LNG Global Market - International Gas Union (IGU) Global Market_Gas... · LNG Global Market....

29

IGU Executive Committee Workshop in Durban, South Africa on 6-7 April 2016 LNG Global Market

Transcript of LNG Global Market - International Gas Union (IGU) Global Market_Gas... · LNG Global Market....

IGU Executive Committee Workshop in Durban, South Africa

on 6-7 April 2016

LNG Global Market

Disclaimer

2

This presentation and the information herein contained is Gas Natural Fenosa (“GNF”)property.Although GNF has taken all reasonable care to ensure that the information herein is accurateand correct, no representation, warranty or undertaking, express or implied, is given by or onbehalf of GNF or any other person as to, and no reliance should be placed on, the fairness,accuracy, completeness or correctness of the information or the opinions contained herein orany other material discussed at the presentation. This presentation may include forward-looking statements that reflect GNF's intentions, beliefs or current expectations, Suchstatements are made on the basis of assumptions and expectations that GNF currently believesare reasonable, but could prove to be wrong. Any forward-looking statements made by or onbehalf of the Company speak only as at the date of this presentation

©Copyright Gas Natural SDG, S.A.

Gas Natural Fenosa

3

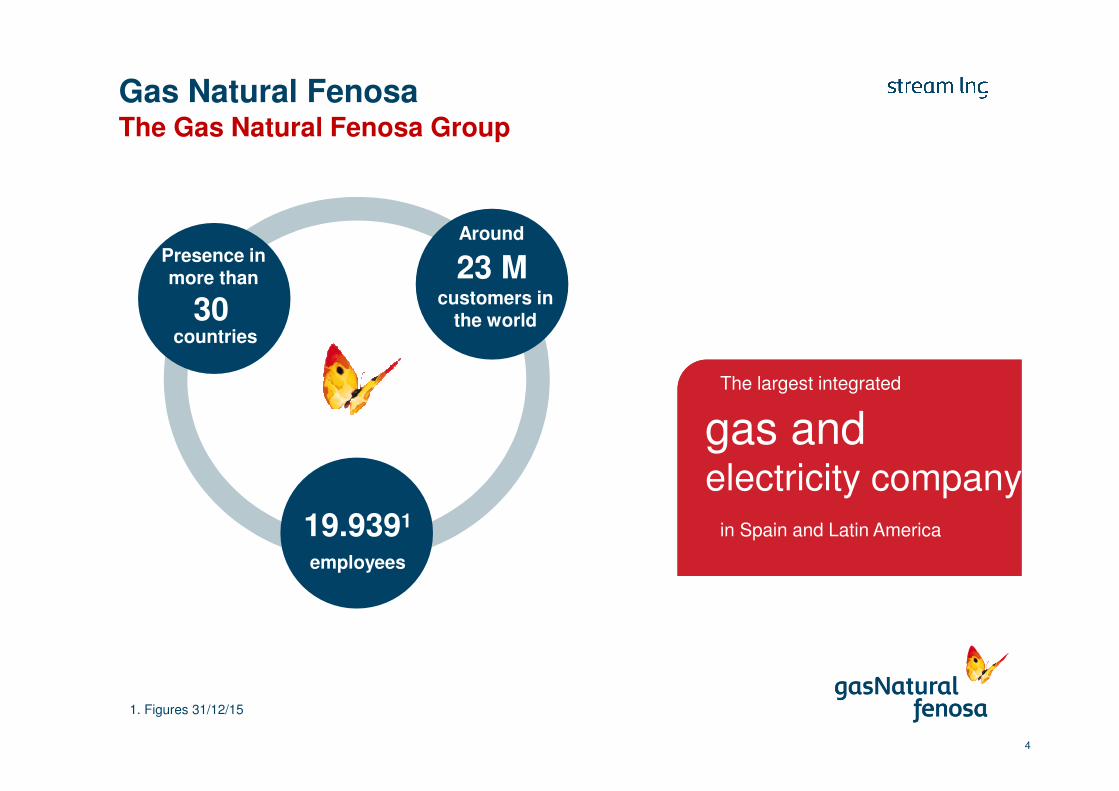

Gas Natural FenosaThe Gas Natural Fenosa Group

1. Figures 31/12/15

4

customers in the world

23 MAround

countries30

Presence in more than

employees

19.9391

The largest integrated

gas andelectricity company

in Spain and Latin America

A multinational company,

leader in the sector of

Gas and Electricity through a

Balanced business model

1 – Figures 31/12/2015

EBITDA

€5.264 M1

Total assets

€48.132 M1

Installed Capacity

15.471 MW

5

Gas Natural FenosaThe Gas Natural Fenosa Group

6

Gas Natural FenosaGNF position in the gas supply chain

• GNF has participation in the liquefaction plant of Damietta (Egypt) and Qalhat (Oman)

• 7 carriers in operation

+

• 4 carriers under construction

• Diversified and flexible portfolio of supply with 30 bcma contracted from T&T, Nigeria, Egypt, Oman, Qatar, USA, Russia, Algeria and Azerbaijan

• Participation in regasificationplants:

•Sagunto and Reganosa(Spain)

•Ecoeléctrica(Puerto Rico)

