Le sfide della transizione energetica italiana Una ...

13

Francesco Gracceva Elena De Luca ENEA Le sfide della transizione energetica italiana Una valutazione quantitativa Le sfide per la transizione energetica del futuro Milano, 1 dicembre 2017, Sala Azionisti Edison

Transcript of Le sfide della transizione energetica italiana Una ...

Francesco Gracceva Elena De Luca ENEA

Le sfide della transizione energetica italiana Una valutazione quantitativa

Le sfide per la transizione energetica del futuro Milano, 1 dicembre 2017, Sala Azionisti Edison

1. Urgenza vs inerzia del sistema: • Slow rates of change in capital (and

infrastructure) intensive energy systems. Historical energy transitions have taken many decades: changeover times 80 to 130 years (Grubler 2012)

• Inertia of socio-technical configurations: disruptive technologies co-evolve with shifts in markets, regulations, infrastructure, user practices, industrial networks, cultural meaning and scientific understanding (Geels 2002)

• Nuove frontiere tecnologiche il cui successo dipende dall’interdipendenza delle decisioni degli operatori nelle diverse fasi delle nuove filiere produttive. (…) Per ogni filiera un reticolato di mille decisioni sequenziali e iterative (Clô 2017)

Interrogativi e sfide della transizione (1/3)

Geels, 2002

Grubler, 2012

Relatore

Note di presentazione

A formal metric was proposed by Marchetti and Nakicenovic (1979) using a set of coupled logistic equations, where the changeover time, or Dt is the time to grow (or decline) from 1 to 50%, or from 10 to 90% market share. Thus a full growth cycle in terms of relative market share spans 2 Dt’s

2. Incentivi: • Low-carbon transition could not imply lower

costs and better quality of energy services: ‟Historically, the important drivers for the energy transitions were the opportunity to produce cheaper and/or better energy services. In a majority of cases, a successful new energy source or technology provided the same service (i.e. heating, power, transport or light) with superior or additional characteristics (e.g. easier, cleaner or more flexible to use)” (Fouquet 2016)

• Diversamente da altre disruptive technologies come internet o telefonia mobile i consumatori possono non vederne i benefici nel breve termine (Clô 2017)

• Necessarie politiche al di fuori di logiche di mercato per assicurare redditività agli enormi investimenti? (Clô 2017)

Interrogativi e sfide della transizione (2/3)

Fouquet, 2016

Relatore

Note di presentazione

A formal metric was proposed by Marchetti and Nakicenovic (1979) using a set of coupled logistic equations, where the changeover time, or Dt is the time to grow (or decline) from 1 to 50%, or from 10 to 90% market share. Thus a full growth cycle in terms of relative market share spans 2 Dt’s

3. Fattibilità tecnologica e trade-offs • A number of challenges were not addressed at the time of the 2009 climate and energy package. (…) The

management challenges linked to the introduction of renewables (…). The Third Energy package (…) did not address the issue of whether the market offered the necessary incentives to invest in a system with greater shares of RES.

• The current climate and energy targets were designed to be mutually supporting and there are indeed interactions between them. (…) There are obvious synergies but there are also potential trade-offs. (…) the lack of overall consistency between policies (…) the need to improve the cost-efficiency of various climate and energy measures (…). The policies have been criticised for having a negative impact on energy prices, adversely impacting affordability of energy for vulnerable households and the competitiveness of energy intensive sectors (COM(2013) 169 final).

