Lonestar West Howard Group Introduction August 2012

14

Lonestar West Inc. “Shedding Daylight On Opportunity” The Howard Group’s Perspective By: Jeff Walker and Grant Howard August 2012 In advance of even describing Lonestar’s (LSI – TSX.V) business, we’d like to pose the question; what makes you think about investing in a company? Could it be hockey stick style profitable growth? Could it be the proper balance between leverage & cash flow? Could it be sector diversification to reduce risk? Could it be customer diversification to reduce risk? Could it be a top quality & highly experienced team? Could it be a heavily invested CEO? Could it be a heavily invested insider group? Could it be board members who have built successful businesses? Could it be a mindset with a calculated growth plan? Could it be attention to detail? Could it be a tight share structure? Could it be a management/board aversion to unnecessary dilution? Should these points make sense, please read on as every bullet is applicable to Lonestar West. Before going much further we must declare that the Insight Limited Partnership II, which is associated with The Howard Group (HG) is an investor Shares Issued: 15,508,000 Recent Price: $1.04 52 Week High: $1.20 52 Week Low: $0.60 Market Cap: $16.13 Million

-

Upload

the-howard-group -

Category

Business

-

view

3.606 -

download

2

Transcript of Lonestar West Howard Group Introduction August 2012

Lonestar West Inc.

“Shedding Daylight On Opportunity”

The Howard Group’s Perspective

By:

Jeff Walker and Grant Howard

August 2012

In advance of even describing Lonestar’s (LSI – TSX.V) business, we’d like to

pose the question; what makes you think about investing in a company?

Could it be hockey stick style profitable growth?

Could it be the proper balance between leverage & cash flow?

Could it be sector diversification to reduce risk?

Could it be customer diversification to reduce risk?

Could it be a top quality & highly experienced team?

Could it be a heavily invested CEO?

Could it be a heavily invested insider group?

Could it be board members who have built successful businesses?

Could it be a mindset with a calculated growth plan?

Could it be attention to detail?

Could it be a tight share structure?

Could it be a management/board aversion to unnecessary dilution?

Should these points make sense, please

read on as every bullet is applicable to

Lonestar West.

Before going much further we must

declare that the Insight Limited

Partnership II, which is associated with

The Howard Group (HG) is an investor

Shares Issued: 15,508,000

Recent Price: $1.04

52 Week High: $1.20

52 Week Low: $0.60

Market Cap: $16.13 Million

in Lonestar. LP II invested in a 2011, $0.60 common share placement. Also,

The Howard Group receives investor relations fees. HG is not a registered

investment advisor. As such, this commentary solely deals with HG’s

perspectives on why it is aligned with Lonestar West. Readers should carefully

consider all opinions and seek registered investment advice.

Although we formally engaged with LSI this past February to conduct and

manage investor and financial market relations programs, our introduction to

LSI came in early 2010.

The conversation was opened by David Prussky who, along with his partner

David Rosenkrantz have successfully built and invested in companies through

their Toronto based merchant banking company, Patica Corporation.

Although we had first been introduced to Patica in 2005, HG began working

much closer with the “two Dave’s” when Carfinco Financial Group (then

Carfinco Income Fund) became an HG client in 2009 and remains so to this

day.

We’ll have more to say about the Carfinco connection further below.

The important point is that Patica isn’t slow but it also doesn’t rush a deal. The

process is to take a company to a certain level, starting with the right

management, backed with a controlled capital structure, financial support,

fundamental performance and detailed growth plan in advance of unveiling the

entity to a broad public audience.

And so we watched, stayed in touch, invested, and then a couple of years later

the consensus was that the time was right to start banging the drum.

In May 2000, Lonestar Vacuum was incorporated as an owner-operated

business by current President and CEO James Horvath.

James, a celebrated athlete and past competing rough and tumble cowboy, cut

his teeth in the energy service trucking business after buying his first vacuum

truck in 2000. Prior to that, James was working in the sector as a drilling fluid

expert who had established multiple business relationships across Canada and

the United States.