• Access capacity in Montoir(France) and in all regasificationterminals in Spain

• Transport: Maghreb-Europapipeline

• Pipeline distribution network: 120,000 km in Spain, Italy, Brazil, Argentina, Colombia, Mexico and Chile

• LNG sales of 12 bcma over long, medium and short term contracts

MarketingTransport

& DistributionRegasificationShippingMidstreamLiquefactionUpstream

• GNF is present in stable markets (Spain)

7

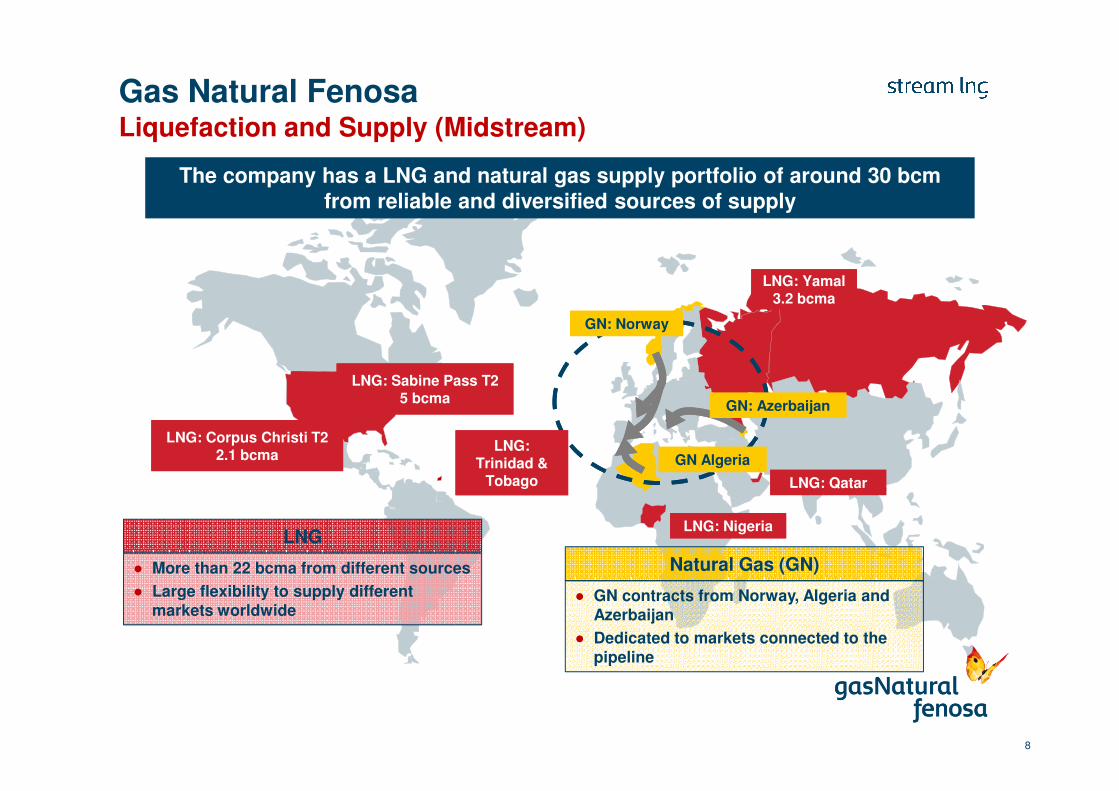

Gas Natural FenosaGNF in the world

Natural Gas (GN)

● GN contracts from Norway, Algeria and Azerbaijan

● Dedicated to markets connected to the pipeline

GN: NorwayGN: Norway

GN AlgeriaGN Algeria

GN: AzerbaijanGN: Azerbaijan

LNG: Yamal3.2 bcma

LNG: Yamal3.2 bcma

LNG: NigeriaLNG: Nigeria

LNG: QatarLNG: Qatar

LNG: Sabine Pass T25 bcma

LNG: Sabine Pass T25 bcma

LNG: Corpus Christi T22.1 bcma

LNG: Corpus Christi T22.1 bcma

LNG: Trinidad &

Tobago

LNG: Trinidad &

Tobago

LNG

● More than 22 bcma from different sources

● Large flexibility to supply different markets worldwide

The company has a LNG and natural gas supply portfolio of around 30 bcmfrom reliable and diversified sources of supply

8

Gas Natural FenosaLiquefaction and Supply (Midstream)

