Solid take-up volume in Q1 2016 - JLL België TAKE-UP VOLUME IN Q1 2016 ... 2016 1 Willebroek...

6

Logistics Property in Belgium Solid take-up volume in Q1 2016 Quarterly Market Update - Pulse - May 2016 Take-up : 215,500 sq.m. in Q1 2016, almost triple the volume recorded in Q1 2015. € 10.1mln invested in Q1 2016; lack of product impacts volumes. Prime rent : € 55/sq.m./year. Prime rent forecast to remain stable. € Prime yield : 6.5%. Trend remains downward. Liège, DL Trilogiport - 150,000 sq.m. logistics development

Transcript of Solid take-up volume in Q1 2016 - JLL België TAKE-UP VOLUME IN Q1 2016 ... 2016 1 Willebroek...

1 / pulse | BELGIAN LOGISTICS MARKET | MAY 2016

Logistics Property in BelgiumSolid take-up volume in Q1 2016

Quarterly Market Update - Pulse - May 2016

Take-up : 215,500 sq.m. in Q1 2016, almost triple the volume recorded in Q1 2015.

€ 10.1mln invested in Q1 2016; lack of product impacts volumes.

Prime rent : € 55/sq.m./year. Prime rent forecast to remain stable.€ Prime yield : 6.5%.

Trend remains downward.

Liège, DL Trilogiport - 150,000 sq.m. logistics development

www.jll.be 2 / pulse | BELGIAN LOGISTICS MARKET | MAY 2016

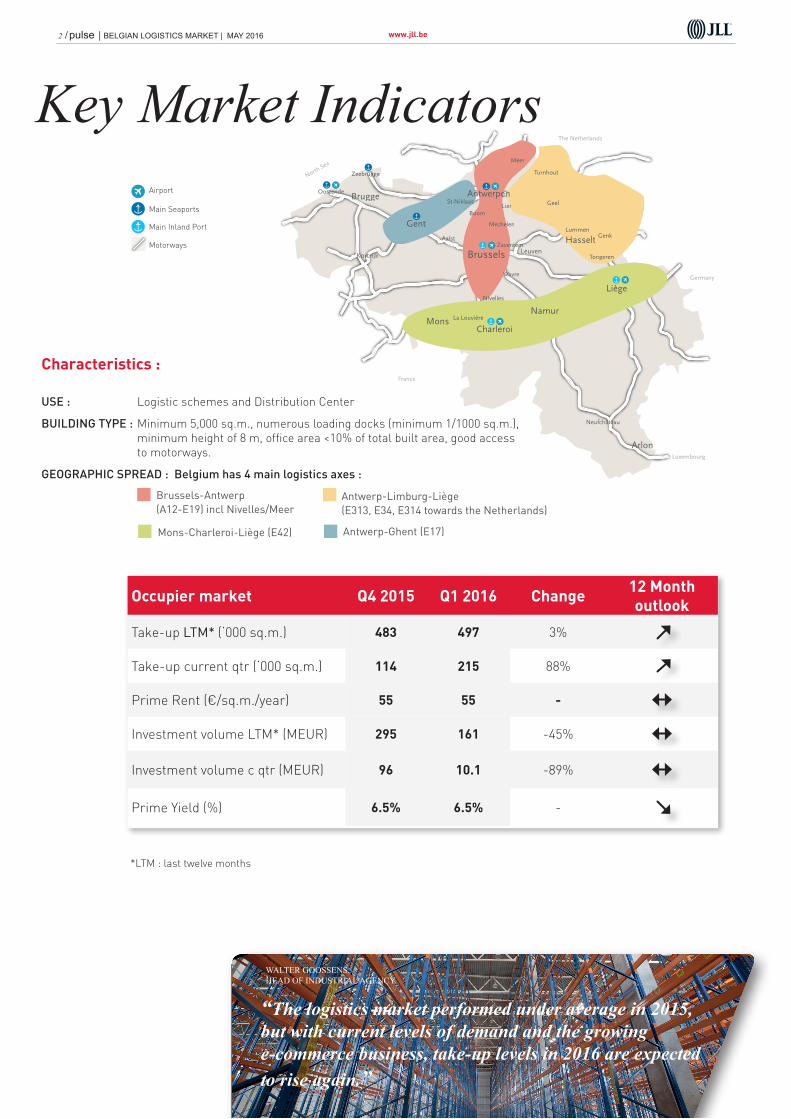

Occupier market Q4 2015 Q1 2016 Change 12 Month outlook

Take-up LTM* (‘000 sq.m.) 483 497 3%

Take-up current qtr (‘000 sq.m.) 114 215 88%

Prime Rent (€/sq.m./year) 55 55 -

Investment volume LTM* (MEUR) 295 161 -45%

Investment volume c qtr (MEUR) 96 10.1 -89%

Prime Yield (%) 6.5% 6.5% -

Key Market Indicators

*LTM : last twelve months

“The logistics market performed under average in 2015, but with current levels of demand and the growing e-commerce business, take-up levels in 2016 are expected to rise again.ˮ

