IV. Introduction to WTO- Law 1. The WTO at a glance 2. Principles of non-discrimination 3. Rules on...

33

IV. Introduction to IV. Introduction to WTO-Law WTO-Law 1. 1. The WTO at a glance The WTO at a glance 2. 2. Principles of non- Principles of non- discrimination discrimination 3. 3. Rules on Market Access Rules on Market Access 4. 4. Rules on unfair Trade Rules on unfair Trade 5. 5. Exceptions from the WTO- Exceptions from the WTO- System

-

Upload

annice-reeves -

Category

Documents

-

view

237 -

download

0

Transcript of IV. Introduction to WTO- Law 1. The WTO at a glance 2. Principles of non-discrimination 3. Rules on...

IV. Introduction to WTO-IV. Introduction to WTO-LawLaw

1.1. The WTO at a glanceThe WTO at a glance

2.2. Principles of non-discriminationPrinciples of non-discrimination

3.3. Rules on Market AccessRules on Market Access

4.4. Rules on unfair TradeRules on unfair Trade

5.5. Exceptions from the WTO-Exceptions from the WTO-SystemSystem

The agreement provides a common The agreement provides a common institutional institutional framework framework for the conduct of international trade for the conduct of international trade relations. Contrary to its predecessor the WTO is a relations. Contrary to its predecessor the WTO is a permanent organisationpermanent organisation which benefits from a legal which benefits from a legal personality.personality.

Objectives of the WTOObjectives of the WTO Raising standards of livingRaising standards of living Ensuring full employment and a growing volume of real income and effective demandEnsuring full employment and a growing volume of real income and effective demand Expanding the production of trade in goods and servicesExpanding the production of trade in goods and services Sustainable development and protection of the environmentSustainable development and protection of the environment Needs of developing countriesNeeds of developing countries

Functions of the WTOFunctions of the WTO Facilitate the implementation, administration and operation of the various trade agreementsFacilitate the implementation, administration and operation of the various trade agreements Provide a forum for multilateral trade negotiationsProvide a forum for multilateral trade negotiations Resolve trade disputes (DSB)Resolve trade disputes (DSB) Review national trade policies (TPRM)Review national trade policies (TPRM) Cooperate with IOCooperate with IO

1. The WTO at a glance1. The WTO at a glance

Structure of the WTO Structure of the WTO © www.wto.org© www.wto.org

Multilateral agreements on trade in goodsMultilateral agreements on trade in goods:: the the General Agreement on Tariffs and Trade 1994 General Agreement on Tariffs and Trade 1994 ('GATT' 1994) ('GATT' 1994)

(which included the GATT 1947); (which included the GATT 1947); the Agreement on Agriculture; the Agreement on Agriculture; the Agreement on the Application of Sanitary and Phytosanitary the Agreement on the Application of Sanitary and Phytosanitary

Measures; Measures; the Agreement on Textiles and Clothing; the Agreement on Textiles and Clothing; the the Agreement on Technical Barriers to TradeAgreement on Technical Barriers to Trade; ; the Agreement on Trade-Related Investment Measures; the Agreement on Trade-Related Investment Measures; the the Agreement on Anti-Dumping MeasuresAgreement on Anti-Dumping Measures; ; the Agreement on Customs Valuation; the Agreement on Customs Valuation; the Agreement on Preshipment Inspection; the Agreement on Preshipment Inspection; the Agreement on Rules of Origin; the Agreement on Rules of Origin; the Agreement on Import Licensing Procedures; the Agreement on Import Licensing Procedures; the the Agreement on Subsidies and Countervailing MeasuresAgreement on Subsidies and Countervailing Measures; ; the the Agreement on SafeguardsAgreement on Safeguards. .

Multilateral agreement on Trade in Services (GATS)Multilateral agreement on Trade in Services (GATS) Multilateral agreement on Trade-Related aspects of Multilateral agreement on Trade-Related aspects of

Intellectual Property Rights (TRIPS)Intellectual Property Rights (TRIPS)

Plurilateral AgreementsPlurilateral Agreements Agreement on Trade in Civil AircraftAgreement on Trade in Civil Aircraft Agreement on Government ProcurementAgreement on Government Procurement Understanding on Rules and Procedures Understanding on Rules and Procedures

Governing the Settlement of Disputes (DSU)Governing the Settlement of Disputes (DSU) Mechanism for reviewing the trade policies of Mechanism for reviewing the trade policies of

WTO members (TPRM)WTO members (TPRM)General rules (e.g.

scope, functions, organisation,

accession) DSU, TPRM

GATT+ special agreements on agriculture, dumping, subsidies

GATS TRIPS

Plurilateral agreements: public procurement, civil aircraft

2. Principles of non-2. Principles of non-discriminationdiscrimination

2.1. Overview2.1. Overview Non-discriminationNon-discrimination is the is the key concept of WTO-law key concept of WTO-law and and

policy:policy: Discriminations are an important contributing cause of economic crisesDiscriminations are an important contributing cause of economic crises Discrimination breeds resentments among countries, manufacturers, Discrimination breeds resentments among countries, manufacturers,

traders, workers and poisons international relations and/or may lead to traders, workers and poisons international relations and/or may lead to conflictconflict

Discrimination makes no or scant economic sense, since it distorts the Discrimination makes no or scant economic sense, since it distorts the markets in favour of products or services that may be more expensive markets in favour of products or services that may be more expensive and of a lesser quality. and of a lesser quality.