HG & Lonestar – We Have History

Lonestar West – The Company

Over the next 8 years, James and his wife Kristin (Vice President of LSI) built

Lonestar into a very profitable but still small business.

They were then ready to take the next step, and now; enter Patica.

In February 2008, Lonestar began discussions with Patica about expanding

into the hydrovac sector and becoming a public company. Things moved

quickly after that with an initial Prospectus filed in August of that year, while a

combination of purchased and leased HVAC trucks were secured and branded

with the Lonestar name. In December 2008, a $1.2 million Initial Public

Offering (IPO) was closed and LSI began trading on the TSX Venture exchange.

At the time, it had six VAC trucks and seven HVAC trucks.

A standard Vacuum truck can be used in many ways. In the oil and gas

industry for:

Tank cleaning

Well Sites and removal of drilling fluids, disposing of fluids in

either spread fields or authorized disposal facilities

Pipeline, non-destructive testing, industrial, fuel tank cleaning,

spill cleanup, car wash, flood damage and septic tanks/sewer work

Currently, Lonestar operates seven VAC trucks (below), each costing

approximately $400,000.

What’s A VAC? Even More – What’s An HVAC?

Hydro-excavation on the other hand, is the process of excavating rock and soil

to expose underground utilities and pipelines, also known as “Daylighting”. The

ground is removed causing what is underneath to be exposed to daylight.

The process uses pressurized water to agitate the earth, and a powerful

vacuum to remove the soil and debris. This process is a non-destructive

method of excavating, replacing a conventional backhoe and manual digging.

It is safer and faster than traditional excavation methods when operating

around sensitive infrastructure. The process can excavate frozen ground

because of onboard water heaters while reducing environmental liabilities and

potential restoration costs normally associated with conventional excavating.

Examples of uses for HVAC trucks are below:

Oil and Gas Industry

Tank cleaning and pipeline trenching

Facility maintenance

Utility Sector

Piling and pole hole excavation

Communications Companies

Uncovering buried utilities

Environmental Cleanup

Debris removal and cleanouts

Construction

Shoring and slot trenching

The cost of a new hydro vacuum truck is about $475,000. Lonestar currently

has twenty eight HVAC trucks (below) in the field as a combination of corporate

owned and lease operated.

In combination with six lease-operator agreements, LSI has thirty-five

trucks in the field as of this writing.

Lonestar has focused its service areas to maximize its relationships in the

energy, infrastructure and mining sectors in Alberta and Saskatchewan and

Manitoba.

With approximately 258 customers, including some of the biggest names in the

oil and gas sector, Lonestar’s diverse customer base mitigates risk as no single

client represents more than 7.3% of its business. In fact, its top five customers

only make up 29% of its overall business. Results speak loudly, as the

historical bad debt expense is negligible!

Operations Areas

De-Risking – Customer Diversification – Avoiding

Concentration

About 70% of the revenue stream is related to the oil and gas sector. The

remainder of sales are generated from infrastructure as well as the mining and

potash industries. The latter was one of the reasons Lonestar established

operations in Saskatchewan.

Not keeping all of its eggs in the energy sector is wise, as cycles are part of

investing life and will always be with us.

Lonestar has gone to great lengths to maintain an impeccable safety record

with high standards being set through training and upgraded “Health, Safety &

Environmental Programs (HSE)”.

This isn’t just talk or corporate niceties. A service company that does not pass

international grading and maintain superior safety records DOES NOT win

business with large companies.

Lonestar has:

AASP approved Certificate of Recognition (COR)

Prequalified by ISNetworld, Complyworks, Canqual & PIC’s Auditing as a

low-risk supplier

Continuously evolving HSE program to stay ahead of changes in the

industry

GPS monitoring enhances safety

Low lost-time incident frequency

To get an idea of the size and scope of this industry, one needs to look no

further than Badger Daylighting Ltd. (TSX:BAD), which has been a stock

market darling the past couple of years.

