LISA Conference - tisa.uk.com€¦ · • Michael Wainwright, Partner, ... • Richard Parkin, Head...

52

LISA Conference Monday 27 th June 2016 JP Morgan @uktisa

Transcript of LISA Conference - tisa.uk.com€¦ · • Michael Wainwright, Partner, ... • Richard Parkin, Head...

LISA ConferenceMonday 27th June 2016

JP Morgan

@uktisa

Jasper Berens - ChairHead of UK Funds

J.P. Morgan Asset Management

@uktisa

Agenda

• Opening remarks by Jasper Berens, Head of UK Funds, J.P. Morgan Asset Management• Paul Cottis, Pensions & Savings Policy, HMRC and Rosie Neilson, Policy Advisor, Pension & Savings, HM

Treasury ‘Implementing the Lifetime ISA – an HMT/HMRC update’• Tom McPhail, Head of Retirement Policy, Hargreaves Lansdown ‘The Lifetime ISA: Meeting consumer

needs’• Michael Wainwright, Partner, Dentons LLP ‘LISA: What could possibly go wrong?’• Coffee Break• Andrew Baddeley-Chappell, Head of Policy & Governance (Mortgages & Savings), Nationwide ‘Lifetime

ISA: Help to Buy’• Rob Booth, Director of Investment and Product Development, NOW:Pensions ‘Does the Lifetime ISA

threaten the success of Auto-Enrolment?’• Richard Parkin, Head of Pensions and Retirement Product, Fidelity ‘Learning to love LISA: integrating the

Lifetime ISA into workplace savings’

@uktisa

Paul Cottis, HMRCand

Rosie Neilson, HM Treasury

@uktisa

Tom McPhailHead of Retirement Policy

Hargreaves Lansdown

@uktisa

The Lifetime ISA: Meeting consumer needs

• Suitability

•Key policy issues

• Self-employed

•Consumer research

•Customer engagement challenges

LISA v Pension

Key policy issues

Age eligibilityLoan-backsQualifying life eventsNon-bonus eligible contributionsApplication of 5% penaltyTidying up