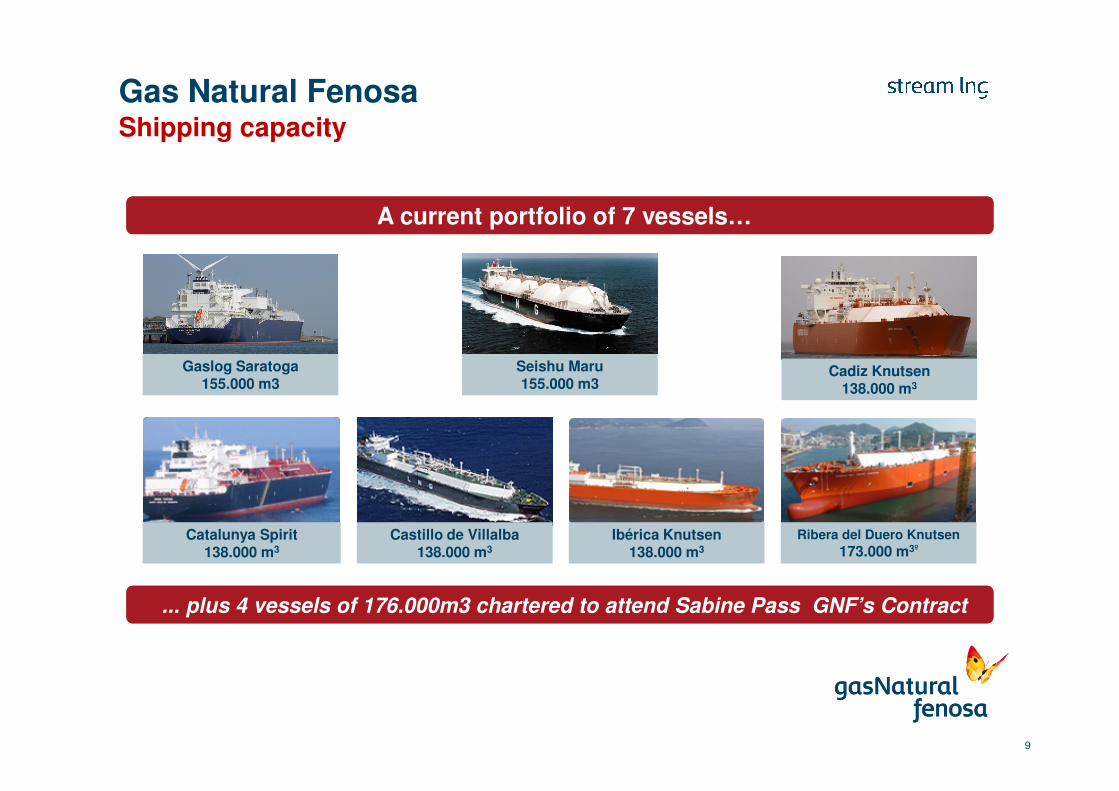

... plus 4 vessels of 176.000m3 chartered to attend Sabine Pass GNF’s Contract... plus 4 vessels of 176.000m3 chartered to attend Sabine Pass GNF’s Contract

A current portfolio of 7 vessels…A current portfolio of 7 vessels…

Cadiz Knutsen138.000 m3

Catalunya Spirit138.000 m3

Castillo de Villalba138.000 m3

Ibérica Knutsen138.000 m3

Ribera del Duero Knutsen

173.000 m3º

9

Gas Natural FenosaShipping capacity

Gaslog Saratoga155.000 m3

Seishu Maru155.000 m3

Puerto Rico: Participation in

Regasification Terminal

Puerto Rico: Participation in

Regasification Terminal

LNG globally marketed through medium/long term contracts

France (Montoir): Regasification

Capacity

France (Montoir): Regasification

Capacity

Spain: - Participation in 2 Regas.

Terminals- Regas capcity in all regas

terminals

Spain: - Participation in 2 Regas.

Terminals- Regas capcity in all regas

terminals

Current LNG route

Future LNG route

LNG Delivery Point

LNG Supply Source

Large experience in the downstream markets.GNF is one of the main

players of gas sales worldwide.

Its active management of long term sale contracts

and spot contracts ensures optimized and secured

supplies

10

Gas Natural FenosaGNF’s regasification terminals and markets

LNG Markets

12

12

LNG MarketsLNG Value Chain

Tra

ns

po

rtU

nlo

ad

ing

an

d s

tora

ge

term

ina

l

Fin

al

Cu

sto

me

rs

Ga

s D

istr

ibu

tio

n

Liquefaction Plant LNG Carrier

Regas terminal (on-shore/ FSRU)

