L’impact des ADAS sur l’assurance automobile A global quantitative analysis of the mobility...

14

PTOLEMUS Consulting Group L’impact des ADAS sur l’assurance automobile Frédéric Bruneteau - Nomadic Breakfast - Paris - 14 février 2018 Propriété intellectuelle de PTOLEMUS Synthèse de notre rapport

Transcript of L’impact des ADAS sur l’assurance automobile A global quantitative analysis of the mobility...

PTOLEMUS Consulting Group

L’impact des ADAS sur l’assurance automobile

Frédéric Bruneteau - Nomadic Breakfast - Paris - 14 février 2018 Propriété intellectuelle de PTOLEMUS

Synthèse de notre rapport

PTOLEMUS

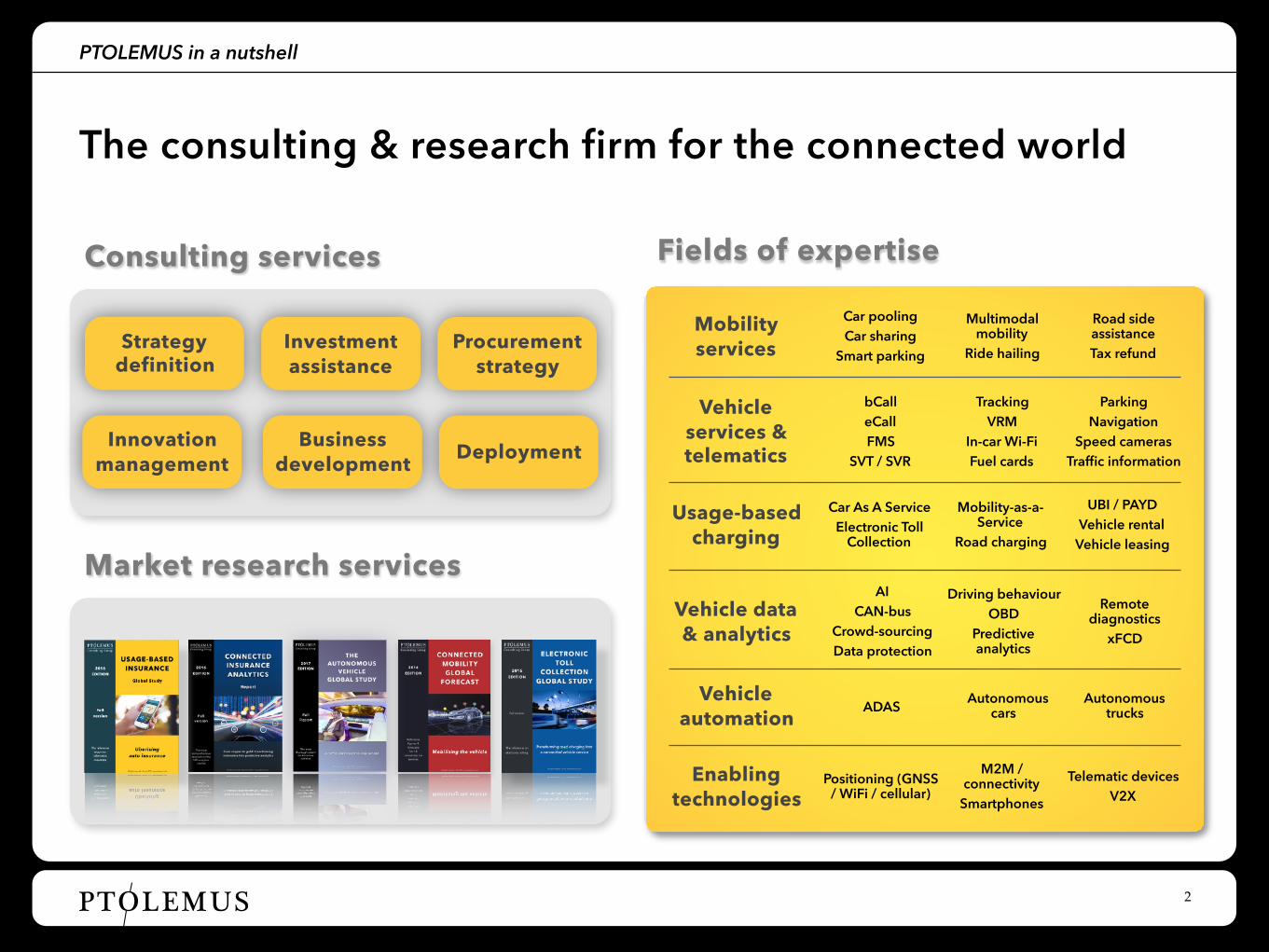

Strategy definition

Investment assistance

Innovation management

Business development

Consulting services

Procurement strategy

Deployment

PTOLEMUS in a nutshell

The consulting & research firm for the connected world

2

Fields of expertise

Fields of expertise

Car pooling Car sharing

Smart parking

Multimodal mobility

Ride hailing

Road side assistance Tax refund

Mobility services

Car As A Service Electronic Toll

Collection

Mobility-as-a-Service

Road charging

UBI / PAYD Vehicle rental

Vehicle leasing

Usage-based charging

AI CAN-bus

Crowd-sourcing Data protection

Driving behaviour OBD

Predictive analytics

Remote diagnostics

xFCD

Vehicle data & analytics

bCall eCall FMS

SVT / SVR

Tracking VRM

In-car Wi-Fi Fuel cards

Parking Navigation

Speed cameras Traffic information

Vehicle services & telematics

ADAS Autonomous cars

Autonomous trucks

Vehicle automation

Positioning (GNSS / WiFi / cellular)

M2M / connectivity

Smartphones

Telematic devices V2X

Enabling technologies

Market research services

PTOLEMUS

Device & location suppliers

PTOLEMUS in a nutshell

Our clients come from across the mobility ecosystem

3

Analytics, maps & applications providers

Mobile telecom operators

3RQWLDFW���� 3RQWLDFW�%RQHYLOOH����

