Kiessling, Ed Dec 0704

26

Presented By: Ed Kiessling President & COO, Commerce Insurance Services

-

Upload

global-interdependence-center -

Category

Documents

-

view

223 -

download

1

description

Presented By: Ed Kiessling President & COO, Commerce Insurance Services (Premium + Return On Invested Assets) - (Losses + Operating Expenses) • The Profit Formula and Operating Measures: –Combined RatioCombinedRatio –Profit Profit INSURANCE BEFORE 9/11 --INSURANCEBEFORE9/11-- THE PERFECT STORMTHEPERFECTSTORM • So, What Does This Mean?

Transcript of Kiessling, Ed Dec 0704

Presented By: Ed Kiessling

President & COO, Commerce Insurance Services

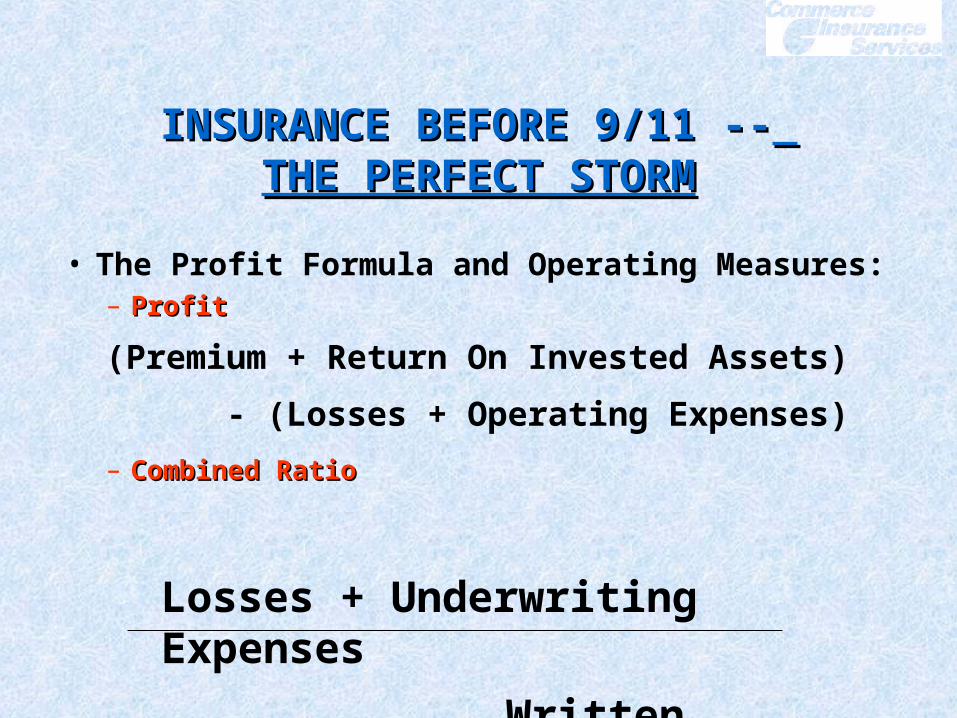

• The Profit Formula and Operating Measures:– ProfitProfit

(Premium + Return On Invested Assets)

