Module 3-WTO Rules on RTAs · 3 WTO Rules on RTAs Click on this icon to move to the next slide ....

53

WTO Rules on RTAs MODULE 3 Click on this icon to move to the next slide

Transcript of Module 3-WTO Rules on RTAs · 3 WTO Rules on RTAs Click on this icon to move to the next slide ....

WTO Rules on RTAs

MO

DU

LE 3

Click on this icon to move to the

next slide

WTO rules on RTAs Module 3

WTO AND REGIONAL RULES RESULT FROM NEGOTIATIONS BETWEEN GOVERNMENTS

Trade rules, either multilateral or regional, are the result of negotiations between representatives of governments (WTO Members for multilateral rules, and parties for RTAs). Though trivial, this should not be forgotten, at least for two reasons:

The process leading to the establishment of rules and disciplines on trade is the result of a complex, not always rational, process involving economic, political, legal, and behavioural components. The economic theory usually constitutes the logical foundation of the process.

The negotiating process leading to the rules is conducted by Members. In the context of the multilateral trading system, as in most

regional trading systems, the participants in the negotiations are usually governments, competent to regulate, inter alia, commerce and economic matters within a defined territory. Consequently, the rights, obligations, and commitments undertaken in the negotiation, which become legally binding when the rules (multilateral as well as regional) enter into force, can only bind those who have made the commitments. In other words, the multilateral rules and most regional rules on trade remedies, the rights and obligations have a direct effect only on measures taken by those who have negotiated, i.e. Governments. The actions and behaviour of most economic actors (producers, sellers, buyers, consumers) cannot be addressed directly by the WTO rules or rules negotiated in the context of, say, a free trade agreement. However, although only measures taken by government must conform to the negotiated rules, these measures may, and do, have a direct impact on various economic operators. This should be recalled when analysing the rules.

1

2 Click on this icon to move to the previous slide

WTO rules on RTAs

ARCHITECTURE OF PRINCIPLES AND EXCEPTIONS UNDER THE WTO

At this stage, it is useful to understand the architecture of multilateral rules, as they apply to RTAs. These rules are the result of multilateral negotiations, which progressively established the legal framework under which RTAs are regulated under WTO law.

STARTING WITH THE MFN PRINCIPLE

Under WTO law, a Member must guarantee that the most preferential market access is immediately and unconditionally granted to all other WTO Members. The objective is to prevent any discrimination based on origin or nationality. This principle is carved in stone for trade in goods through Article I of the GATT, for trade in services through Article II of GATS, and for holders of intellectual property rights through Article 4 of the TRIPS Agreement.

The WTO Agreements nevertheless grant Members the right to derogate from these fundamental obligations, in certain circumstances and under certain conditions. These derogations – some might even consider that they constitute exceptions – are therefore CONDITIONAL RIGHTS granted to WTO Members to take measures that may be inconsistent with one or more basic principles. To exercise their rights, WTO Members must be in a situation that justifies the derogation, satisfy the conditions established by the legal provisions, and follow the required procedures.

WTO rules on RTAs

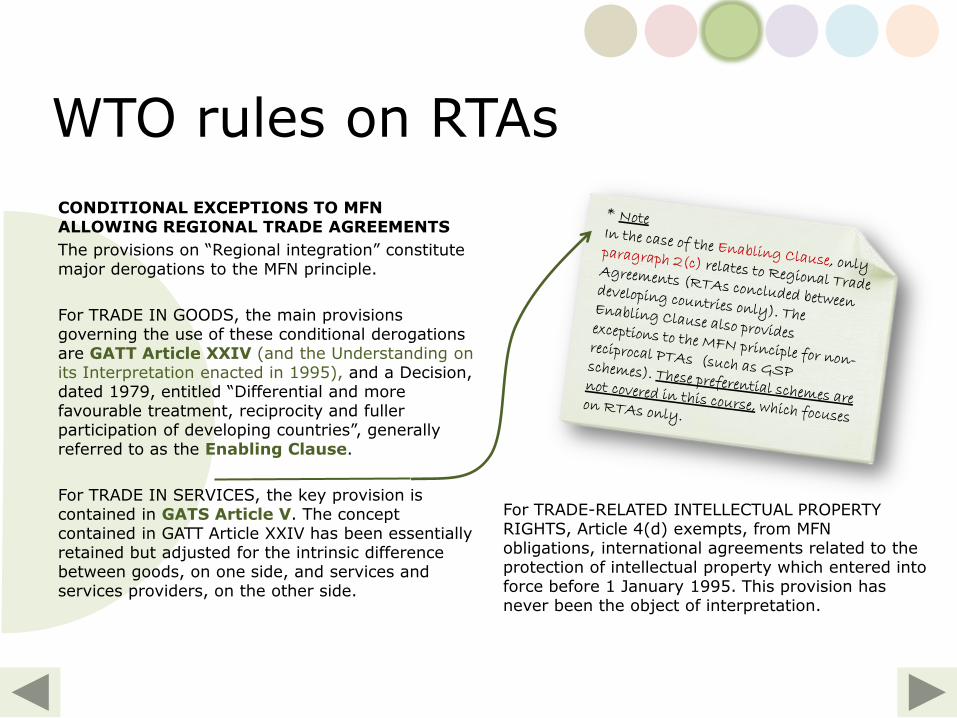

CONDITIONAL EXCEPTIONS TO MFN ALLOWING REGIONAL TRADE AGREEMENTS

The provisions on “Regional integration” constitute major derogations to the MFN principle.

For TRADE IN GOODS, the main provisions governing the use of these conditional derogations are GATT Article XXIV (and the Understanding on its Interpretation enacted in 1995), and a Decision, dated 1979, entitled “Differential and more favourable treatment, reciprocity and fuller participation of developing countries”, generally referred to as the Enabling Clause.

For TRADE IN SERVICES, the key provision is contained in GATS Article V. The concept contained in GATT Article XXIV has been essentially retained but adjusted for the intrinsic difference between goods, on one side, and services and services providers, on the other side.

For TRADE-RELATED INTELLECTUAL PROPERTY RIGHTS, Article 4(d) exempts, from MFN obligations, international agreements related to the protection of intellectual property which entered into force before 1 January 1995. This provision has never been the object of interpretation.

WTO rules on RTAs

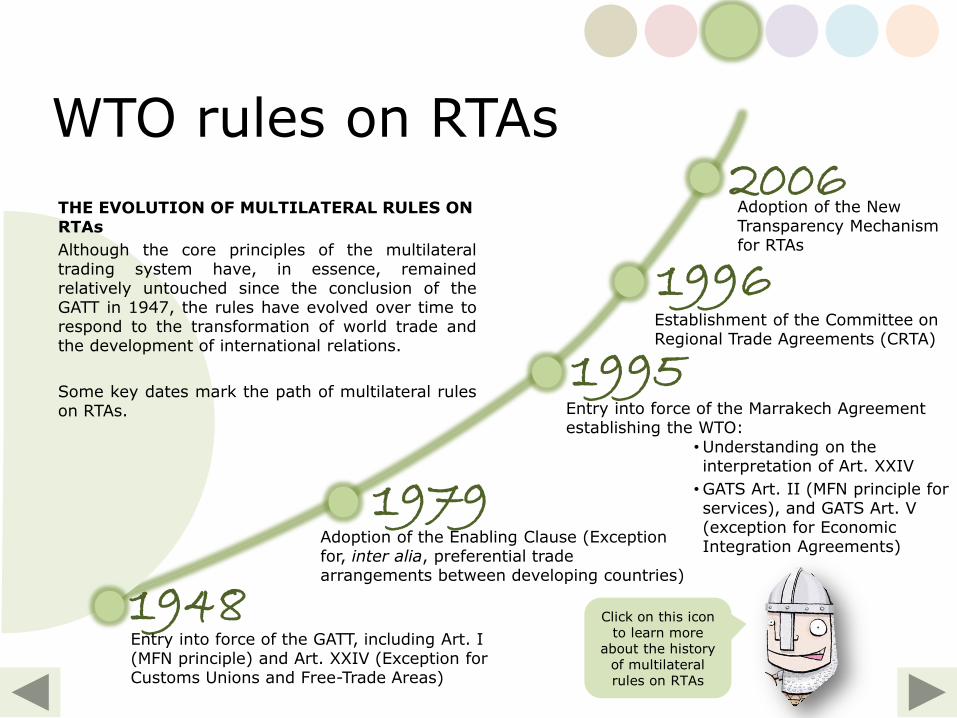

THE EVOLUTION OF MULTILATERAL RULES ON RTAs

Although the core principles of the multilateral trading system have, in essence, remained relatively untouched since the conclusion of the GATT in 1947, the rules have evolved over time to respond to the transformation of world trade and the development of international relations.

Some key dates mark the path of multilateral rules on RTAs.

Click on this icon to learn more

about the history of multilateral rules on RTAs

1948

1979

1995

1996

2006

Entry into force of the GATT, including Art. I (MFN principle) and Art. XXIV (Exception for Customs Unions and Free-Trade Areas)

Adoption of the Enabling Clause (Exception for, inter alia, preferential trade arrangements between developing countries)

Entry into force of the Marrakech Agreement establishing the WTO:

•Understanding on the interpretation of Art. XXIV

•GATS Art. II (MFN principle for services), and GATS Art. V (exception for Economic Integration Agreements)

Establishment of the Committee on Regional Trade Agreements (CRTA)

Adoption of the New Transparency Mechanism for RTAs

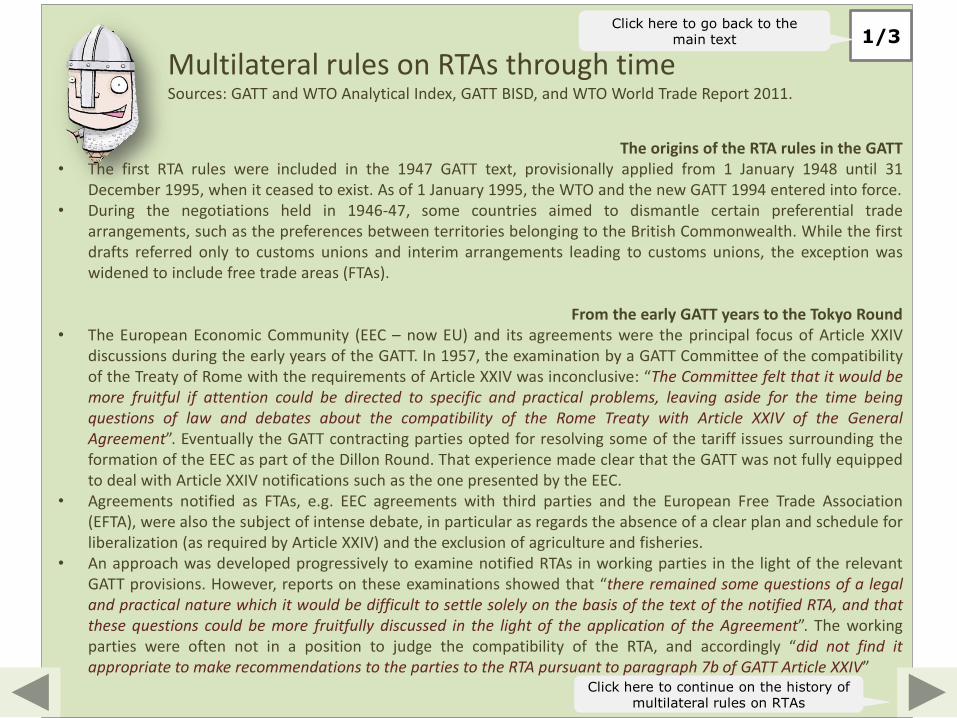

The origins of the RTA rules in the GATT • The first RTA rules were included in the 1947 GATT text, provisionally applied from 1 January 1948 until 31

December 1995, when it ceased to exist. As of 1 January 1995, the WTO and the new GATT 1994 entered into force. • During the negotiations held in 1946-47, some countries aimed to dismantle certain preferential trade

arrangements, such as the preferences between territories belonging to the British Commonwealth. While the first drafts referred only to customs unions and interim arrangements leading to customs unions, the exception was widened to include free trade areas (FTAs).

From the early GATT years to the Tokyo Round • The European Economic Community (EEC – now EU) and its agreements were the principal focus of Article XXIV

discussions during the early years of the GATT. In 1957, the examination by a GATT Committee of the compatibility of the Treaty of Rome with the requirements of Article XXIV was inconclusive: “The Committee felt that it would be more fruitful if attention could be directed to specific and practical problems, leaving aside for the time being questions of law and debates about the compatibility of the Rome Treaty with Article XXIV of the General Agreement”. Eventually the GATT contracting parties opted for resolving some of the tariff issues surrounding the formation of the EEC as part of the Dillon Round. That experience made clear that the GATT was not fully equipped to deal with Article XXIV notifications such as the one presented by the EEC.

• Agreements notified as FTAs, e.g. EEC agreements with third parties and the European Free Trade Association (EFTA), were also the subject of intense debate, in particular as regards the absence of a clear plan and schedule for liberalization (as required by Article XXIV) and the exclusion of agriculture and fisheries.

• An approach was developed progressively to examine notified RTAs in working parties in the light of the relevant GATT provisions. However, reports on these examinations showed that “there remained some questions of a legal and practical nature which it would be difficult to settle solely on the basis of the text of the notified RTA, and that these questions could be more fruitfully discussed in the light of the application of the Agreement”. The working parties were often not in a position to judge the compatibility of the RTA, and accordingly “did not find it appropriate to make recommendations to the parties to the RTA pursuant to paragraph 7b of GATT Article XXIV”

Multilateral rules on RTAs through time Sources: GATT and WTO Analytical Index, GATT BISD, and WTO World Trade Report 2011.

1/3 Click here to go back to the

main text

Click here to continue on the history of multilateral rules on RTAs

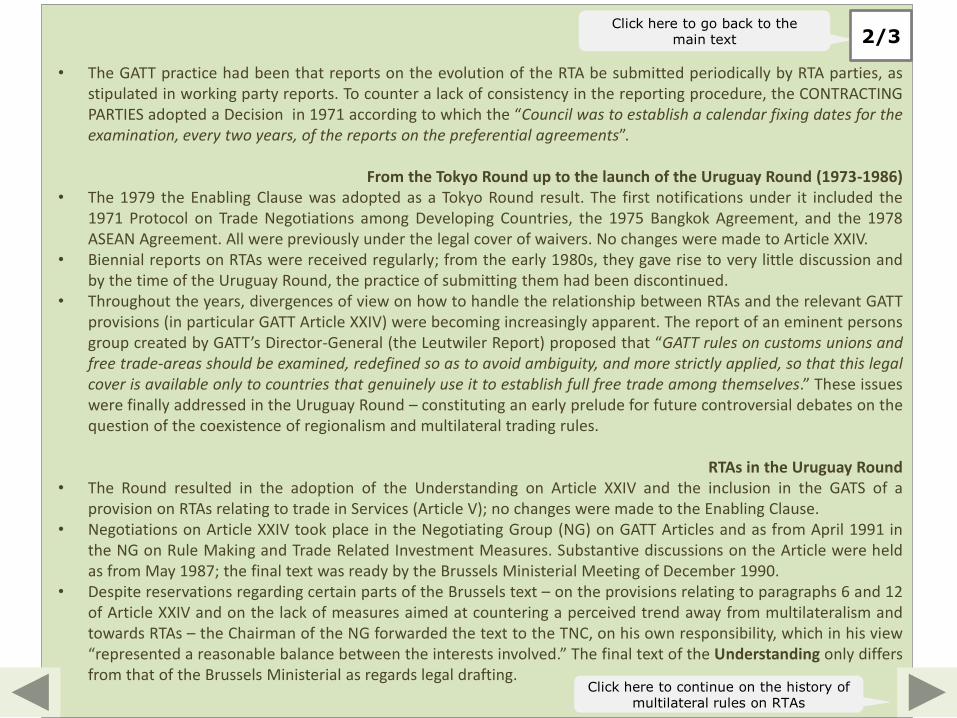

• The GATT practice had been that reports on the evolution of the RTA be submitted periodically by RTA parties, as stipulated in working party reports. To counter a lack of consistency in the reporting procedure, the CONTRACTING PARTIES adopted a Decision in 1971 according to which the “Council was to establish a calendar fixing dates for the examination, every two years, of the reports on the preferential agreements”.

From the Tokyo Round up to the launch of the Uruguay Round (1973-1986)

• The 1979 the Enabling Clause was adopted as a Tokyo Round result. The first notifications under it included the 1971 Protocol on Trade Negotiations among Developing Countries, the 1975 Bangkok Agreement, and the 1978 ASEAN Agreement. All were previously under the legal cover of waivers. No changes were made to Article XXIV.

• Biennial reports on RTAs were received regularly; from the early 1980s, they gave rise to very little discussion and by the time of the Uruguay Round, the practice of submitting them had been discontinued.

• Throughout the years, divergences of view on how to handle the relationship between RTAs and the relevant GATT provisions (in particular GATT Article XXIV) were becoming increasingly apparent. The report of an eminent persons group created by GATT’s Director-General (the Leutwiler Report) proposed that “GATT rules on customs unions and free trade-areas should be examined, redefined so as to avoid ambiguity, and more strictly applied, so that this legal cover is available only to countries that genuinely use it to establish full free trade among themselves.” These issues were finally addressed in the Uruguay Round – constituting an early prelude for future controversial debates on the question of the coexistence of regionalism and multilateral trading rules.

RTAs in the Uruguay Round

• The Round resulted in the adoption of the Understanding on Article XXIV and the inclusion in the GATS of a provision on RTAs relating to trade in Services (Article V); no changes were made to the Enabling Clause.

• Negotiations on Article XXIV took place in the Negotiating Group (NG) on GATT Articles and as from April 1991 in the NG on Rule Making and Trade Related Investment Measures. Substantive discussions on the Article were held as from May 1987; the final text was ready by the Brussels Ministerial Meeting of December 1990.

• Despite reservations regarding certain parts of the Brussels text – on the provisions relating to paragraphs 6 and 12 of Article XXIV and on the lack of measures aimed at countering a perceived trend away from multilateralism and towards RTAs – the Chairman of the NG forwarded the text to the TNC, on his own responsibility, which in his view “represented a reasonable balance between the interests involved.” The final text of the Understanding only differs from that of the Brussels Ministerial as regards legal drafting.

