January 2013 Tax bulletin - SGV & Co. · PDF file2 Tax Bulletin BIR Rulings • An upstream...

33

Tax bulletin January 2013

Transcript of January 2013 Tax bulletin - SGV & Co. · PDF file2 Tax Bulletin BIR Rulings • An upstream...

1

Tax bulletin January 2013

2 Tax Bulletin

BIR Rulings

• Anupstreammerger,wheretheparentcompanywillnotbeissuingsharestothesubsidiariesinexchangefortheassetstobetransferred,isnotconsideredatax-freemergerunderSection40(C)(2)oftheTaxCode.(Page 3)

• UndertheRP-NetherlandsTaxTreaty,the10%preferentialtaxrateondividendsapplieswhentherecipientofthedividendsisacompanywhosecapitaliswhollyorpartlydividedintoshares,andwhichholdsatleast10%ofthecapitalofthecompanypayingthedividends.(Page 4)

• IncomederivedbyaJapaneseenterprisefromservicesrenderedinthePhilippines,foranaggregateperiodofnotmorethan6monthswithinanytaxableyear,isnotsubjecttoPhilippineincometax.

ServicesrenderedinthePhilippinesbyanon-residentinfavorofaPhilippineEconomicZoneAuthority(PEZA)-registeredentityareexemptfromVATunderSection109(K)oftheTaxCode.(Page 4)

BIR Issuances

• RevenueRegulations(RR)No.17-2012prescribestheimplementingguidelinesontherevisedtaxratesonalcoholandtobaccoproducts,pursuanttoRepublicAct(RA)No.10351,otherwiseknownas“AnActRestructuringtheExciseTaxonAlcoholandTobaccoProductsbyAmendingSections141,142,143,144,145,8,131and288ofRepublicActNo.8424,otherwiseknownastheNationalInternalRevenueCodeof1997,asamendedbyRepublicActNo.9334,andforotherpurposes.”(Page 5)

• RRNo.1-2013expandsthecoverageoftaxpayersrequiredtofiletaxreturnsandpaytaxesthroughtheElectronicFilingandPaymentSystem(eFPS),toincludenationalgovernmentagencies(NGAs)mandatorilyrequiredtousetheElectronicTaxRemittanceAdvice(eTRA).(Page 12)

• RevenueMemorandumCircular(RMC)No.84-2012clarifiesthepropertaxtreatmentofinterestincomeearningsonloansthatarenotsecuritized,assignedorparticipatedout.(Page 15)

• RMCNo.90-2012prescribestheinitialclassificationsandtaxratesforalcoholandtobaccoproductsexistinginthemarketpursuanttoRANo.10351.(Page 15)

►• RMCNo.91-2012supplementsRMCNo.63-2012datedOctober29,2012oninvoicingandrecordingofincomepaymentsformediaadvertisingplacementsunderasplitpaymentschemeorarrangement.(Page 16)

►• RMCNo.2-2013clarifiescertainprovisionsofRRNo.12-2012onthedeductibilityofdepreciationexpenseasitrelatestothepurchaseofvehicles,andotherrelatedexpenses,andtheinputtaxesallowed.(Page 17)

• RMCNo.4-2013requirestax-exempthospitalstosecurerevalidatedtaxexemptionrulings/certificates.(Page 17)

• RMCNo.6-2013clarifiestaxpayers’concernsontheauditprogram,andtheirresponsibilityforengagingtaxagents/practitioners.(Page 18)

3

BOC Issuances

• CustomsMemorandumOrder(CMO)No.16-2012prescribesa10-yearvalidityperiodfordutydrawbacktaxcreditcertificates(TCCs).(Page 19)

• CustomsAdministrativeOrder(CAO)No.1-2013prescribestherulesandregulationsimplementingtheSuperGreenLane(SGL)PlusFacility.(Page 19)

SEC Issuances

• SECMemorandumCircular(MC)No.11prescribestheguidelinesforaccreditationofinstitutionaltrainingprovidersoncorporategovernance.(Page 22)

• SECMCNo.12prescribestheguidelinesonthedisclosureoftransactionswithretirementbenefitfunds.(Page 24)

• SECMCNo.1requirestheinclusionoftheTaxpayer’sIdentificationNumber(TIN)orpassportnumberofforeigninvestorsinallforms,papersanddocumentsfiledwiththeSEC.(Page 25)

• SECMCNo.3amendstherulesonthedateofsubmissionoftheinterimsemi-annualfinancialstatementsrequiredforfinancingandlendingcompanies.(Page 25)

BSP Issuances

• CircularNo.779amendstheregulationsonSingleBorrower’sLimit.(Page 26)

• CircularNo.780prescribesguidelinesgoverningtheimplementationoftheSyrianPoundCurrencyExchangeFacility(CEF).(Page 27)

• CircularNo.781amendstheBaselIIIimplementingguidelinesonMinimumCapitalRequirements.(Page 28)

• CircularNo.782amendsAppendix45(NotesonMicrofinance)ofSectionX361oftheMORB.(Page 29)

• CircularNo.783amendstheregulationsonrelocationandvoluntaryclosure/saleofbranches/otherbankingoffices(OBOs).(Page 30)

Court Decision

• Negligence,whetherslightorgross,isnotequivalenttofraudwithintenttoevadetaxthatiscriminallypunishableundertheTaxCode.Fraudmustamounttointentionalwrongdoingwiththesoleobjectofavoidingtax.(Page 31)

BIR Rulings

BIR Ruling No. 614-12 dated November 9, 2012

Facts:

ACo.,adomesticcorporation,enteredintoamergerwithitswholly-owneddomesticsubsidiaries,BCo.andCCo.ACo.isthesurvivingcorporation.Pursuanttothemerger,BCo.andCCo.willtransfertheirallassetsandliabilitiestoACo.However,sinceBCo.andCCo.arewholly-ownedbyACo.priortothemerger,ACo.willnolongerissueanysharesofstockinconsiderationoftheassetsandliabilitiestransferred.

Anupstreammerger,wheretheparentcompanywillnotbeissuingsharestothesubsidiariesinexchangefortheassetstobetransferred,isnotconsid-eredatax-freemergerunderSection40(C)(2)oftheTaxCode.

4 Tax Bulletin

Issue:

IsthemergerbetweenACo.,BCo.andCCo.consideredatax-freemergerunderSection40(C)(2)oftheTaxCode?

Ruling:

No.Theintendedre-organizationisanupstreammergerbetweenaparentcompanyanditssubsidiarieswheretheparentcompanywillnotbeissuinganysharestothesubsidiariesinexchangefortheassetstobetransferredasaresultofthemerger.Ineffect,thetransfertakesthenatureofadonationmadebythesubsidiariestotheirparentcompany,contrarytowhatiscontemplatedinSection40(C)(2)oftheTaxCode.Inthesamemanner,theintendedmergeralsohastheeffectofdissolvingandliquidatingthesubsidiarieswithoutpaymentofcorrespondingtaxes.

BIR Ruling No. ITAD 381-2012 dated November 22, 2012

Facts:

ACo.,aDutchcompanywithcapitalwhollydividedintoshares,isthebeneficialownerof99.99%ofthesharesinBCo.,adomesticcorporation.BCo.declaredandremittedcashdividendsinfavorofACo.

Issue:

Arethedividendssubjecttothe10%preferentialtaxrateundertheRP-NetherlandsTaxTreaty?

Ruling:

Yes.UndertheRP-NetherlandsTaxTreaty,the10%preferentialtaxrateondividendsapplieswhentherecipientofthedividendsisacompanywhosecapitaliswhollyorpartlydividedintoshares,andwhichholdsatleast10%ofthecapitalofthecompanypayingthedividends.

BIR Ruling No. ITAD 393-12 dated December 11, 2012

Facts:

ACo.,aresidentofJapan,renderedconsultancyservicesforafeetoBCo.,aPEZA-registereddomesticcorporation.ACo.sentitspersonneltothePhilippinestoprovidetheservicesforanaggregateperiodof17daysfortheentiredurationoftheagreement.

Issues:

1. IstheincomederivedbyACo.subjecttoPhilippineincometax?

2. AretheservicesrenderedbyACo.inthePhilippinessubjecttovalue-addedtax(VAT)?

Ruling:

1. No.UndertheRP-JapanTaxTreaty,aJapaneseenterpriseshallbesubjecttotaxinthePhilippinesonbusinessprofitstotheextentattributabletoapermanent

UndertheRP-NetherlandsTaxTreaty,the10%preferentialtaxrateondividendsapplieswhentherecipientofthedividendsisacompanywhosecapitaliswhollyorpartlydividedintoshares,andwhichholdsatleast10%ofthecapitalofthecompanypayingthedividends.

IncomederivedbyaJapaneseenter-prisefromservicesrenderedinthePhilippines,foranaggregateperiodofnotmorethan6monthswithinanytaxableyear,isnotsubjecttoPhilippineincometax.

ServicesrenderedinthePhilippinesbyanon-residentinfavorofaPEZA-registeredentityareexemptfromVATunderSection109(K)oftheTaxCode.

5

establishment(PE)situatedinthePhilippines.UndertheRP-JapanTaxTreaty,aJapaneseenterprisemaybedeemedtohaveaPEinthePhilippinesifitfurnishesinthePhilippinesconsultancyservicesorsupervisoryservicesinconnectionwithacontractforabuildingconstructionorinstallationproject,throughemployeesorotherpersonnel–otherthananagentofindependentstatus–providedthatsuchactivitiescontinue(forthesameprojector2ormoreconnectedprojects)foraperiodorperiodsaggregatingmorethan6monthswithinanytaxableyear.

SincetheservicesperformedbyACo.inthePhilippinestotaledanaggregateperiodofonly17days,ACo.isnotdeemedtohaveaPEinthePhilippines.Hence,theincomederivedbyACo.fromtheconsultancyservicesshallnotbesubjecttoPhilippineincometax.

2. No.Asageneralrule,thesaleofgoodsandservicestoentitiesexemptfromVAT,suchasPEZA-registeredentities,iszero-rated.However,insteadofzero-ratingwhichisnotavailabletonon-residentsuppliers,thetransactionwillbetreatedasVATexemptpursuanttoSection109(K)oftheTaxCode,whichprovidesVATexemptionfortransactionsthatareexemptunderspeciallaws.

BIR Issuances

Revenue Regulations No. 17-2012 dated December 21, 2012

Definition of Terms

• ActreferstoRANo.10351,otherwiseknownasAnActRestructuringtheExciseTaxonAlcoholandTobaccoProducts.

• Carbonated Winereferstoaneffervescentwineartificiallychargedwithcarbondioxideandcontainingmorethan0.392ofcarbondioxideper100millilitersofwine.

• Cigarettes Packed by Handreferstothemannerofpackagingcigarettesticksusinganindividualperson’shandsandnotthroughanyothermeans,suchasamechanicaldevice,machineorequipment.

• Compounded Liquorsreferstointoxicatingbeveragesconcoctedbyorresultingfrommixtureof,oradditionto,distilledspirits,eitherbeforeorafterrectification,ofanycoloringmatter,flavoringextractoressenceorotherkindofwine,liquororotheringredient.