Truck loading terminal

Tank truck

LNG Satellites plant

Pipeline

Power Plant Households Industry

Sm

all S

cale

LN

Gap

plicati

on

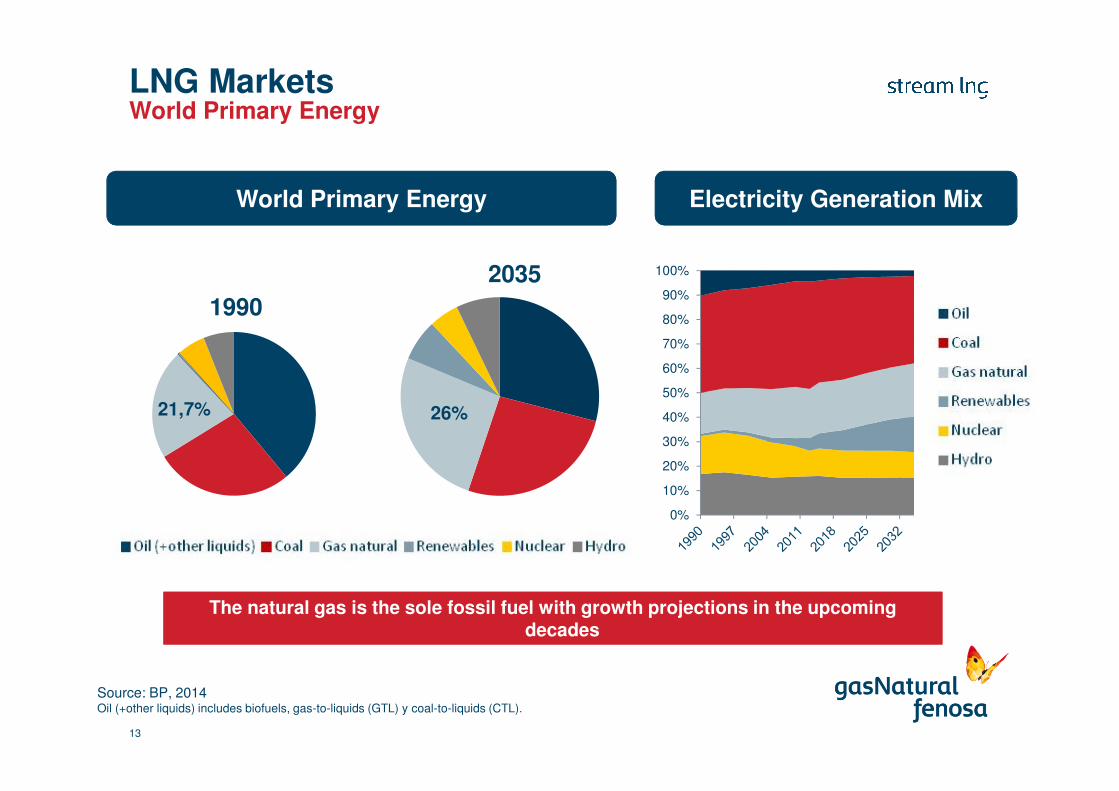

LNG MarketsWorld Primary Energy

Source: BP, 2014Oil (+other liquids) includes biofuels, gas-to-liquids (GTL) y coal-to-liquids (CTL).

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Crudo

Carbón

Gas natural

Renovables

Nuclear

Hidráulica

1990

21,7%

2035

26%

Electricity Generation MixWorld Primary Energy

The natural gas is the sole fossil fuel with growth projections in the upcoming decades

The natural gas is the sole fossil fuel with growth projections in the upcoming decades

13

LNG Markets

14

World gas natural demand

Unit: bcmaSource: GNF’s analysis based on “BP Statistical Review of world energy 2015” and “BP Energy Outlook 2035“(2015).

Expected growth in the consumption of natural gas of 624 bcm from 2013 to 2020

848

Pacific Asia

2013 2020

572

43,7%

838 929

North America

2013 2020

14,5%

Latam

2013 2020

152 179

4,3%

958 1.007

Europe & Eurasia

2013 2020

7,9%

Middle East

2013 2020

386 536

24,1%

Africa

2013 2020

111 145

5,5%

LNG MarketsEvolution of the consumption of LNG and natural gas in the world

Evolution of total demand of natural gas

Fuente: Woodmackenzie

10%

90%

16%

84%

2014

2035

% LNG mix of natural gas demand

% GN of total gas demand % LNG of total gas demand

0

500

1000

1500

2000

2500

3000

3500

1990 1995 2000 2005 2010 2013 2015

Bcm

Total demand of natural gas

The increased consumption of LNG will lead to a more interconnected and globalized gas market

The increased consumption of LNG will lead to a more interconnected and globalized gas market

15

LNG Markets

16

LNG Supply Facilities

Source: GNF’s analysis based on Woodmackenzie reports.

KenaiKenai

Perú LNGPerú LNG

On-StreamOn-Stream

Atlantic LNG 1Atlantic LNG 1Atlantic LNG 2 &3Atlantic LNG 2 &3Atlantic LNG 4Atlantic LNG 4

NLNG BaseNLNG BaseNLNG ExpansionNLNG ExpansionNLNG PlusNLNG PlusNLNG 6NLNG 6

ArzewArzewBethiouaBethiouaSkikdaSkikda

Marsa El BregaMarsa El Brega

EG LNGEG LNG

Angola LNGAngola LNG

Yemen LNGYemen LNG

DamiettaDamiettaELNG 1ELNG 1ELNG 2ELNG 2

SnohvitSnohvit

Qatargas-1Qatargas-1Qatargas-2Qatargas-2Qatargas-3Qatargas-3Qatargas-4Qatargas-4Rasgas IRasgas IRasgas IIRasgas IIRL - 3RL - 3

ADGASADGAS

OLNGOLNGQalhatQalhat

Sakhalin 2Sakhalin 2

ArunArunBruneiBrunei

BontangBontang

TangguhTangguh

PNG LNGPNG LNGMLNGMLNGMLNG DuaMLNG DuaMLNG TigaMLNG TigaMLNG Train 9MLNG Train 9

Under constructionUnder construction

Petronas FLNG 1Petronas FLNG 1

PlutoPlutoNorth West ShelfNorth West ShelfGorgonGorgonWheatstoneWheatstonePrelude FLNGPrelude FLNG

Petronas FLNG 2Petronas FLNG 2

DS LNGDS LNG

IchthysIchthysDarwinDarwin

GLNGGLNG

QLNGQLNGAPLNGAPLNG

CameronCameron

Sabine Pass Trains 1-5Sabine Pass Trains 1-5Freeport Trains 1-3Freeport Trains 1-3Corpus ChristiCorpus Christi