- (Losses + Operating Expenses)– Combined RatioCombined Ratio

INSURANCE BEFORE 9/11 --INSURANCE BEFORE 9/11 -- THE PERFECT STORMTHE PERFECT STORM

Losses + Underwriting Expenses Written Premium

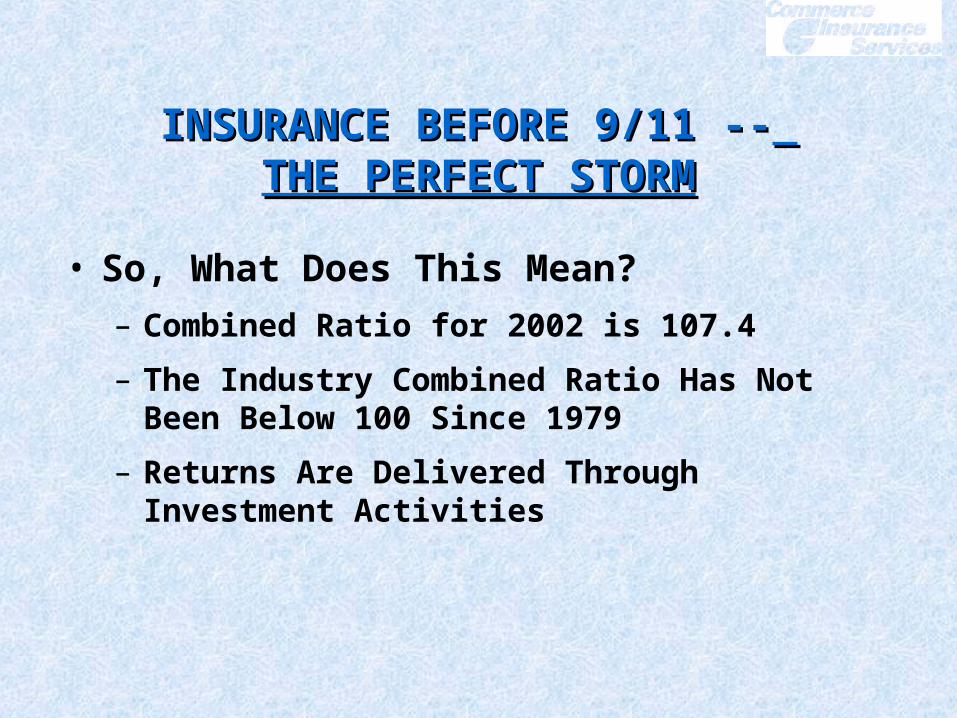

• So, What Does This Mean?– Combined Ratio for 2002 is 107.4

– The Industry Combined Ratio Has Not Been Below 100 Since 1979

– Returns Are Delivered Through Investment Activities

INSURANCE BEFORE 9/11 --INSURANCE BEFORE 9/11 -- THE PERFECT STORMTHE PERFECT STORM

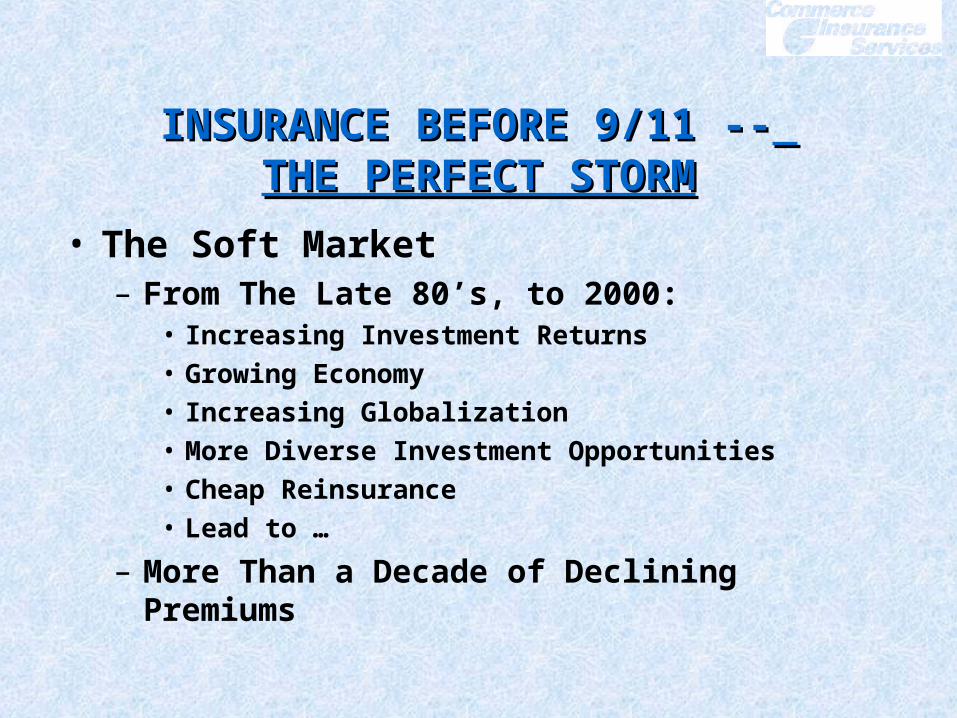

• The Soft Market– From The Late 80’s, to 2000:

• Increasing Investment Returns• Growing Economy• Increasing Globalization• More Diverse Investment Opportunities• Cheap Reinsurance• Lead to …