Click here to go back to the main text

Click here to continue on the history of multilateral rules on RTAs

2/3

• The 1992 notification under the Enabling Clause of the MERCOSUR (comprising Argentina, Brazil, Paraguay, and Uruguay) is also of relevance. Though RTAs under this provision were not, at that time, subject to examination in working parties, MERCOSUR was treated sui generis, being subject to an in-depth examination by a working party “in the light of the relevant provisions of the Enabling Clause and of the GATT, including Article XXIV”, with the examination report being submitted to the CTD with a copy to the Council.

• Discriminatory treatment under RTAs became a topic of increasing concern over the years.

CRTA - Committee on Regional Trade Agreements • The CRTA, established by the General Council in February 1996 (WT/L/127) following a proposal by Canada made in

November 1995, is mandated to carry out the examination of RTAs (instead of individual working parties), to deal with the reporting on the operation of RTAs, to develop procedures to facilitate and improve their examination process, to provide a forum for the consideration of the systemic implications of RTAs and regional initiatives for the multilateral trading system and to carry out any additional functions assigned to it by the General Council.

• Despite the establishment of the CRTA in 1996, the examination of RTAs resulted in stalemate. From 1996 until 2013, not one examination report was adopted by the CRTA, mainly due to continuing disagreements over the inherent ambiguities in GATT Article XXIV, the absence of consensus on the format and content of examination reports under the WTO, the lack of information submitted by RTA parties, and the fact that the consistency of determination was to be made by all WTO members, including those whose RTAs were under examination.

• In 2004, celebrating the 10th anniversary of the WTO, the report from an eminent group of persons - the “Sutherland Report” –proposed a dual solution to counter the proliferation of RTA: “attacking them indirectly through effective reduction of MFN tariffs and non-tariff measures in multilateral trade negotiations” and “a clarification of Article XXIV and a better-organized means of administering its provisions …[by] entrusting the [WTO] Secretariat with the factual presentation of their agreements”.

RTAs and the Doha Development Agenda (DDA), launched in 2001

• These are developed in Module 4 of this Course. • In December 2006, the WTO members adopted a new Transparency Mechanism for Regional Trade Agreements

(WT/L/671) on a provisional basis. Work on systemic issues has continued but as of 2013 no result has been achieved.

3/3 Click here to go back to the

main text

WTO rules on RTAs

GATT X

XIV

Enabling

Cla

use

GATS V

Keywords (Basic principles)

• MFN • GATT Art. I (Trade in goods) • GATS Art. II (Trade in services) • TRIPS Art. 4 (TRIPS)

Keywords (Derogations)

• GATT Art. XXIV (Trade in goods) • Enabling Clause (Trade in goods)

RTAs between developing countries only

• GATS Art. V (Trade in services)

TEST YOUR

BRAIN

Without going back to your notes, try to elaborate on each of the keywords listed below, which correspond to elements discussed in the previous section

When you are through, continue

your journey through the RTA-related provisions

by clicking on one of the tabs on side.

Enabling

Cla

use

GATS V

WTO rules on RTAs

The initial legal foundation

The main, and longest-standing legal rule lies in Article XXIV of the original text of the GATT (GATT 1947). It entered into force on 1 January 1948.

At the time of the establishment of the WTO, in 1995, the provisions of the GATT 1947 were incorporated into the GATT 1994, and made part of the legal texts governing the trade relationships between the WTO Members. In addition the Understanding on the Interpretation of GATT Article XXIV was adopted, clarifying certain notions contained in the original text.

GATT Article XXIV

GATT X

XIV

Un

dersta

nd

ing

Ad

No

tes

GA

TT

XX

IV

Click on the icons to access each legal texts

WTO rules on RTAs

The principle

The first sentence (the “Chapeau”) of Paragraph 5 of Article XXIV presents the principle: The rules contained in the GATT (in particular its Article I establishing that trade measures adopted by governments may not discriminate on the basis of the origin of imported goods) shall not prevent WTO Members from creating(or entering into) free-trade areas or customs unions.

This Chapeau therefore establishes that free-trade areas (FTAs) and customs unions (CUs) may derogate from the MFN principle.

It also sets the forms of regional integration that are authorized (FTAs and CUs), though without defining the conditions to be fulfilled to qualify as an FTA or a CU (this is set out later in the paragraph and in subsequents paragraphs).

GATT Article XXIV, §5:

“(...) the provisions of [GATT] shall

not prevent, as between the

territories of contracting parties*,

the formation of a customs union or a

free-trade area or the adoption of an

interim agreement necessary for the

formation of a customs union or of a

free-trade area; Provided that: ...”

*Replace the term “contracting parties”, (original GATT text) by “WTO Members”.

Enabling

Cla

use

GATS V

G

ATT X

XIV

Click on the icon to access info on

the Case

GATT Article XXIV

WTO rules on RTAs

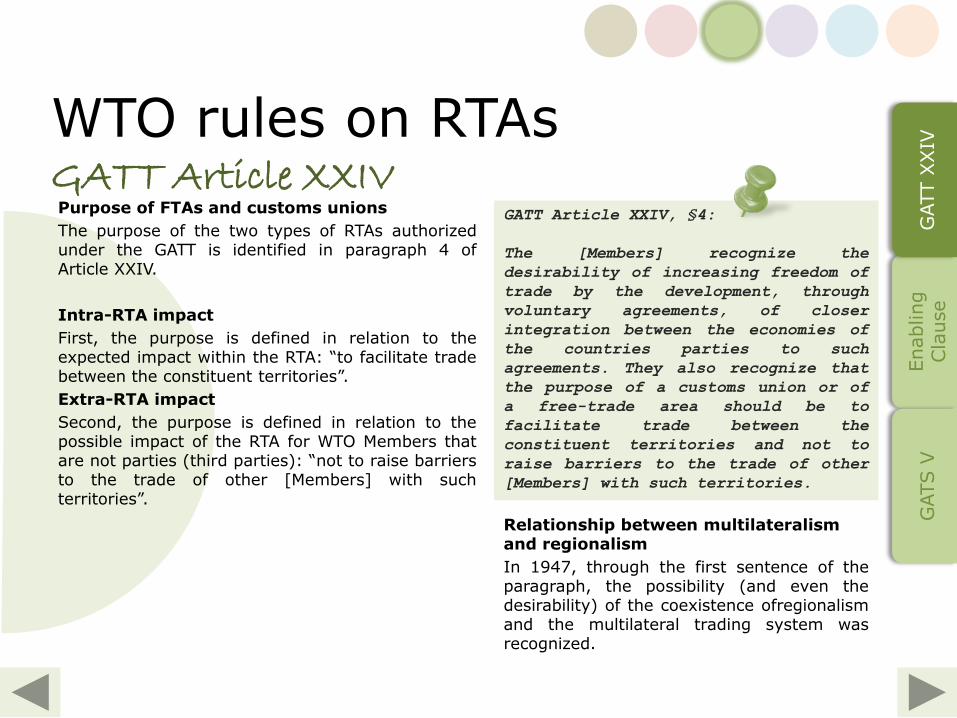

Purpose of FTAs and customs unions

The purpose of the two types of RTAs authorized under the GATT is identified in paragraph 4 of Article XXIV.

Intra-RTA impact

First, the purpose is defined in relation to the expected impact within the RTA: “to facilitate trade between the constituent territories”.

Extra-RTA impact

Second, the purpose is defined in relation to the possible impact of the RTA for WTO Members that are not parties (third parties): “not to raise barriers to the trade of other [Members] with such territories”.

GATT Article XXIV, §4:

The [Members] recognize the

desirability of increasing freedom of

trade by the development, through

voluntary agreements, of closer

integration between the economies of

the countries parties to such

agreements. They also recognize that

the purpose of a customs union or of

a free-trade area should be to

facilitate trade between the

constituent territories and not to

raise barriers to the trade of other

[Members] with such territories.

Enabling

Cla

use

GATS V

G

ATT X

XIV

Relationship between multilateralism and regionalism

In 1947, through the first sentence of the paragraph, the possibility (and even the desirability) of the coexistence ofregionalism and the multilateral trading system was recognized.

GATT Article XXIV

Enabling

Cla

use

GATS V

G

ATT X

XIV

WTO rules on RTAs

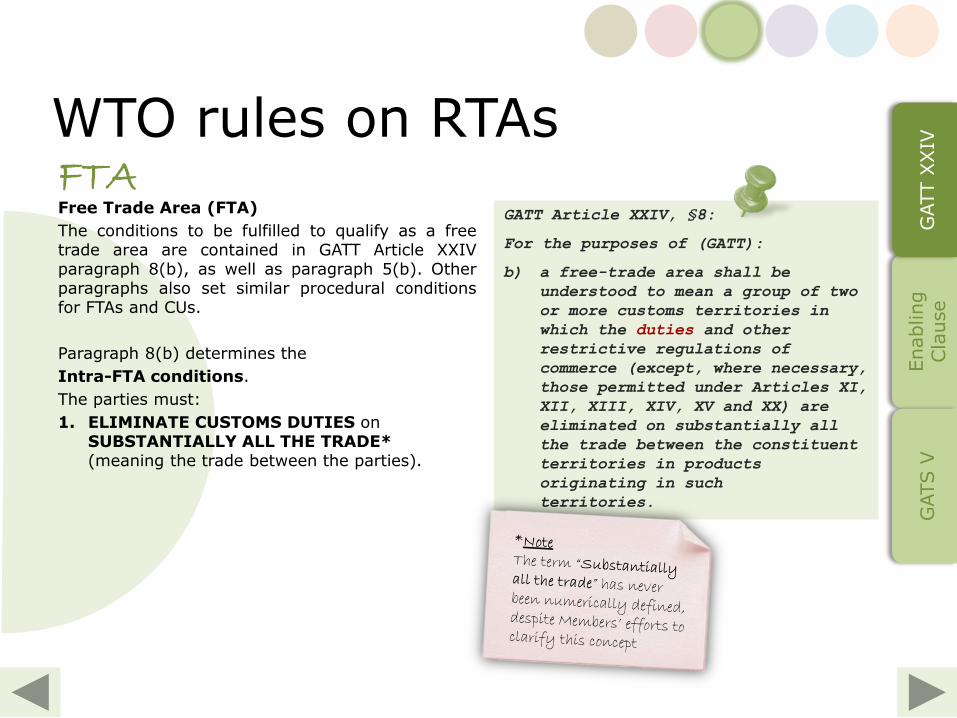

Free Trade Area (FTA)

The conditions to be fulfilled to qualify as a free trade area are contained in GATT Article XXIV paragraph 8(b), as well as paragraph 5(b). Other paragraphs also set similar procedural conditions for FTAs and CUs.

Paragraph 8(b) determines the

Intra-FTA conditions.

The parties must:

1. ELIMINATE CUSTOMS DUTIES on SUBSTANTIALLY ALL THE TRADE* (meaning the trade between the parties).

GATT Article XXIV, §8:

For the purposes of (GATT):

b) a free-trade area shall be

understood to mean a group of two

or more customs territories in

which the duties and other

restrictive regulations of

commerce (except, where necessary,

those permitted under Articles XI,

XII, XIII, XIV, XV and XX) are

eliminated on substantially all

the trade between the constituent

territories in products

originating in such

territories.

FTA

Enabling

Cla

use

GATS V

G

ATT X

XIV

WTO rules on RTAs

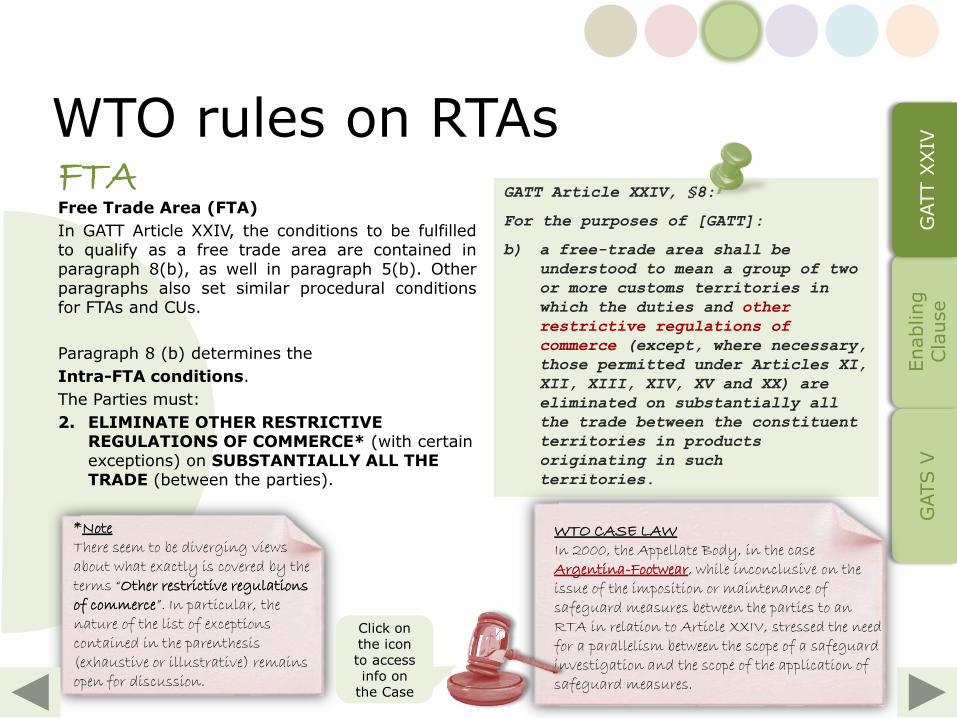

Free Trade Area (FTA)

In GATT Article XXIV, the conditions to be fulfilled to qualify as a free trade area are contained in paragraph 8(b), as well in paragraph 5(b). Other paragraphs also set similar procedural conditions for FTAs and CUs.

Paragraph 8 (b) determines the

Intra-FTA conditions.

The Parties must:

2. ELIMINATE OTHER RESTRICTIVE REGULATIONS OF COMMERCE* (with certain exceptions) on SUBSTANTIALLY ALL THE TRADE (between the parties).

GATT Article XXIV, §8:

For the purposes of [GATT]:

b) a free-trade area shall be

understood to mean a group of two

or more customs territories in

which the duties and other

restrictive regulations of

commerce (except, where necessary,

those permitted under Articles XI,

XII, XIII, XIV, XV and XX) are

eliminated on substantially all

the trade between the constituent

territories in products

originating in such

territories.

*Note There seem to be diverging views about what exactly is covered by the terms “Other restrictive regulations of commerce”. In particular, the nature of the list of exceptions contained in the parenthesis (exhaustive or illustrative) remains open for discussion.

Click on the icon to access info on

the Case

WTO CASE LAW In 2000, the Appellate Body, in the case Argentina-Footwear, while inconclusive on the issue of the imposition or maintenance of safeguard measures between the parties to an RTA in relation to Article XXIV, stressed the need for a parallelism between the scope of a safeguard investigation and the scope of the application of safeguard measures.

FTA

WTO rules on RTAs

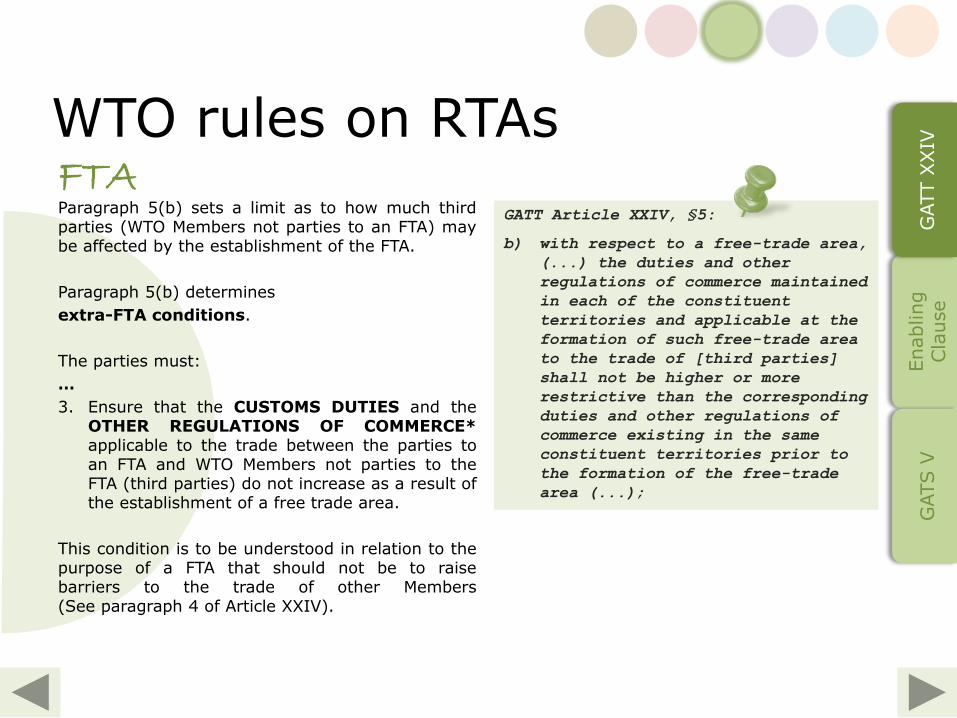

Paragraph 5(b) sets a limit as to how much third parties (WTO Members not parties to an FTA) may be affected by the establishment of the FTA.

Paragraph 5(b) determines

extra-FTA conditions.

The parties must:

…

3. Ensure that the CUSTOMS DUTIES and the OTHER REGULATIONS OF COMMERCE* applicable to the trade between the parties to an FTA and WTO Members not parties to the FTA (third parties) do not increase as a result of the establishment of a free trade area.

This condition is to be understood in relation to the purpose of a FTA that should not be to raise barriers to the trade of other Members (See paragraph 4 of Article XXIV).