H2BContribution limitsJISA

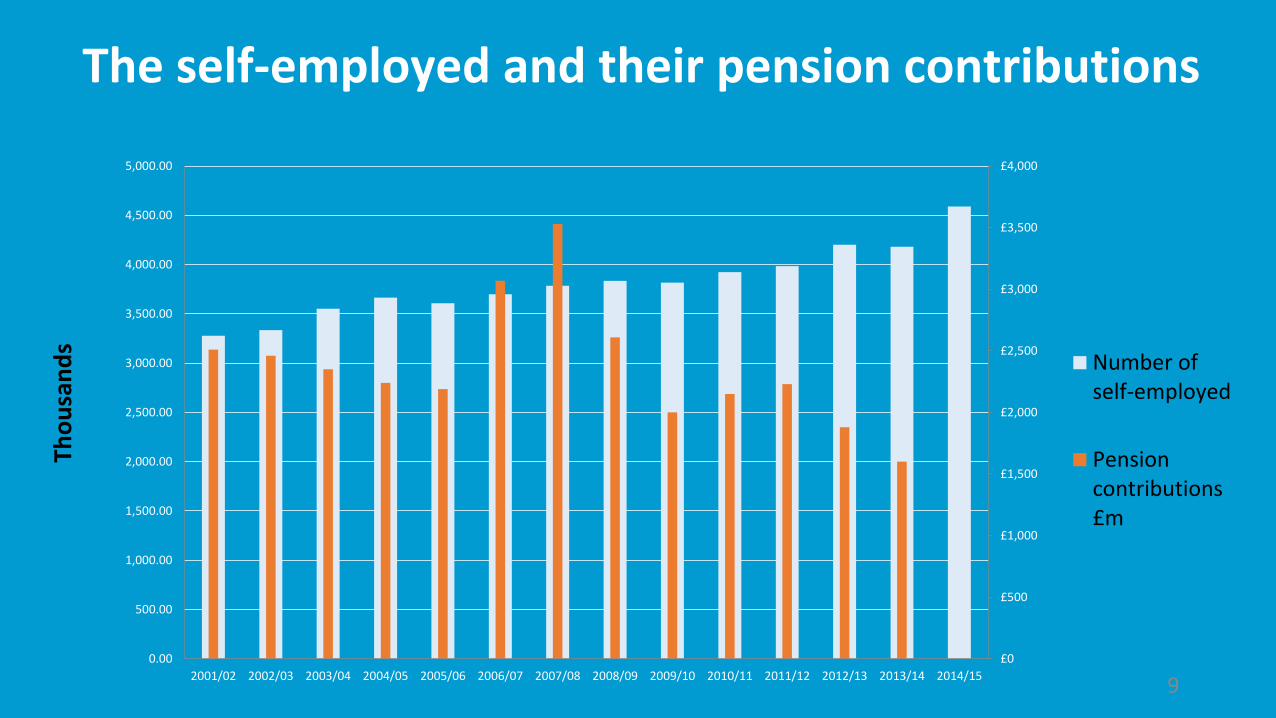

The self-employed and their pension contributions

9

£0

£500

£1,000

£1,500

£2,000

£2,500

£3,000

£3,500

£4,000

0.00

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

4,000.00

4,500.00

5,000.00

2001/02 2002/03 2003/04 2004/05 2005/06 2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

Number ofself-employed

Pensioncontributions£m

Tho

usa

nd

s

LISA demand

LISA demand

Do you think you will open a Lifetime ISA?

Yes

No

Not sure

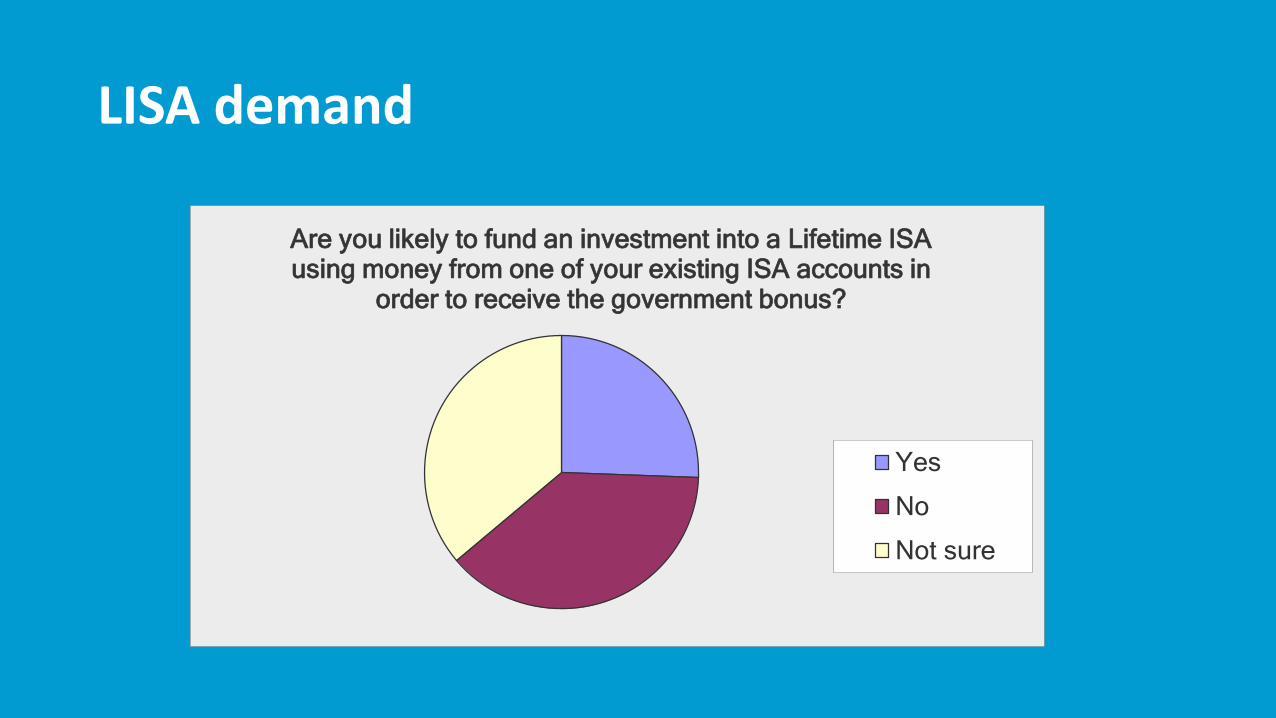

LISA demand

Are you likely to fund an investment into a Lifetime ISA using money from one of your existing ISA accounts in

order to receive the government bonus?