Two main principles Two main principles of non-discrimination (between and of non-discrimination (between and against other countries) concerning trade in goods and services:against other countries) concerning trade in goods and services:

1.1. MFNMFN: most-favoured-nation treatment obligation : most-favoured-nation treatment obligation (2.2.)(2.2.)

2.2. National treatment obligation National treatment obligation (2.3.)(2.3.)

2.2. MFN-principle2.2. MFN-principle2.2.1. Overview2.2.1. Overview Cornerstone and one of the pillars of the WTO trading system Cornerstone and one of the pillars of the WTO trading system

(Appellate Body, (Appellate Body, EC-Tariff Preferences, EC-Tariff Preferences, para 101)para 101) Main Provision: Main Provision: Article I GATT ‘94 (General Most-Favoured-Nation Article I GATT ‘94 (General Most-Favoured-Nation

Treatment, s also II GATS and Art 4 TRIPS): Treatment, s also II GATS and Art 4 TRIPS):

““1. With respect to customs duties and charges of any kind imposed on 1. With respect to customs duties and charges of any kind imposed on or in connection with importation or exportation or imposed on the or in connection with importation or exportation or imposed on the international transfer of payments for imports or exports, and with international transfer of payments for imports or exports, and with respect to the method of levying such duties and charges, and with respect to the method of levying such duties and charges, and with respect to all rules and formalities in connection with importation and respect to all rules and formalities in connection with importation and exportation, and with respect to all matters referred to in paragraphs 2 exportation, and with respect to all matters referred to in paragraphs 2 and 4 of Article III, and 4 of Article III, any any advantage, favour, privilege or immunityadvantage, favour, privilege or immunity granted by any contracting party to any granted by any contracting party to any productproduct originating in originating in or destined for any other country shall be or destined for any other country shall be accorded immediately accorded immediately and unconditionally and unconditionally to the like product originating in or to the like product originating in or destined for the territories of all other contracting partiesdestined for the territories of all other contracting parties.”.”

Further provisions Further provisions of GATT ‘94 requiring MFN- or MFN-like treatment:of GATT ‘94 requiring MFN- or MFN-like treatment: Art III (7) (internal quantitative regulations), Art V (freedom of transit), Art III (7) (internal Art III (7) (internal quantitative regulations), Art V (freedom of transit), Art III (7) (internal

quantitative regulations), Art V (freedom of transit), Art IX (1) (marking requirements)quantitative regulations), Art V (freedom of transit), Art IX (1) (marking requirements)

Art. I:1 prohibits Art. I:1 prohibits discriminationdiscrimination betweenbetween like products originating in, like products originating in, or destined for, different countries. Purpose: or destined for, different countries. Purpose: equality of opportunity equality of opportunity to import from, or to export to, all WTO-membersto import from, or to export to, all WTO-members. S also . S also Appellate Body in Appellate Body in EC-Bananas III, EC-Bananas III, para 190: “The essence of the non-para 190: “The essence of the non-discrimination obligations is that like products should be treated discrimination obligations is that like products should be treated equally irrespective of their origin. As no participant disputes that all equally irrespective of their origin. As no participant disputes that all bananas are like products, the non-discrimination provisions apply to bananas are like products, the non-discrimination provisions apply to all imports of bananas, irrespective of whether and how a Member all imports of bananas, irrespective of whether and how a Member categorizes or subdivides these imports for administrative or other categorizes or subdivides these imports for administrative or other reasons.”reasons.”

Art. I:1 covers not only in law/de jure discrimination but also in Art. I:1 covers not only in law/de jure discrimination but also in fact/de fact/de facto discrimination. facto discrimination. Even measures that are “Even measures that are “origin neutralorigin neutral” can ” can give certain countries more opportunity to trade than others and can give certain countries more opportunity to trade than others and can therefore be in violation of Art. I:1.therefore be in violation of Art. I:1.

Example: Example: EEC-Imports of Beef: EEC-Imports of Beef: An EC-regulation was making the An EC-regulation was making the suspension of an import levy conditional (only) on the production of a suspension of an import levy conditional (only) on the production of a certificate of authenticity. Formally speaking there were no restrictions certificate of authenticity. Formally speaking there were no restrictions on the origin of beef, the regulation was de jure origin neutral. The on the origin of beef, the regulation was de jure origin neutral. The GATT-Panel found that this regulation was nevertheless GATT-Panel found that this regulation was nevertheless inconsistentinconsistent with the with the MFN-obligationMFN-obligation of Art. I:1 after it was established that the of Art. I:1 after it was established that the only certifying agencyonly certifying agency authorised to produce such a certificate of authorised to produce such a certificate of authenticity was authenticity was an agency in the USAan agency in the USA..

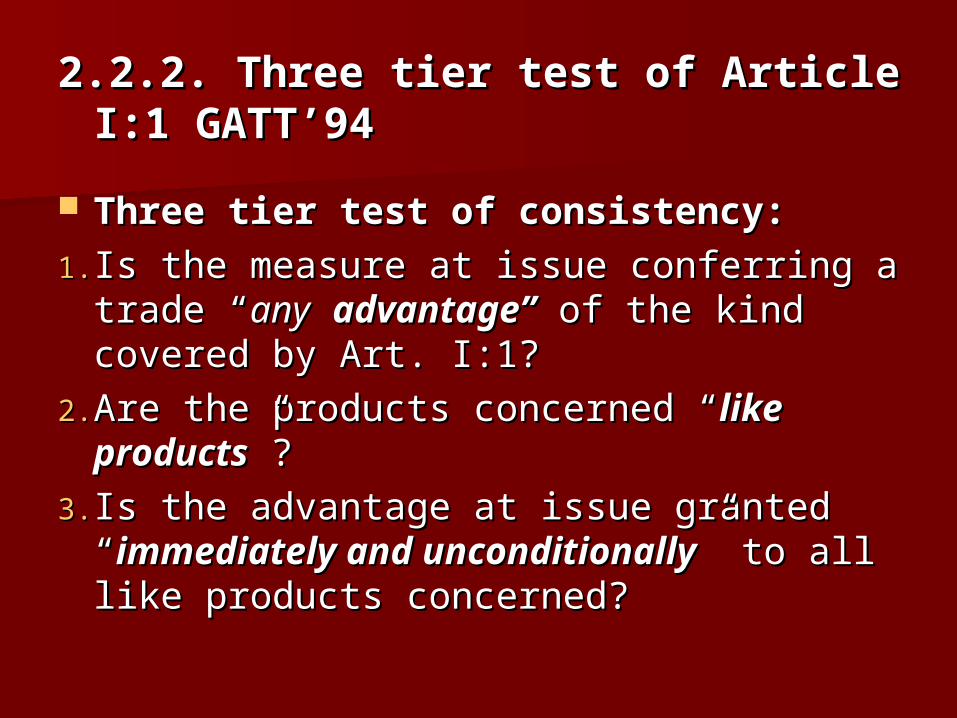

2.2.2. Three tier test of Article I:1 2.2.2. Three tier test of Article I:1 GATT’94GATT’94

Three tier test of consistency:Three tier test of consistency:

1.1. Is the measure at issue conferring a trade Is the measure at issue conferring a trade ““anyany advantage”advantage” of the kind covered by of the kind covered by Art. I:1?Art. I:1?

