysis

• Hypothesis-based analysis has been used to

confirm if perceived behaviours are actually

occurring and to draw insight of knock-on effects

Driver Trees

• Driver trees were used to synthesise codified

analysis of interviews and illustrate the underlying

root causes of each theme and subtheme

Confidential & Commercially Sensitive

MGL.0001.0003.0192

7

Key Findings

Findings from the Risk Culture Review have been grouped into five inter-relating themes

1. Inertia | At multiple levels, people are

disinclined to shift the status quo; as a result

the business has failed to adapt to changes in

its environment

3. Freedom without boundaries | ‘Freedom’

and individualism are core values, creating

difficulties such as executing a cohesive and

effective risk governance model

4. Short-term focus | Overwhelming

emphasis on short term performance over

longer-term, sustainable business

performance and reputational standing

5. Sidelined risk function | The risk function

has been ineffective at strengthening a

culture in MPW that values and instils good

risk and compliance practice

2. Risk insight clouded | MPW does not

identify, share or analyse information effectively

to develop insight on risks facing the business

Self-

perpetuating

cultural drivers

Management

style and

decisions

Freedom

without

boundaries

Sidelined

risk function

Short-term

focus

Confidential & Commercially Sensitive

MGL.0001.0003.0193

8

Summary of insights

1 | Inertia

At multiple levels, people are disinclined to shift the status

quo; as a result the business has failed to adapt to changes in

its environment

Impact

• Regulatory consequences with significant costs and reputational damage

attached

• Failure to respond effectively to external expectations e.g. FoFA

• Recurring failure to uphold internally-set standards

• Challenge for MPW to effectively mobilise and embed the required

changes of the EU implementation plan

Key drivers

A. Leaders do not drive change

B. Learned helplessness prevents people at multiple levels from trying to

initiate change

C. Advisers are unmotivated to spend time improving their compliance

capability

2 | Risk insight clouded

MPW does not identify, share or analyse information

effectively to develop insight on risks facing the business

Impact

• Gaps in senior leader appreciation of serious risk management

inadequacies

• Exposure to unacceptable levels of unmitigated risk

• Inability to respond proactively to risk issues

Key drivers

A. Information flow is stymied

B. The organisation has weaknesses across a range of capabilities that would

improve its ability to recognise and appropriately respond to issues

C. Failure to challenge and ineffective escalation

Theme 1 and 2 are self-perpetuating and multi-faceted aspects of the culture that will be challenging to shift

Confidential & Commercially Sensitive

MGL.0001.0003.0194

9

Summary of insights

3 | Freedom without boundaries

‘Freedom’ and individualism are core values, creating

difficulties such as executing a cohesive and effective risk

governance model

Impact

• Principle that ‘the client is the adviser’ undermines MPW ability to establish

and maintain minimum standards regarding compliance and quality of

advice

• Difficulty providing appropriate and standardised tools and processes to

facilitate effective and efficient compliance outcomes

• Challenging to align, influence and hold people accountable for shared

organisational goals – e.g., management of reputational risk

• Inability to capture benefits of a more team-based environment including

peer review, coaching and tailored training

Key drivers

A. Organisational model and capabilities result in few explicit boundaries

being set across the business

B. There is little acceptance by many Advisers for the (few) boundaries

that are set

4 | Short term focus

Overwhelming emphasis on short term performance over

longer-term, sustainable business performance and

reputational standing

Impact

• A one dimensional driver of revenue among advisers, in some cases

resulting in decisions that compromise integrity, client's interests and

Macquarie’s reputation

• Tight cost management and lack of investments in systems and people

• Multiple ‘band-aid’ solutions that, over time, have simultaneously decreased

effectiveness and increased the cost of compliance relative to peers

• Lack of selectivity on recruitment and acceptance of advisers with

questionable reputations

Key drivers

A. Leaders are regarded as overwhelmingly short-term revenue and cost

focused

B. Adviser/broker culture exacerbates over-emphasis on revenue

C. Broader Macquarie and industry environment places extreme focus on

financial targets without adequate balance on other goals

Themes 3, 4 and 5 are reinforced by a combination of management factors, but possibly less challenging to address than Themes 1 and 2

Confidential & Commercially Sensitive

MGL.0001.0003.0195

10

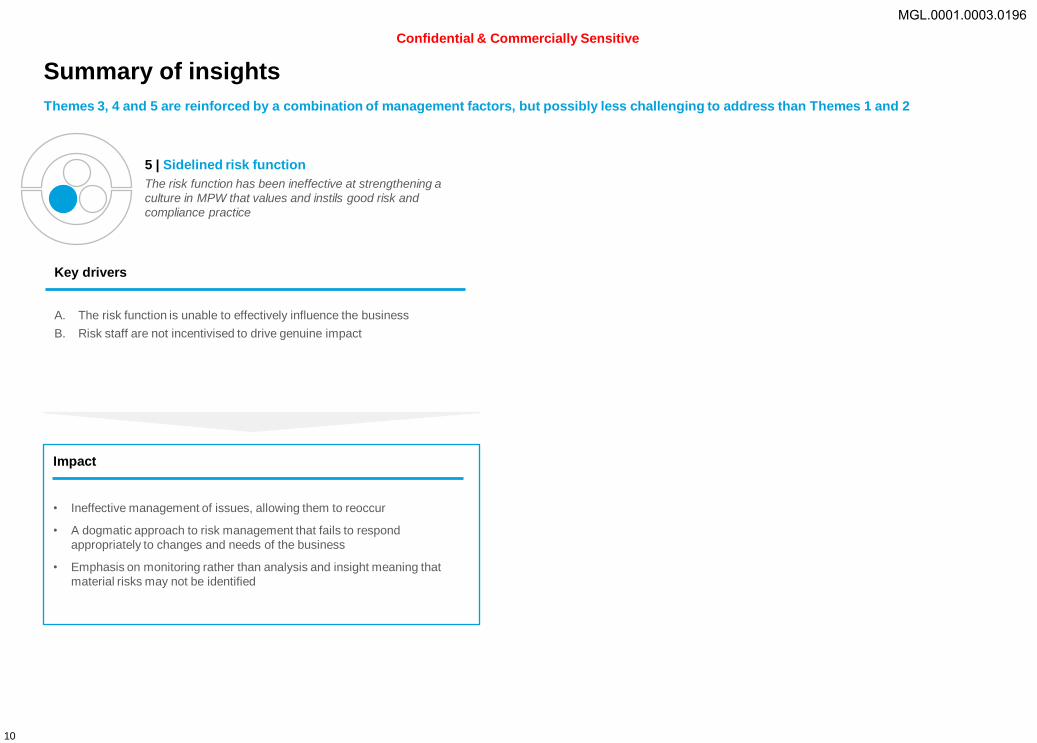

Summary of insights

5 | Sidelined risk function

The risk function has been ineffective at strengthening a

culture in MPW that values and instils good risk and

compliance practice

Impact

• Ineffective management of issues, allowing them to reoccur

• A dogmatic approach to risk management that fails to respond

appropriately to changes and needs of the business

• Emphasis on monitoring rather than analysis and insight meaning that

material risks may not be identified

Key drivers

A. The risk function is unable to effectively influence the business

B. Risk staff are not incentivised to drive genuine impact

Themes 3, 4 and 5 are reinforced by a combination of management factors, but possibly less challenging to address than Themes 1 and 2

Confidential & Commercially Sensitive

MGL.0001.0003.0196

Areas of strength

MGL.0001.0003.0197

12

Strong client orientation amongst a core group of advisers,

particularly Financial Planners

Areas of strength

New leadership recognised as a strong symbol of change

• Financial Planners recognise that long term client relationships are critical to

the sustainability of their business models

• Planners are more focused on compliance activities, evident in the number of

breaches received relative to brokers (see chart below)

• Many planners welcome FoFA changes and the resolution of issues raised in

the EU, providing a capability and behaviour foundation to build upon

• New MPW leadership and direction have set the stage for transformational

change

• Most people recognise the EU as a catalyst for greater focus on risk and

compliance

This kind of regulatory change is a

once-in-a-lifetime opportunity. It’s an

opportunity because it’s a good thing for

clients. So the question is, how do we

make the most of this opportunity?

Financial Planners are very strong at

Risk and Compliance. They come from

a background where all plans are written

by Para-planners before advice is given,

so record keeping, keeping file notes

etc. is embedded in their culture

There has been a lot more engagement

with advisers post EU Because of the EU people’s behaviour

is starting to change…Whether it’s

because of Bill and Greg Ward watching

or whether they feel personally

responsible because of the EU... there

has been a big change since December.

Recognition of need for change has led to some emerging teaming

and collaboration

• Some Adviser recognition of the need for strategic solutions to FoFA – e.g.

Brokers partnering with Financial Planners

• Positive examples of ‘Informal’ teams and networks operate within larger offices

That’s where it helps when you work

with a planner – they can do the

compliance and planning.

I partner up with a Financial Planner… I

have a strong belief that we're better off

offering a holistic service to clients

I want to be a better stockbroker - to do

this, I need more technical training in my

area and to complement this by

partnering up with a Financial Planner.

Whilst the focus of the Risk Culture Review has been on identifying improvement opportunities, some strengths emerged for MPW to build upon

Average breaches per person 2012*

Until Bill started it was the wild west

Advisers are there to look after their

clients – they will put them first, do the

best thing

FOFA is exciting. It’s the last cleanup.