Yes

No

Not sure

LISA demand

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

Instead of apension

As well as apension

Instead of aHelp-to-buy

ISA

Instead of aCash ISA

Instead of aStocks &

Shares ISA

Alongside oneof the above

ISAs

How do you anticipate using the Lifetime ISA?Please select all that apply

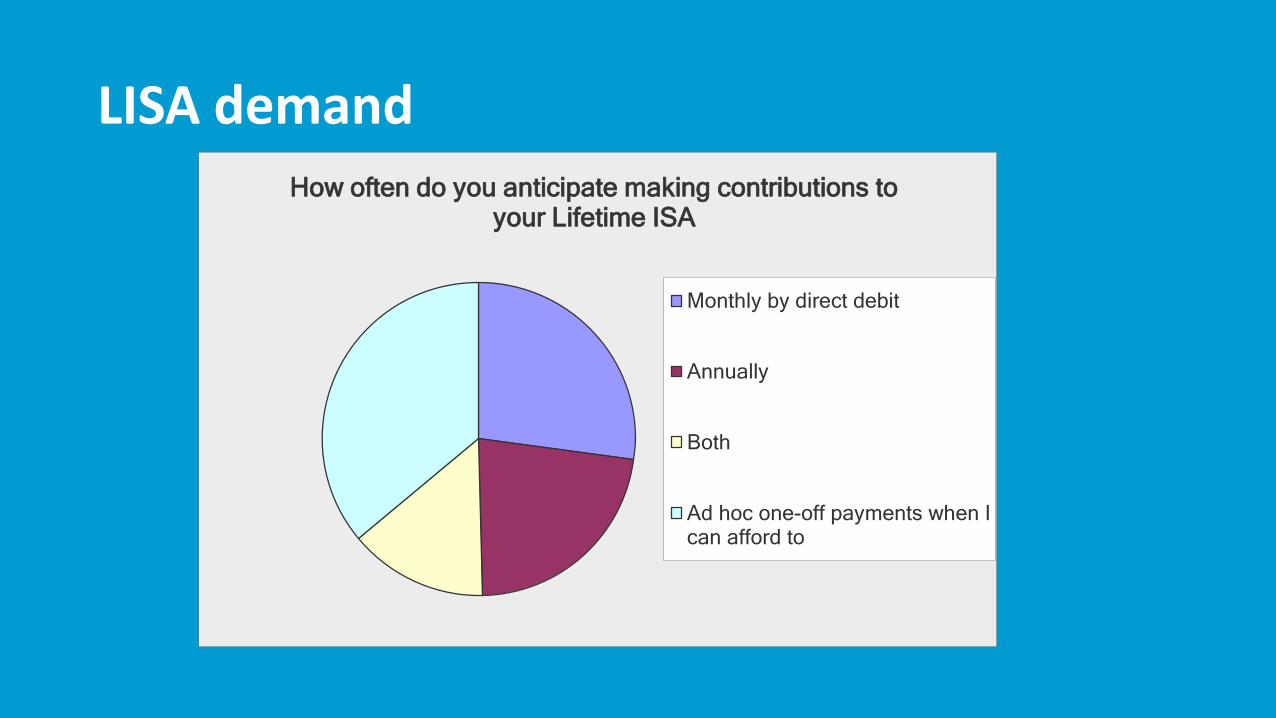

LISA demandHow often do you anticipate making contributions to

your Lifetime ISA

Monthly by direct debit

Annually

Both

Ad hoc one-off payments when Ican afford to

LISA demand

What type of investment will you make in Lifetime ISA?

