M a r k e t S t r uc t ur e P r im e r · Most of the rest are ETFs, which stands for...

15

8/30/2019 primer.prooftrading.com Market Structure Primer Get Started! The purpose of this document is to provide an overview of the US equity trading landscape. It started as an onboarding document to help new hires who aren't as well versed in market structure. It can be read start to finish in order, or you can jump around. The visual Life Cycle of an Order also provides a handy view of the various events and entities involved in the process of a trade - from conception to completion. For those with little to no prior knowledge, the three core sections on market participants, mechanisms of communication between participants, and a birds-eye view of overall market activity should provide a working understanding of trading in the US equities market as it is today. Over time, we will be adding material that delves more deeply into further topics, especially into market stucture history and the conflicts of interest that evolve along with market structure.

Transcript of M a r k e t S t r uc t ur e P r im e r · Most of the rest are ETFs, which stands for...

8/30/2019 primer.prooftrading.com

Market Structure PrimerGet Started!

The purpose of this document is to provide an overview of the US equity trading landscape. It

started as an onboarding document to help new hires who aren't as well versed in market

structure. It can be read start to finish in order, or you can jump around. The visual Life Cycle

of an Order also provides a handy view of the various events and entities involved in the

process of a trade - from conception to completion. For those with little to no prior knowledge,

the three core sections on market participants, mechanisms of communication between

participants, and a birds-eye view of overall market activity should provide a working

understanding of trading in the US equities market as it is today. Over time, we will be adding

material that delves more deeply into further topics, especially into market stucture history

and the conflicts of interest that evolve along with market structure.

8/30/2019 primer.prooftrading.com

Birds-eye View of Overall MarketActivityHow Much and How Often

Now that we've fleshed out the different kinds of entities in the US equities market and the

logistics of communications between them, it's time to zoom out a bit and get a sense of

scale and proportions. How much trading activity happens on a typical day? How it is

distributed by size and time and place? How much variation is there intraday and interday?

Here we will give you some basic answers to these questions. Obviously, there is a lot more

structure and patterns underlying trading than the first order statistics here can capture, but

our goal for now is just to get you started on building a basic intuition for the scale and nature

of market activity.

8/30/2019 primer.prooftrading.com

Venues

There currently 3 large parent companies which each operate several stock exchanges. ICE

operates five (this is often also referred to as the "NYSE family"): NYSE, NYSE Arca, NYSE

American, NYSE National, and NYSE Chicago. CBOE operates four: EDGX, EDGA, BZX,

and BYX. Nasdaq operates three: Nasdaq, BX, and PSX. The only exchange outside of the

three families is IEX, which is operated as an independent company.

There are roughly 30 ATS's, which is down from around 40 in 2014.

8/30/2019 primer.prooftrading.com

Stocks and ETFs

Currently, there are roughly 8300 distinct securities traded in the US equities market. For

each security, the market capitilization is calculated by taking the number of shares

outstanding and multiplying by the current price per share. If we sum up the market

capitalization in each security over all the publicly traded securities, we get the total market

capitilization of the US public market, which passed 32 trillion in 2018. This represents about

38% of the global market.

Of the roughly 8300 securities, approximately 5300 of them are publicly listed companies.

Most of the rest are ETFs, which stands for "Exchange-Traded Funds." More generally, there

are ETPs ("Exchange-Traded Products"). An exchange-traded fund is typically designed to

track the behavior of a particular collection of stocks and/or bonds, and it trades in the market

throughout the trading day like an individual stock. When its price deviates from the

underlying stocks/bonds it is referencing, arbitrageurs will use mechanisms that exchange

shares of the fund for the underlying securities to bring the ETF's price back in line with what

it is intended to track. ETNs ("Exchange-Traded Notes") similarly trade like individual stocks

and relate to a collection of underlying securities, but in this case the underlying securities

are unsecured debt securities.

In terms of scale, 8300 securities may not seem like a very big number, especially when we

are talking about a market that functions electronically. 8300 things is certainly a number of

things that computers can easily manage, right? Well, yes and no. 8300 rows in a database,

or even an excel spreadsheet, is easy enough. But as a multiplier, 8300 can become a real

problem. If a computation and data-intense analysis on one day's data for one stock takes 1

second to run, for example, running it on all stocks in sequence (one at a time) could take

8300 seconds, which is 138 minutes. And this is probably too optimistic - as the program is

likely to save some information into memory as it goes, using up resources, and making each

run of the computation potentially slower than the previous ones. Not to mention that the

running time per stock is likely to vary widely based on how much data there is to churn

through.