$OID�5RPHR���� $OID�5RPHR��������

-HHS���� -HHS�&KHURNHH�������� -HHS�*UDQG�&KHURNHH�����9�

OBD2 Bluetooth Dongle basic compatible car models

<HDU 0DQXIDFWXUHU�0RGHO�(QJLQH�/LWHU�

0*�5RYHU���� 0*�5RYHU�PHPV��HFX���� 0*�=5����/���9

0LQL�&RRSHU���� 0LQL�&RRSHU�6����

6DDE���� 6DDE�������

/RWXV�3URWRQ����a 3URWRQ�*(1�����a 3URWRQ�6DYU\���� /RWXV�3URWRQ�6DYY\�������� /RWXV�3URWRQ�6DYY\�����$07

Telematics solution providers

Insurers, aggregators & assistance providers

Automotive manufacturers & suppliers

Fleet & fuel, ITS & regulators

Banks & private equity investors

2012 Directors’ report

(translation from the Italian original which remains the definitive version)

Financial Statements of the Company and the Group at 31 December 2012

27 March 2013

Legal and Administrative Office: 20121 Milan - Foro Buonaparte, 44

Fully paid-up share capital € 314,225,009.80 Tax Code and Milan Company Register no. 00931330583

www.itkgroup.com

!

PERFORMING THE RED FLAG DUE DILIGENCE OF

MEDIAMOBILE

Final proposal to TIME for Growth and Amundi Asset Management

1st June 2017 Ref. 2017-06-T4G-3 Strictly confidential

Final proposal to TIME for Growth and Amundi Private Equity Funds – 1st June 2017 - Strictly confidential - Ref. 2017-06-T4G-1 1PTOLEMUS, registered with the Belgian Corporate Registration Office under number 0820.589.316 Rue Cervantes 15 - Brussels 1190 - Belgium - www.ptolemus.com

PTOLEMUS

PTOLEMUS associations

In 2017, PTOLEMUS created The Autonomous Club (TAC)

4

T H E A U T O N O M O U S C L U B

Think tank Networking

Contribution to the

debateInsights

Key objectives

Research consortium

creation

Vision

An international, non-profit association jointly created by PTOLEMUS and Lysios Public Affairs

Status

• Connected & autonomous vehicles • All topics at the crossing of technology,

business, & regulatory domains

Scope

• Who will control & access connected autonomous vehicle data?