GATT Article XXIV, §5:

b) with respect to a free-trade area,

(...) the duties and other

regulations of commerce maintained

in each of the constituent

territories and applicable at the

formation of such free-trade area

to the trade of [third parties]

shall not be higher or more

restrictive than the corresponding

duties and other regulations of

commerce existing in the same

constituent territories prior to

the formation of the free-trade

area (...);

Enabling

Cla

use

GATS V

G

ATT X

XIV

FTA

WTO rules on RTAs

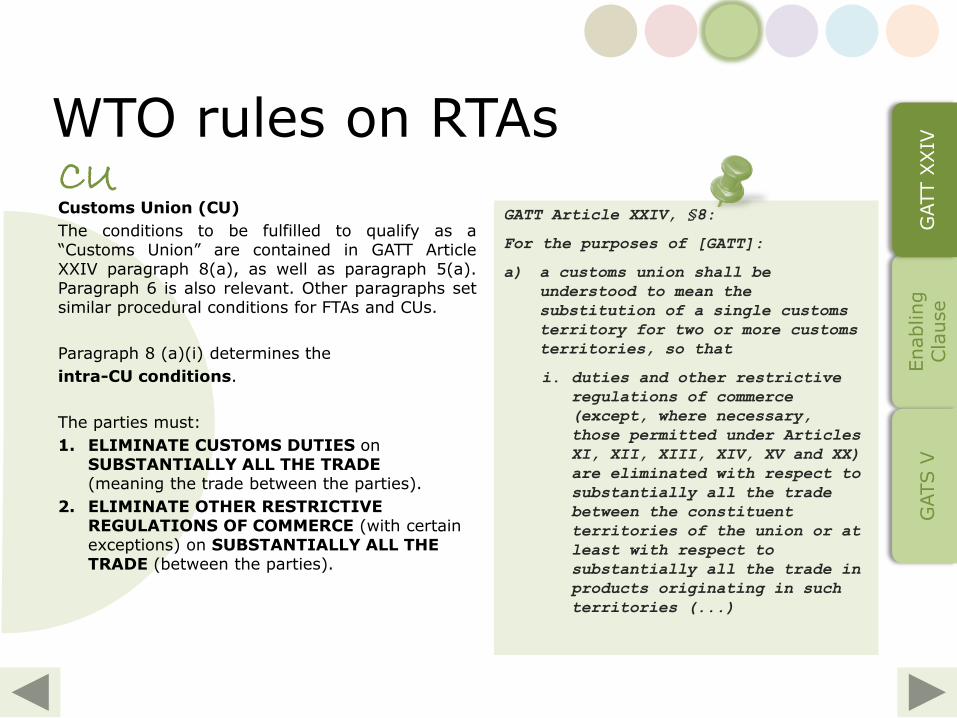

Customs Union (CU)

The conditions to be fulfilled to qualify as a “Customs Union” are contained in GATT Article XXIV paragraph 8(a), as well as paragraph 5(a). Paragraph 6 is also relevant. Other paragraphs set similar procedural conditions for FTAs and CUs.

Paragraph 8 (a)(i) determines the

intra-CU conditions.

The parties must:

1. ELIMINATE CUSTOMS DUTIES on SUBSTANTIALLY ALL THE TRADE (meaning the trade between the parties).

2. ELIMINATE OTHER RESTRICTIVE REGULATIONS OF COMMERCE (with certain exceptions) on SUBSTANTIALLY ALL THE TRADE (between the parties).

GATT Article XXIV, §8:

For the purposes of [GATT]:

a) a customs union shall be

understood to mean the

substitution of a single customs

territory for two or more customs

territories, so that

i. duties and other restrictive

regulations of commerce

(except, where necessary,

those permitted under Articles

XI, XII, XIII, XIV, XV and XX)

are eliminated with respect to

substantially all the trade

between the constituent

territories of the union or at

least with respect to

substantially all the trade in

products originating in such

territories (...)

Enabling

Cla

use

GATS V

G

ATT X

XIV

CU

WTO rules on RTAs

Paragraph 8(a)(ii) also contains an

extra-CU condition.

In essence it implies that :

3. a Common External Tariff (CET) (substantially all the same duties applied to third parties), and a common external regulatory trade regime (substantially all the same regulations of commerce applied to third parties) must be established.

GATT Article XXIV, §8:

For the purposes of [GATT]:

a) a customs union shall be

understood to mean the

substitution of a single customs

territory for two or more customs

territories, so that (...)

ii. substantially the same duties

and other regulations of

commerce are applied by each

of the members of the union to

the trade of territories not

included in the union (...)

Enabling

Cla

use

GATS V

G

ATT X

XIV

Country B

Country A

Country D

Country C

CU

WTO rules on RTAs

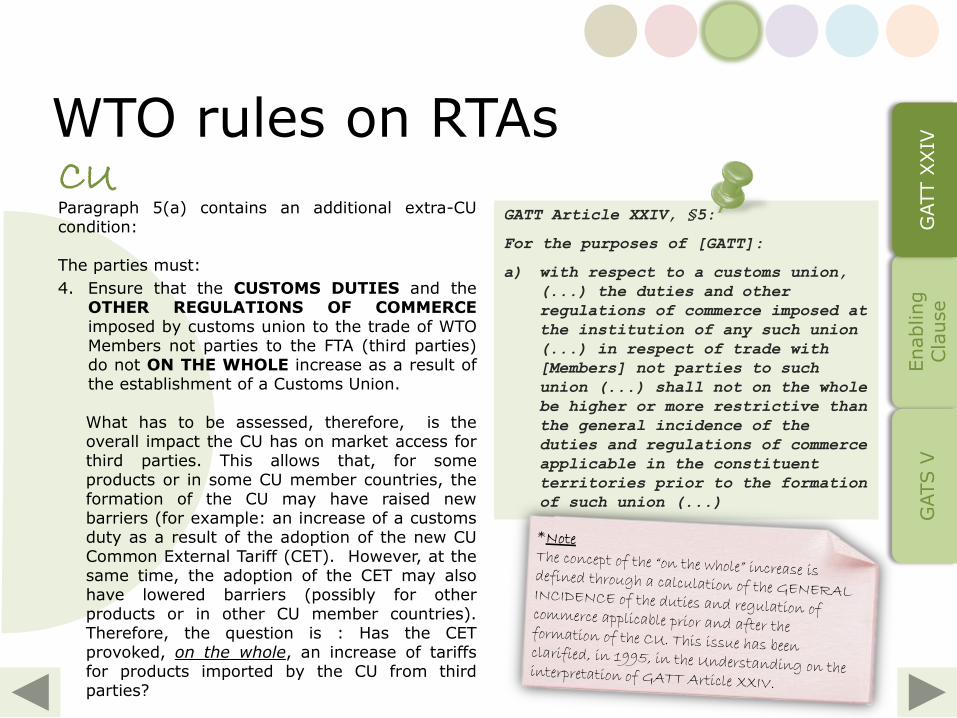

Paragraph 5(a) contains an additional extra-CU condition:

The parties must:

4. Ensure that the CUSTOMS DUTIES and the OTHER REGULATIONS OF COMMERCE imposed by customs union to the trade of WTO Members not parties to the FTA (third parties) do not ON THE WHOLE increase as a result of the establishment of a Customs Union.

What has to be assessed, therefore, is the overall impact the CU has on market access for third parties. This allows that, for some products or in some CU member countries, the formation of the CU may have raised new barriers (for example: an increase of a customs duty as a result of the adoption of the new CU Common External Tariff (CET). However, at the same time, the adoption of the CET may also have lowered barriers (possibly for other products or in other CU member countries). Therefore, the question is : Has the CET provoked, on the whole, an increase of tariffs for products imported by the CU from third parties?

GATT Article XXIV, §5:

For the purposes of [GATT]:

a) with respect to a customs union,

(...) the duties and other

regulations of commerce imposed at

the institution of any such union

(...) in respect of trade with

[Members] not parties to such

union (...) shall not on the whole

be higher or more restrictive than

the general incidence of the

duties and regulations of commerce

applicable in the constituent

territories prior to the formation

of such union (...)

Enabling

Cla

use

GATS V

G

ATT X

XIV

CU

WTO rules on RTAs

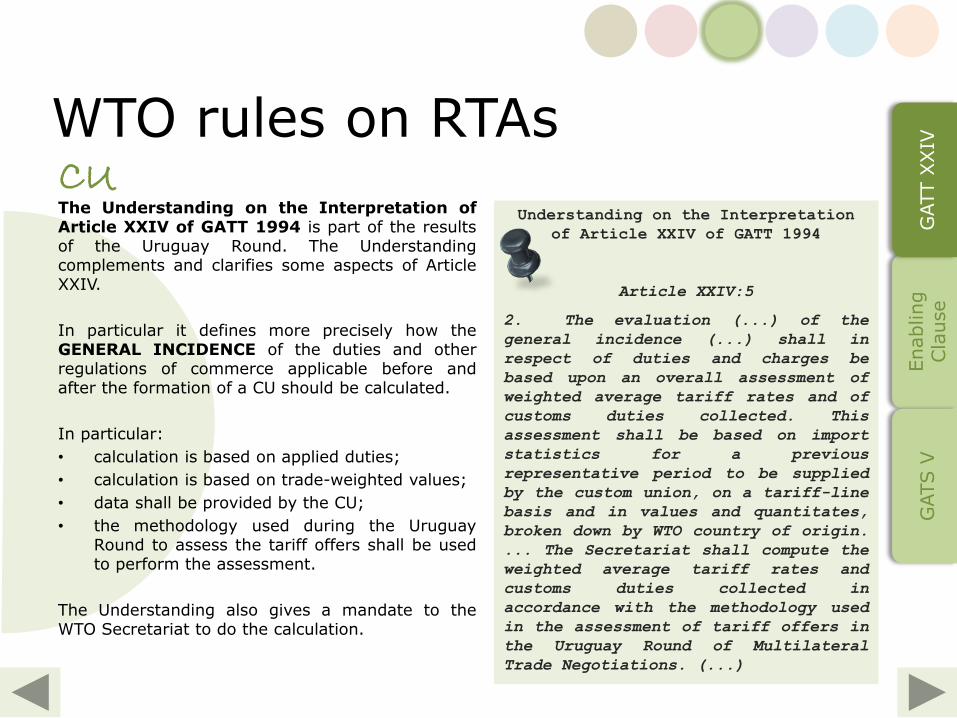

The Understanding on the Interpretation of Article XXIV of GATT 1994 is part of the results of the Uruguay Round. The Understanding complements and clarifies some aspects of Article XXIV.

In particular it defines more precisely how the GENERAL INCIDENCE of the duties and other regulations of commerce applicable before and after the formation of a CU should be calculated.

In particular:

• calculation is based on applied duties;

• calculation is based on trade-weighted values;

• data shall be provided by the CU;

• the methodology used during the Uruguay Round to assess the tariff offers shall be used to perform the assessment.

The Understanding also gives a mandate to the WTO Secretariat to do the calculation.

Understanding on the Interpretation

of Article XXIV of GATT 1994

...

Article XXIV:5

2. The evaluation (...) of the

general incidence (...) shall in

respect of duties and charges be

based upon an overall assessment of

weighted average tariff rates and of

customs duties collected. This

assessment shall be based on import

statistics for a previous

representative period to be supplied

by the custom union, on a tariff-line

basis and in values and quantitates,

broken down by WTO country of origin.

... The Secretariat shall compute the

weighted average tariff rates and

customs duties collected in

accordance with the methodology used

in the assessment of tariff offers in

the Uruguay Round of Multilateral

Trade Negotiations. (...)

Enabling

Cla

use

GATS V

G

ATT X

XIV

CU

WTO rules on RTAs

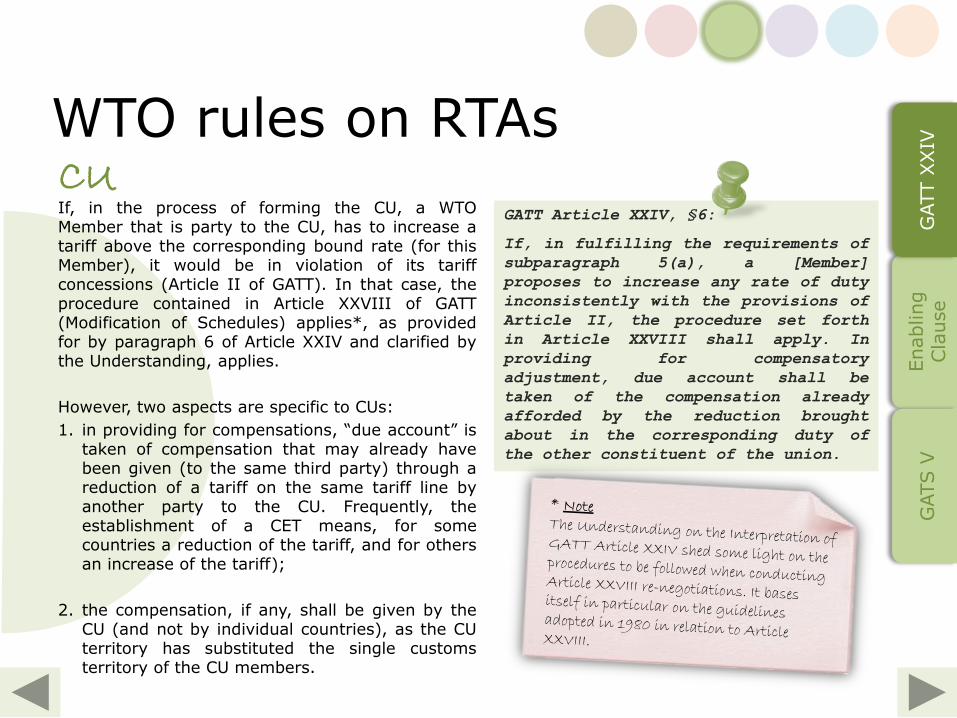

If, in the process of forming the CU, a WTO Member that is party to the CU, has to increase a tariff above the corresponding bound rate (for this Member), it would be in violation of its tariff concessions (Article II of GATT). In that case, the procedure contained in Article XXVIII of GATT (Modification of Schedules) applies*, as provided for by paragraph 6 of Article XXIV and clarified by the Understanding, applies.

However, two aspects are specific to CUs:

1. in providing for compensations, “due account” is taken of compensation that may already have been given (to the same third party) through a reduction of a tariff on the same tariff line by another party to the CU. Frequently, the establishment of a CET means, for some countries a reduction of the tariff, and for others an increase of the tariff);

2. the compensation, if any, shall be given by the CU (and not by individual countries), as the CU territory has substituted the single customs territory of the CU members.

GATT Article XXIV, §6:

If, in fulfilling the requirements of

subparagraph 5(a), a [Member]

proposes to increase any rate of duty

inconsistently with the provisions of

Article II, the procedure set forth

in Article XXVIII shall apply. In

providing for compensatory

adjustment, due account shall be

taken of the compensation already

afforded by the reduction brought

about in the corresponding duty of

the other constituent of the union.

Enabling

Cla

use

GATS V

G

ATT X

XIV

CU

WTO rules on RTAs

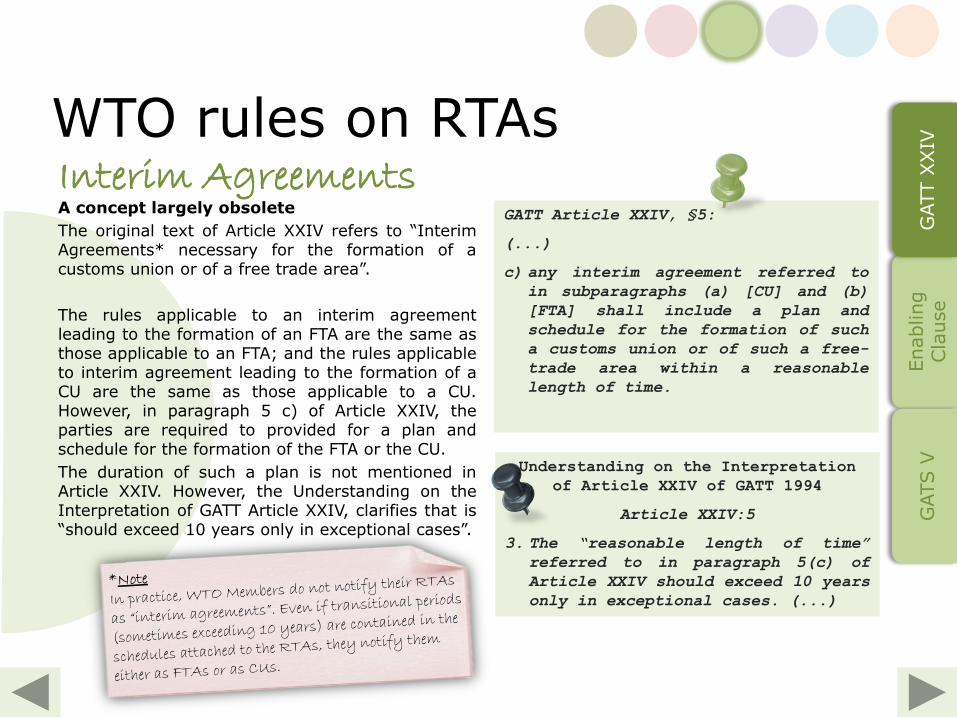

A concept largely obsolete

The original text of Article XXIV refers to “Interim Agreements* necessary for the formation of a customs union or of a free trade area”.

The rules applicable to an interim agreement leading to the formation of an FTA are the same as those applicable to an FTA; and the rules applicable to interim agreement leading to the formation of a CU are the same as those applicable to a CU. However, in paragraph 5 c) of Article XXIV, the parties are required to provided for a plan and schedule for the formation of the FTA or the CU.

The duration of such a plan is not mentioned in Article XXIV. However, the Understanding on the Interpretation of GATT Article XXIV, clarifies that is “should exceed 10 years only in exceptional cases”.

GATT Article XXIV, §5:

(...)

c) any interim agreement referred to

in subparagraphs (a) [CU] and (b)

[FTA] shall include a plan and

schedule for the formation of such

a customs union or of such a free-

trade area within a reasonable

length of time.

Understanding on the Interpretation

of Article XXIV of GATT 1994

Article XXIV:5

3. The “reasonable length of time”

referred to in paragraph 5(c) of

Article XXIV should exceed 10 years

only in exceptional cases. (...)