• Net Retail Price referstothepriceatwhichthealcoholandtobaccoproductsaresoldinretailinatleastfivemajorsupermarketsinMetroManila,excludingtheamountintendedtocovertheapplicableexcisetaxandVAT.ForalcoholandtobaccoproductswhicharemarketedoutsideMetroManila,thenetretailpriceshallmeanthepriceatwhichthealcoholandtobaccoproductsaresoldinatleastfivemajorsupermarketsintheregion,excludingtheamountintendedtocovertheapplicableexcisetaxandVAT.

• Sparkling Wine or Champagnereferstoaneffervescentwinecontainingmorethan0.392gramsofcarbondioxideper100millilitersofwineresultingsolelyfromthesecondaryfermentationofthewinewithinaclosedcontainer.

• Still winereferstowinecontainingnotmorethan0.392ofcarbondioxideper100millilitersofwine.

RRNo.17-2012prescribestheimple-mentingguidelinesontherevisedtaxratesonalcoholandtobaccoproducts,pursuanttoRANo.10351,otherwiseknownas“AnActRestructuringtheExciseTaxonAlcoholandTobaccoProductsbyAmendingSections141,142,143,144,145,8,131and288ofRepublicActNo.8424,otherwiseknownastheNationalInternalRevenueCodeof1997,asamendedbyRepublicActNo.9334,andforotherpurposes.”

6 Tax Bulletin

• Suggested Net Retail PricereferstothenetretailpriceatwhichlocallymanufacturedorimportedalcoholortobaccoproductisintendedtobesoldbythemanufacturerorimporteratretailinmajorsupermarketsorretailoutletsintheprescribedminimumnumberofRevenueRegionsforbrandswithnationalorregionalmarkets.

Revised Tax Rates and Base

Thefollowingscheduleshowstherevisedratesandbasesofthespecifictaxtobelevied,assessedandcollectedonalcoholortobaccoproducts:

PRODUCTDATE OF EFFECTIVITY OF TAX RATES

1Jan 2018Onwards2013 2014 2015 2016 2017

A.ALCOHOLPRODUCTS(1)DistilledSpirits

(a)Ad ValoremTaxRates

Basedonthenetretailpriceperproof(excludingexcisetaxandVAT)

15% 15% 20% 20% 20% 20%

(b)SpecificTax

Perproofliter P20.00 P20.00 P20.00 P20.80 P21.63

Effective1January2016,thespecifictaxrateshallbeincreasedby4%everyyearthereafter.

(2)Wines

(a)Sparklingwines/champagneswherethenetretailprice(excludingexcisetaxandVAT)perbottleof750ml.,regardlessofproofis:(1)P500.00orless

(2)MorethanP500.00

(b)Stillwinesandcarbonatedwinescontaining14%ofalcoholbyvolumeorless

Perliter

P250.00

P700.00

P30.00

Perliter

P260.00

P728.00

P31.20

Perliter

P270.40

P757.12

P32.45

Perliter

P281.22

P787.40

P33.75

Perliter

P292.47

P818.90

P35.10

Effective1January2014,thespecifictaxrateshallbeincreasedby4%everyyearthereafter

7

(c)Stillwinesandcarbonatedwinescontainingmorethan14%ofalcoholbyvolumebutnotmore25%ofalcoholbyvolume

P60.00 P62.40 P64.90 P67.50 P70.20

(d)Fortifiedwinescontainingmorethan25%ofalcoholbyvolumeshallbetaxedasdistilledspirits.

Taxedasdistilledspirits

Taxedasdistilledspirits

Taxedasdistilledspirits

Taxedasdistilledspirits

Taxedasdistilledspirits

(3)Fermentedliquors,wherethenetretailprice(excludingexcisetaxandVAT)perliterofvolumecapacityis:

(a)P50.60orless

(b)MorethanP50.60

Fermentedliquorsbrewedandsoldatmicrobreweriesorsmallestablishmentssuchaspubsandrestaurants,regardlessofthenetretailprice.

Perliter

P15.00

P20.00

P28.00

Perliter

P17.00

P21.00

P29.12

Perliter

P19.00

P22.00

P30.28

Perliter

P21.00

P23.00

P31.50

Perliter

P23.50

P23.50

P32.76

Effective1January2018,thespecifictaxrateshallbeincreasedby4%everyyearthereafter

Effective1January2014,thespecifictaxrateshallbeincreasedby4%everyyearthereafter

B.TOBACCOPRODUCTS(1)TobaccoProducts

(a)Tobaccotwistedbyhandorreducedintoaconditiontobeconsumedinanymannerotherthantheordinarymodeofdryingandcuring

(b)Tobaccopreparedorpartiallypreparedwithorwithouttheuseofanymachineorinstrumentorwithoutbeingpressedorsweetened

Perkg.

P1.75

P1.75

Perkg.

P1.82

P1.82

Perkg.

P1.89

P1.89

Perkg.

P1.97

P1.97

Perkg.

P2.05

P2.05

Effective1January2014,thespecifictaxrateshallbeincreasedby4%everyyearthereafter

8 Tax Bulletin

(c)Fine-cutshortsandrefuse,scraps,clippings,cuttings,stems,midribs,andsweepingsoftobacco

P1.75 P1.82 P1.89 P1.97 P2.05

(2)Chewingtobacco,unsuitableinanyothermanner

P1.50 P1.56 P1.62 P1.68 P1.75

(3)Cigars

(a)Basedonthenetretailpricepercigar(excludingexciseandVAT)

(b)Percigar

PerPiece

20%

P5.00

PerPiece

20%

P5.20

PerPiece

20%

P5.41

PerPiece

20%

P5.62

PerPiece

20%

P5.85

Effective1January2014,thespecifictaxrateshallbeincreasedby4%everyyearthereafter

(4)Cigarettespackedbyhand

PerPackP12.00

PerPackP15.00

PerPackP18.00

PerPackP21.00

PerPackP30.00

Effective1January2018,thespecifictaxrateshallbeincreasedby4%everyyearthereafter

(5)Cigarettespackedbymachine,wherethenetretailprice(excludingexcisetaxandVAT)perpackis:

(a)P11.50andbelow

(b)MorethanP11.50

P12.00

P25.00

P17.00

P27.00

P21.00

P28.00

P25.00

P29.00

P30.00

P30.00

Tax Classification of Alcohol and Tobacco products

►• AnyalcoholortobaccoproductthatisintroducedinthedomesticmarketonoraftertheeffectivityoftheActshallbeinitiallytax-classifiedaccordingtotheirsuggestednetretailpricesasdeclaredintheprescribedmanufacturer’sorimporter’sswornstatement,subjecttotheinitialvalidationandrevalidationrequirementsprescribedunderRRNo.3-2006,asamendedbySection6oftheseRegulations.

• Incaseofanalcoholand/ortobaccoproductthatwasdulyregisteredwiththeBIRbeforetheeffectivityoftheActbutwasnottax-classifiedbytheBIRaccordingtothenewtaxratesprovidedundertheAct,suchproductshallbe

9

treatedasnewlyintroducedproductuponitsre-introductioninthedomesticmarketaftertheeffectivityoftheAct.Accordingly,thetaxclassificationofsuchproductshallbebasedonthesuggestednetretailpricedeclaredintheswornstatement,subjecttotheinitialvalidationandrevalidationrequirements.

• Thepropertaxclassificationofallfermentedliquorsandtobaccoproducts,whetherregisteredbeforeoraftertheeffectivityoftheAct,shallbedeterminedevery2yearsfromthedateofeffectivityoftheAct.

• Forpurposesoftaxclassification,alcoholortobaccoproducts,whetherimportedordomesticallymanufactured,shallbetaxedaccordingtotheirindividualbrandname(whetherornotwithprefixorsuffix),colorand/ordesignoflabel(suchaslogo,font,picturegramandthelike),mannerand/orformofpackagingorsizeofcontaineroftheproduct.Accordingly,situationslike(butnotlimitedto)thefollowinginstancesshallbetaxeddifferently:

1. Twoproductsbearingexactlythesamerootnamebutwithdifferentsuffixesorprefixes;

2. Twoproductsbearingexactlythesamebrandnamebutwithdifferentcolorsand/ordesignoflabels;

3. Twoproductsbearingexactlythesamebrandnameandlabelbutwithdifferentformsofpackaging(e.g.,softpacksandhardpacksforcigarettes,orinbottles,cansorkegsforalcoholproducts);

4. Twoproductsbearingexactlythesamebrandnameandlabelbutwithdifferentsizesofcontainer(e.g.,oneliter,500ml.,330ml.andsoonforalcoholproducts);

5. Oneproductissoldonaregularbasis,whiletheotherproductisintroducedonalimitedbasissuchasaspecialedition,forspecificoccasionandothersimilarinstances.

• AnydownwardreclassificationofanyfermentedliquorproductthatisdulyregisteredwiththeBIRatthetimeofeffectivityoftheAct,whichwillreducethetaximposedintheseRegulations,orthepaymentofsuchtax,shallbeprohibited.Starting1January2014,theapplicabletaxrateshallbeincreasedby4%annually,butitshallnotbelowerthantheratesprescribedundertheseRegulations.

• Therevalidationofthesuggestednetretailpriceofanewlyintroducedalcoholortobaccoproductshallbeconductedaftertheendof9monthsfromtheinitialvalidation.TheinitialvalidationandrevalidationofthesuggestednetretailpriceofallnewlyintroducedalcoholandtobaccoproductsshallbeconductedexclusivelybytheauthorizedrepresentativesoftheBIR.

• Everylocalmanufacturerorimporterofalcoholandtobaccoproductsshallsubmitadulynotarizedmanufacturer’sorimporter’sswornstatementforalcoholortobaccoproductsshowing,amongothers,thefollowinginformation:

1. Name,address,TINandassessmentnumberofthemanufacturerorimporter;

2. Completerootnameofthebrandaswellasthecompletebrandnamewithmodifiers,ifany;

10 Tax Bulletin

3. Completespecificationsofthebranddetailingthespecificmeasurements,weights,mannerofpackagingandsoon;

4. Name(s)oftheregion(s)wherethebrand/sis/aretobemarketed;

5. Wholesalepricepercase,grossandnetofVATandexcisetax;

6. Suggestedretailprice,grossandnetofVATandexcisetax,perpackorperbottle,asthecasemaybe;

7. Detailedproduction/importationcostsandallotherexpensesincurredortobeincurreduntiltheproductisfinallysold(e.g.,materials,labor,overhead,sellingandadministrativeexpenses)percase;

8. Applicablerateofexcisetaxperunitofmeasureorvalue,asthecasemaybe;

9. CorrespondingexciseandVATpercase.

• Themanufacturer’sorimporter’sswornstatementshallbesubmittedasasupportingdocumenttotheprescribedapplicationfortheinitialregistrationofanalcoholortobaccoproduct.Thereafter,anupdatedswornstatementissubmittedonorbeforetheendofJuneandDecemberoftheyear.

• Wheneverthereisachangeinthecosttomanufacture,produceandsellthebrand,orchangeintheactualsellingpriceofthebrand,theupdatedswornstatementshallbesubmittedatleast5daysbeforetheactualremovaloftheproductfromtheplaceofproductionorreleasefromthecustomscustody,asthecasemaybe.

