ITALY Alessia Vatta, University of Trieste Business...ITALY Alessia Vatta, University of Trieste 1....

25

ITALY Alessia Vatta, University of Trieste 1. The Economic Structure and Cultural Properties According to OECD data (2002), in Italy SMEs account for over 99% of firms in manufacturing and in many services and utilities. Enterprises with fewer than 50 employees represent almost 98% of manufacturing firms and at least 99% in the quasi-totality of services. SMEs account for 71% of manufacturing employment and about 90% of employment in construction and many service activities (wholesale and retail trade, hotels and restaurants, business services, real estate). The Italian Civil Code includes also craftsmen in the definition of small entrepreneurs (§ 2083: “small entrepreneurs are…those who practice a professional activity which is mainly organized by their own work and that of their families”, more than by recruiting employees). As a matter of fact, artisan firms are mostly very small, and so are also many agricultural firms. In agriculture, employment often involves the family of the owner and is frequently temporary or part-time, even when it implies the resort to employees (Unioncamere 2001; 2002b). Only a small percentage of agricultural firms counted 3 or more units of labour force between 1999 and 2000 (Charlier 2003). From the data of the Italian Statistics Institute (ISTAT), the predominance of small firms – and of micro-firms, with less than 10 employees – stands out clearly. Between 2000 and 2002, a growing divergence was recorded between the class of firms with 1-9 employees and that with more than 100 employees, in comparison with intermediate size classes (which registered a strong decrease). In particular, the class with 250 employees and more has grown: this has been greeted as a sign that the traditional prevalence of micro-firms could slowly retreat, at least in industry (ISTAT 2003a). 1 A rather negative aspect is that between 2000 and 2002 both the number of active firms and the level of employment have grown rather slowly, whatever the interpretation of the role of SMEs may be (see tables 1-3). Historically, the widespread presence of SMEs influenced the constitution of employers’ organizations. Especially as far as trade, handicraft and cooperatives are concerned, the prolonged ideological cleavage along political lines between the Catholic and the Communist sub-cultures caused the creation of politically opposed ASMEs. The strong preference for the establishment of SMEs is partly considered a consequence of this double cultural heritage, which encourages small entrepreneurship. The relevance of cooperatives’ organizations is also due to the persistence of small-scale productive activities. According to the critical view of a former president of Confindustria, even public initiatives in favour of SMEs (see Section 2) may have led to an excessive protection against market competition, if not to the increase of the “hidden” economy (D’Amato 2004). This view is supported by OECD data on administrative regulation (OECD 2001; Onida 2004a). Another critical aspect regards the scarcity of venture capital and the dependency of firms on short-term loans from banks: this hinders the potential enlargement of firms, since investments become particularly expensive and re-investments tend to be delayed because of pressing indebtedness (Garonna 2004). It has been demonstrated (by Kumar, Rajan and Zingales, 1999) that the average size of firms in industries dependent on external finance is larger in countries with better- functioning financial markets: consequently, financial constraints can keep firms small. Larger firms are more frequent in industries that require little external financing, are physical capital-intensive, hire qualified personnel (by paying high wages) and do a lot of R&D activities. These conditions are often not met in Italy, where especially SMEs frequently 1 However, the most recent yearly report by ISTAT (2004c) confirms that the average firm size is stable (3.7 employees for the total of the sectors). In manufacturing, it is 8.7 employees; in construction, 2.9; and 3.0 in commerce and services.

-

Upload

truongkhue -

Category

Documents

-

view

216 -

download

0

Transcript of ITALY Alessia Vatta, University of Trieste Business...ITALY Alessia Vatta, University of Trieste 1....

ITALY Alessia Vatta, University of Trieste 1. The Economic Structure and Cultural Properties According to OECD data (2002), in Italy SMEs account for over 99% of firms in manufacturing and in many services and utilities. Enterprises with fewer than 50 employees represent almost 98% of manufacturing firms and at least 99% in the quasi-totality of services. SMEs account for 71% of manufacturing employment and about 90% of employment in construction and many service activities (wholesale and retail trade, hotels and restaurants, business services, real estate). The Italian Civil Code includes also craftsmen in the definition of small entrepreneurs (§ 2083: “small entrepreneurs are…those who practice a professional activity which is mainly organized by their own work and that of their families”, more than by recruiting employees). As a matter of fact, artisan firms are mostly very small, and so are also many agricultural firms. In agriculture, employment often involves the family of the owner and is frequently temporary or part-time, even when it implies the resort to employees (Unioncamere 2001; 2002b). Only a small percentage of agricultural firms counted 3 or more units of labour force between 1999 and 2000 (Charlier 2003). From the data of the Italian Statistics Institute (ISTAT), the predominance of small firms – and of micro-firms, with less than 10 employees – stands out clearly. Between 2000 and 2002, a growing divergence was recorded between the class of firms with 1-9 employees and that with more than 100 employees, in comparison with intermediate size classes (which registered a strong decrease). In particular, the class with 250 employees and more has grown: this has been greeted as a sign that the traditional prevalence of micro-firms could slowly retreat, at least in industry (ISTAT 2003a).1 A rather negative aspect is that between 2000 and 2002 both the number of active firms and the level of employment have grown rather slowly, whatever the interpretation of the role of SMEs may be (see tables 1-3). Historically, the widespread presence of SMEs influenced the constitution of employers’ organizations. Especially as far as trade, handicraft and cooperatives are concerned, the prolonged ideological cleavage along political lines between the Catholic and the Communist sub-cultures caused the creation of politically opposed ASMEs. The strong preference for the establishment of SMEs is partly considered a consequence of this double cultural heritage, which encourages small entrepreneurship. The relevance of cooperatives’ organizations is also due to the persistence of small-scale productive activities. According to the critical view of a former president of Confindustria, even public initiatives in favour of SMEs (see Section 2) may have led to an excessive protection against market competition, if not to the increase of the “hidden” economy (D’Amato 2004). This view is supported by OECD data on administrative regulation (OECD 2001; Onida 2004a). Another critical aspect regards the scarcity of venture capital and the dependency of firms on short-term loans from banks: this hinders the potential enlargement of firms, since investments become particularly expensive and re-investments tend to be delayed because of pressing indebtedness (Garonna 2004). It has been demonstrated (by Kumar, Rajan and Zingales, 1999) that the average size of firms in industries dependent on external finance is larger in countries with better-functioning financial markets: consequently, financial constraints can keep firms small. Larger firms are more frequent in industries that require little external financing, are physical capital-intensive, hire qualified personnel (by paying high wages) and do a lot of R&D activities. These conditions are often not met in Italy, where especially SMEs frequently 1 However, the most recent yearly report by ISTAT (2004c) confirms that the average firm size is stable (3.7 employees for the total of the sectors). In manufacturing, it is 8.7 employees; in construction, 2.9; and 3.0 in commerce and services.