2.2. Are the products concerned “Are the products concerned “like like productsproducts”?”?

3.3. Is the advantage at issue granted Is the advantage at issue granted ““immediately and unconditionallyimmediately and unconditionally” to ” to all like products concerned?all like products concerned?

““Any Advantage” (1)Any Advantage” (1) The MFN obligation concerns The MFN obligation concerns any advantage any advantage granted by granted by

any Member any Member to to any other WTO-Memberany other WTO-Member or or Non-WTO-Non-WTO-MemberMember (!)(!) with respect to (1) customs duties, other with respect to (1) customs duties, other charges on imports and exports and other customs matters charges on imports and exports and other customs matters (2) internal taxes (3) internal regulation affecting sale, (2) internal taxes (3) internal regulation affecting sale, distribution and use of products. Generally Art I:1 is distribution and use of products. Generally Art I:1 is very very widewide. .

ExamplesExamples: besides customs duties: import surcharges, : besides customs duties: import surcharges, customs fees or quality inspection fees, charges on customs fees or quality inspection fees, charges on international transfer of payments for imports/exports, international transfer of payments for imports/exports, method of assessing base value on which the duty or method of assessing base value on which the duty or charge is levied, internal taxes and internal charges, etc.charge is levied, internal taxes and internal charges, etc.

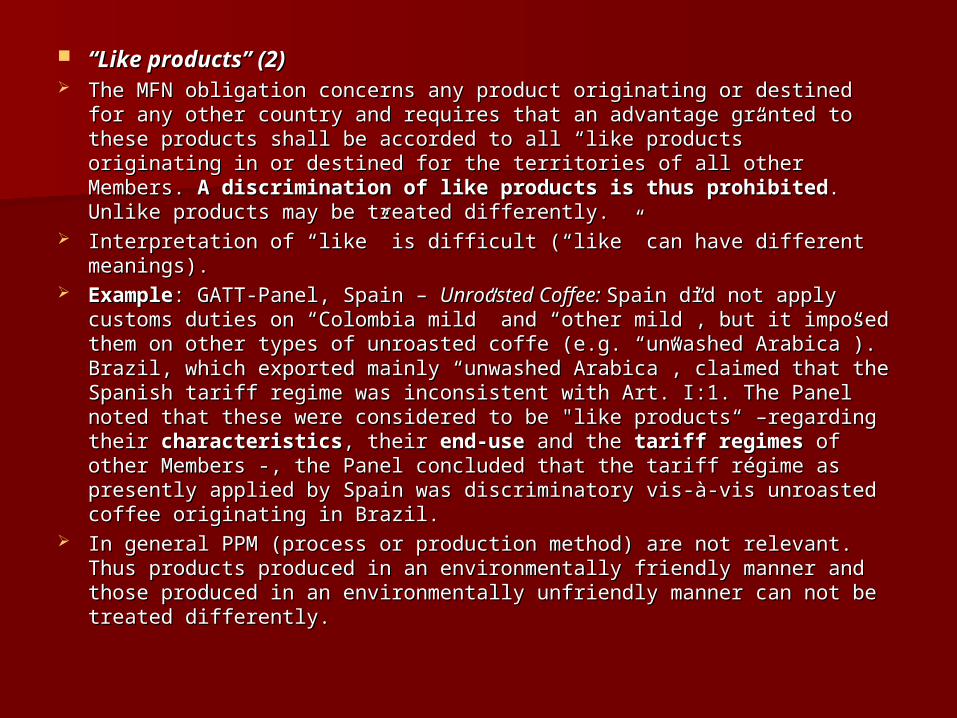

““Like products” (2)Like products” (2) The MFN obligation concerns any product originating or destined for any The MFN obligation concerns any product originating or destined for any

other country and requires that an advantage granted to these products other country and requires that an advantage granted to these products shall be accorded to all “like products” originating in or destined for the shall be accorded to all “like products” originating in or destined for the territories of all other Members. territories of all other Members. A discrimination of like products is A discrimination of like products is thus prohibitedthus prohibited. Unlike products may be treated differently.. Unlike products may be treated differently.

Interpretation of “like” is difficult (“like” can have different meanings). Interpretation of “like” is difficult (“like” can have different meanings). ExampleExample: GATT-Panel, Spain – : GATT-Panel, Spain – Unroasted Coffee: Unroasted Coffee: Spain did not apply Spain did not apply

customs duties on “Colombia mild” and “other mild”, but it imposed customs duties on “Colombia mild” and “other mild”, but it imposed them on other types of unroasted coffe (e.g. “unwashed Arabica”). them on other types of unroasted coffe (e.g. “unwashed Arabica”). Brazil, which exported mainly “unwashed Arabica”, claimed that the Brazil, which exported mainly “unwashed Arabica”, claimed that the Spanish tariff regime was inconsistent with Art. I:1. Spanish tariff regime was inconsistent with Art. I:1. The Panel noted that The Panel noted that these were considered to be "like products“ –regarding their these were considered to be "like products“ –regarding their characteristicscharacteristics, their , their end-useend-use and the and the tariff regimestariff regimes of other of other Members -, the Panel concluded that the tariff régime as presently Members -, the Panel concluded that the tariff régime as presently applied by Spain was discriminatory vis-à-vis unroasted coffee applied by Spain was discriminatory vis-à-vis unroasted coffee originating in Brazil. originating in Brazil.

In general PPM (process or production method) are not relevant. Thus In general PPM (process or production method) are not relevant. Thus products produced in an environmentally friendly manner and those products produced in an environmentally friendly manner and those produced in an environmentally unfriendly manner can not be treated produced in an environmentally unfriendly manner can not be treated differently.differently.