– More Than a Decade of Declining Premiums

INSURANCE BEFORE 9/11 --INSURANCE BEFORE 9/11 -- THE PERFECT STORMTHE PERFECT STORM

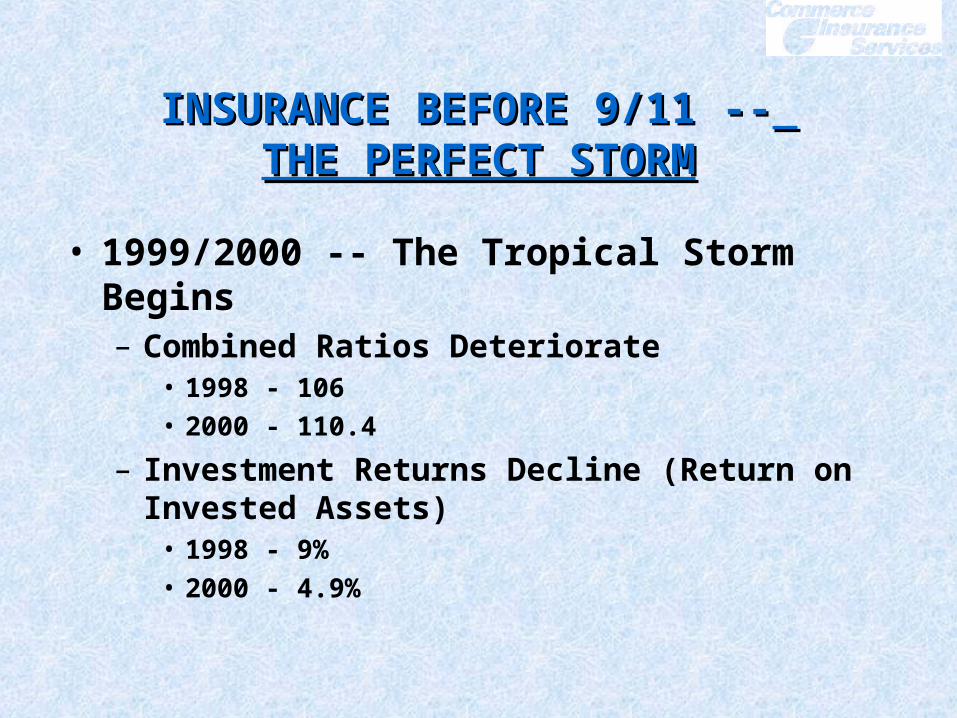

• 1999/2000 -- The Tropical Storm Begins– Combined Ratios Deteriorate

• 1998 - 106• 2000 - 110.4

– Investment Returns Decline (Return on Invested Assets)• 1998 - 9%• 2000 - 4.9%

INSURANCE BEFORE 9/11 --INSURANCE BEFORE 9/11 -- THE PERFECT STORMTHE PERFECT STORM

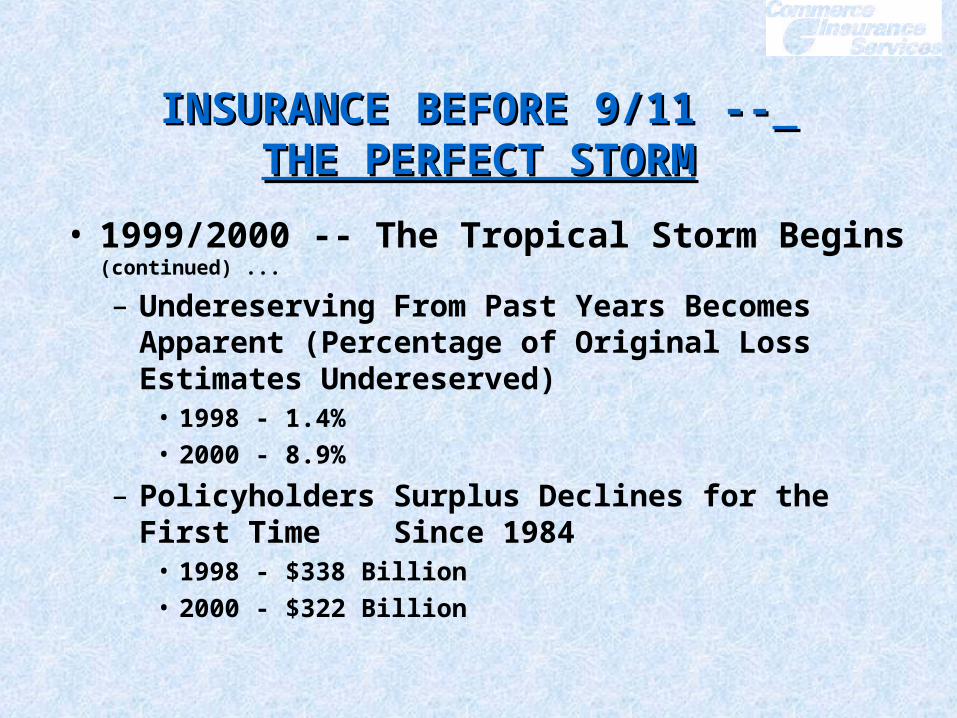

• 1999/2000 -- The Tropical Storm Begins (continued) ...

– Undereserving From Past Years Becomes Apparent (Percentage of Original Loss Estimates Undereserved)