Cash

Stocks & Shares

A combination of cashand stocks & sharesNot sure yet

LISA demand

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

Pensions givemore incentive to

save

Lifetime ISA givemore incentive to

save

Pensions aremore flexible

Lifetime ISA aremore flexible

How do you think the Lifetime ISA compares with a pension?Please select all that apply

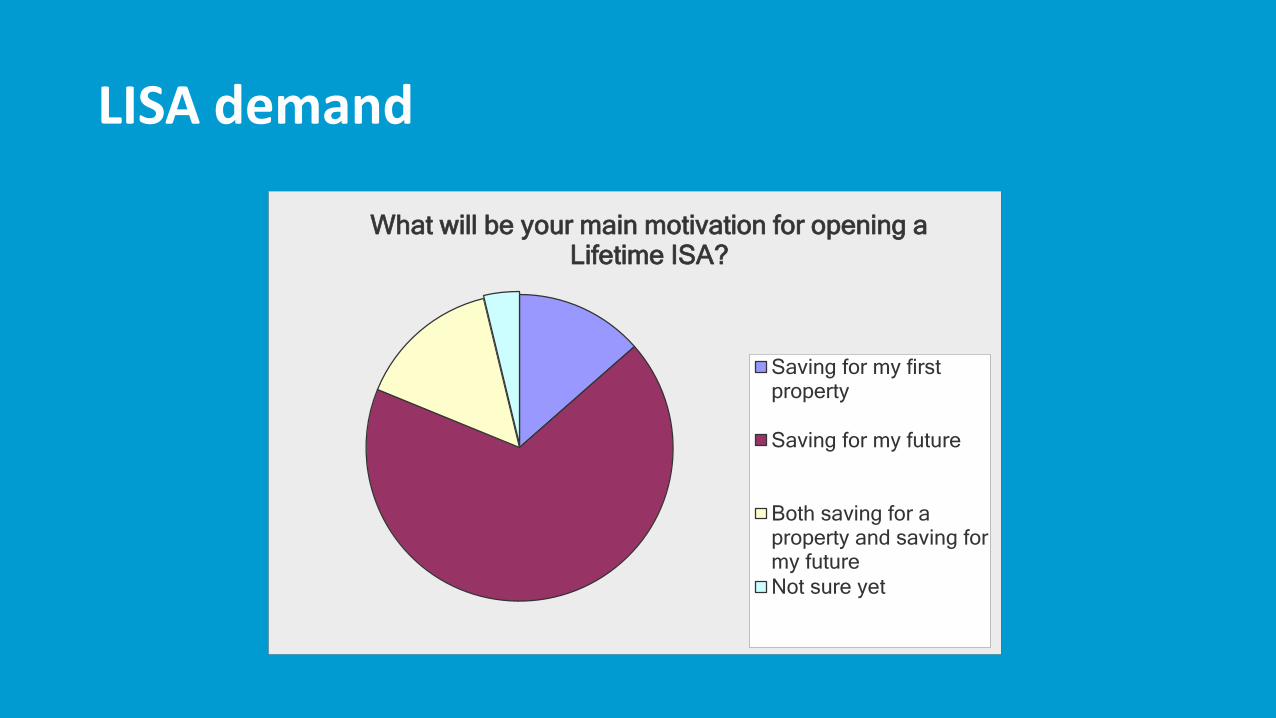

LISA demand

What will be your main motivation for opening a Lifetime ISA?

Saving for my firstproperty

Saving for my future

Both saving for aproperty and saving formy future

Not sure yet

LISA demand

If the government bonus was paid more frequently than proposed would you be:

More likely to save in aLifetime ISA

Less likely to save in aLifetime ISA

Indifferent

Not sure

Customer engagement challenges

• Simplicity is the key

• Differences across ISAs

• Government top-up

• Non-qualifying withdrawals

• Investment choices: cash or shares

• Transfers

• Eligibility post 40: account closures

What investors want

Michael WainwrightPartner

Dentons LLP

@uktisa

Lifetime ISAs

What could possibly go wrong?

