Just The Facts: 3RD Quarter 2013

24

HELPING BOOMERS ADDRESS... THE FIVE “WHAT-IFS” OF RETIREMENT 3RD QUARTER 2013 800.710.1115 Rates available 24/7 at www.greatplainsannuity.com Annuity Help Center Update: Two Major Enhancements for AHC Web Sites Announced (See page 10) 100% Independently Owned! (SEE PAGE 6)

description

Â

Transcript of Just The Facts: 3RD Quarter 2013

HELPING BOOMERS ADDRESS...

THE FIVE “WHAT-IFS” OF RETIREMENT

3RD QUARTER 2013

800.710.1115 Rates available 24/7 atwww.greatplainsannuity.com

Annuity Help Center Update:Two Major Enhancements for AHCWeb Sites Announced (See page 10)

100% Independently Owned!

(SEE PAGE 6)

01.indd 1 8/14/2013 12:17:56 PM

800.710.1115 www.greatplainsannuity.com

JUST the FACTS | 3RD QUARTER 2013PAGE 2

TOP 10REASONS TO OFFERSINGLE PREMIUM LIFE

Opportunity: $40 Trillion in assets will passto heirs by 2052.

By asking ONE simple question, you can discover clients and prospects that have set aside “leave-behind” money, already earmarked for heirs.

Life Insurance is the most efficient way to transfer wealth. SPL is simple to explain and no exams are required.

You already work with people age 60-85 who can benefit by owning SPL.

Client retains control of policy and cash value.

Accelerated benefits like Chronic Care and Return of Premium are available.

Death benefit creates instant increase in legacy and proceeds transfer income tax-free.

SPL provides heirs funds for their inherited taxable gain assets like IRAs.

Great Plains offers multiple carriers and the most competitive SPL products.

Depending on client age and carrier, commissions up to 15%.

PLUS...Ask for your copy of our Agents Guide to Senior Market Life SalesOpportunities!

Annuity Producers! You may be sitting on a GOLD MINE with yourexisting clients!

You probably have SPL cases sitting in your database now! Contact your Great Plains Marketing Specialist today!

02.indd 1 8/14/2013 12:28:54 PM

6

JUST the FACTS is published quarterly for the benefit of independent insurance agents and brokers contracted with Great Plains Annuity & Life Marketing. Great Plains assumes no responsibility for the professional training or continuing education of agents. This publication is for agent use only, and not to be used to solicit sales from the general public. Products noted may not be available in all states. Great Plains does not offer tax, investment or legal advice. While every effort is made to confirm accuracy, published rate and product information is subject to change. Material herein may not be reproduced in any form without permission.

INSIDE

THE 5 “WHAT-IFS” OF RETIREMENT

Athene Annuity launches a new turn-key consumer marketing campaign designed to help you engage prospects and customers with education and solutions to their retirement concerns rather than pushing product. Learn more about the components and opportunities available and how you can make this toolkit part of your marketing efforts.

PRINCIPALS

• Rich Hellerich• Robb Edwards

ANNUITY MARKETING

• Brad Allen• Carlos Rojas • Chad Palmquist • Cindy Nelson• Jane Plumberg• Kara Jones• Mike Lair• Scott Andrew

LIFE MARKETING

• Dick Reynolds, CLU• Jeff Bregovy

ADMINISTRATION

• Cris Larson• Naomi Mayekawa• Mackenzie Oakley• Kathy Putnam

10901 W 84th Terrace., Ste. 125 Lenexa, KS 66214Toll Free: 800-710-1115

Local: 913-492-9994 • Fax: 913-492-9998www.greatplainsannuity.com

PAGE 3JUST the FACTS | 3RD QUARTER 2013

3RD QUARTER 2013

10 BECOME THE TRUSTED ANNUITY RESOURCE WITH AN ANNUITY HELP CENTER

How can you stand out from the crowd trying to reach Boomer prospects looking for retirement and income planning assistance? Great Plains offers you the opportunity to incorporate a low-cost marketing tool that can make a big difference on helping you build trust in the marketplace, find new prospects and write more business.

16 K.I.S.S. RMD SALES!

Many times, Required Minimum Distributions can be a source of irritation for clients and prospects. Mike Lair shares an actual case study that can help you turn your clients’ RMD frustrations into peace of mind and additional sales!

20 ESTATE PLANNING MERRY-GO-ROUND CONTINUES

Thanks to the Obama administration 2014 budget proposal, estate tax reform is back on the table. Dick Reynolds, V.P. of Life Sales reviews the “wait and see” options available to you and your clients on this important topic.

14 HOW I CAN HELP STRUCTURE YOUR NEXT CASE

GPALM Annuity Specialist Scott Andrew reviews a specific example of how your Great Plains’ Annuity Sales Team assists producers in finding the best solutions to their clients’ retirement and income planning needs. Read how you can better serve your clients by looking to your Annuity Specialist for additional solutions, concepts and recommendations that often come from our annuity case development process.

22 TWO INNOVATIVE LIFE INSURANCE PRODUCTS

While Living Benefits and Income Planning are two topics agents working the senior market are familiar with, here are two life insurance solutions you may not be aware of. Call the Great Plains Life department for more details.

03.indd 1 8/14/2013 12:29:45 PM

PAGE 4 JUST the FACTS | 3RD QUARTER 2013

I mentioned in my column last issue that Great Plains now brokers Structured Settlement Annuities. While this market does not fit many agents, it can be very significant for those with Attorney relationships, especially personal injury lawyers. Due to the response I received and your questions, I’m going to cover what this market is, and where you may have an opportunity to take advantage of our assistance.

Structured Settlement AnnuitiesA Structured Settlement Annuity (SSA) provides tax-free, periodic payments over a specific period of time, uniquely designed to meet an injured party’s needs. Specialized brokers facilitate the settlement process, as well as help design and negotiate the structure. Over $6 billion dollars of structured settlements are purchased annually. Utilizing Structured Settlement, streams of payments are established at the time of the settlement by mutual agreement between the injury victim and the defendant, or by a court order to meet the needs of each individual payee. Because the settlement payment terms are unique to each case and can vary over time, including balloon payments and conditions not found in a traditional income annuity, a limited number of insurance carriers participate in this market.

The payments help address ongoing financial challenges injury victims may face, including:

• Basic living expenses• Medical costs• Educational costs• Specially modified vehicles• And more, per court order or settlement terms

What are the product features?• A stream of tax-free payments for a scheduled

period of time. • Meets the ongoing financial needs of the injured

party and/or their dependents, including medical expenses and replacement income.

• Funded by a fixed income annuity backed by a large, financially strong life insurance company.

Common Structured Settlement DesignsStructured settlement payment designs commonly offered include:

• Designated-Period Annuity - Payments are guaranteed for a specific period of time, up to 50 years1.

• Life Annuity- Payments are guaranteed throughout the claimant’s lifetime.

• Life Annuity with Designated Period—Provides periodic income for as long as the payee lives, in addition to guaranteed payments for a designated period, up to 50 years1.

• Lump Sum Payments - Annuity benefits can be supplemented by guaranteed lump sum payments designed to address future needs, such as medical procedures or equipment, purchasing a home, or children’s educational costs.

• Life Annuity with Installment Refund - Provides income for as long as the payee lives, with a minimum guaranteed payout equal to the purchase price.

• Joint and Survivor Life Annuity2 - Provides income payments for the lifetime of two payees (e.g., a husband and wife). Upon the death of one payee, payments continue during the lifetime of the survivor at 100% of the original benefit, or at a reduced percentage.

The Opportunity for YouThis market has traditionally been served by a very limited number of firms. If you have existing relationships with Personal Injury Attorneys and can direct them to Great Plains we can develop and quote the case. All you need are the contacts, and we will handle everything for you. Please contact me directly for more information: 800-710-1115 or by email:[email protected].

JUST the FACTS

New Market Opportunity. Rich Hellerich, Principal

Rich Hellerich1. The period certain must be expected to be paid during the life of the recipient. 2. Not available for attorneys. Guarantees are based on the claims-paying ability of the insurance company and are subject to certain limitations, terms and conditions.