depend on external financing, financial markets are comparatively underdeveloped, firms are labour-intensive in many crucial economic sectors and do not invest on R&D (nor can hire graduated personnel or PhD holders, which would imply paying high wages). According to OECD data (Main Science and Technology Indicators, 2003, 1, p. 29), investments on R&D by Italian firms were equivalent to 0.56% of GDP in 2001: in Germany the figure was 1.76, in France 1.37 and in the USA 2.1 (Onida 2004a, 164). Among policy variables, institutional development seems to be positively correlated with lower dispersion in firm size within an industry (Kumar, Rajan and Zingales 1999, 22). In particular, legal institutions related to firms (like patent rights, brand names and other forms of protection of intellectual property, innovative processes and property rights, combined with transparent and effective regulations on accountancy and financial markets) can be connected with an increase in firm size. This happens because entrepreneurs are supported in their control on the productive activity, and are encouraged to enlarge the firms. An efficient legal system also protects outside investors and reduces co-ordination costs. On the contrary, high corporate taxes and costly regulations may drive firms towards a smaller size, in order to avoid such costs. These observations may help to explain the spread of SMEs in Italy, because corporate taxes are comparatively high and only SMEs can partly elude regulations (see note 12). Moreover, SMEs are often family-owned: this can be very problematic as far as management and financing are concerned, since the division of property and prerogatives is not always clear (Onida 2004b, 266). In spite of all these difficulties, SMEs have proved successful in the many productive districts of the country, thanks to flexible specialization, innovation capabilities and quality productions (Piore and Sabel 1984; Pike, Sengenberger and Becattini 1990; Onida 2004a; Fortis 2004). They have increased employment at an average rate of about 3.4% per year between 1982 and 2001, while in the same period large firms have decreased employment at an average yearly rate of 3.1% (Conti e Varetto 2004). As regards professionalism, it is commonly intended as the stable, systematic and non-occasional practice of a given activity. There is no particular legal requirement for industrial production, but there are some exceptions. Brokers, agents and mediators (in financial and tourist services) must hold at least a high school certificate, follow a course of lessons at the local chamber of commerce and overcome a final examination. Alternatively, they must hold a degree. Some other professional categories must overcome a specific exam: maritime mediators and agents, taxi drivers, import-export carriers (they must go through a two-year apprenticeship in a registered firm), restaurant and bar owners. After passing the exam, these entrepreneurs get a license and are registered at the chamber. Chambers of commerce, regional public authorities and representative organizations organize training courses, especially for beginners (e.g. in the food and beverage sector) and in order to spread the knowledge of legal and technological innovations. Craftsmen are registered separately from other categories, in order to benefit from fiscal and financial provisions. Since the definition of SME given in the civil code is very general, the consequences on legislation were mainly two: the enactment of separate sectoral provisions and the gradual extension of some of them to other sectors. Provisions may either apply to handicraft, commercial and industrial SMEs simultaneously, or be handicraft-only.2 Handicraft representative organizations regularly 2 In recent years, state budget laws have offered further opportunities to SMEs. Currently, measures common to handicraft, commerce and industry are as follows: - underdeveloped areas fund (established according to the budget law 2003, § 37): it includes all the financial resources for the development of economically depressed areas, mainly in the Mezzogiorno. Resources are assigned to the regions according to specific criteria (population, average income and sectoral workforce); - unitary fund: it includes several previously existing provisions for the various sectors – among which the Artigiancassa, a sort of crafts’ fund originally established in 1947. Regional public authorities manage 50% of such resources;

insist on the need to extend favourable initiatives to their sector. However, separate registration does not mean that handicraft enjoys particular privileges in comparison to other forms of production.3 As a matter of fact, lots of micro and small-medium firms are of craft nature and characterized by traditional and specialized productions. Representative organizations tend to stress the specificity of craft productions also in pressure politics (“Only Handicraft” is a motto of Casartigiani), and it is often remarked how the Italian Constitution (Basic Law) officially states the importance of handicraft (§ 45). This is also the sector where apprenticeship contracts are most widespread. Also goldsmiths, bakers, car repairers, electricians, employers in the disinfestations and cleaning sector must get a license from the chamber of commerce in order to start their activity. Alternatively, they must have followed a professional training course, have a secondary school certificate or hold a degree. 2. The Legal and Administrative Framework for Associational Action Officially, there are not organizational privileges regarding BIAs and ASMEs. The only possible exception regards consultation by the government in matters of legislation or public policy-making. Usually, the larger BIAs and ASMEs are consulted more regularly, but there is not a “right” in the strict sense. Representativeness is not properly measured according to quantitative criteria: empirically, what counts is “to be comparatively more representative”. However, membership in a large and supposedly influential organization can be an incentive for firms, especially if they are SMEs. From the organizational point of view, the enrolment and the payment of dues entitle to the services supplied by organizations. In absence of specific criteria, political representativeness is more de facto than de iure. There is not any obligation to extend collective agreements erga omnes, but also non-member firms are covered by “minimal provisions” entailed in the agreements, thanks to jurisprudence (court rulings). The Italian Constitution states that receiving a minimum wage is a right of the worker, and the courts take the sectoral collectively agreed wage rates as the levels of fair or minima wages to be paid to workers (Dell’Aringa 2003) As regards collective bargaining coverage, it is generally estimated around 90% of the workforce4; firms with up to 100

- according to the budget law 2003, small entrepreneurs are allowed to claim a further reduction of their personal income tax (named IRPEF); the regional tax on productive activities (IRAP) was reduced with the possibility to deduct part of the employment-related costs. Facilities were introduced in order to resolve queries related to tax evasion and fiscal disputes between employers and the state. According to Act 383/2001, taxation on re-invested profits was cut; - according to Act 488/1992, incentives are offered for the establishment of new firms, technological innovation and research, with specific regard to southern and economically depressed areas; - the governmental decree 185/2000 introduced “honour loans”: jobless people may ask for loans at favourable conditions in order to start an entrepreneurial activity; - in case of new recruitments, employers are allowed to delay the payment of payroll taxes. In general, provisions regarding payroll taxes are important for artisans because, according to jurisprudence, labour should prevail on capital (as a productive factor) in artisan firms. Handicraft-specific provisions include: - reduced taxation in case of building restructuring; - in case of severe necessity, artisans can count on relatives – up to the second degree – as employees for a maximum period of 3 months per year without paying pension contributions. 3 The grievances echoed by SMEs representative organizations are very similar among the different sectors, e.g. as far as fiscal pressure is concerned. Other common problems regard the high costs of electric power, the heavy bureaucratic regulations, the inefficiencies in transport and infrastructures. From the political point of view, the defence of the quality of handicraft and high-standard products has gradually gained importance in external politics, especially against low standard imports from foreign competitors (like China) and against questionable EU-level policies in matter of artisan and quality productions. 4 Dell’Aringa (2003) reports a coverage of 82% of the workforce.

employees are mainly covered by sectoral/national bargaining, but those with fewer than 20 employees may also be uncovered.5 Those with more than 100 employees are mainly covered by company bargaining, which in principle should be in line with sectoral arrangements. However, over 1990-1994 company agreements were signed only in 8.7% of enterprises with 20-99 employees, in 19.9% of enterprises with 100-499 employees and 32.9% of those with more than 500 employees (Bellardi and Bordogna 1997; EIRObserver 1999).6 According to EUROSTAT data referred to 1997, company bargaining covers about one third of Italian firms (Boeri 2004b). As far as the constitution of employers’ organizations is concerned, there are not either supportive or obstructive norms, since general rules on associations provided by the civil code also apply to employers’ organizations. The basic legal precondition for collective bargaining is the autonomy of trade unions and of their representation and mandate on behalf of their members (§ 39 Constitution), while employers’ organizations are free to organize themselves according to § 19 and § 41 of the Constitution (regarding freedom of association and economic organization). As a rule, collective bargaining actors are those collective entities entitled to exert autonomous negotiation power by their members. Usually, such prerogatives are recognized permanently and mainly de facto. As a consequence, the largest organizations in terms of membership can claim the right to negotiate, and this is true also for the ASMEs. There are several ongoing initiatives in favour of SMEs. Their goals are: - to simplify fiscal rules; - to extend the availability of loans and credit (for craftsmen through the Artigiancassa; for other small and medium employers through the grant fund for SMEs, which guarantees the consorzi di garanzia fidi, i.e. consortia for the guarantee of loans, which have been operating for about 30 years by now at the Ministry for Productive Activities, formerly Ministry of Economy); - to collect all the incentives in force in a single law (“incentive code”); - to amend bankruptcy norms in a way favourable to SMEs; - to encourage technological innovation (Act 46/1982, Act 675/1977, Act 341/1995), also through the electronic deposit of patents and the periodical consultation of ASMEs regarding the protection of industrial property; - to support female and young entrepreneurs (Act 44/1986 and Act 266/1997), also at regional level (Act 44/1986, Act 215/1992, Act 236/1993 and Act 95/1995); - to put firms in touch with the R&D institutions (universities and research centres) and create innovative SMEs (Startech project). Innovation and R&D investments at firm level are supported by Act 297/99; - to increase the spread of E-business among SMEs; - to promote exports and internationalization (Act 277/1997 and Act 394/1981).