Michael Wainwright

#43570011.01

27/06/2016

22

Lessons from the past

23

• Inflexibility and unfairness in workplace pensions

• New product gives transparency and control

24

Pension Transfers and Opt-Outs

• Existing products complex and expensive

• Government framework for simple low cost products

25

Stakeholder Products

• Repayment mortgage seen as a wasted investment opportunity

• Tax advantaged investment as repayment vehicle gives profit opportunity

26

Endowment /PEP Mortgages

• Shares give a mix of income and capital but some investors want one or the other

• Financial engineering to create income shares and capital shares

27

Split Cap Investment Trusts

• Equity funds have variable returns and high charges

• Product offers fixed return subject to clearly defined contingency based on market performance

28

Precipice Bonds

• Standard fund achieves competitive return investing in highly liquid assets

• Possible to achieve marginally higher return by accepting greater risk on duration and liquidity

29

AIG Life Enhanced Fund

• Intense competition on price (interest rate) for consumer finance products

• Opportunity to subsidise through higher pricing on bundled products

30

PPI

• LISA is a targeted initiative based on a product with a long history of success

• Combination of incentives and restrictions creates a dilemma compared with the vanilla version

31

Conclusion

Thank you

Dentons UKMEA LLP

One Fleet Place

London

EC4M 7WS

United Kingdom

Dentons is the world's first polycentric global law firm. A top 20 firm on the Acritas 2015 Global Elite Brand Index, the Firm is committed to

challenging the status quo in delivering consistent and uncompromising quality and value in new and inventive ways. Driven to provide clients

a competitive edge, and connected to the communities where its clients want to do business, Dentons knows that understanding local cultures

is crucial to successfully completing a deal, resolving a dispute or solving a business challenge. Now the world's largest law firm, Dentons'

global team builds agile, tailored solutions to meet the local, national and global needs of private and public clients of any size in more than 125

locations serving 50-plus countries. www.dentons.com.

© 2016 Dentons. Dentons is a global legal practice providing client services worldwide through its member firms and affiliates. This publication is not designed to provide legal or other advice and you should not take, or refrain from taking, action based on its content. Please see dentons.com for Legal Notices.

32

Andrew Baddeley-ChappellHead of Policy & Governance (Mortgages & Savings)

Nationwide

@uktisa

Rob BoothDirector of Investment and Product Development

NOW:Pensions

@uktisa

Smarter. Simpler. Better. 35

Smarter. Simpler. Better.

Does the Lifetime ISA threaten the success of auto enrolment?

Smarter. Simpler. Better. 36

So many questions?

• Has auto enrolment been a success so far?

• If yes, will it continue to be so?

• Is LISA an alternative to a Pension?

• What impact will LISA have on member behaviour?

• What about employer behaviour?

• Is this just the beginning of a long term savings revolution?

Smarter. Simpler. Better. 37

Work and Pensions Committee – May 2016

• “Pensions automatic enrolment (AE) has so far been a tremendous success”

• “An additional 6.1 million people are enrolled in a workplace pension and saving for their retirement, with many more to follow”

• “Employer compliance rates are high and employee opt-out rates are low”

• “it is now at a crucial and risky stage of its development”

• “It is imperative that it is not undermined by other government-sponsored forms of saving”

Smarter. Simpler. Better. 38

But we are far from a job well done

• Inertia is both friend and enemy to auto enrolment success

• Increasing contributions will increase opt-out rates

• 8% of band earnings must be just the starting point

• Small employers need more support

• Any obstacle in the road is dangerous

• Promotion of LISA will raise questions amongst employers and savers which maybe didn’t exist

Smarter. Simpler. Better. 39

What about LISA

Smarter. Simpler. Better. 40

What they said…DWP:

The LISA is not a part of the pension system but an additional flexible savings productthat can complement pension savings.

Chancellor, George Osborne:

The LISA is for those under 40, many of whom haven’t had such a good deal from thepension system.

ABI:

LISA risks undermining AE’s success in encouraging young people to save. Whilst youngpeople who switch to the LISA are still saving, they will not be saving in the mosteffective way.