Enabling

Cla

use

GATS V

G

ATT X

XIV

Interim Agreements

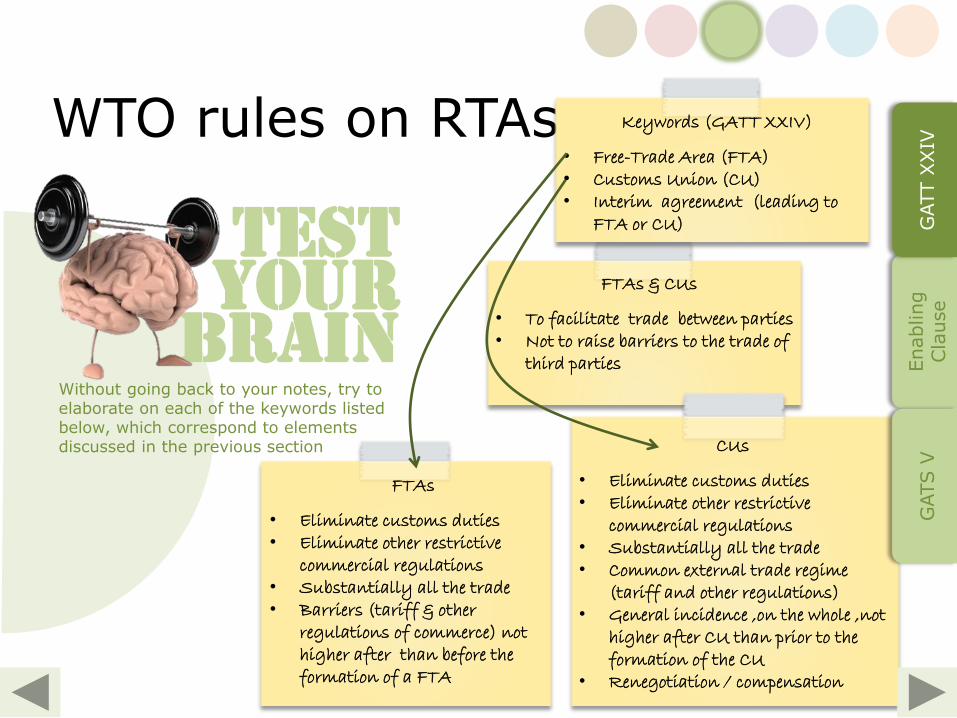

FTAs & CUs

• To facilitate trade between parties • Not to raise barriers to the trade of

third parties

WTO rules on RTAs

TEST YOUR

BRAIN Without going back to your notes, try to elaborate on each of the keywords listed below, which correspond to elements discussed in the previous section

Keywords (GATT XXIV)

• Free-Trade Area (FTA) • Customs Union (CU) • Interim agreement (leading to

FTA or CU)

FTAs

• Eliminate customs duties • Eliminate other restrictive

commercial regulations • Substantially all the trade • Barriers (tariff & other

regulations of commerce) not higher after than before the formation of a FTA

CUs

• Eliminate customs duties • Eliminate other restrictive

commercial regulations • Substantially all the trade • Common external trade regime

(tariff and other regulations) • General incidence ,on the whole ,not

higher after CU than prior to the formation of the CU

• Renegotiation / compensation

Enabling

Cla

use

GATS V

G

ATT X

XIV

GATT X

XIV

G

ATS V

WTO rules on RTAs

1979: Special and differential treatment for RTAs

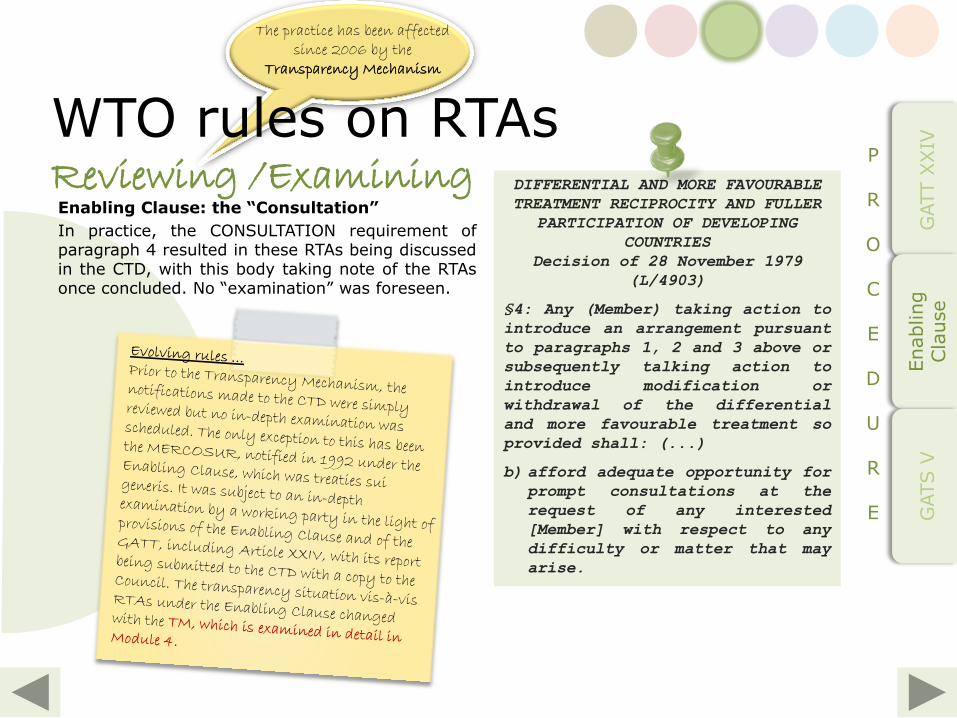

The Tokyo Round of multilateral trade negotiations ended, in 1979, with the adoption of a Decision entitled “Differential and More Favourable Treatment, Reciprocity and Fuller Participation of Developing Countries”. This Decision was later called the ENABLING CLAUSE because, inter alia, it enables developing countries to grant each other preferences without having to apply the MFN treatment to the other WTO Members. The Enabling Clause has contributed to make SPECIAL AND DIFFERENTIAL TREATMENT in favour of products from developing countries a permanent part of the legal framework of the multilateral trading system.

Enabling

Cla

use

Click on the icon to access the legal text

En

ab

lin

g C

lau

se

Enabling Clause

WTO rules on RTAs

The principle

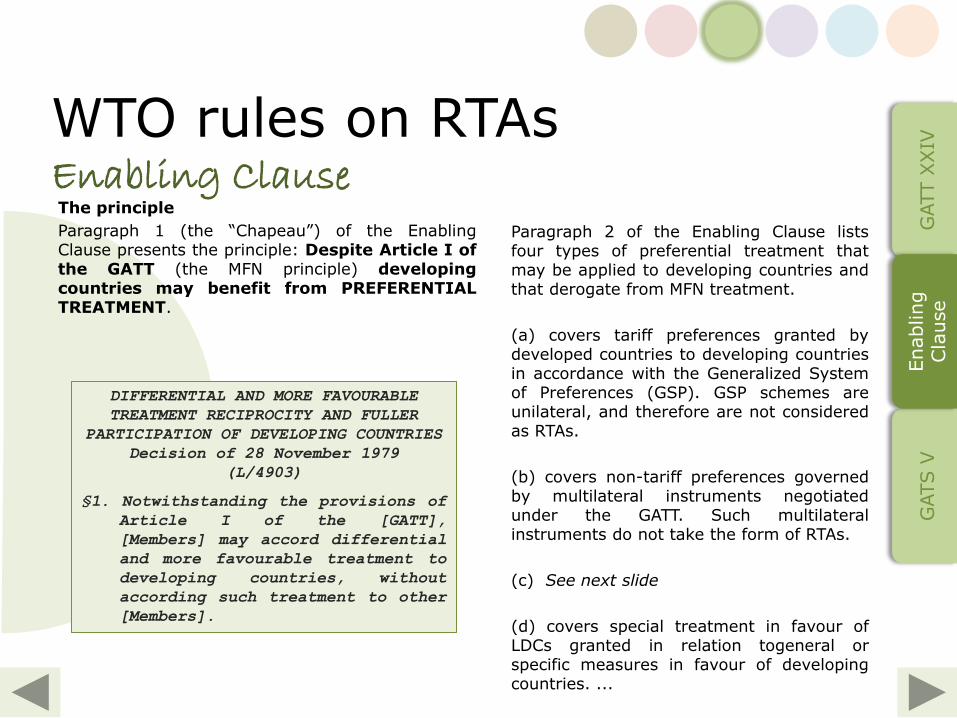

Paragraph 1 (the “Chapeau”) of the Enabling Clause presents the principle: Despite Article I of the GATT (the MFN principle) developing countries may benefit from PREFERENTIAL TREATMENT.

DIFFERENTIAL AND MORE FAVOURABLE

TREATMENT RECIPROCITY AND FULLER

PARTICIPATION OF DEVELOPING COUNTRIES

Decision of 28 November 1979

(L/4903)

§1. Notwithstanding the provisions of

Article I of the [GATT],

[Members] may accord differential

and more favourable treatment to

developing countries, without

according such treatment to other

[Members].

Paragraph 2 of the Enabling Clause lists four types of preferential treatment that may be applied to developing countries and that derogate from MFN treatment.

(a) covers tariff preferences granted by developed countries to developing countries in accordance with the Generalized System of Preferences (GSP). GSP schemes are unilateral, and therefore are not considered as RTAs.

(b) covers non-tariff preferences governed by multilateral instruments negotiated under the GATT. Such multilateral instruments do not take the form of RTAs.

(c) See next slide

(d) covers special treatment in favour of LDCs granted in relation togeneral or specific measures in favour of developing countries. ...

GATT X

XIV

G

ATS V

Enabling

Cla

use

Enabling Clause

WTO rules on RTAs

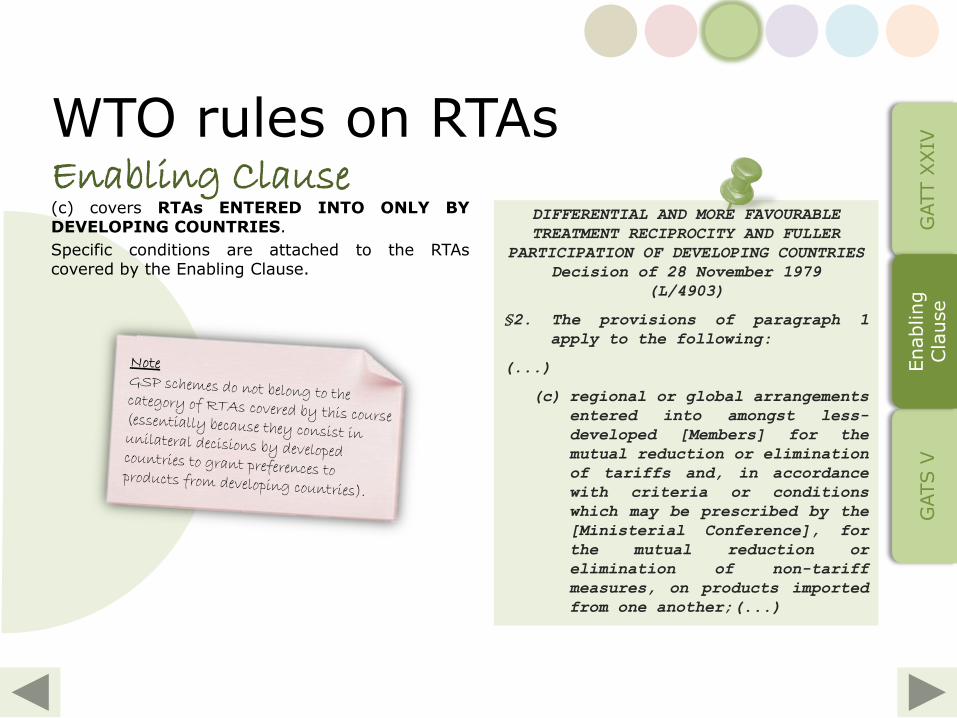

(c) covers RTAs ENTERED INTO ONLY BY DEVELOPING COUNTRIES.

Specific conditions are attached to the RTAs covered by the Enabling Clause.

DIFFERENTIAL AND MORE FAVOURABLE

TREATMENT RECIPROCITY AND FULLER

PARTICIPATION OF DEVELOPING COUNTRIES

Decision of 28 November 1979

(L/4903)

§2. The provisions of paragraph 1

apply to the following:

(...)

(c) regional or global arrangements

entered into amongst less-

developed [Members] for the

mutual reduction or elimination

of tariffs and, in accordance

with criteria or conditions

which may be prescribed by the

[Ministerial Conference], for

the mutual reduction or

elimination of non-tariff

measures, on products imported

from one another;(...)

GATT X

XIV

G

ATS V

Enabling

Cla

use

Enabling Clause

WTO rules on RTAs

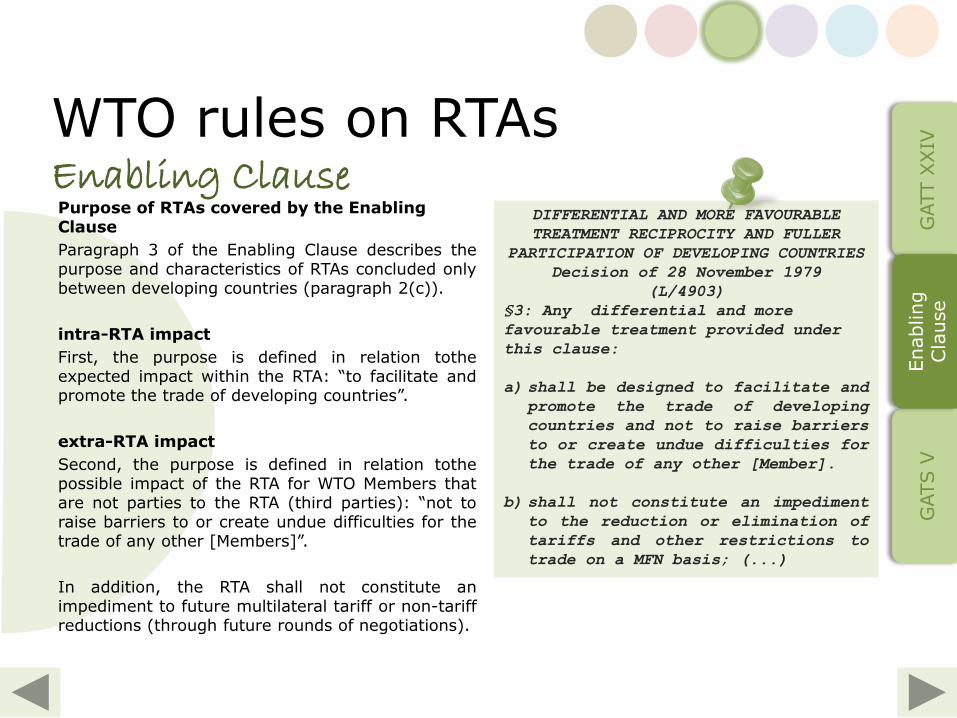

Purpose of RTAs covered by the Enabling Clause

Paragraph 3 of the Enabling Clause describes the purpose and characteristics of RTAs concluded only between developing countries (paragraph 2(c)).

intra-RTA impact

First, the purpose is defined in relation tothe expected impact within the RTA: “to facilitate and promote the trade of developing countries”.

extra-RTA impact

Second, the purpose is defined in relation tothe possible impact of the RTA for WTO Members that are not parties to the RTA (third parties): “not to raise barriers to or create undue difficulties for the trade of any other [Members]”.

In addition, the RTA shall not constitute an impediment to future multilateral tariff or non-tariff reductions (through future rounds of negotiations).

DIFFERENTIAL AND MORE FAVOURABLE

TREATMENT RECIPROCITY AND FULLER

PARTICIPATION OF DEVELOPING COUNTRIES

Decision of 28 November 1979

(L/4903)

§3: Any differential and more

favourable treatment provided under

this clause:

a) shall be designed to facilitate and

promote the trade of developing

countries and not to raise barriers

to or create undue difficulties for

the trade of any other [Member].

b) shall not constitute an impediment

to the reduction or elimination of

tariffs and other restrictions to

trade on a MFN basis; (...)

GATT X

XIV

G

ATS V

Enabling

Cla

use

Enabling Clause

WTO rules on RTAs

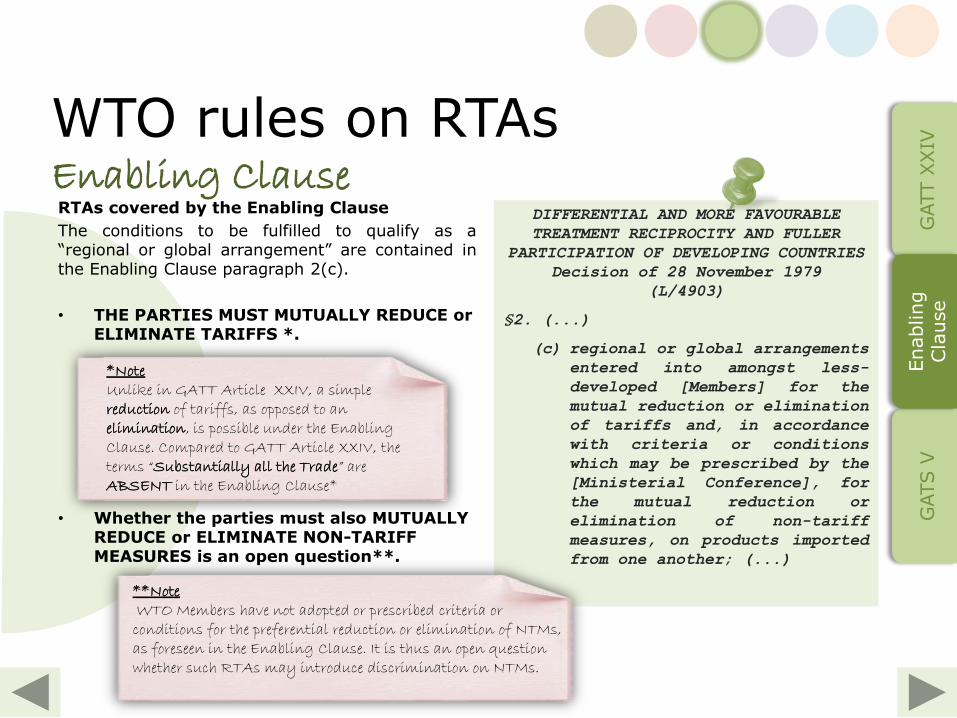

RTAs covered by the Enabling Clause

The conditions to be fulfilled to qualify as a “regional or global arrangement” are contained in the Enabling Clause paragraph 2(c).