5 Apart from these estimates, it must be remembered that “black” or “grey” labour remains a serious problem, especially in agriculture (about 30% of workers). Other affected sectors are building, catering, retail, tourism, personal care and domestic services. Undeclared work is about 15% of the total labour force (18% among employees) and is particularly widespread in the south, where one in every five workers is irregular (Broughton 2004). According to the same source, the “hidden” economy oscillates between 15.2 and 16.9% of GDP. According to CNEL data, in metalworking 50% of the employees is not covered by second-level bargaining (see note 6), while in the commercial distribution the percentage rises to 80% (CNEL 2002). 6 The July 1993 tripartite agreement envisages two levels of collective bargaining: sectoral bargaining and either company- or territorial-level bargaining, according to the specific features and traditions of the different sectors (Pedersini 2002). Company-level bargaining is the usual second level of collective bargaining in manufacturing and services, while territorial bargaining takes place essentially in agriculture, construction and artisan activities. Company-level bargaining is strictly connected to firm size. A 1997 ISTAT survey on firms having at least 10 employees showed that, in 1995-‘96, company-level bargaining took place only in 9.9% of firms belonging to that size class.

Historically, SMEs have frequently resorted to a specific act (the so-called “Sabatini Act” 1329/1965), which guaranteed loans at cut interest rates for investments on new machineries. The massive resort to legal instruments for the promotion of SMEs has been criticised because large public resources have often been spent without success or with uncertain results (Onida 2004a, 192-193).7 In the latest years, small entrepreneurs have taken advantage from “one-stop counters”, i.e. local civil service offices which provide businesses with all the information they need for dealing with government departments and agencies, especially for submitting applications and obtaining licences. These counters are operative in about 59% of communal districts, covering 71% of the population (OECD 2002). Tax relief is offered in exchange for training and facilities provided to employees (e.g. crèches), for recruiting skilled personnel, financing grants for PhD students and contracting out industrial research. A state agency, Sviluppo Italia (www.sviluppoitalia.it), finances entrepreneurial development in Southern regions. Employers’ organizations are involved in these policies by way of concertation (at local and national level), particularly for the elaboration and implementation of “territorial pacts” (patti territoriali, according to Act 662/1996) aimed at the development of economically depressed areas. At the Ministry for Productive Activities, a specific roundtable for the definition of supportive initiatives for the SMEs has been set with the participation of representatives from Confindustria, Confapi, CNA and Confartigianato. 3. The System of Social Dialogue and Public Policy Making At national level, Confindustria and the major confederations are consulted by trade unions more often than other organizations, also for collective bargaining, because they are reputed to be more representative. At local or sectoral level, regional/provincial branches and sectoral organizations are often involved, also as mediators in bargaining at firm level. At these levels, it may happen that employers’ organizations take different positions in comparison to those taken at national level. Confindustria is considered the most representative and “general” employers’ organization. In the other sectors, Confcommercio and Confartigianato are often consulted by the government, but there is not any “preference” in strict terms, since the other organizations may be asked to give their opinion, too. Since the post-WWII years, representatives from the social partners’ organizations have been involved in the administration of social security bodies and welfare programmes.8 The social partners participate in the implementation of public policies in a “relatively formalized and stable” way (Regalia and Regini 1998, 495). The most important nation-wide and cross-sectoral tripartite institution of social dialogue is the CNEL (Consiglio Nazionale dell’Economia e del Lavoro, National council for economy and labour, www.cnel.it), which is recognized by the Constitution and whose activity is disciplined by Act 936/1986 and Act 383/2000. Among its 121 members, it includes 14 representatives from Confindustria and 2 from Confapi (industry), 5 from Confcommercio and 2 from Confesercenti (trade and services), 2 from Confartigianato, 1 each from CNA, Casartigiani and CLAAI (handicraft), 1 each from Legacoop, UNCI, Confcooperative and AGCI (cooperatives), plus 3 representatives from autonomous sectoral associations for services, transport and shipping, and 9 from agricultural organizations. The

7 It has been estimated that about 2% of GDP is devolved in public subsidies to firms (Ostellino 2004). 8 Both the trade unions and the employers’ organizations take part in the management of INPS, the institute which administers the pension scheme for most employees in the private sector. Representatives from Confindustria, Confcommercio, Confesercenti, CNA, Confapi and from the main agricultural organizations also sit in the INPS’s supervisory council.

CNEL has merely consultative and research functions. However, there are other opportunities for the associations to participate in social dialogue, either bipartite or tripartite, at national level (through formal and informal consultations, e.g. via the enti bilaterali – bilateral bodies with trade unions and employers’ representatives which deliver services to workers and organize training schemes in the handicraft sector) or at a more decentralized level (De Lucia and Ciuffini 2004). At regional level, the CREL (Consigli regionali dell’economia e del lavoro, regional councils for economy and labour) reproduce the tripartite structure (Regalia 1997; CNEL 2004); but there are also more flexible solutions, with negotiations at regional, provincial and even local level (like the cabina di regía – a sort of permanent consultation body at regional level -, within commissions and periodical consultations). Local forms of concertation have received a strong impulse after the 1998 national social pact, because of the decentralization of public functions and resources and the consequent empowerment of regional authorities according to the subsidiarity principle.9 Micro-concertation at firm level has been recorded and studied (e.g. see Regini 1991), though Act 300/1970 – which has led to the establishment of workers’ representational structures (currently known as RSUs, rappresentanze sindacali unitarie, after the 1991 framework agreement among the three main trade union confederations) – applies only to firms with more than 15 employees, leaving out the majority of small firms, whose employees can elect delegates.10 Consultation and information subjects typically involve the economic and financial situation of the firm, the provisions set in industry and company collective agreements, and the employment situation (especially regarding work organization, new technologies and possible redundancies) (European Foundation 2002). The dissolution of the party system in the early 1990s after the bribe scandals related to Tangentopoli and the adoption of the mixed majority electoral system encouraged an increasing distance of the employers’ organizations from the parties. In the past, the “left/right” cleavage had exerted its influence on most organizations in the various sectors (e.g. left-leaning CNA vs. centre-right Confartigianato, Confesercenti vs. Confcommercio, Legacoop vs. Confcooperative). This was due to the strong ideological polarization and the powerful role of political parties as factors of integration and actors in public policy-making. The lack of autonomy of the associations from the parties was known as collateralismo and has remarkably weakened the system of interest groups’ representation in comparison with political parties and parliamentary representation (Mattina 1997). In the post-WWII years, Confindustria had kept a so-called “consonance” with the small Partito Liberale (Liberal Party), and later an “alliance of necessity” with the Democrazia Cristiana (Christian Democratic Party): in the first case, it was a sort of ideological similarity, while in the second it seemed necessary to stay in good terms with the predominant party, given the presence of a particularly strong Communist party in Italy. Nevertheless, since the early 1990s Confindustria has repeatedly asserted its apartitical orientation.11 Even after the reconstitution 9 The operation of local concertation strongly increased in the 1990s, following a constitutional reform, but it still needs improvement. There are wide regional differences concerning the effective involvement of social partners in economic and financial policies, and local concertation has to be integrated into national level agreements (CNEL 2002a). It is also necessary to check the effectiveness of pacts, in order to avoid the dispersion of financial resources, and to monitor their implementation in accordance with clear purposes (CNEL 2002b). 10 Originally, Act 300/1970 defined the representational structures as RSA (rappresentanze sindacali aziendali) and conceived them as trade unionist bodies. Historically, they followed the commissioni interne (internal commissions), which dated back to the beginning of the 20th century and represented the workforce as a whole. The current bodies (RSUs) were established in 1993 and devised as a unitary institution, in order to overcome dualistic representation. 11 In the early 2000s some criticisms were expressed against possible “affinities” between the leadership of Confindustria (then led by Antonio D’Amato, a SMEs’ representative) and the centre-right national government (Sarfatti 2003).