Pensions Minister, Ros Altmann:

A pension is a pension and an ISA, whatever you call it, is not a pension … It doesconcern me if people are trying to suggest that this Lifetime ISA is somehow a pension;in my view it is not.

Smarter. Simpler. Better. 41

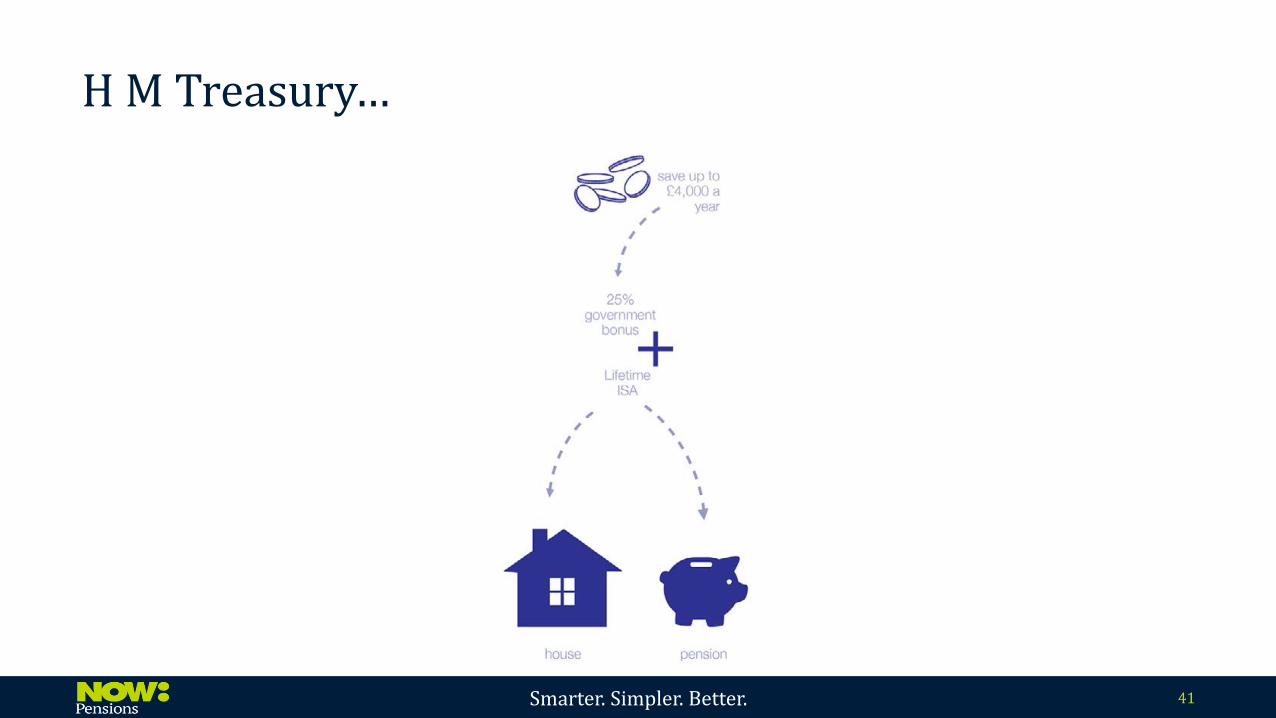

H M Treasury…

Smarter. Simpler. Better. 42

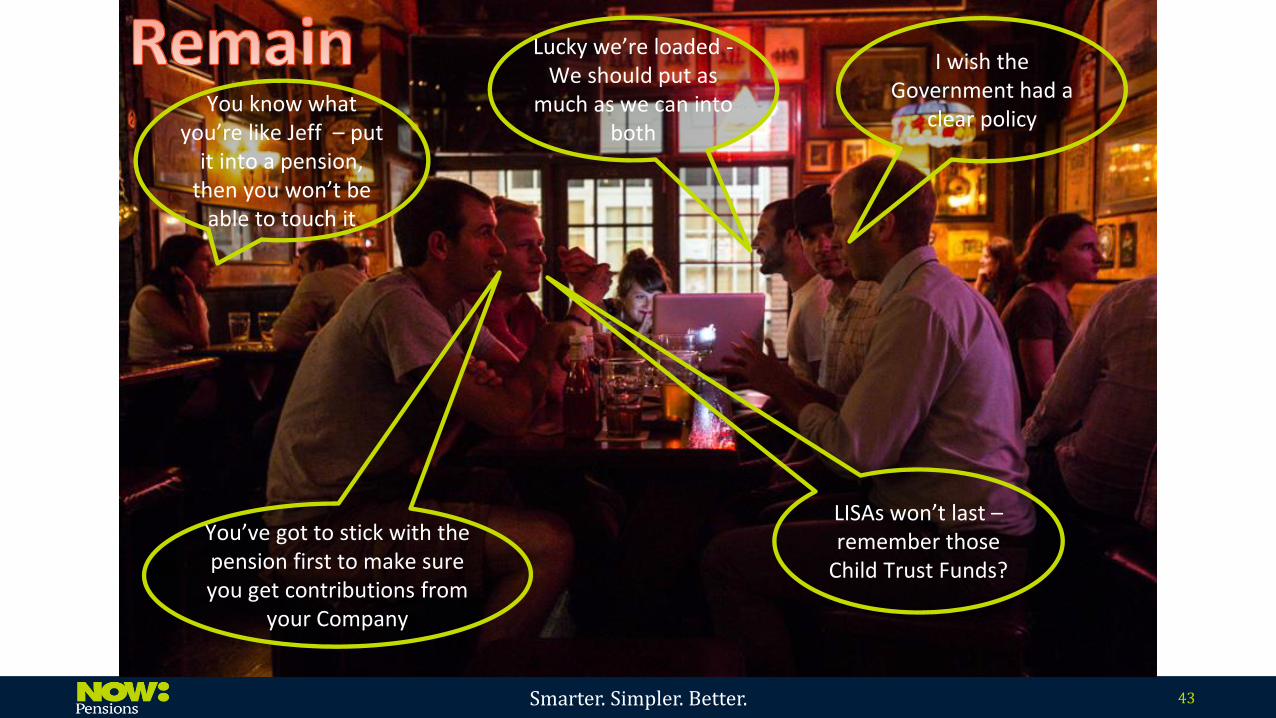

LISA or Workie

Smarter. Simpler. Better. 43

LISAs won’t last –remember those

Child Trust Funds?

I wish the Government had a

clear policy

You’ve got to stick with the pension first to make sure you get contributions from

your Company

You know what you’re like Jeff – put

it into a pension, then you won’t be

able to touch it

Lucky we’re loaded -We should put as

much as we can into both

Smarter. Simpler. Better. 44

I’m always being told I should have an emergency fund – I can get my money out from a LISA if I

need to

What about those poor BHS pension members

– I wouldn’t trust pensions so I’m going

to go for the LISAI’m going to have to pay 5% of my salary to my pension – LISA

has no minimum and I can vary it

Steve and I want to buy a house as soon as we can so we’re both going to save in a LISA – we can’t afford a

pension as well

They’re all so boring

Smarter. Simpler. Better. 45

The Logical Argument

Age 60Projected Fund

Value

Fund attributable to member’s

savingsNet Available Fund

Available Fund as a percentage of

“member’s savings”

Pension £973,900 £479,200 £974,000 203%

LISA £599,000 £479,200 £599,000 125%

Start at age 22. Individual pays £4,000 pa out of take home pay. Investment return of 5% net of all charges.Assumes auto enrolment contributions increase in line with current legislation. Pension Liberation assumes 55% tax charge only

Age 50Projected Fund

Value

Fund attributable to member’s

savingsNet Available Fund

Available Fund as a percentage of

“member’s savings”

Pension £533,000 £261,800 £240,000 92%

LISA £327,000 £261,800 £249,000 95%

Smarter. Simpler. Better. 46

The Emotional Argument

OR

Smarter. Simpler. Better. 47

What about Employers?

• What will small businesses do?

