JLL Columbus Industrial Outlook: Q1 2017

8

JLL Research Columbus | Q1 2017 Industrial Outlook An in-depth look at the Columbus industrial market. Analysis includes leasing, sales, construction and employment.

-

Upload

andrew-batson -

Category

Real Estate

-

view

20 -

download

1

Transcript of JLL Columbus Industrial Outlook: Q1 2017

JLL Research

Columbus | Q1 2017

Industrial Outlook

An in-depth look at the Columbus industrial market. Analysis includes leasing, sales, construction and employment.

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Q1 2017

Insight

Columbus Industrial Outlook

The Columbus industrial market is experiencing a slow start to 2017 following a record breaking year as expected investment activity lingers. Just over 225,000 square feet was absorbed in Q1 2017, most of which can be attributed to a 717,000 square foot lease by Treehouse Foods at the close of 2016. Millions of square feet is proposed throughout the region, including within emerging submarkets of Etna, New Albany, and West Jefferson. Developers are ramping up the size of their proposed buildings to fulfill a market gap; existing inventory for large users is minimal throughout the market thus spurring plans for buildings between 750,000 and 1,000,000 square feet. Similar developments are also proposed in close proximity to Rickenbacker due to the Southeast’s existing availability of modern space. There are four recently completed, speculative buildings with availability ranging from 225,000 to 567,000 square feet. While these spaces may not satisfy the larger users, full occupancy is expected by the end of 2017.

The region is also experiencing sustained investment from manufacturers. Over 800,000 square feet of BTS space delivered in 2016 and similar activity is expected in 2017. Recent announcements include expansions from two automotive suppliers, in addition to a future 200,000 square foot lease for a credit card production company in the Southwest submarket.

OutlookWith overall vacancy at a staggering 5.4 percent, as well as a moderate construction pipeline of speculative space, the market will either experience a steadied or slightly rising vacancy rate as more space comes online. However, the overall effect on the market will be marginal despite slowed leasing velocity in the first quarter. Developers have taken note of strong market fundamentals and active tenants with both build-to-suit and speculative plans for new bulk warehouses that have shown to outperform older inventory, which will continue to attract users and push rents throughout the market.

Fundamentals Forecast

YTD net absorption 225,457 s.f. ▲QTD net absorption 225,457 s.f. ▲Under construction 2,597,527 s.f. ▲Total vacancy 5.4% ▶Average asking rent (NNN) $3.75 p.s.f. ▲Tenant improvements Falling ▼

0

5,000,000

10,000,000

2013 2014 2015 2016 YTD

2017

Supply and demand (s.f.) Net absorptionDeliveries

Proposed construction in line to meet user demand

9.5%

6.9% 6.4%5.3% 5.4%

2013 2014 2015 2016 YTD 2017

Total vacancy

$3.20

$3.40

$3.60

$3.80

2013 2014 2015 2016 YTD 2017

Average asking rents ($/s.f.)

• Recently completed speculative space remains available in the Southeast

• Submarkets throughout the region are seeing millions of square feet in proposed development

• Manufacturers are betting high on Central Ohio as investment and expansion continue