of the party system, employers’ organizations appear more legitimated as representative actors than in the past; this could strengthen their political position in the coming years, especially if they prove able to keep their distance from the parties (Lanza and Lavdas 2000). The 1990s were characterized by a series of social pacts between the governments and the social partners. Two main factors supported the development of concertation. First, the economic changes induced by globalization and the beginning of the European Monetary Union pushed towards the adoption of incomes policy, the reform of the welfare system and of labour policy. Second, the crisis of political parties favoured the empowerment of interest organizations as political “substitutes” (Trentini and Zanetti 2001). The 1992 agreement blocked the automatic pay indexation and corrected it according to predicted inflation rates. The 1993 protocol introduced a coordinated two-tier system of collective bargaining and included the social partners in incomes policy-making. The 1996 pact renovated labour policy, introduced several forms of work flexibility and relaunched vocational training. The 1998 pact confirmed the previously agreed commitments, and fostered the reform of public administration and the adoption of concertation at local level. In 2002 the Pact for Italy proclaimed the need to reform taxation, the welfare system, the initiatives in favour of Southern regions and the regulation of dismissals.12 In 2003 a pact for development, employment and competitiveness asserted the need to reserve funds to research and development, to vocational training (especially in Southern regions) and to the building of new infrastructures. All the employers’ organizations included in this paper signed the agreements between 1992 and 200213: in absence of “quantitative” criteria for admission, some observers remarked that the influence of ASMEs has gradually improved and apparently increased in latest years (Ferrante 1998, 82-84; Lanzalaco 2000). However, in 2002 handicraft and trade associations had to insist in order to get the extension of fiscal cuts, originally conceived for industrial firms in the Pact for Italy. In 2003, only Confindustria signed the pact in representation of employers: this raised criticisms from other organizations, fearful of a possible exclusion from future agreements and of a new hegemony of the main BIA. Other tensions regarded the adoption of the EU Directive on fixed-term work in 2001. Trade unions and employers’ organizations produced a joint document on the implementation of the directive, which was then submitted to the government; but Confcommercio, CNA, Confesercenti, Legacoop (plus Confservizi, a sectoral autonomous organization of the tertiary sector) did not sign it. In March 2004, employers and trade unions in the artisan sector reached an agreement for the reorganization of collective bargaining in handicraft, after having retired from the 1993 two-tier structure in 2000. The new system gives more importance to pay bargaining at local level, for the compensation of the difference between predicted and actual inflation in the definition of pay increases. This innovation could next be extended to other sectors: proposals in this sense have been made regarding SMEs affiliated to Confindustria. 4. The System of Cross-Sectoral Business Associations

12 Following an intense debate among the social partners, a referendum on the extension to all companies of the right to reinstatement for unfairly dismissed workers provided by § 18 of the Workers’ Statute (Act 300/1970, valid only for firms with more than 15 employees) failed in 2003, because of insufficient turnout. In general, employers’ organizations were against the extension. For a discussion of the potential effects of employment protection regulations on firm size, see Garibaldi, Pacelli and Borgarello (2003). 13 Confartigianato did not sign the 1992 agreement, because it entailed tax and social contribution increases which were considered too heavy for the artisans.

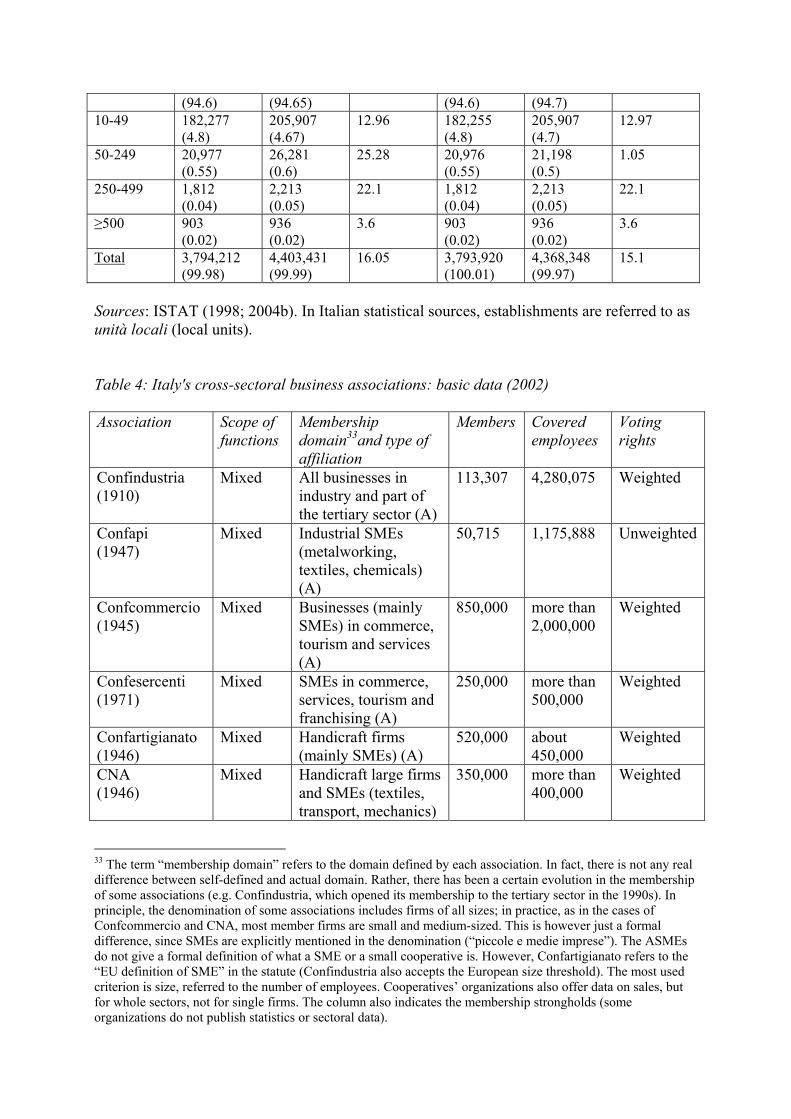

According to the prerequisites set in the project outline, 12 organizations can be taken into consideration (see table 4).14 By sector, they are Confindustria (Confederazione generale dell’industria italiana) and Confapi (Confederazione italiana della piccola e media industria) in industry; Confcommercio (Confederazione generale del commercio, del turismo, dei servizi e delle piccole e medie imprese), Confesercenti (Confederazione generale italiana esercenti attività commerciali e turistiche) in commerce; Confartigianato (Confederazione generale italiana dell’artigianato), CNA (Confederazione nazionale dell’artigianato e della piccola e media impresa), Casartigiani (Confederazione autonoma dei sindacati artigiani, also known as CASA) and CLAAI (Confederazione delle libere associazioni artigiane italiane) in handicraft. Four organizations include cooperatives: Legacoop (Lega nazionale cooperative e mutue), Confcooperative (Confederazione cooperative italiane), UNCI (Unione nazionale delle cooperative italiane) and AGCI (Associazione generale delle cooperative italiane). Apart from Confindustria, which was originally founded in 1910 and definitely established in 1919, the oldest organizations are Legacoop (1886) and Confcooperative (1919). All the others were founded after World War II, since the right to free organization had been recognized after the end of the Fascist corporatist system, in which Confindustria played a central role. The membership in these organizations is voluntary. Eight of them organize lower-level associations. The cooperatives’ organizations adopt direct membership followed by the enrolment of member cooperatives in territorial and sectoral structures. All the organizations have a mixed scope of functions: usually, collective bargaining involves sectoral affiliates, while confederations are active at national level for the “inter-confederal” agreements. An exception is given by Confindustria, whose territorial branches are frequently bargaining partners, and partially by Confartigianato (sectoral agreements have to be transposed at regional level). As for membership domain, in some cases it is open in principle to all firm sizes (Confindustria, Legacoop), while in others small size is officially stated, either in the statute or in the official denomination (Confapi, Confcommercio, Confesercenti). Handicraft organizations may include firms of all sizes, but the membership is mainly small-sized.