04.indd 3 8/14/2013 12:30:03 PM

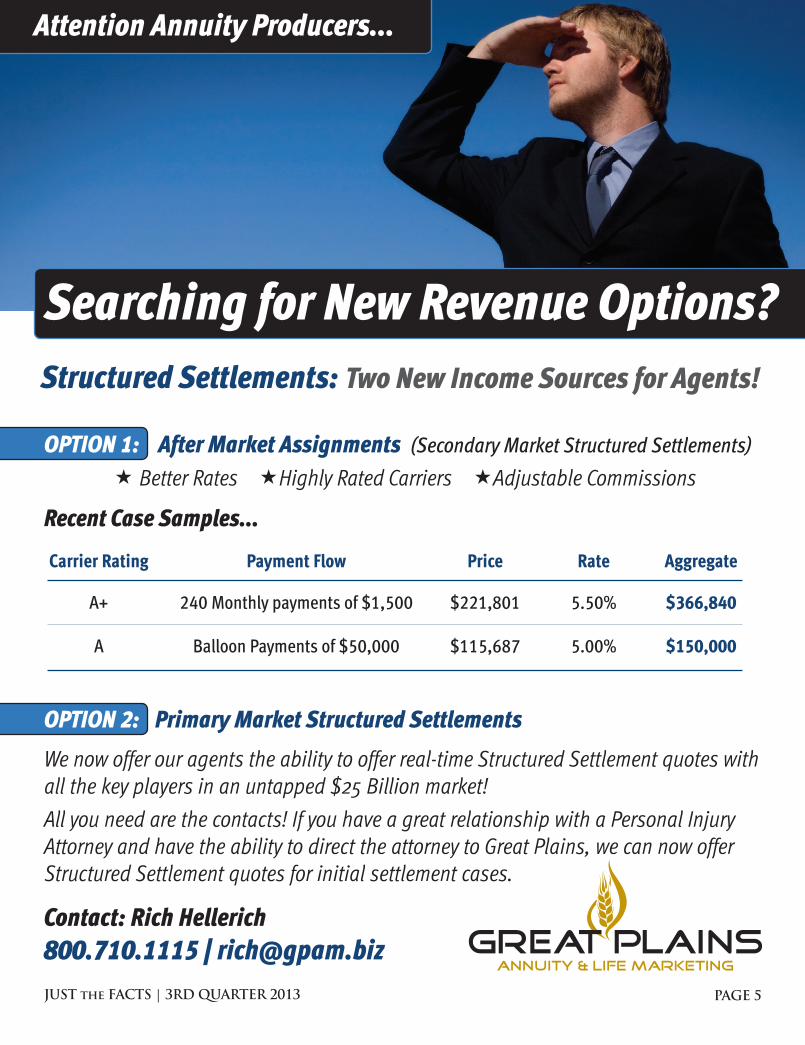

Structured Settlements: Two New Income Sources for Agents!

OPTION 1: After Market Assignments (Secondary Market Structured Settlements)

Better Rates Highly Rated Carriers Adjustable Commissions

Recent Case Samples...

Carrier Rating Payment Flow Price Rate Aggregate

A+ 240 Monthly payments of $1,500 $221,801 5.50% $366,840

A Balloon Payments of $50,000 $115,687 5.00% $150,000

OPTION 2: Primary Market Structured Settlements

We now offer our agents the ability to offer real-time Structured Settlement quotes with all the key players in an untapped $25 Billion market!

All you need are the contacts! If you have a great relationship with a Personal Injury Attorney and have the ability to direct the attorney to Great Plains, we can now offer Structured Settlement quotes for initial settlement cases.

Contact: Rich Hellerich800.710.1115 | [email protected]

PAGE 5JUST the FACTS | 3RD QUARTER 2013

Attention Annuity Producers...

Searching for New Revenue Options?

05.indd 3 8/14/2013 12:30:37 PM

PAGE 6 JUST the FACTS | 3RD QUARTER 2013

Helping Boomer clients and prospects address their future retirement income needs requires you be equipped with more than just a crystal ball. Boomers are flooding the retirement landscape, full of uncertainty and facing a new economic paradigm where the “old school” financial concepts, truisms and theories that worked for their parents and grandparents could spell disaster if applied to today’s retirement planning.

Because they are living longer than previous generations, and plan on more active retirement lifestyles, Boomers are looking for guidance and education on issues they fear could impact this vision of retirement rather than simply buying a specific financial product to create an income. They are motivated by protecting their anticipated retirement lifestyle, and creating a plan to address the “what-ifs” of longevity, health and dependence on Social Security.

Retirement Planning Stress: According to reported results from the 2013 Franklin Templeton Retirement Income Strategies and Expectations Survey (RISE), 37%

of respondents indicated they were now more concerned about outliving their assets, or having to make major sacrifices to their retirement plans today, than they were 12 months ago. It was also noted that 67% of those surveyed indicated a willingness to make financial sacrifices now in order to live better in retirement.

What are the five “what-ifs” of today’s retirement planning?

1. What if Social Security is reduced?

2. What if I can’t care for myself due to health reasons?

3. What if I live a long time?

4. What if I don’t live a long time?

5. What if I’m confined to a healthcare facility?

Every day, your clients and prospects ask you similar questions on their most pressing retirement concerns.

Do you need a strategic way to answer them? Great Plains can help you access a complete

marketing toolkit to address these concerns and engage your clients and prospects in a solution-based discussion of their needs rather than a product pitch.

This toolkit includes:• Phone Script• Pre-Approach Letter• Mailers• Client Presentation• Point-of-sale Tools• Client Fact-finder

These tools can be incorporated with any practice, from using them with a well-established client database to educating new prospects with client workshops.Thoroughly addressing these “what-ifs” is the foundation to creating a viable retirement plan that will help your clients sleep better at night and can really grow your business.

Contact your Great Plains Annuity Marketing Specialist at 800-710-1115 to learn how you can engage prospects and address client concerns to the Five “What-Ifs” of Retirement!

The Five“What-Ifs” of

RetirementDon’t sell product... sell solutions to problems.

06.indd 3 8/14/2013 12:30:54 PM

Introducing a new 10-Year FIA with a 5-In-1 Rider!

FOR PRODUCER USE ONLY. NOT TO BE USED WITH THE OFFER OR SALE OF ANNUITIES.

* In Texas, the Enhanced Benefit Rider is known as the Guaranteed Living Benefit with Enhanced Benefits Rider.

** Current as of May 4, 2013.† Entire benefit base is paid when death benefit is paid over a five-year period.

This contract is issued by Athene Annuity & Life Assurance Company and contains exclusions, limitations and charges. Please see product literature for details. ATHENE Benefit 10 is issued by Athene Annuity & Life Assurance Company, Wilmington, DE. Products/features not available in all states.

Five benefits in one flexible solution—all funded from a single benefit base! Wouldn’t it help simplify your business if you had one product that addresses your clients’ key retirement “what ifs” instead of searching for multiple products?

To learn more, call 1.800.710.1115.

(5-13)

with Enhanced Benefit Rider*

SINGLE BENEFIT BASEYour clients can use one benefit—or all five. The entire benefit base will be paid.†

AN-1324

Refreshingly New. Refreshingly Inclusive.

