m3commentary - m3property Strategists · | P1 Key Research Contacts: m3commentary MELBOURNE CBD...

8

| P1 www.m3property.com.au Key Research Contacts: m3commentary MELBOURNE CBD OFFICE Autumn | 2017 m3property.com.au Jennifer Williams National Director | NSW (02) 8234 8116 Casey Robinson Research Manager | QLD (07) 3620 7906 Erin Obliubek Research Manager | VIC (03) 9605 1075 Zoe Haskett Research Manager | SA (08) 7099 1807

Transcript of m3commentary - m3property Strategists · | P1 Key Research Contacts: m3commentary MELBOURNE CBD...

| P1www.m3property.com.au

Key Research Contacts:

m3commentary MELBOURNE CBD OFFICE

Autumn | 2017

m3property.com.au

Jennifer Williams

National Director | NSW

(02) 8234 8116

Casey Robinson

Research Manager | QLD

(07) 3620 7906

Erin Obliubek

Research Manager | VIC

(03) 9605 1075

Zoe Haskett

Research Manager | SA

(08) 7099 1807

| P2www.m3property.com.au

m3property Research

Market Overview 3

Key Influences 4

Key Indicators 5

Significant Sales 7

Outlook 8

CONTENTS

•Sales activity was healthy in the twelve months to

March 2017, albeit below the year prior;

•Prime yields continued to compress while

secondary yields stabilised over the year to March

2017;

•Supply levels increased in the second half of

2016, however, new supply will be limited in 2017

with just one significant project expected to

complete;

•Leasing conditions improved towards the end of

2016 and set to strengthen further in 2017;

•The CBD vacancy rate declined in January 2017,

driven by a combination of stock withdrawals and

improved leasing conditions; and

•Prime effective rental growth of 8.9% was

recorded in the twelve months to March 2017.

TENANT DEMAND

STRENGTHENS IN

THE MELBOURNE

CBD OFFICE

MARKET

DEFINITIONS

A-REIT: ASX listed Australian Real

Estate Investment Trust

Completion date: determined by issue

of a “Certificate of Occupancy”

Grade: is determined using the PCA

report “A Guide to Office Building

Quality”.

Net absorption: is the change in

occupied stock within a market over a

specified period of time.

Net lettable area (NLA): defined in

accordance with the PCA “Method of

Measurement”

Pre-commitment: contract signed to

occupy space in new or refurbished

space prior to construction commencing.

Prime: Combination of premium and

grade A.

Secondary: Combination of grades B, C

and D.

WALE: Weighted average lease expiry.

m3commentary Autumn 2017

| P3www.m3property.com.au

Market fundamentals remain positive for the Melbourne CBD office market leading into

2017, with both state economic growth and business confidence above the national

average. The sector experienced improved levels of tenant demand over the year to

March 2017. This, combined with limited new supply and stock withdrawals, contributed

to the Melbourne CBD office vacancy rate declining in January 2017. In turn, effective

rental growth was recorded in the March 2017 quarter as incentives start to trend down

from historical highs. Yields continued to tighten over the past year for core assets, with

the spread between government bonds and prime yields considered wide compared to

the long-term average.

Melbourne’s diverse range of sectors and office users remain

a key driver of low unemployment and white collar

employment for the State, with Melbourne’s unemployment

rate 6.1% in the month of February 2017.

Tenant demand improved over the twelve months to March

2017, driven by the migration of tenants from suburban and

city fringe locations and strong demand from the IT, Financial

and Government sectors.

Supply levels improved over the second half of 2016.

However, new supply in the Melbourne CBD office market will

be limited in 2017 with 14,246 square metres to be

completed.

The CBD vacancy rate declined from 7.0% to 6.4% over the

period July 2016 to January 2017, driven by a combination of

stock withdrawals and improved leasing conditions.

Investment activity in the Melbourne CBD office market

waned over 2016 driven by a lack of stock available to the

market.

MARKET OVERVIEW

m3property Research

121 Exhibition Street (SX1) &

111 Bourke Street (SX2)

m3commentary Autumn 2017

| P4www.m3property.com.au

ECONOMIC GROWTHGross Domestic Product (GDP) grew by 2.4% during 2016. Strongest growth was

recorded in the Mining, Agriculture, Forestry and Fishing; and Professional, Scientific and

Technical Services sectors. Victoria State Final Demand, a key indicator of the health of

the state’s economy, grew by 3.4% during 2016. Economic growth in Victoria is forecast to

outperform national economic growth over the long-term.

