Tax Bulletin - SGV & Co....4 Tax Bulletin BIR Rulings BIR Ruling No. 1168-2018 dated 6 September...

28

Tax Bulletin September 2018

Transcript of Tax Bulletin - SGV & Co....4 Tax Bulletin BIR Rulings BIR Ruling No. 1168-2018 dated 6 September...

1Tax Bulletin |

Tax BulletinSeptember 2018

2 | Tax Bulletin

Highlights

BIR Rulings

• Thegrossreceiptsofnon-bankfinancialintermediariesaresubjecttoGrossReceiptsTax(GRT)andnottoVAT.(Page 4)

• Thesale,importationorleaseofpassengerorcargovesselsandaircraft,includingengine,equipmentandsparepartsthereof,fordomesticorinternationaltransportoperationsisexemptfromVAT.(Page 4)

BIR Issuances

• RevenueRegulation(RR)No.21-2018implementstheamendmentsintroducedbytheTRAINLawontheimpositionofinterestunderSection249oftheTaxCode.(Page 4)

• RevenueMemorandumCircular(RMC)No.72-2018reiteratesandsupplementstheexistingpoliciesrelativetothevalidationofsalesgeneratedfromPointofSale(POS),CashRegisterMachine(CRM),SpecialPurposeMachine(SPM),OtherSalesReceiptingSystemSoftware,ReceiptingandInvoicingofComputerizedAccountingSystem(CAS),includingonlinesalestransactionsandfrommanualinvoices,receiptsandsupplementalcommercialdocuments.(Page 5)

• RMCNo.73-2018circularizestheavailabilityofthenewBIRFormNos.0619-E[MonthlyRemittanceFormofCreditableIncomeTaxesWithheld(Expanded)]and0619-F(MonthlyRemittanceFormofFinalIncomeTaxesWithheld),bothJanuary2018versions.(Page 6)

• RMCNo.75-2018circularizesthesalientpointsoftheSupremeCourtdecisioninthecaseofMedicardPhilippinesvs.CommissionerofInternalRevenue(G.R.No.222743dated5April2017)onthemandatorystatutoryrequirementofaLetterofAuthority(LOA)forthevalidityofataxassessment.(Page 7)

• RMCNo.78-2018providesguidelinesontheregistrationofPhilippineOffshoreGamingOperatorsandtheiraccreditedserviceproviders.(Page 8)

Customs Updates

• CustomsMemorandumCircular(CMC)No.176-2018providesfortheTemporaryLiftingoftheSpecialSafeguardDuty(SSD)onOnionscoveredbyTariffHeading0703.10.19.(Page 10)

• CMONo.13-2018providesfortheDecentralizationoftheManagementInformationSystemandTechnologyGroup(MISTG)Non-InformationTechnology(IT)Functions.(Page 10)

• CMONo.14-2018providesfortheGuidelinesontheImplementationoftheFreeTradeAgreement(FTA)betweentheEuropeanFreeTradeAssociation(EFTA)StatesandthePhilippines(PH).(Page 12)

SEC Issuances and Opinion

• SECMCNo.11providesfortherulesgoverningtheadministrationofthePhilippinePeso-DenominatedGovernmentSecurities(GS)Benchmarks.(Page 13)

3Tax Bulletin |

• SECMCNo.12providestheguidelinesontheissuanceofgreenbondsundertheASEANGreenBondsStandardsinthePhilippines.(Page 14)

• Thenationalityrequirementforaninvestmenthouserefersonlytothestocksentitledtovote.(Page 15)

BSP Issuances

• CircularNo.1012providesforRevisedRulesofProcedureonAdministrativeCasesinvolvingDirectorsandOfficersofBSP-SupervisedFinancialInstitutions.(Page 15)

• CircularNo.1013providesforAmendmentstotheRulesGoverningPrejudicialActs,Practices,orOmissionsofNon-StockSavingsandLoanAssociations(NSSLA).(Page 17)

• CircularNo.1014providesforaCurrencyRateRiskProtectionProgram(CRPPFacility).(Page 18)

Court Decisions

• Everyformofcompensationforservices,whetherpaidincashorinkind,isgenerallysubjecttoincometax,andconsequently,towithholdingtax.Thenamedesignatedtothecompensationincomeisimmaterial.

Thus,salaries,wages,emoluments,andhonoraria,allowances,commissions,fees(includingdirector’sfees,ifthedirectoris,atthesametime,anemployeeoftheemployerorthecorporation),bonuses,fringebenefits(exceptthosesubjecttothefringebenefitstaxundertheTaxCode),pensions,retirementpay,andotherincomeofasimilarnature,constitutecompensationincomethataretaxableandsubjecttowithholdingtax.(Page 19)

• Ataxevasioncasefiledbythegovernmentagainstanerringtaxpayerhas,foritspurpose,theimpositionofcriminalliability.Ontheotherhand,ataxpayer’sPetitionforReviewtoquestionadeficiencytaxassessmentisintendedtopreventitfrombecomingfinalandexecutory.AcquittalofthetaxpayerinthecriminalcasewillnotresultinthedismissalofthePetitionforReview,whichisnotdeemedinstitutedwiththecriminalcasefortaxevasion.

Whatisdeemedinstitutedwiththecriminalactionisonlytheactiontorecovercivilliabilityarisingfromthecrime.Civilliabilityarisingfromadifferentsourceofobligation,suchaswhentheobligationiscreatedbylaw,isnotdeemedinstitutedwiththecriminalaction.(Page 21)

• The3-yearprescriptiveperiodmaybeextended,ifawaiverwasdulyexecutedbeforeitsexpiration.(Page 23)

• FinancialorTechnicalAssistanceAgreement(FTAA)contractorsareliabletopayVATonimportedgoodsandservicesandcustomsdutiesandfeesonimportedproductsonlyaftertheirrecoveryperiod.(Page 24)

• A“Build-To-Own”or“Build-Your-Own”schemeisnotasaleofrealpropertythatissubjecttoExpandedWithholdingTax(EWT)andDocumentaryStampTax(DST).(Page 26)

4 | Tax Bulletin

BIR Rulings

BIR Ruling No. 1168-2018 dated 6 September 2018

Facts:

XCo.,adomesticcorporation,isaBSP-supervisednon-bankfinancialinstitution.Itisprimarilyengagedintheoperationofaninvestmenthousewhereitearnsincomefrominterests,commissionsanddiscounts.XCo.soughtaconfirmationfromtheBIRthatitsgrossreceiptsaresubjecttoGRTandnottoVAT.

Issue:

IsXCo.subjecttoGrossReceiptsTax(GRT)? Ruling:

Yes.XCo.,beinganon-bankfinancialintermediary,issubjecttoGRTunderSection122oftheTaxCode.ItisnotsubjecttoVATpursuanttoSection109(1)(V)oftheTaxCode,whichexemptsfromVATtheservicesofnon-bankfinancialintermediaries,amongothers,

BIR Ruling No. 1169-2018 dated 7 September 2018

Facts:

ABCCo.isadomesticcorporationandalicensedaircraftoperatorauthorizedtoperformcommercialairoperations.Itimported3aircraftforuseinitsDomesticNon-ScheduledandInternationalNon-ScheduledAirTransportationServices.

Issue:

IstheimportationoftheaircraftsubjecttoVAT?

Ruling:

No.Section109(1)(T)oftheTaxCodeandSection4.109(B)(1)(t)ofRRNo.16-2005,asamended,providesthatthesale,importationorleaseofpassengerorcargovesselsandaircraft,includingengine,equipmentandsparepartsthereof,fordomesticorinternationaltransportoperationsshallbeexemptfromVAT.

BIR Issuances

RR No. 21-2018 issued on 14 September 2018

• InterestatdoubletheeffectivelegalinterestrateforloansorforbearanceofmoneyintheabsenceofanexpressstipulationassetbytheBangkoSentralngPilipinas(BSP)shallbeassessedandcollectedonanyunpaidamountoftaxfromthedateprescribedforpaymentuntiltheamountisfullypaid.

1. PursuanttoBSPMemorandumNo.799,Seriesof2013,theinterestrateforloansorforbearanceofmoneyintheabsenceofanexpressstipulationis6%.

2. Thus,therateoflegalinterestimposableunderSection249shallbe12%.

Thegrossreceiptsofnon-bankfinancialintermediariesaresubjecttoGRTandnottoVAT.

Thesale,importationorleaseofpassengerorcargovesselsandaircraft,includingengine,equipmentandsparepartsthereof,fordomesticorinternationaltransportoperationsisexemptfromVAT.

RRNo.21-2018implementstheamendmentsintroducedbytheTRAINLawontheimpositionofinterestunderSection249oftheTaxCode.

5Tax Bulletin |

3. ACircularshallbeissuedbytheCommissionerincasetheBSPprescribesanewrateofinterest.

• UpontheeffectivityoftheTRAINLaw,deficiencyanddelinquencyinterestsshall,innocase,beimposedsimultaneously.

1. Deficiencyinterestshallbeimposedonanydeficiencytaxdue,fromthedateprescribedforitspaymentuntilfullpaymentoruponissuanceofanoticeanddemandbytheCommissionerorhisauthorizedrepresentative,whichevercomesfirst.

2. Delinquencyinterestshallbeimposedonthefailuretopay:

• Theamountofthetaxdueonanyreturntobefiled;

• Theamountofthetaxdueforwhichnoreturnisrequired;or

• Adeficiencytax,oranysurchargeorinterestthereonontheduedateappearinginthenoticeanddemandoftheCommissionerorhisauthorizedrepresentativeuntiltheamountisfullypaid,whichinterestshallformpartofthetax.

• FortaxliabilitiesthatbecameduebeforetheeffectivityoftheTRAINLawon1January2018,butwerefullypaidafterthesaideffectivitydate,theinterestratesshallbeappliedasfollows:

Period Applicable Interest Type and Rate

Fortheperiodupto31December2017

Deficiencyand/ordelinquencyinterestat20%

Fortheperiod1January2018untilfullpaymentofthetaxliability

Deficiencyand/ordelinquencyinterestat12%

1. Betweenthedateprescribedforpaymentuntil31December2017,thedoubleimpositionofbothdeficiencyanddelinquencyinterestunderSection249oftheTaxCodepriortoitsamendmentwillstillbeallowed.