Since the majority of Italian firms are SMEs, this determines a large presence of employers’ organizations representing their interests. As explained in Section 1, the pre-eminence of SMEs in Italy has several reasons: cultural, historical, economic (raw materials are scarce and there is a consequent emphasis on transformation and commercialization of goods) and legal (mostly for flexibility reasons). ASMEs are either “self-declared” (by statute or denomination) or de facto (even though they would accept also larger firms, actually they are specialized in the representation of small and medium firms). In the first sub-group there are Confapi, Confesercenti and the handicraft organizations. To the second sub-group belong the cooperatives’ organizations, which often take common positions on public policy matters. This is because their membership is mostly small and medium-sized, though they may have members of larger size (like Legacoop). Confcommercio includes SMEs in its denomination and represents them de facto. In general, the number of employees is the main criterion to determine firm size, with the specification that employers’ organizations often have to deal with micro-firms (fewer than 10 employees). Most organizations have weighted voting rights, with forms of proportionality regulated in their statutes. However, a potential problem of representation for SMEs affects only Confindustria, in which large firms traditionally exert a disproportional influence in comparison to SMEs. In fact, the most renowned case of unweighted voting rights is that of 14 The research regards only cross-sectoral associations according to the NACE classification. Within single sectors, other relevant BIAs can be found: it is the case of ABI (Associazione bancaria italiana), whose members count 300,000 employees in banking, and of Confetra (Confederazione generale italiana dei trasporti e della logistica), with 500,000 employees in the transport sector.

Confapi (where the principle “one firm, one vote” applies in the general assembly), due to the origins of the association.15 Regarding direct membership associations affiliated to peak confederations, within the sectoral federations and the branch associations of Confindustria proportionality prevails, either referred to the level of paid contributions or to the number of employees in member firms. The “one firm, one vote” principle may apply in some cases (e.g. for the amendment of statutes). Within branch associations of Confcommercio, proportionality may also be calculated with reference to the volume of sales of member firms. Unweighted voting seems to be more common here, especially within branch associations including individual firms (e.g. in sectors like communications or consulting). Within Confartigianato, the member associations have to follow the criteria set in the confederal statute (see Section 5). The services offered by the organizations are generally free of charge for member firms. They are usually provided by territorial (e.g. regional and provincial) branches. However, legal or fiscal assistance may be subject to a modest fee, and it is possible that member associations charge some services at local level. Especially in recent years, inter-organizational competition regarding services has increased. The cross-sectoral nature of the organizations opens several chances for employers when it comes to joining an association, and the choice often depends on the range and quality of services and on the costs to pay. Sometimes – as in the case of Confindustria – membership becomes a matter of social prestige (Ferrante 1998, 108). Handicraft and commerce organizations also include specific associations for retired members and for the provision of social security subsidies. Among services, an increasing role has been taken by information on international developments (e.g. concerning EU-level initiatives) and the start-up of new firms. A “bulk” of services is common to virtually all associations, i.e. fiscal, legal and concerning labour relations. Another range of services is related to financial resources and access to credit: this is particularly important for handicraft and cooperatives’ organizations, which are connected with specific funds and saving banks. Fiscal consulting regards not only taxes and social contributions, but also social security and pensions. Legal consulting concerns norms related to any aspect of productive activity, from licenses to environmental protection and work safety. Another common series of services is related to information. Most organizations provide training courses, run statistical databases and publish newsletters or bulletins. An important and ubiquitous offer relates to institutional relations (usually with the chamber of commerce and the regional and local public authorities). Many services also regard management, development, informatization and E-business. Some associations run research centres (Confindustria, Confcommercio, Confcooperative). The similarities among the services on offer suggest that competition can be based either on a constant qualitative refinement or on the amount of fees to be paid. The combination of good and extensive services at moderate prices could be attractive for many small and medium employers. However, should quality improvement imply cost increases, this could prove in contrast with the “mutual assistance” image that associations often defend. A stronger professionalization in this sense would imply a remarkable change in the reciprocal attitude between firms and associations, especially in the case of ASMEs. Another source of competition could be located in the offer of international services; here, some organizations (Confindustria, CNA and Legacoop) currently look better equipped than others, especially with regard to the opening of new markets for firms.

15 It was established in 1947 by small firms which exited from Confindustria, as a protest against the inefficient representation of SMEs’ interests, especially regarding the access to bank credit (Alacevich 1996). Another sign of the commitment to the potential membership is the rule according to which firms enrolling in an API (APIs are the provincial branches of Confapi) are automatically enrolled in the related national union (the sectoral branches) without paying additional contributions.

In the 1990s and more recently, many reform attempts have been made by employers’ organizations. In some cases there have been explicit projects in this sense, whereas in others a more informal and pragmatic trend towards structural innovation and strategic modernization prevailed. This is true for Confesercenti, and for the handicraft organizations in particular. These have intensified reciprocal cooperation; as a result, they participate jointly in official hearings and release joint documents. They are currently trying to unify their service structures and simplify bureaucratic procedures. Following the adoption of the “Confapi 2000” project, with the implementation of a new confederal statute, Confapi has supported regional decentralization and the resort to network methods, according to the subsidiarity principle. Also cooperatives’ organizations have joined forces, and tried to improve their effectiveness. Confcooperative has established a database in order to let regional branches have access to documents and information, while AGCI has insisted on decentralization and rationalization of management. In comparison with the other BIAs, cooperatives’ organizations rely more often on voluntary work: this practice is currently seen as no longer appropriate, since it can reduce efficiency and effectiveness. Steps in the direction of substituting volunteers with employed personnel on a regular basis have recently been made (e.g. by AGCI at its 2002 organizational conference). Reforms within Confindustria, Confcommercio and Confartigianato are dealt with in the following section of the paper. In Italy the chambers of commerce are mainly administrative structures, which are assimilated to the public administration since they are public law institutions. They are reunited in a national association, called Unioncamere. All firms must be registered at the local chamber, and this gives chambers a privileged view on the state of Italian economy. Because of their institutional role, the chambers also perform public functions related to firm’s activities (like the release of licenses), organize training courses and conferences, and are usually rather active in external relationships, in particular with foreign economic partners. But they are normally excluded from collective bargaining, which remains a domain of voluntary organizations. 5. Confindustria, Confcommercio and Confartigianato in Comparison According to the criteria set in the research outline, Confindustria and Confcommercio are respectively the selected BIA and ASME. They are the largest in terms of employees in member firms, have a nation-wide domain, are peak-level and cover at least 3 one-digit activities as defined in the NACE classification. Being the most important BIA, Confindustria occupies a central position in the representation of entrepreneurial interests. Among the associations which represent SMEs, Confcommercio was originally founded for the representation of commerce in general. In practice, SMEs have proved to be the vast majority of its members and Confcommercio is specialized in their representation. Because of the importance of the artisan sector in the national economy (about 1,420,000 firms and more than 1,500,000 employees), the main representative organization, Confartigianato, is also included in the analysis. Membership: Domains, Composition and Figures Currently, Confindustria includes 18 regional associations, with 105 territorial (mainly provincial) associations, 12 aggregated members, 13 sectoral federations and 112 branch associations.16 Sectorally, manufacturing was the main stronghold in 2002, while other major 16 Branch associations, which represent firms performing similar activities or sharing similar interests, normally belong to sectoral federations. The statute of Confindustria prescribes that only one federation can correspond to