2.3. National Treatment2.3. National Treatment2.3.1. Overview2.3.1. Overview Art III GATT’ 94 (s also Art. XVII GATS, Art 3 TRIPS): Art III GATT’ 94 (s also Art. XVII GATS, Art 3 TRIPS):

“ “ 1. The contracting parties recognize that 1. The contracting parties recognize that internal taxes internal taxes and other and other internal chargesinternal charges, , and and laws, regulations and requirements laws, regulations and requirements affecting the affecting the internal sale, offering internal sale, offering for sale, for sale, purchasepurchase, , transportationtransportation, , distributiondistribution or or use of productsuse of products, and , and internal quantitative regulations internal quantitative regulations requiring the mixture, processing or use of requiring the mixture, processing or use of products in specified amounts or proportions, should not be applied to imported or products in specified amounts or proportions, should not be applied to imported or domestic products so as to domestic products so as to afford protection to domestic productionafford protection to domestic production..

2. The products of the territory of any contracting party imported into the territory of 2. The products of the territory of any contracting party imported into the territory of any other contracting party any other contracting party shall not be subject, directly or indirectly, to shall not be subject, directly or indirectly, to internal taxes or other internal charges of any kind in excess of those internal taxes or other internal charges of any kind in excess of those applied, directly or indirectly, to like domestic productsapplied, directly or indirectly, to like domestic products. Moreover, no . Moreover, no contracting party shall otherwise apply internal taxes or other internal charges to contracting party shall otherwise apply internal taxes or other internal charges to imported or domestic products in a manner contrary to the principles set forth in imported or domestic products in a manner contrary to the principles set forth in paragraph 1. […]paragraph 1. […]

4. The products of the territory of any contracting party imported into the territory of 4. The products of the territory of any contracting party imported into the territory of any other contracting party shall be accorded any other contracting party shall be accorded treatment no less favourable treatment no less favourable than than that accorded to like products of national origin in respect of that accorded to like products of national origin in respect of all laws, regulations all laws, regulations and requirementsand requirements affecting their internal sale, offering for sale, purchase, affecting their internal sale, offering for sale, purchase, transportation, distribution or use. The provisions of this paragraph shall not prevent transportation, distribution or use. The provisions of this paragraph shall not prevent the application of differential internal transportation charges which are based the application of differential internal transportation charges which are based exclusively on the economic operation of the means of transport and not on the exclusively on the economic operation of the means of transport and not on the nationality of the product.”nationality of the product.”

Does Does not apply not apply to laws/acts governing to laws/acts governing government procurement government procurement and and subsidiessubsidies..

Other National Treatment obligations can be found in the Other National Treatment obligations can be found in the TBT TBT AgreementAgreement, the , the SPS AgreementSPS Agreement and the and the Agreement on Trade-Agreement on Trade-Related Investment MeasuresRelated Investment Measures..

PurposePurpose: Art III : Art III prohibits discrimination against imported prohibits discrimination against imported productsproducts. Imported products must not be treated less . Imported products must not be treated less favourably than like domestic products once the imported favourably than like domestic products once the imported product has entered the domestic market.product has entered the domestic market.

S Appellate Body, S Appellate Body, Japan Alcoholic Beverages IIJapan Alcoholic Beverages II: “The broad and : “The broad and fundamental purpose of Article III is to fundamental purpose of Article III is to avoid protectionism avoid protectionism in in the the application of internal tax application of internal tax and and regulatory measuresregulatory measures. . More specifically, the purpose of Article III ‘is to ensure that More specifically, the purpose of Article III ‘is to ensure that internal measures not be applied to imported or domestic internal measures not be applied to imported or domestic products so as to afford protection to domestic production’. products so as to afford protection to domestic production’. Toward this end, Article III obliges Members of the WTO to Toward this end, Article III obliges Members of the WTO to provide equality of competitive conditions for imported provide equality of competitive conditions for imported products products in relation to domestic products. ‘[T]he intention of in relation to domestic products. ‘[T]he intention of the drafters of the Agreement was clearly the drafters of the Agreement was clearly to treat the to treat the imported products in the same way as the like domestic imported products in the same way as the like domestic productsproducts once they had been cleared through customs. once they had been cleared through customs. Otherwise Otherwise indirect protection indirect protection could be given’.could be given’.

Art. III only applies to Art. III only applies to internal measuresinternal measures, not border , not border measures (like Art. II, tariff concessions or Art. XI, measures (like Art. II, tariff concessions or Art. XI, quantitative restrictions). quantitative restrictions). Distinction between internal Distinction between internal and border measures is crucialand border measures is crucial..

Not always easy, esp. when the internal measure is applied Not always easy, esp. when the internal measure is applied to imported products at the time or point of importation. to imported products at the time or point of importation. E.g. a product is barred at the border because it fails to E.g. a product is barred at the border because it fails to meet a public health or consumer safety requirement (in meet a public health or consumer safety requirement (in this case Art. III is applicable)this case Art. III is applicable)

ExampleExample: : India – AutosIndia – Autos: India imposed an obligation on : India imposed an obligation on automotive manufacturers to automotive manufacturers to (1) (1) use a certain proportion use a certain proportion of local parts and components in the manufacture of cars of local parts and components in the manufacture of cars and other automotive vehicles and it also imposed an and other automotive vehicles and it also imposed an obligation obligation (2) (2) to offset the amount of their purchases of to offset the amount of their purchases of previously imported kits and components, already on the previously imported kits and components, already on the Indian market, by exports of equivalent value. Furthermore Indian market, by exports of equivalent value. Furthermore it imposed an obligation on these manufacturers to it imposed an obligation on these manufacturers to (3) (3) balance their importation of kits and components with balance their importation of kits and components with exports of equivalent value.exports of equivalent value.

India – Autos (cont’d): The DSB found that (1) and (2) were India – Autos (cont’d): The DSB found that (1) and (2) were inconsistent with Art III:4. Furthermore India acted inconsistently inconsistent with Art III:4. Furthermore India acted inconsistently with Article XI by imposing (3) on automotive manufacturers.with Article XI by imposing (3) on automotive manufacturers.