The downturn in the market has already

done an initial hosing down, and now it’s

time for the final cleanup

I think they [advisers] can change – I

have seen this post EU and with FoFA

requirements. I’ve actually been

surprised to see some able to adapt

* Based on a headcount of 60 Financial Planners, and 320 Brokers obtained from staff

listing as at 6/12/12

0.76

0.08

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Brokers Planners

Confidential & Commercially Sensitive

MGL.0001.0003.0198

Theme 1: Inertia

MGL.0001.0003.0199

14

2339 38

50 40 10

1

2

3

4

5

2011 2012 2013

J M A M J J A S O N D F Mar A M J J A S O N D J M F

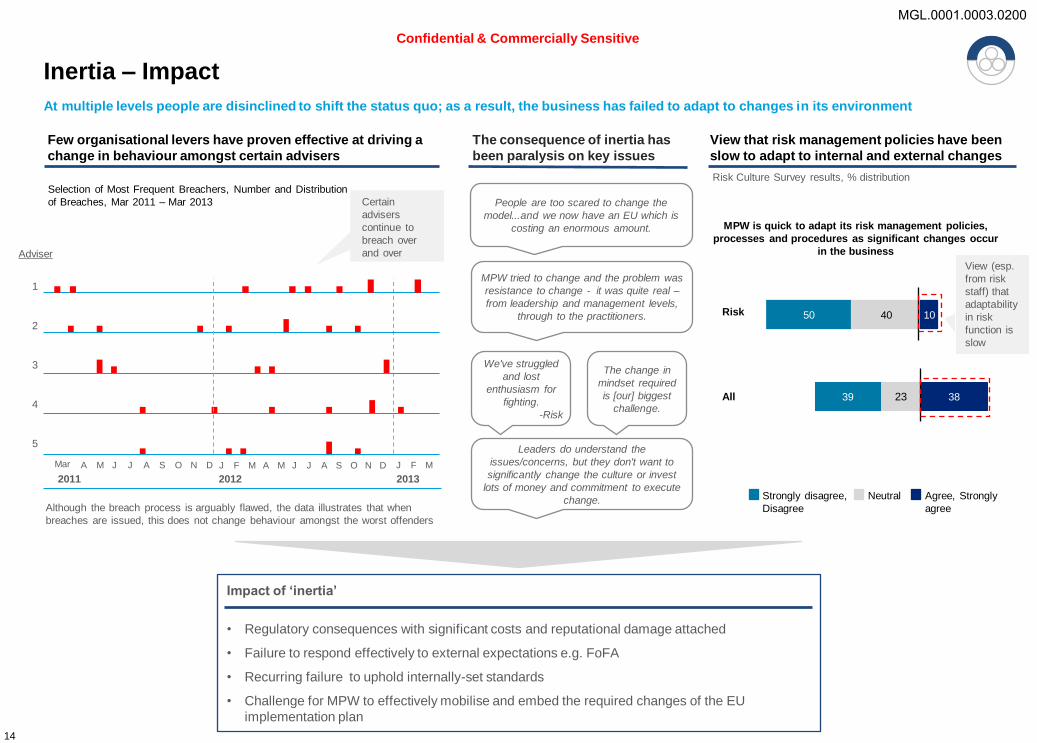

Inertia – Impact

Few organisational levers have proven effective at driving a

change in behaviour amongst certain advisers

The consequence of inertia has

been paralysis on key issues

View that risk management policies have been

slow to adapt to internal and external changes

Impact of ‘inertia’

• Regulatory consequences with significant costs and reputational damage attached

• Failure to respond effectively to external expectations e.g. FoFA

• Recurring failure to uphold internally-set standards

• Challenge for MPW to effectively mobilise and embed the required changes of the EU

implementation plan

Risk

All

MPW is quick to adapt its risk management policies,

processes and procedures as significant changes occur

in the business Adviser View (esp.

from risk

staff) that

adaptability

in risk

function is

slow

Certain

advisers

continue to

breach over

and over

Selection of Most Frequent Breachers, Number and Distribution

of Breaches, Mar 2011 – Mar 2013

At multiple levels people are disinclined to shift the status quo; as a result, the business has failed to adapt to changes in its environment

Risk Culture Survey results, % distribution

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

People are too scared to change the

model...and we now have an EU which is

costing an enormous amount.

We've struggled

and lost

enthusiasm for

fighting.

-Risk

The change in

mindset required

is [our] biggest

challenge.

MPW tried to change and the problem was

resistance to change - it was quite real –

from leadership and management levels,

through to the practitioners.

Leaders do understand the

issues/concerns, but they don't want to

significantly change the culture or invest

lots of money and commitment to execute

change. Although the breach process is arguably flawed, the data illustrates that when

breaches are issued, this does not change behaviour amongst the worst offenders

Confidential & Commercially Sensitive

MGL.0001.0003.0200

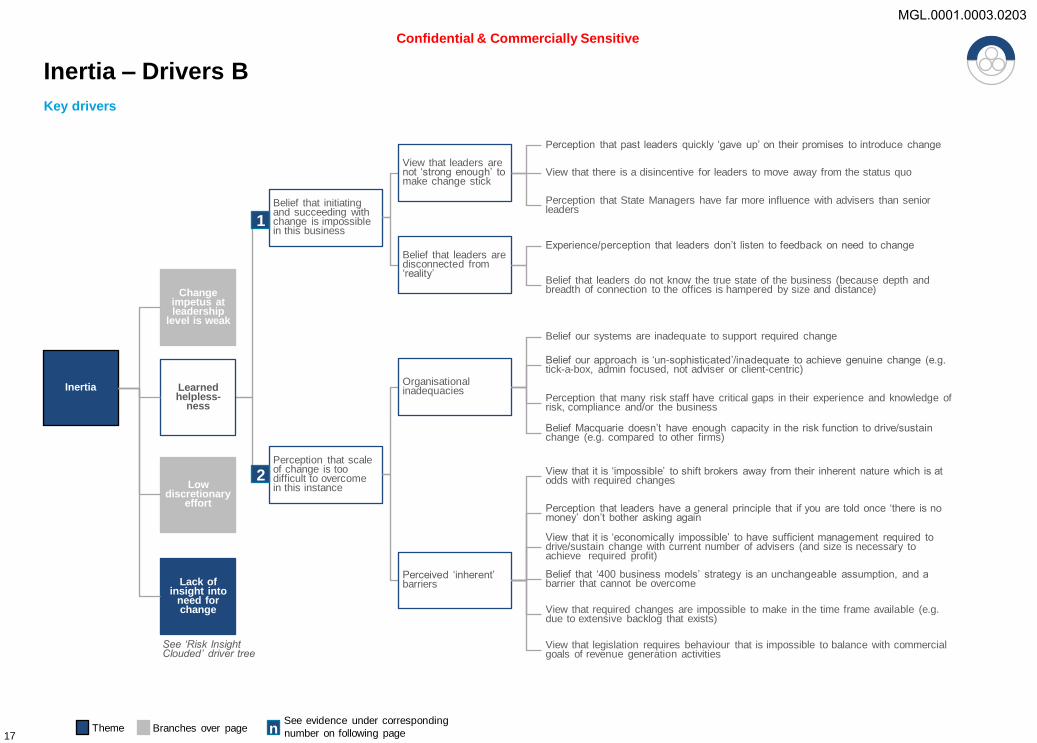

Inertia – Drivers A

Inertia Learned helpless-

ness

Change impetus at leadership

level is weak

Low discretionary

effort

Lack of insight into

need for change

Lack of a unifying purpose to drive change

Difficulty creating a compelling, cohesive vision

Belief that trying to get advisers to conform will be fruitless

Influential State Management level creates localised identity and focus, and a barrier to higher level, division-wide purpose

Flat leadership organisation structure, geographic spread and size of business decreases practicality of personal leadership engagement

FOFA, EU and general external environment have made it difficult to predict ‘what the future holds’ for people in MPW

Many individual cultures (e.g. Brokers vs Planners, team ‘acquisitions’) difficult to reconcile into a single compelling vision and purpose

Highly independent values of adviser population somewhat ‘at odds’ with creating a single vision

Fear that advisers who don’t buy-in to the vision may choose to leave (and take all their clients with them)

See ‘Risk Insight Clouded’ driver tree

No accountability for longer-term goals

Organisation structure

Personal ‘ownership’ of longer-term goals is weak

Central staff who receive profit share are incentivised based on short-term BHAG

achievement

Very strong focus by senior leaders on BHAG gives impression it is the ‘only thing that matters’

Past experiences of being guided to prioritise short-term BHAG leads to perception that this is a general principle

Little articulation of who is accountable for longer-term goals

Intense focus on BHAG undermines prioritisation of longer-term goals

Perception there are few consequences for failing to meet longer-term goals

Diffusion of accountabilities across multiple committees undermines individual accountability

In some cases, ‘empire building’ in head office roles has resulted in diluted focus in key functions that should be more focused on longer-term outcomes

Management structure inhibits decision making

Barriers to decision making

Interpersonal styles a barrier to achieving alignment

Difficulty achieving agreement across complex web of committees and individual

stakeholders

Scope of role/concentration of control makes it unfeasible for senior leaders to be

across everything in a timely manner

Strong personalities that overpower discussions, leading to ‘agreement’ in meetings,

but not genuine buy-in

In some people/situations, a preference to avoid open conflict, resulting in avoidance

rather than honest conversations

1

2

1

Key drivers

Branches over page See evidence under corresponding

number on following page n Theme 15

Confidential & Commercially Sensitive

MGL.0001.0003.0201

23 21 57

29 14 57

26 52 22 52

30 23 47

Inertia – Evidence A

Little impetus to set aspirations to improve risk and

compliance if it might result in lower financial performance

A lack of open, constructive debate amongst leaders regarding

key risk issues stifles the drive for change

Focus on goals

overrides other

drivers like risk

appetite

MPW's business objectives are consistent with

Macquarie's risk tolerance

People in MPW are inclined to take excessive risk

DD

Risk management concerns are discussed openly and

honestly in MPW Australia

AD

SM

Mgr

AM

SA

Assoc

Especially at senior levels,

there is a perception that

risk issues are not debated

freely

1 2

Change impetus at leadership level is weak

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

If Bill has to make money over the next two years

and change the culture he will fail...Greg and

Nicholas will say the business has to make money.

For Head Office to ignore the need of advisers (and

ASIC’s requirements) for SO LONG without us

seeing positive change makes me wonder about the

bonus structures at head office and if change is a

genuine concern.

If I'm used to getting paid more

by generating revenue as

efficiently as I can and you want

me to do something to reduce

risk and there is no upside for

me and no downside if I don't do

it, except for making the state

manager unhappy, then I won’t

do it.

People seek to build up empires. If you are doing

this, the core influence is building your empire and

you might end up ignoring risk. This is driven by

promotion and profit share - people get promoted if

they grow their empires.