8/30/2019 primer.prooftrading.com

Though trading in different stocks may frequently exhibit correlation (e.g. multiple stocks

impacted by common news or other market drivers), at a mechanical level trading in different

stocks is separable, and can be implemented in parallel on different machines. To match a

trade in Microsoft, for example, you only have to keep track of the orders and current price

information for Microsoft, and you don't need to know anything about the other stock orders

and prices. Stock exchanges will typically split the 8300 securities into several groups, and

the trading for each group will be processed by its own machine. In the extreme case, you

could imagine 8300 different machines, each acting in parallel to process the orders and

produce trades for a single security. The same kind of trick can be used to speed up analytics

or any other computational process that looks only at the data for one stock at a time.

Parallelization is one tool that keeps things running quickly in the US equities market,

mitigating the effect of the 8300 multiplier.

8/30/2019 primer.prooftrading.com

Trades and Sizes

On any given day, around 6.7 billion shares are traded in the US equities market. ETFs

represent about 18-20% of these volumes. Trades typically happen in round "lots," which for

most stocks are multiples of 100 shares. The average trade size is currently very small -

roughly 200 shares per trade. This is not to say that large trades aren't also common. Block

trades (trades of at least 10,000 shares) happen frequently. For example, looking at the

Nasdaq daily market summary of all trading in Nasdaq-listed securities for June 7, 2019,

we see that there were over 8000 block trades, accounting for close to 20% of the day's total

trading volume. The 200 share average trade size hides a much more varied distribution,

comprised of many large trades, many small trades of 200 or 100 shares, and some even

smaller "odd lot" trades of less than 100 shares.

Since there are roughly 6.7 billion shares traded each day with an average trade size of

roughly 200 shares, we can infer that the number of trades per day is approximately 34

million. These are not spaced evenly throughout the trading day. There are often bursts of

activity in one or many stocks, followed by stretches of relative inactivity. These bursts are

often at speeds a human observer cannot keep pace with - frequently events are following

within less than 1 millisecond of each other. Trading is also typically heavy in the closing

auction: for NYSE-listed securities, for example, the closing auctions represent about 7% of

the volume in those securities.

8/30/2019 primer.prooftrading.com

Orders, Quotes, and Ticks

The number of orders that are transmitted to a venue is typically much higher than the

number of resulting trades. This can be seen, for example, in the data that the SEC provides

concerning the ratio of order cancelations to trades at each exchange.

The ratio of cancelations to trades varies widely by date and by venue, but something like

20/1 is somewhat typical. This gives us a general sense that there is on average a lot of

nimble maneuvering of quotes around each trade.

Over the course of a trading day across all listed securities, there are tens of millions of times

when an NBO price or NBB price changes. NBO stands for "National Best Offer," and it

refers to the lowest price advertised by a would-be seller across exchanges. NBB stands for

the "National Best Bid," and it refers to the highest price advertised by a would-be buyer

across exchanges. The "NBBO" is a shorthand often used to refer to the pair of the NBB and

NBO prices. Naturally, the NBB/NBO are time-dependent constructs, and practically

speaking they are also latency-dependent constructs, as information about price changes

takes time to travel from one market participant to another.

The number of NBBO changes per day is roughly on the same order of magnitude as the

number of trades. Note that this does not count times when the total size available at the best

bid or best offer price changes, but the prices themselves do not change. Nor does it count

the times when displayed orders away from these best prices are changed or canceled.

A fairly high percentage of NBBO price changes occur in rapid succession: nearly 40% of

them occur within 1 millisecond of another NBBO price change. To put this in context, we can

calculate the number of milliseconds (ms) in the trading day as: 6.5 hours x 60 minutes/hr x

60 seconds/minute x 1000 ms/s = 23,400,000. If we approximate the total number of NBBO

price changes across all roughly 8300 listed securities as 20 million, then we have on

average about 2400 NBBO price changes per trading day per stock. So this is about 1 NBBO

price change every 10,000 milliseconds. So the fact that they often ocurr within 1 ms of each

8/30/2019 primer.prooftrading.com

other reflects a rather extreme amount of clustering, suggesting that we should conceptualize

price changes as isolated bursts of activity, punctuating long stretches of relative calm.