• Theseregulationsareeffectivebeginning1January2018,theeffectivitydateoftheTRAINLaw.

(Editor’s Note: RR No. 21-2018 was published in the ManilaBulletin on 17 September 2018)

RMC No. 72-2018 issued on 30 August 2018

• ThePostEvaluationofPointofSale(POS),CashRegisterMachine(CRM),SpecialPurposeMachine(SPM),othersalesreceiptingsystemsoftware,includingreceiptingorinvoicingofComputerizedAccountingSystem(CAS),maybeconductedsimultaneouslywithotherenforcementactivities,suchasTaxComplianceVerificationDrive(TCVD),surveillance,inventorystocktakingandauditorinvestigation.

• TheinventoryofallPOS,CRM,SPMandotherreceiptingmachineorsoftware,whetherusedforissuanceofinvoicesorforinternalcontrolpurposes,shallbetaken,matchedandreconciledwiththelistfromtheBIRdatabase.

RMCNo.72-2018reiteratesandsupplementstheexistingpoliciesrelativetothevalidationofsalesgeneratedfromPOS,CRM,SPM,OtherSalesReceiptingSystemSoftware,ReceiptingandInvoicingofCAS,includingonlinesalestransactionsandfrommanualinvoices,receiptsandsupplementalcommercialdocuments.

6 | Tax Bulletin

• Within5daysfromreceiptofaLetterNoticeonanyunmatchedorunaccountedmachine,thetaxpayershallreconcileandexplaininwritingthediscrepancyandaccountfortheunmatchedPOS/CRM/SPMandotherreceiptingmachineorsoftware.

• TheServiceProvider/Supplier/Contractor/Developerofmachine,softwareorsystemssubjectedtoPostEvaluationshallassistintheextractionofsalesdataand/orZ-readingasrequiredbytheBIRorthetaxpayer.

• Salesdatashallbevalidatedandextractedfromallsources,suchasbutnot

limitedto,thefollowing:

1. CRM/POS/othersalesreceiptingsoftwareandCAS,consistingofZ-reading,e-Journal,back-endreportsfromthestand-alonesystem,server,middlewareorconsolidatordependingonthesystemorsoftwareset-up.

2. Salesfromonlinetransactions,unmannedbill,coinortokenoperatedmachines,unregisteredmachinesusedtorecordsalestransactionsanddefectiveordamagedmachines,whichwerenotreportedorwithpendingapplicationforcancellationwiththeconcernedLTS-Office,Division,LTDOorRDO.

3. Salesbook,accountingrecordsandmanualinvoicesorreceipts,includingunregisteredorexpiredreceipts,invoicesorrecords,ifany.

4. AllSPMsusedforsupplementaryinvoicingorreceipting,suchascollectionandacknowledgementreceiptorbillspayment,withoutcorrespondingprincipalinvoiceorreceipt.

• ASubpoena Duces Tecum(SDT)shallbeissuedtocompelsubmissionandpresentationofdocumentsandmachinesnotyetavailableaftertherequiredcompliancedate.

• FailuretocomplywiththeSDTshallwarranttheuseof“BestEvidenceObtainableRule”forunregistered,unaccounted,missing,lostsalesmachinesormanualreceiptsorinvoicesandsimultaneously,thereferraloftheSDTtotheProsecutionorLegalDivisionforfilingofacriminalcaseonfailuretoobeysubpoena.

RMC No. 73-2018 issued on 31 August 2018

• ThefollowingnewBIRformsshallbeusedbythewithholdingagentinremittingthewithholdingtaxofthefirst2monthsofeverycalendarquarter:

1. BIRFormNo.0619-E-MonthlyRemittanceFormforCreditableIncomeTaxesWithheld(Expanded)

2. BIRFormNo.0619-F–MonthlyRemittanceFormofFinalIncomeTaxesWithheld

• Taxpayersshallfiletheirrespectiveremittanceformsonthefollowingduedates:

1. Non-eFPStaxpayers–within10thdayofthefollowingmonthinwhichwithholdingwasmade

2. eFPStaxpayers–withinthe15thdayofthefollowingmonth,dependingontheindustrygroupingasprescribedunderRevenueRegulation(RR)No.26-2002

RMCNo.73-2018circularizestheavailabilityofthenewBIRFormNos.0619-E[MonthlyRemittanceFormofCreditableIncomeTaxesWithheld(Expanded)]and0619-F(MonthlyRemittanceFormofFinalIncomeTaxesWithheld),bothJanuary2018version.

7Tax Bulletin |

• Thetaxpayershallfileand/orpaythroughthefollowingmodes:

1. ManualReturn

2. ElectronicBureauofInternalRevenueForms(eBIRForms)

3. ElectronicFilingandPaymentSystem(eFPS)

• ThenewBIRFormNos.0619-Eand0619-Farealreadyavailableunder:

1. BIRForms–Payment/RemittanceFormssectionoftheBIRwebsite(manualfilers)

2. OfflineeBIRFormsPackagev7.1(eBIRFormsfilers)

3. eFPSsystem(eFPSfilers)

• ManualfilersandeBIRFormsfilerscanchoosebetweenmanualoronlinepayment/remittanceofthewithholdingtaxdue.

1. ManualPayment/Remittance:

• Over-the-counteroftheAuthorizedAgentBank(AAB)locatedwithintheterritorialjurisdictionoftheRevenueDistrictOffice(RDO)wherethetaxpayerisregistered.

• InplaceswheretherearenoAABs,thereturnshallbefiledandthetaxdueshallbepaidwiththeconcernedRevenueCollectionOfficer(RCO),throughthemobilerevenuecollectionofficerssystem(MRCOS)facility,underthejurisdictionoftheRDO.

2. OnlinePayment/Remittance:

• ThroughGCashMobilePayment

• LandbankofthePhilippines(LBP)LinkbizPortal,fortaxpayerswhohaveATMaccountswithLBPand/orholdersofBancnetATM/DebitCard

• DevelopmentBankofthePhilippines(DBP)TaxOnline,forholdersofVISA/MasterCreditCardand/orBancnetATM/Debit

• Ifthemanualfilerhasnowithholdingtaxdueforthemonth,thetaxpayerisstillrequiredtofileandfollowtheexistingprocedurefor“NoPayment”,whichistofilethroughtheuseofeBIRForms.

RMC No. 75-2018 issued on 5 September 2018

InthecaseofMedicard Philippines, Inc. vs. Commissioner of Internal Revenue (G.R. No. 222743, 5 April 2017),theSupremeCourtheldasfollows:

• NotaxassessmentscanbeissuedornoassessmentfunctionsorproceedingscanbedonewithoutpriorapprovalandauthorizationoftheCommissionerofInternalRevenue(CIR)orhisdulyauthorizedrepresentativethroughaLetterofAuthority(LOA).

RMCNo.75-2018circularizesthesalientpointsoftheSupremeCourtdecisioninthecaseofMedicardPhilippinesvs.CommissionerofInternalRevenue(G.R.No.222743dated5April2017)onthemandatorystatutoryrequirementofaLOAforthevalidityofataxassessment.

8 | Tax Bulletin

• Assuch,anytaxassessmentwithoutanLOAviolatesthetaxpayer’srighttodueprocessandis,therefore,“inescapablyvoid.”

• ThecircumstancesprovidedunderSection6oftheTaxCodewherethetaxpayermaybeassessedthroughbestevidenceobtainable,inventory-taking,orsurveillance,amongothers,havenothingtodowithanLOAsincetheseareonlymethodsofexaminingthetaxpayertoarriveatthecorrectamountoftaxes.

• ALetterNotice(LN)isdifferentfromanLOA.AnLNisissuedtonotifythetaxpayerofanauditwhileanLOAistheauthoritytoconductanauditorexaminationofthetaxpayerleadingtotheissuanceofdeficiencyassessments.Thus,aftertheLNhasbeenserved,therevenueofficershouldsecureanLOAbeforeproceedingwithfurtherexaminationandassessmentofthetaxpayer.

RMC No. 78-2018 issued on 7 September 2018

• Alloperators,whetherPhilippine-basedorforeign-based,includingthosewhopossessanOffshoreGamingLicenseissuedbyPAGCOR,arerequiredtoregisterwiththeBIRupontheoccurrenceofanyofthefollowingevents,whichevercomesfirst:

1. Commencementofbusiness;

2. Paymentofanytaxdue;or

3. Filingofanyapplicabletaxreturn,statementordeclarationasrequiredbytheTaxCode.

• Commencementofbusinessshallbereckonedfromthedaywhenthefirstsaletransactionoccurredorwithin30calendardaysfromtheissuanceofMayor’sPermit/ProfessionalTaxReceipt(PTR)bythelocalgovernmentunit(LGU),orCertificateofRegistrationissuedbytheSEC,whichevercomesearlier.

• AnOffshoreGamingLicenseisanauthoritygrantedbyPAGCORtoPhilippineOffshoreGamingOperators(POGO)fortheestablishment,maintenanceandtheconductofoffshoregamingoperationsinaspecificsitewithinthejurisdictionofPAGCOR.

• AllPhilippine-basedandforeign-basedoperators,includingserviceproviders,shallregisterintheRevenueDistrictOffice(RDO)havingjurisdictionovertheplacewheretheHeadOfficeand/orbranchorPOGOHubislocated.Thefollowingarethedocumentaryrequirementsforregistrationofnon-individuals:

1. BIRFormNo.1903

2. SECCertificateofIncorporationorSECCertificateofRecording(incaseofpartnership)orSECLicensetoDoBusinessinthePhilippines(inthecaseofforeigncorporations):

• InlieuoftheSECLicensetoDoBusinessregistration,thefollowingmaybesubmittedbyaforeign-basedoperatorwhoisnotrequiredtoberegisteredwiththeSEC:

RMCNo.78-2018providesguidelinesontheregistrationofPhilippineOffshoreGamingOperatorsandtheiraccreditedserviceproviders.