• 1998 - 1.4%• 2000 - 8.9%

– Policyholders Surplus Declines for the First Time Since 1984

• 1998 - $338 Billion• 2000 - $322 Billion

INSURANCE BEFORE 9/11 --INSURANCE BEFORE 9/11 -- THE PERFECT STORMTHE PERFECT STORM

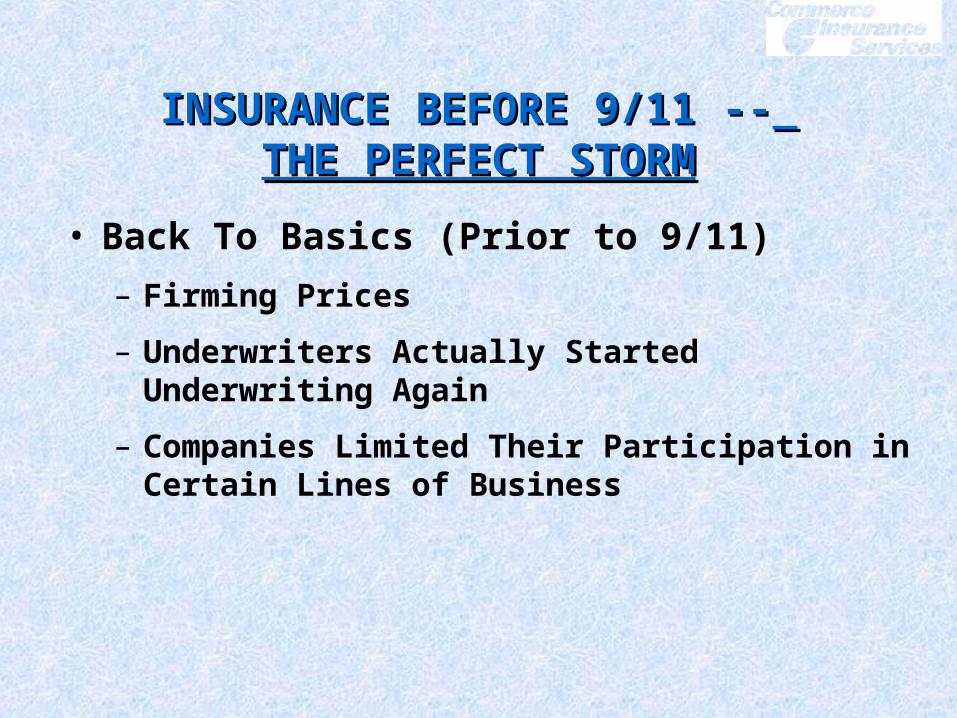

• Back To Basics (Prior to 9/11)– Firming Prices

– Underwriters Actually Started Underwriting Again

– Companies Limited Their Participation in Certain Lines of Business

