Lombard Risk Management plc · 44 Southampton Buildings London WC2A 1AP ... especially the case in...

44

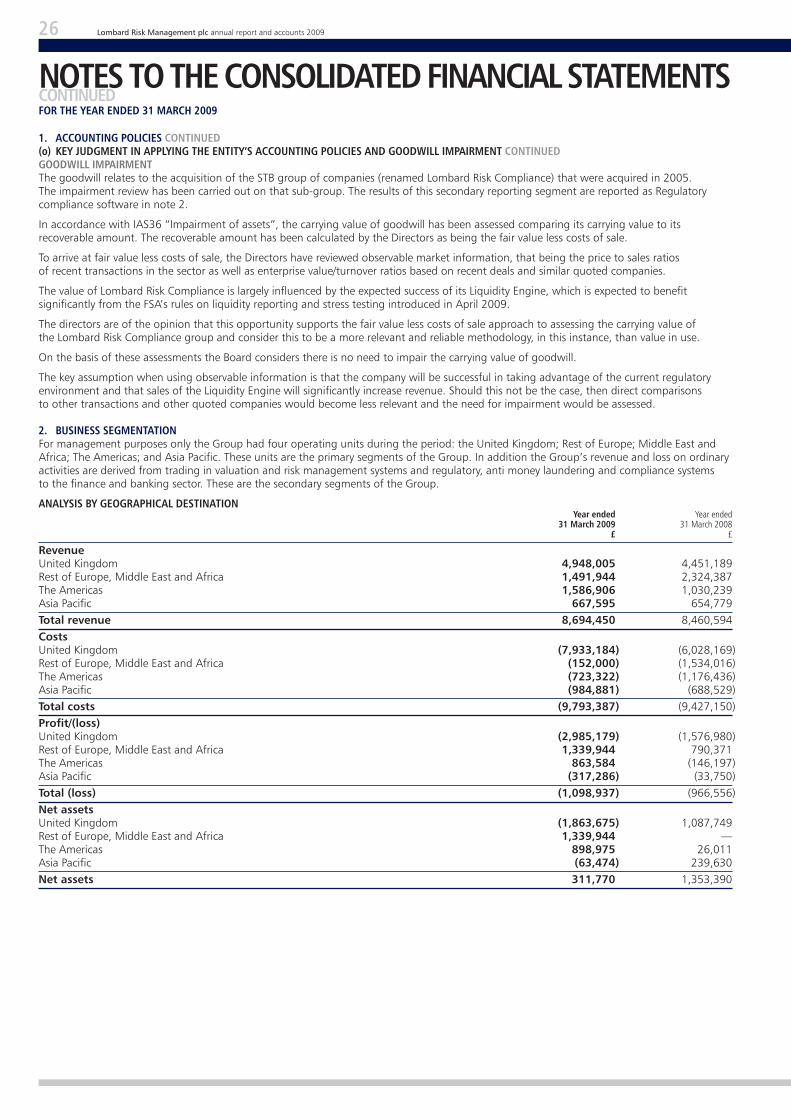

Lombard Risk Management plc Annual Report & Accounts 2009 Managing Collateralised Trading. Enabling Regulatory Compliance.

Transcript of Lombard Risk Management plc · 44 Southampton Buildings London WC2A 1AP ... especially the case in...

Lombard Risk Management plcAnnual Report & Accounts 2009

Managing Collateralised Trading. Enabling Regulatory Compliance.

corporate statement

company informationThe mission at Lombard Risk has always been to help the financial industry to improve the approach to managing the operational risk in their businesses. That mission remains unchanged today as Lombard Risk continues to deliver innovative specialised software solutions that help our customers improve the management of collateralised trading and regulatory compliance.

For over 20 years Lombard Risk Management plc (“Lombard Risk”) has delivered industry-leading global risk management and regulatory compliance software. Today, Lombard Risk is one of the world’s recognised leading providers of collateral management and regulatory compliance solutions to financial organisations and large corporations around the world. Our award-winning global solutions enable the financial industry to improve the management of counterparty risk, collateral risk, trading risk, liquidity risk reporting, financial crime detection and global regulatory reporting.

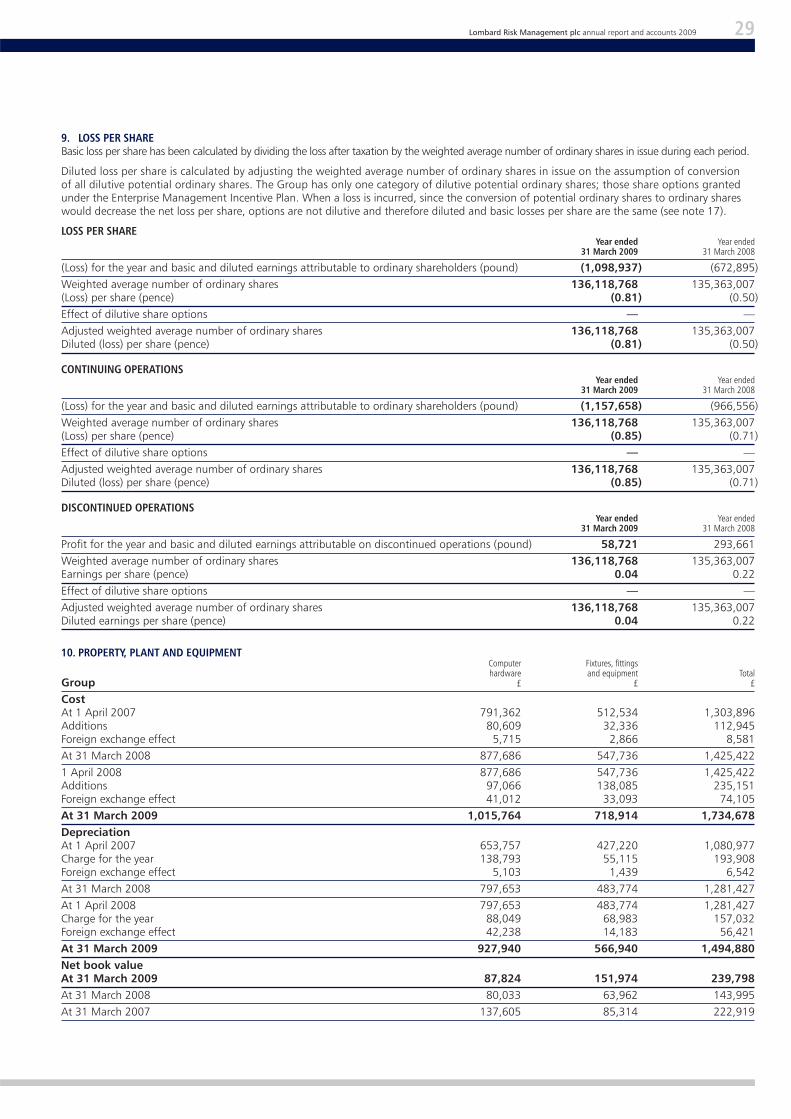

company registration number3224870

directorsJohn Wisbey Chairman

ian peacock Deputy Chairman

brian croWe

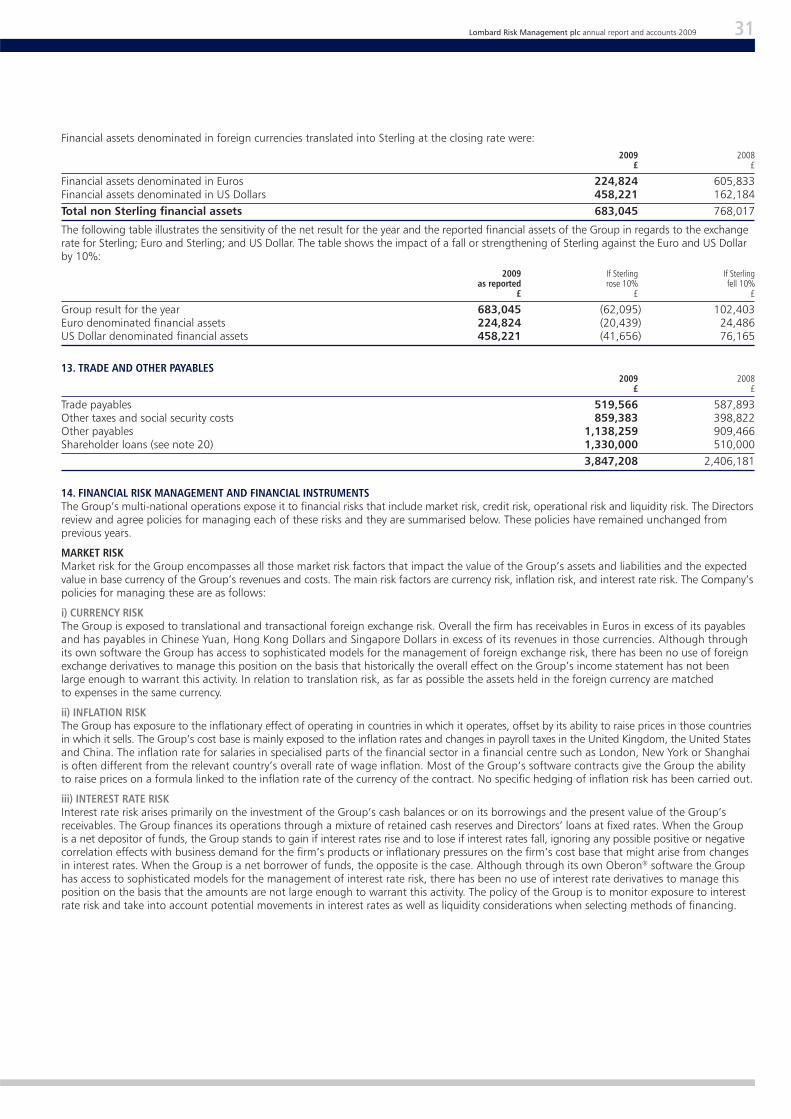

keith butcher

company secretaryJane Fineman

registered officeIndia House 45 Curlew Street London SE1 2ND

nominated advisor and brokernobLe & company Limited120 Old Broad Street London EC2N 1AR