• THE PARTIES MUST MUTUALLY REDUCE or ELIMINATE TARIFFS *.

• Whether the parties must also MUTUALLY REDUCE or ELIMINATE NON-TARIFF MEASURES is an open question**.

DIFFERENTIAL AND MORE FAVOURABLE

TREATMENT RECIPROCITY AND FULLER

PARTICIPATION OF DEVELOPING COUNTRIES

Decision of 28 November 1979

(L/4903)

§2. (...)

(c) regional or global arrangements

entered into amongst less-

developed [Members] for the

mutual reduction or elimination

of tariffs and, in accordance

with criteria or conditions

which may be prescribed by the

[Ministerial Conference], for

the mutual reduction or

elimination of non-tariff

measures, on products imported

from one another; (...)

...

*Note Unlike in GATT Article XXIV, a simple reduction of tariffs, as opposed to an elimination, is possible under the Enabling Clause. Compared to GATT Article XXIV, the terms “Substantially all the Trade” are ABSENT in the Enabling Clause*

**Note WTO Members have not adopted or prescribed criteria or conditions for the preferential reduction or elimination of NTMs, as foreseen in the Enabling Clause. It is thus an open question whether such RTAs may introduce discrimination on NTMs.

GATT X

XIV

G

ATS V

Enabling

Cla

use

Enabling Clause

WTO rules on RTAs

TEST YOUR

BRAIN Without going back to your notes, try to elaborate on each of the keywords listed below, which correspond to elements discussed in the previous section

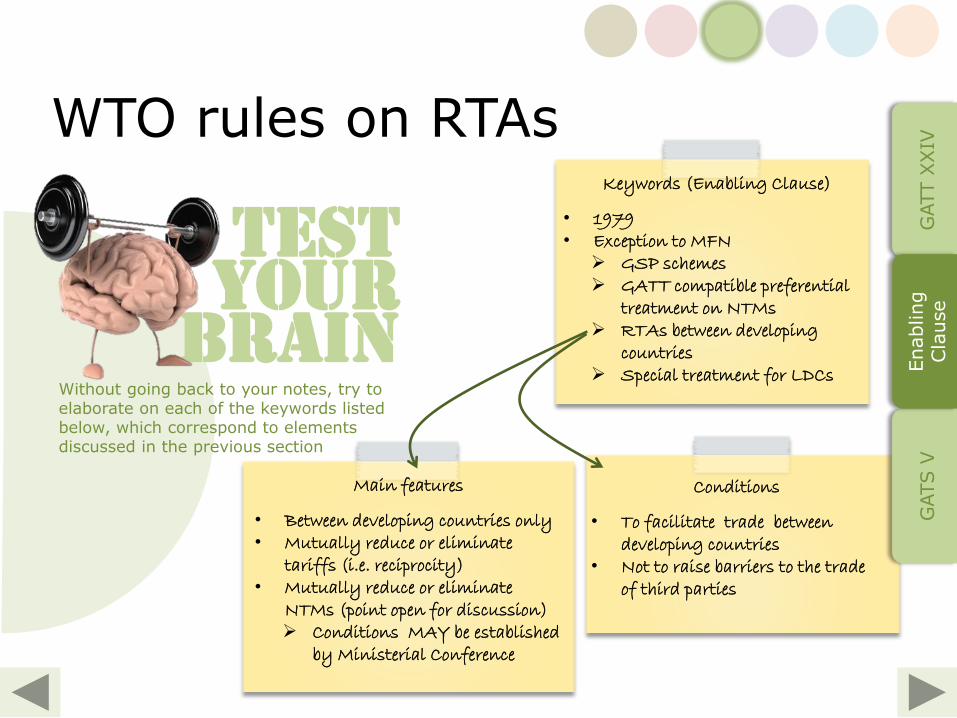

Keywords (Enabling Clause)

• 1979 • Exception to MFN

GSP schemes GATT compatible preferential

treatment on NTMs RTAs between developing

countries Special treatment for LDCs

Main features

• Between developing countries only • Mutually reduce or eliminate

tariffs (i.e. reciprocity) • Mutually reduce or eliminate

NTMs (point open for discussion) Conditions MAY be established

by Ministerial Conference

Conditions

• To facilitate trade between developing countries

• Not to raise barriers to the trade of third parties

GATT X

XIV

G

ATS V

Enabling

Cla

use

GATT X

XIV

Enabling

Cla

use

WTO rules on RTAs

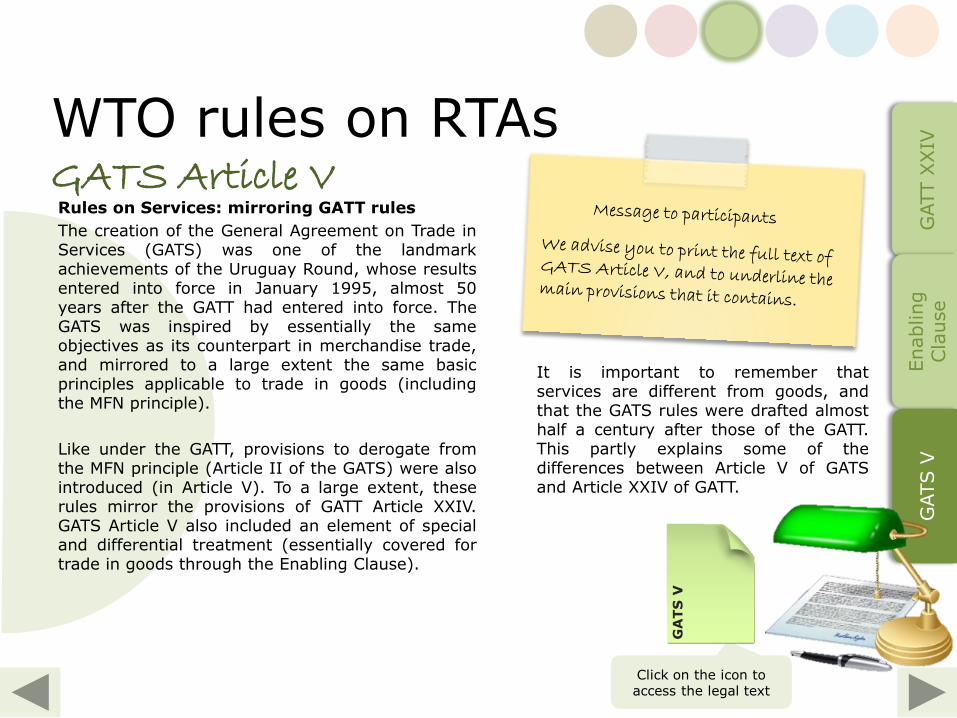

Rules on Services: mirroring GATT rules

The creation of the General Agreement on Trade in Services (GATS) was one of the landmark achievements of the Uruguay Round, whose results entered into force in January 1995, almost 50 years after the GATT had entered into force. The GATS was inspired by essentially the same objectives as its counterpart in merchandise trade, and mirrored to a large extent the same basic principles applicable to trade in goods (including the MFN principle).

Like under the GATT, provisions to derogate from the MFN principle (Article II of the GATS) were also introduced (in Article V). To a large extent, these rules mirror the provisions of GATT Article XXIV. GATS Article V also included an element of special and differential treatment (essentially covered for trade in goods through the Enabling Clause).

GATS V

Click on the icon to access the legal text

GA

TS

V

It is important to remember that services are different from goods, and that the GATS rules were drafted almost half a century after those of the GATT. This partly explains some of the differences between Article V of GATS and Article XXIV of GATT.

GATS Article V

WTO rules on RTAs

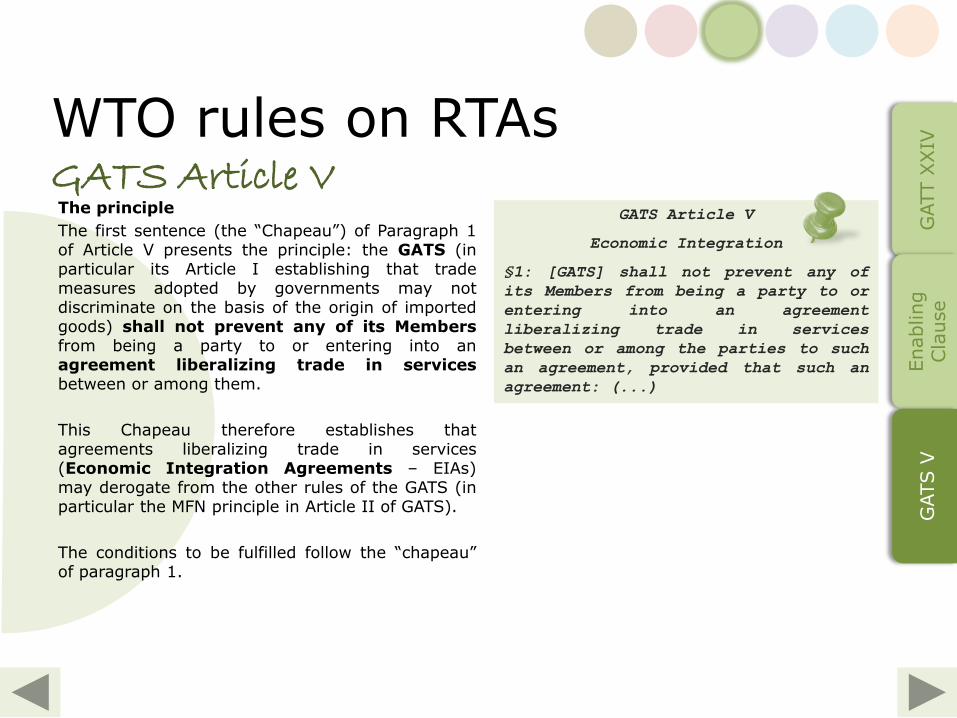

The principle

The first sentence (the “Chapeau”) of Paragraph 1 of Article V presents the principle: the GATS (in particular its Article I establishing that trade measures adopted by governments may not discriminate on the basis of the origin of imported goods) shall not prevent any of its Members from being a party to or entering into an agreement liberalizing trade in services between or among them.

This Chapeau therefore establishes that agreements liberalizing trade in services (Economic Integration Agreements – EIAs) may derogate from the other rules of the GATS (in particular the MFN principle in Article II of GATS).

The conditions to be fulfilled follow the “chapeau” of paragraph 1.

GATS Article V

Economic Integration

§1: [GATS] shall not prevent any of

its Members from being a party to or

entering into an agreement

liberalizing trade in services

between or among the parties to such

an agreement, provided that such an

agreement: (...)

GATT X

XIV

Enabling

Cla

use

GATS V

GATS Article V

WTO rules on RTAs

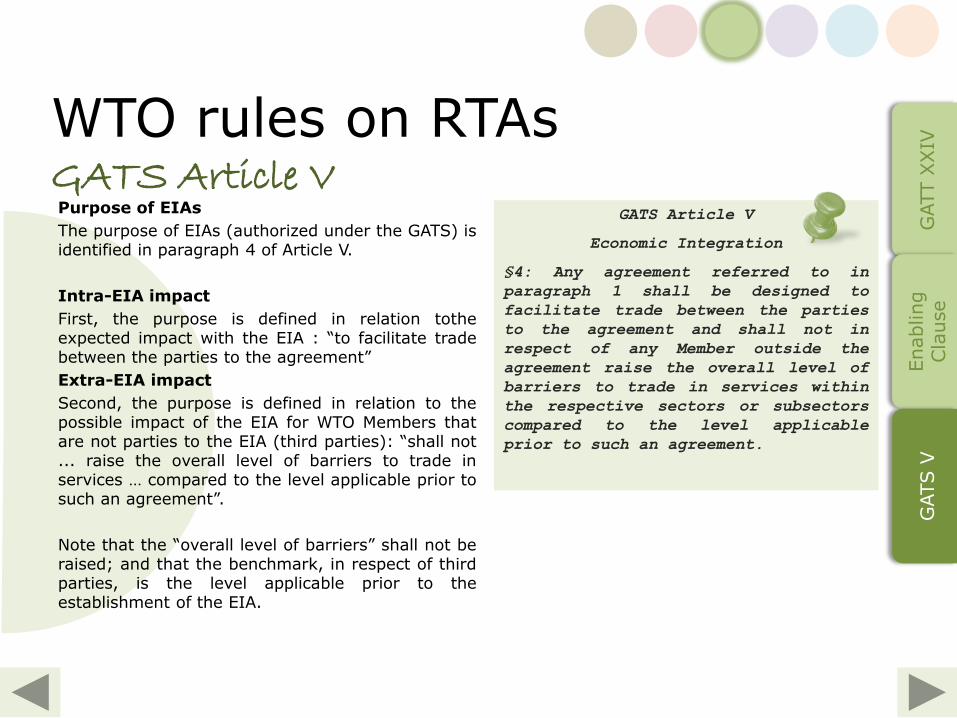

Purpose of EIAs

The purpose of EIAs (authorized under the GATS) is identified in paragraph 4 of Article V.

Intra-EIA impact

First, the purpose is defined in relation tothe expected impact with the EIA : “to facilitate trade between the parties to the agreement”

Extra-EIA impact

Second, the purpose is defined in relation to the possible impact of the EIA for WTO Members that are not parties to the EIA (third parties): “shall not ... raise the overall level of barriers to trade in services … compared to the level applicable prior to such an agreement”.

Note that the “overall level of barriers” shall not be raised; and that the benchmark, in respect of third parties, is the level applicable prior to the establishment of the EIA.

GATS Article V

Economic Integration

§4: Any agreement referred to in

paragraph 1 shall be designed to

facilitate trade between the parties

to the agreement and shall not in

respect of any Member outside the

agreement raise the overall level of

barriers to trade in services within

the respective sectors or subsectors

compared to the level applicable

prior to such an agreement.

GATT X

XIV

Enabling

Cla

use

GATS V

GATS Article V

WTO rules on RTAs

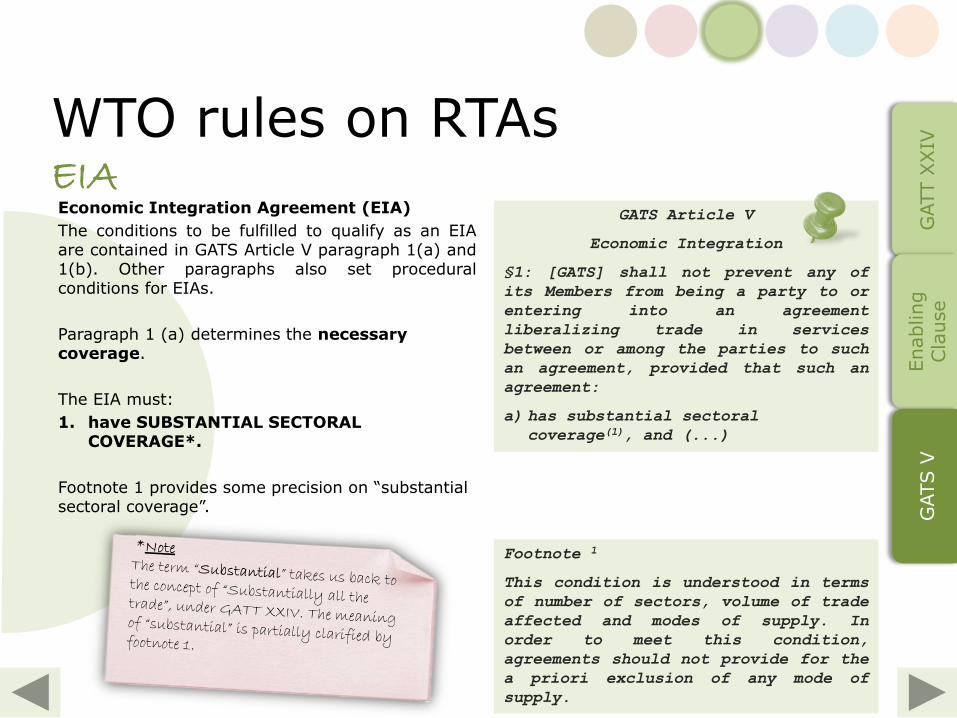

Economic Integration Agreement (EIA)

The conditions to be fulfilled to qualify as an EIA are contained in GATS Article V paragraph 1(a) and 1(b). Other paragraphs also set procedural conditions for EIAs.

Paragraph 1 (a) determines the necessary coverage.

The EIA must:

1. have SUBSTANTIAL SECTORAL COVERAGE*.

Footnote 1 provides some precision on “substantial sectoral coverage”.

GATS Article V

Economic Integration

§1: [GATS] shall not prevent any of

its Members from being a party to or

entering into an agreement

liberalizing trade in services

between or among the parties to such

an agreement, provided that such an

agreement:

a) has substantial sectoral

coverage(1), and (...)

Footnote 1

This condition is understood in terms

of number of sectors, volume of trade

affected and modes of supply. In

order to meet this condition,

agreements should not provide for the

a priori exclusion of any mode of

supply.