The personality of ExCo members

[varies]... there is a low level of

leadership training. Bully behaviours

[are used to] shut down others. There is

an inconsistent way of pulling up the

aggressive leaders... no-one will actually

say it’s wrong.

Maybe we could have pushed and

peddled harder [but] that’s the nature of

big organisations...

It's very closed doors, so critical

decisions won't always involve the right

people. I think the corridor

conversations need to stop. Why no

decisioning? Too many people. Eric had

more than 20 direct reports. He inherited

all these legacy reporting lines with

people who felt they were entitled to

report directly to the head of the

business.

Risk Culture Survey results, % distribution Risk Culture Survey results, % distribution

50% of the leaders wanted this

change to happen but didn't

have the tools/systems/

mechanisms or the conviction

to see this change through.

29 25 46

36 23 41

37 25 37

50 8 42

44 23 33

16

Confidential & Commercially Sensitive

MGL.0001.0003.0202

Inertia – Drivers B

Key drivers

Belief that initiating and succeeding with change is impossible in this business

Perception that scale of change is too difficult to overcome in this instance

Belief that leaders are disconnected from ‘reality’

Experience/perception that leaders don’t listen to feedback on need to change

Belief that leaders do not know the true state of the business (because depth and breadth of connection to the offices is hampered by size and distance)

View that leaders are not ‘strong enough’ to make change stick

Perception that past leaders quickly ‘gave up’ on their promises to introduce change

View that there is a disincentive for leaders to move away from the status quo

Perception that State Managers have far more influence with advisers than senior leaders

Perceived ‘inherent’ barriers

View that it is ‘impossible’ to shift brokers away from their inherent nature which is at odds with required changes

View that it is ‘economically impossible’ to have sufficient management required to drive/sustain change with current number of advisers (and size is necessary to achieve required profit)

View that required changes are impossible to make in the time frame available (e.g. due to extensive backlog that exists)

View that legislation requires behaviour that is impossible to balance with commercial goals of revenue generation activities

Organisational inadequacies

Belief our systems are inadequate to support required change

Belief our approach is ‘un-sophisticated’/inadequate to achieve genuine change (e.g. tick-a-box, admin focused, not adviser or client-centric)

Belief Macquarie doesn’t have enough capacity in the risk function to drive/sustain change (e.g. compared to other firms)

Perception that leaders have a general principle that if you are told once ‘there is no money’ don’t bother asking again

Perception that many risk staff have critical gaps in their experience and knowledge of risk, compliance and/or the business

Belief that ‘400 business models’ strategy is an unchangeable assumption, and a barrier that cannot be overcome

1

2

Branches over page See evidence under corresponding

number on following page n Theme

Inertia Learned helpless-

ness

Change impetus at leadership

level is weak

Low discretionary

effort

Lack of insight into

need for change

17

See ‘Risk Insight Clouded’ driver tree

Confidential & Commercially Sensitive

MGL.0001.0003.0203

19 45 35

13 88

Inertia – Evidence B

View that deep-seated barriers prevent leaders from initiating and

succeeding at change within this business

Perception that scale of current challenges (e.g., FoFA) are

almost too difficult to overcome

Onerous/complicated processes

are one of the main reasons why

people fail to comply

Too much credit or creed around here is

based on precedents... We can't do it now

because we didn't do it in 2006.

There is a lack of openness to

upward feedback - it just goes in

one ear and out the other.

When Bill and Greg [visited this

office] everything they said was

met with absolute scepticism.

“We’ve heard that before; we’ve

been told that before.”

MPW has the right skills and

expertise to manage the various risks

to which it is exposed

It’s very hard to teach brokers a planning

mindset... They don’t know what they

don’t know... You can’t teach 300 brokers

how to be advisers... You need to

fundamentally change the structure. But I

don’t think they will...

The real problem was there was

never going to be enough time to

make all these changes happen in

time. So people became disillusioned

because it seemed like the task was

impossible. It was both time and the

scale of change required.

My impression is that we aren’t in people’s

minds [in the state locations]. In Sydney

you have access to people like Peter

Maher, Bill and even people like Matt

Whitehead. You can’t get things fixed as

easily – you can’t just go downstairs...

There are too many grey areas. They'll

find something to breach you on. There's

always something, and with FoFA there

will be even more grey.

When all your time is taken up with SoAs,

reporting tools etc (which you shouldn’t be

doing) and you’ve got to talk to clients, and

you’ve got to prospect, then the result is that

you don’t dedicate enough time to it

[compliance activities]. But if we had the right

tools I’m 100% sure everyone would do it.

It’s not difficult to adhere to

Statement of Advice (SoA)

regulations

Significant disconnects

seem to exist, giving

advisers a sense their

feedback isn’t heard and

change will be difficult to

achieve

12 12 76 Advice

40 60

20 80 Adviser

Solutions

Risk Mgt

28 34 38

MPW

Australian

Advisers

2013

MPW

Canada

Advisers

2011

9 3 88

Confidence in

organisational risk

skill is extremely

low, for example,

compared to the

Canadian adviser

population

1 2

Learned helplessness prevents people from trying to initiate change

21 34 45

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Risk Culture Survey results, % distribution Risk Culture Survey results, % distribution

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

18

Confidential & Commercially Sensitive

MGL.0001.0003.0204

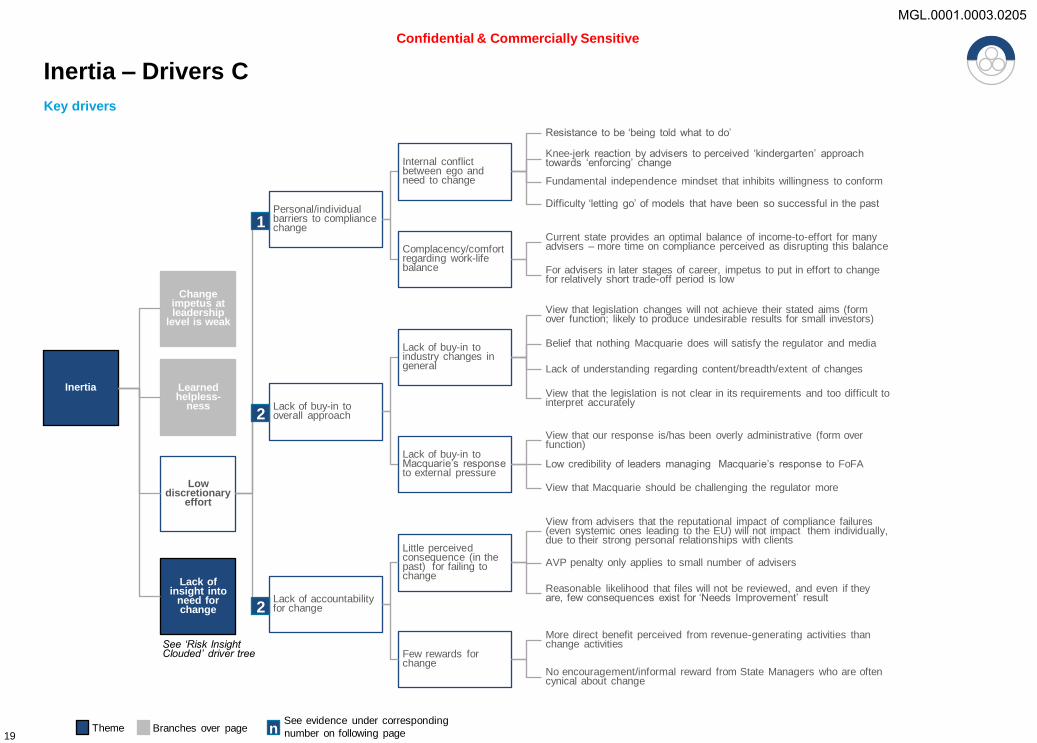

Inertia – Drivers C

Key drivers

Inertia Learned helpless-

ness

Change impetus at leadership

level is weak

Low discretionary

effort

Personal/individual barriers to compliance change

Lack of buy-in to overall approach

Complacency/comfort regarding work-life balance

Current state provides an optimal balance of income-to-effort for many advisers – more time on compliance perceived as disrupting this balance

For advisers in later stages of career, impetus to put in effort to change for relatively short trade-off period is low

Lack of insight into

need for change

Internal conflict between ego and need to change

Resistance to be ‘being told what to do’

Knee-jerk reaction by advisers to perceived ‘kindergarten’ approach towards ‘enforcing’ change

Difficulty ‘letting go’ of models that have been so successful in the past

Lack of buy-in to Macquarie’s response to external pressure

View that our response is/has been overly administrative (form over function)

View that Macquarie should be challenging the regulator more

Lack of buy-in to industry changes in general

View that legislation changes will not achieve their stated aims (form over function; likely to produce undesirable results for small investors)

Belief that nothing Macquarie does will satisfy the regulator and media

View that the legislation is not clear in its requirements and too difficult to interpret accurately

Lack of accountability for change

Little perceived consequence (in the past) for failing to change

Few rewards for change

View from advisers that the reputational impact of compliance failures (even systemic ones leading to the EU) will not impact them individually, due to their strong personal relationships with clients

More direct benefit perceived from revenue-generating activities than change activities

AVP penalty only applies to small number of advisers

No encouragement/informal reward from State Managers who are often cynical about change

Reasonable likelihood that files will not be reviewed, and even if they are, few consequences exist for ‘Needs Improvement’ result

Fundamental independence mindset that inhibits willingness to conform

Lack of understanding regarding content/breadth/extent of changes

Low credibility of leaders managing Macquarie’s response to FoFA

1

2

2

Branches over page See evidence under corresponding

number on following page n Theme 19

See ‘Risk Insight Clouded’ driver tree

Confidential & Commercially Sensitive

MGL.0001.0003.0205

29 39 33

11 22 67

13 16 71

27 73

28 23 49

39

Inertia – Evidence C

Many advisers resent the compliance activities expected of them

currently (let alone increasing the expectation)

Buy-in to the risk framework is weak and the business has not

created many compelling incentives to reinforce compliance

35

65

Advisers

audited

Advisers not

audited

% Advisers that had BRP file reviews conducted

1 April - 31 Dec 2012, Nationally

Advisers know the

likelihood of being

audited is less than 50-

50, lessening the impact

of the BRP in identifying

and penalising non-

compliant advisers

The time required to complete risk management activities

exceeds the value they add

Advisers

Risk Mgt

Bus. Strat. & Perf.