Cove PointCove Point

La Creciente FLNGLa Creciente FLNG

Yamal LNGYamal LNG

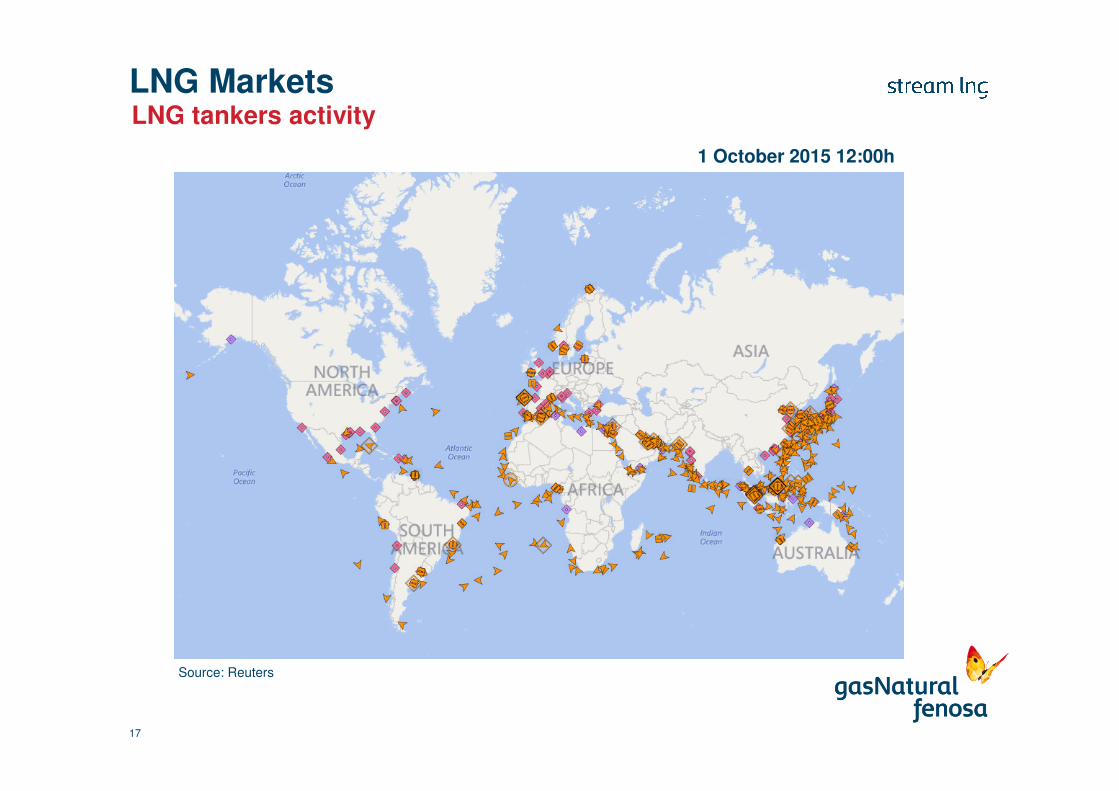

LNG Markets

17

LNG tankers activity

Source: Reuters

1 October 2015 12:00h

LNG Markets

18

Current situation

0

100

200

300

400

500

600

700

800

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Operational Under Construction

Probable Development Possible

Speculative LNG demand

Liquefaction Capacity vs LNG Demand

Source: Compilated based on Woodmackenzie data.

Price conditions for consumers would be very favourable in the coming years thanks to a reduced demand grow and the LNG avalaibility