INSURANCE BEFORE 9/11 --INSURANCE BEFORE 9/11 -- THE PERFECT STORMTHE PERFECT STORM

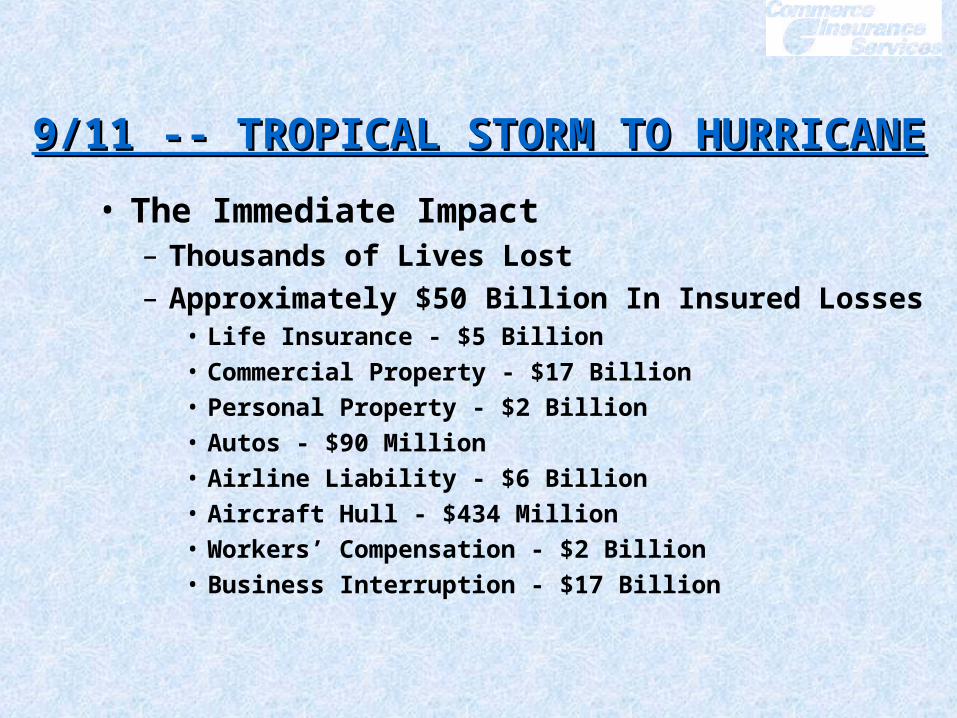

• The Immediate Impact– Thousands of Lives Lost– Approximately $50 Billion In Insured Losses

• Life Insurance - $5 Billion• Commercial Property - $17 Billion• Personal Property - $2 Billion• Autos - $90 Million• Airline Liability - $6 Billion• Aircraft Hull - $434 Million• Workers’ Compensation - $2 Billion• Business Interruption - $17 Billion