GATT X

XIV

Enabling

Cla

use

GATS V

EIA

WTO rules on RTAs

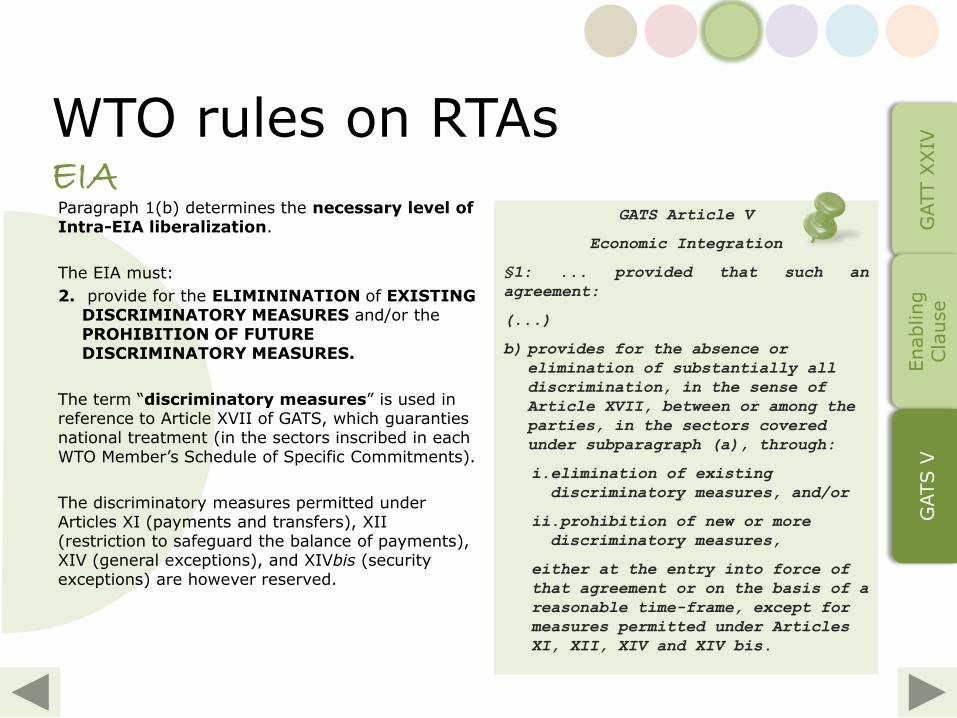

Paragraph 1(b) determines the necessary level of Intra-EIA liberalization.

The EIA must:

2. provide for the ELIMININATION of EXISTING DISCRIMINATORY MEASURES and/or the PROHIBITION OF FUTURE DISCRIMINATORY MEASURES.

The term “discriminatory measures” is used in reference to Article XVII of GATS, which guaranties national treatment (in the sectors inscribed in each WTO Member’s Schedule of Specific Commitments).

The discriminatory measures permitted under Articles XI (payments and transfers), XII (restriction to safeguard the balance of payments), XIV (general exceptions), and XIVbis (security exceptions) are however reserved.

GATS Article V

Economic Integration

§1: ... provided that such an

agreement:

(...)

b) provides for the absence or

elimination of substantially all

discrimination, in the sense of

Article XVII, between or among the

parties, in the sectors covered

under subparagraph (a), through:

i.elimination of existing

discriminatory measures, and/or

ii.prohibition of new or more

discriminatory measures,

either at the entry into force of

that agreement or on the basis of a

reasonable time-frame, except for

measures permitted under Articles

XI, XII, XIV and XIV bis.

GATT X

XIV

Enabling

Cla

use

GATS V

EIA

WTO rules on RTAs

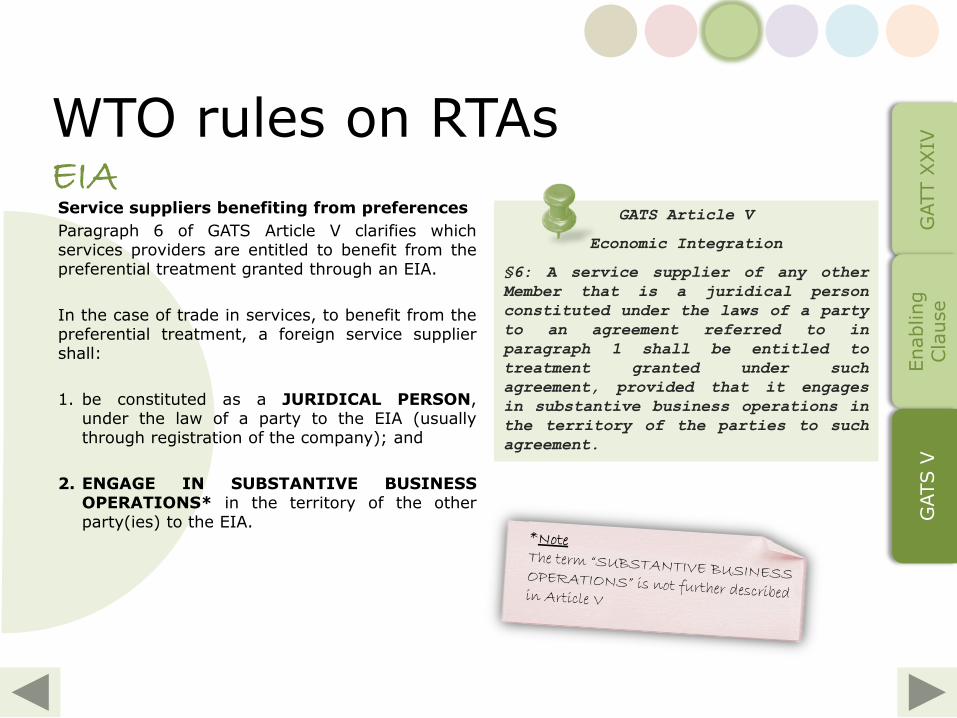

Service suppliers benefiting from preferences

Paragraph 6 of GATS Article V clarifies which services providers are entitled to benefit from the preferential treatment granted through an EIA.

In the case of trade in services, to benefit from the preferential treatment, a foreign service supplier shall:

1. be constituted as a JURIDICAL PERSON, under the law of a party to the EIA (usually through registration of the company); and

2. ENGAGE IN SUBSTANTIVE BUSINESS OPERATIONS* in the territory of the other party(ies) to the EIA.

GATS Article V

Economic Integration

§6: A service supplier of any other

Member that is a juridical person

constituted under the laws of a party

to an agreement referred to in

paragraph 1 shall be entitled to

treatment granted under such

agreement, provided that it engages

in substantive business operations in

the territory of the parties to such

agreement.

GATT X

XIV

Enabling

Cla

use

GATS V

EIA

WTO rules on RTAs

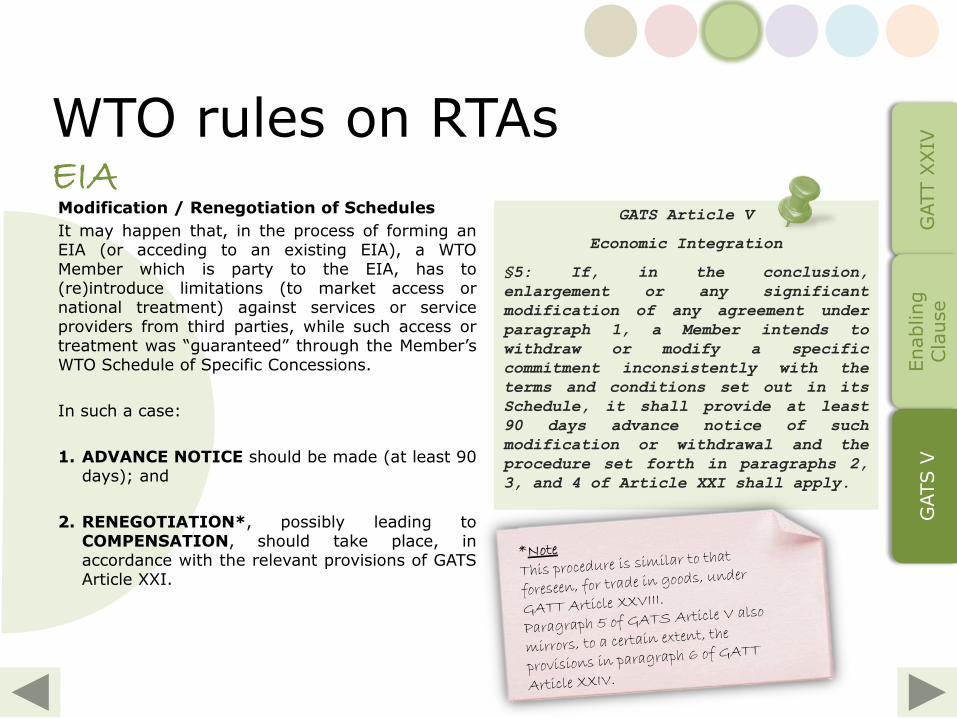

Modification / Renegotiation of Schedules

It may happen that, in the process of forming an EIA (or acceding to an existing EIA), a WTO Member which is party to the EIA, has to (re)introduce limitations (to market access or national treatment) against services or service providers from third parties, while such access or treatment was “guaranteed” through the Member’s WTO Schedule of Specific Concessions.

In such a case:

1. ADVANCE NOTICE should be made (at least 90 days); and

2. RENEGOTIATION*, possibly leading to COMPENSATION, should take place, in accordance with the relevant provisions of GATS Article XXI.

GATS Article V

Economic Integration

§5: If, in the conclusion,

enlargement or any significant

modification of any agreement under

paragraph 1, a Member intends to

withdraw or modify a specific

commitment inconsistently with the

terms and conditions set out in its

Schedule, it shall provide at least

90 days advance notice of such

modification or withdrawal and the

procedure set forth in paragraphs 2,

3, and 4 of Article XXI shall apply.

GATT X

XIV

Enabling

Cla

use

GATS V

EIA

WTO rules on RTAs

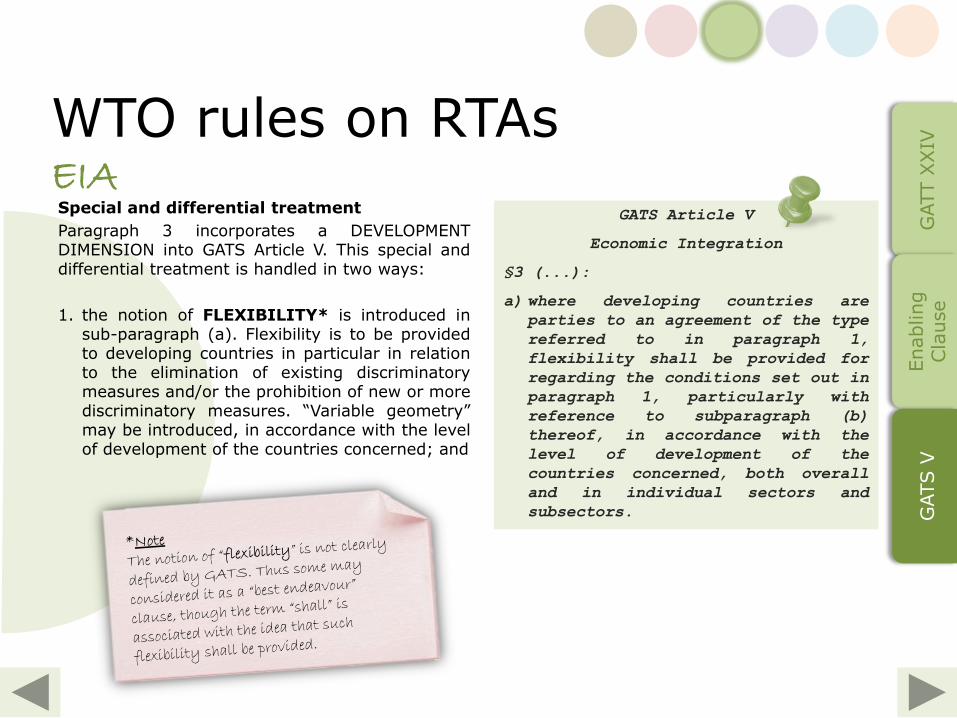

Special and differential treatment

Paragraph 3 incorporates a DEVELOPMENT DIMENSION into GATS Article V. This special and differential treatment is handled in two ways:

1. the notion of FLEXIBILITY* is introduced in sub-paragraph (a). Flexibility is to be provided to developing countries in particular in relation to the elimination of existing discriminatory measures and/or the prohibition of new or more discriminatory measures. “Variable geometry” may be introduced, in accordance with the level of development of the countries concerned; and

GATS Article V

Economic Integration

§3 (...):

a) where developing countries are

parties to an agreement of the type

referred to in paragraph 1,

flexibility shall be provided for

regarding the conditions set out in

paragraph 1, particularly with

reference to subparagraph (b)

thereof, in accordance with the

level of development of the

countries concerned, both overall

and in individual sectors and

subsectors.

GATT X

XIV

Enabling

Cla

use

GATS V

EIA

WTO rules on RTAs

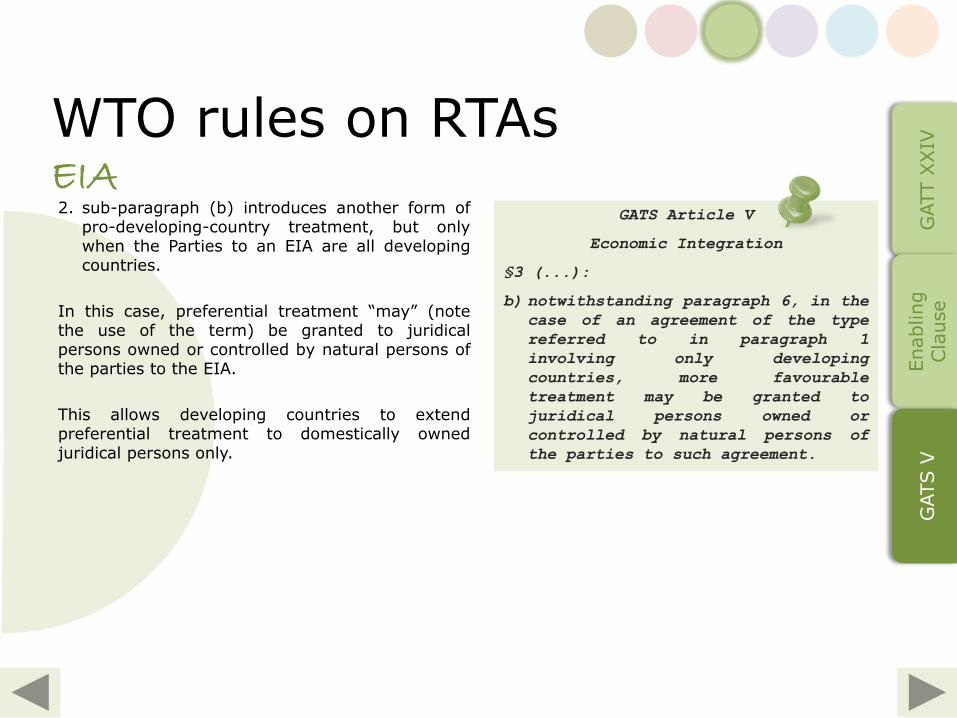

2. sub-paragraph (b) introduces another form of pro-developing-country treatment, but only when the Parties to an EIA are all developing countries.

In this case, preferential treatment “may” (note the use of the term) be granted to juridical persons owned or controlled by natural persons of the parties to the EIA.

This allows developing countries to extend preferential treatment to domestically owned juridical persons only.

GATS Article V

Economic Integration

§3 (...):

b) notwithstanding paragraph 6, in the

case of an agreement of the type

referred to in paragraph 1

involving only developing

countries, more favourable

treatment may be granted to

juridical persons owned or

controlled by natural persons of

the parties to such agreement.

GATT X

XIV

Enabling

Cla

use

GATS V

EIA

WTO rules on RTAs

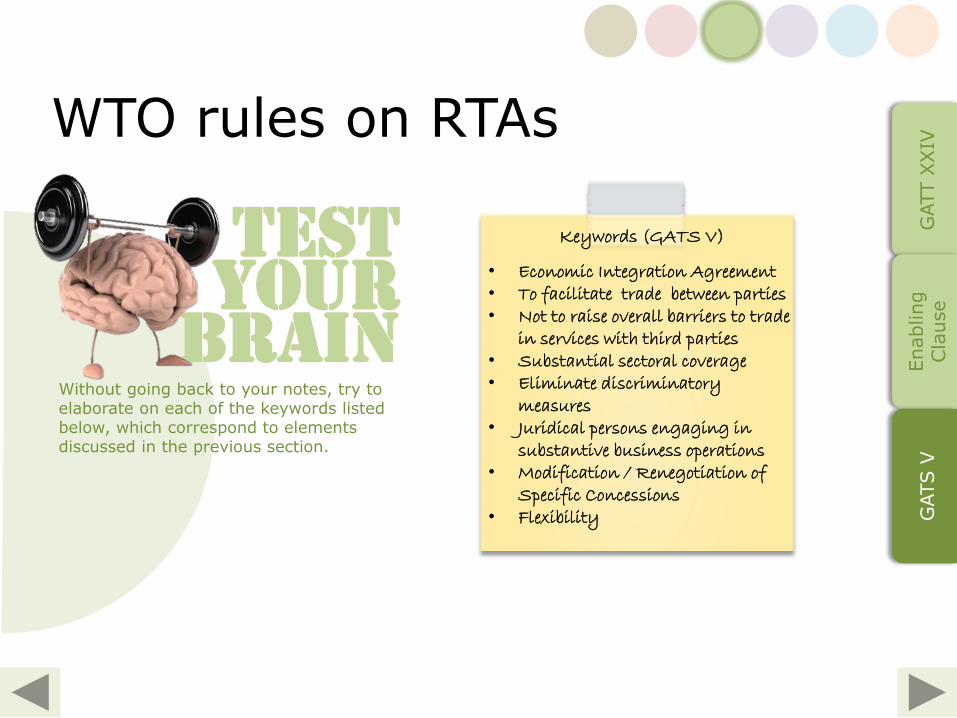

TEST YOUR

BRAIN Without going back to your notes, try to elaborate on each of the keywords listed below, which correspond to elements discussed in the previous section.