ATHENE Benefit 10SM

+Guaranteed

Lifetime Income

Enhanced Guaranteed

Lifetime Income

Confinement Terminal Illness

Death Benefit

Annual 7.5% roll up rate for the first 10 years**

6% premium bonus**

Early income bonus

What does the future hold for your clients?Watch this short video discussing how you can help clients plan for their future “what ifs”—and get access to a helpful product comparison worksheet. To view, go to:bit.ly/ridercomparison

800.710.1115www.greatplainsannuity.com

PAGE 7JUST the FACTS | 3RD QUARTER 2013

800.710.1115 www.greatplainsannuity.com

07.indd 1 8/14/2013 12:33:02 PM

PAGE 8 JUST the FACTS | 3RD QUARTER 2013

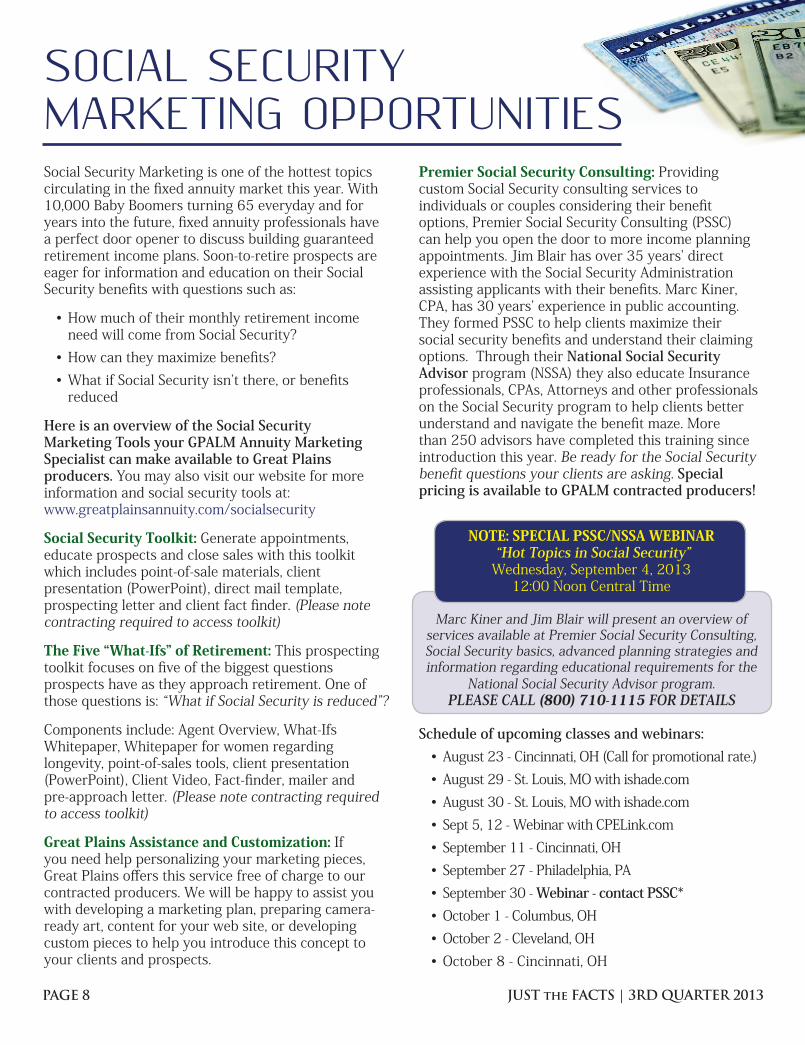

Social Security Marketing is one of the hottest topics circulating in the fixed annuity market this year. With 10,000 Baby Boomers turning 65 everyday and for years into the future, fixed annuity professionals have a perfect door opener to discuss building guaranteed retirement income plans. Soon-to-retire prospects are eager for information and education on their Social Security benefits with questions such as:

• How much of their monthly retirement income need will come from Social Security?

• How can they maximize benefits?• What if Social Security isn’t there, or benefits

reduced

Here is an overview of the Social Security Marketing Tools your GPALM Annuity Marketing Specialist can make available to Great Plains producers. You may also visit our website for more information and social security tools at: www.greatplainsannuity.com/socialsecurity

Social Security Toolkit: Generate appointments, educate prospects and close sales with this toolkit which includes point-of-sale materials, client presentation (PowerPoint), direct mail template, prospecting letter and client fact finder. (Please note contracting required to access toolkit)

The Five “What-Ifs” of Retirement: This prospecting toolkit focuses on five of the biggest questions prospects have as they approach retirement. One of those questions is: “What if Social Security is reduced”?

Components include: Agent Overview, What-Ifs Whitepaper, Whitepaper for women regarding longevity, point-of-sales tools, client presentation (PowerPoint), Client Video, Fact-finder, mailer and pre-approach letter. (Please note contracting required to access toolkit)

Great Plains Assistance and Customization: If you need help personalizing your marketing pieces, Great Plains offers this service free of charge to our contracted producers. We will be happy to assist you with developing a marketing plan, preparing camera-ready art, content for your web site, or developing custom pieces to help you introduce this concept to your clients and prospects.

Premier Social Security Consulting: Providing custom Social Security consulting services to individuals or couples considering their benefit options, Premier Social Security Consulting (PSSC) can help you open the door to more income planning appointments. Jim Blair has over 35 years’ direct experience with the Social Security Administration assisting applicants with their benefits. Marc Kiner, CPA, has 30 years’ experience in public accounting. They formed PSSC to help clients maximize their social security benefits and understand their claiming options. Through their National Social Security Advisor program (NSSA) they also educate Insurance professionals, CPAs, Attorneys and other professionals on the Social Security program to help clients better understand and navigate the benefit maze. More than 250 advisors have completed this training since introduction this year. Be ready for the Social Security benefit questions your clients are asking. Special pricing is available to GPALM contracted producers!

NOTE: SPECIAL PSSC/NSSA WEBINAR “Hot Topics in Social Security”Wednesday, September 4, 2013

12:00 Noon Central Time

Marc Kiner and Jim Blair will present an overview of services available at Premier Social Security Consulting, Social Security basics, advanced planning strategies and information regarding educational requirements for the

National Social Security Advisor program.PLEASE CALL (800) 710-1115 FOR DETAILS

Schedule of upcoming classes and webinars:• August 23 - Cincinnati, OH (Call for promotional rate.)• August 29 - St. Louis, MO with ishade.com• August 30 - St. Louis, MO with ishade.com• Sept 5, 12 - Webinar with CPELink.com• September 11 - Cincinnati, OH• September 27 - Philadelphia, PA• September 30 - Webinar - contact PSSC*• October 1 - Columbus, OH• October 2 - Cleveland, OH• October 8 - Cincinnati, OH

SOCIAL SECURITY MARKETING OPPORTUNITIES

08.indd 3 8/14/2013 12:33:26 PM

Withdrawals before age 59 1/2 may result in a 10% IRS penalty tax. Withdrawals do not participate in index growth. Surrender of the contract may be subject to surrender charge and market value adjustment. Product and rider not available in all states. Contract may vary by state. MarketTwelve Bonus Index fixed indexed annuity is issued on contract form series ET-MPP-2000(02-05) with Rider ET-AVBR(06-09). Group Certificate issues on Form Series ET-MPP-2000C(01-07) and ET-IMVAC(07-09). Income Rider provisions and availability may vary by state. Rider issued on Form Series ET-IBR(06-08). Contract issued by EquiTrust Life Insurance Company, West Des Moines, IA.For Producer Use Only. AC13-M12-1103

800.710.1115 www.greatplainsannuity.com

MarketTwelve Bonus IndexTM Annuity•FullAccountValueatDeath–NoAnnuitizationRequired

•10%WithdrawalAvailableafterYear1

Income For Life 0ptional Rider•6.5%IncomeRiderRollupRate

•AnnualRiderFeeisOnly.50%

•Rollupfor15Years

12.00%BonusPaidOver3Years

8.50%MGACommission(Ages0-75)

THINK BIG!

PAGE 9JUST the FACTS | 3RD QUARTER 2013

09.indd 1 8/14/2013 12:34:01 PM

PAGE 10

The days of mailing annuity lead postcards, expecting a 2% response and submitting at least $250,000 in premium are rapidly disappearing. Especially if you do not have a “Bricks and Mortar” office and no presence on the internet.

Today’s Baby Boomer prospect is more educated, often does significant research (usually by computer), and craves information. They want to be educated rather than sold, and want an Advisor/Mentor rather than a sales pitch.

I believe we have truly entered the “internet age” and if you do not currently have a web site you will not be in practice five years from now, or if you are, you will be working for someone who does have a web site. A web site, YOUR web site, gives you instant credibility with consumers. It is another way to build rapport and trust with prospects, no different than your goal with seminar or other marketing efforts.