• Status of the Autonomous Vehicle market and key implications

• Fostering a European-wide liability framework for AVs

Recent subjectsCorporate members

Recent speakers

Note: Next meetings on 7th March and 5th June in Brussels

PTOLEMUS

PTOLEMUS is the premium quality provider of business intelligence on connected mobility

PTOLEMUS in a nutshell - Research

For more information and pricing details, please contact [email protected] 5

The most comprehensive

research on insurance analytics

The reference report on UBI, quoted by The Economist, the

Financial Times & the Wall Street

Journal

Reference figures &

forecasts for 14 connected car

services

The most thorough

analysis of ADAS and AVs

The reference on vehicle payment

services

The most comprehensive report on truck fleet services,

already quoted by the Financial Times

PTOLEMUS

• 600+ pages of research using: - 60 interviews in 8 countries - 12 months of research performed by 10

consultants - A uniquely precise and complete

methodology - over 200 figures (charts, tables, etc.)

• Assessment of the key factors affecting the start, the acceleration speed and the penetration of the different level of automation from today to 2030 - Overview of the regulatory background,

applicable regulation, evolution and trends globally

- Complete analysis of the technology building blocks including suppliers and cost analysis

- A global quantitative analysis of the mobility market and its role in delivering driverless cars

• 27 ADAS explained and their impact on claims analysed

• 21 OEMs and technology providers analysed and their AV strategy compared

• A qualitative & quantitative evaluation of the impacts of automation on - Safety - Personal data protection - Connected services - The automotive industry - The risk sector

• 2015-2030 bottom-up ADAS & AV market forecasts

- Global forecast over 18 markets - ADAS and AV penetration forecast by

level and car segment - Forecast on crash volumes and severity,

claims costs and insurance premiums

The most thorough investigation of the

driverless future

The Autonomous Vehicle Global Study quantifies the impact of ADAS & AVs on safety and on the ecosystem

PTOLEMUS in a nutshell - Research

6

PTOLEMUS

The autonomous trip starts with ADAS features

7

What are ADAS and autonomous functions?

Source: PTOLEMUS. *ADAS: Advanced Driver Assistance Systems

Assists Decides & executesAlerts Fully controlsImproves

•Night Vision System • Autonomous Park Assist

• Rear View System

• Rear View System • Parking Aid

• Remote Garage Parking• Road Sign Recognition• Adaptive High Beam

• Forward Collision Warning

• Predictive Pedestrian Protection

• Emergency Brake Assist

•Driver Monitoring System• Cognitive Distractions Detection

• Adaptive Cruise Control

• Highway Chauffeur

• Cooperative Adaptive Cruise Control

• Lane Departure Warning Assistant

• Lane Keeping Support

• Lane Change Assist

• Cross Traffic System

• Traffic Jam Assist

• City chauffeur

• Heads Up Display•Night Vision System

Lane control Cruise systems

Collision avoidance

Vision systems

Parking systems

Vital signs monitoring

• AEB cyclist• Side collision avoidance

• AEB pedestrian

• Rear Cross Traffic Alerts

PTOLEMUS

Autonomous vehicles (L4) will emerge in less than 5 years

8

Tesla Model 3

LEVEL 3

3D / HD maps

Full liability

Advanced Cruise Control

2017

LEVEL 4

Mercedes E Class

Lidar, V2V, V2I

Partial liability

Autonomous car

2021

LEVEL 5

Rolls-Royce Vision Next 100

Full AI HA GNSS

No liability

Driverless car

2030?