Keywords (GATS V)

• Economic Integration Agreement • To facilitate trade between parties • Not to raise overall barriers to trade

in services with third parties • Substantial sectoral coverage • Eliminate discriminatory

measures • Juridical persons engaging in

substantive business operations • Modification / Renegotiation of

Specific Concessions • Flexibility

GATT X

XIV

Enabling

Cla

use

GATS V

The practice has been affected since 2006 by the

Transparency Mechanism

P R

O C E

D

U R E

WTO rules on RTAs

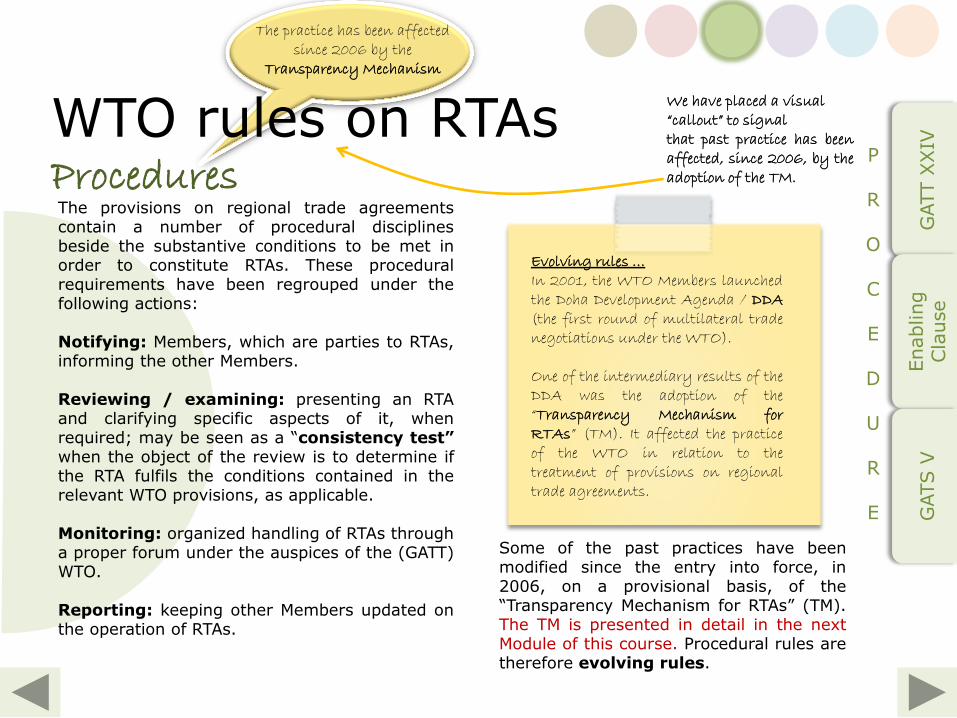

The provisions on regional trade agreements contain a number of procedural disciplines beside the substantive conditions to be met in order to constitute RTAs. These procedural requirements have been regrouped under the following actions:

Notifying: Members, which are parties to RTAs, informing the other Members.

Reviewing / examining: presenting an RTA and clarifying specific aspects of it, when required; may be seen as a “consistency test” when the object of the review is to determine if the RTA fulfils the conditions contained in the relevant WTO provisions, as applicable.

Monitoring: organized handling of RTAs through a proper forum under the auspices of the (GATT) WTO.

Reporting: keeping other Members updated on the operation of RTAs.

Procedures

GATT X

XIV

Enabling

Cla

use

GATS V

Evolving rules … In 2001, the WTO Members launched the Doha Development Agenda / DDA (the first round of multilateral trade negotiations under the WTO). One of the intermediary results of the DDA was the adoption of the “Transparency Mechanism for RTAs” (TM). It affected the practice of the WTO in relation to the treatment of provisions on regional trade agreements.

We have placed a visual “callout” to signal that past practice has been affected, since 2006, by the adoption of the TM.

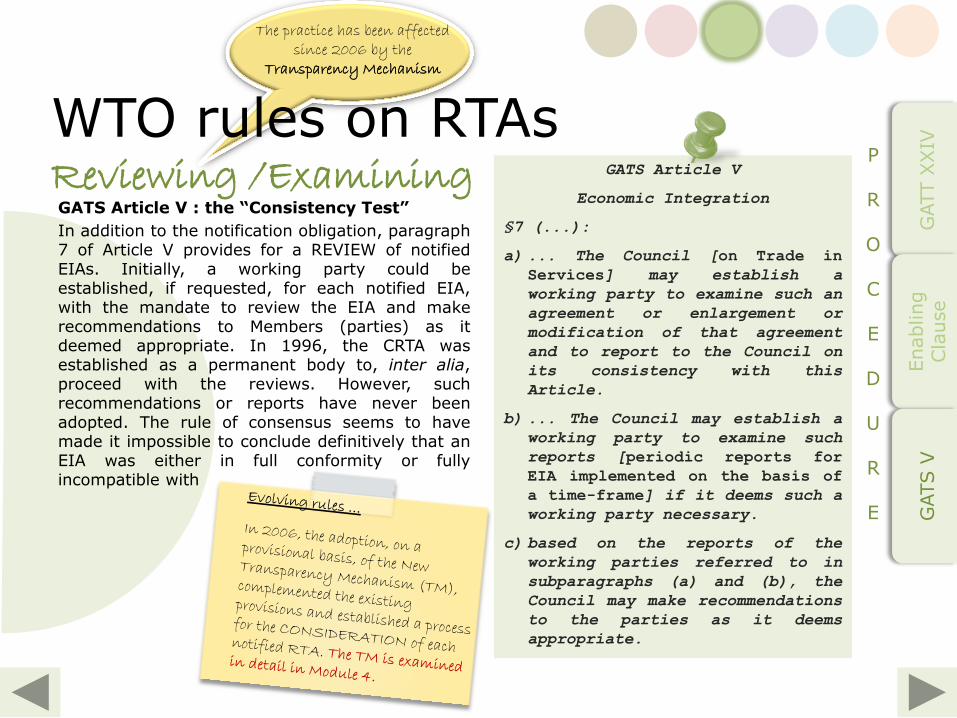

Some of the past practices have been modified since the entry into force, in 2006, on a provisional basis, of the “Transparency Mechanism for RTAs” (TM). The TM is presented in detail in the next Module of this course. Procedural rules are therefore evolving rules.

The practice has been affected since 2006 by the

Transparency Mechanism

Article XXIV of GATT 1994

GATT §7 (...):

a) any [Member] deciding to enter

into a customs union or free-

trade area, (...) shall

promptly notify the

[Ministerial Conference] and

shall make available to it

such information regarding the

proposed union or area as will

enable [it] to make such

reports and recommendations to

[Members] as it may deem

appropriate.

WTO rules on RTAs

GATT Article XXIV

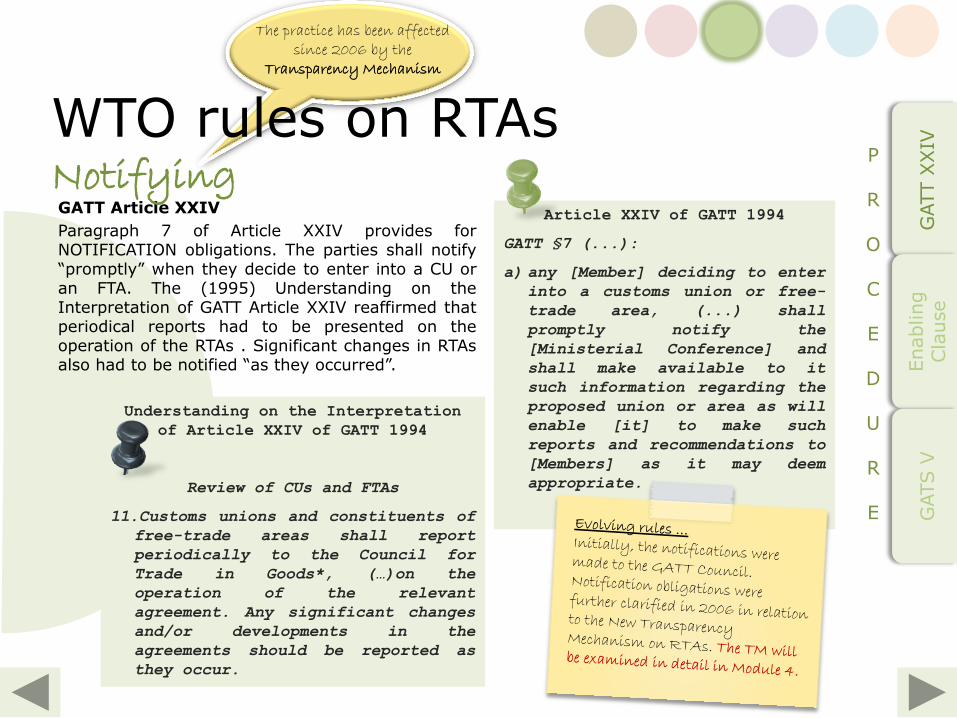

Paragraph 7 of Article XXIV provides for NOTIFICATION obligations. The parties shall notify “promptly” when they decide to enter into a CU or an FTA. The (1995) Understanding on the Interpretation of GATT Article XXIV reaffirmed that periodical reports had to be presented on the operation of the RTAs . Significant changes in RTAs also had to be notified “as they occurred”.

Understanding on the Interpretation

of Article XXIV of GATT 1994

...

Review of CUs and FTAs

11.Customs unions and constituents of

free-trade areas shall report

periodically to the Council for

Trade in Goods*, (…)on the

operation of the relevant

agreement. Any significant changes

and/or developments in the

agreements should be reported as

they occur.

Notifying P R

O C E

D

U R E

GATT X

XIV

Enabling

Cla

use

GATS V

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

Enabling Clause

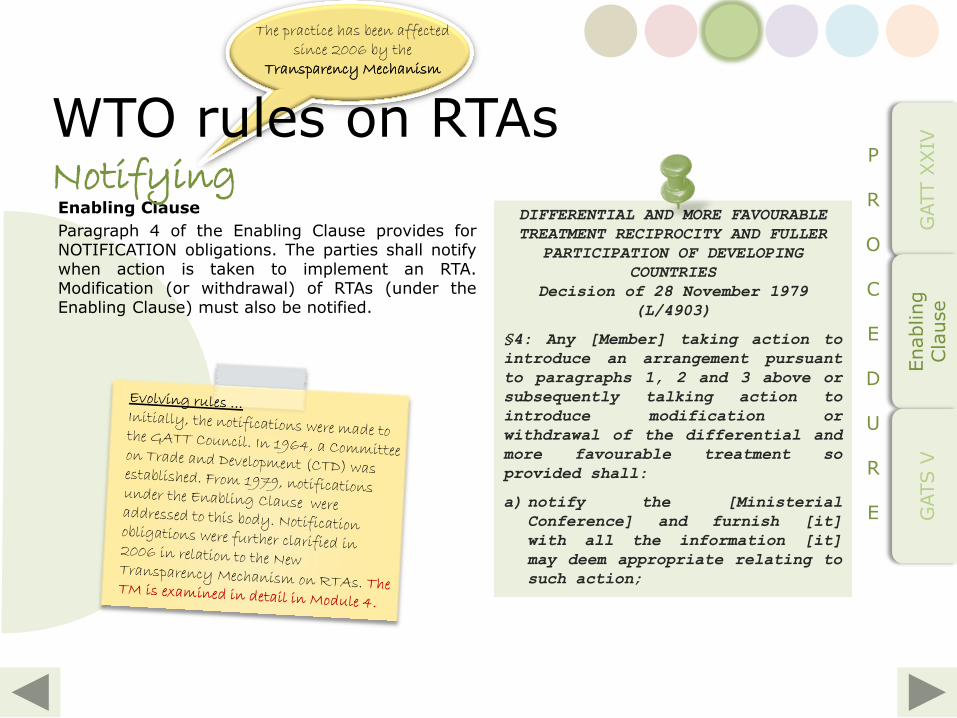

Paragraph 4 of the Enabling Clause provides for NOTIFICATION obligations. The parties shall notify when action is taken to implement an RTA. Modification (or withdrawal) of RTAs (under the Enabling Clause) must also be notified.

DIFFERENTIAL AND MORE FAVOURABLE

TREATMENT RECIPROCITY AND FULLER

PARTICIPATION OF DEVELOPING

COUNTRIES

Decision of 28 November 1979

(L/4903)

§4: Any [Member] taking action to

introduce an arrangement pursuant

to paragraphs 1, 2 and 3 above or

subsequently talking action to

introduce modification or

withdrawal of the differential and

more favourable treatment so

provided shall:

a) notify the [Ministerial

Conference] and furnish [it]

with all the information [it]

may deem appropriate relating to

such action;

Notifying P R

O C E

D

U R E

GATT X

XIV

Enabling

Cla

use

GATS V

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

GATS V

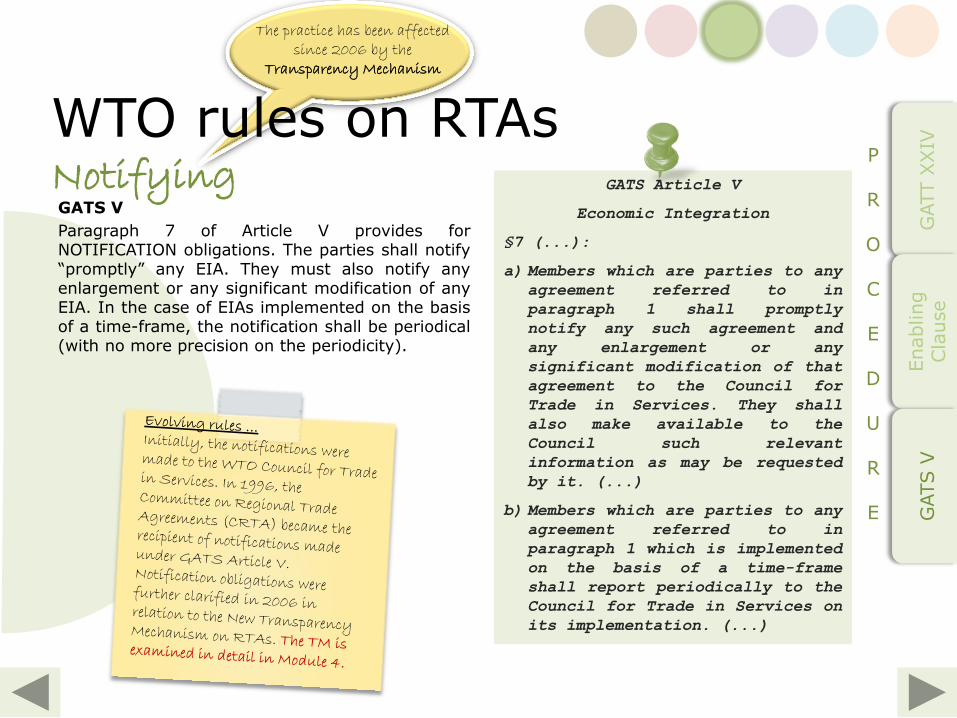

Paragraph 7 of Article V provides for NOTIFICATION obligations. The parties shall notify “promptly” any EIA. They must also notify any enlargement or any significant modification of any EIA. In the case of EIAs implemented on the basis of a time-frame, the notification shall be periodical (with no more precision on the periodicity).

GATS Article V

Economic Integration

§7 (...):

a) Members which are parties to any

agreement referred to in

paragraph 1 shall promptly

notify any such agreement and

any enlargement or any

significant modification of that

agreement to the Council for

Trade in Services. They shall

also make available to the

Council such relevant

information as may be requested

by it. (...)

b) Members which are parties to any

agreement referred to in

paragraph 1 which is implemented

on the basis of a time-frame

shall report periodically to the

Council for Trade in Services on

its implementation. (...)

Notifying P R

O C E

D

U R E

GATT X

XIV

Enabling

Cla

use

GATS V

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

GATT Article XXIV: the “Consistency Test”(I)

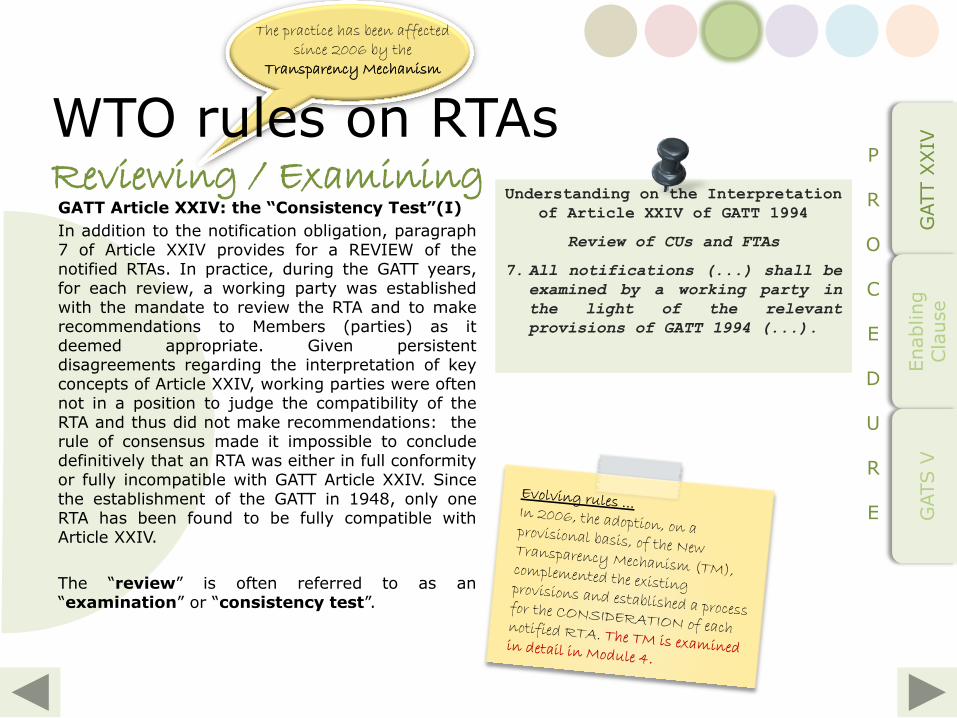

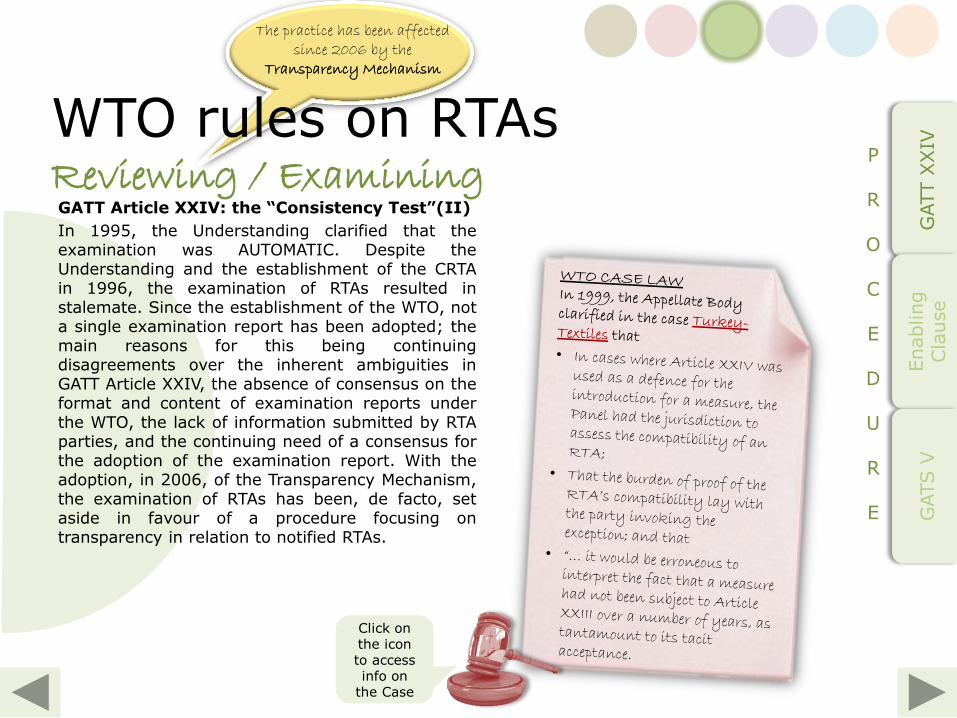

In addition to the notification obligation, paragraph 7 of Article XXIV provides for a REVIEW of the notified RTAs. In practice, during the GATT years, for each review, a working party was established with the mandate to review the RTA and to make recommendations to Members (parties) as it deemed appropriate. Given persistent disagreements regarding the interpretation of key concepts of Article XXIV, working parties were often not in a position to judge the compatibility of the RTA and thus did not make recommendations: the rule of consensus made it impossible to conclude definitively that an RTA was either in full conformity or fully incompatible with GATT Article XXIV. Since the establishment of the GATT in 1948, only one RTA has been found to be fully compatible with Article XXIV.