If you visit www.your.annuityhelpcenter.com you’ll notice we intentionally set the custom copy up to encourage annuity and life insurance producers to contact us for more information about this great lead generation tool disguised as a web site. This year we have generated scores of agent requests in promoting the Annuity Help Center tool. In addition over the past four months, with no promotion of the web address to consumers, we have had several inquiries from consumers. While that may not send you to your phone to call us, or prompt you to fire us an email to learn more, I believe it does confirm how consumers are using the internet to conduct research on topics that interest them.

The primary offer of an Annuity Help Center website is access to a free e-book — “Your Personal Financial Help Center” written by consumer advocate Bruce Sankin. Bruce has been interviewed on NBC, CNBC and in numerous publications including Money magazine and The Wall Street Journal. He is also an industry arbitrator for FINRA for over 20 years, specializing in securities, and has written numerous financial columns.

Annuity Help Center offers a simple solution for agents that do not have a web site, or for producers that do not have a call to action on their existing web site. Here a few reasons to consider creating a site:

• Easy to set up - You can have your site up and running in a matter of minutes

• A Primary Call-to-Action - FREE e-book• Additional Calls-to-Action - Resources Tab

• Building Your Retirement Income Strategy• Maximizing Social Security

• Automatic Notification of lead via email• Immediate gratification to consumer - they receive

the book or other resources requested immediately • Site effectively brands you and your agency —

you can add your picture and agency logo along with a bio

• Low price point with potential of high value

See the next page for more information and a special Annuity Help Center offer. We will also be scheduling a webinar featuring Bruce Sankin for interested producers soon, so watch your email for our invitation. If you have any specific questions, please contact your GPALM Marketing Specialist or me at 1-800-710-1115.

Using Book Marketing to Educate Prospects and Generate Leads

Robb Edwards, [email protected]

10.indd 3 8/14/2013 2:13:52 PM

800.710.1115 www.greatplainsannuity.com

A PROVEN Lead GenerationTool disguised as a website!In less than five minutes, “Annuity Help Center” gives insurance agents and financial advisors a unique referral and prospecting system that generates annuity leads.

Three special offers from Great Plains:Annual Subscription, e-bookplus 10 books $306.45(Savings: $300.00)

Annual Subscription PlusPersonally Customized e-book $395.00(Savings: $395.00)

Annual Subscription, e-bookand 30 books $495.00 (Savings: $300.00)

Go to www.annuityhelpcenter.com/admin and usecoupon code ahc1 when you create your account.

Your Annuity Help Center subscription includes: • Unlimited supply of “Your Personal Financial Help Center”

e-book ($19.95 value) to give each prospect.

• Easy-to-create Annuity Help Center Website

• Website Hosting

• Marketing ideas, letters, scripts and more to generate5% - 50% in referral leads!

• Annual subscription fee of $99.95 beginning in the 2nd year.

Call today! Don’t miss this opportunity to brandyourself as an Annuity Help Center at a ridiculously low cost! This promotion is good until September 30, 2013.

Special savings and coupon code available to GPALM producers... Call today for details!

PAGE 11JUST the FACTS | 3RD QUARTER 2013

11.indd 1 8/14/2013 12:35:02 PM

PAGE 12 JUST the FACTS | 3RD QUARTER 2013

RICH’S HOT ANNUITY & LIFE PICKS!Equitrust Life Certainty & Certainty Select 3 2% guaranteed for 3 years, issues to age 90

Guggenheim Life Preserve MYG 4 2.25% / 2.35% 4 year rate, issues to age 90

Equitrust Life Certainty & Certainty Select 5 2.70% 5 year rate , issues to age 90

Equitrust Life Certainty & Certainty Select 6 3.0% 6 year rate, issues to age 90

Guggenheim Life Preserve MYG 7 3.1% / 3.2% year rate, issues to age 90

Equitrust Life Certainty & Certainty Select 8 3.15% 8 year rate, issues to age 90

Guggenheim Life Preserve MYG 9 3.3% / 3.4% 9 year rate, issues to age 90

Guggenheim Life Preserve 10 3.4% / 3.5% 10 year rate, issues to age 90

RICH’S FAVORITE MULTI YEAR GUARANTEE ANNUITIES:

American Equity Retirement Gold Good Bonus, Strong Income Rider, Good Commission

Athene Annuity Benefit 10 5 in 1 Riders for death, income & LTC Great Commission

Equitrust Life Market 12 12% Bonus, Great long term income rider, Awesome Commission

Equitrust Life Market Value Top Index Crediting Rates, great long term income rider

Gen Worth Index 7 Top Index Crediting Rates, Short 7 year surrender, Bailout Cap Option

Great American Amn Legend II Top Index Crediting Rates, Short 7 year contract, excellent Income/DB Rider Options

Great American Safe Return Top Index Crediting Rates, Bailout Cap Rate, ROP Option, excellent Income/DB Rider Options

NACOLAH Freedom Choice Incredible High Index Crediting Rates

RICH’S FAVORITE FIXED INDEX ANNUITIES

12-13RichPicks.indd 1 8/14/2013 12:35:48 PM

Equitrust Life Choice 4 5.5% Commission on 6 Year Contract, Excellent Alternative to MYGA’s, 3.7% First Year Rate with Minimum Rate Guarantee of 2%

Equitrust Life Wealth Max Bonus SPWL Great Annuity Alternative, ROP Option Included Day 1, No Exam, LTC Benefit Included, Great Wealth Transfer, No Suitability, EXCELLENT COMMISSIONS!

JUST the FACTS | 3RD QUARTER 2013

RICH’S HOT ANNUITY & LIFE PICKS!

PAGE 13

Phoenix Life Personal Income Annuity Top Income Payout starting immediately to 2 years, shines at older ages too

Great American All Index Contracts Top Income Payout starting years 2 - 5. Includes Death Benefit Option.

American Equity (Tied) All Index Contracts Top Income Payouts years 7-20, Includes Additional Benefits

Equitrust Life (Tied) All Index Contracts Top Income Payouts years 7-20, Includes Lowest Charge

Athene Annuity All Index Contracts Great Income Payouts, Overall Value includes Death Benefit & Chronic Care

RICH’S FAVORITE INCOME RIDERS

OTHER PRODUCTS RICH REALLY LIKES!

12-13RichPicks.indd 2 8/14/2013 12:35:58 PM

Editor’s Note: All the Marketing Specialists at Great Plains share this approach to case development. Our goal is to make you aware of the best possible solutions, and follow through with the best back room support to get the case issued and paid.

PAGE XXPage 14

Proper case design is imperative to successful annuity sales, especially in today’s world of suitability review and varying carrier practices. Some marketing organizations seem to peddle a specific product and take a “one-size-fits-all” approach. They look at a one product solution rather than exploring the best solution(s) to help you meet the client’s needs, consider additional benefits and offer flexibility if circumstances change. While one product may well be the answer some of the time, I have not yet seen an annuity product that fits every retirement planning need.

I want to share an excellent example of how I approach case development for each and every agent I work for. Recently, I helped an agent successfully place a $1.4 Million annuity sale which not only represented the vast majority of the client’s assets, but also put the them in the best possible position for liquidity, income, and flexibility.

The client’s stated goals were to retire with a set amount of income in roughly 10 years. During this time they wanted safety of principal, and guaranteed growth. The agent I was working with was in competition with another agent who had suggested putting the clients’ money into an income rider deferring out 10 years then initiating income. While this was perhaps the easy road, it may not have been the best approach in terms of suitability.

I believe this approach was inappropriate for several reasons. If the client needed extra liquidity,

they were limited to 10%. Should interest rates increase, they were stuck in a product with a 16-year surrender schedule. They had very little control in taking advantage of future rate increases, if available. There was no flexibility in this proposal.

When I looked at this case, two additional benefits I wanted to provide the client and the agent were flexibility and options. I could have used alternative income riders and provided a higher income versus the competitor, but the client would have all of their money tied up with no available out except surrender. I ended up taking the client’s funds and suggested a laddered strategy incorporating five different products to provide them maximum benefit and flexibility.