EMPLOYMENTIn the year to February 2017 Victoria added over 95,000 jobs, compared to the year prior,

with most of the growth occurring towards the end of 2016. Although Victoria’s seasonally

adjusted unemployment rate increased in the month of February to 6.1%, the

underemployment rate declined by 0.2 percentage points. The IT, Finance and Insurance

sectors remain the main drivers of white collar employment in the State.

CASH RATE AND GOVERNMENT BOND RATESThe Reserve Bank of Australia (RBA) has lowered the official cash rate by 75 basis points

over the past two years, with the most recent reduction (1.50%) being in August 2016. The

low cost of debt remains a key driver of investor demand for commercial property assets.

Historically low returns on government bonds have also encouraged strong demand for

property during recent years. However, it’s anticipated the gap between government

bonds and commercial yields will compress in 2017 as bond yields commence to rise.

BUSINESS CONFIDENCEThe National Australia Bank’s monthly business survey remained strong at 7 index points

in February 2017 (0 = neutral). This is above the long-term average for business

confidence and remains favourable for future economic growth. Business confidence in

Victoria remained above the national average at 14 index points. Confidence is a driving

force behind tenant decisions to relocate, expand or contract.

EXCHANGE RATEWhile the value of the exchange rate has increased over the past year, it remains

considerably lower than it was between mid-2009 and mid-2015, when it didn’t fall below

80 cents. The lower value has been a driving force behind strong investment demand from

foreign investors.

KEY INFULENCES

m3property Research

575 Bourke Street, Melbourne520 Bourke Street, Melbourne

$

m3commentary Autumn 2017

| P5www.m3property.com.au

TENANT DEMAND

Despite the lack of stock available to the market in 2016,

tenant demand in the Melbourne CBD office market

strengthened over the second half of 2016. Net absorption in

the six months to January 2017 up 7,641 square metres.

Prime stock accounted for over 75% of positive net absorption

in the year to January 2017. This is consistent with the market

experiencing a rise in tenant enquiry for prime CBD office

space, with several tenants seeking to secure lease

agreements given the current lack of prime stock available.

Although tenant demand is expected to remain strong over the

short term, demand is anticipated to soften in the second half

of 2017 as tenants pre-commit to new builds forecast to

complete in 2018 and 2019.