9Tax Bulletin |

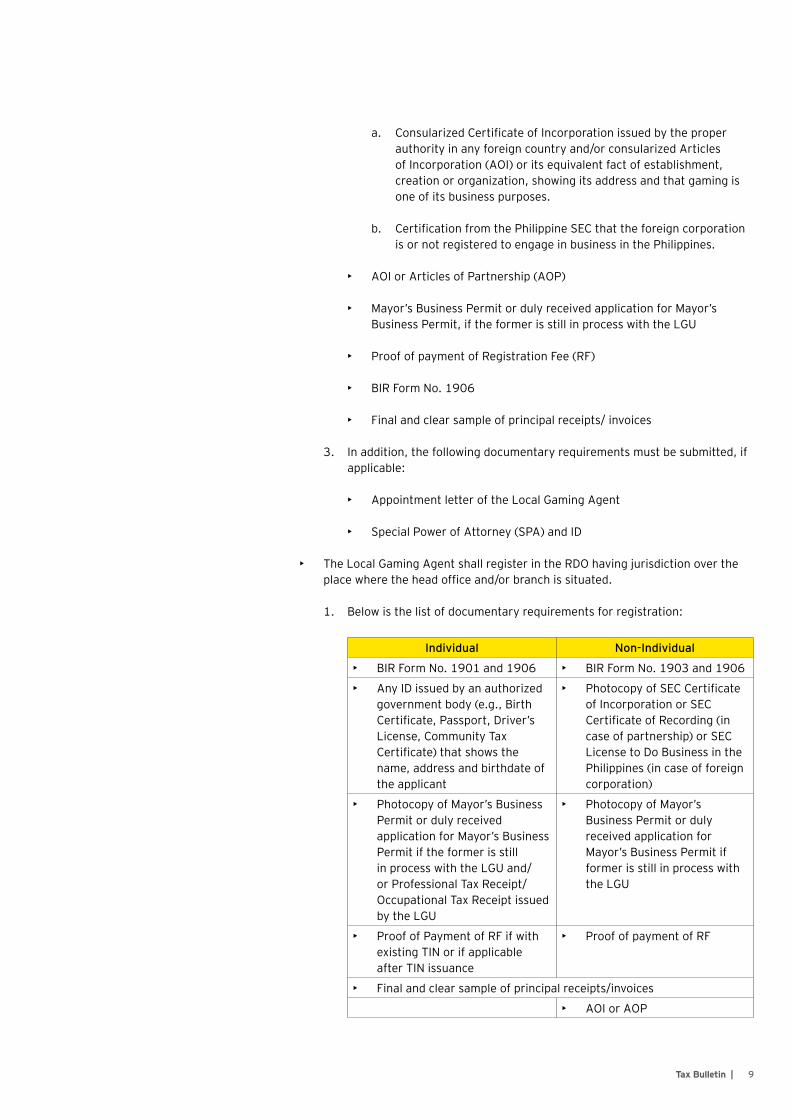

a. ConsularizedCertificateofIncorporationissuedbytheproperauthorityinanyforeigncountryand/orconsularizedArticlesofIncorporation(AOI)oritsequivalentfactofestablishment,creationororganization,showingitsaddressandthatgamingisoneofitsbusinesspurposes.

b. CertificationfromthePhilippineSECthattheforeigncorporationisornotregisteredtoengageinbusinessinthePhilippines.

• AOIorArticlesofPartnership(AOP)

• Mayor’sBusinessPermitordulyreceivedapplicationforMayor’sBusinessPermit,iftheformerisstillinprocesswiththeLGU

• ProofofpaymentofRegistrationFee(RF)

• BIRFormNo.1906

• Finalandclearsampleofprincipalreceipts/invoices

3. Inaddition,thefollowingdocumentaryrequirementsmustbesubmitted,ifapplicable:

• AppointmentletteroftheLocalGamingAgent

• SpecialPowerofAttorney(SPA)andID

• TheLocalGamingAgentshallregisterintheRDOhavingjurisdictionovertheplacewheretheheadofficeand/orbranchissituated.

1. Belowisthelistofdocumentaryrequirementsforregistration:

Individual Non-Individual

• BIRFormNo.1901and1906 • BIRFormNo.1903and1906

• AnyIDissuedbyanauthorizedgovernmentbody(e.g.,BirthCertificate,Passport,Driver’sLicense,CommunityTaxCertificate)thatshowsthename,addressandbirthdateoftheapplicant

• PhotocopyofSECCertificateofIncorporationorSECCertificateofRecording(incaseofpartnership)orSECLicensetoDoBusinessinthePhilippines(incaseofforeigncorporation)

• PhotocopyofMayor’sBusinessPermitordulyreceivedapplicationforMayor’sBusinessPermitiftheformerisstillinprocesswiththeLGUand/orProfessionalTaxReceipt/OccupationalTaxReceiptissuedbytheLGU

• PhotocopyofMayor’sBusinessPermitordulyreceivedapplicationforMayor’sBusinessPermitifformerisstillinprocesswiththeLGU

• ProofofPaymentofRFifwithexistingTINorifapplicableafterTINissuance

• ProofofpaymentofRF

• Finalandclearsampleofprincipalreceipts/invoices

► • AOIorAOP

10 | Tax Bulletin

2. Inaddition,theBoardResolutionindicatingthenameoftheauthorizedrepresentativeandtheSecretary’sCertificateorSPAandIDoftheauthorizedperson,inthecaseoftheauthorizedrepresentativewhowilltransactwiththeBIR,mustbesubmitted,ifapplicable.

• TheBooksofAccountsofOperators,ServiceProvidersandLocalGamingAgentsmustberegisteredwithin30daysfromthedateofitsregistration.

• AllexistingPOGOLicenseespriortotheissuanceofthisCircularshallregisterwiththeRDOhavingjurisdictionovertheplacewheretheHeadOfficeand/orbranchorPOGOHubislocatedandsubmitthefollowingdocumentaryrequirements:

1. BIRFormNo.1903;

2. CopyofAOI/AOPorCertificateofIncorporationissuedbytheproperauthorityinanyforeigncountry;

3. ProofofPaymentofRF;

4. BIRFormNo.1906;

5. Finalandclearsampleofprincipalreceipts/invoices;and

6. SPAandIDofauthorizedperson,inthecaseofanauthorizedrepresentativewhowilltransactwiththeBIR.

• Incaseofthetransferoftheregisteredaddresstoanewlocation,thePOGOLicenseeoritsLocalGamingAgentmustinformtheRDOwhereitisregisteredofsuchfactbyflingtheprescribedBIRFormspecifyingthecompleteaddresswhereitintendstotransfer.

Customs Updates

Customs Memorandum Circular (CMC) No. 176-2018 dated 31 August 2018

• Withreferencetotheletterrequestdated23August2018fromSecretaryEmmanuelF.Piñol,DepartmentofAgriculture,theCommissionerofCustomstemporarilyliftedtheimpositionoftheSpecialSafeguardDuty(SSD)ononionstocushiontheimpactofrisingpricesandmitigatetheimpactofsoaringinflation.

(Editor’s Note: CMC No. 176-2018 was signed by the Commissioner of Customs on 3 September 2018)

Customs Memorandum Order (CMO) No. 13-2018 dated 4 September 2018

• TheobjectiveofthisCMOistopromoteefficiencyintheaccreditationandClientProfileRegistrationSystem(CPRS)activationprocessandstrengthenaccountabilitybyallowingManagementInformationSystemandTechnologyGroup(MISTG)toconcentrateonitsITroleintheBureauofCustoms(BOC)bytransferringnon-ITfunctionscurrentlybeingperformedbyMISTGtootherauthorizedgroups/agencieswhoseprimaryrolesaremorealignedwithsuchfunctions.

CMCNo.176-2018providesfortheTemporaryLiftingoftheSSDonOnionscoveredbyTariffHeading0703.10.19.

CMONo.13-2018providesfortheDecentralizationoftheMISTGNon-ITFunctions.

11Tax Bulletin |

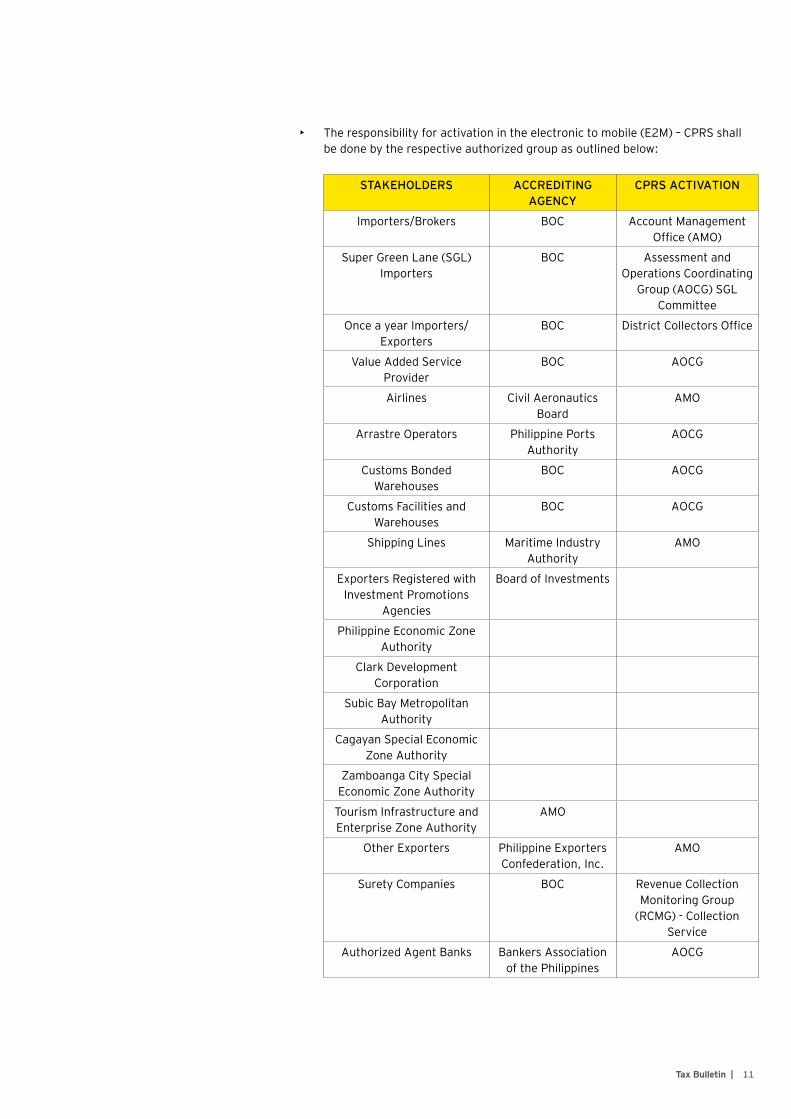

• Theresponsibilityforactivationintheelectronictomobile(E2M)–CPRSshallbedonebytherespectiveauthorizedgroupasoutlinedbelow:

STAKEHOLDERS ACCREDITING AGENCY

CPRS ACTIVATION

Importers/Brokers BOC AccountManagementOffice(AMO)

SuperGreenLane(SGL)Importers

BOC AssessmentandOperationsCoordinating

Group(AOCG)SGLCommittee

OnceayearImporters/Exporters

BOC DistrictCollectorsOffice

ValueAddedServiceProvider

BOC AOCG

Airlines CivilAeronauticsBoard

AMO

ArrastreOperators PhilippinePortsAuthority

AOCG

CustomsBondedWarehouses

BOC AOCG

CustomsFacilitiesandWarehouses

BOC AOCG

ShippingLines MaritimeIndustryAuthority

AMO

ExportersRegisteredwithInvestmentPromotions

Agencies

BoardofInvestments

PhilippineEconomicZoneAuthority

ClarkDevelopmentCorporation

SubicBayMetropolitanAuthority

CagayanSpecialEconomicZoneAuthority

ZamboangaCitySpecialEconomicZoneAuthority

TourismInfrastructureandEnterpriseZoneAuthority

AMO

OtherExporters PhilippineExportersConfederation,Inc.