• LISA membership instead of auto enrolment will save the employer money

• It’s illegal to encourage staff to opt-out of auto enrolment

• It’s not illegal to:

• Promote a workplace ISA

• Talk about the advantages of LISA

• Let nature take its course

Smarter. Simpler. Better. 48

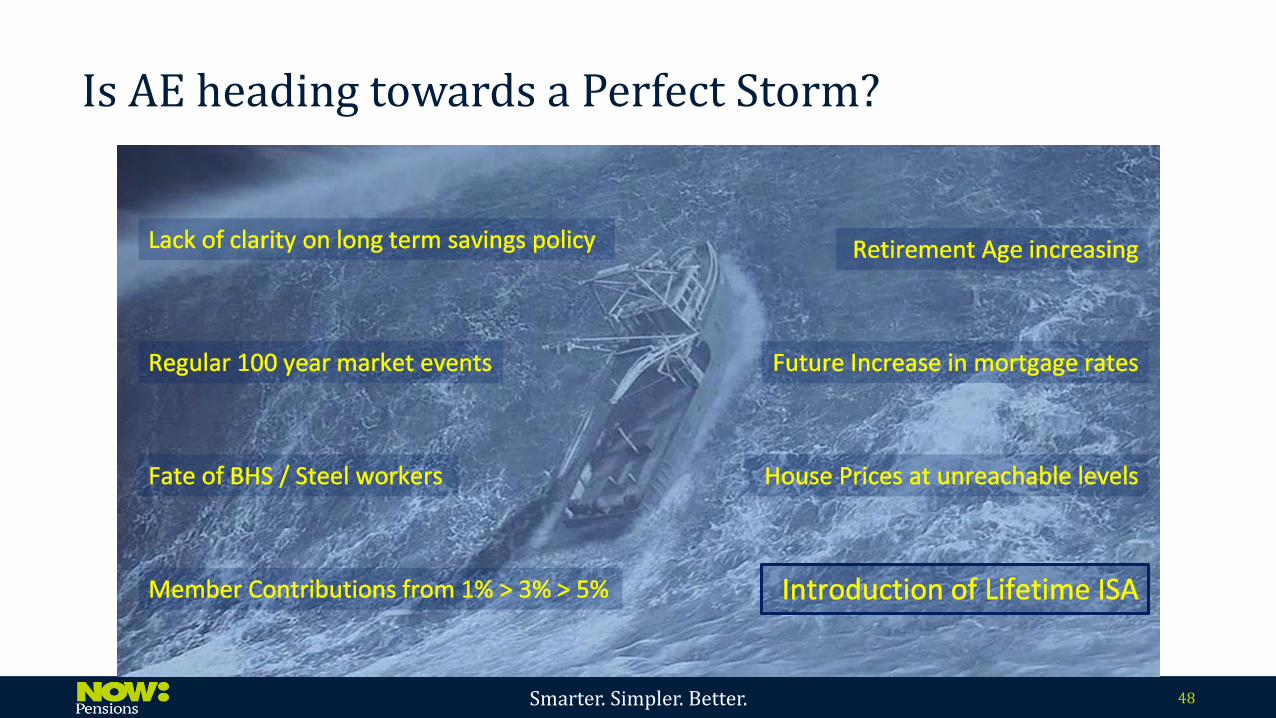

Is AE heading towards a Perfect Storm?

Smarter. Simpler. Better. 49

“We recommend the Government develop a communicationscampaign that highlights the differences between the LISA andworkplace pensions”

“The Government should also conduct urgent research on any effectof the LISA on pension saving through AE”

“The findings of this research should be reported in time for the 2016Autumn Statement”

Conclusions

Work and Pensions Committee – Recommendations

Smarter. Simpler. Better. 50

The start of a long-term savings revolution?

Richard ParkinHead of Pensions & Retirement Product

Fidelity Worldwide Investments

@uktisa

Thank You!

TISADakota House

25 Falcon CourtPreston Farm Business Park

STOCKTON-ON-TEESTS18 3TX

www.tisa.uk.com01642 666999

@uktisa