Interrogativi e sfide della transizione (3/3)

Jacobson et al, 2017

• Modelli e scenari • Indicatori:

– Indice ISPRED/ENEA: indice sintetico del trilemma (interdipendenze e trade-off); confronto con target 2020 e 2030; scomposizione sicurezza energetica; confronto con principali Paesi UE; dati infra-annuali

– Indicatori Energy Union: no indice sintetico; 5 dimensioni (trilemma + efficienza energetica + R&S); valutazione decarbonizzazione vs target 2020

– WEC: indice sintetico del trilemma (interdipendenze e trade-off); ottica globale, confronta la posizione relativa di oltre 100 Paesi; non include valutazione trend vs target nazionali; componente di contesto Paese

Valutare la transizione

Boston, 2013

Relatore

Note di presentazione

The Energy Union aims to ensure that EU consumers have secure, affordable, competitive and sustainable energy. It is made up of five closely related and mutually reinforcing dimensions, progress against which should also be measured through key indicators. (…) to transparently inform on past developments, including potential discrepancies with Energy Union objectives, while allowing for the anticipation of future trends and potential impacts of policy options. This way, inconsistencies between market and policy developments and overall objectives can be detected at an early stage, allowing for swift implementation of response measures at EU and Member State level

6

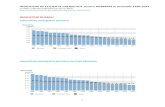

Indice Sicurezza energetica, Prezzo Energia e Decarbonizzazione, 27 indicatori, 3 dimensioni • Ultimi due anni discontinuità nella transizione energetica italiana. Ragioni strutturali (insieme a fattori

congiunturali) dietro al rallentamento della decarbonizzazione: ritorno alla crescita, caduta prezzi petrolio/gas; frenata dell’incentivazione delle rinnovabili elettriche

• Alcuni risvolti positivi: miglioramenti sui prezzi; effetti positivi della ripresa del gas sul mercato elettrico. Ma con la parziale ripresa della domanda di gas riemerse fragilità dei sistemi elettrico e gas

• Negli anni 2011-2016 indicazioni di possibili trade-off fra le tre dimensioni del trilemma

ISPRED – Le tre dimensioni del trilemma

0.00.10.20.30.40.50.60.70.80.91.0

I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II

2011 2012 2013 2014 2015 2016 2017

Decarbonizzione Sicurezza Prezzi energia industria

Fine recessione e leggera ripresa; Calo prezzo petrolio e gas naturale 2015 e 2016 meno caldi del 2014

TRADE-OFF DECARB./PREZZI

Forte aumento accise

TRADE-OFF DECARB./SICUREZZA SISTEMA ELETTRICO E PETROLIF.

Progressi mercati elettricità/gas; Chiusura centrali e raffinerie

PEGGIORANO DECARB. E SICUREZZA DEL SISTEMA ELETTRICO E GAS

Forti cali di PIL, prod. Ind. (2012-13) e traffico merci (2011-12); Alto prezzo del petrolio

Forte crescita FRNP (2011-14); calo prod. el., alto idro (2013-14) I e IV trimestre 2014 molto miti

Aumento oneri di sistema

Crisi nucleare FR Calo idro

ACP applicata agli indicatori ISPRED – anni 2011-2016

7

• ISPRED: soddisfazione parziale del trilemma, valore assoluto < 0.5 (range 0-1); trend in miglioramento dal 2011 al 2015, in peggioramento dal 2015 ad oggi

• Indice WEC: buona soddisfazione del trilemma, tripla A costante (range A-D); indice in leggero miglioramento dal 2015 al 2017

Valutare il trilemma energetico

-30%

-20%

-10%

0%

10%

20%

30%

0.30

0.40

0.50

0.60

0.70

I II III IV I II III IV I II III IV I II III IV I II III IV I II III IV I II

2011 2012 2013 2014 2015 2016 2017

Variazione % tendenziale (asse dx) ISPRED (asse sin)

8

Energy markets / Energy prices / Competitiveness

• ISPRED: confronto dei prezzi italiani pagati dall’industria con i prezzi degli altri principali Paesi UE; situazione stabilmente critica soprattutto per le fasce di consumo basse, in particolare per l’energia elettrica

• Indicatori Energy Union: variazione prezzi (legati ai mercati internazionali energia); includono concentrazione mercato e prezzi per i consumatori

• WEC: dimensione più critica delle tre; include accesso all’energia e qualità dell’offerta