S Panel, S Panel, India – AutosIndia – Autos, para 8.1: , para 8.1:

India acted inconsistently with its obligations under India acted inconsistently with its obligations under Article III:4 Article III:4 of of the GATT 1994 by imposing on automotive manufacturers, under the GATT 1994 by imposing on automotive manufacturers, under the terms of Public Notice No. 60 [...] an obligation to use a certain the terms of Public Notice No. 60 [...] an obligation to use a certain proportion of local parts and components in the manufacture of proportion of local parts and components in the manufacture of cars and automotive vehicles (cars and automotive vehicles ("indigenization" condition"indigenization" condition););

India acted inconsistently with its obligations under India acted inconsistently with its obligations under Article XI Article XI of the of the GATT 1994 by imposing on automotive manufacturers an GATT 1994 by imposing on automotive manufacturers an obligation to balance any importation of certain kits and obligation to balance any importation of certain kits and components with exports of equivalent value (components with exports of equivalent value ("trade balancing" "trade balancing" conditioncondition););

India acted inconsistently with its obligations under India acted inconsistently with its obligations under Article III:4 Article III:4 of of the GATT 1994 by imposing, in the context of the trade balancing the GATT 1994 by imposing, in the context of the trade balancing condition an obligation to condition an obligation to offset the amount of any purchases offset the amount of any purchases of previously imported restricted kits of previously imported restricted kits and and componentscomponents on on the Indian market, by exports of equivalent value.” the Indian market, by exports of equivalent value.”

2.3.2. Art III:1, Art III:2 and Art III:42.3.2. Art III:1, Art III:2 and Art III:4 Art. III:1 general principle which is elaborated by Art. III:2 Art. III:1 general principle which is elaborated by Art. III:2

((internal taxationinternal taxation) and Art III:4 () and Art III:4 (internal regulationinternal regulation).). Art. III:2Art. III:2:: First sentenceFirst sentence: obligation relating to internal taxation of : obligation relating to internal taxation of

““like productslike products” ” Second sentenceSecond sentence: obligation relating to internal taxation : obligation relating to internal taxation

of “of “directly competitive or substitutable productsdirectly competitive or substitutable products” ” (competition has to be involved).(competition has to be involved).

Effect: S Appellate Body, Effect: S Appellate Body, Canada – PeriodicalsCanada – Periodicals: First check : First check sentence 1 – if it does not apply then check sentence 2 sentence 1 – if it does not apply then check sentence 2

“ “ […] the following two questions need to be answered to determine whether there is a […] the following two questions need to be answered to determine whether there is a violation of Article III:2 of GATT 1994: (a) Are imported "split-run" periodicals and violation of Article III:2 of GATT 1994: (a) Are imported "split-run" periodicals and domestic non "split-run" periodicals like products?; and (b) Are imported "split-run" domestic non "split-run" periodicals like products?; and (b) Are imported "split-run" periodicals subject to an internal tax in excess of that applied to domestic non "split-periodicals subject to an internal tax in excess of that applied to domestic non "split-run" periodicals? If the answers to both questions are affirmative, there is a violation run" periodicals? If the answers to both questions are affirmative, there is a violation of Article III:2, first sentence. of Article III:2, first sentence. If the answer to the first question is negativeIf the answer to the first question is negative, we , we need to need to examine further whether there is a violation of Article III:2examine further whether there is a violation of Article III:2, second , second sentence.”sentence.”

Art. III:2 first sentenceArt. III:2 first sentence: obligation : obligation relating to internal taxation of “relating to internal taxation of “like like productsproducts”: Three-tier-test: ”: Three-tier-test:

1.1.Are the measures Are the measures internal taxes internal taxes and other charges of any kind, which and other charges of any kind, which are applied directly or indirectlyare applied directly or indirectly

2.2.are the imported and the domestic are the imported and the domestic products are products are like productslike products??

3.3.Are the imported products are Are the imported products are taxed taxed in excess in excess of the domestic products?of the domestic products?

(1) Internal taxes (1) Internal taxes (=fiscal measure) which are applied “(=fiscal measure) which are applied “on or in on or in connectionconnection” ” (directly, indirectly=tax is applied on the processing of the (directly, indirectly=tax is applied on the processing of the product. No fiscal measure: security deposit (EEC-Animal Feed Proteins)product. No fiscal measure: security deposit (EEC-Animal Feed Proteins)

(2) (2) Like productLike product: : ExampleExample ( (Japan – Alcoholic Beverages IIJapan – Alcoholic Beverages II): Under the ): Under the Japanese tax system the internal tax imposed on domestic shochu Japanese tax system the internal tax imposed on domestic shochu (alcoholic beverage) was the same as that imposed on imported shochu. (alcoholic beverage) was the same as that imposed on imported shochu. A higher tax was imposed on imported vodka (but the same as on A higher tax was imposed on imported vodka (but the same as on domestic vodka). The question was, if shochu and vodka were found to domestic vodka). The question was, if shochu and vodka were found to be like.be like.

The Appellate body ruled that “The Appellate body ruled that “like productslike products” in the meaning of Art III:2 ” in the meaning of Art III:2 first sentence should be first sentence should be interpreted narrowly interpreted narrowly because of the because of the existence of the concept of “directly competitive or substitutable existence of the concept of “directly competitive or substitutable products” of the second sentence of Art III:2. “[…] the Appellate Body products” of the second sentence of Art III:2. “[…] the Appellate Body affirms the Panel's conclusions that shochu and vodka are like products affirms the Panel's conclusions that shochu and vodka are like products [and] that shochu and other distilled spirits and liqueurs listed in HS [and] that shochu and other distilled spirits and liqueurs listed in HS 2208, except for vodka, are ‘directly competitive or substitutable 2208, except for vodka, are ‘directly competitive or substitutable products’ (violation of Article III:2, second sentence).”products’ (violation of Article III:2, second sentence).”

(3)(3) “In excess of”“In excess of” means “even the smallest amount of ‘excess’ is too means “even the smallest amount of ‘excess’ is too much – much – no trade effects test – no trade effects test – “it is irrelevant that the ‘trade effects’ “it is irrelevant that the ‘trade effects’ of the tax differential between imported and domestic products, as of the tax differential between imported and domestic products, as reflected in the volumes of imports, are insignificant or even non-reflected in the volumes of imports, are insignificant or even non-existent.”existent.” (Appellate Body, Japan – (Appellate Body, Japan – Alcoholic Beverages IIAlcoholic Beverages II))

Art. III:2 second sentenceArt. III:2 second sentence: relating to : relating to internal taxation of “internal taxation of “directly directly competitive or substitutable competitive or substitutable productsproducts”: Three-tier-test:”: Three-tier-test:

(1) (1) Are the imported and domestic Are the imported and domestic products products directly competitive or directly competitive or substitutablesubstitutable??