auditorsgrant thornton uk LLpGrant Thornton House Melton Street Euston Square London NW1 2EP

corporate soLicitorsmemery crystaL44 Southampton Buildings London WC2A 1AP

registrarscomputershare investor services pLcPO Box 859 The Pavilions Bridgwater Road Bristol BS99 1XZ

bankersnationaL Westminster bank pLc180 Brompton Road London SW3 1HL

hsbc bank28 Borough High Street London SE1 1YB

datesannuaL generaL meeting 23 October 2009

_cover.indd 2 28/09/2009 11:38:33

01Lombard Risk Management plc annual report and accounts 2009

HigHligHts

Highlights* Revenue £8.69m, up 2.8% on same period last year (2008: £8.46m)

Loss after tax £1.10m (2008: Loss £0.67m)

Profitabilityachievedbyriskmanagementandtradingsoftwarebusiness,withCOLLINE®CollateralManagementsoftwarebreakingthroughtoprofitabilityforfirsttime

RegulatoryCompliancebusinessSTBSystemsLimitedrestructuredandrenamedLombardRiskComplianceLimitedinDecember2008 and re-branding exercise largely completed

ConsolidationofLondonoperationsintoonebuilding,andcontinued reductions in London headcount; move to larger premisesinShanghai

MajorcontractwinsforCOLLINE®includingaTier1ContinentalEuropeanbank

Future prospects Continuedstrongdemandbybanksforcollateralmanagement

products and likely further changes in bank regulation in 2009willcreate ongoing commercial opportunities despite theglobaldownturn

Costcuttingmeasuresimplementedinlate2008,includingreductioninBoardsize,shouldensurethatthebusinessis cash generative again during FY 2010

Fund-raisingandbalancesheetrestructuringafterthefinancialyearendcombinedwithgoodcommercialprospectsleavetheCompanywellplacedforgrowthwithastrongsetofinstitutionalshareholders capable of funding the Group’s future expansion.

* Financial results for the year ended 31 March 2009 have been delivered in line with Board expectations and are prepared under International Financial Reporting Standards (“IFRS”) as adopted by the European Union.

20092008200720062005

Revenue (£m)

8.698.46

6.94

4.704.62

£8.69m+2.8%

01 HigHligHts 02 CHaiRman’s statement 08 BoaRd of diReCtoRs 10 lomBaRd RisK’s management team 12 diReCtoRs’ RepoRt 14 CoRpoRate goveRnanCe RepoRt 15 RepoRt of tHe audit Committee 16 Consolidated finanCial statements 17 RepoRt of tHe independent auditoR

– Consolidated finanCial statements 18 Consolidated inCome statement

19 Consolidated BalanCe sHeet 20 Consolidated statement of CHanges

in sHaReHoldeRs’ equity 21 Consolidated CasH flow statement 22 notes to tHe Consolidated

finanCial statements 35 paRent Company finanCial statements 36 RepoRt of tHe independent auditoR

– paRent Company finanCial statements 37 Company BalanCe sHeet 38 notes to tHe Company finanCial statements iBC Company infoRmation

Contentsto be updated.

_2_LRM_ar09_front.indd 1 28/09/2009 11:37:01

02 Lombard Risk Management plc annual report and accounts 2009

HigHligHts of tHe CHaiRman’s statement

ForwardmomentumfollowingTier1Bankcontractwin

Revenueincreaseinthefaceofdifficulteconomic times

CollateralManagementsoftwarebrokenthroughtoprofitability

Liquidity reporting to offer more opportunities for the company in the years ahead

CHaiRman’s statement

summaRyAlthough the financial year saw unprecedented turbulence in world financial markets, Lombard Risk continued to win contracts and grow organically. This was especially the case in the Collateral Management Software business, which has excellent forward momentum following a large contract win with a Tier 1 German bank announced in April 2009. The move away from a light touch regulatory regime in the UK beginning with a complete reform of Liquidity Reporting offers considerable opportunity to the firm in the coming year and years ahead. The challenge in FY 2009 at a time that no‑one could be sure of the financial outlook for the banking system in the next month let alone the next few years was to steer the right course between reducing costs while not damaging the future prospects of a promising company. We believe we got this balance about right, and that the Group is now well placed to grow significantly over the next few years.

As anticipated, the Group made a loss for the year, most of it in the first half. Revenues for the year ended 31 March 2009 were £8.69m. This is only a modest rise of 2.8% overall from the £8.46m in the previous year. The overall loss of £1.10m was, as already highlighted in the last Interim Reports and explained again below, largely due to various issues in the Regulatory Compliance business which should not affect FY 2010 to any material extent. The Trading and Risk business achieved overall profitability in the full year of around £0.87m including full apportionment of central overheads. Within the Trading and Risk division the collateral management software product COLLINE® also broke through to profitability during the year and ended the year ahead of budget, a clear example of how parts of our business are not affected by, and are possibly even benefiting from, the liquidity crunch in markets. We concluded nine contract wins for COLLINE® during the year, a good achievement.

continued growth...

1 excellent forward momentum 2 strong

growth opportunities

3 major fund-raising after year end 4 benefiting

from increased regulation

_2_LRM_ar09_front.indd 2 28/09/2009 11:37:02

03Lombard Risk Management plc annual report and accounts 2009

The outlook for our COLLINE® collateral management software remains very positive with strong new business demand expected to continue and revenue growth likely from existing customers. This is due both to the current market focus on counterparty risk and liquidity risk, and to the considerable advances in the product in maturity, scalability and resilience. This now makes COLLINE® an ideal and suitable product for Tier 1 banks, as well as for smaller banks, asset managers and other firms.

Our Oberon® product continued to be our most profitable product and saw the completion of the installation at its first client in China as well as satisfactory product advances.

Given that most of our revenues come from banks and financial services companies, it is hard to see that our products could be much better placed for FY 2010 than to have our emphasis on collateral management (as part of risk and liquidity management) and regulatory compliance. We are the global number 2 in both collateral management software and bank regulatory reporting software.

On the regulatory compliance side we continued to sign significant contracts in Europe and Asia for STB‑Reporter despite the fact that some projects were put on hold due to cuts in bank IT spending or bank mergers. With it now clear that there will be previously unforeseen regulatory change in 2009 and future years in many

countries owing to the demand for reform of the financial system, we believe there will continue to be significant opportunities worldwide for our regulatory business. This is particularly significant for us in the UK where new Liquidity Reporting regulations come into effect in early 2010 as part of the new heavier touch regulatory regime.

We have invested heavily in technical resource since the balance sheet date, and more recently have strengthened our Board with the appointment of a new Finance Director Keith Butcher, but various cost actions that we took at the end of 2008 should allow us to operate in FY 2010 on a similar cost base to that in FY 2009 despite increasing revenues.

...innovative solutions

Lombard Risk is trusted by financial institutions and large organisations across the globe to provide specialised solutions.

Our innovative specialised products stay a step ahead of the ongoing risk and compliance reporting demands.

Lombard risk is abLe to provide software for the broad spectrum of compLiance and risk reporting

_2_LRM_ar09_front.indd 3 28/09/2009 11:37:05

04 Lombard Risk Management plc annual report and accounts 2009

Increased revenue despite tough economic conditions.

Strategy to reduce cost base coming to fruition.

£1,800,000 placing after year end will strengthen balance sheet.

FinancialRevenue increased to £8.69m against £8.46m in the comparable period last year. Loss before tax was £1.25m against £1.12m in the previous year. Cash at the end of the period was £0.15m and there were no bank borrowings. The Group’s balance sheet and cash position will be significantly strengthened in October 2009 when the proceeds of a placing, concluded at the end of September 2009, are received. At the same time £1.03m of the £1.33m director loans outstanding at the year end will be converted to equity and the remaining £0.30m, along with a further £0.30m of director loans received in July/August 2009, will be repaid in full, leaving the Group with a strong cash position and no borrowings. All software development and R&D expenditure expenditure during the year was expensed in full when incurred.