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Q1 2017

Statistics

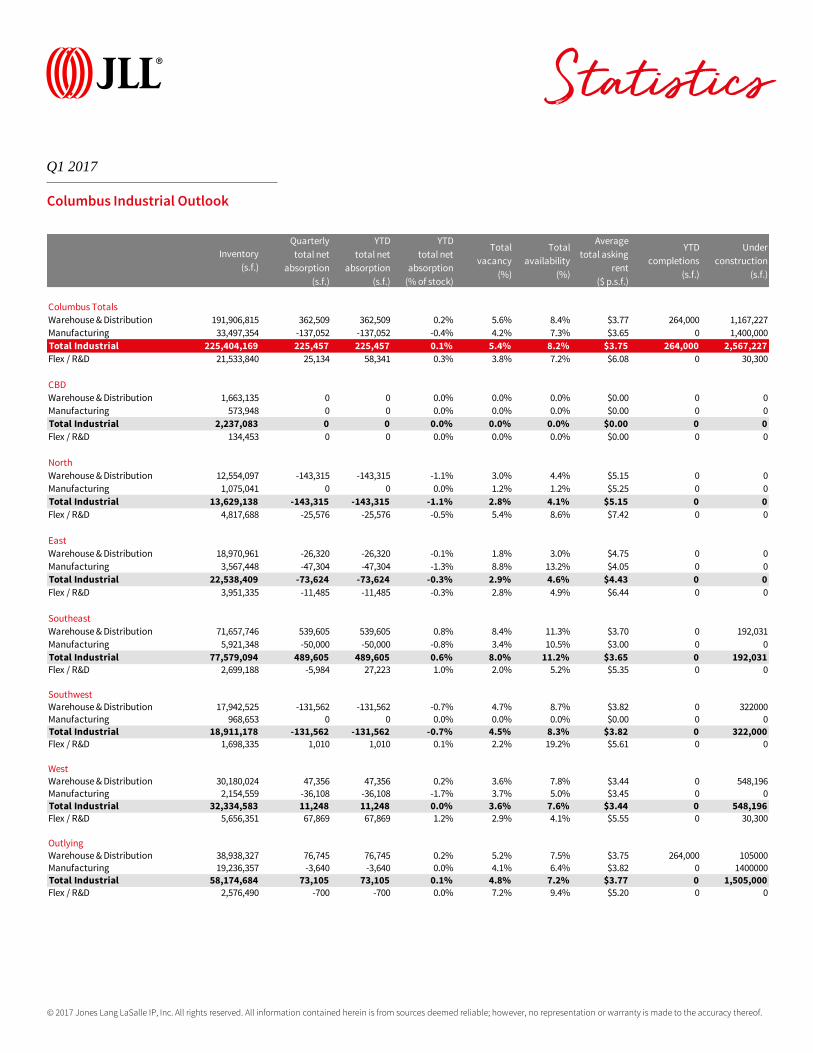

Columbus Industrial Outlook

Inventory

(s.f.)

Quarterly

total net

absorption

(s.f.)

YTD

total net

absorption

(s.f.)

YTD

total net

absorption

(% of stock)

Total

vacancy

(%)

Total

availability

(%)

Average

total asking

rent

($ p.s.f.)

YTD

completions

(s.f.)

Under

construction

(s.f.)

Columbus Totals

Warehouse & Distribution 191,906,815 362,509 362,509 0.2% 5.6% 8.4% $3.77 264,000 1,167,227

Manufacturing 33,497,354 -137,052 -137,052 -0.4% 4.2% 7.3% $3.65 0 1,400,000

Total Industrial 225,404,169 225,457 225,457 0.1% 5.4% 8.2% $3.75 264,000 2,567,227

Flex / R&D 21,533,840 25,134 58,341 0.3% 3.8% 7.2% $6.08 0 30,300

CBD

Warehouse & Distribution 1,663,135 0 0 0.0% 0.0% 0.0% $0.00 0 0

Manufacturing 573,948 0 0 0.0% 0.0% 0.0% $0.00 0 0

Total Industrial 2,237,083 0 0 0.0% 0.0% 0.0% $0.00 0 0

Flex / R&D 134,453 0 0 0.0% 0.0% 0.0% $0.00 0 0

North

Warehouse & Distribution 12,554,097 -143,315 -143,315 -1.1% 3.0% 4.4% $5.15 0 0

Manufacturing 1,075,041 0 0 0.0% 1.2% 1.2% $5.25 0 0

Total Industrial 13,629,138 -143,315 -143,315 -1.1% 2.8% 4.1% $5.15 0 0

Flex / R&D 4,817,688 -25,576 -25,576 -0.5% 5.4% 8.6% $7.42 0 0

East

Warehouse & Distribution 18,970,961 -26,320 -26,320 -0.1% 1.8% 3.0% $4.75 0 0

Manufacturing 3,567,448 -47,304 -47,304 -1.3% 8.8% 13.2% $4.05 0 0

Total Industrial 22,538,409 -73,624 -73,624 -0.3% 2.9% 4.6% $4.43 0 0

Flex / R&D 3,951,335 -11,485 -11,485 -0.3% 2.8% 4.9% $6.44 0 0

Southeast

Warehouse & Distribution 71,657,746 539,605 539,605 0.8% 8.4% 11.3% $3.70 0 192,031