We placed roughly 50% of the client’s assets into income riders to provide the desired income after 10 years deferral. We then placed about 20% of the client’s assets into an index annuity that provides a high minimum guarantee, high potential for growth, an immediate bonus, and an option to move 50% of the AV after 5 years should they need that money for a life event, or to capture better rates at that time. Lastly, we divided the remaining 30% of the assets into two highest fixed rate annuities using a three and 10 year chassis. This way, at the end of the three and 10 year terms, the clients have options. They can place the money into another fixed product, they can purchase a SPIA at future rates to provide income, which we can all

agree with mostly likely be higher than today’s rates, or they have access to the money liquid free and clear with easy access. This approach made the client much happier, and gave them control of their money and future income. This also netted the agent over $85,000 in total commission and happy clients that now view the agent as a trusted advisor. She can expect repeat business from these happy clients, and the probability of referrals based on the great advice they received.

I take this approach to case design every time I assist a producer. I ask what the client’s goals are, determine how best to maximize those goals, and help the agent place their clients’ in the best possible position. Allow me an opportunity to help you close your next big case.

How I Can Help Structure Your Next Case!

ANNUITY CASE DEVELOPMENT:

Scott AndrewAnnuity Specialist [email protected]

14.indd 1 8/14/2013 12:36:59 PM

PAGE 15JUST the FACTS | 3RD QUARTER 2013

800.710.1115 www.greatplainsannuity.com

FOR AGENT USE ONLY. NOT FOR USE WITH CLIENTS AS SALES LITERATURE.The above is simply a highlight. Please contact AltiSure to obtain complete information about the product including risks, fees and limitations, so you can decide if this could be right for your clients. Bonus products may have less-favorable fees and benefits than similar products that do not offer a premium bonus. Withdrawals and Inheritance Benefit are subject to tax. The Phoenix Next Generation BONUS Annuity with Protected Inheritance Benefit (IIC09EIA, 10FIA, 11RSP, 11GLWB2, and 11GMDB-A.1) is a single-premium indexed annuity issued by PHL Variable insurance Company (PHLVIC), Hartford, CT. PHLVIC is not authorized to conduct business in NY and ME. PHLVIC, The AltiSure Group, and associated marketing organizations are not affiliated. Guarantees are based upon the claims-paying ability of PHL Variable Insurance Company. BPD38643 02/13

For You...• Open New Doors• Competitive Compensation

For Your Clients...• Extra Cap/Interest Credit - 1st Period Only• Phoenix Next Generation Annuity Protected

Inheritance Benefit• GLWB - after Year 1 or Higher after Year 5• 100%, 75% or 50% Return of Premium upon Death1

• 10% Premium Bonus Available to age 852

• Qualified and Non-Qualified1 In 5 annual installments 2 7% or 6% in some states

Contact Us Today for Details!

15.indd 1 8/14/2013 12:37:16 PM

While Stretch IRA’s and other estate planning techniques can often help our agents and their clients maximize funds left behind from qualified accounts, I was working on a personal case the other day with a neighbor that reminded me of the old K.I.S.S. idea. If your clients don’t need their RMD’s for income, use them to maximize what they can leave behind to their loved ones.

My 67 year old neighbor, let’s call him Tim, has $173,000 in an IRA invested in the market that he’s really not planning on using for income. He also has other IRA’s he’s not intending on using for income. He has plenty of money coming in from his pensions, social security and other sources. His possible LTC needs are also met through an existing policy. He doesn’t want or need the RMD’s he will soon be forced to take out of his IRA and confided he was really just trying to leave as much behind as he could for his family and that some additional income would be nice but not his primary concern. After speaking to a financial advisor in his local bank about options he could consider, he was presented with a variable annuity with a rider that could provide income and guarantee my neighbor got all of his initial deposit back as a death benefit. What the advisor seemed to completely ignore was Tim’s conservative nature and his desire to maximize his legacy and did not have a real need for additional income. Tim is in excellent health as well. Luckily I had talked to Tim about what I do for a living so he came to ask for my advice. I proposed the idea you see below. After confirming we could get him life insurance on a preferred basis we decided to do the following:

For the first three years we are withdrawing funds from another of his IRA’s he had prior to his having to take the RMD’s. We then put the $173,000 IRA into a 10 year MYGA paying a 3% rate and

will use RMD’s from the $173,000 IRA starting at age 70 ½ to pay for his life insurance policy’s annual premium. We had more than enough left over after paying taxes and the insurance premium to give him a small amount of additional income. So now his beneficiaries will receive an additional $255,920 of income tax free death benefit from the life insurance policy in addition to the IRA that they can either stretch or take out as needed.

The key to this sale was simply asking what the client really wanted. If your clients are forced to take out RMD’s that they really don’t need, this idea might work for you too.

PS – I also earned a little over $10K in commissions. 3% commission on the MYGA sale and 85% commission on the life insurance sale (with trails years 2+).

Mike LairSenior Vice President

Mike’s 24 years of insurance experience includes direct sales, home office marketing and training positions and assisting independent agents with case development and training primarily in the Fixed Annuity market. During his previous tenure at GPALM, agents working with Mike represented an average of more than $45 M in annual annuity sales.

K.I.S.SRMD SALES!

JUST the FACTS | 3RD QUARTER 2013Page 16

Help Clients Maximize the Value of Their RMDs!

Annuity Sales Idea Using an RMD to Fund Life Policy!

16-17.indd 1 8/14/2013 12:38:29 PM

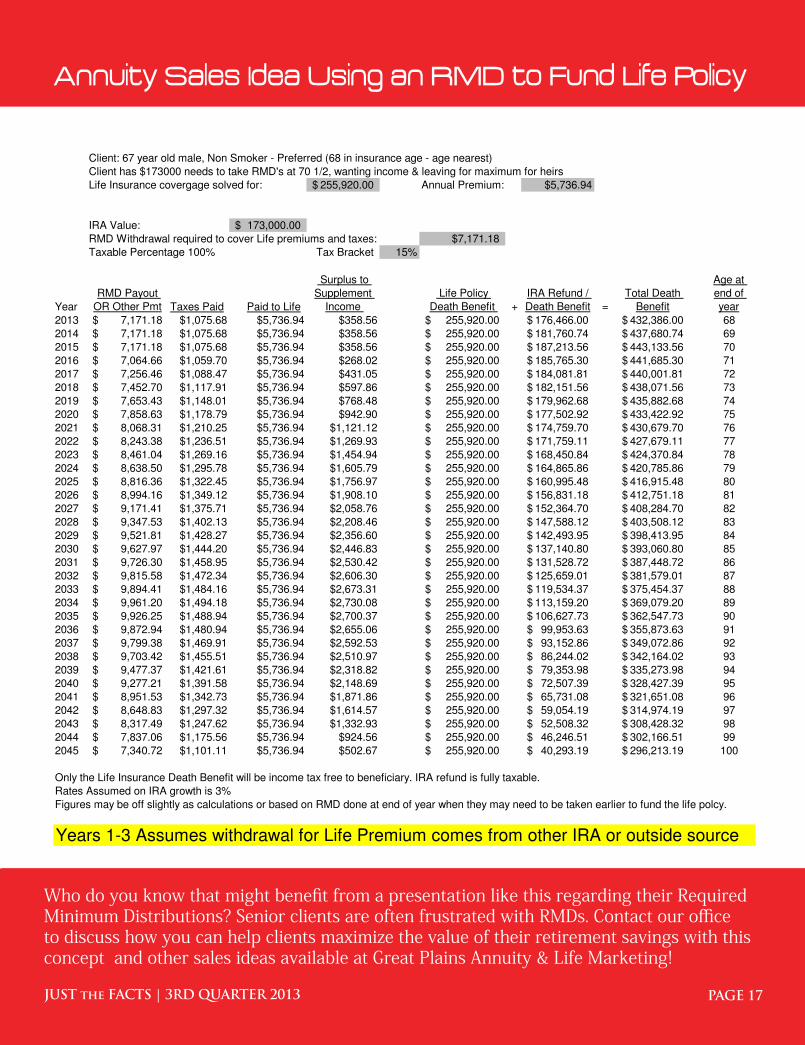

Annuity Sales Idea

Using an RMD to Fund Life Policy

Client: 67 year old male, Non Smoker - Preferred (68 in insurance age - age nearest)