The fall in Sterling has clearly helped the Sterling recognition of revenue denominated in foreign currency. This has two conclusions:

a) Given that about £4.0m of our revenue was in USD, EUR and Asian currencies, it might have been expected that the revenue would have risen by more than it did. On a like for like basis, last year’s £8.46m would have equated to about £8.8m at the average rates prevailing during the FY 2009. The reason revenue did not achieve this level is wholly accounted for by the shortfall in ability to recognise revenues from Regulatory Compliance projects as described below.

b) We have a higher revenue base for FY 2010 given the fall in Sterling than we did at the beginning of FY 2009 which is helpful to our revenue outlook. Although Sterling has recovered at the time of writing from a low of US$1.35 to around US$1.64, this range is lower than the average for FY 2009 which was US$1.69.

Recurrent revenue has historically been a high proportion of revenues at Lombard Risk. Recurrent annual revenues for the Group are running at around £4.4m. In addition, the revenue profile remains fairly well dispersed. moving to

profitability...

chairman’s statementcontinued

Full year revenue growth since 2007

27%post acquisition oF lombard risk compliance

Fortis Investments is the autonomous global asset management arm of the Fortis group.

After a rigorous review of the major providers of collateral management, the team determined that Colline was ideally suited to meet Fortis Investment’s requirements.

In addition to improving the timeliness and accuracy of margin calls and full support for disputes, Colline provided:

05Lombard Risk Management plc annual report and accounts 2009

Lombard risk group is weLL positioned to take fuLL advantage of aLL that is needed to enabLe finanicaL institutions manage heir risk and compLiance requirements.

both in functionality, scalability and resilience which now makes COLLINE® a very suitable product for Tier 1 banks with large trading books, as well as for smaller firms. COLLINE® is ahead of budget for this year, and has a large and growing pipeline including opportunities with some of the biggest market participants.

Oberon®, the trading and risk management system, saw the completion of its first installation in China. Oberon® remains our most profitable product and it continues to provide capital to support the development of other products. Functionally the product has made good progress. Support for inflation trades has been much improved which allows inflation based instruments to be managed more effectively in Oberon®. A new yield curve module has been developed

that uses a consistent B‑Spline methodology for all types of curves and allows users a greater degree of control over the smoothness and accuracy of the curves produced. Finally, performance and scalability of Oberon® has been further improved, with particular emphasis on commonly used functions within Oberon® and on Oberon®’s API.

Overall this division earned revenue for the year in excess of £3.85m and a profit of £0.87m after full allocation of group overhead costs.

RegulatoRy and ComplianCe softwaRe pRoduCtsThere are appreciable opportunities now for this part of our business with the move away from light touch regulation generally and, specifically in the UK, the introduction of new regulatory

requirements for Liquidity Reporting and Liquidity Stress Testing. However, during the year, our Regulatory Compliance business underestimated the work effort around the Basel 2 roll‑out programme. This caused both increased costs and delayed revenue recognition on a number of fixed price contracts committed in mid‑2007 which have consequently in some cases been significantly loss‑making. Most of the impact of this has now worked its way through the accounts, and we expect that substantially all the rest will do so in the Group’s current financial year. The Regulatory Compliance business has undergone a reconstruction exercise including a review of management and processes, and the Board now looks forward to the future.

tRading and RisK softwaRe pRoduCts As anticipated this time last year, the credit crisis has been beneficial for our COLLINE® collateral management software product. This product now substantially handles all the key requirements of a collateral business including margining, repo and securities lending, trade reconciliation and inventory management. We secured nine contract wins for COLLINE® in the financial year. These included contracts with Lombard Odier Darier Hentsch & Cie, Jyske Bank A/S, SBAB, Daiwa Securities and SMBC Europe, as well as with a large US East Coast based asset manager and two US hedge funds, and a major contract with a Tier 1 Continental European bank concluded at the end of the financial year. At the same time there has been considerable innovation in the product this year

...major tier 1 bank win

“we are an agile operation that is very customer service driven. we looked for a system that could

offer broad product coverage and selected Lombard risk’s colline® as much for its features as for the company’s collateral management expertise and

excellent reputation within the market.”global head of derivative operations

fortis investments

wideproductcoverageincludingRepo,Energy,SecuritiesLendingandOTCDerivatives.

thefamiliarityofanintuitiveandeasy-to-useweb-basedinterfacetoensure a seamless transition.

ahighlyexperiencedsalesandserviceteam,manyofwhomwereformercollateralmanagerswithakeenunderstandingofcollateralmanagement

_2_LRM_ar09_front.indd 5 28/09/2009 11:37:06

06 Lombard Risk Management plc annual report and accounts 2009

buoyant sales pipeline...

CHaiRman’s statementContinued

The problems described above in UK Regulatory Compliance contracts committed in 2007 do not apply to UK contracts signed more recently, and we had some notable successes during the year with large institutions including Bank of Scotland Treasury Services and a large German bank. In addition, we successfully handled the move by UK, Irish and other regulators to Mandatory Electronic Reporting (“MER”).

Lombard Risk is the market leader for UK Bank Regulatory Reporting with approximately 130 of the 360 banks and foreign branches, and approximately 15 investment firms in the UK using the STB‑ Reporter product for regulatory reporting to the FSA. This depth of customer base clearly gives opportunities to sell additional functionality to existing customers, and we believe this puts us in a very strong position to roll out our solutions for Liquidity Reporting and Liquidity Stress Testing to many of our customers later in this financial year after the final version of the FSA’s new rules

are published in October 2009. We already have considerable activity going on in this area in the UK and a number of early engagements. All the current indications are that there will be more regulation in the next year with appreciable extra focus on liquidity reporting and stress testing.

The firm’s ability to offer global solutions has been greatly enhanced through it now having regulatory offerings available or under production for several EMEA and Asian countries as well as the United States. Our Singapore office has made a number of worthwhile product wins including business in Singapore won away from our main competitor, and we obtained our first two customers for Japanese reporting. In addition, the AML product STB‑Detector has seen more contract wins.

In December 2008 the name of the Regulatory Compliance business changed from STB Systems Ltd to Lombard Risk Compliance Ltd. We have kept the STB name in

the products STB‑Reporter and STB‑Detector but under the unified brand for the whole firm of Lombard Risk.

peRsonnel and pRemisesDuring the year we continued to make new hires appropriate to the expected growth of parts of the business, but we also took cost actions designed to establish profitability in the business as a whole, and to allow us to re‑allocate resources to those parts of the business where we see the best prospects. Costs should continue to be contained overall and to reduce as a percentage of any revenue rises as more work proportionately is done in Shanghai.

After the year end we appointed Keith Butcher as Finance Director of the Group. This is an important appointment for us at a time when the Group has broken through to profitability for COLLINE® and sees appreciable opportunity in the regulatory area. Jane Fineman, who has been our Chief Financial Officer for the last two years will be leaving

us shortly. Our arrangement with her had been a part time one, and Jane was unable to change this to full time which the Board felt it now needed. Our thanks go to her for her work in those two years.

Following the successful fund‑raising concluded at the end of September 2009, and my own shareholding reducing to slightly under 50% for the first time, it is entirely appropriate to move towards splitting the roles of Chairman and Chief Executive. We have announced that these roles will be divided in due course, a move that is welcomed by new investors into the Company.

As part of our cost reduction measures the Board collectively decided to reduce the size of our Non‑executive Board to two, from its four at the start of the year. Ian Peacock and Brian Crowe have remained on the Board, while Christopher Wright and Dan Kochav volunteered to step down in January 2009. In addition Michael Thomas, formerly

oveR

250CustomeRs

20of tHe woRld’s top 50 BanKs

_2_LRM_ar09_front.indd 6 28/09/2009 11:37:06

07Lombard Risk Management plc annual report and accounts 2009

...strengthened governance

than in normal times. Quite apart from the increase in bank regulation there are also a number of “Business as Usual” regulatory software projects in the pipeline, and we are winning contracts especially in Europe and Asia.

The fund‑raising concluded at the end of September 2009 is a very positive move as it will allow the company to operate aggressively in its chosen areas. With a much strengthened balance sheet we also believe this will have commercial advantages to us in an environment where credit risk is still an important issue to many firms.

In this changing environment, the Board continues to believe that as changes in legislation are adopted and credit risk and liquidity management are ever more tightly controlled, risk and regulatory software will be in

demand. Lombard Risk, as the global number 2 in both collateral management software and bank regulatory reporting software, should be well positioned to take advantage of this.

I would like to thank all my colleagues, as well as our advisors, for their hard work and support. Many went the extra mile to win new business and provide good service to our customers, and they deserve my special thanks.

JoHn wisBeyCHaiRman and CHief exeCutive offiCeR24 septemBeR 2009

Chief Executive Officer of STB Systems (renamed Lombard Risk Compliance), has stepped down from the Board. He will remain on the boards of our subsidiaries in Asia. I would like to personally thank all of them for their useful contribution to the Board over several years.