Source: OIES with Platts, EIA, Argus CME

LNG price evolution

LNG Markets

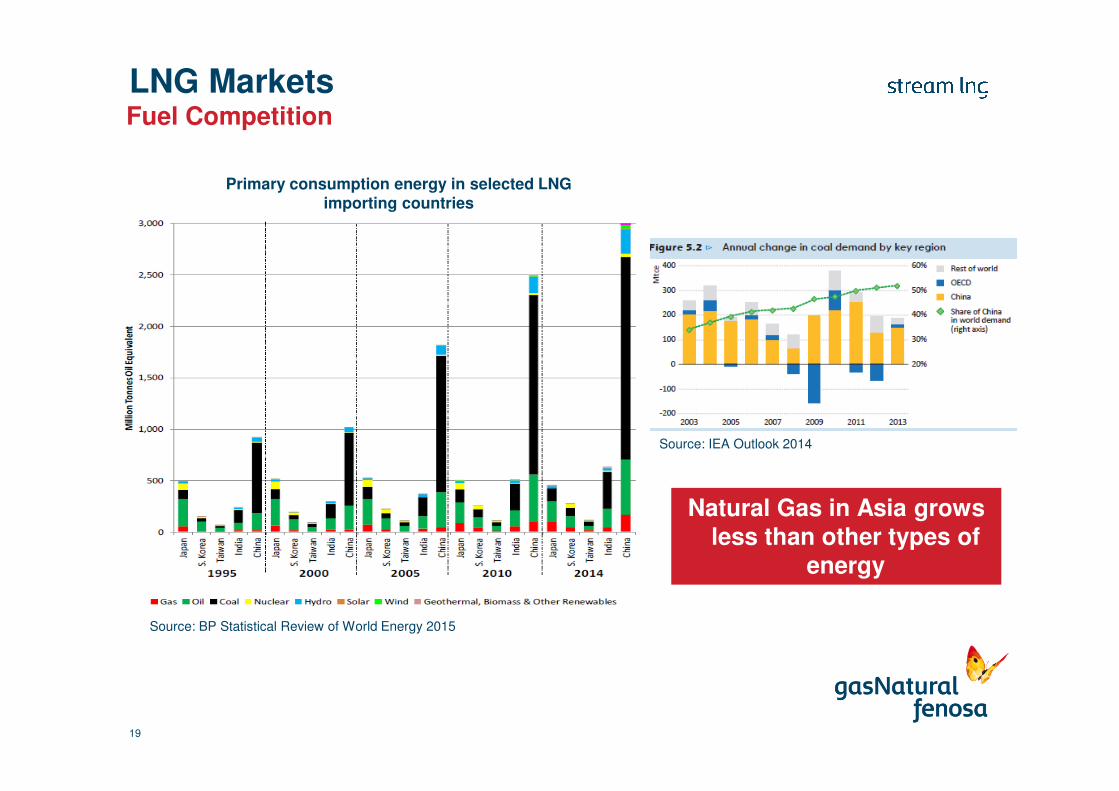

19

Fuel Competition

Natural Gas in Asia grows less than other types of

energy

Primary consumption energy in selected LNG importing countries

Source: BP Statistical Review of World Energy 2015

Source: IEA Outlook 2014

LNG Markets

20

LNG / Natural gas prospects

� Long term factors

�New LNG Importing countries as Egypt, Pakistan, Israel, Jordan and private

Chinese buyers

�New supplies and discoveries

�Alternative uses of Natural Gas/LNG as transportation

�New technology, as FNLG, can lower the upstream costs of LNG

�LNG contribution to the Security of Supply

�Short term factors

�Current level of prices can deter the investment of new supplies leading to a

“boom & bust cycle” and a new tight period

Security of SupplyFukushima example

LNG Markets helped Japan to cope with the nuclear collapse after the 2011 tsunami. Many cargoes were re-

routed to Japan responding to the high prices

LNG Markets helped Japan to cope with the nuclear collapse after the 2011 tsunami. Many cargoes were re-

routed to Japan responding to the high prices

62.19

7.35

4.70

1.06

0.29

0.17

63.91

60

62

64

66

68

70

Q1 2011 Asia Europe North AmericaLatin America Middle East Q1 2012

mmtons Global LNG Imports: Q1 2012 vs. Q1 2011

Source: Waterborne LNG, US Department of Energy, PFC Energy

Global LNG Imports: Q1 2012 vs Q1 2011 Japan fuel consumption for electricity generation

Source: The Fukushima nuclear accident and its effect on global energy security , Energy Policy 59, 2013

GNF to supply LNGin Africa

22

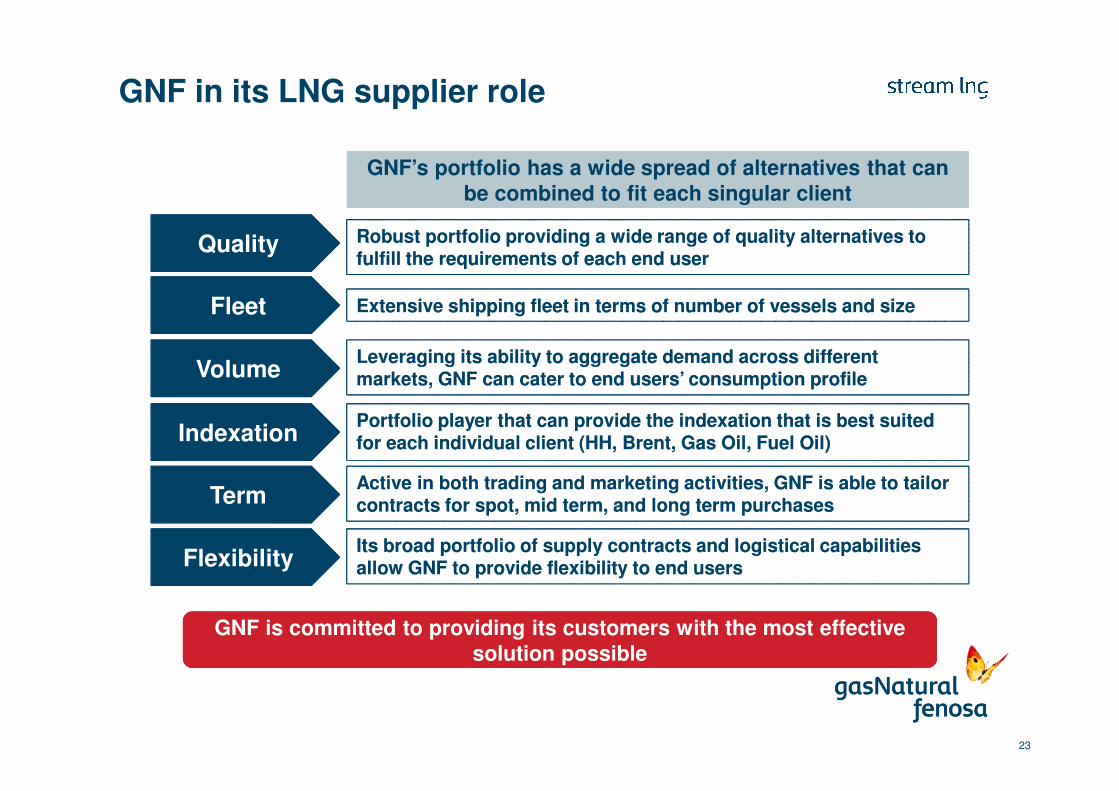

23

GNF’s portfolio has a wide spread of alternatives that can be combined to fit each singular client