• Ifthemanufacturerorimportersellsorallowssuchgoodstobesoldat

wholesaleinanotherestablishmentofwhichheistheowner,orwheneverhehasaninterestintheprofitsofsuchestablishment,thesellingpriceinsuchestablishmentshallconstitutethewholesaleprice.Shouldsuchpricebelessthanthesaidcostsandexpenses,aproportionatemarginofprofitofnotlessthan10%shallbeaddedtoconstitutethewholesaleprice.

• Withrespecttoimportedalcoholortobaccoproducts,thecostofimportationshallinnocasebelessthanthevalueindicatedinthereferencebooksoranyotherreferencematerialsusedbytheBureauofCustoms(BOC)indeterminingthepropervaluationoftheimportedproducts,orthedutiablevalueasdefinedundertheTariffandCustomsCodeofthePhilippines,whicheverishigher.

• Incasethenewlyintroducedalcoholortobaccoproductshallbesubsequentlymarketedinanotherregion/otherregionsbeforethepropertaxclassificationisfinallydeterminedbytheBIR,anupdatedswornstatementshallbesubmittedtotheappropriateBIROfficebeforethesameshallberemovedfromtheplaceofproduction.

• TheswornstatementprescribedintheseRegulationsshallbesubjecttoverificationbytheBIRtovalidateitscontentswithrespecttoitsaccuracyandcompleteness.Intheeventthecontentsoftheswornstatementarefoundtobeinaccurateand/orincomplete,thetaxpayershallberequiredtosubmitarevisedswornstatement,withoutprejudicetotheimpositionofcorrespondingsanctionsandpenalties.

11

►• Theunderstatementofthesuggestednetretailpricebyasmuchas15%oftheactualnetretailpriceshallrenderthemanufacturerorimporterliableforadditionalexcisetaxequivalenttothetaxdueanddifferencebetweentheunderstatedsuggestednetretailpriceandtheactualnetretailprice.

►• Theimportationofalcoholortobaccoproducts,evenifdestinedfortaxandduty-freeshops,DutyFreePhilippines,orintocharteredorlegislatedeconomicand/orfreeportzonesshallbesubjecttoexcisetaxpursuanttotheprovisionsoftheAct,notwithstandingtheprovisionofanyspecialorgenerallawtothecontrary.

• UpontheeffectivityoftheAct,theimportationofanyalcoholortobaccoproductbearingsuffixesorprefixestotherootname,colorand/ordesignofthelabel(suchaslogo,font,picturegram,andthelike),mannerand/orformofpackagingorsizeofcontaineroftheproductthatisdifferentfromthatalreadyregisteredandlocallybeingsoldinthedomesticmarketshallbetreatedasanewlyintroducedproduct.Accordingly,thesameshallbeinitiallyclassifiedaccordingtoitssuggestednetretailprice,subjecttothevalidationandrevalidationrequirementsprescribedbytheseRegulations.

• NotobaccoproductsmanufacturedinthePhilippinesandproducedforexportshallberemovedfromtheirplaceofmanufactureorexported,withoutpostinganexportbondequivalenttotheamountoftheexcisetaxdueonsaidproductsifsolddomestically.

• However,tobaccoproductsforexportmaybetransferredfromtheplaceofmanufacturetoabondedfacilityuponpostingofatransferbondpriortoexport.

►• TobaccoproductsimportedintothePhilippinesanddestinedforforeigncountriesshallnotbeallowedentrywithoutpostingabondequivalenttotheamountofcustomsduty,excisetaxandVATdueonsaidproductsifsolddomestically.

• Allcigaretteswhetherpackedbyhandorpackedbymachineshallonlybepackedin20s,andthroughotherpackagingcombinationswhichshallresulttonotmorethan20sticksofcigarettes.

• Incaseofcigarettespackedinnotmorethan20sticks,whetherin5sticks,10sticksandotherpackagingcombinationsbelow20sticks,thenetretailpriceofeachindividualpackageof5s,10s,etc.shallbethebasisofimposingthetaxrateprescribedundertheAct.

• UpontheeffectivityoftheAct,thefollowingtransitoryprovisionsshallbestrictlyobserved:

1. AllalcoholandtobaccoproductsexistinginthemarketatthetimeoftheeffectivityoftheActshallbeinitiallyclassifiedaccordingtothetaxratesprescribedbytheAct,basedonthe2010pricesurveyoftheseproductsconductedbytheBIR,subjecttotheprohibitionagainstdownwardreclassificationonfermentedliquors.*

* [Editor’s Note: See page 15 below for RMC No. 90-2012, dated December 27, 2012.]

12 Tax Bulletin

2. Incaseofalcoholandortobaccoproductsthatwereintroducedafterthe2010pricesurveybutbeforetheeffectivityoftheAct,theirrespectivetaxclassificationorrateshallbebasedonthesuggestednetretailpricedeclaredinthelatestswornstatementfiledbythelocalmanufacturerorimporter,asthecasemaybe.

3. Forpurposesofdeterminingtheactualvolumeoflocallymanufacturedalcoholandtobaccoproductsthatshallbeimposedwiththenewtaxratesupontheremovalofsaidproductsfromtheplaceofproduction,anactualstocktakingshallbeconductedbytheBIRonallstocksoflocallymanufacturedalcoholandtobaccoproductsheldinpossessionbythemanufacturerasoftheeffectivityoftheAct.

4. ThespecifictaxthatwaspaidonthephysicalinventoryofethylalcoholheldinpossessionbymanufacturersofcompoundedliquorsasoftheeffectivityoftheActandsubsequentlyusedasrawmaterialsintheproductionofcompoundedliquorsshallnotbeentitledtotaxcredit/refundorshallnotbedeductedfromthetotalexcisetaxdueoncompoundedliquors.

• ViolationsoftheseRegulationsshallbesubjecttothecorrespondingpenaltiesunderTitleXoftheTaxCode.ThefollowingarethepenaltyprovisionsprescribedpursuanttotheprovisionsoftheAct:

1. Anymanufacturerorimporterwhomisdeclaresormisrepresentsinhisoritsswornstatementanypertinentdataorinformationshall,upondiscovery,bepenalizedbyasummarycancellationorwithdrawalofhisoritspermittoengageinbusinessasamanufacturerorimporterofalcoholortobaccoproducts.

2. Anycorporation,associationorpartnershipliableforanyoftheactsoromissionsinviolationoftheActandimplementedbytheseRegulationsshallbefinedtrebletheaggregateamountofdeficiencytaxes,surchargesandinterestwhichmaybeassessedpursuanttotheprovisionsoftheAct.

3. AnypersonliableforanyoftheactsoromissionprohibitedundertheActandimplementedbytheseRegulationsshallbecriminallyliableandpenalizedunderSection254oftheTaxCode.

4. IftheoffenderisnotacitizenofthePhilippines,heshallbedeportedimmediatelyafterservingthesentencewithoutfurtherproceedingsfordeportation.

• ►TheseRegulationsshalltakeeffectuponpublicationinaleadingnewspaperofgeneralcirculation.

(Editor’s Note: RR No. 17-2012 was published in the PhilippineStar on December 28, 2012.)

Revenue Regulations No. 1-2013 dated January 23, 2013

Definition of Terms:

►►• Electronic Tax Remittance Advice (eTRA) Systemreferstotheprocessofremittingtaxeswithheldbynationalgovernmentagencies(NGAs)throughthe

RRNo.1-2013expandsthecoverageoftaxpayersrequiredtofiletaxreturnsandpaytaxesthroughtheeFPS,toincludeNGAsmandatorilyrequiredtousetheeTRA.

13

internetusingtheeFPSfacilityoftheBIR,inlieuofthemanualfilingofTaxRemittanceAdvice.

►• Electronic Filing and Payment System (eFPS)referstothesystemdevelopedandmaintainedbytheBIRforelectronicallyfilingtaxreturns,includingattachments,ifany,andpayingtaxesduethereon,specificallythroughtheinternet.

►►• e-filingreferstotheprocessofelectronicallyfilingtaxreturns,includingattachments,ifany,specificallythroughtheinternet.

►• e-paymentreferstotheprocessofelectronicallypayingataxliabilitythroughtheinternetbankingfacilitiesofAABs.

►• Authorized Agent Bank (AAB)referstoanybankcertifiedbytheBangkoSentralngPilipinas(BSP)whichhassatisfiedthecriteriaonaccreditationandisactuallyaccreditedtocollectinternalrevenuetaxes.

►• Tax Remittance Advice (TRA)referstoaserially-numbereddocumentprescribedbytheDepartmentofBudgetandManagement(DBM)thatshouldbeusedbyNGAsintheremittanceofwithheldtaxesonfundscomingfromDBM.ThisformisdistributedbytheBIRtobeaccomplishedbytheNGAs.ThesameshallbedulycertifiedbytheChiefAccountantandapprovedbytheHeadoftheconcernedNGAorhisdulyauthorizedrepresentative,andattachedtoeverywithholdingtaxreturnfiledaspaymentfortaxeswithheld.ThisshallbethebasisfortheBIRandtheBureauofTreasury(BTr)torecordthetaxcollectionintheirrespectivebooksofaccounts.

►• Electronic Tax Remittance Advice (eTRA)referstoaTRAwhichisaccomplishedonlineviatheBIR’seFPSfacility.

►• National Government Agencies (NGAs)referstogovernmentagencieswhosemainfund/budgetcomesfromtheDBMbasedontheyearlybudgetallotmentasprovidedundertheGeneralAppropriationsAct.

►• ReturnreferstothetaxreturnsrequiredtobefiledbyNGAswhichinclude,butarenotlimitedto,thefollowing:

Tax Return Description Due Date for Filing

BIRForm1601-C

MonthlyRemittanceReturnofIncomeTaxesWithheldonCompensation

Onorbeforethe10thdayfollowingthemonthinwhichwithholdingwasmade,exceptfortaxeswithheldforthemonthofDecemberofeachyear,whichshallbefiledonorbeforeJanuary15ofthesucceedingyear.

BIRForm1601-E

MonthlyRemittanceReturnofCreditableIncomeTaxesWithheld(Expanded)[Exceptfortransactionsinvolvingoneroustransferofrealpropertyclassifiedasordinaryasset]

Onorbeforethe10thdayfollowingthemonthinwhichwithholdingwasmade,exceptfortaxeswithheldforthemonthofDecemberofeachyear,whichshallbefiledonorbeforeJanuary15ofthesucceedingyear.

14 Tax Bulletin

BIRForm1601-F

MonthlyRemittanceReturnofFinalIncomeTaxesWithheld

Onorbeforethe10thdayfollowingthemonthinwhichwithholdingwasmade,exceptfortaxeswithheldforthemonthofDecemberofeachyear,whichshallbefiledonorbeforeJanuary15ofthesucceedingyear.

Tax Return Description Due Date for Filing

BIRForm1603

QuarterlyRemittanceReturnofFinalIncomeTaxesWithheldonFringeBenefitsPaidtoEmployeesOtherthanRankandFile

Onorbeforethe10thdayofthemonthfollowingthequarterinwhichthewithholdingwasmade.

BIRForm1600

MonthlyRemittanceReturnofValue-AddedTaxandOtherPercentageTaxesWithheld

Onorbeforethe10thdayofthemonthfollowingthemonthinwhichwithholdingwasmade.