Manufacturing 5,921,348 -50,000 -50,000 -0.8% 3.4% 10.5% $3.00 0 0

Total Industrial 77,579,094 489,605 489,605 0.6% 8.0% 11.2% $3.65 0 192,031Flex / R&D 2,699,188 -5,984 27,223 1.0% 2.0% 5.2% $5.35 0 0

SouthwestWarehouse & Distribution 17,942,525 -131,562 -131,562 -0.7% 4.7% 8.7% $3.82 0 322000Manufacturing 968,653 0 0 0.0% 0.0% 0.0% $0.00 0 0Total Industrial 18,911,178 -131,562 -131,562 -0.7% 4.5% 8.3% $3.82 0 322,000Flex / R&D 1,698,335 1,010 1,010 0.1% 2.2% 19.2% $5.61 0 0

WestWarehouse & Distribution 30,180,024 47,356 47,356 0.2% 3.6% 7.8% $3.44 0 548,196Manufacturing 2,154,559 -36,108 -36,108 -1.7% 3.7% 5.0% $3.45 0 0Total Industrial 32,334,583 11,248 11,248 0.0% 3.6% 7.6% $3.44 0 548,196Flex / R&D 5,656,351 67,869 67,869 1.2% 2.9% 4.1% $5.55 0 30,300

OutlyingWarehouse & Distribution 38,938,327 76,745 76,745 0.2% 5.2% 7.5% $3.75 264,000 105000Manufacturing 19,236,357 -3,640 -3,640 0.0% 4.1% 6.4% $3.82 0 1400000Total Industrial 58,174,684 73,105 73,105 0.1% 4.8% 7.2% $3.77 0 1,505,000Flex / R&D 2,576,490 -700 -700 0.0% 7.2% 9.4% $5.20 0 0