8/30/2019 primer.prooftrading.com

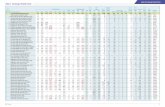

Market Share

The market share of a venue is calculated as the amount of trading volume that occurs on

that venue on a given day, divided by the total volume across the US equities market. Thus,

the sum of the market share over all venues will be equal to 1. Roughly 62% of trading

volume happens on exchanges, with the remaining 38% happening elsewhere (dark pools

or internalizers). Within the exchange landscape, each of the 3 major exchange families,

CBOE, Nasdaq, and NYSE, represents about 20% of trading volume (summing up all of the

individual exchanges within each family). The remaining 2.5% market share belongs to IEX.

8/30/2019 primer.prooftrading.com

Indices

There are several indices which are commonly used as heuristic indicators of overall market

health. The behavior of indices is a frequent headline of financial reporting (e.g. "The Dow

Crossed 20,000 Today!"), presumably because indices are quick and easy to report,

whereas more detailed statements like "these 1345 stocks trended up by small amounts

today, whereas these 1642 stocks trended down by small amounts today, these 587 stocks

wiggled a lot but ultimately landed in roughly the same place, and these 763 stocks..." well,

you get the idea.

So how do indices condense the more detailed activity into a single number? Each index

represents a hypothetical portfolio of holdings that an investor could choose to maintain

among all of the publicly listed stocks. To form a hypothetical portfolio, one must choose

which stocks to include, and in what proportions. Once that is decided, the "value" of the

portfolio can be calculated by multiplying the current prices of the stocks in the portfolio and

summing these with weightings by the specified proportions. Naturally this gives you a

number that changes dynamically as prices change. The underlying unit (whether you

imagine you are holding 100 shares of Microsoft and 200 shares of Intel vs. 200 shares of

Microsoft and 400 shares of Intel, etc.) doesn't really matter, as long as it is consistent. It is

the relative behavior of the index over time that tells you something about the evolution of

stock market over time.

Sometimes what it tells you is pretty limited or difficult to interpret. There are many degrees of

freedom in defining an index, as there are many ways to decide which stocks to include, and

many ways to decide the relative proportions. Some indices are clearly more meaningful

than others. An "index" that is comprised of simply one stock, for example, presumably tells

you fairly little about the behavior of other stocks. The price movements in a single stock will

perhaps reflect general trends across the entire market and more granular trends across the

relevant sector (e.g. energy, financials, utilities, etc.), but will also be driven by the specifics

of that particular company. If we want the meaning of an index to transcend the details of any

8/30/2019 primer.prooftrading.com

one particular company or small subset of companies, we need to choose a reasonably

"representative" sample of stocks and proportions to define our index.

S&P 500

A very commonly used example of this is the S&P 500 index, which is comprised of the

roughly 500 top companies, primarily chosen by market capitilization (recall: market cap =

price per share times number of outstanding shares). The weighting for the S&P 500 Index

corresponds to market cap, meaning that the relative weight given to a particular company is

propotional to its market cap. This allows a rather clean interpretation of changes in the

index: if the index increases by 10%, for example, that means the total market capitilization of

all the included companies has increased by 10%.

The S&P 500 is often used as a proxy for general market health, which is quite reasonable,

as the included companies cover about 80% of the total value of the US stock market. This

tells us that the stock market is pretty top heavy: total market capitalization is fairly

concentrated in the top 500 companies among the many thousands of total companies.

Looking at the S&P 500 over time gives us a broad sense of how the market has historically

trended up and down.

DOW

The DOW Jones Industrial Average is comprised of 30 stocks of large companies. The

included companies change over time, as individual companies may rise and fall in

influence. When the index was created by Charles Dow and Edward Jones in the late 1800s,

it included 12 companies, and it was calculated by simplying adding the price of 1 share of

each of the companies and dividing by 12. It is still calculated by added the prices of 1 share

of stock for each company in the index and dividing by a single number, but that number is

now called the "divisor" and has historically been adjusted to make the index consistent

across stock splits and mergers. In between adjustments of the divisor, we can think of the

DOW as an average of the 30 stock prices with equal weight on each. This means, for

example, that a 10% relative increase in the price of one of the higher priced stocks will

cause a greater relative increase in the DOW than a 10% relative increase in the price of one

8/30/2019 primer.prooftrading.com

of the lower priced stocks. In contrast, a $1 absolute price increase in any one of the

component stock prices will have an indentical effect on the index.