KEY INDICATORS

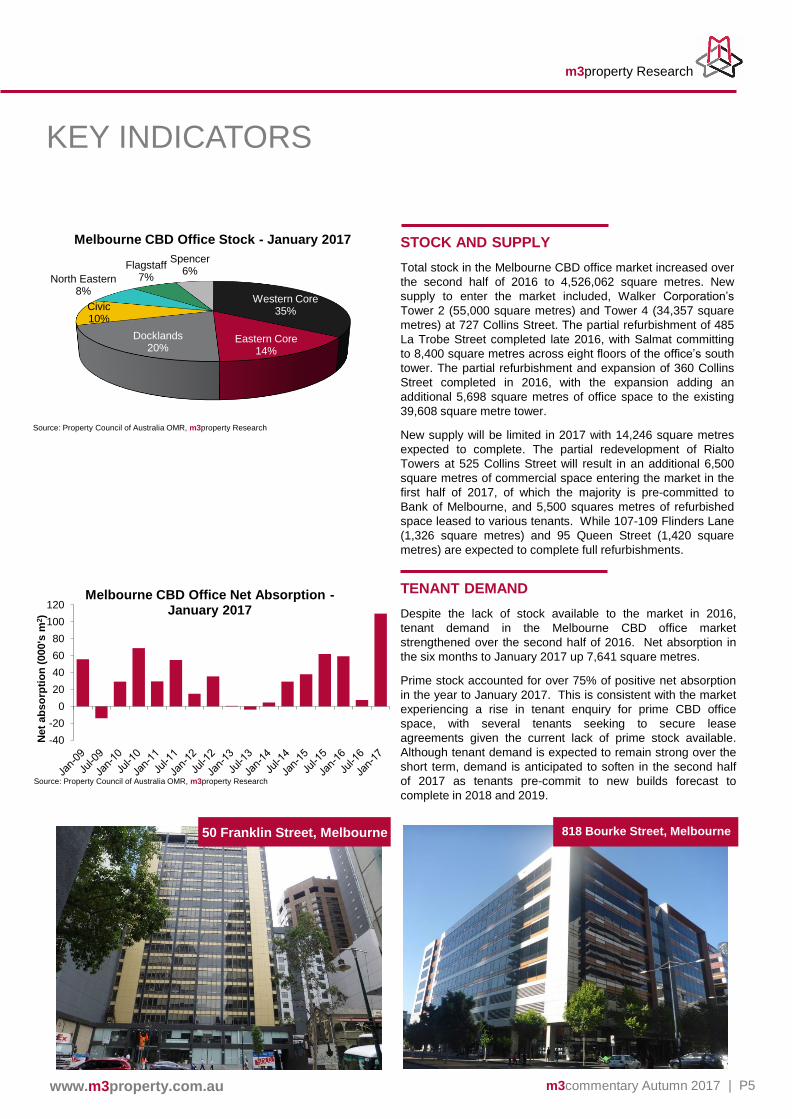

STOCK AND SUPPLY

Total stock in the Melbourne CBD office market increased over

the second half of 2016 to 4,526,062 square metres. New

supply to enter the market included, Walker Corporation’s

Tower 2 (55,000 square metres) and Tower 4 (34,357 square

metres) at 727 Collins Street. The partial refurbishment of 485

La Trobe Street completed late 2016, with Salmat committing

to 8,400 square metres across eight floors of the office’s south

tower. The partial refurbishment and expansion of 360 Collins

Street completed in 2016, with the expansion adding an

additional 5,698 square metres of office space to the existing

39,608 square metre tower.

New supply will be limited in 2017 with 14,246 square metres

expected to complete. The partial redevelopment of Rialto

Towers at 525 Collins Street will result in an additional 6,500

square metres of commercial space entering the market in the

first half of 2017, of which the majority is pre-committed to

Bank of Melbourne, and 5,500 squares metres of refurbished

space leased to various tenants. While 107-109 Flinders Lane

(1,326 square metres) and 95 Queen Street (1,420 square

metres) are expected to complete full refurbishments.

m3property Research

818 Bourke Street, Melbourne50 Franklin Street, Melbourne

-40

-20

0

20

40

60

80

100

120

Net

ab

so

rpti

on

(000's

m2)

Melbourne CBD Office Net Absorption -January 2017

Source: Property Council of Australia OMR, m3property Research

Western Core35%

Eastern Core14%

Docklands20%

Civic10%

North Eastern8%

Flagstaff7%

Spencer6%

Melbourne CBD Office Stock - January 2017

Source: Property Council of Australia OMR, m3property Research

m3commentary Autumn 2017

| P6www.m3property.com.au

INVESTMENT MARKET AND YIELDS

Investor activity in the Melbourne CBD slowed in the twelve

months to March 2017 with approximately $1.3 billion worth of

office stock traded. Transactional activity was below the

previous year’s total of $2.9 billion.

Significant transactions to occur the past twelve months include

the sale of 100 Queen Street to GPT Wholesale Office Fund in

the order of $274.5 million, 114 William Street having sold to a

European based fund for $161.4 million and 438 Elizabeth

Street which was purchased by an offshore private investor for

$75.6 million.

Prime yields compressed 25 basis points over the year to

March 2017, with prime yields ranging from 5.00% to 6.00%.

Over the same period, secondary yields remained stable

continuing to range from 6.00% to 7.00%.

Yields within the Melbourne CBD office market have reached

historically low levels, the current spread between Melbourne’s

CBD prime office yields and government bonds is

approximately 2.7%, which is considered wide when compared

to the 20-year average of around 1.6%.

VACANCY

The total vacancy rate for Melbourne’s CBD office market fell to

6.4% in January 2017 with prime grade vacancy at 6.7% in July

2016 falling to 6.6% over the six month period. Secondary

grade vacancy was recorded at 6.4% in January 2017 down

1.2% over the same period. The vacancy rate as at January

2017 remained well below the long term (since 1990) average

of 11.4% and the lowest since July 2012 (5.5%)

RENTAL GROWTH AND INCENTIVES

Face rental growth in Melbourne’s CBD office market

remained relatively flat over the year to March 2017, with

prime net face rents ranging from $380 to $700 per square

metre.