WALTER GOOSSENS, HEAD OF INDUSTRIAL AGENCY

Brussels

Wavre

Lummen

GeelLier

Mechelen

Aalst

Boom

St-Niklaas

OostendeBrugge

Zeebrugge

Zaventem

Turnhout

Meer

Genk

Tongeren

Nivelles

La Louvière

Neufchâteau

Arlon

Namur

HasseltLeuven

Mons

Kortrijk

Antwerpen

Gent

Charleroi

Liège

The Netherlands

France

Germany

Luxembourg

North Sea

Airport

Main Sea Ports

Main Inland Ports

Motorway

Characteristics :

USE : Logistic schemes and Distribution Center

BUILDING TYPE : Minimum 5,000 sq.m., numerous loading docks (minimum 1/1000 sq.m.), minimum height of 8 m, office area <10% of total built area, good access to motorways.

GEOGRAPHIC SPREAD : Belgium has 4 main logistics axes :

Brussels

Wavre

Lummen

GeelLier

Mechelen

Aalst

Boom

St-Niklaas

Oostende Brugge

Zeebrugge

Zaventem

Turnhout

Genk

Tongeren

Nivelles

La Louvière

Neufchateau

Arlon

Namur

Hasselt

Mons

Kortrijk

Antwerpen

Gent

Charleroi

LiègeE42

E42

E429

E403

E314

E313

E34

E314

E40

E40

E17

N49

E17

E411

E19

A12

E19

E411

E25Airport

Main Seaports

Main Inland Port

Motorways

Main Railways

Main Rivers and Canals

Golden triangle

Airport

Main Seaports

Main Inland Port

Motorways

www.jll.be 3 / pulse | BELGIAN LOGISTICS MARKET | MAY 2016

SOLID TAKE-UP VOLUME IN Q1 2016

A total of 215,500 sq.m. was taken up in Q1 2016, almost triple the volume registered in Q1 2015, and the highest quarterly volume since end 2013. Logistics take-up seems to recover from a modest year 2015.

The highest volume was recorded on the E313 axis, 81,400 sq.m., including the largest transaction of the year so far : a build-to-suit project for Casa International in Olen (50,000 sq.m.). Other large transactions were registered in the Port of Antwerp (left bank), where 32,000 sq.m. were developed for ACS, and a 25,000 sq.m. project for Delhaize in Ninove. In April, a turn-key project of 51,500 sq.m. was pre-let in Antwerp East Port.

MORE LARGE TRANSACTIONS

13 transactions were registered in the first quarter, slightly above the 5-y average of #12. The average size of a transaction was 30% up on the 5-year average in the period 2011-2015. With already 7 transactions above 20,000 sq.m. as at end April against an annual average of 10 in the past five year, the market performance in 2016 will largely exceed its modest performance of 2015.

HIGH DEVELOPMENT VOLUME IN 2016, BUT NO SPECULATION

Just over 35,000 sq.m. were delivered in Q1, rising to 80,000 sq.m. at end April. Apart from 10,000 sq.m. delivered speculatively in the Antwerp East Port project, all projects were non-speculative. In addition, another 450,000 sq.m. is under construction non-speculatively throughout Belgium for completion in 2016 and 145,000 sq.m. are under way for delivery in 2017. The volume delivered in 2016 will be 67% in excess of the the 5-year average, which stands at 319,000 sq.m. The three largest projects under construction are on the E313 axis : Mobis Parts in Beringen (55,000 sq.m.), 51,500 sq.m. in Antwerp East Port and 50,000 sq.m. for Casa International in Olen.

TAKE-UP VOLUMES PER AXIS

Occupier market

HIGH #TRANSACTIONS IN Q1 2016

0

300.000

600.000

900.000

1.200.000

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

Q1

20

16

sq.m.

Antwerp-Brussels Antwerp-Ghent E313

Walloon Axis Other Belgium 10-yr Ave

0

10

20

30

40

50

60

2012 2013 2014 2015 Q1 2016

29 3123

17

2

1 1

15

2

912

6 7

4

84

63

1

58

78

4

#

Antwerp-Brussels Antwerp-Ghent E313 Walloon axis Other

Source all charts : JLL

COMPLETIONS AND FUTURE SUPPLY

318.885

- 50.000

100.000 150.000 200.000 250.000 300.000 350.000 400.000 450.000 500.000

2011 2012 2013 2014 2015 Q12016

2017e

sq.m.