(2)(2) Are these products Are these products similarily similarily taxedtaxed??

(3)(3) Is the dissimilar taxation applied so Is the dissimilar taxation applied so as to afford as to afford protection to domestic protection to domestic productionproduction??

(1) (1) Directly competitive or substitutableDirectly competitive or substitutable?? S Appellate Body, S Appellate Body, Korea – Alcoholic BeveragesKorea – Alcoholic Beverages: “: “The first The first

sentence of Article III:2 also forms part of the context of the sentence of Article III:2 also forms part of the context of the term. term. ‘Like’ products are a subset of directly competitive ‘Like’ products are a subset of directly competitive or substitutable productsor substitutable products: all like products are, by definition, : all like products are, by definition, directly competitive or substitutable products, whereas not all directly competitive or substitutable products, whereas not all ‘directly competitive or substitutable’ products are ‘like’. The ‘directly competitive or substitutable’ products are ‘like’. The notion of notion of like products must be construed narrowlylike products must be construed narrowly but the but the category of directly competitive or substitutable products category of directly competitive or substitutable products is broaderis broader. While perfectly substitutable products fall within . While perfectly substitutable products fall within Article III:2, first sentence, imperfectly substitutable products can Article III:2, first sentence, imperfectly substitutable products can be assessed under Article III:2, second sentence.be assessed under Article III:2, second sentence. “ “

Products are “direct competitive or substitutable, when they are Products are “direct competitive or substitutable, when they are interchangeable, in that they offer alternative ways of interchangeable, in that they offer alternative ways of satisfying a particular need or tastesatisfying a particular need or taste. Similar to ‘like . Similar to ‘like products’: physical characteristics, common end-use, tariff products’: physical characteristics, common end-use, tariff classifications, the competitive conditions in the relevant market.classifications, the competitive conditions in the relevant market.

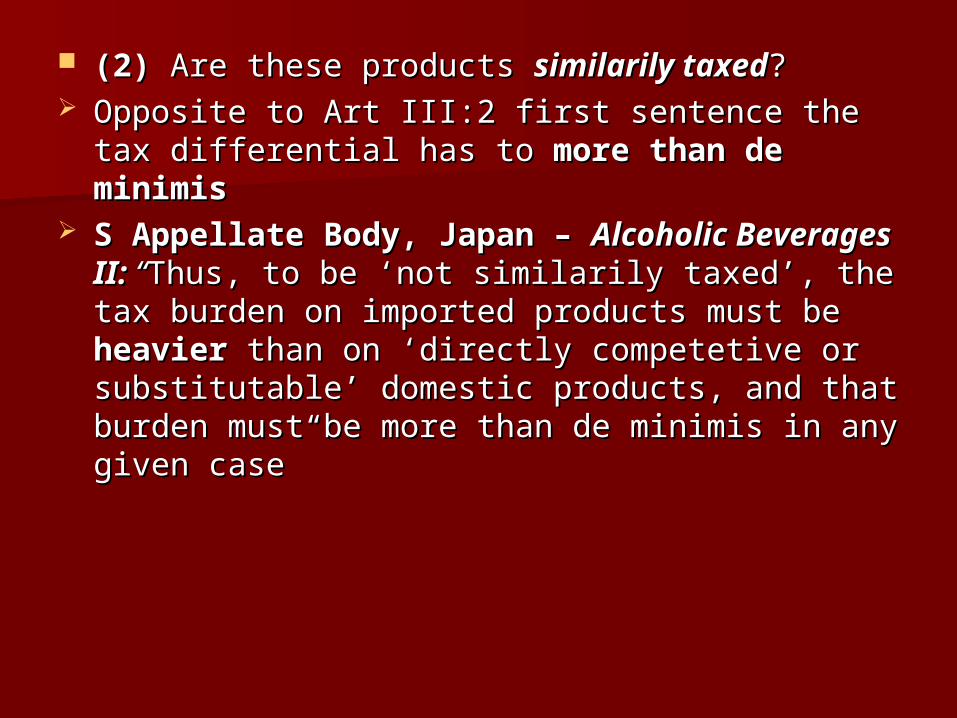

(2)(2) Are these products Are these products similarily taxedsimilarily taxed?? Opposite to Art III:2 first sentence the tax Opposite to Art III:2 first sentence the tax

differential has to differential has to more than de minimismore than de minimis S Appellate Body, Japan – S Appellate Body, Japan – Alcoholic Alcoholic

Beverages II: Beverages II: ““Thus, to be ‘not similarily taxed’, Thus, to be ‘not similarily taxed’, the tax burden on imported products must be the tax burden on imported products must be heavierheavier than on ‘directly competetive or than on ‘directly competetive or substitutable’ domestic products, and that burden substitutable’ domestic products, and that burden must be more than de minimis in any given case”must be more than de minimis in any given case”

(3)(3) Is the dissimilar taxation applied so as Is the dissimilar taxation applied so as to afford to afford protection to domestic protection to domestic productionproduction??

Objective analysis of the structure and Objective analysis of the structure and application of the measure in question on application of the measure in question on domestic as compared to imported domestic as compared to imported products.products.

ExampleExample: The tax measure operates in : The tax measure operates in such a way that the lower tax brackets such a way that the lower tax brackets cover almost exclusively domestic cover almost exclusively domestic production, whereas the higher tax production, whereas the higher tax brackets embrace almost exclusively brackets embrace almost exclusively imported products (domestic production).imported products (domestic production).

Art III:4Art III:4 Internal regulation is dealt Internal regulation is dealt

primarily in Art. III:4.primarily in Art. III:4. Three-tier-test:Three-tier-test:1.1. Is the measure a Is the measure a law, regulation or law, regulation or

requirementrequirement covered by Art. III:4? covered by Art. III:4?

2.2. Are the imported and domestic products Are the imported and domestic products like productslike products??

3.3. Are the imported products accorded a Are the imported products accorded a less less favourable treatmentfavourable treatment??

(1) Laws, regulations and requirements (1) Laws, regulations and requirements affecting the affecting the internal sale, offering for sale, purchase, transportation, internal sale, offering for sale, purchase, transportation, distribution or use of productsdistribution or use of products

Short: Is the sale or use affected? Broadly interpreted: All Short: Is the sale or use affected? Broadly interpreted: All measures that may modify the measures that may modify the conditions of competitionconditions of competition..