Client has $173000 needs to take RMD's at 70 1/2, wanting income & leaving for maximum for heirs

Life Insurance covergage solved for: 255,920.00$ Annual Premium: $5,736.94

IRA Value: 173,000.00$

RMD Withdrawal required to cover Life premiums and taxes: $7,171.18

Taxable Percentage 100% Tax Bracket 15%

Year

RMD Payout

OR Other Pmt Taxes Paid Paid to Life

Surplus to

Supplement

Income

Life Policy

Death Benefit +

IRA Refund /

Death Benefit =

Total Death

Benefit

Age at

end of

year

2013 7,171.18$ $1,075.68 $5,736.94 $358.56 255,920.00$ 176,466.00$ 432,386.00$ 68

2014 7,171.18$ $1,075.68 $5,736.94 $358.56 255,920.00$ 181,760.74$ 437,680.74$ 69

2015 7,171.18$ $1,075.68 $5,736.94 $358.56 255,920.00$ 187,213.56$ 443,133.56$ 70

2016 7,064.66$ $1,059.70 $5,736.94 $268.02 255,920.00$ 185,765.30$ 441,685.30$ 71

2017 7,256.46$ $1,088.47 $5,736.94 $431.05 255,920.00$ 184,081.81$ 440,001.81$ 72

2018 7,452.70$ $1,117.91 $5,736.94 $597.86 255,920.00$ 182,151.56$ 438,071.56$ 73

2019 7,653.43$ $1,148.01 $5,736.94 $768.48 255,920.00$ 179,962.68$ 435,882.68$ 74

2020 7,858.63$ $1,178.79 $5,736.94 $942.90 255,920.00$ 177,502.92$ 433,422.92$ 75

2021 8,068.31$ $1,210.25 $5,736.94 $1,121.12 255,920.00$ 174,759.70$ 430,679.70$ 76

2022 8,243.38$ $1,236.51 $5,736.94 $1,269.93 255,920.00$ 171,759.11$ 427,679.11$ 77

2023 8,461.04$ $1,269.16 $5,736.94 $1,454.94 255,920.00$ 168,450.84$ 424,370.84$ 78

2024 8,638.50$ $1,295.78 $5,736.94 $1,605.79 255,920.00$ 164,865.86$ 420,785.86$ 79

2025 8,816.36$ $1,322.45 $5,736.94 $1,756.97 255,920.00$ 160,995.48$ 416,915.48$ 80

2026 8,994.16$ $1,349.12 $5,736.94 $1,908.10 255,920.00$ 156,831.18$ 412,751.18$ 81

2027 9,171.41$ $1,375.71 $5,736.94 $2,058.76 255,920.00$ 152,364.70$ 408,284.70$ 82

2028 9,347.53$ $1,402.13 $5,736.94 $2,208.46 255,920.00$ 147,588.12$ 403,508.12$ 83

2029 9,521.81$ $1,428.27 $5,736.94 $2,356.60 255,920.00$ 142,493.95$ 398,413.95$ 84

2030 9,627.97$ $1,444.20 $5,736.94 $2,446.83 255,920.00$ 137,140.80$ 393,060.80$ 85

2031 9,726.30$ $1,458.95 $5,736.94 $2,530.42 255,920.00$ 131,528.72$ 387,448.72$ 86

2032 9,815.58$ $1,472.34 $5,736.94 $2,606.30 255,920.00$ 125,659.01$ 381,579.01$ 87

2033 9,894.41$ $1,484.16 $5,736.94 $2,673.31 255,920.00$ 119,534.37$ 375,454.37$ 88

2034 9,961.20$ $1,494.18 $5,736.94 $2,730.08 255,920.00$ 113,159.20$ 369,079.20$ 89

2035 9,926.25$ $1,488.94 $5,736.94 $2,700.37 255,920.00$ 106,627.73$ 362,547.73$ 90

2036 9,872.94$ $1,480.94 $5,736.94 $2,655.06 255,920.00$ 99,953.63$ 355,873.63$ 91

2037 9,799.38$ $1,469.91 $5,736.94 $2,592.53 255,920.00$ 93,152.86$ 349,072.86$ 92

2038 9,703.42$ $1,455.51 $5,736.94 $2,510.97 255,920.00$ 86,244.02$ 342,164.02$ 93

2039 9,477.37$ $1,421.61 $5,736.94 $2,318.82 255,920.00$ 79,353.98$ 335,273.98$ 94

2040 9,277.21$ $1,391.58 $5,736.94 $2,148.69 255,920.00$ 72,507.39$ 328,427.39$ 95

2041 8,951.53$ $1,342.73 $5,736.94 $1,871.86 255,920.00$ 65,731.08$ 321,651.08$ 96

2042 8,648.83$ $1,297.32 $5,736.94 $1,614.57 255,920.00$ 59,054.19$ 314,974.19$ 97

2043 8,317.49$ $1,247.62 $5,736.94 $1,332.93 255,920.00$ 52,508.32$ 308,428.32$ 98

2044 7,837.06$ $1,175.56 $5,736.94 $924.56 255,920.00$ 46,246.51$ 302,166.51$ 99

2045 7,340.72$ $1,101.11 $5,736.94 $502.67 255,920.00$ 40,293.19$ 296,213.19$ 100

Only the Life Insurance Death Benefit will be income tax free to beneficiary. IRA refund is fully taxable.

Rates Assumed on IRA growth is 3%

Figures may be off slightly as calculations or based on RMD done at end of year when they may need to be taken earlier to fund the life polcy.

Years 1-3 Assumes withdrawal for Life Premium comes from other IRA or outside source

Annuity Sales Idea Using an RMD to Fund Life Policy

Who do you know that might benefit from a presentation like this regarding their Required Minimum Distributions? Senior clients are often frustrated with RMDs. Contact our office to discuss how you can help clients maximize the value of their retirement savings with this concept and other sales ideas available at Great Plains Annuity & Life Marketing!

PAGE 17JUST the FACTS | 3RD QUARTER 2013

16-17.indd 2 8/14/2013 12:38:39 PM

PAGE 18 JUST the FACTS | 3RD QUARTER 2013

Social SecurityEducationPresentations

There’s no doubt about the popularity of the new Social Security Planning methods that are being integrated into many producer’s practices. The seminar attendance is very high and can be presented with out meals. That’s a significant savings. Not serving meals also improves the sincerity of the attendees. They are definitely there to hear the presentation. Social Security Planning is a three-pronged discussion. The three issues to be addressed are Income Option Solutions, Survivorship planning and Tax savings. There are agents who are becoming experts at Social Security Planning just solving these three problems.

Option Planning helps the client decide when would be the best time to take Social Security. As a single person, the decision is straightforward, now or later. Of course income riders allow a retiree to defer his Social Security check until a better time. Couples have a more complex decision.

Survivorship planning also involves a rider, which rolls-up rapidly to overcome the loss of the smaller Social Security check. Then, of course, there’s the old, tried and true tax savings on Social Security earnings.

Annuities are the solution to all three problems.

The presentations are about an hour in length and the PowerPoint is already prepared to present. An effective mailer is also available. All of these can be presented with a non-meal seminar. Response without a meal has been very good, depending on the age group you wish to market. Since money is saved by not providing a meal, you can do more seminars. Seminarsforless.com can show you how to produce and present these effective seminars. The owner, Kim Magdalein is also a producer. He can offer clear and effective insight. Kim provides coaching in seminar content and presentation. He teaches a seminar presentation school which covers best practices in presenting, what to present, appointment setting, follow up techniques for keeping the appointment, cost control, best mailing methods, demographics and even some sales tips. Kim offers this at no charge with the seminar production package. You can have a total “turn-key” program that works for you.