Completions FS Spec FS Non-Spec 5-y Average

www.jll.be 4 / pulse | BELGIAN LOGISTICS MARKET | MAY 2016

55

45 43

40

45

50

55

60

Q4 11 Q4 12 Q4 13 Q4 14 Q4 15 Q1 16

€/sqm p.a.

Antwerp-Brussels Antwerp-GhentE313 Walloon Axis

PRIME RENTS BY AXIS

Source all Charts: JLL

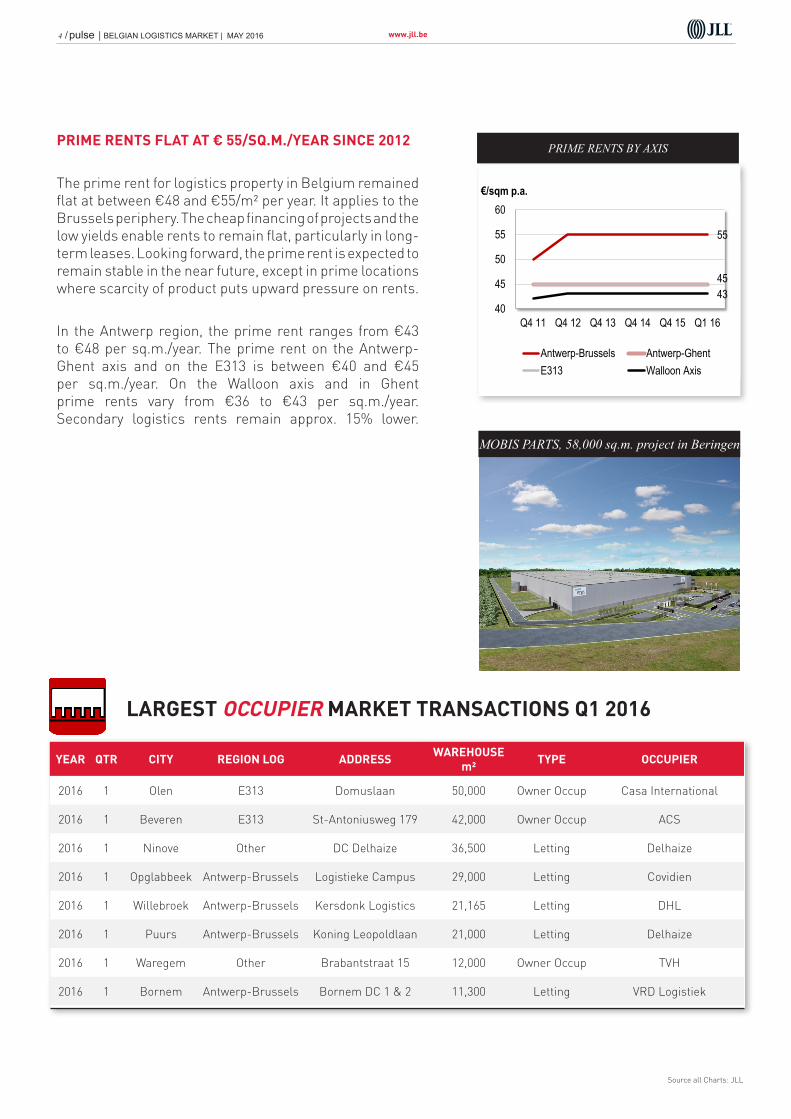

PRIME RENTS FLAT AT € 55/SQ.M./YEAR SINCE 2012

The prime rent for logistics property in Belgium remained flat at between €48 and €55/m² per year. It applies to the Brussels periphery. The cheap financing of projects and the low yields enable rents to remain flat, particularly in long-term leases. Looking forward, the prime rent is expected to remain stable in the near future, except in prime locations where scarcity of product puts upward pressure on rents.

In the Antwerp region, the prime rent ranges from €43 to €48 per sq.m./year. The prime rent on the Antwerp-Ghent axis and on the E313 is between €40 and €45 per sq.m./year. On the Walloon axis and in Ghent prime rents vary from €36 to €43 per sq.m./year. Secondary logistics rents remain approx. 15% lower.