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Q1 2017

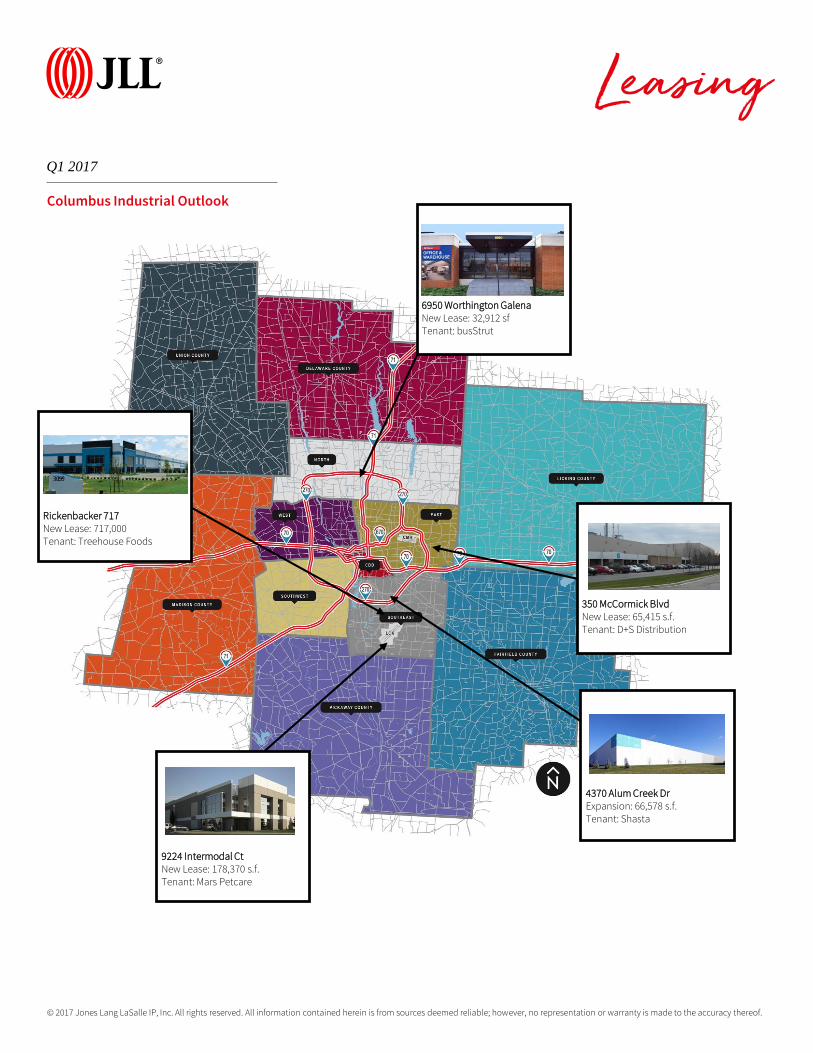

Leasing

Columbus Industrial Outlook

350 McCormick BlvdNew Lease: 65,415 s.f.Tenant: D+S Distribution

6950 Worthington GalenaNew Lease: 32,912 sfTenant: busStrut

4370 Alum Creek DrExpansion: 66,578 s.f.Tenant: Shasta

Rickenbacker 717New Lease: 717,000Tenant: Treehouse Foods

9224 Intermodal CtNew Lease: 178,370 s.f.Tenant: Mars Petcare

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Q1 2017

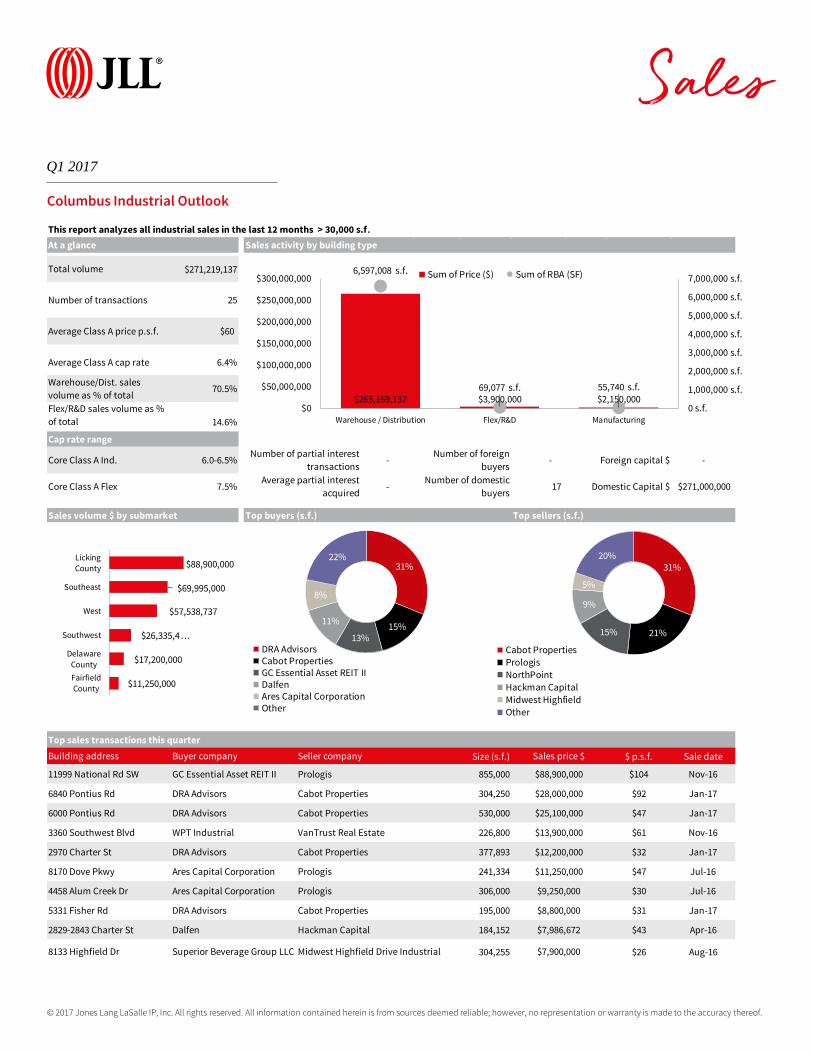

Sales

Columbus Industrial Outlook

This report analyzes all industrial sales in the last 12 months > 30,000 s.f.

$271,219,137

25

$60

6.4%

70.5%

14.6%

6.0-6.5% - - -

7.5% - 17 $271,000,000

Top sales transactions this quarter

Size (s.f.) $ p.s.f. Sale date

855,000 $104 Nov-16

304,250 $92 Jan-17

530,000 $47 Jan-17

226,800 $61 Nov-16

377,893 $32 Jan-17

241,334 $47 Jul-16

306,000 $30 Jul-16

195,000 $31 Jan-17

184,152 $43 Apr-16

304,255 $26 Aug-16

Sales activity by building type

Transactions details

Number of partial interest

transactions

Top sellers (s.f.)Top buyers (s.f.)

Number of domestic

buyers

Foreign capital $

Average partial interest

acquired

Number of foreign

buyers

Domestic Capital $

Average Class A price p.s.f.

At a glance

Total volume

Number of transactions

Average Class A cap rate

Sales volume $ by submarket

Warehouse/Dist. sales

volume as % of total

Flex/R&D sales volume as %

of total

Cap rate range

Core Class A Ind.

Core Class A Flex

11999 National Rd SW GC Essential Asset REIT II Prologis $88,900,000