Prime CBD office incentives declined in the six months to

March 2017 to range from 25.0% to 32.0%. It is anticipated

incentives will continue to trend downwards due to improved

tenant leasing conditions and the lack of new supply entering

the market in 2017.

Strong prime effective rental growth is anticipated over 2017,

while prime net face rents are expected to grow at average in

2017.

KEY INDICATORS

m3property Research

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

Civic EasternCore

Flagstaff NorthEastern

Spencer WesternCore

Docklands

Vacan

cy (

%)

Melbourne CBD Office Vacancy January 2017

CBD 6.4%

Source: Property Council of Australia OMR, m3property Research

$0

$100

$200

$300

$400

$500

$600

Net

Fa

ce R

en

ts (

$/m

2)

Melbourne Prime and SecondaryAverage Net Face Rents

Prime Secondary

Source: m3property Research.

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Sale

s v

olu

me (

$m

illi

on

s)

Melbourne CBD Office Sales Volume

Source: m3property Research. *Office Sales over $5 million to end March 2017.

.

*

m3commentary Autumn 2017

| P7www.m3property.com.au

Property Date Price Equated

Market

Yield

Vendor Purchaser

50 Franklin Street, Melbourne Jan-17 $51,500,000 5.80% Selected Growth Properties Offshore Investor

Esso House, 51-65 Southbank

Promenade, SouthbankDec-16 $160,000,000 *6.06% ExxonMobil Offshore Investor

100 Queen Street, Melbourne Dec-16 $274,500,000 5.51% ANZ Banking GroupGPT Wholesale Office

Fund

438 Elizabeth Street, Melbourne Dec-16 $75,600,000 5.80% Selected Growth Properties Offshore Private Investor

301 Flinders Lane, Melbourne Dec-16 $34,200,000 4.67% KLW Holdings Local Private Investor

114 William Street, Melbourne Oct-16 $161,457,704 6.05% CorVal / Straits Real Estate European Based Fund

Twenty8 Freshwater Place,

SouthbankAug-16 $290,000,000 *6.00% GPT/Frasers Property TBA

51 Queen Street, Melbourne Jun 16 $25,000,000 5.71% Queville Pty Ltd Undisclosed

120 Spencer Street, Melbourne Mar-16 $165,200,000 6.60% Harry Stamoulis Anton Capital

1 Collins Street, Melbourne Feb-16 $125,000,000 5.40% Robert Magid Harry Stamoulis

*Initial Yield

Please contact one of our Commercial Valuers for a detailed sales analysis.

SELECT SALES TO DATE

m3property Research

55 King Street, Melbourne

m3commentary Autumn 2017

KEY COMMERCIAL VALUATION

CONTACTS

The outlook for the Melbourne CBD office market remains

positive. The sector will continue to benefit from strong

annual population growth, increased productivity, and an

expanding Victorian economy.

Tenant demand is expected to strengthen over the short

term, driven by a lack of available stock, with incentive

levels likely to reduce over the year.

Vacancy is expected to remain contained over 2017 before

increasing in 2018 on the back of new supply and backfill

space entering the market.

Limited new supply and improved tenant demand will result

in above average prime effective rental growth in 2017,

while secondary effective rents are expected to grow at

average.

Offshore purchasers are expected to remain active in the

Melbourne CBD office market, attracted to Victoria’s

positive fundamentals. Solid economic growth, strong

annual population growth, and increasing white collar

employment are expected to drive appetite from local and

offshore investors in 2017.

Investment opportunities, particularly for premium CBD

assets, are expected to remain limited, this coupled with

strengthening market fundamentals will result in a

continued low yielding environment in 2017.

OUTLOOKMELBOURNE CBD OFFICE

DISCLAIMER

© m3property Australia. This report has been derived, in part, from sources other than m3property. In passing on this information, m3property makes no

representation that any information or assumption contained in this material is accurate or complete.

To the extent that this material contains any statement as to the future, it is simply an estimate or opinion based on information currently available to m3property

and contains assumptions which may be incorrect. m3property makes no representation that any such statements are, or will be, accurate.

Gary Longden

Director | VIC

(03) 9605 1040

Andrew Duguid

Managing Director | NSW

(02) 8234 8101

Ross Perkins

Managing Director | QLD

(07) 3620 7901

Adrian Burg

Director | SA

(08) 7099 1801

m3property Research

m3property provides national

coverage in all States and Territories.