BIRForm1702

AnnualIncomeTaxReturnforCorporations,PartnershipsandOtherNon-IndividualTaxpayers

Onorbeforethe15thdayofthefourthmonthfollowingthecloseofthetaxableyear(calendarorfiscal)

BIRForm1702Q

AnnualIncomeTaxReturnforCorporations,PartnershipsandOtherNon-IndividualTaxpayers

Withinsixty(60)calendardaysfollowingthecloseofeachofthefirstthree(3)quartersofthetaxableyear(calendarorfiscalyear)

BIRForm2550M

MonthlyValue-AddedTaxDeclaration

Onorbeforethe20thdayafterthecloseofthemonth

BIRForm2550Q

QuarterlyValue-AddedTaxReturn

Onorbeforethe25thdayafterthecloseofthetaxablequarter

BIRForm2551M

MonthlyPercentageTaxReturn

Onorbeforethe20thdayafterthecloseofthemonth

BIRForm2000

DocumentaryStampTaxReturn

Onorbeforethe5thdayafterthecloseofthemonthwhenthetransactionsubjecttoDSToccur.

►• TheBIRshallissueanotificationlettertoallNGAs,includingtheirbranchesandextensionofficeslocatednationwidewhichhavetheirowndisbursementfunctions,toinformthemthattheyaremandatedtousetheeFPSinfilingtherequiredreturnsandinpayingthetaxesduethereon.

►• ItshallbetheresponsibilityoftheHeadOfficeoftheconcernedNGAtoprovidetheBIRwiththelistofallitsbranches/fieldorextensionofficeslocatednationwidewhichhavetheirowndisbursementfunctions,withinformationastotheirrespectivebusinessaddresses,agencycodesandTINs.

►• AllNGAsnotifiedthruthenotificationlettershallenrollintheeTRAsystembyenrollingfirstwiththeBIR’seFPSfacility.

►• Aspartoftheenrollmentprocedures,NGAsshallberequiredtosubmit

totheRevenueDistrictOfficewheretheyareregisteredthenamesoftwoauthorizedofficersdesignatedtofiletherequiredtaxreturnspursuanttoSection52(A)oftheTaxCode.Likewise,NGAsshallenrollwithanyAABwheretheyintendtopaythroughthebankdebitsystem,incasesofremittanceofwithheldtaxesonfundsnotcomingfromtheDBMorthepaymentofinternalrevenuetaxesthrucashandnotthroughTRA.

15

►• NGAsmandatedtofileelectronicallythrutheissuanceofthenotificationlettershallfiletheirtaxreturnsviatheeFPS,whetherornottheymakeuseoftheeTRAinthepayment.

►• Staggeredfilingofreturnsallowedforwithholdingagents/taxpayersenrolledintheeFPSshallnotapplyinthecaseofNGAs.Alltaxreturnsmustbeelectronicallyfiled(e-filed)followingtheprescribedduedates.Paymentofthetaxduemustalsobemadeonthesamedaythereturnise-filedbyaccomplishingon-linetheTRA.

►• TheuseofeTRAaspaymentislimitedonlytotheNGAs’taxliabilitiesarisingfromtheuseoffundscomingfromtheDBM.Aseparatetaxreturnmustbeaccomplishedforthesetaxliabilitiessinceaparticularfundisrequiredtohaveaseparatebranchcode.

►• Theseregulationsshalltakeeffectafter15daysfollowingthepublicationintheOfficialGazetteorinanewspaperofgeneralcirculation.

(Editor’s Note: RR No. 1-2013 was published in ManilaBulletin on January 25, 2013.)

Revenue Memorandum Circular No. 84-2012 dated December 21, 2012

• InterestincomereceivedbybanksfrompayorsbelongingtotheTop20,000Corporationsandstrictlyarisingfromindividualloansobtainedfrombanksthatarenotsecuritized,assignedorparticipatedoutremainssubjectto2%creditablewithholdingtax(CWT).

• InterestincomepaidbybanksdesignatedasTop20,000Corporationsand

strictlyarisingfromloansmadetosuchbanksthatarenotsecuritizedorparticipatedoutremainssubjectto2%CWT.

• The20%finalWTandCWTimposedundertheTaxCodeandexistingregulationscoverinterestarisingfromorpaidoutofdebtsecurities.

Revenue Memorandum Circular No. 90-2012 dated December 27, 2012

►• TheinitialclassificationsofallalcoholandtobaccoproductsexistinginthemarketatthetimeofeffectivityofRANo.10351asprovidedinthisCirculararebasedonthe2010pricesurveyofthealcoholandtobaccoproductsconductedbytheBIR.

►• Incaseofalcoholand/ortobaccoproductsthatwereintroducedafterthe2010pricesurveybutbeforetheeffectivityofRANo.10351,theirtaxclassificationorrateisbasedonthesuggestednetretailpricedeclaredinthelatestswornstatementfiledbylocalmanufacturerorimporter,asthecasemaybe.

• TheinitialclassificationsandtaxratesofalcoholandtobaccoproductsarelistedintheannexesattachedtoRMC90-2012,asfollows:

AnnexA-1 LocallyManufacturedFermentedLiquors

AnnexA-2 ImportedFermentedLiquors

AnnexB-1 LocallyManufacturedDistilledSpirits

RMCNo.84-2012clarifiesthepropertaxtreatmentofinterestincomeearn-ingsonloansthatarenotsecuritized,assignedorparticipatedout.

RMCNo.90-2012prescribestheinitialclassificationsandtaxratesforalcoholandtobaccoproductsexistinginthemarketpursuanttoRANo.10351.

16 Tax Bulletin

AnnexC ImportedSparklingWines

AnnexD-1 LocallyManufacturedCigaretteBrands

AnnexD-2 ImportedCigaretteBrands

Revenue Memorandum Circular No. 91-2012 dated December 28, 2012

►• Underasplitpaymentarrangement,theadvertisermayengageorcontractdirectlywithamediaentity/supplierandanadvertisingagencyformediaadvertisingplacements.Theincomepaymentsdirectlymadebytheadvertisertothemediasupplierandtotheadvertisingagencyarelimitedtothecostoftheserviceprovidedbyeachentity(i.e.,billingofthemediasupplierforthetotalcostofproductionandmediaplacementandbillingofadvertisingagencyforcommission/servicefee).

►• Thefollowingaretheaccountingentries:

AssumethatthetotalcostoftheadvertiserforthetotalmediaadvertisementisP100,000comprisedofP85,000mediaentity/supplierbillingandP15,000advertisingagencycommission/servicefee,inclusiveofVAT:

AccountingEntriesintheBooksofAccountsoftheAdvertiser:

Debit Credit

►►• Receiptofbillingfrommediaentity/supplier:

AdvertisingExpense P85,000

DeferredInputVAT 10,200

AccountsPayable–MediaEntity/Supplier P95,200

►►• PaymenttoMediaEntity/Supplier:

AccountsPayable–MediaEntity/Supplier P95,200

CreditableITWithheld P1,700

Cash 93,500

►• ►ReceiptofBillingfromAdvertisingAgency:

ServiceExpense P15,000

DeferredInputVAT 1,800

AccountsPayable–AdvertisingAgency P16,800

►►• PaymentofAdvertisingAgency:

AccountsPayable–AdvertisingAgency P16,800

CreditableITWithheld P300

Cash 16,500

AccountingEntriesintheBooksofAccountsoftheMediaEntity/Supplier:

Debit Credit

►• ►BillingtoClient/AdvertiserfortheMediaPlacement:

AccountsReceivable–Advertiser P95,200

Income/Fees–MediaPlacement P85,000

DeferredVATPayable 10,200

RMCNo.91-2012supplementsRMCNo.63-2012datedOctober29,2012oninvoicingandrecordingofincomepaymentsformediaadvertisingplace-mentsunderasplitpaymentschemeorarrangement.

17

• PaymenttoMediaEntity/Supplier:

AccountsPayable–MediaEntity/Supplier P95,200

CreditableITWithheld P1,700

Cash 93,500

Debit Credit

►►• ReceiptofIncomePaymentfromAdvertiser:

Cash P93,500

CreditableWithholdingTax 1,700

AccountsReceivable–Advertiser P95,200

AccountingEntriesintheBooksofAccountsoftheAdvertisingAgency:

Debit Credit

►►• BillingtoClient/AdvertiserfortheCommission/ServiceFee:

AccountsReceivable–Advertiser P16,800

CommissionIncome/ServiceFees P15,000

DeferredVATPayable 1,800

►►• ReceiptofIncomePaymentfromAdvertiser:

Cash P16,500

CreditableITWithheld 300

AccountsReceivable–Advertiser P16,800

Revenue Memorandum Circular No. 2-2013 dated December 28, 2012

►• RRNo.12-2012appliesprospectivelytolandvehiclespurchasedupontheeffectivityofRRNo.12-2012wherethepurchasepriceexceededtheamountofP2,400,000.00.

►• RRNo.12-2012waspublishedlastOctober17,2012and,basedonitsprovisions,itshalltakeeffectimmediately.Hence,theRRtookeffectonOctober17,2012.

►• Incasethevehicles(definedintheRRaspassengervehiclesofalltype,whetherbyland,water,orair)whicharenotalloweddepreciationexpense,orthenon-depreciablevehicleswillbesoldataloss,thelosstobeincurredfromsuchsaleshallnotbedeductiblefromgrossincome.

►• Forincometaxpurposes,allexpensesrelatedtothenon-depreciablevehiclessuchasbutnotlimitedtorepairsandmaintenance,oilandlubricants,gasoline,spareparts,tiresandaccessories,premiumpaidforinsurancecoveringsaidvehiclesandregistrationfeesshallnotbeallowedasadeductionintheirentirety.ForVATpurposes,allinputtaxescorrespondingtothedisallowedexpensesforincometaxpurposesarelikewisenotallowed.

Revenue Memorandum Circular No. 4-2013 dated January 11, 2013

►• Allhospitalsandnon-stock,non-profitorganizationsoperatinghospitalswhichwereissuedtax-exemptrulingsbytheBIRshallsubmitarequest

RMCNo.2-2013clarifiescertainprovisionsofRRNo.12-2012onthedeductibilityofdepreciationexpenseasitrelatestothepurchaseofvehicles,andotherrelatedexpenses,andtheinputtaxesallowed.

RMCNo.4-2013requirestax-exempthospitalstosecurerevalidatedtaxexemptionrulings/certificates.

18 Tax Bulletin

forrevalidationoftheirtax-exemptstatusbysubmittingthefollowingdocumentstotheRevenueDistrictOfficewheretheorganizationisregistered:

1. LetterapplicationwhichmuststatethespecificparagraphofSection30oftheTaxCodeunderwhichitseeksexemption;

2. Copiesofthecorporation’slatestArticlesofIncorporationandBy-LawsdulycertifiedbytheSEC;

3. BIRCertificateofRegistration;4. TaxClearanceissuedbytheRevenueDistrictOfficewherethecorporation

isregistered;5. CopiesofIncomeTaxReturnsorAnnualInformationReturnsand

FinancialStatementsforthelastthreeyears;and6. Astatementofitsmodusoperandistatingthereinitssourcesofrevenues.

►• Inthecourseofreviewoftheapplicationfortaxexemption,theBIRmayrequirethesubmissionofotherdocumentsasthecircumstancesmaywarrant.