Advisers

The risk policies, processes and procedures utilised by

MPW help us manage various types of risk more effectively

Adviser Solutions

Advisers are

not bought-in

to the value of

compliance

activities

1 2

Low discretionary effort expended on changing the status quo

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

My view is that the current

"issues" are every bit

about a lack of investment

in information technology

than poorly drafted

legislation

Coming to Macquarie was

an out and out shock.

Systems were shocking,

compliance was by

comparison draconian. To

treat grown men and

women as school children

is just….

[What are the

consequences?] There

wasn't any until recently. I

hadn't been audited since

my first year - I asked to

be audited..

The amount of time and effort we have

to put into risk these days is many times

that of years ago. We are still expected

to reach financial targets with a much

higher risk burden... Remuneration is

98% skewed to revenue performance

and 2% risk - that sums it up!

As people get older, change gets harder

– I see it in myself. Especially when you

have a successful model that has

worked for so long and worked well for

so long.

I hate being told what to do. I’m getting

older now and sometimes I think

“seriously mate, you’re 30 years old and

you’re telling me what to do?”

What does it take to be successful?

Independence. You need to be

independent and focus on what you’re

here to do – make money for your

clients. So clients and independence

comes first, and what is best for

Macquarie comes second.

The Head Office risk structure is...

ineffective and does not seek to improve

the system. They are the ‘police’ and

issue ‘fines’ rather than making the

systems workable... The truth is

advisers do NOT have the most basic

tools we need in order to be compliant.

Risk Culture Survey results, % distribution Risk Culture Survey results, % distribution

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

20

Confidential & Commercially Sensitive

MGL.0001.0003.0206

Theme 2: Risk insight clouded

MGL.0001.0003.0207

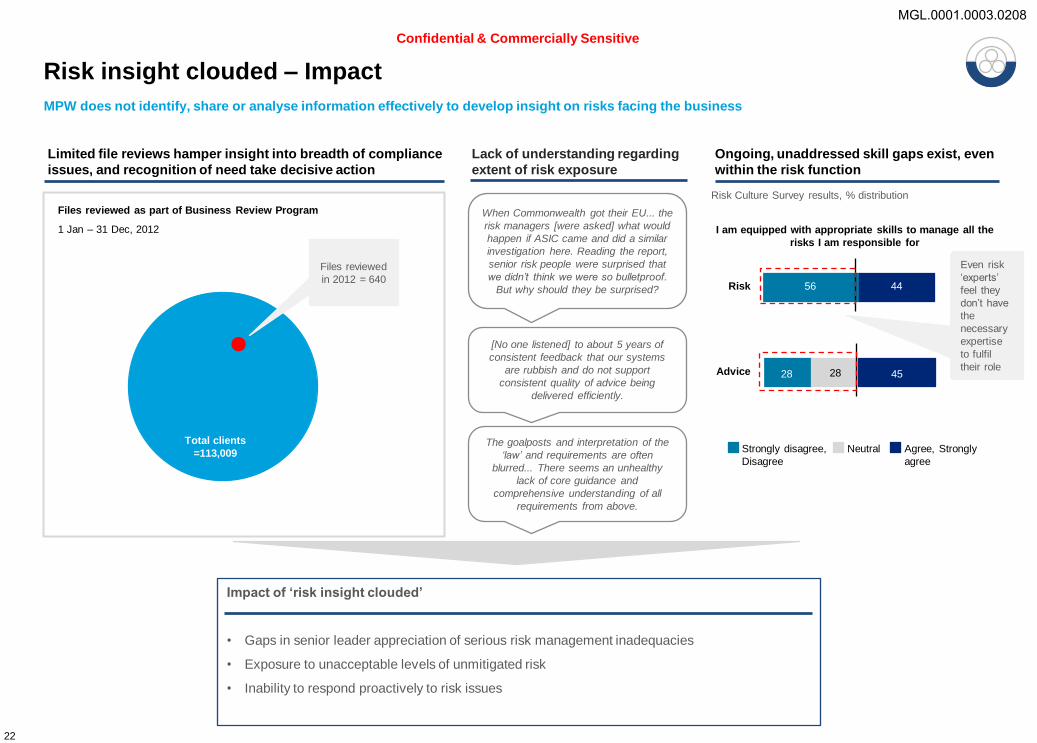

Risk insight clouded – Impact

Limited file reviews hamper insight into breadth of compliance

issues, and recognition of need take decisive action

Lack of understanding regarding

extent of risk exposure

Ongoing, unaddressed skill gaps exist, even

within the risk function

Impact of ‘risk insight clouded’

• Gaps in senior leader appreciation of serious risk management inadequacies

• Exposure to unacceptable levels of unmitigated risk

• Inability to respond proactively to risk issues

28 45 28

56 44 Risk

Advice

I am equipped with appropriate skills to manage all the

risks I am responsible for

Files reviewed as part of Business Review Program

1 Jan – 31 Dec, 2012

Even risk

‘experts’

feel they

don’t have

the

necessary

expertise

to fulfil

their role

MPW does not identify, share or analyse information effectively to develop insight on risks facing the business

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

When Commonwealth got their EU... the

risk managers [were asked] what would

happen if ASIC came and did a similar

investigation here. Reading the report,

senior risk people were surprised that

we didn’t think we were so bulletproof.

But why should they be surprised?

[No one listened] to about 5 years of

consistent feedback that our systems

are rubbish and do not support

consistent quality of advice being

delivered efficiently.

The goalposts and interpretation of the

‘law’ and requirements are often

blurred... There seems an unhealthy

lack of core guidance and

comprehensive understanding of all

requirements from above.

Risk Culture Survey results, % distribution

Files reviewed

in 2012 = 640

Total clients

=113,009

22

Confidential & Commercially Sensitive

MGL.0001.0003.0208

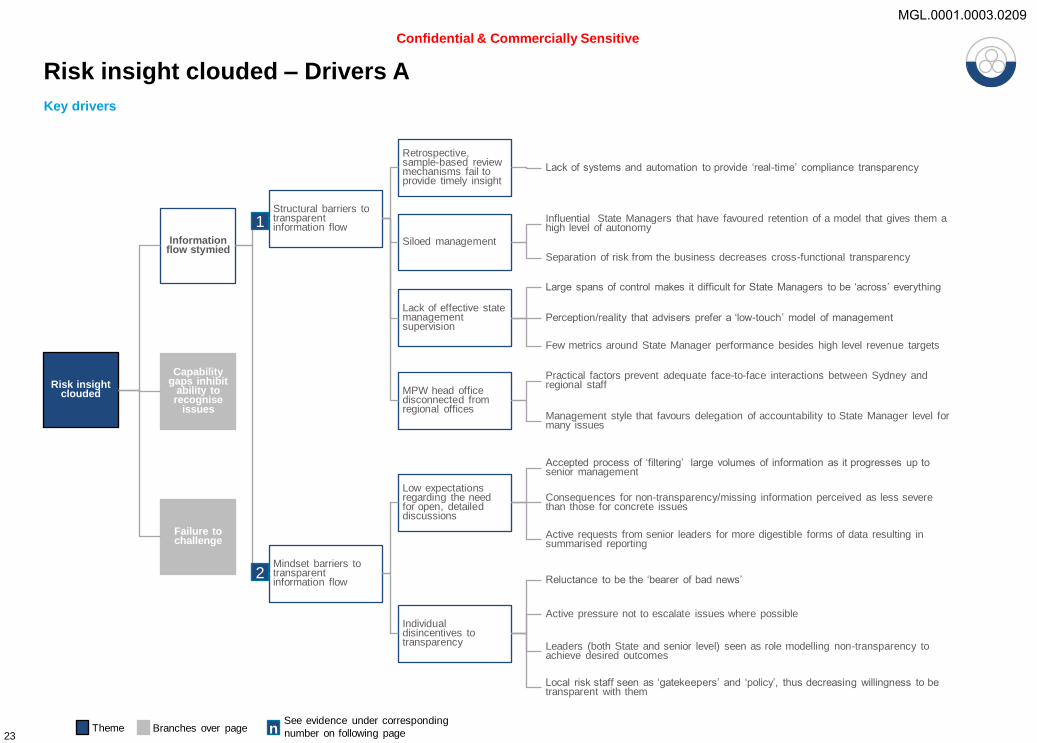

Risk insight clouded – Drivers A

Risk insight clouded

Capability gaps inhibit

ability to recognise

issues

Information flow stymied

Failure to challenge

Structural barriers to transparent information flow

Mindset barriers to transparent information flow

Siloed management

Lack of effective state management supervision

Influential State Managers that have favoured retention of a model that gives them a high level of autonomy

Separation of risk from the business decreases cross-functional transparency

MPW head office disconnected from regional offices

Low expectations regarding the need for open, detailed discussions

Large spans of control makes it difficult for State Managers to be ‘across’ everything

Perception/reality that advisers prefer a ‘low-touch’ model of management

Practical factors prevent adequate face-to-face interactions between Sydney and regional staff

Management style that favours delegation of accountability to State Manager level for many issues

Individual disincentives to transparency

Accepted process of ‘filtering’ large volumes of information as it progresses up to senior management

Consequences for non-transparency/missing information perceived as less severe than those for concrete issues

Active requests from senior leaders for more digestible forms of data resulting in summarised reporting

Reluctance to be the ‘bearer of bad news’

Active pressure not to escalate issues where possible

Leaders (both State and senior level) seen as role modelling non-transparency to achieve desired outcomes

Few metrics around State Manager performance besides high level revenue targets

Local risk staff seen as ‘gatekeepers’ and ‘policy’, thus decreasing willingness to be transparent with them