Kim MagdaleinKim Magdalein has presented to over 1,000 audiences in the last 10 years resulting in over $150 million of annuity production averaging $150,000 per presentation. His marketing company, Seminars for Less, has produced thousands of seminars for client agents generating over $2.5 billion of annuity premium. Kim can be reached at 800.909.9894 or visit his web site: www.seminarsforless.com.

Kim Magdalein and Seminars for Less provides turn-key solutions for producers interested in lead generation through seminars and workshops.

18.indd 1 8/14/2013 12:47:14 PM

PAGE 19JUST the FACTS | 3RD QUARTER 2013

800.710.1115

COMMISSIONBLITZ BONUSSPECIALon all NAC RetireChoice applications received from 02-11-13 to 09-30-13

NAC RetireChoiceSM Fixed Index Annuity Offers:— Uncapped Crediting Method Options Available (a Participation Rate may be applied)

— Up to 10% Premium Bonus1 With Optional Additional Benefit Rider

Plus...• Up to 3.10% Annual Point-to-Point Cap Rate2

• Five Index Options with Uncapped and Capped Crediting Methods (a Participation Rate may be applied)

• Partial Interest Credits at Death

• Return of Premium with Optional Additional Benefit Rider for an annual cost of 0.55% for the 10 Year Option and 0.60% for the 14 Year Option

FOR AGENT USE ONLY. NOT TO BE USED FOR CONSUMER SOLICITATION PURPOSES. Fixed Index Annuities are not a direct investment in the stock market. They are long term insurance products with guarantees backed by the issuing company. They provide the potential for interest to be credited based in part on the performance of specific indices, without the risk of loss of premium due to market downturns or fluctuation. They may not be appropriate for all clients. This product is issued by North American Company for Life and Health Insurance®, West Des Moines, IA. Product features and riders may not be available in all states. The NAC RetireChoiceSM is issued on form LC/LS160A (certificate/contract), LR431A, LR424A-1, LR423A, AE520A, AE533A, AE529A, AE532A, AE531A, LR433A, AE530A, AE528A, AE511A and LR427A (riders/endorsements) or appropriate state variation. Please consult brochure and disclosure for further product details and limitations. In order to be eligible for the 1% commission bonus the application must be received between 02-11-13 and 09-30-13. The NAC RetireChoice fixed index annuity may not be available in all states. All taxes generated by earnings are the agent’s responsibility. IRS Form 1099 will be issued. The commission bonus applies to personal production only. The commission bonus is not available to agents who do not earn commission or agents who have commission assigned. The 1% commission bonus applies to new applications only. Renewal premium in existing NAC RetireChoice annuity products is not eligible for the commission bonus. Applications received prior to 02-11-13 will receive the current commission rates without the 1% commission bonus. All decisions are at the sole discretion of North American Company and all decisions are final. Commission bonus may be modified or discontinued at any time without any advance notice given. Please allow a minimum of 20 business days for bonus to be paid after contract is fully issued. 1. 10% premium bonus based on the NAC RetireChoice 14 with the optional Additional Benefit Rider added at an additional cost. Products that have premium bonuses may offer lower credited interest rates, lower Index Cap Rates and or lower Participation rates than products that don’t offer a premium bonus. Over time and under certain scenarios the amount of the premium bonus may be offset by the lower credited interest rates, lower Index Cap Rates and or lower Participation Rates. 2. Rate is current as of 2-27-13 and is subject to change. Rate listed is for the S&P 500 Annual Point-to-Point for the NAC RetireChoice 14. “Standard & Poor’s®”, “S&P®”, “S&P 500®”, “Standard & Poor’s 500” “Standard & Poor’s MidCap 400” and “S&P MidCap 400®” are trademarks of The McGraw-Hill Companies, Inc. and have been licensed for use by North American Company for Life and Health Insurance®. The product(s) is not sponsored, endorsed, sold or promoted by Standard & Poor’s and Standard & Poor’s makes no representation regarding the advisability of purchasing the product(s).Form # DK1815-7J955

1%

19.indd 1 8/14/2013 12:42:52 PM

PAGE 20

By now some if not all of you have heard that the 2014 budget proposal put forth by the Obama administration includes provisions that put estate tax reform back on the table. Instead of the “permanent reform” that recent legislation has been called, the new proposal calls for a reduction in the lifetime exclusion.

The ultimate insurance buyer, and perhaps their CPA or Attorney, is largely under the impression that the latest reform was final. This has been seen with cases we had in underwriting that were “not taken” due to these higher amounts passed by Congress. I’m sure many firms experienced this same behavior.

A safer view might be one that says tax revenues, from any source, are probably on the table given the enormity of the deficit. If clients determine down the road they do need to buy life insurance because of lower limits passed, they run the risk of being older and perhaps had serious changes in their health.

Clients, as well as Agents, may be surprised to know that there are “wait and see” options for estate planning focused on getting covered now. These solutions either minimize outlay or offer contractually guaranteed exit strategies that allow clients to defer any significant premium commitments until much, much later.

Here are some examples of a “wait and see” strategy from carriers we represent:

• Pay Target Premium for the first three policy years.• Skip as long as you can, in some cases as many as 15

years• Resume premium payments on a minimum annual

funding basis OR

• Pay a no-lapse guaranteed premium for 1 to 5 years to get a 15 year guarantee duration

• In year 10, decide to wait an additional 5 years, or collect your contractually guaranteed 90% of premiums paid in surrender value.

• If waiting longer, skip years 11 – 14. In policy year 15, decide to cash out for 100% of premiums paid to date or resume premiums to catch up the guarantees and extend the coverage

If you have had some experience with clients, prospects or their advisors who no longer saw the need to fund for estate taxes given the last reform, you might want to bring up this newest tax proposal by the Obama administration. I’d be more than happy to discuss this issue should you have questions or a case to quote.

Dick Reynolds, CLU V.P., Life [email protected]

Estate Planning Merry-Go-Round Continues

20.indd 1 8/15/2013 10:15:23 AM

PAGE 21JUST the FACTS | 3RD QUARTER 2013

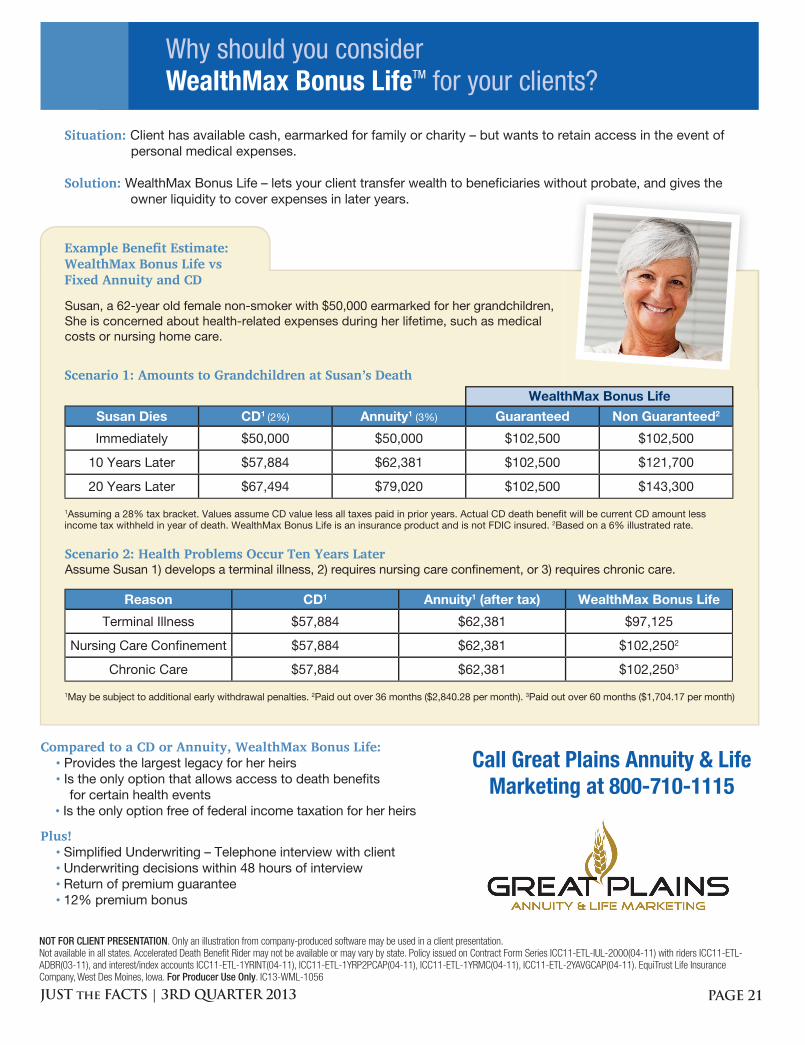

Situation: Client has available cash, earmarked for family or charity – but wants to retain access in the event of personal medical expenses.