• Procedures

1. Uponreceiptoftheapplicationtogetherwiththesupportingdocuments,theRevenueDistrictOfficeshallevaluatethesameandshalldeterminewhetheritqualifiesasanexemptcorporationunderSection30oftheTaxCode.

2. Iftheapplicationisfoundtobeinsufficient,thecorporationshallbenotifiedofsuchfindingsandtheapplicationwiththesupportingdocumentsshouldbereturned.

3. Iftheapplicationisfoundtobevalid,areportshallbepreparedbytheRevenueDistrictOfficestatingthereinwhy,initsopinion,theorganizationisqualifiedtobetaxexemptunderSection30.

4. ThedocketofthecaseshallbeforwardedtotheOfficeoftheRegionalDirectorforreview.IftheRegionalDirectoragreeswiththerecommendationoftheRevenueDistrictOffice,thesameshallbeforwardedtotheOfficeoftheAssistantCommissioner,LegalService.TheLawDivisionshallreviewandevaluatethedocumentssubmitted,andifinorder,preparetheappropriateCertificateofTaxExemptionforsignatureoftheCommissionerorherdulyauthorizedrepresentative.

►• AllrulingsissuedpriortoNovember1,2012whichgranttaxexemptiontoproprietarynon-profithospitalsortonon-stock,non-profitentitiesoperatinghospitalsunderSection30oftheTaxCodeshallnolongerbevalid.

Revenue Memorandum Circular No. 6-2013 dated December 19, 2012

►►• ThefollowingaredeemedtobeengagedintaxpracticeandarerequiredtoapplyforaccreditationpursuanttoSection2(e)ofRRNo.11-2006,asamended:

1. Taxagents/practitionerswhoareengagedintheregularpreparation,certification,auditandfilingoftaxreturns,informationreturnsorotherstatementsorreportsrequiredbytheTaxCodeorRegulations;

RMCNo.6-2013clarifiestaxpayers’concernsontheauditprogram,andtheirresponsibilityforengagingtaxagents/practitioners.

19

2. Thosewhoareengagedintheregularpreparationofrequestsforruling,petitionsforreinvestigation,protests,requestsforrefundortaxcreditcertificates,compromisesettlementand/orabatementoftaxliabilitiesandotherofficialpapersandcorrespondencewiththeBIR,andothersimilarorrelatedactivities;

3. Thosewhoregularlyappearinmeetings,conferences,andhearingsbeforeanyofficeoftheBIRofficiallyonbehalfofataxpayerorclientinallmattersrelatingtoaclient’srights,privileges,orliabilitiesunderlawsorregulationsadministeredbytheBIR.

►►• InaccordancewithRRNo.11-2006,theBIRcanrefusetotransactofficialbusinesswithtaxagents/practitionerswhoarenotaccreditedbytheBIR.

►• Alltaxpayersareenjoinedtoensurethatthetaxagents/practitionerswhomtheywillengageareaccreditedwiththeBIR.Taxpayersshouldbeawareoftheirfollowingresponsibilities:

1. Beforeengagingthetaxserviceofataxagent/practitioner,theyshouldsecureacopyofhis/itsBIRcertificateofaccreditationandtakenoteofthefollowing:

►• TIN►• Accreditationnumber►• Dateofissuance►• Dateofexpiry

2. ConstantlyvisittheBIRwebsiteforthepublicationoftheupdatedmasterlistofaccreditedtaxagents/practitioner.

BOC Issuances

Customs Memorandum Order No. 16-2012 dated November 27, 2012

►• Dutydrawbacktaxcreditcertificates(TCCs)jointlyissuedbytheOne-StopShop(OSS)Inter-AgencyTaxCreditandDutyDrawbackCenter,DepartmentofFinance(DOF)andtheBOCpursuanttoSection106oftheTariffandCustomsCodeofthePhilippines(TCCP)donotprovideadefinitevalidityperiod.

►• TCCsissuedpursuanttoExecutiveOrder(EO)No.226arevalidforten(10)years,whileTCCsissuedundertheTaxCodearevalidfor5yearsfromdateofissue,subjecttorevalidationforanother5years.

►• ToalignandharmonizethevalidityperiodofTCCs,dutydrawbackTCCsissuedpursuanttotheTCCPshallbevalidforten(10)yearsfromdateofissue,pursuanttoResolutionNo.308-48-2011datedFebruary14,2011oftheOSS-CenterExecutiveCommittee.

Customs Administrative Order No. 1-2013 dated January 22, 2013

►• CAONo.1-2013coverstheaccreditationofqualifiedimportersasSuperGreenLane(SGL)Plususers,andtheprocessingofshipmentsofSGLPlususersatthePortofManila(POM),ManilaInternationalContainerPort(MICP),NAIACustomsHouse,andotherportsasmaybedeemednecessary.

CMONo.16-2012prescribesa10-yearvalidityperiodfordutydrawbackTCC.

CAONo.1-2013prescribestherulesandregulationsimplementingtheSGLPlusFacility.

20 Tax Bulletin

►• InadditiontothebenefitsenjoyedbyregularSGLmembers,anaccreditedSGLPlususershallbeentitledtothefollowingbenefits:

1. Three(3)yearsuspensionontheconductofaudit2. Five(5)yearvalidityperiodoftheimporter’saccreditation3. ImportationofarticlesnotincludedintheListofImportables,providedthat

amendmentstothesaidlistaresubmittedatleastten(10)daysbeforearrivaloftheimportation

4. 24-hourClientCoordinatorServiceforqueries5. OtherbenefitsgrantedbytheSGLPlusTaskGroupendorsedbythe

CommissionerandapprovedbytheSecretaryofFinance

►• TheSGLPlusTaskGroupshallbecomposedofthefollowing:

1. DeputyCommissionerforIntelligenceGroup–Chairman2. Chief,RiskManagementOffice(RMO)3. AssistantChief,RMO4. Director,ImportAssessmentSystem(IAS)5. Chief,PlanningandPolicyResearchDivision(PPRD)6. ChiefofStaff,AssessmentOperationsCoordinatingGroup(AOCG)7. ExecutiveAssistant,OfficeoftheCommissioner8. AssistantOIC,ProductionSection,CustomsIntelligenceandInvestigation

Service(CIIS)

►• TheSGLPlusSecretariatshallbeappointedbytheSGLPlusTaskGroupCommander.

►• TheSGLPlusAccreditationSub-groupshallbecomposedoftheCIISDirector,theHeadoftheSGLPlusSecretariat,theHeadsoftheInternalControlSystems(ICS)inthethreemajorpointsofentry,arepresentativefromthePost-EntryAuditGroup–TradeInformationandRiskandAnalysisOffice(PEAG-TIRAO),aCIISrepresentative,andothersassignedbytheTaskGrouptoserveasmembers.

►• TheSGLPlusImportComplianceSub-groupshallbecomposedoftheICSDirectororhisduly-designatedrepresentative,theheadsofICSGsinthePOM,MICPandNAIACustomsHouse,theChiefofValuationandClassificationDivision,andothersdesignatedbytheTaskGroupChairman.

►• TheSGLPlusClientCoordinatingCenter(SPCCC)shallbeorganizedbytheSGLPlusTaskGroupChairman.

►• ThefollowingarethequalificationsforaccreditationundertheSGLPlusfacility:

1. TheimporterisaccreditedasanSGLmembertransactingwiththeBOCforatleastoneyearpriortotheapplication.

2. Theapplicanthasaclearandspecificnatureofbusiness.3. TheSGLPlusAssociationhasbeenconsultedonthemembershipofthe

applicant.4. Theimportermusthaveagoodreputationbasedonitstrackrecord.5. Theimportermustnothavemisusedcustomsfacilitiesforatleastone

yearpriortoitsapplication,orhasnotbeenthesubjectofderogatoryinformation.

6. Theimporteriswillingtoundergoacomplianceaudit.

21

• Thefollowingaretheconditionsoftheaccreditation:

1. TheimporterisaregisteredSGLuser.2. Theshipmentsmaybesubjecttorandomorspot-checkinspectionatthe

importer’spremiseswhilethegoodsarebeingunloaded.3. Theimportershallberesponsibleforanymisuseorabuseoftheprivilege.4. Theimportershallcomplywiththerulesandregulationsimplementingthe

SGLPlusprogram.5. AnywillfulviolationoftheCertificateofAccreditation(CA)shallbea

groundforitssuspension,revocationorcancellation.6. TheuseoftheCAshallbesubjecttoreviewandshallbevaliduntil

suspended,revoked,orcancelled.

• Accreditationmaybeviathefollowingmodes:

1. By Invitation.TheSGLPlusAssociationshallselectandinvitetopSGLuserstobecomeSGLPlususersbasedondutiesandtaxespaidforthepreviousyear.

2. By Application.AnySGLuserwhomeetstherequirementsofCAONo.1-2013mayapplyforSGLPlusaccreditationbysubmittingtheSGLPlusapplicationformtogetherwiththerequiredsupportingdocumentstotheSGLPlusSecretariat.

• Suspension, Cancellation, or Revocation of Accreditation

ACAshallremainvalidunlesssuspended,cancelled,orrevokedbytheCommissioneruponrecommendationoftheSGLPlusTaskGroup,afterduenoticeandhearing,onanyofthefollowinggrounds:

1. Failureorrefusal,withoutjustifiablecause,tosubmitwithintheprescribedperiodhardcopiesofimportentriesorsupportingdocuments.

2. FraudulentorwillfulmisrepresentationofSGLPlusapplicationorimportation.

3. Submissionoffakedocumentsintheaccreditationorimportationprocess.4. Failureorrefusal,withoutjustifiablecause,topayadditionaldutiesand

taxeslawfullydemandedafterpostentry(release)verificationbytheSGLPlusICSwithintheprescribedperiod.

5. Violationofthetermsofaccreditation,e.g.failuretopromptlyupdateorinformtheSGLPlusTaskGroupofanychangesinthecommoditiesbeingimported,aswellasintheirdescription,unitvalues,etc.

6. Failureorrefusal,withoutjustifiablecause,tocomplywithlawfulordersordirectivesissuedbytheSGLPlusTaskGrouporanyofitssub-groups,orbyhigherauthorities.

• Conditions on Shipment

1. OnlySGLPlus-accreditedimportersshallbeallowedtoclearshipmentsthroughtheSGLPlusfacility.

2. SGLPlusentriesshallbefiledunderexistingproceduresforSGLshipments.

3. SGLPlusentriesshallbesubjecttoPost-ReleaseVerificationandPost-ReleaseInspection,providedthatanSGLPlusshipmentshallnotbeexaminedexceptwhenitisthesubjectofaderogatoryintelligenceinformationorwhendirectedbytheSGLPlusTaskGroupHead.

22 Tax Bulletin

4. ShipmentsshallqualifyforSGLPlustreatmentonlywhen:

• TheyareinthelistofimportablesintheSGLPlususer’saccreditationorintheamendedlistofimportablessubmittedatleast10daysbeforearrivaloftheimportation.

• Theyarefreelyimportablecommoditiesorifregulated,coveredbycontinuingImportAuthorityissuedbytheappropriategovernmentagency.

• Theyaredeclaredunderconsumptionentries,thussubjecttodutiesandtaxes.

• Theydonotcontainprohibitedarticlesunderexistinglaws,rules,andregulations.