In Shanghai we moved to larger offices in August 2008, having outgrown the previous office. In London we have consolidated our operations into our Curlew Street premises, made possible by a reduced UK headcount. We were not successful in letting out the Earls Court premises, but thankfully the lease expires at the end of September 2009. All residual rent, rates and service charges of the Earls Court lease were provided for in FY 2009, so there will be no further P&L effect in FY 2010. This is a saving of around £0.3m per annum.

pRospeCtsThe Group continues to forecast a buoyant sales pipeline for its COLLINE® collateral management software following the major contract win with a top continental European bank. In addition the Board foresees no end to the increase in bank and securities firm regulation, and is optimistic that this will have a positive effect on the Group’s Regulatory Compliance business. The climate in 2009 is for mandatory spend on bank regulation, and the only issue is what share of this spend the Group can achieve rather than whether it exists. The Board believes that these positive effects well outweigh any residual issues from the 2008 banking crisis and resulting liquidity crunch, although it can be expected that there will continue to be bank mergers and branch closures at a higher rate

china merchants bank is the sixth largest commercial bank by assets in china and is currently among the top 100 banks in the world.

“using stb-reporter from Lombard risk increases our operational transparency and makes

operational control and regulatory reporting easier, faster and ultimately more cost-efficient.

we now have complete ownership over the line-items that we report to our regulators.”

Joseph LoffredoVice President and Chief Financial Officer

china merchants bank, new York

_2_LRM_ar09_front.indd 7 28/09/2009 11:37:07

08 Lombard Risk Management plc annual report and accounts 2009

BoaRd of diReCtoRs

1 2

3 4

_2_LRM_ar09_front.indd 8 28/09/2009 11:37:24

09Lombard Risk Management plc annual report and accounts 2009

1. JoHn wisBey (B.1956) CHaiRman and CHief exeCutive offiCeRJohn Wisbey founded Lombard Risk in 1989, and has led the Company from start‑up, when the only product was Oberon®, to its current international and multi‑product status. He is responsible for the main strategic issues of the Group and plays a major part in the firm’s client relationships. He has also led the Company’s M&A initiatives, including the acquisition of STB Systems, the acquisition and subsequent spin‑out on AIM of what is now IDOX plc, and the sale to Fitch Ratings of the ValuSpread business for £6m. John was Chairman of IDOX plc until 2005 and continued as a non‑executive director until 2008.

Prior to establishing Lombard Risk, John Wisbey was Head of Option Trading and a Director in the Swap Group at Kleinwort Benson Limited. Before that he spent eight years at Kleinwort Benson in the banking division where he acquired his initial experience in the area of credit risk. This period included several years based in Hong Kong and Singapore.

2. KeitH ButCHeR (B.1962) finanCe diReCtoRKeith Butcher is the newest member of the Lombard Risk team, joining in September 2009. He qualified as a Chartered Accountant with KPMG. Prior to Lombard Risk, he was Finance Director of Flomerics Group plc where he managed the successful sale to a NASDAQ listed business for almost triple the pre‑bid valuation. Before that, he was Finance Director at DataCash Group plc during which time the market capitalisation grew from £8m to almost £300m. He previously worked for PriceWaterhouseCoopers and Diagonal plc.

3. ian peaCoCK (B.1947) non‑exeCutive deputy CHaiRmanIan Peacock joined the Board of Lombard Risk in 2000. He is also the Chairman of Mothercare plc, a consultant to the Board of the UK bank C.Hoare & Co (founded in 1672), and Chairman of the Family Mosaic Housing Association. Ian Peacock previously held a number of other senior positions including serving on the Barclays Bank Group Credit Committee, and the Group Board of Kleinwort Benson Group plc as well as Chairman of the Kleinwort Benson Credit Committee. He was also Chairman of Galiform plc from 2000‑2006, a special advisor to the Bank of England from 1998–2000 and was a Non‑executive Director of Norwich and Peterborough Building Society until 2005.

4. BRian CRowe (B.1957) non‑exeCutive diReCtoRBrian Crowe joined the Board of Lombard Risk in 2004 at the time of its IPO on AIM. He was the Chief Executive of Global Banking & Markets at the Royal Bank of Scotland plc (“RBS”) until October 2008. During his tenure at RBS, Brian Crowe was a member of the Group ALCO, Credit and Investment Committees of RBS and a member of the Group Executive Management Committee. He was chairman of the Wholesale Committee of the British Bankers Association from 2006 to 2008, and was a member of the Global Banking Issues Committee of the European Banking Federation (or Fédération Bancaire Européenne) from 2005 to 2008. He was also a member of the City of London EU Strategy Group for 2007/8. Prior to joining RBS, he was Head of Derivatives at Chase Manhattan Bank in London. He is a former Board member of the International Swaps and Derivatives Association (ISDA).

the group is run by its board of directors, which currently has four members including two non-executive directors and meets regularly. the non-executive directors make a valuable contribution by bringing a breadth of business and relevant professional experience to the board. the board has overall responsibility for the group and there is a formal schedule of matters specifically reserved for decision by the board. it is responsible for the overall group strategy, acquisition and divestment policy, approval of major capital expenditure and consideration of significant capital matters.

_2_LRM_ar09_front.indd 9 28/09/2009 11:37:24

10 Lombard Risk Management plc annual report and accounts 2009

lomBaRd RisK’s management team

_2_LRM_ar09_front.indd 10 28/09/2009 11:37:25

11Lombard Risk Management plc annual report and accounts 2009

Lombard risk’s management team has been constructed from experts in their respective fields. Many have banking backgrounds and have used risk management and regulatory software in previous roles, giving them first hand knowledge of customer needs and desires.

these individuals’ skills and experience have been brought together to create a team that now has the ability to respond to and anticipate customer requirements. this gives considerable market advantage when competing for business and delivering to plan.

_2_LRM_ar09_front.indd 11 28/09/2009 11:37:25

12 Lombard Risk Management plc annual report and accounts 2009

Directors’ report For the year enDeD 31 March 2009

The Directors submit their Annual Report together with the consolidated financial statements for the year ended 31 March 2009.

Directors’ responsibilitiesThe Directors are responsible for preparing the Annual Report and the financial statements in accordance with applicable law and regulations.

Company law requires the Directors to prepare financial statements for each financial year. Under that law the Directors have prepared consolidated financial statements in accordance with International Financial Reporting Standards (“IFRS”) as adopted by the European Union, and Parent Company financial statements in accordance with UK Generally Accepted Accounting Practice (“UK GAAP”). The financial statements are required by law to give a true and fair view of the state of affairs of the Group and the Company and of the profit or loss of the Group for that period. In preparing these financial statements, the Directors are required to:

select suitable accounting policies and then apply them consistently;

make judgments and estimates that are reasonable and prudent;

state whether applicable IFRS and UK GAAP have been followed, subject to any material departures disclosed and explained in the financial statements; and

prepare the financial statements on the going concern basis unless it is inappropriate to presume that the Company will continue in business.

The Directors are responsible for keeping proper accounting records that disclose with reasonable accuracy at any time the financial position of the Company and enable them to ensure that the financial statements comply with the Companies Act 1985. They are also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for the prevention and detection of fraud and other irregularities.

In so far as each of the Directors is aware:

there is no relevant audit information of which the Company’s auditors are unaware; and

the Directors have taken all steps that they ought to have taken to make themselves aware of any relevant audit information and to establish that the auditors are aware of that information.

The Directors are responsible for the maintenance and integrity of the corporate and financial information included on the Company’s website. Legislation in the United Kingdom governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

principal activities anD business reviewThe Company is a holding company. The principal activities of the Group are the provision of trading, valuation and risk management systems and regulatory, anti money laundering and compliance systems to the financial markets. A review of these activities, future developments and financial risk management is provided in the Chairman’s statement and note 14 Financial risk management. This information forms a part of the Directors’ report.

results anD DiviDenDsThe audited financial statements for the year ended 31 March 2009 are set out on pages 18 to 21. The Group’s loss for the year after taxation amounted to £1,098,937 (2008: loss £672,895). The Directors do not propose a dividend for the year (2008: £Nil).

Directors anD their interestsThe Directors who served during the year and their beneficial interests in the Company’s ordinary share capital were as follows: 31 March 2009 31 March 2008 number Number

John Wisbey1 81,889,562 81,324,562Ian Peacock 1,088,532 1,088,532Brian Crowe 625,000 625,000Michael Thomas (resigned from Board 1 July 2009) 4,958,360 4,958,360Dan Kochav (resigned from Board 31 January 2009) 375,000 375,000Christopher Wright (resigned from Board 31 January 2009) 1,205,066 1,205,0661 77,939,562 shares are owned directly. In addition John Wisbey is a beneficiary of Advanced Technology Trust which owns a further 3,950,000 shares.

In addition to these shareholdings listed above, the Directors have been granted options over ordinary shares.