components were construction, transport, tourism, services and the production of energy and raw materials (see table 5). “Aggregated members” are associations representing activities that are similar or affiliated to those of full-member organizations; they may also be associations of Italian firms operating abroad. Aggregated members pay special dues and do not have the same internal status as full members. Traditionally, territorial associations are more relevant than sectoral associations for the day-to-day activities of the confederation. This seems to be historically related to the origins of the confederation, which was established in Turin, with the north-western regions of the country being the front-runners of industrialization (Lanzalaco 1989). However, in the course of time some sectoral federations have gained a remarkable status, like Federmeccanica (established in 1971 for the representation of the metalworking sector) and, more recently, Federchimica (1984, for chemical firms). According to the data of Unioncamere (2002), active industrial firms were 1,295,543 (including the construction sector) in 2002, with 6,932,000 working units (employees were 5,394,000) (ISTAT 2004a). This means that the coverage of Confindustria is relatively high as far as employment is concerned (around 59.4% in industry, about 31.3% if services – without commerce- are enclosed), while the data on membership reveal a heavy imbalance between large firms and SMEs.17 According to confederal data, in 2003 the size class with 0-50 employees included 83% of member firms (with 23% of total employees), the 51-250 size class included 14% of firms (with 32% of employees), and the size class with more than 250 employees included 3% of member firms (and 45% of employees). Then, SMEs constitute about 97% of the membership. By dividing the number of employees by the number of firms, the resulting average size is about 36 employees. There is a specific board for the representation of small and medium employers (the consiglio centrale per la piccola industria, central council for small industry), whose president sits in the confederal directive committee. Twenty representatives of small industry, appointed by the central council, take part in the giunta, the confederal executive body. However, the proportional voting system (based on the level of contributions in the general assembly and on the number of employees in the giunta) tends to curtail the role of SMEs within the confederation. At the same time, while other confederal organizations compete for the membership of SMEs, some observers maintain that the lobbying power of Confindustria is further diminished by the opening of the membership to the tertiary sector and by “weak” members, like the firms inherited from the former representative organizations of state-owned firms, Intersind (Associazione sindacale Intersind) and ASAP (Associazione sindacale aziende petrolchimiche), which were dissolved in the 1990s. In many cases, such firms have gone through privatization processes (like telecommunications) or still remain problematic in terms of efficiency and budget (e.g. the railways). Like Confindustria, Confcommercio considers itself as a “system” made up of different components, which may also enjoy a certain autonomy of action.18 These are commerce (about 500,000 firms), tourism (about 200,000 firms) and services (about 80,000 firms). The confederation counts 21 regional unions, 103 provincial associations and 152 a given sector. However, if a branch association represents interests which cannot be included in any existing sectoral federation, then “that” branch association can be recognized by the giunta (the executive confederal body) as functionally equivalent to a federation. Thus, not all the associations belong to federations (actually, they are allowed to join even more than one federation, provided they pay the related dues), and that is why they are indicated separately from sectoral federations. 17 Considering the main components within the confederation, in 2002 the density ratio related to firms was 4.1% for industry only (5.2% if construction firms are enclosed in the calculation). For services only (without commerce), the density ratio was about 3.8%.Considering industry, construction and services together, the density ratio was 4.5%. In commerce, employees were 1,723,000 in 2002 (ISTAT 2004a). 18 Confartigianato and CNA also have extensive structures, usually referred to as “systems”.

national branch associations. The most important member associations are Confturismo (in tourism, covering about 1,100,000 employees), Conftrasporto (in transport, about 320,000 employees) and FAID (Federazione Associazioni Imprese Distribuzione, in commercial distribution and franchising, about 223,000 employees). Altogether, the confederation member firms count more than 2,000,000 employees. A research made on behalf of Confcommercio and Microsoft on the adoption of information technology, made in 2002 on a sample of 1,000 firms in the tertiary sector, showed that 34.7% of them belonged to Confcommercio, 9.5% to Confesercenti, 8.2% to Confartigianato and 3.4% to Confindustria (NetConsulting 2003). Moreover, 17.2% did not belong to any organization. On one side, this proves that Confcommercio strongly attracts the tertiary sector firms, but on the other it shows that a noteworthy percentage of SMEs – typical of this sector – may well choose not to join any association. The main reason given by associated firms was the possibility to get services, assistance and political representation through the selected associations. According to Unioncamere data (2002a), there were 2,603,564 active firms in the tertiary sector in 2002, employing about 13,800,000 working units (about 4,000,000 of which were self-employed) (ISTAT 2004a). As for the number of firms, the coverage of Confcommercio looks rather high (the density ratio is around 33%) but the coverage of employees is not so relevant as it might be expected (it should approximately range between 20 and 24%). This may depend on the fact that employment is tendentially more volatile in the sectors covered by Confcommercio than elsewhere, due to the resort to part-time and flexible contractual forms. It is then more difficult to ascertain the level of “actual” employment, especially in certain areas (e.g. for seasonal employment in tourism). Consequently, one cannot rule out the possibility that even the data given by Confcommercio do not reflect precisely the reality of its different components. In 2002, the average number of employees per firm in the tertiary sector was about 15, while in commerce it was about 3 (NetConsulting 2003): thus, the degree of fragmentation is particularly high. However, this does not seem to have serious consequences on the internal balances of the confederation, since the vast majority of the membership is made of SMEs. Proportionality is based on the number of member firms of the associations: in the general assembly and in the council, each association has a vote plus a number of votes depending on the number of member firms. A similar principle applies for the calculation of votes per sector in the giunta. The “system” of Confartigianato is composed by 121 territorial associations and 20 regional federations. It also encloses 12 branch organizations, which are sectoral subdivisions of the confederation. The membership includes about 520,000 firms, covering 450,000 employees. The domain is formally defined in the statute and covers artisan firms, the self-employed, small firms, the tertiary sector and services. The average number of employees is about 2.4 per firm. It is estimated that about 30% of all artisan firms belong to Confartigianato, and that its membership covers about 30% of the total employment in the artisan firms (amounting to about 1,546,000 employees in 2002).19 The general assembly is composed by the presidents and/or by the delegates of the member associations. Each association has one vote, plus another one every 2,000 associated firms and fractions superior to 1,000 for further associated firms, calculated at regional level. Each associated firm must have paid the membership fee in order to be included in the calculation. It can be said that, even though each member association has a vote, voting rights are “territorially weighted”, since territorial associations enclosing larger numbers of associated firms can count on extra votes. The same dispositions are valid for the member associations, which have to respect the confederal statute in drawing their own statutes. 19 These data were given by Confartigianato (elaboration on Unioncamere data). There are no data available on the sectoral composition of the confederation.

Tasks and Activities Table 6 summarizes the tasks and activities implemented by Confindustria, Confcommercio and Confartigianato. As far as Confindustria is concerned, representation towards trade unions and the state is exerted directly (at national and inter-confederal level) and indirectly, through the territorial and sectoral organizations. In the field of product market interest, sectoral organizations play the main role. In public policy-making, Confindustria participates directly or via the territorial associations, especially at regional level. Standardization of products and product quality do not involve the confederation. This is considered a public interest matter, in which state agencies and chambers of commerce are active, especially if it implies compliance with EU norms. However, the confederation may lobby the government in case quality and standardization matters entail political and legal effects (see note 3). As for services, they are normally free of charge for members, but territorial structures – which usually provide most services – may ask for limited ad hoc contributions (e.g. for fiscal assistance). Territorial branches can also certificate the quality of products or of firms themselves. Even if the confederal statute stresses the importance of offering services to members, the focus of activities is on interest representation. This is encouraged by the pre-eminence of territorial organizations, though interest representation has gradually become more “political” than referred to “unionist” functions. In order to achieve the adoption of favourable public policies, lobbying has gained a noteworthy strategic importance. However, the impression is that the confederation still lacks a long-term perspective in this sense and needs a proper strategy for the development of industrial relations in the next future (Bordogna 2004). In matters of tasks and activities the attitude of Confcommercio resembles that of Confindustria, but with a stronger focus on services and conventions for members. Nevertheless, the division of roles among territorial and sectoral associations is less clear cut, since Confcommercio applies the double affiliation for member firms. This means that each firm enters the related sectoral and the nearest territorial structure of the confederal system simultaneously. The provincial ramifications of Confcommercio, called Ascom, play both the sectoral and territorial role.20 Services are free of charge for members, but extraordinary dues can be charged locally. For example, this regards the quality certification of firms and products, which can be provided by local and sectoral member associations. Confartigianato organizes only lower-level associations and does not accept direct membership of firms. These are registered by territorial associations and are automatically included in the sectoral structures of the confederation. Services are offered at territorial level and are mostly charged. Regional federations have coordinating functions and should become gradually more important in the future, following the delegation of state policy-making prerogatives to the regional public authorities. Concerning product quality standardization, the confederation takes part in state working committees for the establishment of technical and legal norms, with a specific interest for the setting of a single system for quality certification. Confartigianato is also involved in EU programmes through the UEAPME/NORMAPME initiative. Human and Financial Resources

20 Confindustria has repeatedly tried to impose the same principle, which is enshrined in the confederal statute, to its member firms, but unsuccessfully (Regini and Regalia 1998). Among cooperatives’ organizations, UNCI and AGCI also apply automatic double affiliation. Like Confartigianato, also CNA applies automatic double affiliation in the handicraft sector.