AMO

SuretyCompanies BOC RevenueCollectionMonitoringGroup

(RCMG)-CollectionService

AuthorizedAgentBanks BankersAssociationofthePhilippines

AOCG

12 | Tax Bulletin

• TheactivationofAuthoritytoReleaseImportedGoods(ATRIG)tospecificTariffCodesshallbetheAOCG’sresponsibility.

• ThisCMOshalltakeeffect15daysafteritscompletepublicationintheOfficialGazetteoranewspaperofgeneralcirculation.

(Editor’s Note: CMO No. 13-2018 was published in the ManilaTimes on 6 September 2018)

CMO No. 14-2018 dated 17 September 2018

• ExecutiveOrder(EO)No.61dated2August2018wasissuedbythePresidentofthePhilippinesandbecameeffectiveimmediatelyafteritscompletepublicationon10August2018inordertomodifyimportduties,includingnecessarychangesinclassificationandotherimportrestrictionsasarerequiredorappropriatetocarryoutandpromotethePhilippines-EuropeanFreeTradeAssociationFreeTradeAgreement(PH-EFTAFTA).

• ThisCMOwasissuedtofacilitatetheprocessingofimportationsandexportationsofgoodscomingtoandfromthePartyunderPH-EFTAFTA,toprovidetheprocedureforgrantingpreferentialtreatmentongoodscoveredbyanOriginDeclaration,andtoestablishappropriatemechanismsinaccreditingexporters/producers/manufacturersasan“ApprovedExporter.”

• GeneralProvisions

1. “OriginDeclaration(OD)”referstotheproofoforiginrequiredunderthePH-EFTAFTAintheformofadeclarationsufficienttoascertaintheoriginatingstatusofthegoods.Thedeclarationmustbecompletedonaninvoice,packinglist,deliverynoteoranyotherrelevantcommercialdocumentthatidentifiestheexporterandtheoriginatinggoods.

2. ExportersandtheirrepresentativesshallbeallowedtomakeanODasProofofOrigin.

3. ImporterssourcingfromEFTAStatesshallbeallowedtoclaimpreferentialtarifftreatmenttooriginatinggoodsonthebasisoftheOD.

4. An“ApprovedExporter(AE)”referstoaproducer,manufacturer,ortraderauthorizedbytherespectivecustomsauthorityoftheParties(thePhilippines,Iceland,NorwayorthecustomsterritoryofSwitzerland)tocompletetheODwithoutsignatureaftercomplyingwiththerequirementsoftheCMO.

5. AnAEisnotrequiredtosigntheODbutmustindicateitsCustomsAuthorizationNumber(CAN).Anon-AEmustaffixthesignatureabovetheprintednameofitsauthorizedsignatoryandleavethefieldonCANblank.

• OperationalProvisions

1. Producers,manufacturers,ortradersmaysubmit,inwritingorelectronically,totheDeputyCommissionerofAOCG,throughtheExportCoordinationDivision(ECD),itsintentiontobeaccreditedasanAE,togetherwiththeotherrequireddocuments.

CMONo.14-2018providesfortheGuidelinesontheImplementationoftheFTAbetweentheEFTAStatesandthePhilippines.

13Tax Bulletin |

2. ExportersmayoptnottoapplywiththeBOCasanAE.However,theODmustindicatethecompletenameandbeartheoriginalsignaturesofitssignatory.Anon-AEmayhaveahigherriskofretro-verificationcomparedtoanAE.

3. ForshipmentsavailingofthepreferentialtarifftreatmentunderthePH-EFTAFTA,theexistingcustomsimportproceduresshallstillapply,exceptthattheimportdocumentsmustbeaccompaniedbyanODwhichmustbepresentedpriortothereleaseofthegoods.

4. IfanimporterisnotinpossessionofanODatthetimeofimportation,theimportermaypresentitatalaterstagesubjecttotherulesontentativereleaseofgoods.AnODmustbesubmittedtotheBOCwithin12monthsfromitscompletion.

5. Forimportationbyinstallments,onlyoneODisrequiredwhichmustbesubmittedupontheimportationofthefirstinstallment.

6. TheBOCshallcarryouttheverificationsofODsupontherequestofcustomsauthoritiesofimportingEFTAparties.Inrelationtothis,importersandexportersbenefittingfromthePH-EFTAFTAmustcooperatewiththeBOC,inaccordancewiththeirobligationsenumeratedintheCMO.

7. TheECDshallconductanauditandevaluationoftheexporter’spremisesandshallmakethenecessarycommunicationtotheEFTASecretariatabouttheresultsofitsoriginverificationwithin6monthsfromthedateoftheverificationrequest.

8. Penalties:IfproventohavecommittedfraudincompliancewiththeCMO:

• Importersshallnotbeallowedtoavailofthepreferentialtariffrates.

• ExportersshallbesuspendedasanAE.

ImpositionoftheabovepenaltiesshallbewithoutprejudicetopossiblefilingofcriminalcasesundertheapplicableprovisionsoftheCustomsModernizationandTariffAct(CMTA)andtheRevisedPenalCode.

• ThisCMOshalltakeeffectimmediately.

(Editor’s Note: CMO No. 14-2018 was received by the UP Law Center on 21 September 2018)

SEC Issuances and Opinion

SEC Memorandum Circular No. 11 series of 2018 dated 31 August 2018

InlinewiththepolicyoftheStatetopromotethedevelopmentofthecapitalmarketandprotectionoftheinvestors,theSECissuesrulestogovernPhilippine-PesoGovernmentSecurities(GS)withthefollowingkeyfeatures:

• RulesapplytoalegalpersonwhointendstogenerateanindexinrelationtogovernmentsecuritiesandwhichwillobtainlicensetoperformGSBenchmarkAdministration.

SECMCNo.11providesfortherulesgoverningtheadministrationofthePhilippinePeso-DenominatedGSBenchmarks.

14 | Tax Bulletin

• AlegalpersonshouldapplyforanAdministratorlicensetoadministertheGSBenchmark;

• ContinuingReportingRequirements:AdministratorsarerequiredtoreporttotheSECanydisruption,businesscontinuityactivation,oranyothereventthatcouldaffecttheintegrityofthebenchmarkdeterminationprocess;

• NotificationRequirement:Administratorsarerequiredtoreportsuspectedmarketmanipulationofthebenchmark;

• Administratorsareprimarilyresponsibleforallaspectsofthebenchmarkdeterminationprocessandarerequiredtodiscloseanyexistingorpotentialconflictsofinterest;

• Thedataonwhichthebenchmarkisconstructedshouldhavebeenbasedonsufficientandreliablyrepresentativeinterestmeasuredbythebenchmark;

• Themethodologyshouldbedocumentedandpublished;itshouldprovidesufficientdetailtoallowstakeholderstounderstandhowthebenchmarkisderived;

• Thereshouldbeappropriateinternalcontrolsoverdatacollectedfromexternalsources;and

• TheAdministratorisrequiredtoestablishacomplaintsprocedure,appointanauditandcompliancereviewerandmaintainanaudittrail.

(Editor’s Note: Published in the ManilaBulletin & the ManilaTimes on 31 August 2018)

SEC Memorandum Circular No. 12 series of 2018 dated 22 August 2018

Inrecognitionoftheimportanceofgreenfinanceandtheincreasingdemandforgreeninvestments,thePhilippinesadoptstheASEANGreenBondsStandardssummarizedasfollows:

• ASEANGreenBondscanonlybeissuedbyacorporationincorporatedintheASEANorthegreenprojectisinanASEANcountry.

• ASEANGreenBondsissuancemustoriginatefromanASEANmembercountry.

• TheproceedsofASEANGreenBondsmustbeexclusivelyappliedtofinanceorrefinanceexistingeligibleGreenProjects.

• Tobeeligible,adesignatedgreenprojectmusthaveclearenvironmentalbenefitsthathavebeenassessedandquantified.

(Editor’s Note: Published in the ManilaBulletin and the ManilaStandard on 11 September 2018)

SECMCNo.12providestheguidelinesontheissuanceofgreenbondsundertheASEANGreenBondsStandardsinthePhilippines.

15Tax Bulletin |

SEC-OGC Opinion No. 18-17 dated 5 September 2018

Facts:

On22May2013,theSECreleasedMemorandumCircularNo.08-13ortheGuidelinesonCompliancewiththeFilipino-ForeignOwnershipRequirementsintheConstitutionand/orCorporationsEngagedinNationalizedand/orPartlyNationalizedActivities.

UCo.,aninvestmenthouse,hasthefollowingownershipstructure:

100%ofthepreferrednon-votingsharesofUBSPhilippines-heldbyUBSAG,aSwissnational.40%ofcommonvotingshares-Filipino60%ofcommonvotingshares-Foreign

Issues:

WhetheraninvestmenthouseiscoveredunderMCNo.08-13andwhetherthereisaneedtoreviseoramendthecurrentownershipstructureofUBSPhilippinespursuanttoMCNo.08-13.