LEVEL 4 DRIVERLESS

Navya Arma shuttle

Lidar, V2V, V2I

No liability

Driverless car

2021

Driver responsibility

Defining application

Enabling technologies

LEVEL 2

Sensors (Camera, radar)

ADAS

Ford Focus 2016

Launch date

Example

Full liability

2010

What are ADAS and autonomous functions?

Source: PTOLEMUS

PTOLEMUS Source: PTOLEMUS market forecasts 9

Market forecast - Adoption

Penetration in passenger cars on the road (%, Europe) Rationale and comments

0%

10%

20%

30%

40%

50%

2015 2020 2025 2030

Driver assistance L1Partial automation L2Conditional automation L3High automation L4 driven

In Europe, ADAS/AV penetration will reach 37% by 2030

• By 2024, we expect the number of level 2 passenger cars in Europe to exceed vehicles with (L1) driver assistance features

• L2 cars will grow their share beyond 10% mark by 2023 and will reach 20% by 2028

• From 2018 to 2020, L3 cars will be introduced in most EU countries, starting with the executive segments. Progressively, news cars sold in the upper and lower medium segments will become L3

• Most L3 cars are going to be on the road of the UK and Germany by 2030

Strictly

reserved fo

r internal u

se

of BBBB. D

istrib

ution to

third

parties is

prohibited.

Strictly

reserved fo

r internal u

se

of BBBB. D

istrib

ution to

third

parties is

prohibited.