1

2

Key drivers

Branches over page See evidence under corresponding

number on following page n Theme

Retrospective, sample-based review mechanisms fail to provide timely insight

Lack of systems and automation to provide ‘real-time’ compliance transparency

23

Confidential & Commercially Sensitive

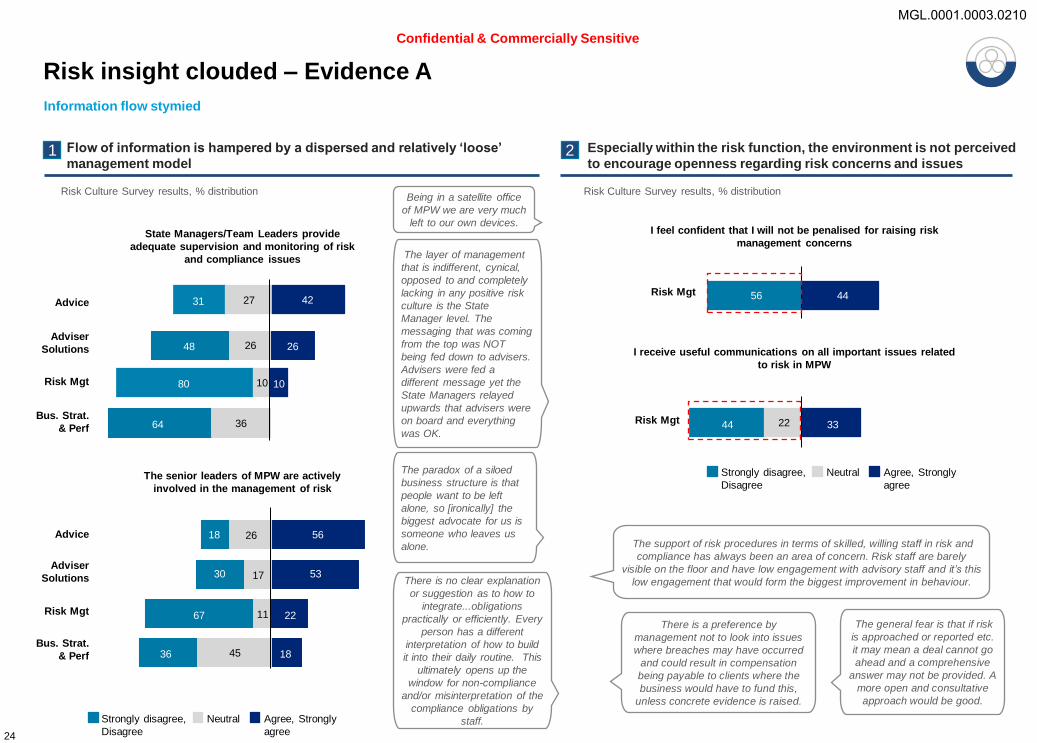

MGL.0001.0003.0209

27

26

26

17

11

45

10 10 80

56 44

22 44 33

Risk insight clouded – Evidence A

Especially within the risk function, the environment is not perceived

to encourage openness regarding risk concerns and issues

Flow of information is hampered by a dispersed and relatively ‘loose’

management model

I feel confident that I will not be penalised for raising risk

management concerns

I receive useful communications on all important issues related

to risk in MPW

Risk Mgt

Risk Mgt

1 2

Information flow stymied

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

There is a preference by

management not to look into issues

where breaches may have occurred

and could result in compensation

being payable to clients where the

business would have to fund this,

unless concrete evidence is raised.

The support of risk procedures in terms of skilled, willing staff in risk and

compliance has always been an area of concern. Risk staff are barely

visible on the floor and have low engagement with advisory staff and it’s this

low engagement that would form the biggest improvement in behaviour.

The general fear is that if risk

is approached or reported etc.

it may mean a deal cannot go

ahead and a comprehensive

answer may not be provided. A

more open and consultative

approach would be good.

Risk Culture Survey results, % distribution

48 26

36 64

State Managers/Team Leaders provide

adequate supervision and monitoring of risk

and compliance issues

The senior leaders of MPW are actively

involved in the management of risk

Adviser

Solutions

Risk Mgt

Bus. Strat.

& Perf

56 18

53 30

67 22

36 18

Advice

Risk Culture Survey results, % distribution

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Adviser

Solutions

Risk Mgt

Bus. Strat.

& Perf

Advice

There is no clear explanation

or suggestion as to how to

integrate...obligations

practically or efficiently. Every

person has a different

interpretation of how to build

it into their daily routine. This

ultimately opens up the

window for non-compliance

and/or misinterpretation of the

compliance obligations by

staff.

The paradox of a siloed

business structure is that

people want to be left

alone, so [ironically] the

biggest advocate for us is

someone who leaves us

alone.

Being in a satellite office

of MPW we are very much

left to our own devices.

The layer of management

that is indifferent, cynical,

opposed to and completely

lacking in any positive risk

culture is the State

Manager level. The

messaging that was coming

from the top was NOT

being fed down to advisers.

Advisers were fed a

different message yet the

State Managers relayed

upwards that advisers were

on board and everything

was OK.

31 42

24

Confidential & Commercially Sensitive

MGL.0001.0003.0210

Risk insight clouded – Drivers B

Risk insight clouded

Capability gaps inhibit

ability to recognise

issues

Information flow stymied

Failure to challenge

Significant risk capability gaps in adviser population

Many incumbents in risk roles lack extensive risk

experience

Professional backgrounds of many advisers lack risk depth

Opportunity to improve effectiveness of professional development

Large broker population requires minimal risk knowledge to attain certification (e.g. compared to planners)

Even brokers with relatively lengthy experience have not been required to develop strong compliance skills

Structural barriers to demonstrating deep risk insight as an adviser

State Managers not in a position to identify risk gaps

Industry-wide tendency to achieve required number of training hours as a priority – genuine learning is a secondary aim

Use of channels and techniques (possibly due to capacity constraints) that don’t engage advisers – lack of tailored coaching, in-person, ‘war-stories’ etc

Complex nature of incoming legislation difficult for even risk professionals to interpret, let alone advisers

Tendency for advisers to specialise in certain strategies/products means breadth of risk knowledge is limited

Risk expertise and knowledge not leveraged to develop management insight into risk topics

State Managers often delegate majority of risk issues to Risk Managers and therefore do not develop expertise themselves

Breadth of models being managed within offices makes it very difficult to demonstrate risk insight across range of strategies/products

Capacity and system constraints inhibit proactive analysis by risk function to aid management in understanding risk ‘profile’ of their office

Little attempt to provide external insight around best practice to up-skill management on ‘what good looks like’

Some advisers don’t see the individual value proposition for developing their risk expertise – e.g. at later stages of their careers, or work-life goals

Management lacks in-depth risk expertise

Many State Managers from a broking background may not have deep risk skill in general, particularly for planning-oriented risks

See Ineffective Risk Function tree

Focus of adviser capabilities (qualification) is around minimum standards

Treatment of risk management effectiveness in performance management for advisers is very inconsistent and not embedded

Lack of leadership development for State Managers

Key drivers

Branches over page See evidence under corresponding

number on following page n Theme

1

2

25

Confidential & Commercially Sensitive

MGL.0001.0003.0211

25 20 56

29 52 19 27 48 25

27 35 39

Risk insight clouded – Evidence B

I regularly receive feedback on my ability to

manage risk effectively

My risk management capabilities are assessed

regularly

Advice

Advice

Our risk management professionals take a lead

role in guiding key risk decisions

Risk management professionals provide critical

input to the strategy/product development

process in MPW

Management lacks individual risk expertise, and also fails to

leverage the risk function to bolster their ability to manage risk

Many advisers are ‘unconsciously unskilled’ in risk, especially those

from a broking background 1 2

Capability gaps inhibit ability to recognise issues

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

It’s very hard to teach brokers a

planning mindset. They’re just about

‘give me 10k and I’ll invest it for you’.

They don’t know what they don’t know.

The heritage of the business is stockbroking,

but financial services reforms in recent years

have increasingly brought brokers’ obligations

in line with financial planners/advisers.

Brokers still largely believe this stuff does not

apply to them...when in fact the law requires

everybody to be advisers when advising retail

clients.

Advisers put the onus on their assistants to

make them compliant - but assistants don't

know anything about the regulations. I

wouldn't know what a compliant SoA looks

like. I feel wealth managers are

much more in touch with their

legal and fiduciary obligations

under the AFSL requirements

whereas the brokers tend to

be either unaware, untrained,

or not interested in meeting

compliance requirements.

Over the past few years, there has been a big push from

MPW management for advisers to ‘diversify’ their service

offering and become accredited to provide advice in other

areas outside traditional stockbroking services...This has

resulted in advisers providing advice in areas in which they

have little skill or experience and poor record keeping and

documentation of the advice processes.

When [a member of management] gave a

heads up that management were really

unhappy about the EU, he said the things

you need to be doing are watching how you

carry yourself, dress around town... [and yet]

we have no directions on what to do for

FoFA!

The risk manager isn’t involved in

recruiting at all. HR was completing the

checks on these people after they’d

already begun working for us. And now

we are still dealing with some of these

people.

Since merger of broking/planning majority of

management are brokers with little

understanding of the planning business. I

have no confidence speaking with

management.

Most State Managers are either

stockbrokers or former stockbrokers

and given where MPW currently finds

itself, I now question if these former

stockbrokers have the skill set going

forward in managing risk which has

become a much more complicated

process.