Ruling:

No,UCo.neednotreviseoramenditscurrentownershipstructurepursuanttoMCNo.08-13.

Sec.2ofMCNo.08-13excludesfromitscoveragecorporationscoveredbyspeciallaws.MCNo.08-13specificallyidentifiedtheLendingCompanyRegulationActof2000andtheFinancingCompanyActof1998,andtheInvestmentHousesLaw.

UndertheInvestmentHousesLaw,atleast40%ofthevotingstockofaninvestmenthouseshallbeownedbycitizensofthePhilippines.Indeterminingcompliancewiththenationalityrequirement,thebasisisonlythevotingstockandnotthetwo-tieredtestmentionedinMCNo.08-13(i.e.thetotalnumberofoutstandingsharesofstockentitledtovoteintheelectionofdirectorsandthetotalnumberofoutstandingsharesofstock,whetherornotentitledtovote).

BSP Issuances

BSP Circular No. 1012 dated 12 September 2018

• ThefollowingRevisedRulesofProcedureonAdministrativeCasesInvolvingDirectorsandOfficersofBSP-SupervisedFinancialInstitutions(theRules)wereapprovedbytheMonetaryBoardpursuanttoSection37ofRepublicActNo.7653(The New Central Bank Act),andSections16and66ofRepublicActNo.8791(The General Banking Law of 2000).

• Section1ofRuleIontitleprovidesthattheRulesshallbeknownastheBangkoSentralngPilipinas(BSP)RevisedRulesofProcedureonAdministrativeCasesInvolvingDirectorsandOfficersofBSP–SupervisedFinancialInstitutions.

CircularNo.1012providesforRevisedRulesofProcedureonAdministrativeCasesinvolvingDirectorsandOfficersofBSP-SupervisedFinancialInstitutions.

Thenationalityrequirementforaninvestmenthouserefersonlytothestocksentitledtovote.

16 | Tax Bulletin

• Section2ofRuleIonapplicabilityprovidesthattheRulesshallapplytoadministrativecasesfiledwiththeOfficeofSpecialInvestigation(OSI),BSP,involvingdirectorsandofficersofBSP-supervisedfinancialinstitutions,andadministrativecasesarisingoutofthefact-findinginvestigationsconductedbytheOSI.TheRulesshallnotapplytocomplaintsagainstBSP-supervisedfinancialinstitutions(asajuridicalentity),andsupervisoryandenforcementactions.

• Section3ofRuleIprovidesthattheproceedingsundertheRulesshallbesummaryinnatureandthatthepertinentprovisionsoftheRulesofCourtmaybeappliedsuppletorily.

• Section4ofRuleIonappearanceofcounselprovidesthatpartiesmaybeassistedorrepresentedbycounsel.

• Section5ofRuleIonconfidentialityofproceedingsprovidesthattheproceedingsundertheRulesshallbeconfidential,excepttotheextentasmaybeprovidedunderexistinglaws.

• Section6ofRuleIIprovidesthatthetermsintheManualofRegulationsareadoptedintheRules.

• Section7ofRuleIIIoncomplaintprovidesthatthesamemustbeinwriting,andsubscribedandsworntobythecomplainant.Noanonymouscomplaintshallbeentertained.

• Section8ofRuleIIIprovidesthatthecomplaintshallbefiledwithOSI.

• Section9ofRuleIIIoncontentsofthecomplaintprovidesthatthecomplaintshallcontaintheultimatefactsofthecase,andshallincludetheitemsenumeratedinthisSection.

• Section10ofRuleIIIonactiononthecomplaintprovidesthatwhenacomplaintissufficientinformandsubstance,OSIshallissueanoticerequiringtherespondenttofileaswornanswertothecomplaint.Ifotherwise,theOSIshalldismissthecomplaint,withoutprejudice,ortakesuchappropriateactionasmaybewarranted.

• Section11onanswerprovidesthatwithin10daysfromthereceiptofthenoticetofileananswerandacopyofthecomplaint,respondentshallsubmitaswornanswer,copyofwhichshallbefurnishedtothecomplainant.Thefailureoftherespondenttofileananswerwithintheprescribedperiodshallbeconsideredasawaiveroftherespondent’srighttofilethesame,andthecaseshallberesolvedbasedsolelyontheevidencepresentedbythecomplainant.

• Section12ofRuleIIIonprohibitedpleadingsandmotionsenumeratesthefollowingprohibitedpleadingsandmotions,namely,Motiontodismiss(exceptonthegroundoflackofjurisdiction),Motionforbillofparticulars,Motionfortheissuanceofsubpoenaduces tecumand/orad testificandum,provisionalremedies,modesofdiscovery,andsimilarreliefs,Dilatorymotions,andOtherpleadingsormotionsofasimilarnature.

• Section13ofRuleIVonmodesofserviceprovidesthatpleadings,motions,orders,orprocessesmaybemadebypersonaldelivery,registeredmail,courier,orothermodesofservice.

17Tax Bulletin |

• Section14ofRuleIVonothermodesofserviceprovidesthatservicemayalsobemadebyelectronicmailorotherelectronicformthatprovidesarecordofdelivery.

• Section15ofRuleVprovidesforcompletenessofservice.

• Section16ofRuleVontheacquisitionofjurisdictionovertherespondentprovidesthatitisacquiredonceserviceofthenoticetofileanswerandacopyofthecomplaintiscompleted.

• RuleVIoftheRulesonproceedingsbeforethehearingofficercoversthesubmissionofpositionpapers,andcomments,andtheissuanceofclarificatoryorders.

• RuleVIIoftheRulesonresolutionofthecasecoversthesubmissionofreport,issuanceandfinalityofresolution,motionforreconsideration,andenforcement.

• RuleVIIIoftheRulesonappealprovidesthatanappealfromtheresolutionoftheMonetaryBoardmaybefiledbeforetheCourtofAppealswithintheperiodandinthemannerprovidedunderRule43oftheRulesofCourt.Theappealshallnotstaytheenforcementoftheresolutionsoughttobereviewed,unlesstheCourtofAppealsshalldirectotherwiseuponsuchtermsasitmaydeemjust.

• RuleIXonmiscellaneousprovisioncoverstherepeal,separabilityclause,effectivity,andtransitoryprovision.

(Editor’s Note: BSP Circular No. 1012, s. 2018 was published in ThePhilippineStar on 18 September 2018)

BSP Circular No. 1013 dated 17 September 2018

• ThefollowingaretheamendmentstotheprovisionsoftheManualofRegulationsforNon-BankFinancialInstitutions(MORNBFI)ontherulesgoverningprejudicialacts,practicesoromissionsofNon-StockSavingsandLoanAssociations(NSSLA).

• Itemb(1)ofSubsection4184S.1oftheMORNBFIwasamendedtoaddaprovisionthataservicefeeisconsideredunreasonablyhighiftheservicefeerateexceeds50%oftheannualnominalinterestratechargedonaloan.

• Itemb(3)ofSubsection4184S.1oftheMORNBFIwasamendedtoprovidethatnon-disclosuretoborrowersofborrowingcostsshallbeconsideredacts,practices,oromissionsprejudicialtotheinterestofmembers.

• Itemb(4)ofSubsection4184S.1oftheMORNBFIwasamendedtoprovidethatadoptingandimplementingpoliciesthatarediscriminatory(e.g.limitingcapitalcontributionsofmembersthathastheeffectofconcentratingcontroltoaparticularfamily)shallbeconsideredacts,practices,oromissionsprejudicialtotheinterestofmembers.Forthispurpose,afamilyreferstotheemployee-memberand/orretiree-memberandtheirrelativesuptoseconddegreeofconsanguinityoraffinity.

CircularNo.1013providesforAmendmentstotheRulesGoverningPrejudicialActs,Practices,orOmissionsofNSSLA.

18 | Tax Bulletin

• Itemb(5)ofSubsection4184S.1oftheMORNBFIwasamendedtoprovidethatgrantingofunauthorizedcompensationtotrusteesand/orofficersshallbeconsideredacts,practices,oromissionsprejudicialtotheinterestofmembers.Forthispurpose,compensationshallbeconsideredunauthorizedwhennotallowedintheBy-LawsornotapprovedbyauthorizedbodiessuchasthemembersinageneralassemblyortheBoardofTrustees.

• Itemb(6)ofSubsection4184S.1oftheMORNBFIwasamendedtoprovidethatgrantingneworadditionalloanstoborrowerswhohaveinsufficientpayingcapacityorpoorcredithistoryshallbeconsideredacts,practices,oromissionsprejudicialtotheinterestofmembers

• Itemb(7)ofSubsection4184S.1oftheMORNBFIwasamendedtoprovidethatcollectingpaymentsfrommembersevenafterfullpaymentoftheirloans,includingfailuretorefundover-collectionstomembersshallbeconsideredacts,practices,oromissionsprejudicialtotheinterestofmembers.

• Itemb(8)ofSubsection4184S.1oftheMORNBFIwasamendedtoprovidethatchargingand/orpayingmaterialunauthorizeddisbursements,includingexpenses,orengaginginthepracticeofchargingand/orpayingunauthorizeddisbursementsevenifnotmaterialbutwhenaggregated,resultinmaterialfinanciallosstotheNSSLAshallbeconsideredacts,practices,oromissionsprejudicialtotheinterestofmembers.

• Itemb(9)ofSubsection4184S.1oftheMORNBFIwasamendedtoprovidethatallowingtheuseofNSSLA’spropertiesorprivilegeswithoutduecompensationshallbeconsideredacts,practices,oromissionsprejudicialtotheinterestofmembers.

• Subsection4184S.2oftheMORNBFIonenforcementactionswasamendedtoprovide,amongothers,thattheMonetaryBoardmayorderthesuspensionorrevocationofanNSSLA’slicensetooperateassuchiftheprejudicialacts,practices,oromissionsamounttowillfulviolations.Forthispurpose,theact,practice,oromissionisdeemedwillfulif,despiteaBSPdirectivetostopthesaidact,practice,oromission,theNSSLAand/oritstrusteesand/orofficerscontinuetocommitthesameorrelatedacts.Theterm“relatedacts”refertospecificactswhichresultinthesameprejudicialact,practiceoromission.

• ThisCircularshalltakeeffect15daysafteritspublicationeitherintheOfficialGazetteorinanewspaperofgeneralcirculation.