In accordance with the Articles of Association, John Wisbey is due to retire at the forthcoming Annual General Meeting and, being eligible, will offer himself for re‑election.

charitable anD political DonationsThe Group made no charitable donations in the year (2008: £Nil) and no political donations (2008: £Nil).

payMent oF creDitorsIt is the Group’s practice to agree credit terms with all suppliers and to pay all approved invoices within these agreed terms. The average trade creditor days for the year was 75 days (2008: 71 days).

_1_LRM_ar09_back.indd 1 28/09/2009 11:36:37

13Lombard Risk Management plc annual report and accounts 2009

substantial shareholDingsAs at 31 March 2009 the Company was aware of the following interests in 3% or more of its issued share capital: Number of shares % holding

John Wisbey 81,889,562 60.13AMF (NBF) Holdings Inc. 12,222,222 8.98Merifin Capital NV 7,525,264 5.53Royal Bank Ventures Investments Ltd 5,536,990 4.07Michael Thomas 4,958,360 3.64Anthony Brown 4,808,360 3.53

research anD DevelopMentResearch and development expenditure incurred on the Group’s suite of products has all been expensed to the income statement in the relevant period.

post balance sheet eventsThe Company entered into additional Director loans from Brian Crowe, Non‑executive Director, for £200,000 and a further £100,000 from John Wisbey, Chairman and Chief Executive Officer. These funds have been used to provide the Company with additional working capital. This raised the overall total of Director loans (the “Loans”) to £1,600,000 (excluding the £30,000 loan from Michael Thomas who was a director at year end but stood down in July 2009). The Loans, which bear interest at 1% per month, are on a demand basis from the point of view of the lenders and repayable at any time at the Company’s option.

On 23 September 2009 the Company concluded a fund‑raising in which, subject to EGM approval and the meeting of various placing conditions, it will raise £1,800,000 of new money (before expenses) in a placing from institutional investors and other shareholders. At the same time as completion of the placing, there will be conversions of director loans into equity by John Wisbey in the amount of £790,000, £200,000 by Brian Crowe, £10,000 by Ian Peacock and £30,000 by a former director Michael Thomas. There will also be a repayment of the remaining £600,000 of director loans. The proceeds of the fund‑raising are being used partly to strengthen the Company’s balance sheet and partly to repay in their entirety, the director loans not converted into equity.

As a result of these events the Company will, on completion of the placing, have no external debt including debt due to Directors.

going concernThe financial statements have, as in previous years, been prepared on a going concern basis. The Directors have formally considered this issue in the light of the operating losses and the consequent operating cash outflows in the period.

In forming an opinion that the Company and the Group are going concerns, the Directors have taken into account the Group’s strong sales pipeline helped by its contract win earlier this year with a Tier 1 bank for collateral management, the opportunity in the regulatory space for UK Liquidity Reporting in the next year, the fund‑raising of £1,800,000 concluded at the end of September 2009, subject to EGM approval and the meeting of various placing conditions (expected to complete in October 2009), and the simultaneous capitalisation of £1,030,000 of loans from directors and a former director and the elimination of all debt from the balance sheet.

The Directors have prepared cashflow forecasts for the period to 31 March 2011. Within these forecasts certain assumptions have been made over the timing of revenues and costs and take into account the £1,800,000 fundraising concluded at the end of September 2009.

The forecasts show that the Company and Group have sufficient facilities for ongoing operations. Whilst there will always remain some inherent uncertainty within the aforementioned cashflow, the Directors believe the Company and Group have sufficient resources to continue in operational existence for at least twelve months from the date of approval of these financial statements.

Accordingly the Directors continue to adopt the going concern basis in preparing the financial statements for the year ended 31 March 2009.

auDitorsA resolution to re‑appoint Grant Thornton UK LLP as auditors and to authorise the Directors to agree their remuneration will be placed before the forthcoming Annual General Meeting of the Company.

On behalf of the Board

John wisbeyDirector

registereD oFFiceIndia House 45 Curlew Street London SE1 2ND

24 septeMber 2009

_1_LRM_ar09_back.indd 2 28/09/2009 11:36:37

14 Lombard Risk Management plc annual report and accounts 2009

corporate governance report For the year enDeD 31 March 2009

policy stateMentThe Board is committed to high standards of integrity and Corporate Governance, consistently seeking to apply the principles set out in the Combined Code (“the Code”) although recognising that as an AIM company the Company is not required to comply with the provisions of the Code and, largely because of its size, does not comply with a number of them. This statement, together with the Directors’ report and the Report of the Board to shareholders on Directors’ remuneration, explains how the Group has applied the principles set out in the Code.

internal controlsThe Directors are responsible for the systems of internal control. Although no system of internal control can provide absolute assurance against material misstatement or loss, the Group’s systems are designed to provide the Directors with reasonable assurance that problems are identified on a timely basis and dealt with appropriately. The Board considers that there have been no substantial weaknesses in internal financial controls resulting in any material losses, contingencies or uncertainties, and thus disclosable in the accounts. The Board has considered the need for an internal audit function and has concluded that there is no current need for such a function within the Company.

accounting policiesThe Board considers the appropriateness of its accounting policies on an annual basis. The Board believes that its accounting policies and estimation techniques are appropriate in particular in relation to income recognition, research and development and deferred expenses.

boarD oF DirectorsThe Board, comprising an Executive Chairman, one Executive Director and two Non‑executive Directors, is responsible for the overall strategy and direction of Lombard Risk Management plc as well as for approving potential acquisitions, major capital expenditure items and financing matters. The Board has a formal schedule of business reserved to it and meets regularly during the year. Advice from independent sources is available if required. The Board monitors exposure to key business risks, reviews the strategic direction of the Company, the annual budgets and progress against those budgets.

The Board members and their roles are described on page 9. The Executive Directors have service contracts, which are terminable upon periods between three and twelve months’ notice. In accordance with the Company’s Articles of Association, one third of the Directors are required to retire by rotation at the Annual General Meeting.

shareholDer relationsThe Company recognises the importance of dialogue with all of its shareholders. The Annual General Meeting is an opportunity to communicate with institutional and other shareholders. Additional information is supplied through the circulation of the interim report and the Annual Report and accounts. Lombard Risk Management plc maintains up to date information on the investor section of its website www.lombardrisk.com.

Every shareholder receives a full Annual Report after each year end and has access to an interim report online after each half year end. Care is taken to ensure that any price sensitive information is released to all its shareholders, institutional and private, at the same time in accordance with London Stock Exchange requirements.

auDit coMMitteeThe Audit Committee is a committee of the Board chaired by Ian Peacock and also comprises Brian Crowe and John Wisbey. The Report of the Audit Committee can be found on page 15.

reMuneration coMMitteeThe Remuneration Committee is chaired by Brian Crowe and also comprises Ian Peacock and John Wisbey. The committee reviews the remuneration structures and performance of the Executive Directors and reviews the remuneration policy for senior management. The Remuneration Committee meets as and when necessary and has access to professional advice from inside and outside the Company. No Executive Director may participate in decisions regarding his own remuneration. The Board as a whole determines the remuneration arrangements of the Non‑executive Directors.

_1_LRM_ar09_back.indd 3 28/09/2009 11:36:37

15Lombard Risk Management plc annual report and accounts 2009

report oF the auDit coMMittee For the year enDeD 31 March 2009

MeMbership anD Meetings oF the auDit coMMitteeThe Audit Committee is a committee of the Board and the majority is composed of Non‑executive Directors, whom the Board considers to be independent. The Audit Committee invites the Executive Directors and other senior managers to attend its meetings as appropriate.

During the year the Audit Committee was chaired by Christopher Wright and also Ian Peacock, who adopted this role from 1st February 2009. John Wisbey remained a committee member, while Brian Crowe became a member on 1 February 2009. The Audit Committee is considered to have sufficient, recent and relevant financial experience to discharge its functions. The Audit Committee invites others, including the external auditors, to attend its meetings as appropriate.

During the period under review, the Audit Committee met four times.

role, responsibilities anD terMs oF reFerenceThe Audit Committee’s role is to assist the Board in the effective discharge of its responsibilities for financial reporting and internal control.

The Audit Committee’s responsibilities include:

reviewing the integrity of the annual and interim financial statements of the Group ensuring they comply with legal requirements, accounting standards and the AIM rules, and any other formal announcements relating to the Group’s financial performance;

reviewing the Group’s internal financial control and risk management systems;

monitoring and reviewing the requirement for an internal audit function; and

overseeing the relationship with the external auditors, including approval of their remuneration, reviewing the scope of the audit engagement, assessing their independence, monitoring the provision of non‑audit services, and considering their reports on the Group’s financial statements.

inDepenDence oF external auDitorsThe Audit Committee keeps under review the relationship with the external auditors including:

the independence and objectivity of the external auditors, taking into account the relevant UK professional and regulatory requirements and the relationship with the auditors as a whole, including the provision of non‑audit services;

recommending to the Board and shareholders the re‑appointment or otherwise of the external auditors for the following financial period; and

the consideration of audit fees and any fees for non‑audit services.