Without regular

feedback many

advisers don’t know

they have gaps in

their compliance

behaviour/skill

Risk Culture Survey results, % distribution Risk Culture Survey results, % distribution

The Risk function

may be under-

leveraged in providing

input

Advice

Advice

26

Confidential & Commercially Sensitive

MGL.0001.0003.0212

Risk insight clouded – Drivers C

Risk insight clouded

Capability gaps inhibit

ability to recognise

issues

Information flow stymied

Failure to challenge

Arguments to increase risk management effectiveness lack organisational support

Risk message often holds little weight

Perception that risk management improvement ideas will be too expensive

Those with a risk ‘agenda’ often dismissed as ‘non-commercial’

Risk activities seen as not contributing to the bottom line, and thus less important

Widely held view that Macquarie compares favourably to peers

Individuals avoid raising concerns openly

View that ‘best practice’ approaches are too expensive to implement with Macquarie’s model (e.g. enough ARAs to review all SoAs)

Perception that gap between Macquarie and other firms with ‘leading’ approaches is too large to address economically

Vocal opinions that Macquarie compares favourably to peers sway general opinion

Difficulty accessing reliable benchmarking data regarding practices at other firms

Response to raising issues not constructive

Inappropriate pressure from those in positions of influence on subordinates not to raise issues

Individualised nature of adviser culture decreases sense of personal responsibility and confidence for raising concerns regarding other advisers

‘Good news culture’ means concerns are often met with consternation, not welcome

Tendency to delegate problem solving to issue raiser dis-incentivises raising of issues

Previous attempts to request funding have been denied leading to generalised expectation that future requests will also be denied

Ineffective escalation of concerns

Challenge in open forums not seen as culturally appropriate

Fear that asking for help will result in penalty rather than help

Perception that challenges regarding favoured advisers may be simply ignored and/or penalised informally

Instances of public belittling and other consequences for raising issues

Perception that bulk of compliance activities are, practically speaking, optional

Influence of leadership and management messaging in adviser perceptions (e.g. “The EU is mostly about systems”)

1

2

Key drivers

Branches over page See evidence under corresponding

number on following page n Theme 27

Confidential & Commercially Sensitive

MGL.0001.0003.0213

26 40 34

Risk insight clouded – Evidence C

I found MPW's risk framework far more

comprehensive then competitors - and

this was before the EU. I was surprised

MQG got targeted for this.

60% of people

interviewed

selected “Easily

yielding to

inappropriate

pressure from

others” as ‘more

like’ MPW

People in MPW are expected to do what they are

told, no matter what

People in MPW challenge others constructively if

they think that they are not doing the right thing

[There has been a] lack of investment by

the Business into staffing resources and

integrated surveillance systems.

The only real problem MPW has in terms

of risk management [is] IT systems.

Many

advisers

and

managers

are ‘blind’

to any

problems in

the risk

function

(besides IT

systems)... I believe the risk mindsets are on the

whole good at Macquarie...when

compared to other firms I have worked

at... The issue for me is the systems.

Systems are rubbish... lack of investment

is biggest ongoing obstacle to advisers

being able to meet all performance goals

set by management, including both

revenue and risk management.

..which

reduces

the

impetus to

invest in

the risk

function in

general

Discussion of risk issues is stymied in a culture that does not manage challenge

productively, on all fronts (advisers, management and risk) 1 Concerns regarding under-investment in the risk

function have been met with resistance 2

Failure to challenge

We have [risk] resources now with

[name], but you should ask [name] why

they left. They felt management didn’t

believe there was any value in their role. I

thought they were a real asset to the

group...The State Manager said it straight

to them, “I don’t believe in the value of

your role.”

25 40 35

Desirable Developing Detrimental

29 36 35

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Raising issues of compliance some years

ago in relation to our handling of IPOs

with State Manager just got me labelled

as a whinger. And told that this is they

way we are doing it.

Ever since the GFC, MPW has been

doing everything to indiscriminately chase

the dollar. When staff have raised risk

concerns, management have ignored

them and when the risk team has tried to

ensure the business meets the

regulations they have been treated with

derision.

All risk management decisions are made,

managed and reported [in line with

management maintaining the status quo].

Anyone who holds management to

account is bullied and/or de-resourced.

If you do not get along with your risk

manager you tend to be crucified for any

mistakes and held up as their example

that they are doing their job.

There have been a number of incidents

raised in past times where the Business

has challenged Risk and adviser penalties

have not been imposed or enforced

because of ‘associations’ with Business

Leaders.

Risk Culture Survey results, % distribution

% of behaviours selected as representative of

MPW across all interviews

Behaviours relating to “Challenge”

Risk behaviour interview analysis

28

Confidential & Commercially Sensitive

MGL.0001.0003.0214

Theme 3: Freedom without boundaries

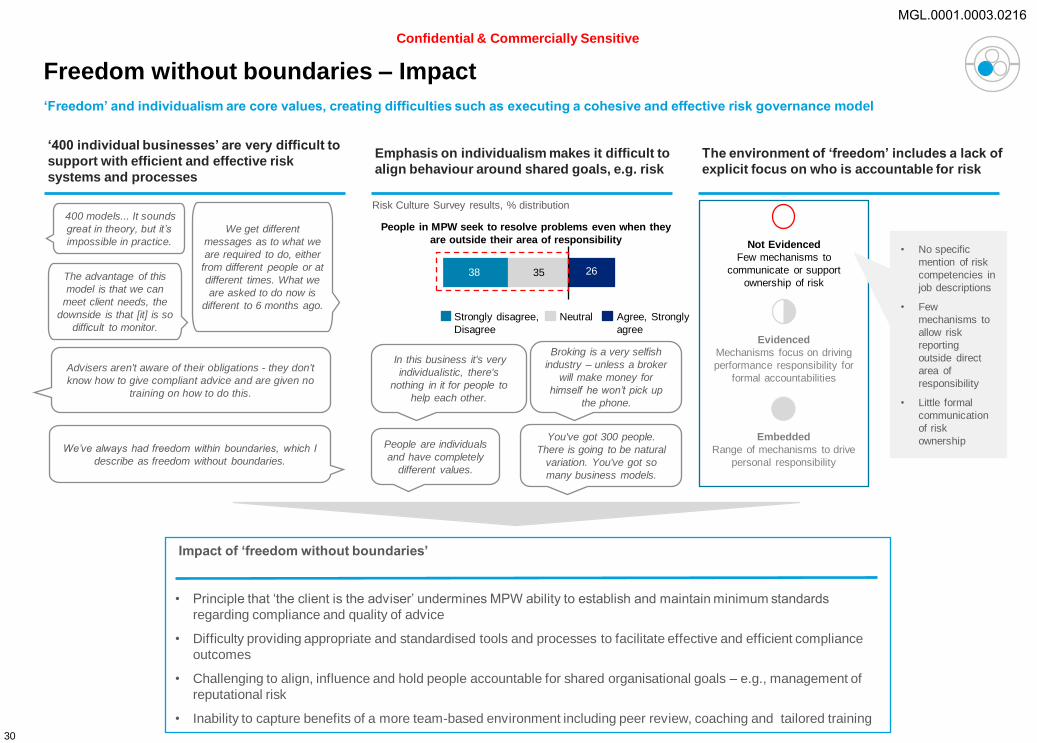

MGL.0001.0003.0215

35 38 26

Freedom without boundaries – Impact

‘Freedom’ and individualism are core values, creating difficulties such as executing a cohesive and effective risk governance model

‘400 individual businesses’ are very difficult to

support with efficient and effective risk

systems and processes

Emphasis on individualism makes it difficult to

align behaviour around shared goals, e.g. risk

The environment of ‘freedom’ includes a lack of

explicit focus on who is accountable for risk

400 models... It sounds

great in theory, but it’s

impossible in practice.

We get different

messages as to what we

are required to do, either

from different people or at

different times. What we

are asked to do now is

different to 6 months ago.

We’ve always had freedom within boundaries, which I

describe as freedom without boundaries.

Advisers aren't aware of their obligations - they don't

know how to give compliant advice and are given no

training on how to do this.

People in MPW seek to resolve problems even when they

are outside their area of responsibility

Embedded

Range of mechanisms to drive

personal responsibility

Evidenced

Mechanisms focus on driving

performance responsibility for

formal accountabilities

Not Evidenced

Few mechanisms to

communicate or support

ownership of risk

Impact of ‘freedom without boundaries’

• Principle that ‘the client is the adviser’ undermines MPW ability to establish and maintain minimum standards

regarding compliance and quality of advice

• Difficulty providing appropriate and standardised tools and processes to facilitate effective and efficient compliance

outcomes

• Challenging to align, influence and hold people accountable for shared organisational goals – e.g., management of

reputational risk

• Inability to capture benefits of a more team-based environment including peer review, coaching and tailored training

In this business it's very

individualistic, there's

nothing in it for people to

help each other.

Broking is a very selfish

industry – unless a broker

will make money for

himself he won’t pick up

the phone.

People are individuals

and have completely

different values.

The advantage of this

model is that we can

meet client needs, the

downside is that [it] is so

difficult to monitor.

You've got 300 people.

There is going to be natural

variation. You've got so

many business models.

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Risk Culture Survey results, % distribution

• No specific

mention of risk

competencies in

job descriptions

• Few

mechanisms to

allow risk

reporting

outside direct

area of

responsibility

• Little formal

communication

of risk

ownership

30

Confidential & Commercially Sensitive

MGL.0001.0003.0216

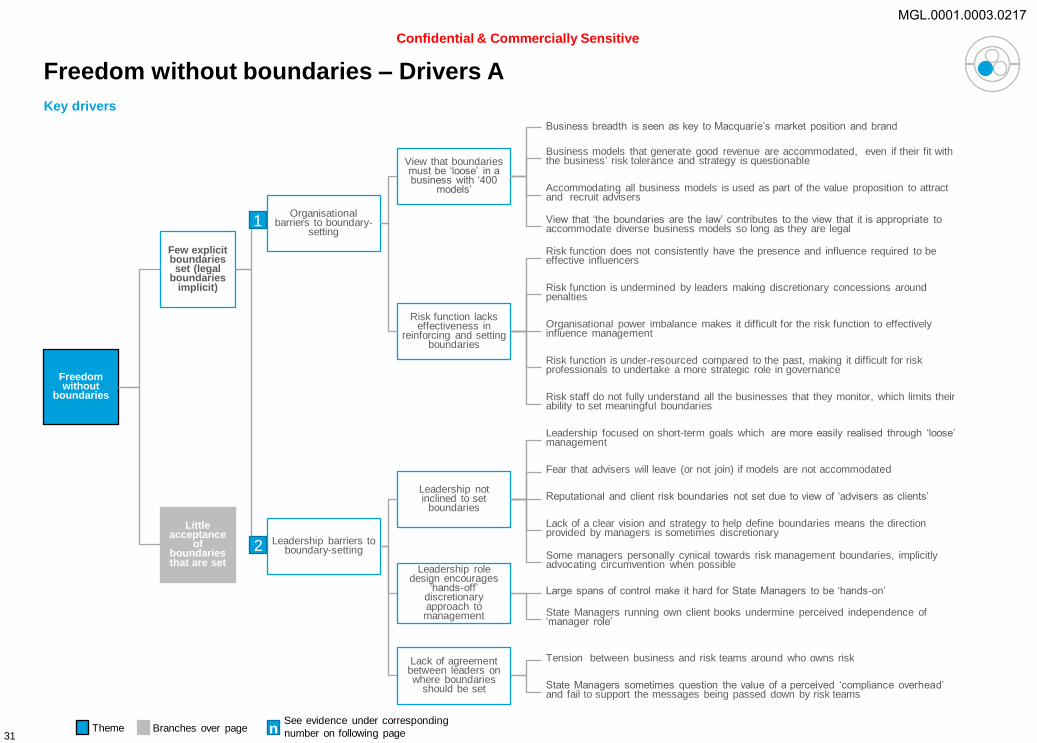

Freedom without boundaries – Drivers A

Freedom without

boundaries

Organisational barriers to boundary-

setting

Leadership barriers to boundary-setting

Leadership role design encourages

‘hands-off’ discretionary approach to management

Large spans of control make it hard for State Managers to be ‘hands-on’