Solution: WealthMax Bonus Life – lets your client transfer wealth to benefi ciaries without probate, and gives the owner liquidity to cover expenses in later years.

Example Benefi t Estimate: WealthMax Bonus Life vs Fixed Annuity and CD

Susan, a 62-year old female non-smoker with $50,000 earmarked for her grandchildren, She is concerned about health-related expenses during her lifetime, such as medical costs or nursing home care.

Reason CD1 Annuity1 (after tax) WealthMax Bonus Life

Terminal Illness $57,884 $62,381 $97,125

Nursing Care Confi nement $57,884 $62,381 $102,2502

Chronic Care $57,884 $62,381 $102,2503

1May be subject to additional early withdrawal penalties. 2Paid out over 36 months ($2,840.28 per month). 3Paid out over 60 months ($1,704.17 per month)

Susan Dies CD1 (2%) Annuity1 (3%) Guaranteed Non Guaranteed2

Immediately $50,000 $50,000 $102,500 $102,500

10 Years Later $57,884 $62,381 $102,500 $121,700

20 Years Later $67,494 $79,020 $102,500 $143,300

1Assuming a 28% tax bracket. Values assume CD value less all taxes paid in prior years. Actual CD death benefi t will be current CD amount less income tax withheld in year of death. WealthMax Bonus Life is an insurance product and is not FDIC insured. 2Based on a 6% illustrated rate.

Scenario 1: Amounts to Grandchildren at Susan’s DeathWealthMax Bonus Life

Scenario 2: Health Problems Occur Ten Years LaterAssume Susan 1) develops a terminal illness, 2) requires nursing care confi nement, or 3) requires chronic care.

Why should you consider WealthMax Bonus LifeTM for your clients?

NOT FOR CLIENT PRESENTATION. Only an illustration from company-produced software may be used in a client presentation.Not available in all states. Accelerated Death Benefi t Rider may not be available or may vary by state. Policy issued on Contract Form Series ICC11-ETL-IUL-2000(04-11) with riders ICC11-ETL-ADBR(03-11), and interest/index accounts ICC11-ETL-1YRINT(04-11), ICC11-ETL-1YRP2PCAP(04-11), ICC11-ETL-1YRMC(04-11), ICC11-ETL-2YAVGCAP(04-11). EquiTrust Life Insurance Company, West Des Moines, Iowa. For Producer Use Only. IC13-WML-1056

Compared to a CD or Annuity, WealthMax Bonus Life: • Provides the largest legacy for her heirs • Is the only option that allows access to death benefi ts for certain health events • Is the only option free of federal income taxation for her heirs

Plus! • Simplifi ed Underwriting – Telephone interview with client • Underwriting decisions within 48 hours of interview • Return of premium guarantee • 12% premium bonus

Call Great Plains Annuity & Life Marketing at 800-710-1115

21.indd 1 8/14/2013 12:52:29 PM

Jeff Bregovy Life Specialist

1: Universal Life with a Unique Added BenefitIncreased longevity is not just a possibility – statistics show it’s very likely. Living longer comes with a major financial concern of outliving your retirement income! Over 60% of Americans surveyed are more afraid of outliving their assets than they are of dying. Individuals looking to buy life insurance may well find this innovative UL product, from a well-known A.M. Best’s “A” rated company, a better product option that could generate income at a critical time.Prospect -

• Individual needs the death benefit protection of life insurance

• Is age 50-70 and in reasonably good health• Is risk averse and wants a guaranteed death benefit• Seeks a policy that can adapt to changing circumstances• Sees value in additional income later in life if retirement assets are diminishing too quickly.

Rider* produces an income stream while maintaining a guaranteed death benefit to 100.*Income option Rider not yet approved in MO, IN, NC, PA, NY, ME, CT, MA, AK, and DE

2: A Very Different Term Product Term policies have been bought for years in the event of death. But many of these insured’s, at all ages, will suffer a CRITICAL ILLNESS like cancer or a heart attack or a CHRONIC ILLNESS long before they reach age 60.

Medical insurance does not pay all the costs that will mount up for long-term ongoing treatments. Some spend their savings, mortgage their homes, lose their jobs or file for bankruptcy. Imagine it’s one of YOUR clients and instead of being financially depleted, they bought this term policy because you gave them a choice.

Here is your opportunity to show LIVING BENEFITS, from a well-known A.M Bests “A+” Carrier, when individuals or business owners ask for Term Insurance.

Make Life Easy! Contact Dick or Jeff to discuss how these two innovative life insurance products can help your clients protect their financial futures!

Two InnovativeLife Insurance Products

Dick Reynolds, CLU V.P., Life Sales

22.indd 1 8/14/2013 1:05:38 PM

800.710.1115 www.greatplainsannuity.com

Stop ignoring wealth transfer sales in the Senior Market!Retired Baby Boomers...+ Trillions in Assets= Incredible Opportunity!

It’s estimated that Baby Boomers will pass more than $40 trillion of wealth to their heirs over the next 40 years. If you have senior citizen prospects and clients because you sell Annuities and/or Medicare Supplements, you are already positioned to greatly improve your client’s (AND their heirs) situation, and earn $thousands in new commissions.

YOUR NEXT STEP IS QUITE SIMPLE!

• Majority of Retirees are unaware of this important planning product• Some sales actually free up money to spend any way clients choose• Simplified & fast underwriting...easy to qualify, easy to SELL!• EXCELLENT Commissions!

One of our agents found $155,000 of “leave-behind” money, created a tax-free legacy amounting to over $275,000 and a $23,000 Commission check!

If you’re in the Senior Market, you should be talking to our Life insurance experts who show agents daily how to make these sales...

Call Dick Reynolds, CLU or Jeff Bregovy today and ask them to share the questions that could make you a hero to your clients and put Thousands of Commissions in your pocket!

Looking forLife Support?Contact our Life Insurance Experts for:

• Top carriers!• Advanced underwriting!• Case development expertise!

PAGE 23JUST the FACTS | 3RD QUARTER 2013

23.indd 10 8/14/2013 12:53:09 PM

10901 W 84th Terrace., Ste. 125Lenexa, KS 66214

800.710.1115 www.greatplainsannuity.com

100% Independently Owned!

GPALM PRODUCERS ACCESS ANNUITY & LIFE RATES 24 HOURS A DAY!

The Five“What-Ifs” of Retirement White Paper...

Available at our website or call for your copy!

Every day, your clients and prospects ask you similar questions on their most pressing retirement concerns.

Do you need a strategic way to answer them? A way to remove the typical trust barrier with new prospects and focus on their needs?

This toolkit can help! Now, you can address the five “what-if’s” of retirement with your prospects and clients and increase your chances of closing the next annuity sale:

Call (800) 710-1115 or visit our website today and learn how to access the complete “What Ifs” of Retirement Toolkit!

1. What if . . . Social Security is reduced?2. What if . . . I have a large medical expense?3. What if . . . I am confined to a healthcare facility?4. What if . . . I live a long time?5. What if . . . I don’t live a long time?

FOR PRODUCER USE ONLY. NOT TO BE USED WITH THE OFFER OR SALES OF ANNUITIES

24.indd 1 8/14/2013 12:53:29 PM