• TheaccreditedSGLPlusimportershallpayaservicefeeforeveryentryfiledthroughtheSGLPlusfacilitybasedontheFOBvalueofthesubjectimportsinaccordancewiththefollowingschedule:

FOB Value Amount

BelowUS$5,000 P500.00

US$5,001toUS$100,000 P1,000.00

US$100,001toUS$200,000 P1,500.00

US$200,001toUS$500,000 P2,000.00

AboveUS$500,000 P2,500.00• CAONo.1-2013shalltakeeffectimmediately.

SEC Issuances

SEC Memorandum Circular No. 11 dated December 20, 2012

InlinewiththethrustoftheCommissiontocontinuouslypromoteahigherlevelofcorporategovernancethroughqualitytrainingongoodcorporategovernanceprinciplesandstandardsforthedirectorsofcoveredcompanies,theCommissionEn Bancadoptedthefollowingguidelines:

Accreditation

• TheCommission,throughtheCorporateGovernanceDivisionoftheCorporationFinanceDepartment,shallaccreditallprivateorgovernmentinstitutionaltrainingproviders(ITPs).

• AnITPmaybeaccreditedprovideditfollowstheproceduralrequirementsoftheseGuidelinesandthefollowingminimumstandardsoftheCommission:

1. Thatitisformallyorganizedtoconducttrainingactivitiesandthatithasanadequatetrackrecordofsuccessfullyconductingcorporatetrainingprogramsincludingpreferablytrainingincorporategovernance;

2. Thatithasasoundbusinessplanincludingreasonabletrainingfeesforconductingcorporategovernancetrainingandadequatefinancialandorganizationalresourcestoexecutethesame;

3. Thatitcanguaranteeaqualifiedline-upoftrainerswhocaneffectivelydeliver,asaminimum,therequiredtraininginaccordancewiththeCodewithspecialemphasisonthefollowingmandatedtopics:

SECMCNo.11prescribestheguidelinesforaccreditationofinstitutionaltrainingprovidersoncorporategovernance.

23

• Illegalactivitiesofcorporations/directors/officers►• Insidertrading• Protectionofminoritystockholders• Shortswingtransactions• Liabilitiesofdirectors• Confidentiality• Conflictofinterest• Relatedpartytransactions• Casestudies

4. Thatthetrainersline-uppercourseofferingshouldatleasthaveoneexperiencedcorporatedirector/CEO;

5. ThatitcanprovideforreviewitsintendedcoursematerialsandconductadryrunfortheCommission.

• TheauthorizedofficeroftheapplicantITPmustsubmittotheCommissionthefollowing:

1. WrittenapplicationforaccreditationasanITP;2. CertificationthatitmeetstherequirementsoftheCommissionasset

forthinparagraph2above;3. Supportingdocuments,i.e.,summaryofbusinessexperienceandplan,

credentialsofresourcepersons,courseprogramandtrainingmaterials;and

4. ProcessingfeeamountingtoP5,000.00shallbepaidtotheCommissionbytheapplicant.

• TheCommission,uponrecommendationoftheCorporateGovernanceDivision,shallapprovetheapplicationforaccreditationoftheITP,subjecttothecriteriaandrequirementsenumeratedherein.

• TheaccreditationofanITPshallexpireorbeautomaticallydelistedafter3yearsfromthedateofapprovaloftheaccreditation,unlessanapplicationforitsrenewalisfilednotlaterthan30businessdaysbeforeitsexpiration.TheapplicationfortherenewaloftheaccreditationoftheITPshallbeaccompaniedbyanapplicationfeeofP5,000.00.

Training Program

• AnaccreditedITPshallsubmittotheCommissiondetailsofanyproposedtrainingprogramoncorporategovernanceforclearance.Itshallincludetheproposedline-upoftrainersmeetingtheminimumrequirementsofthisCircular.

• TheCommissionmayobservetheconductofanytrainingprogramandundertakeanindependentevaluationofanyaspectofthetrainingprogram.

• ThetrainingprovidersshallsubmittotheCommissionaCompletionReportofTrainingnotlaterthan15daysafterthetraining.

• TheCommissionreservestherighttowithdrawitsaccreditationfromanyITPwhichisnotcomplyingwithitstrainingguidelines.

• AllexistingaccreditedITPsaredirectedtosubmitanapplicationfortherenewaloftheiraccreditationwithin30businessdaysfrompostingofthis

24 Tax Bulletin

MemorandumCircular.Otherwise,theiraccreditationshallbedeemedexpired.TheapplicationforrenewalofaccreditationshallbeevaluatedbytheCommissiononthebasisofthecriteriaandrequirementsenumeratedherein.

• SECMemorandumCircularNo.15,Seriesof2002andallotherissuancesrelativetheretoaresupersededbythisCircular.

SEC Memorandum Circular No. 12 dated December 20, 2012

• TheseguidelinesshallapplytocompaniesthataremandatedunderSecuritiesRegulationCode(SRC)Rule68,asamended,toadoptthePhilippineFinancialReportingStandards(PFRS)astheirfinancialreportingframework,andthathaveafundedretirementfundforitsemployees.

• TheentityisrequiredunderPAS24“todiscloseinformationaboutanytransactionwitharelatedparty(theretirementfund,inthiscase)andoutstandingbalancesnecessaryforanunderstandingofthepotentialeffectoftherelationshiponthefinancialstatements.Ataminimum,disclosuresshallinclude:

1. Theamountofthetransactions;

2. Theamountofoutstandingbalances,theirtermsandconditionsincludingwhethertheyaresecured,andthenatureoftheconsiderationtobeprovidedinsettlement,anddetailsofanyguaranteesgivenorreceived;

3. Provisionsfordoubtfuldebtsrelatedtotheamountofoutstandingbalances;and

4. Theexpenserecognizedduringtheperiodinrespectofbadordoubtfuldebtsduefromrelatedparties.

• GiventhatthedisclosuresunderPAS24donotprovideanunderstandingofthepotentialeffectsofthetransactionsofthereportingentitywithitsemployees’retirementfund,theseguidelinesshallbeobservedbydisclosingthespecificandmoredetailedinformationontransactionsofareportingentitywitharetirementfundforitsemployees.

• Thefollowingdisclosuresmustbeprovidedintheannualfinancialstatementsofareportingentitythathastransactionseitherdirectlyorindirectlythroughitssubsidiaries,withitsemployees’retirementbenefitfund(the“fund”):

1. Informationwhetherthereportingentity’sfundisintheformofatrustbeingmaintainedbyatrusteebankortrustcompany,orintheformofacorporationwhichhasbeencreatedforthepurposeofmanagingthefund;

2. Thecarryingamountandfairvalueofthefund;

3. Descriptionoftheassetsandinvestmentsofthefund.Thedisclosureshallincludeabriefdescriptionofeachcategorysuchasthemarketforequityordebtsecurities,informationonthelandorbuilding;

4. Volumeandoutstandingbalancesoftransactionsofthefundwiththereportingentityoritssubsidiariesincludingthetermsandconditionsthereof.Thesetransactionsmayincludeamongothers,loans,investment,lease,guaranteeorsurety.

SECMCNo.12prescribestheguide-linesonthedisclosureoftransactionswithretirementbenefitfunds.

25

5. Ifthetransactionismaterial,adiscussionofthenatureofrelationshipofthepersonswhoapproveditwiththereportingentity,itssubsidiaries,oranyofitsdirectorsandofficers.

6. Ifthefundhasinvestmentsinthesecurities(debtorequity)oftherelatedentity,adisclosureofthefollowinginformation:

a. Theamountofinvestmentineachtypeofsecuritiesofreportingentityand/oritssubsidiaries,includinglimitationsorrestrictionsprovidedintheplan(ifany);

b. Incaseofequityinvestment,natureoftherelationshipoftheperson/swhoexercisesvotingrightovertheshares,withthereportingentity,itssubsidiaries,oranyofitsdirectorsorofficers;

c. Theamountofgainsorlossesofthefundarisingfromitsinvestmentinthesecuritiesofthereportingentityand/oritssubsidiaries.Thegainsandlossesshallbepresentedpertypeofsecurity.

• TheseDisclosureGuidelinesshallbeapplicabletoannualfinancialstatementsfortheperiodendedDecember31,2012andonwards.Exceptforthe2012financialstatments,thepresentationoftherequiredinformationshallbeinatwo-yearcomparativeperiod.Failuretocomplywiththedisclosurerequirementsshallconstituteamaterialdeficiencyandshallsubjecttheentitytopenaltiesundertheexistingscaleoffines.

SEC Memorandum Circular No. 1 dated January 7, 2013

• Thefollowingguidelinesareissuedwithrespecttoapplications/documentsfiledbycorporations/partnershipswithforeigninvestors:

1. Noapplicationforincorporationofacorporation,orregistrationofapartnershipshallbeacceptedunlesstheTINorpassportnumberofallitsforeigninvestorsareindicatedinitsregistrationdocuments(i.e.,ArticlesofIncorporation).

2. Forapplicationsforamendments,thesameshallnotbeacceptedunlesstheTINofalltheforeigninvestors,naturalorjuridical,residentornon-resident,areindicatedtherein.

3. AlldocumentstobefiledwiththeSECbycorporationsandpartnershipsaftertheirincorporation(i.e.,GeneralInformationSheets)shallnotbeacceptedunlesstheTINofallitsforeigninvestors,naturalorjuridical,residentornon-resident,areindicatedtherein.

SEC Memorandum Circular No. 3 dated January 15, 2013

• Financingandlendingcompaniesarerequiredtosubmitinterimsemi-annualfinancialstatements(ISAFS),otherwiseknownasFCIF(FinancingCompaniesInterimFinancialStatements)andLCIF(LendingCompaniesFinancialStatements),forfinancingandlendingcompanies,respectively.

• Rule8(a)oftheimplementingrulesandregulations(IRR)ofRANo.9474,otherwiseknownastheLendingCompanyRegulationActof2007,whichrequireslendingcompaniestosubmitISAFSorLCIFeveryJuly15andJanuary15,failedtoconsiderlendingcompanieswithfiscalyearsendingonDecember31.

SECMCNo.1requirestheinclusionoftheTINorpassportnumberofforeigninvestorsinallforms,papersanddocu-mentsfiledwiththeSEC.

SECMCNo.3amendstherulesonthedateofsubmissionoftheinterimsemi-annualfinancialstatementsrequiredforfinancingandlendingcompanies.

26 Tax Bulletin

• Section6ofSECMCNo.3,Seriesof2007requiresfinancingcompaniestosubmitISAFSorFCIFwithin15calendardaysfromtheendofthesemester.

• FinancingandlendingcompaniesshallsubmitISAFSwithin45calendardaysfromtheendoftheinterimsemi-annualperiodcoveredbythereport.

• Rule8(a)oftheIRRofRANo.9474andSection6ofSECMCNo.3,seriesof2007,pertainingtotheduedateofsubmissionofISAFSareherebyamendedaccordingly.