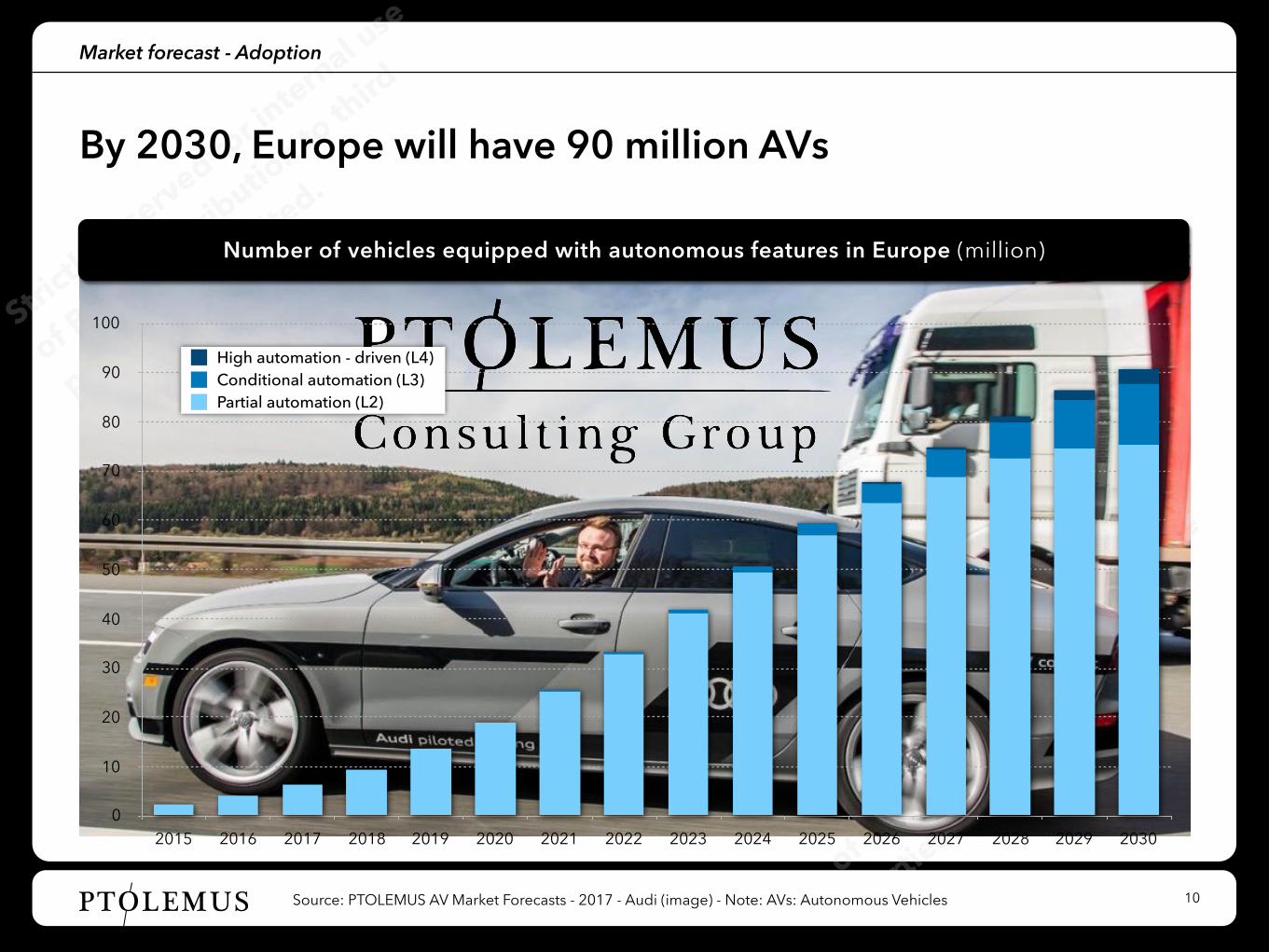

PTOLEMUS Source: PTOLEMUS AV Market Forecasts - 2017 - Audi (image) - Note: AVs: Autonomous Vehicles 10

Number of vehicles equipped with autonomous features in Europe (million)

Market forecast - Adoption

0

10

20

30

40

50

60

70

80

90

100

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030

Partial automation (L2)Conditional automation (L3)High automation - driven (L4)

By 2030, Europe will have 90 million AVs

Strictly

reserved fo

r internal u

se

of BBBB. D

istrib

ution to

third

parties is

prohibited.

Strictly

reserved fo

r internal u

se

of BBBB. D

istrib

ution to

third

parties is

prohibited.

PTOLEMUS

In the short term, frontal collision avoidance ADAS will have the greatest impact on reducing vehicle risk

11

Impact of ADAS categories on claims losses reduction - Example of Germany

ADAS impact on claims reduction

Source: PTOLEMUS - *Most damages occur from vehicles reversing out of a parking space, rather than moving into a parking space (Allianz data)

Parking

Lateral collisionavoidance

Cross traffic

Frontal collision avoidance

Advanced-ACC

Highway chauffeur

City chauffeur

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

PTOLEMUS Source: PTOLEMUS market forecasts 12

ADAS impact on claims reduction

US crashes avoided thanks to ADAS & autonomy Rationale and comments

• ADAS has the biggest impact on safety

• Autonomy will not only mitigate crashes, it will avoid many crashes altogether

• L4 vehicles have the greatest potential to reduce crashes but low penetration will limit its overall impact until 2030

• ADAS will still be responsible for the majority of crashes avoided in 2030

• L3 and L4 have a much higher potential of accident avoidance, so will grow much faster after 2030

Nearly 800,000 crashes avoided every year in the US!

L3L2L1 L4

PTOLEMUS

Food for thought

The end of auto insurance?

Merci!

• The impact of autonomy and ADAS on collisions will be considerable in all advanced countries

• Our estimates show that the increase in accident costs due to ADAS equipment costs will be more than compensated by reduction in claims frequency

• However, we do not expect product liability to replace car insurance

• Policyholders will still require independent insurers to claim against any OEM system failures

13

PTOLEMUS Consulting Group

S t r a t e g i e s f o r M o b i l e C o m p a n i e s

Brussels - Boston - Chicago - Düsseldorf London - Milan - New York - Moscow Paris - Pretoria - Toronto

[email protected] www.ptolemus.com @PTOLEMUS

Frédéric Bruneteau Managing Director [email protected] +32 487 96 19 02