In 2004, the staff of the confederal head offices of Confindustria in Rome included 220 people; on the whole, 4,600 professionals were involved in the provision of services and representative functions for members. Between 1992 and 2003, the confederal personnel decreased from 319 to 226 employees, in order to cut costs. In latest years, fixed-term and temporary job contracts have become common for flexibility reasons.21 Apparently, the staff of territorial associations is less numerous in comparison with that of other employers’ organizations (Ferrante 1998, 108).22 The system (i.e. the combination of territorial and branch associations, regional and sectoral federations, plus the confederal structures) possibly offers a minor range of services in comparison with other employers’ organizations, but costs a lot. Every year the organizational system of Confindustria absorbs a sum estimated between 400 and 500 million € (it amounted to 481,798,020 € in 2002), about 93% of which come from membership contributions. The maintenance of the confederal apparatus costs about 35-36 million € per year, but this is just 7-8% of the total costs of the system. Sectoral and territorial associations usually transfer part of the dues paid by member firms to Confindustria, but every association uses different criteria in order to fix its quote (most frequently considering the payroll of member firms). Approximately, each firm pays € 120-130 a year per employee for the enrolment in its territorial association, and more or less the same sum for enrolment in sectoral associations. In theory, this means about € 250 a year per employee; actually, conventions among territorial and sectoral associations provide ceilings for contributions. The contribution to the confederal level is set by the confederal assembly every year and is the same for all member associations, i.e. € 17,80 per employee in 2003-2004 (Rizzo 2004). Since 1996, this contribution has increased by 13%, while the minimal associative contribution registered a 50% increase (it is now around € 25,000) (Lanzalaco 2004).23 Critics maintain that contributions are among the highest in the world, between 3 and 5 times the sum paid in the business associations of the most industrialized countries, Germany included (Carraro 2004). Because of internal resistance to paying contributions, in recent years the organization had to resort to the transfers from its publishing house “Sole 24 Ore”, which – beyond a rich catalogue of books – publishes the financial newspaper with the same name. In 2003 about a quarter of confederal activities was financed in this way. According to data given by the confederation (referred to 2002), about 84% of the confederal budget derives from membership dues and contributions, while 16% derives from shares and holdings (particularly from the ownership of the newspaper, which is very well-known and widespread). The confederation does not sell services and does not receive state subsidies or revenues. A rationalization of staff and structures looks urgent, but there is apparently an equally strong opposition from the internal bureaucracy to downsizing, especially in the periphery of the system. Officially, the proceeds of Confcommercio can derive from three main sources: ordinary and extraordinary contributions, voluntary donations and “other profits”, with the specification that the confederation does not receive state contributions. The organization declares itself as “no profit”, so that even the cost of charged services is defined as “reimbursement” from member associations or firms for the services they have received. 21 As part of a wider internal initiative begun in 2002 for analysing and sharing information on the budget figures of the members, the data on the contributions transferred to the confederation by all member associations were made available for the first time in 2003. In perspective, this could change the way balance sheets are elaborated within the confederation, with the inclusion of data on territorial and sectoral associations. 22 For example, the staff of the provincial association of Trieste, a middle-sized town with a small province, includes about 30 people. However, in comparison, the sectoral federation of food and beverage products (Federalimentare) has only 16 people in the staff of its central office. 23 Since member SMEs often criticize membership costs, it is possible that lower dues were most inflated by the increase. This would be confirmed by another source (Boeri 2004a), according to which contributions paid by territorial associations have remained stable “in real terms” in the last 6 years.

Presumably, contributions represent the most important source of income. However, no data are available on the budget of Confcommercio, nor on its staff.24 This confirms the difficulty in collecting this kind of data on employers’ organizations (Windmuller 1984). In the case of Confartigianato, most financial and staff resources are concentrated on the representation of interests at national and regional level. At territorial level, they are used for services to associated firms. At confederal level, the full-time staff includes 90 employees; the total staff (including member associations and occasional collaborators) amounts to 14,000 people. The proceeds of the confederation derive from member contributions, voluntary offers, real estate income and profits from stock market shares. Nearly 100% of the budget is made of the membership fees from associated firms, collected by territorial associations. Charged services cover a minimal part of the budget. State subsidies are exclusively connected with specific projects and partially cover the implementation costs. Internal Reforms and Restructuring It has been said that since 1970, when the first important reform (the “riforma Pirelli”) was approved, the organizational history of Confindustria has been that of a “continuous and perpetual reform” (Lanzalaco 2004).25 In the 1990s changes were meant to improve effectiveness. With the “riforma Mazzoleni” (1991) the confederal apparatus was re-organized as a network. Internal functional “lines” (in the fields of economic relationships, trade unions’ relationships, external and internal affairs), which had been imposed by the Pirelli reform also on member associations and federations, were eliminated. Former “bureaux” were restructured into departments, currently called “strategic areas” (International Affairs, European Affairs, Organization and Development, Enterprise, Welfare and Human Resources, Fiscal and Corporate Law, Communication, plus the Research Centre), which include specific committees. The competences of vice-presidents (former heads of “lines”) were established by delegation of the president, no longer via statutory rules. In 1994, internal rules were reformed. There was a clear attempt to centralize the confederal leadership and to strengthen the ability to represent interests, also at European level, since the integration of the various components of Confindustria has always been problematic. Until 1994, the attitude was to increase the structural coherence by regulating membership criteria and procedures, assigning competences in a detailed way and standardizing the operation of peripheral structures. At the end of 2002, after a two-year internal debate, the “riforma Mondello-Tognana” was initiated.26 The new principles are free enrolment of firms27, strengthening of sectoral federations, regional decentralization, higher autonomy of local structures, with the possible devolution of representative functions to territorial and sectoral associations. Internal regulations were cut by 70%, in order to introduce higher flexibility. Apparently, this should be a sign of the pressure exerted inside the confederation by the SMEs, still dissatisfied with

24 The answer given to the author of this paper was simply that “these are not data that we usually make public”. 25 In the 1970s, fifteen reform proposals were elaborated inside the confederation. 26 Andrea Mondello was the president of the provincial association of Rome; Nicola Tognana was vice-president of Confindustria and a representative of North-Eastern SMEs. The reform produced the current statute, but did not result in a decrease of membership dues, despite the firm commitment of Mondello (who had publicly denounced the high costs of Confindustria). Once more, this caused discontent among SMEs, which had supported Tognana. 27 This means the official renunciation to apply the principle of double affiliation (i.e. the simultaneous inclusion of each member firm in the related territorial association and sectoral federation/branch association) set in § 6 of the confederal statute. According to the most recent orientation, firms should be “encouraged” to double affiliation through properly devised conventions, aimed at reducing fees. However, in practice firms tend to join whichever association they want – more often territorial than sectoral.

the leadership. It remains to be seen whether this “associative federalism” will be continued in the coming years. As far as Confcommercio is concerned, there was an effort to innovate, strengthen and specialize the confederal services and structures, in order to improve the network of territorial and sectoral activities. This was in line with the main orientation of the organization, which offers a large number of conventions and advantages to its membership. Between the 1980s and 1990s the organization insisted on the point that the tertiary sector had to be recognized as “productive”, like industry and agriculture, and that any discrimination against employers in this sector should be eliminated, especially under the legal profile.28 The fact that the presidency remains tendentially stable (the current president has been on duty since 1995, being re-elected three times up to 2004) proves that there is not any real internal opposition to the main strategic lines of confederal action. Confcommercio has adopted a modern and up-to-date image, with a strong emphasis on technological innovation and product specialization.29 Since 1999 Confartigianato has started an internal restructuring in order to to get the ISO quality certification. This was achieved in 2002 for both human resources and targeted financial management. 6. Conclusions All the employers’ organizations in Italy offer both interest representation and services to their members. The range of services may vary, but usually their substance does not differ very much. Here lies a remarkable source of competition, since services need to be more and more sophisticated in order to ensure the survival of firms, especially when they are SMEs. Moreover, one cannot exclude the possibility of fusions among associations, particularly in the most “overcrowded” sectors.30 In commerce, Confcommercio occupies a predominant position, but Confesercenti has been able to cope quite successfully until now. In industry, notwithstanding critical remarks regularly voiced by SMEs against the lack of internal democracy, Confindustria is largely predominant on Confapi, whose representative activity seems to be more effective at regional and local level than at national level. Here a certain complementarity surfaces, since Confapi apparently attracts those industrial SMEs which do not intend (or cannot afford) to join Confindustria. Cooperatives’ organizations often join forces with the other ASMEs in the representation of interests, even though a debate on their role has been going on in the 1980s and 1990s, in coincidence with a series of acts which amended the related legislation.31