BSP Issuances

BSP Circular No. 779 dated January 9, 2013

• Item“b.2”ofSectionX303oftheManualofRegulationsforBanks(MORB)oncreditexposurelimitstoasingleborrowerisamendedtoreadasfollows:

“Sec. X303 Credit Exposure Limits to a Single Borrower

xxx

b.Thetotalamountofloans,creditaccommodationsandguaranteesprescribedinthefirstparagraphmaybeincreasedforeachofthefollowingcircumstances:

1. xxx;

2. Byanadditionaltwenty-fivepercent(25%)ofthenetworthofsuchbank:Provided,thattheadditionalloans,creditaccommodationsandguaranteesareforthepurposeofundertakinginfrastructureand/ordevelopmentprojectsunderthePublic-PrivatePartnership(PPP)ProgramofthegovernmentdulycertifiedbytheSecretaryofSocio-EconomicPlanning:Provided,further,thatthetotalexposuresofthebanktoanyborrowerpertainingtosuchinfrastructureand/ordevelopmentprojectsunderthePPPProgramshallnotexceedtwenty-fivepercent(25%)ofthenetworthofsuchbank:Provided,furthermore,thattheadditionaltwenty-fivepercent(25%)shallonlybeallowedforaperiodofsix(6)yearsfrom28December2010:Provided,finally,thatthecreditriskconcentrationarisingfromtotalexposurestoallborrowerspertainingtosuchinfrastructureand/ordevelopmentprojectsunderthePPPProgramshallbeconsideredbythebankinitsinternalassessmentofcapitaladequacyrelativetoitsoverallriskprofileandoperatingenvironment.Saidloans,creditaccommodationsandguaranteesbasedonthecontractedamountasoftheendofthesix(6)-yearperiodshallnotbeincreasedthereafter;and

3. xxx.”

• ►ThethirdparagraphofSection4303QoftheManualofRegulationsforNon-bankFinancialInstitutions(MORNBFI)ontheloanlimittoasingleborrowerisamendedtoreadasfollows:

CircularNo.779amendstheregula-tionsonSingleBorrower’sLimit.

27

“Sec. 4303Q Loan Limit to a Single Borrower

xxx

Thetotalamountofloans,creditaccommodationsandguaranteesprescribedinthefirstparagraphmaybeincreasedbyanadditional25%ofthenetworthofsuchquasi-bank:Provided,thattheadditionalloans,creditaccommodationsandguaranteesareforthepurposeofundertakinginfrastructureand/ordevelopmentprojectsunderthePublic-PrivatePartnership(PPP)ProgramofthegovernmentdulycertifiedbytheSecretaryofSocio-EconomicPlanning:Provided,further,thatthetotalexposuresofthequasi-banktoanyborrowerpertainingtosuchinfrastructureand/ordevelopmentprojectsunderthePPPProgramshallnotexceed25%ofthenetworthofsuchquasi-bank:Provided,furthermore,thattheadditional25%shallonlybeallowedforaperiodof6yearsfrom28December2010:Provided,finally,thatthecreditriskconcentrationarisingfromtotalexposurestoallborrowerspertainingtosuchinfrastructureand/ordevelopmentprojectsunderthePPPProgramshallbeconsideredbythequasi-bankinitsinternalassessmentofcapitaladequacyrelativetoitsoverallriskprofileandoperatingenvironment.Saidloans,creditaccommodationsandguaranteesbasedonthecontractedamountasoftheendofthe6-yearperiodshallnotbeincreasedbutmaybereducedand,oncereduced,saidexposuresshallnotbeincreasedthereafter.

xxx”

• ThisCircularshalltakeeffect15calendardaysfollowingitspublicationeitherintheOfficialGazetteorinanewspaperofgeneralcirculation.

[Editor’s Note: Circular No. 779 was published in the PhilippineStar on January 14, 2013.]

BSP Circular No. 780 dated January 10, 2013

• OFWsandfamilymemberswhoreturnedfromSyriaareeligibletoavailoftheCurrencyExchangeFacility(CEF)atthemaximumamountofP10,000.00equivalentofSyriancurrencyperperson.

►• Syriancurrencywhichisconsideredlegaltender(i.e.,hasnotbeendemonetized)inSyriamaybeconvertedtoPhilippinepesosevenifnotfreelyconvertiblewiththeBSPatthetimeofexchange.OnwhethertheSyriancurrencyhasbeendemonetized,BSPofficesandbranchesandAABsshallbeguidedbythelatestofficialinformationfromtheDepartmentofForeignAffairsatthetimeofexchange.

• Inconverting,theBSPOfficesandBranchesandAABsshallusethelatestBSPReferenceExchangeRateBulletin.TheBSP’spurchaseoftheSYPacquiredbyAABsundertheCEFshallbeatthesamerateatwhichtheAABspurchasedthem.

• ThefacilityisopentothosewhoreturnedfromSyriafrom1January2012andshallbeavailablefor4monthsfromeffectivityofthisCircular.

• AABs,particularlythosewithbranchofficesatPhilippineinternationalairports(includingtheNinoyAquinoInternationalAirportTerminals1,2,and3,Clark,Subic,Laoag,Cebu,DavaoandZamboanga)andseaports,shallextendtheirbankinghoursasneeded,toaccommodatethosewhowishtoavailofthefacility.

CircularNo.780prescribesguidelinesgoverningtheimplementationoftheSyrianPoundCEF.

28 Tax Bulletin

• AABsshalladvisetheirbranchesontheactivationoftheCEFnotlaterthanone(1)bankingdayfollowingtheBSP’sissuanceoftheguidelinesforpublicinformation.

• Allbankbrancheslocatedatairports/seaportsshallpostpublicadvisoriesinEnglishandFilipinoabouttheCEFinconspicuousplaces,preferablybeforethebaggagecarouselandcustomsdesk.

• AABsareremindedtocomplywiththeAnti-MoneyLaunderingActof2001.

• BearinginmindtheobjectiveoftheCEFprogramtoprovideassistancetoreturningOFWs,AABsareenjoinednottocollectanykindofservicefeefromthoseavailingoftheprogram.

• AABsshallsubmittoBSP-CashDepartment(BSP–CD,HeadOffice)theConsolidatedSummaryofPurchasesundertheCEF,togetherwithcopiesofthefilled-upConversionSlipsforeachtransactionwithin1bankingdayfromtheendofreferenceweek.

►• CurrencypurchasedbyAABsundertheCEFshallbesurrenderedtotheBSP–CDwithin10bankingdaysfrompurchase.

• ThecurrencypurchasedbyAABsundertheCEFshallnotbeincludedinthecomputationoftheforeignexchangepositionofsaidbanks.

• AABsfoundviolatingthisCircularshallbesubjecttothesanctionsprovidedbySection37ofRANo.7653.

►• ThisCircularshalltakeeffect15daysafterpublication.

[Editor’s Note: Circular No. 780 was published in ThePhilippineDailyInquirer on January 15, 2013.]

BSP Circular No. 781 dated January 15, 2013

►►• ThefollowingsectionandsubsectionoftheMORBareamendedtoreadasfollows:

“Sec. X115 Basel III Risk-Based Capital

Theguidelinesimplementingtherevisedrisk-basedcapitaladequacyframeworkforthePhilippinebankingsystemtoconformtoBaselIIIrecommendationsisprovidedinAppendix63b.

Therisk-basedcapitalratioofabank,expressedasapercentageofqualifyingcapitaltoriskweightedassets,shallnotbelessthan10%forbothsolobasis(headofficeplusbranches)andconsolidatedbasis(parentbankplussubsidiaryfinancialalliedundertakings,butexcludinginsurancecompanies).OtherminimumcapitalratiosincludeCommonEquityTier1ratioandTier1capitalratiosof6.0%and7.5%,respectively.Acapitalconservationbufferof2.5%,comprisedofCET1capital,shalllikewisebeimposed.

(The BSP’s implementation plans for the new international capital standards or Basel 2 contained in the Basel Committee on Banking Supervision document “International Convergence of Capital Measurement and Capital Standards: A Revised Framework”, are shown in Appendix 63)

CircularNo.781amendstheBaselIIIimplementingguidelinesonMinimumCapitalRequirements.

29

Subsection X115.1 Scope.TheBaselIIIguidelinesapplytoallUBsandKBs,aswellastheirsubsidiarybanksandQBs.”

►►• Section4115QoftheMORNBFIisamendedtoreadasfollows:

“Sec. 4115Q (2008 – 4116Q) Basel III Risk-Based Capital.Theguidelinesimplementingtherevisedrisk-basedcapitaladequacyframeworkforthePhilippinebankingsystemtoconformtoBaselIIIrecommendationsisprovidedinAppendix Q-46b.

ThesetemplatesapplytoallUniversalBanks(UBs)andCommercialBanks(KBs),aswellastheirsubsidiarybanksandQBs.Therisk-basedcapitalratioofaQB,expressedasapercentageofqualifyingcapitaltorisk-weightedassets,shallnotbelessthan10%forbothsolobasis(headofficeplusbranches)andconsolidatedbasis(parentQBplussubsidiaryfinancialalliedundertakings,butexcludinginsurancecompanies).OtherminimumcapitalratiosincludeCommonEquityTier1ratioandTier1capitalratiosof6.0%and7.5%,respectively.Acapitalconservationbufferof2.5%comprisedofCET1capital,shalllikewisebeimposed.

Theratiosshallbemaintainedatalltimes.

Subsection 4115Q.1 (2008 – 4116Q) Scope.TheBaselIIIguidelinesapplytoallUBsandKBsaswellastheirsubsidiarybanksandQBs.”

►►• ExistingcapitalinstrumentsasofDecember31,2012whichdonotmeettheeligibilitycriteriaforcapitalinstrumentsundertherevisedcapitalframeworkshallnolongerberecognizedascapitalupontheeffectivityofthisCircular.CapitalinstrumentsissuedunderCircularNos.709and716andbeforetheeffectivityofCircularNo.768dated21September2012shallberecognizedasqualifyingcapitaluntil31December2015.

►►• Theguidelinesshallbeapplicabletoalluniversalandcommercialbanksincludingtheirsubsidiarybanks/quasi-banks.

Stand-alonethriftbanks,ruralbanks,cooperativebanksandquasi-banks,aswellastheirsubsidiarybanks/quasi-banksshallcontinuetobesubjecttotheexistingapplicableregulationsonrisk-basedcapitaladequacyframework.However,capitalinstrumentsissuedbysaidbanksshallbesubjecttothecriteriaforinclusionasqualifyingcapitalprovidedinAnnexesAtoCandEtoFofAppendix63b/Q-46oftheMORB/MORNBFI.

►►• Appendix63doftheMORBandAppendix46coftheMORNBFIaredeleted.

►►• Existingregulationsdeemedinconsistentwiththenewprovisionsaresuperseded.

►►• ThisCirculartakeseffectonJanuary1,2014.

[Editor’s Note: Circular No. 781 was published in BusinessWorld on January 21, 2013.]