GNF’s portfolio has a wide spread of alternatives that can be combined to fit each singular client

Quality Robust portfolio providing a wide range of quality alternatives to fulfill the requirements of each end user Robust portfolio providing a wide range of quality alternatives to fulfill the requirements of each end user

Fleet

Volume

Indexation

Term

Extensive shipping fleet in terms of number of vessels and sizeExtensive shipping fleet in terms of number of vessels and size

Leveraging its ability to aggregate demand across different markets, GNF can cater to end users’ consumption profileLeveraging its ability to aggregate demand across different markets, GNF can cater to end users’ consumption profile

Portfolio player that can provide the indexation that is best suited for each individual client (HH, Brent, Gas Oil, Fuel Oil)Portfolio player that can provide the indexation that is best suited for each individual client (HH, Brent, Gas Oil, Fuel Oil)

Active in both trading and marketing activities, GNF is able to tailor contracts for spot, mid term, and long term purchasesActive in both trading and marketing activities, GNF is able to tailor contracts for spot, mid term, and long term purchases

FlexibilityIts broad portfolio of supply contracts and logistical capabilities allow GNF to provide flexibility to end usersIts broad portfolio of supply contracts and logistical capabilities allow GNF to provide flexibility to end users

GNF in its LNG supplier role

GNF is committed to providing its customers with the most effective solution possible

GNF is committed to providing its customers with the most effective solution possible

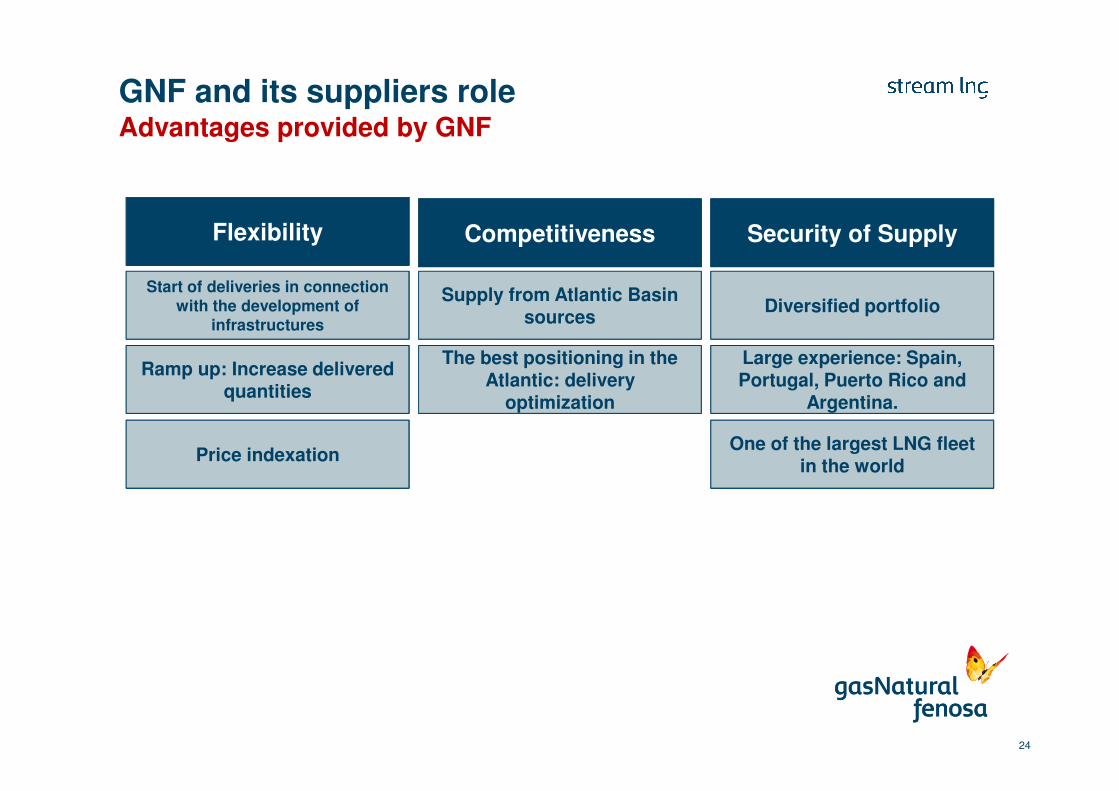

24

Flexibility

Start of deliveries in connection with the development of

infrastructures

Ramp up: Increase delivered quantities

Competitiveness

Supply from Atlantic Basin sources

The best positioning in the Atlantic: delivery

optimization

Price indexation

Security of Supply

Diversified portfolio

Large experience: Spain, Portugal, Puerto Rico and

Argentina.