YEAR QTR CITY REGION LOG ADDRESS WAREHOUSE m² TYPE OCCUPIER

2016 1 Olen E313 Domuslaan 50,000 Owner Occup Casa International

2016 1 Beveren E313 St-Antoniusweg 179 42,000 Owner Occup ACS

2016 1 Ninove Other DC Delhaize 36,500 Letting Delhaize

2016 1 Opglabbeek Antwerp-Brussels Logistieke Campus 29,000 Letting Covidien

2016 1 Willebroek Antwerp-Brussels Kersdonk Logistics 21,165 Letting DHL

2016 1 Puurs Antwerp-Brussels Koning Leopoldlaan 21,000 Letting Delhaize

2016 1 Waregem Other Brabantstraat 15 12,000 Owner Occup TVH

2016 1 Bornem Antwerp-Brussels Bornem DC 1 & 2 11,300 Letting VRD Logistiek

LARGEST OCCUPIER MARKET TRANSACTIONS Q1 2016

MOBIS PARTS, 58,000 sq.m. project in Beringen

www.jll.be 5 / pulse | BELGIAN LOGISTICS MARKET | MAY 2016

LARGEST INVESTMENT TRANSACTIONS 2016

YEAR QTR CITY ADDRESS WHm²

PriceMEUR

YIELD% SELLER BUYER TYPE

2016 2 Willebroek De Hulst - Federal Mogul 29,000 9.1 7.5 MG Real Estate Montea Investment

2016 1 Turnhout Bremheide 10 14,250 5.5 Trans-O-Flex Private Investment

2016 1 Bornem Beherman46,000 (land) 4.6 - Beherman

Invest NV Montea Development

RECORD VOLUME INVESTED IN LOGISTICS IN 2015

10.1 MEUR were invested in logistics in Q1 2016, in 2 transactions, rising to 19.2 MEUR as at today. The market suffers from a lack of product which compresses transaction volumes.

Largest logistics transaction was the sale of the Transoflex site in Turnhout on the E313 axis (5.5MEUR), followed by the sale of the Beherman site in Bornem to B-REIT Montea, a redevelopment project. In April B-REIT Montea acquired the build-to-suit project by MG Real Estate for Federal Mogul in Willebroek for 9.1 MEUR. Sellers and buyers were Belgian, either private investors, B-REIT or property companies.

The prime yield for logistics properties on conventional lease terms remained stable at 6.5%. The prime yield remains under downward pressure given the lack of prime product and the appetite from both national and international investors for this asset class. We may see yields trend toward 6% by year-end.

Investment marketLOGISTICS INVESTMENT VOLUME

227

118 98153

295

10

178

0

50

100

150

200

250

300

Q411

Q412

Q413

Q414

Q415

Q116

€ mln

Volume MEUR 5-Y Ave

Source all Charts: JLL

«Investors’ appetite for this asset class remains high, both from

local and international parties, but there is a lack of product.»

JEAN-PHILIP VRONINKSHEAD OF CAPITAL MARKETS

6 / pulse | BELGIAN LOGISTICS MARKET | MAY 2016

JLL Contacts

JEAN-PHILIP VRONINKS (*)HEAD OF CAPITAL MARKETS - BELUX+32 (0) 2 550 26 [email protected]

WALTER GOOSSENSHEAD OF INDUSTRIAL LEASING - BELGIUM+32 (0)2 550 25 [email protected]

PIERRE-PAUL VERELSTHEAD OF RESEARCH - BELUX+32 (0) 2 550 25 [email protected](*

) R

EV

RO

N G

CV

COPYRIGHT © JONES LANG LASALLE IP, INC. 2016. All rights reserved. No part of this publication may be reproduced or transmitted in any form or by any means without prior written consent of Jones Lang LaSalle. It is based on material that we believe to be reliable. Whilst every effort has been made to ensure its accuracy, we cannot offer any warranty that it contains no factual errors. We would like to be told of any such errors in order to correct them.

Printing information: paper, inks, printing process, recycle directive.

copy

righ

t cov

er p

hoto

: B

iem

ar &

Bie

mar

, Bur

eau

d’Et

udes

-Arc

hite

ctes

JLL Research Advisory Services

JLL time series for quarterly and submarket data are available on request, as well as tailormade consulting. This is a fee-based service.

JLL Research produces on a quarterly basis detailed submarket reports about Brussels office districts, the retail property market and the semi-industrial and logistics property market. These are available on request against paying subscription.

Our Research & Advisory service also prepares micro-location studies for landlords with a focus on rental analysis, existing and future competition analysis with GIS mapping, transaction analysis and SWOT.

Contacts: Pierre-Paul VerelstHead of Research BeLux+ 32 2 550 25 [email protected]

Ann VanderwegenResearch Analyst+ 32 2 550 26 [email protected]