KL Gates Building Bridges III - Tufts Fletcher...

9

Jolanta Wysocka | CEO Mountain Pacific Group www.mountainpacificgroup.com KL Gates Building Bridges III Innovations in Infrastructure Investment Platforms and the role of PPPs Washington, DC November 6, 2015

Transcript of KL Gates Building Bridges III - Tufts Fletcher...

Jolanta Wysocka | CEO Mountain Pacific Group www.mountainpacificgroup.com

KL Gates Building Bridges III Innovations in Infrastructure Investment Platforms and the role of PPPs Washington, DC November 6, 2015

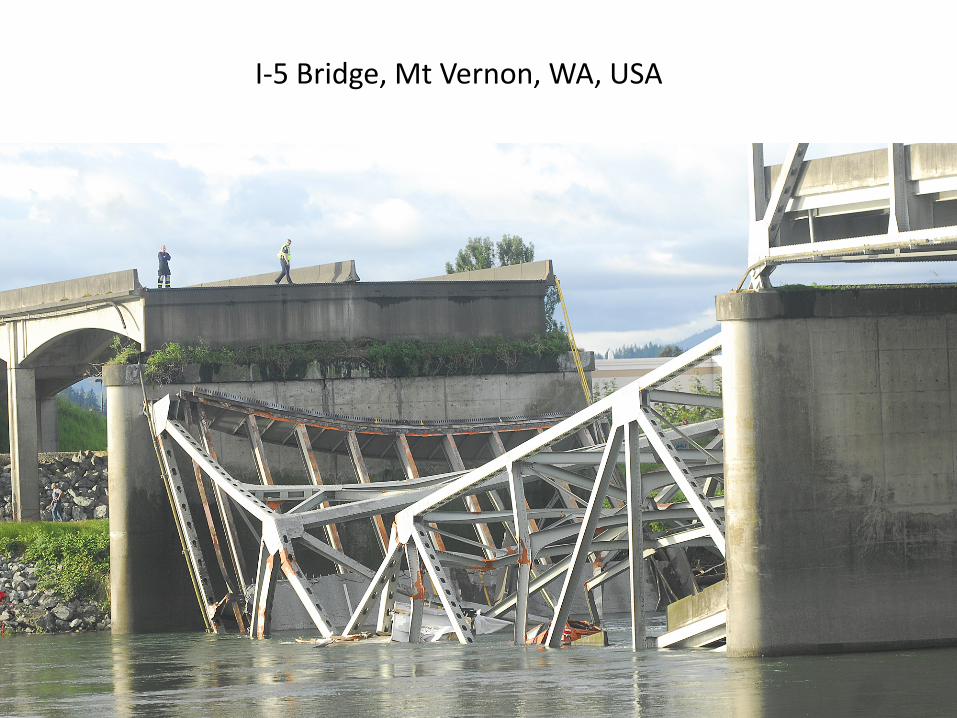

I-5 Bridge, Mt Vernon, WA, USA

Banqiao Dam Failure, China - 231,000 dead • 64 dams failed • 6 miles wide and 9-23 feet high wave sped downwards at 31 mph • It wiped out an area 30 miles long and 10 kilometers wide

Data Source: FRED, October 2015

Total Public Construction Spending as Percent of GDP, USA

1.50%

1.70%

1.90%

2.10%

2.30%

Infrastructure Development Models

• Public Sector – Most of the infrastructure development today is paid out

of public budget. Sponsor engages in procurement and may issue bonds to finance the project

– Private sector’s participation limited to providing the funds

• PPP – tapping private sector resources in designing, implementing and managing the projects – Public Sector – specify what needs to be done – Private Sector – implement, manage and finance – Public Sector – subsidize, if needed