28 In 1998 a specific act reformed the legal discipline of commerce, which had been previously regulated by a 1971 act. Notwithstanding important advances in terms of liberalization and deregulation, the reform proved partial, apparently because of inner resistances in the sector (Pellegrini 2001). The commercial distribution still results so dishomogeneous and differentiated, that it is often accused of being a direct cause of price inflation and tax evasion in economic and political analyses. Supposed “discrimination” may refer to the persistence of bureaucratic and fiscal burdens more than to “comparative disadvantages” in relation to other sectors. Rather, the proper question regards how far a real reform would be accepted in a sector whose firms are highly differentiated in terms of modernity and efficiency. 29 At the EU level, Confcommercio is member of Eurocommerce, which is a further indication of the prevailing interests within the confederation. In Italy, the members of UEAPME are Confapi, Confesercenti, Confartigianato and CNA. 30 In handicraft, there have been talks about a possible fusion of the three confederations in the 1990s (Ferrante 1998, 101). 31 Trade unions and Confindustria had even agreed on the need to overcome the potential “unfair competition” exerted by cooperatives (which have long enjoyed specific fiscal regulations and wage flexibility, e.g. in cooperatives offering jobs to disadvantaged people or starting activities in economically depressed areas). The latest reform of company law (2003) established the duty for cooperatives to enrol in a specific public register, to

More than ever, the multiplicity of employers’ organizations in Italy reflects the fragmentation of production units and the difficulty to reach such a vast and heterogeneous potential membership. SMEs join representative organizations mainly in order to receive services, but it is doubtful whether the second achievement in order of importance, i.e. political pressure, may be effectively exerted by so many organizations on the long term. Some of them have intensified the resort to inter-organizational agreements and joint initiatives, e.g. in handicraft and among cooperatives. This can be a way to increase representativeness, but it may not work in every sector in order to ensure the survival of these collective actors. Another point for further reflection derives from the overlapping membership among organizations and from the effects of tertiarization. If the membership of an organization overlaps that of another (or others, in the case of Italy), it is difficult to imagine a lasting cooperation without tensions. At the same time, as the most important BIA, Confindustria needs to revise its strategy - not only its structure - if it intends to remain a central reference in the system of economic interest groups and in industrial relations in general. The confederation monitors its competitors, particularly as regards their structural features, and stresses its role as representative of SMEs.32 Another challenge regards the reorganization of competences within the confederation, especially at peripheral level. In particular, as far as the defence of the most dynamic productive sectors is concerned, a difficult choice might be necessary between devoting increasing resources to either services or representation. According to confederal data, between 1989 and 2003 member firms in manufacturing have decreased from 73% to about 50% of the membership, while member firms in non-manufacturing industry have increased from 18.5% to 30%. At the same time, the percentage of member firms in services grew from 4.5% to 15% (in 2003, the confederation registered more than 117,000 member firms, with about 4,250,000 employees). Representing tertiary activities (especially those formerly included in the public sector) could prove too expensive and not so rewarding for Confindustria, given the competition from the other representative organizations.

Tables

Table 1: Firms and employees by size classes (included NACE A+B)

Size class 2000 2002 % %

Change in % 2000-2002

1-9 persons Firms 4,380,974 90.6 4,677,834 94.5 6.77

Employees 7,382,151 48.8 7,396,190 46.6 0.19

10-19 Firms 321,527 6.7 207,580 4.2 -35.4

deposit balance sheets and to count at least 9 “working partners” before starting any activity. Moreover, cooperatives will be assimilated to other firm types “in absence of specific rules”. In 2000, another act has clarified the status of working partners (soci lavoratori), i.e. partners in a cooperative who also work within it, with reference to collective bargaining coverage and trade union representation. These innovations should contribute to eliminate any distinction between associations representing cooperatives and those representing enterprises. 32 This is stated in the Bilancio sociale 2003 (Social balance survey) of the confederation, available on-line. In the same document, a reference is made to court rulings which recognized Confindustria as “more representative” than “other organizations specifically involved in the protection of SMEs” (p. 119). However, no further details are given about the identity of these competitors.

Employees 1,715,197 11.3 1,714,936 10.8 -0.01

20-99 Firms 128,599 2.6 56,461 1.14 -56.0

Employees 2,414,367 15.9 2,493,229 15.7 3.26

100-249

Firms Employees

6,376

971,273

0.1

6.4

6,906

1,042,223

0.14

6.6

8.3

7.3 250 and more Firms

2,890 0.05 3,272 0.06 13.2

Employees 2,648,012 17.5 3,202,422 20.2 20.9 Total Firms

4,840,366 100.05 4,952,053 100.04 2.3

Employees 15,131,000 99.9 15,849,000 99.9 4.7 Sources: elaboration on Unioncamere data (Movimprese 2000; 2002a); Charlier (2003); ISTAT (2002; 2003a; 2004a; 2004b). Table 2: Firms and employees by size class (excluded NACE A+B)

Size class 2000 2002 % %

Change in % 2000-2002

1-9 persons Firms 3,626,936 95.9 3,755,177 95.2 3.5

Employees 7,086,520 48.3 7,537,024 49.0 6.3

10-19 Firms 81,527 2.1 129,376 3.3 58.6

Employees 1,610,828 11.0 1,685,245 11.0 4.6

20-99 Firms 63,632 1.7 49,742 1.3 -21.8

Employees 2,363,367 16.1 2,414,790 15.6 2.17

100-249

Firms Employees

6,376

971,273

0.2

6.6

6,906

987,788

0.1

6.4

8.3

1.7 250 and more Firms

2,890 0.08 3,272 0.08 13.2

Employees 2,648,012 18.0 2,762,153 18.0 4.3 Total Firms

3,781,361 99.98 3,944,473 99.98 4.3

Employees 14,680,000 100 15,387,000 100 4.8 Sources: elaboration on Unioncamere and ISTAT data (see previous table). Table 3: Establishments (1998 and 2001) Size class 1998, with

NACE A+B 2001, with NACE A+B

Change in % 1998-’01

1998, minus NACE A+B

2001, minus NACE A+B

Change in % 1998-‘01

1-9 3,588,243 4,168,094 16.1 3,587,974 4,138,094 15.3

(94.6) (94.65) (94.6) (94.7) 10-49 182,277

(4.8) 205,907 (4.67)

12.96 182,255 (4.8)

205,907 (4.7)

12.97

50-249 20,977 (0.55)

26,281 (0.6)

25.28 20,976 (0.55)

21,198 (0.5)

1.05

250-499 1,812 (0.04)

2,213 (0.05)

22.1 1,812 (0.04)

2,213 (0.05)

22.1

≥500 903 (0.02)

936 (0.02)

3.6 903 (0.02)

936 (0.02)

3.6

Total 3,794,212 (99.98)

4,403,431 (99.99)

16.05 3,793,920 (100.01)

4,368,348 (99.97)

15.1

Sources: ISTAT (1998; 2004b). In Italian statistical sources, establishments are referred to as unità locali (local units). Table 4: Italy's cross-sectoral business associations: basic data (2002) Association Scope of

functions Membership domain33and type of affiliation

Members Covered employees

Voting rights

Confindustria (1910)

Mixed All businesses in industry and part of the tertiary sector (A)

113,307 4,280,075 Weighted

Confapi (1947)