Building address Buyer company Seller company Sales price $

3360 Southwest Blvd WPT Industrial

2970 Charter St DRA Advisors

6840 Pontius Rd DRA Advisors

6000 Pontius Rd DRA Advisors

Prologis $11,250,000

4458 Alum Creek Dr Ares Capital Corporation Prologis $9,250,000

8170 Dove Pkwy Ares Capital Corporation

8133 Highfield Dr Superior Beverage Group LLC Midwest Highfield Drive Industrial $7,900,000

5331 Fisher Rd DRA Advisors Cabot Properties $8,800,000

2829-2843 Charter St Dalfen Hackman Capital $7,986,672

Cabot Properties

Cabot Properties

VanTrust Real Estate

Cabot Properties

$28,000,000

$25,100,000

$13,900,000

$12,200,000

$265,169,137 $3,900,000 $2,150,000

6,597,008 s.f.

69,077 s.f. 55,740 s.f.

0 s.f.

1,000,000 s.f.

2,000,000 s.f.

3,000,000 s.f.

4,000,000 s.f.

5,000,000 s.f.

6,000,000 s.f.

7,000,000 s.f.

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,000

Warehouse / Distribution Flex/R&D Manufacturing

Sum of Price ($) Sum of RBA (SF)

31%

15%13%

11%

8%

22%

DRA AdvisorsCabot PropertiesGC Essential Asset REIT IIDalfenAres Capital CorporationOther

31%

21%15%

9%

5%

20%

Cabot Properties

Prologis

NorthPoint

Hackman Capital

Midwest Highfield

Other

$88,900,000

$69,995,000

$57,538,737

$26,335,4…

$17,200,000

$11,250,000

Licking

County

Southeast

West

Southwest

Delaware

County

Fairfield

County

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Q1 2017

Construction

Columbus Industrial Outlook

This report analyzes all industrial developments under construction & new deliveries in the last 12 months > 30,000 s.f.