Excluding mom and pop operators, there are several private companies that

are larger and challenge Lonestar but BAD is still the “Baddest” kid on the

block with about 262 HVAC trucks in Canada and 273 in the U.S.

De-Risking – Sector Diversification

Safety – Good Sense – Good Business

The Competition

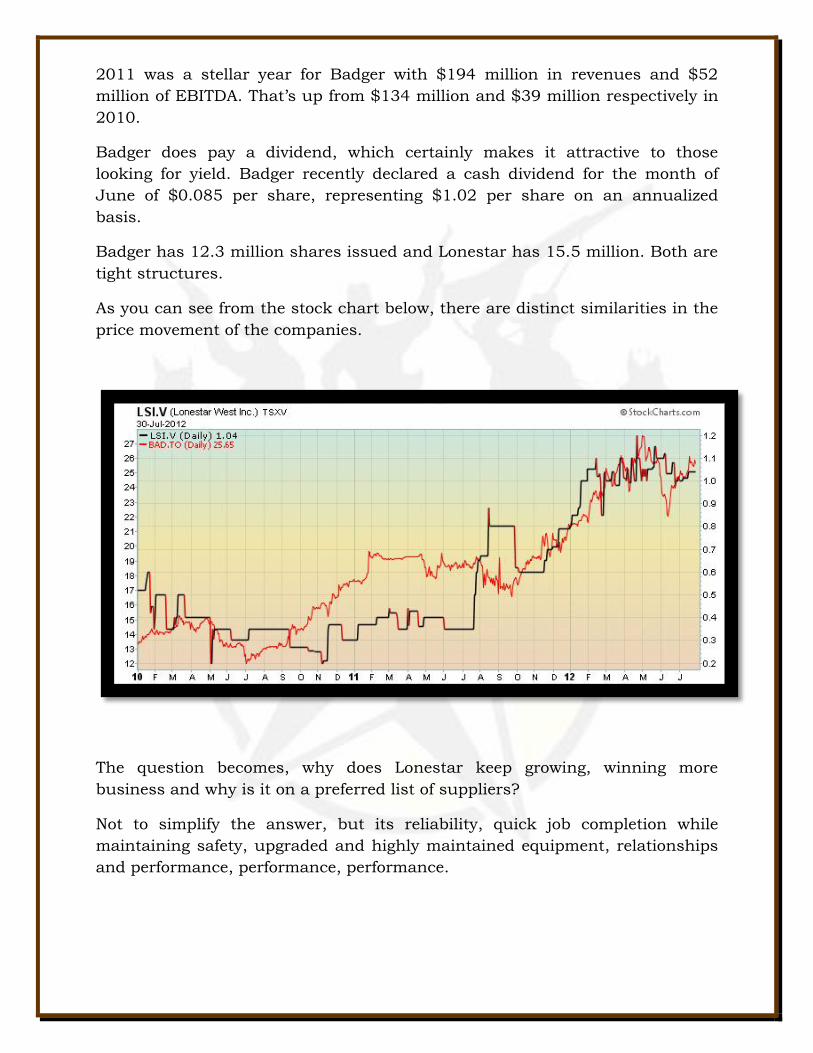

2011 was a stellar year for Badger with $194 million in revenues and $52

million of EBITDA. That’s up from $134 million and $39 million respectively in

2010.

Badger does pay a dividend, which certainly makes it attractive to those

looking for yield. Badger recently declared a cash dividend for the month of

June of $0.085 per share, representing $1.02 per share on an annualized

basis.

Badger has 12.3 million shares issued and Lonestar has 15.5 million. Both are

tight structures.

As you can see from the stock chart below, there are distinct similarities in the

price movement of the companies.

The question becomes, why does Lonestar keep growing, winning more

business and why is it on a preferred list of suppliers?

Not to simplify the answer, but its reliability, quick job completion while

maintaining safety, upgraded and highly maintained equipment, relationships

and performance, performance, performance.