BSP Circular No. 782 dated January 21, 2013

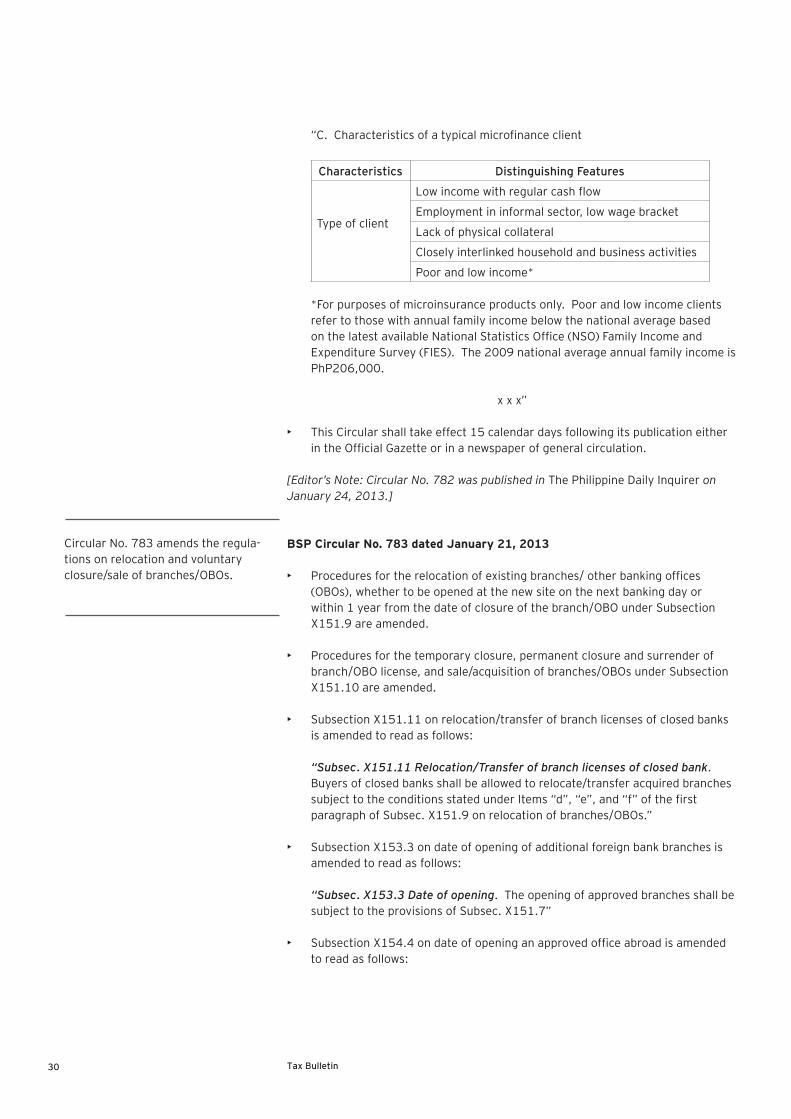

►►• ItemConthe“Characteristicsofatypicalmicrofinanceclient”isamendedtoincludeamongthetypesofclientsthosepoorandlowincomeclientswithannualfamilyincomebelowthenationalaveragebasedonthelatestNationalStatisticsOffice(NSO)FamilyIncomeandExpenditureSurvey(FIES),asfollows:

CircularNo.782amendsAppendix45(NotesonMicrofinance)ofSectionX361oftheMORB.

30 Tax Bulletin

“C.Characteristicsofatypicalmicrofinanceclient

Characteristics Distinguishing Features

Typeofclient

Lowincomewithregularcashflow

Employmentininformalsector,lowwagebracket

Lackofphysicalcollateral

Closelyinterlinkedhouseholdandbusinessactivities

Poorandlowincome*

*Forpurposesofmicroinsuranceproductsonly.PoorandlowincomeclientsrefertothosewithannualfamilyincomebelowthenationalaveragebasedonthelatestavailableNationalStatisticsOffice(NSO)FamilyIncomeandExpenditureSurvey(FIES).The2009nationalaverageannualfamilyincomeisPhP206,000.

xxx”

►►• ThisCircularshalltakeeffect15calendardaysfollowingitspublicationeitherintheOfficialGazetteorinanewspaperofgeneralcirculation.

[Editor’s Note: Circular No. 782 was published in ThePhilippineDailyInquirer on January 24, 2013.]

BSP Circular No. 783 dated January 21, 2013

►►• Proceduresfortherelocationofexistingbranches/otherbankingoffices(OBOs),whethertobeopenedatthenewsiteonthenextbankingdayorwithin1yearfromthedateofclosureofthebranch/OBOunderSubsectionX151.9areamended.

►►• Proceduresforthetemporaryclosure,permanentclosureandsurrenderofbranch/OBOlicense,andsale/acquisitionofbranches/OBOsunderSubsectionX151.10areamended.

►►• SubsectionX151.11onrelocation/transferofbranchlicensesofclosedbanksisamendedtoreadasfollows:

“Subsec. X151.11 Relocation/Transfer of branch licenses of closed bank.Buyersofclosedbanksshallbeallowedtorelocate/transferacquiredbranchessubjecttotheconditionsstatedunderItems“d”,“e”,and“f”ofthefirstparagraphofSubsec.X151.9onrelocationofbranches/OBOs.”

►►• SubsectionX153.3ondateofopeningofadditionalforeignbankbranchesisamendedtoreadasfollows:

“Subsec. X153.3 Date of opening.TheopeningofapprovedbranchesshallbesubjecttotheprovisionsofSubsec.X151.7”

►►• SubsectionX154.4ondateofopeninganapprovedofficeabroadisamendedtoreadasfollows:

CircularNo.783amendstheregula-tionsonrelocationandvoluntaryclosure/saleofbranches/OBOs.

31

“Subsec. X154.4 Date of opening.TheopeningofanyofficeabroadshallbesubjecttotheprovisionsofSubsectionX151.7”

►►• ThisCircularshalltakeeffect15calendardaysfollowingitspublicationeitherintheOfficialGazetteorinanewspaperofgeneralcirculation.

[Editor’s Note: Circular 783 was published in TheManilaTimes on January 24, 2013.]

Court Decision

People of the Philippines vs. Judy Anne Santos y LumaguiCTA(ThirdDivision)Crim.CaseNo.0-012promulgatedJanuary16,2013

Facts:

In2005,theaccusedJudyAnneSantos(Santos)waschargedbeforetheCourtofTaxAppeals(CTA)withviolationofSection255oftheTaxCodeforwillfully,unlawfullyandfeloniouslyfilingafalseandfraudulentincometaxreturn(ITR)fortaxableyear2002.SantosreportedagrossincomeofP8,033,332.70onher2002ITR.TheprosecutionallegedthatSantos’correctincomefor2002totalsP16,396,234.70,oranunder-declarationofP8,362,902.00resultinginanincometaxdeficiencyofP1,395,116.24,excludinginterestandpenalties.

Theprosecutionpresentedbothtestimonialanddocumentaryevidence,includingCertificatesofCreditableTaxWithheldissuedbyABS-CBNBroadcastingCorporation,VivaProductions,Inc.,StarCinemaProductions,Inc.,RegalEntertainment,Inc.andCenturyCanningCorporationshowingthetotaltalentfeespaidtoSantosfor2002andthetaxeswithheld.

ThedefensepresentedSantoswhodeniedtheallegationsofwillfulfilingofafalseandfraudulentITR.Santostestifiedthat:

a. ThesignatureaffixedontopofhernameintheITRfor2002isnothersignature;

b. Sinceshewas12yearsold,shehadengagedtheservicesofMr.AlfonsoLorenzoasManagertowhomsheentrustedalltransactions,i.e.,contractnegotiations,contractsigning,handlingoffees,filingoftaxreturns,payingcorrespondingtaxes,etc.;

c. Mostofthetime,herfees(checks)wereissuedinthenameofherManager,whocollectsthesame,andshehasnoknowledgeofhowmuchshewasearningperproject;

d. WhilesheadmitsthesignaturesappearingontheCounter-AffidavitwithCounter-ChargeandherRejoinder-Affidavitsubmittedin2005,shewasnevergivenachancebyherManagertoreadtheircontents;and

e. ShereallyintendedtosettlethecasewereitnotfortheoppositionbyherManagerandthenlegalcounsel.

Negligence,whetherslightorgross,isnotequivalenttofraudwithintenttoevadeatax,whichiscriminallypunish-ableundertheTaxCode.Fraudmustamounttointentionalwrong-doingwiththesoleobjectofavoidingtax.

32 Tax Bulletin

Santos’testimonywascorroboratedbyherexternalauditor,whotestifiedthatalldocumentsusedinherreportfortheFinancialStatementswereallprovidedbytheManager.

Issue:

IsSantosliableforwillfulfilingofafalseandfraudulentITRinviolationofSection255oftheTaxCode?

Ruling:

No.TheprosecutionfailedtoestablishtheguiltofSantosbeyondreasonabledoubt.

ThereisnoevidenceintherecordstoestablishthekeyelementofwillfulnessonthepartofSantostosupplythecorrectandaccurateinformationonherITR.Santosdeniedthesignatureappearingonthetopofthename“JudyAnneSantos”intheITRfor2002.TheCertifiedPublicAccountant,whoseparticipationislimitedtothepreparationoftheFinancialStatementsattachedtothereturn,alsodeniedsigningthereturnonbehalfoftheaccused.TheintentionofSantostosettlethecasewereitnotfortheoppositionofherManagerandpreviouscounselnegatesanymotivetocommitfraud.

Theprosecutionhastheburdentoprovebeyondreasonabledoubtthataccusedwillfullyfailedtosupplycorrectandaccurateinformationinthereturn.Santos,however,isfoundnegligentbutsuchisnotenoughtoconvictherinthecaseatbench.Negligence,whetherslightorgross,isnotequivalenttothefraudwithintenttoevadethetaxcontemplatedbythelaw.Fraudmustamounttointentionalwrong-doingwiththesoleobjectofavoidingthetax.

Inallcriminalcases,merespeculationcannotsubstituteforproofofestablishingtheguiltoftheaccused.Suspicion,nomatterhowstrong,mustneverswayjudgment.Wherethereisreasonabledoubt,theaccusedmustbeacquittedeventhoughtheirinnocencemaynothavebeenestablished.Whenguiltisnotprovenwithmoralcertainty,ithasbeenalongstandingcourtpolicythatthepresumptionofinnocencemustbefavored,andexonerationgrantedasamatterofright.

However,acquittalforthefailureoftheprosecutiontoproveallelementsofthecriminaloffensebeyondreasonabledoubtdoesnotincludetheextinguishmentofthecivilliability.Santosisliabletopaythedeficiencyincometaxesfortheyear2002intheamountofP3,418,034.78includingpenaltiesandinterest.Inaddition,Santosisorderedtopay20%delinquencyinterestcomputedfromJanuary15,2008untilfullpayment.

34 Tax Bulletin

Wewelcomeyourcomments,ideasandquestions.PleasecontactMa.FidesA.Baliliviae-mailatMa.Fides.A.Balili@ph.ey.comorattelephonenumber894-8113andMarkAnthonyP.Tamayoviae-mailatMark.Anthony.P.Tamayo@ph.ey.comorattelephonenumber894-8391.

SyCip Gorres Velayo & Co.6760AyalaAvenue,MakatiCity,PhilippinesTelephone:(632)891-0307Fax:(632)819-0872

©2013SyCipGorresVelayo&Co.AllRightsReserved.FEAno.1000057

SGV&Co.maintainsofficesinMakati,Cebu,Davao,Bacolod,CagayandeOro,Baguio,GeneralSantosandCavite.

ForanelectroniccopyoftheTaxBulletinorforfurtherinformationaboutTaxServices,pleasevisitourwebsitewww.sgv.ph

Expirydate:noexpiry