Total leased at delivery (%) 66.1%

Total speculative at delivery (s.f.) 1,998,117

Total BTS at delivery (s.f.) 2,798,153

Total Owner-User at delivery (s.f.) 167,000

Total # of properties delivered 13

Asking rental rate (low - high) $3.50 - $4.25

Top projects delivered

Building RBA (s.f.) Delivery dateLeased at

delivery (%)

8820 Smith's Mill Rd 264,000 Q1 2017 77%

Amazon Fulfillment Center 1,000,000 Q3 2016 100%

11801 National Rd 855,000 Q3 2016 100%

Rogue Fitness 600,000 Q4 2016 100%

3219 Rohr Rd 567,000 Q2 2016 0%

Total pre-leased (%) 85.3%

Total speculative under construction (s.f.) 604,331

Total BTS under construction (s.f.) 1,993,196

Total Owner-user under construction (s.f.) -

Total # of properties UC 8

Asking rental rate (low - high) $3.95 - $3.95

Top 5 projects currently under construction

Building RBA (s.f.)Delivery

date

Pre-leased

(%)

Sofidel Plant 1,400,000 Q1 2018 100%

UPS Expansion 348,196 Q4 2017 100%

Southpark Place 322,000 Q2 2017 0%

845 Kaderly Dr 200,000 Q2 2017 100%

RGLP Gateway 2950 192,031 Q3 2017 100%

Southeast VanTrust Speculative

Submarket

Under construction

2,597,527Under construction (s.f.)

Under construction in-depth

Upcoming deliveries by year (s.f., excludes YTD completions)

New deliveries

Completions in-depth

4,963,270Total delivered (s.f.)

Historical deliveries (s.f.)

Construction typeOwnerSubmarket

East

Licking County

Southeast

Licking County

Strait Real Estate LLC

Griffin Capital REIT II

Duke Realty

Pizzuti

BTS

BTS

BTS

Speculative

Southeast

West

Southwest

West

Pickaway County

Speculative

BTS

Owner Construction type

Speculative

Duke Realty

Jim Pattison

Developments

Becknell Industrial

Cleve Corp

Pewamo Ltd

BTS

BTS

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

2011 2012 2013 2014 2015 2016 YTD 2017

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

2017 2018

BTS Speculative

© 2017 Jones Lang LaSalle IP, Inc. All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Q1 2017