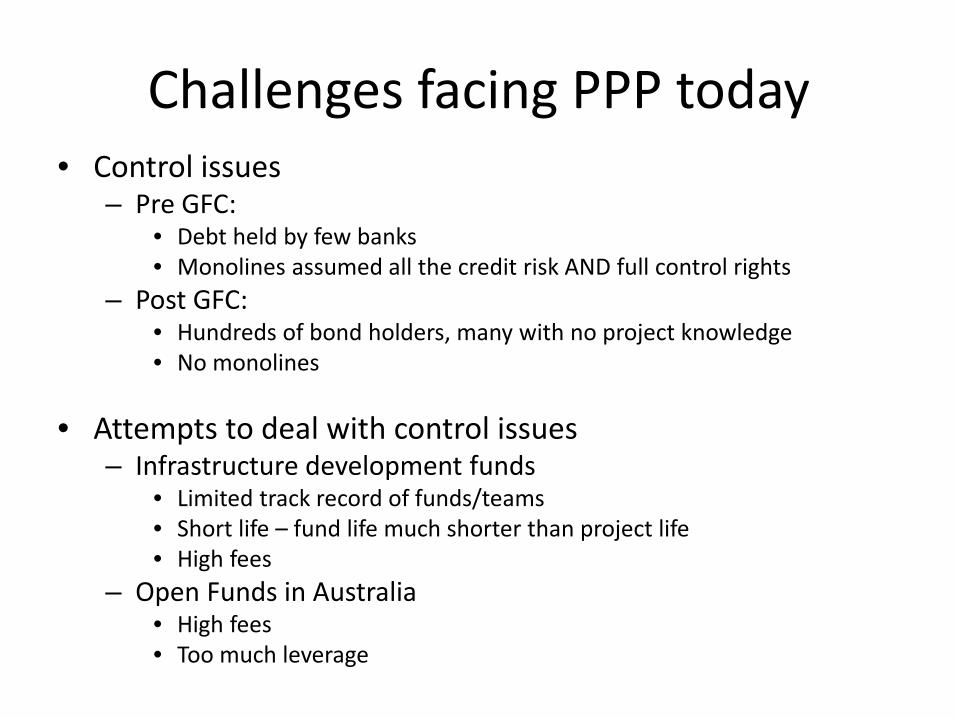

Challenges facing PPP today • Control issues

– Pre GFC: • Debt held by few banks • Monolines assumed all the credit risk AND full control rights

– Post GFC: • Hundreds of bond holders, many with no project knowledge • No monolines

• Attempts to deal with control issues

– Infrastructure development funds • Limited track record of funds/teams • Short life – fund life much shorter than project life • High fees

– Open Funds in Australia • High fees • Too much leverage

PPP in Emerging Markets

• “Sweet spot” - middle income countries: Chile, Colombia, Peru – “Need” is not a good predictor of returns

• Today compared to the 90’s – Local currency financing - “original sin” – Low inflation - high inflation – Benchmark 15-20y government yields available

• IFC, the World Bank and the local partners mitigate the risks

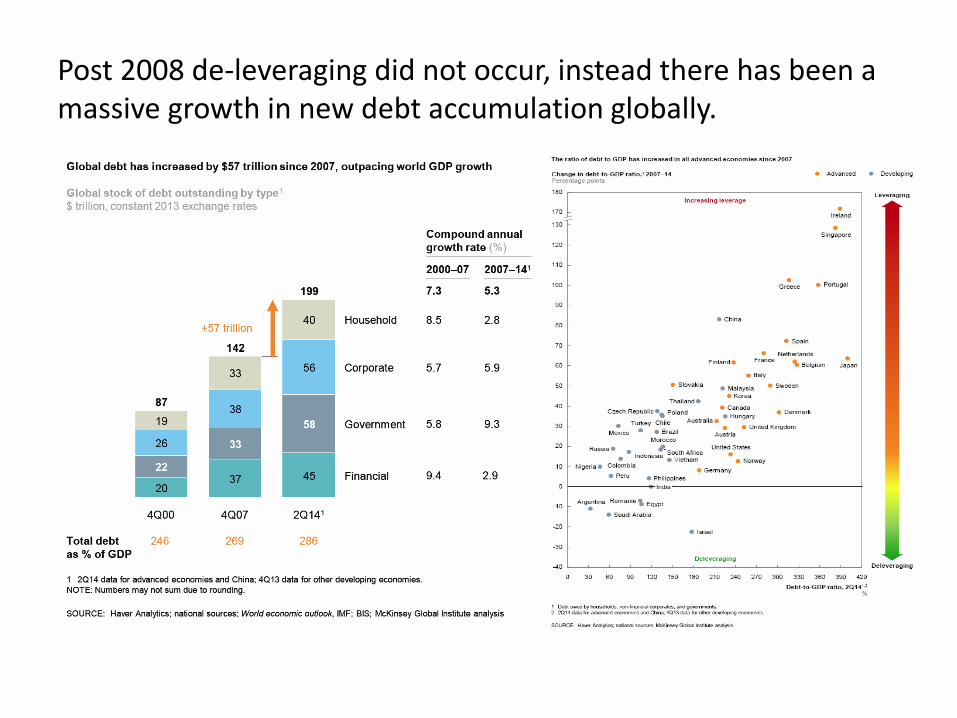

Post 2008 de-leveraging did not occur, instead there has been a massive growth in new debt accumulation globally.

Summary • Pension funds are looking at infrastructure in search of long

duration assets with good yield, and preferably inflation protection. • Unconventional monetary policies are distorting the price of risk • Current yields do not adequately compensate for illiquidity, political

and structural risks • Beware of hidden fees and expenses • Avoid excessive leverage on fund/project level. • Local institutions and super nationals are very helpful partners • Devil is in (deal) details - structuring, such as floating rate debt, can

adversely impact economics • Expert legal advice, including local legal advice, is critical in making

sure incentives are properly aligned and investor’s interests are protected