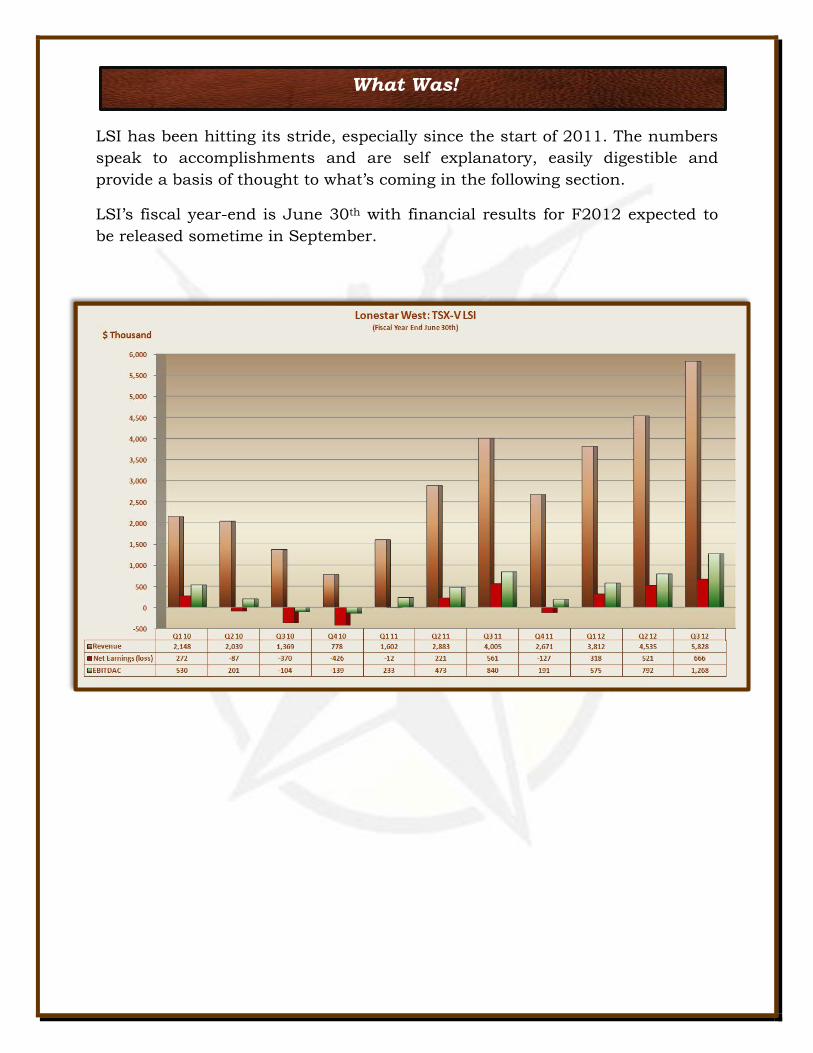

LSI has been hitting its stride, especially since the start of 2011. The numbers

speak to accomplishments and are self explanatory, easily digestible and

provide a basis of thought to what’s coming in the following section.

LSI’s fiscal year-end is June 30th with financial results for F2012 expected to

be released sometime in September.

What Was!

In context of Badger and LSI trading in a multiple of 5 to 5.5 times EBITDA,

one must ask, where’s the future value? While there are no guarantees,

Lonestar’s team has specific objectives for calendar 2012 that provides

perspective on what sort of value the stock could achieve over the coming

months. LSI is currently trading in the $1.00 to $1.10 range.

Grow fleet to 40+ trucks from current 35 (July/12)

Reach annualized EBITDAC of $4.5-$5 million ($0.29 - $0.32/share)

from $1.7 million F2011

Maintain term debt to EBITDAC ratio < 1:1

NO additional equity is required to reach 2012 objectives

What Should Be!

You’ll note the last bullet about no need for equity to meet corporate objectives.

This is rather important and mirrors the philosophy that HG has borne witness

to over Lonestar’s development period. Advisors, board members and

management are loathe to incur dilution unless it is extremely accretive and

leapfrogs the business to much greater levels envisioned for 2014.