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

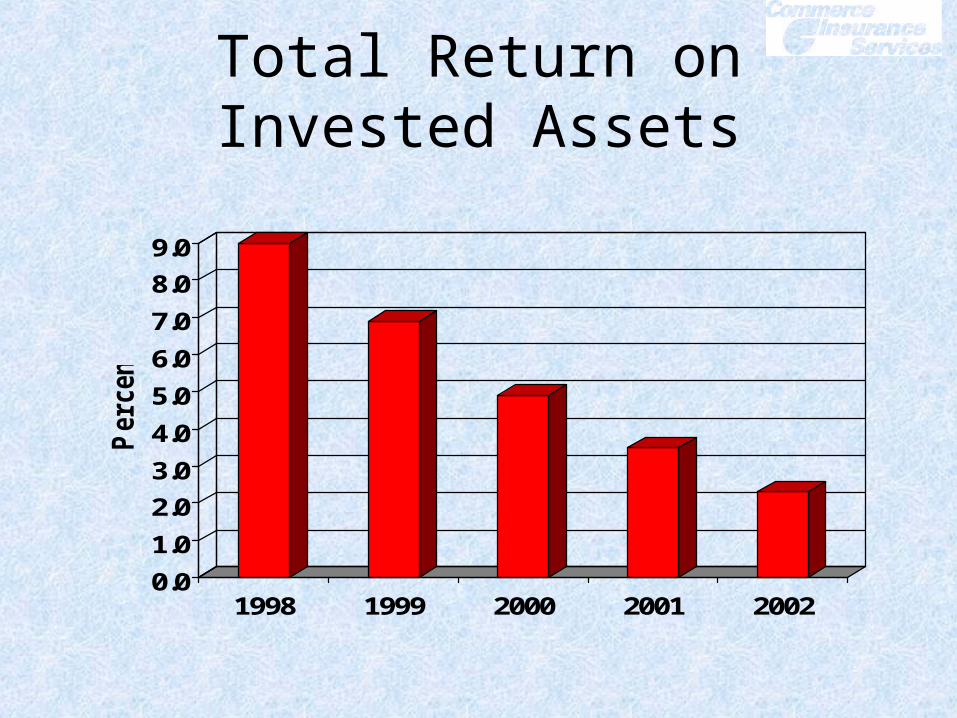

• The Collateral Damage Continues

– Investment Market Collapse

– Slowing Economy

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

Total Return on Invested Assets

0.01.02.03.04.05.06.07.08.09.0

Perc

ent

1998 1999 2000 2001 2002

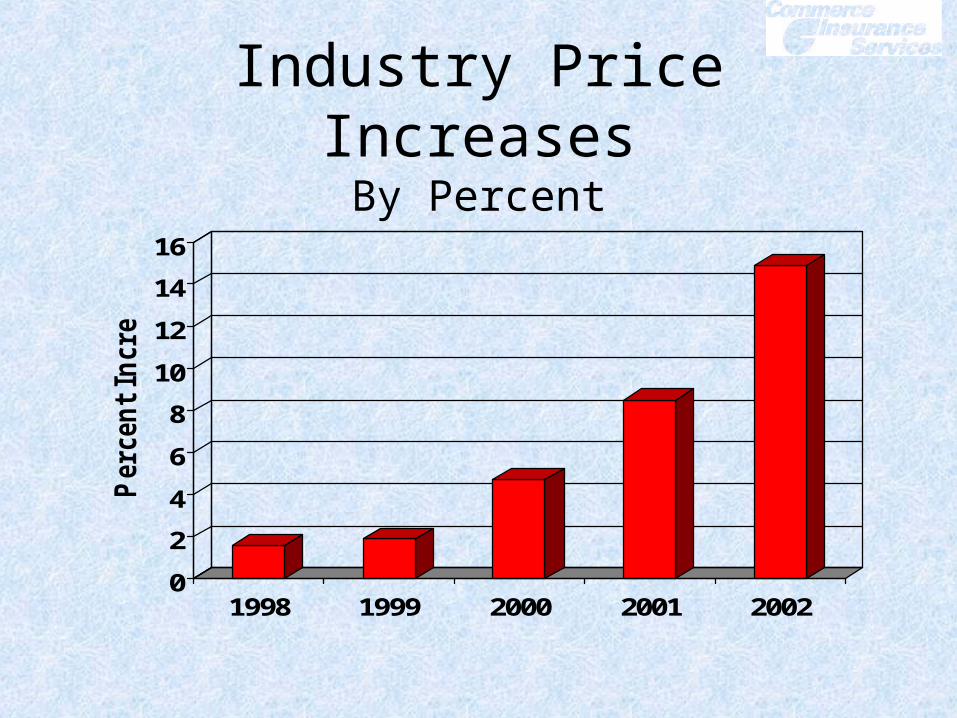

• The Post 9/11 Insurance World

– Rapidly Increasing Prices for the Last Two Years

• 15% to 100%

– Severe Limitations in Reinsurance Capacity and Dramatic Price Increases for Reinsurance