The “review” is often referred to as an “examination” or “consistency test”.

Understanding on the Interpretation

of Article XXIV of GATT 1994

Review of CUs and FTAs

7. All notifications (...) shall be

examined by a working party in

the light of the relevant

provisions of GATT 1994 (...).

Reviewing / Examining P R

O C E

D

U R E

GATT X

XIV

Enabling

Cla

use

GATS V

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

GATT Article XXIV: the “Consistency Test”(II)

In 1995, the Understanding clarified that the examination was AUTOMATIC. Despite the Understanding and the establishment of the CRTA in 1996, the examination of RTAs resulted in stalemate. Since the establishment of the WTO, not a single examination report has been adopted; the main reasons for this being continuing disagreements over the inherent ambiguities in GATT Article XXIV, the absence of consensus on the format and content of examination reports under the WTO, the lack of information submitted by RTA parties, and the continuing need of a consensus for the adoption of the examination report. With the adoption, in 2006, of the Transparency Mechanism, the examination of RTAs has been, de facto, set aside in favour of a procedure focusing on transparency in relation to notified RTAs.

Reviewing / Examining P R

O C E

D

U R E

GATT X

XIV

Enabling

Cla

use

GATS V

Click on the icon to access info on

the Case

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

Enabling Clause: the “Consultation”

In practice, the CONSULTATION requirement of paragraph 4 resulted in these RTAs being discussed in the CTD, with this body taking note of the RTAs once concluded. No “examination” was foreseen.

DIFFERENTIAL AND MORE FAVOURABLE

TREATMENT RECIPROCITY AND FULLER

PARTICIPATION OF DEVELOPING

COUNTRIES

Decision of 28 November 1979

(L/4903)

§4: Any (Member) taking action to

introduce an arrangement pursuant

to paragraphs 1, 2 and 3 above or

subsequently talking action to

introduce modification or

withdrawal of the differential

and more favourable treatment so

provided shall: (...)

b) afford adequate opportunity for

prompt consultations at the

request of any interested

[Member] with respect to any

difficulty or matter that may

arise.

Reviewing /Examining P R

O C E

D

U R E

GATT X

XIV

Enabling

Cla

use

GATS V

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

GATS Article V : the “Consistency Test”

In addition to the notification obligation, paragraph 7 of Article V provides for a REVIEW of notified EIAs. Initially, a working party could be established, if requested, for each notified EIA, with the mandate to review the EIA and make recommendations to Members (parties) as it deemed appropriate. In 1996, the CRTA was established as a permanent body to, inter alia, proceed with the reviews. However, such recommendations or reports have never been adopted. The rule of consensus seems to have made it impossible to conclude definitively that an EIA was either in full conformity or fully incompatible with

GATS Article V

Economic Integration

§7 (...):

a) ... The Council [on Trade in

Services] may establish a

working party to examine such an

agreement or enlargement or

modification of that agreement

and to report to the Council on

its consistency with this

Article.

b) ... The Council may establish a

working party to examine such

reports [periodic reports for

EIA implemented on the basis of

a time-frame] if it deems such a

working party necessary.

c) based on the reports of the

working parties referred to in

subparagraphs (a) and (b), the

Council may make recommendations

to the parties as it deems

appropriate.

Reviewing /Examining P R

O C E

D

U R E

GATT X

XIV

Enabling

Cla

use

GATS V

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

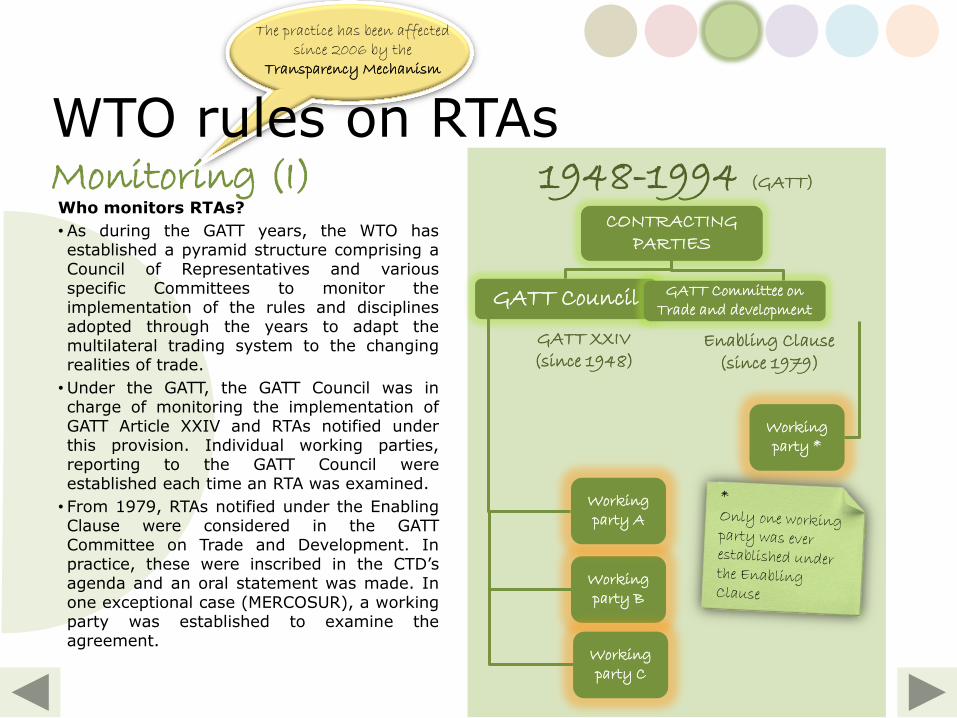

Who monitors RTAs?

• As during the GATT years, the WTO has established a pyramid structure comprising a Council of Representatives and various specific Committees to monitor the implementation of the rules and disciplines adopted through the years to adapt the multilateral trading system to the changing realities of trade.

•Under the GATT, the GATT Council was in charge of monitoring the implementation of GATT Article XXIV and RTAs notified under this provision. Individual working parties, reporting to the GATT Council were established each time an RTA was examined.

• From 1979, RTAs notified under the Enabling Clause were considered in the GATT Committee on Trade and Development. In practice, these were inscribed in the CTD’s agenda and an oral statement was made. In one exceptional case (MERCOSUR), a working party was established to examine the agreement.

1948-1994 (GATT)

GATT XXIV (since 1948)

Enabling Clause (since 1979)

GATT Council

CONTRACTING PARTIES

Working party B

Working party A

Working party *

Working party C

GATT Committee on Trade and development

Monitoring (I)

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

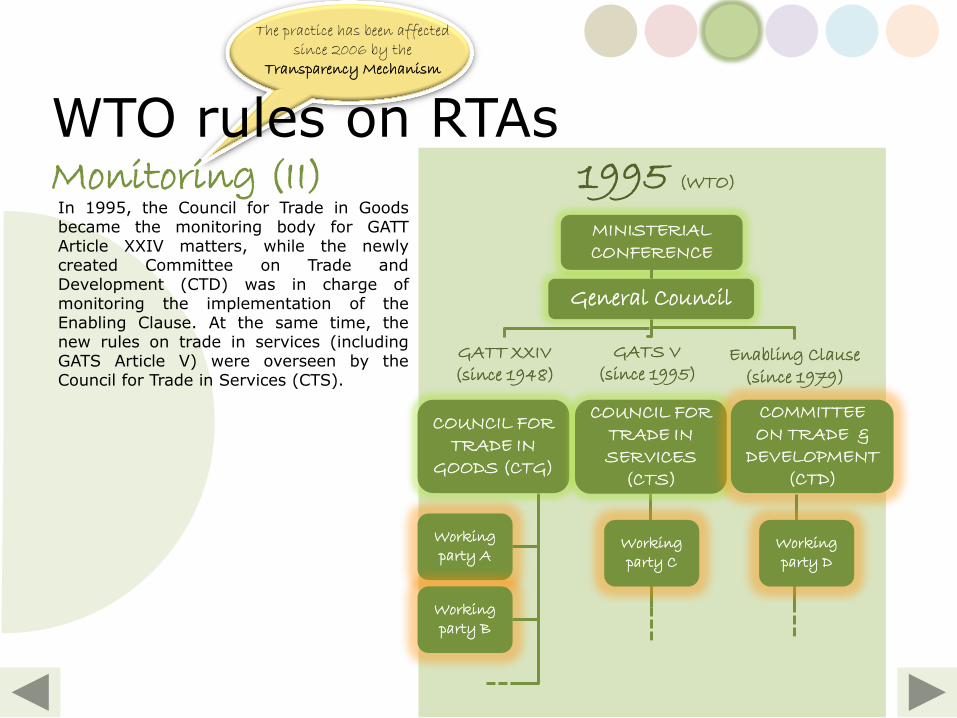

In 1995, the Council for Trade in Goods became the monitoring body for GATT Article XXIV matters, while the newly created Committee on Trade and Development (CTD) was in charge of monitoring the implementation of the Enabling Clause. At the same time, the new rules on trade in services (including GATS Article V) were overseen by the Council for Trade in Services (CTS).

1995 (WTO)

GATT XXIV (since 1948)

Enabling Clause (since 1979)

General Council

MINISTERIAL CONFERENCE

Working party A

Working party B

COUNCIL FOR TRADE IN

GOODS (CTG)

COUNCIL FOR TRADE IN SERVICES

(CTS)

COMMITTEE ON TRADE &

DEVELOPMENT (CTD)

GATS V (since 1995)

Working party C

Working party D

Monitoring (II)

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

A major change in the structure took place in 1996, with the creation of the Committee on Regional Trade Agreements (CRTA). The CRTA became the primary monitoring body for matters related to GATT Article XXIV and GATS Article V; issues related to the Enabling Clause remained under the CTD.

1996 (WTO)

GATT XXIV (since 1948)

Enabling Clause (since 1979)

General Council

MINISTERIAL CONFERENCE

COUNCIL FOR TRADE IN

GOODS (CTG)

COUNCIL FOR TRADE IN SERVICES

(CTS)

COMMITTEE ON TRADE &

DEVELOPMENT (CTD)

GATS V (since 1995)

Monitoring (III)

COMMITTEE ON REGIONAL TRADE

AGREEMENTS (CRTA)

The practice has been affected since 2006 by the

Transparency Mechanism

WTO rules on RTAs

GATT Article XXIV

In 1971, an obligation applicable to customs unions and constituents of free-trade areas to provide biennial reports on the operation of their agreements was established.

(See document BISD 18S/38)

Reporting

WTO rules on RTAs

EXERCISE YOUR Legal SKILLS

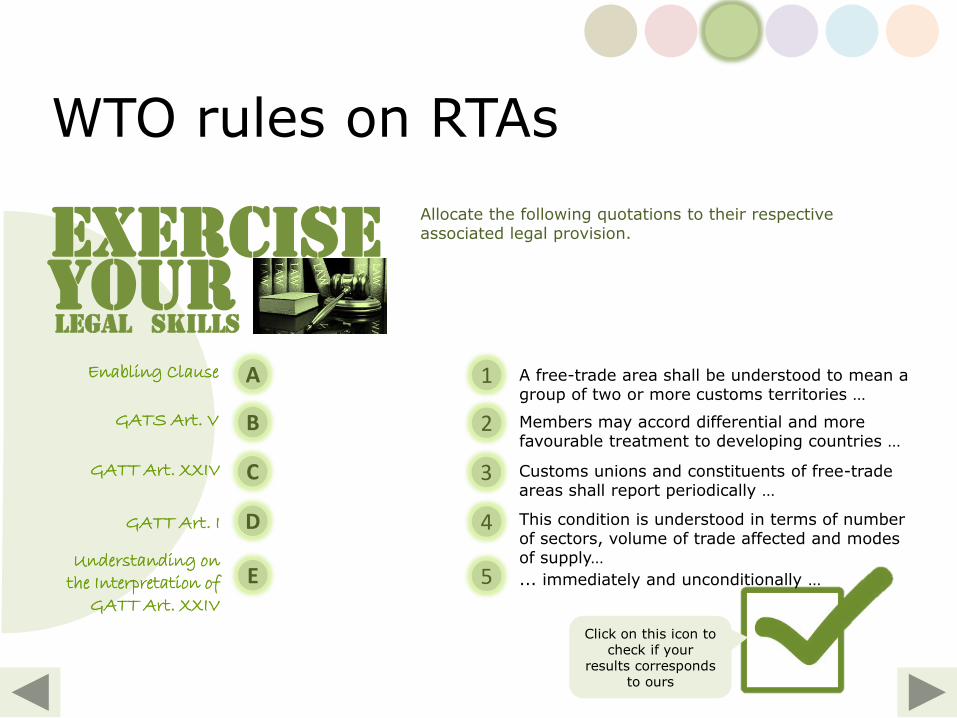

Allocate the following quotations to their respective associated legal provision.

Click on this icon to check if your

results corresponds to ours

A free-trade area shall be understood to mean a group of two or more customs territories …

A Enabling Clause

B

C

D

E

GATS Art. V

GATT Art. XXIV

GATT Art. I

Understanding on the Interpretation of

GATT Art. XXIV

Members may accord differential and more favourable treatment to developing countries …

Customs unions and constituents of free-trade areas shall report periodically …

This condition is understood in terms of number of sectors, volume of trade affected and modes of supply…

... immediately and unconditionally …

1

2

3

4

5

WTO rules on RTAs

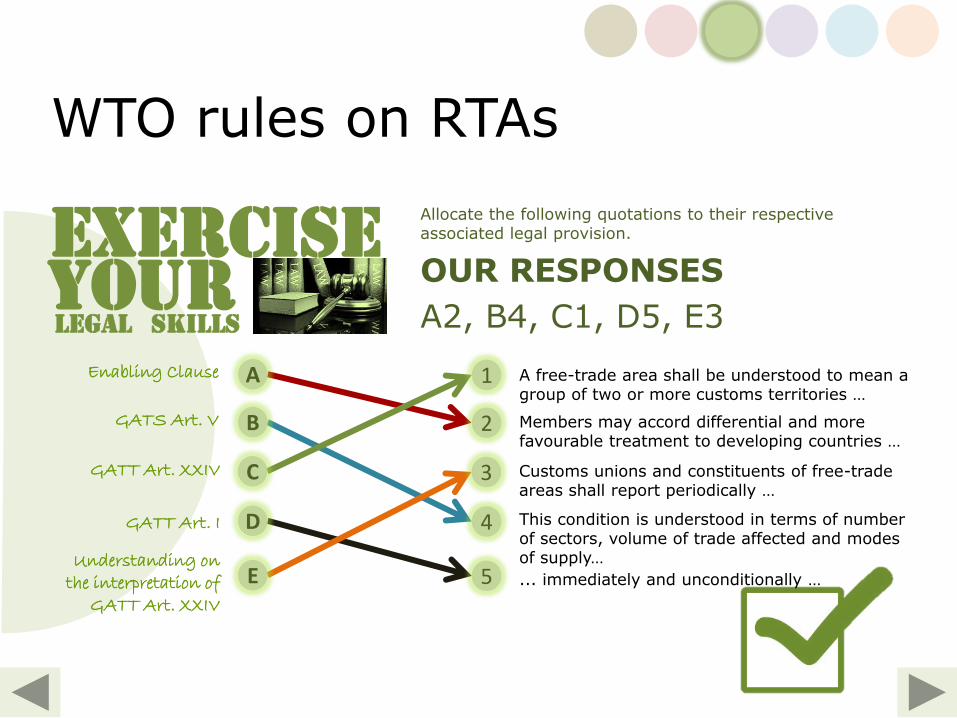

Allocate the following quotations to their respective associated legal provision.

OUR RESPONSES

A2, B4, C1, D5, E3

EXERCISE YOUR Legal SKILLS

A free-trade area shall be understood to mean a group of two or more customs territories …

A Enabling Clause

B

C

D

E

GATS Art. V

GATT Art. XXIV

GATT Art. I

Understanding on the interpretation of

GATT Art. XXIV

Members may accord differential and more favourable treatment to developing countries …

Customs unions and constituents of free-trade areas shall report periodically …

This condition is understood in terms of number of sectors, volume of trade affected and modes of supply…

... immediately and unconditionally …

1

2

3

4

5

WTO rules on RTAs