2016 7%

2014-16 0%

2015 815

2005-2015 -60.5%

2015 2924

2011-2015 39.7%2015 52.3

2013-2015 -16.9%2015 22.2

2013-2015 -20.9%

2015 8%

2009-2015 6%

2015 6.1%

2009-2015 4.8%

2014 7.1%

2005-2014 n.a.

cons

umer

sIn

terc

onne

ctio

n &

who

lesa

le m

arke

t fu

nctio

ning

IM1: Electricity interconnection capacity

IM3: Market concentration index for wholesale gas supply

IM4: Wholesale electricity prices

IM5: Wholesale gas prices

IM2: Market concentration index for power generation

IM6: Annual switching rates -electricity (household customers)

IM7: Annual switching rates - gas household customers)

IM8: Energy affordability - energy expenditure share in final consumption expenditure for the lowest quintile

A fu

lly in

tegr

ated

inte

rnal

ene

rgy

mar

ket

9

Energy security

2014 75.9%

2005-2014 -7.5%

2014 13.3

2005-2014 -2.32016 105.5%

2009-2016 -18.5%Gas

Impo

rt

depe

nden

ce SoS1: Net import dependency

SoS2: Aggregate supplier concentration index

SoS3: N-1 rule for gas infrastructureEner

gy se

curit

y,

solid

arity

and

trus

tValore II 2017

Valore indicatore

Tendenza breve

periodo

Tendenza medio

periodoDipendenza ponderata con

% petrolio su CIL33.2% 0.49 ↔ ↔

Diversif icazione approvvigionamenti (HHI)

0.14 0.76 ↑ ↑

Approvvigionamento prodotti petroliferi

Copertura domanda benzina-gasolio 1.4 0.90 ↔ ↔

Margini di raff inazione ($/bl) 3.9 0.64 ↑ ↑

Utilizzo impianti (%) 77% 0.47 ↑ ↑Dipendenza dall'import

ponderata con il peso del 35% 0.00 ↓ ↓

Diversif icazione approvvigionamenti (HHI) 0.27 0.63 ↔ ↓

Adeguatezza sistema gas

Eccesso capacità import su domanda (%)

18% 0.40 ↓ ↑

Spread PSV-TTF (€/MWh) 2.5 0.00 ↓ ↑

Liquidità PSV (TWh) 214 0.19 ↔ ↑Adeguatezza

sistema elettricoIndice capacità in eccesso 41% 0.53 ↓ ↓

Flessibilità sistema elettrico

Indice ENTSO-E 9.9% 0.51 ↔ ↓

Adeguatezza mercato elettrico

Spark spread (€/MWh) 7.59 0.42 ↑ ↓

Competitività raff inazione

Sicurezza del sistema energetico

Adeguatezza mercato gas

Resilienza sistema

petrolifero

Resilienza sistema gas

naturale

• ISPRED: quadro variegato per la multidimensionalità della sicurezza energetica pluralità di mercati, segmenti supply chain e orizzonti temporali: indicatori di resilienza e flessibilità per il breve termine, indicatori di adeguatezza dei segnali del mercato per gli investimenti nel lungo termine

• Indicatori Energy Union: confrontabilità per i 28 paesi UE, rappresentazione sintetica; mancano raffinazione e sistema elettrico (intermittenza), indicatori di adeguatezza

• WEC: confrontabilità per i 92 paesi WEC, manca dettaglio su raffinazione, adeguatezza sistemi elettrico e gas, intermittenza sistema elettrico

10

Decarbonisation / Environmental sustainability

DecarbonizzazioneValore II 2017

Valore indicatore

Tendenza breve

periodo

Tendenza medio

periodoProiezione emissioni CO2 al 2020

distanza dal target (Mt)-8 0.62 ↓ ↑

Proiezione emissioni CO2 non-ETS 2020 distanza dal target (Mt)

-14 0.83 ↓ ↑

Proiezione sviluppo FER al 2020 19% 0.95 ↓ ↑

Proiezione emissioni CO2 al 2030 distanza dal target (Mt)

3 0.55 ↓ ↑

Proiezione emissioni CO2 non-ETS 2030 distanza dal target (Mt)