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

Industry Price IncreasesBy Percent

0

2

4

6

8

10

12

14

16

Perc

ent I

ncre

ase

1998 1999 2000 2001 2002

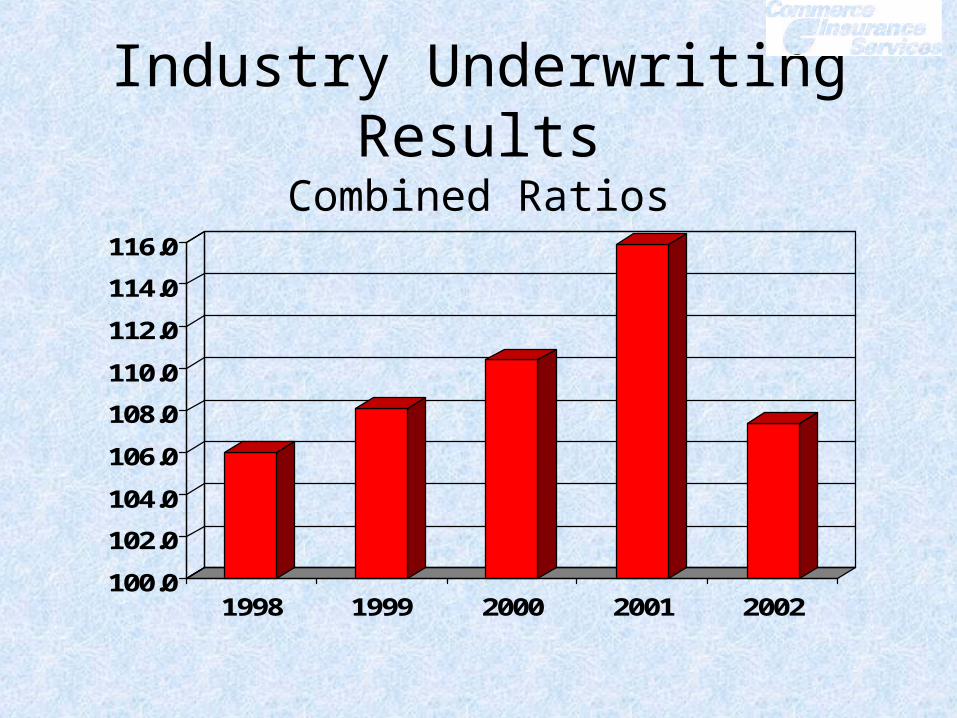

• The Post 9/11 Insurance World

– Industry Focus on Underwriting for the First Time in Over a Decade

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

Industry Underwriting ResultsCombined Ratios

100.0

102.0

104.0

106.0

108.0

110.0

112.0

114.0

116.0

1998 1999 2000 2001 2002

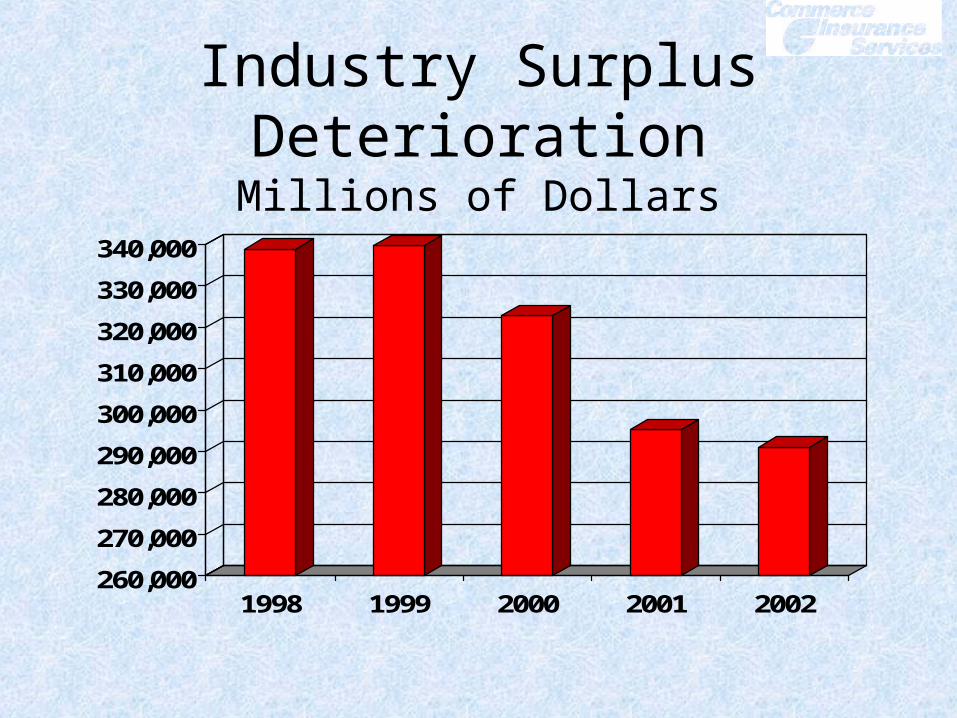

• The Post 9/11 Insurance World– Many Companies Came Into 2002 With Serious

Balance Sheet Problems; Balance Sheet Repair Became a Priority

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

Industry Surplus DeteriorationMillions of Dollars

260,000

270,000

280,000

290,000

300,000

310,000

320,000

330,000

340,000

1998 1999 2000 2001 2002

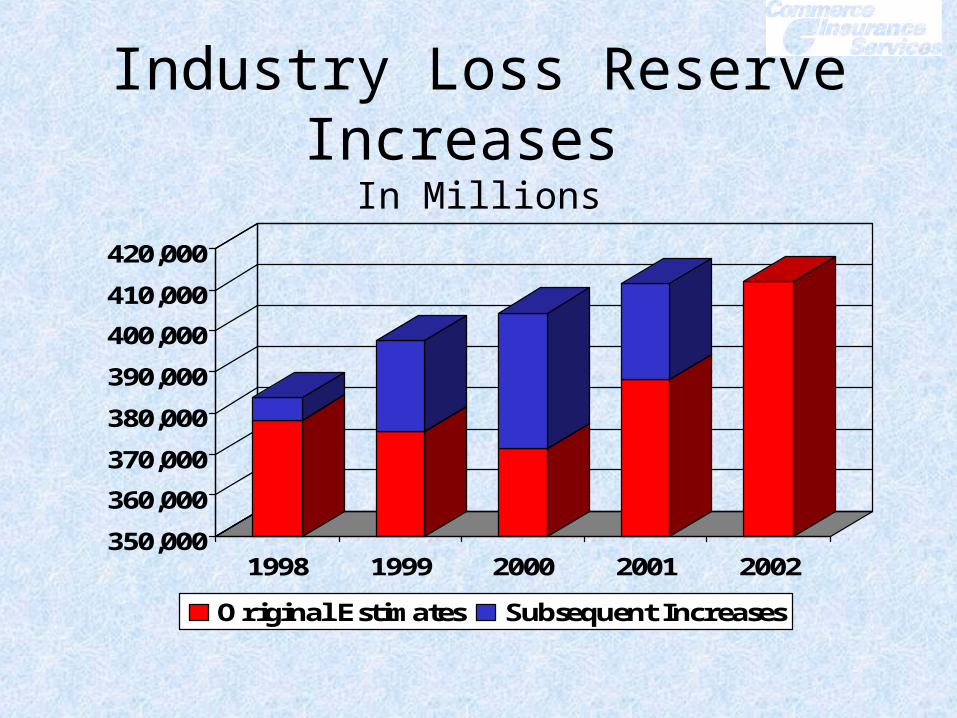

• The Post 9/11 Insurance World– Industry Reserve Strengthening Grew Dramatically as

Asbestos and Other Liabilities From the Past Were Recognized

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

Industry Loss Reserve Increases In Millions

350,000

360,000

370,000

380,000

390,000

400,000

410,000

420,000

1998 1999 2000 2001 2002

Original Estimates Subsequent Increases

• The Post 9/11 Insurance World– Many Insurance Companies Have Failed; Scores of