The Audit Committee develops and recommends to the Board the Company’s policy in relation to the provision of non‑audit services by the auditors, and ensures that the provision of such services does not impair the external auditor independence.

ian peacockchairMan oF the auDit coMMittee24 septeMber 2009

_1_LRM_ar09_back.indd 4 28/09/2009 11:36:38

16 Lombard Risk Management plc annual report and accounts 2009

consoliDateD Financial stateMentsFor the year enDeD 31 March 2009

17 report oF the inDepenDent auDitor – consoliDateD Financial stateMents 18 consoliDateD incoMe stateMent 19 consoliDateD balance sheet 20 consoliDateD stateMent oF changes in shareholDers’ equity 21 consoliDateD cash Flow stateMent 22 notes to the consoliDateD Financial stateMents

_1_LRM_ar09_back.indd 5 28/09/2009 11:36:38

17Lombard Risk Management plc annual report and accounts 2009

report oF the inDepenDent auDitorconsoliDateD Financial stateMents

to the shareholDers oF loMbarD risk ManageMent plcWe have audited the Consolidated financial statements (the “financial statements”) of Lombard Risk Management plc for the year ended 31 March 2009 which comprise the accounting policies, the consolidated income statement, the consolidated balance sheet, the consolidated statement of changes in shareholders’ equity, the consolidated cash flow statement and notes 1 to 22. These financial statements have been prepared under the accounting policies set out therein.

We have reported separately on the Parent Company financial statements of Lombard Risk Management plc for the year ended 31 March 2009.

This report is made solely to the Company’s members, as a body, in accordance with Section 235 of the Companies Act 1985. Our audit work has been undertaken so that we might state to the Company’s members those matters we are required to state to them in an auditors’ report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body for our audit work, for this report or for the opinions we have formed.

respective responsibilities oF Directors anD auDitorThe Directors’ responsibilities for preparing the Annual Report and the Consolidated financial statements in accordance with United Kingdom Law and International Financial Reporting Standards (“IFRS”) as adopted by the European Union are set out in the Statement of Directors’ responsibilities.

Our responsibility is to audit the financial statements in accordance with relevant legal and regulatory requirements and International Standards on Auditing (UK and Ireland).

We report to you our opinion as to whether the Consolidated financial statements give a true and fair view and whether the financial statements have been properly prepared in accordance with the Companies Act 1985. We also report to you whether in our opinion the information given in the Directors’ report is consistent with the financial statements. The information given in the Directors’ report includes that specific information presented in the Chairman’s statement and the Corporate governance report that is cross referred from the Business review section of the Directors’ report.

In addition we report to you if, in our opinion, the Company has not kept proper accounting records, if we have not received all the information and explanations we require for our audit, or if information specified by law regarding Directors’ remuneration and other transactions is not disclosed.

We read other information contained in the Annual Report and consider whether it is consistent with the audited financial statements. The other information comprises only the Highlights, the Chairman’s Statement, the Board of Directors, the Directors’ report, the Corporate governance report and the Report of the Audit Committee. We consider the implications for our report if we become aware of any apparent misstatements or material inconsistencies with the financial statements. Our responsibilities do not extend to any other information.

basis oF auDit opinionWe conducted our audit in accordance with International Standards on Auditing (UK and Ireland) issued by the Auditing Practices Board. An audit includes examination, on a test basis, of evidence relevant to the amounts and disclosures in the Consolidated financial statements. It also includes an assessment of the significant estimates and judgments made by the Directors in the preparation of the Consolidated financial statements and of whether the accounting policies are appropriate to the Group’s circumstances, consistently applied and adequately disclosed.

We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in order to provide us with sufficient evidence to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or other irregularity or error. In forming our opinion we also evaluated the overall adequacy of the presentation of information in the Consolidated financial statements.

opinionIn our opinion:

the Consolidated financial statements give a true and fair view, in accordance with IFRS as adopted by the European Union, of the state of the Group’s affairs as at 31 March 2009 and of the Group’s loss for the year then ended;

the Consolidated financial statements have been properly prepared in accordance with the Companies Act 1985; and

the information given in the Directors’ report is consistent with the financial statements.

grant thornton uk llpregistereD auDitor, chartereD accountantslonDon24 septeMber 2009

_1_LRM_ar09_back.indd 6 28/09/2009 11:36:38

18 Lombard Risk Management plc annual report and accounts 2009

consoliDateD incoMe stateMent For the year enDeD 31 March 2009

year ended Year ended 31 March 2009 31 March 2008 Note £ £

Continuing operations

Revenue 2 8,694,450 8,460,594

Cost of sales (43,936) (52,897)

Gross profit 2 8,650,514 8,407,697

Administrative expenses (9,769,510) (9,458,899)

(Loss) from operations 4 (1,118,996) (1,051,202)

(Loss) on disposal of quoted investment — (40,788)

Finance expense 5 (139,736) (35,218)

Finance income 6 5,000 10,652

(Loss) before taxation (1,253,732) (1,116,556)

Taxation 7 96,074 150,000

(Loss) for the year from continuing operations (1,157,658) (966,556)

Profit for the year from discontinued activities 8 58,721 293,661

(Loss) for the year (1,098,937) (672,895)

(Loss) per share

Basic (pence) 9 (0.81) (0.50)

Diluted (pence) 9 (0.81) (0.50)

(Loss) per share on continuing activities

Basic (pence) 9 (0.85) (0.71)

Diluted (pence) 9 (0.85) (0.71)

Earnings per share on discontinued activities

Basic (pence) 9 0.04 0.22

Diluted (pence) 9 0.04 0.22

The accompanying accounting policies and notes form an integral part of the financial statements.

_1_LRM_ar09_back.indd 7 28/09/2009 11:36:38

19Lombard Risk Management plc annual report and accounts 2009

consoliDateD balance sheet as at 31 March 2009

as at As at 31 March 2009 31 March 2008 Note £ £

Non‑current assets

Property, plant and equipment 10 239,798 143,995

Goodwill 11 3,632,680 3,632,680

Other intangible assets 11 11,441 4,319

3,883,919 3,780,994

Current assets

Trade and other receivables 12 2,842,226 2,320,672

Cash and cash equivalents 150,999 494,894

2,993,225 2,815,566

Total assets 6,877,144 6,596,560

Current liabilities

Trade and other payables 13 (3,847,208) (2,406,181)

Provisions 15 (137,664) (146,794)

Deferred income (2,580,502) (2,690,195)

(6,565,374) (5,243,170)

Total liabilities (6,565,374) (5,243,170)

Net assets 311,770 1,353,390

Equity

Share capital 16 1,110,715 1,108,510

Share premium account 2,512,904 2,490,110

Foreign exchange reserves (9,136) (30,208)

Other reserves 1,649,152 1,637,906

Profit and loss account (4,951,865) (3,852,928)

Total equity 311,770 1,353,390

The financial statements were approved by the Board on 24 September 2009 and signed on its behalf by:

John wisbeychairMan anD chieF executive oFFicer

The accompanying accounting policies and notes form an integral part of the financial statements.

_1_LRM_ar09_back.indd 8 28/09/2009 11:36:39

20 Lombard Risk Management plc annual report and accounts 2009

consoliDateD stateMent oF changes in shareholDers’ equityFor the year enDeD 31 March 2009 Share Foreign Profitand share premium exchange other loss total capital account reserves reserves account equity £ £ £ £ £ £

Balance at 1 April 2008 1,108,510 2,490,110 (30,208) 1,637,906 (3,852,928) 1,353,390

Foreign exchange movements on consolidation of foreign operations — — 21,072 — — 21,072

Income and expense recognised directly in equity — — 21,072 — — 21,072

Loss for the year — — — — (1,098,937) (1,098,937)

Total recognised income and expense for the year — — 21,072 — (1,098,937) (1,077,865)

441,176 new ordinary shares issued 2,205 22,794 — — — 24,999

Share‑based payment charge — — — 11,246 — 11,246

Balance at 31 March 2009 1,110,715 2,512,904 (9,136) 1,649,152 (4,951,865) 311,770

Share Foreign Profitand Share premium exchange Other loss Total capital account reserves reserves account equity £ £ £ £ £ £

Balance at 1 April 2007 1,103,510 2,415,110 (4,196) 1,597,295 (3,180,033) 1,931,686

Foreign exchange movements on consolidation of foreign operations — — (26,012) — — (26,012)

Income and expense recognised directly in equity — — (26,012) — — (26,012)

Loss for the year — — — — (672,895) (672,895)

Total recognised income and expense for the year — — (26,012) — (672,895) (698,907)

1,000,000 new ordinary shares issued 5,000 75,000 — — — 80,000

Share‑based payment charge — — — 40,611 — 40,611

Balance at 31 March 2008 1,108,510 2,490,110 (30,208) 1,637,906 (3,852,928) 1,353,390

Other reserves relate to negative goodwill arising on the acquisition of a subsidiary undertaking prior to 1 April 1997 and the merger reserve.