ExamplesExamples: minimum price requirements applicable to domestic : minimum price requirements applicable to domestic and imported beer; limitations on points of sale; the requirement and imported beer; limitations on points of sale; the requirement that imported beer and wine be sold only through in-State that imported beer and wine be sold only through in-State wholesalers; additional marketing requirements (e.g. add place wholesalers; additional marketing requirements (e.g. add place of origin or formula of the product); trade related investment of origin or formula of the product); trade related investment measures.measures.

(2) Like products(2) Like products see above see above (3) Treatment less favourable(3) Treatment less favourable: “effective equality of : “effective equality of

competitive opportunities”. S Appellate Body, Canada – competitive opportunities”. S Appellate Body, Canada – Provincial Liquor Boards (US): “minimum prices applied equally Provincial Liquor Boards (US): “minimum prices applied equally to imported and domestic beer did not necessarily accord equal to imported and domestic beer did not necessarily accord equal conditions of competition to imported and domestic beer. conditions of competition to imported and domestic beer. Whenever they prevented imported beer from being supplied at Whenever they prevented imported beer from being supplied at a price lower … they accorded in fact treatment to imported beer a price lower … they accorded in fact treatment to imported beer less favourable than that accorded to domestic beer.”less favourable than that accorded to domestic beer.”

Short cases:Short cases:1.1. Newlands (member of the EC) tariff regulation set forth: concerning Newlands (member of the EC) tariff regulation set forth: concerning

the importation of German beer a tariff of 3 Newlanddollars per the importation of German beer a tariff of 3 Newlanddollars per unit, concerning the importation of Austrian beer 4 Newlanddollars.unit, concerning the importation of Austrian beer 4 Newlanddollars.

2.2. Newlands tax system: 20% tax on domestic red wine, 21% on Newlands tax system: 20% tax on domestic red wine, 21% on foreign red wine (alternative: 25 % on foreign white wine).foreign red wine (alternative: 25 % on foreign white wine).

3.3. Newland adopts a minimum price requirement for milk applicable Newland adopts a minimum price requirement for milk applicable for domestic and imported milk.for domestic and imported milk.

4.4. Newland requires its automotive manufacturers to use a certain Newland requires its automotive manufacturers to use a certain use a certain proportion of local parts and components and use a certain proportion of local parts and components and imposes an obligation to balance any importation of certain kits imposes an obligation to balance any importation of certain kits and componentsand components

5.5. The DSB finds that the minimum price requirement is inconsistent The DSB finds that the minimum price requirement is inconsistent with WTO-Law. What are the effects of this decision on national with WTO-Law. What are the effects of this decision on national level?level?

6.6. An Newland-regulation was making the suspension of an import An Newland-regulation was making the suspension of an import levy conditional (only) on the production of a certificate of levy conditional (only) on the production of a certificate of authenticity. The only authority licensed to issue this certificate is authenticity. The only authority licensed to issue this certificate is situated in X-Land.situated in X-Land.

2. Rules on Market Access2. Rules on Market Access2.1. Overview2.1. Overview International trade needs (predictable and growing) access to domestic International trade needs (predictable and growing) access to domestic

markets of other countries. Market access for goods and services from markets of other countries. Market access for goods and services from other countries is frequently impeded/restricted by two main categories other countries is frequently impeded/restricted by two main categories of barriers to market access: of barriers to market access: tariff barriers tariff barriers and and non tariff barriers non tariff barriers (quantitative restrictions, unfair and arbitrary application of trade (quantitative restrictions, unfair and arbitrary application of trade regulations, customs formalities, technical barriers to trade and regulations, customs formalities, technical barriers to trade and governement procurement practices).governement procurement practices).

WTO-law contains four groups of rules regarding market access – WTO-law contains four groups of rules regarding market access – different rules apply to different forms of barriers different rules apply to different forms of barriers (difference in (difference in rules reflects a difference in the negative effects barriers have on trade rules reflects a difference in the negative effects barriers have on trade and on the economy)and on the economy)

Rules on customs duties Rules on customs duties (tariffs)(tariffs) Rules on other duties and chargesRules on other duties and charges Rules on quantitative restrictionsRules on quantitative restrictions Rules on non-tariff-barriers Rules on non-tariff-barriers (e.g. rules on transparency of trade (e.g. rules on transparency of trade

regulations, technical regulations, standards, sanitary and phytosanitary regulations, technical regulations, standards, sanitary and phytosanitary measures, customs formalities, government procurement practices)measures, customs formalities, government procurement practices)

Rules on customs duties: Rules on customs duties: The imposition The imposition of customs duties is not prohibited by WTO-of customs duties is not prohibited by WTO-law and in fact all members of WTO impose law and in fact all members of WTO impose customs duties. WTO law calls upon its customs duties. WTO law calls upon its members to negotiate mutually beneficial members to negotiate mutually beneficial reductions of customs duties (result: tariff reductions of customs duties (result: tariff concessions or bindings set out in a concessions or bindings set out in a member’s Schedule of Concession)member’s Schedule of Concession)

Rules on other duties and charges: Rules on other duties and charges: financial charges other than ordinary financial charges other than ordinary customs tariffs in the context of importation customs tariffs in the context of importation of a good (import surcharge, security of a good (import surcharge, security deposit, statistical tax, customs fee)deposit, statistical tax, customs fee)

2.2. Quantitative restrictions2.2. Quantitative restrictions A QR is a measure which A QR is a measure which limits the quantity limits the quantity of a of a

product that may be imported or exported. WTO product that may be imported or exported. WTO has a clear preference for custom duties over QR has a clear preference for custom duties over QR (tariffs are the accepted form of protection). (tariffs are the accepted form of protection). Different types:Different types:

ProhibitionProhibition or ban of a product (absolute or or ban of a product (absolute or conditional)conditional)

quotaquota: Measure indicating the quantity that may : Measure indicating the quantity that may be imported or exported (global quota, bilateral be imported or exported (global quota, bilateral quota – based on number of units, weight or quota – based on number of units, weight or volume and also value)volume and also value)

Automatic and non-automatic licensingAutomatic and non-automatic licensing Other quantitative restrictions Other quantitative restrictions (e.g. QR made (e.g. QR made

effective through a minimum price)effective through a minimum price)

Art XI GATT’94:Art XI GATT’94:

““No prohibitions or restrictions other than dutiesNo prohibitions or restrictions other than duties , , taxestaxes or or other chargesother charges, whether made effective through quotas, , whether made effective through quotas, import or export licences or other measures, import or export licences or other measures, shall be shall be instituted or maintained instituted or maintained by any contracting party on the by any contracting party on the importationimportation of any product of the territory of any other of any product of the territory of any other contracting party or on the contracting party or on the exportationexportation or sale for export of or sale for export of any product destined for the territory of any other contracting any product destined for the territory of any other contracting party.”party.”