14 0.44 ↓ ↑

Proiezione sviluppo FER al 2030 22% 0.26 ↓ ↓

DE1: GHG emissions reductions (base year=1990)

1990-2015 -16.3%

DE2: Gap between GHG emissions projections and 2020 target in Effort Sharing sectors

gap 2020 -5.4%

DE3: Gap between latest (proxy) inventory of Effort Sharing emissions and interim targets

gap interim 2015

-9.4%

2015 2841990-2015 -28.6%

2014 17.1%2014 -8.2%2014 -0.1%

DE4: GHG intensity of the economy

GHG

em

isio

ns

DE5: Renewable energy shareRESDe

carb

onis

atio

n of

eco

nom

y

• ISPRED: proiezione emissioni totali e settori ESD al 2020 e al 2030 vs obiettivi; proiezione sviluppo FER al 2020 e al 2030 vs obiettivi

• Indicatori Energy Union: scostamenti di GHG e FER rispetto al target 2020; dati relativi al 2014 (confermati nel 2016)

• WEC: indici di intensità delle emissioni e dei consumi finali (storicamente bassi in Italia); no FER; no confronto con obiettivi 2030 (ottica globale)

• ‟Nel 2016, in un contesto internazionale segnato da un rafforzamento dell’attività economica mondiale e da bassi prezzi delle materie prime, l’Italia ha proseguito il suo percorso di rafforzamento della sostenibilità sociale ed ambientale, dell’efficienza e della sicurezza del proprio sistema energetico”

Gli obiettivi al 2030 in linea con il Piano dell’Unione dell’Energia: • raggiungere e superare gli obiettivi ambientali e di decarbonizzazione UE:

– Phase-out carbone entro il 2025 – FER al 28% via politiche abilitanti e semplificazioni (dal 2020), veicoli elettrici (5 mln) – 10 Mtep/a di efficienza via riqualificazione edifici, riduzione mobilità, standard emissivi

• migliorare la competitività del Paese: – Convergenza mix generazione con altri UE – Corridoio liquidità

• continuare a migliorare la sicurezza di approvvigionamento e la flessibilità di sistemi e infrastrutture: – Capacity market – Piano Terna di investimenti per flessibilità – Nuovi gasdotti senza contributi a carico della finanza pubblica, nuovi stoccaggi attesi

Strategie per la transizione: la SEN 2017 ?

13

• Boston A., Delivering a secure electricity supply on a low carbon pathway, Energy Policy 52(2013) • Clack C.T. M. et al., Evaluation of a proposal for reliable low-cost grid power with 100% wind, water, and

solar, Proceedings of the National Academy of Sciences of the United States of America (PNAS), June 27 2017

• Clô A., Energia e clima, Il Mulino, 2017 • EC, GREEN PAPER, A 2030 framework for climate and energy policies, COM(2013) 169 final • EC, Second Report on the State of the Energy Union, COMMISSION STAFF WORKING DOCUMENT,

Monitoring progress towards the Energy Union objectives – key indicators, SWD(2017) 32 final, Brussels, 1.2.2017

• ENEA, Analisi trimestrale del sistema energetico italiano, (http://www.enea.it/it/seguici/pubblicazioni/analisi-trimestrale-del-sistema-energetico-italiano/analisi-trimestrale-del-sistema-energetico-italiano)

• Fouquet R., Lessons from energy history for climate policy: Technological change, demand and economic development, Energy Research & Social Science 22 (2016) 79–93, 2016

• Geels F.W., Technological transitions as evolutionary reconfiguration processes: a multi-level perspective and a case-study, Research Policy 31 (2002) 1257–1274, 2002

• Grubler A., Energy transitions research: Insights and cautionary tales, Energy Policy50(2012)8–16, 2012

• Jacobson et al., 100% Clean and Renewable Wind, Water, and Sunlight All-Sector Energy Roadmaps for 139 Countries of the World, Joule 1, 108–121 September 6, 2017

• WEC, World Energy Trilemma Index 2017

Bibliografia