_1_LRM_ar09_back.indd 9 28/09/2009 11:36:39

21Lombard Risk Management plc annual report and accounts 2009

consoliDateD cash Flow stateMent For the year enDeD 31 March 2009

year ended Year ended 31 March 2009 31 March 2008 £ £

Cash flows from operating activities

Loss for the period excluding discontinued operations (1,157,658) (966,556)

Tax credit (96,074) (150,000)

Finance income (5,000) (10,652)

Finance expense 139,736 35,218

Loss on disposal of quoted investment — 40,788

Operating loss (1,118,996) (1,051,202)

Profit on discontinued activities (58,721) (353,328)

Adjustments for:

Depreciation 157,032 193,908

Amortisation 13,451 20,315

Share‑based payment charge 11,246 40,611

Provision for onerous lease (9,130) 146,794

Increase in trade and other receivables (521,554) (874,248)

Increase in trade and other payables 683,059 296,170

(Decrease)/increase in deferred income (109,693) 180,982

Cash used in operations (953,306) (1,399,998)

Tax credit received 96,074 150,000

Net cash outflow from operating activities (857,232) (1,249,998)

Cash flows from investing activities

Purchase of property, plant and equipment (235,151) (112,945)

Purchase of intangible fixed assets (20,496) (10,195)

Proceeds from sale of IVRS 58,721 691,058

Disposal of IDOX shares — 407,212

Net cash generated by/(used in) investing activities (196,926) 975,130

Cash flows from financing activities

Loans from Directors 820,000 660,000

Repayment of Directors’ loan — (150,000)

Shares issued 24,999 —

Interest received 5,000 10,652

Interest paid (139,736) (35,218)

Net cash generated by financing activities 710,263 485,434

Net (decrease)/increase in cash and cash equivalents (343,895) 210,566

Cash and cash equivalents at beginning of period 494,894 284,328

Cash and cash equivalents at end of period 150,999 494,894

_1_LRM_ar09_back.indd 10 28/09/2009 11:36:39

22 Lombard Risk Management plc annual report and accounts 2009

notes to the consoliDateD Financial stateMents For the year enDeD 31 March 2009

1. accounting policies(a) basis oF preparationThese consolidated financial statements are for the year ended 31 March 2009. They have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and International Financial Reporting Interpretation Committee (“IFRIC”) interpretations as at 31 March 2009, as adopted by the European Union. They have been prepared under the historical cost convention.

The preparation of financial statements under IFRS requires the Board to make judgments, estimates and assumptions that affect the application of accounting policies, the reported amounts of balance sheet items at the period end and the reported amount of revenue and expense during the reporting period. The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances, the results of which form the basis of making judgments that are not readily apparent from other sources. However, the actual results may differ from these estimates. The estimates and underlying assumptions are reviewed on an on‑going basis.

New standards and interpretations currently in issue but not effective for accounting periods commencing on 1 April 2008 are:

a. IAS 1 “Presentation of Financial Statements” (revised 2007)

b. IAS 23 “Borrowing Costs” (revised 2007)

c. Amendment to IAS 32 “Financial Instruments: Presentation” and IAS 1 “Presentation of Financial Statements – Puttable Financial Instruments and Obligations Arising on Liquidation”

d. IAS 27 “Consolidated and Separate Financial Statements” (Revised 2008)

e. Amendment to IFRS 2 “Share‑based Payment – Vesting Conditions and Cancellations”

f. Amendments to IFRS 1 “First‑time Adoption of International Financial Reporting Standards” and IAS 27 “Consolidated and Separate Financial Statements – Costs of Investment in a Subsidiary, Jointly Controlled Entity or Associate”

g. Amendment to IAS 39 “Financial Instruments: Recognition and Measurement – Eligible Hedged Items”

h. “Group Cash‑settled Share‑based Payment Transactions” – Amendment to IFRS 2

i. Amendment to IFRS 7 “Financial Instruments: Disclosures – Improving Disclosures About Financial Instruments”

j. “Embedded Derivatives” – Amendments to IAS 39 and IFRIC 9

k. Improvements to IFRSs 2008

l. Improvements to IFRSs 2009

m. IFRS 3 “Business Combinations” (Revised 2008)

n. IFRS 8 “Operating Segments”

o. IFRIC 13 “Customer Loyalty Programmes”

p. IFRIC 15 “Agreements for the Construction of Real Estate”

q. IFRIC 16 “Hedges of a Net Investment in a Foreign Operation”

r. IFRIC 17 “Distributions of Non‑cash Assets to Owners”

s. IFRIC 18 “Transfers of Assets from Customers”

The Directors do not believe that the implementation of these standards will have a material effect on the reported results.

(b) basis oF consoliDationThe Group accounts consolidate the financial statements of the Parent Company (Lombard Risk Management plc) and its subsidiary undertakings over which it has full control (see note 5 to the Parent Company balance sheet). A description of the principal activities and operations of the Group can be found in the Director’s Report on pages 12 and 13.

The consolidated financial statements include the financial statements of the Company and its subsidiary undertakings made up to 31 March 2009. The acquisition method of accounting has been adopted. Under this method, the results of subsidiary undertakings acquired or disposed of in the year are included in the consolidated income statement from the date of acquisition or up to the date of disposal. All of the Group’s assets and liabilities existing at the date of acquisition are recorded at their fair values reflecting their condition at that date. Profits or losses on intra‑group transactions are eliminated in full. Goodwill arising on consolidation was written off to reserves prior to 1 April 1999. Goodwill arising after this date is capitalised and under IFRS 3 goodwill is not amortised, but an impairment test is performed as appropriate, but at least annually. The value of goodwill is to be written down according to the outcome of the impairment test.

_1_LRM_ar09_back.indd 11 28/09/2009 11:36:39

23Lombard Risk Management plc annual report and accounts 2009

(c) going concernThe financial statements have, as in previous years, been prepared on a going concern basis. The Directors have formally considered this issue in the light of the operating losses and the consequent operating cash outflows in the period.

In forming an opinion that the Company and the Group are going concerns, the Directors have taken into account the Group’s strong sales pipeline helped by its contract win earlier this year with a Tier 1 bank for collateral management, the opportunity in the regulatory space for UK Liquidity Reporting in the next year, the fund‑raising of £1,800,000 concluded at the end of September 2009, subject to EGM approval and the meeting of various placing conditions (expected to complete in October 2009), and the simultaneous capitalisation of £1,030,000 of loans from directors and a former director and the elimination of all debt from the balance sheet.

The Directors have prepared cashflow forecasts for the period to 31 March 2011. Within these forecasts certain assumptions have been made over the timing of revenues and costs and take into account the £1,800,000 fundraising concluded at the end of September 2009.

The forecasts show that the Company and Group have sufficient facilities for ongoing operations. Whilst there will always remain some inherent uncertainty within the aforementioned cashflow, the Directors believe the Company and Group have sufficient resources to continue in operational existence for at least twelve months from the date of approval of these financial statements.

Accordingly the Directors continue to adopt the going concern basis in preparing the financial statements for the year ended 31 March 2009.

(d) revenueRevenue represents the value of goods sold and services provided during the year, stated net of Value Added Tax. Revenue and pre‑tax profit are wholly attributable to the principal activities of the Group.

The recognition of revenue depends on the type of income:

Licence income For long‑term projects which do not include the up‑front delivery of immediately usable software, revenue is recognised on both the consultancy and initial licence elements in line with the estimated percentage of completion of the project. That part of licence and maintenance revenue invoiced simultaneously with the initial licence but considered to relate to the period when the licence is deemed to be live is deferred in its entirety until the live date, following which it is released to profit in equal daily instalments over the duration of the relevant licence or maintenance. For other projects which do include the up‑front delivery of immediately usable software, revenue is recognised in accordance with the invoicing schedule, on a percentage completion basis. For non‑refundable licences revenue is recognised in full on customer acceptance.

Customisation income Recognised once the customisation has taken place.

Maintenance income Recognised evenly over the term of the maintenance contract.

Rental income Recognised evenly over the term of the rental contract.

Data subscription income Recognised evenly over the term of the data contract.

Training income Recognised when the relevant courses are run.

(e) property, plant anD equipMentProperty, plant and equipment are stated at cost, net of depreciation and any provision for impairment. No depreciation is charged during the period of construction. Leasehold property is included in property, plant and equipment only where it is held under a finance lease.

The cost of computer hardware, fixtures, fittings and equipment, is written down to the residual value and is depreciated in equal annual instalments over the estimated useful lives of the assets. The residual values of assets or groups of like assets and their useful lives are reviewed annually.

The estimated useful lives of the assets are as follows:

Computer hardware two years Fixtures, fittings and equipment four years

(f) gooDwillGoodwill, representing the excess of the cost of acquisition over the fair value of the Group’s share of the identifiable net assets acquired, is capitalised and reviewed annually for impairment. Goodwill is carried at cost less accumulated impairment losses. Negative goodwill is recognised immediately after acquisition in the Income statement.

(g) intangible assetsresearch anD DevelopMentExpenditure on research is recognised as an expense in the period in which it is incurred.