(Editor’s Note: BSP Circular No. 1013, s. 2018 was published in ThePhilippineStar on 24 September 2018)

BSP Circular No. 1014 dated 24 September 2018

• ThefollowingprovisionswerecreatedintheManualofRegulationsforBanks(MORB)toprovidefortherevisedguidelinesfortheCurrencyRateRiskProtectionProgram(CRPP)Facility.

• Section1603oftheMORBwasaddedtoprovidefortheCRPPFacilitywhichisanon-deliverableUSD/PHPforwardcontract(NDF)betweentheBangkoSentralngPilipinasandauniversal/commercialbank(the“Bank”)inresponsetotherequestofbankclientsdesiringtohedgetheireligibleforeigncurrencyobligations.TransactionsundertheCRPPfacilityareconsideredpartofbanks’GenerallyAuthorizedDerivativesActivities(GADA).Moreover,banks’exposuresarisingfromNDFtransactionsundertheCRPPfacilityshallnotbeincludedin

CircularNo.1014providesfortheCRPPFacility.

19Tax Bulletin |

thecomputationoftotalgrossNDFexposuresforthepurposeofdeterminingcompliancewiththelimitprescribedinAppendix101.Inaddition,themarketriskcapitalchargeforthenetopenpositionforNDFsunderthisfacilityshallbecalculatedbyapplyingthestandard125percentmultiplicationfactorinsteadofthe187.5percentfactorprescribedforotherNDFsunderAppendix46.

• Subsection1603.1oftheMORBwasaddedtoprovideforthecoveragethateligibleobligationsundertheCRPPFacilityaretheunhedgedforeigncurrencyobligationsinamountsofnotlessthanUS$50,000.00thatarecurrentandoutstandingasofthedateofapplication.Pastdueforeigncurrencyobligationsarenoteligible.ThemaximumtenoroftheCRPPcontractis90days.Forthispurpose,unhedged obligationsshallrefertothosewithoutoutstandinghedgeeitherthroughforwardcontracts,optionsormatchedforeigncurrencyassets.Partiallyhedgedforeignexchangeobligationsshallbeevaluatedonacase-to-casebasis.

• Subsection1603.2–1603.4oftheMORBwasreserved

• Subsection1603.5oftheMORBwasaddedtoprovidefortheBSP’ssupervisoryenforcementactions.ItstatesthattheBSPreservestherighttodeployitsrangeofsupervisorytoolstopromoteadherencetotherequirementssetforthintheguidelinesandbringabouttimelycorrectiveactionsandcompliance.

• Theterms,conditions,andthereportingrequirementsoftheCRPPFacilitywillbecoveredbyaseparateissuanceontheimplementingguidelinesoftheCRPPFacility.

• TheCircularrepealsCircularNo.470,aswellaspartsofothercircularsinconsistentherewith.

• ThisCircularshalltakeeffect15calendardaysfollowingitspublicationeitherintheOfficialGazetteorinanewspaperofgeneralcirculationinthePhilippines.

(Editor’s Note: No publication yet as of date)

Court Decisions

Consolidated Cases of Confederation for Unity, Recognition and Advancement of Government Employees et al. vs. Commissioner, Bureau of Internal Revenue, et al. and Judge Armando A. Yanga, in his personal capacity and in his capacity as President of the RTC Judges Association of Manila, et al. vs. Hon. Commissioner Kim S. Jacinto-Henares, in her capacity as Commissioner of the Bureau of Internal Revenue SupremeCourt(En Banc)G.R.Nos.213446and213658,promulgated3July2018

Facts:

On20June2014,RespondentCommissionerofInternalRevenue(CIR)issuedRevenueMemorandumOrder(RMO)No.23-2014toclarifytheresponsibilitiesofthepublicsectortowithholdtaxesonitstransactionsascustomer(onitspurchasesofgoodsandservices)andasemployer(oncompensationpaidtoitsofficialsandemployees)undertheTaxCodeandspeciallaws.

Everyformofcompensationforservices,whetherpaidincashorinkind,isgenerallysubjecttoincometaxandconsequentlytowithholdingtax.Thenamedesignatedtothecompensationincomeisimmaterial.

Thus,salaries,wages,emoluments,andhonoraria,allowances,commissions,fees(includingdirector’sfees,ifthedirectoris,atthesametime,anemployeeoftheemployerorthecorporation),bonuses,fringebenefits(exceptthosesubjecttothefringebenefitstaxundertheTaxCode),pensions,retirementpay,andotherincomeofasimilarnature,constitutecompensationincomethataretaxableandsubjecttowithholdingtax.

20 | Tax Bulletin

Petitioner-organizationsandunionsofemployeesfromvariousgovernmentagenciesquestionedtheconstitutionalityoftheRMOandaskedthatparagraphsA,BCandDofSectionIII(enumerationofvariousbenefitsandallowancesofgovernmentemployeeswhichareconsideredcompensationsubjecttoincometax),SectionsIV(enumerationofnon-taxablecompensationincomeofpublicsector),VI(personsresponsibleforwithholding)andVII(penaltyfornon-compliancebythenamedgovernmentofficialsoftheirobligationaswithholdingagents)bedeclarednull,voidandunconstitutional.

PetitionersallegedthattheRMOclassifiedastaxablecompensationvariousallowances,bonuses,andcompensationforservicesgrantedtogovernmentemployeessuchasthoseinthelegislativebranchandjudiciary,whichareconsideredbylawasnon-taxablefringeandde minimisbenefits. Petitionersalsoallegethattheimpositionofwithholdingtaxontheseallowances,bonusesandbenefits,whichhavebeenallottedbytheGovernmenttoitsemployeesfreeoftaxforalongtime,violatestheprohibitiononnon-diminutionofbenefitsunderArticle100oftheLaborCode.

Issue:

ArethequestionedprovisionsofRMONo.23-2014valid?

Ruling:

SectionIII(enumerationofvariousbenefitsandallowancesofgovernmentemployeeswhichareconsideredcompensationsubjecttoincometax)andSectionIV(enumerationofnon-taxablecompensationincomeofpublicsector)ofRMONo.23-2014arevalidanddonotchargeanyneworadditionaltax.

Theprovisionssimplyreinforcetherulethateveryformofcompensationforpersonalservicesreceivedbyallemployeesisdeemedsubjecttoincometaxand,consequently,towithholdingtax,unlessspecificallyexemptedorexcludedbytheTaxCode,andalsothedutyoftheGovernment,asanemployer,towithholdandremitthecorrectamountofwithholdingtaxesdue.

UndertheTaxCode,everyformofcompensationforservices,whetherpaidincashorinkind,isgenerallysubjecttoincometaxandconsequentlytowithholdingtax.Thenamedesignatedtothecompensationincomeisimmaterial.Thus,salaries,wages,emoluments,andhonoraria,allowances,commissions,fees(includingdirector’sfees,ifthedirectoris,atthesametime,anemployeeoftheemployerorthecorporation),bonuses,fringebenefits(exceptthosesubjecttothefringebenefitstaxunderSection33oftheTaxCode),pensions,retirementpay,andotherincomeofasimilarnature,constitutecompensationincomethataretaxableandsubjecttowithholding.

Thetermemployee“coversallemployees,includingofficersandemployees,whetherelectedorappointed,oftheGovernmentofthePhilippines,oranypoliticalsubdivisionthereoforanyagencyorinstrumentality”whileanemployer“embracesnotonlyanindividualandanorganizationengagedintradeorbusiness,butalsoincludesanorganizationexemptfromincometax,suchascharitableandreligiousorganizations,clubs,socialorganizationsandsocieties,aswellastheGovernmentofthePhilippines,includingitsagencies,instrumentalities,andpoliticalsubdivisions.”

21Tax Bulletin |

WhileSectionIIIenumeratescertainallowanceswhichmaybesubjecttowithholdingtax,itdoesnotexcludethepossibilitythattheseallowancemayfallundertheexemptionsinSectionIV.SectionsIIIandIVarticulateingeneralandbroadlanguagetheTaxCodeprovisionsontheformsofcompensationincomedeemedsubjecttowithholdingtaxandthoseexemptedfromincometax.

SectionVII(onpenaltiesfornon-compliancebythenamedgovernmentofficialsoftheirobligationtowithhold)ofRMONo.23-2014isvalidwhileSectionVI(personsresponsibleforwithholding)contravenes,inpart,theTaxCodeprovisionsanditsimplementingrules.

SectionVIIdoesnotdefineacrimeandprescribeapenalty,butsimplymirrorstherelevantprovisionsoftheTaxCodeonpenaltiesforfailureofthewithholdingagenttowithholdandremitcorrectamountoftaxes.

However,withrespecttoSectionVI,theCIRoversteppedtheboundariesofhisauthoritytointerpretprovisionsoftheTaxCode.

TheGovernment,oranyofitspoliticalsubdivisionsoragencies,oranygovernment-ownedor–controlledcorporation(GOCC),asanemployer,isconstitutedbylawasthewithholdingagent,mandatedtodeduct,withholdandremitthecorrectamountoftaxesonthecompensationincomereceivedbyitsemployees.

ThewithholdingtaxregulationsidentifytheProvincialTreasurerinprovinces,theCityTreasurerincities,theMunicipalTreasurerinmunicipalities,BarangayTreasurerinbarangays,TreasurersofGOCCs,andtheChiefAccountantoranypersonholdingsimilarpositionandperformingsimilarfunctioninnationalgovernmentofficesaspersonsrequiredtodeductandwithholdtheappropriatetaxesontheincomepaymentsmadebythegovernment.

NowhereintheTaxCodeorintheregulationswouldonefindtheProvincialGovernor,Mayor,BarangayCaptainandtheHeadofGovernmentOfficeorthe“Officialholdingthehighestposition”inanAgencyorGOCCasoneoftheofficialsrequiredtodeduct,withholdandremitthecorrectamountofwithholdingtaxes.SectionVIofRMONo.23-2014isdeclarednullandvoidinsofarasitnamestheseofficersaspersonsrequiredtowithholdandremittaxes.

Macario Lim Gaw, Jr. vs. Commissioner of Internal Revenue (CIR)SupremeCourt(FirstDivision)G.R.No.222837,promulgated23July2018

Facts:

MacarioLimGaw,Jr.sold10parcelsoflandforwhichhepaidCapitalGainsTax(CGT)andDocumentaryStampTax(DST).TheBIRissuedthecorrespondingCertificatesAuthorizingRegistrationandTaxClearanceCertificates.