Others Have Received Lower Agency Ratings– Many Carriers Have Entered the Markets to Raise

Additional Capital, But Many Have Not– New Capital Has Come Into the Market, Particularly

Offshore

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

• The Post 9/11 Insurance World

– The US Government Passes the Terrorism Risk Insurance Act (TRIA) of 2002

– Severe Limitations on Some Coverages and Concentrations of Exposures

9/11 -- TROPICAL STORM TO HURRICANE9/11 -- TROPICAL STORM TO HURRICANE

• Positive– Underwriting Discipline Has Been Re-Established– 2003 Combined Ratios May Reach Below 100– Investment Market Gains Are Increasing– Balance Sheets Are Getting Healthier– Weaker Players Are Being Weeded Out– Some Coverage Limitations Are Being Eased– Prices In Some Lines of Coverage are Stabilizing

(Although Not All)

PROGNOSIS FOR THE FUTUREPROGNOSIS FOR THE FUTURE

• Negative– More Companies Will Fail In The Next Few Years– Reinsurance Company Balance Sheets Are Still Weak– More Reserve Strengthening is Inevitable (Estimates

Are the Industry is Between $40 Billion to $120 Billion Undereserved)

PROGNOSIS FOR THE FUTUREPROGNOSIS FOR THE FUTURE

• Negative– The Industry as a Whole Will Have Much Higher

Financial Leverage Than In The Past– There is a Possibility that as the Investment Markets

Return, a “Soft” Cycle Could Re-Emerge with Uncertain Industry Consequences

PROGNOSIS FOR THE FUTUREPROGNOSIS FOR THE FUTURE