Few explicit boundaries set (legal

boundaries implicit)

Little acceptance

of boundaries that are set

Risk function lacks effectiveness in

reinforcing and setting boundaries

Organisational power imbalance makes it difficult for the risk function to effectively influence management

Risk function is under-resourced compared to the past, making it difficult for risk professionals to undertake a more strategic role in governance

Risk function is undermined by leaders making discretionary concessions around penalties

Lack of agreement between leaders on where boundaries

should be set

State Managers running own client books undermine perceived independence of ‘manager role’

Tension between business and risk teams around who owns risk

State Managers sometimes question the value of a perceived ‘compliance overhead’ and fail to support the messages being passed down by risk teams

View that boundaries must be ‘loose’ in a business with ‘400

models’

Business breadth is seen as key to Macquarie’s market position and brand

Business models that generate good revenue are accommodated, even if their fit with the business’ risk tolerance and strategy is questionable

Accommodating all business models is used as part of the value proposition to attract and recruit advisers

View that ‘the boundaries are the law’ contributes to the view that it is appropriate to accommodate diverse business models so long as they are legal

Leadership not inclined to set

boundaries

Fear that advisers will leave (or not join) if models are not accommodated

Leadership focused on short-term goals which are more easily realised through ‘loose’ management

Lack of a clear vision and strategy to help define boundaries means the direction provided by managers is sometimes discretionary

Some managers personally cynical towards risk management boundaries, implicitly advocating circumvention when possible

Risk staff do not fully understand all the businesses that they monitor, which limits their ability to set meaningful boundaries

Risk function does not consistently have the presence and influence required to be effective influencers

Reputational and client risk boundaries not set due to view of ‘advisers as clients’

1

2

Key drivers

Branches over page See evidence under corresponding

number on following page n Theme 31

Confidential & Commercially Sensitive

MGL.0001.0003.0217

21 52 26

Boundaries are undermined because they are difficult to set in a

multi-model environment, and Risk is a toothless tiger in

reinforcing them

% of behaviours selected as representative of

MPW across all interviews

Behaviours relating to “Communications”

Freedom without boundaries – Evidence A

…no one in leadership

can tell you what model

we should be in 5 years.

Accountability is lacking at

leadership levels. For

leadership it’s easier that

way.

Culture starts at the top

and leadership is very

short sighted about the

messages they send out.

Embedded

Range of organisational

mechanisms to facilitate visible

involvement and role modelling

of senior leaders in risk issues

Evidenced

Senior leaders

required to participate

in some risk issues

Not Evidenced

Little systematic involvement

of senior leaders in risk-related

activities and/or

communications

22 33 45

Senior Leadership Organisation Mechanisms

Leaders are not focused on boundary setting for a range of

reasons 1 2

Although there are some risk KPIs, and risk features as a standing item in selected

leadership forums (e.g. Advice EMC), many formal mechanisms are missing, e.g.:

• Job descriptions explicitly calling out risk accountabilities

• Formalised two-way cascading communication opportunities

• Visible senior leadership involvement in risk activities is missing

Few explicit boundaries set (legal boundaries implicit)

38% of people selected

“Misaligned messages

communicated by

leaders at different

levels of the

organisation” as ‘more

like’ MPW

Commerciality and flexibility to

accommodate a number of different

business and adviser models. This is

both a strength and a weakness.

I think we go out to hire 'big

writers' regardless of their history.

If they write good revenue, we let

them in on our licence.

It's always been our selling point…if

you have a business model we can

accommodate it.

When advisers come to

Macquarie the message is we will

modify to fit their business model

- not "here is the Macquarie

business model“. 400 models...”the clarity is the law”.

The boundaries people are expected

to operate under is the letter of the

law.

State Managers/Team Leaders in MPW tend to

be cynical about risk policies, processes and

procedures

26% of people believe their

State Manager is cynical

about risk policies,

procedures and processes,

which may undermine the

risk function’s effectiveness

Desirable Developing Detrimental

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Risk behaviour interview analysis

400 advisers with 400 different

models – do they [RMG] really

understand the risk they’re taking

on at an aggregated level?

How can you run 400 businesses and

manage them? How can you even

audit it when there are 400 different

ways of obtaining information?

Risk Culture Survey results, % distribution

32

Confidential & Commercially Sensitive

MGL.0001.0003.0218

Freedom without

boundaries

Lack of personal ownership regarding

compliance obligations

Low affinity with Macquarie

Tension in the Adviser Value

Proposition

Some advisers do not feel they receive sufficient support for the proportion of revenue they share with Macquarie

Feeling that Macquarie takes all the upside and none of the downside with regards to risk and revenue generated

Few explicit boundaries set (legal

boundaries implicit)

Little acceptance

of boundaries that are set

View of risk and compliance as a task

rather than an outcome

Acceptance of advisers using their assistants and other junior resources to complete compliance activities, rather than take personal responsibility

Adviser culture of individualism and

entitlement

Precedent of exceptions in consequence management

Advisers highly value independence, with Macquarie regarded as a ‘third party’

Adviser belief that ‘my model is different to everyone else’s,’ providing an excuse to play by their own rules

Preferential treatment of advisers to retain loyalty, especially for large writers

Many individual cultures

Past recruitment focused on ‘bums on seats’ rather than cultural alignment

Legacy of acquisitions with few attempts to instil MPW culture

Geographic spread and size of business creates sub-cultures where primary affinity is to the local office

Little support for collaboration

Incentive model discourages partnering, referrals and teamwork

No formalised coaching or mentoring arrangements to facilitate collaboration and knowledge sharing

Reluctance to partner due to different levels of capabilities amongst advisers and close guarding of client relationships

Lack of understanding

regarding obligations

Knowledge and skill gaps around risk obligations specific to the retail advice industry

View that breaches may be ‘negotiated’ undermines clear accountability

History of ‘popular’ risk professionals assisting with compliance completion, rather than pushing responsibility back to advisers

Risk function focus on efficiency of compliance activities rather than monitoring around compliance quality has reinforced a ‘tick-a-box’ mindset

Legislation is very ‘grey’ on expectations making it difficult for advisers to understand what they will be held accountable for

Poor reinforcement of desirable risk

behaviour Perceptions of ineffective

consequence management

Inconsistent application of breach policy

BRP interrogates a small proportion of files and focuses on discovered issues, with no systematic review of other files for the same adviser or for recurring issues

Lack of standard recruitment and induction process to establish and reinforce minimum standards and expectations

1

2

1

Freedom without boundaries – Drivers B

Key drivers

Branches over page See evidence under corresponding

number on following page n Theme 33

Confidential & Commercially Sensitive

MGL.0001.0003.0219

24 22 54

Freedom without boundaries – Evidence B

My ability to operate relatively independently as an

‘entrepreneur’ under Macquarie’s brand is critical to my

job satisfaction

Risk management activities tend to limit, rather than

promote, business growth

Behaviours relating to “Personal

Responsibility”

13 51 36

The understanding and individual ‘value proposition’ required to

foster personal responsibility for risk and compliance is weak

A shared culture of independence means advisers do not feel

obliged to ‘play by Macquarie’s rules’ 1 2

15 11 74

27 29 44

25 47 28

Little acceptance of boundaries that are set

It doesn’t matter if you’re

known for breaching, all

that matters is your

revenue. The higher

revenue writers are

protected.

If there is no incentive to drive positive behaviours, it is

just the same as giving incentives for bad behaviour -

you won’t correct it by threatening people.

Behaviours relating to

“Incentives and Consequences”

29 36 35

Advice

Other

Advice

Other

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree

Desirable Developing Detrimental

74% of advisers see

operating as an

entrepreneur as critical to

their job satisfaction,

compared to 44% for

other functions

54% of advisers see risk

management as limiting

business growth,

compared to 28% for

other functions

% of behaviours selected as representative of

MPW across all interviews

Risk behaviour interview analysis

Compliance risk is

pushed to advisers by

Macquarie - then the

adviser pushes it to

their assistant.

A lot of advisers don’t

think that they own

risk; they don’t think

about owning risk.

Everyone likes the big pay

cheques, the big expense

accounts, the big titles.

But when it comes down

to it they've all got

responsibility, but they've

shirked them all. There is a lack of

accountability…when things

go wrong it is [seen as] the

fault of Compliance

because Compliance didn’t

pick it up.

Macquarie offers a franchise

to advisers. But that doesn’t

come with any brand

management. The clients are

seen as owned by the

advisers, not owned by the

advisers and Macquarie.

Macquarie is often described

as a third-party: “they haven't

done this", "their systems

don't work"... rather than

work together because they

have the client relationship

and bring in the money.