Subsequently,theCommissionerofInternalRevenue(CIR)opinedthatGawwasnotliableforthe6%CGTbutforthe32%regularincometaxand12%ValueAddedTax(VAT)becausethepropertiessoldwereordinary,andnotcapitalassets.TheCIRfoundthatGawmisdeclaredhisincome,misclassifiedtheproperties,andusedmultipletaxidentificationnumberstoavoidbeingassessedthecorrecttaxes.

TheCIRissuedaLetterofAuthoritytoauditGaw’staxaccountandalsofiledaJointComplaintaffidavitfortaxevasionbeforetheDepartmentofJustice(DOJ).

Ataxevasioncasefiledbythegovernmentagainstanerringtaxpayerhas,foritspurpose,theimpositionofcriminalliability.Ontheotherhand,ataxpayer’sPetitionforReviewtoquestionadeficiencytaxassessmentisintendedtopreventitfrombecomingfinalandexecutory.AcquittalofthetaxpayerinthecriminalcasewillnotresultinthedismissalofthePetitionforReview,whichisnotdeemedinstitutedwiththecriminalcasefortaxevasion.

Whatisdeemedinstitutedwiththecriminalactionisonlytheactiontorecovercivilliabilityarisingfromthecrime.Civilliabilityarisingfromadifferentsourceofobligation,suchaswhentheobligationiscreatedbylaw,isnotdeemedinstitutedwiththecriminalaction.

22 | Tax Bulletin

TheDOJfiledtwocriminalinformationsfortaxevasionagainstGaw.Halfwaythroughtrial,theCIRissuedherFinalDecisiononDisputedAssessment(FDDA),assessingGawdeficiencyincometaxandVATfortaxableyears2007and2008.

GawfiledaPetitionforReviewwiththeCourtofTaxAppeals(CTA)forthe2007deficiencytaxassessment.

Forthe2008deficiencytaxassessment,whichinvolvedthesametaxliabilitiessoughttoberecoveredinthependingcriminalcase,GawfiledamotionwiththeCTAtoclarifywhetherhehastofileaseparatepetitiontoquestionthedeficiencyassessment.

TheCTAheldthattherecoveryofthecivilliabilitieswasdeemedinstitutedwiththeconsolidatedcriminalcases,withoutprejudicetotherightofGawtoavailofwhateveradditionallegalremedyhemayhavetopreventthe2008FDDAfrombecomingfinalandexecutory.GawfiledaPetitionforReviewAd Cautelam(withaMotionforConsolidationwiththeCTAcriminalcases)docketedasCTACaseNo.8503,uponwhichtheclerkofcourtassessedzerofilingfee.

TheCTAacquittedGawinthecriminalcasesanddirectedthelitigationofthecivilaspectinthetaxevasioncase.TheCIRaskedforthedismissalofthepetitioninCTACaseNo.8503becausetheCTAFirstDivisionlackedjurisdictionduetoGaw’snon-paymentoffilingfees,whichtheCTAgranted.Hence,GawappealedtotheSupremeCourt. Issues:

1. Isthecivilactiontoquestionthe2008FDDAdeemedinstitutedwiththecriminalcasefortaxevasion?

2. IstheCTAcorrectindismissingthecaseforfailureofGawtopaydocketfees?

Rulings:

1. No,thecivilactionfiledbyGawtoquestionthe2008FDDAisnotdeemedinstitutedwiththecriminalcasefortaxevasion.

Whatisdeemedinstitutedwiththecriminalactionisonlytheactiontorecovercivilliabilityarisingfromthecrime.Civilliabilityarisingfromadifferentsourceofobligation,suchaswhentheobligationiscreatedbylaw,isnotdeemedinstitutedwiththecriminalaction.

Thetaxpayer’sobligationtopaythetaxisanobligationcreatedbylawanddoesnotarisefromtheoffenseoftaxevasionandassuch,thesameisnotdeemedinstitutedinthecriminalcase.

Anacquittalinacriminalcasecannotoperatetodischargethetaxpayerfromthedutyofpayingthetaxwhichthelawrequirestobepaidsincethatdutyisimposedbystatutepriorto,andindependentlyofanyattemptbythetaxpayertoevadepayment.

Whilethetaxevasioncaseispending,theBIRisnotprecludedfromissuinganFDDA,suchasinthepresentcase.Topreventtheassessmentfrombecomingfinal,executoryanddemandable,thelawallowsthetaxpayertofileaPetitionforReviewwiththeCTAwithin30daysfromreceiptofthedecisionortheinactionoftheCIR.

23Tax Bulletin |

Thetaxevasioncasefiledbythegovernmentagainsttheerringtaxpayerhas,foritspurpose,theimpositionofcriminalliability.Ontheotherhand,thePetitionforReviewfiledbyGawwasaimedtoquestionthe2008FDDAandtopreventitfrombecomingfinal.Hence,thePetitionforReviewAd Cautelam is notdeemedinstitutedwiththecriminalcasefortaxevasion.

2. No.ThecaseshouldnothavebeendismissedbytheCTA.

Whilethecourtacquiresjurisdictionoveracaseonlyuponthepaymentoftheprescribeddocketfees,itsnon-paymentatthetimeoffilingtheinitiatorypleading,thePetitionforReviewinthiscase,doesnotautomaticallycauseitsdismissalsolongasthedocketfeesarepaidwithinareasonableperiod,andthatthepartyhadnointentiontodefraud.

GawreliedingoodfaithontheCTA’sadvicethatheisnolongerrequiredtopaythedocketfees.TheCTAshouldhavedirectedtheclerktoassessthecorrectdocketfeesandorderedGawtopaytheamountwithinareasonableperiod.

TheissueonwhetherthetransactionisoneinvolvingcapitalorordinaryassetsshouldbeproperlyresolvedbytheCTAsincetheSupremeCourtisnotatrieroffacts.ThecaseisreturnedtotheCTAforfurtherproceedings.

Commissioner of Internal Revenue vs. Coral Bay Nickel CorporationCTA(En Banc)CaseNo.1652promulgated14August2018

Facts:

PetitionerCIRassessedRespondentCoralBayNickelCorporation(CBNC)for,amongothers,allegeddeficiencyfinalwithholdingtax(FWT)for2007.CBNCprotestedtheassessment.UpontheCIR’sdenialofitsprotest,CBNCfiledPetitionforReviewwiththeCTA.

AttheCTA,CBNCarguedthatthewaiverisnotvalid.CBNCexecutedawaiveron20April2010extendingtheperiodtoassessuntil31December2010,whichwasacceptedbytheBIRon30April2010.Itexecutedasecondwaiveron12November2010andthereafter,3morewaiversextendingtheperiodtoassessuntil31December2011,31October2012and30June2013.AllwaiverswereexecutedbyCBNC’sPresident.

CNBCarguedthattheCIR’srighttoassessthedeficiencyFWTforJanuarytoMarch2007hadprescribedasithadonlyuntil15February2010,10March2010,and16April2010toassessfordeficiencyEWTforJanuarytoMarch2007.ItalsoinsistedthatapriorTaxTreatyReliefApplicationisnotrequiredtoavailofthepreferentialratesundertheapplicabletaxtreaty,pursuanttotheSupremeCourt’srulinginDeutsche Bank AG Manila Branch vs. CIR, GR 188550 promulgated on 19 August 2013.

TheBIRcounteredthatitsrighttoassesshasnotprescribed,allegingthatCBNCfiledafalseorfraudulentFWTreturns,justifyingtheapplicationofthe10-yearprescriptiveperiod.ItalsoarguedthatCBNCisestoppedfromquestioningthevalidityofthewaiveritvoluntarilyexecuted,citingtheSupremeCourt’sdecisioninCIR vs. Next Mobile, Inc., GR 212825 promulgated on 7 December 2015.ItlikewisetookthepositionthattheperiodoflimitationtoassessandcollectdeficiencytaxesunderSection203oftheNIRConlyextendstoassessmentofallinternalrevenuetaxesandnotfromassessmentofpenaltiesonawithholdingagentforfailuretoremittheproperamountoftaxeswithheld.

The3-yearprescriptiveperiodmaybeextended,ifawaiverwasdulyexecutedbeforeitsexpiration.

24 | Tax Bulletin

TheCTAThirdDivisioncancelledandsetasidetheFDDAfordeficiencyFWT,promptingtheCIRtoelevatethecasetotheCTAEn Banc.

Issues:

1. HastherightoftheBIRtoassessprescribed?

2. Doestheperiodoflimitationapplytowithholdingtaxes?

3. IsCBNCliabletoFWT?

Ruling:

1. Yes,theBIR’srighttoassessfordeficiencyFWTforJanuarytoMarch2007hasprescribed.The3-yearprescriptiveperiodmaybeextendedifawaiverwasdulyexecutedbeforeitsexpiration.Thefirstwaiverbecameeffectiveonlyon30April2010whenthewaiverwasacceptedbytheBIR.ThelastdaytoassessthedeficiencyFWTforMarch2007wason16April2010.

The“in pari delicto”principleintheNext Mobilecase,whereitwasheldthatifboththeBIRandthetaxpayerareequallyatfaultinexecutingandacceptingdefectivewaiversthenthetaxpayerwillbeartheconsequenceofsuchdeliberateact,isnotapplicableinthiscase.CBNCisnotestoppedfromquestioningthevalidityofthewaiverasitwasnotremissinassertingitsright.

2. Yes.Inaplethoraofcases,theSupremeCourthasconsistentlyanduniformlyappliedthe3-yearprescriptiveperiodontheassessmentofwithholdingtaxes,withoutqualificationordistinction.

SinceSection203oftheNIRCappliestoallinternalrevenuetaxesandthatnorestrictionorqualificationisindicatedastoitsapplicationoncertaintaxes,thereisnobasisnottoapplytheruleonprescriptiontowithholdingtaxes.

3. No.CBNCcorrectlyappliedthepreferentialtaxratesonitsincomepaymentstoJapanesenon-residentforeigncorporationspursuanttothePhilippines-JapanTaxTreaty.ApriorapplicationfortaxtreatyreliefisnotrequiredbeforeataxpayercanavailofthepreferentialratesfollowingtheDeutscheBankcase.