ExamplesExamples: The USA imposed an import ban on shrimp and : The USA imposed an import ban on shrimp and shrimp products harvested by vessels of foreign nations where shrimp products harvested by vessels of foreign nations where the exporting country had not been certified by the US the exporting country had not been certified by the US authorities as using methods not leading to the accidental authorities as using methods not leading to the accidental killing of sea turtles above certain levels (Panel, killing of sea turtles above certain levels (Panel, US-ShrimpUS-Shrimp). ). The EEC imposed minimum prices on imports (Panel, The EEC imposed minimum prices on imports (Panel, EEC-EEC-Minimum Import PricesMinimum Import Prices).).

Art XI does not refer to laws or regulations but to measures Art XI does not refer to laws or regulations but to measures (legal status of measure is irrelevant) – even non mandatory (legal status of measure is irrelevant) – even non mandatory measures can be a QR (s Panel, Japan – measures can be a QR (s Panel, Japan – Semi-ConductorsSemi-Conductors))

Further example: (Panel, Further example: (Panel, US-TunaUS-Tuna))

To reduce the incidental intake of dolphins by Yellowfin tuna fisheries, To reduce the incidental intake of dolphins by Yellowfin tuna fisheries, the United States enacted the Marine Mammal Protection Act in 1972, the United States enacted the Marine Mammal Protection Act in 1972, which bans imports of Yellowfin tuna and their processed products which bans imports of Yellowfin tuna and their processed products from Mexico and other countries where fishing methods result in the from Mexico and other countries where fishing methods result in the incidental intake of dolphins. To prevent circumvention, the United incidental intake of dolphins. To prevent circumvention, the United States also demands that similar import restrictions be adopted by States also demands that similar import restrictions be adopted by third countries importing Yellowfin tuna or their processed products third countries importing Yellowfin tuna or their processed products from countries subjected to the above import restrictions and from countries subjected to the above import restrictions and prohibits imports of Yellowfin tuna and their products from countries prohibits imports of Yellowfin tuna and their products from countries which do not comply with this demand. Japan, the European Union, which do not comply with this demand. Japan, the European Union, and others have been targeted by the US measures.and others have been targeted by the US measures.

The report of the Panel noted that the United States' import prohibitions The report of the Panel noted that the United States' import prohibitions are designed to force policy changes in other countries and indeed are designed to force policy changes in other countries and indeed can only be effective if such changes are made. Since these can only be effective if such changes are made. Since these prohibitions are not measures necessary to protect the life and health prohibitions are not measures necessary to protect the life and health of animals exempted by nor primarily aimed at the conservation of of animals exempted by nor primarily aimed at the conservation of exhaustible natural resources, the report concluded that the US exhaustible natural resources, the report concluded that the US measures are contrary to GATT Article XI:1, and are not covered by measures are contrary to GATT Article XI:1, and are not covered by the exceptions in Articles XX:(b) or (g).the exceptions in Articles XX:(b) or (g).

Case:Case:In an effort to reduce its trade deficit with Japan, Korea instituted in 1980 In an effort to reduce its trade deficit with Japan, Korea instituted in 1980

a source diversification system for specific imports, as amended by a source diversification system for specific imports, as amended by Article 25 of the Executive Order of Korea's Foreign Trade Law of 1987. Article 25 of the Executive Order of Korea's Foreign Trade Law of 1987. Article 14(2) of this law authorizes the Minister of Trade, Industry and Article 14(2) of this law authorizes the Minister of Trade, Industry and Energy to approve exports and imports of certain products designated Energy to approve exports and imports of certain products designated in accordance with standards set forth in a presidential order for the in accordance with standards set forth in a presidential order for the purpose of balancing trade with countries. Under this system, the purpose of balancing trade with countries. Under this system, the approval of the Association of Foreign Trading Agents of Korea is approval of the Association of Foreign Trading Agents of Korea is required for imports of products exported by the country that had the required for imports of products exported by the country that had the largest trade surplus with Korea for the last five years (Notice of largest trade surplus with Korea for the last five years (Notice of Ministry of Trade, Industry and Energy Proclamation on Import Source Ministry of Trade, Industry and Energy Proclamation on Import Source Diversification Article 2). This approval is not normally given. Diversification Article 2). This approval is not normally given.

At the outset of its administration, the system applied to Japan, the At the outset of its administration, the system applied to Japan, the country having the largest trade surplus with Korea during the previous country having the largest trade surplus with Korea during the previous year. However, when Saudi Arabia became the country with the largest year. However, when Saudi Arabia became the country with the largest trade surplus in 1982, the system was amended in 1983 to apply to trade surplus in 1982, the system was amended in 1983 to apply to the country with the largest trade surplus "in the past five years." As a the country with the largest trade surplus "in the past five years." As a result, Japanese products have been continuously subjected to the result, Japanese products have been continuously subjected to the import restrictions. import restrictions.

(1) This approval is not normally given, (1) This approval is not normally given, thereby functioning as a de facto import thereby functioning as a de facto import ban. This measure is clearly in violation of ban. This measure is clearly in violation of Article XI of the GATT, which prohibits Article XI of the GATT, which prohibits quantitative restrictions.quantitative restrictions.

(2) As quantitative import restrictions are (2) As quantitative import restrictions are applied in a discriminatory fashion applied in a discriminatory fashion against a specific country, the system is against a specific country, the system is inconsistent with Articles I and [XIII] of inconsistent with Articles I and [XIII] of the GATT, which require the non-the GATT, which require the non-discriminatory administration of such discriminatory administration of such restrictions. restrictions.