One of the largest LNG fleet in the world

GNF and its suppliers roleAdvantages provided by GNF

Small Scale LNG applicationsDistribution by trucks / LNG satellite plants

25

LNG can be transported by trucks to Satellite LNG Plants or industrial clients

LNG can be transported by trucks to Satellite LNG Plants or industrial clients

Small Scale LNG applicationsAdvantages

26

�They allow to transport the gas natural to anywhere in the country withoutinvesting in pipeline network

�They allow to transport the gas natural to anywhere in the country withoutinvesting in pipeline network

�They do not require large investments and it has very competitiveoperating/maintenance costs

�They do not require large investments and it has very competitiveoperating/maintenance costs

�Creates natural gas demand before the development of large gas infrastructurein the region

�Creates natural gas demand before the development of large gas infrastructurein the region

�Technologies tested and proved in mature markets (Spain)�Technologies tested and proved in mature markets (Spain)

�They are used, and they are still implemented by GNF in the gasification

model in Spain

�They are used, and they are still implemented by GNF in the gasification

model in Spain

Small Scale LNG applicationsAdvantages

27

�Its development and implementation allows an important growth vector indifferent sectors

�Its development and implementation allows an important growth vector indifferent sectors

�With applications in all sectors of economic activity: industrial / agriculture /services / residential / vehicle / power generation, regardless of their location

�With applications in all sectors of economic activity: industrial / agriculture /services / residential / vehicle / power generation, regardless of their location

�Main mechanism for the development of generation projects (electricity forthermal energy / industrial cooling)

�Main mechanism for the development of generation projects (electricity forthermal energy / industrial cooling)

�GNF has a large experience in the construction and operation of

LNG satellite plants

�GNF has a large experience in the construction and operation of

LNG satellite plants

�This model has been exported to other countries in Europe:

France, Italy, Germany, Belgium, Holland

�This model has been exported to other countries in Europe:

France, Italy, Germany, Belgium, Holland

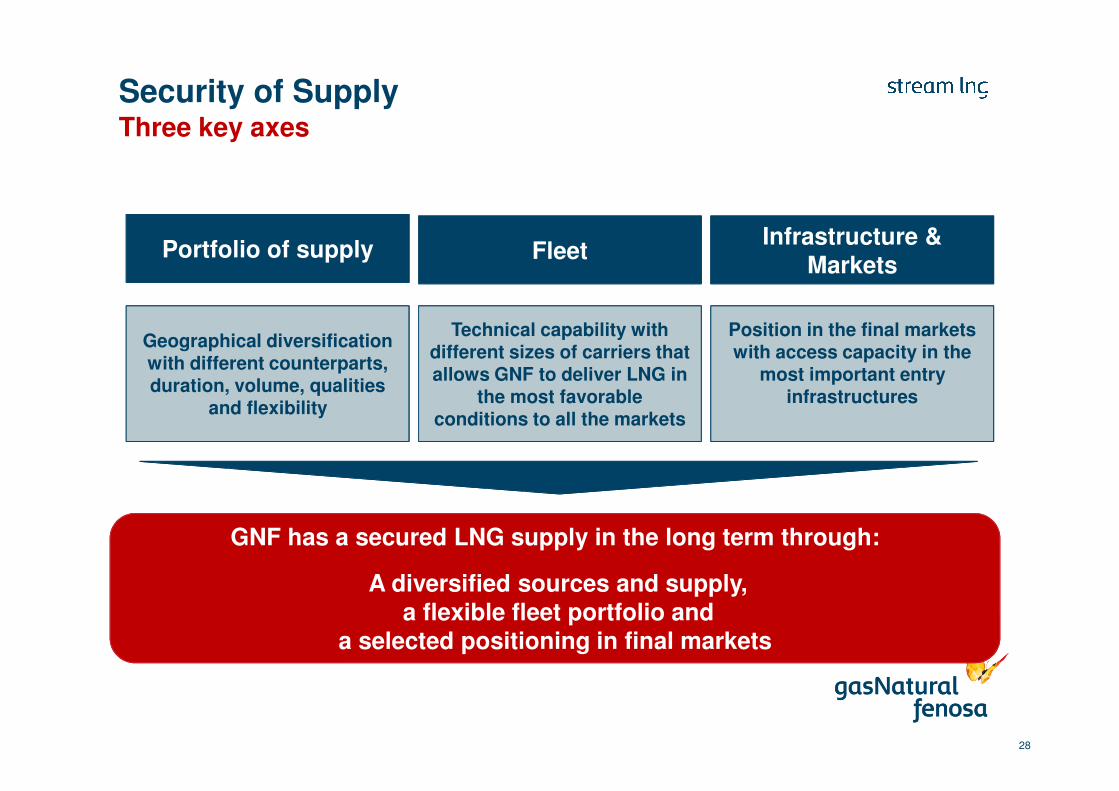

28

Portfolio of supply FleetInfrastructure &

Markets

GNF has a secured LNG supply in the long term through:

A diversified sources and supply,a flexible fleet portfolio and

a selected positioning in final markets

Security of SupplyThree key axes

Geographical diversification with different counterparts, duration, volume, qualities

and flexibility

Technical capability with different sizes of carriers that allows GNF to deliver LNG in

the most favorable conditions to all the markets

Position in the final markets with access capacity in the

most important entry infrastructures

Thank you