FCF Minerals Corporation vs. Commissioner of CustomsCTA(En Banc)CaseNo.1620promulgated14August2018

Facts:

PetitionerFCFMineralsCorporation(FMC)filedwithRespondentCommissionerofCustomsanapplicationforrefundofallegederroneouslypaidValue-AddedTax(VAT)andcustomsdutiesandfeesonitsimportationofcapitalequipment.FMCenteredintoaFinancialorTechnicalAssistanceAgreement(FTAA)withthegovernmentinSeptember2009forthegold-molybdenumprojectinNuevaVizcayapursuanttoRepublicAct7942orthePhilippineMiningAct.

FMCarguedthatitisnotliabletopayVATandcustomsdutiesandfeesonimportedcapitalequipment,citingRA7942whichprovidesthatthe“governmentshare”intheFTAAsofminingcompanies,whichincludesVATandcustomsdutieson

FTAAcontractorsareliabletopayVATonimportedgoodsandservicesandcustomsdutiesandfeesonimportedproductsonlyaftertheirrecoveryperiod.

25Tax Bulletin |

importationofcapitalgoods,shallbecollectedonlyaftertheFTAAcontractorhasfullyrecovereditspre-operatingexpensesandexplorationanddevelopmentexpenditures.

ItalsocontendedthatRevenueMemorandumCircular17-2013whichrequiresFTAAcontractorstopaynationaltaxesduringandaftertheirrecoveryperiodviolatesRA7942.

DuetotheCOC’sinactionontherefundapplication,FMCfiledaPetitionforReviewattheCTA.

TheCTAThirdDivisionruledthatVATonimportedgoodsandservicesandcustomsdutiesandfeesonimportedproductsmustbepaidonlyaftertherecoveryperiod.However,theThirdDivisionheldthatFMCfailedtoestablishthatthetaxesforrefundwerepaidduringitsrecoveryperiodorthatithasnotyetrecovereditspre-operatingexpenses.

UponthedenialofitsMotionforReconsideration,FMCfiledaPetitionforReviewattheCTAEn Banc.

Issue:

IsFMCentitledtorefundtheVATandcustomsdutiesandfeespaidduringitsrecoveryperiod?

Ruling:

Yes.Thetaxesanddutiescollectedduringtherecoveryperiodareeligibleforrefund.VATonimportedgoodsandservicesandcustomsdutiesandfeesonimportedproductsmustbepaidonlyaftertherecoveryperiod,asprovidedunderDepartmentofEnvironmentandNaturalResources(DENR)AdministrationOrder(DAO)2007-12.

Therecoveryperiodisforamaximumof5yearsoratadatewhentheaggregateofthenetcashflowsfromtheminingoperationsisequaltotheaggregateofitspre-operatingexpenses,reckonedfromthedateofcommencementofcommercialproduction,whichevercomesfirst.

AlthoughtheFTAAwassignedin2009,theDeclarationofMiningProjectFeasibility(DMPF)wasapprovedonlyon18October2011.TheshipmentsthatwereerroneouslysubjectedtoVATweremadein2013.Itwasonlyon9September2016or5yearsaftertheDMPFand3yearsaftertheshipments,thattheDeclarationofCommencementofCommercialOperations(DCCO)wasfiledbyFMC.TheCTAEn Bancruledthat9September2016isnoteventhestartoftherecoveryperiodasthiswasonlythefilingoftheDCCOandnotyetapprovedbytheRegionalOffice.

TheCTAEn BancheldthatwiththesubmissionoftheDCCO,itwasestablishedthattheperiodtocollecttaxeshasnotyetbegunascommercialoperationshavenotevenstarted.ThecasewasremandedtotheCTAThirdDivisionforfurtherproceedingstodetermineandruleonthemeritsoftherefundclaim.

26 | Tax Bulletin

Commissioner of Internal Revenue vs. G & W Architects, Engineers & Project Development Consultants Co.CTA(En Banc)CaseNo.1449promulgated29August2018

Facts:

PetitionerCIRassessedRespondentG&WArchitects,EngineersandProjectConsultants,Co.(G&W)forallegeddeficiencyEWTandDSTfor2004coveringthetransferof340unitsinfourcondominiumprojects.G&WprotestedtheassessmentbasedonfourBIRrulingsissuedbetween2003and2007,wheretheBIRconfirmedthatits“Build-To-Own”or“Build-Your-Own”schemeisnotataxabletransactionasitdoesnotconstituteasaleordispositionofrealproperty.Underthearrangement,unitownerspooltheirfundsfortheconstructionofcondominiumunitsandexecutethefollowingagreements:

a. ContracttoManageandExecutetheConstructionbetweenG&Wandtheunitowners;

b. TrustAgreementestablishedbytheunitownersnamingatrusteetoholdintrustthepooledfundsoftheunitownersandthelandwheretheprojectwillbelocated;and,

c. DepositoryandDisbursingAgreementsbetweenthetrusteeandtheunitowners.

AstheCIRfailedtoactontheprotest,G&WfiledPetitionsforReviewwiththeCTA.

AttheCTA,theCIRallegedthatundertheso-calledco-development/building-to-own/build-your-ownandsimilarschemes,thedevelopersimplymadeitappearthatitmerelymanagedtheconstructionofthecondominiumprojectsandthatthefundsascontributedbytheindividualinvestorsweremanagementfeesonly.Theassignmentanddeliveryofthedevelopedunitstoindividualinvestorsweresupposedlynottaxablebeingmerelyatransferofpropertyheldintrustbythetrusteefortheindividualtrustors.TheCIRclaimsthatthebuild-to-ownconceptisconsideredpre-sellingthatshouldhavebeensubjectedtoEWTandDST.TheCIRalsonotedthatitissuedRMC55-2010statingthatG&Wmisrepresentedfactsintherequestforruling,declaredtherulingsasvoid,andorderedataxinvestigation.

TheCTAFirstDivisionruledthatthetransactionbetweenG&Wandtheunitownerswasforasaleofservices,notasaleofproperty.AsexplainedbytheDivision,G&Wonlyearnedfeesforthemanagementandconstructionoftheunits.AsG&Whadnocompletecontroloverthefunds,nopartofsuchfundscanbeconsideredaspaymentforthetransferofthecondominiumunitsfromwhichtheassessedEWTcanbededucted.

A“Build-To-Own”or“Build-Your-Own”schemeisnotasaleofrealpropertythatissubjecttoEWTandDST.

27Tax Bulletin |

TheCTAEn BancsubsequentlyheldthatG&Wisnotmerelytheprojectmanagerofthecondominiumprojectsbuttheownerthereof,whoisliableforEWTandDST.G&W’sclaimthatitismerelyaprojectmanagerisbeliedbyitsownevidence,particularlytheContracttoManageandExecutetheConstruction,whichprovidesthatG&Whastheauthoritytoterminatethecontractinanyoftheeventsofdefaultandidentifyasubstituteclientorbuyerwhowillassumethecorrespondingremainingobligation.

G&WfiledaMotionforReconsiderationofthedecisionoftheCTAEn Banc.

Issue:

Isthe“Build-To-Own”or“Build-Your-Own”schemeconsideredasaleofrealpropertythatissubjecttoEWTandDST?

Ruling:

No.Thetransactionwasforasaleofservicestoclients,notasaleofproperty.G&Wmerelyearnedprofessionalfeesequivalentto4%oftheconstructionfunding.IntheAmendedDecision,theCTAEn BancheldthatthetrueintentofthepartiesisclearlyexpressedinthecontractsandthereisnothingtoshowthatG&Wwouldbethelawfulownerofthecondominiumprojectsandthelandonwhichthesewerebuilt.G&Wmerelyactsforandonbehalfofitsclientswheneveritexercisesitsobligationsasprojectmanager,trusteeandattorney-in-factofitsclients.

AccordingtotheCTAEn Banc,itcanbegatheredthatwhileallnecessarycontractsand/ordocumentsarisingoutoforasaconsequenceoftheconstructionoftheprojectmayhavebeenexecutedbyandinthenameofG&W,theexecutionshallbeunderstoodtobeforandonbehalfoftheclients.

UnderSection57oftheNIRCandRevenueRegulations2-98,thewithholdingagentisresponsibletofilethereturn,withholdthetaxandremitthesametotheBIR.SinceG&Wisnotawithholdingagent,itcannotbeheldliableforthenon-filingofthewithholdingtaxes.Further,noevidencewaspresentedtoprovethattheentirecontractpricewaspaidtoG&W,ifitisindeedtheseller.

(Editor’s Note: The CTA En Banc voted 4-4 with Presiding Justice Roman G. Del Rosario dissenting on the amended decision)

28 | Tax Bulletin

About SGV & Co.SGV is the largest professional services firm in the Philippines that provides assurance, tax, transaction and advisory services. The insights and quality services we deliver help build trust and confidence in the capital markets and in economies the world over. We develop outstanding leaders who team to deliver on our promises to all of our stakeholders. In so doing, we play a critical role in building a better working world for our people, for our clients and for our communities. SGV & Co. is a member firm of Ernst & Young Global Limited.

EY refers to the global organization, and may refer to one or more, of the member firms of Ernst & Young Global Limited, each of which is a separate legalentity. Ernst & Young Global Limited, a UK company limited by guarantee, does not provide services to clients.

For more information about our organization, please visit www.ey.com/PH.

© 2018 SyCip Gorres Velayo & Co.All Rights Reserved.APAC No. 10000367Expiry date: no expiry

SGV |Assurance|Tax|Transactions|Advisory

SGV & Co. maintains offices in Makati, Cebu, Davao, Bacolod, Cagayan de Oro, Baguio, General Santos and Cavite.

For an electronic copy of the Tax Bulletin or for further information about Tax Services, please visit our websitewww.ey.com/ph

We welcome your comments, ideas and questions. Please contact Victor C. De Dios via e-mail at [email protected] or at telephone number 8910307 loc. 7929 andReynante M. Marcelo via e-mail at [email protected] or at telephone number 894-8335 loc. 8335.

This publication contains information in summary form and is therefore intended for general guidance only. It is not intended to be a substitute for detailed research or the exercise of professional judgment. Neither SGV & Co. nor any other member of the global Ernst & Young organization can accept any responsi-bility for loss occasioned to any person acting or refraining from action as a result of any material in this publication. On any specific matter, reference should be made to the appropriate advisor.