Of course, an M & A deal has to make a lot of sense, as Lonestar has proven it

can spur organic growth quite nicely.

We opened this commentary with background on Patica and its business

building philosophy. It’s not only Patica as represented on the LSI board by

David Prussky, but also director Tracy Graf, who is Carfinco’s CEO. Not to

ignore other board members, but these are the people HG knows, and we have

seen them define the word “meticulous” in building businesses.

We’ve also spent a good deal of time with CEO James Horvath, who thinks

nothing of grabbing wrenches late into the evening to bring a truck up to

“grade” when all hands are needed on deck.

Management and insiders are definitely aligned with shareholders. As we

mentioned above, any shares issued for new equity have been jealously

guarded and there have been only two equity financings. James Horvath

obtained his share position after rolling his business into the public entity in

conjunction with an independent third-party appraisal.

Issued:

Insiders: free-trading 9.5 m

CEO (Horvath) 7.1m

Public float 6.0 m

Total Issued: 15.5 m

Options: 1,024,000

Fully Diluted: 16.5 m

Financings: Dec/08 $1.2m IPO @ $0.50

Aug/11 $1.2m @ $0.60

Sometimes Stingy Is Good!

Shares – The Big Insider Stake – Interests Aligned

Lonestar is not quite a blue-sky, “I just hit a thousand barrels of oil a day” or

“10 million ounces of gold” story.

Neither is it comfy like an old pair of slippers as it has the potential to generate

excitement. However, we’d like to suggest it probably won’t cause you to pop

Valium, especially in context of the investing and economic climate that is and

likely will be for a very long time.

If the points we’ve covered make some sense, and one could reasonably expect

the LSI team to continue to deliver fundamental, sensible, planned growth, and

not add to your sleepless nights; then Lonestar deserves a look.

The links below will allow you to reach The Howard Group when you require investor

information:

Email: [email protected]

Website: http://www.howardgroupinc.com/clients/Clients/LonestarWestInc.aspx

Newsletter Direct: http://howardgroupinsightnewsletter.blogspot.com/

Contact Information:

Jeff Walker/Grant Howard

The Howard Group Inc.

Toll Free: 1-888-221-0915

Phone: (403) 221-0915

The Wrap

To receive future news and commentary on Lonestar West please email: [email protected] Subject Line – Receive Lonestar information

Please provide us with relevant contact information and whether or not you are an individual investor, investment advisor, analyst or fund manager. Also, please indicate if you would like someone to call you to discuss Lonestar West.

We also appreciate your comments & feedback.

Disclaimer

The Howard Group is not a registered investment advisor and as such, individuals

should consult a registered investment advisor prior to making investment decisions

in relation to the company discussed in this commentary. The information presented

in these website pages was obtained from sources believed to be reliable but is not

guaranteed, is not all conclusive and should not be relied upon as the sole source of

information/opinion for making an investment decision. The Howard Group or its

employees may own securities in the company discussed in this commentary. The

Howard Group receives remuneration for Investor Relations activities from the

company discussed in this commentary.

Except for the statements of historical fact contained herein, certain statements

contained in this presentation constitute “forward-looking statements” as such term is

used in applicable Canadian and US laws. These statements relate to analyses and

other information that are based on forecasts of future results and assumptions of

management. Any statements that express or involve discussions with respect to

predictions, expectations, beliefs, plans or future events or performance (often, but not

always, using words or phrases such as “expects” or “does not expect”, “is expected”,

“anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that

certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken,

occur or be achieved) are not statements of historical fact and should be viewed as

“forward-looking statements”.

Forward-looking statements are made based on management’s beliefs, estimates and

opinions on the date the statements are made and the Corporation undertakes no

obligation to update forward-looking statements if these beliefs, estimates and

opinions or other circumstances should change, except as required by applicable law.

THIS IS NOT A RECOMMENDATION TO BUY OR SELL ANY SECURITY