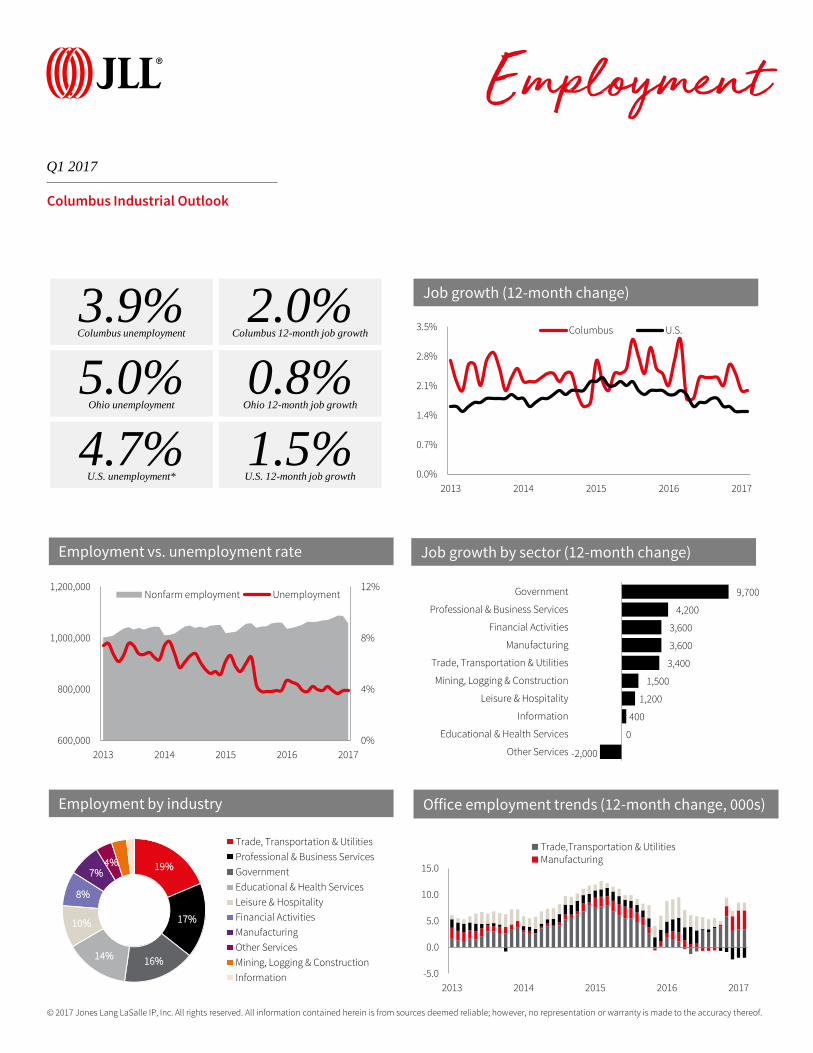

Employment

Columbus Industrial Outlook

Job growth by sector (12-month change)

4.7%U.S. unemployment*

1.5%U.S. 12-month job growth

3.9%Columbus unemployment

2.0%Columbus 12-month job growth

5.0%Ohio unemployment

0.8%Ohio 12-month job growth

-5.0

0.0

5.0

10.0

15.0

2013 2014 2015 2016 2017

Trade,Transportation & UtilitiesManufacturing

0.0%

0.7%

1.4%

2.1%

2.8%

3.5%

2013 2014 2015 2016 2017

Columbus U.S.

-2,000

0

400

1,200

1,500

3,400

3,600

3,600

4,200

9,700

-4,300 -2,300 -300 1,700 3,700 5,700 7,700 9,700 11,700

Other Services

Educational & Health Services

Information

Leisure & Hospitality

Mining, Logging & Construction

Trade, Transportation & Utilities

Manufacturing

Financial Activities

Professional & Business Services

Government

19%

17%

16%14%

10%

8%

7%4%

Trade, Transportation & Utilities

Professional & Business Services

Government

Educational & Health Services

Leisure & Hospitality

Financial Activities

Manufacturing

Other Services

Mining, Logging & Construction

Information

0%

4%

8%

12%

600,000

800,000

1,000,000

1,200,000

2013 2014 2015 2016 2017

Nonfarm employment Unemployment

Job growth (12-month change)

Job growth by sector (12-month change)Employment vs. unemployment rate

Employment by industry Office employment trends (12-month change, 000s)

© 2017 Jones Lang LaSalle IP, Inc.

All rights reserved. All information contained herein is from sources deemed reliable; however, no representation or warranty is made to the accuracy thereof.

Andrew BatsonVice President, Director of Research+1 216 937 [email protected]

Sam StoufferResearch Analyst+1 614 460 [email protected]

About JLL

JLL (NYSE: JLL) is a leading professional services firm that specializes in real estate and investment management. AFortune 500 company, JLL helps real estate owners, occupiers and investors achieve their business ambitions. In 2016, JLL had revenue of $6.8 billion and fee revenue of $5.8 billion and, on behalf of clients, managed 4.4 billion square feet, or 409 million square meters, and completed sales acquisitions and finance transactions of approximately $136 billion. At year-end 2016, JLL had nearly 300 corporate offices, operations in over 80 countries and a global workforce of more than 77,000. As of December 31, 2016, LaSalle Investment Management has $60.1 billion of real estate under asset management. JLL is the brand name, and a registered trademark, of Jones Lang LaSalle Incorporated. For further information, visit www.jll.com.

About JLL Research

JLL’s research team delivers intelligence, analysis and insight through market-leading reports and services that illuminate today’s commercial real estate dynamics and identify tomorrow’s challenges and opportunities. Our more than 400 global research professionals track and analyze economic and property trends and forecast future conditions in over 60 countries, producing unrivalled local and global perspectives. Our research and expertise, fueled by real-time information and innovative thinking around the world, creates a competitive advantage for our clients and drives successful strategies and optimal real estate decisions.