Risk Culture Survey results, % distribution

33% of people interviewed selected

“Ignoring risk issues outside own

area of responsibility” as ‘more like’

MPW

• 48% of people interviewed

selected “Lack of consistent

consequences for behaviour that

is clearly misaligned with risk

principles” as ‘more like’ MPW

• 31% selected “Excessive risk

taking rewarded”

34

There tends to be a ‘hands-

off’ approach. People don’t

want to touch things

because there’s a culture of

“if you touch it you own it”

Confidential & Commercially Sensitive

MGL.0001.0003.0220

Theme 4: Short-term focus

MGL.0001.0003.0221

22 30 48

23 34 44

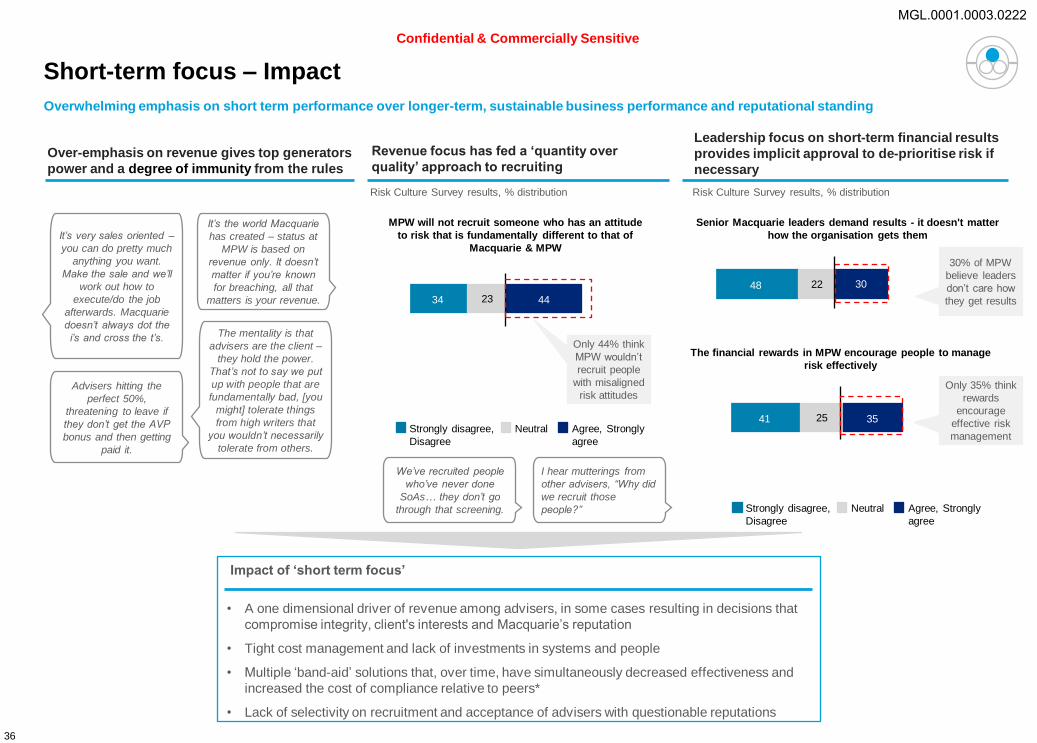

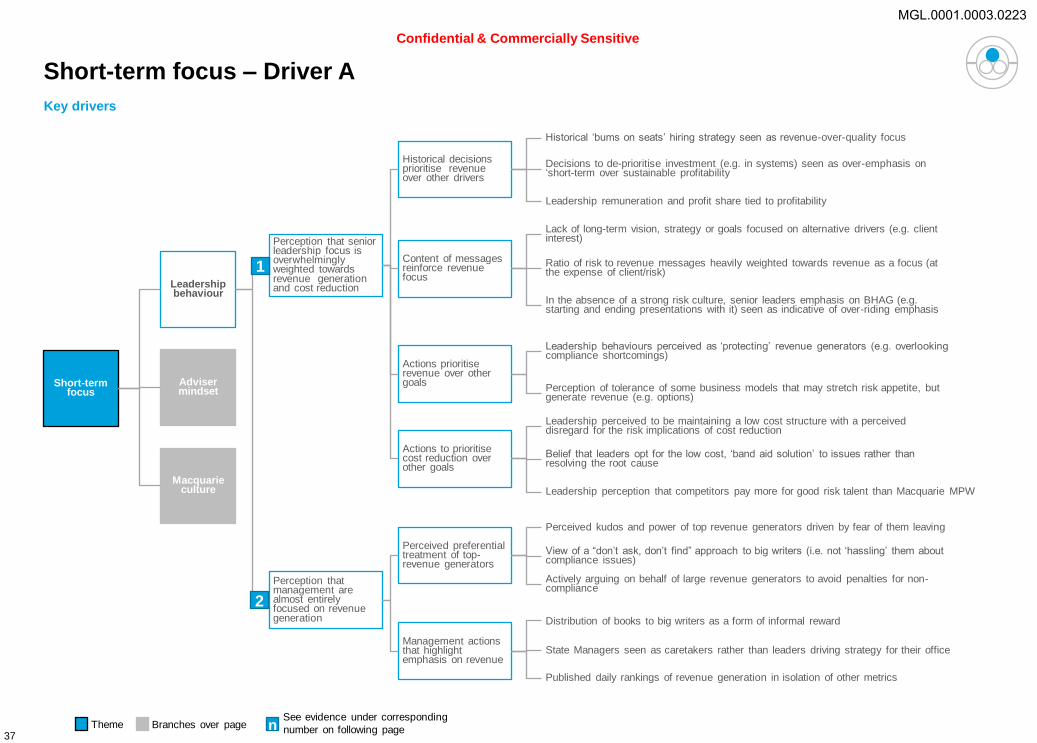

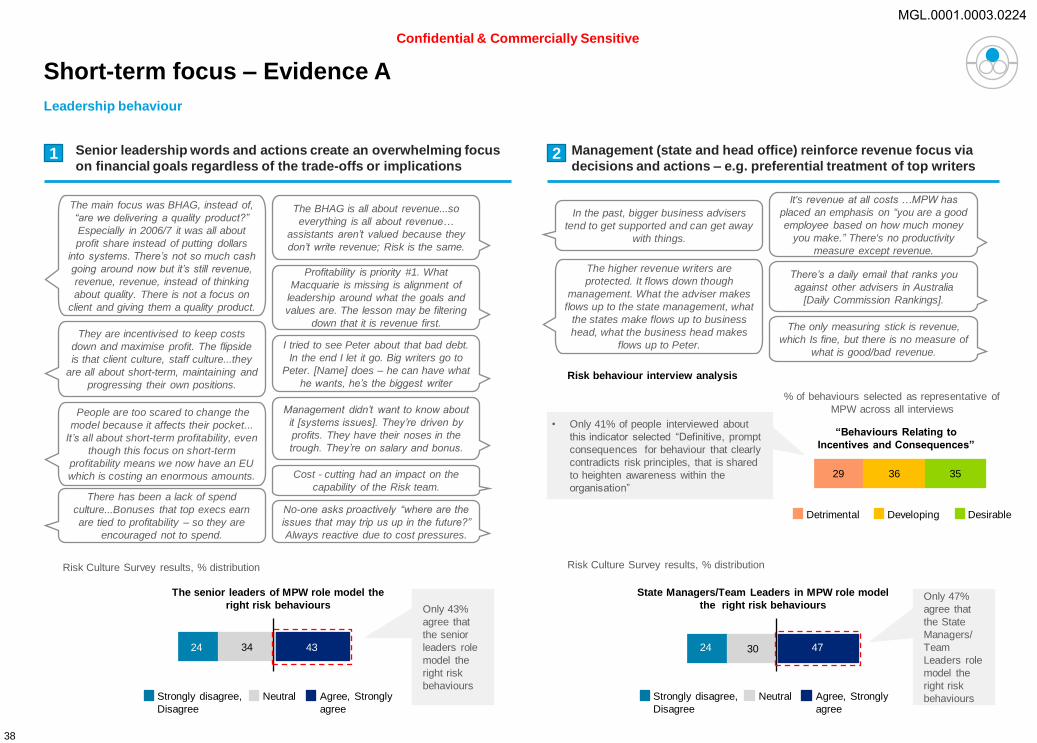

Short-term focus – Impact

Revenue focus has fed a ‘quantity over

quality’ approach to recruiting

Leadership focus on short-term financial results

provides implicit approval to de-prioritise risk if

necessary

Impact of ‘short term focus’

• A one dimensional driver of revenue among advisers, in some cases resulting in decisions that

compromise integrity, client's interests and Macquarie’s reputation

• Tight cost management and lack of investments in systems and people

• Multiple ‘band-aid’ solutions that, over time, have simultaneously decreased effectiveness and

increased the cost of compliance relative to peers*

• Lack of selectivity on recruitment and acceptance of advisers with questionable reputations

25 35 41

Senior Macquarie leaders demand results - it doesn't matter

how the organisation gets them

The financial rewards in MPW encourage people to manage

risk effectively

MPW will not recruit someone who has an attitude

to risk that is fundamentally different to that of

Macquarie & MPW

Overwhelming emphasis on short term performance over longer-term, sustainable business performance and reputational standing

Over-emphasis on revenue gives top generators

power and a degree of immunity from the rules

It’s very sales oriented –

you can do pretty much

anything you want.

Make the sale and we’ll

work out how to

execute/do the job

afterwards. Macquarie

doesn’t always dot the

i’s and cross the t’s.

It’s the world Macquarie

has created – status at

MPW is based on

revenue only. It doesn’t

matter if you’re known

for breaching, all that

matters is your revenue.

Advisers hitting the

perfect 50%,

threatening to leave if

they don’t get the AVP

bonus and then getting

paid it.

We’ve recruited people

who’ve never done

SoAs… they don’t go

through that screening.

The mentality is that

advisers are the client –

they hold the power.

That’s not to say we put

up with people that are

fundamentally bad, [you

might] tolerate things

from high writers that

you wouldn’t necessarily

tolerate from others.

30% of MPW

believe leaders

don’t care how

they get results

Only 35% think

rewards

encourage

effective risk

management

Only 44% think

MPW wouldn’t

recruit people

with misaligned

risk attitudes

Agree, Strongly

agree

Neutral Strongly disagree,

Disagree