Development costs incurred are capitalised when all the following conditions are satisfied:

completion of the intangible asset is technically feasible so that it will be available for use or sale;

the Group intends to complete the intangible asset and use or sell it;

the Group has the ability to use or sell the intangible asset;

the intangible asset will generate probable future economic benefits. Among other things, this requires that there is a market for the output from the intangible asset or for the intangible asset itself, or, if it is to be used internally, the asset will be used in generating such benefits;

there are adequate technical, financial and other resources to complete the development and to use or sell the intangible asset; and

the expenditure attributable to the intangible asset during its development can be measured reliably.

Development costs not meeting the criteria for capitalisation are expensed as incurred.

_1_LRM_ar09_back.indd 12 28/09/2009 11:36:39

24 Lombard Risk Management plc annual report and accounts 2009

notes to the consoliDateD Financial stateMents continueDFor the year enDeD 31 March 2009

1. accounting policies continueD(g) intangible assets continueDcoMputer soFtwareThe cost of computer software, net of estimated residual value and impairment, is depreciated in equal annual instalments over one to two years based on the estimated useful lives of the assets. The residual values of assets or group of like assets are reviewed annually.

(h) Financial instruMentsFinancial assets and liabilities are recognised on the Group’s balance sheet when the Group becomes a party to the contractual provisions of the instrument. The Group’s financial instruments comprise cash, trade receivables and trade and other payables. Derivative instruments are not used by the Group and the Group does not enter into speculative derivative contracts.

loans anD receivablesLoans and receivables are stated at their fair value plus transaction costs, then subsequently at amortised cost using the effective interest method, if applicable, less impairment losses. Provisions against trade receivables are made when there is objective evidence that the Group will not be able to collect all amounts due to it in accordance with the original terms of those receivables. The amount of the write‑down is determined as the difference between the assets carrying amount and the present value of the estimated future cash flows.

cash anD cash equivalentsThe Group manages short‑term liquidity through the holding of cash and highly liquid interest bearing deposits. Only deposits that are readily convertible into cash, with no penalty of lost interest, are shown as cash or cash equivalent.

traDe payablesFinancial liabilities are obligations to pay cash or other financial assets and are recognised when the Group becomes a party to the contractual provisions of the instrument. Financial liabilities categorised as at fair value through profit or loss are recorded initially at fair value; all transaction costs are recognised immediately in the income statement. All other financial liabilities are recorded initially at fair value, net of direct issue costs.

Financial liabilities categorised as at fair value through profit or loss are re‑measured at each reporting date at fair value, with changes in fair value being recognised in the income statement. All other financial liabilities are recorded at amortised cost using the effective interest method, with interest‑related charges recognised as an expense in finance cost in the Income statement.

A financial liability is derecognised only when the obligation is extinguished, that is, when the obligation is discharged or cancelled or expires.

(i) Foreign exchangeTransactions in foreign currencies are translated at the exchange rate ruling at the date of the transaction. Monetary assets and liabilities in foreign currencies are translated at the rates of exchange ruling at the balance sheet date. Non‑monetary items that are measured at historical cost in a foreign currency are translated at the exchange rate at the date of the transaction. Non‑monetary items that are measured at fair value in a foreign currency are translated using the exchange rates at the date when the fair value was determined.

Any exchange differences arising on the settlement of monetary items or on translating monetary items at rates different from those at which they were initially recorded are recognised in the profit or loss in the period in which they arise. Exchange differences on non‑monetary items are recognised in the statement of recognised income and expenses to the extent that they relate to a gain or loss on that non‑monetary item taken to the statement of recognised income and expenses, otherwise such gains and losses are recognised in the income statement.

The assets and liabilities in the financial statements of foreign subsidiaries are translated at the rate of exchange ruling at the balance sheet date. Income and expenses are translated at the actual rate at the date of transaction. The exchange differences arising from the retranslation of the opening net investment in subsidiaries are taken directly to the “Foreign exchange reserve” in equity. On disposal of a foreign operation the cumulative translation differences (including, if applicable, gains and losses on related hedges) are transferred to the income statement as part of the gain or loss on disposal.

(j) taxationCurrent tax is the tax currently payable based on taxable profit for the year. The tax credit arises from the UK legislation regarding the treatment of certain qualifying research and development costs, allowing for the surrender of tax losses attributable to such costs in return for a tax rebate.

Deferred income taxes are calculated using the liability method on temporary differences. Deferred tax is generally provided on the difference between the carrying amounts of assets and liabilities and their tax bases. However, deferred tax is not provided on the initial recognition of goodwill, nor on the initial recognition of an asset or liability unless the related transaction is a business combination or affects tax or accounting profit. Deferred tax on temporary differences associated with shares in subsidiaries and joint ventures is not provided if reversal of these temporary differences can be controlled by the Group and it is probable that reversal will not occur in the foreseeable future. In addition, tax losses available to be carried forward as well as other income tax credits to the Group are assessed for recognition as deferred tax assets.

Deferred tax liabilities are provided in full, with no discounting. Deferred tax assets are recognised to the extent that it is probable that the underlying deductible temporary differences will be able to be offset against future taxable income. Current and deferred tax assets and liabilities are calculated at tax rates that are expected to apply to their respective period of realisation, provided they are enacted or substantively enacted at the balance sheet date.

Changes in deferred tax assets or liabilities are recognised as a component of tax expense in the income statement, except where they relate to items that are charged or credited directly to equity (such as the revaluation of land) in which case the related deferred tax is also charged or credited directly to equity.

_1_LRM_ar09_back.indd 13 28/09/2009 11:36:39

25Lombard Risk Management plc annual report and accounts 2009

(k) leaseD assetsThe Group does not hold any finance leases.

All leases referred to are regarded as operating leases and the payments made under them are charged to the income statement on a straight line basis over the lease term. Lease incentives are spread over the term of the lease.

Where leased buildings are vacated or under‑utilised a provision is made for the loss of benefit over the remainder of the lease.

(l) pension costsThe Group operates a number of defined contribution pension schemes. The assets of the schemes are held separately from those of the Group in independently administered funds. The amount charged to the income statement represents the contributions payable to the schemes in respect of the accounting period.

(m) share options issueD to eMployeesAll share‑based payment arrangements granted after 7 November 2002 that had not vested prior to 1 April 2006 are recognised in the financial statements.

All goods and services received in exchange for the grant of any share‑based payment are measured at their fair values. Where employees are rewarded using share‑based payments, the fair values of employees’ services are determined indirectly by reference to the fair value of the instrument granted to the employee. This fair value is appraised at the grant date using a Binomial model, taking into account the terms and conditions upon which the options were granted.

All equity‑settled share‑based payments are ultimately recognised as an expense in the income statement with a corresponding credit to “other reserves”.

If vesting periods or other non‑market vesting conditions apply, the expense is allocated over the vesting period, based on the best available estimate of the number of share options expected to vest. Estimates are subsequently revised if there is any indication that the number of share options expected to vest differs from previous estimates. Any cumulative adjustment prior to vesting is recognised in the current period. No adjustment is made to any expense recognised in prior periods if share options ultimately exercised are different to that estimated on vesting.

Upon exercise of share options the proceeds received net of attributable transaction costs are credited to share capital, and where appropriate, share premium.

(n) iMpairMent testing oF gooDwill, other intangible assets anD property, plant anD equipMentFor the purposes of assessing impairment, assets are grouped at the lowest levels for which there are separately identifiable cash flows (cash‑generating units). As a result, some assets are tested individually for impairment and some are tested at cash‑generating unit level. Goodwill is allocated to those cash‑generating units that are expected to benefit from synergies of the related business combination and represent the lowest level within the Group at which management monitors the related cash flows.

Goodwill, other individual assets or cash‑generating units that include goodwill, other intangible assets with an indefinite useful life, and those intangible assets not yet available for use are tested for impairment at least annually. All other individual assets or cash‑generating units are tested for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable.

An impairment loss is recognised for the amount by which the asset’s or cash‑generating unit’s carrying amount exceeds its recoverable amount. The recoverable amount is the higher of fair value, reflecting market conditions less costs to sell, and value in use based on an internal discounted cash flow evaluation. Impairment losses recognised for cash‑generating units, to which goodwill has been allocated, are credited initially to the carrying amount of goodwill. Any remaining impairment loss is charged pro rata to the other assets in the cash‑generating unit. With the exception of goodwill, all assets are subsequently reassessed for indications that an impairment loss previously recognised may no longer exist.

(o) key JuDgMent in applying the entity’s accounting policies anD gooDwill iMpairMentThe Group’s management makes estimates and assumptions regarding the future. Estimates and judgments are continually evaluated based on historical experience and other factors, including expectations of future events that are believed to be reasonable under the circumstances. In the future, actual experience may differ from these estimates and assumptions. The estimates and assumptions that have a reasonable risk of causing material adjustment to the carrying amounts of assets and liabilities within the next financial year are discussed below.

recognition oF revenueRevenue is recognised according to the accounting policies as stated and is dependent upon the type of income. Where contracts include different elements of revenue, those elements are recognised in line with those policies, with fair values attributed to each component part.

Judgement is used in the recognition of revenue from long term projects.