The companies included in the DOW index represent about a quarter of the value in the total

US stock market. But because of the smaller sample size and the fact that the index is not

weighted by market cap, the DOW is not really a great proxy for overall market health. It

remains a popular data point mostly because of its historical longevity and broad familiarity.

Russell Indices

The Russell Indices, e.g. the Russell 3000 Index, the Russell 2000 Index, and the Russell

1000 Index, etc., pick out different subsets of stocks based on market capitilization. For

example, the Russell 3000 Index includes the largest 3000 companies by market

capitalization, while the Russell 1000 includes only the top 1000 companies and the Russell

2000 includes the next 2000. Once the subset of stocks is determined, their individual

contributions to the index are weighted proportionally to market cap. The Russell indices can

be used as proxies for the cummulative performance of different categories of stocks: large

cap, small cap, etc.

Index Funds

Since an index corresponds to a hypothetical portfolio of stocks, it is possible to maintain a

portfolio matching the hypothetical one, and turn the hypothetical behavior into realized

returns. This process isn't quite perfect, since sometimes the stocks or weights in an index

change, and adjusting a real portfolio to keep in sync with the hypothetical one involves

buying and selling that incurs additional cost and risk. But to a reasonable extent, one can

approximate the performance of an index with a real portfolio, and this is what index funds

are designed to do. Investing in an index fund that is properly managed should allow you to

achieve approximately the returns corresponding to the hypothetical index it is implementing.

This is why index funds that simulate the S&P 500 index, for example, are popular

investments for investors who just want to generally benefit from stock market growth in an

overall sense, without entangling their returns too closely with the performance of a smaller

number of individual stocks.

8/30/2019 primer.prooftrading.com

When the constitution of an index changes, a lot of market activity will result as index funds

seek to adjust their holdings accordingly. The Russell indices, for example, are reconsituted

on a scheduled yearly basis. This is to adjust for changes to market capitilization that have

occurred over the preceding year. Trading on and around such scheduled events will be

markedly heavier (and different in distribution) from ordinary trading activity.

8/30/2019 primer.prooftrading.com

Volatility and Variation

Over time, there is a lot of variation in the kind of daily stats we have quoted above. Some

variation in trading behavior is driven by structural things: e.g. index rebalancing or the fact

that stock options have certain standardized expiration dates (following the third Friday of a

given month). But even aside from these anticipated structural events, within a day or hour or

minute, etc. there can be wild changes in activity and prices within a single stock, multiple

stocks, or broadly across the market. The number of NBBO changes in a day for instance,

can vary by a multiplicative factor of 3 or 4 (or more) when we compare a relatively calm

trading day to a relatively turbulent one.

In a technical sense, "volatility" in the context of stock trading usually refers to the standard

deviation or variance of prices for a particular security or set of securities. Roughly, this is a

measure of how far prices tend to drift above and below their average over a specified unit of

time. This gives additional color around price trends that mere averages or medians do not.

For example, if we say "the average price of Microsoft over the trading day today was X," we

mean that we took all the trades of Microsoft over the day and averaged their prices

(presumably weighted by their sizes). But this alone tells us nothing about whether we had,

say, many trades at price exactly X, or trades that swung widely between lows of X/2 and

highs of 2X, averaging out to X overall. Volatility disambiguates these disparate situations.

Low volatility means that we had trades mostly clustered tightly around the average price,

while high volatility means that prices oscillated considerably.

Information about expected future volatility can be inferred by looking at option prices. Since

the value of an option depends on the probability that a stock price will go above or go below

a specified strike price in the future, the price of an option right now can tell us something

about "the market's" estimate of the likelihood of particular future price movements. The

CBOE Volatility Index, or VIX, measures this kind of "implied volatility" by using SPX option

trades to infer the market's expection of 30-day volatility in the S&P 500 index.

Further reading:

8/30/2019 primer.prooftrading.com

SIFMA Insights: US equity Market Structure Primer, July 2018 (*this was a source for many

of the stats above)